ALLIANZ Index Advantage Income® VARIABLE ANNUITY CONTRACT

An individual flexible purchase payment index-linked and variable deferred annuity contract (the Contract)

Issued by Allianz Life® Variable Account B (the Separate Account) and

Allianz Life Insurance Company of North America (Allianz Life, we, us, our)

Prospectus Dated: April 30, 2021

| Standard Annuity Features | Available Investment Options | Additional Features |

| • Five fixed annuitization options (Annuity Options)• Free withdrawal privilege during the six-year withdrawal charge period• Systematic withdrawal program• Minimum distribution program for certain tax-qualified Contracts• Waiver of withdrawal charge benefit (not available in all states)• Guaranteed death benefit (Traditional Death Benefit) | • 31 index-linked investment options (Index Options) based on different combinations of five credit calculation methods (Crediting Methods), four nationally recognized third-party broad based equity securities indexes and an exchange-traded fund (Index or Indexes), and three time periods for measuring Index performance (Term) | • Income Benefit: Provides guaranteed lifetime income (Income Payments) based on a percentage of your investment value that can begin as early as age 50, or as late as age 100.This benefit is automatically included in the Contract, can be removed after three years, and has an additional rider fee. If you remove the Income Benefit you will have paid for the benefit without receiving any of its advantages.• Maximum Anniversary Value Death Benefit: Locks in any annual investment gains to potentially provide a death benefit greater than the Traditional Death Benefit. This optional benefit must be selected at issue, cannot be removed, and has an additional rider fee. |

| The risk of loss can become greater in the case of an early withdrawal due to withdrawal charges. Withdrawals will be subject to federal and state taxation, and withdrawals taken before age 59 1⁄2 may also be subject to a 10% additional federal tax. If this is a Non-Qualified Contract, a withdrawal will be taxable to the extent that gain exists within the Contract. A Non-Qualified Contract is a Contract that is not purchased under a pension or retirement plan that qualifies for special tax treatment under sections of the Internal Revenue Code (the Code). | ||

| Crediting Methods Currently Available Only the Index Performance Strategy offers 1-year, 3-year, and 6-year Terms. All other Crediting Methods only offer 1-year Terms. | Indexes Currently Available with 1-year Terms | Indexes Currently Available with 3-year and 6-year Terms (Index Performance Strategy only) |

| • Index Protection Strategy with Declared Protection Strategy Credit (the DPSC is the return you receive if Index performance is zero or positive) • Index Protection Strategy with Cap • Index Precision Strategy (only available before Income Payments begin) • Index Guard Strategy (only available before Income Payments begin) • Index Performance Strategy (only available before Income Payments begin) | • S&P 500® Index • Russell 2000® Index • Nasdaq-100® Index • EURO STOXX 50® • iShares® MSCI Emerging Markets ETF | • S&P 500® Index • Russell 2000® Index |

| Crediting Methods, Indexes, and the 3-year and 6-year Terms may not be available in all states, or to Contracts issued before April 30, 2021, as detailed in Appendix H. | ||

Allianz Index Advantage Income® Variable Annuity Prospectus – April 30, 2021

1

| Crediting Method Highlights All Crediting Methods provide a level of protection against negative Credits from negative Index performance, and a limit on positive Credits from positive Index performance. Credits are the return you receive from the Index Options. | ||

| Negative Index Performance Protection | Positive Index Performance Participation Limit | |

| Index Protection Strategy with DPSC | • 100% – You will never receive a negative Credit | • Declared Protection Strategy Credits (DPSCs) – DPSCs cannot be less than 0.50% |

| Index Protection Strategy with Cap | • 100% – You will never receive a negative Credit | • Caps (the upper limit on positive Index performance) – Caps cannot be less than 0.50% |

| Index Precision Strategy | • Buffers (the amount of negative Index performance we absorb over the duration of a Term) – Buffers cannot be less than 5% | • Precision Rates (the return you receive if Index performance is zero or positive) – Precision Rates cannot be less than 3% |

| Index Guard Strategy | • Floors (the maximum amount of negative Index performance you absorb) – Floors cannot be less than -25% | • Caps – Caps cannot be less than 3% |

| Index Performance Strategy | • Buffers – Buffers cannot be less than 5% | • 1-year Term: Caps – Caps cannot be less than 3% |

| • 3-year Term: Caps (available to Contracts issued before April 30, 2021) – Caps cannot be less than 5% – Can be uncapped | ||

| • 3-year and 6-year Terms: Caps and Participation Rates (a percentage of Index performance) (available to Contracts issued on or after April 30, 2021) – Caps for 3-year Terms cannot be less than 5% – Caps for 6-year Terms cannot be less than 10% – Both 3-year and 6-year Terms can be “uncapped” (i.e., we do not declare a Cap for that Term) – Participation Rates cannot be less than 100% | ||

The Contract’s risks are described in Risk Factors on page 28 of this prospectus.

| Variable Investment Option – AZL® Government Money Market Fund |

You can allocate the money you put into the Contract (Purchase Payments) to any or all of the available Index Options. However, you cannot allocate Purchase Payments to the AZL Government Money Market Fund. The sole purpose of the AZL Government Money Market Fund is to hold Purchase Payments until they are transferred to the Index Options on the Index Effective Date or the next Index Anniversary. You may also reallocate and transfer Contract Value among the Index Options subject to certain restrictions described in this prospectus. Your Contract Value is the value of your Purchase Payments based on the returns of your selected Index Options and the AZL Government Money Market Fund reduced for Contract fees, expenses and withdrawals.

The Index Options provide Credits calculated by us based on the performance of one or more Indexes over a Term as measured by the Index Return and the applicable Buffer, Floor, Precision Rate, Cap, and/or Participation Rate. The Participation Rate may allow you to receive more than the Index Return if the Index Return is positive. We do not apply the Participation Rate if the Index Return is zero or negative. Only the Index Performance Strategy 3-year and 6-year Terms available to Contracts issued on or after April 30, 2021 include a Participation Rate. The Index Return is the percentage change in Index value from the Term Start Date to the Term End Date. The Term Start Date is the date on which a Term begins and we set the DPSCs, Precision Rates, Caps, and Participation Rates for an Index Option; this can occur on either the Index Effective Date or an Index Anniversary. The Term End Date is the date on which a Term ends and we apply Credits; this can only occur on an Index Anniversary. The Index Effective Date is the first day we allocate assets to an Index Option. An Index Anniversary is a twelve-month anniversary of the Index Effective Date. Because we calculate Index Returns only on a single date in time, you may experience negative or flat performance even though the Index you selected for a given Crediting Method experienced gains through some, or most, of the Term.

Allianz Index Advantage Income® Variable Annuity Prospectus – April 30, 2021

2

Credits may be positive, negative, or equal to zero, depending on the applicable Crediting Method and the performance of the applicable Index. The Index Precision Strategy, Index Guard Strategy, and Index Performance Strategy allow negative Performance Credits. A negative Performance Credit means you can lose principal and previous earnings. These losses could be significant. A Performance Credit is the Credit you receive on a Term End Date for any Index Option with the Index Precision Strategy, Index Guard Strategy, or Index Performance Strategy.

DPSCs, Precision Rates, Caps, and Participation Rates that we use to determine Credits for a Contract can change on each Term Start Date and may vary substantially based on market conditions. However, in extreme market environments, it is possible that all DPSCs, Precision Rates, Caps, and Participation Rates will be reduced to their respective minimums of 0.50%, 3%, 5%, 10%, or 100% as stated above. Buffers and Floors that we use to determine Credits for a Contract do not change once they are established. The Crediting Methods are described in greater detail in the Summary, and in section 5, Valuing Your Contract – Calculating Credits. The Indexes are described in Appendix A. For historical information on the Buffers, Floors, DPSCs, Precision Rates, Caps, and Participation Rates, see Appendix C. For historical Index Option performance information, see Appendix D.

The value of Purchase Payments held in the AZL Government Money Market Fund (Variable Account Value) increase and decrease based on the AZL Government Money Market Fund’s performance. The Separate Account holds the shares of the AZL Government Money Market Fund subaccounts that underlie the Contract. The AZL Government Money Market Fund does not provide any protection against loss of principal.

Index-linked and variable annuity contracts are complex insurance and investment vehicles. Before you invest, be sure to ask your Financial Professional (the person who advises you regarding the Contract) about the Contract’s features, benefits, risks, fees and expenses, whether the Contract is appropriate for you based upon your financial situation and objectives, and for a specific recommendation to purchase the Contract. The Contract may be available through third-party financial advisers who charge a financial adviser fee for their services. If you choose to pay financial adviser fees from this Contract, the deduction of this financial adviser fee is in addition to this Contract’s fees and expenses, may be subject to a withdrawal charge, reduces your guaranteed values, reduces any lifetime payments, and may be subject to federal and state income taxes and a 10% additional federal tax.

All guarantees under the Contract, including Credits, are the obligations of Allianz Life and are subject to our claims paying ability and financial strength.

We base Income Payments on a percentage (Lifetime Income Percentage) of your Contract Value, not a guaranteed value. Income Payments made while your Contract Value is positive are a withdrawal of your own assets and reduce your Contract Value. If your Contract Value remains above zero when the Income Payments end, you may not realize a benefit from the Income Benefit; the chances of your Contract Value being reduced to zero may be minimal.

If you change ownership or Beneficiary(s) (the person(s) you designate to receive any death benefit) this may cause Income Payments to be unavailable or end prematurely.

Annual increases to the Lifetime Income Percentage(s) used to calculate Income Payments are not available until age 45. Income Payments have a minimum waiting period and must begin no later than age 100. Joint Income Payments may not be available if the age difference between spouses is too great as stated in section 2, Eligible Person(s) and Covered Person(s).

If your Contract Value is reduced due to negative Credits and/or deductions for Contract fees, expenses, and/or withdrawals and your initial annual maximum Income Payment cannot meet the $100 required minimum, the Income Benefit ends and you will have paid for the benefit without receiving any of its advantages. Income Payments and the Income Benefit may also end prematurely if you withdraw more than the allowed annual maximum Income Payment, or you annuitize the Contract. For more information on the Income Benefit and Income Payments, see “How Does the Income Benefit Work” and “What Happens During the Income Period?” in the Summary; “Risks Associated with the Income Benefit” in Risk Factors; and section 9.

Please read this prospectus before investing and keep it for future reference. The prospectus describes all material rights and obligations of purchasers under the Contract. It contains important information about the Contract and Allianz Life that you ought to know before investing including material state variations. This prospectus is not offered in any state, country, or jurisdiction in which we are not authorized to sell the Contracts. You should rely only on the information contained in this prospectus. We have not authorized anyone to give you different information.

Allianz Index Advantage Income® Variable Annuity Prospectus – April 30, 2021

3

The Securities and Exchange Commission (SEC) has not approved or disapproved these securities or determined if this prospectus is truthful or complete. Any representation to the contrary is a criminal offense. An investment in this Contract is not a deposit of a bank or financial institution and is not federally insured or guaranteed by the Federal Deposit Insurance Corporation or any other federal government agency. An investment in this Contract involves investment risk including the possible loss of principal.

Allianz Life Variable Account B is the Separate Account that contains the assets held in the AZL Government Money Market Fund. Additional information about the Separate Account has been filed with the SEC and is available upon written or oral request without charge. A Statement of Additional Information (SAI) dated the same date as this Form N-4 prospectus includes additional information about the Contract. The SAI is also filed with the SEC on Form N-4 under File Number 333-222815 and is incorporated by reference into this prospectus. The SAI is available without charge by contacting us at the telephone number or address listed at the back of this prospectus. The SAI’s table of contents appears after the Privacy and Security Statement in this prospectus. The prospectus and SAI are also available on our website at www.allianzlife.com. The prospectus, SAI and other Contract information are also available on the EDGAR database on the SEC’s website (www.sec.gov).

Allianz Index Advantage Income® Variable Annuity Prospectus – April 30, 2021

4

TABLE OF CONTENTS

| 7 | ||

| 14 | ||

| 17 | ||

| 17 | ||

| 18 | ||

| 20 | ||

| 23 | ||

| 24 | ||

| 24 | ||

| 25 | ||

| 26 | ||

| 26 | ||

| 28 | ||

| 28 | ||

| 28 | ||

| 29 | ||

| 30 | ||

| 30 | ||

| 31 | ||

| 32 | ||

| 33 | ||

| 33 | ||

| 34 | ||

| 34 | ||

| 35 | ||

| 35 | ||

| 35 | ||

| 35 | ||

| 36 | ||

| 36 | ||

| 36 | ||

| 36 | ||

| 37 | ||

| 1. | 37 | |

| 38 | ||

| 38 | ||

| 39 | ||

| 103 | ||

| 103 | ||

| 103 | ||

| 104 | ||

| 104 | ||

| 105 | ||

| 106 | ||

| 108 | ||

| 108 | ||

| 108 | ||

| 110 | ||

| 110 | ||

| 111 | ||

| 111 | ||

| 113 | ||

| 113 | ||

| 113 | ||

| 114 | ||

| 114 | ||

| 115 | ||

| 116 | ||

| 116 | ||

| 116 | ||

| 118 | ||

| 123 | ||

| 124 | ||

| 124 | ||

| 124 | ||

| 124 | ||

| 129 | ||

| 129 | ||

| 129 | ||

| 130 | ||

| 130 | ||

Allianz Index Advantage Income® Variable Annuity Prospectus – April 30, 2021

6

Glossary

This prospectus is written in plain English. However, there are some technical words or terms that are capitalized and are used as defined terms throughout the prospectus. For your convenience, we included this glossary to define these terms.

Accumulated Alternate Interest – the sum of alternate interest earned for the entire time you own your Contract. We use the Accumulated Alternate Interest to calculate the Alternate Minimum Value for certain Contracts as stated in Appendix G. The alternate interest for each Index Year is equal to either 70% or 87.5% of the Index Option Base multiplied by the alternate interest rate. The alternate interest rate is stated in your Contract and does not change for the entire time you own your Contract.

Accumulation Phase – the first phase of your Contract before you request Annuity Payments. The Accumulation Phase begins on the Issue Date.

Alternate Minimum Value – for certain Contracts as stated in Appendix G, the guaranteed minimum Index Option Value we provide for each Crediting Method if you take a withdrawal (including Income Payments), annuitize the Contract, or if we pay a death benefit.

Annuitant – the individual upon whose life we base the Annuity Payments. Subject to our approval, the Owner designates the Annuitant, and can add a joint Annuitant for the Annuity Phase. There are restrictions on who can become an Annuitant.

Annuity Date – the date we begin making Annuity Payments to the Payee from the Contract.

Annuity Options – the annuity income options available to you under the Contract.

Annuity Payments – payments made by us to the Payee pursuant to the chosen Annuity Option.

Annuity Phase – the phase the Contract is in once Annuity Payments begin.

Beneficiary – the person(s) or entity the Owner designates to receive any death benefit, unless otherwise required by the Contract or applicable law.

Buffer – for any Index Option with the Index Precision Strategy or Index Performance Strategy, this is the negative Index Return that we absorb over the duration of a Term (which can be either one, three, or six years) before applying a negative Performance Credit. We do not apply the Buffer annually on a 3-year or 6-year Term Index Option. On the Issue Date we establish a Buffer for each Index Option with the Index Precision Strategy and Index Performance Strategy. However, if after the Issue Date we add a new Index Option to the Index Precision Strategy or Index Performance Strategy, we establish the Buffer for it on the date we add the Index Option to your Contract. Buffers are stated in your Contract and do not change once they are established.

Business Day – each day on which the New York Stock Exchange is open for trading, except, with regard to the AZL Government Money Market Fund, when it does not value its shares. Allianz Life is open for business on each day that the New York Stock Exchange is open. Our Business Day ends when regular trading on the New York Stock Exchange closes, which is usually at 4:00 p.m. Eastern Time.

Cap – for any Index Option with the Index Protection Strategy with Cap, Index Performance Strategy, or Index Guard Strategy, this is the upper limit on positive Index performance after application of any Participation Rate over the duration of a Term (which can be either one, three, or six years) and the maximum potential Credit for an Index Option. We do not apply the Cap annually on a 3-year or 6-year Term Index Option. On each Term Start Date, we set a Cap for each Index Option with the Index Protection Strategy with Cap, Index Performance Strategy, and Index Guard Strategy. The Caps applicable to your Contract are shown on the Index Options Statement.

Charge Base – the Contract Value on the preceding Quarterly Contract Anniversary (or the initial Purchase Payment received on the Issue Date if this is before the first Quarterly Contract Anniversary), adjusted for subsequent Purchase Payments and any Contract Value withdrawn. Withdrawal adjustments include all withdrawals (even Penalty-Free Withdrawals) and any amounts we withdraw for any Contract fees and expenses. We use the Charge Base to determine the next product and rider fees we deduct.

Contract – the individual flexible purchase payment index-linked and variable deferred annuity contract described by this prospectus.

Contract Anniversary – a twelve-month anniversary of the Issue Date or any subsequent Contract Anniversary.

Allianz Index Advantage Income® Variable Annuity Prospectus – April 30, 2021

7

Contract Value – the value of your Purchase Payments based on the returns of your selected Index Options reduced for previously assessed Contract fees and expenses, and withdrawals. On any Business Day, your Contract Value is the sum of your Index Option Value(s) and Variable Account Value. The Variable Account Value component of the Contract Value fluctuates each Business Day that money is held in the AZL Government Money Market Fund. The Index Option Value component of the Contract Value is adjusted on each Term End Date to reflect Credits, which can be negative with the Index Precision Strategy, Index Guard Strategy, and Index Performance Strategy. A negative Credit means that you can lose principal and previous earnings. The Index Option Values for each Index Option with the Index Precision Strategy, Index Guard Strategy, and Index Performance Strategy also reflect the Daily Adjustment on every Business Day other than the Term Start Date or Term End Date. The Contract Value reflects any previously deducted Contract fees and expenses, but does not reflect Contract fees and expenses that we would apply on liquidation. The cash surrender value reflects all Contract fees and expenses that we would apply on liquidation.

Contract Year – any period of twelve months beginning on the Issue Date or a subsequent Contract Anniversary.

Covered Person(s) – the person(s) upon whose age and lifetime(s) we base Income Payments as discussed in section 2. Covered Person(s) are based on the Eligible Person(s) and the Income Payment type you select on the Income Benefit Date.

Credit – the return you receive on the Term End Date from the Index Options. Credits may be positive, zero, or, in some instances, negative if you select the Index Precision Strategy, Index Guard Strategy, or Index Performance Strategy. A negative Credit means that you can lose principal and previous earnings.

Crediting Method – a method we use to calculate Credits for the Index Options.

Daily Adjustment – how we calculate Index Option Values on days other than the Term Start Date or Term End Date for each Index Option with the Index Precision Strategy, Index Guard Strategy, and Index Performance Strategy as discussed in the Summary – What is the Daily Adjustment?; section 5, Valuing Your Contract – Daily Adjustment for the Index Precision Strategy, Index Guard Strategy, and Index Performance Strategy; and Appendix B. The Daily Adjustment approximates the Index Option Value that will be available on the Term End Date. It is the estimated present value of the future Performance Credit that we will apply on the Term End Date.

Declared Protection Strategy Credit (DPSC) – the positive Credit you receive on a Term End Date for any Index Option with the Index Protection Strategy with DPSC if Index performance is zero or positive. You receive a Credit equal to the DPSC on the Term End Date if the current Index Value is equal to or greater than the Index Value on the Term Start Date. We set the DPSCs on each Term Start Date. The DPSCs provide predefined upside potential. The DPSCs applicable to your Contract are shown on the Index Options Statement.

Determining Life (Lives) – the person(s) designated at Contract issue and named in the Contract on whose life we base the guaranteed Traditional Death Benefit or Maximum Anniversary Value Death Benefit.

Eligible Person(s) – the person(s) whose age determines each Income Percentage and Income Percentage Increase that we use to calculate the Lifetime Income Percentages and Income Payments, and on whose lifetime we base Income Payments. There are restrictions on who can become an Eligible Person as stated in section 2.

Excess Withdrawal – while you are taking Income Payments, this is the amount of any withdrawal you take during an Income Benefit Year that when added to other withdrawals and scheduled Income Payments is greater than your annual maximum Income Payment. Excess Withdrawals reduce your Contract Value, future Income Payments, Guaranteed Death Benefit Value, and may end your Contract. The Income Benefit is discussed in section 9.

Financial Professional – the person who advises you regarding the Contract.

Floor – for any Index Option with the Index Guard Strategy, this is the maximum amount of negative Index Return you absorb as a negative Performance Credit. On the Issue Date we establish a Floor for each Index Option with the Index Guard Strategy. However, if after the Issue Date we add a new Index Option to the Index Guard Strategy, we establish the Floor for it on the date we add the Index Option to your Contract. Floors are stated in your Contract and do not change once they are established.

Good Order – a request is in “Good Order” if it contains all of the information we require to process the request. If we require information to be provided in writing, “Good Order” also includes providing information on the correct form, with any required certifications, guarantees and/or signatures, and received at our Service Center after delivery to the correct mailing, email, or website address, which are all listed at the back of this prospectus. If you have questions about the

Allianz Index Advantage Income® Variable Annuity Prospectus – April 30, 2021

8

information we require, or whether you can submit certain information by fax, email or over the web, please contact our Service Center. If you send information by email or upload it to our website, we send you a confirmation number that includes the date and time we received your information.

Guaranteed Death Benefit Value – the guaranteed value that is available to your Beneficiary(s) on the first death of any Determining Life during the Accumulation Phase. The Guaranteed Death Benefit Value is either total Purchase Payments adjusted for withdrawals if you select the Traditional Death Benefit, or the Maximum Anniversary Value if you select the Maximum Anniversary Value Death Benefit. Withdrawal adjustments include all withdrawals (even Penalty-Free Withdrawals) and any withdrawal charges, but not amounts we withdraw for other Contract fees and expenses.

Income Benefit – a benefit that is automatically included in your Contract at issue which is described in the Summary and section 9. Income Benefit has an additional rider fee and is intended to provide a payment stream for life in the form of partial withdrawals.

Income Benefit Anniversary – a twelve-month anniversary of the Income Benefit Date or any subsequent Income Benefit Anniversary. It is the date we determine Income Payment increases. Income Benefit Anniversaries always occur on Index Anniversaries.

Income Benefit Date – the date you choose to begin receiving Income Payments under the Income Benefit and the Income Period begins. The Income Benefit Date must be on an Index Anniversary.

Income Benefit Supplement – the supplement that must accompany this prospectus which contains the terms used to determine Income Payments for your Contract. The Income Benefit Supplement includes the Income Payment waiting period and the table showing the Income Percentages and Income Percentage Increases. We cannot change these terms for your Contract once they are established. We publish any changes to the Income Benefit Supplement at least seven calendar days before they take effect on our website at www.allianzlife.com/indexincomerates. The Income Benefit Supplement is also filed on EDGAR at www.sec.gov under Form S-1 File Number 333-255317.

Income Benefit Year – a twelve-month period beginning on the Income Benefit Date or a subsequent Income Benefit Anniversary.

Income Payments – the guaranteed payments we make to you under the Income Benefit for the lifetime(s) of the Covered Person(s) that are generally based on the Contract Value and Lifetime Income Percentage for the payment type you select. Payment types include single or joint payments under either the Level Income or Increasing Income payment options. However, if you choose the Level Income payout option and meet certain age requirements, your initial annual maximum Income Payment will not be less than the Level Income Guarantee Payment Percentage multiplied by your total Purchase Payments adjusted for withdrawals. Income Payments are discussed in section 9.

Income Percentages – amounts we use to determine the Lifetime Income Percentages. We establish Income Percentages for each payment type. Income Percentages are generally higher for single payments compared to joint, and for the Level Income payment option compared to Increasing Income. The Income Percentages are stated in the Income Benefit Supplement. Please see Appendix F for the Income Percentages for previous versions of the Income Benefit.

Income Percentage Increases – the amount that each Income Percentage can increase on each Index Anniversary up to and including the Income Benefit Date. We establish Income Percentage Increases for each Eligible Person based on their current age on the Index Effective Date. Income Percentage Increases are not available until the Eligible Person(s) reaches age 45. The Income Percentage Increases are stated in the Income Benefit Supplement. Please see Appendix F for the Income Percentage Increases for previous versions of the Income Benefit.

Income Period – the period your Contract is in if you take Income Payments. The Income Period occurs during the Accumulation Phase and starts on the Income Benefit Date.

Increasing Income – a payment option available under the Income Benefit. It provides Income Payment increases on each Income Benefit Anniversary during the Income Period if your selected Index Option(s) receives a Credit. These increases can continue even if your Contract Value reduces to zero or if your Income Payments are converted to Annuity Payments.

Index (Indexes) – one (or more) of the nationally recognized third-party broad based equity securities Indexes or exchange-traded fund available to you under your Contract. The Indexes are described in Appendix A.

Index Anniversary – a twelve-month anniversary of the Index Effective Date or any subsequent Index Anniversary. It is the date we apply Income Percentage Increases.

Allianz Index Advantage Income® Variable Annuity Prospectus – April 30, 2021

9

Index Effective Date – the first day we allocate assets to an Index Option and we establish Income Percentage Increases for each Eligible Person. The Index Effective Date is stated on the Index Options Statement and starts the first Index Year. When you purchase this Contract you select the Index Effective Date as discussed in section 3, Purchasing the Contract – Allocation of Purchase Payments and Contract Value Transfers.

Index Guard Strategy – one of the Crediting Methods available before the Income Period described in the Summary; and in section 5, Valuing Your Contract – Calculating Credits. The Index Guard Strategy calculates Performance Credits based on Index Returns subject to a Cap and Floor. You can receive negative Performance Credits under this Crediting Method, which means you can lose principal and previous earnings. The Index Guard Strategy is more sensitive to smaller negative market movements that persist over time because the Floor reduces the impact of large negative market movements. In an extended period of smaller negative market returns, the risk of loss is greater with the Index Guard Strategy than with the Index Performance Strategy and Index Precision Strategy.

Index Option – the index-linked investment options to which you can allocate Purchase Payments or transfer Contract Value. Each Index Option is the combination of an Index, a Crediting Method, and a Term. For the Index Performance Strategy 3-year and 6-year Term Index Options we also include the Buffer amount.

Index Option Base – an amount we use to calculate Credits and the Daily Adjustment. The Index Option Base is equal to the amounts you allocate to an Index Option adjusted for withdrawals, Contract fees and expenses, transfers into or out of the Index Option, and the application of any Credits.

Index Option Value – on any Business Day, it is equal to the portion of your Contract Value in a particular Index Option. We establish an Index Option Value for each Index Option you select. Each Index Option Value includes any Credits from previous Term End Dates and reflects deduction of any previously assessed contract maintenance charge, product fee, rider fee, and withdrawal charge. On each Business Day, other than the Term Start Date or Term End Date, the Index Option Values for each Index Option with the Index Precision Strategy, Index Guard Strategy, and Index Performance Strategy also include the Daily Adjustment.

Index Options Statement – the account statement we mail to you on the Index Effective Date and each Index Anniversary thereafter. On the Index Effective Date, the statement shows the initial Index Values, DPSCs, Precision Rates, Caps, and Participation Rates for the Index Options you selected. On each Index Anniversary, the statement shows the new Index Values, Credits received, and renewal DPSCs, Precision Rates, Caps, and Participation Rates that are effective for the next Term for the Index Options you selected that have reached their Term End Date. The Index Options Statement also shows any applicable Buffer or Floor for your selected Index Option(s). For any 3-year or 6-year Term Index Option you selected that has not reached its Term End Date the statement shows the current Index Anniversary’s Index Option Value, which includes the Daily Adjustment. During the Accumulation Phase and before the Income Period, the statement will also show the current Lifetime Income Percentages for each payment type available under the Income Benefit. During the Income Period it will show the maximum Income Payment available for the next year.

Index Performance Strategy – one of the Crediting Methods available before the Income Period described in the Summary; and in section 5, Valuing Your Contract – Calculating Credits. This Crediting Method offers 1-year, 3-year, and 6-year Terms. The Index Performance Strategy calculates Performance Credits based on Index Returns subject to any applicable Participation Rate, Cap, and Buffer. You can receive negative Performance Credits under this Crediting Method, which means you can lose principal and previous earnings. The Index Performance Strategy is more sensitive to large negative market movements because small negative market movements are absorbed by the Buffer. In a period of extreme negative market performance, the risk of loss is greater with the Index Performance Strategy than with the Index Guard Strategy.

Index Precision Strategy – one of the Crediting Methods available before the Income Period described in the Summary; and in section 5, Valuing Your Contract – Calculating Credits. The Index Precision Strategy calculates Performance Credits based on Index Values and Index Returns subject to the Precision Rate and Buffer. You can receive negative Performance Credits under this Crediting Method, which means you can lose principal and previous earnings. The Index Precision Strategy may perform best in periods of small positive market movements because the Precision Rates will generally be greater than the DPSCs, but less than the Index Performance Strategy Caps. The Index Precision Strategy is more sensitive to large negative market movements because small negative market movements are absorbed by the Buffer. In a period of extreme negative market performance, the risk of loss is greater with the Index Precision Strategy than with the Index Guard Strategy.

Index Protection Strategy with DPSC – one of the Crediting Methods available during the entire Accumulation Phase, including the Income Period, described in the Summary; and in section 5, Valuing Your Contract – Calculating Credits.

Allianz Index Advantage Income® Variable Annuity Prospectus – April 30, 2021

10

The Index Protection Strategy with DPSC provides Credits equal to the DPSCs on the Term End Date if the current Index Value is equal to or greater than the Index Value on the Term Start Date. The Index Protection Strategy with DPSC does not allow negative Credits, and offers the least growth opportunity as DPSCs will generally be less than Precision Rates and Caps.

Index Protection Strategy with Cap – one of the Crediting Methods available during the entire Accumulation Phase, including the Income Period, described in the Summary; and in section 5, Valuing Your Contract – Calculating Credits. The Index Protection Strategy with Cap provides a Protection Credit based on Index Returns subject to a Cap, but does not allow negative Credits. The Index Protection Strategy with Cap offers more growth opportunity than Index Protection Strategy with DPSC, but less than Index Precision Strategy, Index Guard Strategy, or Index Performance Strategy.

Index Return – the percentage change in Index Value from the Term Start Date to the Term End Date, which we use to determine the Protection Credits for any Index Option with the Index Protection Strategy with Cap, Performance Credits for any Index Option with the Index Performance Strategy or Index Guard Strategy, and negative Performance Credits for any Index Option with the Index Precision Strategy. The Index Return is the Index Value on the Term End Date, minus the Index Value on the Term Start Date, divided by the Index Value on the Term Start Date.

Index Value – an Index’s price at the end of the Business Day on the Term Start Date and Term End Date as provided by Bloomberg or another market source if Bloomberg is not available.

Index Year – a twelve-month period beginning on the Index Effective Date or a subsequent Index Anniversary.

Issue Date – the date we issue the Contract. The Issue Date is stated in your Contract and starts your first Contract Year. Contract Anniversaries and Contract Years are measured from the Issue Date.

Joint Owners – the two person(s) designated at Contract issue and named in the Contract who may exercise all rights granted by the Contract. Joint Owners must be spouses within the meaning of federal tax law.

Level Income – an Income Benefit payment option that provides an automatic annual increase to your Income Payments if your Contract Value increases from one Income Benefit Anniversary to the next during the Income Period.

Level Income Guarantee Payment Percentage – the minimum percentage of total Purchase Payments adjusted for withdrawals you can receive as an Income Payment if you choose the Level Income payout option and meet certain age requirements as stated in section 9 – Calculating Your Income Payments.

Lifetime Income Percentage – the maximum percentage of Contract Value you can receive as an Income Payment on the Income Benefit Date. The Lifetime Income Percentages available to you before the Income Period are stated on the Index Options Statement.

Lock Date – for each Index Option with the Index Precision Strategy, Index Guard Strategy, and Index Performance Strategy this is the Business Day we execute a Performance Lock and capture an Index Option Value (which includes the Daily Adjustment) before the Term End Date.

Maximum Anniversary Value – the highest Contract Value on any Index Anniversary before age 91, adjusted for subsequent Purchase Payments and withdrawals, used to determine the Maximum Anniversary Value Death Benefit as discussed in the Summary and section 10. Withdrawal adjustments include all withdrawals (even Penalty-Free Withdrawals) and any withdrawal charges, but not amounts we withdraw for other Contract fees and expenses.

Maximum Anniversary Value Death Benefit – an optional benefit described in the Summary and section 10 that has an additional rider fee and is intended to potentially provide a death benefit greater than the Traditional Death Benefit. The Maximum Anniversary Value Death Benefit can only be added to a Contract at issue.

Non-Qualified Contract – a Contract that is not purchased under a pension or retirement plan that qualifies for special tax treatment under sections of the Code.

Owner – “you,” “your” and “yours.” The person(s) or entity designated at Contract issue and named in the Contract who may exercise all rights granted by the Contract.

Participation Rate – may allow you to receive more than the Index Return if the Index Return is positive, but the Participation Rate cannot boost Index Returns beyond any declared Cap. We do not apply the Participation Rate if the Index Return is zero or negative. We do not apply the Participation Rate annually. The Participation Rate is only available on the the Index Performance Strategy 3-year and 6-year Terms to Contracts issued on or after April 30, 2021. The Participation Rate is not available on Index Performance Strategy 1-year Terms, or on 3-year Terms that were available to

Allianz Index Advantage Income® Variable Annuity Prospectus – April 30, 2021

11

Contracts issued before April 30, 2021. We set Participation Rates on each Term Start Date. The Participation Rates applicable to your Contract are shown on the Index Options Statement.

Payee – the person or entity who receives Annuity Payments during the Annuity Phase.

Penalty-Free Withdrawals – withdrawals you take under the free withdrawal privilege or waiver of withdrawal charge benefit, payments you take under our minimum distribution program, and Income Payments. Penalty-Free Withdrawals are not subject to a withdrawal charge.

Performance Credit – the Credit you receive on a Term End Date for any Index Option with the Index Precision Strategy, Index Guard Strategy, or Index Performance Strategy. We base Performance Credits on Index Values and Index Returns after application of any Participation Rate as limited by the applicable Buffer, Floor, Precision Rate, or Cap. Performance Credits can be negative, which means you can lose principal and previous earnings.

Performance Lock – a feature that allows you to capture the current Index Option Value during the Term for each Index Option with the Index Precision Strategy, Index Guard Strategy, and Index Performance Strategy. A Performance Lock applies to the total Index Option Value in an Index Option, and not just a portion of that Index Option Value. After the Lock Date, Daily Adjustments do not apply to a locked Index Option for the remainder of the Term and the Index Option Value will not receive a Performance Credit on the Term End Date.

Precision Rate – the positive Performance Credit you receive for any Index Option with the Index Precision Strategy if Index performance is zero or positive. You receive a Performance Credit equal to the Precision Rate on the Term End Date if the current Index Value is equal to or greater than the Index Value on the Term Start Date. We set a Precision Rate for each Index Precision Strategy Index Option on each Term Start Date. The Precision Rates applicable to your Contract are shown on the Index Options Statement.

Protection Credit – the Credit you receive on the Term End Date for any Index Option with the Index Protection Strategy with Cap. We base Protection Credits on positive Index Returns limited by the Cap. Protection Credits cannot be negative.

Proxy Investment – provides a current estimate of what the Performance Credit will be on the Term End Date taking into account any applicable Buffer, Floor, Precision Rate, Cap, and/or Participation Rate. We use the Proxy Investment to calculate the Daily Adjustment on Business Days other than the Term Start Date or Term End Date. For more information, see Appendix B.

Proxy Value – the hypothetical value of the Proxy Investment used to calculate the Daily Adjustment as discussed in Appendix B.

Purchase Payment – the money you put into the Contract.

Qualified Contract – a Contract purchased under a pension or retirement plan that qualifies for special tax treatment under sections of the Code (for example, 401(a) and 401(k) plans), Individual Retirement Annuities (IRAs), or Tax-Sheltered Annuities (referred to as TSA contracts). Currently, we issue Qualified Contracts that may include, but are not limited to Roth IRAs, traditional IRAs and Simplified Employee Pension (SEP) IRAs.

Quarterly Contract Anniversary – the day that occurs three calendar months after the Issue Date or any subsequent Quarterly Contract Anniversary.

Separate Account – Allianz Life Variable Account B is the Separate Account that issues the variable investment portion of your Contract. It is a separate investment account of Allianz Life. The Separate Account holds the shares of the AZL Government Money Market Fund subaccounts that underlie the Contracts. The Separate Account is divided into subaccounts, each of which invests exclusively in a variable investment option. The only currently available variable investment option is the AZL Government Money Market Fund. The Separate Account is registered with the SEC as a unit investment trust, and may be referred to as the Registered Separate Account.

Service Center – the area of our company that issues Contracts and provides Contract maintenance and routine customer service. Our Service Center address and telephone number are listed at the back of this prospectus. The address for mailing applications and/or checks for Purchase Payments may be different and is also listed at the back of this prospectus.

Term – The period of time, from the Term Start Date to the Term End Date, in which we measure Index Return to determine Credits.

Term End Date – The day on which a Term ends and we apply Credits. A Term End Date may only occur on an Index Anniversary. If a Term End Date does not occur on a Business Day, we consider it to occur on the next Business Day.

Allianz Index Advantage Income® Variable Annuity Prospectus – April 30, 2021

12

Term Start Date – The day on which a Term begins and we set the DPSCs, Precision Rates, Caps, and Participation Rates for an Index Option. A Term Start Date may only occur on the Index Effective Date or an Index Anniversary. If a Term Start Date does not occur on a Business Day, we consider it to occur on the next Business Day.

Traditional Death Benefit – the guaranteed death benefit automatically provided by the Contract for no additional fee described in the Summary and section 10.

Valid Claim – the documents we require to be received in Good Order at our Service Center before we pay any death claim. This includes the death benefit payment option, due proof of death, and any required governmental forms. Due proof of death includes a certified copy of the death certificate, a decree of court of competent jurisdiction as to the finding of death, or any other proof satisfactory to us.

Variable Account Value – on any Business Day, it is the value of the shares in the AZL Government Money Market Fund subaccounts which hold your Purchase Payments until the Index Effective Date or the next Index Anniversary. We create an AZL Government Money Market Fund subaccount for each of your selected Index Options. The Variable Account Value increases and decreases based on the performance of the AZL Government Money Market Fund and reflects deduction of the fund’s operating expenses, any previously assessed contract maintenance charge, product fee, rider fee, and withdrawal charge.

Withdrawal Charge Basis – the total amount under your Contract that is subject to a withdrawal charge as discussed in section 6, Expenses – Withdrawal Charge.

Allianz Index Advantage Income® Variable Annuity Prospectus – April 30, 2021

13

Summary

The Index Advantage Income® is a product that offers index-linked investment options and allows you to defer taking regular fixed periodic payments (Annuity Payments) to a future date. During the first phase of your Contract (Accumulation Phase) your Contract Value fluctuates based on the performance of your selected Index Options and the AZL Government Money Market Fund (for Purchase Payments that have not yet been transferred to the Index Options) and deduction of Contract fees and expenses. During this phase you can make additional Purchase Payments (until you request Income Payments), you can take withdrawals, and if you die we pay a death benefit to your named Beneficiary(s). If you request Income Payments, your Contract will enter the Income Period. The Income Period occurs during the Accumulation Phase. If you request Annuity Payments, the Accumulation Phase and Income Period (if applicable) ends and the Annuity Phase begins. Annuity Payments are fixed payments we make based on the Annuity Option you select and your Contract Value.

| Purchasing a Contract: Key Features at a Glance | |

| Issue Age (see section 3) | On the date we issue the Contract (the Issue Date), all Owners and the Annuitant must be either: • age 80 or younger, or • age 75 or younger if you select the Maximum Anniversary Value Death Benefit. The Owner is the person or entity designated at issue who may exercise all Contract rights. The Annuitant is the individual upon whose life we base Annuity Payments. |

| Purchase Payment Standards (see section 3) | • $5,000 minimum initial Purchase Payment due on the Issue Date. • We restrict additional Purchase Payments during the Accumulation Phase. Each Index Year before the Income Period you cannot add more than your initial amount without our prior approval. An Index Year is a twelve-month period beginning on the Index Effective Date or a subsequent Index Anniversary. Your initial amount is all Purchase Payments received before the first Quarterly Contract Anniversary of the first Contract Year. A Quarterly Contract Anniversary is the day that occurs three calendar months after the Issue Date or any subsequent Quarterly Contract Anniversary. A Contract Year is any period of twelve months beginning on the Issue Date or a subsequent Contract Anniversary. A Contract Anniversary is a twelve-month anniversary of the Issue Date or any subsequent Contract Anniversary. We allow you to add up to the initial amount in the remainder of the first Index Year, and each Index Year thereafter before the Income Period begins. The minimum additional Purchase Payment we will accept is $50. • $1 million maximum in total Purchase Payments unless we give prior approval for a higher amount. • We do not accept additional Purchase Payments during the Income Period or the Annuity Phase. |

| Allocation of Purchase Payments and Contract Value Transfers (see section 3) | You can allocate your Purchase Payments to any or all of the Index Options available under your Contract. We only allow assets to move into the Index Options on the Index Effective Date and on subsequent Index Anniversaries. • As a result, we hold Purchase Payments in the AZL Government Money Market Fund until we transfer them to your selected Index Options according to your instructions. For additional Purchase Payments we receive after the Index Effective Date, we transfer the amounts held in the AZL Government Money Market Fund to your selected Index Options on the next Index Anniversary. However, you cannot allocate Purchase Payments to the AZL Government Money Market Fund. • On each Index Option’s Term End Date, you can transfer Index Option Value (the portion of your Contract Value in a particular Index Option) between Index Options. • We do not allow assets to move into an established 3-year or 6-year Term Index Option until the Term End Date. • Purchase Payments you allocate to an Index Option must be held in the Index Option for the full Term before they can receive a Credit. Therefore, additional Purchase Payments we receive after the Index Effective Date that you allocate to a 1-year Term Index Option are not eligible to receive a Credit until the second Index Anniversary after we receive them, or the fourth Index Anniversary after we receive them for allocations to a 3-year Term Index Option, or the seventh Index Anniversary after we receive them for allocations to a 6-year Term Index Option. |

Allianz Index Advantage Income® Variable Annuity Prospectus – April 30, 2021

14

| Purchasing a Contract: Key Features at a Glance | |

| Daily Adjustment (see “What is the Daily Adjustment?” in this Summary and section 5) | The Daily Adjustment is how we calculate Index Option Values on days other than the Term Start Date or Term End Date for each Index Option with the Index Precision Strategy, Index Guard Strategy, and Index Performance Strategy. The Daily Adjustment approximates the Index Option Value that will be available on the Term End Date. It is the estimated present value of the future Performance Credit that we will apply on the Term End Date. The Daily Adjustment takes into account any Index gains subject to the applicable Precision Rate, Cap, and/or Participation Rate, or either any Index losses greater than the Buffer or Index losses down to the Floor, but in the form of the estimated present value. Therefore, the Daily Adjustment could result in a loss beyond the protection of the Buffer or Floor. |

| Performance Lock (see “What is the Performance Lock?” in this Summary and section 5) | A feature that allows you to capture the current Index Option Value during the Term for each Index Option with the Index Precision Strategy, Index Guard Strategy, and Index Performance Strategy. If we execute a Performance Lock for an Index Option we do not apply the Daily Adjustment to it for the remainder of the Term and the Index Option Value will not receive a Performance Credit on the Term End Date. |

| Product and Rider Fees (see the Fee Tables and section 6) | Accrued daily and deducted on each Quarterly Contract Anniversary. Each fee is calculated as a percentage of the Charge Base, which is the Contract Value on the preceding Quarterly Contract Anniversary adjusted for subsequent Purchase Payments and withdrawals. • Product fee is 1.25%. • Rider fee is 0.70% for the Income Benefit. • Rider fee is 0.20% for the Maximum Anniversary Value Death Benefit. If you select this benefit, you will pay 2.15% in total annual Contract fees (product fee plus the rider fees). |

| Other Contract Fees and Expenses (see the Fee Tables and section 6) | • An 8.5% declining withdrawal charge applies to withdrawals taken within six years after receipt of each Purchase Payment during the Accumulation Phase, and during the Income Period to Excess Withdrawals (the amount of any withdrawal taken during an Index Year that when added to other withdrawals and scheduled Income Payments is greater than your annual maximum Income Payment). • $50 contract maintenance charge assessed annually if the total Contract Value is less than $100,000. • AZL Government Money Market Fund operating expenses before fee waivers and expense reimbursements of 0.66% of the average daily net assets. |

| You can withdraw your Contract Value, subject to any applicable withdrawal charge, and federal and state taxation. Withdrawals taken before age 59 1⁄2 may also be subject to a 10% additional federal tax. | |

| Free Withdrawal Privilege (see section 7) | Allows you to withdraw 10% of your total Purchase Payments each Contract Year during the Accumulation Phase and before the Income Period without incurring a withdrawal charge. • Any unused free withdrawal privilege in one Contract Year is not added to the amount available in the next Contract Year. • If you withdraw more than the free withdrawal privilege we will assess a withdrawal charge if the withdrawal is taken from a Purchase Payment we received within the last six years. • Not available if you take a full withdrawal of your total Contract Value or during the Income Period. |

| Systematic Withdrawal Program (see section 7) | Before the Income Period, it provides automatic withdrawals of at least $100 to you at a frequency you select. These withdrawals: • reduce the amount available under the free withdrawal privilege, and • are subject to a withdrawal charge if you exceed the free withdrawal privilege. |

| Minimum Distribution Program and Required Minimum Distribution (RMD) Payments (see section 7) | If you own an Individual Retirement Annuity (IRA) or SEP IRA Contract, this program provides payments to you designed to meet the Code’s minimum distribution requirements. These withdrawals: • reduce the amount available under the free withdrawal privilege before the Income Period, but • are not subject to a withdrawal charge if you exceed the free withdrawal privilege before the Income Period, and are not considered to be an Excess Withdrawal during the Income Period. |

| Waiver of Withdrawal Charge Benefit (see section 7) | In most states, this benefit allows you to take a withdrawal without incurring a withdrawal charge if you are confined to a nursing home for a period of at least 90 consecutive days. |

Allianz Index Advantage Income® Variable Annuity Prospectus – April 30, 2021

15

| Purchasing a Contract: Key Features at a Glance | |

| Annuity Payments (see section 8) | Annuity Payments can provide a guaranteed lifetime fixed income stream with certain tax advantages. We designed the Annuity Payments for Owners who no longer need immediate access to Contract Value to meet their short-term income needs. • We offer five Annuity Options that provide payments for life, life and term certain, or life with refund. • We base Annuity Payments on your Contract Value, the Annuity Option you select, and the lifetime and age of the Annuitant(s). • For an individually owned Contract, Annuity Payments can be either single or joint. |

| Income Benefit (see “How Does the Income Benefit Work?” later in this Summary and section 9) | The Income Benefit (0.70% rider fee) is automatically included in your Contract. It provides guaranteed lifetime Income Payments based on a percentage of your Contract Value. • Once the Income Payment waiting period has expired, Income Payments can begin as early as age 50 or as late as age 100. • Unlike Annuity Payments, the Income Benefit allows access to your Contract Value and death benefit for a period of time after Income Payments begin. • Once Income Payments begin your Crediting Methods are limited to the Index Protection Strategy with DPSC and Index Protection Strategy with Cap. • If you no longer want or need the Income Benefit, you can remove it from your Contract on or after the third Index Anniversary if you have not begun Income Payments and your Contract Value is positive. If you remove the Income Benefit, we stop assessing the Income Benefit rider fee. For information on the terms used to determine your Income Payments, please see the Income Benefit Supplement. |

| Death Benefit (see section 10) | When you purchase the Contract you select either the Traditional Death Benefit (no additional fee) or the Maximum Anniversary Value Death Benefit (0.20% rider fee). In either case, the death benefit is paid upon the first death of any Determining Life during the Accumulation Phase. • We establish the Determining Lives at Contract issue and they generally do not change unless there is a change of ownership due to divorce or establishment of a Trust. • The Determining Life (or Lives) is either the Owner(s) or the Annuitant if the Owner is a non-individual.If a Determining Life dies during the Accumulation Phase your Beneficiary(s) will receive the greater of the Contract Value or the Guaranteed Death Benefit Value. The Guaranteed Death Benefit Value is either: • total Purchase Payments adjusted for withdrawals if you select the Traditional Death Benefit, or • the Maximum Anniversary Value (the highest Contract Value on any Index Anniversary before age 91, adjusted for subsequent Purchase Payments and withdrawals) if you select the Maximum Anniversary Value Death Benefit. |

| • Withdrawals (including Income Payments) reduce your Guaranteed Death Benefit Value proportionately, which means this value may be reduced by more than the amount withdrawn. • The Maximum Anniversary Value Death Benefit cannot be less than the Traditional Death Benefit, but they can be equal. • If you change Owner(s) the death benefit may be reduced to Contract Value. | |

| Material Contract Variations (see Appendix H) | The product or certain product features may not currently be available in all states or all Contracts, may vary in your state (such as the free look), or may not be available from all selling firms or from all Financial Professionals. Your Financial Professional can also provide information regarding availability of Index Options. |

| Customer Service (see the last page of this prospectus) | If you need customer service (for Contract changes, information on Contract Values, requesting a withdrawal or transfer, changing your allocation instructions, etc.) please contact our Service Center at (800) 624-0197. Our Service Center is the area of our company that issues Contracts and provides Contract maintenance and routine customer service. You can also contact us by: • mail at Allianz Life Insurance Company of North America, P.O. Box 561, Minneapolis, MN 55440-0561, or • email at Contact.Us@allianzlife.com. |

Allianz Index Advantage Income® Variable Annuity Prospectus – April 30, 2021

16

Who Should Consider Purchasing the Contract?

We designed the Contract for people who are looking for guaranteed lifetime income with continued access to Contract Value and a death benefit for a period of time, and a level of protection for their principal while providing potentially higher returns than are available on traditional fixed annuities. This Contract is not intended for someone who is seeking complete protection from downside risk, nor someone who is seeking unlimited investment potential.

We offer other annuity contracts that may address your investment and retirement needs. These contracts include variable annuities, registered index-linked annuities and fixed index annuities. These annuity products may offer different features and benefits more appropriate for your needs, including allocation options, fees and/or expenses that are different from those in the Contract offered by this prospectus. Not every contract is offered through every Financial Professional. Some Financial Professionals or selling firms may not offer and/or limit offering of certain features and benefits, as well as limit the availability of the contracts based on criteria established by the Financial Professional or selling firm. For more information about other annuity contracts, please contact your Financial Professional.

For example, these other annuity contracts may have different Index Options, and different rates and minimums for the Buffers, Floors, DPSCs, Precision Rates, Caps, and Participation Rates. DPSCs, Precision Rates, Caps, and Participation Rates may also be affected, positively or negatively, by expenses we incur in providing other contract features. For example, a product that deducts fees and expenses from Index Options may have higher DPSCs, Precision Rates, Caps, and Participation Rates than a contract that deducts fees and expenses only from variable investment options.

How Do the Crediting Methods Work?

All Crediting Methods provide a Credit on the Term End Date based on Index Values and Index Returns. The Index Value is the Index’s price at the end of the Business Day on the Term Start Date and Term End Date, which we use to calculate the Index Return. A Business Day is each day the New York Stock Exchange is open for trading and it ends when regular trading on the New York Stock Exchange closes, which is usually at 4:00 p.m. Eastern Time. All of the Crediting Methods offer 1-year Term Index Options, but only the Index Performance Strategy also offers 3-year and 6-year Term Index Options.

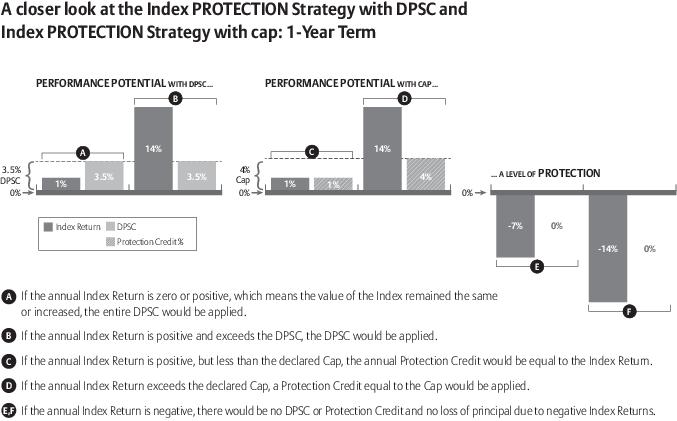

The Index Protection Strategy with DPSC provides a Credit equal to the DPSC if the Index Value on the Term End Date is equal to or greater than the Index Value on the Term Start Date, regardless of the amount of actual Index Return. If the current Index Value is less than it was on the Term Start Date, the Credit is zero.

The Index Protection Strategy with Cap provides a Protection Credit.

| • | If the Index Return is positive, the Protection Credit is equal to the Index Return up to the Cap. |

| • | If the Index Value on the Term End Date is equal to or less than the Index Value on the Term Start Date, the Protection Credit is zero. |

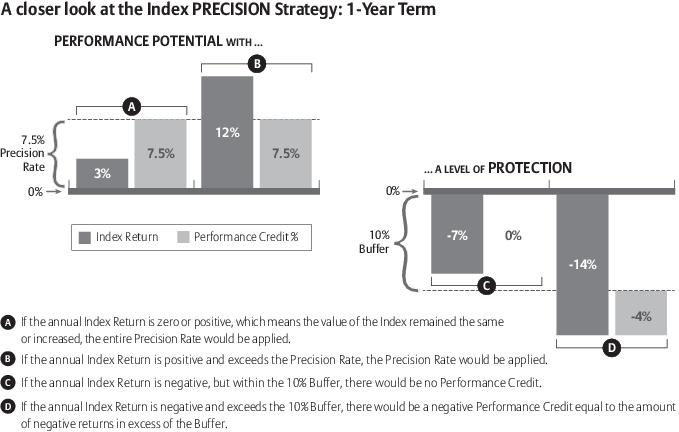

The Index Precision Strategy provides a Performance Credit.

| • | If the Index Value on the Term End Date is equal to or greater than the Index Value on the Term Start Date, regardless of the amount of actual Index Return, the Performance Credit is equal to the Precision Rate. |

| • | If the Index Return is negative and the loss is: |

| – | less than or equal to the Buffer, the Performance Credit is zero. We absorb any loss up to the Buffer. |

| – | greater than the Buffer, the negative Performance Credit is equal to the negative Index Return in excess of the Buffer. You participate in any losses beyond the Buffer. |

The Index Guard Strategy also provides a Performance Credit.

| • | If the Index Return is positive, the Performance Credit is equal to the Index Return up to the Cap. |

| • | If the Index Value on the Term End Date is equal to the Index Value on the Term Start Date, the Performance Credit is zero. |

| • | If the Index Return is negative, the negative Performance Credit is equal to the negative Index Return down to the Floor. You participate in any losses down to the Floor. We absorb any negative Index Return beyond the Floor. |

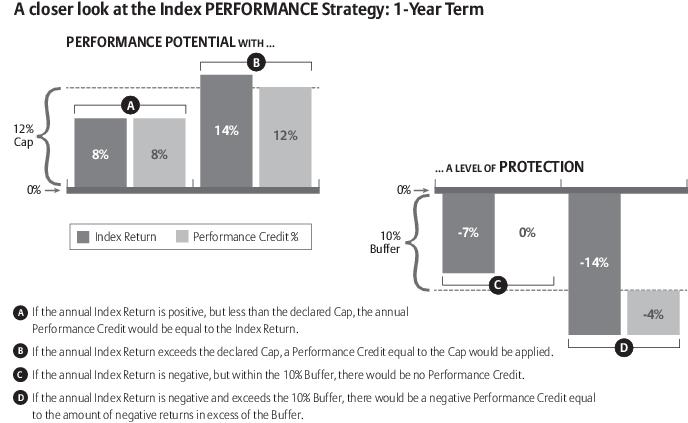

The Index Performance Strategy also provides a Performance Credit.

| • | If the Index Return is positive, the Performance Credit is equal to: |

| – | the Index Return up to the Cap for a 1-year Term. |

Allianz Index Advantage Income® Variable Annuity Prospectus – April 30, 2021

17

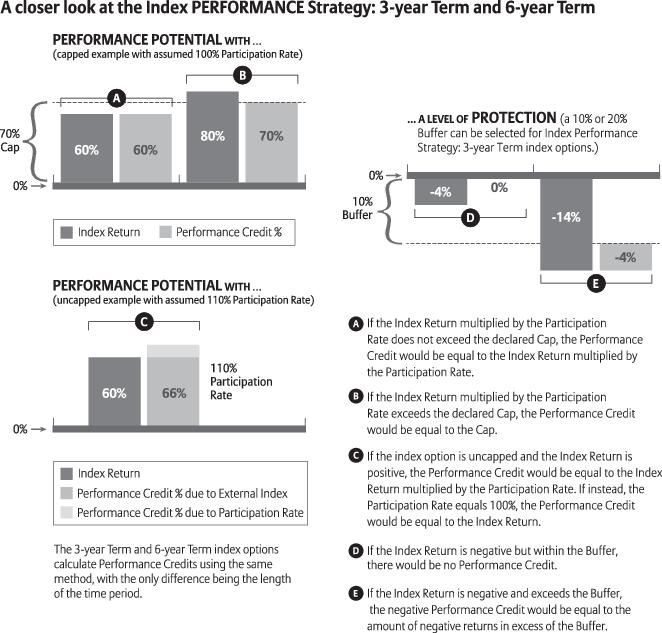

| – | the Index Return up to the Cap for a 3-year Term available to Contracts issued before April 30, 2021. If a 3-year Term is uncapped, the Performance Credit is equal the Index Return. We apply the Cap for the entire Term length; we do not apply the Cap annually on a 3-year. |

| – | Index Return multiplied by the Participation Rate, up to the Cap for a 3-year or 6-year Term available to Contracts issued after April 30, 2021. If the 3-year or 6-year Term is uncapped, the Performance Credit is equal to the Index Return multiplied by the Participation Rate. We apply the Participation Rate and Cap for the entire Term length; we do not apply the Participation Rate and Cap annually on a 3-year or 6-year Term. |

| • | If the Index Value on the Term End Date is equal to the Index Value on the Term Start Date, the Performance Credit is zero. |

| • | If the Index Return is negative and the loss is: |

| – | less than or equal to the Buffer, the Performance Credit is zero. We absorb any loss up to the Buffer. We apply the Buffer for the entire Term length; we do not apply the Buffer annually on a 3-year or 6-year Term Index Option. |

| – | greater than the Buffer, the negative Performance Credit is equal to the negative Index Return in excess of the Buffer. You participate in any losses beyond the Buffer. |

A more detailed description of how we calculate Credits, including numerical examples, is included in section 5, Valuing Your Contract – Calculating Credits.

| • The Index Precision Strategy, Index Guard Strategy, and Index Performance Strategy allow negative Performance Credits. A negative Performance Credit means you can lose principal and previous earnings. These losses could be significant. |

| • Because we calculate Index Returns only on a single date in time, you may experience negative or flat performance even though the Index you selected for a given Crediting Method experienced gains through some, or most, of the Term. |

| • If a 3-year or 6-year Term Index Option is “uncapped” for one Term (i.e., we do not declare a Cap for that Term) it does not mean that we will not declare a Cap for it on future Term Start Dates. On the next Term Start Date we can declare a Cap for the next Term, or declare it to be uncapped. |

How Do the Crediting Methods Compare?

The Crediting Methods have different risk and return potentials.

| What is the asset protection? | |

| Index Protection Strategy with DPSC | • Most protection. • If the Index loses value, the Credit is zero. You do not receive a negative Credit. |

| Index Protection Strategy with Cap | • Most protection. • If the Index loses value, the Credit is zero. You do not receive a negative Credit. |

| Index Precision Strategy | • Less protection than the Index Protection Strategy with DPSC, Index Protection Strategy with Cap, and Index Guard Strategy. Protection may be more or less than what is available with the Index Performance Strategy depending on Buffers. • Buffer absorbs a percentage of loss, but you receive a negative Performance Credit for losses greater than the Buffer. • Potential for large losses in any Term. • More sensitive to large negative market movements because small negative market movements are absorbed by the Buffer. In a period of extreme negative market performance, the risk of loss is greater with the Index Precision Strategy than with the Index Guard Strategy. |

| Index Guard Strategy | • Less protection than the Index Protection Strategy with DPSC and Index Protection Strategy with Cap, but more than Index Precision Strategy and Index Performance Strategy. • Permits a negative Performance Credit down to the Floor. • Protection from significant losses. • More sensitive to smaller negative market movements that persist over time because the Floor reduces the impact of large negative market movements. • In an extended period of smaller negative market returns, the risk of loss is greater with the Index Guard Strategy than with the Index Performance Strategy and Index Precision Strategy. • Provides certainty regarding the maximum loss in any Term. |

Allianz Index Advantage Income® Variable Annuity Prospectus – April 30, 2021

18

| What is the asset protection? | |

| Index Performance Strategy | • Less protection than the Index Protection Strategy with DPSC, Index Protection Strategy with Cap, and Index Guard Strategy. Protection may be more or less than what is available with the Index Precision Strategy depending on Buffers. • Buffers may be different between 1-year, 3-year, and 6-year Terms. Buffers can also be different between Index Options with the same Term Length. • Buffer absorbs a percentage of loss, but you receive a negative Performance Credit for losses greater than the Buffer. • Potential for large losses in any Term. • More sensitive to large negative market movements because small negative market movements are absorbed by the Buffer. In a period of extreme negative market performance, the risk of loss is greater with the Index Performance Strategy than with the Index Guard Strategy. • In extended periods of moderate to large negative market performance, 3-year and 6-year Terms may provide less protection than the 1-year Terms because, in part, the Buffer is applied over a longer period of time. |

| What is the growth opportunity? | |

| Index Protection Strategy with DPSC | • Growth opportunity limited by the DPSCs. • Least growth opportunity. • May perform best in periods of small positive market movements. • DPSCs will generally be less than the Precision Rates and Caps. |

| Index Protection Strategy with Cap | • Growth opportunity limited by the Caps. • May perform best in periods of small positive market movements. • Generally more growth opportunity than the Index Protection Strategy with DPSC, but less than the Index Precision Strategy, Index Guard Strategy, and Index Performance Strategy. • Caps will generally be greater than DPSCs, but less than the Precision Rates and Caps for the Index Guard Strategy and Index Performance Strategy. |

| Index Precision Strategy | • Growth opportunity limited by the Precision Rates. • May perform best in periods of small positive market movements. • Generally more growth opportunity than the Index Protection Strategy with DPSC and Index Protection Strategy with Cap, but less than the Index Performance Strategy. • Growth opportunity may be more or less than the Index Guard Strategy depending on Precision Rates and Caps. |

| Index Guard Strategy | • Growth opportunity limited by the Caps. • May perform best in a strong market. • Growth opportunity that generally may be matched or exceeded only by the Index Performance Strategy. However, growth opportunity may be more or less than the Index Precision Strategy or Index Performance Strategy depending on Precision Rates and Caps. |

| Index Performance Strategy | • Growth opportunity limited by the Caps and/or Participation Rates. If we do not declare a Cap for a 3-year or 6-year Term Index Option there is no maximum limit on the positive Index Return for that Index Option. In addition, you can receive more than the positive Index Return if the Participation Rate applies and is greater than its 100% minimum. • May perform best in a strong market. • Generally the most growth opportunity. However, growth opportunity may be less than the Index Precision Strategy or Index Guard Strategy depending on Precision Rates, Caps, and/or Participation Rates. |

| What can change within a Crediting Method? | |

| Index Protection Strategy with DPSC | • Renewal DPSCs for existing Contracts can change on each Term Start Date. • DPSCs are subject to a 0.50% minimum. |

| Index Protection Strategy with Cap | • Renewal Caps for existing Contracts can change on each Term Start Date. • Caps are subject to a 0.50% minimum. |

Allianz Index Advantage Income® Variable Annuity Prospectus – April 30, 2021

19

| What can change within a Crediting Method? | |

| Index Precision Strategy | • Renewal Precision Rates for existing Contracts can change on each Term Start Date. • If we add a new Index Option to your Contract after the Issue Date, we establish the Buffer for it on the date we add the Index Option to your Contract. Your actual Buffers cannot change once they are established. • Precision Rates are subject to a 3% minimum, and Buffers are subject to a 5% minimum. |

| Index Guard Strategy | • Renewal Caps for existing Contracts can change on each Term Start Date. • If we add a new Index Option to your Contract after the Issue Date, we establish the Floor for it on the date we add the Index Option to your Contract. Your actual Floors cannot change once they are established. • Caps are subject to a 3% minimum, and Floors are subject to a -25% minimum. |

| Index Performance Strategy | • Renewal Caps and/or Participation Rates for existing Contracts can change on each Term Start Date. • If we add a new Index Option to your Contract after the Issue Date, we establish the Buffer for it on the date we add the Index Option to your Contract. Your actual Buffers cannot change once they are established. • Caps are subject to a 3% minimum for 1-year Terms, 5% for 3-year Terms, or 10% for 6-year Terms. Participation Rates are subject to a 100% minimum. Buffers are subject to a 5% minimum. |

| • For any Index Option with the Index Precision Strategy or Index Performance Strategy, you participate in any negative Index Return in excess of the Buffer, which reduces your Contract Value. For example, if we set the Buffer at 5% we would absorb the first -5% of Index Return and you could lose up to 95% of the Index Option Value. However, for any Index Option with the Index Guard Strategy, we absorb any negative Index Return in excess of the Floor. For example, if we set the Floor at -25%, your maximum loss would be limited to -25% of the Index Option Value due to negative Index Returns. |

| • The minimum Buffer and Floor are the least amount of protection that you could receive from negative Index Returns for any Index Option with the Index Precision Strategy, Index Guard Strategy, or Index Performance Strategy. |

| • DPSCs, Precision Rates, Caps, and Participation Rates as set by us from time-to-time may vary substantially based on market conditions. However, in extreme market environments, it is possible that all DPSCs, Precision Rates, Caps, and Participation Rates will be reduced to their respective minimums of 0.50%, 3%, 5%, 10%, or 100% as stated above. |

| • Buffers, Floors, DPSCs, Precision Rates, Caps, and Participation Rates can be different from Index Option to Index Option. For example, Caps for the Index Performance Strategy 1-year Terms can be different between the S&P 500® Index and the Nasdaq-100® Index, and Caps for the S&P 500® Index can be different between 1-year and 3-year Terms on the Index Performance Strategy, and between the 1-year Terms for the Index Guard Strategy and Index Performance Strategy. They may also be different from Contract-to-Contract depending on the Index Effective Date and the state of issuance. |

Bar Chart Examples of the Crediting Methods Performance

The following hypothetical examples show conceptually how the Crediting Methods might work in different market environments and assume no change in the hypothetical DPSCs, Precision Rates, Caps, and/or Participation Rates. All values below are for illustrative purposes only. The examples do not reflect any Buffers, Floors, DPSCs, Precision Rates, Caps, and/or Participation Rates that may actually apply to a Contract. The examples do not predict or project the actual performance of the Index Advantage Income®. Although an Index or Indexes will affect your Index Option Values, the Index Options do not directly participate in any stock or equity investment and are not a direct investment in an Index. The Index Values do not include the dividends paid on the stocks comprising an Index. An allocation to an Index Option is not a purchase of shares of any stock or index fund. These examples do not reflect deduction of the Contract fees and expenses. Historical Index Option performance information is also included in Appendix D.

Allianz Index Advantage Income® Variable Annuity Prospectus – April 30, 2021

20

Can the Crediting Methods, Terms, or Indexes Change?