As filed with the Securities and Exchange Commission on May 24, 2024

Registration No. 333-______

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM S-4

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

IPALCO ENTERPRISES, INC.

(Exact Name of Registrant as Specified in Its Charter)

| Indiana | 4911 | 35-1575582 |

(State or Other Jurisdiction of

Incorporation or Organization) | (Primary Standard Industrial

Classification Code Number) | (I.R.S. Employer

Identification No.) |

| | | |

| | One Monument Circle

Indianapolis, Indiana 46204

317-261-8261 | |

| (Address, Including Zip Code, and Telephone Number, Including Area Code, of Registrant’s Principal Executive Offices) |

|

Brian Hylander, Esq.

Vice President, General Counsel and Secretary

IPALCO Enterprises, Inc.

One Monument Circle

Indianapolis, Indiana 46204 317-261-8261 |

| (Name, Address, Including Zip Code, and Telephone Number, Including Area Code, of Agent For Service) |

| |

| | Copies to: | |

Richard D. Truesdell, Jr., Esq. Joseph S. Payne, Esq.

Davis Polk & Wardwell LLP

450 Lexington Avenue

New York, New York 10017

(212) 450-4000 |

Approximate date of commencement of proposed sale to the public: As soon as practicable after the effective date of this Registration Statement.

If the securities being registered on this form are being offered in connection with the formation of a holding company and there is compliance with General Instruction G, check the following box. ☐

If this form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

If this form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

Large accelerated filer ☐ Accelerated filer ☐ Non-accelerated filer ☒

Smaller reporting company ☐ Emerging growth company ☐

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 7(a)(2)(B) of the Securities Act. ☐

If applicable, place an X in the box to designate the appropriate rule provision relied upon in conducting this transaction:

Exchange Act Rule 13e-4(i) (Cross-Border Issuer Tender Offer) ☐

Exchange Act Rule 14d-l(d) (Cross-Border Third-Party Tender Offer) ☐

| (1) | Estimated solely for the purpose of computing the amount of the registration fee pursuant to Rule 457 under the Securities Act of 1933. |

The Registrant hereby amends this Registration Statement on such date or dates as may be necessary to delay its effective date until the Registrant shall file a further amendment which specifically states that this Registration Statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933, as amended or until the Registration Statement shall become effective on such date as the Commission, acting pursuant to said Section 8(a), may determine.

The information in this prospectus is not complete and may be changed. We may not sell these securities until the registration statement filed with the Securities and Exchange Commission is effective. This prospectus is not an offer to sell these securities and is not soliciting offers to buy these securities in any state where the offer or sale is not permitted.

PROSPECTUS SUBJECT TO COMPLETION, DATED MAY 24, 2024

IPALCO Enterprises, Inc.

Offer to Exchange

5.750% Senior Secured Notes due 2034

for

New 5.750% Senior Secured Notes due 2034

We are offering to exchange up to $400,000,000 of our new registered 5.750% Senior Secured Notes due 2034 (the “new notes” or “notes”) for up to $400,000,000 of our existing unregistered 5.750% Senior Secured Notes due 2034 (the “old notes”). The terms of the new notes are identical in all material respects to the terms of the old notes, except that the new notes have been registered under the Securities Act of 1933, as amended (the “Securities Act”), and the transfer restrictions and registration rights relating to the old notes do not apply to the new notes. The new notes will represent the same debt as the old notes and we will issue the new notes under the same indenture.

To exchange your old notes for new notes:

| ● | you are required to make the representations described on page 3 to us; and |

| ● | you should read the section called “The Exchange Offer” starting on page 124 for further information on how to exchange your old notes for new notes. |

The exchange offer will expire at 5:00 P.M. New York City time on , 2024 unless it is extended.

No public market currently exists for the old notes and we cannot assure you that any public market for the new notes will develop. The new notes will not be listed on any national securities exchange.

See “Risk Factors” beginning on page 6 of this prospectus for a discussion of risk factors that should be considered by you prior to tendering your old notes in the exchange offer.

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of the securities to be issued in the exchange offer or passed upon the adequacy or accuracy of this prospectus. Any representation to the contrary is a criminal offense.

, 2024

table of contents

Page

We have not authorized anyone to provide you with any information other than that contained in this prospectus or to which we have referred you. We take no responsibility for and can provide no assurance as to the reliability of, any other information that others may give you. You should assume that the information appearing in this prospectus is accurate only as of the date on the front cover of this prospectus. Our business, financial condition, results of operations and prospects may have changed since that date.

This prospectus is based on information provided by us and by other sources that we believe are reliable. We cannot assure you that this information is accurate or complete. This prospectus summarizes certain documents and other information and we refer you to them for a more complete understanding of what we discuss in this prospectus. In making an investment decision, you must rely on your own examination of our company and the terms of the offering and the notes, including the merits and risks involved.

We are not making any representation to any purchaser of the notes regarding the legality of an investment in the notes by such purchaser under any legal investment or similar laws or regulations. You should not consider any information in this prospectus to be legal, business or tax advice. You should consult your own attorney, business advisor and tax advisor for legal, business and tax advice regarding an investment in the notes.

Neither the Securities and Exchange Commission (“SEC”) nor any state securities commission has approved or disapproved of these securities or determined if this prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

Glossary of Terms

The following is a list of frequently used terms, abbreviations or acronyms that are found in this prospectus.

Term | | Definition |

| 2016 Base Rate Order | | The order issued in March 2016 by the IURC authorizing AES Indiana to, among other things, increase its basic rates and charges by $30.8 million annually |

| 2018 Base Rate Order | | The order issued in October 2018 by the IURC authorizing AES Indiana to, among other things, increase its basic rates and charges by $43.9 million annually |

| 2024 IPALCO Notes | | $405 million of 3.70% IPALCO Enterprises, Inc. Senior Secured Notes due September 1, 2024 |

| 2030 IPALCO Notes | | $475 million of 4.25% IPALCO Enterprises, Inc. Senior Secured Notes due May 1, 2030 |

| 2034 IPALCO Notes | | $400 million of 5.75% IPALCO Enterprises, Inc. Senior Secured Notes due April 1, 2034 |

| $200 million Term Loan Agreement | | $200 million AES Indiana Term Loan Agreement, dated as of June 23, 2022 |

| $300 million Term Loan Agreement | | $300 million AES Indiana Term Loan Agreement, dated as of November 21, 2023 |

| ACE | | Affordable Clean Energy |

| AES | | The AES Corporation |

| AES Indiana | | Indianapolis Power & Light Company and its consolidated subsidiaries, which does business as AES Indiana |

| AES U.S. Investments | | AES U.S. Investments, Inc. |

| AFUDC | | Allowance for Funds Used During Construction |

| AOCI | | Accumulated Other Comprehensive Income |

| AOCL | | Accumulated Other Comprehensive Loss |

| ARO | | Asset Retirement Obligation |

| ASC | | Accounting Standards Codification |

| ASU | | Accounting Standards Update |

| BESS | | Battery Energy Storage System |

| BTA | | Best Technology Available |

| CAA | | U.S. Clean Air Act |

| CCGT | | Combined Cycle Gas Turbine |

| CCR | | Coal Combustion Residuals |

| CDPQ | | CDP Infrastructures Fund L.P., a wholly-owned subsidiary of La Caisse de dépôt et placement du Québec |

| CO2 | | Carbon Dioxide |

| COVID-19 | | The disease caused by the novel coronavirus that resulted in a global pandemic beginning in 2020 |

| CPCN | | Certificate of Public Convenience and Necessity |

| CPP | | Clean Power Plan |

| Credit Agreement | | $350 million AES Indiana Revolving Credit Facilities Second Amended and Restated Credit Agreement, dated as of December 22, 2022 |

| CSAPR | | Cross-State Air Pollution Rule |

| Cumulative Deficiencies | | Cumulative Net Operating Income Deficiencies. The Cumulative Deficiencies calculation provides that only five years’ worth of historical earnings deficiencies or surpluses are included, unless it has been greater than five years since the most recent rate case. |

| CWA | | U.S. Clean Water Act |

| D.C. Circuit | | U.S. Court of Appeals for the District of Columbia Circuit |

| Defined Benefit Pension Plan | | Employees’ Retirement Plan of AES Indiana |

| DOJ | | U.S. Department of Justice |

| DSM | | Demand Side Management |

| ECCRA | | Environmental Compliance Cost Recovery Adjustment |

| EDG | | Excess Distributed Generation |

Term | | Definition |

| EGUs | | Electrical Generating Units |

| ELG | | Effluent Limitation Guidelines |

| EPA | | U.S. Environmental Protection Agency |

| EPAct | | Energy Policy Act of 2005 |

| ERISA | | Employee Retirement Income Security Act of 1974 |

| EV | | Electric Vehicle |

| FAC | | Fuel Adjustment Clause |

| FASB | | Financial Accounting Standards Board |

| FERC | | Federal Energy Regulatory Commission |

| FGD | | Flue Gas Desulfurization |

| Financial Statements | | Audited and Unaudited Consolidated Financial Statements of IPALCO included herein |

| FIP | | Federal Implementation Plan |

| FTRs | | Financial Transmission Rights |

| GAAP | | Generally Accepted Accounting Principles in the United States |

| GHG | | Greenhouse Gas |

| Hardy Hills JV | | Hardy Hills JV, LLC |

| HLBV | | Hypothetical Liquidation Book Value |

| IBEW | | International Brotherhood of Electrical Workers |

| IDEM | | Indiana Department of Environmental Management |

| IOSHA | | Indiana Occupational Safety and Health Administration |

| IPALCO | | IPALCO Enterprises, Inc. and its consolidated subsidiaries |

| IPL | | Indianapolis Power & Light Company and its consolidated subsidiaries, which does business as AES Indiana |

| IRA | | Inflation Reduction Act of 2022 |

| IRP | | Integrated Resource Plan |

| ITC | | Investment Tax Credit |

| IURC | | Indiana Utility Regulatory Commission |

| kWh | | Kilowatt hours |

| MATS | | Mercury and Air Toxics Standards |

| Mid-America | | Mid-America Capital Resources, Inc. |

| MISO | | Midcontinent Independent System Operator, Inc. |

| MW | | Megawatts |

| MWh | | Megawatt hours |

| NAAQS | | National Ambient Air Quality Standards |

| NERC | | North American Electric Reliability Corporation |

| NOV | | Notice of Violation |

| NOx | | Nitrogen Oxide |

| NPDES | | National Pollutant Discharge Elimination System |

| NSPS | | New Source Performance Standards |

| NSR | | New Source Review |

| OUCC | | Indiana Office of Utility Consumer Counselor |

| Pension Plans | | Employees’ Retirement Plan of AES Indiana and Supplemental Retirement Plan of AES Indiana |

| PTC | | Production Tax Credit |

| PM2.5 | | Fine particulate matter or particulate matter with an aerodynamic diameter less than or equal to a nominal 2.5 micrometers |

| PSD | | Prevention of Significant Deterioration |

| RF | | ReliabilityFirst |

| RFP | | Request for Proposal |

| RSP | | AES Retirement Savings Plan |

| RTO | | Regional Transmission Organization |

| SEC | | United States Securities and Exchange Commission |

| Securities Act | | Securities Act of 1933, as Amended |

| Service Company | | AES US Services, LLC |

| SIP | | State Implementation Plan |

Term | | Definition |

| SO2 | | Sulfur Dioxide |

| SOFR | | Secured Overnight Financing Rate |

| Supplemental Retirement Plan | | Supplemental Retirement Plan of AES Indiana |

| TCJA | | Tax Cuts and Jobs Act |

| TDSIC | | Transmission, Distribution, and Storage System Improvement Charge |

| Third Amended and Restated Articles of Incorporation | | Third Amended and Restated Articles of Incorporation of IPALCO Enterprises, Inc. |

| Thrift Plan | | Employees’ Thrift Plan of AES Indiana |

| URT | | Utility Receipts Tax |

| U.S. | | United States of America |

| USD | | United States Dollars |

| VEBA | | Voluntary Employees’ Beneficiary Association |

| VIE | | Variable Interest Entity |

| WOTUS | | Waters of the U.S. |

Summary

This summary highlights information contained elsewhere in this prospectus. This summary may not contain all of the information that may be important to you. You should read this entire prospectus before making a decision to exchange your old notes for new notes, including the section entitled “Risk Factors” in this prospectus. Unless otherwise indicated or the context otherwise requires, the terms “IPALCO,” we,” “our,” “us,” and “the Company” refer to IPALCO Enterprises, Inc., including all of its subsidiaries, collectively. The term “IPALCO Enterprises, Inc.” refers only to IPALCO Enterprises, Inc., excluding its subsidiaries and affiliates

OUR COMPANY

IPALCO is a holding company incorporated under the laws of the state of Indiana whose principal subsidiary is Indianapolis Power & Light Company, which does business as AES Indiana. AES Indiana is a regulated electric utility operating in the state of Indiana. Substantially all of our business consists of the generation, transmission, distribution and sale of electric energy conducted through AES Indiana. Our business segments are “utility” and “all other.” All of our operations are conducted within the U.S. and principally within the state of Indiana. Please see Note 12, “Business Segments” to the audited Consolidated Financial Statements of IPALCO and related notes included elsewhere in this prospectus.

IPALCO owns all of the outstanding common stock of AES Indiana. AES Indiana was incorporated under the laws of the state of Indiana in 1926. AES Indiana is engaged primarily in generating, transmitting, distributing and selling electric energy to approximately 524,000 retail customers in the city of Indianapolis and neighboring areas within the state of Indiana. AES Indiana has an exclusive right to provide electric service to those customers. AES Indiana’s service area covers about 528 square miles with an estimated population of approximately 969,000. AES Indiana’s generation, transmission and distribution facilities, and changes to our sources of electric generation, are further described below under “Properties.” There have been no significant changes in the services rendered by AES Indiana during 2024.

AES Indiana is a transmission company member of RF. RF is one of eight Regional Reliability Councils under the NERC, which has been designated as the Electric Reliability Organization under the EPAct. RF seeks to preserve and enhance electric service reliability and security for the interconnected electric systems within the RF geographic area by setting and enforcing electric reliability standards. RF members cooperate under agreements to augment the reliability of its members’ electricity supply systems in the RF region through coordination of the planning and operation of the members’ generation and transmission facilities. Smaller electric utility systems, independent power producers and power marketers can participate as full members of RF.

Our principal executive offices are located at One Monument Circle, Indianapolis, Indiana 46204, and our telephone number is (317) 261-8261. Our website address is www.aesindiana.com. The information on our website is not incorporated by reference into this prospectus.

SUMMARY OF THE EXCHANGE OFFER

| Securities Offered | We are offering up to $400 million aggregate principal amount of our new 5.750% Senior Secured Notes due 2034, which will be registered under the Securities Act. |

| | |

| The Exchange Offer | We are offering to issue the new notes in exchange for a like principal amount of your old notes. We are offering to issue the new notes to satisfy our obligations contained in the registration rights agreement entered into when the old notes were sold in transactions permitted by Rule 144A and Regulation S under the Securities Act and therefore not registered with the SEC. For procedures for tendering, see “The Exchange Offer.” |

| | |

| Tenders, Expiration Date, Withdrawal | The exchange offer will expire at 5:00 p.m. New York City time on , 2024 unless it is extended. If you decide to exchange your old notes for new notes, you must acknowledge that you are not engaging in, and do not intend to engage in, a distribution of the new notes. If you decide to tender your old notes in the exchange offer, you may withdraw them at any time prior to , 2024. If we decide for any reason not to accept any old notes for exchange, your old notes will be returned to you without expense to you promptly after the exchange offer expires. You may only exchange old notes in denominations of $2,000 and integral multiples of $1,000 in excess thereof. |

| | |

| Federal Income Tax Consequences | Your exchange of old notes for new notes in the exchange offer will not result in any income, gain or loss to you for federal income tax purposes. See “Material United States Tax Consequences of the Exchange Offer.” |

| | |

| Use of Proceeds | We will not receive any proceeds from the issuance of the new notes in the exchange offer. |

| | |

| Exchange Agent | U.S. Bank Trust Company, National Association is the exchange agent for the exchange offer. |

| | |

| Failure to Tender Your Old Notes | If you fail to tender your old notes in the exchange offer, you will not have any further rights under the registration rights agreement, including any right to require us to register your old notes or to pay you additional interest or liquidated damages. All untendered old notes will continue to be subject to the restrictions on transfer set forth in the old notes and in the indenture. In general, the old notes may not be offered or sold, unless registered under the Securities Act, except pursuant to an exemption from, or in a transaction not subject to, the Securities Act and applicable state securities laws. We do not currently anticipate that we will register such untendered old notes under the Securities Act and, following this exchange offer, will be under no obligation to do so. |

| | |

You will be able to resell the new notes without registering them with the SEC if you meet the requirements described below.

Based on interpretations by the SEC’s staff in no-action letters issued to third parties, we believe that new notes issued in exchange for the old notes in the exchange offer may be offered for resale, resold or otherwise transferred by you without registering the new notes under the Securities Act or delivering a prospectus, unless you are a broker-dealer receiving securities for your own account, so long as:

| ● | you are not one of our “affiliates,” which is defined in Rule 405 of the Securities Act; |

| ● | you acquire the new notes in the ordinary course of your business; |

| ● | you do not have any arrangement or understanding with any person to participate in the distribution of the new notes; and |

| ● | you are not engaged in, and do not intend to engage in, a distribution of the new notes. |

If you are an affiliate of IPALCO Enterprises, Inc., or you are engaged in, intend to engage in or have any arrangement or understanding with respect to, the distribution of new notes acquired in the exchange offer, you (1) should not rely on our interpretations of the position of the SEC’s staff and (2) must comply with the registration and prospectus delivery requirements of the Securities Act in connection with any resale transaction.

If you are a broker-dealer and receive new notes for your own account in the exchange offer and/or in exchange for old notes that were acquired for your own account as a result of market-making or other trading activities:

| ● | you must represent that you do not have any arrangement or understanding with us or any of our affiliates to distribute the new notes; |

| ● | you must acknowledge that you will deliver a prospectus in connection with any resale of the new notes you receive from us in the exchange offer; and |

| ● | you may use this prospectus, as it may be amended or supplemented from time to time, in connection with the resale of new notes received in exchange for old notes acquired by you as a result of market-making or other trading activities. |

For a period of 90 days after the expiration of the exchange offer, we will make this prospectus available to any broker-dealer for use in connection with any resale described above.

SUMMARY DESCRIPTION OF THE NOTES

The terms of the new notes and the old notes are identical in all material respects, except that the new notes have been registered under the Securities Act, and the transfer restrictions and registrations rights relating to old notes do not apply to the new notes. The new notes will represent the same debt as the old notes and will be governed by the same indenture under which the old notes were issued.

| Issuer | | IPALCO Enterprises, Inc. |

| | | |

| Notes Offered | | $400 million aggregate principal amount of new 5.75% senior secured notes due 2034. |

| | | |

| Maturity | | April 1, 2034. |

| | | |

| Interest Payment Dates | | Interest will be payable semiannually on April 1 and October 1 of each year. |

| | | |

| Denominations | | Minimum denominations of $2,000 and integral multiples of $1,000 in excess thereof. |

| | | |

| Collateral | | The notes are secured by our pledge of all of the outstanding common stock of AES Indiana. The lien on the pledged shares will be shared equally and ratably with our existing senior secured notes, and, subject to certain limitations, we may secure other Indebtedness (as defined herein) equally and ratably with the notes. |

| | | |

| Ranking | | The notes will be secured and rank equally with our senior secured indebtedness secured by a pledge of the same assets. The notes will rank senior, to the extent of the assets securing such indebtedness, to our senior unsecured indebtedness and senior to our subordinated indebtedness. The notes will effectively rank junior to our subsidiaries’ liabilities. As of March 31, 2024: ● IPALCO had outstanding $1,280 million of senior secured indebtedness; and ● AES Indiana had total long-term debt and current liabilities of approximately $3,467 million. |

| | | |

| Optional Redemption | | We may redeem some or all of the notes at any time or from time to time at a redemption price as described under the caption “Description of Notes—Optional Redemption.” |

| | | |

| Change of Control | | When a Change of Control Triggering Event (as defined herein) occurs, each holder of notes may require us to repurchase all or a portion of its notes at a purchase price equal to 101% of the principal amount of the notes, plus accrued interest. See “Description of Notes—Repurchase at the Option of Holders.” |

| | | |

| Covenants | | The indenture governing the notes contains covenants that, among other things, will limit our ability and, in the case of restrictions on liens, the ability of our significant subsidiaries to: ● create certain liens on assets and properties; and ● consolidate or merge, or convey, transfer or lease all or substantially all of our consolidated properties and assets These covenants are subject to important exceptions and qualifications, which are described in “Description of Notes—Covenants.” The indenture does not restrict or prevent AES Indiana or any other subsidiary from incurring unsecured indebtedness. |

| | | |

| Book-Entry Form | | The notes will be issued in registered book-entry form represented by one or more global notes to be deposited with or on behalf of DTC or its nominee. Transfers of the notes will be effected only through the facilities of DTC. Beneficial interests in the global notes may not be exchanged for certificated notes except in limited circumstances. See “Description of Notes—Form, Denomination and Registration of Notes.” |

| | | |

| Further Issues | | We may from time to time, without notice to or the consent of the holders of the notes, create and issue additional debt securities under the indenture governing the notes having the same terms as, and ranking equally with, the notes in all respects (except for the offering price and issue date), as described more fully in “Description of Notes—Basic Terms of Notes.” |

| | | |

| Trustee, Registrar and Paying Agent | | U.S. Bank Trust Company, National Association |

| | | |

| Governing Law | | The indenture and the notes are governed by, and construed in accordance with, the laws of the State of New York. |

Risk Factors and Risk Factor Summary

If any of the following risks occur, our business, results of operations or financial condition could be materially adversely affected. You should also read the section captioned “Cautionary Note Regarding Forward-Looking Statements” for a discussion of what types of statements are forward-looking as well as the significance of such statements in the context of this prospectus. The risks described below are not the only ones we face. Additional risks of which we are not presently aware or that we currently believe are immaterial may also harm our business, results of operations or financial condition.

Risk Factor Summary

| ● | If you choose not to exchange your old notes in the exchange offer, the transfer restrictions currently applicable to your old notes will remain in force and the market price of your old notes could decline. |

| ● | You must follow the exchange offer procedures carefully in order to receive the new notes. |

| ● | There are state securities law restrictions on the resale of the new notes. |

| ● | The notes will be structurally subordinated to claims of creditors of our current and future subsidiaries. |

| ● | We may incur additional indebtedness, which may affect our financial health and our ability to repay the notes. |

| ● | We are a holding company and are dependent on AES Indiana for dividends to meet our debt service obligations. |

| ● | We may not be able to repurchase the notes upon a change of control triggering event. |

| ● | Redemptions may adversely affect your return on the notes. |

| ● | Regulatory considerations may affect the ability of the collateral agent to exercise certain rights with respect to the collateral securing the notes. |

| ● | Credit rating downgrades could adversely affect the trading price of the notes. |

| ● | Our electric generating facilities are subject to operational risks that at times result in unscheduled plant outages, unanticipated operation and/or maintenance expenses, increased fuel or purchased power costs and other liabilities, and these liabilities could become significant for which we may not have adequate insurance coverage. |

| ● | We may be negatively affected by a lack of growth or a decline in the number of customers or in customer usage. |

| ● | The cost of fuel and other commodities have experienced and could continue to experience volatility and we may not be able to hedge the entire exposure of our operations from availability and price volatility. In addition, until our coal units are converted or retired, a portion of our electricity is generated by coal. |

| ● | Catastrophic events could adversely affect our facilities, systems and operations. |

| ● | Our business is sensitive to weather and seasonal variations. |

| ● | Our membership in a RTO presents risks that could have a material adverse effect on our results of operations, financial condition and cash flows. |

| ● | Our transmission and distribution system is subject to operational, reliability and capacity risks. |

| ● | Current and future conditions in the economy may adversely affect our customers, suppliers and other counterparties in a way which could materially and adversely affect our results of operations, financial condition and cash flows. |

| ● | Economic conditions relating to the asset performance and interest rates of the Pension Plans could materially and adversely impact our results of operations, financial condition and cash flows. |

| ● | Counterparties providing materials or services may fail to perform their obligations, which could materially and adversely impact our results of operations, financial condition and cash flows. |

| ● | The COVID-19 pandemic, or the future outbreak of any other highly infectious or contagious diseases, could impact our business and operations. |

| ● | Failure to maintain an effective system of internal controls over financial reporting could result in material misstatements in our financial statements, the disallowance of cost recovery, or incorrect payment processing. |

| ● | If we are unable to maintain a qualified and properly motivated workforce, it could have a material adverse effect on our results of operations, financial condition and cash flows. |

| ● | We are subject to collective bargaining agreements that could adversely affect our business, results of operations, financial condition and cash flows. |

| ● | The use of non-derivative and derivative instruments in the normal course of business could result in losses that could materially and adversely impact our results of operations, financial position and cash flows. |

| ● | Potential security breaches (including cybersecurity breaches) and terrorism risks could materially and adversely affect our businesses. |

| ● | Failure or disruption in our information systems or those of businesses we rely on, or implementation of new processes and information systems could, if significant, interrupt our operations and adversely affect our business, results of operations, financial condition and cash flows in a material manner. |

| ● | We may not always be able to recover our costs to deliver electricity to our retail customers. The costs we can recover and the return on capital we are permitted to earn for certain aspects of our business are regulated and governed by the laws of Indiana and the rules, policies and procedures of the IURC. |

| ● | Concerns about GHG emissions and the potential risks associated with climate change have led to increased regulation and other actions that could impact our business. |

| ● | We are subject to numerous environmental laws, rules and regulations that require capital expenditures, increase our cost of operations, may expose us to environmental liabilities or make continued operation of certain generating units unprofitable. |

| ● | If we were found not to be in compliance with the mandatory reliability standards, we could be subject to sanctions, including substantial monetary penalties, which likely would not be recoverable from customers through regulated rates. |

| ● | We are subject to extensive laws and local, state and federal regulation, as well as litigation and other proceedings that affect our operations and costs. |

| ● | Tax legislation initiatives or challenges to our tax positions could adversely affect our results of operations and financial condition. |

| ● | We rely on access to the financial markets. General economic conditions and disruptions in the financial markets could adversely affect our ability to raise capital on favorable terms or at all, and cause increases in our interest expense. |

| ● | The level of our indebtedness, and the security provided for this indebtedness, could adversely affect our financial flexibility. |

| ● | IPALCO is a holding company and parent of AES Indiana and other subsidiaries. IPALCO’s cash flow is dependent on operating cash flows of AES Indiana and its ability to pay cash to IPALCO. |

| ● | Our ownership by AES subjects us to potential risks that are beyond our control. |

RISK FACTORS

Risks Related to the Exchange Offer

If you choose not to exchange your old notes in the exchange offer, the transfer restrictions currently applicable to your old notes will remain in force and the market price of your old notes could decline.

If you do not exchange your old notes for new notes in the exchange offer, then you will continue to be subject to the transfer restrictions on the old notes as set forth in the offering memorandum distributed in connection with the private offering of the old notes. In general, the old notes may not be offered or sold unless they are registered or exempt from registration under the Securities Act and applicable state securities laws. Except as required by the registration rights agreement entered into in connection with the private offering of the old notes, we do not intend to register resales of the old notes under the Securities Act. The tender of old notes under the exchange offer will reduce the principal amount of the old notes outstanding, which may have an adverse effect upon, and increase the volatility of, the market price of the old notes due to reduction in liquidity.

You must follow the exchange offer procedures carefully in order to receive the new notes.

If you do not follow the procedures described in this prospectus, you will not receive any new notes. If you want to tender your old notes in exchange for new notes, you will need to contact a DTC participant to complete the book-entry transfer procedures, as described under “The Exchange Offer,” prior to the expiration date, and you should allow sufficient time to ensure timely completion of these procedures to ensure delivery. No one is under any obligation to give you notification of defects or irregularities with respect to tenders of old notes for exchange. For additional information, see the section captioned “The Exchange Offer” in this prospectus.

There are state securities law restrictions on the resale of the new notes.

In order to comply with the securities laws of certain jurisdictions, the new notes may not be offered or resold by any holder, unless they have been registered or qualified for sale in such jurisdictions or an exemption from registration or qualification is available and the requirements of such exemption have been satisfied. We currently do not intend to register or qualify the resale of the new notes in any such jurisdictions. However, generally an exemption is available for sales to registered broker-dealers and certain institutional buyers. Other exemptions under applicable state securities laws also may be available.

Risks Related to the Notes

The notes will be structurally subordinated to claims of creditors of our current and future subsidiaries.

The notes will be structurally subordinated to indebtedness and other liabilities of our subsidiaries, including AES Indiana. Our subsidiaries may also incur additional indebtedness in the future. Any right that we have to receive any assets of any of our subsidiaries upon the liquidation or reorganization of those subsidiaries, and the consequent rights of holders of the notes to realize proceeds from the sale of any of those subsidiaries’ assets, will be effectively subordinated to the claims of those subsidiaries’ creditors, including trade creditors and holders of preferred equity interests of those subsidiaries. Accordingly, in the event of a bankruptcy, liquidation or reorganization of any of our subsidiaries, these subsidiaries will pay the holders of their debts, holders of their preferred equity interests and their trade creditors before they will be able to distribute any of their assets to us. The security interest in the common stock of AES Indiana pledged by us to secure the notes will not alter the effective subordination of the notes to the creditors of our subsidiaries.

We may incur additional indebtedness, which may affect our financial health and our ability to repay the notes.

As of March 31, 2024, we had on a consolidated basis $4,321.3 million of indebtedness and total common shareholders’ equity of $1,074.3 million. Our indebtedness includes $1,280.0 million aggregate principal of senior secured notes. AES Indiana had $2,769.2 million of First Mortgage Bonds outstanding as of March 31, 2024, which are secured by the pledge of substantially all of the assets of AES Indiana under the terms of AES Indiana’s mortgage and deed of trust. The indenture governing the notes does not restrict AES Indiana’s or any of our subsidiaries’ ability to incur unsecured indebtedness. As of March 31, 2024, AES Indiana had $195.0 million outstanding borrowings under its $350 million revolving Credit Agreement. This level of indebtedness and related security could have important consequences, including the following:

| ● | increasing our vulnerability to general adverse economic and industry conditions; |

| ● | requiring us to dedicate a substantial portion of our cash flow from operations to make payments on our indebtedness, thereby reducing the availability of our cash flow to fund other corporate purposes; |

| ● | limiting our flexibility in planning for, or reacting to, changes in our business and the industry in which we operate; and |

| ● | limiting, along with the financial and other restrictive covenants in our indebtedness, our ability to borrow additional funds, as needed. |

We expect to incur additional debt in the future, subject to the terms of our debt agreements and regulatory approvals for any AES Indiana debt. To the extent we or AES Indiana become more leveraged, the risks described above would increase. Further, actual cash requirements in the future may be greater than expected. Accordingly, our cash flow from operations may not be sufficient to repay at maturity all of the outstanding debt as it becomes due and, in that event, we may not be able to borrow money, sell assets or otherwise raise funds on acceptable terms or at all to refinance our debt as it becomes due.

We are a holding company and are dependent on AES Indiana for dividends to meet our debt service obligations.

We are a holding company with no material assets other than the common stock of our subsidiaries, and accordingly substantially all cash is generated by the operating activities of our subsidiaries, principally AES Indiana. None of our subsidiaries, including AES Indiana, is obligated to make any payments with respect to the notes, and none of our subsidiaries will guarantee the notes; however, the common stock of AES Indiana is pledged to secure payment of these notes. Accordingly, our ability to make payments on the notes is dependent not only on the ability of our subsidiaries to generate cash in the future, but also on the ability of our subsidiaries to distribute cash to us. AES Indiana’s mortgage and deed of trust, its amended articles of incorporation and its Credit Agreement contain restrictions on AES Indiana’s ability to issue certain securities or pay cash dividends to us under certain circumstances.

We may not be able to repurchase the notes upon a change of control triggering event.

Upon the occurrence of specific kinds of change of control triggering events, we will be required to offer to repurchase all outstanding notes at 101% of their principal amount plus accrued and unpaid interest (see “Description of Notes-Repurchase at the Option of Holders”). The source of funds for any such purchase of the notes will be our available cash or cash generated from our subsidiaries’ operations or other sources, including borrowings, sales of assets or sales of equity. We may not be able to satisfy our obligations to repurchase the notes upon a change of control triggering event because we may not have sufficient financial resources to purchase all of the notes that are tendered upon a change of control triggering event.

Redemptions may adversely affect your return on the notes.

The notes are redeemable at our option, and therefore we may choose to redeem the notes at times when the prevailing interest rates are relatively low. As a result, you may not be able to reinvest the proceeds you receive from the redemption in a comparable security at an effective interest rate as high as the interest rate on your notes being redeemed.

Regulatory considerations may affect the ability of the collateral agent to exercise certain rights with respect to the collateral securing the notes.

Regulatory considerations may affect the ability of the collateral agent to exercise certain rights with respect to the common stock of AES Indiana pledged by us to secure the notes upon the occurrence of an event of default under the indenture governing the notes. Because AES Indiana is a regulated public utility, foreclosure proceedings and the enforcement of the pledge agreement and the right to take other actions with respect to the pledged shares of AES Indiana common stock may be limited and subject to regulatory approval. AES Indiana is subject to regulation at the state level by the IURC. At the federal level, it is subject to regulation by the FERC. See “Business—Regulation.” Regulation by the IURC and FERC includes regulation with respect to the change of control, transfer or ownership of utility property. In particular, foreclosure proceedings and the enforcement of the pledge agreement and the right to take other actions with respect to the pledged shares of AES Indiana common stock would require (i) FERC approval to the extent such actions resulted in a change in control or a transfer of the ownership of the pledged shares of AES Indiana common stock and (ii) IURC approval to the extent such actions resulted in a transfer of the ownership of the pledged shares of AES Indiana common stock to another Indiana utility. There can be no assurance that any such regulatory approval can be obtained on a timely basis, or at all.

Credit rating downgrades could adversely affect the trading price of the notes.

The trading price for the notes may be affected by our credit rating, and our credit rating may be affected by the credit rating of AES. Credit ratings are continually revised and there can be no assurance that our current credit rating or the current credit rating of AES will remain the same for any given period of time or that such ratings will not be downgraded or withdrawn entirely by a rating agency if, in that rating agency’s judgment, future circumstances relating to the basis of the rating, such as adverse changes, so warrant. Any downgrade in, or withdrawal of, our credit rating or the credit rating of AES could adversely affect the trading price of the notes or the trading markets for the notes to the extent trading markets for the notes develop. Credit ratings are not recommendations to purchase, hold or sell the notes. Additionally, credit ratings may not reflect the potential effect of risks related to the structure or marketing of the notes. One rating agency’s rating should be evaluated independently of any other rating agency’s rating.

Risks Associated with Our Operations

Our electric generating facilities are subject to operational risks that at times result in unscheduled plant outages, unanticipated operation and/or maintenance expenses, increased fuel or purchased power costs and other liabilities, and these liabilities could become significant for which we may not have adequate insurance coverage.

We operate generating facilities, including those using coal, oil, natural gas, and renewable energy, which involve certain risks that can adversely affect energy costs, output and efficiency levels. These risks include:

| ● | unit or facility shutdowns due to a breakdown or failure of equipment or processes; |

| ● | increased prices for fuel and fuel transportation as existing contracts expire or as such contracts are adjusted through price re-opener provisions or automatic adjustments; |

| ● | disruptions in the availability or delivery of fuel and lack of adequate inventories; |

| ● | shortages of or delays in obtaining equipment; |

| ● | loss of cost-effective disposal options for solid waste generated by the facilities; |

| ● | reliability of our suppliers; |

| ● | inability to comply with regulatory or permit requirements; |

| ● | operational restrictions resulting from environmental or permit limitations or governmental interventions; |

| ● | construction delays and cost overruns; |

| ● | disruptions in the delivery of electricity; |

| ● | labor disputes or work stoppages by employees; |

| ● | the availability of qualified personnel; |

| ● | events occurring on third party systems that interconnect to and affect our system; |

We experience unscheduled plant outages, unanticipated operation and/or maintenance expenses, increased capital expenditures and/or increased fuel and purchased power costs from time to time, any of which could have a material adverse effect on our results of operations, financial condition and cash flows. These risks are partially mitigated by our ability to generally pass fuel and purchased power costs through to customers through the FAC. If unexpected plant outages occur frequently and/or for extended periods of time, this could result in adverse regulatory action that may have a significant impact on our results of operations, financial condition and cash flows.

Additionally, as a result of the above risks and other potential hazards associated with the power generation industry, we may from time to time become exposed to significant liabilities for which we may not have adequate insurance coverage. Power generation involves hazardous activities, including acquiring, transporting and unloading fuel, operating large pieces of rotating equipment and delivering electricity to transmission and distribution systems. The control and management of these risks depend upon adequate development and training of personnel and on the existence of operational procedures, preventative maintenance plans and specific programs supported by quality control systems which reduce, but do not eliminate, the possibility of the occurrence and impact of these risks.

The hazardous activities described above can also cause personal injury or loss of life, damage to and destruction of property, plant and equipment, contamination of, or damage to, the environment and suspension of operations. The occurrence of any one of these events results in us from time to time being named as a defendant in lawsuits asserting claims for damages, environmental cleanup costs, personal injury and fines and/or penalties. We maintain an amount of insurance protection that we believe is adequate, but there can be no assurance that our insurance will be sufficient or effective under all circumstances and against all hazards or liabilities to which we may be subject. A successful claim that is significant for which we are not fully insured could adversely and materially affect our results of operations, financial condition and cash flows. In addition, except for our large substations, transmission and distribution assets are not covered by insurance and are considered to be outside the scope of property insurance. Further, due to rising insurance costs and changes in the insurance markets, we cannot provide assurance that insurance coverage will continue to be available on terms similar to those presently available to us or at all. Any such losses not covered by insurance could have a material adverse effect on our financial condition, results of operations and cash flows.

We may be negatively affected by a lack of growth or a decline in the number of customers or in customer usage.

Customer growth and customer usage are affected by a number of factors outside our control, such as energy efficiency and DSM measures, population changes, job and income growth, housing starts, new business formation and the overall level of economic activity. A significant lack of growth, or a decline, in the number of customers in our service territory or in customer demand for electricity could have a material adverse effect on our results of operations, financial condition and cash flows and may cause us to fail to fully realize anticipated benefits from investments and expenditures.

The cost of fuel and other commodities have experienced and could continue to experience volatility and we may not be able to hedge the entire exposure of our operations from availability and price volatility. In addition, until our coal units are converted or retired, a portion of our electricity is generated by coal.

Our business is sensitive to changes in the price of natural gas, coal, purchased power and emissions allowances. In addition, changes in the prices of steel, copper and other raw materials can have a significant impact on our costs. We also are dependent on purchased power, in part, to meet our seasonal planning reserve margins. Any changes in fuel prices could affect the prices we charge, our operating costs and our competitive position with respect to our products and services. The cost of fuel and other commodities has been volatile in recent years and we expect that volatility to continue.

Our exposure to fluctuations in the price of fuel is limited because, pursuant to Indiana law, we apply to the IURC for a change in our FAC every three months to recover our estimated fuel costs, which may be above or below the levels included in our basic rates and charges. In addition, we apply to recover the energy portion of our purchased power costs in these quarterly FAC proceedings subject to a benchmark (please see Note 2, “Regulatory Matters—FAC and Authorized Annual Jurisdictional Net Operating Income” to the consolidated financial statements and related notes included elsewhere in this prospectus for additional details regarding the benchmark and the process to recover fuel costs). As part of this cost-recovery process, we must present evidence in each proceeding that we have made every reasonable effort to acquire fuel and generate or purchase power or both so as to provide electricity to our retail customers at the lowest fuel cost reasonably possible. If we are unable to timely or fully recover our fuel and purchased power costs, it could have a material adverse effect on our results of operations, financial condition and cash flows.

Approximately 36% of the energy we produced in 2023 was generated by coal as compared to approximately 58% and 72% in 2022 and 2021, respectively. As of December 31, 2023, while we had approximately 83% in total of our current coal requirements for the two-year period ending December 31, 2025 under long-term contracts, the balance was yet to be purchased and would be purchased under a combination of long-term contracts, short-term contracts and on the spot market. Prices can be highly volatile in both the short-term market and on the spot market. The coal market has experienced price volatility in the last several years. We are now in a global market for coal in which our domestic price is increasingly affected by international supply disruptions and demand balance. Coal exports from the U.S. have increased significantly at times in recent years. In addition, domestic developments such as government-imposed direct costs and permitting issues that affect mining costs and supply availability, and the variable demand of retail customer load and the performance of our generation fleet have an impact on our fuel procurement operations. In addition, pricing provisions in some of our coal contracts with terms of one year or more allow for price changes under certain circumstances.

Because of our dependence on coal to meet customer demand for electricity, our business and operations could be materially adversely affected by unexpected price volatility in the coal market, price increases pursuant to the provisions of certain of our long-term coal contracts, and the continued regulatory and political scrutiny of coal. As discussed below, regulators, politicians and non-governmental organizations have expressed concern about GHG emissions and are taking actions which, in addition to the potential physical risk associated with climate change, could have a material adverse impact on our results of operations, financial condition and cash flows. Our dependence on coal also means that the output of our coal-fired generation units can be greatly affected by the costs of other fuels combusted by generation facilities that compete with our coal-fired generation units. Until 2021, natural gas prices over the last several years have been relatively low and some gas-fired generators that previously were primarily used during periods of peak and intermediate electric demand have run even during periods of relatively low demand. This can cause many coal-fired generators, including ours, to run fewer hours during these periods of base-load demand. The cyclical nature of commodity markets makes this a possibility in the future, however, we would expect any retirement of our coal-fired generators to reduce the potential impact of these events due to lower volumes of coal in our generation fleet.

In addition, substantially all of our coal supply is currently mined in the state of Indiana, and all of our coal supply is currently mined by unaffiliated suppliers or third parties. Our current goal is to carry a 25-50 day system supply of coal to offset unforeseen occurrences such as equipment breakdowns and transportation or mine delays. AES Indiana typically has long-term contracts with a small number of suppliers of coal. In recent years, the coal industry has undergone significant restructuring as a result of debt restructurings, bankruptcy proceedings and other factors. Further restructuring may result in a failure of our suppliers to fulfill their contractual obligations or fewer suppliers and, consequently, increased dependency on any one supplier. Any significant disruption in the ability of our suppliers, particularly our most significant suppliers, to mine or deliver coal or other fuel, or any failure on the part of our suppliers to fulfill their contractual obligations could have a material adverse effect on our business. In the event of disruptions or failures, there can be no assurance that we would be able to find another supplier of fuel on similarly favorable terms, which could also limit our ability to recover fuel costs through the FAC proceedings.

Catastrophic events could adversely affect our facilities, systems and operations.

Catastrophic events such as fires, explosions, cyber-attacks, terrorist acts, acts of war, acts of sabotage or vandalism, pandemic events, or natural disasters such as floods, earthquakes, tornadoes, severe winds, ice or snow storms, droughts or other similar occurrences could adversely affect our generation facilities, transmission and distribution systems, results of operations, financial condition and cash flows. Our Petersburg Plant, which is our largest source of generating capacity, is located in the Wabash Valley seismic zone, adjacent to the New Madrid seismic zone, which are both areas of significant seismic activity in the central U.S.

Our business is sensitive to weather and seasonal variations.

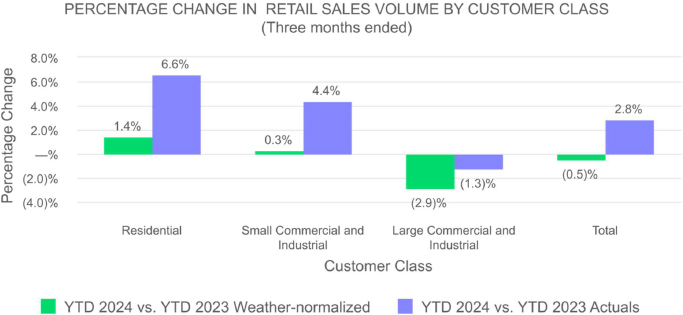

Weather conditions significantly affect the demand for electric power, and accordingly, our business is affected by variations in general weather conditions and unusually severe weather. As a result of these factors, our operating revenue and associated operating expenses are not generated evenly by month during the year. We forecast electric sales on the basis of normal weather, which represents a long-term historical average. Significant variations from normal weather (such as warmer winters and cooler summers) could have a material impact on our revenue, operating income and net income and cash flows. In addition, severe or unusual weather, such as floods, tornadoes and ice or snow storms, may cause outages and property damage that may require us to incur additional costs that may not be insured or recoverable from customers. While we are permitted to seek recovery of certain severe storm damage costs, if we are unable to fully recover such costs in a timely manner, it could have a material adverse effect on our results of operations, financial condition and cash flows.

Our membership in a RTO presents risks that could have a material adverse effect on our results of operations, financial condition and cash flows.

We are a member of MISO, a FERC-regulated RTO. MISO serves the electrical transmission needs of a 15-state area including much of the Mid-U.S. and Canada and maintains functional operational control over our electric transmission facilities, as well as that of the other utility members of MISO. We retain control over our distribution facilities. As a result of membership in MISO and its operational control, our continued ability to import power, when necessary, and export power to the wholesale market has been, and may continue to be, impacted. We offer our generation and bid our load into this market on a day-ahead basis and settle differences in real time. Given the nature of MISO’s policies regarding use of transmission facilities, and its administration of the energy and ancillary services markets, it is difficult to predict near-term operational impacts. We cannot assure MISO’s reliable operation of the regional transmission system, or the impact of its operation of the energy and ancillary services markets.

The rules governing the various regional power markets may also change from time to time which could affect our costs and revenue and have a material adverse effect on our results of operations, financial condition and cash flows. We may expand or otherwise change our transmission system according to decisions made by MISO in addition to our internal planning process. In addition, various proposals and proceedings before the FERC relating to MISO or otherwise may cause transmission rates to change from time to time. We also incur fees and costs to participate in MISO.

To the extent that we rely, at least in part, on the performance of MISO to maintain the reliability of our transmission system, it puts us at some risk for the performance of MISO. In addition, actions taken by MISO to secure the reliable operation of the entire transmission system operated by MISO could result in voltage reductions, rolling blackouts, or sustained system-wide blackouts on AES Indiana’s transmission and distribution system, any of which could have a material adverse effect on our results of operations, financial condition and cash flows.

Our transmission and distribution system is subject to operational, reliability and capacity risks.

The ongoing reliable performance of our transmission and distribution system is subject to risks due to, among other things, weather damage, intentional or unintentional damage, equipment or process failure, catastrophic events, such as fires and/or explosions, facility outages, labor disputes, accidents or injuries, operator error, or inoperability of key infrastructure internal or external to us and events occurring on third party systems that interconnect to and affect our system. The failure of our transmission and distribution system to fully operate and deliver the energy demanded by customers could have a material adverse effect on our results of operations, financial condition and cash flows, and if such failures occur frequently and/or for extended periods of time, could result in adverse regulatory action. In addition, the advent and quick adaptation of new products and services that require increased levels of electrical energy cannot be predicted and could result in insufficient transmission and distribution system capacity. As with all utilities, potential concern with the adequacy of transmission capacity on AES Indiana’s system or the regional systems operated by MISO could result in MISO, the NERC, the FERC or the IURC requiring us to upgrade or expand our transmission system through additional capital expenditures or share in the costs of regional expansion. Also, as a result of the above risks and other potential risks and hazards associated with transmission and distribution operations, we may from time to time become exposed to significant liabilities for which we may not have adequate insurance coverage. Except for AES Indiana’s large substations, transmission and distribution assets are not covered by insurance and are considered to be outside the scope of property insurance. Otherwise, we maintain an amount of insurance protection that we believe is adequate, but there can be no assurance that our insurance will be sufficient or effective under all circumstances and against all hazards or liabilities to which we may be subject. Further, any increased costs or adverse changes in the insurance markets may cause delays or inability in maintaining insurance coverage on terms similar to those presently available to us or at all. A successful claim for which we are not fully insured could have an adverse impact on our results of operations, financial condition and cash flows.

Current and future conditions in the economy may adversely affect our customers, suppliers and other counterparties in a way which could materially and adversely affect our results of operations, financial condition and cash flows.

Our business, results of operations, financial condition and cash flows have been and will continue to be affected by general economic conditions. Slowing economic growth, credit market conditions, fluctuating consumer and business confidence, fluctuating commodity prices, and other challenges affecting the general economy, have caused and may continue to cause some of our customers to experience deterioration of their businesses, cash flow shortages, and difficulty obtaining financing. As a result, existing customers may reduce their electricity consumption and may not be able to fulfill their payment obligations to us in the normal, timely fashion. In addition, some existing commercial and industrial customers may discontinue their operations. Sustained downturns, recessions or a sluggish economy generally affect the markets in which we operate and negatively influence our energy operations. A contracting, slow or sluggish economy could reduce the demand for energy in areas in which we are doing business. For example, during economic downturns, our commercial and industrial customers may see a decrease in demand for their products, which in turn may lead to a decrease in the amount of energy they require. Furthermore, projects which may result in potential new customers may be delayed until economic conditions improve. Some of our suppliers, customers and other counterparties, and others with whom we transact business experience financial difficulties, which may impact their ability to fulfill their obligations to us. For example, our counterparties on forward purchase contracts and financial institutions involved in our credit facility may become unable to fulfill their contractual obligations to us or result in their declaring bankruptcy or similar insolvency-like proceedings. We may not be able to enter into replacement agreements on terms as favorable as our existing agreements. Reduced demand for our electric services, failure by our customers to timely remit full payment owed to us and supply delays or unavailability could have a material adverse effect on our results of operations, financial condition and cash flows. In particular, the projected economic growth and total employment in Indianapolis are important to the realization of our forecasts for annual energy sales.

Economic conditions relating to the asset performance and interest rates of the Pension Plans could materially and adversely impact our results of operations, financial condition and cash flows.

Pension costs are based upon a number of actuarial assumptions, including an expected long-term rate of return on pension plan assets, level of employer contributions, the expected life span of pension plan beneficiaries and the discount rate used to determine the present value of future pension obligations. Any of these assumptions could prove to be wrong, resulting in a shortfall of our Pension Plans’ assets compared to pension obligations under the Pension Plans. Further, the performance of the capital markets affects the values of the assets that are held in trust to satisfy future obligations under the Pension Plans. These assets are subject to market fluctuations and will yield uncertain returns, which may fall below our projected return rates. A decline in the market value of the Pension Plans’ assets will increase the funding requirements under the Pension Plans if the actual asset returns do not recover these declines in value in the foreseeable future. Future pension funding requirements, and the timing of funding payments, may also be subject to changes in legislation. We are responsible for funding any shortfall of our Pension Plans’ assets compared to obligations under the Pension Plans, and a significant increase in our pension liabilities could materially and adversely impact our results of operations, financial condition, and cash flows. We are subject to the Pension Protection Act of 2006, which requires underfunded pension plans to improve their funding ratios within prescribed intervals based on the level of their underfunding. As a result, our required contributions to these plans, at times, have increased and may increase in the future. In addition, our pension and postemployment benefit plan liabilities are sensitive to changes in interest rates. If interest rates decrease, the discounted liabilities increase benefit expense and funding requirements. Further, changes in demographics, including increased numbers of retirements or changes in life expectancy assumptions, may also increase the funding requirements for the obligations related to the pension and other postemployment benefit plans. Declines in market values and increased funding requirements could have a material adverse effect on our results of operations, financial condition and cash flows. Please see Note 8, “Benefit Plans” to the audited Consolidated Financial Statements of IPALCO and related notes included elsewhere in this prospectus for further discussion.

Counterparties providing materials or services may fail to perform their obligations, which could materially and adversely impact our results of operations, financial condition and cash flows.

We enter into transactions with and rely on many counterparties in connection with our business, including for the purchase and delivery of inventory, including fuel and equipment components, for our capital improvements and additions and to provide professional services, such as actuarial calculations, payroll processing and various consulting services. If any of these counterparties fails to perform its obligations to us or becomes unavailable, our business plans may be materially disrupted, we may be forced to discontinue or delay certain operations if a cost-effective alternative is not readily available or we may be forced to enter into alternative arrangements at then-current market prices that may exceed our contractual prices and cause delays. Although our agreements are designed to mitigate the consequences of a potential default by the counterparty, our actual exposure may be greater than the relief provided by these mitigation provisions. Any of the foregoing could result in regulatory actions, cost overruns, delays or other losses, any of which (or a combination of which) could have a material adverse effect on our results of operations, financial condition and cash flows.

Further, our construction program calls for extensive expenditures for capital improvements and additions, including the installation of environmental upgrades, improvements to and replacements of generation, transmission and distribution facilities, as well as other initiatives. As a result, we have engaged, and will continue to engage, numerous contractors and have entered into a number of agreements to acquire the necessary materials and/or obtain the required construction related services. In addition, some contracts provide for us to assume the risk of price escalation and availability of certain metals and key components. This could force us to enter into alternative arrangements at then-current market prices that may exceed our contractual prices or cause construction delays in a significant manner. It could also subject us to enforcement action by regulatory authorities to the extent that such a contractor failure resulted in a failure by AES Indiana to comply with requirements or expectations, particularly with regard to the cost of the project. As a result of these events, we might incur losses or delays in completing construction.

The COVID-19 pandemic, or the future outbreak of any other highly infectious or contagious diseases, could impact our business and operations.

The COVID-19 pandemic has impacted global economic activity, caused significant volatility and negative pressure in financial markets and reduced the demand for energy in our service territory in recent years. In addition to reduced revenue and lower margins resulting from decreased energy demand within our service territory, we also have incurred expenses relating to COVID-19, including expenses relating to events outside of our control. In addition to contributing to economic slowdown or a recession, COVID-19 or another pandemic could have material and adverse effects on our results of operations, financial condition and cash flows due to, among other factors:

| ● | further decline in customer demand as a result of general decline in business activity; |

| ● | further destabilization of the markets and decline in business activity negatively impacting our customer growth or the number of customers in our service territory as well as our customers’ ability to pay for our services when due (or at all); |

| ● | delay or inability in obtaining regulatory actions and outcomes that could be material to our business, including for recovery of COVID-19 related expenses and losses, such as uncollectible customer amounts, and the review and approval of our applications, rates and charges by the IURC; |

| ● | difficulty accessing the capital and credit markets on favorable terms, or at all, a disruption and instability in the global financial markets, or deteriorations in credit and financing conditions which could affect our access to capital necessary to fund business operations or address maturing liabilities on a timely basis; |

| ● | negative impacts on the health of our essential personnel, especially if a significant number of them are affected, and on our operations as a result of implementing stay-at-home, quarantine and other social distancing measures; |

| ● | a deterioration in our ability to ensure business continuity during a disruption, including increased cybersecurity attacks related to the work-from-home environment; |

| ● | delays or inability to access, transport and deliver fuel or other materials to our facilities due to restrictions on business operations or other factors affecting us and our third-party suppliers; |

| ● | the inability to hedge sufficient exposure of our operations from availability and cost of fuel and other commodities that experience significant volatility; |

| ● | delays or inability to access equipment or the availability of personnel to perform planned and unplanned maintenance, which can, in turn, lead to disruption in operations; |

| ● | delays or inability in achieving our financial goals, growth strategy and digital transformation; and |

| ● | delays in the implementation of expected rules and regulations. |

The impact of the COVID-19 pandemic also depends on factors, including the effectiveness and timing of updated vaccines to address new variants, the development of more virulent COVID-19 variants as well as third-party actions taken to contain its spread and mitigate its public health effects. A resurgence or material worsening of the COVID-19 pandemic could present material uncertainty which could materially and adversely affect our generation facilities, transmission and distribution systems, results of operations, financial condition and cash flows. To the extent COVID-19 adversely affects our business and financial results, it may also have the effect of heightening many of the other risks described in this “Risk Factors” section, such as those relating to our level of indebtedness, our need to generate sufficient cash flows to service our indebtedness and our ability to comply with the covenants contained in the agreements that govern our indebtedness.

Failure to maintain an effective system of internal controls over financial reporting could result in material misstatements in our financial statements, the disallowance of cost recovery, or incorrect payment processing.

Our internal controls, accounting policies and practices and internal information systems are designed to enable us to capture and process transactions and information in a timely and accurate manner in compliance with GAAP, laws and regulations, taxation requirements and federal securities laws and regulations in order to, among other things, disclose and report financial and other information in connection with the recovery of our costs and with our reporting requirements under federal securities, tax and other laws and regulations and to properly process payments. We have also implemented corporate governance, internal control and accounting policies and procedures in connection with the Sarbanes-Oxley Act of 2002. Our internal controls and policies have been and continue to be closely monitored by management and our Board of Directors. While we believe these controls, policies, practices and systems are adequate to verify data integrity, the identification of significant deficiencies or material weaknesses in our internal controls that we cannot remediate in a timely manner could lead to undetected errors that could result in material misstatements in our financial statements, the disallowance of cost recovery, or incorrect payment processing. The consequences of these events could have a material adverse effect on our results of operations, financial condition and cash flows.

We have identified a material weakness in our internal control over financial reporting that resulted from the design and operation of information technology general controls. While we believe that this material weakness did not result in a material misstatement of our financial statements, this control deficiency was not remediated as of December 31, 2023. Since there is a reasonable possibility that the control deficiency could result in a material misstatement in our financial statements that would not be detected, we determined that this control deficiency constituted a material weakness. While we have taken steps to implement a remediation plan, the material weakness will not be considered remediated until the enhanced controls operate for a sufficient period of time and management has concluded, through testing, that the related controls are effective. Furthermore, we can give no assurance that the measures we take will remediate the material weakness. We can give no assurance that additional material weaknesses will not arise in the future. Any failure to remediate the material weakness, or the development of new material weaknesses in our internal control over financial reporting, could result in material misstatements in our financial statements and cause us to fail to meet our reporting and financial obligations.

If we are unable to maintain a qualified and properly motivated workforce, it could have a material adverse effect on our results of operations, financial condition and cash flows.