Exhibit 99.3

![]()

| Note to the reader The Monthly Report on Financial Transactions provides an overview of the Québec government’s monthly financial results. It is produced to increase the transparency of public finances and to provide regular monitoring of the achievement of the budgetary balance target for the fiscal year. The financial information presented in this report is unaudited and is based on the accounting policies used in the government’s annual financial statements.(1) In March 2020, the World Health Organization declared a COVID-19 pandemic. The pandemic and the measures implemented to deal with it are having significant impacts, in particular on the Québec government’s financial situation. The Monthly Report on Financial Transactions at June 30, 2021 will be published on September 24, 2021. |

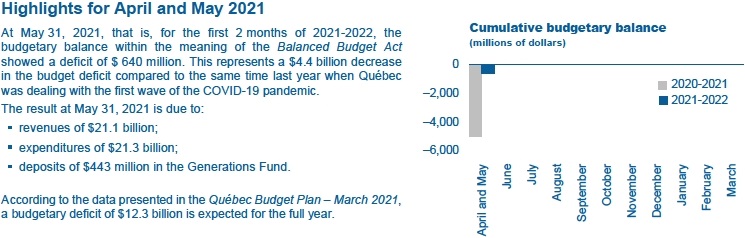

| SUMMARY OF CONSOLIDATED RESULTS | ||||||||||||

| (unaudited data, millions of dollars) | ||||||||||||

| April and May | ||||||||||||

| 2020-2021 | 2021-2022 | Change | Change (%) | |||||||||

| Own-source revenue | 10 952 | 16 621 | 5 669 | 51.8 | ||||||||

| Federal transfers | 4 091 | 4 497 | 406 | 9.9 | ||||||||

| Consolidated revenue | 15 043 | 21 118 | 6 075 | 40.4 | ||||||||

| Portfolio expenditures(2) | -18 497 | -19 848 | -1 351 | 7.3 | ||||||||

| Debt service | -1 198 | -1 467 | -269 | 22.5 | ||||||||

| Consolidated expenditure | -19 695 | -21 315 | -1 620 | 8.2 | ||||||||

| SURPLUS (DEFICIT)(3) | -4 652 | -197 | 4 455 | - | ||||||||

| BALANCED BUDGET ACT | ||||||||||||

| Deposits of dedicated revenues in the Generations Fund | -388 | -443 | -55 | - | ||||||||

| BUDGETARY BALANCE(4) | -5 040 | -640 | 4 400 | - |

1

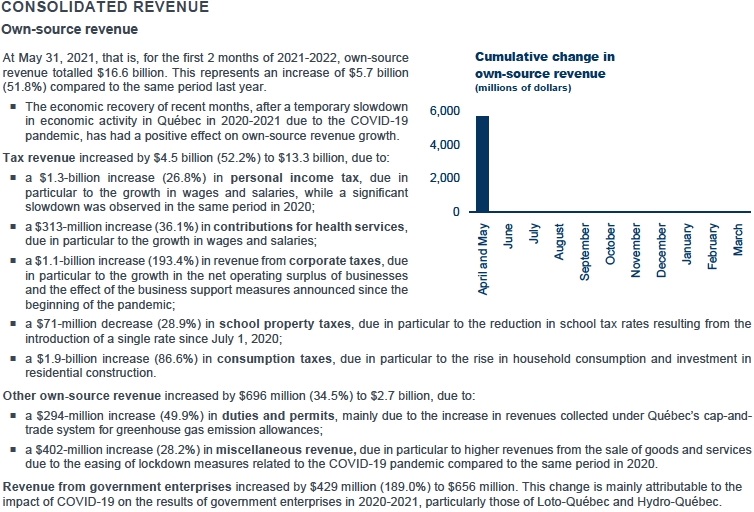

| OWN-SOURCE REVENUE | ||||||||||||

| (unaudited data, millions of dollars) | ||||||||||||

| April and May | ||||||||||||

| 2020-2021 | 2021-2022 | Change | Change (%) | |||||||||

| Income and property taxes | ||||||||||||

Personal income tax | 4 808 | 6 095 | 1 287 | 26.8 | ||||||||

Contributions for health services | 866 | 1 179 | 313 | 36.1 | ||||||||

Corporate taxes | 560 | 1 643 | 1 083 | 193.4 | ||||||||

School property tax | 246 | 175 | -71 | -28.9 | ||||||||

| Consumption taxes | 2 230 | 4 162 | 1 932 | 86.6 | ||||||||

| Tax revenue | 8 710 | 13 254 | 4 544 | 52.2 | ||||||||

| Duties and permits | 589 | 883 | 294 | 49.9 | ||||||||

| Miscellaneous revenue | 1 426 | 1 828 | 402 | 28.2 | ||||||||

| Other own-source revenue | 2 015 | 2 711 | 696 | 34.5 | ||||||||

| Total own-source revenue excluding revenue from government enterprises | 10 725 | 15 965 | 5 240 | 48.9 | ||||||||

| Revenue from government enterprises | 227 | 656 | 429 | 189.0 | ||||||||

| TOTAL | 10 952 | 16 621 | 5 669 | 51.8 | ||||||||

2

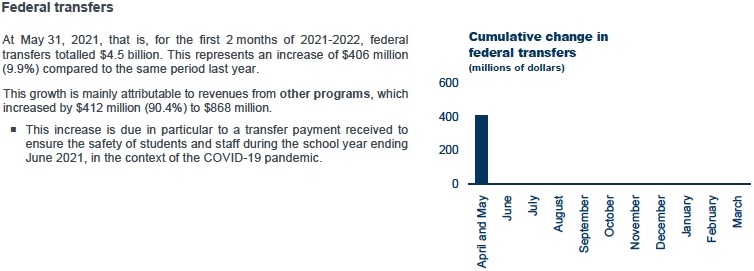

| FEDERAL TRANSFERS | |||||||||||

| (unaudited data, millions of dollars) | |||||||||||

| April and May | |||||||||||

| 2020-2021 | 2021-2022 | Change | Change (%) | ||||||||

| Equalization | 2 209 | 2 186 | -23 | -1.0 | |||||||

| Health transfers | 1 149 | 1 171 | 22 | 1.9 | |||||||

| Transfers for post-secondary education and other social programs | 277 | 272 | -5 | -1.8 | |||||||

| Other programs | 456 | 868 | 412 | 90.4 | |||||||

| TOTAL | 4 091 | 4 497 | 406 | 9.9 | |||||||

3

| CONSOLIDATED EXPENDITURES BY PORTFOLIO(6) | ||||||||||||

| (unaudited data, millions of dollars) | ||||||||||||

| April and May | ||||||||||||

| 2020-2021(6) | 2021-2022 | Change | Change (%) | |||||||||

| Santé et Services sociaux | 8 541 | 9 667 | 1 126 | 13.2 | ||||||||

| Éducation | 2 779 | 3 029 | 250 | 9.0 | ||||||||

| Enseignement supérieur | 1 346 | 1 431 | 85 | 6.3 | ||||||||

| Other portfolios(7) | 6 028 | 5 923 | -105 | -1.7 | ||||||||

| Change in application of the accounting standard respecting transfer payments(8) | -197 | -202 | 5 | 2.5 | ||||||||

| Portfolio expenditures | 18 497 | 19 848 | 1 351 | 7.3 | ||||||||

| Debt service | 1 198 | 1 467 | 269 | 22.5 | ||||||||

| TOTAL | 19 695 | 21 315 | 1 620 | 8.2 | ||||||||

4

NET FINANCIAL SURPLUSES OR REQUIREMENTS

| Composition of net financial surpluses or requirements The government’s revenues and expenditures are established on an accrual basis of accounting. Revenues are recognized when earned and expenses when incurred, regardless of when receipts and disbursements occur. Net financial surpluses (requirements), on the other hand, consist of the difference between receipts and disbursements resulting from government activities. To meet its net financial requirements, the government uses a variety of financing sources, including cash and borrowings. The various items for net financial requirements represent net receipts and disbursements generated by the government’s loans, interests in its enterprises, fixed assets and other investments, as well as by retirement plans and other employee future benefits, and by other accounts. This last item includes the payment of accounts payable and the collection of accounts receivable. Deposits in the Generations Fund also result in financial requirements. Beginning with the Monthly Report on Financial Transactions at December 31, 2020, the presentation of net financial surpluses (requirements) has been modified to make it comparable to the presentation used in the Québec Budget Plan - March 2021. Thus, the heading “Investments, loans and advances” now includes the change in short-term investments, and the heading “Retirement plans and other employee future benefits” now takes into account the reinvestment of investment income from the Retirement Plans Sinking Fund and specific funds. A new heading, “Deposits in the Generations Fund,” includes the financial requirements generated by the revenues dedicated to the Generations Fund. |

For the period of April and May 2021, net financial requirements amount to $4.1 billion and are due to:

the $197-million deficit resulting from the difference between government revenues and expenditures;

the $2.7-billion financial requirements for investments, loans and advances, due primarily to an increase in short-term investments of $2.1 billion as part of overall cash management, as well as the growth in the consolidation value of government enterprises;(9)

the $132-million financial surplus related to government capital investments, mainly due to investments of $604 million, offset by amortization expenses of $712 million;(9)

the $534-million financial requirements related to retirement plans and other employee future benefits liabilities, resulting from the payment of government employee benefits of $1.1 billion, partially offset by the net cost of plans of $541 million;(9)

the $376-million financial requirements for other accounts;(10)

the $443-million financial requirements generated by the deposits in the Generations Fund.

| NET FINANCIAL SURPLUSES OR REQUIREMENTS | ||||||

| (unaudited data, millions of dollars) | ||||||

| April and May | ||||||

| 2020-2021 | 2021-2022 | |||||

| SURPLUS (DEFICIT)(3) | -4 652 | -197 | ||||

| Non-budgetary transactions | ||||||

| Investments, loans and advances | -5 013 | -2 722 | ||||

| Capital investments | 240 | 132 | ||||

| Retirement plans and other employee future benefits | -461 | -534 | ||||

| Other accounts(10) | -5 367 | -376 | ||||

| Deposits in the Generations Fund | -388 | -443 | ||||

| Total non-budgetary transactions | -10 989 | -3 943 | ||||

| NET FINANCIAL SURPLUSES (REQUIREMENTS) | -15 641 | -4 140 | ||||

5

APPENDIX 1: BUDGET FORECASTS

| BUDGET FORECASTS FOR 2021-2022 | ||||||

| (millions of dollars) | ||||||

| March 2021 | ||||||

| Budget (11) | Change (%)(12) | |||||

| CONSOLIDATED REVENUE | ||||||

| Income and property taxes | ||||||

Personal income tax | 35 921 | 2.0 | ||||

Contributions for health services | 6 796 | 5.3 | ||||

Corporate taxes | 8 013 | 0.4 | ||||

School property tax | 1 113 | -4.5 | ||||

| Consumption taxes | 23 325 | 14.8 | ||||

| Tax revenue | 75 168 | 5.7 | ||||

| Duties and permits | 4 853 | 10.8 | ||||

| Miscellaneous revenue | 10 989 | 4.5 | ||||

| Other own-source revenue | 15 842 | 6.4 | ||||

| Total own-source revenue excluding revenue from government enterprises | 91 010 | 5.8 | ||||

| Revenue from government enterprises | 4 658 | 16.8 | ||||

| Total own-source revenue | 95 668 | 6.3 | ||||

| Federal transfers | 26 899 | -11.1 | ||||

| Total consolidated revenue | 122 567 | 1.9 | ||||

| CONSOLIDATED EXPENDITURE | ||||||

| Santé et Services sociaux | -52 358 | -2.6 | ||||

| Éducation | -18 312 | 3.9 | ||||

| Enseignement supérieur | -9 491 | 8.5 | ||||

| Other portfolios(7) | -40 981 | -3.8 | ||||

| Change in application of the accounting standard respecting transfer payments | -732 | - | ||||

| Portfolio expenditures | -121 874 | -1.2 | ||||

| Debt service | -8 613 | 12.4 | ||||

| Total consolidated expenditure | -130 487 | -0.4 | ||||

| Provision for economic risks and other support and recovery measures | -1 250 | - | ||||

| SURPLUS (DEFICIT)(3) | -9 170 | - | ||||

| BALANCED BUDGET ACT | ||||||

| Deposits of dedicated revenues in the Generations Fund | -3 080 | - | ||||

| BUDGETARY BALANCE(4) | -12 250 | - | ||||

6

APPENDIX 2: EXPENDITURES BY MISSION

Government expenditures are broken down into five public service missions. This breakdown of the government’s expenditures into its main areas of activity is a stable indicator over time because it is usually not influenced by Cabinet shuffles. Moreover, since this breakdown is also used in the Public Accounts, its presentation in the Monthly Report on Financial Transactions allows for a better monitoring of actual results over the course of the year.

The public service missions are:

Health and Social Services, which consists primarily of the activities of the health and social services network and the programs administered by the Régie de l’assurance maladie du Québec;

Education and Culture, which consists primarily of the activities of the education networks, student financial assistance, programs in the culture sector and immigration-related programs;

Economy and Environment, which primarily includes programs related to economic development, employment assistance measures, international relations, the environment and infrastructure support;

Support for Individuals and Families, which includes, in particular, last resort financial assistance, assistance measures for families and seniors, and certain legal aid measures;

Administration and Justice, which consists mainly of the activities of the legislature, central bodies and public security, as well as administrative programs.

| CONSOLIDATED EXPENDITURES BY MISSION EXCLUDING DEBT SERVICE | ||||||

| (unaudited data, millions of dollars) | ||||||

| April and May | ||||||

| 2020-2021(6) | 2021-2022 | |||||

| Health and Social Services | 8 319 | 9 488 | ||||

| Education and Culture | 4 333 | 4 605 | ||||

| Economy and Environment | 2 481 | 2 557 | ||||

| Support for Individuals and Families | 2 138 | 2 032 | ||||

| Administration and Justice | 1 423 | 1 368 | ||||

| Change in application of the accounting standard respecting transfer payments(8) | -197 | -202 | ||||

| TOTAL | 18 497 | 19 848 | ||||

7

Consolidated financial information

Consolidated results include the results of all entities that are part of the government’s reporting entity, i.e. that are under its control. To determine consolidated results, the government eliminates transactions carried out between entities in the reporting entity. Additional information on the government’s financial organization and the financing of public services can be found on pages 13 to 18 of the document titled “Budgetary Process and Documents: Public Financial Accountability” (in French only).

Change in application of the accounting standard respecting transfer payments

The Québec government contributes to the financing of public infrastructure owned by third parties. In most cases, financing is provided through annual transfers paid according to a schedule that corresponds to the rate of repayment of the loans contracted by the recipients to carry out the projects.

For these projects, the government changed the application of PS 3410, Transfer payments, to account for transfer expenditures based on the period of completion of eligible work by transfer recipients. Previously, transfer expenditures were recorded at the rate of disbursements authorized by Parliament and the balance of funded work was reported in contractual obligations. This change results in more timely recognition of transfer expenditures in the government’s consolidated financial statements.

In this monthly report, the estimated impact of this change has been accounted for retroactively and is presented in the consolidated expenditures in the line "Change in application of the accounting standard respecting transfer payments." Public Accounts 2020-2021, which will be published in the fall, will present the final impact of the application of the accounting standard, including the government’s accumulated deficit as at March 31, 2021.

Notes

| (1) | A summary of the government’s accounting policies can be found on pages 82 to 85 of Volume 1 of the Public Accounts 2019-2020. |

| (2) | Portfolio expenditure includes the impact of the change in application of the accounting standard respecting transfer payments. |

| (3) | Balance as defined in the Public Accounts. |

| (4) | Budgetary balance within the meaning of the Balanced Budget Act. |

| (5) | Consolidated expenditures by mission are presented in Appendix 2. |

| (6) | Certain expenditures were reclassified between portfolios and between missions to take into account the transition to the 2021-2022 budgetary structure. |

| (7) | Other portfolios include inter-portfolio eliminations resulting from the elimination of reciprocal transactions between entities in different portfolios. |

| (8) | The change in application of the accounting standard respecting transfer payments decreases cumulative expenditure at May 31, 2020 and 2021. Expenditures that were previously recorded in the first months of the fiscal year are now recorded based on the estimated progress of the work performed by the recipients. |

| (9) | These items, which are included in the government’s budgetary surplus (deficit), are eliminated in non-budgetary transactions because they have no effect on cash flow. |

| (10) | The financial surpluses or requirements pertaining to other accounts can vary significantly from one month to the next, in particular according to the time when the government collects or disburses funds related to its activities. For example, when the last day of the month is not a business day, QST remittances are collected at the beginning of the following month, such that the equivalent of two months’ remittances can be collected in a given month. |

| (11) | The presentation of the budgetary information in this monthly report is consistent with that of the financial framework as published in the Québec Budget Plan - March 2021. |

| (12) | This is the annual change compared to results in 2020-2021. |

For more information, contact the Direction des communications of the Ministère des Finances at 418-528-7382. | |

| The report is also available on the Ministère des Finances website: www.finances.gouv.qc.ca. |

8