EEI Financial Conference

November 6, 2007

forward-looking statement…

During the course of this presentation, there will be forward-

looking statements within the meaning of the “safe harbor”

provisions of the Private Securities Litigation Reform Act of

1995. Forward-looking statements often address our expected

future business and financial performance, and often contain

words such as “expects,” “anticipates,” “intends,” “plans,”

“believes,” “seeks,” or “will.”

These statements are based upon our current expectations and

speak only as of the date hereof. Our actual future business and

financial performance may differ materially and adversely from

those expressed in any forward-looking statements. Although our

expectations and beliefs are based on reasonable assumptions,

actual results may differ materially. The factors that may affect

our results are listed in certain of our press releases and disclosed

in the Company’s public filings with the SEC.

2

NorthWestern today…

Company moving forward as a stand alone

company

Regulated electric and natural gas business

Strong financial profile

Poised for growth

3

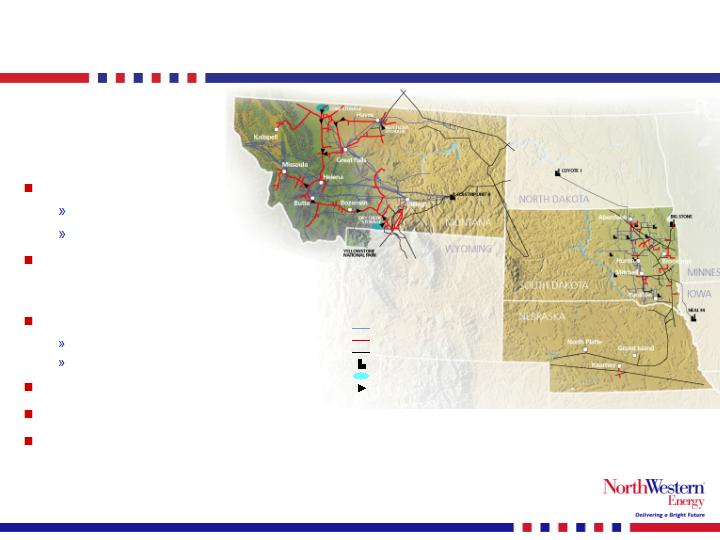

who we are…

Electric transmission lines

Natural gas distribution lines

Supplier-owned electric or natural gas lines

Electric generating plant

Natural gas storage fields

Natural gas compressor stations

(1) As of 9/30/07.

(2)

Book capitalization calculated as short-term debt plus long-

term debt plus shareholders’ equity.

640,000 customers

382,000 electric

258,000 natural gas

Approximately 123,000 square miles

of service territory in Montana,

Nebraska and South Dakota

Total Generation (all base load coal)

MT – 222 MW – unregulated

SD – 310 MW – regulated

Total Assets: (1) $2,386 MM

Total Capitalization: (1)(2) $1,445 MM

Total Employees: (1) 1,350

4

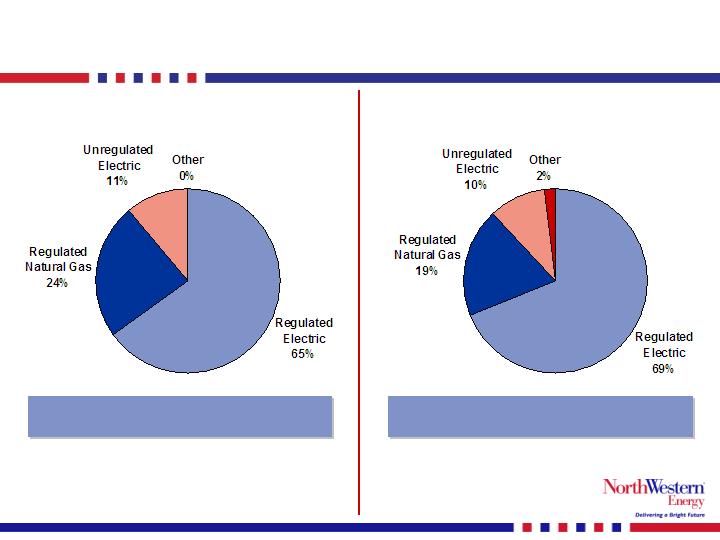

contribution of segments…

$662

$359

83

77

$119

*EBITDA = Op. Inc. + Depr

(trailing twelve months)

Gross Margin Contribution

EBITDA* Contribution

Approximately 90% of gross margin is

provided by the regulated businesses.

Approximately 90% of EBITDA is provided

by the regulated businesses.

5

poised for significant growth…

Strong balance sheet

Experienced management team to execute plan

Average 25 years of utility experience

Earnings and cash flow growth from existing businesses

Existing regulated and unregulated businesses provide

stable predictable earnings

Continued customer and load growth

Capital investments continue to increase

Only small rate increases to customers

(5%-7% of total bill or $4-$7/month-varies by jurisdiction)

Approximately $1 billion of growth capex opportunities

over the next 6 years

All state and FERC regulated projects

$1.2 billion rate base as of December 31, 2006

(88% growth potential)

6

growth opportunities…

Existing Business

Service territory

Customer growth –

1.6% annually

Load growth in electric segment –

3.2% annually

Capital investments have

increased an average of

$4.2 million per year since 2004

Natural gas pipelines – serve the

growing ethanol industry

Potential for capital deployment

of approximately $40 million in

the next 3 years

Equity investment protected by

letters of credit

Growth Opportunities

Transmission development

Upgrade Colstrip 500kV

transmission line

Mountain States Transmission

Intertie line (MSTI)

Potential generation development

in Montana

Effect of House Bill 25 –

2007 Montana legislative session

7

earnings/cashflow drivers – rate cases…

Montana

Requested revenue increase of approximately $41.9 million

annually

Last case was in 2000 (test year 1999)

Represents only a 6.6% increase of total bill to electric

consumers

a 3.9% increase in total bill to gas customers ($4-$5/month in

each case)

Target date of commission decision = late April 2008

FERC

Requested revenue increase of approximately $8.6 million

annually

Currently collecting the rate increase

Target date of commission decision = Spring 2008

South Dakota

Requested revenue increase of approximately $3.7 million annually

Last natural gas rate case was in 1998 (test year 1997)

Represents only a 5.7% increase in in total bill (about $7/month)

Target date of commission decision = late 2007

Nebraska

Requested revenue increase of approximately $2.8mm annually

Last natural gas rate case was in 2000 (test year 1999)

Represents only a 5.5% increase of total bill (about $6.50/month)

Target settlement date of with cities = late 2007

Rev Request = $57M

(Tax effected) X 60%

Net income on rate increases

up to $33.2M

***DISCLAIMER*** – not intended to be a prediction of the outcome.

Intended to be an estimation of value up to the requested increases.

(A)

(B)

(C)

(D)

(A*B*D)

(A*B*C)

in millions

in millions

Rate Base

Requested

Requested

Earned

'06 Earned

Requested

in millions

Cap structure

ROE

ROE

Income

Income

MT Electric

667.4

$

51.46%

12.00%

6.72%

23.1

$

41.2

$

MT Natural Gas

264.5

$

51.46%

11.75%

7.66%

10.4

$

16.0

$

SD Natural Gas

53.2

$

51.46%

11.25%

-1.58%

(0.4)

$

3.1

$

NE Natural Gas

25.6

$

51.46%

11.25%

2.70%

0.4

$

1.5

$

FERC

244.6

$

51.46%

12.00%

8.16%

10.3

$

15.1

$

43.7

$

76.9

$

8

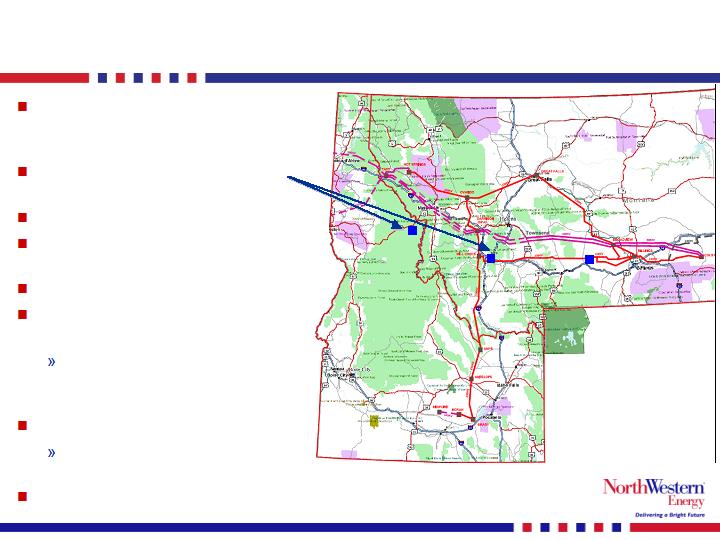

Colstrip 500 kV upgrade…

“Traditional” pathway to

West Coast and California

markets

New substations near

Townsend and Missoula, MT

Upgrade to existing stations

No new line construction

necessary

Capacity increase: 500-700 MW

Working with other Colstrip

transmission owners

NWEC’s ownership share of

upgrade project is assumed

to be 50%

Capital cost: $250 Million

NWEC’s share dependant on

other owners participation

Assumed ROE: 10%-11%

9

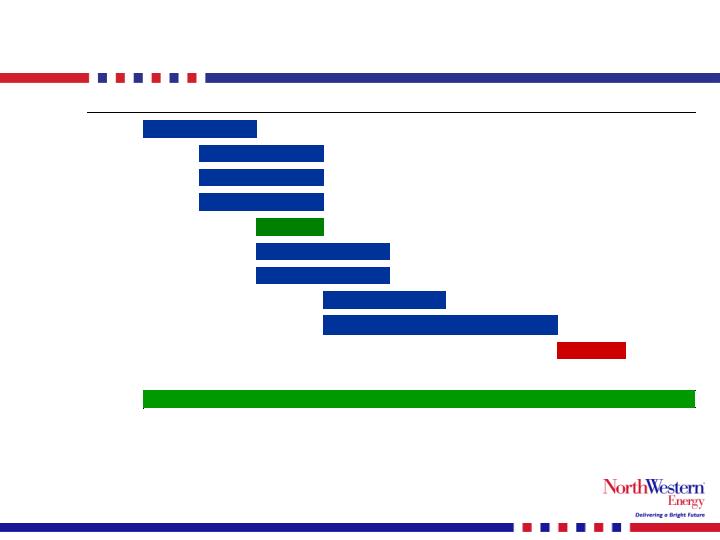

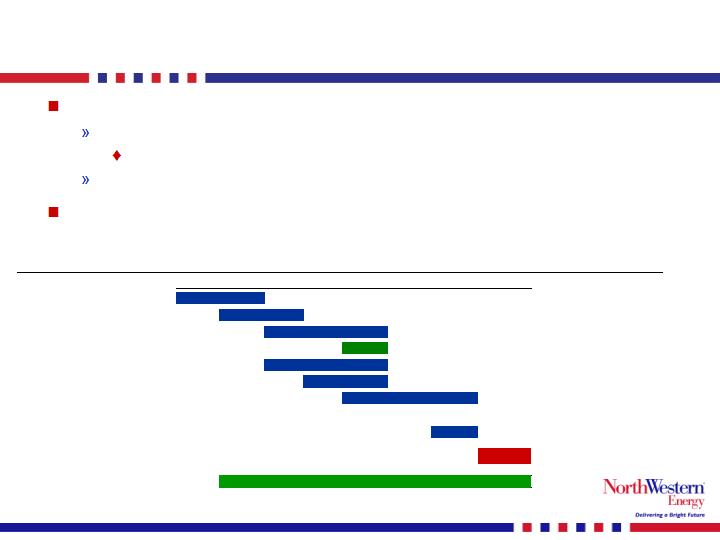

next steps on Colstrip 500 kV upgrade…

Assumes 50% ownership in the project.

The costs represent NorthWestern’s pro rata portion of the capital invested.

Go/No Go

Operation

Cumulative Dollars Spent:

$1-2M

$20-30M

$100-125M

2011

2007

2008

2009

2010

Substation design

WECC planning

Land acquisition

Construction

Engineering studies

Rates with BPA

Tx agreements

WECC approval

10

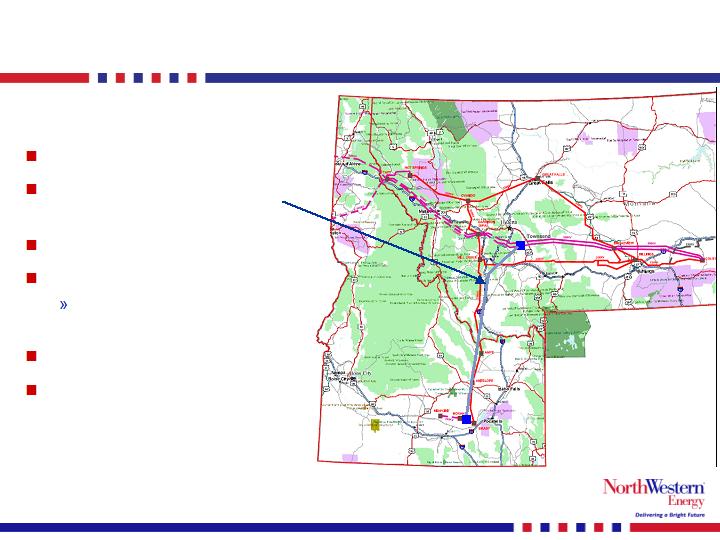

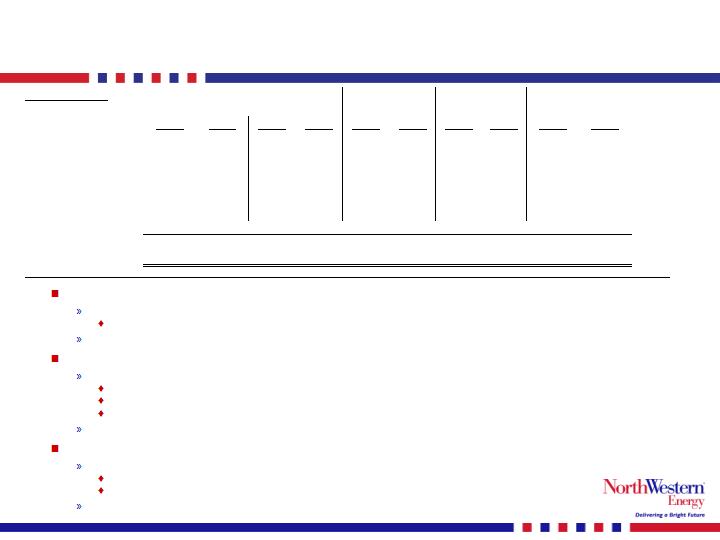

Mountain States Transmission Intertie Line…

500 kV AC Line

Southwestern Montana

to Southeastern Idaho

Length: approx. 400 miles

Capacity: 1,500 MW

Deposits from subscribers

of approx. 1,050 MW

Capital Cost: $800 million

Assumed ROE 10%-13%

11

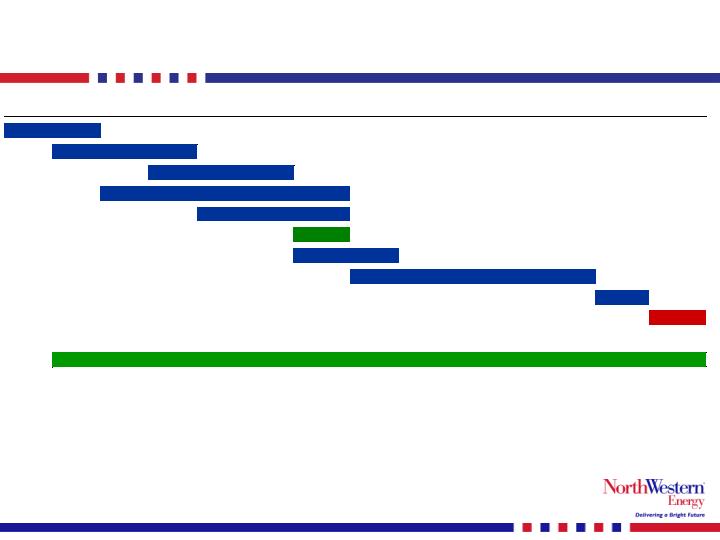

MSTI timeline…

Go/No Go

Test

Operation

Cumulative Dollars Spent:

$3-5M

$200M

$500M

$800M

2011

2012

2013

Open Season

2007

2008

2009

2010

Rights of Way

Construction

Support of Agencies

Major facility Siting

Contracts

EIS

12

potential for generation development…

2007 Montana Legislature passed House Bill 25:

Allows ownership of rate base generation

Prior legislation didn’t allow generation in rate base

Provides for project approval by PSC prior to construction

NorthWestern is considering a 100-150 MW gas fired

generation facility for wind firming and high demand periods

Go/No Go

Testing

Operation

Cumulative Dollars Spent:

$1-2M

$12-$15M

$100-$125M

Economic analysis

2007

2008

2009

2010

Construction

Reserve equip.

Feasibility study

MPSC review process

Major engineering design

13

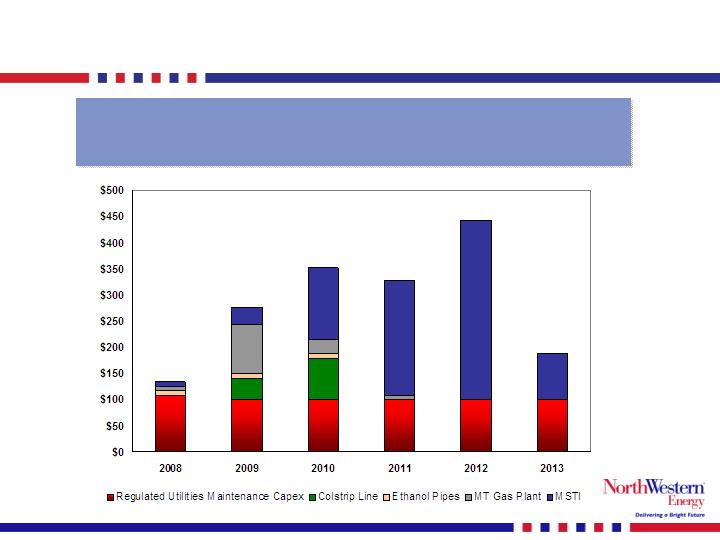

cap ex spending – next few years…

Includes more than $1 billion of potential generation

and transmission growth projects

(includes Colstrip 500KV upgrade at 50% ownership of new project)

Approximately $1.6 billion in

capital expenditures to 2013

14

value of growth potential…

Possible earnings capacity of future opportunities

Significant financial opportunity long term

(in millions)

Annual Earnings

Opportunity

On-line

MSTI transmission line

$800 million times 50% equity ratio times estimated ROE of 11%

$44.0

Jan 2013

Colstrip 500 kV transmission upgrade

$120 million times 50% equity ratio times estimated ROE of 10%

$6.0

Jan 2011

Montana Nat Gas generator

$110 million times 50% equity ratio times estimated ROE of 10%

$5.5

July 2010

Ethanol pipelines - SD/NE

$20 million times 50% equity ratio times estimated ROE of 10%

$1.0

Thru 2009

***Disclaimer*** – not intended to be guidance or a prediction of share price.

Intended to be an estimation of intrinsic value drivers of possible outcomes.

15

other value drivers…

(in millions)

NPV of

contribution

per share

GE Lease:

2011-2018 decrease of lease $11.5M/yr

$50.9

$1.30

Accretion of owner participant purchase

$15.1

$0.39

DB contract expires 12/31/2010

$15.8

$0.40

Puget contract expires 12/31/2010

$9.0

$0.23

Potential Value of NOL

NPV of NOL (net of FIN 48 reserve)

$67.5

$1.73

Other value drivers

$158.3

$4.05

All discounted at 8.46%

***Disclaimer*** – not intended to be guidance or a prediction of share price.

Intended to be an estimation of intrinsic value drivers of possible outcomes.

16

investment highlights…

Attractive Transmission and Distribution Business

Strong, Predictable Growth in Earnings

Significant Investment Potential in

Transmission and New Generation

Experienced Team Committed to

Shareholder Value

17

exhibits…

Select Financial Data

18

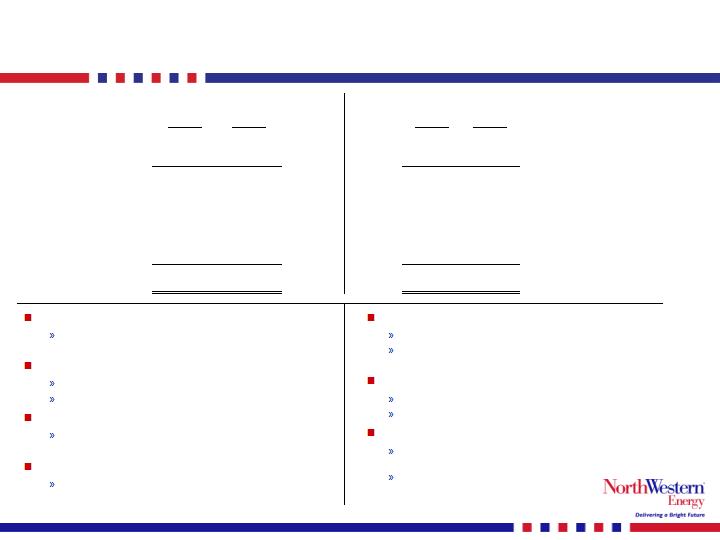

y-t-d 9/30/07 financial results…

Gross margin:

Driven by customer growth and warmer summer

weather

OA&G:

Lower BBI transaction costs and lease expense

2006 insurance recovery of $9.3 million

Interest expense:

Increase due to CU4 buyout and Ammundson

verdict

Taxes:

Portions of BBI expenses were not deductible

until process terminated

Gross margin:

Driven by cust. growth and favorable weather

Higher cost of sales in 2006 on $4.1 million

stipulation with MCC

OA&G:

Lower BBI transaction costs and lease expense

Offset by 2006 insurance recovery of $9.3 million

Other:

Prior year included gain on interest rate

swap of $3.8 million

Prior year included sale of oil/gas

partnership of $2.3 million

19

3Q '07

3Q '06

3Q '07

3Q '06

Gross Margin

126.8

$

123.7

$

392.5

$

380.0

$

Operating, general & admin

(93.6)

(90.2)

(296.7)

(296.0)

Operating income

33.2

33.5

95.8

84.0

Interest expense

(14.6)

(13.8)

(42.4)

(42.8)

Other income/(expense)

0.9

(0.4)

1.6

8.0

Income taxes

(6.3)

(7.9)

(20.3)

(19.7)

Disco Ops

0.4

Net Income

13.2

$

11.4

$

34.8

$

30.0

$

y-t-d

3Q '07

y-t-d 9/30/07 operating income by segment…

Regulated electric:

Improvement was due primarily to increased margins

driven by customer growth and warmer summer weather

Partially offset by higher property taxes and depreciation expense

Regulated gas:

Improvement driven by gross margin increase

primarily due to customer growth

increased transportation and storage revenue and

transferring assets from unreg gas

Partially offset by higher property taxes and depreciation expense

Unregulated electric:

Gross margin decrease

primarily due to lower contracted prices and increased coal costs

offset by increased volumes

Partially offset by lower operating costs due to lease buyout

20

Nine Month Results:

3Q '07

3Q '06

3Q '07

3Q '06

3Q '07

3Q '06

3Q '07

3Q '06

3Q '07

3Q '06

Gross Margin

260,563

$

244,923

$

88,886

$

82,132

$

42,008

$

49,138

$

1,024

$

3,800

$

392,481

$

379,993

$

Operating, general & admin

96,770

96,300

47,490

45,373

23,695

31,286

5,656

9,425

173,611

182,384

Property and other taxes

43,040

40,171

16,098

14,351

2,470

2,538

37

86

61,645

57,146

Depreciation

45,955

43,464

12,168

10,946

2,423

1,148

866

875

61,412

56,433

Operating income

74,798

$

64,988

$

13,130

$

11,462

$

13,420

$

14,166

$

(5,535)

$

(6,586)

$

95,813

$

84,030

$

Regulated

Unregulated

Total

Electric

Gas

Electric

Other

expected rest of 2007…

Company expects 4Q ’07 earnings to approximate 4Q ‘06

(excluding the impact of the Ammondson verdict on ’06 results)

21

Actual

2006 Quarterly Results:

Q1

Q2

Q3

Q4

2006

Net income

21,025

(2,446)

11,398

7,923

37,900

Ammondson verdict

11,400

11,400

Net income (

adjusted for Ammondson}

21,025

(2,446)

11,398

19,323

49,300

EPS

0.59

$

(0.07)

$

0.32

$

0.22

$

1.07

$

EPS

(adjusted for Ammondson)

0.59

$

(0.07)

$

0.32

$

0.54

$

Estimated

Estimated

2007 Quarterly Results:

Low end

High end

Low end

High end

Q1

Q2

Q3

Q4

Q4

2007

2007

Net income

19,142

2,434

13,177

18,897

21,047

53,650

55,800

EPS

0.54

$

0.07

$

0.36

$

0.51

$

0.58

$

1.45

$

1.55

$

Shares

35,720

35,998

36,471

37,000

36,000

37,000

36,000

ACTUAL RESULTS