Exhibit 99.1 |

PSLA Disclaimer This presentation includes forward-looking statements which AmericanWest intends to be covered by the safe harbor provisions of the Private Securities Litigation Act of 1995. These forward- looking statements describe management’s expectations regarding future events, including but not limited to: improvements in operation performance from the merger with Far West Bancorporation and expense reduction initiatives, asset quality and net charge-offs, loan and deposit growth and the net interest margin. Future event are difficult to predict and subject to risk and uncertainty which could cause actual results to differ materially and adversely. Addition information regarding risks and uncertainties is included in AmericanWest’s periodic filings on Forms 10-K and 10-Q with the Securities and Exchange Commission. AmericanWest undertakes no obligation to revise or amend any forward-looking statements to reflect subsequent events or circumstances. |

Overview • $2.0 billion single-bank holding company based in Spokane, Washington • Traded on NASDAQ Global Select Market under symbol “AWBC” • Market Capitalization of $350 million as of May 1, 2007 • Originally founded in 1974 (United Security Bank) • Operates 62 financial centers and 4 loan production offices throughout Eastern/Central Washington, Northern Idaho and Utah • Unique Inner Mountain region community bank franchise |

|

AWBC Executive Management Team Joined Prior Industry Name Title Age AWBC Experience Robert M. Daugherty President & CEO 53 Sep-04 Humboldt Bancorp, Draper Bank & Trust, US Bank Patrick J. Rusnak EVP/COO/CFO 43 Sep-06 Western Sierra Bancorp, Humboldt Bancorp, United Community Banks, Inc. Rick Shamberger EVP/CCO 46 Oct-03 US Bank Nicole Sherman EVP/Retail Banking 38 Dec-04 Zions Bank Robert M. Bowen EVP/Utah Commercial Lending Utah 54 May-06 US Bank Robert A. Harris EVP/Director of Commercial Lending WA/ID 45 Mar-05 US Bank |

Turn Around Story – Chapter 1 (2004-5) Getting Out of the Regulatory Doghouse • Faced with a compliance MOU and regulatory directive to resolve credit quality deficiencies, the board initiated a CEO search in Q3 2004 • Bob Daugherty hired as President/CEO in September 2004 • Immediate action taken to strengthen credit culture and change focus from transactional to relationship lending • Several key executive management changes, including CFO, EVP/Retail Banking and General Counsel • MOU and regulatory directive both lifted in Q4 2005 |

Turn Around Story – Chapter 2 (2006) Reinvesting in the Franchise • Opened 4 new financial centers in key growth markets and relocated 2 financial centers • Rolled out new concept “end-cap” financial center • <2,000 square feet; per unit investment of $700,000 • Initiated private banking services division • Completed acquisition of Columbia Trust Bancorp (Q1 2006) |

Reinvesting in the Franchise (cont’d) • Several key technology investments, including • Upgraded ATMs • New teller and new accounts platforms • Remote deposit capture • Opened LPO in South Jordan, Utah (Q3 2006) • Contributed 50% of organic loan growth for 2006 ($50MM) and 70% for Q1 2007 • Loan pricing is significantly better than WA/ID; being compensated for credit risk on construction loans |

Spokane/West Plains Financial Center Opened 12/06 |

Strategic Expansion Focus - Utah • Utah has excellent long-term growth prospects and a dynamic economy • Projected population growth well in excess of national averages • Provo MSA expected growth of 24% by 2011 • Flagship financial center to open in the Walker Center Building in the downtown Salt Lake City financial district in Q3 2007 • Temporary LPO opened in March 2007 • SBA lending team hired in Q1 2007 |

Strategic Focus – Utah De Novo Expansion (cont’d) • Niche opportunity for a larger service- focused community bank given current competitive composition in Utah banking market: Utah Deposits as of June 30, 2006* Deposits in millions Number of Total Deposits Average Banks Deposits % Deposits National/Regional 7 31,347 78% 4,478 Community 49 8,802 22% 180 56 40,149 100% *Excludes $103 billion of brokerage/specialty deposits. Source: FDIC. |

Walker Center Building, Salt Lake City, Utah |

Turn Around Story – Chapter 3 (2007) Focus on Performance Improvement • Completed acquisition of Far West Bancorporation effective April 1 • Far West among the top performing banks in the West • All Utah financial centers operating under Far West Bank brand • Principal focus is now on earnings performance and efficiency improvement • Announced 5% staffing reduction in March 2007 • $2MM in annual expense reductions achieved • New financial center expansion substantially completed • 3 new financial centers planned for 2007 plus 2 relocations of existing financial centers • Will continue to evaluate selected de novo and acquisition expansion opportunities in existing or contiguous high- growth markets |

Q1 2007 Financial Highlights • Diluted EPS $0.19; $0.21 excluding non-recurring items • Severance, merger costs, OREO gain • Annualized loan growth of 9%; 16% excluding reduction in agricultural loans • $11MM in disengagements from marginal credits • Annualized deposit growth of 16% • Increase in quarterly cash dividend of 33%, to $0.04 |

Q1 2007 Financial Highlights (cont’d) • Net interest margin of 4.69%, a decrease of 33 bp from Q4 2006 and a decrease of 46 bp from Q1 2006 • 25 of the 33 bp linked quarter decline due to change in accounting for deferred loan fees for loans with maturities of one year or less |

Asset Quality Trends • Non-performing loan and asset levels at 3/31/07 fell to lowest level in over five years • 0.47% of total loans and assets • Q1 2007 net charge-offs of 15 bp (annualized) • Disengaged from approximately $11MM in marginal agriculture credits during Q1 • Potential problem loans declined by 20% from year-end 2007 • Allowance for credit losses/loan ratio of 1.25% at March 31, 2007; 1.41% pro forma with Far West merger. |

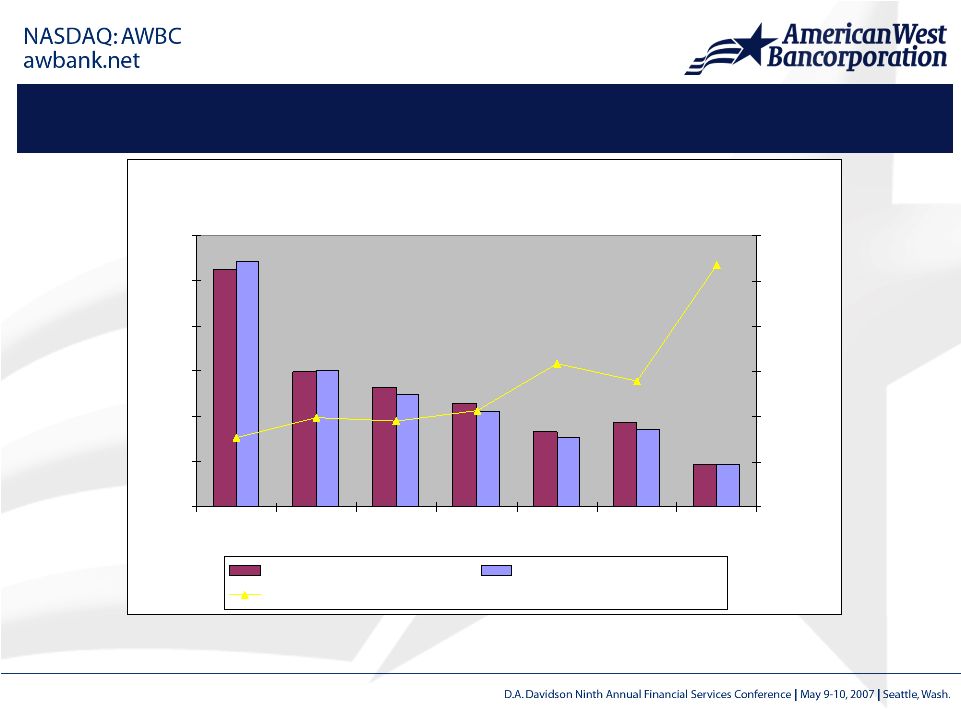

Asset Quality Trends *Excluding government guaranteed amounts ** Allowance for credit losses, which is comprised of the allowance for loan losses and reserve for unfunded commitments. AmericanWest Bancorporation Credit Quality Trends 0.00% 0.50% 1.00% 1.50% 2.00% 2.50% 3.00% 12/31/04 12/31/05 3/31/06 6/30/06 9/30/06 12/31/06 3/31/07 0.00% 50.00% 100.00% 150.00% 200.00% 250.00% 300.00% Non-performing loans/loans* Non-performing assets/assets* ACL**/non-performing loans |

Far West Bank Merger • Credit administration processes fully integrated and under standard underwriting policies • Regional credit administrator relocated from Spokane to Provo (with significant loan approval authority) • Expect to achieve targeted cost savings of 15% ($2.5MM annual) by end of Q2 2007 • Purchase accounting adjustments substantially completed • No significant adjustments for loans/deposits • Core deposit intangible of $12.9MM • First year accelerated amortization of $3.2MM, in line with original projections |

Far West Bank Merger – Pro Forma 4/30/07 AmericanWest Bancorporation Selected Financial Information (unaudited) (in thousands, except per share data) Pro Forma 3/31/2007 4/30/2007 Loans, net 1,231,731 $ 1,605,570 $ Deposits 1,167,148 1,538,165 Shareholders' equity 154,731 280,000 Goodwill and intangibles 40,288 148,000 Book value per share 13.54 16.29 Tangible book value per share 10.02 7.68 Allowance for credit losses (ACL) 15,571 $ 23,333 $ Shares outstanding 11,413 17,185 ACL/total loans 1.25% 1.41% |

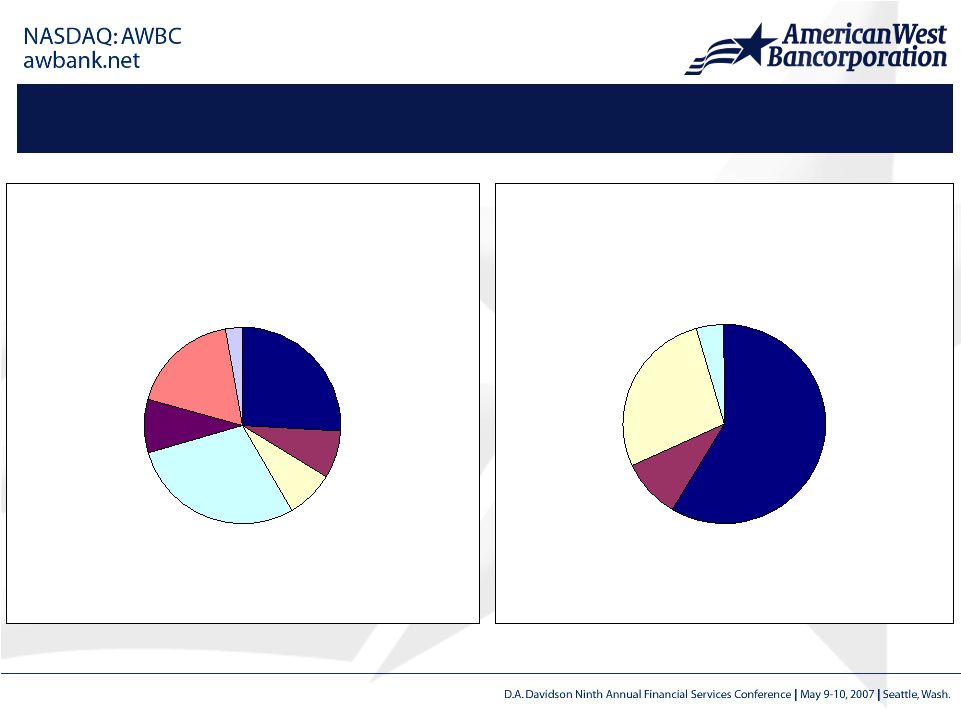

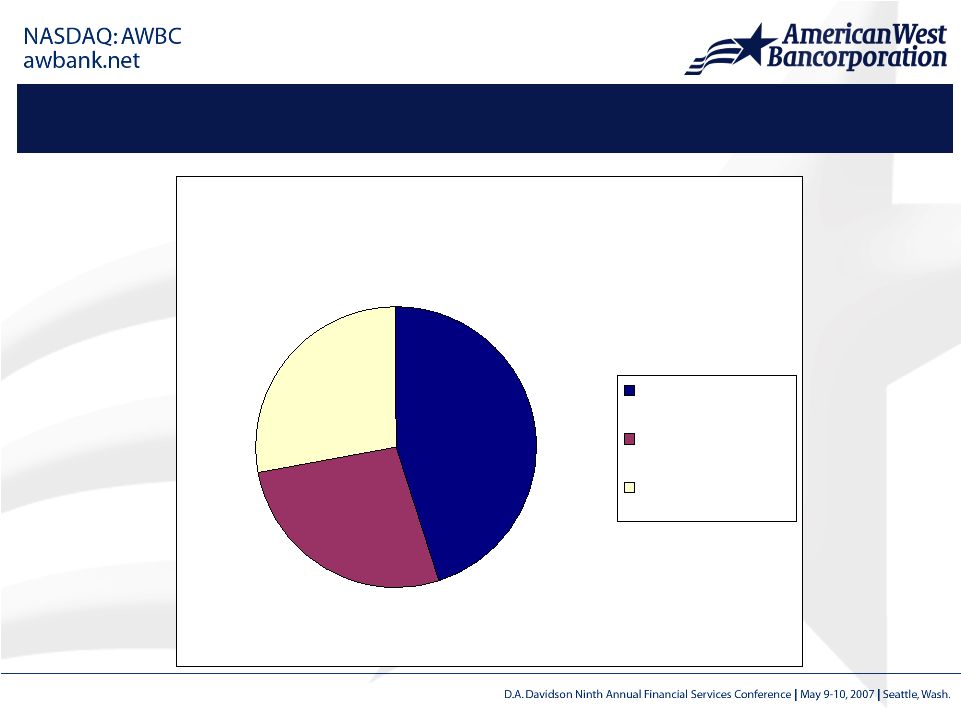

Loan Portfolio Composition – Pro Forma Combined as of March 31, 2007 Loans by Type Construction/ Land Development 26% Residential Mortgage 8% Multifamily 8% CRE 28% Agriculture 9% Commercial & Industrial 18% Consumer & Other 3% Loans by State Utah 28% Idaho 10% Other 4% Washington 58% |

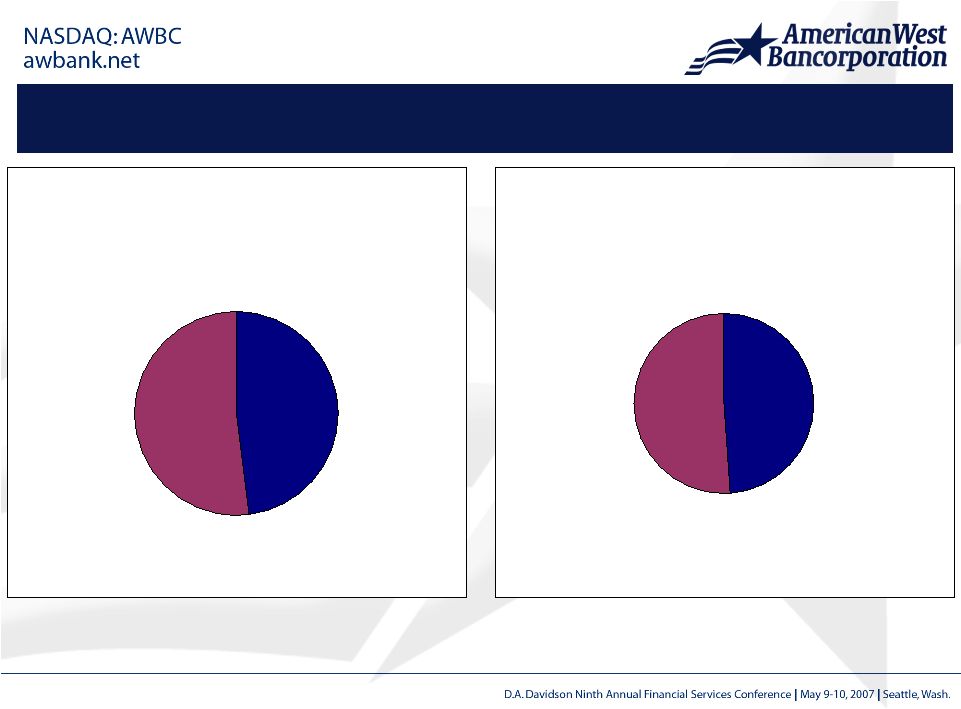

Loan Portfolio – Combined with Far West as of March 31, 2007 Commercial Real Estate Owner Occupied 49% Investor 51% Construction/Acquisition & Development Commercial 48% Residential 52% |

Loan Repricing Mix - Pro Forma as of March 31, 2007 Repricing Mix 45% 27% 28% 0-3 Month Reset Adj. 6 Months - 5 Years Fixed (WAM 91 Months) |

SFAS 159 – A Headache Avoided • Did not elect early adoption of SFAS 159 • Minor restructuring of bond portfolio in Q2 2007; no significant gain/loss anticipated • $10MM of trust preferred callable in Q3 2007 • Expect to refinance issuance; current market rates are about 200 bp lower • Issuance cost will be fully amortized by call date so no loss is expected |

2007 Outlook and Beyond • NPA/total assets: 50 to 75 bp • Net charge-offs: 25 to 35 bp (annualized) • Organic Loan growth: 12% to 15% • Organic Deposit growth: 8% to 11% • Net interest margin*: 5.15% to 5.35% • Efficiency ratio** (Q4 2007): 60% – 62% • Target ROA/ROE/ROTE (2009):1.30%/12%/18% * For Q2-Q4 2007 **excluding intangible amortization |

Summary of Recent M&A Activity AmericanWest Bancorporation Recent M&A Activity (in thousands) Date Deal Assets Consideration Target Company Closed Value Acquired Mix Far West Bancorporation 4/1/2007 154,423 $ 488,816 $ 80% stock/20% cash Columbia Trust Bancorp 3/15/2006 39,554 $ 229,972 $ 56% stock/44% cash Bank of Latah 7/31/2002 17,500 $ 141,372 $ 23% stock/77% cash |

|