Exhibit 99.1

Exhibit 99.1

Guggenheim Securities Roadshow

December 18-19, 2013

For further information on Seacoast Banking Corporation of Florida contact:

Dennis S. Hudson, III

William R. Hahl

CEO

CFO

Phone: 772-288-6085

Phone: 772-221-2825

Email: denny.hudson@seacoastnational.com

Email: w.hahl@seacoastnational.com

CONFIDENTIAL

Cautionary Notice Regarding Forward-Looking Statements

This slide deck contains “forward-looking statements” within the meaning of Section 27A of the Securities Act of 1933 and Section 21E of the Securities Exchange Act of 1934, including, without limitation, statements about future financial and operating results, ability to realized deferred tax assets, cost savings, enhanced revenues, economic and seasonal conditions in our markets, and improvements to reported earnings that may be realized from cost controls and for integration of banks that we have acquired, as well as statements with respect to Seacoast’s objectives, expectations and intentions and other statements that are not historical facts. Actual results may differ from those set forth in the forward-looking statements.

Forward-looking statements include statements with respect to our beliefs, plans, objectives, goals, expectations, anticipations, estimates and intentions, and involve known and unknown risks, uncertainties and other factors, which may be beyond our control, and which may cause the actual results, performance or achievements of Seacoast to be materially different from future results, performance or achievements expressed or implied by such forward-looking statements. You should not expect us to update any forward-looking statements.

You can identify these forward-looking statements through our use of words such as “may,” “will,” “anticipate,” “assume,” “should,” “support”, “indicate,” “would,” “believe,” “contemplate,” “expect,” “estimate,” “continue,” “further”, “point to,” “project,” “could,” “intend” or other similar words and expressions of the future. These forward-looking statements may not be realized due to a variety of factors, including, without limitation: the effects of future economic and market conditions, including seasonality; governmental monetary and fiscal policies, as well as legislative, tax and regulatory changes; changes in accounting policies, rules and practices; the risks of changes in interest rates on the level and composition of deposits, loan demand, liquidity and the values of loan collateral, securities, and interest sensitive assets and liabilities; interest rate risks, sensitivities and the shape of the yield curve; the effects of competition from other commercial banks, thrifts, mortgage banking firms, consumer finance companies, credit unions, securities brokerage firms, insurance companies, money market and other mutual funds and other financial institutions operating in our market areas and elsewhere, including institutions operating regionally, nationally and internationally, together with such competitors offering banking products and services by mail, telephone, computer and the Internet; and the failure of assumptions underlying the establishment of reserves for possible loan losses. The risks of mergers and acquisitions, include, without limitation: unexpected transaction costs, including the costs of integrating operations; the risks that the businesses will not be integrated successfully or that such integration may be more difficult, time-consuming or costly than expected; the potential failure to fully or timely realize expected revenues and revenue synergies, including as the result of revenues following the merger being lower than expected; the risk of deposit and customer attrition; any changes in deposit mix; unexpected operating and other costs, which may differ or change from expectations; the risks of customer and employee loss and business disruption, including, without limitation, as the result of difficulties in maintaining relationships with employees; increased competitive pressures and solicitations of customers by competitors; as well as the difficulties and risks inherent with entering new markets.

All written or oral forward-looking statements attributable to us are expressly qualified in their entirety by this cautionary notice, including, without limitation, those risks and uncertainties described in our annual report on Form 10-K for the year ended December 31, 2012 under “Special Cautionary Notice Regarding Forward-Looking Statements” and “Risk Factors”, and otherwise in our SEC reports and filings. Such reports are available upon request from the Company, or from the Securities and Exchange Commission, including through the SEC’s Internet website at http://www.sec.gov.

CONFIDENTIAL

2

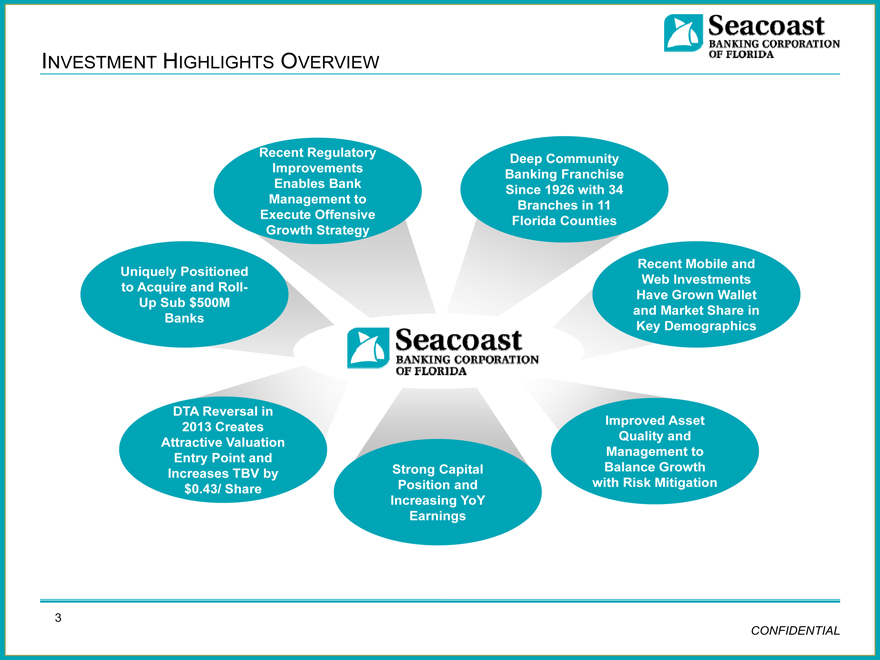

INVESTMENT HIGHLIGHTS OVERVIEW

Recent Regulatory

Improvements

Enables Bank

Management to

Execute Offensive

Growth Strategy

Uniquely Positioned

to Acquire and Roll-

Up Sub $500M

Banks

DTA Reversal in

2013 Creates

Attractive Valuation

Entry Point and

Increases TBV by Strong Capital

$0.43/ Share Position and

Increasing YoY

Earnings

Deep Community

Banking Franchise

Since 1926 with 34

Branches in 11

Florida Counties

Recent Mobile and

Web Investments

Have Grown Wallet

and Market Share in

Key Demographics

Improved Asset

Quality and

Management to

Balance Growth

with Risk Mitigation

CONFIDENTIAL

3

COMPANY OVERVIEW

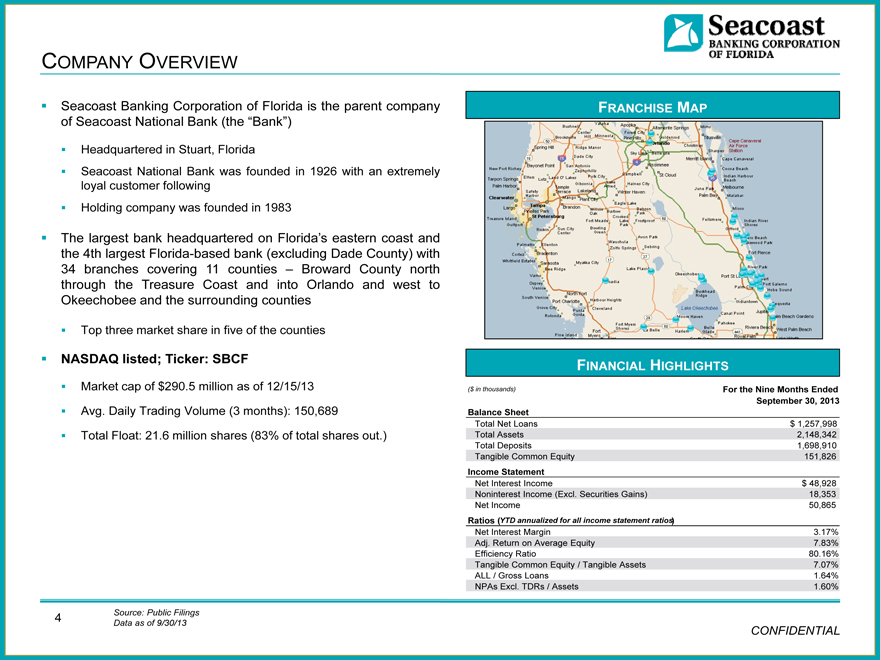

Seacoast Banking Corporation of Florida is the parent company of Seacoast National Bank (the “Bank”)

Headquartered in Stuart, Florida

Seacoast National Bank was founded in 1926 with an extremely loyal customer following

Holding company was founded in 1983

The largest bank headquartered on Florida’s eastern coast and the 4th largest Florida-based bank (excluding Dade County) with 34 branches covering 11 counties – Broward County north through the Treasure Coast and into Orlando and west to Okeechobee and the surrounding counties

Top three market share in five of the counties

NASDAQ listed; Ticker: SBCF

Market cap of $290.5 million as of 12/15/13

Avg. Daily Trading Volume (3 months): 150,689

Total Float: 21.6 million shares (83% of total shares out.)

FRANCHISE MAP

FINANCIAL HIGHLIGHTS

($ in thousands) For the Nine Months Ended

September 30, 2013

Balance Sheet

Total Net Loans $ 1,257,998

Total Assets 2,148,342

Total Deposits 1,698,910

Tangible Common Equity 151,826

Income Statement

Net Interest Income $ 48,928

Noninterest Income (Excl. Securities Gains) 18,353

Net Income 50,865

Ratios (YTD annualized for all income statement ratios)

Net Interest Margin 3.17%

Adj. Return on Average Equity 7.83%

Efficiency Ratio 80.16%

Tangible Common Equity / Tangible Assets 7.07%

ALL / Gross Loans 1.64%

NPAs Excl. TDRs / Assets 1.60%

4 Source: Public Filings Data as of 9/30/13

CONFIDENTIAL

COMPANY HISTORY

Incorporated in 1983, Seacoast Banking Corporation of Florida is a bank holding company headquartered in Stuart, Florida, that conducts its operations through its subsidiary, Seacoast National Bank, which was founded in 1926 and is one of the oldest, longest running banks in Florida

1933

1985

2002

2006

2013

Commenced operations as

Acquired a de novo

Citizens Bank of Stuart

banking subsidiary,

First National Bank

and Trust Company

Entered Palm Beach

The bank name was changed

Sept. 2013 the OCC

County by establishing a

from First National Bank &

lifted the Bank’s Formal

new branch office

Trust Company of the

Written Agreement and

Treasure Coast to Seacoast

the Bank was upgraded

National Bank

1983

1991

2005

2006

Seacoast Banking

Acquired approximately

Acquired Century National

Acquired Big Lake National

Corporation of Florida, a

$110.0mm of core deposits of

Bank, a commercial bank

Bank, a commercial bank

bank holding company,

a failed thrift, American

headquartered in Orlando,

headquartered in

is incorporated

Pioneer Federal Savings Bank

Florida

Okeechobee, Florida, with

nine offices in seven counties

CONFIDENTIAL

5

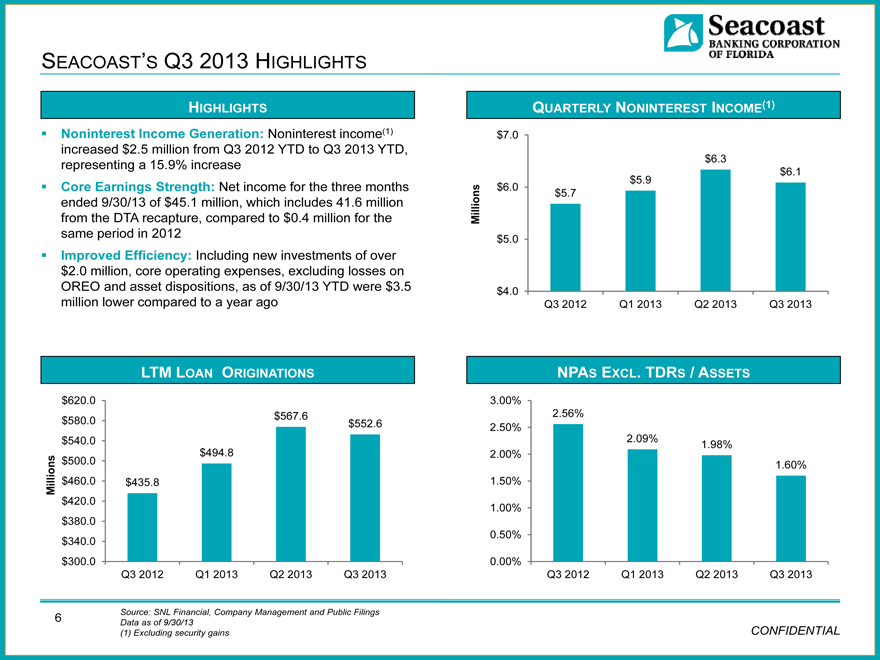

SEACOAST’S Q3

2013

HIGHLIGHTS

HIGHLIGHTS

Noninterest Income Generation: Noninterest income(1) increased $2.5 million from Q3 2012 YTD to Q3 2013 YTD, representing a 15.9% increase

Core Earnings Strength: Net income for the three months ended 9/30/13 of $45.1 million, which includes 41.6 million from the DTA recapture, compared to $0.4 million for the same period in 2012

Improved Efficiency: Including new investments of over $2.0 million, core operating expenses, excluding losses on OREO and asset dispositions, as of 9/30/13 YTD were $3.5 million lower compared to a year ago

QUARTERLY NONINTEREST INCOME(1)

$ 7.0

$ 6.3

$ 6.1

$ 5.9

Millions $ 6.0 $ 5.7

$ 5.0

$ 4.0

Q3 2012 Q1 2013 Q2 2013 Q3 2013

LTM LOAN ORIGINATIONS NPAS EXCL. TDRS / ASSETS

$ 620.0 3.00%

$ 567.6 2.56%

$ 580.0 $552.6 2.50%

$ 540.0 2.09% 1.98%

$ 494.8 2.00%

$ 500.0 1.60%

Millions $ 460.0 $435.8 1.50%

$ 420.0 1.00%

$ 380.0

$ 340.0 0.50%

$ 300.0 0.00%

Q3 2012 Q1 2013 Q2 2013 Q3 2013 Q3 2012 Q1 2013 Q2 2013 Q3 2013

Source: SNL Financial, Company Management and Public Filings

6 Data as of 9/30/13

(1) Excluding security gains CONFIDENTIAL

THE SEACOAST VIEW: COMMUNITY BANKING 2014+

Three transformational forces are driving disruption across the community banking landscape, fundamentally reshaping the industry:

Digital technologies are being used by bank and non-bank financial services providers to better meet customer needs, giving the customer more choices about where to send their business;

Data and improved analytics are moving bank and non-bank financial services providers closer to the customer, building trust and bringing in more business; and

Distribution channels are rapidly aligning with broader changes in consumer behavior, making branch-only based systems unsustainable.

Consumers and businesses alike are quickly discovering new ways to more conveniently access their money and manage their financial lives, placing demands on historical big bank and community bank business models. New competitors are reshaping the landscape.

Community banks must invest in digital delivery of current product sets and develop new ones just to maintain “table stakes” in the game going forward; and reduce fixed high-cost structures associated with traditional branch based systems as they implement variable low-cost distribution platforms that meet current and future customer needs.

CONFIDENTIAL

7

THE SEACOAST VIEW: COMMUNITY BANKING 2014+(CONTINUED…)

Seacoast is uniquely positioning its business model to address these transformational challenges to build greater value for shareholders and sustainable performance over the long term:

We are observing digital technology customer adoption rates that suggest the transformational impact on community banks will be far more rapid than widely believed;

Nearly 40% of our online customers have switched to our mobile products;

Mobile users have increased over 300% since our initial deployment in 2011 and grew at an annual rate of over 92% in the most recent quarter;

The average mobile user interacts with us 50 times per month

We have been using our position as the largest consumer and small business bank in our core footprint to test and explore new growth tactics;

10.4% CAGR for core customer funding since 2010;

Fee revenues have increased 15.9% when compared with the first nine months of 2012;

Over half of our household base now uses our digital servicing capabilities

We are building an integrated distribution system to improve revenue growth and reduce our fixed costs;

More than 20% of our branches have been closed;

We have added 24 new products to our digital product suite;

We have rolled out an innovative small business platform to three Florida metro markets

Source: Company Management

CONFIDENTIAL

8

THE SEACOAST VIEW: COMMUNITY BANKING 2014+(CONTINUED…)

Opportunities for growth are significant. Traditional community bank business models are being challenged which will drive faster consolidation:

Smaller banks have done little to integrate digital technology;

Most are still executing branch based business models; and

Most leadership teams have a traditional banking mindset

Seacoast will continue to refine the tactics that underpin our successful customer growth strategy to achieve better revenue improvements;

We are advancing the integration of our digital, ATM and branch based delivery platforms to achieve better revenue growth with lower fixed costs; and

We believe executing the right acquisitions are a low-cost path to meaningful customer acquisition and faster distribution integration which will drive greater cost efficiencies and scale.

CONFIDENTIAL

9

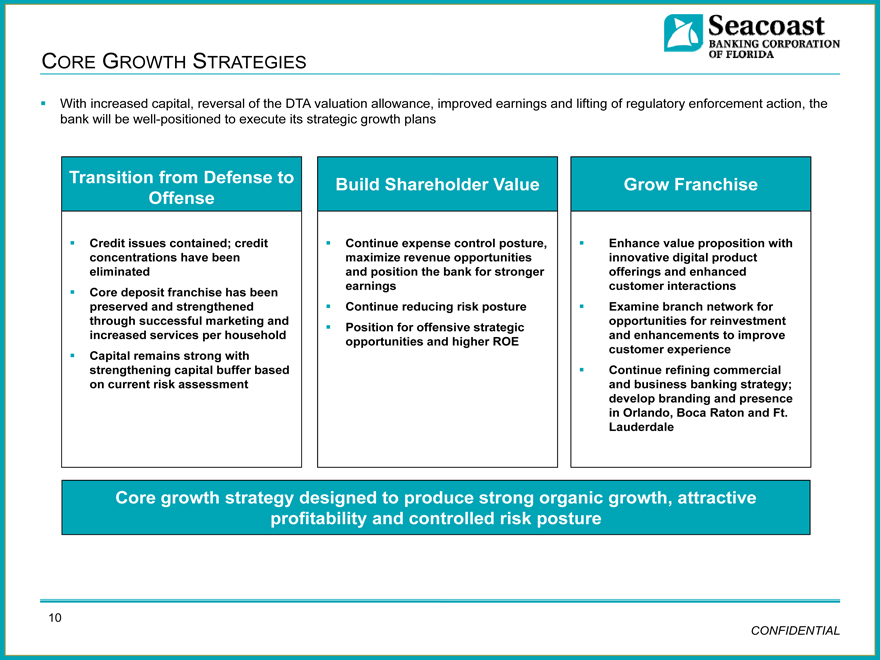

CORE GROWTH STRATEGIES

With increased capital, reversal of the DTA valuation allowance, improved earnings and lifting of regulatory enforcement action, the bank will be well-positioned to execute its strategic growth plans

Transition from Defense to Offense

Credit issues contained; credit concentrations have been eliminated

Core deposit franchise has been preserved and strengthened through successful marketing and increased services per household

Capital remains strong with strengthening capital buffer based on current risk assessment

Build Shareholder Value

Continue expense control posture, maximize revenue opportunities and position the bank for stronger earnings

Continue reducing risk posture

Position for offensive strategic opportunities and higher ROE

Grow Franchise

Enhance value proposition with innovative digital product offerings and enhanced customer interactions

Examine branch network for opportunities for reinvestment and enhancements to improve customer experience

Continue refining commercial and business banking strategy; develop branding and presence in Orlando, Boca Raton and Ft.

Lauderdale

Core growth strategy designed to produce strong organic growth, attractive profitability and controlled risk posture

CONFIDENTIAL

10

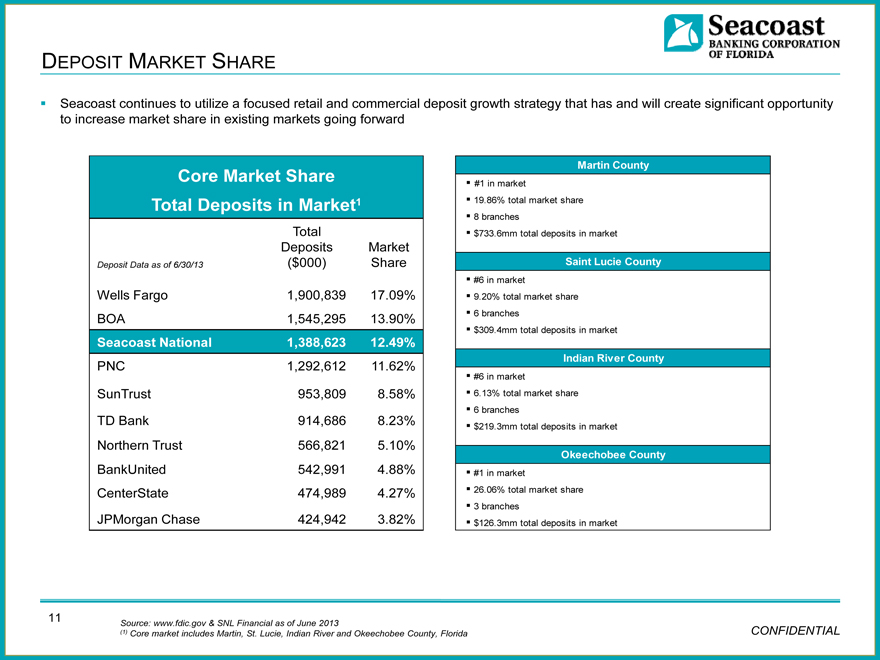

DEPOSIT MARKET SHARE

Seacoast continues to utilize a focused retail and commercial deposit growth strategy that has and will create significant opportunity to increase market share in existing markets going forward

Core Market Share

Total Deposits in Market1

Total

Deposits

Market

Deposit Data as of 6/30/13

($000)

Share

Wells Fargo

1,900,839

17.09%

BOA

1,545,295

13.90%

Seacoast National

1,388,623

12.49%

PNC

1,292,612

11.62%

SunTrust

953,809

8.58%

TD Bank

914,686

8.23%

Northern Trust

566,821

5.10%

BankUnited

542,991

4.88%

CenterState

474,989

4.27%

JPMorgan Chase

424,942

3.82%

Martin County

#1 in market

19.86% total market share

8 branches

$733.6mm total deposits in market

Saint Lucie County

#6 in market

9.20% total market share

6 branches

$309.4mm total deposits in market

Indian River County

#6 in market

6.13% total market share

6 branches

$219.3mm total deposits in market

Okeechobee County

#1 in market

26.06% total market share

3 branches

$126.3mm total deposits in market

11

Source: www.fdic.gov & SNL Financial as of June 2013

(1) Core market includes Martin, St. Lucie, Indian River and Okeechobee County, Florida

CONFIDENTIAL

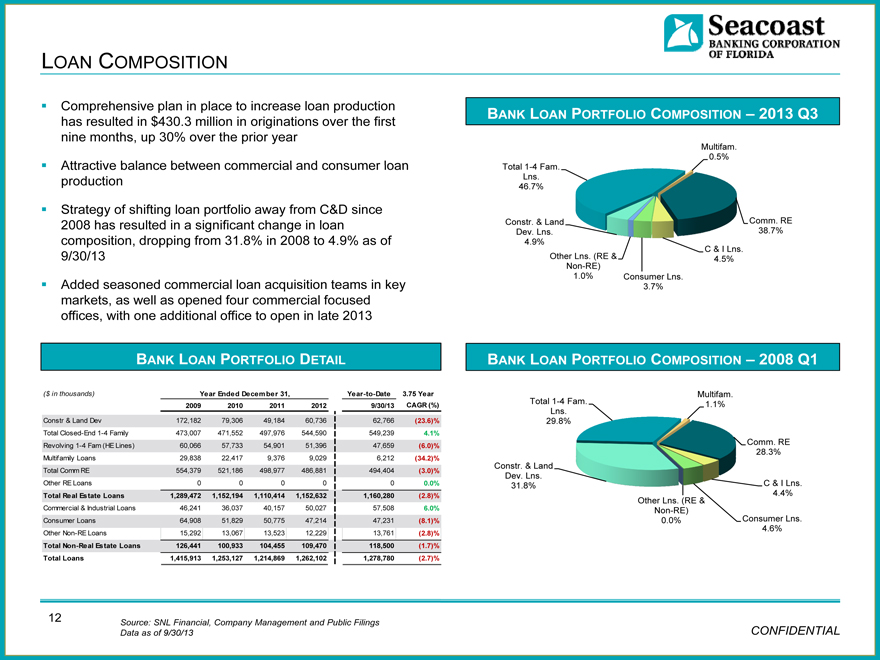

LOAN COMPOSITION

Comprehensive plan in place to increase loan production has resulted in $430.3 million in originations over the first nine months, up 30% over the prior year

Attractive balance between commercial and consumer loan production

Strategy of shifting loan portfolio away from C&D since 2008 has resulted in a significant change in loan composition, dropping from 31.8% in 2008 to 4.9% as of 9/30/13

Added seasoned commercial loan acquisition teams in key markets, as well as opened four commercial focused offices, with one additional office to open in late 2013

BANK LOAN PORTFOLIO DETAIL

BANK LOAN PORTFOLIO COMPOSITION – 2013 Q3

Multifam.

0.5%

Total 1-4 Fam.

Lns.

46.7%

Constr. & Land

Comm. RE

Dev. Lns.

38.7%

4.9%

C & I Lns.

Other Lns. (RE &

4.5%

Non-RE)

1.0%

Consumer Lns.

3.7%

BANK LOAN PORTFOLIO COMPOSITION – 2008 Q1

($ in thousands) Year Ended December 31, Year-to-Date 3.75 Year Multifam.

2009 2010 2011 2012 9/30/13 CAGR (%) Total 1-4 Fam. 1.1%

Lns.

Constr & Land Dev 172,182 79,306 49,184 60,736 62,766(23.6)% 29.8%

Total Closed-End 1-4 Family 473,007 471,552 497,976 544,590 549,239 4.1%

Revolving 1-4 Fam (HE Lines) 60,066 57,733 54,901 51,396 47,659(6.0)% Comm. RE

28.3%

Multifamily Loans 29,838 22,417 9,376 9,029 6,212(34.2)%

Constr. & Land

Total Comm RE 554,379 521,186 498,977 486,881 494,404(3.0)% Dev. Lns.

Other RE Loans 0 0 0 0 0 0.0% 31.8% C & I Lns.

Total Real Estate Loans 1,289,472 1,152,194 1,110,414 1,152,632 1,160,280(2.8)% 4.4%

Other Lns. (RE &

Commercial & Industrial Loans 46,241 36,037 40,157 50,027 57,508 6.0% Non-RE)

Consumer Loans 64,908 51,829 50,775 47,214 47,231(8.1)% 0.0% Consumer Lns.

Other Non-RE Loans 15,292 13,067 13,523 12,229 13,761(2.8)% 4.6%

Total Non-Real Estate Loans 126,441 100,933 104,455 109,470 118,500(1.7)%

Total Loans 1,415,913 1,253,127 1,214,869 1,262,102 1,278,780(2.7)%

12 Source: SNL Financial, Company Management and Public Filings

Data as of 9/30/13 CONFIDENTIAL

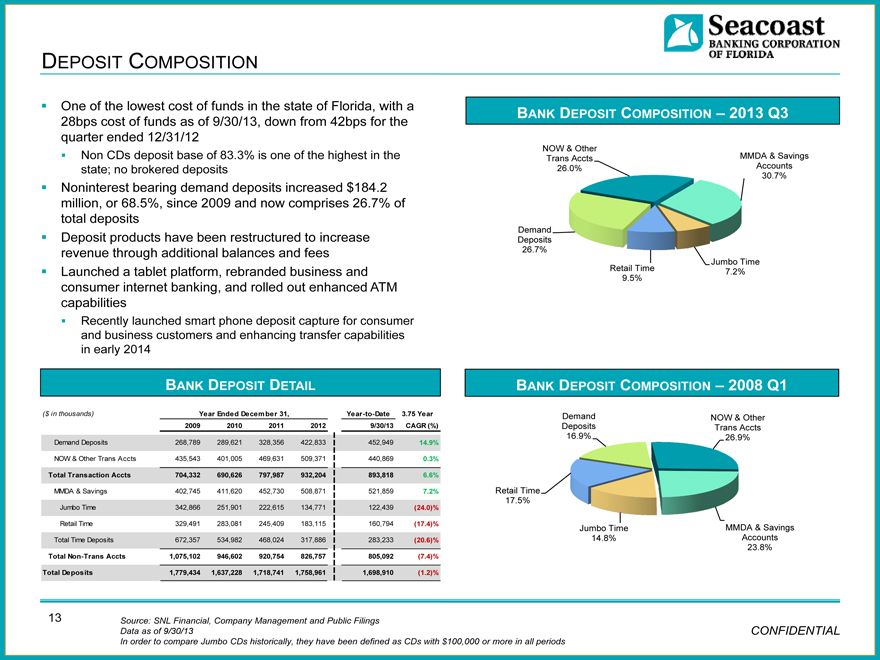

DEPOSIT COMPOSITION

One of the lowest cost of funds in the state of Florida, with a 28bps cost of funds as of 9/30/13, down from 42bps for the quarter ended 12/31/12

Non CDs deposit base of 83.3% is one of the highest in the state; no brokered deposits

Noninterest bearing demand deposits increased $184.2 million, or 68.5%, since 2009 and now comprises 26.7% of total deposits

Deposit products have been restructured to increase revenue through additional balances and fees

Launched a tablet platform, rebranded business and consumer internet banking, and rolled out enhanced ATM capabilities

Recently launched smart phone deposit capture for consumer and business customers and enhancing transfer capabilities in early 2014

BANK DEPOSIT DETAIL

BANK DEPOSIT COMPOSITION – 2013 Q3

NOW & Other

Trans Accts MMDA & Savings

26.0% Accounts

30.7%

Demand

Deposits

26.7%

Jumbo Time

Retail Time 7.2%

9.5%

BANK DEPOSIT COMPOSITION – 2008 Q1

($ in thousands) Year Ended December 31, Year-to-Date 3.75 Year Demand NOW & Other

2009 2010 2011 2012 9/30/13 CAGR (%) Deposits Trans Accts

Demand Deposits 268,789 289,621 328,356 422,833 452,949 14.9% 16.9% 26.9%

NOW & Other Trans Accts 435,543 401,005 469,631 509,371 440,869 0.3%

Total Transaction Accts 704,332 690,626 797,987 932,204 893,818 6.6%

MMDA & Savings 402,745 411,620 452,730 508,871 521,859 7.2% Retail Time

17.5%

Jumbo Time 342,866 251,901 222,615 134,771 122,439(24.0)%

Retail Time 329,491 283,081 245,409 183,115 160,794(17.4)% Jumbo Time MMDA & Savings

Total Time Deposits 672,357 534,982 468,024 317,886 283,233(20.6)% 14.8% Accounts

23.8%

Total Non-Trans Accts 1,075,102 946,602 920,754 826,757 805,092(7.4)%

Total Deposits 1,779,434 1,637,228 1,718,741 1,758,961 1,698,910(1.2)%

13 Source: SNL Financial, Company Management and Public Filings

Data as of 9/30/13 CONFIDENTIAL

In order to compare Jumbo CDs historically, they have been defined as CDs with $100,000 or more in all periods

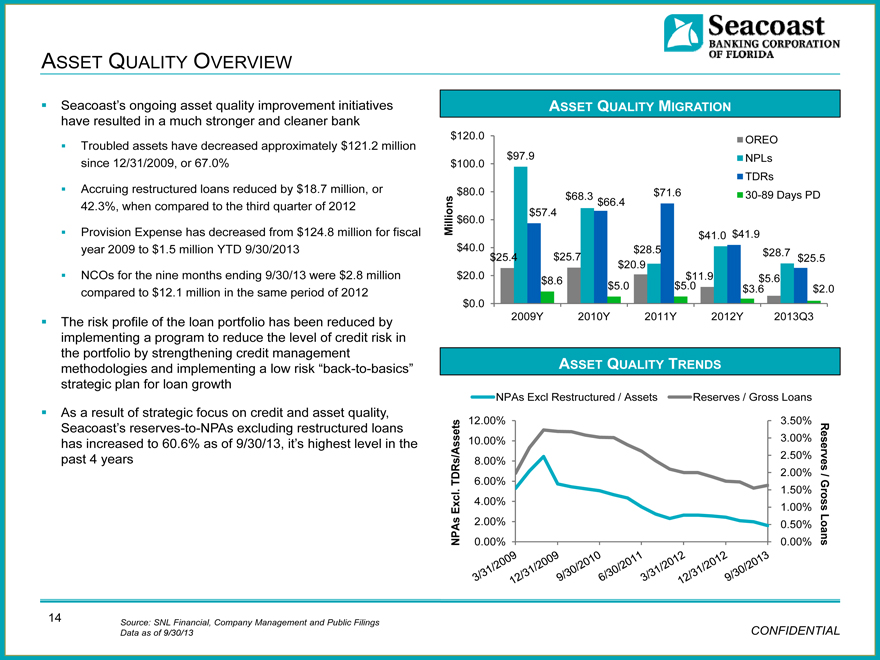

ASSET QUALITY OVERVIEW

Seacoast’s ongoing asset quality improvement initiatives have resulted in a much stronger and cleaner bank

Troubled assets have decreased approximately $121.2 million since 12/31/2009, or 67.0%

Accruing restructured loans reduced by $18.7 million, or 42.3%, when compared to the third quarter of 2012

Provision Expense has decreased from $124.8 million for fiscal year 2009 to $1.5 million YTD 9/30/2013

NCOs for the nine months ending 9/30/13 were $2.8 million compared to $12.1 million in the same period of 2012

The risk profile of the loan portfolio has been reduced by implementing a program to reduce the level of credit risk in the portfolio by strengthening credit management methodologies and implementing a low risk “back-to-basics” strategic plan for loan growth

As a result of strategic focus on credit and asset quality, Seacoast’s reserves-to-NPAs excluding restructured loans has increased to 60.6% as of 9/30/13, it’s highest level in the past 4 years

ASSET QUALITY MIGRATION

$120.0 OREO

$100.0 $97.9 NPLs

TDRs

$80.0 $68.3 $71.6 30-89 Days PD

$66.4

Millions $60.0 $57.4

$41.0 $41.9

$40.0 $25.4 $25.7 $28.5 $28.7 $25.5

$20.9

$20.0 $8.6 $11.9 $5.6

$5.0 $5.0 $3.6 $2.0

$0.0

2009Y 2010Y 2011Y 2012Y 2013Q3

ASSET QUALITY TRENDS

NPAs Excl Restructured / Assets Reserves / Gross Loans

12.00% 3.50%

10.00% 3.00%

8.00% 2.50%

2.00% /

TDRs/Assets 6.00% Reserves

. 1.50% Gr

l

Exc 4.00% 1.00% oss

2.00% 0.50%

NPAs 0.00% 0.00% Loans

14 Source: SNL Financial, Company Management and Public Filings

Data as of 9/30/13 CONFIDENTIAL

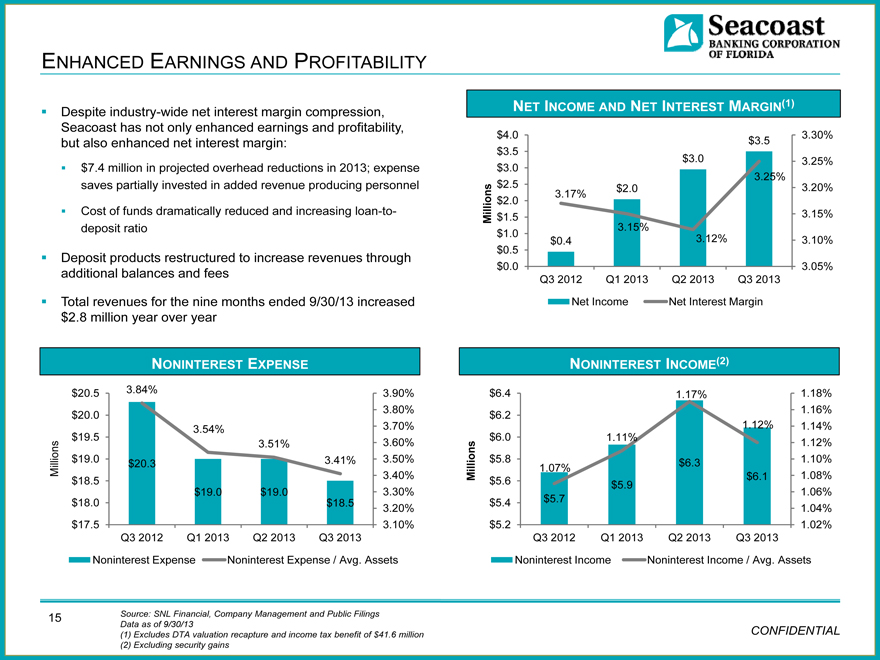

ENHANCED EARNINGS AND PROFITABILITY

Despite industry-wide net interest margin compression, Seacoast has not only enhanced earnings and profitability, but also enhanced net interest margin:

$7.4 million in projected overhead reductions in 2013; expense saves partially invested in added revenue producing personnel

Cost of funds dramatically reduced and increasing loan-to- deposit ratio

Deposit products restructured to increase revenues through additional balances and fees

Total revenues for the nine months ended 9/30/13 increased $2.8 million year over year

NONINTEREST EXPENSE

$ 20.5 3.84% 3.90%

$ 20.0 3.80%

3.54% 3.70%

$ 19.5 3.51% 3.60%

Millions $ 19.0 $20.3 3.41% 3.40% 3.50%

$ 18.5

$19.0 $19.0 3.30%

$ 18.0 $18.5 3.20%

$ 17.5 3.10%

Q3 2012 Q1 2013 Q2 2013 Q3 2013

Noninterest Expense Noninterest Expense / Avg. Assets

NET INCOME AND NET INTEREST MARGIN(1)

$ 4.0 3.30%

$3.5

$ 3.5

$ 3.0 $3.0 3.25%

3.25%

$ 2.5 $2.0 3.20%

$ 2.0 3.17%

Millions $ 1.5 3.15%

3.15%

$ 1.0 $0.4 3.12% 3.10%

$ 0.5

$ 0.0 3.05%

Q3 2012 Q1 2013 Q2 2013 Q3 2013

Net Income Net Interest Margin

NONINTEREST INCOME(2)

$ 6.4 1.17% 1.18%

$ 6.2 1.16%

1.12% 1.14%

$ 6.0 1.11% 1.12%

$ 5.8 $6.3 1.10%

1.07%

Millions $ 5.6 $6.1 1.08%

$5.9 1.06%

$ 5.4 $5.7

1.04%

$ 5.2 1.02%

Q3 2012 Q1 2013 Q2 2013 Q3 2013

Noninterest Income Noninterest Income / Avg. Assets

15 Source: SNL Financial, Company Management and Public Filings

Data as of 9/30/13

(1) Excludes DTA valuation recapture and income tax benefit of $41.6 million CONFIDENTIAL

(2) Excluding security gains

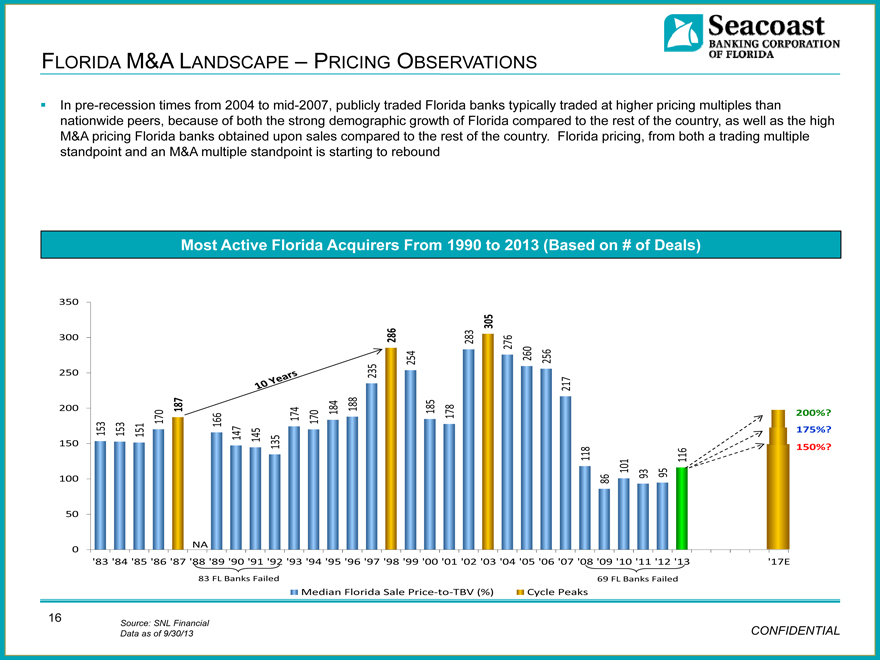

FLORIDA M&A LANDSCAPE – PRICING OBSERVATIONS

In pre-recession times from 2004 to mid-2007, publicly traded Florida banks typically traded at higher pricing multiples than nationwide peers, because of both the strong demographic growth of Florida compared to the rest of the country, as well as the high M&A pricing Florida banks obtained upon sales compared to the rest of the country. Florida pricing, from both a trading multiple standpoint and an M&A multiple standpoint is starting to rebound

Most Active Florida Acquirers From 1990 to 2013 (Based on # of Deals)

350

305

6

300 28 283 276

254 260 256

250 235

217

200 187 4 84 188 185 78

0 7 0 1 200%

17 166 1 17 1

153 153 151 147 145 175%

150 135

118 116 150%

101 93 95

100 86

50

0 NA

‘83 ‘84 ‘85 ‘86 ‘87 ‘88 ‘89 ‘90 ‘91 ‘92 ‘93 ‘94 ‘95 ‘96 ‘97 ‘98 ‘99 ‘00 ‘01 ‘02 ‘03 ‘04 ‘05 ‘06 ‘07 ‘08 ‘09 ‘10 ‘11 ‘12 ‘13 ‘17E

83 FL Banks Failed 69 FL Banks Failed

Median Florida Sale Price-to-TBV (%) Cycle Peaks

16 Source: SNL Financial

Data as of 9/30/13 CONFIDENTIAL

BANKING LANDSCAPE –FLORIDA M&A LANDSCAPE OVERVIEW

FDIC Deals Becoming a Thing of the Past

Focus Now on Open-Bank Deals

Price Expectation Gap is Shrinking

Buyer Landscape Has Narrowed

Buyers’ Currencies will Dictate Pricing

Timing is Everything – Start Preparing Now

Massive Consolidation on the Horizon

Florida has only 12 banks with TX Ratios greater than 200% — a few more failures to come

Most failures are now considered “zombie” banks — best employees and customers have left

Buyers have turned their attention to open-bank deals — lots of discussions and action taking place

Pricing has been increasing rapidly over the last year (with recent deals topping 150% of book value)

Motivated sellers have begun to “pull the trigger” as M&A pricing is showing signs of life

Motivated buyers remain fairly patient but we are starting to see a willingness to stretch on price

Florida’s historic serial buyers are all gone with limited replacements in place (especially public ones) – Opening the door for new Florida acquirers, such as Seacoast now that it is in good regulatory standing

Very few banks with over $1 billion in assets, which is the size that larger regionals and nationwide banks want to focus on

Peak M&A pricing will largely be dictated by the buyers’ trading values

Buyer currencies have started to move up (towards 2x tangible book value)

A few premium priced deals were recently done and there is a feel the next M&A wave is coming

Many small sellers under $500 million in assets could flood the market and many buyers could make an early exit themselves

Expect significant consolidation in Florida over the next 5 years — 100 banks could disappear

After the last major recession in the early 1990s, 180 Florida banks sold in 6 years (~3 per month)

CONFIDENTIAL

17

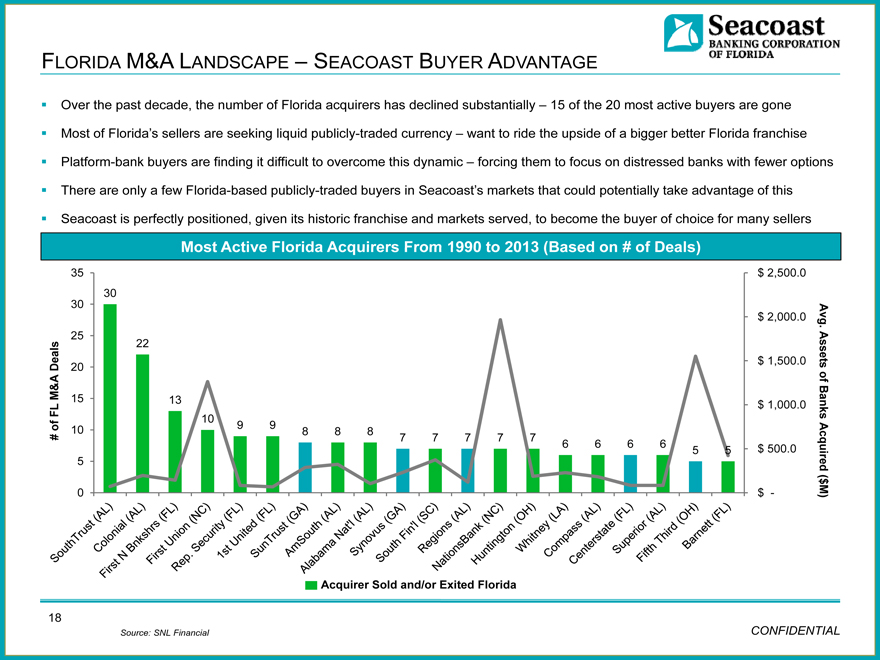

FLORIDA M&A LANDSCAPE – SEACOAST BUYER ADVANTAGE

Over the past decade, the number of Florida acquirers has declined substantially – 15 of the 20 most active buyers are gone

Most of Florida’s sellers are seeking liquid publicly-traded currency – want to ride the upside of a bigger better Florida franchise

Platform-bank buyers are finding it difficult to overcome this dynamic – forcing them to focus on distressed banks with fewer options

There are only a few Florida-based publicly-traded buyers in Seacoast’s markets that could potentially take advantage of this

Seacoast is perfectly positioned, given its historic franchise and markets served, to become the buyer of choice for many sellers

Most Active Florida Acquirers From 1990 to 2013 (Based on # of Deals)

FL M&A Deals

35 30 25 20 15 10 5 0

30

22

13

10 9 9

8 8 8

7 7 7 7 7 6 6 6 6 5 5

$ 2,500.0 $ 2,000.0 $ 1,500.0 $ 1,000.0 $ 500.0 $ -

Avg. Assets of Banks Acquired ($M)

Acquirer Sold and/or Exited Florida

Source: SNL Financial

CONFIDENTIAL

SouthTrust (AL)

Colonial (AL)

First N Bnkshrs (FL)

First Union (NC)

Rep. Security (FL)

1st United (FL)

SunTrust (GA)

AmSouth (AL)

Alabama Nat’l (AL)

Synovus (GA)

South Fin’l (SC)

Regions (AL)

NationsBank (NC)

Huntington (OH)

Whitney (LA)

Compass (AL)

Centerstate (FL)

Superior (AL)

Fifth Third (OH)

Barnett (FL)

18

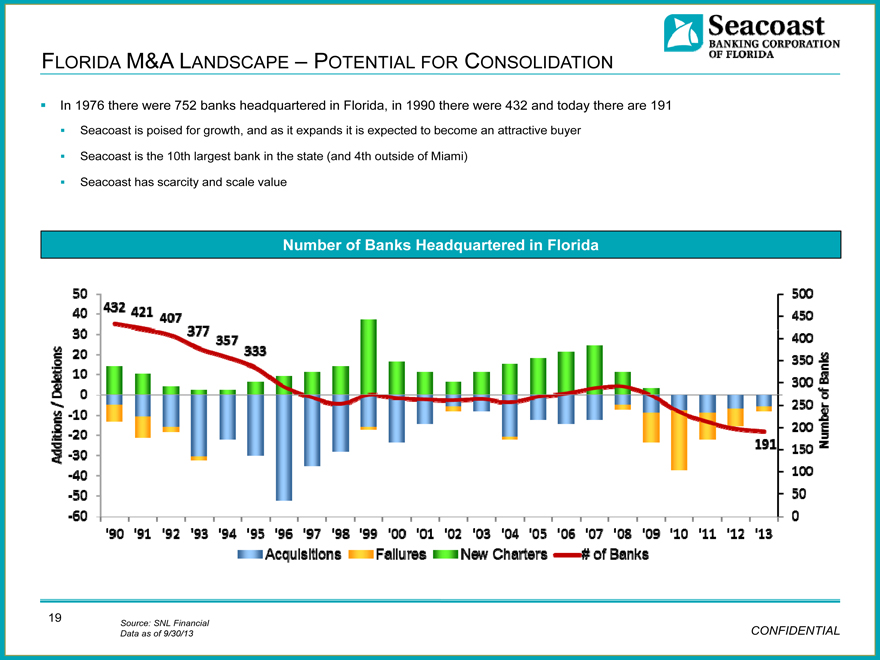

FLORIDA M&A LANDSCAPE – POTENTIAL FOR CONSOLIDATION

In 1976 there were 752 banks headquartered in Florida, in 1990 there were 432 and today there are 191

Seacoast is poised for growth, and as it expands it is expected to become an attractive buyer

Seacoast is the 10th largest bank in the state (and 4th outside of Miami)

Seacoast has scarcity and scale value

Number of Banks Headquartered in Florida

Additions / Deletions

Number of Banks

Acqulsltions

Fallures

New Charters

# of Banks

50 40 30 20 10 0 -10 -20 -30 -40 -50 -60

90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 12 12

0 50 100 150 200 250 300 350 400 450 500

19

Source: SNL Financial

Data as of 9/30/13

CONFIDENTIAL

IN SUMMARY, WHY INVEST IN SEACOAST

Our operating performance is improving rapidly as we have grown our households and market share and emerge from the worst recession to hit Florida since the Great Depression.

Seacoast has significant scarcity value; we are arguably among the most valuable bank franchises in Florida.

We are a leader among community banks in understanding how we will harness technology to meet the evolving needs and demands of our customers in the future.

We have a proven ability to grow our franchise and believe there is unprecedented opportunity for additional organic growth and growth via acquisitions.

CONFIDENTIAL

20