0000072971wfc:OtherNoninterestIncomeMemberus-gaap:FairValueHedgingMemberus-gaap:InterestRateContractMember2023-01-012023-06-300000072971us-gaap:EquitySecuritiesMemberus-gaap:PurchaseCommitmentMember2023-12-31

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-Q

(Mark One)

| | | | | |

| ☑ | QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the quarterly period ended June 30, 2024

OR

| | | | | |

| ☐ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from __________ to __________

Commission file number 001-2979

WELLS FARGO & COMPANY

(Exact name of registrant as specified in its charter)

| | | | | | | | | | | | | | |

| Delaware | | No. | 41-0449260 | |

| (State of incorporation) | | (I.R.S. Employer Identification No.) |

420 Montgomery Street, San Francisco, California 94104

(Address of principal executive offices) (Zip code)

Registrant’s telephone number, including area code: 1-866-249-3302

Securities registered pursuant to Section 12(b) of the Act:

| | | | | | | | |

| Title of Each Class | Trading Symbol | Name of Each Exchange

on Which Registered |

| Common Stock, par value $1-2/3 | WFC | New York Stock Exchange (NYSE) |

| 7.5% Non-Cumulative Perpetual Convertible Class A Preferred Stock, Series L | WFC.PRL | NYSE |

| Depositary Shares, each representing a 1/1000th interest in a share of Non-Cumulative Perpetual Class A Preferred Stock, Series Y | WFC.PRY | NYSE |

| Depositary Shares, each representing a 1/1000th interest in a share of Non-Cumulative Perpetual Class A Preferred Stock, Series Z | WFC.PRZ | NYSE |

| Depositary Shares, each representing a 1/1000th interest in a share of Non-Cumulative Perpetual Class A Preferred Stock, Series AA | WFC.PRA | NYSE |

| Depositary Shares, each representing a 1/1000th interest in a share of Non-Cumulative Perpetual Class A Preferred Stock, Series CC | WFC.PRC | NYSE |

| Depositary Shares, each representing a 1/1000th interest in a share of Non-Cumulative Perpetual Class A Preferred Stock, Series DD | WFC.PRD | NYSE |

| Guarantee of Medium-Term Notes, Series A, due October 30, 2028 of Wells Fargo Finance LLC | WFC/28A | NYSE |

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes þ No ¨

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes þ No ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

Large accelerated filer þ Accelerated filer ¨

Non-accelerated filer ¨ Smaller reporting company ☐

Emerging growth company ☐

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ¨

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ☐ No þ

Indicate the number of shares outstanding of each of the issuer’s classes of common stock, as of the latest practicable date.

| | | | | | | | |

| | Shares Outstanding |

| | July 23, 2024 |

| Common stock, $1-2/3 par value | | 3,403,770,246 |

| | | | | | | | | | | | | | |

| FORM 10-Q | |

| CROSS-REFERENCE INDEX | |

| PART I | Financial Information | |

| Item 1. | Financial Statements | Page |

| Consolidated Statement of Income | |

| Consolidated Statement of Comprehensive Income | |

| Consolidated Balance Sheet | |

| Consolidated Statement of Changes in Equity | |

| Consolidated Statement of Cash Flows | |

| Notes to Financial Statements | |

| 1 | | — | Summary of Significant Accounting Policies | |

| 2 | | — | Trading Activities | |

| 3 | | — | Available-for-Sale and Held-to-Maturity Debt Securities | |

| 4 | | — | Equity Securities | |

| 5 | | — | Loans and Related Allowance for Credit Losses | |

| 6 | | — | Mortgage Banking Activities | |

| 7 | | — | Intangible Assets and Other Assets | |

| 8 | | — | Leasing Activity | |

| 9 | | — | Preferred Stock | |

| 10 | | — | Legal Actions | |

| 11 | | — | Derivatives | |

| 12 | | — | Fair Values of Assets and Liabilities | |

| 13 | | — | Securitizations and Variable Interest Entities | |

| 14 | | — | Guarantees and Other Commitments | |

| 15 | | — | Securities and Other Collateralized Financing Activities | |

| 16 | | — | Pledged Assets and Collateral | |

| 17 | | — | Operating Segments | |

| 18 | | — | Revenue and Expenses | |

| 19 | | — | Employee Benefits | |

| 20 | | — | Earnings and Dividends Per Common Share | |

| 21 | | — | Other Comprehensive Income | |

| 22 | | — | Regulatory Capital Requirements and Other Restrictions | |

| Item 2. | Management’s Discussion and Analysis of Financial Condition and Results of Operations (Financial Review) | |

| Summary Financial Data | |

| Overview | |

| Earnings Performance | |

| Balance Sheet Analysis | |

| Off-Balance Sheet Arrangements | |

| Risk Management | |

| Capital Management | |

| Regulatory Matters | |

| Critical Accounting Policies | |

| Current Accounting Developments | |

| Forward-Looking Statements | |

| Risk Factors | |

| Glossary of Acronyms | |

| Item 3. | Quantitative and Qualitative Disclosures About Market Risk | |

| Item 4. | Controls and Procedures | |

| | |

| PART II | Other Information | |

| Item 1. | Legal Proceedings | |

| Item 1A. | Risk Factors | |

| Item 2. | Unregistered Sales of Equity Securities and Use of Proceeds | |

| Item 5. | Other Information | |

| Item 6. | Exhibits | |

| | | | |

| Signature | |

FINANCIAL REVIEW

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Summary Financial Data | | | | | | | | | | | | | | | |

| Quarter ended | | Jun 30, 2024

% Change from | | Six months ended | | |

| ($ in millions, except ratios and per share amounts) | Jun 30,

2024 | | Mar 31,

2024 | | Jun 30,

2023 | | Mar 31,

2024 | | Jun 30,

2023 | | Jun 30,

2024 | | Jun 30,

2023 | | %

Change |

| Selected Income Statement Data | | | | | | | | | | | | | | | |

| Total revenue | $ | 20,689 | | | 20,863 | | | 20,533 | | | (1) | % | | 1 | | | $ | 41,552 | | | 41,262 | | | 1 | % |

| Noninterest expense | 13,293 | | | 14,338 | | | 12,987 | | | (7) | | | 2 | | | 27,631 | | | 26,663 | | | 4 | |

| Pre-tax pre-provision profit (PTPP) (1) | 7,396 | | | 6,525 | | | 7,546 | | | 13 | | | (2) | | | 13,921 | | | 14,599 | | | (5) | |

| Provision for credit losses (2) | 1,236 | | | 938 | | | 1,713 | | | 32 | | | (28) | | | 2,174 | | | 2,920 | | | (26) | |

| Wells Fargo net income | 4,910 | | | 4,619 | | | 4,938 | | | 6 | | | (1) | | | 9,529 | | | 9,929 | | | (4) | |

| Wells Fargo net income applicable to common stock | 4,640 | | | 4,313 | | | 4,659 | | | 8 | | | — | | | 8,953 | | | 9,372 | | | (4) | |

| Common Share Data | | | | | | | | | | | | | | | |

| Diluted earnings per common share | 1.33 | | | 1.20 | | | 1.25 | | | 11 | | | 6 | | | 2.53 | | | 2.48 | | | 2 | |

| Dividends declared per common share | 0.35 | | | 0.35 | | | 0.30 | | | — | | | 17 | | | 0.70 | | | 0.60 | | | 17 | |

| Common shares outstanding | 3,402.7 | | | 3,501.7 | | | 3,667.7 | | | (3) | | | (7) | | | | | | | |

| Average common shares outstanding | 3,448.3 | | | 3,560.1 | | | 3,699.9 | | | (3) | | | (7) | | | 3,504.2 | | | 3,742.6 | | | (6) | |

| Diluted average common shares outstanding | 3,486.2 | | | 3,600.1 | | | 3,724.9 | | | (3) | | | (6) | | | 3,543.2 | | | 3,772.4 | | | (6) | |

| Book value per common share (3) | $ | 47.01 | | | 46.40 | | | 43.87 | | | 1 | | | 7 | | | | | | | |

| Tangible book value per common share (3)(4) | 39.57 | | | 39.17 | | | 36.53 | | | 1 | | | 8 | | | | | | | |

| Selected Equity Data (period-end) | | | | | | | | | | | | | | | |

| Total equity | 178,148 | | | 182,674 | | | 181,952 | | | (2) | | | (2) | | | | | | | |

| Common stockholders’ equity | 159,963 | | | 162,481 | | | 160,916 | | | (2) | | | (1) | | | | | | | |

| Tangible common equity (4) | 134,660 | | | 137,163 | | | 133,990 | | | (2) | | | 1 | | | | | | | |

| Performance Ratios | | | | | | | | | | | | | | | |

| Return on average assets (ROA) (5) | 1.03 | % | | 0.97 | | | 1.05 | | | | | | | 1.00 | % | | 1.07 | | | |

| Return on average equity (ROE) (6) | 11.5 | | | 10.5 | | | 11.4 | | | | | | | 11.0 | | | 11.6 | | | |

| Return on average tangible common equity (ROTCE) (4) | 13.7 | | | 12.3 | | | 13.7 | | | | | | | 13.0 | | | 13.9 | | | |

| Efficiency ratio (7) | 64 | | | 69 | | | 63 | | | | | | | 66 | | | 65 | | | |

| Net interest margin on a taxable-equivalent basis | 2.75 | | | 2.81 | | | 3.09 | | | | | | | 2.78 | | | 3.14 | | | |

| Selected Balance Sheet Data (average) | | | | | | | | | | | | | | | |

| Loans | $ | 916,977 | | | 928,075 | | | 945,906 | | | (1) | | | (3) | | | $ | 922,526 | | | 947,271 | | | (3) | |

| Assets | 1,914,647 | | | 1,916,974 | | | 1,878,253 | | | — | | | 2 | | | 1,915,810 | | | 1,871,005 | | | 2 | |

| Deposits | 1,346,478 | | | 1,341,628 | | | 1,347,449 | | | — | | | — | | | 1,344,052 | | | 1,352,046 | | | (1) | |

| Selected Balance Sheet Data (period-end) | | | | | | | | | | | | | | | |

| Debt securities | 520,254 | | | 506,280 | | | 503,468 | | | 3 | | | 3 | | | | | | | |

| Loans | 917,907 | | | 922,784 | | | 947,960 | | | (1) | | | (3) | | | | | | | |

| Allowance for credit losses for loans | 14,789 | | | 14,862 | | | 14,786 | | | — | | | — | | | | | | | |

| Equity securities | 60,763 | | | 59,556 | | | 67,471 | | | 2 | | | (10) | | | | | | | |

| Assets | 1,940,073 | | | 1,959,153 | | | 1,876,320 | | | (1) | | | 3 | | | | | | | |

| Deposits | 1,365,894 | | | 1,383,147 | | | 1,344,584 | | | (1) | | | 2 | | | | | | | |

| | | | | | | | | | | | | | | |

| Headcount (#) (period-end) | 222,544 | | | 224,824 | | | 233,834 | | | (1) | | | (5) | | | | | | | |

| Capital and Other Metrics | | | | | | | | | | | | | | | |

| Risk-based capital ratios and components (8): | | | | | | | | | | | | | | | |

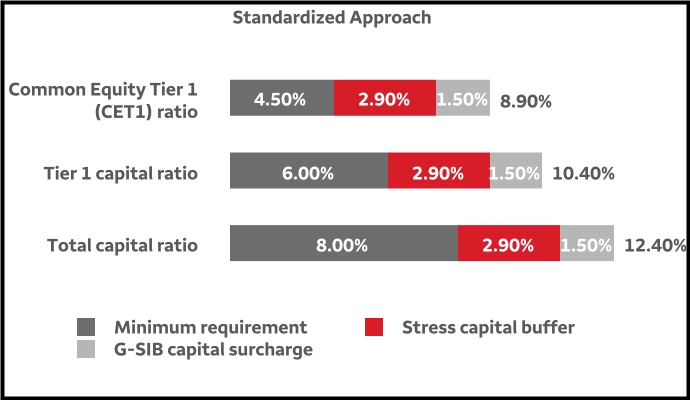

| Standardized Approach: | | | | | | | | | | | | | | | |

| Common Equity Tier 1 (CET1) | 11.01 | % | | 11.19 | | | 10.73 | | | | | | | | | | | |

| Tier 1 capital | 12.34 | | | 12.68 | | | 12.25 | | | | | | | | | | | |

| Total capital | 15.02 | | | 15.40 | | | 15.00 | | | | | | | | | | | |

| Risk-weighted assets (RWAs) (in billions) | $ | 1,219.5 | | | 1,221.6 | | | 1,250.7 | | | — | | | (2) | | | | | | | |

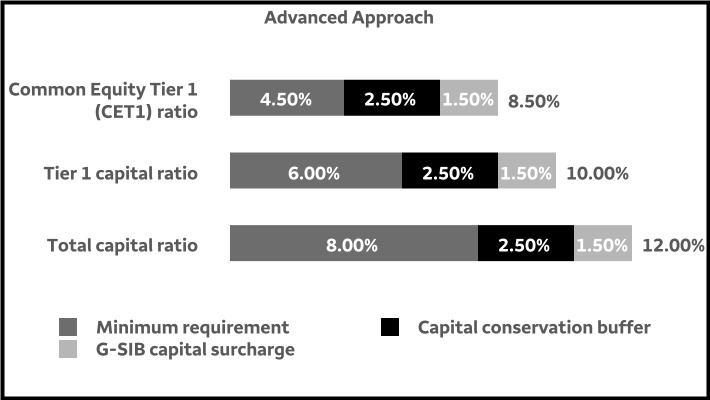

| Advanced Approach: | | | | | | | | | | | | | | | |

| Common Equity Tier 1 (CET1) | 12.28 | % | | 12.43 | | | 12.00 | | | | | | | | | | | |

| Tier 1 capital | 13.77 | | | 14.09 | | | 13.70 | | | | | | | | | | | |

| Total capital | 15.82 | | | 16.17 | | | 15.82 | | | | | | | | | | | |

| Risk-weighted assets (RWAs) (in billions) | $ | 1,093.0 | | | 1,099.6 | | | 1,118.4 | | | (1) | | | (2) | | | | | | | |

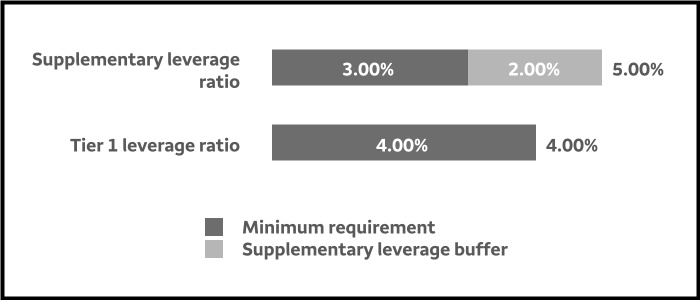

| Tier 1 leverage ratio | 7.98 | % | | 8.20 | | | 8.28 | | | | | | | | | | | |

Supplementary Leverage Ratio (SLR) | 6.67 | | | 6.85 | | | 6.91 | | | | | | | | | | | |

| Total Loss Absorbing Capacity (TLAC) Ratio (9) | 24.78 | | | 25.10 | | | 23.12 | | | | | | | | | | | |

| Liquidity Coverage Ratio (LCR) (10) | 124 | | | 126 | | | 123 | | | | | | | | | | | |

(1)Pre-tax pre-provision profit (PTPP) is total revenue less noninterest expense. Management believes that PTPP is a useful financial measure because it enables investors and others to assess the Company’s ability to generate capital to cover credit losses through a credit cycle.

(2)Includes provision for credit losses for loans, debt securities, and other financial assets.

(3)Book value per common share is common stockholders’ equity divided by common shares outstanding. Tangible book value per common share is tangible common equity divided by common shares outstanding.

(4)Tangible common equity is a non-GAAP financial measure and represents total equity less preferred equity, noncontrolling interests, goodwill, certain identifiable intangible assets (other than mortgage servicing rights) and goodwill and other intangibles on investments in consolidated portfolio companies, net of applicable deferred taxes. The methodology of determining tangible common equity may differ among companies. Management believes that return on average tangible common equity and tangible book value per common share, which utilize tangible common equity, are useful financial measures because they enable management, investors, and others to assess the Company’s use of equity. For additional information, including a corresponding reconciliation to generally accepted accounting principles (GAAP) financial measures, see the “Capital Management – Tangible Common Equity” section in this Report.

(5)Represents Wells Fargo net income divided by average assets.

(6)Represents Wells Fargo net income applicable to common stock divided by average common stockholders’ equity.

(7)The efficiency ratio is noninterest expense divided by total revenue (net interest income and noninterest income).

(8)For additional information, see the “Capital Management” section and Note 22 (Regulatory Capital Requirements and Other Restrictions) to Financial Statements in this Report.

(9)Represents TLAC divided by RWAs, which is our binding TLAC ratio, determined by using the greater of RWAs under the Standardized and Advanced Approaches.

(10)Represents average high-quality liquid assets divided by average projected net cash outflows, as each is defined under the LCR rule.

This Quarterly Report, including the Financial Review and the Financial Statements and related Notes, contains forward-looking statements, which may include forecasts of our financial results and condition, expectations for our operations and business, and our assumptions for those forecasts and expectations. Do not unduly rely on forward-looking statements. Actual results may differ materially from our forward-looking statements due to several factors. Factors that could cause our actual results to differ materially from our forward-looking statements are described in this Report, including in the “Forward-Looking Statements” section, and in the “Risk Factors” and “Regulation and Supervision” sections of our Annual Report on Form 10-K for the year ended December 31, 2023 (2023 Form 10-K).

When we refer to “Wells Fargo,” “the Company,” “we,” “our,” or “us” in this Report, we mean Wells Fargo & Company and Subsidiaries (consolidated). When we refer to the “Parent,” we mean Wells Fargo & Company. See the “Glossary of Acronyms” for definitions of terms used throughout this Report.

Financial Review

Wells Fargo & Company is a leading financial services company that has approximately $1.9 trillion in assets. We provide a diversified set of banking, investment and mortgage products and services, as well as consumer and commercial finance, through our four reportable operating segments: Consumer Banking and Lending, Commercial Banking, Corporate and Investment Banking, and Wealth and Investment Management. Wells Fargo ranked No. 34 on Fortune’s 2024 rankings of America’s largest corporations. We ranked fourth in assets and third in the market value of our common stock among all U.S. banks at June 30, 2024.

Wells Fargo’s top priority remains building a risk and control infrastructure appropriate for its size and complexity. The Company is subject to a number of consent orders and other regulatory actions, some of which are described below. These regulatory actions may require the Company, among other things, to undertake certain changes to its business, operations, products and services, and risk management practices. Addressing these regulatory actions is expected to take multiple years, and we are likely to continue to experience issues or delays along the way in satisfying their requirements. We are also likely to continue to identify more issues as we implement our risk and control infrastructure, which may result in additional regulatory actions. Regulators have indicated the potential for escalating consequences for banks that do not timely resolve open issues or have repeat issues. Furthermore, issues or delays with one regulatory action could affect our progress on others. Failure to satisfy the requirements of a regulatory action on a timely basis could result in additional fines, penalties, business restrictions, limitations on subsidiary capital distributions, increased capital or liquidity requirements, enforcement actions, and other adverse consequences, which could be significant. While we still have significant work to do and have not yet satisfied certain aspects of these regulatory actions, the Company is committed to devoting the resources necessary to operate with strong business practices and controls, maintain the highest level of integrity, and have an appropriate culture in place.

Federal Reserve Board Consent Order Regarding Governance Oversight and Compliance and Operational Risk Management

On February 2, 2018, the Company entered into a consent order with the Board of Governors of the Federal Reserve System (FRB). As required by the consent order, the Company’s Board of Directors (Board) submitted to the FRB a plan to further enhance the Board’s governance and oversight of the Company, and the Company submitted to the FRB a plan to further improve the Company’s compliance and operational risk management program. The Company continues to engage with the FRB as the

Company works to address the consent order provisions. The consent order also requires the Company, following the FRB’s acceptance and approval of the plans and the Company’s adoption and implementation of the plans, to complete an initial third-party review of the enhancements and improvements provided for in the plans. Until this third-party review is complete and the plans are adopted and implemented to the satisfaction of the FRB, the Company’s total consolidated assets as defined under the consent order will be limited to the level as of December 31, 2017. Compliance with this asset cap is measured on a two-quarter daily average basis to allow for management of temporary fluctuations. After removal of the asset cap, a second third-party review must also be conducted to assess the efficacy and sustainability of the enhancements and improvements.

Consent Orders with the Consumer Financial Protection Bureau and Office of the Comptroller of the Currency Regarding Compliance Risk Management Program, Automobile Collateral Protection Insurance Policies, and Mortgage Interest Rate Lock Extensions

On April 20, 2018, the Company entered into consent orders with the Consumer Financial Protection Bureau (CFPB) and the Office of the Comptroller of the Currency (OCC) to pay an aggregate of $1 billion in civil money penalties to resolve matters regarding the Company’s compliance risk management program and past practices involving certain automobile collateral protection insurance policies and certain mortgage interest rate lock extensions. As required by the consent orders, the Company submitted to the CFPB and OCC an enterprise-wide compliance risk management plan and a plan to enhance the Company’s internal audit program with respect to federal consumer financial law and the terms of the consent orders. In addition, as required by the consent orders, the Company submitted for non-objection plans to remediate customers affected by the automobile collateral protection insurance and mortgage interest rate lock matters, as well as a plan for the management of remediation activities conducted by the Company. The Company continues to work to address the provisions of the consent orders. On September 9, 2021, the OCC assessed a $250 million civil money penalty against the Company related to insufficient progress in addressing requirements under the OCC’s April 2018 consent order and loss mitigation activities in the Company’s Home Lending business. On December 20, 2022, the CFPB modified its consent order to clarify how it would terminate.

Consent Order with the OCC Regarding Loss Mitigation Activities

On September 9, 2021, the Company entered into a consent order with the OCC requiring the Company to improve the execution, risk management, and oversight of loss mitigation activities in its Home Lending business. In addition, the consent order restricts the Company from acquiring certain third-party residential mortgage servicing and limits transfers of certain mortgage loans requiring customer remediation out of the Company’s mortgage servicing portfolio until remediation is provided.

Consent Order with the CFPB Regarding Automobile Lending, Consumer Deposit Accounts, and Mortgage Lending

On December 20, 2022, the Company entered into a consent order with the CFPB requiring the Company to provide customer remediation for multiple matters related to automobile lending, consumer deposit accounts, and mortgage lending; maintain practices designed to ensure auto lending customers receive refunds for the unused portion of certain guaranteed automobile protection agreements; comply with certain business practice requirements related to consumer deposit accounts; and pay a $1.7 billion civil penalty to the CFPB. The required actions related to many of these matters were already substantially complete at the time we entered into the consent order, and the consent order lays out a path to termination after the Company completes the remainder of the required actions.

Customer Remediation Activities

Our work to build a better company has included an effort to identify areas or instances where customers may have experienced financial harm, provide remediation as appropriate, and implement additional operational and control procedures. We are working with our regulatory agencies in this effort.

We have accrued for the probable and estimable costs related to our customer remediation activities, which amounts may change based on additional facts and information, as well as ongoing reviews and communications with our regulators. We had $678 million and $819 million of accrued liabilities for customer remediation activities as of June 30, 2024, and December 31, 2023, respectively. As our ongoing reviews continue and as we continue to strengthen our risk and control infrastructure, we have identified and may in the future identify additional items or areas of potential concern. To the extent issues are identified, we will continue to assess any customer harm and provide remediation as appropriate.

Recent Developments

Capital Matters

On June 28, 2024, the Company announced that it had completed the 2024 Comprehensive Capital Analysis and Review (CCAR) stress test process. The Company expects its stress capital buffer (SCB) to be 3.80% for the period October 1, 2024, through September 30, 2025. The FRB has indicated that it will publish the Company's final SCB by August 31, 2024. Our SCB for the period October 1, 2023, through September 30, 2024, is 2.90%.

On July 23, 2024, the Board approved an increase to the Company's third quarter 2024 common stock dividend to $0.40 per share.

In July 2024, we issued $2.0 billion of our Preferred Stock, Series FF.

For additional information about capital planning, see the “Capital Management – Capital Planning and Stress Testing” section in this Report.

Federal Deposit Insurance Corporation Special Assessment

In November 2023, the Federal Deposit Insurance Corporation (FDIC) finalized a rule to recover losses to the FDIC deposit insurance fund as a result of bank failures in the first half of 2023. Under the rule, the FDIC will collect a special assessment based on an insured depository institution’s estimated amount of uninsured deposits. Upon the FDIC’s finalization of the rule, we expensed an estimated amount of our special assessment of $1.9 billion (pre-tax) in fourth quarter 2023. During 2024, the FDIC provided updates on losses to the deposit insurance fund, and we expensed an additional $52 million and $336 million (pre-tax) in the second quarter and first half of 2024, respectively, for the estimated amount of the special assessment. We expect the ultimate amount of the special assessment may continue to change as the FDIC determines the actual net losses to the deposit insurance fund.

Overdraft Fees Proposal

On January 17, 2024, the CFPB issued a proposed rule that would limit overdraft fees charged by certain banks. We expect a significant reduction to our overdraft fees, which are included in deposit-related fees, if the rule is adopted as currently proposed.

Debit Card Interchange Fees Proposal

On October 25, 2023, the FRB issued a proposed rule that would reduce the amount of debit card interchange fees received by debit card issuers. In addition, the proposed rule would allow for an update to the debit card interchange fee cap every other year based on an analysis of certain costs incurred by debit card issuers. We expect a significant reduction to our debit card interchange fees, which are included in card fees, if the rule is adopted as currently proposed.

Financial Performance

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Consolidated Financial Highlights | | | | | | | | | | | | | | | |

| Quarter ended June 30, | | | | | | Six months ended June 30, | | | | |

| ($ in millions) | 2024 | | 2023 | | $ Change | | % Change | | 2024 | | 2023 | | $ Change | | % Change |

| Selected income statement data | | | | | | | | | | | | | | | |

| Net interest income | $ | 11,923 | | 13,163 | | (1,240) | | | (9) | % | | $ | 24,150 | | 26,499 | | (2,349) | | | (9) | % |

| Noninterest income | 8,766 | | 7,370 | | 1,396 | | | 19 | | | 17,402 | | 14,763 | | 2,639 | | | 18 | |

| Total revenue | 20,689 | | 20,533 | | 156 | | | 1 | | | 41,552 | | 41,262 | | 290 | | | 1 | |

| Net charge-offs | 1,303 | | 764 | | 539 | | | 71 | | | 2,460 | | 1,328 | | 1,132 | | | 85 | |

| Change in the allowance for credit losses | (67) | | 949 | | (1,016) | | | NM | | (286) | | 1,592 | | (1,878) | | | NM |

| Provision for credit losses (1) | 1,236 | | 1,713 | | (477) | | | (28) | | | 2,174 | | 2,920 | | (746) | | | (26) | |

| Noninterest expense | 13,293 | | 12,987 | | 306 | | | 2 | | | 27,631 | | 26,663 | | 968 | | | 4 | |

| Income tax expense | 1,251 | | 930 | | 321 | | | 35 | | | 2,215 | | 1,896 | | 319 | | | 17 | |

| Wells Fargo net income | 4,910 | | 4,938 | | (28) | | | (1) | | | 9,529 | | 9,929 | | (400) | | | (4) | |

| Wells Fargo net income applicable to common stock | 4,640 | | 4,659 | | (19) | | | — | | | 8,953 | | 9,372 | | (419) | | | (4) | |

| | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | |

NM – Not meaningful

(1)Includes provision for credit losses for loans, debt securities, and other financial assets.

In second quarter 2024, we generated $4.9 billion of net income and diluted earnings per common share (EPS) of $1.33, compared with $4.9 billion of net income and diluted EPS of $1.25 in the same period a year ago. In the first half of 2024, we generated $9.5 billion of net income and diluted EPS of $2.53, compared with $9.9 billion of net income and diluted EPS of $2.48 in the same period a year ago. Financial performance for the second quarter and first half of 2024, compared with the same periods a year ago, included the following:

•total revenue increased due to higher noninterest income, partially offset by lower net interest income;

•provision for credit losses reflected decreases for auto loans, commercial real estate loans, and residential mortgage loans, partially offset by increases for credit card loans;

•noninterest expense increased due to higher operating losses, and technology, telecommunications and equipment expense, partially offset by lower professional and outside services expense;

•average loans decreased driven by a decline in loans in both our commercial and consumer loan portfolios; and

•average deposits decreased driven by reductions in Consumer Banking and Lending and Wealth and Investment Management, partially offset by growth in Corporate and Investment Banking and Corporate.

Capital and Liquidity

We maintained a strong capital position in the first half of 2024, with total equity of $178.1 billion at June 30, 2024, compared with $187.4 billion at December 31, 2023. In addition, capital and liquidity at June 30, 2024, included the following:

•our Common Equity Tier 1 (CET1) ratio was 11.01% under the Standardized Approach (our binding ratio), which continued to exceed the regulatory minimum and buffers of 8.90%;

•our total loss absorbing capacity (TLAC) as a percentage of total risk-weighted assets was 24.78%, compared with the regulatory minimum of 21.50%; and

•our liquidity coverage ratio (LCR) was 124%, which continued to exceed the regulatory minimum of 100%.

See the “Capital Management” and the “Risk Management – Asset/Liability Management – Liquidity Risk and Funding” sections in this Report for additional information regarding our capital and liquidity, including the calculation of our regulatory capital and liquidity amounts.

Credit Quality

Credit quality reflected the following:

•The allowance for credit losses (ACL) for loans of $14.8 billion at June 30, 2024, decreased $299 million from December 31, 2023.

•Our provision for credit losses for loans was $2.2 billion in the first half of 2024, compared with $3.0 billion in the same period a year ago. The ACL for loans and the provision for credit losses for loans reflected decreases for auto loans, commercial real estate loans, and residential mortgage loans, partially offset by increases for credit card loans.

•The allowance coverage for total loans was 1.61% at both June 30, 2024, and December 31, 2023.

•Commercial portfolio net loan charge-offs were $468 million, or 35 basis points of average commercial loans, in second quarter 2024, compared with net loan charge-offs of $200 million, or 15 basis points, in the same period a year ago, due to higher losses in all commercial portfolios, primarily in our commercial real estate portfolio driven by the office property type.

•Consumer portfolio net loan charge-offs were $833 million, or 88 basis points of average consumer loans, in second quarter 2024, compared with net loan charge-offs of $564 million, or 58 basis points, in the same period a year ago, due to higher losses in our credit card portfolio.

•Nonperforming assets (NPAs) of $8.7 billion at June 30, 2024, increased $207 million, or 2%, from December 31, 2023, driven by an increase in commercial real estate nonaccrual loans, predominantly within the office property type. NPAs represented 0.94% of total loans at June 30, 2024.

•Criticized loans in the commercial portfolio were $35.5 billion at June 30, 2024, compared with $33.0 billion at December 31, 2023, predominantly driven by increases in criticized commercial and industrial loans and criticized commercial real estate loans.

Wells Fargo net income for second quarter 2024 was $4.9 billion ($1.33 diluted EPS), compared with $4.9 billion ($1.25 diluted EPS) in the same period a year ago. Net income was stable in second quarter 2024, compared with the same period a year ago, predominantly due to a $1.2 billion decrease in net interest income, a $321 million increase in income tax expense, and a $306 million increase in noninterest expense, offset by a $1.4 billion increase in noninterest income and a $477 million decrease in provision for credit losses.

Net income for the first half of 2024 was $9.5 billion ($2.53 diluted EPS), compared with $9.9 billion ($2.48 diluted EPS) in the same period a year ago. Net income decreased in the first half of 2024, compared with the same period a year ago, predominantly due to a $2.3 billion decrease in net interest income and a $1.0 billion increase in noninterest expense, partially offset by a $2.6 billion increase in noninterest income.

Net Interest Income

Net interest income and net interest margin decreased in both the second quarter and first half of 2024, compared with the same periods a year ago, driven by the impact of higher interest rates on interest-bearing deposits and long-term debt, as well as lower loan balances, partially offset by higher interest rates on interest-earning assets. Late in second quarter 2024, we increased pricing on sweep deposits in advisory brokerage accounts, which we expect will lower future net interest income.

Table 1 presents the individual components of net interest income and net interest margin. Net interest income and net interest margin are presented on a taxable-equivalent basis in Table 1 to consistently reflect income from taxable and tax-exempt loans and debt and equity securities. The calculation for taxable-equivalent basis was based on a federal statutory tax rate of 21%.

For additional information about net interest income and net interest margin, see the “Earnings Performance – Net Interest Income” section in our 2023 Form 10-K.

Table 1: Average Balances, Yields and Rates Paid (Taxable-Equivalent Basis) (1)

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Quarter ended June 30, |

| 2024 | | 2023 |

| ($ in millions) | Average

balance | | Interest

income/

expense | | Average interest rates | | Average

balance | | Interest

income/

expense | | Average interest rates |

| Assets | | | | | | | | | | | |

| Interest-earning deposits with banks | $ | 196,436 | | | 2,467 | | | 5.05 | % | | $ | 129,236 | | | 1,450 | | | 4.50 | % |

| Federal funds sold and securities purchased under resale agreements | 71,769 | | | 942 | | | 5.27 | | | 69,505 | | | 820 | | | 4.73 | |

| Debt securities: | | | | | | | | | | | |

| Trading debt securities | 120,590 | | | 1,247 | | | 4.14 | | | 102,605 | | | 898 | | | 3.50 | |

| Available-for-sale debt securities | 150,024 | | | 1,577 | | | 4.21 | | | 149,320 | | | 1,388 | | | 3.72 | |

| Held-to-maturity debt securities | 258,631 | | | 1,706 | | | 2.64 | | | 279,093 | | | 1,829 | | | 2.62 | |

| Total debt securities | 529,245 | | | 4,530 | | | 3.43 | | | 531,018 | | | 4,115 | | | 3.10 | |

| Loans held for sale (2) | 7,091 | | | 133 | | | 7.53 | | | 6,031 | | | 94 | | | 6.22 | |

| Loans: | | | | | | | | | | | |

| Commercial and industrial – U.S. | 307,034 | | | 5,501 | | | 7.21 | | | 307,858 | | | 5,156 | | | 6.72 | |

| Commercial and industrial – Non-U.S. | 64,480 | | | 1,167 | | | 7.28 | | | 75,503 | | | 1,249 | | | 6.64 | |

| Commercial real estate mortgage | 123,731 | | | 2,058 | | | 6.69 | | | 130,222 | | | 2,076 | | | 6.39 | |

| Commercial real estate construction | 23,019 | | | 469 | | | 8.21 | | | 24,438 | | | 468 | | | 7.68 | |

| Lease financing | 16,519 | | | 226 | | | 5.47 | | | 15,010 | | | 178 | | | 4.76 | |

| Total commercial loans | 534,783 | | | 9,421 | | | 7.08 | | | 553,031 | | | 9,127 | | | 6.62 | |

| Residential mortgage – first lien | 245,876 | | | 2,143 | | | 3.49 | | | 253,797 | | | 2,109 | | | 3.32 | |

| Residential mortgage – junior lien | 10,313 | | | 191 | | | 7.45 | | | 12,331 | | | 210 | | | 6.83 | |

| Credit card | 52,642 | | | 1,668 | | | 12.75 | | | 46,762 | | | 1,511 | | | 12.96 | |

| Auto | 45,164 | | | 571 | | | 5.09 | | | 51,880 | | | 603 | | | 4.67 | |

| Other consumer | 28,199 | | | 601 | | | 8.56 | | | 28,105 | | | 582 | | | 8.29 | |

| Total consumer loans | 382,194 | | | 5,174 | | | 5.43 | | | 392,875 | | | 5,015 | | | 5.11 | |

| Total loans (2) | 916,977 | | | 14,595 | | | 6.40 | | | 945,906 | | | 14,142 | | | 5.99 | |

| Equity securities | 26,332 | | | 195 | | | 2.99 | | | 27,891 | | | 194 | | | 2.79 | |

| Other | 8,128 | | | 110 | | | 5.42 | | | 10,118 | | | 120 | | | 4.76 | |

| Total interest-earning assets | $ | 1,755,978 | | | 22,972 | | | 5.25 | % | | $ | 1,719,705 | | | 20,935 | | | 4.88 | % |

| Cash and due from banks | 28,398 | | | — | | | | | 27,344 | | | — | | | |

| Goodwill | 25,172 | | | — | | | | | 25,175 | | | — | | | |

| Other | 105,099 | | | — | | | | | 106,029 | | | — | | | |

| Total noninterest-earning assets | $ | 158,669 | | | — | | | | | 158,548 | | | — | | | |

| Total assets | $ | 1,914,647 | | | 22,972 | | | | | 1,878,253 | | | 20,935 | | | |

| Liabilities | | | | | | | | | | | |

| Deposits: | | | | | | | | | | | |

| Demand deposits | $ | 450,930 | | | 2,448 | | | 2.18 | % | | $ | 415,886 | | | 1,667 | | | 1.61 | % |

| Savings deposits | 353,715 | | | 1,123 | | | 1.28 | | | 386,831 | | | 734 | | | 0.76 | |

| Time deposits | 183,251 | | | 2,396 | | | 5.26 | | | 115,025 | | | 1,260 | | | 4.40 | |

| Deposits in non-U.S. offices | 18,910 | | | 182 | | | 3.86 | | | 19,144 | | | 144 | | | 3.02 | |

| Total interest-bearing deposits | 1,006,806 | | | 6,149 | | | 2.46 | | | 936,886 | | | 3,805 | | | 1.63 | |

| Short-term borrowings: | | | | | | | | | | | |

| Federal funds purchased and securities sold under agreements to repurchase | 91,572 | | | 1,227 | | | 5.39 | | | 66,568 | | | 811 | | | 4.89 | |

| Other short-term borrowings | 15,113 | | | 149 | | | 3.98 | | | 16,491 | | | 150 | | | 3.65 | |

| Total short-term borrowings | 106,685 | | | 1,376 | | | 5.19 | | | 83,059 | | | 961 | | | 4.64 | |

| Long-term debt | 182,201 | | | 3,164 | | | 6.95 | | | 170,843 | | | 2,693 | | | 6.31 | |

| Other liabilities | 34,613 | | | 271 | | | 3.13 | | | 34,496 | | | 208 | | | 2.41 | |

| Total interest-bearing liabilities | $ | 1,330,305 | | | 10,960 | | | 3.31 | % | | $ | 1,225,284 | | | 7,667 | | | 2.51 | % |

| Noninterest-bearing deposits | 339,672 | | | — | | | | | 410,563 | | | — | | | |

| Other noninterest-bearing liabilities | 63,118 | | | — | | | | | 57,963 | | | — | | | |

| Total noninterest-bearing liabilities | $ | 402,790 | | | — | | | | | 468,526 | | | — | | | |

| Total liabilities | $ | 1,733,095 | | | 10,960 | | | | | 1,693,810 | | | 7,667 | | | |

| Total equity | 181,552 | | | — | | | | | 184,443 | | | — | | | |

| Total liabilities and equity | $ | 1,914,647 | | | 10,960 | | | | | 1,878,253 | | | 7,667 | | | |

| | | | | | | | | | | |

| Interest rate spread on a taxable-equivalent basis (3) | | | | | 1.94 | % | | | | | | 2.37 | % |

| Net interest income and net interest margin on a taxable-equivalent basis (3) | | | $ | 12,012 | | | 2.75 | % | | | | $ | 13,268 | | | 3.09 | % |

(continued on following page)

Earnings Performance (continued)

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| |

| Six months ended June 30, |

| | | | | 2024 | | | | | | 2023 | | | | | | |

| ($ in millions) | Average

balance | | Interest

income/

expense | | Average interest rates | | Average

balance | | Interest

income/

expense | | Average interest rates | | | | | | |

| Assets | | | | | | | | | | | | | | | | | |

| Interest-earning deposits with banks | $ | 202,002 | | | 5,040 | | | 5.02 | % | | $ | 122,087 | | | 2,617 | | | 4.32 | % | | | | | | |

| Federal funds sold and securities purchased under resale agreements | 70,744 | | | 1,856 | | | 5.28 | | | 69,071 | | | 1,516 | | | 4.43 | | | | | | | |

| Debt securities: | | | | | | | | | | | | | | | | | |

| Trading debt securities | 116,380 | | | 2,391 | | | 4.11 | | | 99,522 | | | 1,699 | | | 3.42 | | | | | | | |

| Available-for-sale debt securities | 145,005 | | | 2,973 | | | 4.11 | | | 147,616 | | | 2,670 | | | 3.63 | | | | | | | |

| Held-to-maturity debt securities | 261,693 | | | 3,489 | | | 2.67 | | | 279,522 | | | 3,609 | | | 2.59 | | | | | | | |

| Total debt securities | 523,078 | | | 8,853 | | | 3.39 | | | 526,660 | | | 7,978 | | | 3.04 | | | | | | | |

| Loans held for sale (2) | 6,463 | | | 247 | | | 7.66 | | | 6,320 | | | 191 | | | 6.05 | | | | | | | |

| Loans: | | | | | | | | | | | | | | | | | |

| Commercial and industrial – U.S. | 306,097 | | | 10,938 | | | 7.18 | | | 307,519 | | | 9,928 | | | 6.51 | | | | | | | |

| Commercial and industrial – Non-U.S. | 67,457 | | | 2,444 | | | 7.28 | | | 75,800 | | | 2,383 | | | 6.34 | | | | | | | |

| Commercial real estate mortgage | 125,013 | | | 4,161 | | | 6.69 | | | 130,532 | | | 4,025 | | | 6.22 | | | | | | | |

| Commercial real estate construction | 23,404 | | | 957 | | | 8.23 | | | 24,333 | | | 906 | | | 7.51 | | | | | | | |

| Lease financing | 16,440 | | | 444 | | | 5.40 | | | 14,922 | | | 350 | | | 4.69 | | | | | | | |

| Total commercial loans | 538,411 | | | 18,944 | | | 7.07 | | | 553,106 | | | 17,592 | | | 6.41 | | | | | | | |

| Residential mortgage – first lien | 247,067 | | | 4,287 | | | 3.47 | | | 254,404 | | | 4,197 | | | 3.30 | | | | | | | |

| Residential mortgage – junior lien | 10,553 | | | 389 | | | 7.41 | | | 12,647 | | | 420 | | | 6.68 | | | | | | | |

| Credit card | 52,175 | | | 3,357 | | | 12.94 | | | 46,304 | | | 2,951 | | | 12.85 | | | | | | | |

| Auto | 46,139 | | | 1,155 | | | 5.04 | | | 52,470 | | | 1,200 | | | 4.61 | | | | | | | |

| Other consumer | 28,181 | | | 1,204 | | | 8.59 | | | 28,340 | | | 1,127 | | | 8.02 | | | | | | | |

| Total consumer loans | 384,115 | | | 10,392 | | | 5.43 | | | 394,165 | | | 9,895 | | | 5.04 | | | | | | | |

| Total loans (2) | 922,526 | | | 29,336 | | | 6.39 | | | 947,271 | | | 27,487 | | | 5.84 | | | | | | | |

| Equity securities | 23,841 | | | 345 | | | 2.91 | | | 28,269 | | | 364 | | | 2.59 | | | | | | | |

| Other | 8,534 | | | 224 | | | 5.27 | | | 10,578 | | | 245 | | | 4.67 | | | | | | | |

| Total interest-earning assets | $ | 1,757,188 | | | 45,901 | | | 5.25 | % | | $ | 1,710,256 | | | 40,398 | | | 4.75 | % | | | | | | |

| Cash and due from banks | 27,957 | | | — | | | | | 27,743 | | | — | | | | | | | | | |

| Goodwill | 25,173 | | | — | | | | | 25,174 | | | — | | | | | | | | | |

| Other | 105,492 | | | — | | | | | 107,832 | | | — | | | | | | | | | |

| Total noninterest-earning assets | $ | 158,622 | | | — | | | | | 160,749 | | | — | | | | | | | | | |

| Total assets | $ | 1,915,810 | | | 45,901 | | | | | 1,871,005 | | | 40,398 | | | | | | | | | |

| Liabilities | | | | | | | | | | | | | | | | | |

| Deposits: | | | | | | | | | | | | | | | | | |

| Demand deposits | $ | 445,053 | | | 4,702 | | | 2.12 | % | | $ | 418,347 | | | 3,046 | | | 1.47 | % | | | | | | |

| Savings deposits | 352,261 | | | 2,030 | | | 1.16 | | | 394,515 | | | 1,281 | | | 0.66 | | | | | | | |

| Time deposits | 185,004 | | | 4,849 | | | 5.27 | | | 97,045 | | | 1,985 | | | 4.12 | | | | | | | |

| Deposits in non-U.S. offices | 19,522 | | | 379 | | | 3.90 | | | 18,695 | | | 254 | | | 2.74 | | | | | | | |

| Total interest-bearing deposits | 1,001,840 | | | 11,960 | | | 2.40 | | | 928,602 | | | 6,566 | | | 1.43 | | | | | | | |

| Short-term borrowings: | | | | | | | | | | | | | | | | | |

| Federal funds purchased and securities sold under agreements to repurchase | 85,244 | | | 2,281 | | | 5.38 | | | 52,977 | | | 1,227 | | | 4.67 | | | | | | | |

| Other short-term borrowings | 15,592 | | | 313 | | | 4.04 | | | 17,868 | | | 304 | | | 3.43 | | | | | | | |

| Total short-term borrowings | 100,836 | | | 2,594 | | | 5.17 | | | 70,845 | | | 1,531 | | | 4.36 | | | | | | | |

| Long-term debt | 189,659 | | | 6,513 | | | 6.87 | | | 171,700 | | | 5,204 | | | 6.07 | | | | | | | |

| Other liabilities | 33,717 | | | 506 | | | 3.01 | | | 33,964 | | | 386 | | | 2.29 | | | | | | | |

| Total interest-bearing liabilities | $ | 1,326,052 | | | 21,573 | | | 3.27 | % | | $ | 1,205,111 | | | 13,687 | | | 2.28 | % | | | | | | |

| Noninterest-bearing deposits | 342,212 | | | — | | | | | 423,444 | | | — | | | | | | | | | |

| Other noninterest-bearing liabilities | 63,435 | | | — | | | | | 58,079 | | | — | | | | | | | | | |

| Total noninterest-bearing liabilities | $ | 405,647 | | | — | | | | | 481,523 | | | — | | | | | | | | | |

| Total liabilities | $ | 1,731,699 | | | 21,573 | | | | | 1,686,634 | | | 13,687 | | | | | | | | | |

| Total equity | 184,111 | | | — | | | | | 184,371 | | | — | | | | | | | | | |

| Total liabilities and equity | $ | 1,915,810 | | | 21,573 | | | | | 1,871,005 | | | 13,687 | | | | | | | | | |

| | | | | | | | | | | | | | | | | |

| Interest rate spread on a taxable-equivalent basis (3) | | | | | 1.98 | % | | | | | | 2.47 | % | | | | | | |

Net interest margin and net interest income on a taxable-equivalent basis (3) | | | $ | 24,328 | | | 2.78 | % | | | | $ | 26,711 | | | 3.14 | % | | | | | | |

(1)The average balance amounts represent amortized costs, except for certain held-to-maturity (HTM) debt securities, which exclude unamortized basis adjustments related to the transfer of those securities from available-for-sale (AFS) debt securities. The average interest rates are based on interest income or expense amounts for the period and are annualized. Interest rates and amounts include the effects of hedge and risk management activities associated with the respective asset and liability categories.

(2)Nonaccrual loans and any related income are included in their respective loan categories.

(3)Includes taxable-equivalent adjustments of $89 million and $105 million for the quarters ended June 30, 2024 and 2023, respectively, and $178 million and $212 million for the first half of 2024 and 2023, respectively, predominantly related to tax-exempt income on certain loans and securities.

Noninterest Income

Table 2: Noninterest Income

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Quarter ended June 30, | | | | | | Six months ended June 30, | | | | |

| | | | | | | | | | | |

| ($ in millions) | 2024 | | 2023 | | $ Change | | % Change | | 2024 | | 2023 | | $ Change | | % Change |

| Deposit-related fees | $ | 1,249 | | | 1,165 | | | 84 | | | 7 | % | | $ | 2,479 | | | 2,313 | | | 166 | | | 7 | % |

| Lending-related fees | 369 | | | 352 | | | 17 | | | 5 | | | 736 | | | 708 | | | 28 | | | 4 | |

| Investment advisory and other asset-based fees | 2,415 | | | 2,163 | | | 252 | | | 12 | | | 4,746 | | | 4,277 | | | 469 | | | 11 | |

| Commissions and brokerage services fees | 614 | | | 570 | | | 44 | | | 8 | | | 1,240 | | | 1,189 | | | 51 | | | 4 | |

| Investment banking fees | 641 | | | 376 | | | 265 | | | 70 | | | 1,268 | | | 702 | | | 566 | | | 81 | |

| Card fees | 1,101 | | | 1,098 | | | 3 | | | — | | | 2,162 | | | 2,131 | | | 31 | | | 1 | |

| Net servicing income | 127 | | | 100 | | | 27 | | | 27 | | | 252 | | | 212 | | | 40 | | | 19 | |

| Net gains on mortgage loan originations/sales | 116 | | | 102 | | | 14 | | | 14 | | | 221 | | | 222 | | | (1) | | | — | |

| Mortgage banking | 243 | | | 202 | | | 41 | | | 20 | | | 473 | | | 434 | | | 39 | | | 9 | |

| Net gains from trading activities | 1,442 | | | 1,122 | | | 320 | | | 29 | | | 2,896 | | | 2,464 | | | 432 | | | 18 | |

| Net gains (losses) from debt securities | — | | | 4 | | | (4) | | | (100) | | | (25) | | | 4 | | | (29) | | | NM |

| Net gains (losses) from equity securities | 80 | | | (94) | | | 174 | | | 185 | | | 98 | | | (451) | | | 549 | | | 122 | |

| Lease income | 292 | | | 307 | | | (15) | | | (5) | | | 713 | | | 654 | | | 59 | | | 9 | |

| Other | 320 | | | 105 | | | 215 | | | 205 | | | 616 | | | 338 | | | 278 | | | 82 | |

| Total | $ | 8,766 | | | 7,370 | | | 1,396 | | | 19 | | | $ | 17,402 | | | 14,763 | | | 2,639 | | | 18 | |

NM – Not meaningfulSecond quarter 2024 vs. second quarter 2023

Deposit-related fees increased reflecting higher treasury management fees on commercial accounts driven by increased transaction service volumes and repricing.

Investment advisory and other asset-based fees increased driven by higher asset-based fees reflecting higher market valuations.

Fees from the majority of Wealth and Investment Management (WIM) advisory assets are based on a percentage of the market value of the assets at the beginning of the quarter. For additional information on certain client investment assets, see the “Earnings Performance – Operating Segment Results – Wealth and Investment Management – WIM Advisory Assets” section in this Report.

Investment banking fees increased due to increased activity across all products.

Net gains from trading activities increased driven by higher revenue in equities and structured products.

Net gains (losses) from equity securities increased driven by higher unrealized gains on nonmarketable equity securities from our venture capital investments.

Other income increased driven by impacts related to the expanded use of the proportional amortization method of accounting for renewable energy tax credit investments as a result of our adoption in first quarter 2024 of Accounting Standards Update (ASU) 2023-02 – Investments – Equity Method and Joint Ventures (Topic 323): Accounting for Investments in Tax Credit Structures Using the Proportional Amortization Method. For additional information on our adoption of ASU 2023-02, see Note 1 (Summary of Significant Accounting Policies) to Financial Statements in this Report.

First half of 2024 vs. first half of 2023

Deposit-related fees increased reflecting higher treasury management fees on commercial accounts driven by increased transaction service volumes and repricing.

Investment advisory and other asset-based fees increased driven by higher asset-based fees reflecting higher market valuations.

Investment banking fees increased due to increased activity across all products.

Net gains from trading activities increased driven by higher revenue in structured products, equities, and foreign exchange, partially offset by lower revenue in rates.

Net gains (losses) from equity securities increased driven by:

•lower impairment of equity securities from our venture capital investments; and

•higher unrealized gains on nonmarketable equity securities from our venture capital investments.

Lease income increased driven by a gain associated with the resolution of a legacy lease transaction.

Other income increased driven by impacts related to the expanded use of the proportional amortization method of accounting for renewable energy tax credit investments as a result of our adoption of ASU 2023-02 in first quarter 2024.

Earnings Performance (continued)

Noninterest Expense

Table 3: Noninterest Expense

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Quarter ended June 30, | | | | | | Six months ended June 30, | | | | |

| | | | | | | | | | | |

| ($ in millions) | 2024 | | 2023 | | $ Change | | % Change | | 2024 | | 2023 | | $ Change | | % Change |

| Personnel | $ | 8,575 | | | 8,606 | | | (31) | | | — | % | | $ | 18,067 | | | 18,021 | | | 46 | | | — | % |

| Technology, telecommunications and equipment | 1,106 | | | 947 | | | 159 | | | 17 | | | 2,159 | | | 1,869 | | | 290 | | | 16 | |

| Occupancy | 763 | | | 707 | | | 56 | | | 8 | | | 1,477 | | | 1,420 | | | 57 | | | 4 | |

| Operating losses (1) | 493 | | | 232 | | | 261 | | | 113 | | | 1,126 | | | 499 | | | 627 | | | 126 | |

| Professional and outside services | 1,139 | | | 1,304 | | | (165) | | | (13) | | | 2,240 | | | 2,533 | | | (293) | | | (12) | |

| Leases (2) | 159 | | | 180 | | | (21) | | | (12) | | | 323 | | | 357 | | | (34) | | | (10) | |

| Advertising and promotion | 224 | | | 184 | | | 40 | | | 22 | | | 421 | | | 338 | | | 83 | | | 25 | |

| | | | | | | | | | | | | | | |

| Other | 834 | | | 827 | | | 7 | | | 1 | | | 1,818 | | | 1,626 | | | 192 | | | 12 | |

| Total | $ | 13,293 | | | 12,987 | | | 306 | | | 2 | | | $ | 27,631 | | | 26,663 | | | 968 | | | 4 | |

(1)Includes expenses for customer remediation activities of $184 million and $106 million for second quarter 2024 and 2023, respectively, and $612 million and $163 million for the first half of 2024 and 2023, respectively.

(2)Represents expenses for assets we lease to customers.

Second quarter 2024 vs. second quarter 2023

Personnel expense decreased due to the impact of efficiency initiatives, partially offset by higher revenue-related compensation expense driven by higher fees in our Wealth and Investment Management business.

Technology, telecommunications and equipment expense increased due to higher expense for the amortization of internally developed software.

Operating losses increased driven by higher expense for legal actions and higher expense for customer remediation activities related to the further refinement of the remediation costs for historical mortgage lending and other consumer products matters. For additional information on customer remediation activities, see the “Overview” section above.

As previously disclosed, we have outstanding legal actions and customer remediation activities that could impact operating losses in the coming quarters.

For additional information on operating losses, see Note 18 (Revenue and Expenses) to Financial Statements in this Report.

Professional and outside services expense decreased driven by efficiency initiatives to reduce our spending on consultants and contractors.

First half of 2024 vs. first half of 2023

Personnel expense increased due to higher revenue-related compensation expense driven by higher fees in our Wealth and Investment Management business, partially offset by the impact of efficiency initiatives.

Technology, telecommunications and equipment expense increased due to higher expense for the amortization of internally developed software.

Operating losses increased driven by higher expense for legal actions and higher expense for customer remediation activities related to the further refinement of the remediation costs for historical mortgage lending and other consumer products matters.

As previously disclosed, we have outstanding legal actions and customer remediation activities that could impact operating losses in the coming quarters.

Professional and outside services expense decreased driven by efficiency initiatives to reduce our spending on consultants and contractors.

Advertising and promotion expense increased due to higher marketing volume.

Other expense increased reflecting an additional expense of $336 million for the estimated FDIC special assessment. For additional information on the FDIC’s special assessment, see Note 18 (Revenue and Expenses) to Financial Statements in this Report.

Income Tax Expense

Table 4: Income Tax Expense

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | |

| Quarter ended June 30, | | | | | | Six months ended June 30, | | | | | |

| ($ in millions) | 2024 | | 2023 | | $ Change | | % Change | | 2024 | | 2023 | | $ Change | | % Change | |

| Income before income tax expense | $ | 6,160 | | | 5,833 | | | 327 | | | 6 | % | | $ | 11,747 | | | 11,679 | | | 68 | | | 1 | % | |

| Income tax expense | 1,251 | | | 930 | | | 321 | | | 35 | | | 2,215 | | | 1,896 | | | 319 | | | 17 | | |

| Effective income tax rate (1) | 20.3 | % | | 15.8 | | | | | | | 18.9 | % | | 16.0 | | | | | | |

(1)Represents (i) Income tax expense (benefit) divided by (ii) Income (loss) before income tax expense (benefit) less Net income (loss) from noncontrolling interests.

The increase in the effective income tax rate for the second quarter and first half of 2024, compared with the same periods a year ago, was driven by the impacts related to the expanded use of the proportional amortization method of accounting for renewable energy tax credit investments. For additional information on our adoption in first quarter 2024 of Accounting Standards Update (ASU) 2023-02 – Investments – Equity Method and Joint Ventures (Topic 323): Accounting for Investments in Tax Credit Structures Using the Proportional Amortization Method, see Note 1 (Summary of Significant Accounting Policies) to Financial Statements in this Report.

For additional information on income taxes, see Note 23 (Income Taxes) to Financial Statements in our 2023 Form 10-K.

Earnings Performance (continued)

Operating Segment Results

Our management reporting is organized into four reportable operating segments: Consumer Banking and Lending; Commercial Banking; Corporate and Investment Banking; and Wealth and Investment Management. All other business activities that are not included in the reportable operating segments have been included in Corporate. For additional information, see Table 5 below. We define our reportable operating segments by type of product and customer segment, and their results are based on our management reporting process. The management reporting process measures the performance of the reportable operating segments based on the Company’s management structure, and the results are regularly reviewed with our Chief Executive Officer and relevant senior management. The management reporting process is based on U.S. GAAP and includes specific adjustments, such as funds transfer pricing for asset/liability management, shared revenue and expenses, and taxable-equivalent adjustments to consistently reflect income from taxable and tax-exempt sources, which allows management to assess performance consistently across the operating segments.

Funds Transfer Pricing Corporate treasury manages a funds transfer pricing methodology that considers interest rate risk, liquidity risk, and other product characteristics. Operating segments pay a funding charge for their assets and receive a funding credit for their deposits, both of which are included in net interest income. The net impact of the funding charges or credits is recognized in corporate treasury.

Revenue and Expense Sharing When lines of business jointly serve customers, the line of business that is responsible for providing the product or service recognizes revenue or expense with a referral fee paid or an allocation of cost to the other line of

business based on established internal revenue-sharing agreements.

When a line of business uses a service provided by another line of business or enterprise function (included in Corporate), expense is generally allocated based on the cost and use of the service provided. We periodically assess and update our revenue and expense allocation methodologies.

Taxable-Equivalent Adjustments Taxable-equivalent adjustments related to tax-exempt income on certain loans and debt securities are included in net interest income, while taxable-equivalent adjustments related to income tax credits for affordable housing and renewable energy investments are included in noninterest income, in each case with corresponding impacts to income tax expense (benefit). Adjustments are included in Corporate, Commercial Banking, and Corporate and Investment Banking and are eliminated to reconcile to the Company’s consolidated financial results.

Allocated Capital Reportable operating segments are allocated capital under a risk-sensitive framework that is primarily based on aspects of our regulatory capital requirements, and the assumptions and methodologies used to allocate capital are periodically assessed and updated. Management believes that return on allocated capital is a useful financial measure because it enables management, investors, and others to assess a reportable operating segment’s use of capital.

Selected Metrics We present certain financial and nonfinancial metrics that management uses when evaluating reportable operating segment results. Management believes that these metrics are useful to investors and others to assess the performance, customer growth, and trends of reportable operating segments or lines of business.

Table 5: Management Reporting Structure

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Wells Fargo & Company | | | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | Consumer Banking and Lending | | | | Commercial Banking | | | | Corporate and Investment Banking | | | | Wealth and Investment Management | | | Corporate | | | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | |

• Consumer, Small and Business Banking

• Home Lending

• Credit Card

• Auto

• Personal Lending | | | |

• Middle Market Banking

• Asset-Based Lending and Leasing | | | |

• Banking

• Commercial Real Estate

• Markets | | | |

• Wells Fargo Advisors

• The Private

Bank | | | |

• Corporate Treasury

• Enterprise Functions

• Investment Portfolio

• Venture capital and private equity investments

• Non-strategic businesses | | | |

| | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Table 6 and the following discussion present our results by reportable operating segment. For additional information, see Note 17 (Operating Segments) to Financial Statements in this Report.

Table 6: Operating Segment Results – Highlights

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| |

| (in millions) | Consumer Banking and Lending | | Commercial Banking | | Corporate and Investment Banking | | Wealth and Investment Management | | Corporate (1) | | Reconciling Items (2) | | Consolidated Company |

| Quarter ended June 30, 2024 | | | | | | | | | | | | | |

| Net interest income | $ | 7,024 | | | 2,281 | | | 1,945 | | | 906 | | | (144) | | | (89) | | | 11,923 | |

| Noninterest income | 1,982 | | | 841 | | | 2,893 | | | 2,952 | | | 392 | | | (294) | | | 8,766 | |

| Total revenue | 9,006 | | | 3,122 | | | 4,838 | | | 3,858 | | | 248 | | | (383) | | | 20,689 | |

| Provision for credit losses | 932 | | | 29 | | | 285 | | | (14) | | | 4 | | | — | | | 1,236 | |

| Noninterest expense | 5,701 | | | 1,506 | | | 2,170 | | | 3,193 | | | 723 | | | — | | | 13,293 | |

| Income (loss) before income tax expense (benefit) | 2,373 | | | 1,587 | | | 2,383 | | | 679 | | | (479) | | | (383) | | | 6,160 | |

| Income tax expense (benefit) | 596 | | | 402 | | | 598 | | | 195 | | | (157) | | | (383) | | | 1,251 | |

| Net income (loss) before noncontrolling interests | 1,777 | | | 1,185 | | | 1,785 | | | 484 | | | (322) | | | — | | | 4,909 | |

| Less: Net income (loss) from noncontrolling interests | — | | | 3 | | | — | | | — | | | (4) | | | — | | | (1) | |

| Net income (loss) | $ | 1,777 | | | 1,182 | | | 1,785 | | | 484 | | | (318) | | | — | | | 4,910 | |

| Quarter ended June 30, 2023 | | | | | | | | | | | | | |

| Net interest income | $ | 7,490 | | | 2,501 | | | 2,359 | | | 1,009 | | | (91) | | | (105) | | | 13,163 | |

| Noninterest income | 1,965 | | | 868 | | | 2,272 | | | 2,639 | | | 121 | | | (495) | | | 7,370 | |

| Total revenue | 9,455 | | | 3,369 | | | 4,631 | | | 3,648 | | | 30 | | | (600) | | | 20,533 | |

| Provision for credit losses | 874 | | | 26 | | | 933 | | | 24 | | | (144) | | | — | | | 1,713 | |

| Noninterest expense | 6,027 | | | 1,630 | | | 2,087 | | | 2,974 | | | 269 | | | — | | | 12,987 | |

| Income (loss) before income tax expense (benefit) | 2,554 | | | 1,713 | | | 1,611 | | | 650 | | | (95) | | | (600) | | | 5,833 | |

| Income tax expense (benefit) | 640 | | | 429 | | | 401 | | | 163 | | | (103) | | | (600) | | | 930 | |

| Net income before noncontrolling interests | 1,914 | | | 1,284 | | | 1,210 | | | 487 | | | 8 | | | — | | | 4,903 | |

| Less: Net income (loss) from noncontrolling interests | — | | | 3 | | | — | | | — | | | (38) | | | — | | | (35) | |

| Net income | $ | 1,914 | | | 1,281 | | | 1,210 | | | 487 | | | 46 | | | — | | | 4,938 | |

| Six months ended June 30, 2024 | | | | | | | | | | | | | |

| Net interest income | $ | 14,134 | | | 4,559 | | | 3,972 | | | 1,775 | | | (112) | | | (178) | | | 24,150 | |

| Noninterest income | 3,963 | | | 1,715 | | | 5,848 | | | 5,825 | | | 683 | | | (632) | | | 17,402 | |

| Total revenue | 18,097 | | | 6,274 | | | 9,820 | | | 7,600 | | | 571 | | | (810) | | | 41,552 | |

| Provision for credit losses | 1,720 | | | 172 | | | 290 | | | (11) | | | 3 | | | — | | | 2,174 | |

| Noninterest expense | 11,725 | | | 3,185 | | | 4,500 | | | 6,423 | | | 1,798 | | | — | | | 27,631 | |

| Income (loss) before income tax expense (benefit) | 4,652 | | | 2,917 | | | 5,030 | | | 1,188 | | | (1,230) | | | (810) | | | 11,747 | |

| Income tax expense (benefit) | 1,169 | | | 743 | | | 1,264 | | | 323 | | | (474) | | | (810) | | | 2,215 | |

| Net income (loss) before noncontrolling interests | 3,483 | | | 2,174 | | | 3,766 | | | 865 | | | (756) | | | — | | | 9,532 | |

| Less: Net income (loss) from noncontrolling interests | — | | | 6 | | | — | | | — | | | (3) | | | — | | | 3 | |

| Net income (loss) | $ | 3,483 | | | 2,168 | | | 3,766 | | | 865 | | | (753) | | | — | | | 9,529 | |

| Six months ended June 30, 2023 | | | | | | | | | | | | | |

| Net interest income | $ | 14,923 | | | 4,990 | | | 4,820 | | | 2,053 | | | (75) | | | (212) | | | 26,499 | |

| Noninterest income | 3,896 | | | 1,686 | | | 4,713 | | | 5,276 | | | 126 | | | (934) | | | 14,763 | |

| Total revenue | 18,819 | | | 6,676 | | | 9,533 | | | 7,329 | | | 51 | | | (1,146) | | | 41,262 | |

| Provision for credit losses | 1,741 | | | (17) | | | 1,185 | | | 35 | | | (24) | | | — | | | 2,920 | |

| Noninterest expense | 12,065 | | | 3,382 | | | 4,304 | | | 6,035 | | | 877 | | | — | | | 26,663 | |

| Income (loss) before income tax expense (benefit) | 5,013 | | | 3,311 | | | 4,044 | | | 1,259 | | | (802) | | | (1,146) | | | 11,679 | |

| Income tax expense (benefit) | 1,258 | | | 828 | | | 1,016 | | | 315 | | | (375) | | | (1,146) | | | 1,896 | |

| Net income (loss) before noncontrolling interests | 3,755 | | | 2,483 | | | 3,028 | | | 944 | | | (427) | | | — | | | 9,783 | |

| Less: Net income (loss) from noncontrolling interests | — | | | 6 | | | — | | | — | | | (152) | | | — | | | (146) | |

| Net income (loss) | $ | 3,755 | | | 2,477 | | | 3,028 | | | 944 | | | (275) | | | — | | | 9,929 | |

| | | | | | | | | | | | | |

| | | | | | | | | | | | | |

| | | | | | | | | | | | | |

| | | | | | | | | | | | | |

| | | | | | | | | | | | | |

| | | | | | | | | | | | | |

| | | | | | | | | | | | | |

| | | | | | | | | | | | | |

| | | | | | | | | | | | | |

| | | | | | | | | | | | | |

| | | | | | | | | | | | | |

(1)All other business activities that are not included in the reportable operating segments have been included in Corporate. For additional information, see the “Corporate” section below.

(2)Taxable-equivalent adjustments related to tax-exempt income on certain loans and debt securities are included in net interest income, while taxable-equivalent adjustments related to income tax credits for affordable housing and renewable energy investments are included in noninterest income, in each case with corresponding impacts to income tax expense (benefit). Adjustments are included in Corporate, Commercial Banking, and Corporate and Investment Banking and are eliminated to reconcile to the Company’s consolidated financial results.

Earnings Performance (continued)

Consumer Banking and Lending offers diversified financial products and services for consumers and small businesses with annual sales generally up to $10 million. These financial products and services include checking and savings accounts, credit and

debit cards, as well as home, auto, personal, and small business lending. Table 6a and Table 6b provide additional information for Consumer Banking and Lending.

Table 6a: Consumer Banking and Lending – Income Statement and Selected Metrics | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Quarter ended June 30, | | | | | | Six months ended June 30, | | | | | | | | | | |

| ($ in millions, unless otherwise noted) | 2024 | | 2023 | | $ Change | | % Change | | 2024 | | 2023 | | $ Change | | % Change | | | | | | |

| Income Statement | | | | | | | | | | | | | | | | | | | | | |

| Net interest income | $ | 7,024 | | | 7,490 | | | (466) | | | (6) | % | | $ | 14,134 | | | 14,923 | | | (789) | | | (5) | % | | | | | | |

| Noninterest income: | | | | | | | | | | | | | | | | | | | | | |

| Deposit-related fees | 690 | | | 666 | | | 24 | | | 4 | | | 1,367 | | | 1,338 | | | 29 | | | 2 | | | | | | | |

| Card fees | 1,036 | | | 1,022 | | | 14 | | | 1 | | | 2,026 | | | 1,980 | | | 46 | | | 2 | | | | | | | |

| Mortgage banking | 135 | | | 132 | | | 3 | | | 2 | | | 328 | | | 292 | | | 36 | | | 12 | | | | | | | |

| Other | 121 | | | 145 | | | (24) | | | (17) | | | 242 | | | 286 | | | (44) | | | (15) | | | | | | | |

| Total noninterest income | 1,982 | | | 1,965 | | | 17 | | | 1 | | | 3,963 | | | 3,896 | | | 67 | | | 2 | | | | | | | |

| Total revenue | 9,006 | | | 9,455 | | | (449) | | | (5) | | | 18,097 | | | 18,819 | | | (722) | | | (4) | | | | | | | |

| Net charge-offs | 907 | | | 621 | | | 286 | | | 46 | | | 1,788 | | | 1,210 | | | 578 | | | 48 | | | | | | | |

| Change in the allowance for credit losses | 25 | | | 253 | | | (228) | | | (90) | | | (68) | | | 531 | | | (599) | | | NM | | | | | | |

| Provision for credit losses | 932 | | | 874 | | | 58 | | | 7 | | | 1,720 | | | 1,741 | | | (21) | | | (1) | | | | | | | |

| Noninterest expense | 5,701 | | | 6,027 | | | (326) | | | (5) | | | 11,725 | | | 12,065 | | | (340) | | | (3) | | | | | | | |

| Income before income tax expense | 2,373 | | | 2,554 | | | (181) | | | (7) | | | 4,652 | | | 5,013 | | | (361) | | | (7) | | | | | | | |

| Income tax expense | 596 | | | 640 | | | (44) | | | (7) | | | 1,169 | | | 1,258 | | | (89) | | | (7) | | | | | | | |

| Net income | $ | 1,777 | | | 1,914 | | | (137) | | | (7) | | | $ | 3,483 | | | 3,755 | | | (272) | | | (7) | | | | | | | |

| Revenue by Line of Business | | | | | | | | | | | | | | | | | | | | | |

| Consumer, Small and Business Banking | $ | 6,129 | | | 6,448 | | | (319) | | | (5) | | | $ | 12,221 | | | 12,822 | | | (601) | | | (5) | | | | | | | |

| Consumer Lending: | | | | | | | | | | | | | | | | | | | | | |

| Home Lending | 823 | | | 847 | | | (24) | | | (3) | | | 1,687 | | | 1,710 | | | (23) | | | (1) | | | | | | | |

| Credit Card | 1,452 | | | 1,449 | | | 3 | | | — | | | 2,948 | | | 2,866 | | | 82 | | | 3 | | | | | | | |

| Auto | 282 | | | 378 | | | (96) | | | (25) | | | 582 | | | 770 | | | (188) | | | (24) | | | | | | | |

| Personal Lending | 320 | | | 333 | | | (13) | | | (4) | | | 659 | | | 651 | | | 8 | | | 1 | | | | | | | |

| Total revenue | $ | 9,006 | | | 9,455 | | | (449) | | | (5) | | | $ | 18,097 | | | 18,819 | | | (722) | | | (4) | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | |

| Selected Metrics | | | | | | | | | | | | | | | | | | | | | |

| Consumer Banking and Lending: | | | | | | | | | | | | | | | | | | | | | |

| Return on allocated capital (1) | 15.1 | % | | 16.9 | | | | | | | 14.8 | % | | 16.7 | | | | | | | | | | | |

| Efficiency ratio (2) | 63 | | | 64 | | | | | | | 65 | | | 64 | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | |

| Retail bank branches (#, period-end) | 4,227 | | | 4,455 | | | | | (5) | | | | | | | | | | | | | | | |

| Digital active customers (# in millions, period-end) (3) | 35.6 | | | 34.2 | | | | | 4 | | | | | | | | | | | | | | | |

| Mobile active customers (# in millions, period-end) (3) | 30.8 | | | 29.1 | | | | | 6 | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | |

| Consumer, Small and Business Banking: | | | | | | | | | | | | | | | | | | | | | |

| Deposit spread (4) | 2.5 | % | | 2.6 | | | | | | | 2.5 | % | | 2.6 | | | | | | | | | | | |

| Debit card purchase volume ($ in billions) (5) | $ | 128.2 | | | 124.9 | | | 3.3 | | | 3 | | | $ | 249.7 | | | 242.2 | | | 7.5 | | | 3 | | | | | | | |

| Debit card purchase transactions (# in millions) (5) | 2,581 | | | 2,535 | | | | | 2 | | | 5,023 | | | 4,904 | | | | | 2 | | | | | | | |

(continued on following page)

(continued from previous page)

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Quarter ended June 30, | | | | | | Six months ended June 30, | | | | | | | | | | |

| ($ in millions, unless otherwise noted) | 2024 | | 2023 | | $ Change | | % Change | | 2024 | | 2023 | | $ Change | | % Change | | | | | | |

| Home Lending: | | | | | | | | | | | | | | | | | | | | | |

| Mortgage banking: | | | | | | | | | | | | | | | | | | | | | |

| Net servicing income | $ | 89 | | | 62 | | | 27 | | | 44 | % | | $ | 180 | | | 146 | | | 34 | | | 23 | % | | | | | | |

| Net gains on mortgage loan originations/sales | 46 | | | 70 | | | (24) | | | (34) | | | 148 | | | 146 | | | 2 | | | 1 | | | | | | | |

| Total mortgage banking | $ | 135 | | | 132 | | | 3 | | | 2 | | | $ | 328 | | | 292 | | | 36 | | | 12 | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | |

| Retail originations ($ in billions) | $ | 5.3 | | | 7.7 | | | (2.4) | | | (31) | | | $ | 8.8 | | | 13.3 | | | (4.5) | | | (34) | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | |

| % of originations held for sale (HFS) | 38.6 | % | | 45.3 | | | | | | | 40.6 | % | | 46.0 | | | | | | | | | | | |

| Third-party mortgage loans serviced ($ in billions, period-end) (6) | $ | 512.8 | | | 609.1 | | | (96.3) | | | (16) | | | | | | | | | | | | | | | |

| Mortgage servicing rights (MSR) carrying value (period-end) | 7,061 | | | 8,251 | | | (1,190) | | | (14) | | | | | | | | | | | | | | | |

| Ratio of MSR carrying value (period-end) to third-party mortgage loans serviced (period-end) (6) | 1.38 | % | | 1.35 | | | | | | | | | | | | | | | | | | | |

| Home lending loans 30+ days delinquency rate (period-end) (7)(8)(9) | 0.33 | | | 0.25 | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | |

| Credit Card: | | | | | | | | | | | | | | | | | | | | | |

| Point of sale (POS) volume ($ in billions) | $ | 42.9 | | | 38.3 | | | 4.6 | | | 12 | | | $ | 82.0 | | | 72.5 | | | 9.5 | | | 13 | | | | | | | |

| New accounts (# in thousands) | 677 | | | 618 | | | | | 10 | | | 1,328 | | | 1,197 | | | | | 11 | | | | | | | |

| Credit card loans 30+ days delinquency rate (period-end) (8)(9) | 2.71 | % | | 2.31 | | | | | | | | | | | | | | | | | | | |

| Credit card loans 90+ days delinquency rate (period-end) (8)(9) | 1.40 | | | 1.10 | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | |

| Auto: | | | | | | | | | | | | | | | | | | | | | |