UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 10-K

ý ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE

SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended December 31, 2015

OR

o TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE

SECURITIES EXCHANGE ACT OF 1934

For the transition period from to

COMMISSION FILE NO. 001-10308

AVIS BUDGET GROUP, INC.

(Exact name of Registrant as specified in its charter)

| DELAWARE | 06-0918165 | |

| (State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification Number) | |

6 SYLVAN WAY PARSIPPANY, NJ | 07054 | |

| (Address of principal executive offices) | (Zip Code) | |

973-496-4700

(Registrant’s telephone number, including area code)

SECURITIES REGISTERED PURSUANT TO SECTION 12(b) OF THE ACT:

| TITLE OF EACH CLASS | NAME OF EACH EXCHANGE ON WHICH REGISTERED | |

| Common Stock, Par Value $.01 | The NASDAQ Global Select Market | |

SECURITIES REGISTERED PURSUANT TO SECTION 12(g) OF THE ACT: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes þ No o

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes o No þ

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the Registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes þ No o

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes þ No o

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§229.405 of this chapter) is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer or a smaller reporting company. See the definition of “large accelerated filer”, “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

Large accelerated filer þ | Accelerated filer o | Non-accelerated filer o | Smaller reporting company o |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes o No þ

As of June 30, 2015, the aggregate market value of the registrant’s common stock held by non-affiliates of the registrant was $4,532,680,060 based on the closing price of its common stock on the NASDAQ Global Select Market. All executive officers and directors of the registrant have been deemed, solely for the purpose of the foregoing calculation, to be “affiliates” of the registrant.

As of January 29, 2016, the number of shares outstanding of the registrant’s common stock was 97,039,594.

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the registrant’s definitive proxy statement to be mailed to stockholders in connection with the registrant’s annual stockholders’ meeting scheduled to be held on May 25, 2016 (the “Annual Proxy Statement”) are incorporated by reference into Part III hereof.

TABLE OF CONTENTS

| Item | Description | Page |

| PART I | ||

| 1 | ||

| 1A | ||

| 1B | ||

| 2 | ||

| 3 | ||

| 4 | ||

| PART II | ||

| 5 | ||

| 6 | ||

| 7 | ||

| 7A | ||

| 8 | ||

| 9 | ||

| 9A | ||

| 9B | ||

| PART III | ||

| 10 | ||

| 11 | ||

| 12 | ||

| 13 | ||

| 14 | ||

| PART IV | ||

| 15 | ||

FORWARD-LOOKING STATEMENTS

Certain statements contained in this Annual Report on Form 10-K may be considered “forward-looking statements” as that term is defined in the Private Securities Litigation Reform Act of 1995. The forward-looking statements contained herein are subject to known and unknown risks, uncertainties, assumptions and other factors that may cause our actual results, performance or achievements to be materially different from those expressed or implied by any such forward-looking statements. Forward-looking statements include information concerning our future financial performance, business strategy, projected plans and objectives. These statements may be identified by the fact that they do not relate to historical or current facts and may use words such as “believes,” “expects,” “anticipates,” “will,” “should,” “could,” “may,” “would,” “intends,” “projects,” “estimates,” “plans,” and similar words, expressions or phrases. The following important factors and assumptions could affect our future results and could cause actual results to differ materially from those expressed in such forward-looking statements:

| • | the high level of competition in the vehicle rental industry and the impact such competition may have on pricing and rental volume; |

| • | a change in travel demand, including changes in airline passenger traffic; |

| • | a change in our fleet costs as a result of a change in the cost of new vehicles, manufacturer recalls, disruption in the supply of new vehicles, and/or a change in the price at which we dispose of used vehicles either in the used vehicle market or under repurchase or guaranteed depreciation programs; |

| • | the results of operations or financial condition of the manufacturers of our cars, which could impact their ability to perform their payment obligations under our agreements with them, including repurchase and/or guaranteed depreciation arrangements, and/or their willingness or ability to make cars available to us or the rental car industry as a whole on commercially reasonable terms or at all; |

| • | any change in economic conditions generally, particularly during our peak season or in key market segments; |

| • | our ability to continue to achieve and maintain cost savings and successfully implement our business strategies; |

| • | our ability to obtain financing for our global operations, including the funding of our vehicle fleet through the issuance of asset-backed securities and use of the global lending markets; |

| • | an occurrence or threat of terrorism, pandemic disease, natural disasters, military conflict or civil unrest in the locations in which we operate; |

| • | our dependence on third-party distribution channels, third-party suppliers of other services and co-marketing arrangements with third parties; |

| • | our ability to utilize derivative instruments, and the impact of derivative instruments we utilize, which can be affected by fluctuations in interest rates, gasoline prices and exchange rates, changes in government regulations and other factors; |

| • | our ability to accurately estimate our future results; |

| • | any major disruptions in our communication networks or information systems; |

| • | our exposure to uninsured claims in excess of historical levels; |

| • | risks associated with litigation, governmental or regulatory inquiries, or any failure or inability to comply with laws, regulations or contractual obligations or any changes in laws, regulations or contractual obligations, including with respect to personally identifiable information and taxes; |

| • | any impact on us from the actions of our licensees, dealers and independent contractors; |

| • | any substantial changes in the cost or supply of fuel, vehicle parts, energy, labor or other resources on which we depend to operate our business; |

| • | risks related to our indebtedness, including our substantial outstanding debt obligations and our ability to incur substantially more debt; |

| • | our ability to meet the financial and other covenants contained in the agreements governing our indebtedness; |

| • | risks related to tax obligations and the effect of future changes in accounting standards; |

| • | risks related to completed or future acquisitions or investments that we may pursue, including any incurrence of incremental indebtedness to help fund such transactions and our ability to promptly and effectively integrate any acquired businesses; |

| • | risks related to protecting the integrity of our information technology systems and the confidential information of our employees and customers against security breaches, including cyber-security breaches; and |

| • | other business, economic, competitive, governmental, regulatory, political or technological factors affecting our operations, pricing or services. |

We operate in a continuously changing business environment and new risk factors emerge from time to time. New risk factors, factors beyond our control, or changes in the impact of identified risk factors may cause actual results to differ materially from those set forth in any forward-looking statements. Accordingly, forward-looking statements should not be relied upon as a prediction of actual results. Moreover, we do not assume responsibility for the accuracy and completeness of those statements. Other factors and assumptions not identified above, including those discussed in “Management’s Discussion and Analysis of Financial Condition and Results of Operations” set forth in Item 7, in “Risk Factors” set forth in Item 1A and in other portions of this Annual Report on Form 10-K, may contain forward-looking statements and involve uncertainties that could cause actual results to differ materially from those projected in such statements.

Although we believe that our assumptions are reasonable, any or all of our forward-looking statements may prove to be inaccurate and we can make no guarantees about our future performance. Should unknown risks or uncertainties materialize or underlying assumptions prove inaccurate, actual results could differ materially from past results and/or those anticipated, estimated or projected. Except to the extent of our obligations under the federal securities laws, we undertake no obligation to release any revisions to any forward-looking statements, to report events or to report the occurrence of unanticipated events. For any forward-looking statements contained in any document, we claim the protection of the safe harbor for forward-looking statements contained in the Private Securities Litigation Reform Act of 1995.

PART I

| ITEM 1. BUSINESS |

Except as expressly indicated or unless the context otherwise requires, the “Company,” “Avis Budget,” “we,” “our” or “us” means Avis Budget Group, Inc. and its subsidiaries. “Avis,” “Budget,” “Budget Truck,” “Zipcar,” “Payless” and “Apex” refer to our Avis Rent A Car System, LLC, Budget Rent A Car System, Inc., Budget Truck Rental, LLC, Zipcar, Inc., Payless Car Rental and Apex Car Rentals operations, respectively, and, unless the context otherwise requires, do not include the operations of our licensees, as further discussed below.

| OVERVIEW |

We are a leading global provider of vehicle rental and car sharing services, operating three of the most recognized brands in the industry through Avis, Budget and Zipcar. We are a leading vehicle rental operator in North America, Europe, Australia, New Zealand and certain other regions we serve. We and our licensees operate the Avis and Budget brands in approximately 180 countries throughout the world. We generally maintain a leading share of airport car rental revenue in North America, Europe, Australia and New Zealand, and we operate one of the leading truck rental businesses in the United States.

Our brands are differentiated to help us meet a wide range of customer needs throughout the world. Avis is a leading rental car supplier positioned to serve the premium commercial and leisure segments of the travel industry, and Budget is a leading rental vehicle supplier focused primarily on more value-conscious segments of the industry.

On average, our rental fleet totaled more than 580,000 vehicles and we completed more than 38 million vehicle rental transactions worldwide in 2015. We generate approximately 70% of our vehicle rental revenue from on-airport locations and approximately 30% of our revenue from off-airport locations. We also license the use of the Avis and Budget trademarks to licensees in areas in which we do not operate directly. Our brands have an extended global reach with more than 11,000 car and truck rental locations throughout the world, including approximately 5,000 car rental locations operated by our licensees. We believe that Avis,Budget and Zipcar enjoy complementary demand patterns with mid-week commercial demand balanced by weekend leisure demand.

Our Zipcar brand is the world’s leading car sharing company, with nearly one million members in the United States, Canada and Europe. We operate Budget Truck, one of the leading truck rental businesses in the United States, with a fleet of approximately 21,000 vehicles that operate through a network of approximately 1,000 dealer-operated and 450 Company-operated locations throughout the continental United States. We also own Payless, a car rental brand that operates in the deep-value segment of the industry, and Apex, which is a leading deep-value car rental brand in New Zealand and Australia. We also have investments in certain of our Avis and Budget licensees outside of the United States, including licensees in India and China.

| COMPANY HISTORY |

Founded in 1946, Avis is believed to be the first company to rent cars from airport locations. Avis expanded its geographic reach throughout the United States through growth in licensed and Company-operated locations in the 1950s and 1960s. In 1963, Avis introduced its award winning “We try harder®” advertising campaign, which was recognized as one of the top ten advertising campaigns of the 20th century by Advertising Age magazine.

HFS Incorporated acquired Avis in 1996 and merged with our predecessor company in 1997, with the combined entity being renamed Cendant Corporation. The Company is a Delaware corporation headquartered in Parsippany, New Jersey.

In 2002, Cendant acquired the Budget brand and Budget vehicle rental operations in North America, Australia and New Zealand. Budget was founded in 1958 as a car rental company for the value-conscious vehicle rental customer and grew its business rapidly during the 1960s, expanding its rental car offerings throughout North America and significantly expanding its Budget truck rental business in the 1990s.

3

In 2006, Cendant completed the sales and spin-offs of several significant subsidiaries and changed its name to Avis Budget Group, Inc. In 2011, we expanded our international operations with the acquisition of Avis Europe, which was previously an independently-owned licensee operating the Avis and Budget brands in Europe, the Middle East and Africa, and the Avis brand in Asia. Upon the completion of the acquisition of Avis Europe, the Avis and Budget brands were globally re-united under a single company, making Avis Budget Group one of the largest vehicle rental companies in the world.

In 2013, we acquired Zipcar, the world’s leading car sharing company, to further increase our growth potential and our ability to better serve a greater variety of our customers’ mobility needs. In 2012 and 2013, we acquired our Apex and Payless brands, respectively, which allowed us to expand our presence in the deep-value segment of the car rental industry. In 2014, we also acquired our long-standing Budget licensee for Southern California and Las Vegas, which further expanded our Company-operated locations in the United States. In 2015, we acquired the operations of our former Avis and Budget licensees in Brazil, Norway, Sweden and Denmark; our Avis licensee in Poland; and Maggiore Group, a leading provider of vehicle rental services in Italy. These acquisitions have allowed us to further expand our global footprint of Company-operated locations.

We have a long history of innovation in the vehicle rental and car sharing business, including:

| • | in 1973, we launched our proprietary Wizard system, a constantly updated information-technology system that is the backbone of our operations; |

| • | in 1987, we introduced our Roving Rapid Return program, powered by a handheld computer device that allows customers to bypass the car return counter; |

| • | in 1996, we became one of the first car rental companies to accept online reservations; |

| • | in 2000, we introduced Avis Interactive, the first Internet-based reporting system in the car rental industry; |

| • | in 2009, we launched what we believe to be the first car rental iPhone application in the United States; |

| • | in 2012, we believe that our Avis brand became the first in the industry to offer mobile applications to customers on all four major mobile platforms; |

| • | in 2015, our Avis brand was the first in the industry to offer an Android application that allows customers to use voice-activated technology to make, confirm or cancel their car rental reservations; |

| • | in 2015, our Avis brand was the first U.S. car rental company to offer an application for the Apple Watch, which enables our customers to email themselves a car rental receipt and view current, upcoming and past car rental reservations from their wrists; and |

| • | in 2015, we continued to expand our use of yield management systems, which the Company designed to help optimize its decision-making with respect to pricing and fleet management. |

Our Zipcar operations have been a constantly innovating pioneer in using advanced vehicle technologies as the first car sharing company in the United States to develop a self-service solution to managing the complex interactions of real-time, location-based activities inherent in a large-scale car sharing operation, including new member application, reservations and keyless vehicle access, fleet management and member management. Zipcar was also the first to allow members to reserve the specific make, model and type of car by phone, Internet or wireless mobile device.

Since becoming an independent vehicle rental services company in 2006, we have focused on strengthening our brands, our operations, our competitiveness and our profitability. In conjunction with these efforts, we have implemented process improvements impacting virtually all areas of the business; realized significant cost savings through the integration of acquired businesses with our pre-existing operations; achieved reductions in operating and selling, general and administrative expenses, including significant reductions in staff; assessed location, segment and customer profitability to address less-profitable aspects of our business; implemented price increases and changes to our sales, marketing and affinity programs to improve profitability; and sought to better

4

optimize our acquisition, deployment and disposition of fleet in order to lower costs and better meet customer demand.

| SEGMENT INFORMATION |

We categorize our operations into two reporting segments:

| • | Americas, provides and licenses the Company’s brands to third parties for vehicle rentals and ancillary products and services in North America, South America, Central America and the Caribbean, and operates the Company’s car sharing business in certain of these markets; and |

| • | International, provides and licenses the Company’s brands to third parties for vehicle rentals and ancillary products and services in Europe, the Middle East, Africa, Asia, Australia and New Zealand, and operates the Company’s car sharing business in certain of these markets. |

The following table presents key operating metrics for each of our two reporting segments:

| Total 2015 Rental Days | Average 2015 Time and Mileage (“T&M”) Revenue per Day | Average 2015 Rental Fleet Size | ||||

| Americas | 99 million | $40.55 | 383,000 | |||

| International | 43 million | $33.57 | 164,000 | |||

| 142 million | 547,000 | |||||

________

Note: Operating metrics exclude Zipcar and U.S. truck rental operations, which had average fleets of 13,000 and 21,000 vehicles, respectively, in 2015.

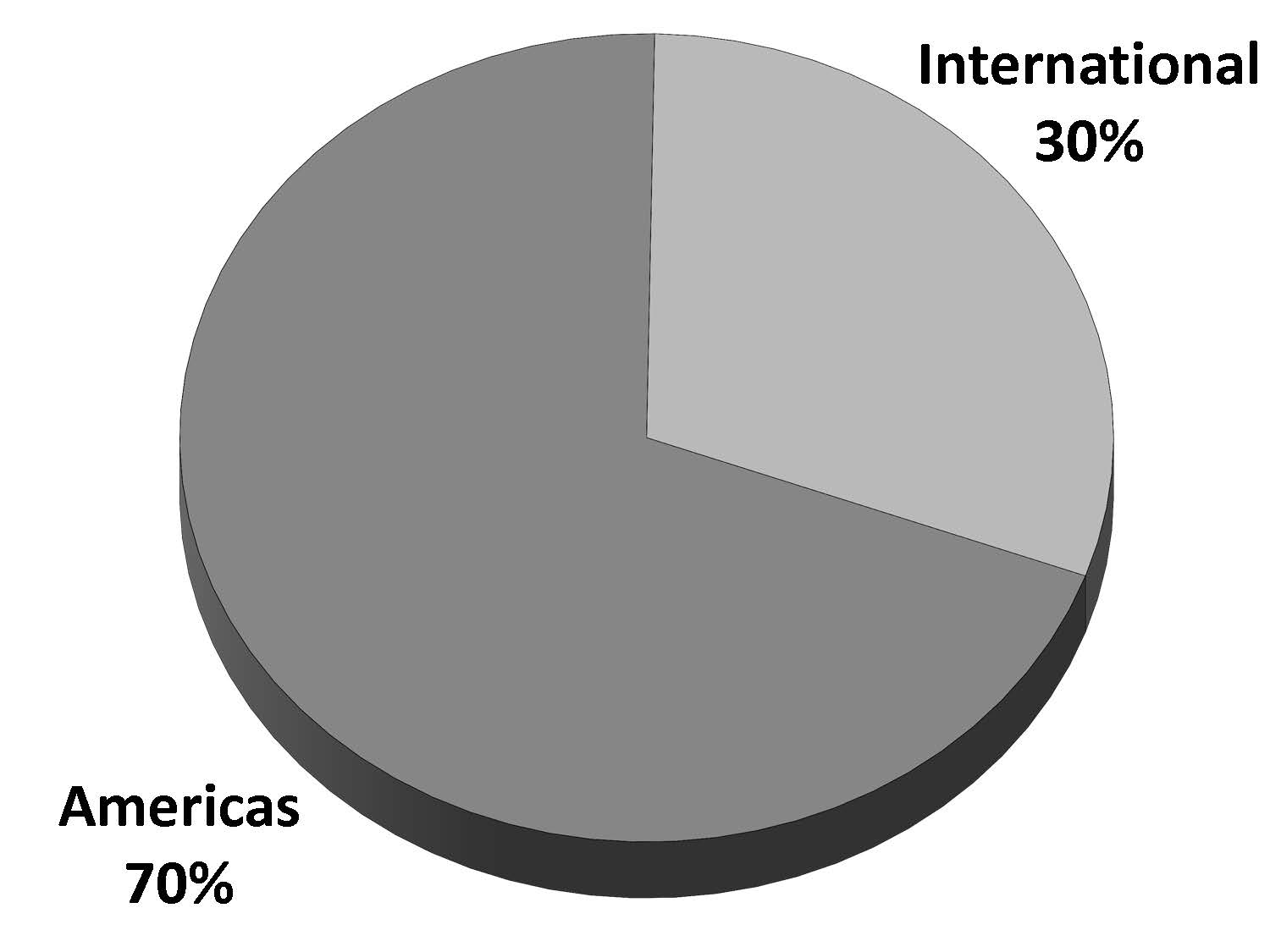

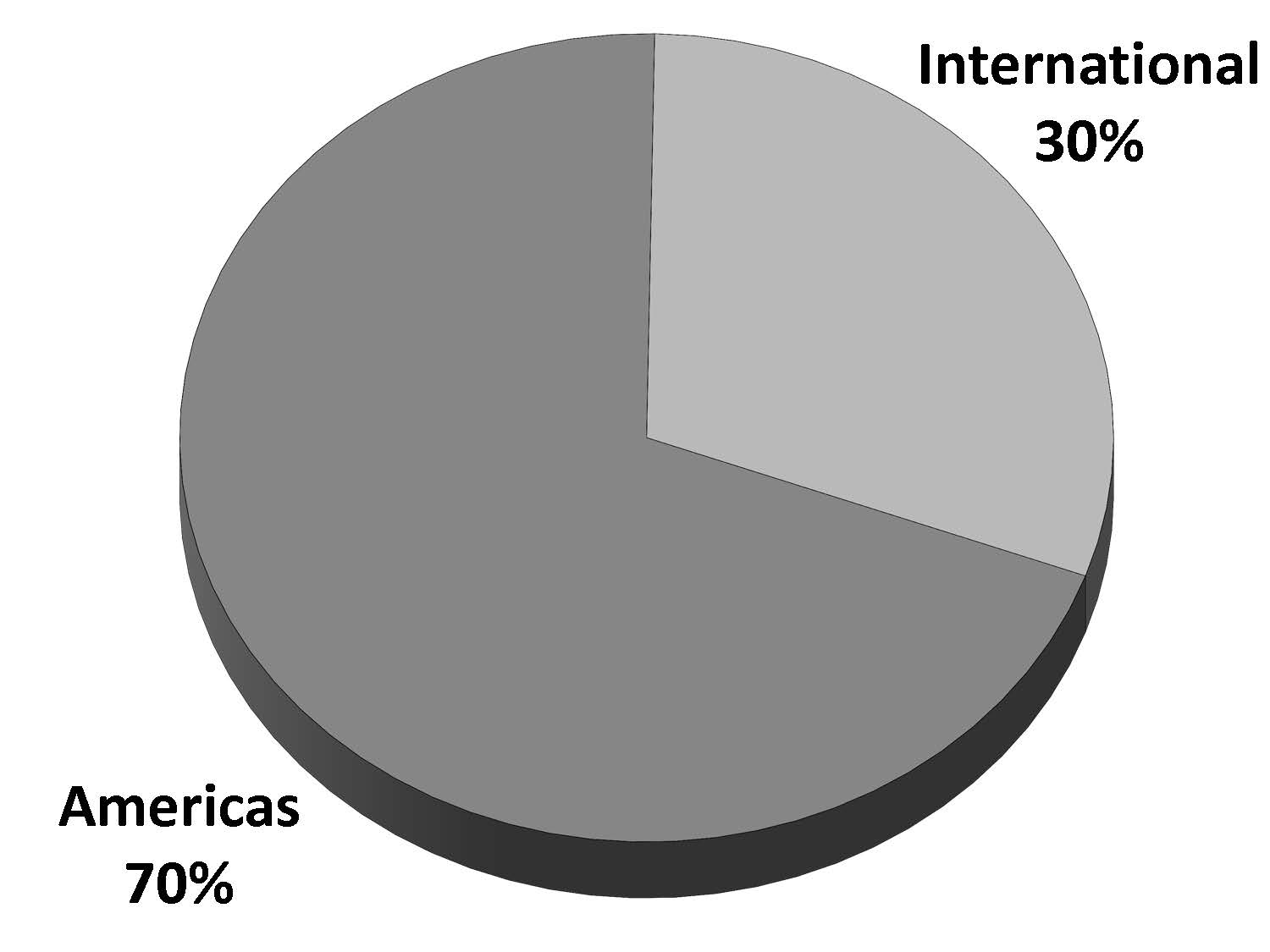

The following graphs present the composition of our rental days and our average rental fleet in 2015, by segment:

Composition of 2015 Rental Days | Composition of 2015 Rental Fleet | |||

|  | |||

Financial data for our segments and geographic areas are reported in Note 19-Segment Information to our Consolidated Financial Statements included in Item 8 of this Annual Report on Form 10-K.

| OUR STRATEGY |

Our objective is to strategically accelerate our growth, strengthen our global position as a leading provider of vehicle rental services, enhance our customers’ rental experience, control costs and drive efficiency throughout the organization. We expect to achieve our goals by focusing our efforts on the following core strategic initiatives:

| • | Strategically Accelerate Growth. We have pursued and will continue to pursue numerous opportunities intended to increase our revenues and make disproportionate contributions to our earnings. For instance: |

| ◦ | We are focused on promoting car class upgrades, adjusting our mix of vehicles to match customer demand, growing our rentals to small-business and international travelers, increasing |

5

the number of rentals that customers book through our own websites and mobile applications, increasing the proportion of transactions in which customers prepay us, and expanding our ancillary revenues derived from offering additional ancillary products and services to the rental transactions of an increasing percentage of our customers. We believe these efforts will not only enhance the rental experience, but also generate incremental revenue and add to profitability.

| ◦ | We are focused on yield management and pricing optimization in an effort to increase the rental fees we earn per rental day. We have implemented, and plan to continue to implement, new technology systems that strengthen our yield management and enable us to tailor our product, service and price offerings not only to meet our customers’ needs, but also in response to actions taken by our competitors. We expect to continue to adjust our pricing to bolster profitability and match changes in demand. |

| ◦ | We continue to see significant growth opportunities related to our Zipcar brand. We expect to increase our Zipcar membership base by growing the number of businesses, government agencies and universities that Zipcar serves within its existing markets, as well as expanding the brand into new markets where our existing car rental presence will help enable the introduction of Zipcar’s car sharing services. We expect that such growth will include making more Zipcars available at airport locations, offering one-way usage of Zipcars at certain locations, cross-marketing partnerships through our well-established corporate and affinity relationships and expanding our car sharing footprint outside of the United States. |

| ◦ | We continue to focus on addressing the need of the deep-value segment of the vehicle rental industry with our Payless and Apex brands and look to increase our profitability in this segment as we grow our revenues. |

| • | Strengthening Our Global Position. While we currently operate, either directly or through licensees, in approximately 180 countries around the world, we will continue to strengthen and further expand our global footprint through organic growth and potentially through acquisitions, joint ventures, licensing agreements or other relationships: |

| ◦ | In countries where we have Company-operated locations, we will continue to identify opportunities to add new rental locations, to grant licenses to independent third parties for regions where we do not currently operate and/or do not wish to operate directly, to strengthen the presence of our brands and to re-acquire previously granted license rights in certain cases. |

| ◦ | In countries operated by licensees, including our joint ventures in India and China, we will seek to ensure that our licensees are well positioned to realize the growth potential of our brands in those countries and are aggressively growing their presence in those markets, and we expect to consider the re-acquisition of previously granted license rights in certain cases. |

| ◦ | Zipcar represents a substantial growth opportunity for us as we believe that there are numerous geographic markets outside the United States, particularly in Europe and the Asia Pacific region, where Zipcar’s proven car sharing model can be utilized to meet substantial, currently unmet transportation needs. |

| • | Enhancing Customers’ Rental Experience. We are committed to serving our customers and enhancing their rental experience, including through our Customer Led, Service Driven™ initiative, which is aimed at improving our customers’ rental experience with our brands, our systems and our employees. Following an extensive review of the ways, places and occasions in which our brands, our systems and our employees interact with existing and potential customers, we have implemented actions that further enhance the service we provide at these customer “touch points.” For example: |

| ◦ | We offer Avis Preferred Select & Go™, a vehicle-choice program for customers, and have revised our rental agreements and receipts to improve transparency, and mobile applications to accept reservations and to better communicate with customers. We have also significantly expanded customer-service-oriented training of our employees, achieving significant increases in customer satisfaction. |

6

| ◦ | We continue to upgrade our technology, to make the reservation, pick-up and return process more convenient and user-friendly, with a particular emphasis on enabling and simplifying our customers’ online interactions with us. |

| ◦ | We have significantly expanded our tracking of customer-satisfaction levels so that we now receive location-specific feedback from more than 1 million customers annually, and we have implemented numerous service and process changes in response to this feedback. |

We expect to continue to invest in these efforts, with a particular emphasis on self-service technologies that we believe will allow us to serve customers more effectively and efficiently.

| • | Controlling Costs and Driving Efficiency throughout the Organization. We have continued our efforts to rigorously control costs. We continue to aggressively reduce expenses throughout our organization, and we have consistently eliminated or reduced significant costs through the integration of acquired businesses. In addition: |

| ◦ | We continued to develop and implement our Performance Excellence process improvement initiative to increase efficiencies, reduce operating costs and create sustainable cost savings using LEAN, Six Sigma and other tools. This initiative, which we have expanded to cover our operations in our International segment, has generated substantial savings since its implementation and is expected to continue to provide incremental benefits. |

| ◦ | Through our Transformation 2015 initiative, we have taken significant actions to further streamline our administrative and shared-services infrastructure through a restructuring program that identifies and replicates best practices, leverages the scale and capabilities of third-party service providers, and will increase the global standardization and consolidation of non-rental-location functions over time. |

| ◦ | We have implemented initiatives to integrate our acquired businesses, to realize cost efficiencies from combined maintenance, systems, technology and administrative infrastructure, as well as fleet utilization benefits and savings by combining our car rental and car sharing fleets at times to reduce the number of unutilized vehicles. |

| ◦ | We have also continued to implement technology solutions, including self-service voice reservation technology, mobile communications with customers and fleet optimization technologies to reduce costs, and we will further continue to pursue innovative solutions to support our strategic initiatives. |

We believe such steps will continue to aid our financial performance.

In executing our strategy, we plan to continue to position our distinct and well-recognized global brands to focus on different segments of customer demand, complemented by our other brands in their respective regional markets. With Avis as a premium brand preferred more by corporate and upscale leisure travelers, Budget as a mid-tier brand preferred more by value-conscious travelers, Payless as a deep-value brand, Maggiore and Apex as well-recognized regional brands and Zipcar offering its members an economical alternative to car ownership, we believe we are able to target a broad range of demand, particularly since the brands often share the same operational and administrative infrastructure while providing differentiated though consistently high levels of customer service.

We aim to provide vehicles, products, services and pricing, to use various marketing channels and to maintain marketing affiliations and corporate account contracts that complement each brand’s positioning. We plan to continue to invest in our brands through a variety of efforts, including television commercials, print advertisements and on-line and off-line marketing. We see particular growth opportunities for our Budget brand in Europe, as Budget’s share of airport car rentals is significantly smaller in Europe than in other parts of the world, and for Zipcar internationally, where the brand’s proven car sharing model can be expanded into numerous geographic markets.

7

We operate in a highly competitive industry, and our results can be impacted by external factors, such as travel demand and uncertain economic conditions in various parts of the world. We seek to mitigate our exposure to risks in numerous ways, including delivering upon the core strategic initiatives described above and through continued optimization of fleet levels to match changes in demand for vehicle rentals, maintenance of liquidity to fund our fleet and our operations, and adjustments in the size, nature and terms of our relationships with vehicle manufacturers.

| OUR BRANDS AND OPERATIONS |

OUR BRANDS

Our Avis, Budget and Zipcar brands are three of the most recognized brands in our industry. We believe that we enjoy significant benefits from operating our Avis and Budget brands to target different rental customers but share the same maintenance facilities, fleet management systems, technology and administrative infrastructure. In addition, we are able to recognize significant benefits and savings by combining our car rental and car sharing maintenance activities and fleets at times to reduce the number of unutilized cars and to meet demand peaks. We believe that Avis, Budget and Zipcar all enjoy complementary demand patterns with mid-week commercial demand balanced by weekend leisure demand. We also operate the Apex and Payless brands, which operate in the deep-value segment of the car rental industry, and augment our Avis, Budget and Zipcar brands.

Avis

Avis is a leading rental car supplier positioned to serve the premium commercial and leisure segments of the travel industry. The Avis brand provides high-quality car rental services at price points generally above non-branded and value-branded national car rental companies. We operate or license the Avis car rental system (the “Avis System”), one of the largest car rental systems in the world, comprised of approximately 5,550 locations worldwide, including in virtually all of the largest commercial airports and cities in the world.

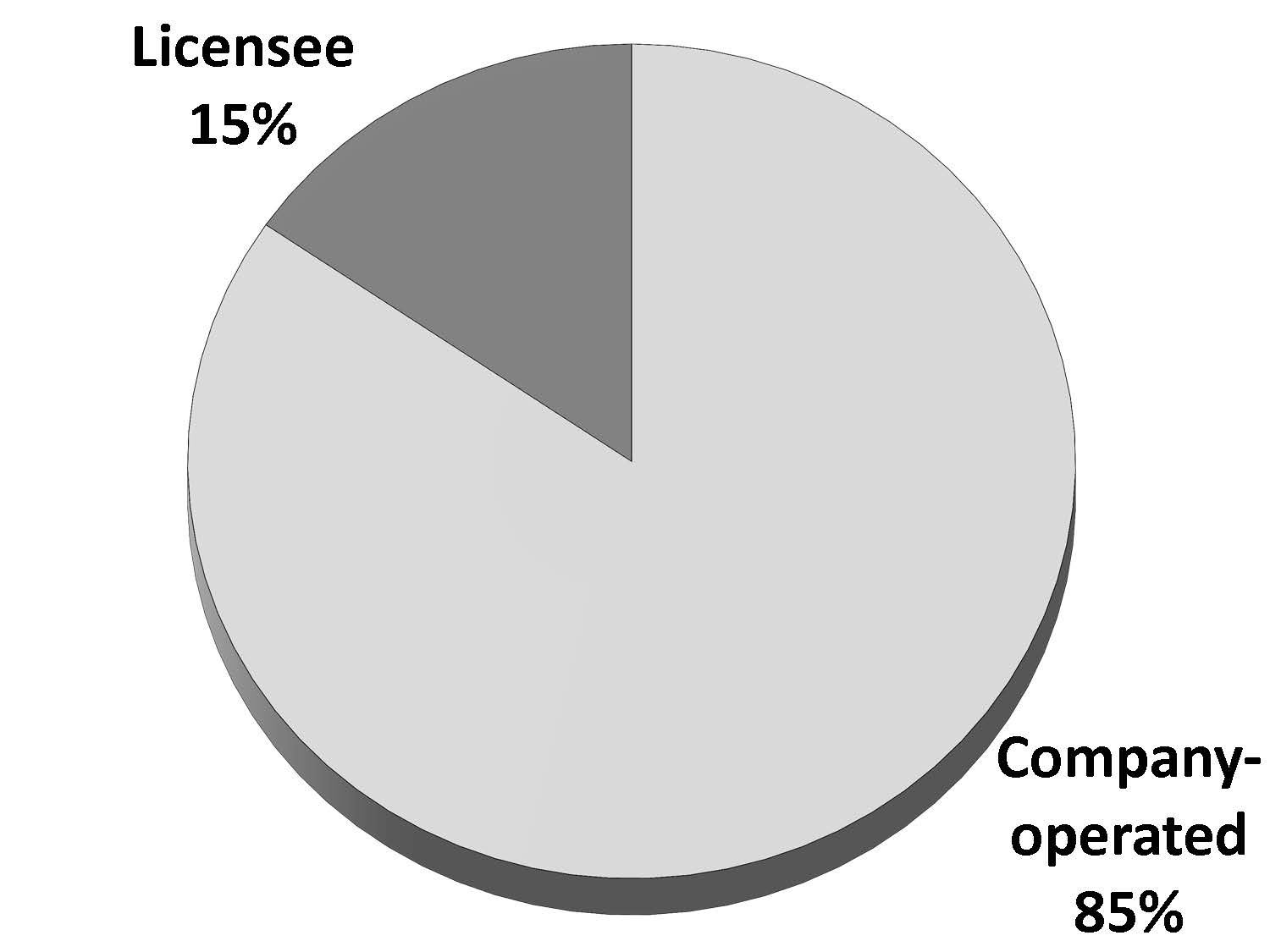

We operate approximately 2,700 Avis car rental locations worldwide, in both the on-airport and off-airport, or local, rental markets. In 2015, our Avis operations generated total revenue of approximately $5.0 billion, of which approximately 64% (or $3.2 billion) was derived from operations in the Americas. In addition, we license the Avis brand to other independent commercial owners in approximately 2,850 locations throughout the world. In 2015, approximately 71% of the Avis System total revenue was generated by our Company-operated locations and the remainder was generated by locations operated by independent licensees, which generally pay royalty fees to us based on a percentage of applicable revenue.

The table below presents the approximate number of locations that comprise the Avis System:

| Avis System Locations | ||||||||

| Americas | International | Total | ||||||

| Company-operated locations | 1,500 | 1,200 | 2,700 | |||||

| Licensee locations | 750 | 2,100 | 2,850 | |||||

| Total Avis System Locations | 2,250 | 3,300 | 5,550 | |||||

8

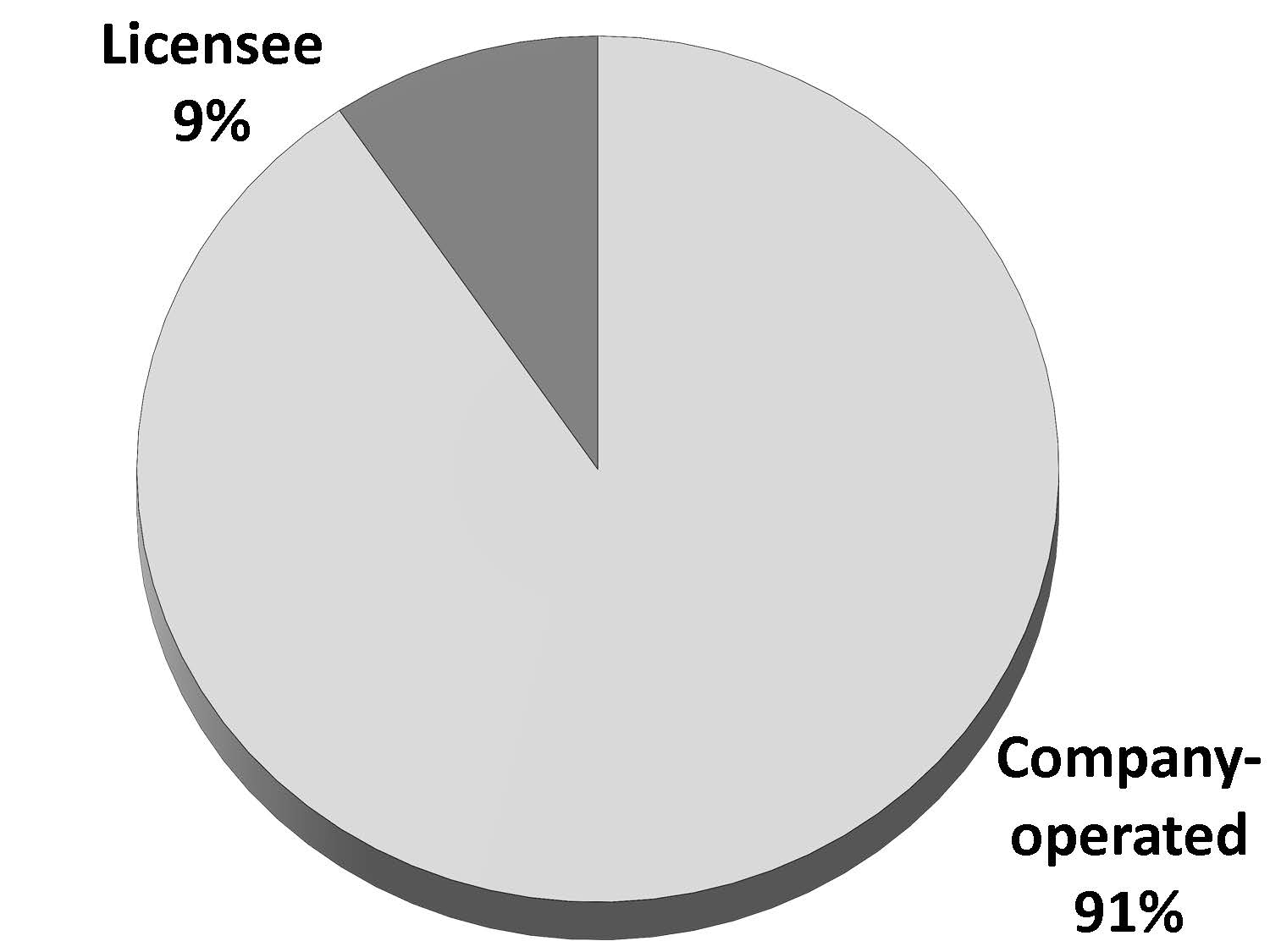

The graphs below present the approximate composition of the Americas Avis System revenue and global Avis System revenue in 2015:

Composition of Americas Avis System Revenue | Composition of Global Avis System Revenue | |||

|  | |||

In 2015, Avis derived approximately $1.8 billion and $1.7 billion (or 51% and 49%) of its vehicle rental revenue from commercial and leisure customers, respectively, and $2.4 billion and $1.1 billion (or 69% and 31%) of its vehicle rental revenue from customers renting at airports and locally, respectively.

We offer Avis customers a variety of premium services, including:

| • | Avis Preferred, a frequent renter rewards program that offers counter bypass at major airport locations and reward points for every dollar spent on vehicle rentals and related products; |

| • | Avis Preferred Select & Go, a service that allows customers at certain locations to select an alternate vehicle or upgrade their vehicle choice without visiting the rental counter; |

| • | Avis Signature Series, a selection of luxury vehicles including BMWs, Corvettes, Mercedes and Maseratis; |

| • | rental of portable GPS navigation units, tablets and in-dash satellite radio service; |

| • | availability of premium, sport and performance vehicles as well as eco-friendly vehicles, including gasoline/electric hybrids; |

| • | roadside assistance; |

| • | e-receipts; |

| • | a 100% smoke-free car rental fleet in North America; |

| • | electronic toll collection services that allow customers to pay highway tolls without waiting in toll booth lines; |

| • | amenities such as Avis Access, a full range of special products and services for drivers and passengers with disabilities; |

| • | Avis Interactive, a proprietary management tool that allows corporate clients to easily view and analyze their rental activity via the Internet, permitting these clients to better manage their travel budgets and monitor employee compliance with applicable travel policies; and |

| • | supporting online interactions with our customers through various mobile platforms, including an application for the Apple Watch and an updated Android application featuring voice-activated reservations. |

Avis was named World’s Leading Car Rental Company by the World Travel Awards in 2015, and was named the leading car rental company in customer loyalty in the Brand Keys Customer Loyalty Engagement Index for the

9

16th consecutive year. In addition, Avis was named to the 2015 Brand Keys Loyalty Leaders List and received numerous other awards.

Budget

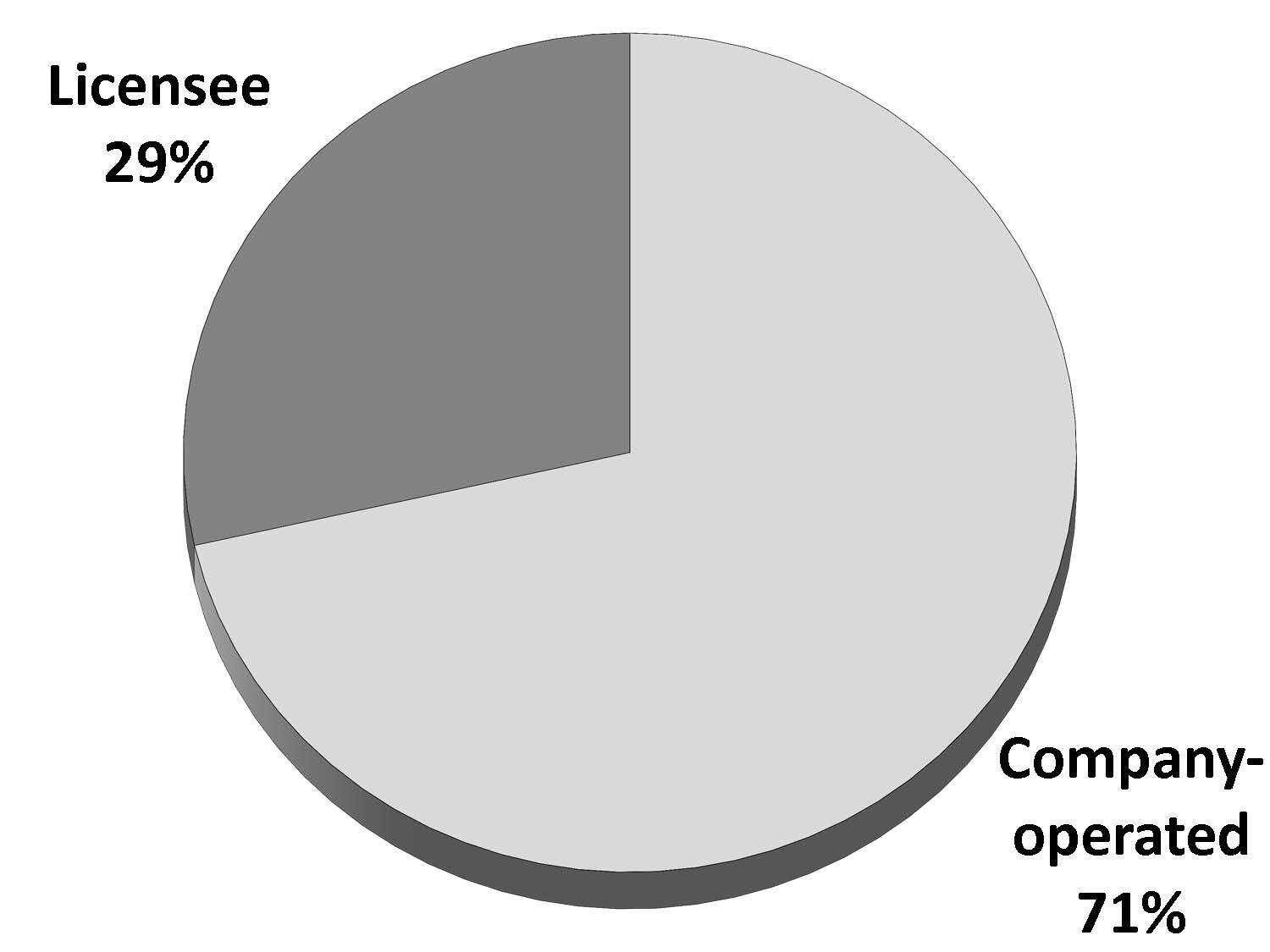

Budget is a leading rental car supplier focused primarily on more value-conscious segments of the industry. We operate or license the Budget vehicle rental system (the “Budget System”), which is comprised of approximately 3,900 car rental locations and represents one of the largest car rental systems in the world. The Budget System encompasses locations at most of the largest airports and cities in the world.

We operate approximately 1,950 Budget car rental locations worldwide. In 2015, our Budget car rental operations generated total revenue of approximately $2.4 billion, of which 84% (or $2.0 billion) was derived from operations in the Americas. We also license the Budget System to independent business owners who operate approximately 1,950 locations worldwide. In 2015, approximately 71% of the Budget System total revenue was generated by our Company-operated locations with the remainder generated by locations operated by independent licensees, which generally pay royalty fees to us based on a percentage of applicable revenue.

The table below presents the approximate number of locations that comprise the Budget System:

| Budget System Locations | ||||||||

| Americas | International | Total | ||||||

| Company-operated locations | 1,350 | 600 | 1,950 | |||||

| Licensee locations | 650 | 1,300 | 1,950 | |||||

| Total Budget System Locations | 2,000 | 1,900 | 3,900 | |||||

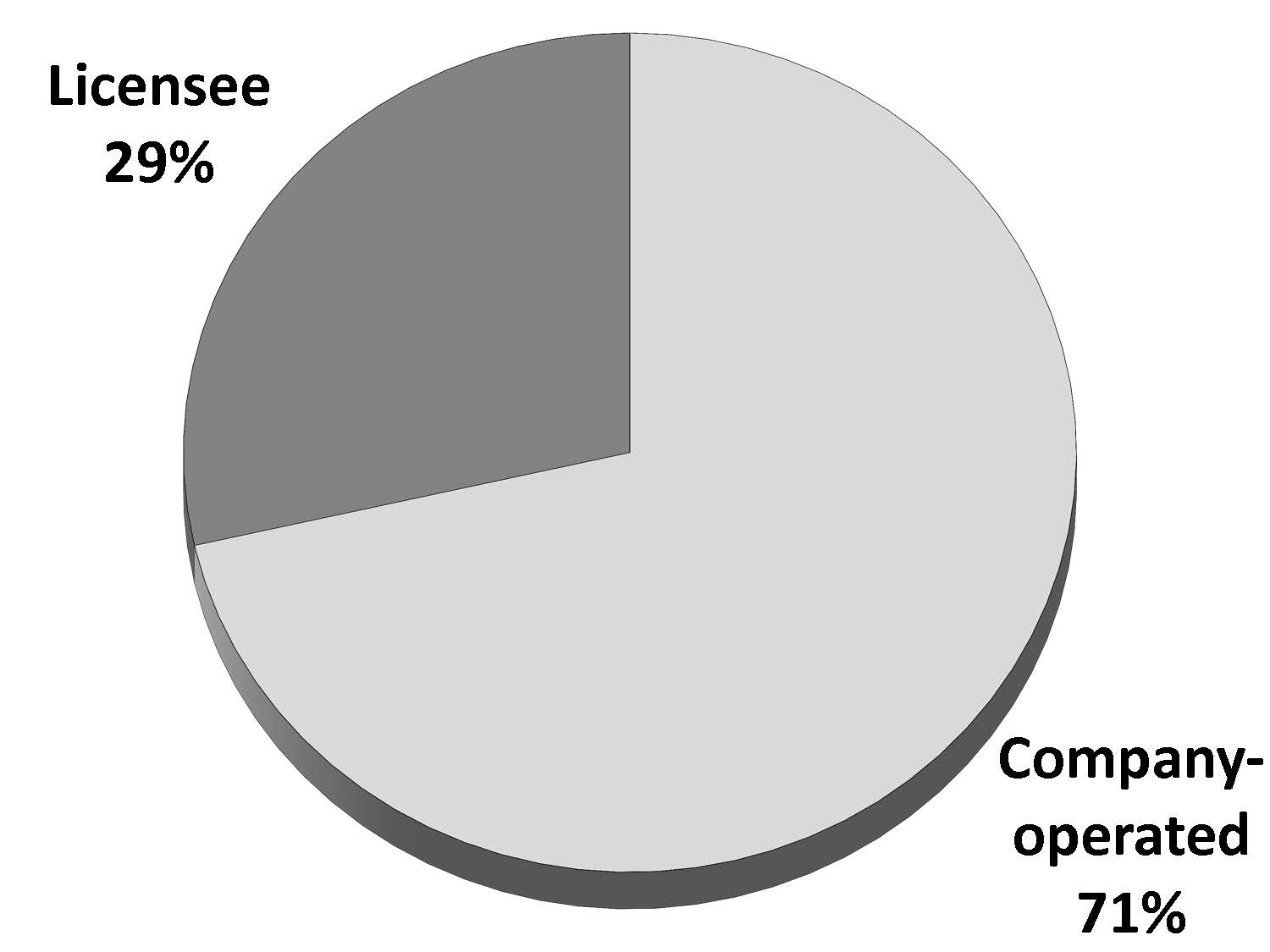

The graphs below present the approximate composition of the Americas Budget System revenue and global Budget System revenue in 2015:

Composition of Americas Budget System Revenue | Composition of Global Budget System Revenue | |||

|  | |||

In 2015, Budget derived approximately $445 million and $1.3 billion (or 26% and 74%) of its vehicle rental revenue from commercial and leisure customers, respectively, and $1.3 billion and $415 million (or 76% and 24%) of its vehicle rental revenue from customers renting at airports and locally, respectively.

Budget offers its customers several products and programs similar to Avis, such as portable GPS navigation units, roadside assistance, electronic toll collection, emailed receipts and refueling options, as well as special rental rates for frequent renters and Budget’s Fastbreak service, an expedited rental service for frequent travelers.

In 2015, Budget received numerous awards, including for its award-winning loyalty program, Unlimited Rewards®, which was selected by Travel Weekly as a 2015 Gold Magellan Award Winner.

Zipcar

Founded in 2000, Zipcar operates the world’s leading membership-based car sharing network that provides “wheels when you want them” to nearly one million members, also known as “Zipsters,” in over 30 major

10

metropolitan areas and over 500 college campuses in the United States, Canada and Europe. Zipcar provides its members self-service vehicles in reserved parking spaces located in residential neighborhoods, business districts, college campuses, business office complexes and airports.

Our members may reserve vehicles by the hour or by the day at rates that include gasoline, insurance and other costs associated with vehicle ownership, and they can make their reservations through Zipcar’s reservation system, which is available by phone, Internet or through the Zipcar application on their smartphone. Our members have the flexibility to choose from a variety of makes and models of vehicles that they want depending on their specific needs and desires for each trip and the available Zipcars in their neighborhoods. The flexibility and affordability of our service, as well as broader consumer trends toward responsible and sustainable living, provide a significant platform for future growth.

We continue to make substantial investment in refining, innovating and enhancing Zipcar’s operations and fleet management systems, and we have integrated numerous elements of Zipcar’s operations and fleet management into our existing processes. We believe that the experience that we have gained and continue to accumulate while growing and operating our network is a key advantage, informing our decisions regarding our existing operations and services as well as our plans for expansion.

Zipcar offers its members the freedom of on-demand access to a fleet of vehicles at any hour of the day or night, in their neighborhood or in any of our Zipcar cities and locations. Benefits to members include:

| • | Cost-effective alternative to car ownership - Members pay for time they reserve the vehicle and have no responsibility for the additional costs and hassles associated with car ownership, including parking, gasoline, taxes, registration, insurance, maintenance and lease payments. |

| • | Convenience and accessible fleet - Zipcars are interspersed throughout local neighborhoods, colleges and corporate campuses where they are parked in reserved parking spaces and garages within an easy walk of where our members live, study and work. Members can book a designated vehicle online, by phone or via their mobile device, unlock the selected vehicle using a keyless entry card (called a “Zipcard”), and drive away. Because each Zipcar has a designated parking space, members are spared the often time-consuming undertaking of finding an available parking spot. |

| • | Freedom and control - We provide our members with much of the freedom associated with car ownership while being complementary to public transportation options. Like car owners, our members can choose when and where they want to drive. They also have the added benefit of being able to choose, based upon the readily available Zipcars in their neighborhoods, the make, model and type of vehicle they want to drive based on their specific needs and desires for each trip. |

| • | Responsible and sustainable living - We are committed to providing our members with socially responsible, sustainable options that support the global environment, their communities and city livability. Studies show that car sharing reduces the number of miles driven, the number of personally-owned vehicles on the road and carbon emissions. |

| • | Zipcar for Universities - We provide college students, faculty, staff and local residents living in or near rural and urban campuses with access to Zipcars. Zipcars are located on over 500 college and university campuses. Our program for universities helps university administrators maximize the use of limited parking space on campus and reduce campus congestion while providing an important amenity for students, faculty, staff and local residents. In some cases, Zipcar may be the only automobile transportation available to students, since many traditional rental car services have higher age restrictions. |

In 2015, we rolled out our Instant Join program, reducing the time it takes to become a Zipcar member from up to a week to as little as 2.5 minutes. In addition, we launched Zipcar’s ONE>WAY program in selected markets, allowing members to take on-demand one-way trips. The Zipcar brand has continued to be recognized as the world’s leading car sharing network and for the quality of the customer experience it offers.

11

Budget Truck

Our Budget Truck rental business is one of the largest local and one-way truck rental businesses in the United States. Our Budget Truck fleet is comprised of approximately 21,000 vehicles that are rented through a network of approximately 1,000 dealers and 450 Company-operated locations throughout the continental United States. These dealers are independently-owned businesses that generally operate other retail service businesses. In addition to their principal businesses, the dealers rent our light- and medium-duty trucks to consumers and to our commercial accounts and are responsible for collecting payments on our behalf. The dealers receive a commission on all truck and ancillary equipment rentals. The Budget Truck rental business serves both the consumer and light commercial sectors. The consumer sector consists primarily of individuals who rent trucks to move household goods on either a one-way or local basis. The light commercial sector consists of a wide range of businesses that rent light- to medium-duty trucks, which we define as trucks having a gross vehicle weight of less than 26,000 pounds, for a variety of commercial applications.

Other Brands

Our Payless brand is a leading rental car supplier positioned to serve the deep-value segment of the car rental industry. We operate or license the Payless brand, which is comprised of approximately 200 vehicle rental locations worldwide, including approximately 80 Company-operated locations and more than 100 locations operated by licensees. All Company-operated Payless locations are in the United States, the majority of which are at or near major airport locations. Payless’ base T&M fees are often lower than those of larger, more established brands, but Payless has historically achieved a greater penetration of ancillary products and services with its customers. The Payless business model allows the Company to extend the life cycle of a portion of our fleet, as we “cascade” certain vehicles that exceed certain Avis and Budget age or mileage thresholds to be used by Payless.

Our Apex brand operates primarily in the deep-value segment of the car rental industry in New Zealand and Australia, where we have approximately 20 Apex rental locations. Apex operates its own rental fleet, separate from Avis and Budget vehicles and generally older and less expensive than vehicles offered by Avis, Budget and other traditional car rental companies. Apex generates substantially all of its reservations through its proprietary websites and contact center and typically has a greater than average length of rental. The substantial majority of Apex locations are at or near major airport locations.

In 2015, we acquired Maggiore Group, a leading vehicle rental services company in Italy, and we continue to operate more than 100 rental locations in Italy under the Maggiore brand. Our Maggiore brand is the fourth-largest vehicle rental brand in Italy and has a strong domestic reputation in the commercial, leisure and insurance replacement/leasing segments. Maggiore benefits from a strong presence at airport, off-airport and railway locations. We have integrated numerous elements of Maggiore’s operations and fleet management into our existing processes.

RESERVATIONS, MARKETING AND SALES

Reservations

Our customers can make vehicle rental reservations through our brand-specific websites and through our toll-free reservation centers, by calling a specific location directly, through brand-specific mobile applications, through online travel agencies, through travel agents or through selected partners, including many major airlines. Travel agents can access our reservation systems through all major global distribution systems (“GDSs”), which provide information with respect to rental locations, vehicle availability and applicable rate structures.

Our Zipcar members may reserve cars by the hour or by the day through Zipcar’s reservation system, which is accessible by phone, Internet or through the Zipcar application on their smartphone. We also provide two-way SMS texting, enabling us to proactively reach out to members during their reservation via their mobile device to manage their reservation, including instant reservation extension.

In 2015, we generated approximately 28% of our vehicle rental reservations through our brand-specific websites, 11% through our contact centers, 26% through GDSs, 13% through online travel agencies, 10% through direct-connect technologies and 12% through other sources. Virtually all of our Zipcar car sharing reservations were

12

generated online or through our Zipcar mobile applications. We use a voice reservation system that allows customers to conduct certain transactions such as confirmation, cancellation and modification of reservations using self-service interactive voice response technology. In addition to our Zipcar mobile applications, we have also developed Avis and Budget mobile applications for various mobile platforms, allowing our customers to more easily manage their car rental reservations on their mobile devices.

Marketing and Sales

We support our brands through a range of marketing channels and campaigns, including traditional media, such as television, radio and print advertising, as well as Internet and email marketing and wireless mobile device applications. We also utilize a customer relationship management system that enables us to deliver more targeted and relevant offers to customers across both online and offline channels and allows our customers to benefit through better and more relevant marketing, improved service delivery and loyalty programs that reward frequent renters with free rental days and car class upgrades.

We use social media to promote our brands and to provide our customers with the tools to interact with our brands electronically through social media and other web-based platforms. We also use digital marketing activities to drive international reservations.

Our Zipcar brand also utilizes localized marketing initiatives, which include low-cost, word-of-mouth marketing strategies and the use of marketing “brand ambassadors” that target potential members on a more personal, local level. These efforts highlight simple messages that communicate the benefits of “wheels when you want them.” Zipcar members also actively recruit new members as incentivized by Zipcar’s member referral program, which awards driving credit for new member referrals.

In 2015, we maintained, expanded or entered into marketing alliances with key marketing partners that include brand exposure and cross-marketing opportunities for each of the brands involved. For example, in 2015, Avis and Budget were named the “Official Car Rental Partners” of Universal Parks & Resorts, and as the “Official Rental Car of the PGA TOUR,” Avis promoted its products and services to millions of golf enthusiasts worldwide through prominent advertising placements in PGA TOUR television broadcasts, scoreboards at tournaments, online media channels and additional official partner channels.

We continue to maintain strong links to the travel industry and we expanded or entered into marketing alliances with numerous marketing partners in 2015:

| • | We maintain marketing partnerships with many major airlines, including Air Canada, Air France, Air New Zealand, American Airlines, British Airways, Frontier Airlines, Iberia, Japan Airlines, JetBlue Airlines, KLM, Lufthansa, Qantas, SAS, Southwest Airlines and Virgin America. |

| • | We maintain marketing partnerships with several major hotel companies, including Best Western International, Inc., Hilton Hotels Corporation, Hyatt Corporation, MGM Resorts International, Radisson Hotels and Resorts, Starwood Hotels and Resorts Worldwide, Inc., Universal Parks & Resorts and Wyndham Worldwide. |

| • | We offer customers the ability to earn frequent traveler points with many major airlines’ and hotels’ frequent traveler programs, and we are the exclusive rental partner of the Wyndham Rewards program. |

| • | And we have marketing relationships with numerous non-travel-related entities, including affinity groups, membership organizations, retailers, financial institutions and credit card companies. |

In 2015, approximately 62% of vehicle rental transactions from our Company-operated Avis locations were generated by travelers who rented from Avis under contracts between Avis and the travelers’ employers or through membership in an organization with which Avis has a contractual affiliation (such as AARP and Costco Wholesale). Avis maintains marketing relationships with other organizations such as American Express, MasterCard International and Sears, through which we are able to provide their customers with incentives to rent from Avis. Avis licensees also generally have the option to participate in these affiliations.

13

Additionally, we offer “Unlimited Rewards®,” an award-winning loyalty incentive program for travel agents, and the Budget Small Business Program, a program for small businesses that offers discounted rates, central billing options and rental credits to its members. Budget has contractual arrangements with American Express, MasterCard International and other organizations, which offer members incentives to rent from Budget.

Budget Truck also maintains certain truck-rental-specific marketing and/or co-location relationships, including those with Sears, Simply Self Storage and Extra Space Storage. We also have an exclusive agreement to advertise Budget Truck rental services in the Mover’s Guide, an official U.S. Postal Service change of address product.

Our Zipcar brand also partners with other active lifestyle brands that appeal to our Zipcar members and organizes, sponsors and participates in charitable and community events with organizations important to us and our Zipcar members. Zipcar maintains close relationships with universities that allow us to market to the “next generation consumer” that, upon graduation, may migrate to the major metropolitan areas that we serve, continue their relationship with us and advocate for broad sponsorship of Zipcar membership at their places of work. Through our Zipcar for Business program, we also offer reduced membership fees and weekday driving rates to employees of companies, federal agencies and local governments that sponsor the use of Zipcars.

LICENSING

We have licensees in approximately 165 countries throughout the world. Royalty fee revenue derived from our vehicle rental licensees in 2015 totaled $131 million, with approximately $93 million in our International segment and $38 million in our Americas segment. Licensed locations are independently operated by our licensees and range from large operations at major airport locations and territories encompassing entire countries to relatively small operations in suburban or rural locations. Our licensees generally maintain separate independently owned and operated fleets. Royalties generated from licensing provide us with a source of high-margin revenue because there are relatively limited additional fixed costs associated with fees paid by licensees to us. Locations operated by licensees represented approximately 50% of our Avis and Budget car rental locations worldwide and approximately 29% of total revenue generated by the Avis and Budget Systems in 2015. We facilitate one-way car rentals between Company-operated and licensed locations, which enables us to offer an integrated network of locations to our customers.

We generally enjoy good relationships with our licensees and meet regularly with them at regional, national and international meetings. Our relationships with our licensees are governed by license agreements that grant the licensee the right to operate independently operated vehicle rental businesses in certain territories. Our license agreements generally provide our licensees with the exclusive right to operate in their assigned territory. These agreements impose obligations on the licensee regarding its operations and most agreements restrict the licensee’s ability to sell, transfer or assign its license agreement and capital stock. Licensees are generally required to adhere to our system standards for each brand as updated and supplemented by our policy bulletins, brand manuals and service program.

The terms of our license agreements, including duration, royalty fees and termination provisions, vary based upon brand, territory, and original signing date. Royalty fees are generally structured to be a percentage of the licensee’s gross rental income. We maintain the right to monitor the operations of licensees and, when applicable, can declare a licensee to be in default under its license agreement. We perform audits as part of our program to assure licensee compliance with brand quality standards and contract provisions. Generally, we can terminate license agreements for certain defaults, including failure to pay royalties or adhere to our operational standards. Upon termination of a license agreement, the licensee is prohibited from using our brand names and related marks in any business. In the United States, these license relationships constitute “franchises” under most federal and state laws regulating the offer and sale of franchises and the relationship of the parties to a franchise agreement.

OTHER REVENUE

In addition to revenue from our vehicle rentals and licensee royalties, we generate revenue from our customers through the sale and/or rental of optional ancillary products and services and membership fees. We offer products to customers that will enhance their rental experience, including collision and loss damage waivers, under which we agree to relieve a customer from financial responsibility arising from vehicle damage incurred during the rental

14

period if the customer has not breached the rental agreement. Other products offered include insurance products such as additional/supplemental liability insurance or personal accident/effects insurance, products for driving convenience such as portable GPS navigation units, tablet rentals, optional roadside assistance services, fuel service options, electronic toll collection, access to satellite radio and child safety seat rentals. We also supplement our daily truck rental revenue by offering customers automobile towing equipment and other moving accessories such as hand trucks, furniture pads and moving supplies. In addition, we receive payment from our customers for certain operating expenses that we incur, including gasoline and vehicle licensing fees, as well as airport concession fees that we pay in exchange for the right to operate at airports and other locations. In 2015, approximately 6% of our revenue was generated by the sale of collision and loss damage waivers.

OUR TECHNOLOGIES

Car Rental

We use a broad range of technologies in our car rental operations, substantially all of which are linked to what we call our Wizard system, which is a worldwide reservation, rental, data processing and information management system. The Wizard system enables us to process millions of incoming customer inquiries each day, providing our customers with accurate and timely information about our locations, rental rates and vehicle availability, as well as the ability to place or modify reservations. Additionally, the Wizard system is linked to all major travel distribution networks worldwide and provides real-time processing for travel agents, travel industry partners (such as airlines and online travel sites), corporate travel departments and individual consumers through our websites or contact centers. The Wizard system also provides personal profile information to our reservation and rental agents to help us better serve our customers.

We also use data supplied from the Wizard system and other third-party reservation and information management systems to maintain centralized control of major business processes such as fleet acquisition and logistics, sales to corporate accounts and determination of rental rates. The principal components of the systems we employ include:

| • | Fleet planning model. We have a comprehensive decision tool to develop fleet plans and schedules for the acquisition and disposition of our fleet, along with fleet age, mix, mileage and cost reports based upon these plans and schedules. This tool allows management to monitor and change fleet volume and composition on a daily basis and to optimize our fleet plan based on estimated business levels and available repurchase and guaranteed depreciation programs. We also use third-party software to further optimize our fleet acquisition, rotation and disposition activities. |

| • | Yield management. We have a yield management system which is designed to enhance profits by providing greater control of vehicle availability and rate availability changes at our rental locations. Our system monitors and forecasts supply and demand to support our efforts to optimize volume and rate at each location. Integrated into this yield management system is a fleet distribution module that takes into consideration the costs as well as the potential benefits associated with distributing vehicles to various rental locations within a geographic area to accommodate rental demand at these locations. The fleet distribution module makes specific recommendations for movement of vehicles between locations. |

| • | Pricing decision support systems. Pricing in the vehicle rental industry is highly competitive and complex. To improve our ability to respond to rental rate changes in the marketplace, we have utilized sophisticated systems to gather and report competitive industry rental rate changes every day. Our systems, using data from third-party reservation systems as its source of information, automatically scan rate movements and report significant changes to our staff of pricing analysts for evaluation. These systems greatly enhance our ability to gather and respond to rate changes in the marketplace. In 2015, we began to implement an integrated pricing and fleet optimization tool that has allowed us to test and implement improved pricing strategies and optimization algorithms, as well as automate the implementation of certain price changes. |

| • | Customer service application. Our customer service application is a comprehensive case management system that our customer care agents use to handle a variety of issues and questions from our customers around the world. The multi-branded system interfaces seamlessly with our Wizard system and gives our agents current and historical information about a caller so that they are better equipped to provide |

15

informed and expedited assistance, while at the same time allowing us to be consistent in our case handling and responses.

| • | Enterprise data warehouse. We have developed a sophisticated and comprehensive electronic data storage and retrieval system which retains information related to various aspects of our business. This data warehouse allows us to take advantage of comprehensive management reports and provides easy access to data for strategic decision making for our brands. |

| • | Sales and marketing systems. We have developed a sophisticated system of online data tracking which enables our sales force to analyze key account information of our corporate customers including historical and current rental activity, revenue and booking sources, top renting locations, rate usage categories and customer satisfaction data. We use this information, which is updated weekly and captured on a country-by-country basis, to assess opportunities for revenue growth, profitability and improvement. |

| • | Campaign management. We have deployed tools that enable us to recognize customer segments and value, and to automatically present appropriate offers on our websites. |

| • | Interactive adjustments. We have developed a customer data system that allows us to easily retrieve pertinent customer information and make needed adjustments to completed rental transactions online for superior customer service. This data system links with our other accounting systems to handle any charge card transaction automatically. |

| • | Interactive voice response system. We have developed an automated voice response system that enables the automated processing of customer reservation confirmations, cancellations, identification of rental locations, extension of existing rentals and requests for copies of rental receipts over the phone using speech recognition software. |

Car Sharing

Our Zipcar car sharing technology was specifically designed and built for our car sharing business and has been continually refined and upgraded to optimize the Zipcar experience for our members. Our fully-integrated platform centralizes the management of our Zipcar reservations, member services, fleet operations and financial systems to optimize member experience, minimize costs and leverage efficiencies. Through this platform, we:

| • | process new member applications; |

| • | manage reservations and keyless vehicle access; |

| • | manage and monitor member interactions; |

| • | manage billing and payment processing across multiple currencies; |

| • | manage our car sharing fleet remotely; and |

| • | monitor and analyze key metrics of each Zipcar such as utilization rate, mileage and maintenance requirements. |

Each Zipcar is equipped with a telematics control unit, including mobile data service, radio frequency identification card readers, wireless antennae, wiring harness, vehicle interface modules and transponders for toll systems. This hardware, together with internally developed embedded firmware and vehicle server software, allows us to authorize secure access to our Zipcars from our data centers and provides us with a comprehensive set of fleet management data that is stored in our centralized database.

Each interaction between members and our Zipcars is captured in our system, across all communication channels, providing us with knowledge we use to improve our members’ experiences and better optimize our business processes. We have built and continue to innovate our technology platform in order to support growth and scalability.

16

OUR FLEET

We offer a wide variety of vehicles in our rental fleet, including luxury cars and specialty-use vehicles. Our fleet consists primarily of vehicles from the current and immediately preceding model year. We maintain a single fleet of vehicles for Avis and Budget in countries where we operate both brands. The substantial majority of Zipcar’s fleet is dedicated to use by Zipcar, but we have developed processes to share vehicles between the Avis/Budget fleet and Zipcar’s fleet primarily to help meet Zipcar’s demand peaks. We maintain a diverse car rental fleet, in which no vehicle manufacturer represented more than 21% of our 2015 fleet purchases, and we regularly adjust our fleet levels to be consistent with demand. We participate in a variety of vehicle purchase programs with major vehicle manufacturers. In 2015, we purchased vehicles from Audi, BMW, Chrysler, Fiat, Ford, General Motors, Honda, Hyundai, Land Rover, Kia, Maserati, Mazda, Mercedes, Mitsubishi, Nissan, Peugeot, Porsche, Renault, Subaru, Toyota and Volkswagen, among others. During 2015, approximately 21%, 17% and 7% of the cars acquired for our car rental fleet were manufactured by Ford, General Motors and Chrysler, respectively.

Fleet costs represented approximately 25% of our aggregate expenses in 2015. Fleet costs can vary from year to year based on the prices at which we are able to purchase and dispose of rental vehicles.

In 2015, on average, approximately 49% of our rental car fleet was comprised of vehicles subject to agreements requiring automobile manufacturers to repurchase vehicles at a specified price during a specified time period or guarantee our rate of depreciation on the vehicles during a specified period of time, or were vehicles subject to operating leases. We refer to cars subject to these agreements as “program” cars and cars not subject to these agreements as “risk” cars because we retain the risk associated with such cars’ residual values at the time of their disposition. Such agreements typically require that we pay more for program cars and maintain them in our fleet for a minimum number of months and impose certain return conditions, including car condition and mileage requirements. When we return program cars to the manufacturer, we receive the price guaranteed at the time of purchase and are thus protected from fluctuations in the prices of previously-owned vehicles in the wholesale market. In 2015, approximately 64% of the vehicles we disposed of were sold pursuant to repurchase or guaranteed depreciation programs. The future percentages of program and risk cars in our fleet will depend on several factors, including our expectations for future used car prices, our seasonal needs and the availability and attractiveness of manufacturers’ repurchase and guaranteed depreciation programs. The Company has agreed to purchase approximately $7.2 billion of vehicles from manufacturers over the next twelve months.

We dispose of our risk cars largely through automobile auctions, including auctions that enable dealers to purchase vehicles online more quickly than through traditional auctions, as well as through direct-to-dealer sales. In 2015, we continued to expand the number of states that can participate in our Ultimate Test Drive consumer car sales program, which offers customers the ability to purchase our rental vehicles. Alternative disposition channels such as Ultimate Test Drive, online auctions and direct to dealer sales represented approximately 34% of our risk vehicle dispositions in the Americas in 2015 and provide us with per-vehicle cost savings compared to selling cars at auctions.

For 2015, our average monthly vehicle rental fleet size (including U.S. rental trucks) ranged from a low of approximately 494,000 vehicles in January to a high of approximately 690,000 vehicles in July. Our average monthly car rental fleet size typically peaks in the summer months. Average fleet utilization for 2015, which is based on the number of rental days (or portion thereof) that vehicles are rented compared to the total amount of time that vehicles are available for rent, ranged from 65% in January to 75% in August. Our calculation of utilization may not be comparable to other companies’ calculation of similarly titled statistics.

We place a strong emphasis on vehicle maintenance for customer safety and customer satisfaction reasons, and because quick and proper repairs are critical to fleet utilization. To accomplish this task we employ a fully-certified National Institute for Automotive Service Excellence technician instructor and have developed a specialized training program for our technicians. Our technician training department prepares its own technical service bulletins that can be retrieved electronically at our repair locations. In addition we have implemented policies and procedures to promptly address manufacturer recalls as part of our ongoing maintenance and repair efforts.

CUSTOMER SERVICE

We believe our commitment to delivering a consistently high level of customer service across all of our brands is a critical element of our success and strategy. Our Customer Led, Service Driven™ program focuses on improving

17

the overall customer experience based on our research of customer service practices, improved customer insights, executing our customer relationship management strategy and delivering customer-centric employee training.

Our associates and managers at our Company-operated locations are trained and empowered to resolve most customer issues at the location level. In addition, we have simplified our rental agreements for both the Avis and Budget brands to make them easier for our customers to read and understand. We also continuously track customer-satisfaction levels by sending location-specific surveys to recent customers and utilize detailed reports and tracking to assess and identify ways that we can improve our customer service delivery and the overall customer experience. In 2015, we received feedback from more than 1 million customers. Our location-specific surveys ask customers to evaluate their overall satisfaction with their rental experience, among other things. Results are analyzed in aggregate and by location to help further enhance our service levels to our customers.

In 2015, we also introduced a new comprehensive case management system that our customer care agents use to consistently and expeditiously handle a variety of issues and questions from our customers around the world.

EMPLOYEES

As of December 31, 2015, we employed approximately 30,000 people worldwide, of whom approximately 7,300 were employed on a part-time basis. Of our approximately 30,000 employees, approximately 21,000 were employed in our Americas segment and 9,000 in our International segment.

In our Americas segment, the majority of our employees are at-will employees and, therefore, not subject to any type of employment contract or agreement. Certain of our executive officers may be employed under employment contracts that specify a term of employment and specify pay and other benefits. In our International segment, we enter into employment contracts and agreements in those countries in which such relationships are mandatory or customary. The provisions of these agreements correspond in each case with the required or customary terms in the subject jurisdiction. Many of our employees are covered by a wide variety of union contracts and governmental regulations affecting, among other things, compensation, job retention rights and pensions.

As of December 31, 2015, approximately 35% of our employees were covered by collective bargaining agreements with various labor unions. We believe our employee relations are satisfactory. We have never experienced a large-scale work stoppage.

AIRPORT CONCESSION AGREEMENTS

We generally operate our vehicle rental and car sharing services at airports under concession agreements with airport authorities, pursuant to which we typically make airport concession payments and/or lease payments. In general, concession fees for on-airport locations are based on a percentage of total commissionable revenue (as defined by each airport authority), subject to minimum annual guaranteed amounts. Concessions are typically awarded by airport authorities every three to ten years based upon competitive bids. Our concession agreements with the various airport authorities generally impose certain minimum operating requirements, provide for relocation in the event of future construction and provide for abatement of the minimum annual guarantee in the event of extended low passenger volume.

| OTHER BUSINESS CONSIDERATIONS |

SEASONALITY

Our car rental business is subject to seasonal variations in customer demand patterns, with the spring and summer vacation periods representing our peak seasons. We vary our fleet size over the course of the year to help manage any seasonal variations in demand, as well as localized changes in demand.

COMPETITION

The competitive environment for the vehicle rental industry is generally characterized by intense price and service competition among global, local and regional competitors. Competition in our vehicle rental operations is based primarily upon price, customer service quality, including usability of booking systems and ease of rental and

18

return, vehicle availability, reliability, rental locations, product innovation and national or international distribution. In addition, competition is also influenced strongly by advertising, marketing, loyalty programs and brand reputation.

The use of technology has increased pricing transparency among vehicle rental companies by enabling cost-conscious customers to more easily compare on the Internet and their mobile devices the rental rates available from various vehicle rental companies for any given rental. This transparency has further increased the prevalence and intensity of price competition in the industry.

Our vehicle rental and car sharing operations compete primarily with Enterprise Holdings, Inc., which operates the Enterprise, National and Alamo car rental brands; Europcar Group; Hertz Global Holdings, Inc., which operates the Hertz, Dollar and Thrifty brands; and Sixt AG. We also compete with smaller regional vehicle rental and car sharing companies as well as truck rental companies such as U-Haul International, Inc., Penske Truck Leasing Corporation, and Ryder Systems, Inc.

INSURANCE AND RISK MANAGEMENT

Our vehicle rental operations and corporate operations expose us to various types of claims for bodily injury, death and property damage related to the use of our vehicles and/or properties, as well as general employment-related matters stemming from our operations. We generally assume the risk of liability to third parties arising from vehicle rental and car sharing services in the United States, Canada, Puerto Rico and the U.S. Virgin Islands, in accordance with the minimum financial responsibility requirements (“MFRs”) and primacy of coverage laws of the relevant jurisdiction. In certain cases, we assume liability above applicable MFRs, but to no more than $1 million per occurrence, other than in cases involving a negligent act on the part of the Company, for which we purchase insurance coverage for exposures beyond retained amounts from a combination of unaffiliated excess insurers.

In Europe, we insure the risk of liability to third parties arising from vehicle rental and car sharing services in accordance with local regulatory requirements through a combination of insurance policies provided by unaffiliated insurers and through reinsurance. We may retain a portion of the insured risk of liability, including reinsuring certain risks through our captive insurance subsidiary AEGIS Motor Insurance Limited. We limit our retained risk of liability through the unaffiliated insurers. We insure the risk of liability to third parties in Argentina, Australia, Brazil and New Zealand through a combination of unaffiliated insurers and one of our affiliates. These insurers provide insurance coverage supplemental to minimum local requirements.