UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 10-K

|

|

x | Annual Report Pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 |

| For the fiscal year ended June 30, 2009 |

Or |

|

o | Transition Report Pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 |

| For the transition period from ______________________________ to ______________________________ |

|

|

Commission file number0-12944

|

ZYGO CORPORATION |

(Exact name of registrant as specified in its charter) |

|

|

|

|

Delaware |

| 06-0864500 |

|

|

| ||

(State or other jurisdiction of |

| (IRS Employer Identification Number) |

|

incorporation or organization) |

|

|

|

|

|

|

| Laurel Brook Road, Middlefield, Connecticut 06455-1291 |

|

|

| |

| (Address of principal executive offices) (Zip Code) |

|

|

|

|

| (860) 347-8506 |

|

|

| |

| (Registrant’s telephone number, including area code:) |

|

|

|

|

| Securities registered pursuant to Section 12(b) of the Act: |

|

|

| |

| None |

|

|

|

|

| Securities registered pursuant to Section 12(g) of the Act: |

|

|

| |

| Common Stock, $.10 Par Value |

|

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in rule 12b-2 of the Exchange act. (Check one):

|

|

|

|

|

Large accelerated filer | o |

| Accelerated filer x | |

Non-accelerated filer | o | (Do not check if a smaller reporting company) | Smaller reporting company o | |

The aggregate market value of the registrant’s Common Stock held by non-affiliates, based upon the closing price of the Common Stock on December 31, 2008, as reported by the NASDAQ National Market, was $64,026,111. Shares of Common Stock held by each executive officer and director and by each person who owns 5% or more of the outstanding Common Stock, based on filings with the Securities and Exchange Commission, have been excluded since such persons may be deemed affiliates. This determination of affiliate status is not necessarily a conclusive determination for other purposes.

Indicate the number of shares outstanding of each of the registrant’s classes of Common Stock, as of the latest practicable date.

16,988,156 Shares of Common Stock, $.10 Par Value, at September 1, 2009

Documents incorporated by reference: Specified portions of the registrant’s Proxy Statement related to the registrant’s 2009 Annual Meeting of Stockholders, to be filed pursuant to Regulation 14A of the Securities Exchange Act of 1934 with the Securities and Exchange Commission, are incorporated by reference into Part II (Item 5) and Part III (Items 10-14) of this Annual Report on Form 10-K to the extent stated herein.

TABLE OF CONTENTS

|

|

|

|

|

|

|

| Page | |

|

|

| ||

|

|

|

|

|

------ |

| 1 |

| |

|

|

|

|

|

|

|

|

| |

|

|

|

|

|

| 2 |

| ||

|

|

|

|

|

------ |

| 9 |

| |

|

|

|

|

|

| 10 |

| ||

|

|

|

|

|

| 14 |

| ||

|

|

|

|

|

| 15 |

| ||

|

|

|

|

|

| 16 |

| ||

|

|

|

|

|

| 16 |

| ||

|

|

|

|

|

|

|

| ||

|

|

|

|

|

| 17 |

| ||

|

|

|

|

|

| 20 |

| ||

|

|

|

|

|

Management’s Discussion and Analysis of Financial Condition and Results of Operations |

| 21 |

| |

|

|

|

|

|

| 31 |

| ||

|

|

|

|

|

| 32 |

| ||

|

|

|

|

|

Changes in and Disagreements With Accountants on Accounting and Financial Disclosure |

| 32 |

| |

|

|

|

|

|

| 33 |

| ||

|

|

|

|

|

| 34 |

| ||

|

|

|

|

|

|

|

| ||

|

|

|

|

|

| 34 |

| ||

|

|

|

|

|

| 34 |

| ||

|

|

|

|

|

Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters |

| 34 |

| |

|

|

|

|

|

Certain Relationships and Related Transactions, and Director Independence |

| 34 |

| |

|

|

|

|

|

| 34 |

| ||

|

|

|

|

|

|

|

| ||

|

|

|

|

|

| 35 |

| ||

|

|

|

|

|

| 38 |

| ||

As used in this Annual Report on Form 10-K, unless the context otherwise requires, the terms “we,” “us,” “our,” “Company,” and “ZYGO” refer to Zygo Corporation, a Delaware corporation.

All statements other than statements of historical fact included in this Annual Report regarding our financial position, business strategy, plans, anticipated sales, orders, market acceptance, growth rates, market opportunities, and objectives of management for future operations are forward-looking statements. These forward-looking statements include without limitation statements under “Business,” “Management’s Discussion and Analysis of Financial Condition and Results of Operations,” and “Risk Factors.” Forward-looking statements are intended to provide management’s current expectations or plans for the future operating and financial performance based upon information currently available and assumptions currently believed to be valid. Forward-looking statements can be identified by the use of words such as “anticipate,” “believe,” “estimate,” “expect,” “intend,” “plans,” “strategy,” “project,” and other words of similar meaning in connection with a discussion of future operating or financial performance. Actual results could differ materially from those contemplated by the forward-looking statements as a result of certain factors such as those disclosed under “Risk Factors.” Such statements reflect our current views with respect to future events and are subject to these and other risks, uncertainties, and assumptions relating to the operations, results of operations, and our growth strategy.

Any forward-looking statements included in this Annual Report speak only as of the date of this document. ZYGO undertakes no obligation to publicly update or revise forward-looking statements to reflect events or circumstances occurring after the date of this Annual Report on Form 10-K.

1

OVERVIEW

Zygo Corporation (“ZYGO,’’ “we,’’ “us,’’ “our,’’ or “Company’’) designs, develops, and manufactures ultra-high precision measurement solutions to improve our customers’ manufacturing yields, and top-tier optical sub-systems and components for original equipment manufacturers (“OEM”) and end-user applications. We operate within two divisions. Our Metrology Solutions Division (also referred to herein as the “Metrology segment”) manufactures products to improve quality, increase productivity, and decrease the overall cost of product development and manufacturing for high-technology companies. Our Optical Systems Division (also referred to herein as the “Optics segment”) provides leading-edge product development and manufacturing services that leverage a variety of core technologies across medical, defense, semiconductor, laser fusion research, biomedical, and other industrial markets.

Our Metrology Solutions Division serves the industrial and semiconductor markets by providing process control for surface shape, roughness and film thickness, which are critical to all of our markets, and through product offerings that measure surface and material characteristics such as roughness, figure, film thickness and transmitted wavefront of flat, spherical, and aspheric components. Our industrial market products serve the defense/aerospace, automotive, consumer electronics, and commercial optics markets, as well as various other miscellaneous markets other than semiconductor. Industrial market products include measurement-based process control systems for defense and aerospace customers, and measurement-based process control and yield-enhancement systems for automotive, consumer electronics, and commercial optical customers.

Our semiconductor product offerings include semiconductor metrology tools, OEM solutions, in-line automated yield improvement systems for both flat panel displays and advanced integrated circuit packaging manufacturing and technology development projects for the semiconductor capital equipment industry. Our displacement measurement systems are used extensively in ultra-precise wafer positioning systems for the semiconductor capital equipment industry. One of our continuing strategic initiatives is to expand our product offerings by applying our patented technology to integrated in-line technology.

In June 2009, we agreed to a supply agreement with Nanometrics Incorporated (“Nanometrics”), whereby we will supply interferometer sensors to Nanometrics for incorporation into the UniFire™ line of products as well as Nanometrics’ family of automated metrology systems. This agreement enables us to accomplish our goal of accelerating the commercial deployment and market penetration of our core interferometer technology into the worldwide semiconductor industry without the investment associated with system integration, distribution, applications and support. In addition to the applications currently addressed by Nanometrics and ZYGO products, the business partnership allows for the joint development of additional technology solutions targeted at the semiconductor and related industries.

In February 2008, we acquired the assets of Solvision, Inc., a Canadian-based company, including its Singapore subsidiary, and entered the market for in-line inspection of flip chip substrates and integrated circuits (“IC”) packaging.

The worldwide economic recession has had a severe impact on our orders, sales, and net results. As a result of the economic downturn, among other things, we have reevaluated our strategic initiatives and our overall business strategy and operations. We are focusing sales, marketing, and research and development efforts on our core metrology and optics technologies, including the potential for strategic alternatives, which could include partnerships, joint ventures, divestitures, or alliances.

Our solutions are primarily based on optical interferometric technology. We continue to be a world leader in optical interferometry with a patent portfolio of over 300 active patents, most of which are related to the broad field of interferometry and its practical application.

Our Metrology Solutions Division is headquartered in Middlefield, Connecticut with operations in various domestic and international locations.

Our Optical Systems Division specializes in producing high precision integrated optical systems and unique system-critical optical components for a variety of applications that include medical laser delivery systems, U.S. Department of Defense (“Defense Department”) applications, 3D medical imaging, and semiconductor lithography. The division creates long-term customer value through, among other things, proprietary manufacturing technology, design for manufacturing and assembly services and specialized manufacturing know-how required to produce Food and Drug Administration (“FDA”) regulated medical devices.

Our integrated system assembly operation for our Optical Systems Division located in Tucson, Arizona is a tier-one optical system assembly facility for high-precision, volume production. We assemble and integrate devices ranging from medical laser

2

delivery systems to 3D dental imaging to opto-electronic surveillance devices. Our integrated system design and prototyping operation, located in Costa Mesa, California, designs and manufactures prototypes utilizing multi-axis alignment, optical contact assembly, custom tooling, single point diamond turning, and our proprietary metrology equipment such as those used to produce lithographic optical systems. We also operate a large format optical fabrication and coating center located in our Middlefield, Connecticut facility. Our vertically integrated approach encompasses CNC glass machining and lightweighting, rotational and double-sided polishing, magneto rheological finishing polishing, and thin film coating, supported by our proprietary metrology equipment. We are one of the world’s largest manufacturers of laser fusion optics and meter-class plano optics, including advanced materials such as sapphire.

We were incorporated in 1970 under the laws of the State of Delaware. The address of our principal executive offices is Laurel Brook Road, Middlefield, Connecticut, 06455-1291. Our telephone number at this address is (860) 347-8506. Our website address is www.zygo.com. The information on our website is not part of this Annual Report on Form 10-K.

MARKETS, PRODUCTS, AND CUSTOMERS

Our business is organized into two operating divisions – Metrology Solutions and Optical Systems. The Metrology segment consists of OEM, in-line, and research instrument products primarily for the semiconductor and industrial markets. The Optics segment consists of components and opto-mechanical assemblies primarily for the medical, defense, and aerospace industries, which are part of the industrial market.

Manufacturers in the semiconductor and industrial markets strive to improve their manufacturing processes and product performance. These improvements allow them to compete more effectively in a marketplace characterized by decreasing product dimensions, increasingly complex manufacturing processes, decreasing product life cycles, declining product prices, and intensifying global competition, among other factors. As such, our precision metrology and optical components and systems are designed to help these manufacturers continually achieve process and design improvements.

Metrology Solutions Division

Semiconductor Market

We serve several areas of the semiconductor market, notably semiconductor manufacturers and capital equipment suppliers, as well as the flat panel display and advanced semiconductor and integrated circuit packaging manufacturers. We have a broad and growing range of products that serve these market areas.

Semiconductor manufacturing processes require demanding metrology and inspection technologies. From bare silicon wafers through the packaged die, metrology and inspection are critical to meeting technology development and process control demands. Recent products introduced by us are enabling high volume semiconductor manufacturing customers to address the challenges of today as well as advanced processing down to and lower than the 45 nanometer (“nm”) node. The majority of our automated semiconductor systems are built on a common, high-throughput platform with a common, configurable sensor head. This approach allows us to leverage engineering and manufacturing investments to produce reliable and cost effective solutions for our customers.

Semiconductor Products

The transistor and associated integrated circuit have transformed the way people work, live and play, creating several multi-billion dollar industries that thrive through innovation, technology, and ultra-large scale integration of micro/nano circuitry. These industries provide components used in everyday appliances, including the more modern mobile phones and wireless internet devices. Due to the ubiquity of the integrated circuit, it is sometimes difficult to fathom the complexities involved in development and manufacturing. State-of-the-art microprocessors have in excess of a billion transistors comprised of components which have physical dimensions as small as 32 nm.

3

In June 2009, we agreed to a supply agreement with Nanometrics, whereby we will supply interferometer sensors to Nanometrics for incorporation into the UniFire™ line of products as well as Nanometrics’ family of automated metrology systems. The in-line semiconductor systems we developed over the last five years, encompassing the UniFire product line, will now be manufactured, sold, and serviced through Nanometrics. These systems are designed to help semiconductor and data storage customers control their high volume manufacturing process. The semiconductor products target wafer based applications (prior to die singulation) and can be utilized for all parts of the process flow, from the production of silicon substrates, through the transistor formation in the front end of the line to the interconnects and bump redistribution layers in the back end of the line. Our single, configurable sensor sits on a common platform, each system having a unique sensor configuration and associated applications. Each system incorporates multiple sensors. The multifunction capability of the overall system enables the consolidation of different metrology measurements into a single system, thereby lowering the overall metrology cost of ownership for the customer.

Photolithography scanners and stepper systems form the core of the semiconductor manufacturing process. These systems image the patterns of stacked layers of circuitry that make up transistors. The photolithographic systems image the circuitry onto silicon wafers for both microprocessors and memory chips, as well as flat panel displays for computers, televisions, and other display products. Several of our products enable these systems to image these circuit patterns reliably and with nanometer precision.

Precision Positioning Systems

The layers of circuit patterns must overlay on top of each other to nanometer precision. To achieve nanometer precision overlay, the silicon wafer must be repeatably positioned to one-tenth the overlay tolerance. Photolithography systems, mask and reticle writers, and yield improvement metrology tools rely on displacement measuring interferometers to provide precise feedback to control the position of the silicon wafer. Our Metrology Solutions Division’s ZMI™ 2400 and ZMI™ 4000 precision positioning feedback systems are designed primarily for photolithography systems. They are also used in a broad range of semiconductor metrology and back-end process tools.

Technology Development Projects

Photolithography scanners image the electronic circuit pattern through a precision projection lens. The optical performance of the lenses required for next-generation photolithography scanners often exceeds the capabilities of commercially available measurement systems. Our expertise in optical interferometer technology, and the practical skills needed to apply this technology, make us well suited to deliver custom solutions to leading photolithography equipment suppliers.

Display Solutions

Flat panel displays (“FPD”) were first used in cell phones and laptop computers, and have grown in popularity for most personal electronics. Many large screen televisions are based on flat panel display technology. Our systems, with ultra high precision measurement solutions, enable our customers to improve flat panel display manufacturing yields. Our OneShot and SureShot™ systems are in-line process control yield enhancement tools. The FPD OneShot tool measures the topography and critical dimensions of key color filter features prior to being combined with the thin-film-transistor panel in the ‘one drop fill’ assembly process. This fully automated system incorporates the latest ZYGO Intellisensor™, optical profiler technology, integrated conveyors or robotics with motion stages, mini-clean room environmental enclosures, and factory floor command and control software. The system measures the height and width of key optical components and predicts the fill volume to increase upstream manufacturing yields.

The SureShot™ FPD product provides overlay and critical dimensions metrology of the individual mask layers post-lithography and helps identify process control problems such as those found in the half tone process. These defects, left unchecked, can lead to product performance issues including variances in luminescence (called MURA) in the finished display. The SureShot tool can be used as an off-line process analysis device or in-line in conjunction with closed loop lithography process control.

In addition to process control, ZYGO manufactures inspection tools used to protect color filter manufacturing processes from the yield-robbing effects caused by the introduction of foreign particles. The ZYGO ClearShot™ tool works in conjunction with automated optical inspection systems to review particles and sort those that will cause optical defects due to their height and lateral dimensions, from those that will not. The use of ZYGO technology in the inspection area results in increased manufacturing yields and increased utilization of the panel maker’s deployed capital.

4

Advanced Chip Packaging and Assembly

During the manufacture of a semiconductor chip, after the chip making process is complete, the silicon wafer on which the chips are fabricated must be diced into individual chips and packaged for customer use. In advanced chip packaging fabrication facilities, the new CP 6300i™ system measures patterned features and films on the surfaces of diced and un-diced chips for process control and yield improvement. The system incorporates a specialized ZYGO NewView optical profiler and wafer positioning system with pattern recognition software. It can be configured for clean room or laboratory use.

Advanced IC Packaging and Assembly

Before an individual semiconductor chip can be placed on a printed circuit board it must be packaged or encased for protection, identification, and wiring/electrical connection. ZYGO AV9000™ systems inspect these final packages for defects using standard 2D image defect and metrology analysis, as well as rapid 3D metrology. The AV9000 systems are based on ZYGO’s FMI technology acquired with the Solvision, Inc. assets. This product is designed to meet today’s requirements, as well as future requirements of the rapidly growing IC Packaging market.

Printed Circuit Board Substrates

Printed circuit substrates interface IC flip chip packages to printed circuit boards. These substrates make the circuit connection via arrays of miniature solder bumps and balls and ZYGO manufactures several tools to measure these bump and ball arrays for process control and yield improvement. Tool applications range from quality control (NANO 3D™) to high volume manufacturing (HS1000), on singulated substrates (HS2000). The newly released Flip Chip CSP2000H tool enables process control on strip and panel formats. These systems are based on technology acquired with the assets of Solvision, Inc.

Industrial Market

Our industrial market covers all areas other than semiconductor. Metrology products for defense and aerospace companies include measurement-based process control systems. Products for automotive, consumer electronics and other customers are measurement-based process control and yield enhancement systems.

Consumer Electronics

Consumer electronics, including cell phones, digital cameras, DVD and CD players, and optical computer drives, have significant optical content. Consumer electronic optics, which provides imaging and data storage, are manufactured in quantities in the hundreds of thousands to millions of components per year. These complex miniature optical systems require precise optical testing—from development to in-line process control—which our measurement-based process control and yield enhancement systems are designed to perform.

VeriFire Asphere System

The VeriFire Asphere provides high resolution 3-Dimensional surface metrology for aspheric shaped surfaces using patented non-contact interferometric techniques for production and process control. Aspheres are important in consumer electronics products, cameras, military/defense optics, and commercial optics and represent a growing segment in the optics markets.

GPI and VeriFire Systems

The development of new optical systems for any application requires flexible and easy to use test equipment. The ZYGO GPI and VeriFire systems are our latest products in our established product family that has improved optical testing and continues to evolve to meet changing requirements. Consumer electronics production applications for larger optics, greater than a 25 mm diameter, and research and development for any size application rely on these products for critical developmental data and process control feedback in production. These products are widely used due to their configuration flexibility in both hardware set ups and ZYGO’s MetroPro™ data analysis software.

PTI™ 250

Consumer electronics typically contain small optics, less than 30 mm diameter. The PTI 250 is a small bench top optical test system in the tradition of our industry standard GPI. The system meets the consumer market demand by combining high-quality optics with ZYGO’s MetroPro data analysis software.

5

DVD™ 400, BluRay™, and HD DVD™

The next generation of DVD players and computer memories use blue light at 405 nm wavelength to increase the amount of data on a DVD disk. ZYGO’s DVD 400 interferometer is used by developers of these next generation systems. ZYGO’s DVD 400P is our system for the production floor.

Automotive Industry

The automotive industry is striving to improve fuel economy and decrease environmental pollution to meet customer demand and adhere to government regulation. Improving both requires more efficient engines, including the fuel injection system. Since high-pressure valves and sealing surfaces found in the fuel injection system must be manufactured to high precision, our measurement-based process control and yield-enhancement systems are used in the development and manufacture of these components.

NewView 7200/7300 and Delta Systems

Our high precision metrology equipment is well suited for fuel injector components, which are ground or lapped to tolerances of one-hundred billionths of a meter. Our patented “FDA” data acquisition system for the NewView optical profiler meets this high-precision measurement requirement. The NewView Delta is a production floor packaged system, also targeted to this growing market.

Defense/Aerospace

GPI and VeriFire Systems

Developing state-of-the-art optical designs and manufacturing technology for the defense/aerospace market also requires leading edge metrology systems for manufacturing process control and development. Our industry standard GPI and VeriFire optical interferometers test both the optical components and systems for design compliance. Our VeriFire Asphere rapidly measures asphere shaped optics in a production environment. Our GPI PE continues our move to the production floor, providing laboratory level results in a production environment. Using patented algorithms, the GPI PE removes the degrading effects of vibration from the measurement without the need for new expensive hardware. This system is primarily used in the production of military and commercial optics.

The GPI FlashPhase system operates on the production floor where standard interferometers cannot measure or do not meet the demanding requirements of the defense/aerospace market. With our proprietary data acquisition, GPI FlashPhase can measure in the turbulent and vibrating environments that are often found in defense/aerospace applications. We are also active in designing and manufacturing custom systems for defense/aerospace applications, especially interferometers that operate at infrared wavelengths, which are unique to this market.

Our major metrology customers include: AU Optronics, Bosch, Canon, Lockheed Martin, Raytheon, and Nikon.

Optical Systems Division

Industrial Market

Supporting both the projection lens and stage positioning systems, we supply high precision stage mirrors and lithographic lenses to leading photolithographic OEM’s and end users. In addition, we design and manufacture deep UV objectives, inspection systems and components to a wide range of industrial customers as well as supporting the optical needs of our Metrology Solutions division.

Defense/Aerospace

Defense and aerospace companies use optical technology in a broad range of applications. One application is the enhancement of human sight through imaging systems, such as telescopes, that are used in satellite and airborne reconnaissance, fire-control systems, and hand-held viewers. Defense Department areas of focus include fire control, remote sensing, flight simulation, avionics, tracking, stealth systems and high energy weapon systems. Our Optical Systems Division participates in a variety of defense applications ranging from high performance sapphire electro magnetic interference (“EMI”) windows used in stealth aircraft and ships to satellite optical sensing packages and state of the art flight simulation helmet mounted displays. In addition to mainstream Defense Department and foreign government applications, we are a leading manufacturer of several critical path components to the largest nuclear research laser system ever deployed by the National Ignition Facility (“NIF”), which is used for both weapons maintenance programs and the development of nuclear fusion energy sources. In addition, our Optical Systems Division has expanded into long range surveillance systems valuable to homeland security applications, such as nuclear power plant perimeter control, border surveillance, and seaport monitoring.

6

Nuclear research for both weapons maintenance programs and the development of nuclear fusion energy sources also use large optical lasers at a number of worldwide facilities, including NIF. In addition, projection systems in computer-based flight and battlefield simulation use sophisticated optical systems. Several of our products support these and other defense/aerospace programs.

Medical/Biomedical

The medical and biomedical markets are growing rapidly. The increased demand for high precision medical devices continues to be driven by an aging population and consumers’ desire to improve their quality of life. Our Optical Systems Division addresses this demand with specialized design for manufacturing and assembly services tailored to producing high-end diagnostic, processing and surgical devices. In addition, the group offers a variety of process control advantages including medical device quality management systems, such as ISO 13485:2003. Key application areas are diagnostic and surgical ophthalmic devices, inter-oral 3D imaging, and biomedical cell sorting. Supporting these applications are our facilities in Tucson, Arizona (manufacturing) and Costa Mesa, California (development and prototype manufacturing). Strategically located, these facilities are capable of providing highly focused engineering support to fast growing medical and biomedical regions for both manufacturing and research.

Our major optics customers include Commissariat à l’énergie atomique, Abbott Medical Optics, Lawrence Livermore National Laboratory, 3M, Brontes, and others.

For further information on the Metrology Solutions Division and the Optical Systems Division, see Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations and the Financial Statements.

Competition

The semiconductor and industrial markets in which we participate are intensely competitive and are characterized by price pressure and rapid technological change. Furthermore, these markets are dominated by a few market leaders. We are one of a limited number of companies that develop and market yield-enhancement solutions. Our primary yield enhancement competitors include Agilent’s Laser Interferometer Positioning Systems Division, Veeco’s Metrology Division, SNU Precision, KLA-Tencor, and Rank Taylor Hobson. The principal factors upon which we compete are performance, flexibility, value, on-time delivery, responsive customer service and support, and breadth of product line.

High precision optics manufacturing is dominated by relatively few companies who have both strong engineering depth and metrology capability. The competition is further segmented by the two groups within the division, Optical Components and Electro-Optics. The Optical components primary competitors include L-3 Tinsley, Exotic Electro-Optics and Sagem, which are able to provide similar performance levels for both meter class plano optics and airborne reconnaissance windows. The Electro-Optics group which provides significant value added engineering coupled with metrology based manufacturing and FDA regulatory control has various levels of competition from Elcan Optical Technologies, Jenoptik and ASML. The principal factors upon which we compete are high precision metrology based manufacturing, value-added engineering, regulatory and quality controls and customer service.

Research, Development and Engineering Operations

We operate in industries that are subject to rapid technological change and engineering innovation. As such, we dedicate substantial resources to research and development. At June 30, 2009, we employed 126 individuals, or approximately 25% of our workforce, within our research and development and engineering operations. Our strategy is to form close technical working relationships with customers and OEM suppliers in our markets to ensure that our products are commercially relevant. We also maintain a close working relationship with various research groups and academic institutions in the United States and abroad. We have been recognized as an innovator in commercializing technology, as evidenced by our numerous achievement awards, including R&D 100 Awards, Photonics Spectra Circle of Excellence Awards, and others. We believe that continued enhancement, development, and commercialization of new and existing products and systems are essential to maintaining and improving our leadership position.

Patents and Other Intellectual Property

Our success and ability to compete depend substantially on our technology. We have been developing a portfolio of intellectual property for over 30 years, and we rely on a combination of patent, copyright, trademark, trade secret laws, and license agreements to establish and protect our proprietary rights for our products.

Since we introduced the first optical interferometer in 1972, we have had 297 United States patents issued, of which approximately 230 are currently active, and approximately 130 foreign patents issued, of which approximately 100 are active. We have approximately 40 United States and approximately 140 foreign patent applications pending. In addition, we have a number of registered and unregistered trademarks.

7

While we rely on patent, copyright, trademark, and trade secret laws to protect our technology, we also believe that the technological and creative skills of our personnel, new product developments, frequent product enhancements, and reliable product maintenance are essential to establishing and maintaining a technology leadership position. We do not expect expirations in the near future related to our active patents to have a material effect on our business.

BACKLOG AND ORDERS

Backlog at June 30, 2009 was $38.3 million, a decrease of $34.0 million as compared with $72.3 million at June 30, 2008. The fiscal 2009 year-end backlog consisted of $18.6 million, or 49%, in the Metrology segment and $19.7 million, or 51%, in the Optics segment. Orders for the fiscal year ended June 30, 2009 totaled $82.0 million and consisted of $57.8 million, or 70%, in the Metrology segment and $24.2 million, or 30%, in the Optics segment.

MARKETING AND SALES

Our sales and marketing strategy is to establish and/or solidify strategic relationships with leading OEMs and end-users in targeted sectors within our markets. The selling process for our products is performed through our worldwide sales organization operating out of regional sales offices in California, China, Connecticut, Germany, Japan, Singapore, and Taiwan. Supporting this core sales team are business development, marketing, service, and engineering specialists representing our various optics and metrology units in Connecticut, Arizona, California, Florida, Canada, and Singapore. Product promotion is done through trade shows, printed and e-business advertising, and industry technical organizations.

The following table sets forth the percentage of our total sales by region (based on shipping destination, including sales delivered through distributors) during the past three years:

|

|

|

|

|

|

|

|

|

|

|

|

| Fiscal Year Ended June 30, |

| |||||||

|

|

| ||||||||

|

| 2009 |

| 2008 |

| 2007 |

| |||

|

|

|

|

| ||||||

Americas |

|

| 47 | % |

| 48 | % |

| 39 | % |

|

|

|

|

| ||||||

Far East: |

|

|

|

|

|

|

|

|

|

|

Japan |

|

| 23 | % |

| 28 | % |

| 37 | % |

Pacific Rim |

|

| 18 | % |

| 10 | % |

| 13 | % |

|

|

|

|

| ||||||

Total Far East |

|

| 41 | % |

| 38 | % |

| 50 | % |

|

|

|

|

| ||||||

Europe |

|

| 12 | % |

| 14 | % |

| 11 | % |

|

|

|

|

| ||||||

Total |

|

| 100 | % |

| 100 | % |

| 100 | % |

|

|

|

|

| ||||||

Customer service is an essential part of our business since product up time is critical given its effect on our customers’ production efficiency. As of June 30, 2009, our global sales customer support and service organization consisted of 93 people skilled in sales, marketing, optical and electro component repair, software, application and system integration, diagnostics, and problem-solving capabilities.

MANUFACTURING, RAW MATERIALS, AND SOURCES OF SUPPLY

Our principal manufacturing activities are conducted at our facilities in Middlefield, Connecticut and Tucson, Arizona. We also perform manufacturing activities in our Canada, Singapore, and China facilities and utilize a third-party assembly operation in Taiwan for our flat panel display systems.

We maintain an advanced optical components manufacturing facility in Middlefield, Connecticut, specializing in the fabrication, polishing, and coating of plano, or flat, optics for sales to third parties, as well as the manufacturing of a wide variety of optics that are used in our metrology products. Our manufacturing activities for our metrology products consist primarily of assembling and testing components and sub-assemblies supplied by us and third-party vendors, and then integrating these components and sub-assemblies into our finished products.

Our optical assembly manufacturing activities are conducted in our Tucson, Arizona facility. We integrate our optics, optics from third party vendors, and mechanical sub-systems utilizing our metrology in this facility.

Certain components and sub-assemblies incorporated into our systems are obtained from a limited group of suppliers. We routinely monitor limited source supply parts, and we endeavor to ensure that adequate inventory is available to maintain manufacturing schedules should the supply of any part be interrupted. Although we seek to reduce our dependence on limited source suppliers, we have not qualified a second source for some of these products and the partial or complete loss of certain of these sources could have a negative impact on our results of operations and damage customer relationships.

8

AVAILABLE INFORMATION

We make available free of charge through our website, www.zygo.com, our annual reports on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K, proxy statements, and all amendments to those reports as soon as reasonably practicable after such material is electronically filed with the Securities and Exchange Commission (“SEC”). These reports may also be obtained without charge by contacting Investor Relations, Zygo Corporation, Corporate Headquarters, Laurel Brook Road, Middlefield, Connecticut 06455-1291, phone: (860) 347-8506. Our Internet website and the information contained therein or incorporated therein are not intended to be incorporated into this Annual Report on Form 10-K. In addition, the public may read and copy any materials we file with the SEC’s Public Reference Room at 100 F Street, NE, Room 1580, Washington, DC 20549 or may obtain information by calling the SEC at 800-SEC-0330. Moreover, the SEC maintains an Internet website that contains reports, proxy, and information statements, or other information regarding reports that we file electronically with them at http://www.sec.gov.

EMPLOYEES

At June 30, 2009, we employed 484 people and 11 temporary agency and independent contractors worldwide. We employed 194 in manufacturing, 126 in research and development, 93 in sales and marketing, and 82 in management and administration. Our employees are not represented by a labor union or a collective bargaining agreement. We regard our employee relations as satisfactory.

EXECUTIVE OFFICERS OF THE REGISTRANT

J. Bruce Robinson – age 67 – Chief Executive Officer

Mr. Robinson has served as our Chief Executive Officer since June 2009, as Chairman and Chief Executive Officer from December 2006 to May 2009, as Chairman, President, and Chief Executive Officer from November 2000 to November 2006, as President and Chief Executive Officer from November 1999 to November 2000, and as President from February 1999 to November 1999. Previously, he spent 25 years with The Foxboro Company, where his most recent positions were President Worldwide Operations from 1996 to 1998 and President of European Operations from 1990 to 1996. Mr. Robinson is also a director of our company.

John M. Stack – age 44 - President, Optical Systems Division

Mr. Stack joined our company in November 2006 and has served as President of the Optical Systems Division since December 2006. Previously he spent 18 years with Edmund Optics Inc., a supplier of optics and optical components, where his most recent position was President and Chief Operating Officer from 2001 to 2006. Prior to that Mr. Stack held several management positions at Edmund Optics Inc. including Executive Vice President, Director of Engineering and Application Engineering Manager.

Walter A. Shephard – age 55 – Vice President, Finance, Chief Financial Officer, and Treasurer

Mr. Shephard has served as Vice President, Finance, Chief Financial Officer, and Treasurer since February 2004. Previously, he was a Principal with the Loftus Group, LLC, a management consulting firm, from November 2002 to January 2004. From 1983 to 2001, Mr. Shephard served in various capacities with GenRad, Inc., including Vice President Finance and Chief Financial Officer, Vice President of Investor Relations, and Treasurer.

Douglas J. Eccleston – age 60 – Senior Vice President, Precision Positioning Systems

Mr. Eccelston has served as Senior Vice President, Precision Positioning Systems since February 2007 and as Vice President, Precision Positioning Systems from March 2003 to January 2007. From 1977 to 2002, he held various management positions with Corning Incorporated, including most recently as a Business General Manager for the Photonic Technologies division.

William H. Bacon – age 59 – Vice President, Corporate Quality and Support Services

Mr. Bacon has served as Vice President, Corporate Quality and Support Services since March 2003. Previously, he served as our Vice President, Manufacturing from April 2002 to March 2003, Vice President, Metrology Manufacturing from April 2000 to April 2002, and Vice President, Corporate Quality from January 1996 to April 2000. From November 1993 to January 1996, Mr. Bacon was Director of Total Quality and also served as Manager of Instrument Manufacturing from June 1987 to November 1993.

David J. Person - age 61 - Vice President, Human Resources

Mr. Person has served as Vice President, Human Resources since September 1998. Previously, he served in a number of senior human resource management positions with Digital Equipment Corporation from 1972 to September 1998.

Under the By-laws, executive officers serve for a term of one year and until their successors are chosen and qualified unless earlier removed.

9

We are subject to numerous known and unknown risks, many of which are described below and elsewhere in this Annual Report. Any of the events described below could have a material adverse effect on our business, financial condition and results of operations. Additional risks and uncertainties that we are not aware of, or that we currently deem to be immaterial, could also impact our business and results of operations.

General economic conditions and the related deterioration in the global business environment could have a material adverse effect on our business, operating results and financial condition.

Global consumer confidence has eroded amidst concerns over, among other things, declining asset values, inflation, volatility in energy costs, geopolitical issues, the availability and cost of credit, rising unemployment, and the stability and solvency of financial institutions, financial markets, businesses and sovereign nations. These concerns have slowed global economic growth and have resulted in recessions in numerous countries, including many of those in North America, Europe and Asia, where the Company does substantially all of its business. Recent economic conditions had a negative impact on our results of operations during fiscal 2009 due to reduced customer demand and we expect this trend to continue for at least the next several fiscal quarters. As these economic conditions continue to persist, or if they worsen, a number of negative effects on our business could result, including customers or potential customers reducing or delaying orders, the insolvency of key suppliers which could result in production delays, the inability of customers to obtain credit, and the insolvency of one or more customers. Any of these effects could impact our ability to effectively manage inventory levels and collect receivables, create unabsorbed costs due to lower net sales, and ultimately decrease our net sales and profitability including write-downs of assets.

We are subject to environmental laws and regulations and may have liabilities arising from environmental matters.

We are subject to a variety of environmental regulations relating to the use, storage, discharge, and disposal of hazardous chemicals used during our manufacturing processes. Any failure by us to comply with applicable regulations could subject us to future liabilities or the suspension of production. We are aware of certain levels of contamination on our property which are below reportable levels. In addition, we are aware of certain contamination on an adjacent property that we formerly owned. We are unable to determine or reasonably estimate the amount of cost, if any, that we might incur or for which we may potentially be responsible to remediate the situation or for damages which may have resulted or result from the situation. In addition, environmental regulations could restrict our ability to expand our facilities or could require us to acquire costly equipment or to incur other significant expenses to comply with such regulations.

We are dependent on the semiconductor industry which, as a whole, is volatile.

Our business is significantly dependent on capital expenditures and component requirements for manufacturers in the semiconductor industry. This industry is cyclical and has historically experienced periods of oversupply, resulting in significantly reduced demand for capital equipment, including the products manufactured and marketed by us. For the foreseeable future, our operations will continue to be dependent on the capital expenditures in this industry, which in turn is largely dependent on the market demand in the semiconductor markets. There is currently a severe downturn in the capital expenditures of these manufacturers and this downturn may continue for an extended period of time.

We have been dependent on sales to one large customer; the loss of this customer or expected near-term reduction in orders from this customer has and would materially affect our sales and profitability.

During fiscal 2009, 2008, and 2007, sales to Canon, our largest customer in those periods, accounted for 14%, 19%, and 27% of our net sales, respectively. We expect that sales to Canon will continue to represent a significant, yet declining, percentage of our net sales for the near future. Canon is an original investor in our company, the owner at June 30, 2009 of approximately 7% of our outstanding shares of common stock, and is a distributor of certain of our products in the Japanese market. A reduction or delay in orders from this customer, including reductions or delays due to market, economic, or competitive conditions in the industries in which we or our customer serves, could have a material adverse effect upon our results of operations. Our customers, including Canon, generally do not enter into long-term agreements obligating them to purchase our products.

10

Our substantial international sales are subject to risk.

We sell our products internationally, primarily to customers in Japan and throughout the Pacific Rim. Net sales to customers outside the United States accounted for approximately 53%, 52%, and 61% of our net sales in each of the fiscal years ended June 30, 2009, 2008, and 2007, respectively, and are expected to continue to account for a substantial percentage of our net sales.

International sales and foreign operations are subject to inherent risks. These risks include the economic conditions in these various foreign countries and their trading partners, political instability, longer payment cycles, greater difficulty in accounts receivable collection, compliance with foreign laws, changes in regulatory requirements, tariffs or other barriers, difficulties in obtaining export licenses, staffing and managing foreign operations, exposure to currency exchange fluctuations, transportation delays, and potentially adverse tax consequences.

Our sales and costs are negotiated and paid primarily in U.S. dollars. However, changes in the values of foreign currencies relative to the value of the U.S. dollar can render our products comparatively more expensive to the extent locally produced alternative products are available. Such conditions could negatively affect international sales of our products and foreign operations, as would changes in the general economic conditions in those markets. For our sales that are based in local currency, we are exposed to foreign exchange fluctuations from the time customers are invoiced in local currency until collection occurs. For fiscal 2009, approximately 24% of our sales were denominated in foreign currencies. We hedge certain intercompany transactions by entering into forward contracts to reduce the impact of adverse fluctuations on earnings associated with foreign currency exchange rate changes. We do not enter into any derivative transactions for speculative purposes. These contracts are entered into for periods consistent with the currency transaction exposures, generally three to nine months. Generally, any gains and losses on the fair value of these contracts are expected to be largely offset by gains and losses on the underlying transactions. There can be no assurance that risks inherent in international sales and foreign operations will not have a material adverse effect on our results of operations in the future.

Acquisitions may entail certain operational and financial risks.

Our growth strategy includes expanding our products and services, and we may seek acquisitions or make internal investments to strategically expand our business. We regularly review potential acquisitions of businesses, technologies, or products complementary to our business and periodically engage in discussions regarding such possible acquisitions. Acquisitions involve numerous risks, including some or all of the following: substantial cash expenditures and capital investments; potentially dilutive issuance of equity securities; incurrence of debt and contingent liabilities; amortization of certain intangible assets; difficulties in assimilating the operations and products of the acquired companies; diverting our management’s attention away from other business concerns; risks of entering markets in which we have limited or no direct experience; the inability to manage the growth expected for various acquisitions; potential loss of key employees of the acquired companies in the process of integrating personnel with disparate business backgrounds; and combining different corporate cultures.

We cannot assure you that any acquisition, including the acquisition of the Solvision, Inc. assets which generated losses in fiscal 2009 and 2008, will result in long-term benefits to us or that our management will be able to effectively manage the acquired businesses. We may also incorrectly judge the value or worth of an acquired company or business or of a line of business to which we devote internal resources and funding. We have in the past disposed or divested ourselves of several companies or lines of business that previously were acquired by us or in which we internally invested, at a significant net loss to us.

Our quarterly operating results fluctuate and may continue to fluctuate in the future.

Our quarterly and annual operating results have varied in the past and may vary significantly in the future depending on factors such as: budgeting cycles of our customers; the size, timing, and recognition of revenue from significant orders; increased competition; our ability to develop innovative products; the timing of new product releases by us or our competitors; market acceptance of our products; changes in our and our competitors’ pricing policies; changes in operating expenses and personnel changes; the effect of our acquisitions and consequent integration; changes in our business strategy; and general economic factors.

Due to these and other factors, we believe that quarter-to-quarter comparisons of our operating results may not be meaningful. You should not rely on our results for one quarter as any indication of our future performance. In future periods, our operating results may be below the expectations of public market analysts or investors. If this occurs, the price of our common stock would likely decrease.

Current conditions in the domestic and global economies are extremely uncertain. As a result, it is difficult to estimate the level of growth for the economy as a whole or of capital expenditures in the semiconductor and industrial markets. Because all of the components of our budgeting and forecasting are dependent on estimates of spending within these markets, the prevailing economic uncertainty renders estimates of future revenue and expenses even more difficult than usual to make.

11

Our scheduled backlog may not result in future sales.

We schedule the production of our systems based in part upon order backlog. Due to possible customer changes in delivery schedules and cancellations of orders, our backlog at any particular date is not necessarily indicative of actual sales for any succeeding period. There can be no assurance that amounts included in our backlog will ultimately result in future sales. We have experienced push-outs and cancellations in the semiconductor capital equipment and electro-optics sectors. A reduction in backlog during any particular period, or the failure of our backlog to result in future sales could adversely affect our results of operations.

Our lengthy sales cycle could affect our manufacturing schedule and cause us to incur expenses without realizing sales.

Our lengthy and variable qualification and sales cycle makes it difficult to predict the timing of a sale or whether a sale will be made, which may cause us to have excess manufacturing capacity or inventory and negatively affect our operating results. As is typical in the industry, our customers generally expend significant efforts in evaluating and qualifying our products and manufacturing process. This evaluation and qualification process frequently results in a lengthy sales cycle, typically ranging from three to six months and sometimes longer. While our customers are evaluating our products and before they place an order with us, we may incur substantial sales, marketing, and research and development expenses, expend significant management efforts, increase manufacturing capacity and order long-lead-time supplies prior to receiving an order. Even after this evaluation process, it is possible that a potential customer will not purchase our products. In addition, product purchases are frequently subject to unplanned processing and other delays, particularly with respect to larger customers for which our products represent a very small percentage of their overall purchasing activity.

If we increase capacity and order supplies in anticipation of an order that does not materialize, our gross margins may be negatively impacted, and we may have to carry or write off excess inventory. Even if we receive an order, the additional manufacturing capacity that we add to service the customer’s requirements may be underutilized in a subsequent quarter. Either situation could cause our results of operations to be adversely affected. Our long sales cycles also may cause our revenues and operating results to vary significantly and unexpectedly from quarter to quarter and make us more susceptible to the effects of general economic downturns.

We face risks associated with manufacturing forecasts.

If we fail to predict our manufacturing requirements accurately, we could incur additional costs or experience manufacturing delays, which could cause us to lose orders or customers and result in lower net sales. We currently use a rolling 12-month forecast based primarily on our anticipated product orders and our product order history to help determine our requirements for components and materials. It is very important that we accurately predict both the demand for our products and the lead-time required to obtain the necessary components and raw materials. Lead times for materials and components that we order vary significantly and depend on factors such as the specific supplier, the size of the order, contract terms, and demand for each component at a given time. If we underestimate our requirements, we may have inadequate manufacturing capacity or inventory, which could interrupt manufacturing of our products and result in delays in shipments and net sales. If we overestimate our requirements, we could have excess inventory of parts. In addition, delays in the manufacturing of our products could cause us to lose orders or customers.

Our stock price may fluctuate significantly due to a variety of risks.

We believe that factors such as the announcement of new products or technologies by us or our competitors, market conditions in the semiconductor and industrial markets, and quarterly fluctuations in financial results can be expected to cause the market price of our common stock to vary substantially. Further, our net sales or results of operations in future quarters may be below the expectations of public market securities analysts and investors. In such event, the price of the common stock would likely decline. In addition, historically the stock market has experienced price and volume fluctuations that have particularly affected the market prices for many high technology companies and which often have been unrelated to the operating performance of such companies. The market volatility may adversely affect the market price of shares of our common stock. Furthermore, our common stock trading price may be more susceptible to market fluctuations due to the relatively small public float and trading volume of our stock and our dependence on a limited number of industries.

12

We operate in a highly competitive industry.

We face competition from a number of companies in all our markets, many of which have greater manufacturing and marketing capabilities, and greater financial, technological, and personnel resources. In addition, we compete with the internal development efforts of our current and prospective customers, some of which may attempt to become vertically integrated. Our competitors can be expected to continue to improve the design and performance of their products and to introduce new products with competitive price/performance characteristics. Competitive pressures may necessitate price reductions, which can adversely affect results of operations. Although we believe that we have certain technical and other advantages over some of our competitors, maintaining such advantages will require a continued high level of investment by our company in research and development and sales, marketing, and service. There can be no assurance that we will have sufficient resources to continue to make such investments or that we will be able to make the technological advances necessary to maintain such competitive advantages. In addition, due to historical relationships and possible prior investments by potential customers in competitive product lines, it may be more difficult for us to realize certain of our growth strategies and initiatives. There can be no assurance that the basis of competition in the industries in which we compete will not shift.

Our inability to anticipate and keep pace with rapidly changing technological developments in the markets in which we operate could have a material adverse effect on our business.

The market for our products is characterized by rapidly changing technology. Our future success will continue to depend upon our ability to enhance our current products and to develop and introduce new products that keep pace with technological developments and evolving industry standards, respond to changes in customer requirements, and achieve market acceptance. The development of new technologically advanced products is a complex and uncertain process requiring high levels of innovation, as well as the accurate anticipation of technological and market trends. With continuing advances in technology, potential product advancements require an increasing allocation of resources, including potentially more resources than we then would have available.

We commit significant financial and personnel resources on a continuous basis to redesign and enhance our instruments, systems, and components and upgrade our proprietary software technology incorporated in our products. Any failure by us to anticipate or respond adequately to technological developments and customer requirements, or any significant delays in product development or introduction, could have a material adverse effect on our business and impact our relationships with customers. This could have an impact on customers’ willingness to share proprietary information about their requirements and participate in collaborative efforts with us. There can be no assurance that our customers will continue to provide us with timely access to such information, that we will be successful in developing and marketing new products and services or product and service enhancements on a timely basis, or respond effectively to technological changes or new product announcements by others. In addition, there can be no assurance the new products and services or product enhancements, if any, which we developed will achieve market acceptance.

We may be unable to enforce or defend our ownership and use of proprietary technology.

Our success is heavily dependent upon our proprietary technology. There can be no assurance that the steps taken by us to protect our proprietary technology will be adequate to prevent misappropriation of our technology by third parties or will be adequate under the laws of some foreign countries, which may not protect our proprietary rights to the same extent as do laws of the United States. We have been experiencing an increased level of sales in China and other foreign countries which historically have created concerns for various companies. In addition, there remains the possibility that others will “reverse engineer” our products in order to determine their method of operation and introduce competing products or that others will develop competing technology independently. Any such adverse circumstances could have a material adverse effect on our results of operations.

Our business depends on management and technical personnel who are in great demand.

Our success depends in large part upon the continued services of many of our highly skilled personnel involved in management, research, development and engineering, sales and marketing, manufacturing, and support and upon our ability to attract and retain additional highly qualified employees. Our employees may voluntarily terminate their employment with us at any time. Competition for these individuals from a variety of employers, including our competitors and companies in computer or technology-related industries, at times is intense. In response to the difficult economic environment, we instituted certain reductions in workforce and furlough programs this past year, which may further make it difficult to attract and retain highly qualified personnel. We cannot assure you that we will be able to retain our existing personnel or attract and retain additional personnel.

13

We are exposed to significant delays and additional costs if we do not receive adequate or timely supplies of raw materials and other supplies upon which we depend.

We are dependent on suppliers for raw materials and various electrical, mechanical, and optical supplies. Although we enter, either directly or through our contract manufacturers, into purchase orders with our suppliers based on our forecasts, we do not have any guaranteed supply arrangements with these suppliers. Moreover, as our demand for supplies increases, we may not be able to obtain these supplies in a timely manner. If any relationship with a key supplier is terminated or if a supplier fails or is unable to provide reliable services or equipment and we are unable to reach suitable alternative solutions quickly, we may experience significant delays and additional costs in the manufacturing of our products. If our key suppliers cease manufacturing the supplies we require, if their manufacturing operations are interrupted for any significant amount of time, or if they are unable or unwilling to supply us for any other reason, including capacity constraints, then we may be at least temporarily unable to obtain these supplies, thus exposing us to significant delays and additional costs. Currently there are only a limited number of companies that are capable of supplying optical materials in the quantity and of the quality we require.

We assemble our flat panel display systems in Taiwan through a third party. We are dependent on the third party to assemble the systems accurately and on a timely basis. To the extent the quality of work, including any individual unit, causes delays or cancellations in shipments to our customers, our results could be adversely affected.

Our products may contain defects that are undetected until after our products are installed which may lead to a loss of reputation and customers.

Our products are deployed in large and complex systems and may contain defects that are not detected until after our products have been installed, which could damage our reputation and cause us to lose customers. We design some of our products for deployment in large and complex optical networks. Because of the nature of these products, they can only be fully tested for reliability when deployed in networks for long periods of time. Our customers may discover defects in our products only after they have been fully deployed and operated under peak stress conditions. In addition, our products are combined with products from other vendors. As a result, should problems occur, it might be difficult to identify the source of the problem. These conditions increase the risk that we could experience, among other things: loss of customers; damage to our brand reputation; failure to attract new customers or achieve market acceptance; diversion of development and engineering resources; and legal actions by our customers. The occurrence of any one or more of the foregoing factors could cause us to experience losses, incur liabilities, and cause our net sales to decline.

Our investments in marketable securities may lose their value if economic conditions were to deteriorate.

Our marketable securities represent approximately 3.6% of our total assets at June 30, 2009. To the extent credit markets tighten, interest rates increase, or other economic conditions influence the liquidity of our marketable securities, the value and liquidity of our marketable securities may be adversely affected. In addition, we may have to record an impairment charge for marketable securities if we determine that an other-than-temporary decline in the fair value of a marketable security has taken place. For fiscal 2009, we have recorded an impairment charge for a marketable security of $0.3 million.

Item 1B. Unresolved Staff Comments

We have received no written comments regarding our periodic or current reports from the staff of the SEC that were issued 180 days or more preceding the end of our fiscal year 2009 that remain unresolved.

14

We own our principal manufacturing facility and corporate headquarters, which is located on Laurel Brook Road in Middlefield, Connecticut. This facility consists of one 153,500-square-foot building on approximately 13 acres. The following table sets forth information with respect to our facilities which are used by both of our operating segments, except as identified otherwise below:

|

|

|

|

|

|

|

|

| Square Footage |

| Owned / Leased | ||

|

|

| ||||

Operation/Location |

| Manufacturing |

| Total |

| |

|

|

| ||||

Corporate Headquarters, Eastern Regional Sales Office, and Metrology and Optics Manufacturing |

|

|

|

|

|

|

Middlefield, Connecticut |

| 89,000 |

| 153,500 |

| Owned |

|

|

|

|

|

|

|

Zygo - Optical Systems |

|

|

|

|

|

|

Tucson, Arizona |

| 14,560 |

| 22,560 |

| Leased - 08/31/11 |

|

|

|

|

|

|

|

Flat Panel Display Metrology Engineering & Support |

|

|

|

|

|

|

Boca Raton, Florida |

| 1,500 |

| 3,000 |

| Leased - 06/30/10 |

|

|

|

|

|

|

|

Zygo - Optical Systems |

|

|

|

|

|

|

Costa Mesa, California |

| 0 |

| 13,714 |

| Leased - 10/18/10 |

|

|

|

|

|

|

|

Western Regional Sales Office and R&D Center |

|

|

|

|

|

|

Freemont, California |

| 0 |

| 5,975 |

| Leased - 02/1/11 |

|

|

|

|

|

|

|

Semiconductor Process Metrology Office |

|

|

|

|

|

|

Hillsboro, Oregon |

| 0 |

| 6,410 |

| Leased - 12/31/12 |

|

|

|

|

|

|

|

Zygo - Laser Technology Metrology (R& D) |

|

|

|

|

|

|

Watsonville, California |

| 0 |

| 1,452 |

| Leased - 04/14/11 |

|

|

|

|

|

|

|

Office |

|

|

|

|

|

|

Franklin, Massachusetts |

| 0 |

| 400 |

| Leased - 06/30/10 |

|

|

|

|

|

|

|

Zygo PTE Ltd |

|

|

|

|

|

|

Singapore |

| 0 |

| 803 |

| Leased - 01/14/10 |

|

|

|

|

|

|

|

Zygo Taiwan |

|

|

|

|

|

|

Sales Office |

| 0 |

| 3,961 |

| Leased - 09/30/09 |

Service Office |

| 0 |

| 2,772 |

| Leased - 09/30/09 |

|

|

|

|

|

|

|

ZygoLOT |

|

|

|

|

|

|

Germany |

| 0 |

| 3,702 |

| Leased - 10/01/09 |

|

|

|

|

|

|

|

Zygo KK |

|

|

|

|

|

|

Japan |

| 0 |

| 1,705 |

| Leased - 07/31/11 |

|

|

|

|

|

|

|

Zygo Lamda |

|

|

|

|

|

|

China |

| 3,552 |

| 12,206 |

| Leased - 09/16/12 |

|

|

|

|

|

|

|

Zygo Canada, Inc. |

|

|

|

|

|

|

Canada |

| 2,447 |

| 6,851 |

| Leased - 07/31/13 |

|

|

|

|

|

|

|

Machine Vision International, PTE |

|

|

|

|

|

|

Singapore |

| 2,500 |

| 10,828 |

| Leased - 04/22/10 |

|

|

|

|

|

|

|

Total |

| 113,559 |

| 249,839 |

|

|

|

|

|

|

| ||

15

From time to time, we are subject to certain legal proceedings and claims that arise in the normal course of our business. In the opinion of management, we are not party to any litigation that we believe could have a material adverse effect on our financial condition, results of operation or liquidity.

Item 4. Submission of Matters to a Vote of Security Holders

The 2008 Annual Meeting of Stockholders was held on June 16, 2009. The following matters were submitted to a vote of the Company’s stockholders:

|

|

|

|

|

|

|

|

|

|

|

Proposal No. 1 – Election of Board of Directors | ||||||||||

| ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

| For |

|

|

|

| Withheld |

| ||

|

|

|

|

|

|

| ||||

Eugene G. Banucci |

|

| 11,152,469 |

|

|

|

|

| 2,630,708 |

|

Stephen D. Fantone |

|

| 12,881,256 |

|

|

|

|

| 901,921 |

|

Samuel H. Fuller |

|

| 13,220,115 |

|

|

|

|

| 563,062 |

|

Seymour E. Liebman |

|

| 13,103,169 |

|

|

|

|

| 680,008 |

|

J. Bruce Robinson |

|

| 11,158,641 |

|

|

|

|

| 2,624,536 |

|

Robert B. Taylor |

|

| 13,116,712 |

|

|

|

|

| 666,465 |

|

Carol P. Wallace |

|

| 13,400,929 |

|

|

|

|

| 382,248 |

|

Gary K. Willis |

|

| 13,167,191 |

|

|

|

|

| 615,986 |

|

Bruce W. Worster |

|

| 11,126,834 |

|

|

|

|

| 2,656,343 |

|

|

|

|

|

|

|

|

|

|

|

|

Proposal No. 2 – Ratification of appointment of Deloitte & Touche LLP as our independent registered public accounting firm for fiscal 2009 were as follows: | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

| For |

| Against |

| Abstain |

| |||

|

|

|

|

| ||||||

|

|

| 13,495,791 |

|

| 81,325 |

|

| 206,060 |

|

There were no other matters submitted to a vote of our stockholders.

16

Item 5. Market for the Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities

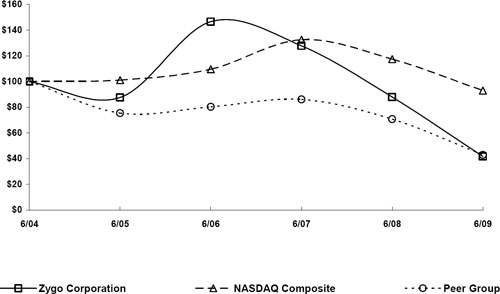

Our shares of common stock are traded over-the-counter and are quoted on the NASDAQ/National Market under the symbol “ZIGO.” The following table provides information about the high and low sales prices of the Company’s common stock by quarter for fiscal 2009 and 2008.

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Fiscal Year Ended June 30, 2009 |

| Fiscal Year Ended June 30, 2008 |

| ||||||||

|

|

|

| ||||||||||

|

| High |

| Low |

| High |

| Low |

| ||||

|

|

|

|

|

| ||||||||

First quarter |

| $ | 13.79 |

| $ | 8.80 |

| $ | 14.55 |

| $ | 11.33 |

|

Second quarter |

| $ | 12.47 |

| $ | 4.66 |

| $ | 13.50 |

| $ | 10.79 |

|

Third quarter |

| $ | 7.93 |

| $ | 3.06 |

| $ | 12.94 |

| $ | 10.72 |

|

Fourth quarter |

| $ | 6.42 |

| $ | 4.11 |

| $ | 13.50 |

| $ | 9.76 |

|