Searchable text section of graphics shown above

[GRAPHIC]

[LOGO]

Annual Stockholders’ Meeting

July 14, 2005

NEW STRENGTH. NEW STRATEGY. NEW ENERGY.

Forward-Looking Statement

During the course of this presentation today, we will be discussing certain subjects including those pertaining to our strategy, and our discussions may contain forward-looking information. Although our expectations and beliefs are based on reasonable assumptions, actual results may differ materially. These factors that may affect our results are listed in certain of our press releases and disclosed in the company’s public filings with the SEC.

2

Introduction

• NorthWestern is a new and stronger company after successful reorganization in 2004

• Significantly reduced debt, strengthened balance sheet

• Transmission and distribution utility operations performing well with solid cash flow

• Demonstrated top quartile customer service and reliability with competitive rates

• Low-risk business profile with solid growth prospects and earnings growth potential

• 2005 is on track to deliver projected financial results and meet performance goals

• Board and management is focused on providing a competitive return to shareholders

[GRAPHIC]

3

NorthWestern Energy Today

• Serving 617,000 electric and natural gas customers in Montana, South Dakota and Nebraska

• Approximately 1,350 employees

• Listed on NASDAQ: NWEC

• Approximately $1.1 billion market capitalization

• Quarterly dividend of 22 cents (88 cents annualized or approximately 3.0% yield)

• Payout ratio of approximately 60% to 65% (income from continuing operations)

[GRAPHIC]

4

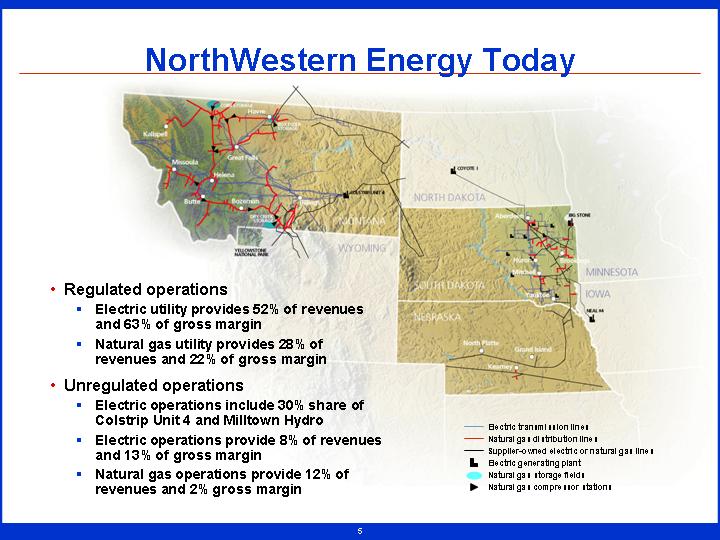

NorthWestern Energy Today

[GRAPHIC]

• Regulated operations

• Electric utility provides 52% of revenues and 63% of gross margin

• Natural gas utility provides 28% of revenues and 22% of gross margin

• Unregulated operations

• Electric operations include 30% share of Colstrip Unit 4 and Milltown Hydro

• Electric operations provide 8% of revenues and 13% of gross margin

• Natural gas operations provide 12% of revenues and 2% gross margin

5

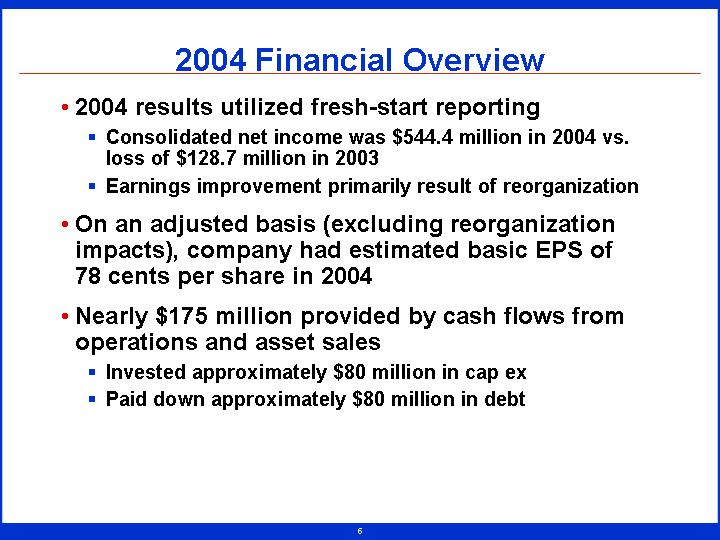

2004 Financial Overview

• 2004 results utilized fresh-start reporting

• Consolidated net income was $544.4 million in 2004 vs. loss of $128.7 million in 2003

• Earnings improvement primarily result of reorganization

• On an adjusted basis (excluding reorganization impacts), company had estimated basic EPS of 78 cents per share in 2004

• Nearly $175 million provided by cash flows from operations and asset sales

• Invested approximately $80 million in cap ex

• Paid down approximately $80 million in debt

6

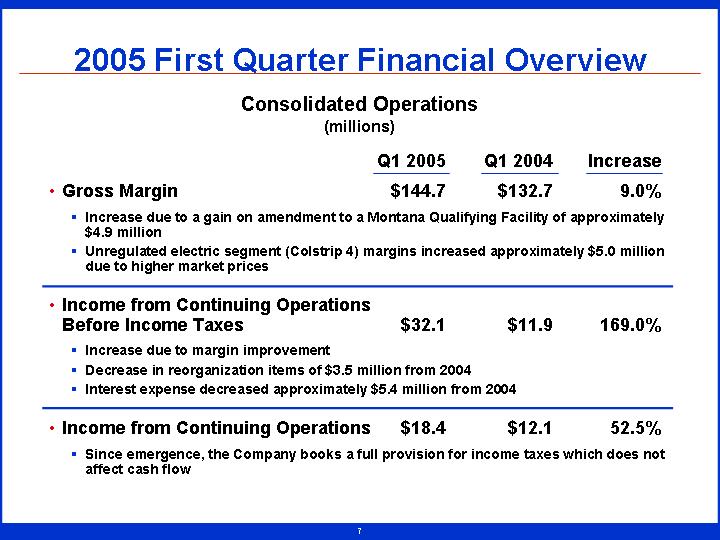

2005 First Quarter Financial Overview

Consolidated Operations

(millions)

|

|

|

| Q1 2005 |

| Q1 2004 |

| Increase |

| ||||

|

|

|

|

|

|

|

|

|

| ||||

• | Gross Margin |

| $ | 144.7 |

| $ | 132.7 |

| 9.0 | % | |||

|

| ||||||||||||

| • | Increase due to a gain on amendment to a Montana Qualifying Facility of approximately $4.9 million |

| ||||||||||

|

| ||||||||||||

| • | Unregulated electric segment (Colstrip 4) margins increased approximately $5.0 million due to higher market prices |

| ||||||||||

|

| ||||||||||||

• | Income from Continuing Operations Before Income Taxes |

| $ | 32.1 |

| $ | 11.9 |

| 169.0 | % | |||

|

| ||||||||||||

| • | Increase due to margin improvement |

| ||||||||||

|

| ||||||||||||

| • | Decrease in reorganization items of $3.5 million from 2004 |

| ||||||||||

|

| ||||||||||||

| • | Interest expense decreased approximately $5.4 million from 2004 |

| ||||||||||

|

| ||||||||||||

• | Income from Continuing Operations |

| $ | 18.4 |

| $ | 12.1 |

| 52.5 | % | |||

|

| ||||||||||||

| • | Since emergence, the Company books a full provision for income taxes which does not affect cash flow |

| ||||||||||

7

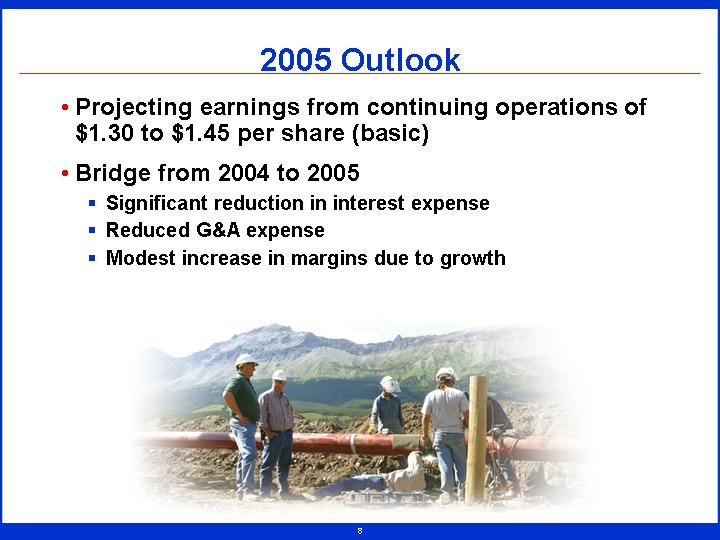

2005 Outlook

• Projecting earnings from continuing operations of $1.30 to $1.45 per share (basic)

• Bridge from 2004 to 2005

• Significant reduction in interest expense

• Reduced G&A expense

• Modest increase in margins due to growth

[GRAPHIC]

8

2005 Cash Flow Overview

|

| T & D Business |

|

| ||

|

|

|

|

|

| $215-$220 million* |

|

| Grow the Business |

| Cash |

|

|

|

|

|

|

|

|

|

|

| Value Creation Strategy |

|

| ||

|

|

|

|

|

|

|

$30-$35 million |

| Pay Dividend |

| Maintain and |

| $80 million |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Reduce Debt |

|

| ||

|

|

|

|

| ||

|

| $75 million |

|

| ||

* Assumes asset sales proceeds of $65-$70 million and uses 2004 cash flow from operations of $150 million as a proxy for ongoing cash flow from operations

9

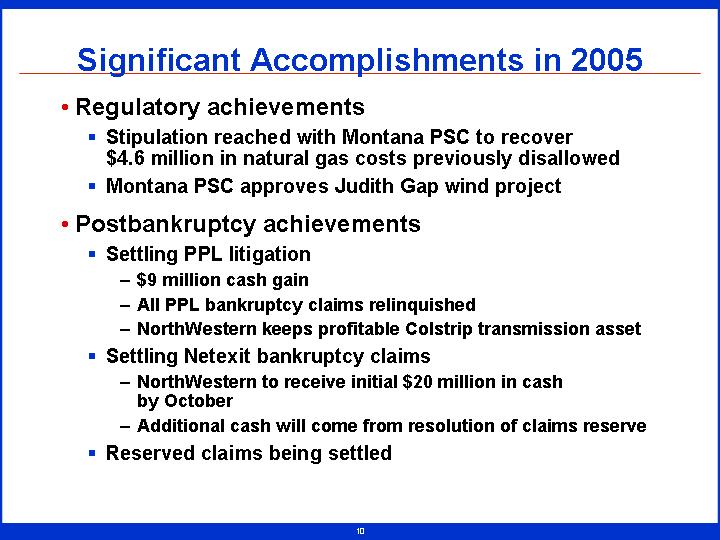

Significant Accomplishments in 2005

• Regulatory achievements

• Stipulation reached with Montana PSC to recover $4.6 million in natural gas costs previously disallowed

• Montana PSC approves Judith Gap wind project

• Postbankruptcy achievements

• Settling PPL litigation

• $9 million cash gain

• All PPL bankruptcy claims relinquished

• NorthWestern keeps profitable Colstrip transmission asset

• Settling Netexit bankruptcy claims

• NorthWestern to receive initial $20 million in cash by October

• Additional cash will come from resolution of claims reserve

• Reserved claims being settled

10

• Reduced total debt from $909 million to $755 million from available cash

• Debt to capitalization ratio down to approximately 50%

• Debt reduction plans met for the year

• Amended $225 million secured facility to $200 million unsecured facility

• Lowered interest expense

• Released $225 million in first mortgage collateral

• Additional refinancing opportunities exist

• Rating agencies upgrade debt

• Fitch upgrades senior secured debt to investment grade (BBB-)

• Added to Russell 3000, Russell 2000 indexes

NorthWestern has reduced debt by $154 million since July 2004.

[CHART]

11

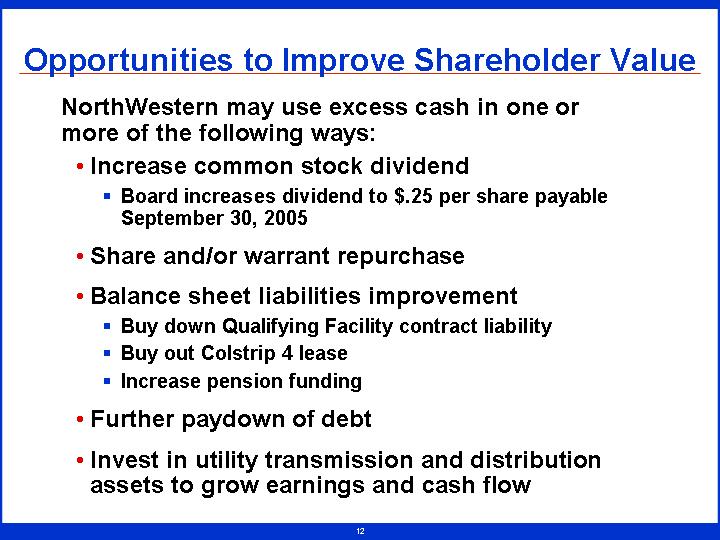

Opportunities to Improve Shareholder Value

NorthWestern may use excess cash in one or more of the following ways:

• Increase common stock dividend

• Board increases dividend to $.25 per share payable September 30, 2005

• Share and/or warrant repurchase

• Balance sheet liabilities improvement

• Buy down Qualifying Facility contract liability

• Buy out Colstrip 4 lease

• Increase pension funding

• Further paydown of debt

• Invest in utility transmission and distribution assets to grow earnings and cash flow

12

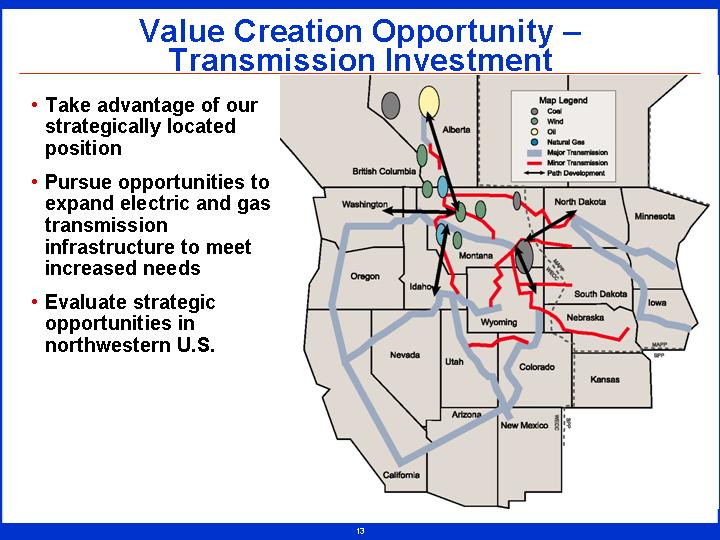

Value Creation Opportunity – Transmission Investment

• Take advantage of our strategically located position

• Pursue opportunities to expand electric and gas transmission infrastructure to meet increased needs

• Evaluate strategic opportunities in northwestern U.S.

[GRAPHIC]

13

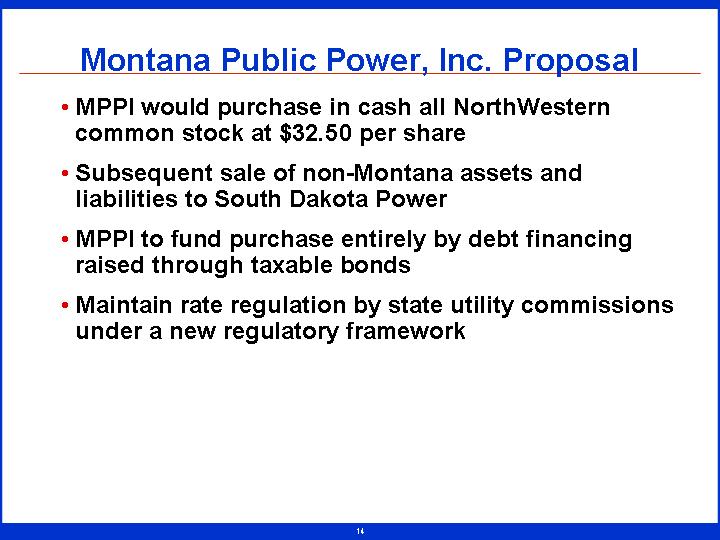

Montana Public Power, Inc. Proposal

• MPPI would purchase in cash all NorthWestern common stock at $32.50 per share

• Subsequent sale of non-Montana assets and liabilities to South Dakota Power

• MPPI to fund purchase entirely by debt financing raised through taxable bonds

• Maintain rate regulation by state utility commissions under a new regulatory framework

14

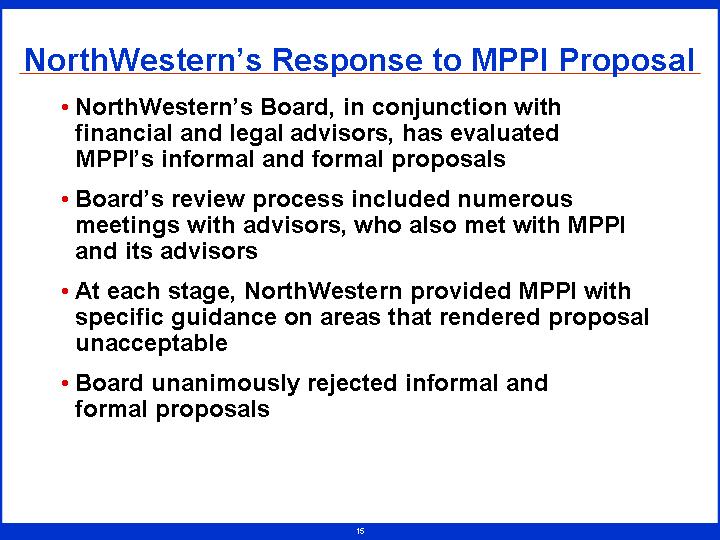

NorthWestern’s Response to MPPI Proposal

• NorthWestern’s Board, in conjunction with financial and legal advisors, has evaluated MPPI’s informal and formal proposals

• Board’s review process included numerous meetings with advisors, who also met with MPPI and its advisors

• At each stage, NorthWestern provided MPPI with specific guidance on areas that rendered proposal unacceptable

• Board unanimously rejected informal and formal proposals

15

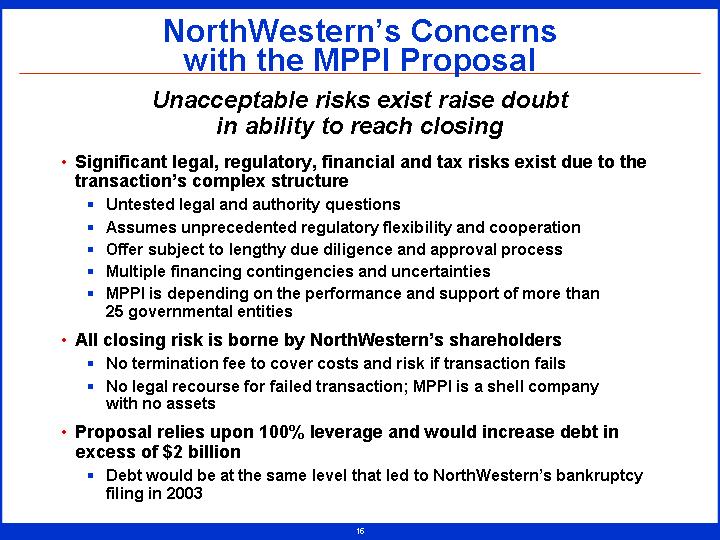

NorthWestern’s Concerns

with the MPPI Proposal

Unacceptable risks exist raise doubt

in ability to reach closing

• Significant legal, regulatory, financial and tax risks exist due to the transaction’s complex structure

• Untested legal and authority questions

• Assumes unprecedented regulatory flexibility and cooperation

• Offer subject to lengthy due diligence and approval process

• Multiple financing contingencies and uncertainties

• MPPI is depending on the performance and support of more than 25 governmental entities

• All closing risk is borne by NorthWestern’s shareholders

• No termination fee to cover costs and risk if transaction fails

• No legal recourse for failed transaction; MPPI is a shell company with no assets

• Proposal relies upon 100% leverage and would increase debt in excess of $2 billion

• Debt would be at the same level that led to NorthWestern’s bankruptcy filing in 2003

16

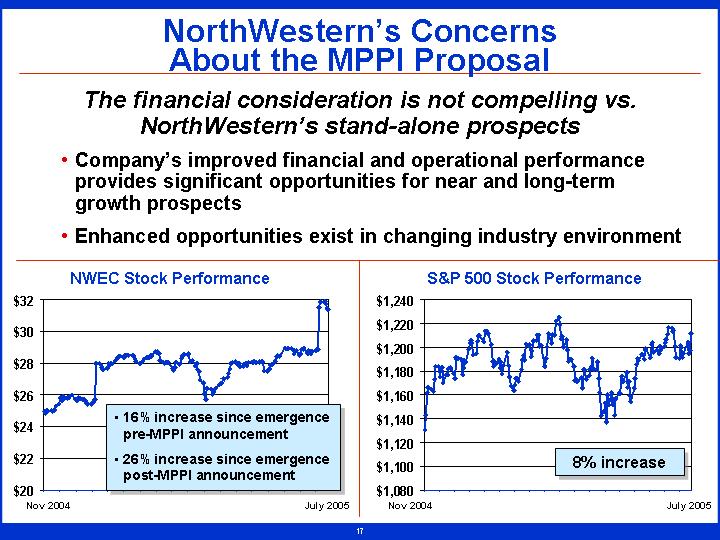

NorthWestern’s Concerns

About the MPPI Proposal

The financial consideration is not compelling vs.

NorthWestern’s stand-alone prospects

• Company’s improved financial and operational performance provides significant opportunities for near and long-term growth prospects

• Enhanced opportunities exist in changing industry environment

NWEC Stock Performance |

| S&P 500 Stock Performance |

|

|

|

[CHART] |

| [CHART] |

17

Why Should Stockholders

Own NWEC Long Term?

• Significant cash flow from operations

• Strong earnings profile of core utility business

• Significant reduction in interest expense due to debt reduction/refinancing

• Company will not pay significant cash taxes through 2008

• Solid dividend with opportunity for growth

• Strong EPS growth

• 2005 vs. 2004 improvement due to lower interest expense, lower overhead expenses, organic growth

• Future utility investment opportunities

• Business model inherently low risk

• Regulated “wires and pipes” business

• Energy costs passed through to customers

• Strong balance sheet

18

[LOGO] |

| [LOGO] |

Our Employees Make the Difference

[GRAPHIC]

| • | 2004 Service One Award winner |

|

|

|

| • | Consistent top quartile reliability |

|

|

|

| • | 24/7 dedication to service |

|

|

|

| • | Giving back to our communities |

19