Exhibit 99.8

PUBLIC ACCOUNTS | Consolidated Financial |

|

Fiscal year ended March 31, 2023

Published in accordance with section 86

of the Financial Administration Act (CQLR, chapter A-6.001)

Public Accounts 2022-2023 – Volume 1

Legal deposit – Bibliothèque et Archives nationales du Québec

December 2023

ISSN 0706-2850 (Print version)

ISSN 1925-1823 (PDF)

© Gouvernement du Québec, 2023

His Honour the Honourable J. Michel Doyon

Lieutenant-Governor of Québec

Parliament Building

Québec

Your Honour,

I am pleased to present you with the Public Accounts of the Gouvernement du Québec for the fiscal year ended March 31, 2023. They are presented in two volumes:

Volume 1 includes the consolidated financial statements of the Gouvernement du Québec audited by the Auditor General of Québec, a financial analysis of these financial statements, the budgetary balance established in accordance with the Balanced Budget Act, the balance of the stabilization reserve as well as changes in main trends, including those of the government’s consolidated revenue and expenditure, net debt and gross debt over 10 fiscal years.

Volume 2 includes the report of excess expenditures and other costs of budgetary departments and bodies over appropriations approved by Parliament and the report of special funds’ excess expenditures and investments over amounts approved by Parliament as well as detailed information for each department, budgetary body, and special fund.

Respectfully yours,

Eric Girard

Minister of Finance

Québec, December 2023

Mr. Eric Girard

Minister of Finance

Parliament Building

Québec

Dear Minister,

In accordance with the commission entrusted to me, I have the honour of presenting the Public Accounts of the Gouvernement du Québec for the fiscal year ended March 31, 2023. These accounts have been prepared under section 86 of the Financial Administration Act (CQLR, chapter A-6.001), in accordance with the government’s accounting policies and the public sector accounting standards.

Respectfully yours,

Lucie Pageau, CPA

Comptroller of Finance

Québec, December 2023

Table of contents

Presentation of the Public Accounts

The Public Accounts 2022-2023 have been prepared by the Comptroller of Finance for the Minister of Finance in accordance with the accounting policies adopted by the Conseil du trésor and the public sector accounting standards and pursuant to the provisions of section 86 of the Financial Administration Act (CQLR, chapter A-6.001). They are published in two volumes. In addition to these volumes, further information is published on the Ministère des Finances website in the section Public Accounts 2022-2023 – In brief.

Volume 1 – Consolidated financial statements of the Gouvernement du Québec

Volume 1 presents the results and financial position of the Gouvernement du Québec. The financial operations include those of the National Assembly, of the people it appoints, of the government departments, and of all bodies, funds and enterprises controlled by the government.

Volume 1 presents a financial analysis to increase the usefulness and transparency of these consolidated financial statements. The analysis includes the highlights for the 2022-2023 fiscal year and compares the actual results with both forecast results forecast in the 2022-2023 budget and the 2021-2022 results. It also presents the government’s budget balance in compliance with the Balanced Budget Act as well as the stabilization reserve’s balance. Finally, it presents the development of main trends relating to important items in the consolidated financial statements and the outcome of the analysis of 11 indicators.

In accordance with the Auditor General Act (CQLR, chapter V-5.01), the Auditor General of Québec prepares an Independent Auditor’s Report included with the government’s consolidated financial statements and in which she expresses her opinion on the financial statements.

Volume 2 – Financial information on the Consolidated Revenue Fund: general fund and special funds

Volume 2 presents the financial information on the Consolidated Revenue Fund, which is made up of the general fund and the special funds. This volume is divided into two sections. The first section shows the revenue of government departments and budget-funded bodies, their authorized appropriations, the expenses and other costs charged to each of these appropriations and, lastly, the financial operations of the specified purpose accounts they administer. The second section presents the revenue of the special funds as well as their approved and realized expenses and investments.

Acknowledgements

Preparing the Public Accounts requires the participation and collaboration of many employees from different government departments, funds, bodies, and organizations in the health and social services, education and higher education networks as well as employees from government enterprises. We would like to thank all of them for their help in preparing these documents.

| PUBLIC ACCOUNTS 2022-2023 | 1 |

CONSOLIDATED

FINANCIAL STATEMENTS

▌ 1. Highlights of the 2022-2023 fiscal year

Summary of consolidated results

Fiscal year ended March 31, 2023

(millions of dollars)

| Budget 2022-2023 (1),(2) | Actual results as at March 31, 2023 | Change compared with Budget | Actual results as at March 31, 2022 (3) | Change compared with the 2021-2022 actual results | ||||||||||||||||||||||||

| M$ | % | (restated) | M$ | % | ||||||||||||||||||||||||

| REVENUE | ||||||||||||||||||||||||||||

| Income and property taxes | 60 506 | 64 521 | 4 015 | 6.6 | 62 328 | 2 193 | 3.5 | |||||||||||||||||||||

| Consumption taxes | 26 706 | 26 597 | (109 | ) | (0.4 | ) | 24 597 | 2 000 | 8.1 | |||||||||||||||||||

| Duties and permits | 5 171 | 5 741 | 570 | 11.0 | 6 057 | (316 | ) | (5.2 | ) | |||||||||||||||||||

| Miscellaneous revenue | 11 680 | 12 083 | 403 | 3.5 | 10 705 | 1 378 | 12.9 | |||||||||||||||||||||

| Revenue from government enterprises | 5 628 | 6 620 | 992 | 17.6 | 5 960 | 660 | 11.1 | |||||||||||||||||||||

| Own-source revenue | 109 691 | 115 562 | 5 871 | 5.4 | 109 647 | 5 915 | 5.4 | |||||||||||||||||||||

| Federal government transfers | 28 790 | 28 737 | (53 | ) | (0.2 | ) | 29 184 | (447 | ) | (1.5 | ) | |||||||||||||||||

| Total revenue | 138 481 | 144 299 | 5 818 | 4.2 | 138 831 | 5 468 | 3.9 | |||||||||||||||||||||

| EXPENDITURE | ||||||||||||||||||||||||||||

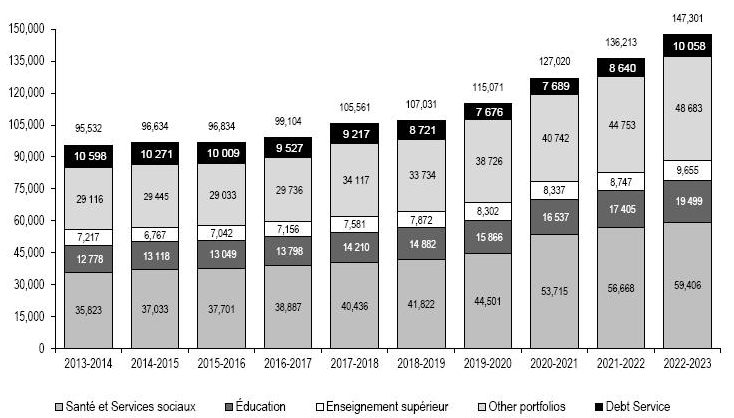

| Santé et Services sociaux | 54 459 | 59 406 | 4 947 | 9.1 | 56 668 | 2 738 | 4.8 | |||||||||||||||||||||

| Éducation | 18 689 | 19 499 | 810 | 4.3 | 17 405 | 2 094 | 12.0 | |||||||||||||||||||||

| Enseignement supérieur | 10 010 | 9 655 | (355 | ) | (3.5 | ) | 8 747 | 908 | 10.4 | |||||||||||||||||||

| Famille | 7 893 | 7 835 | (58 | ) | (0.7 | ) | 7 277 | 558 | 7.7 | |||||||||||||||||||

| Transports et Mobilité durable | 7 115 | 6 451 | (664 | ) | (9.3 | ) | 7 017 | (566 | ) | (8.1 | ) | |||||||||||||||||

| Emploi et Solidarité sociale | 5 390 | 8 983 | 3 593 | 66.7 | 8 385 | 598 | 7.1 | |||||||||||||||||||||

| Affaires municipales et Habitation | 3 929 | 4 928 | 999 | 25.4 | 3 541 | 1 387 | 39.2 | |||||||||||||||||||||

| Économie, Innovation et Énergie | 3 656 | 3 205 | (451 | ) | (12.3 | ) | 3 064 | 141 | 4.6 | |||||||||||||||||||

| Environnement, Lutte contre les changements climatiques, Faune et Parcs | 1 859 | 1 673 | (186 | ) | (10.0 | ) | 1 730 | (57 | ) | (3.3 | ) | |||||||||||||||||

| Others portfolios | 17 144 | 15 608 | (1 536 | ) | (9.0 | ) | 13 739 | 1 869 | 13.6 | |||||||||||||||||||

| Sub-total | 130 144 | 137 243 | 7 099 | 5.5 | 127 573 | 9 670 | 7.6 | |||||||||||||||||||||

| Debt service | 8 842 | 10 058 | 1 216 | 13.8 | 8 640 | 1 418 | 16.4 | |||||||||||||||||||||

| Total expenditure | 138 986 | 147 301 | 8 315 | 6.0 | 136 213 | 11 088 | 8.1 | |||||||||||||||||||||

| Provision for economic risks and other support and recovery measures | 2 500 | (2 500 | ) | (100.0 | ) | |||||||||||||||||||||||

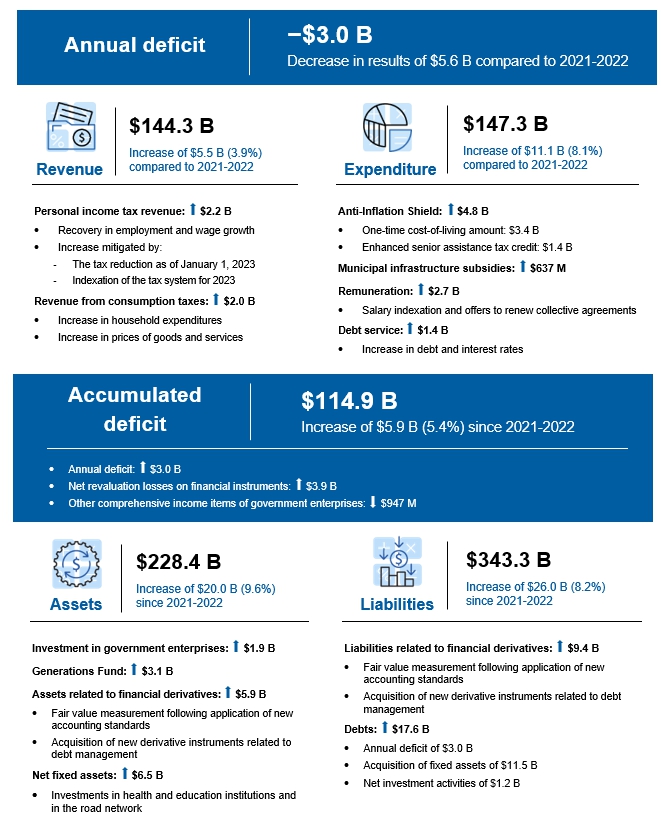

| (DEFICIT) ANNUAL OPERATING SURPLUS | (3 005 | ) | (3 002 | ) | 3 | — | 2 618 | (5 620 | ) | — | ||||||||||||||||||

| (1) | These numbers correspond to data presented in Budget 2022-2023 of the Ministère des Finances tabled on March 22, 2022, adjusted to reflect changes in the composition of portfolios following shifts in ministers’ responsibilities in the fall of 2022. In addition, the forecast related to the change in application of the accounting standard respecting transfer payments as well as certain items that were presented differently in budget have been reclassified in the different portfolios to ensure their comparability with the actual expenditures recorded at March 31, 2023. Details of these reclassifications are presented in Note 3 of the consolidated financial statements. |

| (2) | For the purposes of establishing budget forecasts, certain factors that constitute risk and uncertainty factors do not depend directly on the government but can lead to real results that differ from those anticipated. Such factors are presented in Appendix 1, “Risks and uncertainties”. |

| (3) | Certain figures for 2021-2022 have been reclassified for consistency with the presentation adopted as at March 31, 2023. |

| ANALYSIS OF THE CONSOLIDATED FINANCIAL STATEMENTS | 5 |

1. Highlights of the 2022-2023 fiscal year (cont’d)

| 6 | PUBLIC ACCOUNTS 2022-2023 |

1. Highlights of the 2022-2023 fiscal year (cont’d)

| ANALYSIS OF THE CONSOLIDATED FINANCIAL STATEMENTS | 7 |

1. Highlights of the 2022-2023 fiscal year (cont’d)

Budget balance

In Budget 2022-2023, tabled on March 22, 2022, the government forecast a deficit of $3 005 million for fiscal 2022-2023 as well as a budgetary deficit of $6 450 million within the meaning of the Balanced Budget Act (CQLR, chapter E-12.00001), taking into account the payment of $3 445 million in dedicated revenue to the Generations Fund.

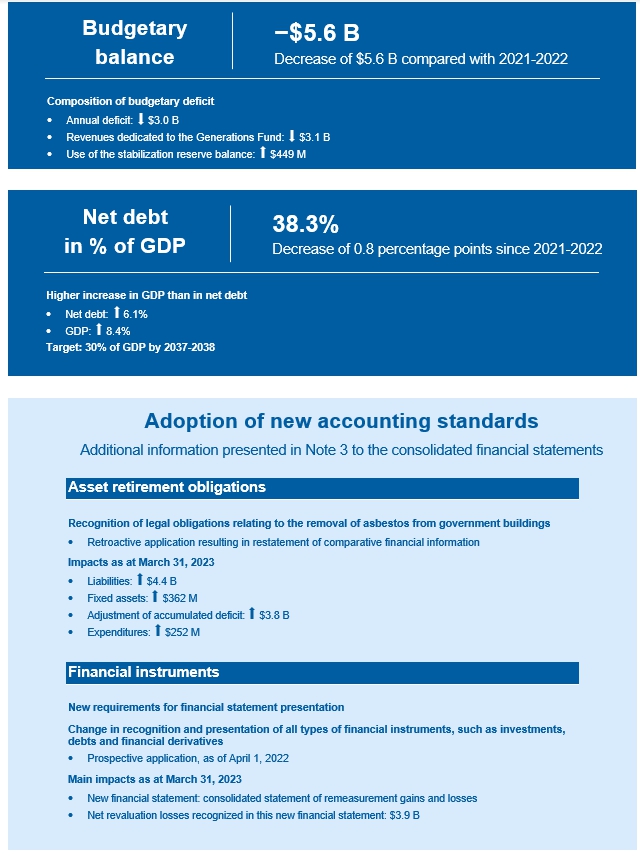

The consolidated financial statements of the Gouvernement du Québec for the fiscal year ended March 31, 2023 show an annual operating deficit of $3 002 million. Taking into account deposits of revenues dedicated to the Generations Fund of $3 082 million, the budgetary balance for the fiscal year ended March 31, 2023 shows a deficit of $6 084 million. Within the meaning of the Balanced Budget Act, after using the entire stabilization reserve, the government’s budgetary balance shows a deficit of $5 635 million.

In 2021-2022, in the context of the pandemic and in order to gradually reduce the deficit without adversely affecting services to Quebecers nor the sustainable recovery of economic growth, the provisions of the Balanced Budget Act prohibiting an actual or forecast budgetary deficit, and those requiring the elimination of any deficit, were suspended. These suspensions remained in effect until 2022-2023. The lifting of these suspensions, announced in the 2023-2024 budget speech, became effective on April 1, 2023. In accordance with the provisions of the Act, the plan to restore fiscal balance that accompanied the 2023-2024 budget provides a framework for forecast deficits until a balanced budget is achieved in 2027-2028.

In accordance with the standards set out by the Public Sector Accounting Board, the financial analysis that accompanies the government’s consolidated financial statements compares real results with those in its initial budget, adjusted to take into account some reclassifications,1 as well as those of the previous fiscal year.

| 1 | The budget forecasts for expenditures by portfolios have been reclassified to ensure comparability with actual expenditures recorded as at March 31, 2023. Details of these reclassifications are presented in Note 3, “Reclassification of comparative financial information” of the consolidated financial statements. |

| 8 | PUBLIC ACCOUNTS 2022-2023 |

2. Variance analysis (cont’d)

Income and property taxes

Fiscal year ended March 31, 2023

(millions of dollars)

| Budget 2022-2023 | Actual results | Change with | Actual results | Change with 2021-2022 actual results | ||||||||||||||||||||||||

| M$ | % | M$ | % | |||||||||||||||||||||||||

| Personal income tax | 41 147 | 42 251 | 1 104 | 2.7 | 40 924 | 1 327 | 3.2 | |||||||||||||||||||||

| Contributions for health services | 7 299 | 7 914 | 615 | 8.4 | 7 402 | 512 | 6.9 | |||||||||||||||||||||

| Corporate taxes | 10 882 | 13 243 | 2 361 | 21.7 | 12 926 | 317 | 2.5 | |||||||||||||||||||||

| School property tax | 1 178 | 1 113 | (65 | ) | (5.5 | ) | 1 076 | 37 | 3.4 | |||||||||||||||||||

| TOTAL | 60 506 | 64 521 | 4 015 | 6.6 | 62 328 | 2 193 | 3.5 | |||||||||||||||||||||

The 2022-2023 forecast of $60 506 million reflected mainly the effects of increased economic activity on tax revenues, including higher personal income tax revenues. This increase was due in particular to growth in household income, which in turn was supported by the recovery in employment and growth in wages and salaries. The forecast for corporate taxes took into account a favourable trend in economic activity, but still reflected a decrease compared with actual results as at March 31, 2022, given the exceptional nature of the increase in the net operating surplus of corporations in 2021-2022, partly supported by non-recurring government support measures related to the pandemic.

The increase in nominal GDP of 8.4% in 2022, compared to the forecast of 6.4% announced in the 2022-2023 budget, essentially reflects stronger-than-expected price growth. This significant rise in prices has translated into favourable trends in tax revenues, up 6.6% compared with the forecast.

The increase in wages and salaries, supported by a strong labour market, had a direct impact on personal income tax revenue and revenue from contributions to health services, explaining a large part of the 2.7% and 8.4% variations from the budget, and the 3.2% and 6.9% increases from the actual results as at March 31, 2022.

The changes associated with personal income tax also take into account the reduction in income attributable to the 1-percentage-point reduction in the first two tax brackets as of January 1, 2023, and the 6.44% indexation of the tax system1 for 2023, linked to the increase in consumer prices.

Moreover, the net operating surplus of corporations, which is higher than in 2021-2022, and its more favourable trend than forecast, account for most of the 2.5% increase in revenues from corporate taxes compared with actual results as at March 31, 2022, and the 21.7% change in revenues from corporate taxes compared with the forecast.

| 1 | Statutory indexation of the main parameters of the personal income tax system, namely the various tax brackets, the basic amount and several deductions and tax credits. The indexation rate is determined by the increase in the Québec consumer price index, excluding alcohol, tobacco and recreational cannabis. |

| ANALYSIS OF THE CONSOLIDATED FINANCIAL STATEMENTS | 9 |

2. Variance analysis (cont’d)

2.1. Own-source revenue (cont’d)

Consumption taxes

Fiscal year ended March 31, 2023

(millions of dollars)

| Budget 2022-2023 | Actual results | Change with 2022-2023 budget | Actual results | Change with 2021-2022 actual results | ||||||||||||||||||||||||

| M$ | % | M$ | % | |||||||||||||||||||||||||

| Sales | 22 940 | 22 911 | (29 | ) | (0.1 | ) | 20 894 | 2 017 | 9.7 | |||||||||||||||||||

| Fuel | 2 141 | 2 157 | 16 | 0.7 | 2 090 | 67 | 3.2 | |||||||||||||||||||||

| Tobacco | 899 | 817 | (82 | ) | (9.1 | ) | 893 | (76 | ) | (8.5 | ) | |||||||||||||||||

| Alcoholic beverages | 637 | 635 | (2 | ) | (0.3 | ) | 638 | (3 | ) | (0.5 | ) | |||||||||||||||||

| Cannabis | 89 | 77 | (12 | ) | (13.5 | ) | 82 | (5 | ) | (6.1 | ) | |||||||||||||||||

| TOTAL | 26 706 | 26 597 | (109 | ) | (0.4 | ) | 24 597 | 2 000 | 8.1 | |||||||||||||||||||

The 2022-2023 forecast of $26 706 million reflected notably the growth in household consumption1 compared with the previous year, supported among other things by reduced uncertainty linked to the pandemic, by government initiatives to offset the rising cost of living, and by the disbursement of a portion of accumulated household savings.

As at March 31, 2023, revenue from consumption taxes, mainly the Québec sales tax, is generally comparable to forecasts, with a downward variation of 0.4%.

Compared with actual results as at March 31, 2022, revenue from consumption taxes is up 8.1%. As forecast, this change is explained by growing domestic demand, despite the mitigating effect of higher interest rates and inflation on household consumption.

Moreover, higher prices for goods and services, exacerbated in particular by supply constraints, rising energy prices, labour shortages and geopolitical tensions, also played a role in the rise in revenue from consumption taxes.

| 1 | Household consumption excluding food expenditures and shelter. |

| 10 | PUBLIC ACCOUNTS 2022-2023 |

2. Variance analysis (cont’d)

2.1. Own-source revenue (cont’d)

Duties and permits

Fiscal year ended March 31, 2023

(millions of dollars)

| Budget 2022-2023 | Actual results | Change with 2022-2023 budget | Actual results | Change with 2021-2022 actual results | ||||||||||||||||||||||||

| M$ | % | M$ | % | |||||||||||||||||||||||||

| Motor vehicles | 1 529 | 1 562 | 33 | 2.2 | 1 525 | 37 | 2.4 | |||||||||||||||||||||

| Natural resources | 1 748 | 2 014 | 266 | 15.2 | 2 371 | (357 | ) | (15.1 | ) | |||||||||||||||||||

| Greenhouse gas emissions | 1 077 | 1 267 | 190 | 17.6 | 1 299 | (32 | ) | (2.5 | ) | |||||||||||||||||||

| Other | 817 | 898 | 81 | 9.9 | 862 | 36 | 4.2 | |||||||||||||||||||||

| TOTAL | 5 171 | 5 741 | 570 | 11.0 | 6 057 | (316 | ) | (5.2 | ) | |||||||||||||||||||

The 2022-2023 forecast of $5 171 million, which was lower than actual results as at March 31, 2022, reflected the especially high level of revenue from duties and permits in 2021-2022, due in particular to non-recurring revenues from the auction of greenhouse gas (GHG) emission allowances. Additional revenues of $664 million were generated in 2021-2022 by the resale of unsold units from the May and August 2020 auctions. Moreover, this forecasted decline also took into account an expected decrease in the economic value of iron, which would affect government royalties from mining operations.

As at March 31, 2023, revenues from duties and permits of $5 741 million exceeded the forecast by 11.0%. This improvement is attributable in particular to a better-than-expected trend in revenue from mining royalties in the average unit price of units sold at the auction of GHG emission allowances.

Compared with actual results for 2021-2022, those for fiscal year 2022-2023 show a decrease of 5.2%, mainly attributable to additional revenues in 2021-2022 from the auction of GHG emission allowances and to variations in mining royalties, influenced by changes in market prices for metals. In this regard, the decrease in mining revenues between the two years can be explained both by the sustained metal prices of recent years and by the significant drop that followed in 2022-2023.

| ANALYSIS OF THE CONSOLIDATED FINANCIAL STATEMENTS | 11 |

2. Variance analysis (cont’d)

2.1. Own-source revenue (cont’d)

| Miscellaneous revenue | ||||

| Fiscal year ended March 31, 2023 | ||||

| (millions of dollars) | ||||

| Budget 2022-2023 | Actual results as at March 31, 2023 | Change with 2022-2023 budget | Actual results as at March 31, 2022 | Change with 2021-2022 actual results | ||||||||||||||||||||||||

| M$ | % | M$ | % | |||||||||||||||||||||||||

| Miscellaneous revenue | 11 680 | 12 083 | 403 | 3.5 | 10 705 | 1 378 | 12.9 | |||||||||||||||||||||

The 2022-2023 forecast of $11 680 million reflected a generalized growth in the various revenues generated by the different organizations that make up the government, particularly those of the health and social services, education and higher education networks. Among other things, the forecast took into account an increase in revenues from tuition fees, linked to an expected growth in the higher education clientele.

Actual miscellaneous revenue as at March 31, 2023 of $12 083 million exceeds the forecast by 3.5%. This variation is due in particular to higher-than-forecast growth in interest income on tax receivables administered by the Agence du revenu du Québec, growth explained in part by the rise in interest rates.

Compared to the previous fiscal year’s actual results, revenue growth can be broken down as follows (millions of dollars):

| Actual results as at March 31, 2023 | Actual results as at March 31, 2022 | Change with 2021-2022 actual results | ||||||||||||||

| M$ | % | |||||||||||||||

| Sales of goods and services | 5 741 | 5 311 | 430 | 8.1 | ||||||||||||

| User contributions | 1 977 | 1 781 | 196 | 11.0 | ||||||||||||

| Income on accounts receivable and loans | 1 052 | 541 | 511 | 94.5 | ||||||||||||

| Income on investments | 525 | 636 | (111 | ) | (17.5 | ) | ||||||||||

| Fines, forfeitures and recoveries | 1 228 | 934 | 294 | 31.5 | ||||||||||||

| Third-party donations | 1 003 | 966 | 37 | 3.8 | ||||||||||||

| Tuition fees | 451 | 410 | 41 | 10.0 | ||||||||||||

| Transfers from entities other than the federal government | 106 | 126 | (20 | ) | (15.9 | ) | ||||||||||

| TOTAL | 12 083 | 10 705 | 1 378 | 12.9 | ||||||||||||

| 12 | PUBLIC ACCOUNTS 2022-2023 |

2. Variance analysis (cont’d)

2.1. Own-source revenue (cont’d)

Miscellaneous revenue (cont’d)

The overall growth of $1 378 million is mainly the result of the increase relating to the sales of goods and services, user contributions as well as income on accounts receivable and loans.

Sales of goods and services

The variation of $430 million is due in particular to the increase in revenues collected by school service centres and school boards, notably for childcare services. This increase is due to revenue losses related to temporary school closures in 2021-2022 linked to the pandemic.

User contributions

The $196-million increase is mainly due to a $143-million increase in revenues from health and social services institutions, attributable among other things to growth in contributions from non-resident users, and to higher revenues from users of adult residential care in rehabilitation centres and residential and long-term care centres, the latter increase being explained in particular by rate increases.

Income on accounts receivable and loans

The $511-million increase is mainly due to higher interest income on tax claims administered by the Agence du revenu du Québec, due to higher interest rates on accounts receivable.

| ANALYSIS OF THE CONSOLIDATED FINANCIAL STATEMENTS | 13 |

2. Variance analysis (cont’d)

2.1. Own-source revenue (cont’d)

Revenue from government enterprises

Fiscal year ended March 31, 2023

(millions of dollars)

| Actual results | Change with | Actual results | Change with | |||||||||||||||||||||||||

| Budget | as at | 2022-2023 | as at | 2021-2022 | ||||||||||||||||||||||||

| 2022-2023 | March 31, 2023 | budget | March 31, 2022 | actual results | ||||||||||||||||||||||||

| M$ | % | M$ | % | |||||||||||||||||||||||||

| Hydro-Québec | 2 525 | 3 665 | 1 140 | 45.1 | 3 059 | 606 | 19.8 | |||||||||||||||||||||

| Société des alcools du Québec | 1 360 | 1 427 | 67 | 4.9 | 1 349 | 78 | 5.8 | |||||||||||||||||||||

| Loto-Québec | 1 383 | 1 597 | 214 | 15.5 | 1 118 | 479 | 42.8 | |||||||||||||||||||||

| Investissement Québec | 256 | (226 | ) | (482 | ) | (188.3 | ) | 341 | (567 | ) | (166.3 | ) | ||||||||||||||||

| Other | 104 | 157 | 53 | 51.0 | 93 | 64 | 68.8 | |||||||||||||||||||||

| TOTAL | 5 628 | 6 620 | 992 | 17.6 | 5 960 | 660 | 11.1 | |||||||||||||||||||||

The 2022-2023 forecast of $5 628 million reflected an increase in revenue from Loto-Québec, due to a return to full operation of its facilities, and a decrease in revenues from Hydro-Québec due to the anticipated drop in the net value of electricity exports.

Hydro-Québec

Contrary to forecasts, supported by sustained economic activity and skyrocketing world energy prices, the net value of Hydro-Québec’s electricity exports increased considerably, explaining both the 45.1% variation compared to the 2022-2023 budget and the 19.8% increase compared to actual results for 2021-2022. The increase compared with 2021-2022 is, however, partially offset by the rise in the corporation’s operating expenses, caused in particular by the growth in the business and the intensification of maintenance activities.

Investissement Québec

Revenues from Investissement Québec were 188.3% lower than forecast, and 166.3% lower than actual results as at March 31, 2022. The unfavourable return on investments in the Venture Capital and Investment Funds portfolio is mainly due to the volatility of rates on the stock markets and the uncertain economic context related to the inflationary environment, restrictive monetary policies and geopolitical risks.

Loto-Québec

The 15.5% variation from the forecast is due in particular to higher-than-expected growth in casino and gaming room customer traffic. In addition to the increase in customer traffic, the 42.8% increase over fiscal year 2022-2023 results from the negative impact of the pandemic on the corporation’s performance in 2021-2022, due in part to the closure of gaming establishments between April and June 2021.

| 14 | PUBLIC ACCOUNTS 2022-2023 |

2. Variance analysis (cont’d)

2.2. Federal government transfers

Federal government transfers

Fiscal year ended March 31, 2023

(millions of dollars)

| Actual results | Change with | Actual results | Change with | |||||||||||||||||||||||||

| Budget | as at | 2022-2023 | as at | 2021-2022 | ||||||||||||||||||||||||

| 2022-2023 | March 31, 2023 | budget | March 31, 2022 | actual results | ||||||||||||||||||||||||

| M$ | % | M$ | % | |||||||||||||||||||||||||

| Equalization | 13 666 | 13 666 | — | — | 13 119 | 547 | 4.2 | |||||||||||||||||||||

| Health transfers | 7 078 | 7 082 | 4 | 0.1 | 8 203 | (1 121 | ) | (13.7 | ) | |||||||||||||||||||

| Transfers for post-secondary education and other social programs | 1 531 | 1 294 | (237 | ) | (15.5 | ) | 1 529 | (235 | ) | (15.4 | ) | |||||||||||||||||

| Other programs | 6 515 | 6 695 | 180 | 2.8 | 6 333 | 362 | 5.7 | |||||||||||||||||||||

| TOTAL | 28 790 | 28 737 | (53 | ) | (0.2 | ) | 29 184 | (447 | ) | (1.5 | ) | |||||||||||||||||

The 2022-2023 forecast of $28 790 million assumed that certain federal government transfers resulting from agreements reached in the context of the pandemic were non-recurring.

As at March 31, 2023, federal government transfers of $28 737 million are essentially in line with the forecast, with a downward variation of $53 million, or 0.2%.

This variation is mainly attributable to a higher-than-forecast increase in the value of the Québec special abatement,1 resulting in a greater-than-forecast decrease of $361 million in transfers for health, and of $222 million in transfers for post-secondary education and other social programs.

Moreover, the following items partially offset this downward variation compared with the forecast:

| ● | a one-time transfer of $450 million in 2022-2023, under the Canada Health Transfer, to catch up on surgeries; |

| ● | higher-than-forecast revenues of $180 million from the “Other programs” category, due in particular to transfer revenues from the federal government for personal protective equipment (PPE) and other supplies received and used by March 31, 2023. |

| 1 | The Québec special abatement (16.5% of federal personal income tax collected in Québec) is subtracted from federal government transfer revenues. |

| ANALYSIS OF THE CONSOLIDATED FINANCIAL STATEMENTS | 15 |

2. Variance analysis (cont’d)

2.2. Federal government transfers (cont’d)

Compared with actual results for 2021-2022, those for 2022-2023 show a decrease of $447 million, due to the net impact of the following items:

Equalization

The growth of $547 million, or 4.2%, in equalization revenues is explained by the increase in the equalization envelope across Canada, whose growth is linked to that of Canada’s nominal GDP.

Health transfers

The $1 121-million decrease in health transfers is due in particular to:

| ● | one-time transfers in 2021-2022, including: |

| ¾ | $902 million as a supplementary Canada Health Transfer to support Québec in managing the pandemic, |

| ¾ | $226 million for Canada’s COVID-19 immunization plan, |

| ¾ | $221 million for the long-term care component of the health funding agreement; |

| ● | a $361-million decrease due to an upward revision in the value of the Québec special abatement, a portion of which is subtracted from the Canada Health Transfer. |

The decrease is partially offset by:

| ● | a one-time transfer of $450 million in 2022-2023 from the Canada Health Transfer to catch up on surgeries; |

| ● | an increase of $402 million in 2022-2023 related to the indexation of the Canada Health Transfer. |

Transfers for post-secondary education and other social programs

The $235-million decrease is mainly due to the increase of the value of the Québec special abatement,1 a portion of which is deducted from the Canada Social Transfer, reducing transfer revenues for post-secondary education and other social programs by $221 million.

Other programs

The $362-million increase in transfer revenues for other programs is explained by various changes:

| ● | a $341-million increase in revenues from the asymmetrical childcare agreement signed in 2021-2022 for a period of 5 years; |

| ● | an additional transfer of $197 million from the federal government to support public transit authorities in the wake of the pandemic; |

| ● | an increase of $152 million in transfers related to the gas tax and Québec contribution programs, mainly for the “Infrastructure and drinking water” component. |

| 16 | PUBLIC ACCOUNTS 2022-2023 |

2. Variance analysis (cont’d)

2.2. Federal government transfers (cont’d)

Other programs (cont’d)

These increases are largely offset by:

| ● | the downward variation of $235 million related to the increase in reimbursements under the youth allowance program, reimbursements which are deducted from revenues; |

| ● | a $239-million decrease in federal transfer revenues related to pandemic-related personal protective equipment (PPE) and other supplies received and used by March 31, 2023; |

| ● | the one-time transfer in 2021-2022 of $130 million related to the Safe Return to Class Fund agreement, aimed at ensuring the safety of students and staff in the context of the pandemic. |

| ANALYSIS OF THE CONSOLIDATED FINANCIAL STATEMENTS | 17 |

2. Variance analysis (cont’d)

Santé et services sociaux

Fiscal year ended March 31, 2023

(millions of dollars)

| Actual results | Change with | Actual results | Change with | |||||||||||||||||||||||||

| Budget | as at | 2022-2023 | as at | 2021-2022 | ||||||||||||||||||||||||

| 2022-2023 | March 31, 2023 | budget | March 31, 2022 | actual results | ||||||||||||||||||||||||

| M$ | % | (restated) | M$ | % | ||||||||||||||||||||||||

| Transfers | 8 168 | 6 626 | 1 542 | 23.3 | ||||||||||||||||||||||||

| Remuneration | 36 490 | 35 969 | 521 | 1.4 | ||||||||||||||||||||||||

| Operating | 14 627 | 13 996 | 631 | 4.5 | ||||||||||||||||||||||||

| Doubtful accounts and other allowances | 121 | 77 | 44 | 57.1 | ||||||||||||||||||||||||

| TOTAL | 54 459 | 59 406 | 4 947 | 9.1 | 56 668 | 2 738 | 4.8 | |||||||||||||||||||||

This portfolio includes mainly the activities of the health and social services network institutions and the programs administered by the Régie de l’assurance maladie du Québec. It also includes the expenditures of other health-related government agencies such as Héma-Québec.

Change with 2022-2023 budget

This portfolio’s expenditures for 2022-2023, at $59 406 million, exceeded forecasts by $4 947 million, a variation of 9.1%. This variance is mainly due to:

| ● | an increase in the senior assistance refundable tax credit announced in the Update on Québec’s Economic and Financial Situation – Fall 2022, resulting in an additional expenditure of $1 444 million. |

The residual variance of $3 503 million is explained in particular by:

| ● | higher-than-anticipated operating expenses, due to higher-than-anticipated inflation in the prices of goods and services; |

| ● | higher-than-expected pandemic management costs, particularly for personal protective equipment (PPE) and other supplies; |

| ● | salary provisions arising from government offers tabled in December 2022, including a lump-sum remuneration to all employees on duty during the 2022-2023 fiscal year. |

Change with 2021-2022 actual results

The growth of $2 738 million, compared with actual results for 2021-2022, is essentially due to higher expenses for transfers, remuneration and operations.

| 18 | PUBLIC ACCOUNTS 2022-2023 |

2. Variance analysis (cont’d)

2.3. Consolidated expenditure (cont’d)

Santé et services sociaux (cont’d)

Transfers

The $1 542-millions increase in transfer expenditures is primarily due to a $1 444-millions increase attributable to an increase in the amount for the senior assistance refundable tax credit starting in 2022.

Remuneration

The $521-million increase in remuneration expenses was mainly due to:

| ● | salary provisions arising from government offers tabled in December 2022 as part of the renewal of collective agreements; |

| ● | an increase in pension plan expenses due to the growth in assessable payroll contributions by plan members; |

| ● | salary indexations and increments. |

These increases are partially offset by additional one-time expenses incurred by health and social services institutions to manage the pandemic in 2021-2022, including remuneration of personnel working for the vaccination campaign and the allocation of incentive bonuses in the health sector.

Operating

The $631-million increase in operating expenses was mainly due to:

| ● | a $428-million increase in expenditures by health and social services institutions, relating in particular to the costs of drugs, food, medical and surgical supplies, as well as maintenance and repairs; |

| ● | a $355-million write-down in the value of personal protective equipment (PPE) and other supplies in inventory as at March 31, 2023, to reflect the decline in the market value of this equipment. |

| ANALYSIS OF THE CONSOLIDATED FINANCIAL STATEMENTS | 19 |

2. Variance analysis (cont’d)

2.3. Consolidated expenditure (cont’d)

Éducation

Fiscal year ended March 31, 2023

(millions of dollars)

| Actual results | Change with | Actual results | Change with | |||||||||||||||||||||||||

| Budget | as at | 2022-2023 | as at | 2021-2022 | ||||||||||||||||||||||||

| 2022-2023 | March 31, 2023 | budget | March 31, 2022 | actual results | ||||||||||||||||||||||||

| M$ | % | (restated) | M$ | % | ||||||||||||||||||||||||

| Transfers | 1 095 | 1 016 | 79 | 7.8 | ||||||||||||||||||||||||

| Remuneration | 14 194 | 12 836 | 1 358 | 10.6 | ||||||||||||||||||||||||

| Operating | 4 200 | 3 548 | 652 | 18.4 | ||||||||||||||||||||||||

| Doubtful accounts and other allowances | 10 | 5 | 5 | 100.0 | ||||||||||||||||||||||||

| TOTAL | 18 689 | 19 499 | 810 | 4.3 | 17 405 | 2 094 | 12.0 | |||||||||||||||||||||

This portfolio mainly covers the activities of preschool, primary and secondary education institutions. It also includes programs to promote leisure and sports activities, and to manage national parks.

Change with 2022-2023 budget

Expenditure in this portfolio was $810 million higher than forecast. This was mainly due to:

| ● | a faster-than-anticipated complete recovery of school service centre and school board activities, resulting in higher-than-anticipated expenditures; |

| ● | higher-than-anticipated expenses for school transportation, following the renewal of agreements with transport companies in 2022-2023; |

| ● | salary provisions arising from government offers tabled in December 2022, including a lump-sum remuneration to all employees in service during the 2022-2023 fiscal year. |

Change with 2021-2022 actual results

The $2 094-million increase in expenditures compared with actual results for 2021-2022 stems primarily from higher remuneration and operating expenses.

| 20 | PUBLIC ACCOUNTS 2022-2023 |

2. Variance analysis (cont’d)

2.3. Consolidated expenditure (cont’d)

Éducation (cont’d)

Remuneration

The $1 358-million increase in remuneration expenses was mainly due to:

| ● | salary indexations, increments and an increase in the number of teachers linked to the rise in the number of students; |

| ● | provisions arising from government offers tabled in December 2022 as part of the renewal of collective agreements; |

| ● | changes in pension plan expenses as a result of growth in assessable payroll contributions by plan members. |

Operating

The $652-million increase in operating expenses is explained in particular by the rise in the cost of school transport, due notably to the renewal of contracts, by the increase in building maintenance expenses, and by the complete post-pandemic resumption of sports, cultural and extracurricular activities.

| ANALYSIS OF THE CONSOLIDATED FINANCIAL STATEMENTS | 21 |

2. Variance analysis (cont’d)

2.3. Consolidated expenditure (cont’d)

Enseignement supérieur

Fiscal year ended March 31, 2023

(millions of dollars)

| Actual results | Change with | Actual results | Change with | |||||||||||||||||||||||||

| Budget | as at | 2022-2023 | as at | 2021-2022 | ||||||||||||||||||||||||

| 2022-2023 | March 31, 2023 | budget | March 31, 2022 | actual results | ||||||||||||||||||||||||

| M$ | % | (restated) | M$ | % | ||||||||||||||||||||||||

| Transfers | 4 597 | 4 095 | 502 | 12.3 | ||||||||||||||||||||||||

| Remuneration | 3 958 | 3 675 | 283 | 7.7 | ||||||||||||||||||||||||

| Operating | 1 119 | 981 | 138 | 14.1 | ||||||||||||||||||||||||

| Doubtful accounts and other allowances | (19 | ) | (4 | ) | (15 | ) | 375.0 | |||||||||||||||||||||

| TOTAL | 10 010 | 9 655 | (355 | ) | (3.5 | ) | 8 747 | 908 | 10.4 | |||||||||||||||||||

This portfolio mainly comprises expenditures on college and university educational institutions. It also includes student financial assistance.

Change with 2022-2023 budget

Expenditures in this portfolio were $355 million lower than forecast. This variance can be explained in particular by:

| ● | a decline in the number of students enrolled in general and vocational colleges (CEGEPs), when an increase had been forecast; |

| ● | lower-than-anticipated expenditures for the Perspective Québec bursary program, effective as of the fall 2022 college and university sessions and designed to promote access to post-secondary studies in targeted programs of study. This variation is explained by a lower-than-expected clientele. |

Change with 2021-2022 actual results

The $908-million increase in expenditures compared with actual results for 2021-2022 stems primarily from higher transfer and remuneration expenses.

| 22 | PUBLIC ACCOUNTS 2022-2023 |

2. Variance analysis (cont’d)

2.3. Consolidated expenditure (cont’d)

Enseignement supérieur (cont’d)

Transfers

The $502-million increase in transfer expenditures is mainly due to:

| ● | an increase of $220 million attributable to higher grants to private universities, notably to reflect the 2022-2023 salary indexation, as well as additional investments in higher education announced in the 2022-2023 budget to improve higher education graduation rates; |

| ● | an increase of $125 million related to the Perspectives Québec bursary program, effective as of the fall 2022 college and university sessions. |

Remuneration

The $283-million increase in remuneration expenses is mainly attributable to:

| ● | staff increments and salary indexations; |

| ● | salary provisions relating to government offers tabled in December 2022 as part of the renewal of collective agreements. |

| ANALYSIS OF THE CONSOLIDATED FINANCIAL STATEMENTS | 23 |

2. Variance analysis (cont’d)

2.3. Consolidated expenditure (cont’d)

Famille

Fiscal year ended March 31, 2023

(millions of dollars)

| Actual results | Change with | Actual results | Change with | |||||||||||||||||||||||||

| Budget | as at | 2022-2023 | as at | 2021-2022 | ||||||||||||||||||||||||

| 2022-2023 | March 31, 2023 | budget | March 31, 2022 | actual results | ||||||||||||||||||||||||

| M$ | % | M$ | % | |||||||||||||||||||||||||

| Transfers | 7 627 | 7 088 | 539 | 7.6 | ||||||||||||||||||||||||

| Remuneration | 117 | 105 | 12 | 11.4 | ||||||||||||||||||||||||

| Operating | 91 | 84 | 7 | 8.3 | ||||||||||||||||||||||||

| Doubtful accounts and other allowances | ― | — | — | — | ||||||||||||||||||||||||

| TOTAL | 7 893 | 7 835 | (58 | ) | (0.7 | ) | 7 277 | 558 | 7.7 | |||||||||||||||||||

This portfolio mainly includes expenses dedicated to the financing of educational childcare services and financial assistance for families.

Change with 2022-2023 budget

Actual results for 2022-2023, amounting to $7 835 million, are comparable to the forecast.

Change with 2021-2022 actual results

Actual results show growth of $558 million compared with 2021-2022, mainly due to higher transfer expenditures.

Transfers

The $539-million increase in transfer expenditures is mainly due to:

| ● | a $193-million increase in subsidies to childcare centres (CPEs) and daycare centres, due in particular to salary increases resulting from the new national agreement signed in December 2021, feedback for management staff resulting from the agreement in principle signed in December 2022, and the creation of new places in the network in 2022-2023; |

| ● | a $122-million increase in expenses associated with the family allowance tax credit, due to indexation of the credit by 2.64% as of January 1, 2022, and by 6.44% as of January 1, 2023. |

| 24 | PUBLIC ACCOUNTS 2022-2023 |

2. Variance analysis (cont’d)

2.3. Consolidated expenditure (cont’d)

Transport et Mobilité durable

Fiscal year ended March 31, 2023

(millions of dollars)

| Actual results | Change with | Actual results | Change with | |||||||||||||||||||||||||

| Budget | as at | 2022-2023 | as at | 2021-2022 | ||||||||||||||||||||||||

| 2022-2023 | March 31, 2023 | budget | March 31, 2022 | actual results | ||||||||||||||||||||||||

| M$ | % | (restated) | M$ | % | ||||||||||||||||||||||||

| Transfers | 2 699 | 3 500 | (801 | ) | (22.9 | ) | ||||||||||||||||||||||

| Remuneration | 708 | 677 | 31 | 4.6 | ||||||||||||||||||||||||

| Operating | 3 035 | 2 832 | 203 | 7.2 | ||||||||||||||||||||||||

| Doubtful accounts and other allowances | 9 | 8 | 1 | 12.5 | ||||||||||||||||||||||||

| TOTAL | 7 115 | 6 451 | (664 | ) | (9.3 | ) | 7 017 | (566 | ) | (8.1 | ) | |||||||||||||||||

This portfolio mainly includes expenditures for the construction, maintenance and operation of road infrastructure, as well as the financing of public transit services. Expenditures also include management of the government’s fleet of rolling stock, aircrafts and ferry services.

Change with 2022-2023 budget

Actual results for 2022-2023, in the amount of $6 451 million, were $664 million below the forecast. This difference is mainly due to:

| ● | subsidies granted for municipal infrastructure and public transit projects that were $586 million lower than forecast, mainly due to the fact that less work was carried out than anticipated; |

| ● | expenditures $373 million lower than forecast due to additional delays in the approval of certain projects under the Programme d’aide gouvernementale d’infrastructures en transport collectif (PAGITC), thus delaying the completion of work scheduled for March 31, 2023. |

This downward variation is partially offset by:

| ● | the granting of an additional $200 million subsidy to the Autorité régionale de transport métropolitain (ARTM) in March 2023, announced as part of the 2023-2024 budget, to support the revival of public transit and help maintain services despite declining ridership; |

| ● | advance payments1 of financial assistance totalling $500 million for infrastructure projects included in the Québec Infrastructure Plan (QIP) 2023-2033, generating expenditures not provided for in the 2022-2023 budget: |

| 1 | This is the financial assistance paid by the government for infrastructure projects before the work is carried out by the recipients. |

| ANALYSIS OF THE CONSOLIDATED FINANCIAL STATEMENTS | 25 |

2. Variance analysis (cont’d)

2.3. Consolidated expenditure (cont’d)

Transport et Mobilité durable (cont’d)

| ¾ | $237 million to the Réseau de transport de la Capitale (RTC) for preparatory work on Québec city’s structuring public transit network project, |

| ¾ | $146 million to the ARTM to contribute to projects aimed at integrating its operations with those of the Réseau express métropolitain (REM), |

| ¾ | $117 million paid to the Société de transport de Laval (STL) for an infrastructure expansion project to increase their capacity and accommodate electric buses. |

Change with 2021-2022 actual results

The $566-million reduction in expenditures compared with actual results for 2021-2022 is primarily due to a decrease in transfer expenditures, partially offset by an increase in operating expenditures.

Transfers

The $801-million decrease in transfer expenditures compared with 2021-2022 is mainly due to:

| ● | a $1 019-million decrease in grants for municipal infrastructure and public transit projects, due to: |

| ¾ | the advance payment1 of $1 120 million in financial assistance for infrastructure projects to the Société de transport de Montréal (STM) in 2021-2022, |

| ¾ | a $399-million decrease in the cost of work compared with the previous year; |

this decrease in partially offset by anticipated payments1 of public transit subsidies totalling $500 million in 2022-2023, namely $237 million granted to the RTC, $146 million granted to the ARTM, and $117 million granted to the STL;

| ● | the $100-million increase in 2022-2023 in subsidies to support public transit authorities faced with the repercussions of the COVID-19 pandemic, subsidies which are granted through the emergency public transit assistance program (PAUTCP) in the continuation of the Safe Restart Agreement; |

| ● | an increase of $105 million in one-time assistance allocated to the ARTM to support the recovery of public transit. |

Operating

The $203-million increase in operating expenditures is mainly due to higher spending on road snow removal, attributable to higher costs for contracts, salt and fuel.

| 1 | This is the financial assistance paid by the government for infrastructure projects before the work is carried out by the recipients. |

| 26 | PUBLIC ACCOUNTS 2022-2023 |

2. Variance analysis (cont’d)

2.3. Consolidated expenditure (cont’d)

Emploi et Solidarité sociale

Fiscal year ended March 31, 2023

(millions of dollars)

| Actual results | Change with | Actual results | Change with | |||||||||||||||||||||||||

| Budget | as at | 2022-2023 | as at | 2021-2022 | ||||||||||||||||||||||||

| 2022-2023 | March 31, 2023 | budget | March 31, 2022 | actual results | ||||||||||||||||||||||||

| M$ | % | M$ | % | |||||||||||||||||||||||||

| Transfers | 8 372 | 7 811 | 561 | 7.2 | ||||||||||||||||||||||||

| Remuneration | 442 | 410 | 32 | 7.8 | ||||||||||||||||||||||||

| Operating | 145 | 140 | 5 | 3.6 | ||||||||||||||||||||||||

| Doubtful accounts and other allowances | 24 | 24 | — | — | ||||||||||||||||||||||||

| TOTAL | 5 390 | 8 983 | 3 593 | 66.7 | 8 385 | 598 | 7.1 | |||||||||||||||||||||

This portfolio mainly includes expenditures on financial assistance programs for individuals, including last-resort assistance and employment assistance programs. Expenditures related to the activities of Services Québec, the Directeur de l’état civil and the Registraire des entreprises, as well as to the administration of the Québec Parental Insurance Plan, are also included in this portfolio.

Change with 2022-2023 budget

Actual results for 2022-2023, amounting to $8 983 million, exceeded forecasts by $3 593 million. This variation is mainly due to:

| ● | a one-time payment to cope with the rising cost of living, announced when the Update on Québec’s Economic and Financial Situation – Fall 2022 was tabled. The expenditure associated with this measure amounts to $3 367 million; |

| ● | the payment of an additional $100 million envelope in March 2023 when the 2023-2024 budget was tabled, earmarked for the short-term training program to support businesses experiencing recruitment difficulties. |

Change with 2021-2022 actual results

The $598-million increase in expenditures compared with actual results for 2021-2022 is essentially due to higher transfer expenditures.

| ANALYSIS OF THE CONSOLIDATED FINANCIAL STATEMENTS | 27 |

2. Variance analysis (cont’d)

2.3. Consolidated expenditure (cont’d)

Emploi et Solidarité sociale (cont’d)

Transfers

The $561-million increase in transfers is mainly due to:

| ● | a one-time payment to cope with the rising cost of living, announced when the Update on Québec’s Economic and Financial Situation – Fall 2022 was tabled. The expenditure associated with this measure amounts to $3 367 million; |

| ● | an increase of $287 million in costs associated with the last-resort financial assistance, due to an increase in the clientele following the significant increase in 2022-2023 from asylum seekers, and to the annual indexation of benefits. This growth is also due to the increase in benefits resulting from the Government Action Plan to Foster Economic Inclusion and Social Participation, which aims to help more than 100 000 people out of poverty and increase the income of people living in poverty; |

| ● | an increase of $215 million in participation allowances granted by the Labour Market Development Fund to support integration into the labour market. This increase is explained in particular by the revision of the policy concerning income support granted to participants; |

| ● | an increase of $155 million for various employment assistance measures, including the announcement, in the 2023-2024 budget, of an additional $100 million for the short-term training program. |

This increase is partially offset by expenditures arising from measures announced in 2021-2022 to mitigate the increase in the cost of living, namely $2 994 million for the one-time amount and $681 million for the exceptional allowance.

| 28 | PUBLIC ACCOUNTS 2022-2023 |

2. Variance analysis (cont’d)

2.3. Consolidated expenditure (cont’d)

Affaires municipales et Habitation

Fiscal year ended March 31, 2023

(millions of dollars)

| Actual results | Change with | Actual results | Change with | |||||||||||||||||||||||||

| Budget | as at | 2022-2023 | as at | 2021-2022 | ||||||||||||||||||||||||

| 2022-2023 | March 31, 2023 | budget | March 31, 2022 | actual results | ||||||||||||||||||||||||

| M$ | % | (restated) | M$ | % | ||||||||||||||||||||||||

| Transfers | 4 624 | 3 430 | 1 194 | 34.8 | ||||||||||||||||||||||||

| Remuneration | 117 | 115 | 2 | 1.7 | ||||||||||||||||||||||||

| Operating | 176 | 163 | 13 | 8.0 | ||||||||||||||||||||||||

| Doubtful accounts and other allowances | 11 | (167 | ) | 178 | (106.6 | ) | ||||||||||||||||||||||

| TOTAL | 3 929 | 4 928 | 999 | 25.4 | 3 541 | 1 387 | 39.2 | |||||||||||||||||||||

This portfolio mainly includes expenditures on financial support for municipalities, notably for infrastructure, social housing and compensation in lieu of taxes, as well as regional and metropolitan development measures.

Change with 2022-2023 budget

Actual results for 2022-2023, amounting to $4 928 million, exceed the forecast by $999 million. This variation is mainly due to:

| ● | subsidies granted for municipal infrastructure projects that were $720 million higher than forecast, a change which was due in particular to larger-than-anticipated projects, as well as subsidy adjustments relating to work carried out in previous years; |

| ● | certain measures announced after the 2022-2023 budget, including: |

| ¾ | subsidies totalling $225 million for the construction of 3 000 social and affordable housing units through a partnership with tax-advantaged funds and Desjardins, announced when the Update on Québec’s Economic and Financial Situation – Fall 2022 was tabled, |

| ¾ | expenses of $251 million announced when the 2023-2024 budget was tabled to accelerate and support the purchase and construction of social and affordable housing. |

Change with 2021-2022 actual results

The $1 387-million increase compared with actual results for 2021-2022 is mainly due to higher transfer expenditures and higher doubtful accounts and other allowances.

| ANALYSIS OF THE CONSOLIDATED FINANCIAL STATEMENTS | 29 |

2. Variance analysis (cont’d)

2.3. Consolidated expenditure (cont’d)

Affaires municipales et Habitation (cont’d)

Transfers

The $1 194-million change in transfer expenditures compared with the previous year’s results is essentially due to the following factors:

| ● | $637 million in additional subsidies granted for municipal infrastructure projects, owing in particular to more substantial work than in 2021-2022 and subsidy adjustments relating to work carried out in previous years; |

| ● | $225 million in subsidies to support the construction of 3 000 social and affordable housing units through a partnership with tax-advantaged funds and Desjardins, announced when the Update on Québec’s Economic and Financial Situation – Fall 2022 was tabled; |

| ● | $145 million to support the RCMs’ local and regional development efforts as part of the 2020-2024 partnership of the Regions and Rurality Fund. |

Doubtfoul accounts and other allowances

The change in expenses for doubtful accounts and other allowances compared with the previous year is mainly due to the introduction, in 2021-2022, of the Société d’habitation du Québec (SHQ) financial assistance program to preserve community housing stock, which has resulted in a downward revision of the provision for losses on loan guarantees by $155 million as at March 31, 2022.

| 30 | PUBLIC ACCOUNTS 2022-2023 |

2. Variance analysis (cont’d)

2.3. Consolidated expenditure (cont’d)

Économie, Innovation et Énergie

Fiscal year ended March 31, 2023

(millions of dollars)

| Actual results | Change with | Actual results | Change with | |||||||||||||||||||||||||

| Budget | as at | 2022-2023 | as at | 2021-2022 | ||||||||||||||||||||||||

| 2022-2023 | March 31, 2023 | budget | March 31, 2022 | actual results | ||||||||||||||||||||||||

| M$ | % | M$ | % | |||||||||||||||||||||||||

| Transfers | 2 744 | 2 763 | (19 | ) | (0.7 | ) | ||||||||||||||||||||||

| Remuneration | 83 | 81 | 2 | 2.5 | ||||||||||||||||||||||||

| Operating | 179 | 173 | 6 | 3.5 | ||||||||||||||||||||||||

| Doubtful accounts and other allowances | 199 | 47 | 152 | 323.4 | ||||||||||||||||||||||||

| TOTAL | 3 656 | 3 205 | (451 | ) | (12.3 | ) | 3 064 | 141 | 4.6 | |||||||||||||||||||

This portfolio mainly includes expenditures dedicated to financing economic development projects, as well as supporting research, innovation and the development of energy resources.

Change with 2022-2023 budget

Actual results for 2022-2023, amounting to $3 205 million, were lower than forecast by $451 million. This variance is notably due to the fact that investment files under the Economic Development Fund progressed differently than planned, resulting in a lower-than-expected provision for doubtful accounts.

Change with 2021-2022 actual results

The $141-million increase in expenditures compared with actual results for 2021-2022 is mainly due to the $152-million increase in the expense for doubtful accounts and other allowances which was exceptionally low as at March 31, 2022 due to the revision of the valuation allowance on certain loans as a result of the improved risk of non-recovery.

| ANALYSIS OF THE CONSOLIDATED FINANCIAL STATEMENTS | 31 |

2. Variance analysis (cont’d)

2.3. Consolidated expenditure (cont’d)

Environnement, Lutte contre les changements climatiques, Faune et Parcs

Fiscal year ended March 31, 2023

(millions of dollars)

| Actual results | Change with | Actual results | Change with | |||||||||||||||||||||||||

| Budget | as at | 2022-2023 | as at | 2021-2022 | ||||||||||||||||||||||||

| 2022-2023 | March 31, 2023 | budget | March 31, 2022 | actual results | ||||||||||||||||||||||||

| M$ | % | M$ | % | |||||||||||||||||||||||||

| Transfers | 1 083 | 1 097 | (14 | ) | (1.3 | ) | ||||||||||||||||||||||

| Remuneration | 293 | 274 | 19 | 6.9 | ||||||||||||||||||||||||

| Operating | 293 | 356 | (63 | ) | (17.7 | ) | ||||||||||||||||||||||

| Doubtful accounts and other allowances | 4 | 3 | 1 | 33.3 | ||||||||||||||||||||||||

| TOTAL | 1 859 | 1 673 | (186 | ) | (10.0 | ) | 1 730 | (57 | ) | (3.3 | ) | |||||||||||||||||

This portfolio mainly includes expenditures on measures to fight climate change, protect the environment and conserve biodiversity. These expenditures also include the operation of public dams, land management of the State’s water domain, and the conservation of wildlife resources and their habitats.

Change with 2022-2023 budget

Expenditure for the portfolio was $186 million lower than forecast. This is due to a number of variations, including lower-than-anticipated expenditures in the form of subsidies for businesses in the industrial sector to support their plans to reduce GHG emissions, and in the form of investments to maximize the efficient use of energy and replace fossil fuels with electricity and other renewable energies. The lower-than-expected subsidies are due in particular to less substantial work than anticipated.

Change with 2021-2022 actual results

Actual results for 2022-2023 are comparable to those for 2021-2022, with a slight decrease of $57 million compared with the previous year’s results.

| 32 | PUBLIC ACCOUNTS 2022-2023 |

2. Variance analysis (cont’d)

2.3. Consolidated expenditure (cont’d)

Other portfolios

Fiscal year ended March 31, 2023

(millions of dollars)

| Budget 2022-2023 | Actual results as at March 31, 2023 | Change with 2022-2023 budget | Actual results as at March 31, 2022 | Change with 2021-2022 actual results | ||||||||||||||||||||||||

| M$ | % | (restated) | M$ | % | ||||||||||||||||||||||||

| Conseil du trésor et Administration gouvernementale | ||||||||||||||||||||||||||||

| Transfers | 68 | 51 | 17 | 33.3 | ||||||||||||||||||||||||

| Remuneration | 863 | 843 | 20 | 2.4 | ||||||||||||||||||||||||

| Operating | 195 | 231 | (36 | ) | (15.6 | ) | ||||||||||||||||||||||

| Doubtful accounts and other allowances | 1 | 1 | — | — | ||||||||||||||||||||||||

| Sub-total | 2 419 | 1 127 | (1 292 | ) | (53.4 | ) | 1 126 | 1 | 0.1 | |||||||||||||||||||

| Others | ||||||||||||||||||||||||||||

| Transfers | 5 799 | 5 103 | 696 | 13.6 | ||||||||||||||||||||||||

| Remuneration | 5 131 | 4 680 | 451 | 9.6 | ||||||||||||||||||||||||

| Operating | 3 187 | 2 523 | 664 | 26.3 | ||||||||||||||||||||||||

| Doubtful accounts and other allowances | 364 | 307 | 57 | 18.6 | ||||||||||||||||||||||||

| Sub-total | 14 725 | 14 481 | (244 | ) | (1.7 | ) | 12 613 | 1 868 | 14.8 | |||||||||||||||||||

| Total | 17 144 | 15 608 | (1 536 | ) | (9.0 | ) | 13 739 | 1 869 | 13.6 | |||||||||||||||||||

This group includes expenditures from the 16 other portfolios, which comprise, in particular, programs in the cultural, immigration, tourism, and natural resources sectors, as well as the activities of the judicial system, the public safety sector, the international relations sector, the legislative branch and central agencies.1 This group also includes sums provided for in the Contingency Fund of the Conseil du trésor et Administration gouvernementale portfolio. These sums aim to cover unexpected expenses that may arise in any of the government’s programs in the various portfolios. However, actual expenses financed by the contingency fund are recognized in the portfolios that benefited from them.

1 | Ministère des Finances, Ministère du Conseil exécutif and Secrétariat du Conseil du trésor. |

| ANALYSIS OF THE CONSOLIDATED FINANCIAL STATEMENTS | 33 |

2. Variance analysis (cont’d)

2.3. Consolidated expenditure (cont’d)

Other portfolios (cont’d)

Change with 2022-2023 budget

As at March 31, 2023, other portfolio expenditures of $15 608 million were $1 536 million lower than forecast. The share attributable to the Conseil du trésor et Administration gouvernementale portfolio is due in particular to various recourses of the Contingency Fund in order to make up for insufficient resources in certain programs, including:

| ● | recourses totalling $327 million for the Emploi et Solidarité sociale portfolio, mainly due to an unplanned increase of $219 million in last-resort financial assistance and the announcement of an additional envelope of $100 million when the 2023-2024 budget was tabled, intended for the short-term training program to support businesses experiencing recruitment difficulties; |

| ● | a recourse of $200 million for the benefit of the Transport et Mobilité durable portfolio for additional financial assistance announced in the 2023-2024 budget to support the recovery of public transit, |

| ● | a recourse of $198 million for the Transport et Mobilité durable portfolio relating to advance payments of subsidies, totalling $500 million, for public transit at the RTC, ARTM and STL; |

| ● | recourses totalling $225 million for the Affaires municipales et Habitation portfolio relating to subsidies to support the construction of 3 000 social and affordable housing units through a partnership with tax-advantaged funds and Desjardins; |

| ● | a recourse of $154 million for the Affaires municipales et Habitation portfolio, relating in particular to the measures announced in the 2023-2024 budget to accelerate and support the purchase and construction of social and affordable housing. |

Change with 2021-2022 actual results

Actual results for 2022-2023 are $1 869 million higher than for 2021-2022. On the one hand, the 2022-2023 actual results of the Conseil du trésor et Administration gouvernementale portfolio are comparable to those of 2021-2022. On the other hand, the other portfolios in this group posted growth of $1 868 million in actual expenditures in 2022-2023, due to higher transfer, remuneration and operating expenses.

| 34 | PUBLIC ACCOUNTS 2022-2023 |

2. Variance analysis (cont’d)

2.3. Consolidated expenditure (cont’d)

Other portfolios (cont’d)

Transfers

The $696-million increase in transfers in 2022-2023 is the result of several variations spread across the group’s portfolios, including:

| ● | a $101 million-increase related to growth in financial assistance for infrastructure projects administered by the Société de financement des infrastructures locales du Québec (SOFIL), which falls under the Finances portfolio, particularly drinking water projects. The growth is linked to the greater volume of work eligible for subsidies than in 2021-2022; |

| ● | $114 million-increase attributable to higher spending under the measure to connect all Quebecers to high-speed Internet, a program administered by the Conseil exécutif portfolio. |

Remuneration

The $451-million increase in remuneration expenditures is attributable in particular to salary indexations and increments.

Operating

The $664-million increase in operating expenditures in 2022-2023 is the result of a number of variations across the group’s 16 portfolios, including a $210-million increase in expenditures in the Ressources naturelles et Forêts portfolio, mainly due to the reassessment of estimated costs for the remediation of contaminated sites.

| ANALYSIS OF THE CONSOLIDATED FINANCIAL STATEMENTS | 35 |

2. Variance analysis (cont’d)

2.3. Consolidated expenditure (cont’d)

Debt service

| Budget 2022-2023 | Actual results as at March 31, 2023 | Change with 2022-2023 | Actual results as at March 31, 2022 | Change with 2021-2022 actual results | |||||||||||||||||||

| M$ | % | M$ | % | ||||||||||||||||||||

| Debt service | 8 842 | 10 058 | 1 216 | 13.8 | 8 640 | 1 418 | 16.4 | ||||||||||||||||

Debt service consists mainly of interest on debt and interest on pension plans and other employee future benefits1 liabilities for the public and parapublic sectors. The composition of debt service is presented in Note 5 to the consolidated financial statements.

Debt service for 2022-2023 of $10 058 million exceeds the forecast by $1 216 million. This change is mainly due to the higher-than-expected rise in interest rates.

Compared to the 2021-2022 actual results, debt service shows a $1 418-million increase which is mainly due to the growth in the average volume of debt contracted on financial markets and higher interest rates.

This variation is partially offset by a $182-million decrease in debt service relating to pension plans and other employee future benefits, due in particular to higher investment income from the Retirement Plans Sinking Fund and the sinking funds of the plans’ special funds, income which is presented as a reduction in the expense.

| 1 | This is interests on obligations related to pension plans and other employee future benefits in the public and parapublic sectors, decreased mainly by investment income from the Retirement Plans Sinking Fund (RPSF) and specific pension funds. |

| 36 | PUBLIC ACCOUNTS 2022-2023 |

Budget balance and stabilization reserve

The purpose of the Balanced Budget Act (the Act) is to balance the budget of the government. It stipulates that the government may not incur a budgetary deficit, which corresponds to the annual operating surplus (deficit) excluding revenues dedicated to the Generations Fund after use of the stabilization reserve. The reserve is allocated to maintaining a balanced budget; its balance is reduced by the amount needed to achieve that balance.

Moreover, the government may, under the conditions it determines, use the reserve to make payments to the Generations Fund. The balance of the reserve is reduced by the amount thus paid into the fund. The amounts allocated annually to the reserve correspond to the amount of the surplus recorded for that fiscal year, that is, a budgetary balance greater than zero. The reserve has no impact on the annual accounting surplus or deficit.

As part of the implementation of the measures presented in the 2023-2024 budget, the Act has been modernized to provide greater flexibility in determining budgetary balance, replace the rules surrounding deficit reduction and abolish the stabilization reserve. This report on budgetary balance is carried out in accordance with the provisions of the Act in effect on March 31, 2023.

Fiscal year 2022-2023

In 2021-2022, in the context of the pandemic and in order to gradually reduce the deficit without adversely affecting services to Quebecers and the sustainable recovery of the economy, the provisions of the Balanced Budget Act prohibiting the recognition or forecasting of a budgetary deficit, and those requiring the elimination of any deficit, were suspended. These suspensions remained in effect until 2022-2023. The lifting of these suspensions, announced in the 2023-2024 budget speech, took effect on April 1, 2023. The budgetary balance representing operations for the fiscal year ended March 31, 2023 is a deficit of $5 635 million after taking into account the allocation of $3 082 million to the Generations Fund and the use of the balance of the stabilization reserve of $449 million.

Budget balance within the meaning of the Balanced Budget Act

Fiscal year ended March 31, 2023

(millions of dollars)

| Budget | Actual results as at | |||||||

| 2022-2023 | March 31, 2023 | |||||||

| Annual deficit | (3 005 | ) | (3 002 | ) | ||||

| Revenue of the Generations Fund | (3 445 | ) | (3 082 | ) | ||||

| Budget balance before use of the stabilization reserve | (6 450 | ) | (6 084 | ) | ||||

| Use of the stabilization reserve | — | 449 | ||||||

| Budget balance | (6 450 | ) | (5 635 | ) | ||||

| ANALYSIS OF THE CONSOLIDATED FINANCIAL STATEMENTS | 37 |

3. Balanced Budget Act (cont’d)

Stabilization reserve

(millions of dollars)

| Fiscal year ended March 31 | ||||||||

| 2023 | 2022 | |||||||

| Opening balance | 449 | 1 221 | ||||||

| Use of the reserve to maintain a balanced budget | (449 | ) | (772 | ) | ||||

| Closing balance | — | 449 | ||||||

Change in budget balance before use of the stabilization reserve and stabilization reserve balance

(millions of dollars)

| Notes: | From an accounting standpoint, this reserve has no impact on the annual surplus (deficit). In accordance with the Balanced Budget Act, the budgetary balance does not include the retroactive effect of a new CPA Canada standard for years prior to its coming into force. Thus, although the annual surpluses (deficits) were restated to reflect the application of the accounting standard relating to asset retirement obligations, these restatements had no impact on the budgetary balance. |

(1) | The provisions of the Balanced Budget Act prohibiting budgetary deficits did not apply to these years. |

The effects of the financial crisis and global recession that had held sway from 2008-2009 led to a substantial deterioration in the government’s financial balances until 2013-2014. The year 2014-2015 represents a turning point, marking the beginning of a period during which the government’s budgetary balances improved continuously until 2018-2019. Consequently, the stabilization reserve balance increased from 2015-2016 to 2019-2020.

| 38 | PUBLIC ACCOUNTS 2022-2023 |

3. Balanced Budget Act (cont’d)

On March 13, 2020, the Québec government declared a health emergency due to the global COVID-19 pandemic. Initiatives to address the crisis and stimulate the economy, combined with the impact of the lockdown and temporary institutional closures, significantly affected the government’s financial results for years 2019-2020 to 2021-20221. This situation required the use of the stabilization reserve in 2020-2021 and in 2021-2022 to achieve a balanced budget within the meaning of the Act.

In 2022-2023, the balance of the stabilization reserve of $449 million was used in full to reduce the budgetary deficit to $5 635 million. This deficit is mainly due to measures put in place to help Quebecers cope with the cost of living.

Generations Fund

The Generations Fund, created under the Act to reduce the debt and establish the Generations Fund, is used exclusively to repay the government’s gross debt. The statement of change in the balance of the Generations Fund is presented in Note 12 “Generations Fund” of the consolidated financial statements.

Budget 2022-2023 forecast that the revenue of the Generations Fund would amount to $3 445 million. The fund’s actual revenue is $3 082 million, or $363 million less than forecast. The fund’s balance is $18 911 million as at March 31, 2023.

| 1 | The change in the application of the accounting standard on government transfers also contributed to the budgetary deficit before use of the stabilization reserve for 2020-2021. |

| ANALYSIS OF THE CONSOLIDATED FINANCIAL STATEMENTS | 39 |

The main trends analysis presented in this section uses financial information from the consolidated financial statements of the Gouvernement du Québec.

The data presented put into perspective the trends observed over the past 10 years for the following main items1:

| ● | the annual surplus (deficit); |

| ● | consolidated revenue by source; |

| ● | consolidated expenditures by portfolios; |

| ● | the net book value of fixed assets; |

| ● | the government’s net debt and gross debt. |

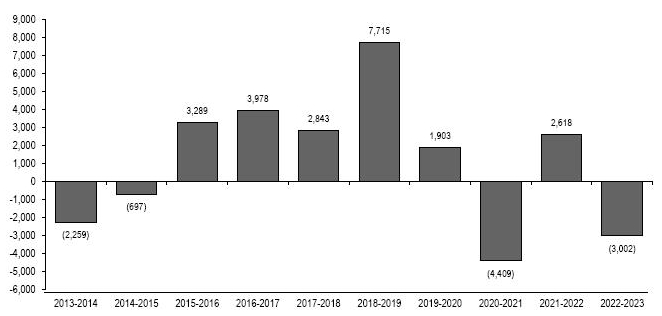

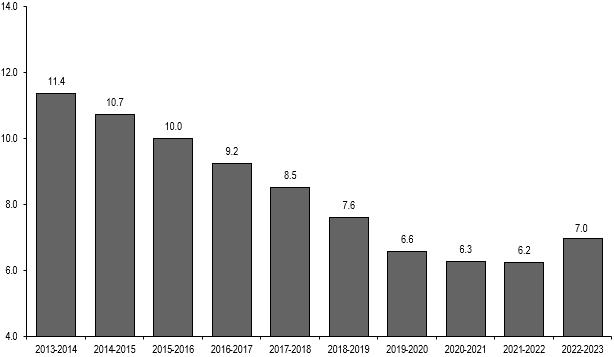

Change in annual surplus (deficit)

(millions of dollars)

| Note: | Annual surpluses (deficits) have been restated to reflect the application of the accounting standard relating to asset retirement obligations. |

Between 2013-2014 and 2018-2019, annual results overall improved, which allowed for the return to a surplus starting in 2015-2016. This was driven by, among other things, restrained growth in program spending and a favourable economic environment. Growth in annual results ended in 2019-2020 due to targeted initiatives in the budget and the COVID-19 pandemic, which resulted in lost revenue and additional expenses for the government. However, the government’s finances were more impacted by the negative effects of the pandemic in 2020-2021, which explains the significant deficit of $4 409 million.

1 | Where financial statements have been restated in a subsequent fiscal year, the restated data has been used. |

| 40 | PUBLIC ACCOUNTS 2022-2023 |

4. Analysis of main trends (cont’d)

Despite the impact of the many measures adopted by the government to address the health emergency in 2021-2022, Québec’s finances benefited from the positive effects of the economic rebound and were particularly stimulated by the easing of the health measures, which resulted in a surplus of $2 618 million.

In 2022-2023, the government recorded a deficit of $3 002 million, mainly attributable to the introduction of the Anti-Inflation Shield to help Quebecers cope with the rising cost of living, which led to an increase in the senior assistance amount, the payment of a new one-time cost-of-living amount and the capping of indexation of several government rates at 3% for a four-year period.

| ANALYSIS OF THE CONSOLIDATED FINANCIAL STATEMENTS | 41 |

4. Analysis of main trends (cont’d)

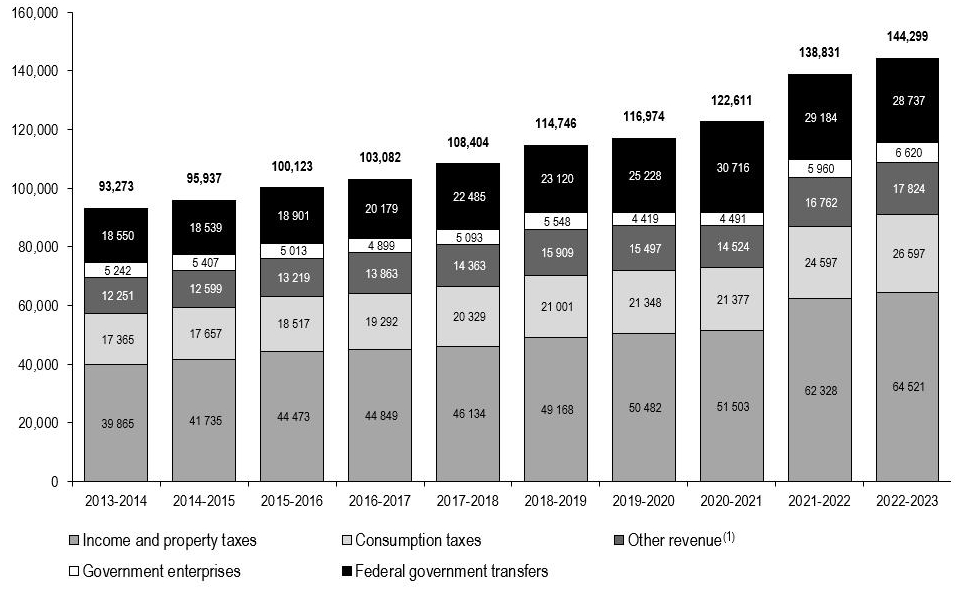

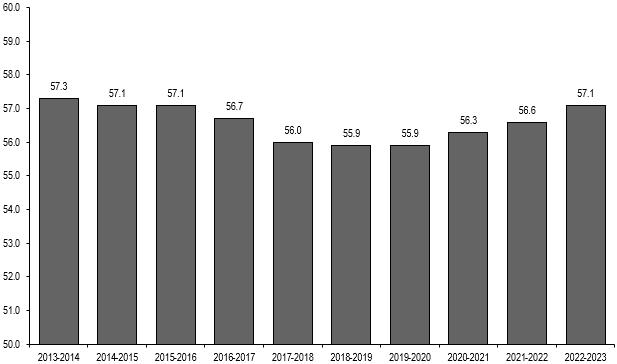

Change in consolidated revenue

Revenue by source

(millions of dollars)

| (1) | Other revenue includes revenue from duties and permits as well as miscellaneous revenue. |

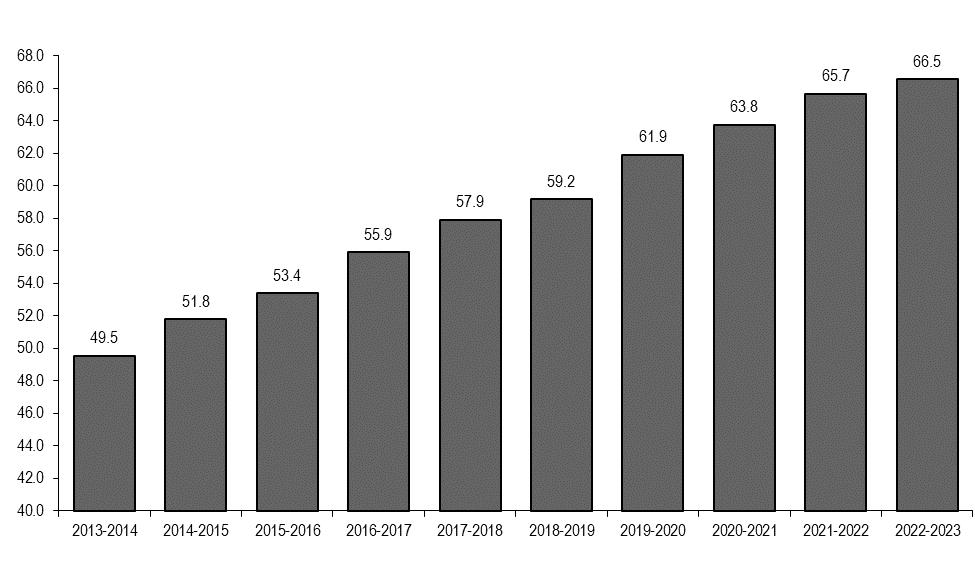

The government’s consolidated revenue rose from $93 273 million to $144 299 million from 2013-2014 to 2022-2023. Over this period, the annual average growth of this revenue was 5.0%, while that of GDP was 4.5%. Since 2013-2014, total revenue has grown constantly.

Following stronger growth of 13.2% between 2020-2021 and 2021-2022 due to the post-pandemic economic recovery, growth in total consolidated revenues slowed by 9.3 percentage points in 2022-2023 to 3.9%. This lower-than-average annual growth is explained by the economic slowdown that began during the year.

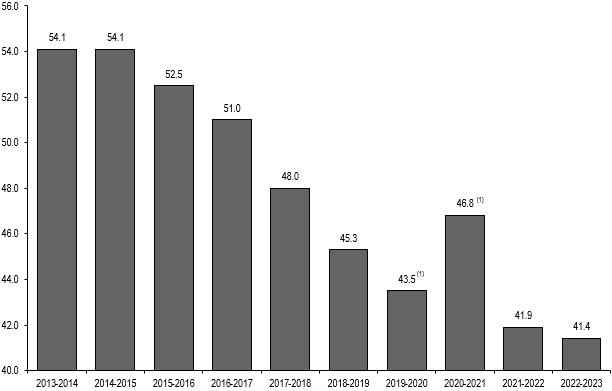

Tax revenue – Income and property taxes

Revenue from income and property taxes rose from $39 865 million in 2013-2014 to $64 521 million in 2022-2023. On average, this revenue grew by 5.5% per year over the period, owing in particular to an increase in the average wage and the number of jobs in Québec.

| 42 | PUBLIC ACCOUNTS 2022-2023 |

4. Analysis of main trends (cont’d)

Change in consolidated revenue (cont’d)

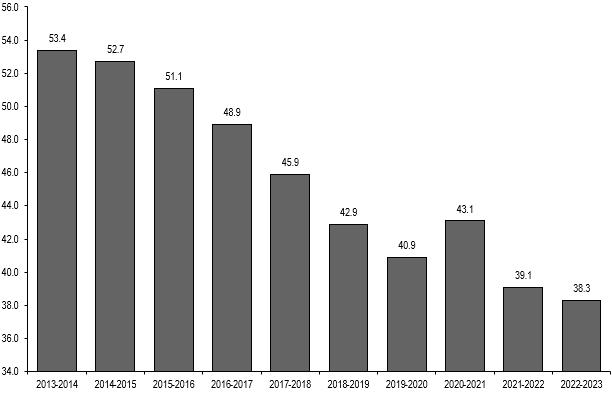

Tax revenue – Consumption taxes

Revenue from consumption taxes has grown regularly since 2013-2014, going from $17 365 million to $26 597 million in 2022-2023. The average annual growth rate for the period was 4.9% owing to sustained growth in retail sales and, particularly for 2022-2023, the high inflation that contributed to the sharp rise in prices of goods and services subject to consumption taxes.

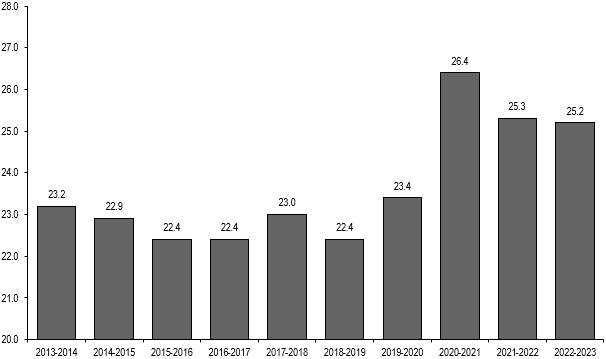

Federal government transfers

Federal government transfer revenue rose from $18 550 million in 2013-2014 to $28 737 million in 2022-2023, which represents an average growth of 5.0% per year. With the exception of 2014-2015, when federal transfers remained relatively stable, this revenue has been growing steadily up to and including 2020-2021.

Between 2014-2015 and 2020-2021, this growth is due to the increase in all categories of federal transfers and more specifically for 2020-2021, to federal government transfers made to support the implementation by the provinces of pandemic-related measures and to partly compensate Québec’s efforts to mitigate the financial impact of the COVID-19 pandemic. The one-time nature of several of these support measures account for the decrease in transfer revenue in 2021-2022 and 2022-2023.

Government enterprises

Revenue from government enterprises, which consists mainly of the results of Hydro-Québec, Loto-Québec, the Société des alcools du Québec and Investissement Québec, went from $5 242 million in 2013-2014 to $6 620 million in 2022-2023, which corresponds to an average growth of 2.6% per year.