46th EEI Financial Conference

November 8, 2011

Presented by:

Bob Rowe, President & CEO

Brian Bird, Vice President, CFO & Treasurer

Outline

Who we are

Financial update

Investment opportunity

outlook

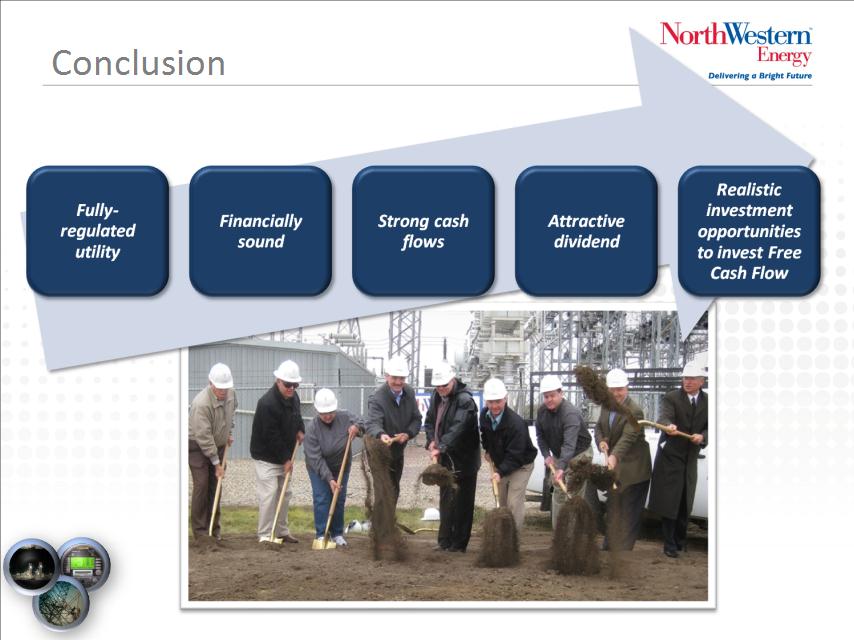

Conclusion

Appendix

- Financial statements

- Regulatory update

- Additional investment opportunity detail

Financial update

Investment opportunity

outlook

Conclusion

Appendix

- Financial statements

- Regulatory update

- Additional investment opportunity detail

2

Forward looking statements

During the course of this presentation, there will be forward-looking

statements within the meaning of the “safe harbor” provisions of the

Private Securities Litigation Reform Act of 1995. Forward-looking

statements often address our expected future business and financial

performance, and often contain words such as “expects,” “anticipates,”

“intends,” “plans,” “believes,” “seeks,” or “will.”

statements within the meaning of the “safe harbor” provisions of the

Private Securities Litigation Reform Act of 1995. Forward-looking

statements often address our expected future business and financial

performance, and often contain words such as “expects,” “anticipates,”

“intends,” “plans,” “believes,” “seeks,” or “will.”

The information in this presentation is based upon our current

expectations as of the date hereof unless otherwise noted. Our actual

future business and financial performance may differ materially and

adversely from our expectations expressed in any forward-looking

statements. We undertake no obligation to revise or publicly update our

forward-looking statements or this presentation for any reason.

Although our expectations and beliefs are based on reasonable

assumptions, actual results may differ materially. The factors that may

affect our results are listed in certain of our press releases and disclosed

in the Company’s public filings with the SEC.

expectations as of the date hereof unless otherwise noted. Our actual

future business and financial performance may differ materially and

adversely from our expectations expressed in any forward-looking

statements. We undertake no obligation to revise or publicly update our

forward-looking statements or this presentation for any reason.

Although our expectations and beliefs are based on reasonable

assumptions, actual results may differ materially. The factors that may

affect our results are listed in certain of our press releases and disclosed

in the Company’s public filings with the SEC.

3

Who we are

ð Our Vision: Enriching lives through a safe, sustainable

energy future

energy future

ð Our Mission: Working together to deliver safe, reliable

and innovative energy solutions

and innovative energy solutions

ð Our Values:

Safety

Excellence

Respect

Value

Integrity

Community

Environment

4

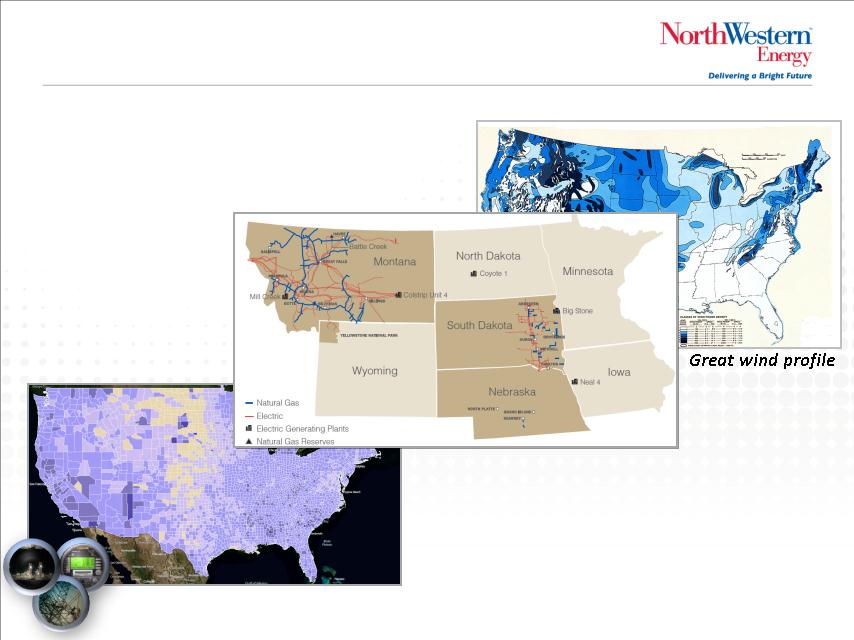

Geographically positioned for success

ð Our service territory covers some of

the best wind regimes in the nation

the best wind regimes in the nation

ð We have the opportunity to provide

transmission services into two different

markets (West and Midwest)

transmission services into two different

markets (West and Midwest)

Low unemployment rates

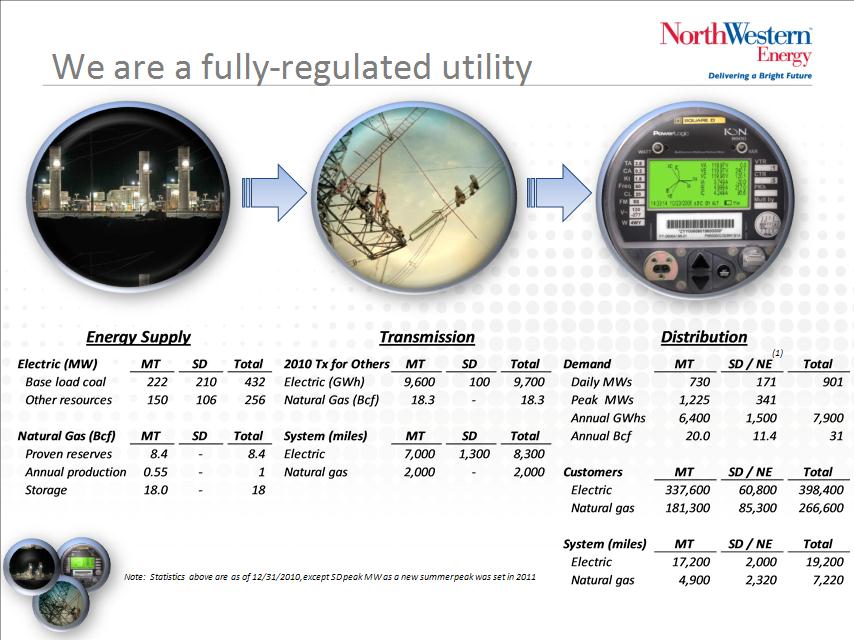

ð A fully-regulated utility located in states

with relatively stable economies with

opportunity for system investment and

grid expansion

with relatively stable economies with

opportunity for system investment and

grid expansion

5

6

(1) Nebraska is a natural gas only jurisdiction

A multi-state electric & natural gas utility

7

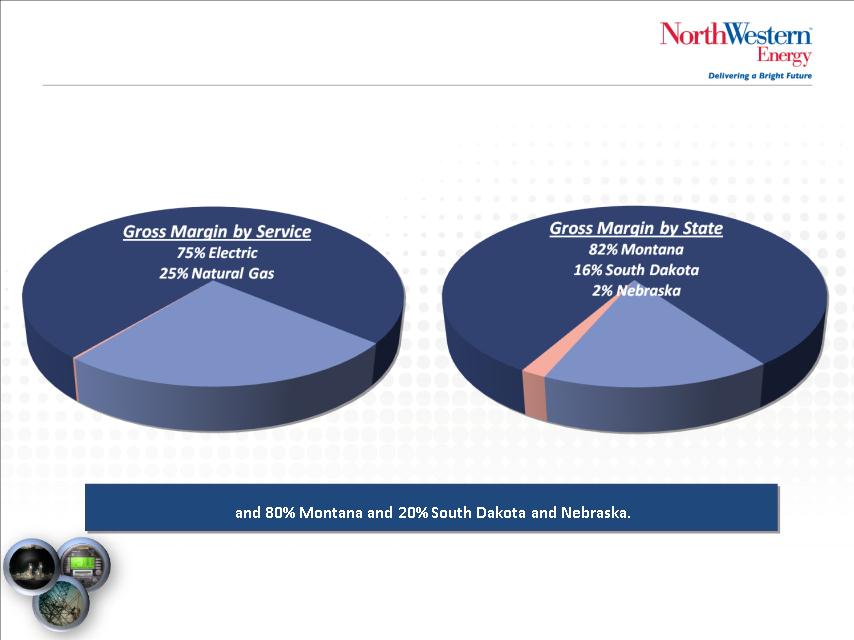

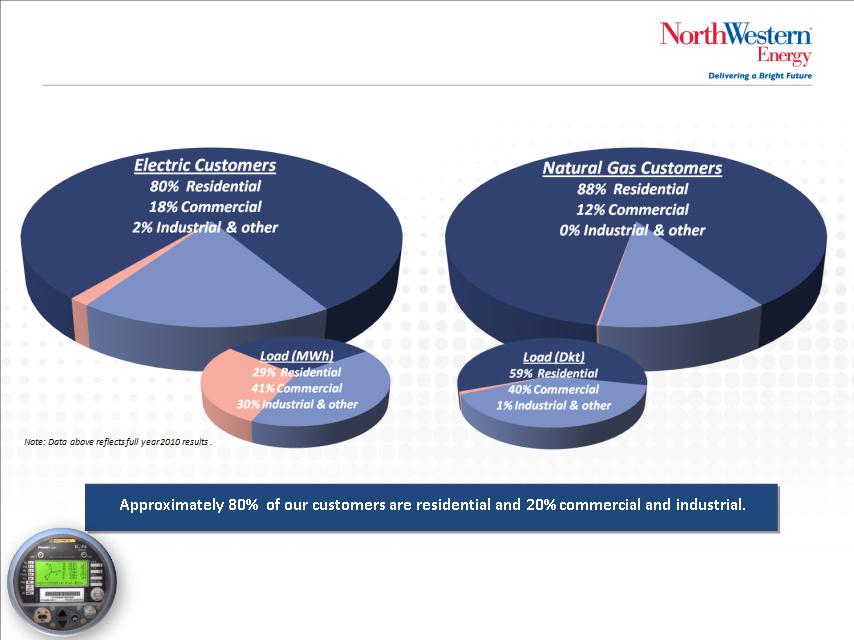

The “80 / 20” rules of NorthWestern. We are approximately 80% electric / 20% natural gas

Note: Data above reflects full year 2010 results .

A diverse distribution customer base

8

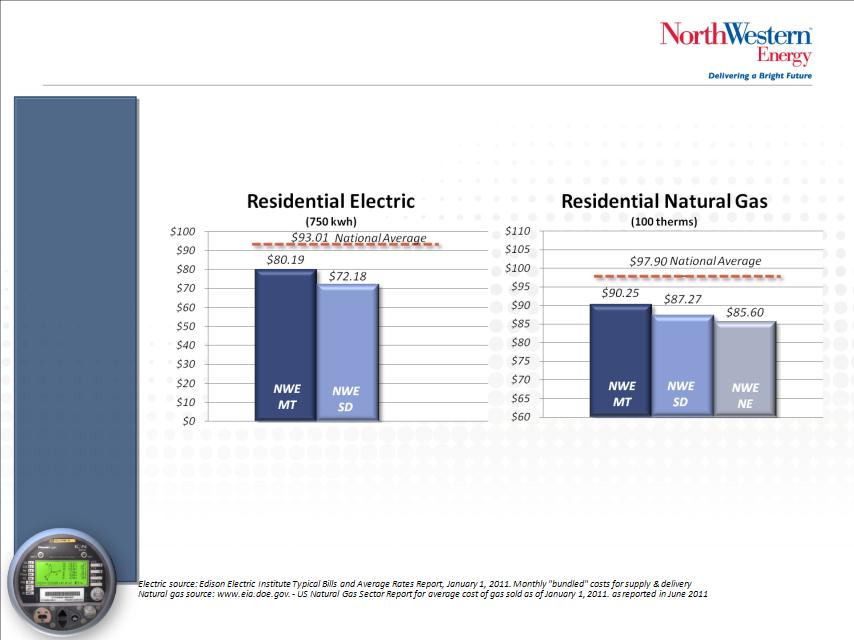

With competitive customer rates

9

Typical

Customer

bills

Customer

bills

Outline

Who we are

Financial update

Investment opportunity

outlook

Conclusion

Appendix

- Financial statements

- Regulatory update

- Additional investment opportunity detail

Financial update

Investment opportunity

outlook

Conclusion

Appendix

- Financial statements

- Regulatory update

- Additional investment opportunity detail

10

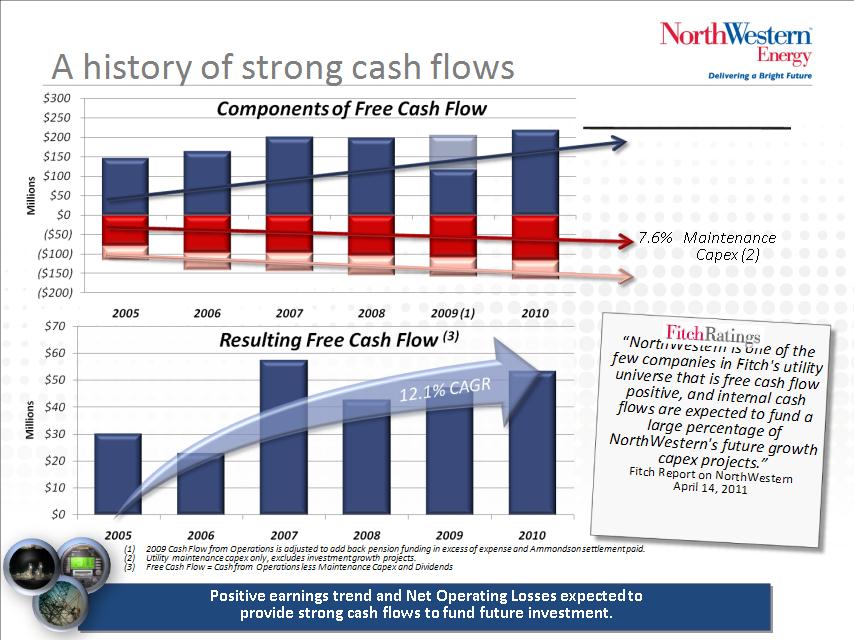

8.3% Cash From

Operations

Operations

6.6% Dividend Growth

Compounded Annual

Growth Rate (CAGR)

Growth Rate (CAGR)

11

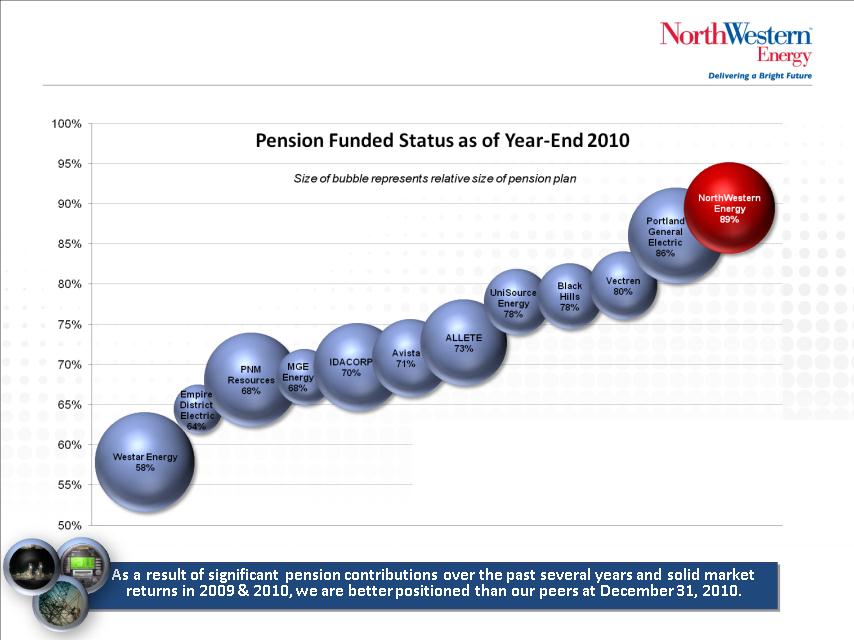

Solid pension funding

12

NorthWestern Energy’s Pension Assumptions

ð Target allocation 50% equity and 50% fixed

income

income

ð Expected long-term rate of return of 7.25%

ð Discount rate of 5.00 - 5.25%

ð Long-term targeted total debt to capitalization

of 50-55% with a current capitalization of

54.9%(1)

ð Total liquidity of $210 million as of Oct 21, ’11

ð Refinanced nearly all debt in the last 2 years

– Lowered average coupon on long-term

debt by 1.2% and extended maturities

debt by 1.2% and extended maturities

– Amended and restated revolving credit

facility extending term, increasing size

and lowering costs.

facility extending term, increasing size

and lowering costs.

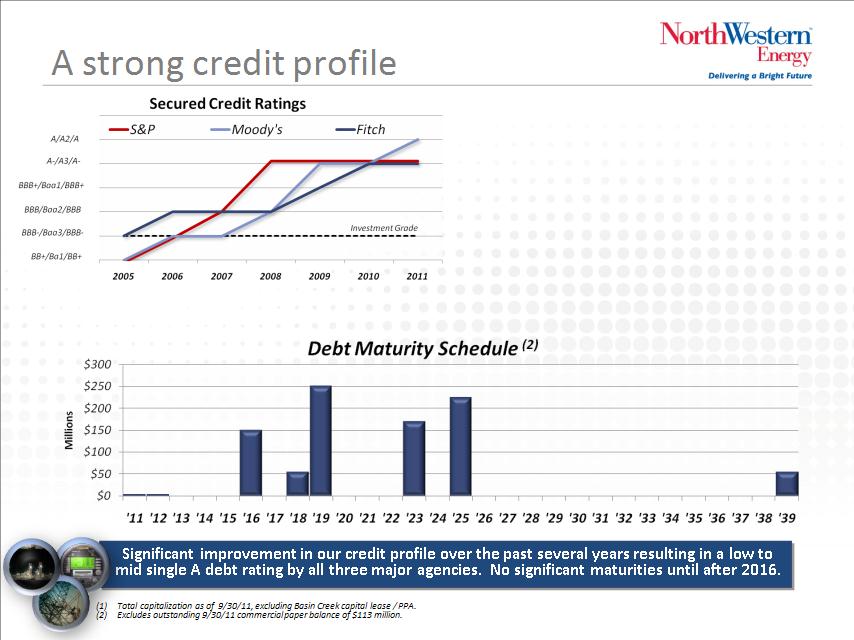

A security rating is not a recommendation to buy, sell or hold securities. Such rating may be subject to revision or

withdrawal at any time by the credit rating agency and each rating should be evaluated independently of any other rating.

withdrawal at any time by the credit rating agency and each rating should be evaluated independently of any other rating.

13

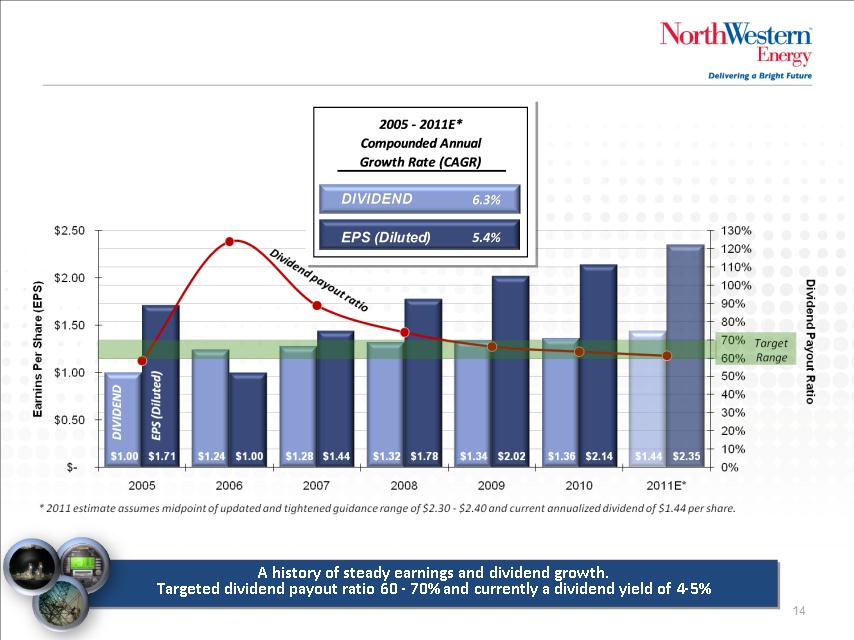

A history of earnings and dividend growth

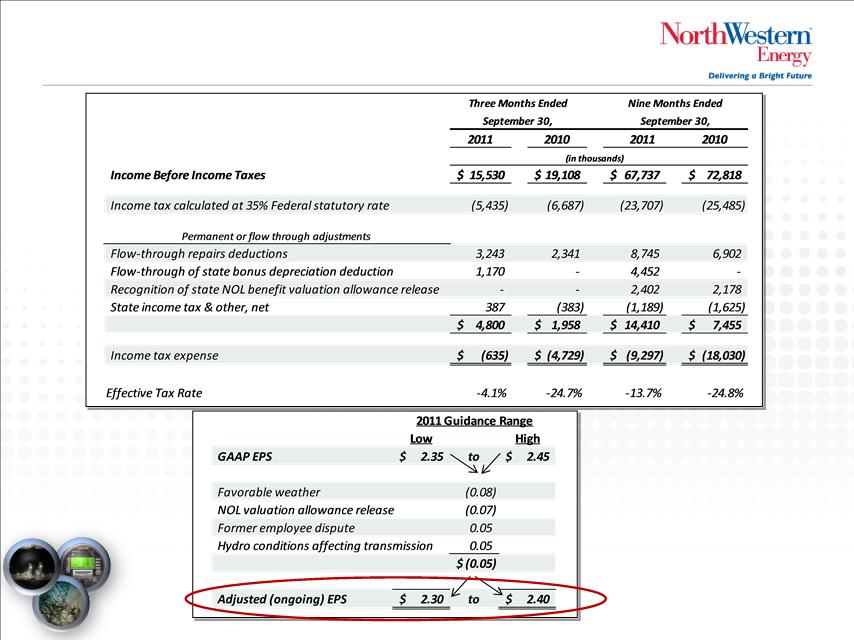

Reaffirming 2011 earning guidance

Reaffirming 2011 guidance range of $2.30-$2.40, which would result in 7-12% growth over 2010,

based upon, but not limited to, the following major assumptions and expectations:

based upon, but not limited to, the following major assumptions and expectations:

• Gross margin will be positively impacted by approximately $6.0 million in the fourth quarter of 2011,

as compared with the fourth quarter of 2010, due to the inclusion of DGGS in rates;

as compared with the fourth quarter of 2010, due to the inclusion of DGGS in rates;

* CAGR is based on the midpoint of 2011 revised guidance range of $2.30-$2.40 per diluted share

Near-term earnings drivers

16

2012 expectations/assumptions:

ð Additional gross margin adding between $.20/share to $.25/share from 2011

– Relates primarily to property tax tracker timing differences, SD rate increase, and

non-weather customer growth

– Also, assumes some increase in wholesale transmission revenues due to demand

recovery and normal hydro conditions in 2012

ð Administrative expenses to decrease from 2011 by $.02/share to $.05/share

– Company focus on cost containment

– Absence of 3Q 2011 former employee dispute in 2012

ð Other income to increase from 2011 by $.05/share to $.10/share:

– AFUDC on capital projects during 2012

ð Interest expense to decrease from 2011 by $.03/share to $.05/share:

– Capitalized as AFUDC on capital projects during 2012

ð Operating expenses are expected to increase about $.10/share to $.15/share from 2011

– Labor to increase about 3%

ð Property tax and other expenses are expected to remain about flat compared with 2011

ð Depreciation expense to increase about $.10/share from 2011

ð Income tax expense to increase about $.05/share to $.10/share from 2011

2013 expectations:

ð If approved, Spion Kop in commercial operation

ð Aberdeen South Dakota peaker in commercial operation

ð AFUDC or rider on South Dakota pollution control projects (Big Stone / Neal)

ð AFUDC on Colstrip 500 kV Upgrade

ð If Battle Creek successfully placed in rate base, likely pursuing additional natural gas reserves

ð Potential rate filings

Well-positioned for future investment

17

Continued

investment in our

system to serve our

customers and

communities is

expected to provide

average earnings per

share growth

and dividend growth

of 4-6% annually.

That, coupled with

dividend yield of

investment in our

system to serve our

customers and

communities is

expected to provide

average earnings per

share growth

and dividend growth

of 4-6% annually.

That, coupled with

dividend yield of

4-5%, should provide

great results for

investors over the

foreseeable future.

great results for

investors over the

foreseeable future.

Outline

Who we are

Financial update

Investment opportunity

outlook

Conclusion

Appendix

- Financial statements

- Regulatory update

- Additional investment opportunity detail

Financial update

Investment opportunity

outlook

Conclusion

Appendix

- Financial statements

- Regulatory update

- Additional investment opportunity detail

18

Investment opportunity outlook

ð Energy Supply

– Big Stone/Neal pollution control

– South Dakota natural gas peaking generation

– Montana Spion Kop Wind facility

– South Dakota Titan Wind facility buyout

– Other vertical integration opportunities in

Montana

Montana

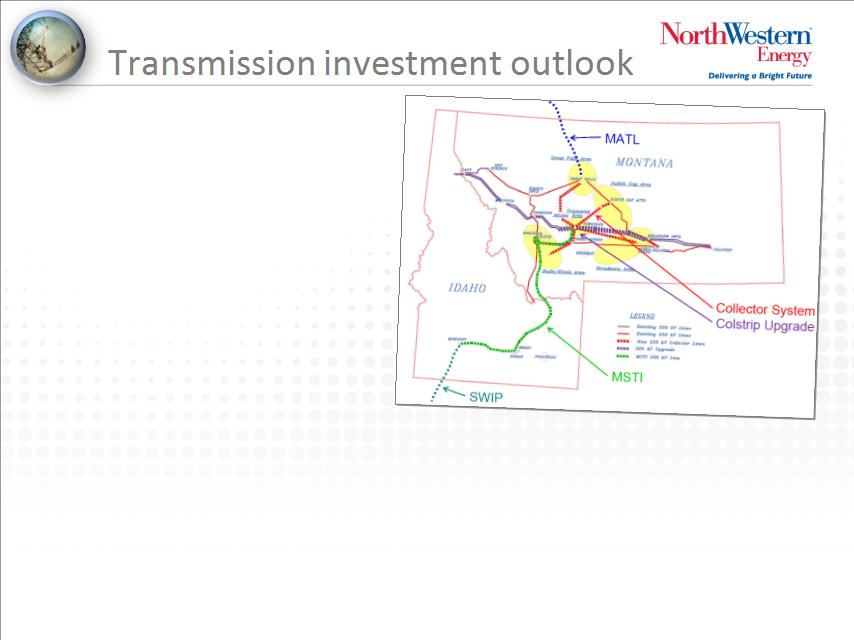

ð Transmission

– Network upgrades and large generation

interconnections

interconnections

– Colstrip 500kV upgrade

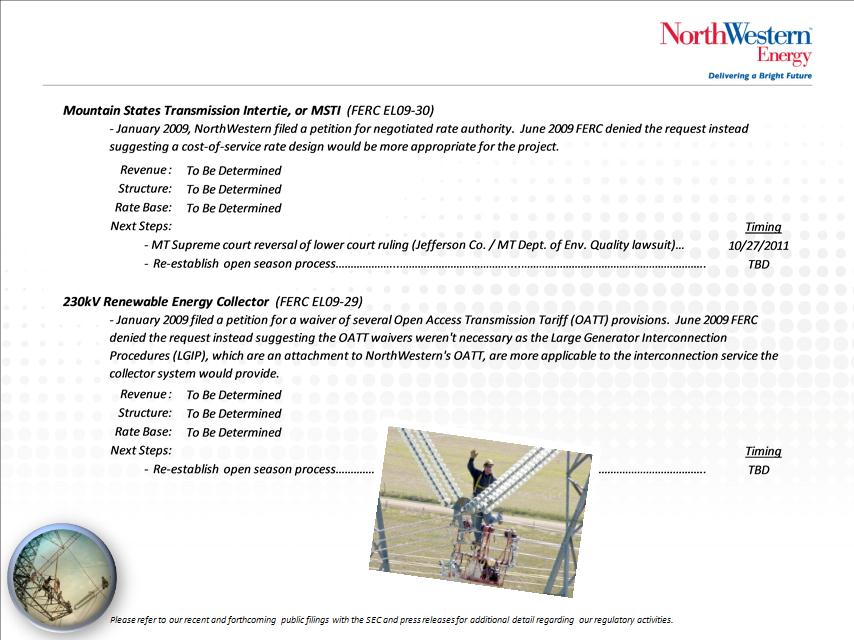

– Mountain States Transmission Intertie (MSTI)

– 230kV Renewable Collector System

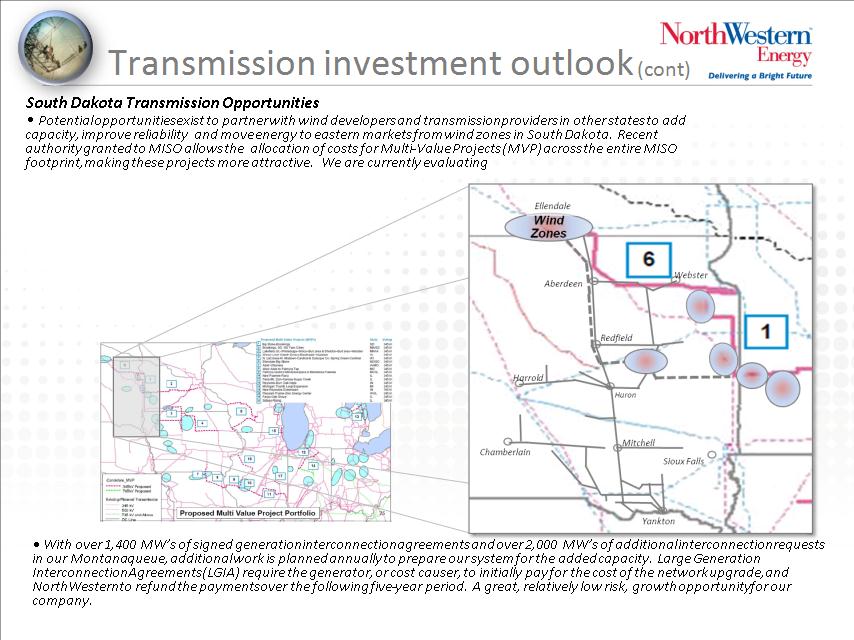

– South Dakota transmission opportunities

ð Distribution

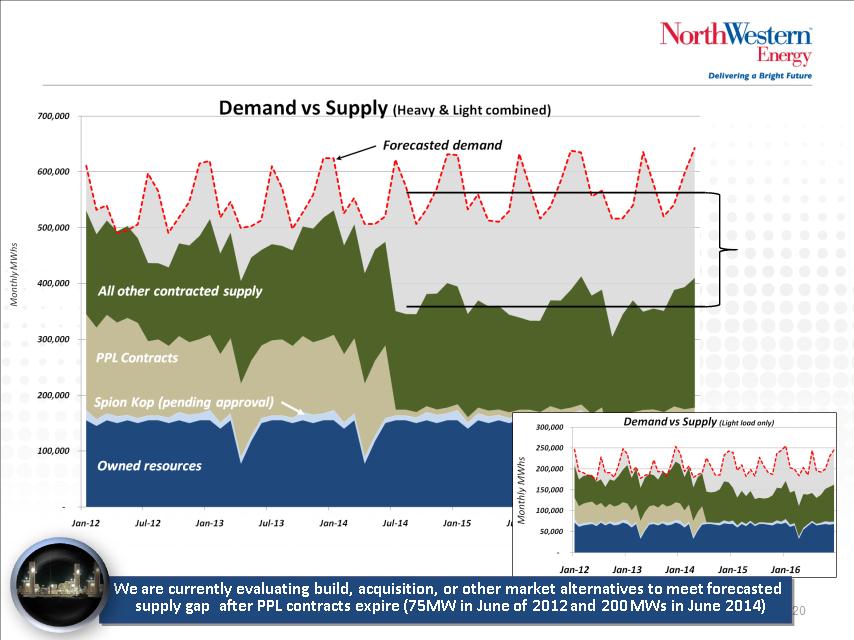

Montana base load opportunity

Our post PPL supply

opportunity is

approximately

200 GWh / month or

about 280 MWs of

capacity

opportunity is

approximately

200 GWh / month or

about 280 MWs of

capacity

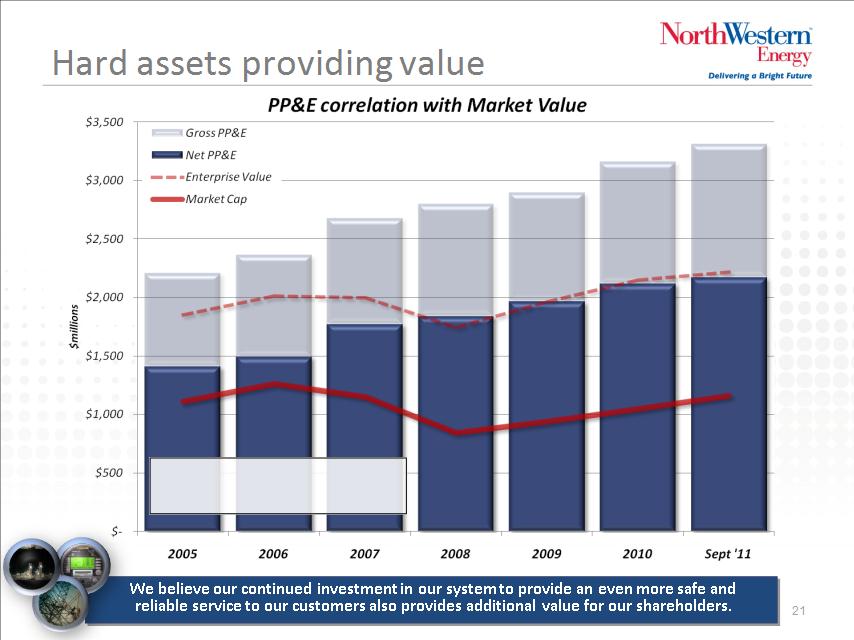

2005-07 valuation affected by pending and

ultimately terminated acquisition

ultimately terminated acquisition

Growing investment in our existing system

22

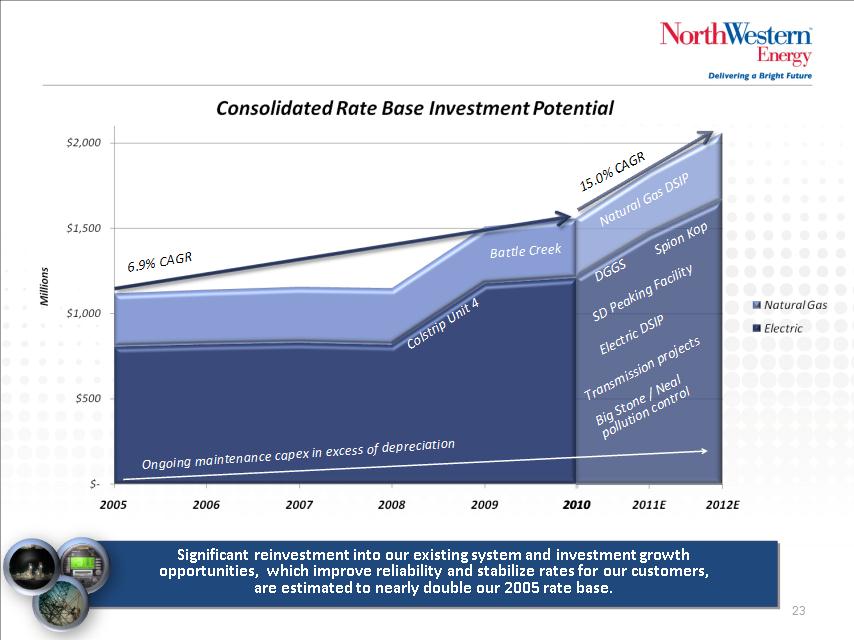

Great investment growth opportunities

Investment project summary

24

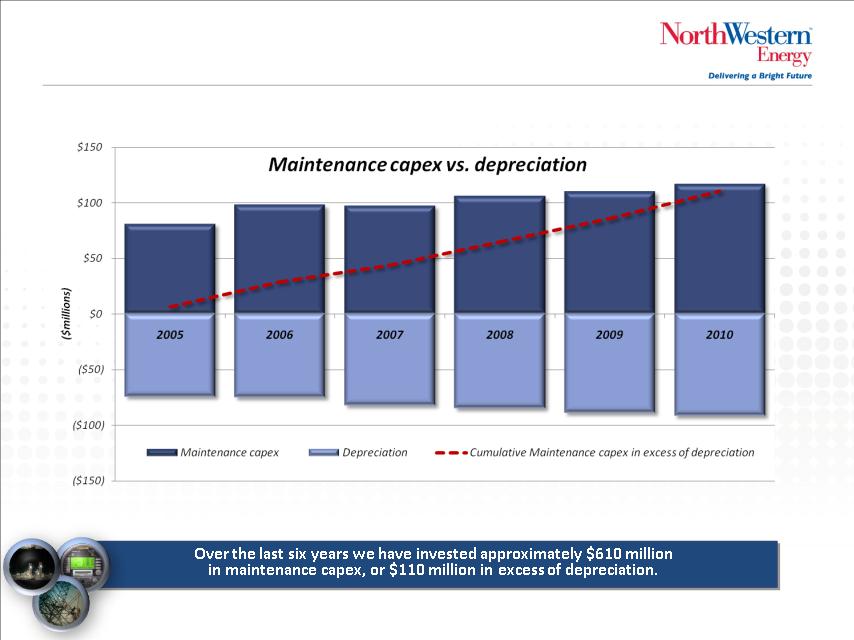

Several opportunities exist to further increase and diversify earnings as compared to our

approximately $1.8 billion of rate base today. Additional Montana base load opportunities are

currently being evaluated and may be incorporated at the appropriate time.

approximately $1.8 billion of rate base today. Additional Montana base load opportunities are

currently being evaluated and may be incorporated at the appropriate time.

Note: Color / label indicate NorthWestern Energy's current probability of execution and timing of expenditures.

Another way to slice the pie

(at midpoint of range)

Outline

Who we are

Financial update

Investment opportunity

outlook

Conclusion

Appendix

- Financial statements

- Regulatory update

- Additional investment opportunity detail

Financial update

Investment opportunity

outlook

Conclusion

Appendix

- Financial statements

- Regulatory update

- Additional investment opportunity detail

26

27

NorthWestern, the 2nd happiest place on Earth

28

QUESTIONS

Thank You

Outline

Who we are

Financial update

Investment opportunity

outlook

Conclusion

Appendix

- Financial statements

- Regulatory update

- Additional investment opportunity detail

Financial update

Investment opportunity

outlook

Conclusion

Appendix

- Financial statements

- Regulatory update

- Additional investment opportunity detail

30

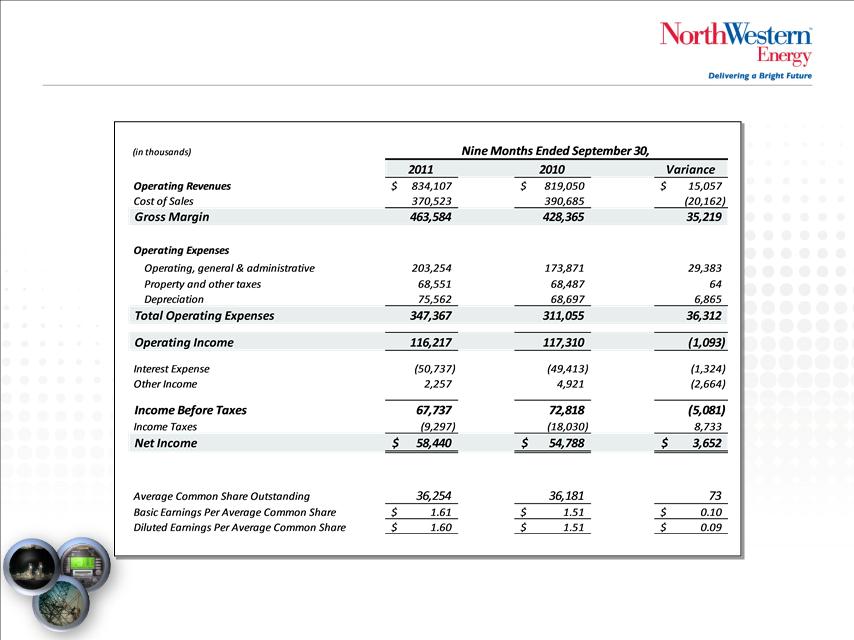

Consolidated statement of income

31

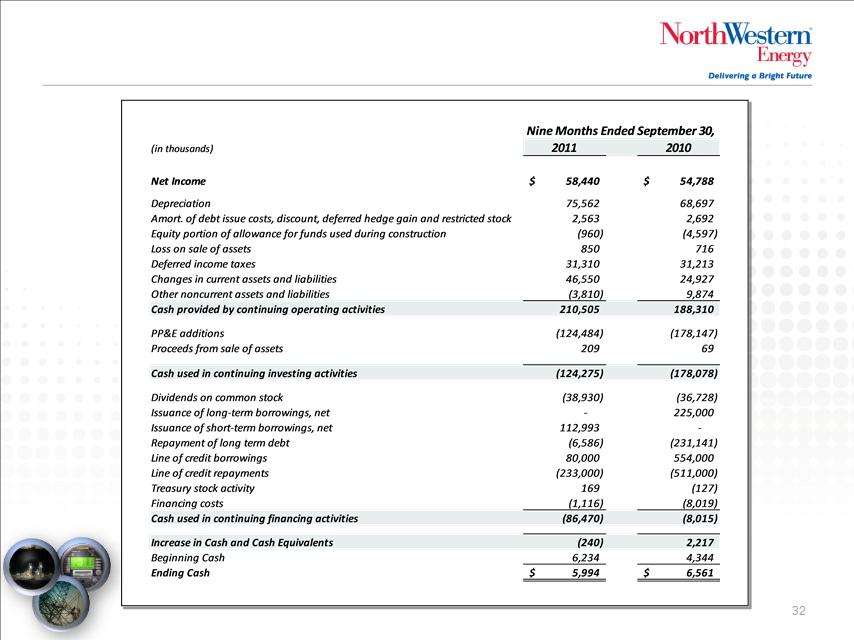

Consolidated statement of cash flows

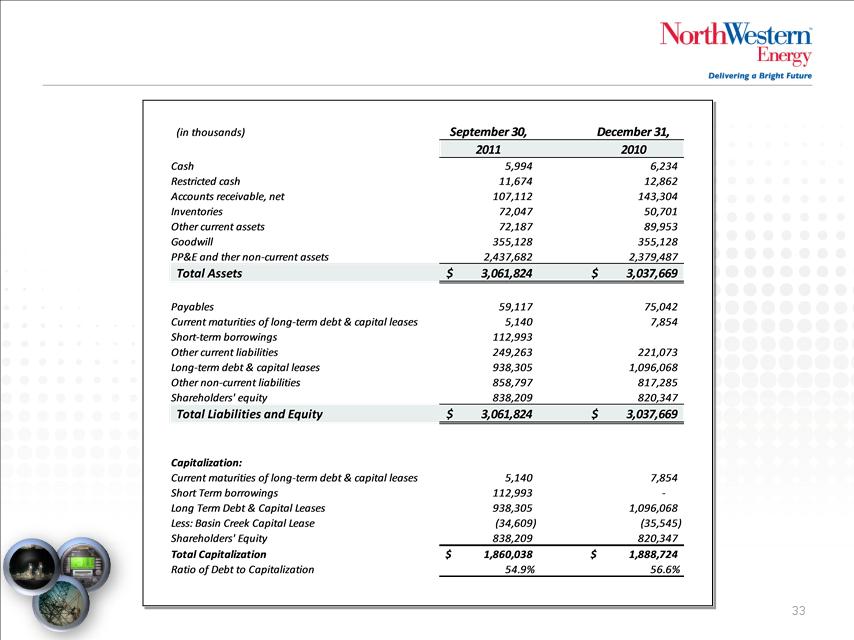

Consolidated balance sheet

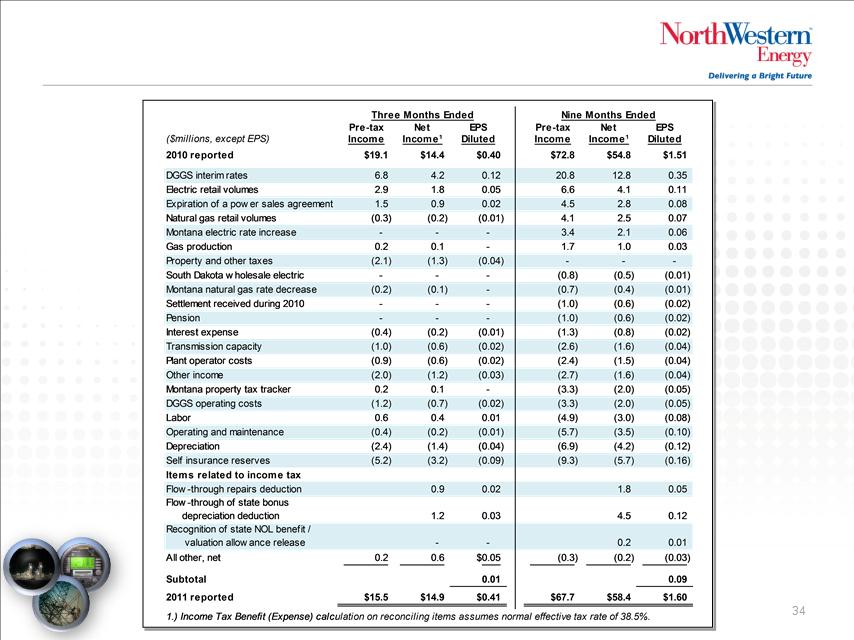

Earnings reconciliation

Other miscellaneous earnings items

35

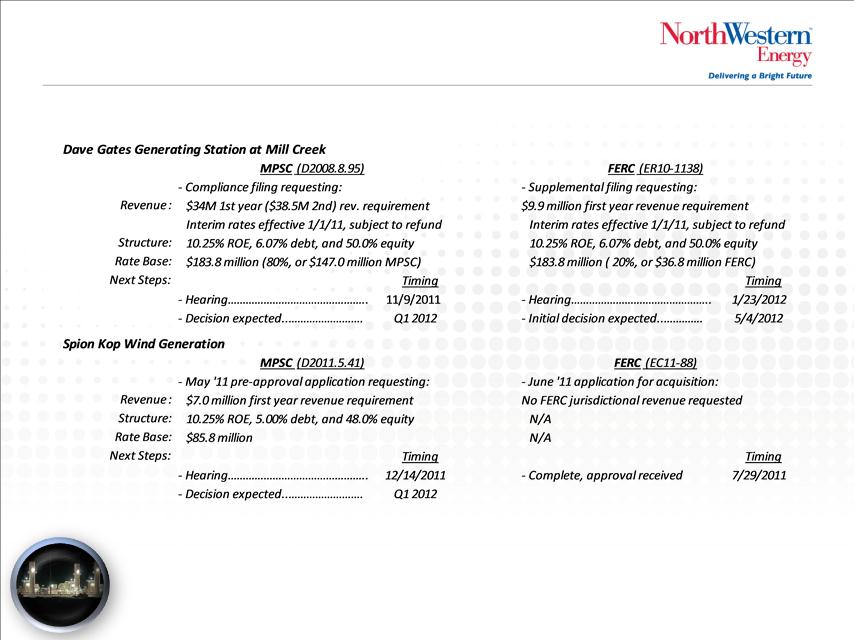

Energy supply regulatory update

36

Please refer to our recent and forthcoming public filings with the SEC and press releases for additional detail regarding our regulatory activities.

Energy supply regulatory update (cont.)

37

Please refer to our recent and forthcoming public filings with the SEC and press releases for additional detail regarding our regulatory activities.

Transmission regulatory update

38

39

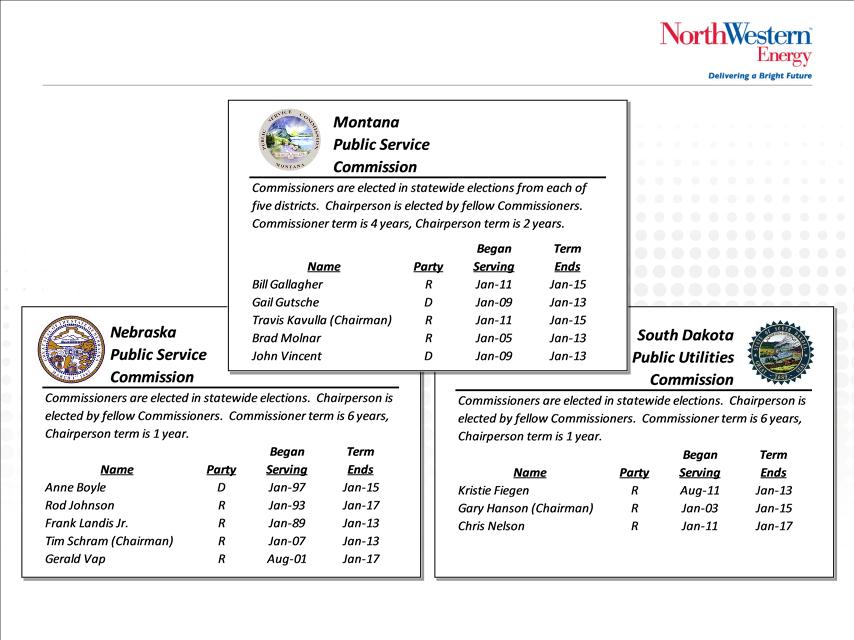

Our Commissioners

40

41

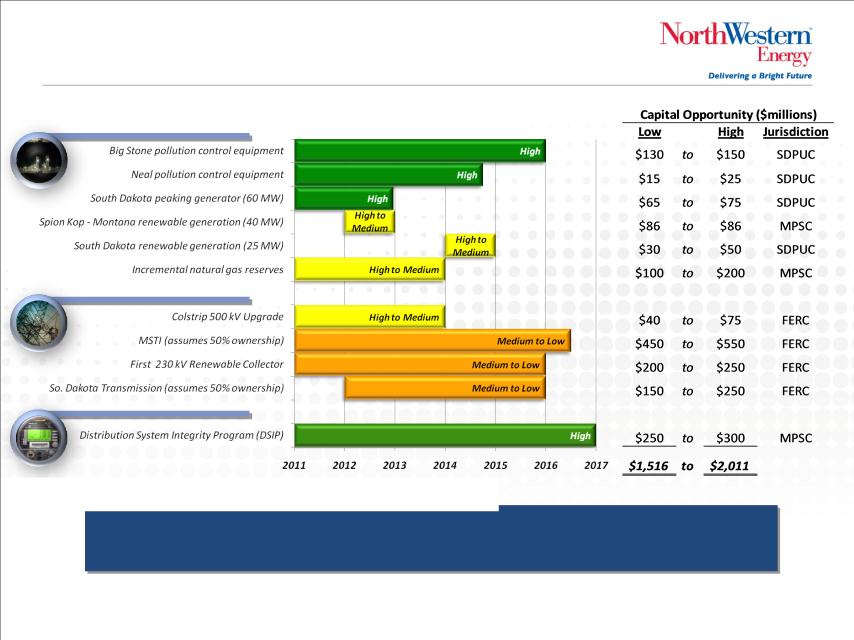

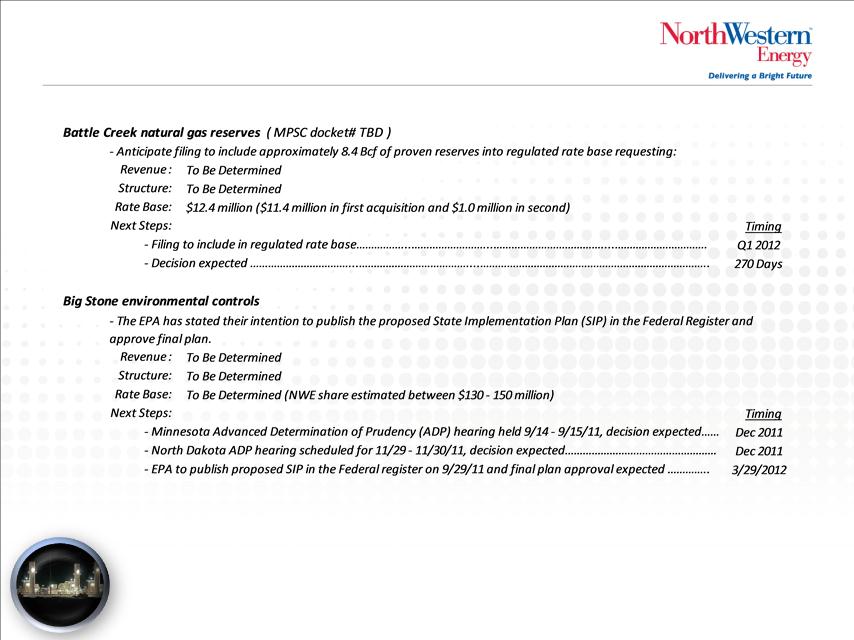

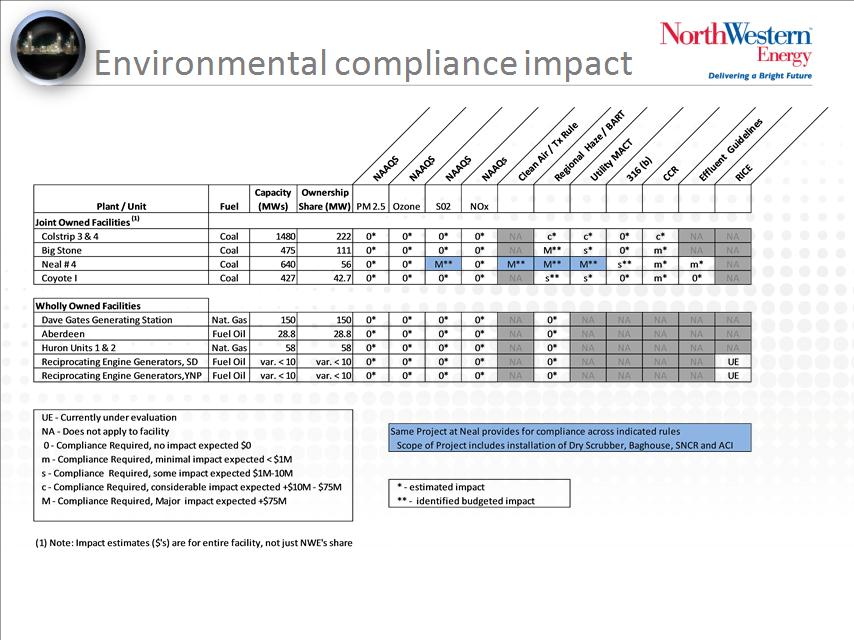

South Dakota pollution control equipment

• Big Stone: 23.4% joint owner in an estimated $500 million project to install SOx (scrubbers), NOx (SCR) and particulate matter (bag

house) emission control technology on a jointly owned 454 MW power plant. We have 5 years from the Environmental Protection Agency’s

house) emission control technology on a jointly owned 454 MW power plant. We have 5 years from the Environmental Protection Agency’s

(EPA) approval of the South Dakota Department of Environmental and Natural Resources (DENR) State Implementation Plan (SIP) to

have the Best Available Retrofit Technology (BART) installed. The SIP was filed in January 2011 and revised in September 2011. We are

unable to predict the EPA’s timing or ultimate approval. A de minimis amount of spend has been incurred in 2011 with the bulk of our

$130-150 million share (including AFUDC and overheads) to be spent over the next 5 years. Estimated completion date mid 2016.

• Neal 4: 8.7% joint owner in a $270 million project to install a scrubber, bag house, SNCR and activated carbonated injection system on

our jointly owned 655 MW facility. A negligible portion of the spend has been incurred in 2011 with the remainder of our $20-25 million

share (including AFUDC and overheads) to be spent over the next 3 years. Estimated completion date of late 2014.

our jointly owned 655 MW facility. A negligible portion of the spend has been incurred in 2011 with the remainder of our $20-25 million

share (including AFUDC and overheads) to be spent over the next 3 years. Estimated completion date of late 2014.

• We expect to seek recovery for these two environmental projects above through a specific environmental rider mechanism made

available through South Dakota State Statute in conjunction with a potential electric rate filing.

available through South Dakota State Statute in conjunction with a potential electric rate filing.

South Dakota natural gas peaking generation

• Approximately $65 million investment to build a 60MW natural gas peaking facility in Aberdeen, South Dakota. The peaker will

provide greater reliability and much needed capacity to our South Dakota system. South Dakota hit a new peak of 341MW in the

summer of 2011 as compared to the previous peak of 315MW in 2007. Construction began in 2011 and the unit is expected to be in-

service by December 1, 2012. We anticipate seeking recovery for this investment through a general electric rate filing after completion.

provide greater reliability and much needed capacity to our South Dakota system. South Dakota hit a new peak of 341MW in the

summer of 2011 as compared to the previous peak of 315MW in 2007. Construction began in 2011 and the unit is expected to be in-

service by December 1, 2012. We anticipate seeking recovery for this investment through a general electric rate filing after completion.

Montana Spion Kop Wind facility

• Approximately $86 million investment, pending regulatory pre-approval, to purchase a 40MW wind facility in Judith Basin County,

Montana. A decision on regulatory pre-approval is anticipated by April 1, 2012. If the decision is favorable, construction would begin,

with the facility’s energy and renewable energy credits flowing into our electric supply portfolio by year-end 2012.

Montana. A decision on regulatory pre-approval is anticipated by April 1, 2012. If the decision is favorable, construction would begin,

with the facility’s energy and renewable energy credits flowing into our electric supply portfolio by year-end 2012.

South Dakota Titan Wind facility buy out

• In December 2008, we entered into a 20-year power purchase agreement for 25 MWs of electric supply from the Titan I Wind Project in

Hand County, South Dakota. Under this agreement, at the end of the fourth and fifth contract year we have an option to purchase the

project.

project.

Montana opportunities to vertically integrate other electric and natural gas assets

• With the passing of HB25 in 2007 and HB294 in 2009 allowing NorthWestern to again own rate based electric generation and natural

gas reserves, we continue to look for opportunities beyond Battle Creek to add reasonably priced base load and other supply resources

that will provide future price stability for our customers.

gas reserves, we continue to look for opportunities beyond Battle Creek to add reasonably priced base load and other supply resources

that will provide future price stability for our customers.

42

43

Colstrip 500kV Upgrade

• A proposed $125 million project to add 500-700 MW’s of

capacity to our existing 500 kV lines running from Colstrip

generation facility to Mid-Columbia area in Oregon by

adding series compensation and a new substation near

Townsend, Montana. It is currently estimated that our

portion of the upgrade project will be $40-75 million

dependent upon participation by Bonneville Power

Administration and the four other Pacific Northwestern

Utilities that are partners in the line. The upgrade

could be completed as early as the end of 2013.

Mountain States Transmission Intertie (MSTI)

• A proposed 500 kV, 1,500 megawatt transmission line

to deliver electricity from Montana to customers in the

Western United States. The intent of the roughly $1 billion,

400+ mile project is to address the need for new electric

transmission service from states like Montana with vast

renewable generating potential to other Western states

in need of the renewable energy credits. They system

would also bolster the western power grid in general. Uncertainty surrounding Federal renewable standards and the general economic

environment has slowed, but not stopped, spending and work on the project until we have more clarity. We continue to evaluate

options for a strategic partner in this project. Assuming all permits / regulatory approvals are received and sufficient demand, current

estimates suggest a late 2016 in-service date.

environment has slowed, but not stopped, spending and work on the project until we have more clarity. We continue to evaluate

options for a strategic partner in this project. Assuming all permits / regulatory approvals are received and sufficient demand, current

estimates suggest a late 2016 in-service date.

230kV Renewable Collector System

• A proposed 230kV collector system project remains in the planning stage. Based on the current interconnection and transmission

service queues, we believe that demand exists for the development of five generator lead lines that would ultimately deliver power to

our MSTI line discussed above. The project would seek to use existing transmission right-of-ways where economical. The first of the lines

is estimated to require $200-250 million investment with in-service timing dependent upon MSTI progress and demand.

service queues, we believe that demand exists for the development of five generator lead lines that would ultimately deliver power to

our MSTI line discussed above. The project would seek to use existing transmission right-of-ways where economical. The first of the lines

is estimated to require $200-250 million investment with in-service timing dependent upon MSTI progress and demand.

44

Network Upgrades and Large Generation Interconnections

the cost of joining MISO as compared to the opportunities and

other benefits that membership may provide. Investment

opportunities are currently estimated to be between

$300-500 million. The map below is from a

September 2011 MVP Business Case Workshop

and expanded to show the overlay of

our South Dakota transmission

system relative to these

MVP projects.

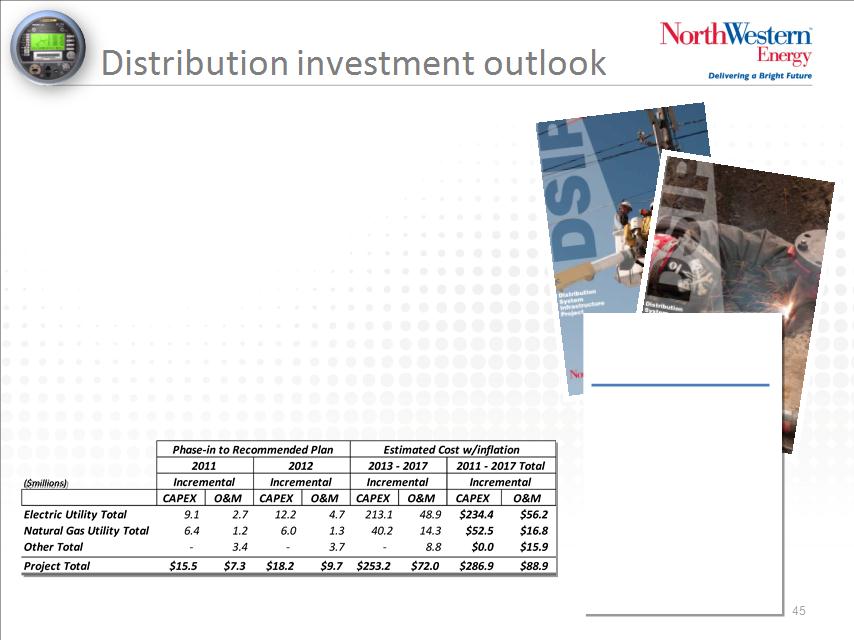

Distribution System Integrity Program (DSIP)

Distribution System Integrity Program (DSIP)

The Project will address the emerging issue of our aging infrastructure and prepare

our natural gas and electric distribution systems for the next generation of

technology.

our natural gas and electric distribution systems for the next generation of

technology.

The Project will address the emerging issue of our aging infrastructure and prepare

our natural gas and electric distribution systems for the next generation of

technology.

our natural gas and electric distribution systems for the next generation of

technology.

For the electric distribution system, the Program’s goals are:

For the electric distribution system, the Program’s goals are:

• Arrest and reverse the trend of aging infrastructure;

• Arrest and reverse the trend of aging infrastructure;

• Build appropriate margin (capacity) back into the system;

• Maintain reliability over the long-term, and improve it for our rural customers; and,

• Position NWE to adopt Smart Grid, by accomplishing those tasks that are necessary,

whether or not Smart Grid is eventually deployed on a wide scale, and regardless of

what form of Smart Grid is eventually deployed.

whether or not Smart Grid is eventually deployed on a wide scale, and regardless of

what form of Smart Grid is eventually deployed.

For the natural gas distribution system, the Program's goals are:

• Embrace the industry's new performance-driven model Natural Gas Distribution

Integrity Management Program (DIMP);

Integrity Management Program (DIMP);

• Employ state-of-the-art analytical capabilities to proactively manage safety; and,

• Improve leak rate performance.

NorthWestern, Delivering

quality at a great value —

yesterday, today and

tomorrow…

quality at a great value —

yesterday, today and

tomorrow…

As a NorthWestern Energy

customer, you expect and deserve

top quality at a reasonable cost - in

other words, great value. We agree.

NorthWestern Energy has one of

the safest and most reliable electric

and natural gas distribution systems

in the country, and we want to keep

it that way. That’s why we created a

multi-year project to aggressively

replace aging infrastructure and to

prepare our network to support the

next generation of new technology.

customer, you expect and deserve

top quality at a reasonable cost - in

other words, great value. We agree.

NorthWestern Energy has one of

the safest and most reliable electric

and natural gas distribution systems

in the country, and we want to keep

it that way. That’s why we created a

multi-year project to aggressively

replace aging infrastructure and to

prepare our network to support the

next generation of new technology.