Exhibit 99.1

|

Metro New York’s Premier Business Bank

July 2014

|

Safe Harbor Statement

“Safe Harbor” Statement under the Private Securities Litigation Reform Act of 1995:

This presentation contains various forward-looking statements with respect to earnings, credit quality and other financial and business matters within the meaning of the Private Securities Litigation Reform Act of 1995. These forward-statements can be identified by words such as “expects,” “anticipates,” “intends,” “believes,” “estimates,” “predicts” and words of similar import. The Company cautions that these forward-looking statements are subject to numerous assumptions, risks and uncertainties, and that statements relating to future periods are subject to uncertainty because of the increased likelihood of changes in underlying factors and assumptions. Actual results could differ materially from forward-looking statements.

Factors that may cause actual results to differ materially from those contemplated by such forward-looking statements, include, but are not limited to, statements regarding: (a) the OCC and other bank regulators may require us to further modify or change our mix of assets, including our concentration in certain types of loans, or require us to take further remedial actions; (b) our inability to deploy our excess cash, reduce our expenses and improve our operating leverage and efficiency; (c) our ability to pay quarterly cash dividends to shareholders in light of our earnings, the current and future economic environment, Federal Reserve Board guidance, our Bank’s capital plan and other regulatory requirements applicable to Hudson Valley or Hudson Valley Bank; (d) the possibility that we may need to raise additional capital in the future and our ability to raise such capital on terms that are favorable to us; (e) further increases in our non-performing loans and allowance for loan losses; (f) ineffectiveness in managing our commercial real estate portfolio; (g) lower than expected future performance of our investment portfolio; (h) inability to effectively integrate and manage the new business and lending teams; (i) a lack of opportunities for growth, plans for expansion (including opening new branches) and increased or unexpected competition in attracting and retaining customers; (j) continued poor economic conditions generally and in our market area in particular, which may adversely affect the ability of borrowers to repay their loans and the value of real property or other property held as collateral for such loans; (k) lower than expected demand for our products and services; (l) possible additional impairment of our goodwill and other intangible assets; (m) our inability to manage interest rate risk; (n) increased expense and burdens resulting from the regulatory environment in which we operate and our ability to comply with existing and future regulatory requirements; (o) our inability to maintain regulatory capital above the minimum levels Hudson Valley Bank has set as its minimum capital levels in its capital plan, or such higher capital levels as may be required; (p) proposed legislative and regulatory action may adversely affect us and the financial services industry; (q) legislative and regulatory actions (including the impact of the Dodd-Frank Wall Street Reform and Consumer Protection Act and related regulations) may subject us to additional regulatory oversight which may result in increased compliance costs and/or require us to change our business model;(r) future increased Federal Deposit Insurance Corporation, or FDIC, special assessments or changes to regular assessments; (s) potential liabilities under federal and state environmental laws; (t) legislative and regulatory changes to laws governing New York State’s taxation of HVB’s REIT subsidiary.

For a more detailed discussion of these factors, see the Risk Factors discussion in the Company’s most recent Annual Report on Form 10-K. The forward-looking statements included in this presentation are made only as of the date hereof and the Company undertakes no obligation to update or revise any of its forward-looking statements.

Unless otherwise noted, information presented is from Company sources.

2

|

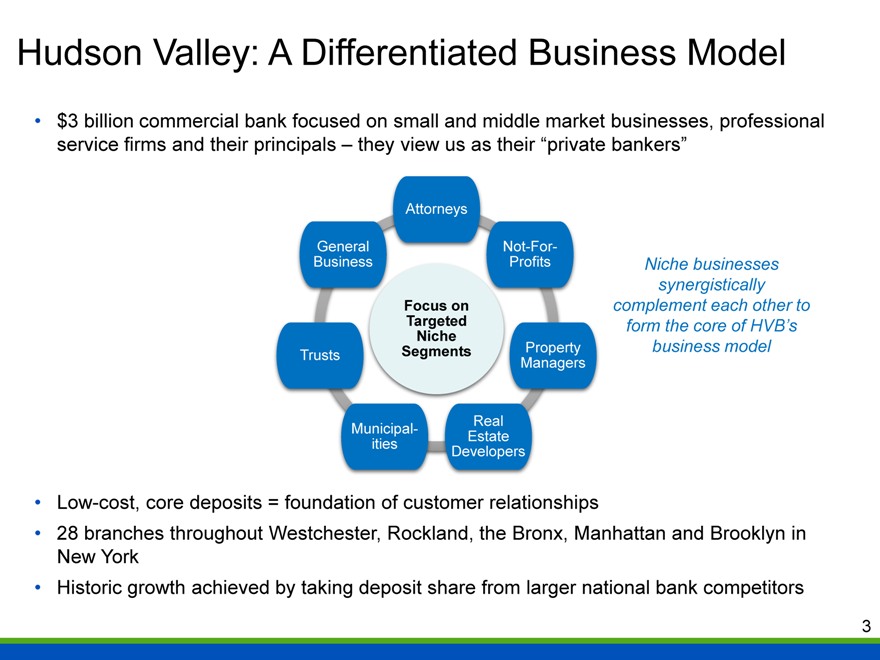

Hudson Valley: A Differentiated Business Model

$3 billion commercial bank focused on small and middle market businesses, professional service firms and their principals – they view us as their “private bankers”

Attorneys

General Not-For-

Business Profits

Focus on

Targeted

Niche

Trusts Segments Property

Managers

Municipal- Real

Estate

ities Developers

Niche businesses synergistically complement each other to form the core of HVB’s business model

Low-cost, core deposits = foundation of customer relationships

28 branches throughout Westchester, Rockland, the Bronx, Manhattan and Brooklyn in New York Historic growth achieved by taking deposit share from larger national bank competitors

3

|

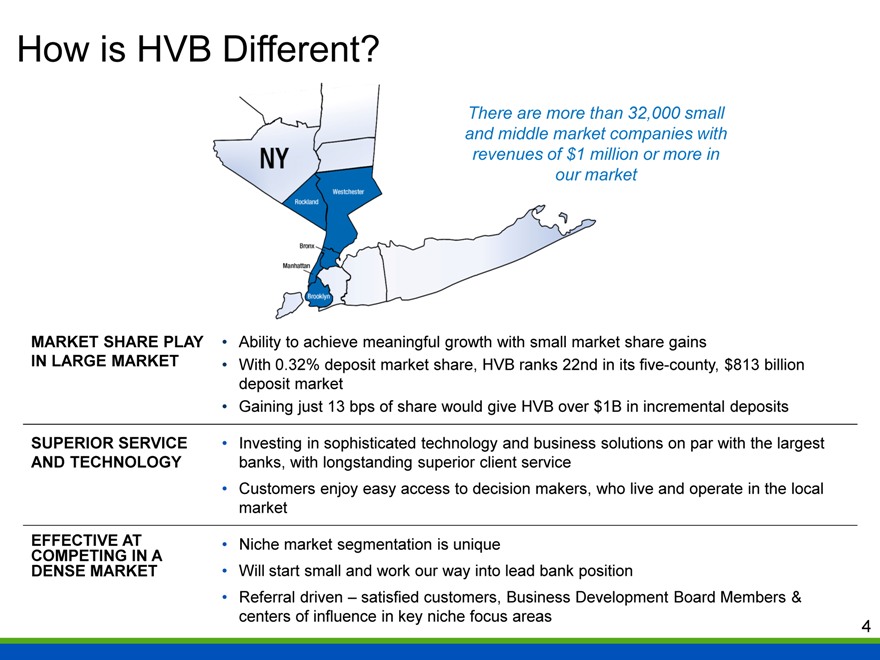

How is HVB Different?

There are more than 32,000 small and middle market companies with revenues of $1 million or more in our market

MARKET SHARE PLAY Ability to achieve meaningful growth with small market share gains

IN LARGE MARKET With 0.32% deposit market share, HVB ranks 22nd in its five-county, $813 billion

deposit market

Gaining just 13 bps of share would give HVB over $1B in incremental deposits

SUPERIOR SERVICE Investing in sophisticated technology and business solutions on par with the largest

AND TECHNOLOGY banks, with longstanding superior client service

Customers enjoy easy access to decision makers, who live and operate in the local

market

EFFECTIVE AT Niche market segmentation is unique

COMPETING IN A

DENSE MARKET Will start small and work our way into lead bank position

Referral driven – satisfied customers, Business Development Board Members &

centers of influence in key niche focus areas 4

|

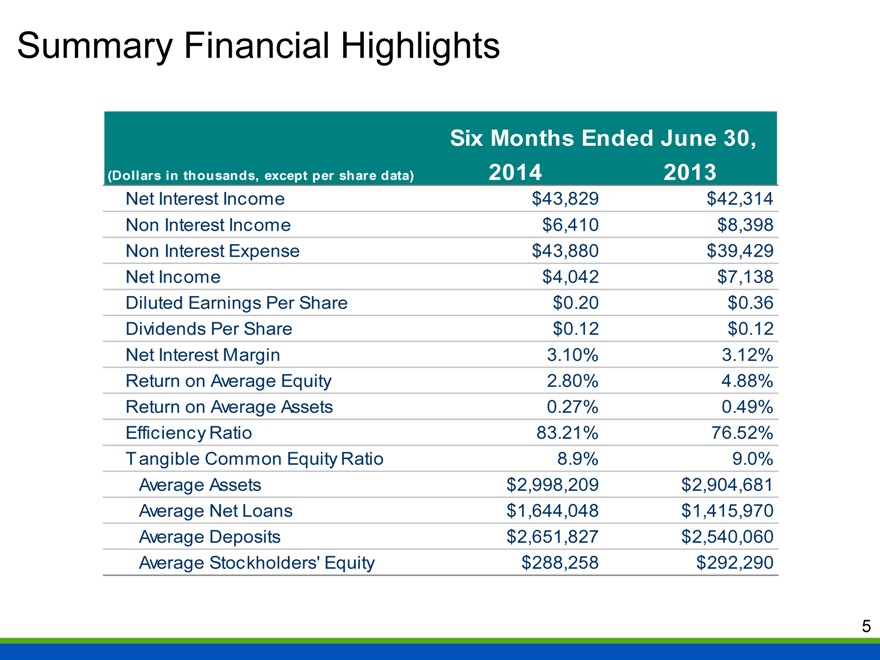

Summary Financial Highlights

Six Months Ended June 30,

(Dollars in thousands, except per share data) 2014 2013

Net Interest Income $43,829 $42,314

Non Interest Income $6,410 $8,398

Non Interest Expense $43,880 $39,429

Net Income $4,042 $7,138

Diluted Earnings Per Share $0.20 $0.36

Dividends Per Share $0.12 $0.12

Net Interest Margin 3.10% 3.12%

Return on Average Equity 2.80% 4.88%

Return on Average Assets 0.27% 0.49%

Efficiency Ratio 83.21% 76.52%

T angible Common Equity Ratio 8.9% 9.0%

Average Assets $2,998,209 $2,904,681

Average Net Loans $1,644,048 $1,415,970

Average Deposits $2,651,827 $2,540,060

Average Stockholders’ Equity $288,258 $292,290

5

|

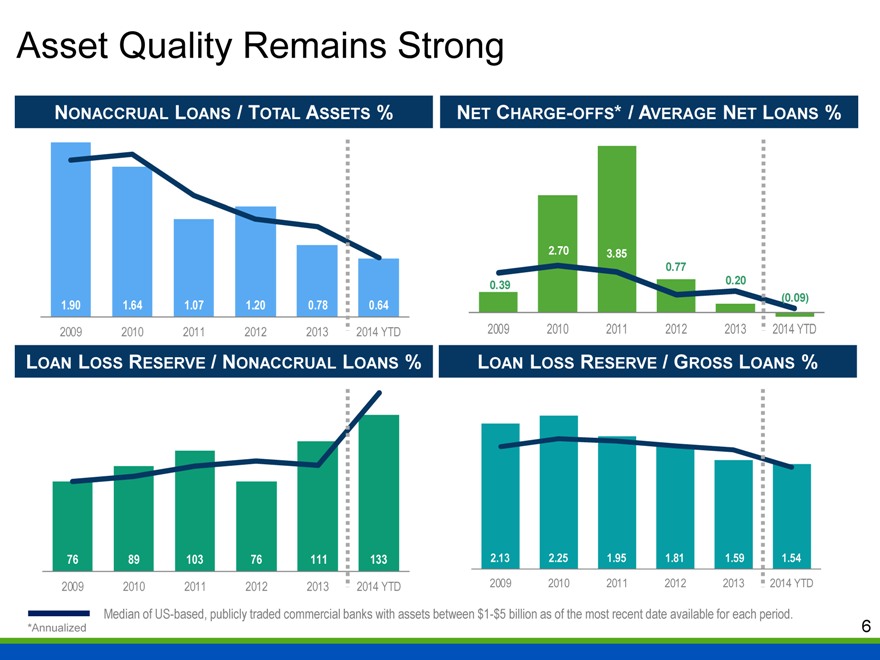

Asset Quality Remains Strong

NONACCRUAL LOANS / TOTAL ASSETS %

1.90 1.64 1.07 1.20 0.78 0.64

2009 2010 2011 2012 2013 2014 YTD

NET CHARGE-OFFS* / AVERAGE NET LOANS %

2.70 3.85

0.77

0.39 0.20

(0.09)

2009 2010 2011 2012 2013 2014 YTD

LOAN LOSS RESERVE / NONACCRUAL LOANS %

76 89 103 76 111 133

2009 2010 2011 2012 2013 2014 YTD

LOAN LOSS RESERVE / GROSS LOANS %

2.13 2.25 1.95 1.81 1.59 1.54

2009 2010 2011 2012 2013 2014 YTD

Median of US-based, publicly traded commercial banks with assets between $1-$5 billion as of the most recent date available for each period.

*Annualized 6

|

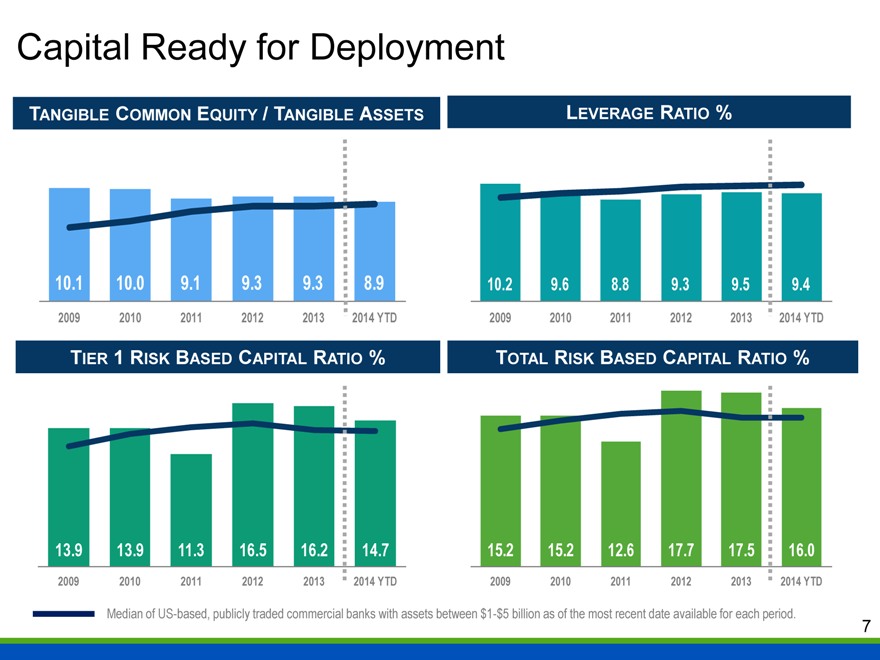

Capital Ready for Deployment

TANGIBLE COMMON EQUITY / TANGIBLE ASSETS

%

10.1 10.0 9.1 9.3 9.3 8.9

2009 2010 2011 2012 2013 2014 YTD

LEVERAGE RATIO %

10.2 9.6 8.8 9.3 9.5 9.4

2009 2010 2011 2012 2013 2014 YTD

TIER 1 RISK BASED CAPITAL RATIO %

13.9 13.9 11.3 16.5 16.2 14.7

2009 2010 2011 2012 2013 2014 YTD

TOTAL RISK BASED CAPITAL RATIO %

15.2 15.2 12.6 17.7 17.5 16.0

2009 2010 2011 2012 2013 2014 YTD

Median of US-based, publicly traded commercial banks with assets between $1-$5 billion as of the most recent date available for each period.

7

|

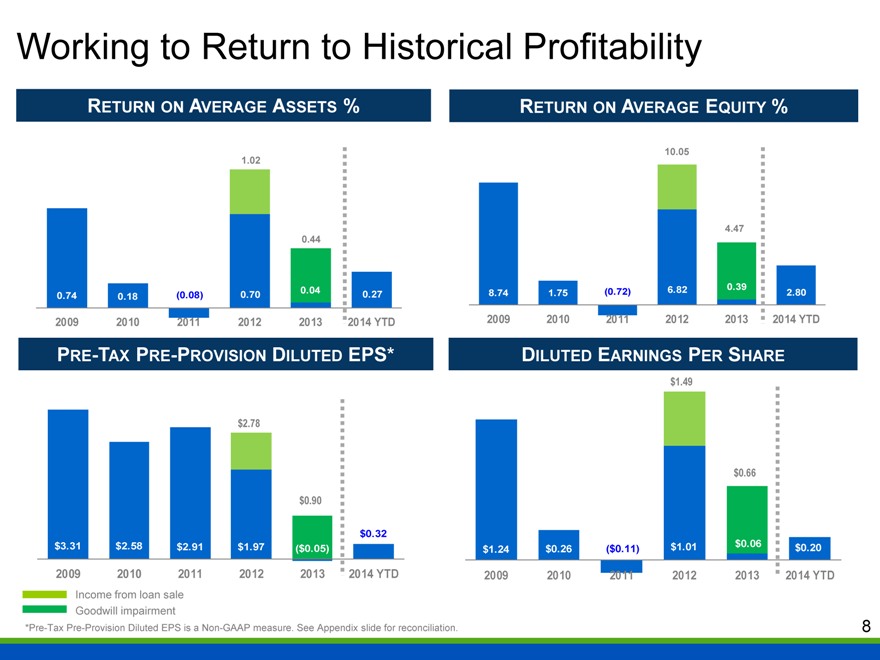

Working to Return to Historical Profitability

RETURN ON AVERAGE ASSETS %

1.02

0.44

0.74 0.18 (0.08) 0.70 0.04 0.27

2009 2010 2011 2012 2013 2014 YTD

RETURN ON AVERAGE EQUITY %

10.05

4.47

8.74 1.75 (0.72) 6.82 0.39 2.80

2009 2010 2011 2012 2013 2014 YTD

PRE-TAX PRE-PROVISION DILUTED EPS*

$ 2.78

$ 0.90

$ 0.32

$ 3.31 $ 2.58 $ 2.91 $1.97 ($0.05)

2009 2010 2011 2012 2013 2014 YTD

DILUTED EARNINGS PER SHARE

$1.49

$0.$661.49

$1.24 $0.26 ($0.11) $1.01 $0.06 $0.20

2009 2010 2011 2012 2013 2014 YTD

Income from loan sale Goodwill impairment

*Pre-Tax Pre-Provision Diluted EPS is a Non-GAAP measure. See Appendix slide for reconciliation.

8

|

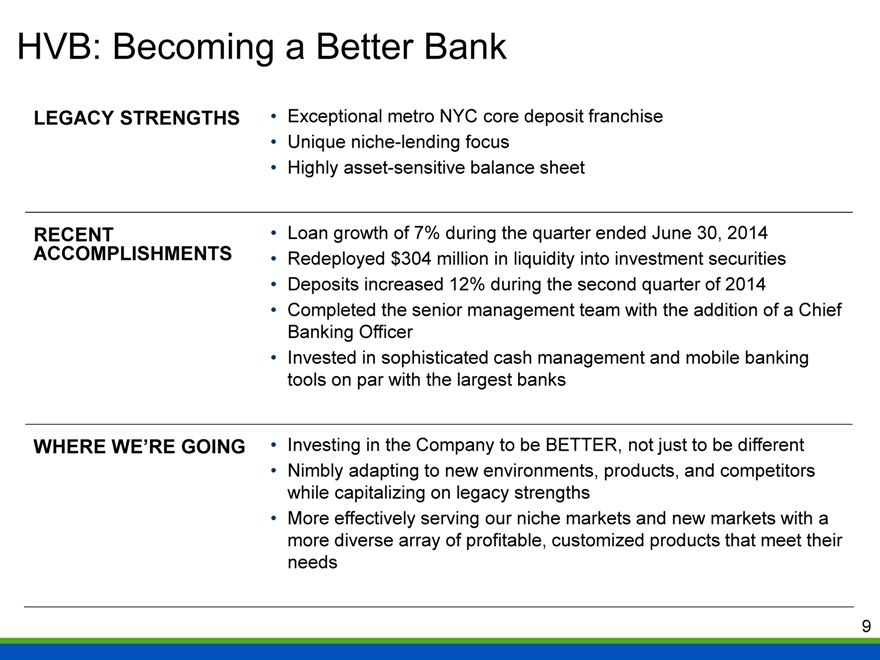

HVB: Becoming a Better Bank

LEGACY STRENGTHS Exceptional metro NYC core deposit franchise

Unique niche-lending focus

Highly asset-sensitive balance sheet

RECENT Loan growth of 7% during the quarter ended June 30, 2014

ACCOMPLISHMENTS Redeployed $304 million in liquidity into investment securities

Deposits increased 12% during the second quarter of 2014

Completed the senior management team with the addition of a Chief

Banking Officer

Invested in sophisticated cash management and mobile banking

tools on par with the largest banks

WHERE WE’RE GOING Investing in the Company to be BETTER, not just to be different

Nimbly adapting to new environments, products, and competitors

while capitalizing on legacy strengths

More effectively serving our niche markets and new markets with a

more diverse array of profitable, customized products that meet their

needs

9

|

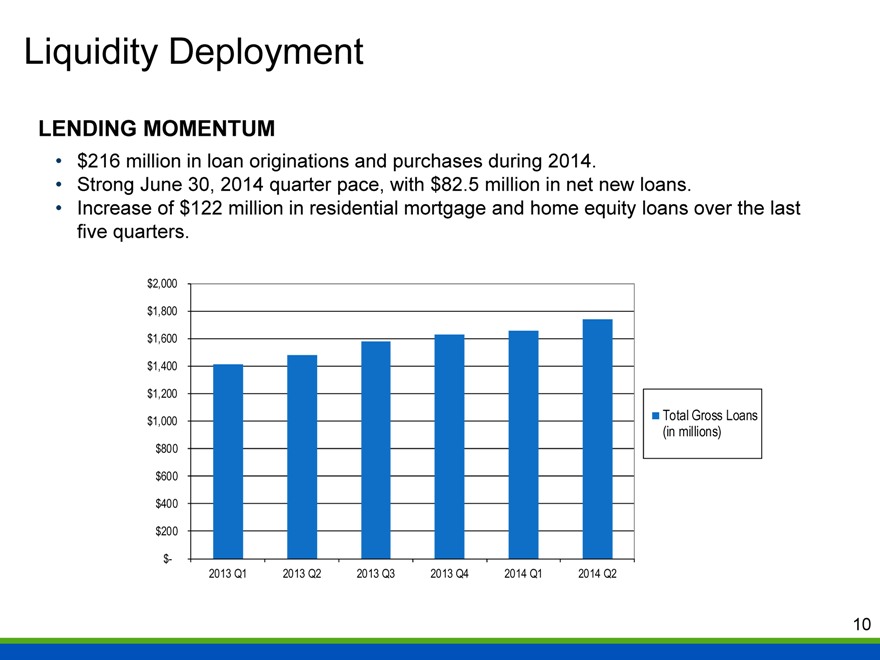

Liquidity Deployment

LENDING MOMENTUM

$216 million in loan originations and purchases during 2014.

Strong June 30, 2014 quarter pace, with $82.5 million in net new loans.

Increase of $122 million in residential mortgage and home equity loans over the last five quarters.

$2,000

$1,800

$1,600

$1,400

$1,200

$1,000

$800

$600

$400

$200

$-

2013 Q1 2013 Q2 2013 Q3 2013 Q4 2014 Q1 2014 Q2

(in Total millions) Gross Loans

10

|

Liquidity Deployment

Balance Sheet Changes by Quarter (in millions)

350

319

304 298

300

250

200

153 161

150

110

100 97

65

50 40 47 40 40 54 54

27

6 12

0

Q2 2013 Q3 2013 Q4 2013 Q1 2014 Q2 2014

-50 -31 -10

-64 -69 -72

-100 -93 -97

-107

-150

Liquidity Invesments Loans Assets Deposits

11

|

Diversifying Offering: Liquidity Deployment

$304 million in securities purchases in June 2014 with an average yield of 1.79%, average life of 4.8 years, and average duration of 3.8 years.

Building on core competency with CRE lending while launching new or expanding products for niche commercial customers and their owners, principals and managers:

1. Jumbo residential mortgage and home equity products complementing commercial offerings

2. Recent launches of asset-based lending (ABL) and equipment financing businesses will increase portfolio diversity

3. Continue to pursue quality in-market CRE, moving up-market and building on strong reputation in our marketplace

12

|

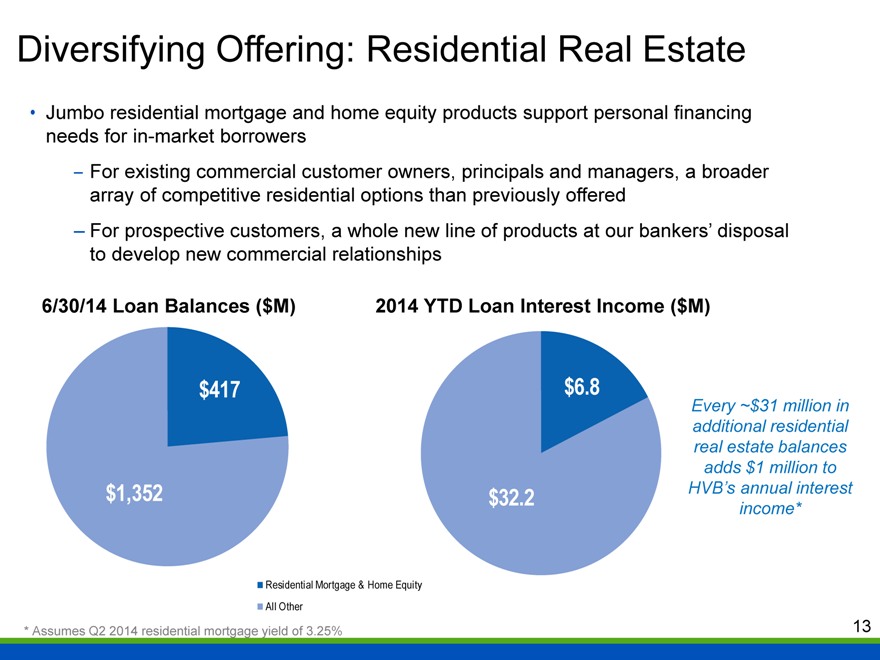

Diversifying Offering: Residential Real Estate

Jumbo residential mortgage and home equity products support personal financing needs for in-market borrowers

– For existing commercial customer owners, principals and managers, a broader array of competitive residential options than previously offered

– For prospective customers, a whole new line of products at our bankers’ disposal to develop new commercial relationships

6/30/14 Loan Balances ($M) 2014 YTD Loan Interest Income ($M)

$417 $6.8

$1,352 $32.2

Every ~$31 million in additional residential real estate balances adds $1 million to HVB’s annual interest income*

Residential Mortgage & Home Equity All Other

* Assumes Q2 2014 residential mortgage yield of 3.25%

13

|

Diversifying Offering: Asset Based Lending

HVB Capital Credit LLC launched in November 2013

Diversifies and improves risk profile of overall portfolio

Offering a growing array of products and services in demand by small- and mid-sized commercial customers and prospects in metro NYC and beyond

Flexible alternative financing solutions to companies with credit needs between $2.5 million and $25 million – a range typically underserved by the country’s largest banks

Addition of veteran ABL team builds on long record of attracting top talent from national/multinational banks

Every ~$29 million in additional ABL balances adds $1 million to HVB’s annual interest income*

* Assumes Q2 2014 ABL origination yield of 3.5%

14

|

Diversifying Offering: Equipment Financing

HVB Equipment Capital LLC launched in March 2014

Nationwide lender to customers, wholesale partners and manufacturers, providing equipment leasing and lending for a wide range of income-producing equipment, including:

– Manufacturing

– Healthcare

– Technology

– Transportation

Focus on seizing opportunities to finance small and middle-market transactions in the $100,000 to $5 million range

Offers new and existing customers a flexible alternative to traditional commercial loans, enhancing cash flow and preserving working capital

15

|

Moving Upmarket with Technology

Over the past two years, implemented risk management systems and capital management framework typical of a $10-$25 billion bank, with our $3 billion balance sheet

An investment of $4 million, recognized over five years, for enhanced technology solutions for business customers will be made, with the solutions rolled out in 2014.

Applications for small and mid-sized companies, including mobile banking applications and enhanced lockbox and other cash management tools

Designing sophisticated cash management resources for larger companies to be competitive with the best cash management platforms offered in our marketplace – on par with the largest banks

– Sophisticated platforms allow us to meet the treasury management needs of larger businesses

» For example, in the past we have served law firms with 5-10 partners; now we can serve firms with 20-100 partners

16

|

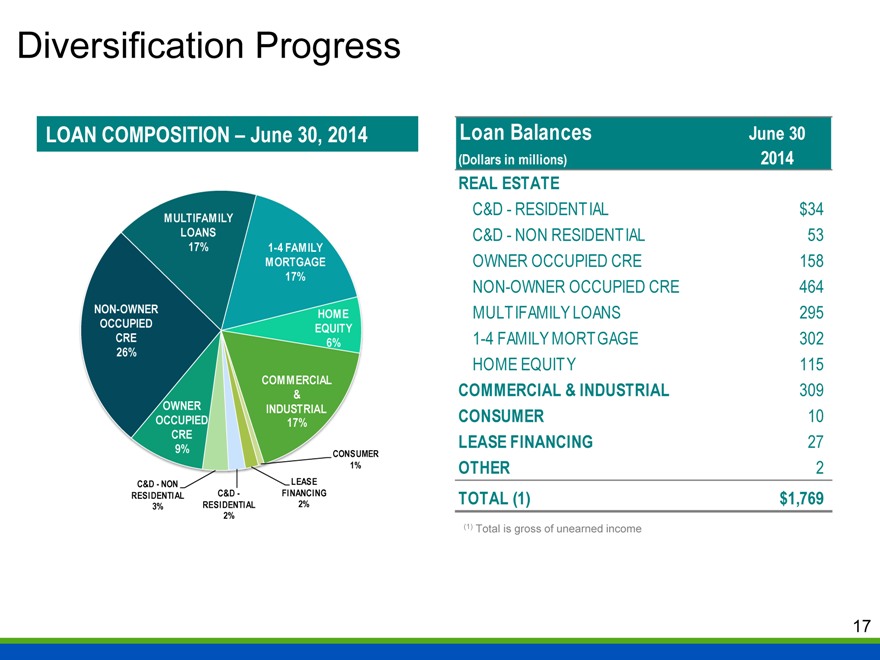

Diversification Progress

LOAN COMPOSITION – June 30, 2014

MULTIFAMILY

LOANS

17% 1-4 FAMILY

MORTGAGE

17%

NON-OWNER HOME

OCCUPIED EQUITY

CRE 6%

26%

COMMERCIAL

&

OWNER INDUSTRIAL

OCCUPIED 17%

CRE

9% CONSUMER

1%

C&D—NON LEASE

RESIDENTIAL C&D— FINANCING

3% RESIDENTIAL 2%

2%

Loan Balances June 30

(Dollars in millions) 2014

REAL ESTATE

C&D—RESIDENTIAL $34

C&D—NON RESIDENTIAL 53

OWNER OCCUPIED CRE 158

NON-OWNER OCCUPIED CRE 464

MULTIFAMILY LOANS 295

1-4 FAMILY MORTGAGE 302

HOME EQUITY 115

COMMERCIAL & INDUSTRIAL 309

CONSUMER 10

LEASE FINANCING 27

OTHER 2

TOTAL (1) $1,769

(1) Total is gross of unearned income

17

|

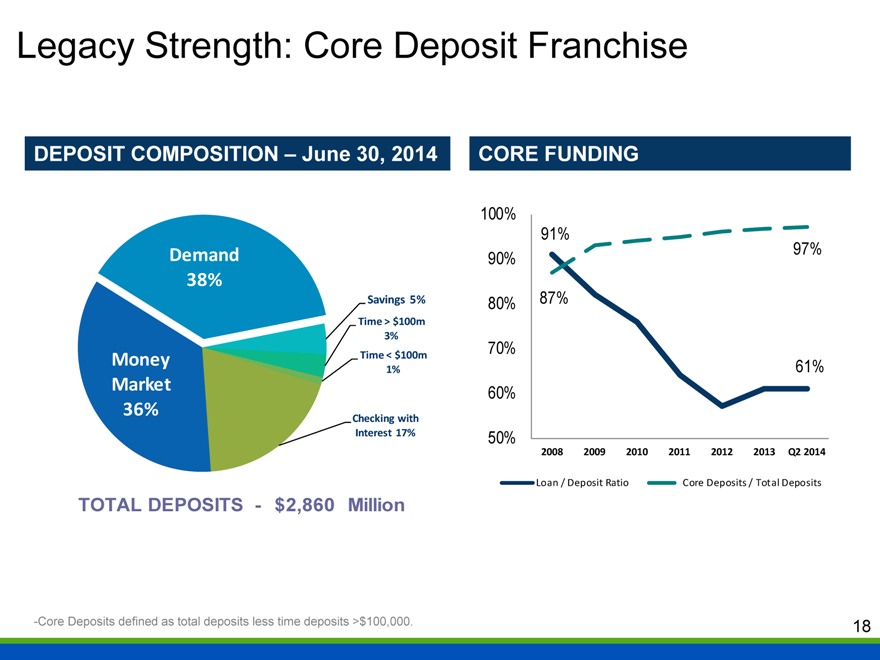

Legacy Strength: Core Deposit Franchise

DEPOSIT COMPOSITION – June 30, 2014

Demand

38%

Savings 5%

Time > $100m

3%

Money Time < $100m

1%

Market

36% Checking with

Interest 17%

TOTAL DEPOSITS— $2,860 Million

CORE FUNDING

100%

91%

90% 97%

80% 87%

70%

61%

60%

50%

2008 2009 2010 2011 2012 2013 Q2 2014

Loan / Deposit Ratio Core Deposits / Total Deposits

-Core Deposits defined as total deposits less time deposits >$100,000.

18

|

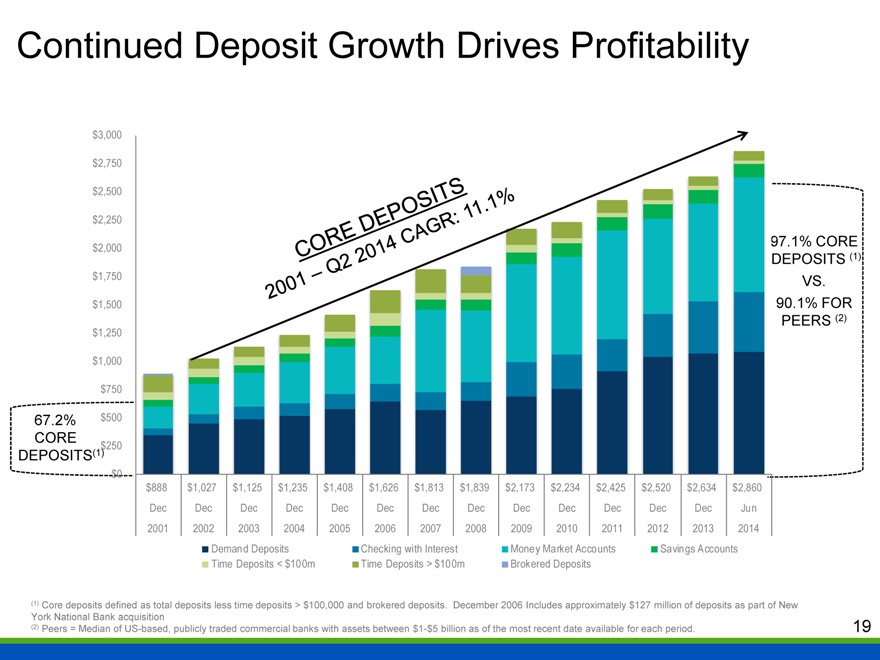

Continued Deposit Growth Drives Profitability

$3,000

$2,750

$2,500

$2,250

$2,000 97.1% CORE

DEPOSITS (1)

$1,750 VS.

$1,500 90.1% FOR

PEERS (2)

$1,250

$1,000

$750

67.2% $500

CORE $250

DEPOSITS(1)

$0

$888 $1,027 $1,125 $1,235 $1,408 $1,626 $1,813 $1,839 $2,173 $2,234 $2,425 $2,520 $2,634 $2,860

Dec Dec Dec Dec Dec Dec Dec Dec Dec Dec Dec Dec Dec Jun

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Demand Deposits Checking with Interest Money Market Accounts Savings Accounts

Time Deposits < $100m Time Deposits > $100m Brokered Deposits

(1) Core deposits defined as total deposits less time deposits > $100,000 and brokered deposits. December 2006 Includes approximately $127 million of deposits as part of New York National Bank acquisition (2) Peers = Median of US-based, publicly traded commercial banks with assets between $1-$5 billion as of the most recent date available for each period.

19

|

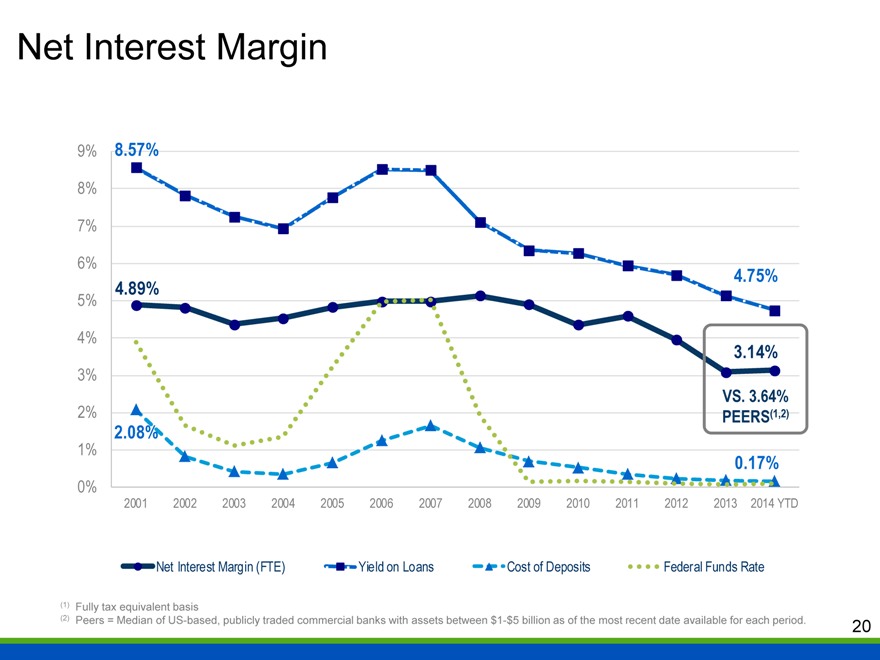

Net Interest Margin

9% 8.57%

8%

7%

6%

5% 4.89% 4.75%

4% 3.14%

3%

VS. 3.64%

2% PEERS(1,2)

1% 2.08%

0.17%

0%

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 YTD

Net Interest Margin (FTE) Yield on Loans Cost of Deposits Federal Funds Rate

(1) Fully tax equivalent basis

(2) Peers = Median of US-based, publicly traded commercial banks with assets between $1-$5 billion as of the most recent date available for each period.

20

|

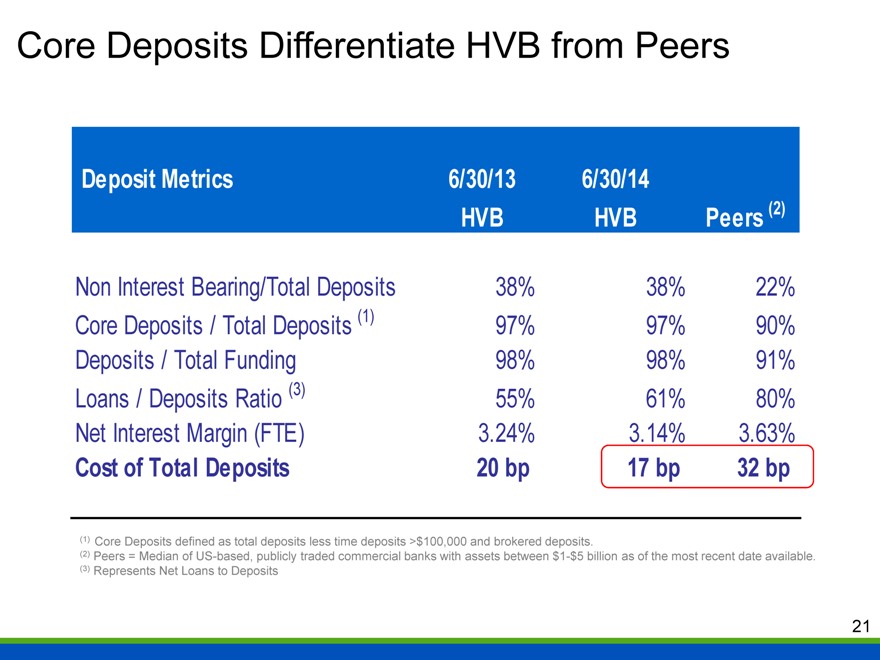

Core Deposits Differentiate HVB from Peers

Deposit Metrics 6/30/13 6/30/14

HVB HVB Peers (2)

Non Interest Bearing/Total Deposits 38% 38% 22%

Core Deposits / Total Deposits (1) 97% 97% 90%

Deposits / Total Funding 98% 98% 91%

Loans / Deposits Ratio (3) 55% 61% 80%

Net Interest Margin (FTE) 3.24% 3.14% 3.63%

Cost of Total Deposits 20 bp 17 bp 32 bp

(1) Core Deposits defined as total deposits less time deposits >$100,000 and brokered deposits.

(2) Peers = Median of US-based, publicly traded commercial banks with assets between $1-$5 billion as of the most recent date available. (3) Represents Net Loans to Deposits

21

|

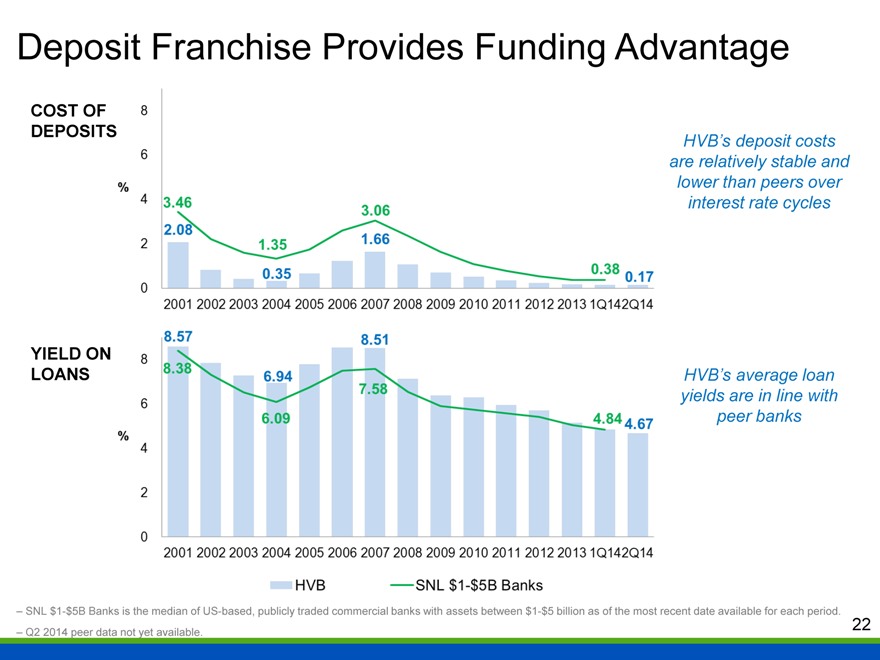

Deposit Franchise Provides Funding Advantage

COST OF DEPOSIT

HVB’s deposit costs re relatively stable and lower than peers over interest rate cycles

YIELD ON LOANS

HVB’s average loan yields are in line with peer banks

– SNL $1-$5B Banks is the median of US-based, publicly traded commercial banks with assets between $1-$5 billion as of the most recent date available for each period.

– Q2 2014 peer data not yet available.

22

|

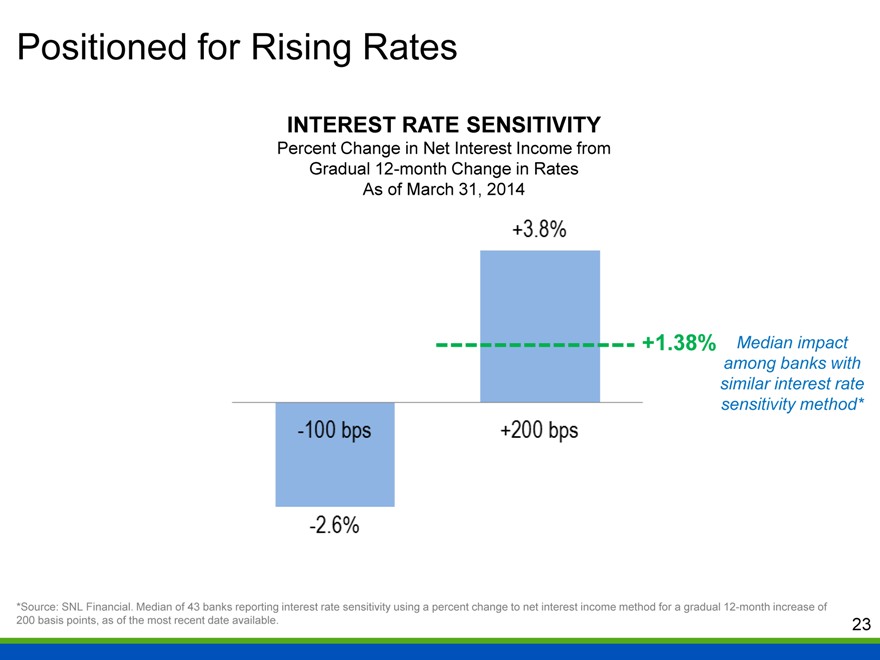

Positioned for Rising Rates

INTEREST RATE SENSITIVITY

Percent Change in Net Interest Income from Gradual 12-month Change in Rates As of March 31, 2014

+3.8%

+1.38%

-100 bps

+200bps

-2.6%

Median impact among banks with similar interest rate sensitivity method*

*Source: SNL Financial. Median of 43 banks reporting interest rate sensitivity using a percent change to net interest income method for a gradual 12-month increase of 200 basis points, as of the most recent date available.

23

|

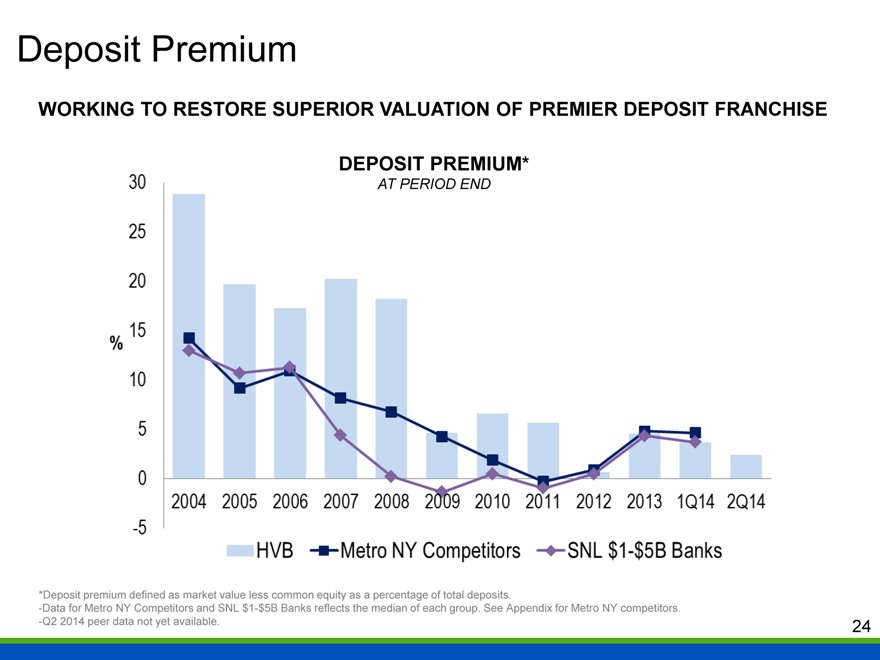

Deposit Premium

WORKING TO RESTORE SUPERIOR VALUATION OF PREMIER DEPOSIT FRANCHISE

DEPOSIT PREMIUM*

AT PERIOD END

30

25

20

15

10

5

0

-5

%

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

1Q14

2Q14

HVB Metro NY Competitors SNL $1-$5B Banks

*Deposit premium defined as market value less common equity as a percentage of total deposits.

-Data for Metro NY Competitors and SNL $1-$5B Banks reflects the median of each group. See Appendix for Metro NY competitors.

-Q2 2014 peer data not yet available.

24

|

HVB: Becoming a Better Bank

LEGACY STRENGTHS

RECENT

ACCOMPLISHMENTS

WHERE WE’RE GOING

Exceptional metro NYC core deposit franchise

Unique niche-lending focus

Highly asset-sensitive balance sheet

Loan growth of 7% during the quarter ended June 30, 2014

Redeployed $304 million in liquidity into investment securities

Deposits increased 12% during the second quarter of 2014

Completed the senior management team with the addition of a Chief Banking Officer

Invested in sophisticated cash management and mobile banking tools on par with the largest banks

Investing in the Company to be BETTER, not just to be different

Nimbly adapting to new environments, products, and competitors

while capitalizing on legacy strengths

More effectively serving our niche markets and new markets with a more diverse array of profitable, customized products that meet their needs

25

|

THANK YOU

FOR YOUR INTEREST IN HUDSON VALLEY HOLDING CORP.

26

|

APPENDIX

FINANCIAL DETAIL AND NON-GAAP RECONCILIATION

27

|

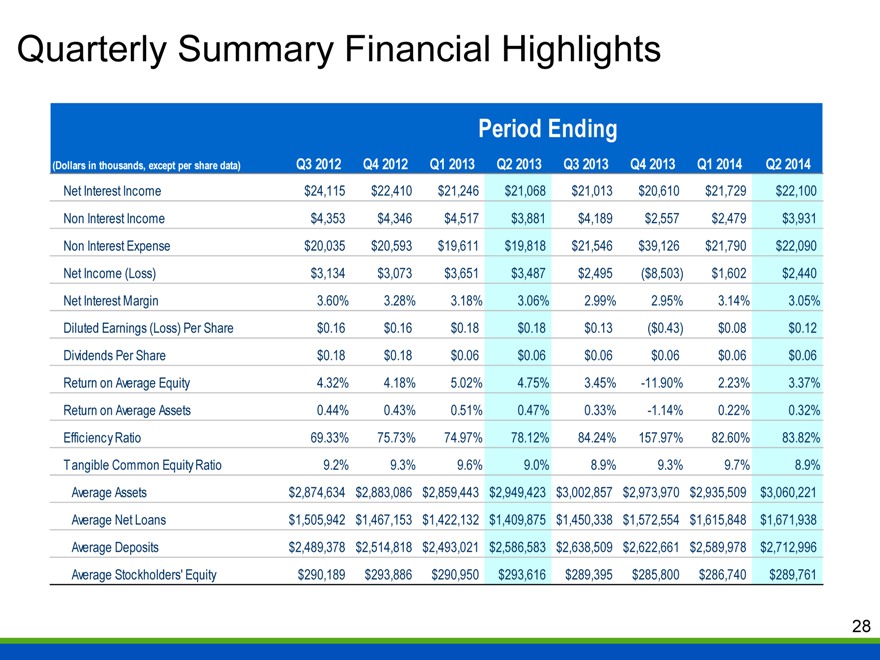

Quarterly Summary Financial Highlights

Period Ending

(Dollars in thousands, except per share data) Q3 2012 Q4 2012 Q1 2013 Q2 2013 Q3 2013 Q4 2013 Q1 2014 Q2 2014

Net Interest Income $24,115 $22,410 $21,246 $21,068 $21,013 $20,610 $21,729 $22,100

Non Interest Income $4,353 $4,346 $4,517 $3,881 $4,189 $2,557 $2,479 $3,931

Non Interest Expense $20,035 $20,593 $19,611 $19,818 $21,546 $39,126 $21,790 $22,090

Net Income (Loss) $3,134 $3,073 $3,651 $3,487 $2,495 ($8,503) $1,602 $2,440

Net Interest Margin 3.60% 3.28% 3.18% 3.06% 2.99% 2.95% 3.14% 3.05%

Diluted Earnings (Loss) Per Share $0.16 $0.16 $0.18 $0.18 $0.13 ($0.43) $0.08 $0.12

Dividends Per Share $0.18 $0.18 $0.06 $0.06 $0.06 $0.06 $0.06 $0.06

Return on Average Equity 4.32% 4.18% 5.02% 4.75% 3.45% -11.90% 2.23% 3.37%

Return on Average Assets 0.44% 0.43% 0.51% 0.47% 0.33% -1.14% 0.22% 0.32%

Efficiency Ratio 69.33% 75.73% 74.97% 78.12% 84.24% 157.97% 82.60% 83.82%

Tangible Common Equity Ratio 9.2% 9.3% 9.6% 9.0% 8.9% 9.3% 9.7% 8.9%

Average Assets $2,874,634 $2,883,086 $2,859,443 $2,949,423 $3,002,857 $2,973,970 $2,935,509 $3,060,221

Average Net Loans $1,505,942 $1,467,153 $1,422,132 $1,409,875 $1,450,338 $1,572,554 $1,615,848 $1,671,938

Average Deposits $2,489,378 $2,514,818 $2,493,021 $2,586,583 $2,638,509 $2,622,661 $2,589,978 $2,712,996

Average Stockholders’ Equity $290,189 $293,886 $290,950 $293,616 $289,395 $285,800 $286,740 $289,761

28

|

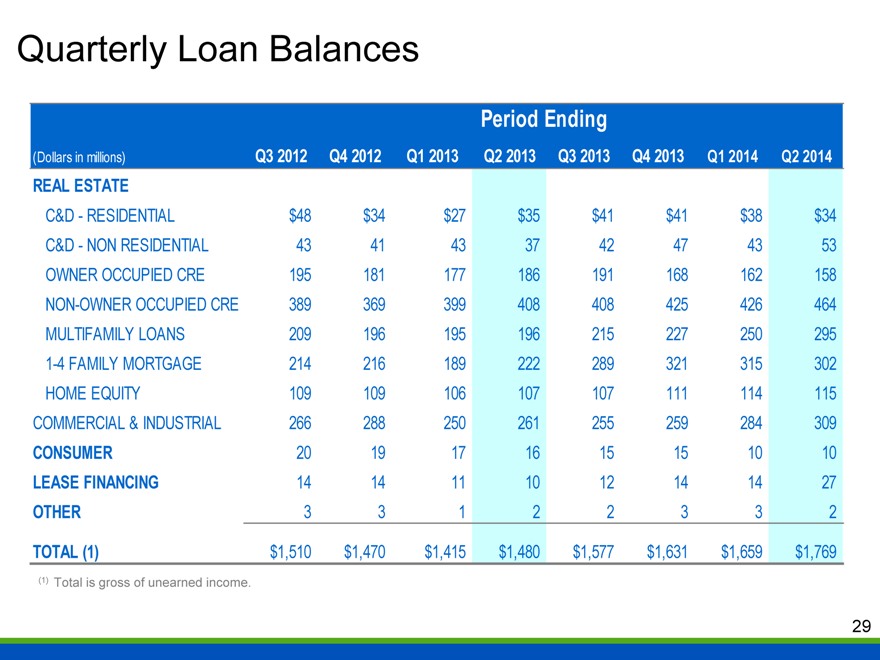

Quarterly Loan Balances

Period Ending

(Dollars in millions) Q3 2012 Q4 2012 Q1 2013 Q2 2013 Q3 2013 Q4 2013 Q1 2014 Q2 2014

REAL ESTATE

C&D - RESIDENTIAL $48 $34 $27 $35 $41 $41 $38 $34

C&D - NON RESIDENTIAL 43 41 43 37 42 47 43 53

OWNER OCCUPIED CRE 195 181 177 186 191 168 162 158

NON-OWNER OCCUPIED CRE 389 369 399 408 408 425 426 464

MULTIFAMILY LOANS 209 196 195 196 215 227 250 295

1-4 FAMILY MORTGAGE 214 216 189 222 289 321 315 302

HOME EQUITY 109 109 106 107 107 111 114 115

COMMERCIAL & INDUSTRIAL 266 288 250 261 255 259 284 309

CONSUMER 20 19 17 16 15 15 10 10

LEASE FINANCING 14 14 11 10 12 14 14 27

OTHER 3 3 1 2 2 3 3 2

TOTAL (1) $1,510 $1,470 $1,415 $1,480 $1,577 $1,631 $1,659 $1,769

(1) Total is gross of unearned income.

29

|

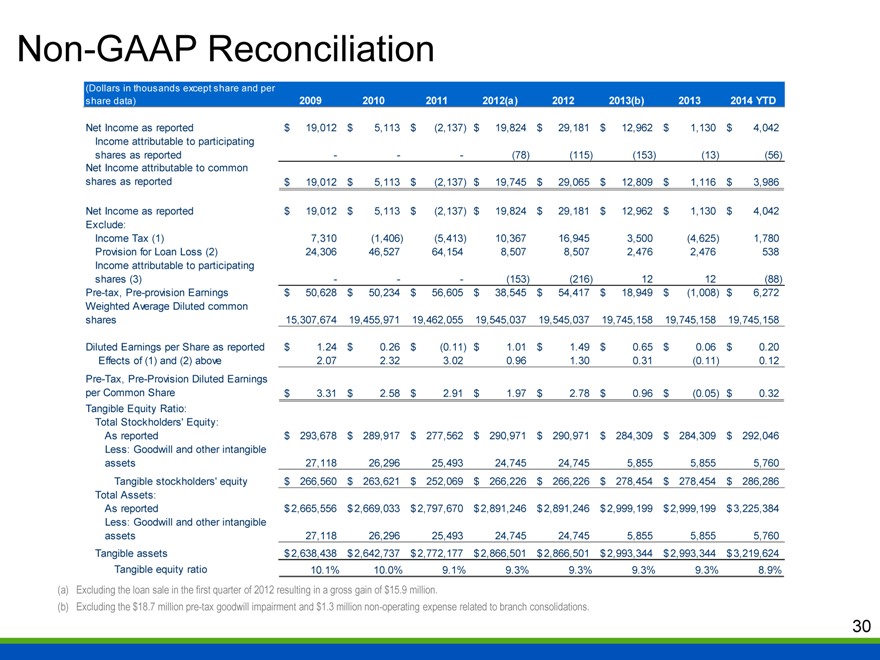

Non-GAAP Reconciliation

(Dollars in thousands except share and per

share data) 2009 2010 2011 2012(a) 2012 2013(b) 2013 2014 YTD

Net Income as reported $19,012 $5,113 $(2,137) $19,824 $29,181 $12,962 $1,130 $4,042

Income attributable to participating shares as reported — — — (78) (115) (153) (13) (56)

Net Income attributable to common shares as reported $19,012 $5,113 $(2,137) $19,745 $29,065 $12,809 $1,116 $3,986

Net Income as reported $19,012 $5,113 $(2,137) $19,824 $29,181 $12,962 $1,130 $4,042

Exclude:

Income Tax (1) 7,310 (1,406) (5,413) 10,367 16,945 3,500 (4,625) 1,780

Provision for Loan Loss (2) 24,306 46,527 64,154 8,507 8,507 2,476 2,476 538

Income attributable to participating shares (3) — — — (153) (216) 12 12 (88)

Pre-tax, Pre-provision Earnings $50,628 $50,234 $56,605 $38,545 $54,417 $18,949 $(1,008) $6,272

Weighted Average Diluted common shares 15,307,674 19,455,971 19,462,055 19,545,037 19,545,037 19,745,158 19,745,158 19,745,158

Diluted Earnings per Share as reported $1.24 $0.26 $(0.11) $1.01 $1.49 $0.65 $0.06 $0.20

Effects of (1) and (2) above 2.07 2.32 3.02 0.96 1.30 0.31 (0.11) 0.12

Pre-Tax, Pre-Provision Diluted Earnings per Common Share $3.31 $2.58 $2.91 $1.97 $2.78 $0.96 $(0.05) $0.32

Tangible Equity Ratio:

Total Stockholders’ Equity:

As reported $293,678 $289,917 $277,562 $290,971 $290,971 $284,309 $284,309 $292,046

Less: Goodwill and other intangible assets 27,118 26,296 25,493 24,745 24,745 5,855 5,855 5,760

Tangible stockholders’ equity $266,560 $263,621 $252,069 $266,226 $266,226 $278,454 $278,454 $286,286

Total Assets:

As reported $2,665,556 $2,669,033 $2,797,670 $2,891,246 $2,891,246 $2,999,199 $2,999,199 $3,225,384

Less: Goodwill and other intangible assets 27,118 26,296 25,493 24,745 24,745 5,855 5,855 5,760

Tangible assets $2,638,438 $2,642,737 $2,772,177 $2,866,501 $2,866,501 $2,993,344 $2,993,344 $3,219,624

Tangible equity ratio 10.1% 10.0% 9.1% 9.3% 9.3% 9.3% 9.3% 8.9%

(a) Excluding the loan sale in the first quarter of 2012 resulting in a gross gain of $15.9 million.

(b) Excluding the $18.7 million pre-tax goodwill impairment and $1.3 million non-operating expense related to branch consolidations.

30

|

Metro New York Competitors

Astoria Financial Corporation

BCB Bancorp, Inc.

Center Bancorp, Inc.

ConnectOne Bancorp, Inc.

Dime Community Bancshares, Inc.

First of Long Island Corporation

Flushing Financial Corporation

Intervest Bancshares Corporation

Investors Bancorp, Inc.

Kearny Financial Corp. (MHC)

Lakeland Bancorp, Inc.

Northfield Bancorp, Inc.

Oritani Financial Corp.

Peapack-Gladstone Financial Corporation

People’s United Financial, Inc.

Signature Bank

Sterling Bancorp

Tompkins Financial Corporation

Unity Bancorp, Inc.

Valley National Bancorp

Webster Financial Corporation

31

|

THANK YOU FOR YOUR INTEREST IN HUDSON VALLEY HOLDING CORP.

HVB

LISTED

NYSE

www.hudsonvalleybank.com

32