Searchable text section of graphics shown above

Forward-Looking Statement

During the course of this presentation today, we will be discussing certain subjects including those pertaining to our strategy, and our discussions may contain forward-looking information. Although our expectations and beliefs are based on reasonable assumptions, actual results may differ materially. These factors that may affect our results are listed in certain of our press releases and disclosed in the company’s public filings with the SEC.

2

Montana Public Power, Inc. Proposal

• MPPI would purchase in cash all NorthWestern common stock at $32.50 per share

• Upon closing, MPPI would sell non-Montana assets and related liabilities to South Dakota Power Company

• MPPI to fund purchase entirely by debt financing

• MPPI states it would maintain rate regulation by state utility commissions; however, this would require a newly invented regulatory framework

3

NorthWestern Board’s Response To MPPI Proposal

• NorthWestern’s Board, in conjunction with financial and legal advisors, has evaluated MPPI’s informal and formal proposals

• Board’s review process included numerous meetings with advisors, who also met with MPPI and its advisors

• At each stage, NorthWestern provided MPPI with specific guidance on areas that rendered the proposal unacceptable

• Board unanimously rejected informal and formal proposals

• Unacceptable risks exist that raise doubt in the ability to reach closing

• Financial consideration is not compelling vs. NorthWestern’s stand-alone prospects

4

NorthWestern’s Concerns With the MPPI Proposal

Financing Risk

• MPPI relies on a highly leveraged, “no equity” financial plan consisting of 100% debt structure

• Rating agencies uncertain as to whether such debt will be investment grade without regulatory safety net

• Financed by customers and utility assets, not by taxing or regulatory authority

• Citigroup offered only a “best efforts” commitment, subject to a myriad of contingencies

• Potential significant tax liability exists from proposed transaction

5

Risks to Stockholders

What MPPI Says (June 30, 2005)

“MPPI has had preliminary discussions about the transaction with rating agencies, and is confident that projected coverage ratios

are consistent with investment grade credit ratings.”

What Standard & Poor’s Says (July 1, 2005)

S&P gave “NorthWestern a ‘BB’ corporate credit rating… with negative implications pending clarity on [MPPI’s] June 30, 2005 offer to buy NorthWestern. The CreditWatch listing reflects Standard & Poor’s lack of information about Montana Public Power and the financing and legal structure of its bid… Should the offer be rejected or withdrawn, it is likely that Standard & Poor’s will affirm ratings and assign a positive outlook. However, if the bid is approved, the ratings could be lowered or withdrawn…”

6

NorthWestern’s Concerns With the MPPI Proposal

Regulatory Risk

• MPPI assumes it can obtain unprecedented regulatory flexibility and cooperation to obtain financing

• Ability to raise rates to assure lenders

• Montana PSC may not have authority to provide flexibility without changing Montana law

• Uncertainty around secondary sale of non-Montana assets

• 100% leverage may be problematic for regulators

• MPPI may be subject to PUHCA and FERC

• Future capital spending would be debt financed which would increase debt and would likely require increases in rates to cover the debt service

• “The MPPI acquisition proposal would appear to me to have created a financial situation where the new venture would have started out at a debt load that equaled 100% of equity. The vast majority of failed businesses have had problems with either undercapitalization or lack of management expertise. MPPI would likely be allowed to launch with both.” Montana PSC Commissioner Doug Mood

7

Legal Risk

• Montana Attorney General opinion does not cover all legal concerns

• Montana law may not permit MPPI to own and operate a utility outside of the cities’ or state’s jurisdiction

• Subsequent sale of non-Montana assets raises the potential for a fraudulent conveyance claim by MPPI’s creditors in the event of a default

• Attorney General opinion is subject to challenge and ultimately will be determined by Montana courts

• No legal recourse exists for a failed transaction

• MPPI is a shell company with no assets

• No termination fee to cover costs and risk of transaction failure

• Montana Open Meeting law could expose process to public disclosure

• Magten letter exposes additional risk to company and large shareholders

8

Local Control/Authority

• MPPI states the primary reason for the acquisition is to provide local control

• Communities will have no control over operations, spending or use of proceeds on a community-by-community basis

• Many communities are telling NorthWestern they are not informed and question the direction of the proposal

• Concerns raised on impact of state and local taxes

• MPPI has not addressed energy procurement issues

• Closing risk exists if MPPI cannot resolve community concerns

9

Timing/Ability to Close

• Significant regulatory, legal, financial and other risks raise concern whether transaction can close

• If concerns could be resolved, it would require at least 18 months to close transaction

• Business and legal due diligence

• Multiple state regulatory approvals with lengthy public process

• Federal Energy Regulatory Commission

• Hart-Scott-Rodino and other possible approvals

• Financing contingency

• Shareholder value would be negatively impacted if transaction fails to close

• Lengthy closing would impact the present value of the proposed transaction and increases financing risk

• Secondary transaction for non-Montana assets has not been formalized and could delay a proposed transaction

• “South Dakota Power’s (proposed) purchase of NorthWestern’s assets from Montana Public Power would probably be years off.” Mark Anderson, Aberdeen, S.D., City Attorney and Vice President of South Dakota Power

10

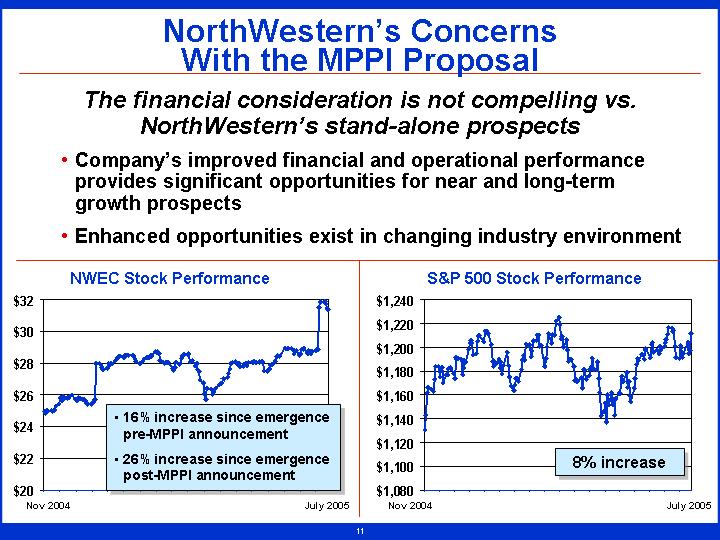

The financial consideration is not compelling vs. NorthWestern’s stand-alone prospects

• Company’s improved financial and operational performance provides significant opportunities for near and long-term growth prospects

• Enhanced opportunities exist in changing industry environment

NWEC Stock Performance |

| S&P 500 Stock Performance |

|

|

|

[CHART] |

| [CHART] |

11

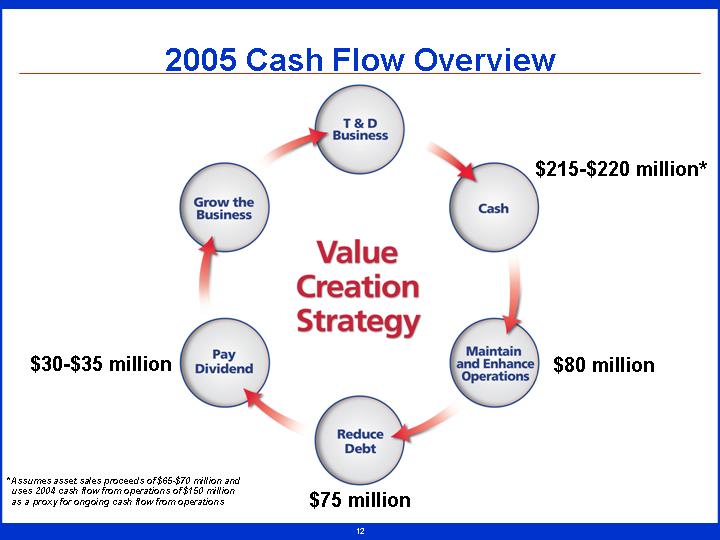

2005 Cash Flow Overview

|

|

|

| T & D |

|

|

|

|

|

|

|

|

|

|

|

| $215-$220 million* |

|

| Grow the |

|

|

| Cash |

|

|

|

|

|

| Value |

|

|

|

|

$30-$35 million |

| Pay |

|

|

| Maintain |

| $80 million |

|

|

|

| Reduce |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| $75 million |

|

|

|

|

* Assumes asset sales proceeds of $65-$70 million and uses 2004 cash flow from operations of $150 million as a proxy for ongoing cash flow from operations

12

NorthWestern’s Stand-Alone Prospects

• Company’s stand-alone prospects have dramatically improved since emergence

• Anticipating solid 2005 earnings and cash flow from continuing operations

• Company achieving targeted capital structure ahead of schedule

• Significantly lower interest expense

• Both cash and noncash interest

• Ongoing cost reductions

• G&A reductions and future restructuring cost reductions

• Won’t be a cash taxpayer through 2008

• Excess cash flow available to increase shareholder value

13

Opportunities to Improve Shareholder Value

NorthWestern may use excess cash in one or more of the following ways:

• Increase common stock dividend

• Share and/or warrant repurchase

• Balance sheet liabilities improvement

• Buy down Qualifying Facility contract liability

• Buy out Colstrip 4 lease

• Increase pension funding

• Invest in utility transmission and distribution assets to grow earnings and cash flow

14

Improving Near-Term Shareholder Value

• Board increases dividend

• 14% increase effective Sept. 30, 2005

• Moves annualized rate to $1.00 per share

• Board will review future action when 2006 guidance is provided

• S-3 Registration Statement revised and submitted to SEC

• Could go effective in 10 days or sooner

• Second quarter results to be announced in early August

• Company ready to support roadshow for secondary offering of shares of large shareholders

15

Why Should Shareholders Own NWEC Long Term?

• Significant cash flow from operations

• Strong earnings profile of core utility business

• Significant reduction in interest expense due to debt reduction/refinancing

• Company will not pay significant cash taxes through 2008

• Cash available to enhance shareholder value

• Solid dividend with opportunity for growth

• Strong EPS growth

• 2005 vs. 2004 improvement due to lower interest expense, lower overhead expenses, organic growth

• Opportunities for future utility investments

• Future balance sheet improvements

• Business model inherently low risk

• Regulated “wires and pipes” business

• Energy costs passed through to customers

• Strong balance sheet

16