RBC Conference – Martha’s Vineyard September 2004

Forward Looking Statements

This news release contains certain forward-looking statements that are included pursuant to the safe harbor provisions of the Private Securities Litigation Reform Act of 1995. Such information involves risks and uncertainties that could result in the Company’s actual results differing from those projected in the forward-looking statements. Important factors that could cause actual results to differ materially from those discussed in such forward-looking statements include, but are not limited to, (1) the Company may incur additional loan loss provision due to negative credit quality trends in the future that may lead to a deterioration of asset quality, or conversely, the Company may incur less, or even negative, loan loss provision due to positive credit quality trends in the future; (2) the Company may not continue to experience significant recoveries of previously charged-off loans and the Company may incur increased charge-offs in the future; (3) the Company may experience increases in the default rates on its previously securitized loans causing the yields on these assets to decline; (4) the Company could have adverse legal actions of a material nature; (5) the Company may face competitive loss of customers; (6) the Company may be unable to manage its expense levels; (7) changes in the interest rate environment may have results on the Company’s operations materially different from those anticipated by the Company’s market risk management functions; (8) changes in general economic conditions and increased competition could adversely affect the Company’s operating results; (9) changes in other regulations and government policies affecting bank holding companies and their subsidiaries, including changes in monetary policies, could negatively impact the Company’s operating results; (10) the Company may experience difficulties growing loan and deposit balances. Forward-looking statements made herein reflect management’s expectations as of the date such statements are made. Such information is provided to assist stockholders and potential investors in understanding current and anticipated financial operations of the Company and is included pursuant to the safe harbor provisions of the Private Securities Litigation Reform Act of 1995. The Company undertakes no obligation to update any forward-looking statement to reflect events or circumstances that arise after the date such statements are made.

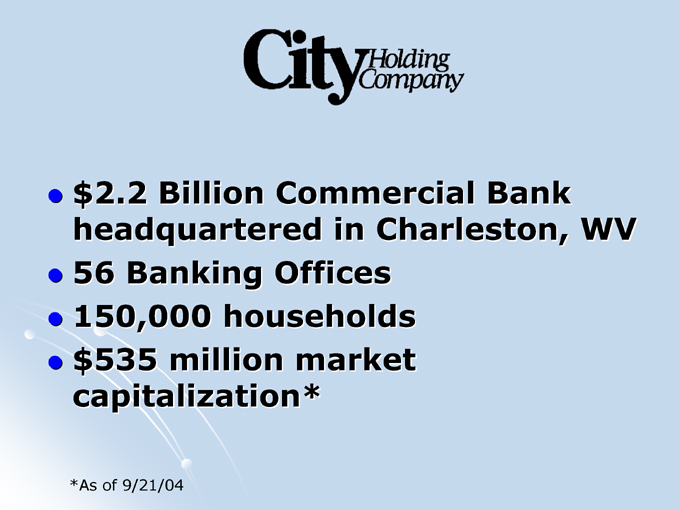

$2.2 Billion Commercial Bank headquartered in Charleston, WV 56 Banking Offices 150,000 households $535 million market capitalization*

*As of 9/21/04

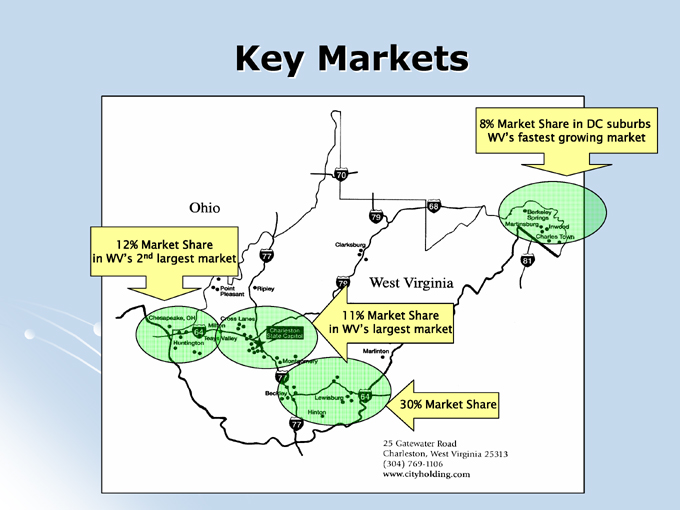

Key Markets

8% Market Share in DC suburbs WV’s fastest growing market

12% Market Share in WV’s 2nd largest market

11% Market Share in WV’s largest market

30% Market Share

Ohio West Virginia

25 Gatewater Road

Charleston, West Virginia 25313

(304) 769-1106

www.cityholding.com

Why Own This Stock?

1. CHCO is highly profitable

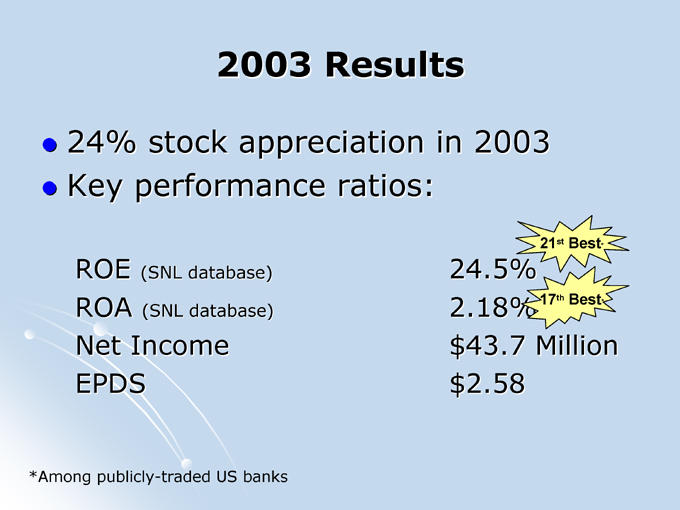

2003 Results

24% stock appreciation in 2003 Key performance ratios:

ROE (SNL database) 24.5%

21st Best*

ROA (SNL database) 2.18%

17th Best*

Net Income $43.7 Million

EPDS $2.58

*Among publicly-traded US banks

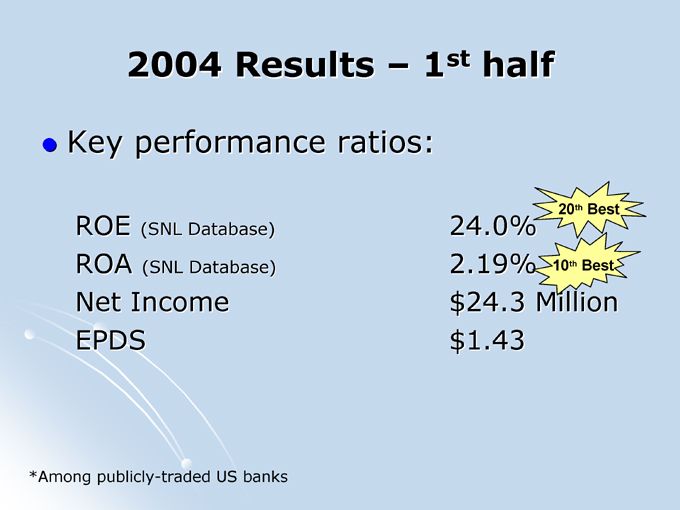

2004 Results – 1st half

Key performance ratios:

ROE (SNL Database) 24.0%

20th Best

ROA (SNL Database) 2.19%

10th Best

Net Income $24.3 Million EPDS $1.43

*Among publicly-traded US banks

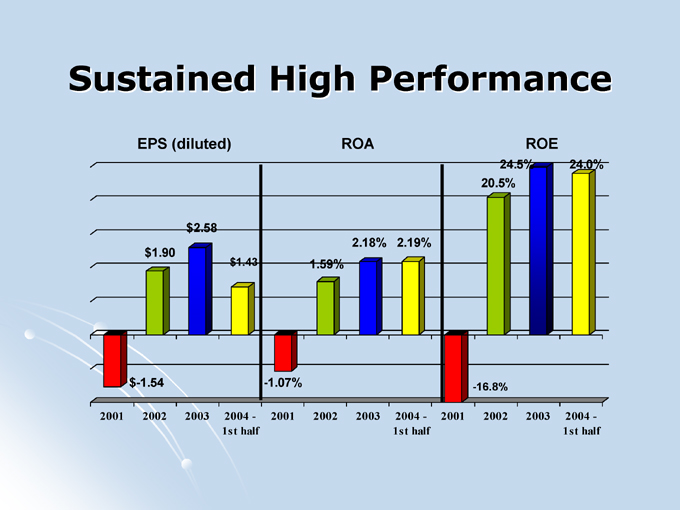

Sustained High Performance

EPS (diluted) ROA ROE $2.58 $1.90 $1.43

2.18% 2.19% 1.59%

24.5% 24.0% 20.5% $-1.54 -1.07% -16.8%

2001 2002 2003 2004 - 1st half 2001 2002 2003 2004 - 1st half 2001 2002 2003 2004 - 1st half

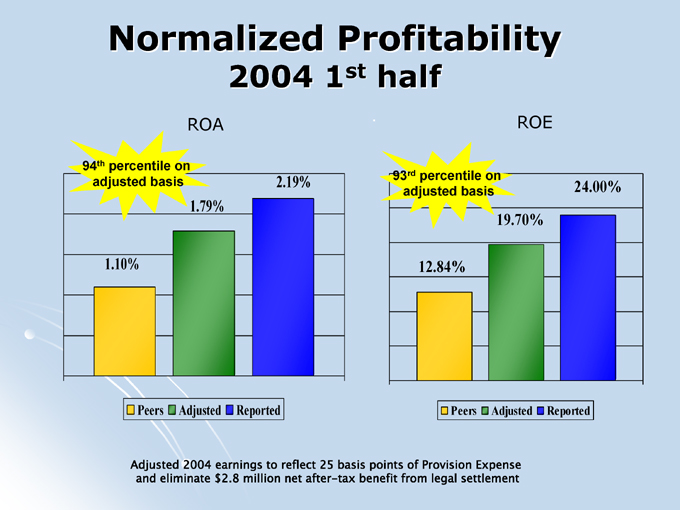

Normalized Profitability

2004 1st half

ROA ROE

94th percentile on adjusted basis

1.10%

1.79%

2.19%

Peers Adjusted Reported

93rd percentile on adjusted basis

12.84%

19.70%

24.00%

Peers Adjusted Reported

Adjusted 2004 earnings to reflect 25 basis points of Provision Expense and eliminate $2.8 million net after-tax benefit from legal settlement

Why Own This Stock?

1. CHCO is highly profitable 2. CHCO is growing share

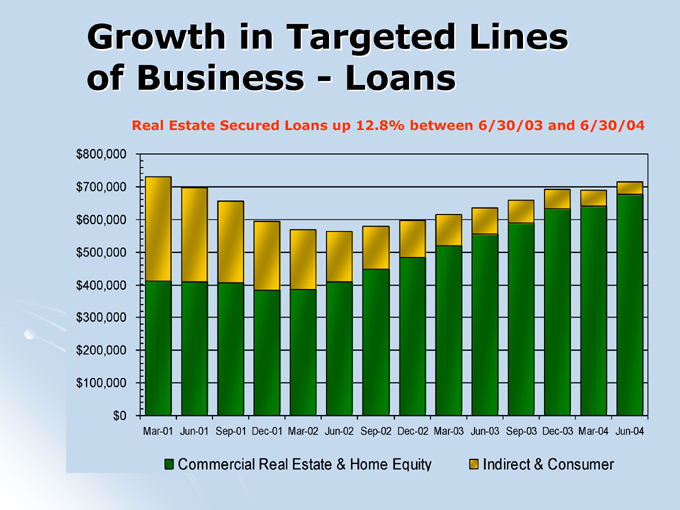

Growth in Targeted Lines of Business - Loans

Real Estate Secured Loans up 12.8% between 6/30/03 and 6/30/04 $800,000 $700,000 $600,000 $500,000 $400,000 $300,000 $200,000 $100,000 $0

Mar-01 Jun-01 Sep-01 Dec-01 Mar-02 Jun-02 Sep-02 Dec-02 Mar-03 Jun-03 Sep-03 Dec-03 Mar-04 Jun-04

Commercial Real Estate & Home Equity Indirect & Consumer

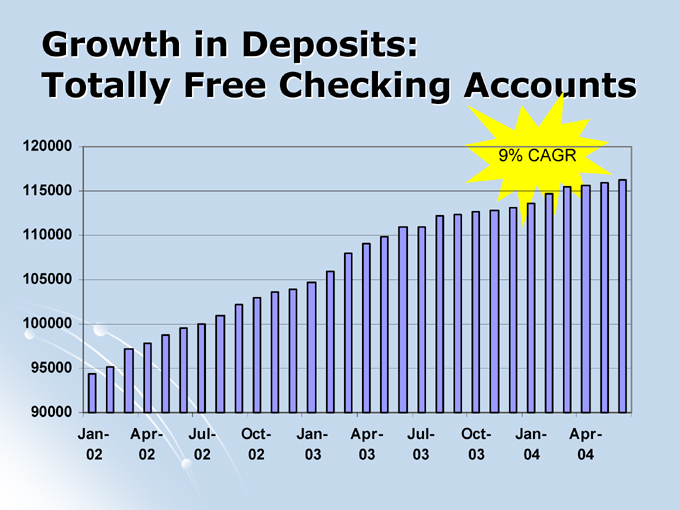

Growth in Deposits:

Totally Free Checking Accounts

9% CAGR

120000 115000 110000 105000 100000 95000 90000

Jan-02

Apr-02

Jul-02

Oct-02

Jan-03

Apr-03

Jul-03

Oct-03

Jan-04

Apr-04

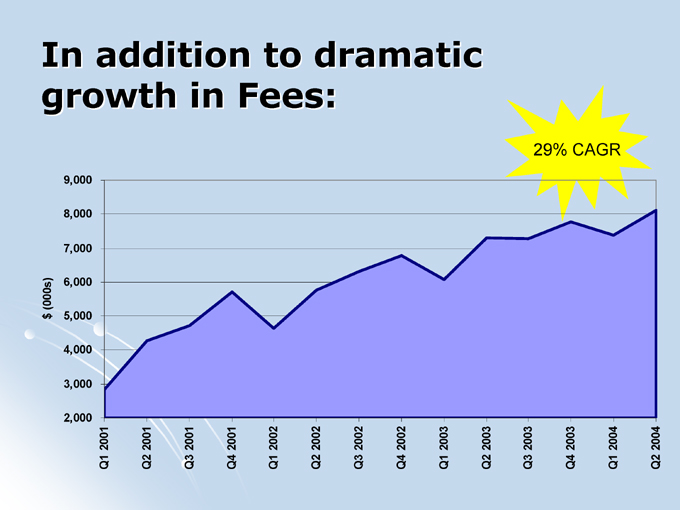

In addition to dramatic growth in Fees:

29% CAGR

9,000 8,000 7,000

$ (000s) 6,000 5,000

4,000 3,000 2,000

Q1 2001 Q2 2001 Q3 2001 Q4 2001 Q1 2002 Q2 2002 Q3 2002 Q4 2002 Q1 2003 Q2 2003 Q3 2003 Q4 2003 Q1 2004 Q2 2004

Why Own This Stock?

1. CHCO is highly profitable 2. CHCO is growing share 3. CHCO is well-positioned for the future

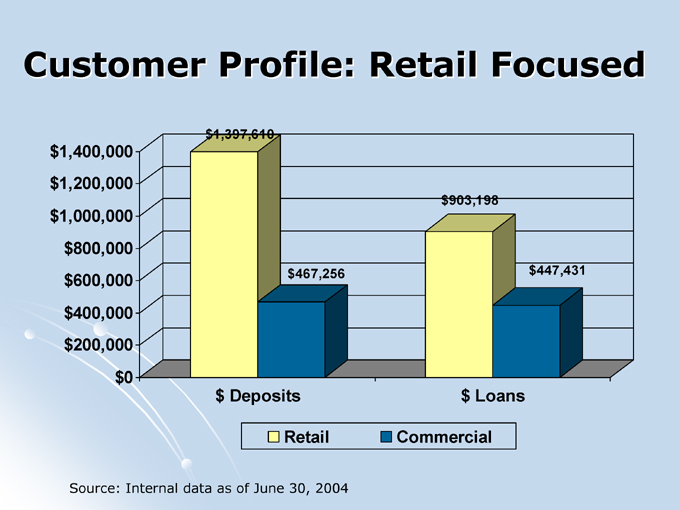

Customer Profile: Retail Focused $1,400,000 $1,200,000 $1,000,000 $800,000 $600,000 $400,000 $200,000 $0 $1,397,610 $467,256 $903,198 $447,431 $ Deposits $ Loans

Retail Commercial

Source: Internal data as of June 30, 2004

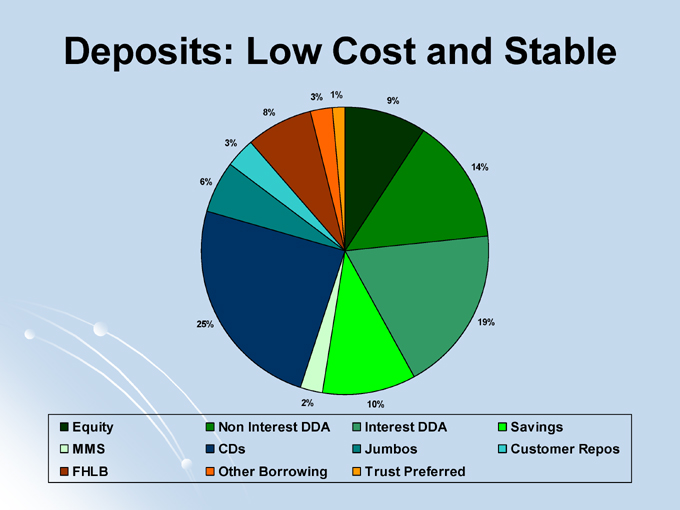

Deposits: Low Cost and Stable

3% 1%

9%

14%

19%

10%

2%

25%

6%

3%

8%

Equity Non Interest DDA Interest DDA Savings

MMS CDs Jumbos Customer Repos FHLB Other Borrowing Trust Preferred

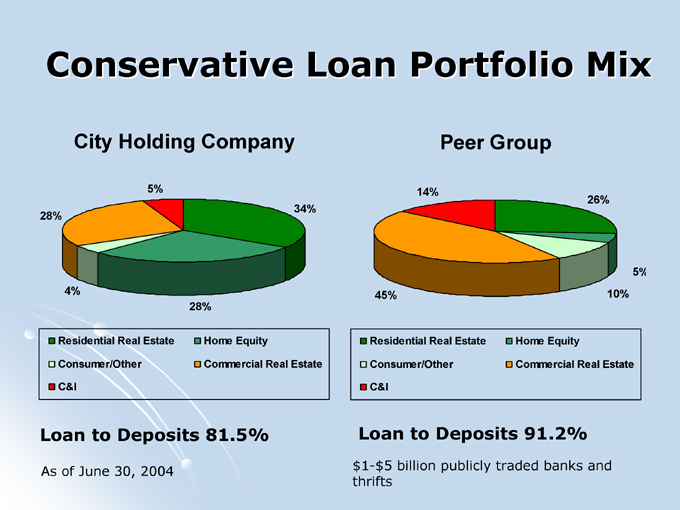

Conservative Loan Portfolio Mix

City Holding Company

28%

5%

34%

4%

28%

Residential Real Estate Home Equity

Consumer/Other Commercial Real Estate

C&I

Loan to Deposits 81.5%

As of June 30, 2004

Peer Group

14%

26%

45%

5%

10%

Residential Real Estate Home Equity

Consumer/Other Commercial Real Estate

C&I

Loan to Deposits 91.2%

$1-$5 billion publicly traded banks and thrifts

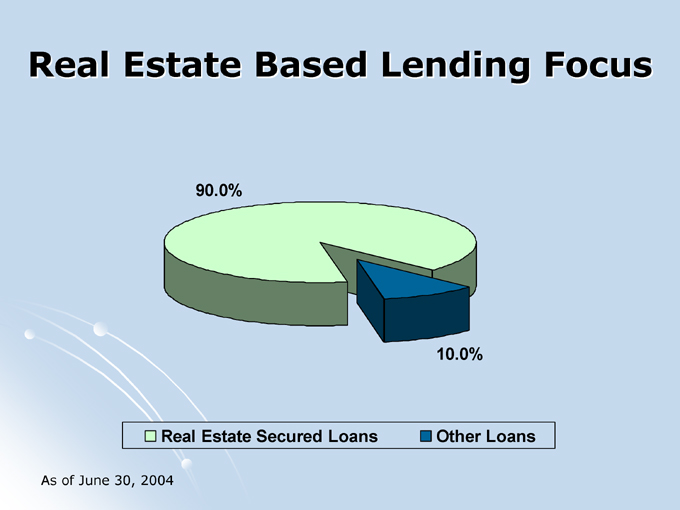

Real Estate Based Lending Focus

90.0%

10.0%

Real Estate Secured Loans Other Loans

As of June 30, 2004

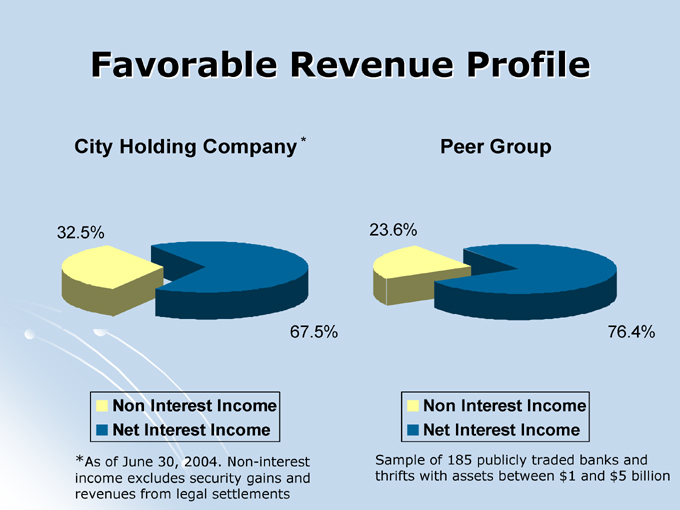

Favorable Revenue Profile

City Holding Company*

32.5%

67.5%

Non Interest Income Net Interest Income

*As of June 30, 2004. Non-interest income excludes security gains and revenues from legal settlements

Peer Group

23.6%

76.4%

Non Interest Income Net Interest Income

Sample of 185 publicly traded banks and thrifts with assets between $1 and $5 billion

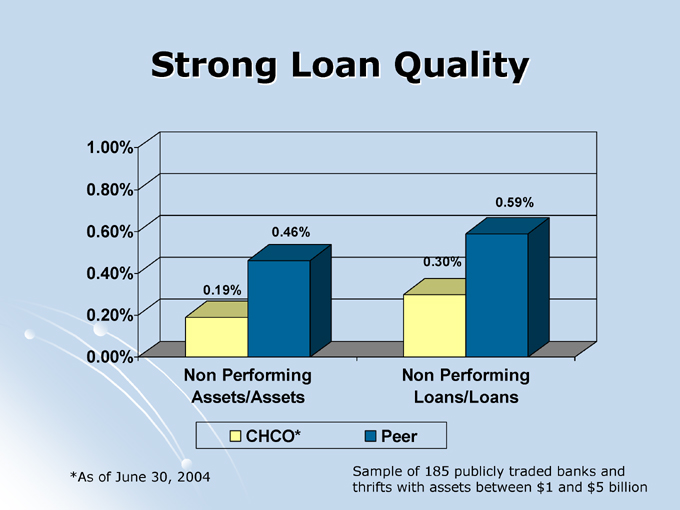

Strong Loan Quality

1.00% 0.80% 0.60% 0.40% 0.20% 0.00%

0.19%

0.46%

0.30%

0.59%

Non Performing Assets/Assets

Non Performing Loans/Loans

CHCO* Peer

*As of June 30, 2004

Sample of 185 publicly traded banks and thrifts with assets between $1 and $5 billion

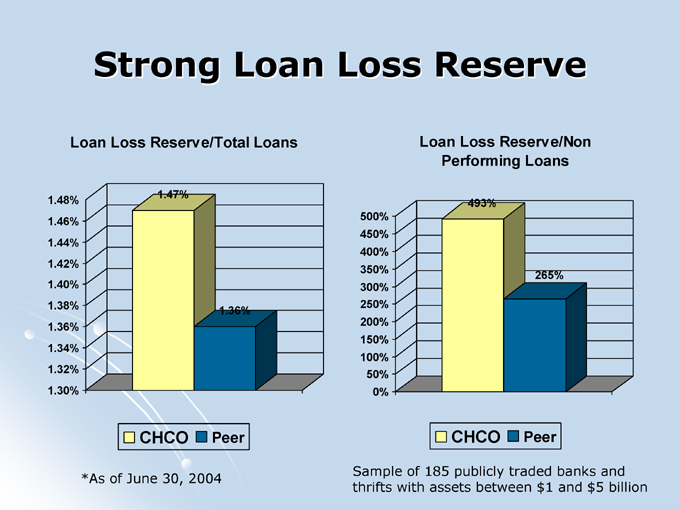

Strong Loan Loss Reserve

Loan Loss Reserve/Total Loans

1.48% 1.46% 1.44% 1.42% 1.40% 1.38% 1.36% 1.34% 1.32% 1.30%

1.47%

1.36%

CHCO Peer

*As of June 30, 2004

Loan Loss Reserve/Non Performing Loans

500% 450% 400% 350% 300% 250% 200% 150% 100% 50% 0%

493%

265%

CHCO Peer

Sample of 185 publicly traded banks and thrifts with assets between $1 and $5 billion

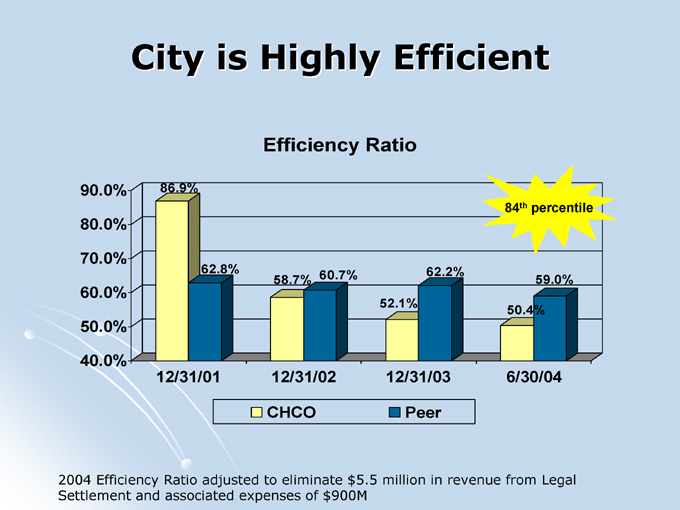

City is Highly Efficient

Efficiency Ratio

90.0% 80.0% 70.0% 60.0% 50.0% 40.0%

86.9%

62.8%

58.7% 60.7%

52.1%

62.2%

50.4%

59.0%

84th percentile

12/31/01 12/31/02 12/31/03 6/30/04

CHCO Peer

2004 Efficiency Ratio adjusted to eliminate $5.5 million in revenue from Legal Settlement and associated expenses of $900M

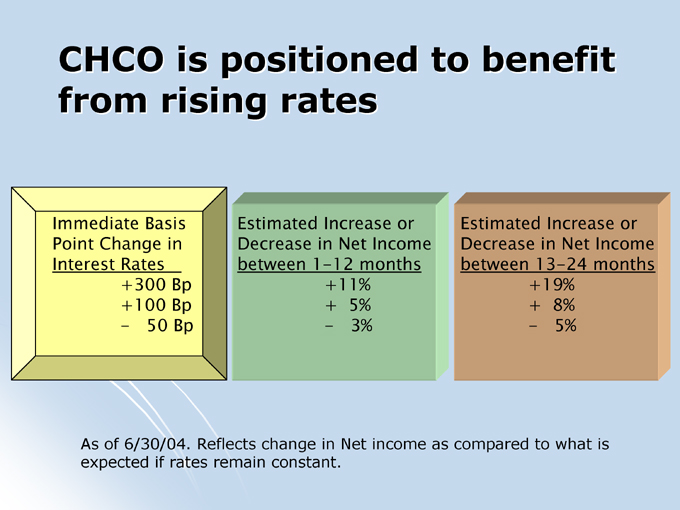

CHCO is positioned to benefit from rising rates

Immediate Basis Point Change in Interest Rates +300 Bp +100 Bp

- 50 Bp

Estimated Increase or Decrease in Net Income between 1-12 months +11%

+ 5%

- 3%

Estimated Increase or Decrease in Net Income between 13-24 months +19%

+ 8%

- 5%

As of 6/30/04. Reflects change in Net income as compared to what is expected if rates remain constant.

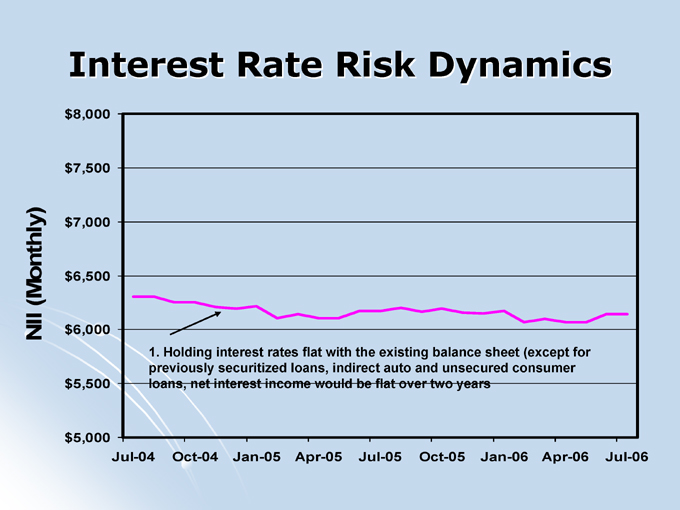

Interest Rate Risk Dynamics $8,000

$7,500

(Monthly) $7,000

$6,500

NII $6,000 $5,500

$5,000

1. Holding interest rates flat with the existing balance sheet (except for previously securitized loans, indirect auto and unsecured consumer loans, net interest income would be flat over two years

Jul-04 Oct-04 Jan-05 Apr-05 Jul-05 Oct-05 Jan-06 Apr-06 Jul-06

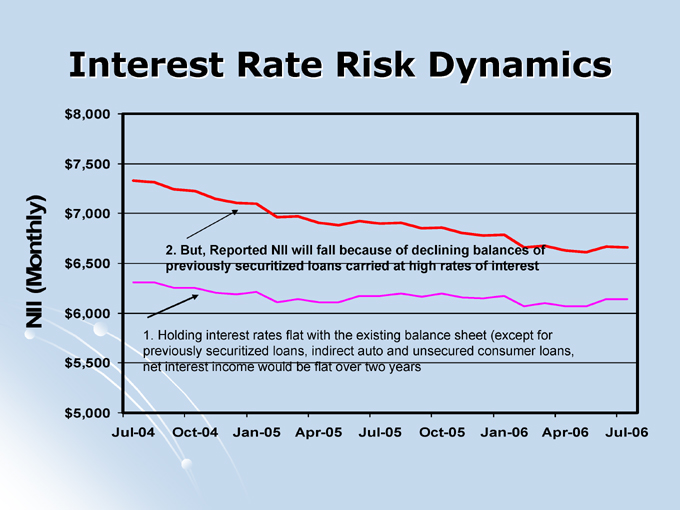

Interest Rate Risk Dynamics $8,000

$7,500

(Monthly)

$7,000

$6,500

NII $6,000 $5,500

$5,000

2. But, Reported NII will fall because of declining balances of previously securitized loans carried at high rates of interest

1. Holding interest rates flat with the existing balance sheet (except for previously securitized loans, indirect auto and unsecured consumer loans, net interest income would be flat over two years

Jul-04 Oct-04 Jan-05 Apr-05 Jul-05 Oct-05 Jan-06 Apr-06 Jul-06

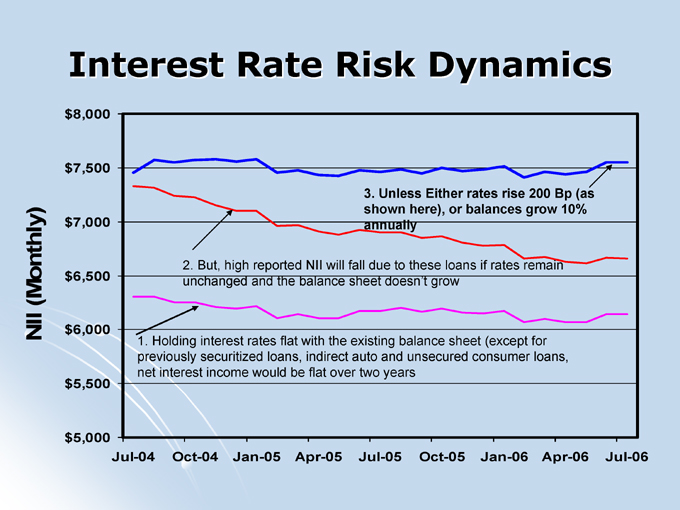

Interest Rate Risk Dynamics $8,000

$7,500

(Monthly) $7,000

$6,500

NII $6,000 $5,500

$5,000

3. Unless Either rates rise 200 Bp (as shown here), or balances grow 10% annually

2. But, high reported NII will fall due to these loans if rates remain unchanged and the balance sheet doesn’t grow

1. Holding interest rates flat with the existing balance sheet (except for previously securitized loans, indirect auto and unsecured consumer loans, net interest income would be flat over two years

Jul-04 Oct-04 Jan-05 Apr-05 Jul-05 Oct-05 Jan-06 Apr-06 Jul-06

Why Own This Stock?

1. CHCO is highly profitable 2. CHCO is growing share 3. CHCO is well positioned for the future

Retail focus

Strong core deposit base Strong non-interest income Conservative loan portfolio

Loans predominately real estate secured Loan quality is extremely strong Well reserved for problem loans Positioned to benefit from rising rates

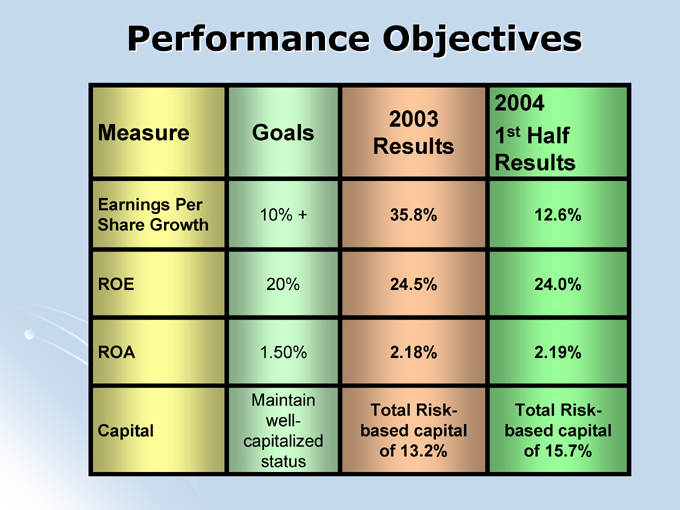

Performance Objectives

Measure

Goals

2003 Results

2004 1st Half Results

Earnings Per Share Growth

10% + 35.8% 12.6%

ROE 20% 24.5% 24.0%

ROA 1.50% 2.18% 2.19%

Capital

Maintain well-capitalized status

Total Risk-based capital of 13.2%

Total Risk-based capital of 15.7%

Strategic Opportunities

Results of Retail Delivery System Study:

City’s distribution is sub-optimal

In WV’s 10 densest markets, City has no presence in 50%

In WV’s 60 densest markets, City is in only 33%

5 year Plan to improve distribution

Consolidate 10% of distribution network Build 3-5 branches Add 3-5 in-store locations

Strategic Opportunities

Moving out to restructure the retail network:

2 new Wal-Mart Branches opened Sept 2004

High-density retail areas in Charleston & Huntington Over 40% of the way to profitability after opening 750 new accounts

Strategic Opportunities

Capital Flexibility – Tier II Capital @ 15.7%

Dividends – Increased 10% in April 2004

Share Repurchases – have repurchased over 1% of outstanding shares since the 2nd Q

Acquisitions are possible

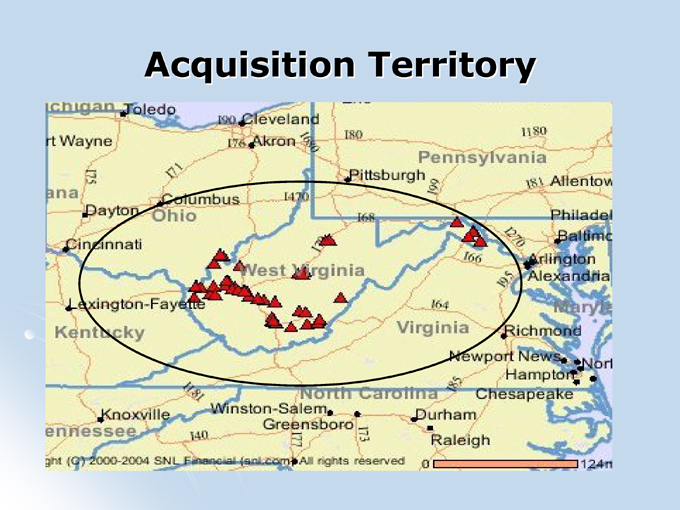

Acquisition Parameters

$100MM to $500MM in assets

Markets in or adjacent to CHCO footprint Retail Deposit Franchise Accretive to EPS in first full year

Acquisition Territory

Why Own This Stock

Highly Profitable Franchise Strong fee-income Strong asset quality Liquid Core-funded Loans are real-estate and retail Strongly capitalized Moving ahead to re-position the retail franchise And yet, priced lower than peers

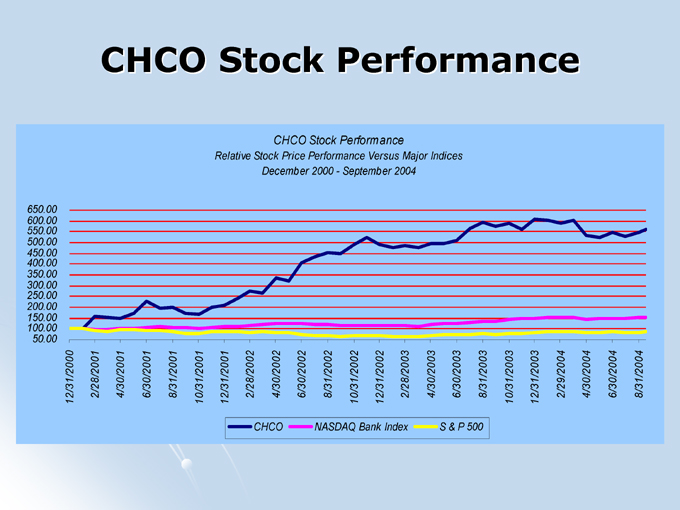

CHCO Stock Performance

CHCO Stock Performance

Relative Stock Price Performance Versus Major Indices December 2000—September 2004

650.00 600.00 550.00 500.00 450.00 400.00 350.00 300.00 250.00 200.00 150.00 100.00 50.00

12/31/2000 2/28/2001 4/30/2001 6/30/2001 8/31/2001 10/31/2001 12/31/2001 2/28/2002 4/30/2002

6/30/2002 8/31/2002 S&P 500 10/31/2002

12/31/2002 2/28/2003 4/30/2003 6/30/2003 8/31/2003 10/31/2003 12/31/2003 2/29/2004 4/30/2004 6/30/2004 8/31/2004

CHCO NASDAQ Bank Index S & P 500

Questions?