UNITED STATES SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

S ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d)

OF THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended December 31, 2010

OR

o TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d)

OF THE SECURITIES EXCHANGE ACT OF 1934

For the transition period from to

Commission file number 1-11533

Parkway Properties, Inc.

(Exact name of registrant as specified in its charter)

| Maryland | 74-2123597 |

| (State or other jurisdiction | (I.R.S. Employer |

| of incorporation or organization) | Identification No.) |

One Jackson Place Suite 1000

188 East Capitol Street

Jackson, Mississippi 39201

(Address of principal executive offices) (Zip Code)

Registrant's telephone number: (601) 948-4091

Registrant's website: www.pky.com

Securities registered pursuant to Section 12(b) of the Act:

Common Stock, $.001 Par Value

8.00% Series D Cumulative Redeemable Preferred Stock $.001 Par Value

New York Stock Exchange

Securities registered pursuant to Section 12(g) of the Act:

None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. o Yes S No

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act.

o Yes S No

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. S Yes o No

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files).

Yes o No o* (*Registrant is not subject to the requirements of Rule 405 of Regulation S-T at this time.)

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant's knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. S

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer or a smaller reporting company. See definition of “large accelerated filer” in Rule 12b-2 of the Exchange Act. (Check one):

Large accelerated filer o Accelerated filer S Non-accelerated filer o Smaller reporting company o (do not check if a smaller reporting company)

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act).

o Yes S No

The aggregate market value of the voting and non-voting common equity held by non-affiliates computed by reference to the price at which the common equity was last sold, or the average bid and asked price of such common equity, at June 30, 2010 was $301.8 million.

The number of shares outstanding in the registrant's class of common stock at March 1, 2011 was 21,962,564.

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the Registrant's Proxy Statement for the 2011 Annual Meeting of Shareholders are incorporated by reference into Part III.

PARKWAY PROPERTIES, INC.

TABLE OF CONTENTS

| | | Page |

| | | |

| PART I. | | |

| Item 1. | Business | 3 |

| Item 1A. | Risk Factors | 6 |

| Item 1B. | Unresolved Staff Comments | 12 |

| Item 2. | Properties | 12 |

| Item 3. | Legal Proceedings | 17 |

| Item 4. | [Removed and Reserved] | 18 |

| | | |

| PART II. | | |

| Item 5. | Market for Registrant's Common Equity, Related Stockholder Matters and Issuer Purchases | |

| | of Equity Securities | 18 |

| Item 6. | Selected Financial Data | 21 |

| Item 7. | Management's Discussion and Analysis of Financial Condition and Results of Operations | 22 |

| Item 7A. | Quantitative and Qualitative Disclosures About Market Risk | 47 |

| Item 8. | Financial Statements and Supplementary Data | 47 |

| Item 9. | Changes in and Disagreements with Accountants on Accounting and Financial Disclosure | 87 |

| Item 9A. | Controls and Procedures | 87 |

| Item 9B. | Other Information | 89 |

| | | |

| PART III. | | |

| Item 10. | Directors, Executive Officers and Corporate Governance | 89 |

| Item 11. | Executive Compensation | 89 |

| Item 12. | Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters | 89 |

| Item 13. | Certain Relationships and Related Transactions, and Director Independence | 90 |

| Item 14 | Principal Accountant Fees and Services | 90 |

| | | |

| PART IV. | | |

| Item 15. | Exhibits and Financial Statement Schedules | 90 |

| | | |

| SIGNATURES | |

| Authorized Signatures | 93 |

PART I

Overview

Parkway Properties, Inc. is a real estate investment trust ("REIT") specializing in the operation, leasing, acquisition and ownership of office properties. The Company performs these services for its own account and for other institutional investors through co-ownership structures such as discretionary funds and/or partnerships. The terms “we,” “us,” “our,” “Parkway,” or the “Company” refer to Parkway Properties, Inc. individually or together with its subsidiaries. The Company is geographically focused on the Southeastern and Southwestern United States and Chicago. Parkway and its predecessors have been public companies engaged in the real estate business since 1971, and the management team has had experience managing a public real estate company through all phases of the real estate business cycle. As part of its strategy, the Company places an emphasis on property operations and customer satisfaction with an ultimate goal of achieving a high level of customer retention. The Company is self-administered, in that it provides its own investment and administrative services internally through its own employees. The Company is also self-managed, as it internally provides the management, maintenance and other real estate services that its properties require through its own employees, such as property managers and engineers and in some cases, leasing professionals. In addition Parkway is self-leased for renewal leases for the majority of its office property portfolio.

At March 1, 2011, Parkway owned or had an interest in 65 office properties located in 11 states with an aggregate of approximately 13.7 million square feet of leasable space. Included in the portfolio are two discretionary funds and several partnership arrangements which encompass 20 properties totaling 4.1 million square feet, representing 30.3% of the portfolio. With the discretionary funds and/or partnerships, the Company receives fees for asset management, property management, leasing and construction management services and potentially receives incentive fees upon sale if certain investment targets are achieved. Increasing the number of co-investments, and consequently the related fee income, is part of the Company’s strategy to transform itself to an operator-owner versus an owner-operator. The strategy highlights the Company’s strength in providing excellent service in the operation and acquisition of office properties for investment clients in addition to its direct ownership of real estate assets. Fee-based real estate services are offered through the Company’s wholly-owned subsidiary, Parkway Realty Services LLC (“PRS”), which also manages and/or leases approximately 1.6 million square feet for third-party owners at March 1, 2011.

Strategic Planning

Parkway is a focused office REIT with a hands-on, service-oriented approach, a disciplined capital allocation program and a willingness to recycle assets. We continue to focus on the Company’s strategy of transforming itself to an operator-owner from an owner-operator, as well as maximizing total return to shareholders. To show our commitment to this goal, our newest strategic plan is centered on a goal of achieving a 12% compounded annual total return to our shareholders over a three-year period. This plan is known as the FOCUS Plan (the “Plan”), which began July 1, 2010 and will extend three full years through June 30, 2013. The goals of the Plan are as follows:

| · | Fund and Fund-Like Investments. The Company believes that fund and fund-like investments have the highest priority of the Company’s capital allocation, because it gives Parkway’s stockholders the highest risk adjusted return as measured by internal rate of return, capitalization rate and accretion per share. |

| · | Operator-Owner. The Company plans to make a full transformation to an operator-owner, with the goal of being a majority operator/owner by the end of the Plan. This has been a goal for several years and will continue to be a core strategy as Parkway seeks to increase fee income and maximize its return on equity and accretion per share. Additionally, the Company will continue to expand PRS, which offers expert real estate management guidance, professional property management services and strategic marketing and leasing services aimed at increasing net operating income and maximizing profit upon exit. |

| · | Capital Allocation Discipline. The Company’s overall capital structure goal is to achieve a net debt to gross asset value ratio of 50% or less, as determined by using a capitalization rate of 8.5% on recurring cash income, and a net debt to earnings before interest, taxes, depreciation and amortization (“EBITDA”) multiple of 6.5 times or less. Beyond the balance sheet, capital allocation refers to the Company’s goal to exit non-strategic markets through the continuation of its Asset Recycling program. Most of the properties |

identified for sale are smaller assets or assets located in smaller markets where Parkway does not have a significant presence. By the end of the FOCUS Plan, the Company’s goal is to be invested in larger, higher-quality properties located in higher-rent growth markets through fund and fund-like investments. The Company will continue to maintain discipline as it relates to managing the balance sheet and the acquisition and disposition of assets.

| · | Uncompromising Focus on Operations. Parkway believes that its uncompromising focus on operations is what sets it apart from other office property owners. An important goal of the FOCUS Plan is to move decision-making authority to the regional office level. The Company’s market leaders already have the responsibility of setting rents, increasing net operating income margins and maintaining a consistent standard of operations and will be given more profit and loss responsibility and investment authority going forward. It is important that we know our markets, which is best achieved when Parkway’s people live and work within the market. An integral part of the FOCUS Plan is a program referred to as “We Know… City.” These three words imply that Parkway employees know more than just how to manage real estate, but that they have a deep understanding of a city’s history, economics, infrastructure, politics and much more. By truly knowing the cities where the Company is invested, we are better positioned for leasing, active asset management, recruitment and investments. |

| · | Shareholder Returns. All of the previously mentioned goals funnel to the ultimate goal of the FOCUS Plan, which is to maximize total return to Parkway’s shareholders. The Company has set a goal of achieving a 12% compounded annual total return to its shareholders for the three-year period starting July 1, 2010. |

Discretionary Funds and Partnerships

Parkway intends to continue raising discretionary funds and forming partnerships with select institutional investors. Under the terms of these funds and partnerships, where applicable, Parkway will manage all phases of the investment cycle including acquisition, financing, operations, leasing and dispositions. The Company will receive fees for providing these services. At March 1, 2011, Parkway had two discretionary funds and two partnership agreements of this nature.

On July 6, 2005, Parkway, through affiliated entities, entered into a limited partnership agreement forming a $500.0 million discretionary fund known as Parkway Properties Office Fund, L.P. (“Fund I”) with Ohio Public Employees Retirement System (“Ohio PERS”) for the purpose of acquiring high-quality multi-tenant office properties. Ohio PERS is a 75% investor and Parkway is a 25% investor in the fund, which is capitalized with approximately $200.0 million of equity capital and $300.0 million of non-recourse, fixed-rate first mortgage debt. At February 15, 2008, Fund I was fully invested.

Fund I targeted properties with a leveraged internal rate of return of greater than 11%. Parkway serves as the general partner of the fund and provides asset management, property management, leasing and construction management services to the fund, for which it is paid market-based fees. After each partner has received a 10% annual cumulative preferred return and a return of invested capital, 60% will be distributed to Ohio PERS and 40% to Parkway. The term of Fund I will be seven years from the date the fund was fully invested until February 2015, with provisions to extend the term for two additional one-year periods.

On May 14, 2008, Parkway, through affiliated entities, entered into a limited partnership agreement forming a $750.0 million discretionary fund known as Parkway Properties Office Fund II, L.P. (“Fund II”) with Teacher Retirement System of Texas (“TRST”) for the purpose of acquiring high-quality multi-tenant office properties. TRST is a 70% investor and Parkway is a 30% investor in the fund, which will be capitalized with approximately $375.0 million of equity capital and $375.0 million of non-recourse, fixed-rate first mortgage debt. Parkway’s share of the equity contribution for the fund will be $112.5 million. The Company intends to fund its share of equity contributions with proceeds from asset sales, issuance of equity securities and/or advances on the credit facility as needed on a temporary basis. Fund II targets acquisitions in the core markets of Houston, Austin, San Antonio, Chicago, Atlanta, Phoenix, Charlotte, Memphis, Nashville, Jacksonville, Orlando, Tampa/St. Petersburg, and Ft. Lauderdale, as well as other growth markets to be determined at Parkway’s discretion.

Fund II targets properties with an anticipated leveraged internal rate of return of greater than 10%. Parkway serves as the general partner of the fund and provides asset management, property management, leasing and construction management services to the fund, for which it is paid market-based fees. Cash will be distributed pro

rata to each partner until a 9% annual cumulative preferred return is received and invested capital is returned. Thereafter, 56% will be distributed to TRST and 44% to Parkway. Parkway has four years from the inception date, or through May 2012, to identify and acquire properties (the “Investment Period”), with funds contributed as needed to close acquisitions. Parkway will exclusively represent the fund in making acquisitions within the target markets and acquisitions with certain predefined criteria. Parkway will not be prohibited from making fee-simple or joint venture acquisitions in markets outside of the target markets, acquiring properties within the target markets that do not meet Fund II’s specific criteria or selling a full or partial interest in currently owned properties. The term of Fund II will be seven years from the expiration of the Investment Period, with provisions to extend the term for two additional one-year periods at the discretion of Parkway. At March 1, 2011, Fund II had remaining investment capacity of $552.1 million of which $81.8 million represents Parkway’s remaining equity contribution that would be due in connection with additional investments in office properties.

Third-Party Management

The Company benefits from a fully integrated management infrastructure, provided by its wholly-owned management subsidiary, PRS. In addition to the Company’s owned properties, PRS currently manages and/or leases approximately 5.7 million net rentable square feet for third-party owners, joint venture interests and fund properties. The Company intends to expand its third-party fee business through funds or similar ventures as well as through third party management and leasing contracts.

Financing Strategy

The Company expects to continue seeking primarily fixed rate, non-recourse mortgage financing with maturities from five to ten years typically amortizing over 25 to 30 years on select office building investments as additional capital is needed. The Company monitors a number of leverage and other financial metrics defined in the loan agreements for the Company’s unsecured credit facility and working capital unsecured credit facility, which includes the Company’s total debt to total asset value. In addition, the Company monitors interest, fixed charge and modified fixed charge coverage ratios as well as the net debt to gross asset value and the net debt to EBITDA multiple. Management believes all of the leverage and other financial metrics it monitors, including those discussed above, provide useful information on total debt levels as well as the Company’s ability to cover interest, principal and/or preferred dividend payments with current income. The Company targets a net debt to gross asset value of 50% or less and a net debt to EBITDA multiple of 6.5 times or less.

Parkway may, in appropriate circumstances, acquire one or more properties in exchange for Parkway's equity securities. Parkway has no set policy as to the amount or percentage of its assets which may be invested in any specific property. Rather than a specific policy, Parkway evaluates each property in terms of whether and to what extent the property meets Parkway's investment criteria and strategic objectives. The strategies and policies set forth above were determined, and are subject to review by, Parkway's Board of Directors which may change such strategies or policies based upon their evaluation of the state of the real estate market, the performance of Parkway's assets, capital and credit market conditions, and other relevant factors.

Capital Allocation

Capital allocation receives constant review by management and the Board of Directors considering many factors including the capital markets, our weighted average cost of capital, buying criteria (written and published), the real estate market and management of the risk associated with the rate of return. We examine all aspects of each type of investment whether it is a fund asset, Parkway common stock, a mortgage loan receivable or a fee simple purchase. Each carries a relationship to replacement cost which is still an important underwriting discipline for us. Each has a current yield and a leveraged and unleveraged internal rate of return that can be measured on a relative and absolute basis. Currently, management views investing in funds and similar ventures as the highest priority of our capital allocation because it produces the highest risk adjusted return as measured by internal rate of return and current cash return. Other investment alternatives are available to us but with lesser return or slightly higher risk so we are principally focused on funds or similar ventures at the present time. During 2010, the REIT industry began to see an increase in investments in real estate as a result of more equity being deployed by investors, as well as a more favorable credit environment. As a result, the Company continues to monitor its buying criteria and to exercise discipline when making capital allocation decisions but expects to begin making more investments in Fund II during 2011.

Industry Segments

Parkway’s primary business is the operation and ownership of office properties. The Company accounts for each office property or groups of related office properties as an individual operating segment. Parkway has aggregated its individual operating segments into a single reporting segment due to the fact that the individual operating segments have similar operating and economic characteristics.

The individual operating segments exhibit similar economic characteristics such as being leased by the square foot, sharing the same primary operating expenses and ancillary revenue opportunities and being cyclical in the economic performance based on current supply and demand conditions. The individual operating segments are also similar in that revenues are derived from the leasing of office space to customers and each office property is managed and operated consistently in accordance with Parkway’s standard operating procedures. The range and type of customer uses of our properties is similar throughout our portfolio regardless of location or class of building and the needs and priorities of our customers do not vary from building to building. Therefore, Parkway’s management responsibilities do not vary from location to location based on the size of the building, geographic location or class.

Management Team

Parkway's management team consists of experienced office property specialists with proven capabilities in office property (i) operations; (ii) leasing; (iii) management; (iv) acquisition/disposition; (v) financing; (vi) capital allocation; and (vii) accounting and financial reporting. Parkway's 14 senior officers have an average of 22 years of real estate industry experience, and have worked together at Parkway for an average of 17 years. Management has developed a highly service-oriented operating culture and believes that its focus on operations, proactive leasing, property management and asset management activities will result in higher customer retention and occupancy and will translate into enhanced stockholder value.

Administration

The Company is self-administered and self-managed and maintains its principal executive offices in Jackson, Mississippi. At December 31, 2010, the Company had 256 employees. The operations of the Company are conducted from approximately 17,000 square feet of office space located at 188 East Capitol Street, One Jackson Place, Suite 1000, Jackson, Mississippi. The building is owned by Parkway and is leased by Parkway at market rental rates.

Available Information

Parkway makes available free of charge on the “Corporate” page of its web site, www.pky.com, its filed and furnished reports on Form 10-K, 10-Q and 8-K and all amendments thereto, as soon as reasonably practicable after Parkway electronically files such material with, or furnishes it to, the Securities and Exchange Commission.

The Company’s Corporate Governance Guidelines, Code of Business Conduct and Ethics and the Charters of the Audit Committee, Nominating and Corporate Governance Committee and Compensation Committee of the Board of Directors are available on the “Corporate” page of Parkway’s web site. Copies of these documents are also available free of charge in print upon written request addressed to Investor Relations, Parkway Properties, Inc., One Jackson Place, Suite 1000, 188 East Capitol Street, Jackson, Mississippi 39201.

ITEM 1A. Risk Factors.

In addition to the other information contained or incorporated by reference in this document, readers should carefully consider the following risk factors. Any of these risks or the occurrence of any one or more of the uncertainties described below could have a material adverse effect on the Company's financial condition and the performance of its business. The Company refers to itself as “we” or “our” in the following risk factors.

Our performance is subject to risks inherent in owning real estate investments.

Our investments are generally made in office properties. We are, therefore, generally subject to risks incidental to the ownership of real estate. These risks include:

| · | changes in supply of or demand for office properties or customers for such properties in an area in which we own buildings; |

| · | the ongoing need for capital improvements; |

| · | increased operating costs, which may not necessarily be offset by increased rents, including insurance premiums, utilities and real estate taxes, due to inflation and other factors; |

| · | changes in tax, real estate and zoning laws; |

| · | changes in governmental rules and fiscal policies; and |

| · | civil unrest, acts of war, acts of God, including earthquakes, hurricanes and other natural disasters (which may result in uninsured losses) and other factors beyond our control. |

Should any of these events occur, our financial condition and our ability to make expected distributions to stockholders could be adversely affected.

The economic conditions of our primary markets affect our operations.

Substantially all of our properties are located in the Southeastern and Southwestern United States and Chicago and, therefore, our financial condition and ability to make distributions to our stockholders is linked to economic conditions in these markets as well as the market for office space generally in these markets. A downturn in these markets may adversely affect our cash flows and ability to make distributions to stockholders.

Customer defaults could adversely affect our operations.

Substantially all of our revenues and income come from rental income from real property. As such, our revenues and income could be adversely affected if a significant number of our customers defaulted under their lease obligations. Our ability to manage our assets is also subject to federal bankruptcy laws and state laws that limit creditors' rights and remedies available to real property owners to collect delinquent rents. If a customer becomes insolvent or bankrupt, we cannot be sure that we could recover the premises from the customer promptly or from a trustee or debtor-in-possession in any bankruptcy proceeding relating to that customer. We also cannot be sure that we would receive rent in the proceeding sufficient to cover our expenses with respect to the premises. If a customer becomes bankrupt, the federal bankruptcy code will apply and, in some instances, may restrict the amount and recoverability of our claims against the customer. A customer’s default on its obligations to us could adversely affect our financial condition and the cash we have available for distributions to our stockholders.

Illiquidity of real estate may limit our ability to vary our portfolio.

Real estate investments are relatively illiquid. Our ability to vary our portfolio by selling properties and buying new ones in response to changes in economic and other conditions may therefore be limited. In addition, the Internal Revenue Code limits our ability to sell our properties by imposing a penalty tax of 100% on the gain derived from prohibited transactions, which are defined as sales of property held primarily for sale to customers in the ordinary course of a trade or business. The frequency of sales and the holding period of the property sold are two primary factors in determining whether the property sold fits within this definition. These considerations may limit our opportunities to sell our properties. If we must sell an investment, we cannot assure you that we will be able to dispose of the investment in the time period we desire or that the sales price of the investment will recoup or exceed our cost for the investment, or that the penalty tax would not be assessed.

Our current and future joint venture investments could be adversely affected by the capital markets, our lack of sole decision-making authority, our reliance on joint venture partners' financial condition and any disputes that may arise between us and our joint venture partners.

Co-investing with third parties through joint ventures is a part of our ongoing business strategy. We may not be in a position to exercise sole decision-making authority regarding the properties owned through joint ventures. Investments in joint ventures may, under certain circumstances, involve risks not present when a third party is not involved, including reliance on our joint venture partners and the possibility that joint venture partners might become bankrupt or fail to fund their share of required capital contributions, thus exposing us to liabilities in excess of our share of the investment. The funding of Parkway’s capital contributions may be dependent on proceeds from asset sales, credit facility advances and/or sales of equity securities. In limited cases, such as gross neglect, the Company can be terminated as the provider of certain fee-based services. Joint venture partners may have business interests or goals that are inconsistent with our business interests or goals and may be in a position to take actions contrary to our policies or objectives. Any disputes that may arise between us and joint venture partners may result in litigation or arbitration that would increase our expenses.

Our properties are subject to various federal, state and local regulatory requirements, such as environmental laws, state and local fire and safety requirements, building codes and land use regulations.

Failure to comply with these requirements could subject us to governmental fines or private litigant damage awards. We believe that our properties are currently in material compliance with all applicable regulatory requirements. However, we do not know whether existing requirements will change or whether future requirements, including any requirements that may emerge from pending or future climate change legislation, will require us to make significant unanticipated expenditures that will adversely impact our business, financial condition and results of operations.

Uninsured and underinsured losses may adversely affect operations.

We, or in certain instances, customers of our properties, carry commercial general liability, fire and extended coverage insurance with respect to our properties. This coverage has policy specifications and insured limits that we believe are customarily carried for similar properties. We plan to obtain similar coverage for properties we acquire in the future. However, certain types of losses, generally of a catastrophic nature, such as earthquakes and floods, may be either uninsurable or not economically insurable. Should a property sustain damage, we may incur losses due to insurance deductibles, to co-payments on insured losses or to uninsured losses. In the event of a substantial property loss, the insurance coverage may not be sufficient to pay the full current market value or current replacement cost of the property. In the event of an uninsured loss, we could lose some or all of our capital investment, cash flow and anticipated profits related to one or more properties. Inflation, changes in building codes and ordinances, environmental considerations, and other factors also might make it not feasible to use insurance proceeds to replace a property after it has been damaged or destroyed. Under such circumstances, the insurance proceeds we receive might not be adequate to restore our economic position with respect to such property.

We have existing debt and refinancing risks that could affect our cost of operations.

We currently have both fixed and variable rate indebtedness and may incur indebtedness in the future, including borrowings under our credit facilities, to finance possible acquisitions and for general corporate purposes. As a result, we are and expect to be subject to the risks normally associated with debt financing including:

| · | that interest rates may rise; |

| · | that our cash flow will be insufficient to make required payments of principal and interest; |

| · | that we will be unable to refinance some or all of our debt; |

| · | that any refinancing will not be on terms as favorable as those of the existing debt; |

| · | that required payments on mortgages and on our other debt are not reduced if the economic performance of any property declines; |

| · | that debt service obligations will reduce funds available for distribution to our stockholders; |

| · | that any default on our debt, due to noncompliance with financial covenants or otherwise, could result in acceleration of those obligations; and |

| · | that we may be unable to refinance or repay the debt as it becomes due. |

An increase in interest rates would reduce our net income and funds from operations. We may not be able to refinance or repay debt as it becomes due which may force us to refinance or to incur additional indebtedness at higher rates and additional cost or, in the extreme case, to sell assets or seek protection from our creditors under applicable law.

A lack of any limitation on our debt could result in our becoming more highly leveraged.

Our governing documents do not limit the amount of indebtedness we may incur. Accordingly, our Board of Directors may incur additional debt and would do so, for example, if it were necessary to maintain our status as a REIT. We might become more highly leveraged as a result, and our financial condition and cash available for distribution to stockholders might be negatively affected and the risk of default on our indebtedness could increase.

The cost and terms of mortgage financings may render the sale or financing of a property difficult or unattractive.

The sale of a property subject to a mortgage may trigger pre-payment penalties, yield maintenance payments or make-whole payments to the lender, which would reduce the amount of gain or increase our loss on the sale of a property and could make the sale of a property less likely. Certain of our mortgages will have significant outstanding principal balances on their maturity dates, commonly known as "balloon payments." There is no assurance that we will be able to refinance such balloon payments on the maturity of the loans, which may force disposition of properties on disadvantageous terms or require replacement with debt with higher interest rates, either of which would have an adverse impact on our financial performance and ability to pay distributions to investors.

If the economic downturn continues in the long-term, our business, results of operations, cash flows and financial condition could be adversely affected.

In the U.S., market and economic conditions continue to be challenging with tighter credit conditions and modest growth. While recent economic data reflects a stabilization of the economy and credit markets, the cost and availability of credit may continue to be adversely affected. Furthermore, deteriorating economic conditions including business layoffs, downsizing, industry slowdowns and other similar factors that affect our customers could negatively impact commercial real estate fundamentals and result in lower occupancy, lower rental rates and declining values in our real estate portfolio. The timing of changes in occupancy levels tends to lag the timing of changes in overall economic activity and employment levels. Additionally, the economic situation could have an impact on our lenders or customers, causing them to fail to meet their obligations to us. No assurances can be given that the effects of the current economic conditions will not have a material adverse effect on our business, financial condition and results of operations.

Litigation against us could distract our management and/or negatively impact our operating results.

As noted above under “Prospectus Supplement Summary — Recent Developments”, our former chief financial officer filed (and later withdrew) a complaint against us with OSHA, filed a personal injury lawsuit against us, and threatened a shareholder derivative lawsuit on behalf of our company against us, our directors and officers. We are disputing the allegations made by Mr. Collins. The Company’s Board of Directors appointed the Audit Committee (the “Committee”) of the board to review and evaluate the claims made in Mr. Collins’ shareholder demand letter. The Committee engaged independent counsel to assist with the review and evaluation of these claims. After thoroughly investigating the allegations in good faith and fully informing itself of all material facts relevant thereto, the Committee believes that the Company did not operate in a fraudulent or misleading manner regarding either the termination of Mr. Collins or the disclosure of the Company’s 2010 earnings guidance. Further, the Committee determined that it would not serve the interests of Parkway or its shareholders for the Company to take any of the further actions requested in the demand letter. Although it is not possible to predict the outcome of litigation with any certainty, claims of this nature present a risk of protracted litigation, regulatory investigations or enforcement, monetary damages, injunctive orders, fines, attorneys’ fees, costs and expenses, and diversion of management’s attention from the operation of our business.

We may amend our investment strategy and business policies without your approval.

Our Board of Directors determines our growth, investment, financing, capitalization, borrowing, REIT status, operating and distribution policies. Although the Board of Directors has no present intention to amend or revise any of these policies, these policies may be amended or revised without notice to and approval from stockholders. Accordingly, stockholders may not have control over changes in our policies.

Loss of our tax status as a real estate investment trust would have significant adverse consequences to us and the value of our securities.

We believe that we qualify for taxation as a REIT for federal income tax purposes, and we plan to operate so that we can continue to meet the requirements for taxation as a REIT. To qualify as a REIT we must satisfy numerous requirements (some on an annual and quarterly basis) established under the highly technical and complex provisions of the Internal Revenue Code (“Code”) applicable to REITs, which include:

| · | maintaining ownership of specified minimum levels of real estate related assets; |

| · | generating specified minimum levels of real estate related income; |

| · | maintaining certain diversity of ownership requirements with respect to our shares; and |

| · | distributing at least 90% of our taxable income on an annual basis. |

The distribution requirement noted above could adversely affect our ability to use earnings for improvements or acquisitions because funds distributed to stockholders will not be available for capital improvements to existing properties or for acquiring additional properties.

Only limited judicial and administrative interpretations exist of the REIT rules. In addition, qualification as a REIT involves the determination of various factual matters and circumstances not entirely within our control.

If we fail to qualify as a REIT, we will be subject to federal income tax (including any applicable alternative minimum tax) on our taxable income at corporate rates. In addition, unless entitled to relief under certain statutory provisions, we will be disqualified from treatment as a REIT for the four taxable years following the year during which we failed to qualify. This treatment would reduce net earnings available for investment or distribution to stockholders because of the additional tax liability for the year or years involved. In addition, we would no longer be required to make distributions to our stockholders. To the extent that distributions to stockholders had been made based on our qualifying as a REIT, we might be required to borrow funds or to liquidate certain of our investments to pay the applicable tax.

As a REIT, we have been and will continue to be subject to certain federal, state and local taxes on our income and property.

The requirements necessary to maintain our REIT status may limit our ability to earn additional fee income at the REIT level, which may cause us to conduct fee-generating activities through a taxable REIT subsidiary.

The REIT provisions of the Code may limit our ability to earn additional management fee and other fee income from joint ventures and third parties. Our aggregate gross income from fees and certain other non-qualifying sources cannot exceed 5% of our annual gross income. As a result, our ability to increase the amount of fee income we earn at the REIT level may be limited, and we may have to conduct fee-generating activities through a taxable REIT subsidiary. Any fee income we earn through a taxable REIT subsidiary would be subject to federal, state, and local income tax at regular corporate rates, which would reduce our net income from our fee-generating activities.

There is a risk of changes in the tax law applicable to real estate investment trusts.

Since the Internal Revenue Service, the United States Treasury Department and Congress frequently review federal income tax legislation, we cannot predict whether, when or to what extent new federal tax laws, regulations, interpretations or rulings will be adopted. Any of such legislative action may prospectively or retroactively modify our tax treatment and, therefore, may adversely affect taxation of us and/or our investors.

Limitations on the ownership of our common stock may preclude the acquisition or change of control of our Company.

Certain provisions contained in our charter and bylaws and certain provisions of Maryland law may have the effect of discouraging a third party from making an acquisition proposal for us and may thereby inhibit a change of control. Provisions of our charter are designed to assist us in maintaining our qualification as a REIT under the Code by preventing concentrated ownership of our capital stock that might jeopardize REIT qualification. Among other things, these provisions provide that, if a transfer of our stock or a change in our capital structure would result in (1) any person (as defined in the charter) directly or indirectly acquiring beneficial ownership of more than 9.8% (in value or in number, whichever is more restrictive) of our outstanding equity stock excluding Excess Stock, (2) our outstanding shares being constructively or beneficially owned by fewer than 100 persons, or (3) our being "closely held" within the meaning of Section 856(h) of the Code, then:

| · | any proposed transfer will be void from the beginning and we will not recognize such transfer; |

| · | we may institute legal proceedings to enjoin such transfer; |

| · | we will have the right to redeem the shares proposed to be transferred; and |

| · | the shares proposed to be transferred will be automatically converted into and exchanged for shares of a separate class of stock, the Excess Stock. |

Excess Stock has no dividend or voting rights but holders of Excess Stock do have certain rights in the event of our liquidation, dissolution or winding up. Our charter provides that we will hold the Excess Stock as trustee for the person or persons to whom the shares are ultimately transferred, until the time that the shares are retransferred to a person or persons in whose hands the shares would not be Excess Stock and certain price-related restrictions are satisfied. These provisions may have an anti-takeover effect by discouraging tender offers or purchases of large blocks of stock, thereby limiting the opportunity for stockholders to receive a premium for their shares over then-prevailing market prices. Under the terms of our charter, our Board of Directors has the authority to waive these ownership restrictions.

Furthermore, under our charter, the Board of Directors has the authority to classify and reclassify any of our unissued shares of capital stock into shares of capital stock with such preferences, rights, powers and restrictions as the Board of Directors may determine. The authorization and issuance of a new class of capital stock could have the effect of delaying or preventing someone from taking control of us, even if a change in control were in our stockholders' best interests.

There may be future dilution of our common stock, and resales of our common stock in the public market following a stock offering that may cause the market price for our common stock to fall.

Our Charter authorizes our Board of Directors to, among other things, issue additional shares of capital stock without stockholder approval. We may issue common stock, preferred stock or securities convertible or exchangeable into equity securities to raise additional capital. Holders of our common stock have no preemptive rights that entitle them to purchase their pro rata share of any offering of shares of any class or series. Accordingly, the issuance of any additional shares of common or preferred stock or convertible securities could be substantially dilutive to existing holders of our common stock. Furthermore, the resale by shareholders of our common stock in the public market following any offering could have the effect of depressing the market price for our common stock. At December 31, 2010, 21,923,610 shares of our common stock and 4,374,896 shares of our Series D preferred stock were issued and outstanding.

The price of our common stock is volatile and may decline.

The market price of our common stock may fluctuate widely as a result of a number of factors, many of which are outside our control. In addition, the stock market is subject to fluctuations in share prices and trading volumes that affect the market prices of the shares of many companies. These broad market fluctuations have adversely affected and may continue to adversely affect the market price of our common stock. Among the factors that could affect the market price of our common stock are:

| · | actual or anticipated quarterly fluctuations in our operating results and financial condition; |

| · | changes in revenues or earnings estimates or publication of research reports and recommendations by financial analysts or actions taken by rating agencies with respect to our securities or those of other REITs; |

| · | the ability of our tenants to pay rent to us and meet their other obligations to us under current lease terms; |

| · | our ability to re-lease spaces as leases expire; |

| · | our ability to refinance our indebtedness as it matures; |

| · | any changes in our distribution policy; |

| · | any future issuances of equity securities; |

| · | strategic actions by us or our competitors, such as acquisitions or restructurings; |

| · | general market conditions and, in particular, developments related to market conditions for the real estate industry; and |

| · | domestic and international economic factors unrelated to our performance. |

Maryland business statutes may limit the ability of a third party to acquire control of us.

Maryland law provides protection for Maryland corporations against unsolicited takeovers by limiting, among other things, the duties of the directors in unsolicited takeover situations. The duties of directors of Maryland corporations do not require them to (a) accept, recommend or respond to any proposal by a person seeking to acquire control of the corporation, (b) authorize the corporation to redeem any rights under, or modify or render inapplicable, any stockholders rights plan, (c) make a determination under the Maryland Business Combination Act, or (d) act or fail to act solely because of the effect of the act or failure to act may have on an acquisition or potential acquisition of control of the corporation or the amount or type of consideration that may be offered or paid to the stockholders in an acquisition. Moreover, under Maryland law the act of a director of a Maryland corporation relating to or affecting an acquisition or potential acquisition of control is not subject to any higher duty or greater scrutiny than is applied to any other act of a director. Maryland law also contains a statutory presumption that an act of a director of a Maryland corporation satisfies the applicable standards of conduct for directors under Maryland law.

The Maryland Business Combination Act provides that unless exempted, a Maryland corporation may not engage in business combinations, including mergers, dispositions of 10 percent or more of its assets, certain issuances of shares of stock and other specified transactions, with an "interested stockholder" or an affiliate of an interested stockholder for five years after the most recent date on which the interested stockholder became an interested stockholder, and thereafter unless specified criteria are met. An interested stockholder is generally a person owning or controlling, directly or indirectly, 10 percent or more of the voting power of the outstanding stock of the Maryland corporation.

ITEM 1B. Unresolved Staff Comments.

None.

ITEM 2. Properties.

General

The Company operates and invests principally in office properties in the Southeastern and Southwestern United States and Chicago, but is not limited to any specific geographical region or property type. At March 1, 2011, the Company owned or had an interest in 65 office properties comprising approximately 13.7 million square feet of office space located in 11 states.

Property acquisitions in 2010 and 2008 were funded through a variety of sources, including:

| · | Cash reserves and cash generated from operating activities; |

· | Sales of equity securities; |

| · | Sales of office properties; |

· | Contributions from partners; and/or |

| · | Advances on the Company’s credit facility. |

Office Buildings

Other than as discussed under "Item 1. Business", the Company intends to hold and operate its portfolio of office buildings for investment purposes. The Company does not propose any program for the renovation or improvement of any of the office buildings other than those discussed in “Item 2 – Properties – Significant Properties”, except as called for under the renewal of existing leases or the signing of new leases or improvements necessary to upgrade recent acquisitions to the Company's operating standards. All such improvements are expected to be financed by cash flow from the portfolio of office properties, advances on the Company’s credit facility or contributions from partners.

We believe that our insurance coverage contains policy specifications and insured limits that are customary for similar properties, business activities and markets, and we believe our properties are adequately insured. However, an uninsured loss could result in loss of capital investment and anticipated profits.

All office building investments compete for customers with similar properties located within the same market primarily on the basis of location, rent charged, services provided and the design and condition of the improvements. The Company also competes with other REITs, financial institutions, pension funds, partnerships, individual investors and others when attempting to acquire office properties.

The following table sets forth certain information about office properties the Company owned or had an interest in at January 1, 2011:

| | | | | | Estimated | | |

| | | | | | Average | % of | |

| | Number | Total Net | % of | Average | Market | Leases | % |

| | of | Rentable | Total Net | Rent Per | Rent Per | Expiring | Leased |

| | Office | Square Feet | Rentable | Square | Square | In | at |

| Location | Properties(1) | (in thousands) | Feet | Foot (2) | Foot (3) | 2011 (4) | 1/1/2011 |

| Chicago, IL | 4 | 2,897 | 22.0% | $29.67 | $27.63 | 7.4% | 88.6% |

| Houston, TX | 12 | 2,031 | 15.4% | 20.36 | 21.33 | 15.8% | 93.6% |

| Atlanta, GA | 9 | 1,778 | 13.5% | 22.52 | 19.74 | 21.1% | 82.5% |

| Memphis, TN | 6 | 1,200 | 9.1% | 21.16 | 18.11 | 9.0% | 83.1% |

| Jackson, MS | 7 | 1,112 | 8.4% | 18.49 | 17.51 | 12.8% | 78.9% |

| Orlando, FL | 5 | 922 | 7.0% | 22.40 | 20.87 | 7.4% | 84.9% |

| Phoenix, AZ | 3 | 689 | 5.2% | 25.95 | 20.70 | 16.8% | 87.5% |

| Richmond, VA | 6 | 495 | 3.8% | 17.58 | 16.16 | 13.0% | 79.7% |

| Jacksonville, FL | 4 | 482 | 3.6% | 19.42 | 17.81 | 4.1% | 93.7% |

| Nashville, TN | 1 | 436 | 3.3% | 18.35 | 16.50 | 2.9% | 83.1% |

| Columbia, SC | 2 | 407 | 3.1% | 14.86 | 16.10 | 4.2% | 75.7% |

| Charlotte, NC | 1 | 327 | 2.5% | 17.69 | 17.00 | 12.6% | 78.1% |

| Ft. Lauderdale, FL | 2 | 216 | 1.6% | 22.50 | 21.26 | 12.9% | 67.6% |

| Hampton Roads, VA | 1 | 172 | 1.3% | 19.26 | 18.00 | 10.3% | 84.1% |

| Other Markets | 1 | 32 | 0.2% | 14.00 | 8.00 | 7.6% | 7.6% |

| | 64 | 13,196 | 100.0% | $22.73 | $21.15 | 11.7% | 85.3% |

(1) Includes 44 office properties owned directly and 20 office properties owned through joint ventures.

(2) Average rent per square foot is defined as the weighted average current gross rental rate including escalations for operating expenses related to leased office space in the building at January 1, 2011.

(3) Estimated average gross market rent per square foot is based upon information obtained from (i) the Company's own experience in leasing space at the properties; (ii) leasing agents in the relevant markets with respect to quoted rental rates and completed leasing transactions for comparable properties in the relevant markets; and (iii) publicly available data with respect thereto. Estimated average market rent is weighted by the net rentable square feet expiring in each property.

(4) The percentage of leases expiring in 2011 represents the ratio of square feet under leases expiring in 2011 divided by total net rentable square feet.

The following table sets forth scheduled lease expirations for properties owned at January 1, 2011 on leases executed at January 1, 2011, assuming no customer exercises renewal options:

| | | Net | | Annualized | Weighted Avg | Weighted Est |

| | | Rentable | Percent of | Rental | Expiring Gross | Avg Market |

| Year of | Number | Square Feet | Total Net | Amount | Rental Rate Per | Rent Per Net |

| Lease | of | Expiring | Rentable | Expiring (1) | Net Rentable | Rentable |

| Expiration | Leases | (in thousands) | Square Feet | (in thousands) | Square Foot (2) | Square Foot (3) |

| 2011 | 314 | 1,549 | 11.7% | $ | 35,774 | $ | 23.10 | $ | 20.62 |

| 2012 | 242 | 1,629 | 12.3% | 38,099 | 23.39 | 21.95 |

| 2013 | 207 | 1,177 | 8.9% | 26,259 | 22.31 | 19.85 |

| 2014 | 154 | 1,376 | 10.4% | 30,186 | 21.93 | 20.25 |

| 2015 | 168 | 1,694 | 12.9% | 35,420 | 20.91 | 16.76 |

| 2016 | 84 | 1,282 | 9.7% | 27,166 | 21.19 | 19.65 |

| Thereafter | 109 | 2,553 | 19.4% | 63,064 | 24.71 | 23.18 |

| | 1,278 | 11,260 | 85.3% | $ | 255,968 | $ | 22.73 | $ | 21.15 |

(1) Annualized rental amount expiring is defined as net rentable square feet expiring multiplied by the weighted average expiring annual rental rate per net rentable square foot.

(2) Weighted average expiring gross rental rate is the weighted current rental rate including escalations for operating expenses.

(3) Estimated weighted average market rent is based upon information obtained from (i) the Company’s own experience in leasing space at the properties; (ii) leasing agents in the relevant markets with respect to quoted rental rates and completed leasing transactions for comparable properties in the relevant markets; and (iii) publicly available data with respect thereto. Estimated weighted average market rent is weighted by the net rentable square feet expiring in each property.

Customers

The office properties are leased to 1,278 customers, which are in a wide variety of industries including banking, insurance, professional services (including legal, accounting, and consulting), energy, financial services and telecommunications. Our largest customer and 25 largest customers accounted for 4.9% and 39.5%, respectively of our annualized rental revenue. The following table sets forth information concerning the 25 largest customers of the properties owned directly or through joint ventures as of January 1, 2011 (in thousands, except footnotes):

| | | | | Leased Square Feet (1) | Annualized Rental Revenue (1) |

| | No. of Props. | Square Footage Expiring | |

| Customer | 2011 | 2012 | 2013 | 2014 | 2015 | 2016 | Thereafter |

| General Services Administration (“GSA”) (2) | 15 | 102 | 21 | 35 | 3 | 46 | - | 265 | 472 | $ | 9,966 |

| Cox Enterprises/AutoTrader.com (3) | 2 | 198 | - | 90 | - | 17 | - | 17 | 322 | 6,982 |

| Health Care Service Corporation (“BCBS”) (4) | 1 | - | 230 | - | - | - | - | - | 230 | 5,945 |

| Blue Cross Blue Shield of Georgia, Inc. (5) | 1 | - | - | - | - | - | - | 199 | 199 | 5,426 |

| Regions Financial Corporation (6) | 2 | 19 | 5 | 5 | - | 4 | 237 | - | 270 | 5,404 |

| Nabors Industries/Nabors Corporate Services | 1 | - | - | - | 216 | - | - | - | 216 | 4,420 |

| Extra Space Storage | 1 | - | - | - | - | 134 | - | - | 134 | 3,042 |

| Bank of America, NA (7) | 6 | 2 | - | 28 | - | 124 | 3 | 16 | 173 | 2,843 |

| Southwestern Energy Company | 2 | - | - | - | 118 | - | - | - | 118 | 2,679 |

| Combined Insurance Company of America (8) | 1 | - | - | - | - | - | - | 99 | 99 | 2,670 |

| Clear Channel Communications | 1 | - | - | - | - | - | - | 74 | 74 | 2,577 |

| Young & Rubicam (9) | 1 | 9 | - | - | - | - | - | 69 | 78 | 2,505 |

| Schlumberger Technology (10) | 1 | - | 155 | - | - | - | - | - | 155 | 2,439 |

| Golin-Harris Communications, Inc. | 1 | - | 67 | - | - | - | - | - | 67 | 2,375 |

| U.S. Cellular Corporation (11) | 1 | - | - | - | - | - | - | 222 | 222 | 2,372 |

| Honeywell (12) | 1 | - | - | - | - | - | - | 102 | 102 | 2,335 |

| United Healthcare Services | 1 | - | 67 | - | - | - | - | - | 67 | 2,328 |

| Louisiana-Pacific Corporation | 1 | - | - | - | - | 105 | - | - | 105 | 2,226 |

| Stein Mart, Inc. | 1 | - | - | - | - | - | 107 | - | 107 | 2,186 |

| Motorola, Inc. | 1 | 15 | - | - | - | 53 | - | - | 68 | 2,106 |

| Shefsky & Froelich, Ltd | 1 | - | - | - | - | 69 | - | - | 69 | 1,881 |

| BDO USA, LLP (13) | 2 | - | 1 | - | 7 | - | 42 | - | 50 | 1,738 |

| Forman, Perry, Watkins, Krutz & Tardy (14) | 1 | - | - | - | - | - | 126 | - | 126 | 1,679 |

| URS Corporation (15) | 2 | 3 | - | - | - | - | 57 | - | 60 | 1,436 |

| Burrell Communications Group, LLC | 1 | - | - | - | - | - | 35 | - | 35 | 1,430 |

| | | 348 | 546 | 158 | 344 | 552 | 607 | 1,063 | 3,618 | $ | 80,990 |

| Total Rentable Square Footage (1) | 13,196 | |

| Total Annualized Rental Revenue (1) | $ | 205,186 | |

| (1) | Annualized Rental Revenue represents the gross rental rate (including escalations) per square foot, multiplied by the number of square feet leased by the customer. Annualized rent for customers in consolidated and unconsolidated joint ventures is calculated based on our ownership interest. However, leased square feet represents 100% of square feet leased through direct ownership or through joint ventures. |

| (2) | GSA’s lease at the Meridian Building in Atlanta, Georgia, provides an option to cancel 16,778 square feet effective February 2015 with 90 days written notice. The GSA’s lease at the Falls Building in Memphis, Tennessee provides two options to cancel. The first is an option to cancel 2,922 square feet effective January 2013. The second option is to cancel 22,973 square feet effective January 2013 with 120 days written notice. The GSA’s lease at Carmel Crossing-Davie in Charlotte, North Carolina, provides an option to cancel 21,384 square feet effective November 2011 with 30 days written notice. GSA has 80,503 square feet of leases in the Jackson, Mississippi Central Business District that are relocating to the newly developed federal courthouse in 2011. |

| (3) | Cox Enterprises, which is located at Peachtree Dunwoody Pavilion in Atlanta, Georgia, has an option to cancel 106,758 square feet between June and December 2012 with a notice date of June 2011. In the event the customer exercises this option at the earliest termination date, the Company expects to receive a fee at the notice date of approximately $950,000 associated with this lease termination which will be recorded into income through the early termination date. Additionally, the customer will continue to pay rent through the early termination date. AutoTrader.com will vacate 193,043 square feet upon expiration in February 2011. Parkway has signed a 46,000 square foot lease to backfill the AutoTrader space and is in letter of intent or lease documentation stages with approximately 37,000 square feet of additional prospects for the space. |

| (4) | BCBS, which is located at 111 East Wacker in Chicago, Illinois, has exercised its option to cancel 168,405 square feet in March 2012. The customer will pay a total termination fee of $7.3 million which will be recorded into income over the remaining term of the lease through March 2012. Additionally, the customer will continue to pay rent through the March 2012 expiration date. |

| (5) | Blue Cross Blue Shield of Georgia, Inc., which is located at Capital City Plaza in Atlanta, Georgia, has the option to cancel 59,222 square feet in either January 2016 or January 2018 with nine months written notice. Additionally, the lease provides the option to cancel an additional 29,610 square feet in January 2018 with nine months written notice. |

| (6) | Regions Financial Corporation, which is located at the Morgan Keegan Tower in Memphis, Tennessee, has the option to cancel 3,197 square feet with four months written notice. |

| (7) | Bank of America, NA at Bank of America Plaza in Nashville, Tennessee, has an option to cancel 123,710 square feet in October 2014 with 12 months notice. Also, Bank of America, successor to Countrywide Home Loans, which is located at Maitland 100 in Orlando, Florida, has the option to cancel 11,779 square feet in June of 2012 with six months written notice. |

| (8) | Combined Insurance Company of America’s lease at 111 East Wacker in Chicago, Illinois, provides a cancellation option in July 2018 with 12 months written notice. |

| (9) | Young & Rubicam, which is located at 233 North Michigan in Chicago, Illinois, has the option to cancel approximately 34,000 square feet in October of 2015 with 12 months written notice. |

| (10) | In February 2011, Schlumberger Technology, which is located at the Schlumberger building in Houston, Texas, signed a 64-month lease extension for 155,324 square feet. The new expiration of Schlumberger’s lease is June 2017 with an option to cancel in June 2015 with a 12-month written notice. |

| (11) | U.S. Cellular Corporation at US Cellular Plaza in Chicago, Illinois, has the option to cancel up to 39,648 square feet in December 2013 and in September 2014 with a notice date of September 2013. |

| (12) | Honeywell, which is located at the Honeywell Building in Houston, Texas, has a lease cancellation option in December 2014, which requires a 12-month notice. |

| (13) | BDO USA, LLP, which is located at Bank of America Plaza in Nashville, Tennessee, has the option to cancel 6,549 square feet in February 2012 with 120 days written notice. Additionally, the customer’s lease at 233 North Michigan in Chicago, Illinois, provides the option to cancel 43,477 square feet in December 2012 with 12 months written notice. |

| (14) | Forman, Perry, Watkins, Krutz & Tardy, which is located at City Centre in Jackson, Mississippi, has certain cancellation rights pending changes in partnership structure. |

| (15) | URS Corporation, which is located at Squaw Peak Corporate Center in Phoenix, Arizona, has the option to cancel 10,000 square feet between December 2011 and December 2013 with 90 days written notice. |

Significant Properties

The Company has one property, 111 East Wacker, whose book value at December 31, 2010, exceeds ten percent of total assets.

The 111 East Wacker building (“111 East Wacker") is a 32-story Class A office property with an attached four-level, below grade parking garage. The Company, through its wholly-owned direct and indirect subsidiaries, acquired fee simple title to 111 East Wacker in July 2006. The building was constructed in 1970 and includes 980,000 rentable square feet (“RSF”) of Class A office and storage space and 33,000 RSF of retail space. The building was 96.4% occupied at January 1, 2011, with an average effective annual rental rate per square foot of $28.64. The average occupancy and rental rate per square foot over the past five years are as follows:

| Year | Average Occupancy | Average Rental Rate per Square Foot |

| 2006 | 89.9% | $ | 24.25 |

| 2007 | 85.0% | $ | 23.90 |

| 2008 | 94.1% | $ | 26.05 |

| 2009 | 95.7% | $ | 27.31 |

| 2010 | 91.2% | $ | 26.72 |

111 East Wacker’s major customers include governmental agencies, an insurance company and businesses that provide legal, accounting, insurance, advertising and other financial services. Retail customers include financial service companies, restaurants and other numerous service-oriented amenity customers.

Lease expirations for 111 East Wacker at January 1, 2011 are as follows (in thousands, except number of leases):

| | Square Feet | Percentage | Annualized | Percentage of | |

| | of Leases | of Total | Rental | Total Annualized | Number of |

| Year | Expiring | Square Feet | Revenue (1) | Rental Revenue | Leases |

| 2011 | 67 | 6.6% | $ | 1,946 | 7.0% | 16 |

| 2012 | 359 | 35.4% | 10,292 | 36.8% | 10 |

| 2013 | 102 | 10.1% | 3,140 | 11.2% | 14 |

| 2014 | 11 | 1.1% | 301 | 1.1% | 3 |

| 2015 | 104 | 10.3% | 2,845 | 10.2% | 7 |

| 2016 | 70 | 6.9% | 2,073 | 7.4% | 6 |

| 2017 | 54 | 5.3% | 1,606 | 5.7% | 5 |

| 2018 | 14 | 1.4% | 452 | 1.6% | 2 |

| 2019 | 44 | 4.3% | 1,322 | 4.7% | 2 |

| 2020 | 19 | 1.9% | 514 | 1.9% | 1 |

| Thereafter | 132 | 13.1% | 3,472 | 12.4% | 2 |

| | 976 | 96.4% | $ | 27,963 | 100.0% | 68 |

| (1) | Annualized rental revenue represents the gross rental rate (including escalations) per square feet, multiplied by the number of square feet leased by the customer. |

111 East Wacker has one customer that occupies 10% or more of the rentable square footage. Information regarding this customer is as follows:

| Nature of Business | Lease Expiration | Effective Rental Rate Per Square Foot | Lease Options |

| Insurance | (1) | $25.85 | (2) |

| (1) | This customer has 230,000 square feet expiring in 2012. This includes 62,000 square feet originally scheduled to expire in 2012 and 168,000 square feet resulting from the exercise of an early termination option. |

| (2) | In September 2010 this customer provided notice they would exercise their option to cancel 168,000 square feet, originally set to expire in 2017. The customer will pay a total termination fee of $7.3 million, of which $3.7 million was paid upon receipt of the termination notice in September 2010. The total termination fee of $7.3 million will be recorded into income from the notice date of September 2010 through the March 2012 expiration. Additionally, the customer will continue to pay rent through the March 2012 expiration date. |

For tax purposes, depreciation is calculated over 39 years for building and garage, 7 to 39 years for building and tenant improvements and 5 to 7 years for equipment, furniture and fixtures. The federal tax basis net of accumulated tax depreciation of 111 East Wacker is as follows at December 31, 2010 (in thousands):

| | 111 East |

| | Wacker |

| Land | $ 23,285 |

| Building and Garage | 150,326 |

| Building Improvements | 18,655 |

| Tenant Improvements | 10,142 |

Real estate tax expense for 2010, 2009 and 2008 for 111 East Wacker was $5.9 million, $7.1 million and $6.1 million, respectively.

111 East Wacker is subject to a non-recourse first mortgage (the "111 Mortgage"). The 111 Mortgage totaled $148.5 million at December 31, 2010 and has a fixed interest rate of 6.3% with payments based on a 30 year amortization and interest only payments for five years or through July 2011. The 111 Mortgage matures on July 11, 2016 at which time a balloon payment of $139.5 million is due.

We compete with a considerable number of other real estate companies seeking to acquire and lease office space in Chicago. Principal factors of competition in our business are the quality of properties (including the design and condition of improvements), leasing terms (including rent and other charges and allowances for tenant improvements), attractiveness and convenience of location, the quality and breadth of tenant services provided and reputation as an owner and operator of quality office properties in the relevant market. Our ability to compete also depends on, among other factors, trends in the national and local economies, financial condition and operating results of current and prospective tenants, availability and cost of capital, taxes and governmental regulations and legislation.

The Company did not have any material liens or encumbrances that exceeded 10% of total assets at December 31, 2010.

Non-Strategic Assets

Since January 1, 1996, Parkway has pursued a strategy of liquidating its non-strategic assets and using the proceeds from such sales to acquire office properties and pay down short-term debt. The Company defines non-strategic assets as all office and parking properties in markets where the Company has not achieved critical mass of greater than one million square feet as well as markets that management believes do not have compelling rent growth potential. Additionally, the Company has 12 acres of undeveloped land in New Orleans, Louisiana, that is considered a non-strategic asset.

ITEM 3. Legal Proceedings.

The Company and its subsidiaries are, from time to time, parties to litigation arising from the ordinary course of their business. Management of Parkway does not believe that any such litigation will materially affect the financial position or operations of Parkway.

The information set forth in Note K in the Notes to the Consolidated Financial Statements included herein is incorporated by reference.

ITEM 4. [Removed and Reserved]

PART II

| | ITEM 5. Market for Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities. |

The Company’s common stock ($.001 par value) is listed and trades on the New York Stock Exchange under the symbol “PKY”. The number of record holders of the Company’s common stock at January 1, 2011, was 2,203.

At March 1, 2011, the last reported sales price per common share on the New York Stock Exchange was $16.20. The following table sets forth, for the periods indicated, the high and low last reported sales prices per share of the Company’s common stock and the per share cash distributions paid by Parkway during each quarter.

| | Year Ended | | Year Ended |

| | December 31, 2010 | | December 31, 2009 |

| Quarter Ended | High | Low | Distributions | | High | Low | Distributions |

| March 31 | $ | 22.93 | $ | 16.35 | $ | 0.075 | | $ | 18.94 | $ | 8.60 | $ | 0.325 |

| June 30 | $ | 20.73 | $ | 14.38 | 0.075 | | $ | 16.22 | $ | 10.17 | 0.325 |

| September 30 | $ | 16.83 | $ | 13.46 | 0.075 | | $ | 20.86 | $ | 10.88 | 0.325 |

| December 31 | $ | 18.54 | $ | 14.71 | 0.075 | | $ | 21.50 | $ | 17.29 | 0.325 |

| | | | $ | 0.300 | | | | $ | 1.300 |

Common stock distributions during 2010 and 2009 ($0.30 and $1.30 per share, respectively) were taxable as follows for federal income tax purposes:

| | Year Ended |

| | December 31 |

| | 2010 | 2009 |

| Ordinary income | $ | 0.23 | $ | 0.71 |

| Unrecaptured Section 1250 gain | 0.06 | - |

| Return of capital | 0.01 | 0.59 |

| | $ | 0.30 | $ | 1.30 |

The following table shows the high and low Series D preferred share prices and per share distributions paid for each quarter of 2010 and 2009 reported by the New York Stock Exchange.

| | Year Ended | | Year Ended |

| | December 31, 2010 | | December 31, 2009 |

| Quarter Ended | High | Low | Distributions | | High | Low | Distributions |

| March 31 | $ | 25.04 | $ | 21.77 | $ | 0.50 | | $ | 17.54 | $ | 10.13 | $ | 0.50 |

| June 30 | $ | 25.00 | $ | 23.38 | 0.50 | | $ | 20.50 | $ | 12.68 | 0.50 |

| September 30 | $ | 25.75 | $ | 23.50 | 0.50 | | $ | 23.07 | $ | 17.90 | 0.50 |

| December 31 | $ | 25.81 | $ | 24.80 | 0.50 | | $ | 24.25 | $ | 20.53 | 0.50 |

| | | | $ | 2.00 | | | | $ | 2.00 |

At January 1, 2011, there were five holders of record of the Company's 4.4 million outstanding shares of Series D preferred stock. Series D preferred stock distributions during 2010 and 2009 were taxable as follows for federal income tax purposes:

| | Year Ended December 31 |

| | 2010 | 2009 |

| Ordinary income | $ | 1.57 | $ | 2.00 |

| Unrecaptured Section 1250 gain | 0.43 | - |

| | $ | 2.00 | $ | 2.00 |

Purchases of Equity Securities by the Issuer

| | | | Total Number | Maximum Number |

| | | | of Shares Purchased | of Shares that |

| | Total Number | Average | as Part of Publicly | May Yet Be |

| | of Shares | Price Paid | Announced Plans | Purchased Under |

| Period | Purchased | per Share | or Programs | the Plans or Programs |

| | | | | |

| 10/01/10 to 10/31/10 | 1,465(1) | $15.48 | - | - |

| 11/01/10 to 11/30/10 | - | - | - | - |

| 12/01/10 to 12/31/10 | - | - | - | - |

| Total | 1,465 | $15.48 | - | - |

| (1) | As permitted under the Company's equity compensation plan, these shares were withheld by the Company to satisfy tax withholding obligations for employees in connection with the vesting of stock. Shares withheld for tax withholding obligations do not affect the total number of shares available for repurchase under any approved common stock repurchase plan. At December 31, 2010, the Company did not have an authorized stock repurchase plan in place. |

Securities Authorized for Issuance Under Equity Compensation Plans

See Item 12 of this Annual Report on Form 10-K, “Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters,” for certain information regarding the Company’s equity compensation plans.

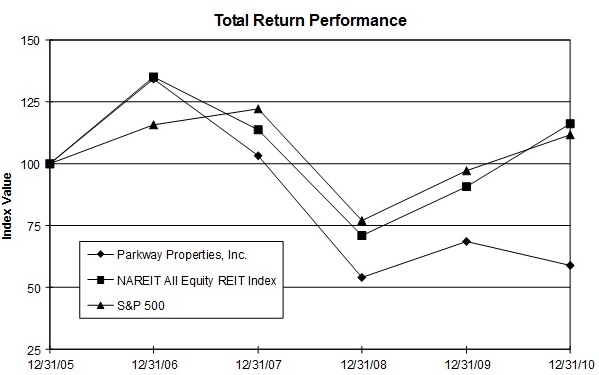

Performance Graph

The following graph provides a comparison of cumulative stockholder return for the period from December 31, 2005 through December 31, 2010 among Parkway, the Standard & Poor’s 500 Index (“S&P 500”) and the National Association of Real Estate Investment Trusts (“NAREIT”) Equity REIT Total Return Index (“NAREIT Equity”). The stock performance graph assumes an investment of $100 in the shares of Parkway common stock and each index and the reinvestment of any dividends. The historical information set forth below is not necessarily indicative of future performance.

The performance graph and related information shall not be deemed “soliciting material” or deemed to be “filed” with the SEC, nor shall such information be incorporated by reference into any future filing, except to the extent that the Company specifically incorporates it by reference into such filing.

| | | Period Ending | |

| Index | 12/31/05 | 12/31/06 | 12/31/07 | 12/31/08 | 12/31/09 | 12/31/10 |

| Parkway Properties, Inc. | 100.00 | 134.46 | 103.17 | 54.11 | 68.69 | 58.84 |

| NAREIT All Equity REIT Index | 100.00 | 135.06 | 113.87 | 70.91 | 90.76 | 116.12 |

| S&P 500 | 100.00 | 115.79 | 122.16 | 76.96 | 97.33 | 111.99 |

ITEM 6. Selected Financial Data.

| | Year Ended 12/31/10 | Year Ended 12/31/09 | Year Ended 12/31/08 | Year Ended 12/31/07 | Year Ended 12/31/06 |

| | (In thousands, except per share data) |

Operating Data: | | | | | |

| Revenues | | | | | |

| Income from office and parking properties | $ | 254,611 | $ | 262,951 | $ | 260,229 | $ | 230,180 | $ | 195,092 |

| Management company income | 1,652 | 1,870 | 1,936 | 1,605 | 5,329 |

| Total revenues | 256,263 | 264,821 | 262,165 | 231,785 | 200,421 |

| Expenses | | | | | |

| Property operating expenses | 117,935 | 126,343 | 124,409 | 106,368 | 91,605 |

| Depreciation and amortization | 92,190 | 92,126 | 91,224 | 73,860 | 61,071 |

| Impairment loss on real estate | 4,120 | - | 2,542 | - | - |

| Management company expenses | 3,961 | 2,299 | 1,947 | 1,188 | 1,141 |

| General and administrative | 7,382 | 6,108 | 9,725 | 6,602 | 4,656 |

| Total expenses | 225,588 | 226,876 | 229,847 | 188,018 | 158,473 |

| Operating income | 30,675 | 37,945 | 32,318 | 43,767 | 41,948 |

| Other income and expenses | | | | | |

| Interest and other income | 1,487 | 1,609 | 1,332 | 526 | 39 |

| Equity in earnings of unconsolidated joint ventures | 326 | 445 | 894 | 1,008 | 751 |

| Gain (loss) on real estate, joint venture interests, | | | | | |

| involuntary conversion and other assets | 40 | (7,524) | - | 20,307 | 17,646 |

| Interest expense | (54,647) | (55,044) | (58,766) | (51,879) | (42,368) |

| | | | | | |

| Income (loss) from continuing operations | (22,119) | (22,569) | (24,222) | 13,729 | 18,016 |

| Income (loss) from discontinued operations | 194 | 404 | (461) | 2,789 | 2,098 |

| Gain on sale of real estate from discontinued operations | 8,518 | - | 22,588 | - | 5,083 |

| Total discontinued operations | 8,712 | 404 | 22,127 | 2,789 | 7,181 |

| Net income (loss) | (13,407) | (22,165) | (2,095) | 16,518 | 25,197 |

| Noncontrolling interest – real estate partnerships | 10,789 | 10,562 | 11,369 | 3,174 | 485 |

| Net income (loss) for Parkway Properties, Inc. | (2,618) | (11,603) | 9,274 | 19,692 | 25,682 |

| Dividends on preferred stock | (6,325) | (4,800) | (4,800) | (4,800) | (4,800) |

| Dividends on convertible preferred stock | - | - | - | - | (1,773) |