Filed Pursuant to Rule 424(b)(2)

File No. 333-236148

This pricing supplement relates to an effective registration statement under the Securities Act of 1933, but is not complete and may be changed. This pricing supplement and the accompanying prospectus supplement and prospectus are not an offer to sell these securities and are not soliciting an offer to buy these securities in any state where the offer or sale is not permitted.

SUBJECT TO COMPLETION, DATED MAY 26, 2020

Pricing Supplement No. 7 dated May , 2020

(to Prospectus Supplement dated February 26, 2020

and Prospectus dated February 25, 2020)

WELLS FARGO & COMPANY

Medium-Term Notes, Series U

Senior RedeemableFixed-to-Floating Rate Notes

You should read the more detailed description of the notes provided under “Description of Notes” in the accompanying prospectus supplement and “Description of Debt Securities” in the accompanying prospectus, as supplemented by this pricing supplement. All payments on the notes are subject to the credit risk of Wells Fargo & Company. If Wells Fargo & Company defaults on its obligations, you could lose some or all of your investment. Certain defined terms used but not defined herein have the meanings set forth in the accompanying prospectus supplement and prospectus.

Aggregate Principal Amount

Offered: | $ |

Trade Date: | May , 2020 |

Original Issue Date: | June , 2020 (T+5) |

Stated Maturity Date: | June , 2024; on the stated maturity date, the holders of the notes will be entitled to receive a cash payment in U.S. dollars equal to 100% of the principal amount of the notes plus any accrued and unpaid interest |

Optional Redemption: | At our option, we may redeem the notes, in whole at any time or in part from time to time on any day included in the Make-Whole Redemption Period, at a redemption price equal to the sum of: (i) 100% of the principal amount of the notes being redeemed plus accrued and unpaid interest thereon, to, but excluding, the Make- Whole Redemption Date and (ii) the Make-Whole Amount, as described under “Description of Debt Securities—Redemption and Repayment—Optional Make-Whole Redemption of Debt Securities” in the accompanying prospectus. As used in connection with the notes: |

The “Make-Whole Redemption Period” is the period commencing on and including June , 2021 and ending on and including June , 2023.

The “Make-Whole Spread” is %.

At our option, we may also redeem the notes (i) in whole, but not in part, on June , 2023 or (ii) in whole at any time or in part from time to time, on or after May , 2024, in each case at a redemption price equal to 100% of the principal amount of the notes being redeemed plus accrued and unpaid interest thereon to, but excluding, the date of such redemption.

Any redemption may be subject to prior regulatory approval and will be effected as described under “Description of Debt Securities—Redemption and Repayment—Optional Redemption By Us” in the accompanying prospectus, modified as provided in this pricing supplement. |

Price to Public (Issue Price): | %, plus accrued interest, if any, from June , 2020 |

Agent Discount

(Gross Spread): | % |

All-in Price (Net of

Agent Discount): | %, plus accrued interest, if any, from June , 2020 |

Net Proceeds: | $ |

Interest Rate: | The notes will bear interest at a fixed rate from June , 2020 to, but excluding, June , 2023 (the “Fixed Rate Period”) and, if not previously redeemed, at a floating rate from, and including, June , 2023 to, but excluding, maturity (the “Floating Rate Period”). |

Fixed Rate Terms

Fixed Rate Period: | See “Description of Debt Securities—Interest and Principal Payments” and “—Fixed Rate Debt Securities” in the accompanying prospectus for additional information. |

Initial Interest Rate: | % |

Interest Payment Dates: | Each June and December , commencing December , 2020 and ending June , 2023 |

Business Day: | For interest payable for the Fixed Rate Period, any day, other than a Saturday or Sunday, that is neither a legal holiday nor a day on which banking institutions are authorized or required by law or regulation to close in New York, New York. |

Benchmark: | UST % due |

Benchmark Yield: | % |

Spread to Benchmark: | + basis points |

Re-Offer Yield: | % |

Floating Rate Terms

Floating Rate Period: | See “Description of Debt Securities—Interest and Principal Payments” and “—Floating Rate Debt Securities” in the accompanying prospectus for additional information, as modified herein. |

2

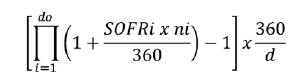

Base Rate: | Compounded SOFR (a compounded average of daily SOFR), calculated in accordance with the formula set forth below, with the resulting percentage being rounded, if necessary, to the nearest one hundred-thousandth of a percentage point (0.000005 being rounded upwards to 0.00001): |

|

where for purposes of applying the above formula to the terms of the notes: |

“d0”, for any observation period, is the number of U.S. Government Securities Business Days in the relevant observation period; |

“i” is a series of whole numbers from one to d0, each representing the relevant U.S. Government Securities Business Day in chronological order from, and including, the first U.S. Government Securities Business Day in the relevant observation period; |

“SOFRi”, for any U.S. Government Securities Business Day “i” in the relevant observation period, is equal to SOFR (as defined below under “Determination of Interest Rate for the Floating Rate Period”) in respect of that day; |

“ni”, for any U.S. Government Securities Business Day “i” in the relevant observation period, is the number of calendar days from, and including, such U.S. Government Securities Business Day “i” to, but excluding, the following U.S. Government Securities Business Day (“i+1”); and |

“d” is the number of calendar days in the relevant observation period. |

Spread: | + basis points |

Minimum Interest Rate for an

Interest Period: | 0% per annum |

Interest Calculation: | In respect of each interest period during the Floating Rate Period, the amount of interest payable on the notes will be equal to the product of (i) the outstanding principal amount of the notes multiplied by (ii) the product of (a) the Base Rate for the relevant interest period plus the Spread multiplied by (b) the quotient of the actual number of calendar days in such interest period divided by 360, subject to the minimum interest rate. An “interest period” |

3

with respect to an interest payment date during the Floating Rate Period means the period from, and including, the immediately preceding interest payment date (or, in the case of the first interest period during the Floating Rate Period, June , 2023) to, but excluding, that interest payment date. |

Index Currency: | U.S. Dollars |

Interest Determination Date: | The date two U.S. Government Securities Business Days before |

each interest payment date during the Floating Rate Period. |

Observation Period: | In respect of each interest period during the Floating Rate Period, the period from, and including, the date two U.S. Government Securities Business Days preceding the first date in such interest period to, but excluding, the date two U.S. Government Securities Business Days preceding the interest payment date for such interest period. |

U.S. Government Securities

Business Day: | Any day other than a Saturday, a Sunday or a day on which the Securities Industry and Financial Markets Association recommends that the fixed income departments of its members be closed for the entire day for purposes of trading in U.S. government securities. |

Business Day: | For interest payable for the Floating Rate Period, any day, other than a Saturday or Sunday, that is neither a legal holiday nor a day on which banking institutions are authorized or required by law or regulation to close in New York, New York that is also a U.S. Government Securities Business Day. If any interest payment date, other than a date of maturity, during the Floating Rate Period falls on a day that is not a business day, it will be postponed to the following business day, except that if that business day would fall in the next calendar month, the interest payment date will be the immediately preceding business day. |

Interest Payment Dates: | Each March , June , September and December , commencing September , 2023, and at maturity. |

Discontinuance of Base Rate: | In certain circumstances, an alternate base rate may replace Compounded SOFR for all purposes relating to the notes. See “Determination of Interest Rate for the Floating Rate Period” below. |

Calculation Agent: | The Calculation Agent for the notes has not been appointed, but we will appoint a Calculation Agent prior to the commencement of the Floating Rate Period. An affiliate of ours may be appointed the Calculation Agent. References to “our designee” in the sections entitled “Determination of Interest Rate for the Floating Rate Period” and “Risk Factors” shall mean the Calculation Agent appointed by us. |

4

Listing: | None | |||

Principal Amount | ||||

Agent (Sole Bookrunner): | Wells Fargo Securities, LLC |

$ | ||

Agents(Co-Managers): | ||||

Total: |

$ | |||

Supplemental Plan of

Distribution: | On May , 2020, we agreed to sell to the Agents, and the Agents agreed to purchase, the notes at a purchase price of %, plus accrued interest, if any, from June , 2020. The purchase price equals the issue price of % less a discount of % of the principal amount of the notes. |

United States Federal

Income Tax Considerations: | In the opinion of Faegre Drinker Biddle & Reath LLP, the notes should be considered variable rate debt securities that provide for stated interest at a fixed rate in addition to a qualified floating rate. See “U.S. Federal Income Tax Considerations—U.S. Federal Income Taxation of U.S. Holders—Variable Rate Debt Securities” in the accompanying prospectus. Notwithstanding that we expect that the notes will be issued at par, under rules governing notes with a fixed rate in addition to a qualified floating rate, it is possible that the notes could be issued with OID. Whether the notes are issued with OID will be determined at the time of issue. Information regarding the determination of the amount of OID, if any, on the notes may be obtained by submitting a written request to Wells Fargo Bank, National Association, Treasury Funding Desk,N9310-060, 550 South Fourth Street, Minneapolis, MN 55415-1529. |

Additional tax considerations are discussed under “U.S. Federal Income Tax Considerations” in the accompanying prospectus. |

CUSIP: | 95000U2R3 |

5

Risk Factors

If A Benchmark Transition Event And Its Related Benchmark Replacement Date Occur With Respect To Compounded SOFR (Including Daily SOFR), The Interest Rate For The Floating Rate Period Will No Longer Be Determined By Reference To Compounded SOFR.

If a Benchmark Transition Event and its related Benchmark Replacement Date occur with respect to Compounded SOFR (including daily SOFR), then the interest rate on the notes during the Floating Rate Period will no longer be determined by reference to Compounded SOFR, but instead will be determined by us or our designee by reference to another rate, as described below under the section entitled “Determination of Interest Rate for the Floating Rate Period.” The composition and characteristics of any Benchmark Replacement may not be the same as Compounded SOFR (including daily SOFR) and there can be no guarantee that any Benchmark Replacement will be a comparable substitute for Compounded SOFR (including daily SOFR). The occurrence of a Benchmark Transition Event and its related Benchmark Replacement Date may adversely affect the value of and your return on the notes.

The Benchmark Replacement Is Uncertain.

The notes provide that the floating rate of interest on the notes will be determined by reference to Compounded SOFR or another rate pursuant to the definition of “Benchmark Replacement” set forth below. The alternative rates referenced in the definition of “Benchmark Replacement” are currently uncertain. If each alternative rate referenced in the definition of “Benchmark Replacement” is unavailable or indeterminable, we or our designee will determine the Benchmark Replacement that will apply to the notes. The substitution of a Benchmark Replacement for Compounded SOFR may adversely affect the value of and your return on the notes.

We Or Our Designee Will Have Authority To Make Determinations, Elections, Calculations And Adjustments That Could Affect The Value Of And Your Return On The Notes.

We or our designee will make determinations, decisions, elections, calculations and adjustments as set forth under the section entitled “Determination of Interest Rate for the Floating Rate Period” below that may adversely affect the value of and your return on the notes. In particular, we or our designee will determine the Benchmark Replacement and the Benchmark Replacement Adjustment and can apply any Benchmark Replacement Conforming Changes deemed reasonably necessary to adopt the Benchmark Replacement. Although we or our designee will exercise judgment in good faith when performing such functions, potential conflicts of interest may exist between us, our designee and you. All determinations, decisions, elections, calculations and adjustments by us or our designee in our or its discretion will be conclusive for all purposes and binding on us and holders of the notes absent manifest error. In making the determinations, decisions, elections, calculations and adjustments noted under the section entitled “Determination of Interest Rate for the Floating Rate Period” below, we or our designee may have economic interests that are adverse to your interests, and such determinations, decisions, elections, calculations and adjustments may adversely affect the value of and your return on the notes. Because the Benchmark Replacement is uncertain, we or our designee are likely to exercise more discretion in respect of calculating interest payable on the notes for the Floating Rate Period than would be the case in the absence of a Benchmark Transition Event and its related Benchmark Replacement Date.

6

SOFR Has A Very Limited History; The Future Performance of SOFR Cannot Be Predicted Based On Historical Performance.

The publication of SOFR began on April 3, 2018, and it therefore has a limited history. In addition, the future performance of SOFR cannot be predicted based on the limited historical performance. The level of SOFR, which will be used to calculate Compounded SOFR, may bear little or no relation to the historical level of SOFR. Prior observed patterns, if any, in the behavior of market variables, such as correlations, may change in the future. While somepre-publication historical data has been released by the Federal Reserve Bank of New York, such analysis inherently involves assumptions, estimates and approximations. The future performance of SOFR is impossible to predict and therefore no future performance of SOFR or the notes may be inferred from any of the historical simulations or historical performance. Hypothetical or historical performance data are not indicative of, and have no bearing on, the potential performance of SOFR or the notes.

Any Failure Of SOFR To Gain Market Acceptance Could Adversely Affect The Notes.

SOFR may fail to gain market acceptance. SOFR was developed for use in certain U.S. Dollar derivatives and other financial contracts as an alternative to U.S. Dollar LIBOR in part because it is considered a good representation of general funding conditions in the overnight Treasury repo market. However, as a rate based on transactions secured by U.S. Treasury securities, it does not measure bank-specific credit risk and, as a result, is less likely to correlate with the unsecured short-term funding costs of banks. This may mean that market participants would not consider SOFR a suitable substitute or successor for all of the purposes for which LIBOR historically has been used (including, without limitation, as a representation of the unsecured short-term funding costs of banks), which may, in turn, lessen market acceptance of SOFR. Any failure of SOFR to gain market acceptance could adversely affect the value of and your return on the notes and the price at which you can sell your notes.

The Secondary Trading Market For Notes Linked To Compounded SOFR May Be Limited.

Since Compounded SOFR is a relatively new market rate, the notes will likely have no established trading market when issued and an established trading market may never develop or may not be very liquid. Market terms for debt securities linked to Compounded SOFR (such as the notes) such as the spread may evolve over time and, as a result, trading prices of the notes may be lower than those of later-issued debt securities that are linked to Compounded SOFR. Similarly, if Compounded SOFR does not prove to be widely used in debt securities similar to the notes, the trading price of the notes may be lower than that of debt securities linked to rates that are more widely used. Investors in the notes may not be able to sell such notes at all or may not be able to sell such notes at prices that will provide them with a yield comparable to similar investments that have a developed secondary market. Further, investors wishing to sell the notes in the secondary market will have to make assumptions as to the future performance of Compounded SOFR during the interest period in which they intend the sale to take place. As a result, investors may suffer from increased pricing volatility and market risk.

The Interest Rate On The Notes During The Floating Rate Period Is Based On A Daily Compounded SOFR Rate, Which Is Relatively New In The Marketplace.

For each interest period during the Floating Rate Period, the interest rate on the notes is based on a daily compounded SOFR rate calculated using the specific formula described in this pricing supplement, not the SOFR rate published on or in respect of a particular date during the related observation period, an average of SOFR rates during such period or the SOFR Index. For this and other reasons, the interest rate on the notes during any observation period within the Floating Rate

7

Period will not be the same as the interest rate on other SOFR-linked investments that use an alternative basis to determine the applicable interest rate. Further, if the SOFR rate in respect of a particular date during an observation period within the Floating Rate Period is negative, the portion of the accrued interest compounding factor specifically attributable to such date will be less than one, resulting in a reduction to the accrued interest compounding factor used to calculate the interest payable on the notes on the related interest payment date; provided that in no event will the interest payable on the notes be less than zero.

In addition, very limited market precedent exists for securities that use SOFR as the interest rate and the method for calculating an interest rate based upon SOFR in those precedents varies. Accordingly, the specific formula for the daily compounded SOFR rate used in the notes may not be widely adopted by other market participants, if at all. If the market adopts a different calculation method, that would likely adversely affect the market value of such notes.

The Amount Of Interest Payable With Respect To Each Interest Period During The Floating Rate Period Will Be Determined Near The End Of The Interest Period.

The level of the base rate applicable to each interest period during the Floating Rate Period and, therefore, the amount of interest payable with respect to such interest period will be determined on the interest determination date for such interest period. Because each such date is near the end of such interest period, you will not know the amount of interest payable with respect to each such interest period until shortly prior to the related interest payment date and it may be difficult for you to reliably estimate the amount of interest that will be payable on each such interest payment date.

Research Reports By Us Or Our Affiliates May Be Inconsistent With An Investment In The Notes.

We or our affiliates may, at present or in the future, publish research reports on Compounded SOFR and SOFR. This research is modified from time to time without notice and may, at present or in the future, express opinions or provide recommendations that are inconsistent with purchasing or holding the notes. Any such research reports could adversely affect the value of and your return on the notes.

The Composition And Characteristics of SOFR Are Not The Same As Those Of LIBOR And SOFR Is Not Expected To Be A Comparable Substitute For LIBOR.

In June 2017, the Federal Reserve Bank of New York’s Alternative Reference Rates Committee announced SOFR as its recommended alternative to U.S. Dollar LIBOR. However, the composition and characteristics of SOFR are not the same as those of LIBOR. SOFR is a broad Treasury repo financing rate that represents overnight secured funding transactions. This means that SOFR is not the economic equivalent of LIBOR (or any other alternative reference rate to LIBOR) for two key reasons. First, SOFR is a secured rate, while LIBOR is an unsecured rate. Second, SOFR is currently only an overnight rate, while LIBOR is a forward-looking rate that represents interbank funding over different maturities. As a result, there can be no assurance that SOFR will perform in the same way as LIBOR would have at any time, including, without limitation, as a result of changes in interest and yield rates in the market, market volatility or global or regional economic, financial, political, regulatory, judicial or other events. For example, since publication of SOFR began on April 3, 2018, daily changes in SOFR have, on occasion, been more volatile than daily changes in comparable benchmark or other market rates Finally, Compounded SOFR is the compounded average of daily SOFRs calculated in arrears while LIBOR is a forward-looking rate that is published with different maturities. Uncertainty surrounding the

8

establishment of market conventions related to the calculation of Compounded SOFR and whether it is a suitable substitute or successor for LIBOR may adversely affect the value of and your return on the notes.

The SOFR Administrator May Make Changes That Could Change The Value of SOFR Or Discontinue SOFR And Has No Obligation To Consider Your Interests In Doing So.

SOFR, which will be used to calculate Compounded SOFR, is a relatively new rate, and The Federal Reserve Bank of New York (or a successor), as administrator of SOFR, may make methodological or other changes that could change the value of SOFR, including changes related to the method by which SOFR is calculated, eligibility criteria applicable to the transactions used to calculate SOFR, or timing related to the publication of SOFR. In addition, the administrator may alter, discontinue or suspend calculation or dissemination of SOFR (in which case an alternative rate referenced in the definition of “Replacement Benchmark” will apply). The administrator has no obligation to consider your interests in calculating, adjusting, converting, revising or discontinuing SOFR.

See “Risk Factors” in the accompanying prospectus for additional risk factors regarding the notes, including, in particular, the risk factor entitled “One Of Our Affiliates May Act As The Calculation Agent With Respect To Our Securities And, As A Result, Potential Conflicts Of Interest Could Arise.”

SOFR

SOFR is published by the New York Federal Reserve and is intended to be a broad measure of the cost of borrowing cash overnight collateralized by Treasury securities. The New York Federal Reserve reports that SOFR includes all trades in the Broad General Collateral Rate plus bilateral Treasury repurchase agreement (repo) transactions cleared through the delivery-versus-payment service offered by the Fixed Income Clearing Corporation (the “FICC”), a subsidiary of the Depository Trust and Clearing Corporation (“DTCC”), and SOFR is filtered by the New York Federal Reserve to remove a portion of the foregoing transactions considered to be “specials.” According to the New York Federal Reserve, “specials” are repos for specific-issue collateral, which take place at cash-lending rates below those for general collateral repos because cash providers are willing to accept a lesser return on their cash in order to obtain a particular security.

The New York Federal Reserve reports that SOFR is calculated as a volume-weighted median of transaction-leveltri-party repo data collected from The Bank of New York Mellon as well as General Collateral Finance Repo transaction data and data on bilateral Treasury repo transactions cleared through the FICC’s delivery-versus-payment service. The New York Federal Reserve also notes that it obtains information from DTCC Solutions LLC, an affiliate of DTCC.

If data for a given market segment were unavailable for any day, then the most recently available data for that segment would be utilized, with the rates on each transaction from that day adjusted to account for any change in the level of market rates in that segment over the intervening period. SOFR would be calculated from this adjusted prior day’s data for segments where current data were unavailable, and unadjusted data for any segments where data were available. To determine the change in the level of market rates over the intervening period for the missing market segment, the New York Federal Reserve would use information collected through a daily survey conducted by its Trading Desk of primary dealers’ repo borrowing activity. Such daily survey would include information reported by Wells Fargo Securities, LLC, our wholly owned subsidiary, as a primary dealer.

The New York Federal Reserve notes on its publication page for SOFR that use of SOFR is subject to important limitations, indemnification obligations and disclaimers, including that the New York

9

Federal Reserve may alter the methods of calculation, publication schedule, rate revision practices or availability of SOFR at any time without notice.

Each U.S. Government Securities Business Day, the SOFR Administrator (as defined below) publishes SOFR on its website at approximately 8:00 a.m., New York City time. If errors are discovered in the transaction data provided by The Bank of New York Mellon or DTCC Solutions LLC, or in the calculation process, subsequent to the initial publication of SOFR but on that same day, SOFR and the accompanying summary statistics may be republished at approximately 2:30 p.m., New York City time. Additionally, if transaction data from The Bank of New York Mellon or DTCC Solutions LLC had previously not been available in time for publication, but became available later in the day, the affected rate or rates may be republished at around this time. Rate revisions will only be effected on the same day as initial publication and will only be republished if the change in the rate exceeds one basis point. Any time a rate is revised, a footnote to the New York Federal Reserve’s publication would indicate the revision. This revision threshold will be reviewed periodically by the New York Federal Reserve and may be changed based on market conditions.

Because SOFR is published by the SOFR Administrator based on data received from other sources, we have no control over its determination, calculation or publication. See “Risk Factors.”

The information contained in this section “SOFR” is based upon the SOFR Administrator’s Website (as defined below) and other U.S. government sources.

Determination of Interest Rate for the Floating Rate Period

Your notes will bear interest for each interest period at a per annum rate equal to Compounded SOFR plus the spread, subject to the terms described above under “Floating Rate Terms.” Compounded SOFR will be determined by us or our designee using the formula described above under “Floating Rate Terms.” SOFR will be determined by us or our designee in the following manner:

| • | “SOFR” means, with respect to any U.S. Government Securities Business Day: |

| • | (1) the Secured Overnight Financing Rate published for such U.S. Government Securities Business Day as such rate appears on the SOFR Administrator’s Website at 3:00 p.m. (New York time) on the immediately following U.S. Government Securities Business Day (the “SOFR Determination Time”); |

| • | (2) if the rate specified in (1) above does not so appear, the Secured Overnight Financing Rate as published in respect of the first preceding U.S. Government Securities Business Day for which the Secured Overnight Financing Rate was published on the SOFR Administrator’s Website; |

where:

“SOFR Administrator” means the Federal Reserve Bank of New York (or a successor administrator of the Secured Overnight Financing Rate); and

“SOFR Administrator’s Website” means the website of the Federal Reserve Bank of New York, or any successor source.

• Notwithstanding the foregoing, if we or our designee determine that a Benchmark Transition Event and its related Benchmark Replacement Date have occurred prior to the interest determination date

10

in respect of any interest payment date for the Floating Rate Period, the Benchmark Replacement will replace the then-current Benchmark for all purposes relating to the notes in respect of such determination on such date and all determinations on all subsequent dates.

In connection with the implementation of a Benchmark Replacement, we or our designee will have the right to make Benchmark Replacement Conforming Changes from time to time.

Any determination, decision, election or calculation that may be made by us or our designee pursuant to the provisions described in this section “Determination of Interest Rate for the Floating Rate Period,” including any determination with respect to a rate or adjustment or of the occurrence ornon-occurrence of an event, circumstance or date and any decision to take or refrain from taking any action or any selection, will be conclusive and binding absent manifest error, may be made in our or our designee’s sole discretion, and, notwithstanding anything to the contrary in the documentation relating to the notes, shall become effective without consent from any other party.

For the avoidance of doubt, after a Benchmark Transition Event and its related Benchmark Replacement Date have occurred, interest payable on the notes for the Floating Rate Period will be an annual rate equal to the sum of the applicable Benchmark Replacement and the spread set forth under the section entitled “Floating Rate Terms” above.

Upon the request of the holder of any note, we or our designee will provide the calculation of the amount of interest payable in respect of any interest payment date during the Floating Rate Period.

As used herein:

The term “Benchmark” means, initially, Compounded SOFR, as defined above; provided that if a Benchmark Transition Event and its related Benchmark Replacement Date have occurred with respect to Compounded SOFR (or the published daily SOFR used in the calculation thereof) or the then-current Benchmark, then “Benchmark” means the applicable Benchmark Replacement.

The term “Benchmark Replacement” means the first alternative set forth in the order below that can be determined by us or our designee as of the Benchmark Replacement Date:

(1) the sum of: (a) the alternate rate of interest that has been selected or recommended by the Relevant Governmental Body as the replacement for the then-current Benchmark and (b) the Benchmark Replacement Adjustment;

(2) the sum of: (a) the ISDA Fallback Rate and (b) the Benchmark Replacement Adjustment;

(3) the sum of: (a) the alternate rate of interest that has been selected by us or our designee as the replacement for the then-current Benchmark giving due consideration to any industry-accepted rate of interest as a replacement for the then-current Benchmark for U.S. dollar-denominated floating rate notes at such time and (b) the Benchmark Replacement Adjustment.

The term “Benchmark Replacement Adjustment” means the first alternative set forth in the order below that can be determined by us or our designee as of the Benchmark Replacement Date:

(1) the spread adjustment, or method for calculating or determining such spread adjustment, (which may be a positive or negative value or zero), that has been selected or recommended by the Relevant Governmental Body for the applicable Unadjusted Benchmark Replacement;

11

(2) if the applicable Unadjusted Benchmark Replacement is equivalent to the ISDA Fallback Rate, then the ISDA Fallback Adjustment;

(3) the spread adjustment (which may be a positive or negative value or zero) that has been selected by us or our designee giving due consideration to any industry-accepted spread adjustment, or method for calculating or determining such spread adjustment, for the replacement of the then-current Benchmark with the applicable Unadjusted Benchmark Replacement for U.S. dollar- denominated floating rate notes at such time.

The term “Benchmark Replacement Conforming Changes” means, with respect to any Benchmark Replacement, any technical, administrative or operational changes (including changes to the definitions of “interest period”, “interest determination date” and “observation period”, timing and frequency of determining rates and making payments of interest, rounding of amounts or tenors, and other administrative matters) that we or our designee decide may be appropriate to reflect the adoption of such Benchmark Replacement in a manner substantially consistent with market practice (or, if we or our designee decide that adoption of any portion of such market practice is not administratively feasible or if we or our designee determine that no market practice for use of the Benchmark Replacement exists, in such other manner as we or our designee determine is reasonably necessary).

The term “Benchmark Replacement Date” means the earliest to occur of the following events with respect to the then-current Benchmark (including the daily published component used in the calculation thereof):

(1) in the case of clause (1) or (2) of the definition of “Benchmark Transition Event,” the later of (a) the date of the public statement or publication of information referenced therein and (b) the date on which the administrator of the Benchmark permanently or indefinitely ceases to provide the Benchmark (or such component); or

(2) in the case of clause (3) of the definition of “Benchmark Transition Event,” the date of the public statement or publication of information referenced therein.

For the avoidance of doubt, if the event giving rise to the Benchmark Replacement Date occurs on the same day as the interest determination date, but earlier than the Reference Time on that date, the Benchmark Replacement Date will be deemed to have occurred prior to the Reference Time for such determination.

The term “Benchmark Transition Event” means the occurrence of one or more of the following events with respect to the then-current Benchmark (including the daily published component used in the calculation thereof):

(1) a public statement or publication of information by or on behalf of the administrator of the Benchmark (or such component) announcing that such administrator has ceased or will cease to provide the Benchmark (or such component), permanently or indefinitely, provided that, at the time of such statement or publication, there is no successor administrator that will continue to provide the Benchmark (or such component);

(2) a public statement or publication of information by the regulatory supervisor for the administrator of the Benchmark (or such component), the central bank for the currency of the Benchmark (or such component), an insolvency official with jurisdiction over the administrator for the Benchmark (or such component), a resolution authority with jurisdiction over the administrator for the Benchmark (or such component) or a court or an entity with similar insolvency or resolution authority over the

12

administrator for the Benchmark (or such component), which states that the administrator of the Benchmark (or such component) has ceased or will cease to provide the Benchmark (or such component) permanently or indefinitely, provided that, at the time of such statement or publication, there is no successor administrator that will continue to provide the Benchmark (or such component); or

(3) a public statement or publication of information by the regulatory supervisor for the administrator of the Benchmark (or such component) announcing that the Benchmark (or such component) is no longer representative.

The term “ISDA Definitions” means the 2006 ISDA Definitions published by the International Swaps and Derivatives Association, Inc. (“ISDA”) or any successor thereto, as amended or supplemented from time to time, or any successor definitional booklet for interest rate derivatives published from time to time.

The term “ISDA Fallback Adjustment” means the spread adjustment (which may be a positive or negative value or zero) that would apply for derivatives transactions referencing the ISDA Definitions to be determined upon the occurrence of an index cessation event with respect to the Benchmark for the applicable tenor.

The term “ISDA Fallback Rate” means the rate that would apply for derivatives transactions referencing the ISDA Definitions to be effective upon the occurrence of an index cessation date with respect to the Benchmark for the applicable tenor excluding the applicable ISDA Fallback Adjustment.

The term “Reference Time” with respect to any determination of the Benchmark means (1) if the Benchmark is Compounded SOFR, the SOFR Determination Time, and (2) if the Benchmark is not Compounded SOFR, the time determined by us or our designee in accordance with the Benchmark Replacement Conforming Changes.

The term “Relevant Governmental Body” means the Federal Reserve Board and/or the Federal Reserve Bank of New York, or a committee officially endorsed or convened by the Federal Reserve Board and/or the Federal Reserve Bank of New York or any successor thereto.

The term “Unadjusted Benchmark Replacement” means the Benchmark Replacement excluding the Benchmark Replacement Adjustment.

13