Investor Update

April 8, 2008

forward-looking statement …

During the course of this presentation, there will be forward-

looking statements within the meaning of the “safe harbor”

provisions of the Private Securities Litigation Reform Act of

1995. Forward-looking statements often address our expected

future business and financial performance, and often contain

words such as “expects,” “anticipates,” “intends,” “plans,”

“believes,” “seeks,” or “will.”

The information in this presentation is based upon our current

expectations as of the date hereof. Our actual future business

and financial performance may differ materially and adversely

from those expressed in any forward-looking statements. We

undertake no obligation to revise or publicly update our forward-

looking statements or this presentation for any reason. Although

our expectations and beliefs are based on reasonable

assumptions, actual results may differ materially. The factors that

may affect our results are listed in certain of our press releases

and disclosed in the Company’s public filings with the SEC.

2

who we are …

Electric transmission lines

Natural gas distribution lines

Supplier-owned electric or natural gas lines

Electric generating plant

Natural gas storage fields

Natural gas compressor stations

(1) As of 12/31/07

(2)

Book capitalization calculated as total debt, excluding capital leases, plus shareholders’ equity.

650,000 customers

388,000 electric

262,000 natural gas

Approximately 123,000 square miles

of service territory in Montana,

Nebraska and South Dakota

Total Generation (mostly base load coal)

MT – 222 MW – unregulated

SD – 312 MW – regulated

Total Assets: (1) $2,547 MM

Total Capitalization: (1)(2) $1,629 MM

Total Employees: (1) 1,350

3

business overview …

Regulated Operations (89% of Gross Margins)

One of the largest providers of electricity and natural gas in the Upper Midwest and Northwest,

serving approximately 650,000 customers in Montana, South Dakota and Nebraska

Electric Operations (65%)

Montana

328,000 customers (transmission/distribution)

Approximately 7,000 miles of transmission

lines and 21,000 miles of distribution lines

South Dakota

60,100 customers (integrated utility)

Approximately 3,200 miles of T&D lines

Owns 312 net MW of power generation

Gas Operations (24%)

Montana

177,000 customers (residential/commercial)

3,900 miles of distribution pipelines

2,000 miles of intrastate transmission

pipelines

16.2 Bcf of gas storage

South Dakota/Nebraska

84,500 customers (residential/commercial)

2,200 miles of distribution pipelines

Unregulated Operations (11%)

Electric — 222 MW - Primarily consists of an equity participation in 30% of Colstrip Unit 4,

a 740 MW coal-fired power plant in Montana

Source: NorthWestern Corporation 10-K.

4

NorthWestern’s future …

Operationally strong

Cost competitive

Above-average reliability

Award-winning customer service

Financially strong

Stable earnings and cash flow profile

Approximately a 50/50 debt to total capitalization ratio

Secured credit ratings of A-(MT) BBB+(SD) / BBB / Baa3

Unsecured credit ratings of investment grade from 2 of 3 agencies

Utilize excess cash flow and debt capacity to invest in the

business

Organic growth in existing service territories

Gas transmission (natural gas pipes to ethanol plants)

Electric generation opportunities (MT Legislation HB 25)

Transmission opportunities (Colstrip 500 kV upgrade and MSTI)

5

2007 full year results …

Unaudited (Dollars in 000's)

2007

2006

Variance

Operating Revenues

1,200,060

1,132,653

67,407

Cost of Sales

668,405

613,582

54,823

Gross Margin

531,655

519,071

12,584

Operating Expenses

Operating, general & administrative

221,566

240,215

(18,649)

Property and other taxes

87,581

74,187

13,394

Depreciation

82,415

75,305

7,110

Ammondson verdict

-

19,000

(19,000)

Total Operating Expenses

391,562

408,707

(17,145)

Operating Income

140,093

110,364

29,729

Interest Expense

(56,942)

(56,016)

(926)

Investment Income and Other

2,428

9,065

(6,637)

Income (Loss) from Cont. Ops. Before Taxes

85,579

63,413

22,166

Benefit (Provision) for Income Taxes

(32,388)

(25,931)

(6,457)

Income (Loss) from Continuing Operations

53,191

37,482

15,709

Discontinued Ops., Net of Taxes

-

418

(418)

Net Income (Loss)

53,191

37,900

15,291

Year Ended December 31,

6

segment information …

7

Unaudited (Dollars in 000's)

YTD December 31, 2007

ELECTRIC

UTILITY

GAS UTILITY

UNREGULATED

ELECTRIC

OTHER /

ELIMINATIONS

TOTAL

% OF TOTAL

Gross Margin

Montana

273,185

103,973

56,152

(207)

433,103

81%

South Dakota / Nebraska

73,791

23,653

-

1,108

98,552

19%

Total

346,976

127,626

56,152

901

531,655

100%

% of Total

65%

24%

11%

0%

100%

Operating Income

Montana

59,973

21,953

20,407

341

102,674

69%

South Dakota / Nebraska

30,719

14,114

-

297

45,130

31%

Total before Corporate

90,692

36,067

20,407

638

147,804

100%

% of Total

61%

24%

14%

0%

100%

Unallocated Corporate Expense

(7,711)

(7,711)

Operating Income

90,692

36,067

20,407

(7,073)

140,093

strong balance sheet …

Debt Ratings

(Dollars in 000's)

December 31,

2007

2006

Cash

12,773

1,930

Restricted Cash

14,482

15,836

Accounts Receivable, Net

143,482

149,793

Inventories

63,586

60,543

Other Current Assets

44,031

40,372

Goodwill

355,128

435,076

PP&E and Other Non-current Assets

1,913,898

1,692,387

Total Assets

2,547,380

$

2,395,937

$

Payables

91,588

78,739

Other Current Liabilities

209,245

192,504

Short & Long Term Capital Leases

40,391

42,462

Short & Long Term Debt

805,977

704,655

Other Non-current Liabilities

577,155

634,806

Shareholders' Equity

823,024

742,771

Total Liabilities and Equity

2,547,380

$

2,395,937

$

Short & Long Term Debt / Total Capitalization

49.5%

48.7%

8

2008 guidance bridge from 2007 results …

2008 = 2007 plus rate increases in MT, SD, NE

Estimates by the three sell side firms covering NWEC average $1.74/fully diluted share for 2008.

2008 Guidance

Reported 2007 - EPS fully diluted

1.44

$

Mid-point

Guidance for 2008 - diluted

1.60

$

1.75

$

1.68

$

Yr over yr increase

0.24

$

per share

9

Bridge to 2008:

Pre-tax

After-tax

shares o/s

Rates - MT (net of 21 MW and non-earning rate base)

0.18

$

12.1

$

7.3

$

39.5

Rates - SD

0.05

$

3.1

$

1.9

$

39.5

Rates - NE

0.02

$

1.5

$

0.9

$

39.5

Anticipated yr over yr changes

0.25

$

per share

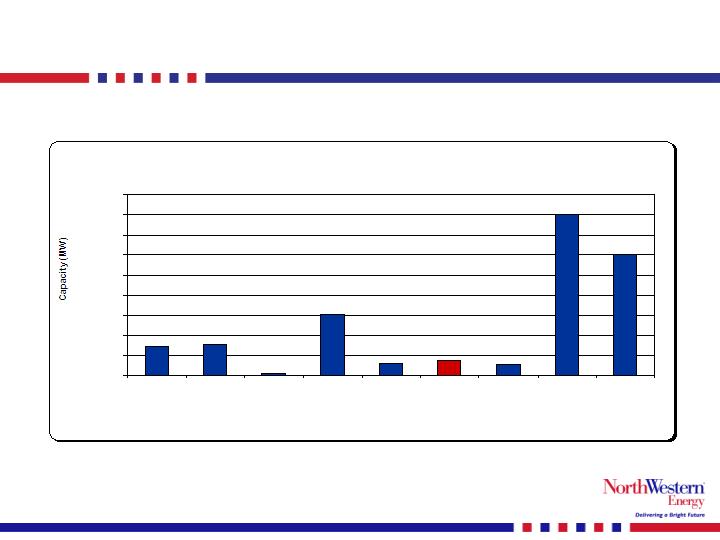

Montana proposed generation landscape …

Potential Generation Development in Montana

722

770

52

1,526

300

375

268

4,012

3,000

-

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

Coal

Gas

Hydro

Wind

MATL

In-Service

Signed

LGIA

Total

MT

Existing

Generation

10

growth project developments …

Mill Creek Generation Plant

Site selected at Mill Creek, near Anaconda, MT

Design phase

Filing expected by end of 2Q ‘08

Construction to begin upon approval

Estimated to be on-line at beginning of 2011

Approximately 120 MW of regulating capacity

Approximately $150 million project

Expandable project

Colstrip 500 KV Upgrade

NorthWestern currently assumes it will be only partner

New proposed generation mix is strong but changing

May effect the timing and the configuration of the project

Cost estimate = $200M - $250M

Estimated to be on-line beginning of 2013

11

growth project developments cont’d …

MSTI

Permitting for 500 KV line

Will scale this project to committed long term contracts

230KV, 270 mile line to move 430 MWs; cost = $250M - $300M

345KV, 370 mile line to move 800 MWs; cost = $650M - $700M

500KV, 400 mile line to move 1,500 MWs; cost = $750M - $900M

Reservations currently at 639 MW’s

Considering a strategic partner for development expertise and

equity capital

12

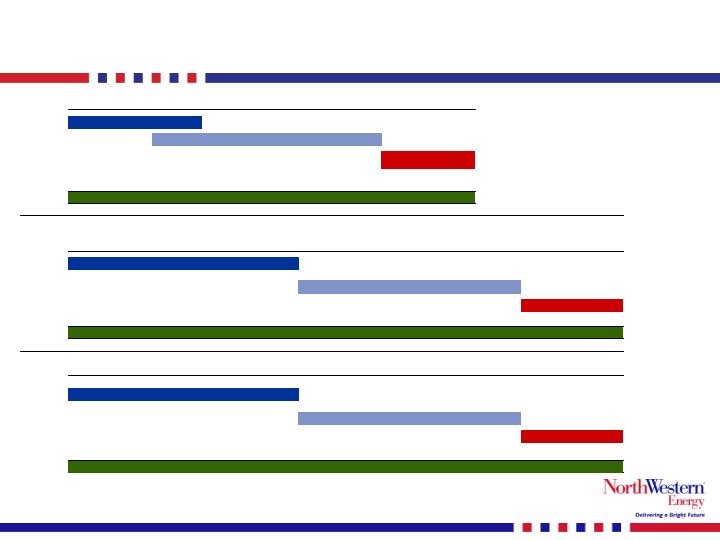

growth project timing …

Mill Creek Generation Plant

Cumulative Dollars Spent:

$4M-$5M

$100M

$150 M

Colstrip 500 KV upgrade

Cumulative Dollars Spent:

$1M-$2M

$100M

$200M-$250M

MSTI

Cumulative Dollars Spent:

$10M-$12M

$40M-$50M

$200M

$400M

$750M - $900M

Planning & Technical Studies

Construction

Planning & Technical Studies

Operation

2012

2013

Operation

Construction

Operation

2011

2011

2011

Construction

2008

2009

2010

2012

2013

2008

2009

2010

Planning

2008

2009

2010

13

growth project potential …

Timing

MSTI transmission line

500 KV scenario

37.5

$

to

45.0

$

750.0

$

to

900.0

$

Jan 2013

345 KV scenario

32.5

$

to

35.0

$

650.0

$

to

700.0

$

Jan 2013

230 KV scenario

12.5

$

to

15.0

$

250.0

$

to

300.0

$

Jan 2013

Colstrip 500 kV transmission upgrade

10.0

$

to

12.5

$

200.0

$

to

250.0

$

Jan 2013

Mill Creek Generator

Located by Anaconda, MT

6.3

$

to

7.5

$

125.0

$

to

150.0

$

Jan 2011

* For illustrative purposes = Cost of project times 50% equity ratio times estimated ROE of 10%

Cost of Project

Annual Earnings

Opportunity *

(in millions)

14

CU4 strategic alternatives update …

Credit Suisse engaged in January to help NorthWestern

evaluate strategic alternatives

Possible sale of NorthWestern’s 30% interest in CU4

Confidential Information Memorandum in market

Bids anticipated in early April 2008

Other considerations

Evaluate possible transfer to rate base

Analyze a long-term index sale to NorthWestern’s regulated

customers

Compare economics of current operations to the

alternatives considered

Timing

Decide which alternative to pursue in 2Q ’08

Execute on alternative pursued in 3Q ‘08

15

why Northwestern?

Value

Dividend yield of 5.15%

Cash taxes lower than book taxes prior to 2011

Currently trading at approximately 15x projected ’08

earnings

Strong balance sheet/credit ratings

Opportunity for Growth

Possibility of rate base growth in excess of $1 billion

Potential additional annual earnings of approximately

$50 million

16

summary …

Attractive

Transmission &

Distribution Business

Regulated electric and gas contribute 90% of gross

margins

Cost-based operating structure approved by regulatory

commissions

Increasing cash flows support growth opportunities

Stable and Predictable

Cash Flow

Strong Balance Sheet

Current Value with

Potential for Growth

Conservative capital structure provides increased

flexibility

Improving credit ratings

Dividend yield of 5.15%

Trading at low multiple of ’08 earnings

Identified projects providing opportunity for rate

base/earnings growth

Regional T&D utility with stable customer growth

Attractive mix of electric and natural gas customers

Reliable and cost competitive operations

17