| UNITED STATES |

| SECURITIES AND EXCHANGE COMMISSION |

| Washington, D.C. 20549 |

FORM N-CSR |

CERTIFIED SHAREHOLDER REPORT OF REGISTERED |

MANAGEMENT INVESTMENT COMPANIES |

| Investment Company Act File Number: 811-3894 |

| T. Rowe Price Short-Term Bond Fund, Inc. |

| (Exact name of registrant as specified in charter) |

| 100 East Pratt Street, Baltimore, MD 21202 |

| (Address of principal executive offices) |

| David Oestreicher |

| 100 East Pratt Street, Baltimore, MD 21202 |

| (Name and address of agent for service) |

| Registrant’s telephone number, including area code: (410) 345-2000 |

| Date of fiscal year end: May 31 |

| Date of reporting period: May 31, 2008 |

Item 1: Report to Shareholders

|

| Short-Term Bond Fund | May 31, 2008 |

The views and opinions in this report were current as of May 31, 2008. They are not guarantees of performance or investment results and should not be taken as investment advice. Investment decisions reflect a variety of factors, and the managers reserve the right to change their views about individual stocks, sectors, and the markets at any time. As a result, the views expressed should not be relied upon as a forecast of the fund’s future investment intent. The report is certified under the Sarbanes-Oxley Act, which requires mutual funds and other public companies to affirm that, to the best of their knowledge, the information in their financial reports is fairly and accurately stated in all material respects.

REPORTS ON THE WEB

Sign up for our E-mail Program, and you can begin to receive updated fund reports and prospectuses online rather than through the mail. Log in to your account at troweprice.com for more information.

Manager’s Letter

Fellow Shareholders

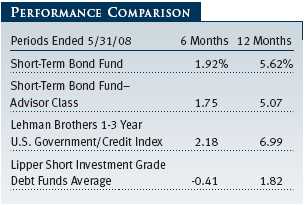

Short-term bonds produced decent returns during the 6- and 12-month periods ended May 31, 2008—periods in which investors fled from riskier securities to the safer haven of high-quality securities. In this environment, Treasuries outperformed other fixed-income classes. Interest rates declined over the past 12 months, although shorter-term yields were relatively stable during the second half of your fund’s fiscal year.

HIGHLIGHTS

• Short-term bonds performed relatively well in an environment characterized by an aversion to risk and a flight to quality.

• The fund’s return lagged the performance of the Lehman Brothers index but surpassed that of our Lipper peer group average in both periods.

• Our underweight in Treasuries was a detriment to relative performance versus the benchmark index, but our overall strategy aided results within our peer group.

• The Fed could begin raising short-term rates by the end of the year to combat nagging inflation, but our portfolio of shorter-term securities is less vulnerable to interest rate fluctuations than one composed of long-term bonds.

MARKET ENVIRONMENT

The relentless march of crude oil prices to record highs fueled deepening concerns about inflation on the part of investors and policymakers. Large increases in gasoline and food prices, along with the swooning U.S. dollar, were paramount on investors’ minds during the fund’s fiscal year. The danger existed that expectations could become reality as consumers demanded higher wages to offset price increases, helping to spur an inflationary spiral.

Bond investors worried in particular about the implications for monetary policy. Federal Reserve Chairman Ben Bernanke released a statement near the end of the period, reiterating that he expected “somewhat better economic conditions” by the end of the year. As though on cue, the Department of Labor reported that the number of Americans applying for unemployment benefits declined 18,000 to 357,000—the lowest level since mid-April. In addition, retailers reported solid results in May, reflecting stronger consumer demand. The news was not all good, however. Unemployment spiked in May from 5.0% to 5.5%, the largest monthly increase in 22 years. The most dramatic news was the price of a barrel of oil, which jumped $11 in a single day to an all-time high of around $139 during the first week of June.

So far, the economy has avoided slipping into an outright recession, although gross domestic product growth has been tepid at best. The sluggish economy, combined with troubling data on the inflation front, puts the nation’s central bank in a quandary. Until recently, the Fed has been vigorously lowering short-term rates to stimulate the economy, but it is likely to turn its attention to fighting inflation as the economy gathers strength—as Bernanke expects—in the months ahead.

PERFORMANCE

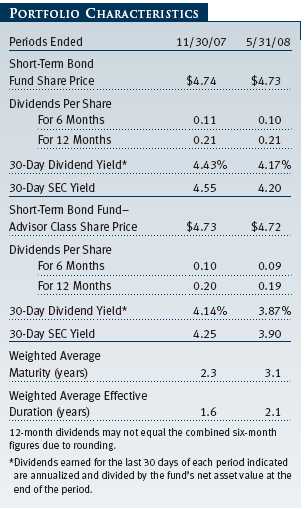

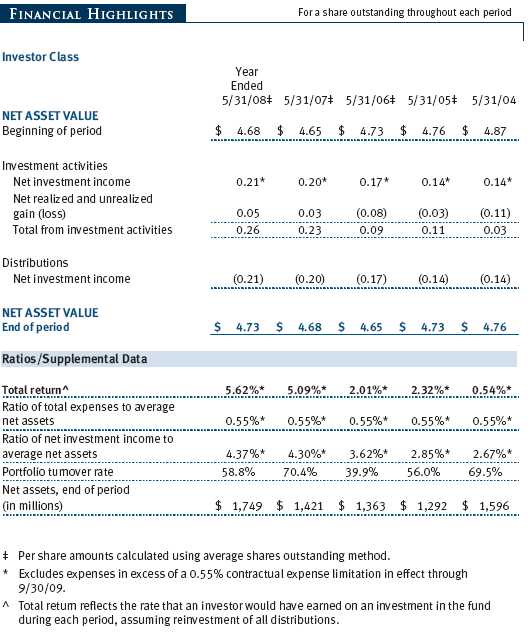

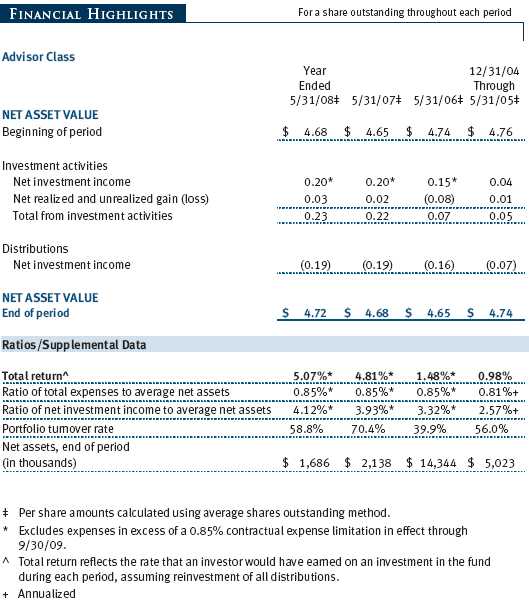

Your fund generated a modest gain over the six months ended May 31, 2008, trailing the Lehman Brothers 1-3 Year U.S. Government/Credit Index but surpassing the Lipper peer group average. Our shortfall versus the Lehman Brothers index was due primarily to our underweight in Treasuries versus the index. During the past 12 months, the fund generated a good return with the same relative results. The fund’s net asset value rose from $4.68 at the end of May 2007 to $4.73 at the end of the current period, and dividends contributed $0.21 per share. (Performance for the Advisor Class shares was lower than the fund’s, reflecting their higher expense ratio; net asset value and dividends were also different.) As we have stated in the past, the objective of the fund is to provide greater income than is available from a money market fund, but with a higher degree of principal risk.

During the past six months, we initially maintained fairly high cash levels to take advantage of opportunities to buy securities on weakness. An opportunity presented itself in February, when the municipal market weakened because of reduced demand and liquidity brought on by turmoil in the auction-rate market and by difficulties faced by monoline insurers. With increased supply and generally favorable fundamentals, municipals offered compelling values relative to taxable bonds. As a result, we initiated exposure to this segment of the market, and we were fortunate to benefit when municipal bonds rallied a month later. At that time, we reduced our exposure to them in the face of their strong performance.

In March, we began to increase our exposure to corporate securities, adding to financial institutions that we believe will withstand additional turmoil in the markets. In addition, we saw a chance to increase the overall yield of the portfolio by beefing up our allotment of mortgage-backed, asset-backed, and commercial mortgage-backed securities, none of which are held in the benchmark. Because of dislocations in the market, we were able to add to our securitized positions on weakness at what appeared to be attractive yield levels. This strategy worked against us, since the flight to quality that occurred halfway through the period had a negative impact on the group and weighed on performance.

From April to May, the market reversed when improved investor sentiment, inflation concerns, and expectations that the Federal Reserve’s easing cycle was nearing an end led investors away from U.S. Treasuries and into higher-risk asset classes. As a result, lower-quality bonds outperformed Treasuries in April, boosting fund results because we remained underweight in Treasuries and overweight in higher-yielding sectors. Collateralized mortgage-backed securities did particularly well.

For the fund’s full fiscal year, the story was similar, dominated as it was by the prevailing flight to quality. Our strategic underweight in Treasuries, coupled with our exposure to higher-yielding segments of the fixed-income market, detracted on a relative basis from returns versus the index—although performance far outpaced that of the Lipper peer group, as mentioned. In May, the fund’s significant position in asset-backed securities contributed positively to relative returns as investor sentiment improved.

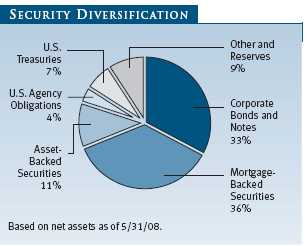

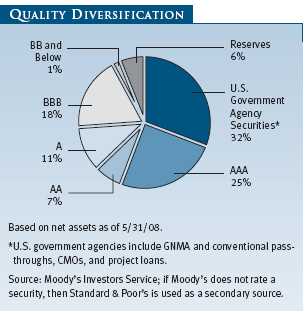

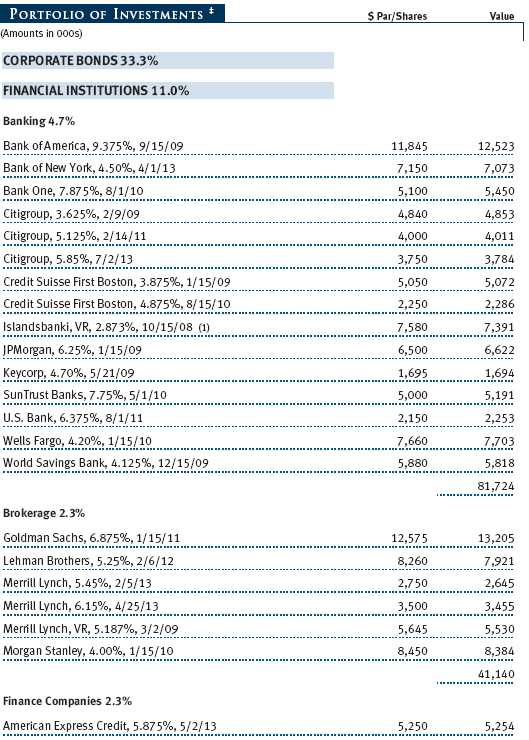

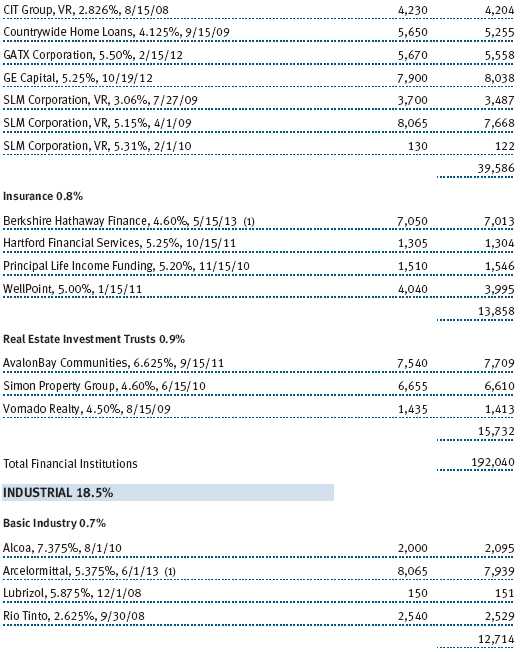

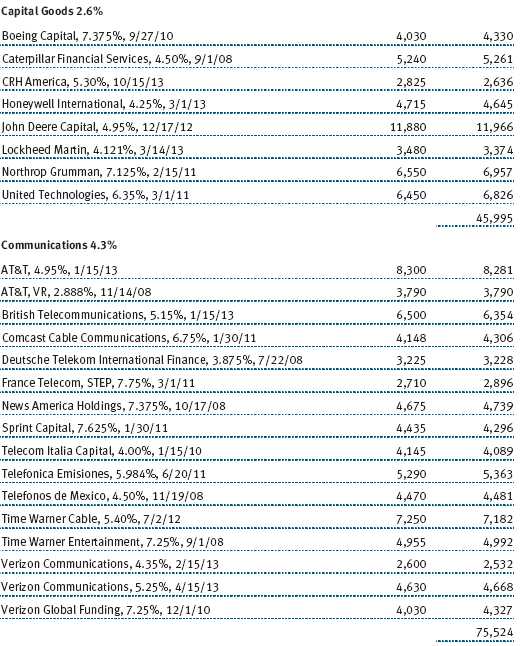

At the end of May, 36% of the portfolio was allocated to mortgage-backed securities; 33% to corporate bonds and notes; 11% to asset-backed securities; and the remaining 20% to U.S. agency obligations, U.S. Treasuries, other securities, and reserves. Only 18% of the portfolio was invested in BBB securities (the lowest end of the investment-grade range) and 1% in BB bonds, while 6% was in cash reserves, and 75% was rated A or higher.

OUTLOOK

The last few months have been marked by aggressive actions from the Federal Reserve and broad-based and successful recapitalization among U.S. banks and brokerage firms, which leads us to believe that the worst of the financial crisis is behind us. Currently, inflation issues—mainly driven by recent spikes in commodity prices—have moved to the forefront on a global scale.

Despite worries over inflation expectations, the Fed may be reluctant to raise interest rates before the housing market has stabilized and employment growth has resumed. Futures contracts currently indicate that investors expect the Fed to begin raising interest rates before the end of the year, but this may be premature. Fortunately, our segment of the market, which encompasses bonds with shorter-term maturities, should not be affected to the same extent as long-term bonds, which are more susceptible to changes in interest rates.

As always, we will continue to monitor bond market conditions closely and look for investment opportunities as they become available.

Thank you for investing with T. Rowe Price.

Respectfully submitted,

Edward A. Wiese

President and chairman of the fund’s Investment Advisory Committee

June 16, 2008

The committee chairman has day-to-day responsibility for managing the portfolio and works with committee members in developing and executing the fund’s investment program.

RISKS OF FIXED-INCOME INVESTING

Bonds are subject to interest rate risk (the decline in bond prices that usually accompanies a rise in interest rates) and credit risk (the chance that any fund holding could have its credit rating downgraded or that a bond issuer will default by failing to make timely payments of interest or principal), potentially reducing the fund’s income level and share price. Mortgage-backed securities are subject to prepayment risk, particularly if falling rates lead to heavy refinancing activity, and extension risk, which is an increase in interest rates that causes a fund’s average maturity to lengthen unexpectedly due to a drop in mortgage prepayments. This could increase the fund’s sensitivity to rising interest rates and its potential for price declines.

GLOSSARY

Duration: A measure of a bond fund’s sensitivity to changes in interest rates. For example, a fund with a duration of two years would fall about 2% in price in response to a one-percentage-point rise in interest rates, and vice versa.

Fed funds rate: The interest rate charged on overnight loans of reserves by one financial institution to another in the United States. The Federal Reserve sets a target federal funds rate to affect the direction of interest rates.

Lehman Brothers 1-3 Year U.S. Government/Credit Index: A total return index that incorporates all bonds in both the Treasury Bond Index and the Agency Bond Index, as well as U.S. corporate and some foreign debentures and secured notes, with maturities of one to three years.

Lipper averages: The averages of available mutual fund performance returns for specified time periods in defined categories as tracked by Lipper Inc.

30-day SEC yield: A method of calculating a fund’s yield that assumes all portfolio securities are held until maturity. The Securities and Exchange Commission (SEC) requires all bond funds to calculate this yield. Yield will vary and is not guaranteed.

Performance and Expenses

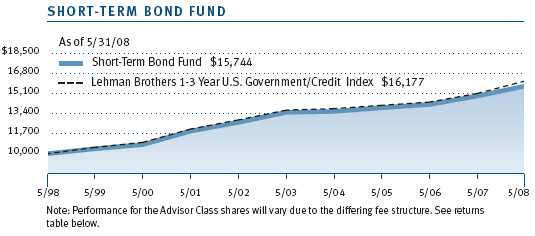

| GROWTH OF $10,000 |

This chart shows the value of a hypothetical $10,000 investment in the fund over the past 10 fiscal year periods or since inception (for funds lacking 10-year records). The result is compared with benchmarks, which may include a broad-based market index and a peer group average or index. Market indexes do not include expenses, which are deducted from fund returns as well as mutual fund averages and indexes.

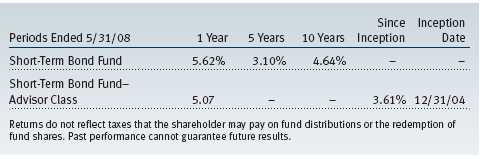

| AVERAGE ANNUAL COMPOUND TOTAL RETURN |

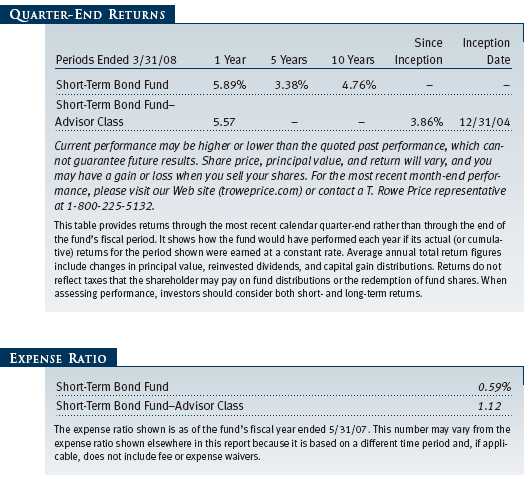

This table shows how the fund would have performed each year if its actual (or cumulative) returns for the periods shown had been earned at a constant rate.

| FUND EXPENSE EXAMPLE |

As a mutual fund shareholder, you may incur two types of costs: (1) transaction costs, such as redemption fees or sales loads, and (2) ongoing costs, including management fees, distribution and service (12b-1) fees, and other fund expenses. The following example is intended to help you understand your ongoing costs (in dollars) of investing in the fund and to compare these costs with the ongoing costs of investing in other mutual funds. The example is based on an investment of $1,000 invested at the beginning of the most recent six-month period and held for the entire period.

Please note that the fund has two share classes: The original share class (“investor class”) charges no distribution and service (12b-1) fee. Advisor Class shares are offered only through unaffiliated brokers and other financial intermediaries and charge a 0.25% 12b-1 fee. Each share class is presented separately in the table.

Actual Expenses

The first line of the following table (“Actual”) provides information about actual account values and expenses based on the fund’s actual returns. You may use the information in this line, together with your account balance, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number in the first line under the heading “Expenses Paid During Period” to estimate the expenses you paid on your account during this period.

Hypothetical Example for Comparison Purposes

The information on the second line of the table (“Hypothetical”) is based on hypothetical account values and expenses derived from the fund’s actual expense ratio and an assumed 5% per year rate of return before expenses (not the fund’s actual return). You may compare the ongoing costs of investing in the fund with other funds by contrasting this 5% hypothetical example and the 5% hypothetical examples that appear in the shareholder reports of the other funds. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period.

Note: T. Rowe Price charges an annual small-account maintenance fee of $10, generally for accounts with less than $2,000 ($500 for UGMA/UTMA). The fee is waived for any investor whose T. Rowe Price mutual fund accounts total $25,000 or more, accounts employing automatic investing, and IRAs and other retirement plan accounts that utilize a prototype plan sponsored by T. Rowe Price (although a separate custodial or administrative fee may apply to such accounts). This fee is not included in the accompanying table. If you are subject to the fee, keep it in mind when you are estimating the ongoing expenses of investing in the fund and when comparing the expenses of this fund with other funds.

You should also be aware that the expenses shown in the table highlight only your ongoing costs and do not reflect any transaction costs, such as redemption fees or sales loads. Therefore, the second line of the table is useful in comparing ongoing costs only and will not help you determine the relative total costs of owning different funds. To the extent a fund charges transaction costs, however, the total cost of owning that fund is higher.

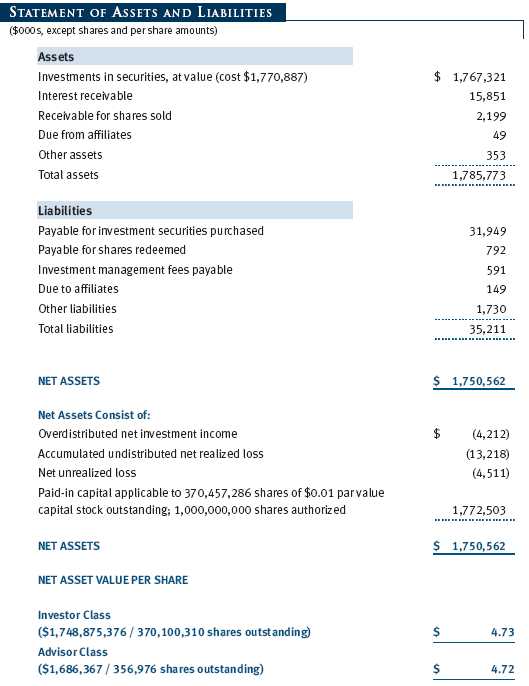

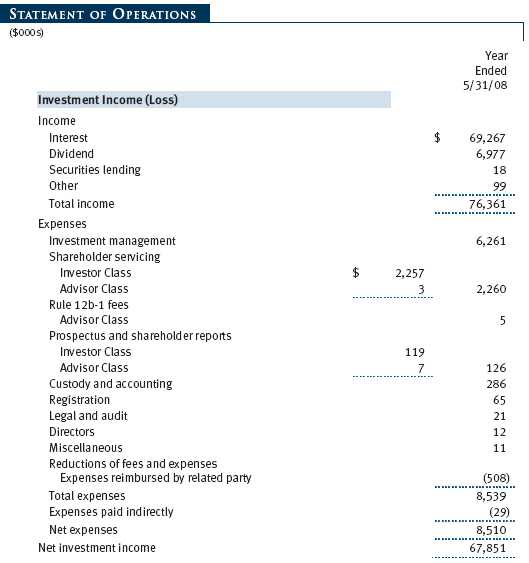

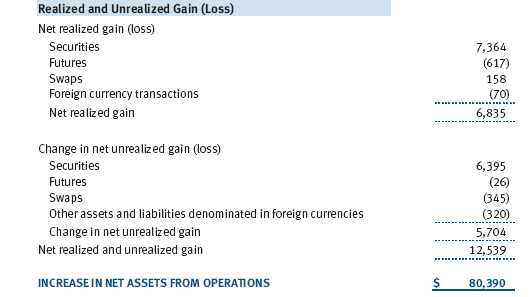

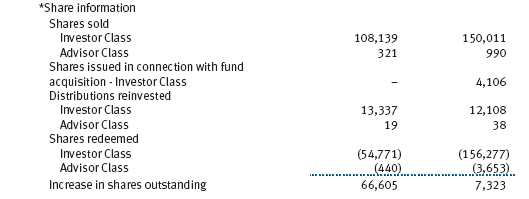

The accompanying notes are an integral part of these financial statements.

The accompanying notes are an integral part of these financial statements.

The accompanying notes are an integral part of these financial statements.

The accompanying notes are an integral part of these financial statements.

The accompanying notes are an integral part of these financial statements.

The accompanying notes are an integral part of these financial statements.

| NOTES TO FINANCIAL STATEMENTS |

T. Rowe Price Short-Term Bond Fund, Inc. (the fund), is registered under the Investment Company Act of 1940 (the 1940 Act) as a diversified, open-end management investment company. The fund seeks a high level of income consistent with minimal fluctuation in principal value and liquidity. The fund has two classes of shares: the Short-Term Bond Fund original share class, referred to in this report as the Investor Class, offered since March 2, 1984, and Short-Term Bond Fund—Advisor Class (Advisor Class), offered since December 31, 2004. Advisor Class shares are sold only through unaffiliated brokers and other unaffiliated financial intermediaries that are compensated by the class for distribution, shareholder servicing, and/or certain administrative services under a Board-approved Rule 12b-1 plan. Each class has exclusive voting rights on matters related solely to that class, separate voting rights on matters that relate to both classes, and, in all other respects, the same rights and obligations as the other class.

NOTE 1 - SIGNIFICANT ACCOUNTING POLICIES

Basis of Preparation The accompanying financial statements were prepared in accordance with accounting principles generally accepted in the United States of America, which require the use of estimates made by fund management. Fund management believes that estimates and security valuations are appropriate; however, actual results may differ from those estimates, and the security valuations reflected in the financial statements may differ from the value the fund ultimately realizes upon sale of the securities.

Investment Transactions, Investment Income, and Distributions Income and expenses are recorded on the accrual basis. Premiums and discounts on debt securities are amortized for financial reporting purposes. Inflation adjustments to the principal amount of inflation-indexed bonds are reflected as interest income. Dividends received from mutual fund investments are reflected as dividend income; capital gain distributions are reflected as realized gain/loss. Dividend income and capital gain distributions are recorded on the ex-dividend date. Income tax-related interest and penalties, if incurred, would be recorded as income tax expense. Investment transactions are accounted for on the trade date. Realized gains and losses are reported on the identified cost basis. Payments (“variation margin”) made or received to settle the daily fluctuations in the value of futures contracts are recorded as unrealized gains or losses until the contracts are closed. Unrealized gains and losses on forward currency exchange contracts are reflected as the change in net unrealized gain or loss in the accompanying financial statements. Net periodic receipts or payments required by swaps are accrued daily and recorded as realized gain or loss in the accompanying financial statements. Fluctuations in the fair value of swaps are reflected in the change in net unrealized gain or loss and are reclassified to realized gain or loss upon termination prior to maturity. Paydown gains and losses are recorded as an adjustment to interest income. Distributions to shareholders are recorded on the ex-dividend date. Income distributions are declared by each class on a daily basis and paid monthly. Capital gain distributions, if any, are declared and paid by the fund, typically on an annual basis.

Currency Translation Assets, including investments, and liabilities denominated in foreign currencies are translated into U.S. dollar values each day at the prevailing exchange rate, using the mean of the bid and asked prices of such currencies against U.S. dollars as quoted by a major bank. Purchases and sales of securities, income, and expenses are translated into U.S. dollars at the prevailing exchange rate on the date of the transaction. The effect of changes in foreign currency exchange rates on realized and unrealized security gains and losses is reflected as a component of security gains and losses.

Class Accounting The Advisor Class pays distribution, shareholder servicing, and/or certain administrative expenses in the form of Rule 12b-1 fees, in an amount not exceeding 0.25% of the class’s average daily net assets. Shareholder servicing, prospectus, and shareholder report expenses incurred by each class are charged directly to the class to which they relate. Expenses common to both classes and investment income are allocated to the classes based upon the relative daily net assets of each class’s settled shares; realized and unrealized gains and losses are allocated based upon the relative daily net assets of each class’s outstanding shares.

Credits The fund earns credits on temporarily uninvested cash balances at the custodian that reduce the fund’s custody charges. Custody expense in the accompanying financial statements is presented before reduction for credits, which are reflected as expenses paid indirectly.

New Accounting Pronouncements Effective November 30, 2007, the fund adopted Financial Accounting Standards Board (FASB) Interpretation No. 48 (FIN 48),Accounting for Uncertainty in Income Taxes, a clarification of FASB Statement No. 109, Accounting for Income Taxes. FIN 48 establishes financial accounting and disclosure requirements for recognition and measurement of tax positions taken or expected to be taken on an income tax return. The adoption of FIN 48 had no impact on the fund’s net assets or results of operations.

In September 2006, the Financial Accounting Standards Board (FASB) released Statement of Financial Accounting Standards No. 157 (FAS 157), Fair Value Measurements. FAS 157 defines fair value, establishes the framework for measuring fair value, and expands the disclosure of fair value measurements in the financial statements. It is effective for the fund’s fiscal year beginning June 1, 2008. Management expects adoption of FAS 157 will have no material impact on the fund’s net assets or results of operations.

In March 2008, the Financial Accounting Standards Board issued Statement of Financial Accounting Standards No. 161, Disclosures about Derivative Instruments and Hedging Activities (“FAS 161”), which is effective for fiscal years and interim periods beginning after November 15, 2008. FAS 161 requires enhanced disclosures about derivative and hedging activities, including how such activities are accounted for and their effect on financial position, performance and cash flows. Management is currently evaluating the impact the adoption of FAS 161 will have on the fund’s financial statements and related disclosures.

NOTE 2 - VALUATION

The fund values its investments and computes its net asset value per share at the close of the New York Stock Exchange (NYSE), normally 4 p.m. ET, each day that the NYSE is open for business.

Debt securities are generally traded in the over-the-counter (OTC) market. Securities with remaining maturities of one year or more at the time of acquisition are valued at prices furnished by dealers who make markets in such securities or by an independent pricing service, which considers the yield or price of bonds of comparable quality, coupon, maturity, and type, as well as prices quoted by dealers who make markets in such securities. Securities with remaining maturities of less than one year at the time of acquisition generally use amortized cost in local currency to approximate fair value. However, if amortized cost is deemed not to reflect fair value or the fund holds a significant amount of such securities with remaining maturities of more than 60 days, the securities are valued at prices furnished by dealers who make markets in such securities or by an independent pricing service.

Investments in mutual funds are valued at the mutual fund’s closing net asset value per share on the day of valuation. Forward currency exchange contracts are valued using the prevailing forward exchange rate. Swaps are valued at net present value of the contract as furnished by counterparties or by an independent pricing service.

Other investments, including restricted securities, and those for which the above valuation procedures are inappropriate or are deemed not to reflect fair value are stated at fair value as determined in good faith by the T. Rowe Price Valuation Committee, established by the fund’s Board of Directors.

For valuation purposes, the last quoted prices of non-U.S. equity securities may be adjusted under the circumstances described below. If the fund determines that developments between the close of a foreign market and the close of the NYSE will, in its judgment, materially affect the value of some or all of its portfolio securities, the fund will adjust the previous closing prices to reflect what it believes to be the fair value of the securities as of the close of the NYSE. In deciding whether it is necessary to adjust closing prices to reflect fair value, the fund reviews a variety of factors, including developments in foreign markets, the performance of U.S. securities markets, and the performance of instruments trading in U.S. markets that represent foreign securities and baskets of foreign securities. A fund may also fair value securities in other situations, such as when a particular foreign market is closed but the fund is open. The fund uses outside pricing services to provide it with closing prices and information to evaluate and/or adjust those prices. The fund cannot predict how often it will use closing prices and how often it will determine it necessary to adjust those prices to reflect fair value. As a means of evaluating its security valuation process, the fund routinely compares closing prices, the next day’s opening prices in the same markets, and adjusted prices.

NOTE 3 - INVESTMENT TRANSACTIONS

Consistent with its investment objective, the fund engages in the following practices to manage exposure to certain risks or to enhance performance. The investment objective, policies, program, and risk factors of the fund are described more fully in the fund’s prospectus and Statement of Additional Information.

Restricted Securities The fund may invest in securities that are subject to legal or contractual restrictions on resale. Prompt sale of such securities at an acceptable price may be difficult and may involve substantial delays and additional costs.

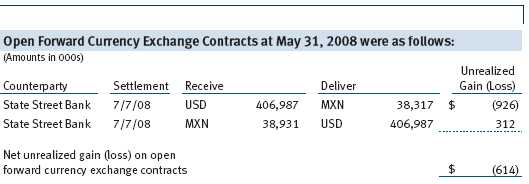

Forward Currency Exchange Contracts During the year ended May 31, 2008, the fund was a party to forward currency exchange contracts under which it is obligated to exchange currencies at specified future dates and exchange rates. Risks arise from the possible inability of counterparties to meet the terms of their agreements and from movements in currency values.

Futures Contracts During the year ended May 31, 2008, the fund was a party to futures contracts, which provide for the future sale by one party and purchase by another of a specified amount of a specific financial instrument at an agreed upon price, date, time, and place. Risks arise from possible illiquidity of the futures market and from movements in security values and/or interest rates.

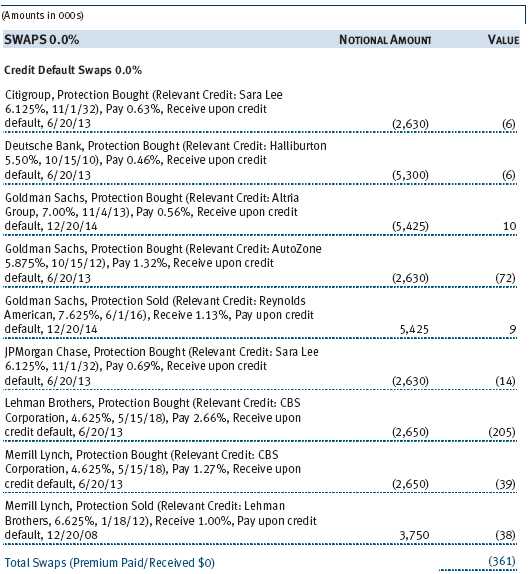

Swaps During the year ended May 31, 2008, the fund was a party to credit default swaps under which it buys or sells credit protection against a defined-issuer credit event. Upon a defined-issuer credit event, the fund is required to either deliver the notional amount of the contract in cash and take delivery of the relevant credit or deliver cash approximately equal to the notional amount of the contract less market value of the relevant credit at the time of the credit event. Risks arise from the possible inability of counterparties to meet the terms of their agreements and from changes in creditworthiness of the relevant underlying issuer. In order to mitigate counterparty risk and subject to specific contractual arrangements, the fund may receive eligible security collateral from such counterparties upon unrealized gain amounts reaching certain thresholds. Eligible security collateral generally includes debt securities issued by the U.S. government or related agencies. At May 31, 2008, no such collateral was received.

TBA Purchase Commitments During the year ended May 31, 2008, the fund entered into to be announced (TBA) purchase commitments, pursuant to which it agrees to purchase mortgage-backed securities for a fixed unit price, with payment and delivery at a scheduled future date beyond the customary settlement period for that security. With TBA transactions, the particular securities to be delivered are not identified at the trade date; however, delivered securities must meet specified terms, including issuer, rate, and mortgage term, and be within industry-accepted “good delivery” standards. The fund generally enters into TBAs with the intention of taking possession of the underlying mortgage securities. Until settlement, the fund maintains cash reserves and liquid assets sufficient to settle its TBAs.

Securities Lending The fund lends its securities to approved brokers to earn additional income. It receives as collateral cash and U.S. government securities valued at 102% to 105% of the value of the securities on loan. Cash collateral is invested by the fund’s lending agent(s) in accordance with investment guidelines approved by fund management. Although risk is mitigated by the collateral, the fund could experience a delay in recovering its securities and a possible loss of income or value if the borrower fails to return the securities or if collateral investments decline in value. Securities lending revenue recognized by the fund consists of earnings on invested collateral and borrowing fees, net of any rebates to the borrower and compensation to the lending agent. At May 31, 2008, there were no securities on loan.

Other Purchases and sales of portfolio securities, other than short-term and U.S. government securities, aggregated $408,254,000 and $266,925,000, respectively, for the year ended May 31, 2008. Purchases and sales of U.S. government securities aggregated $741,949,000 and $568,084,000, respectively, for the year ended May 31, 2008.

NOTE 4 - FEDERAL INCOME TAXES

No provision for federal income taxes is required since the fund intends to continue to qualify as a regulated investment company under Subchapter M of the Internal Revenue Code and distribute to shareholders all of its taxable income and gains. Distributions are determined in accordance with Federal income tax regulations, which differ from generally accepted accounting principles, and, therefore, may differ significantly in amount or character from net investment income and realized gains for financial reporting purposes. Financial reporting records are adjusted for permanent book/tax differences to reflect tax character but are not adjusted for temporary differences.

Reclassifications to paid-in capital relate primarily to a tax practice that treats a portion of the proceeds from each redemption of capital shares as a distribution of taxable net investment income and/or realized capital gain. Reclassifications between income and gain relate primarily to the character of paydown gains and losses on asset-backed securities. For the year ended May 31, 2008, the following reclassifications, which had no impact on results of operations or net assets, were recorded to reflect tax character:

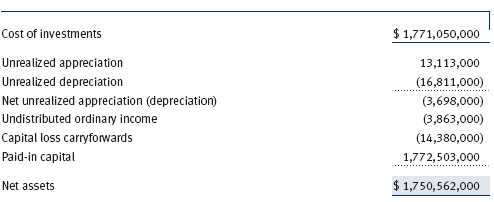

Distributions during the years ended May 31, 2008, and May 31, 2007, totaled $68,200,000 and $63,178,000, respectively, and were characterized as ordinary income for tax purposes. At May 31, 2008, the tax-basis cost of investments and components of net assets were as follows:

The fund intends to retain realized gains to the extent of available capital loss carryforwards. During the year ended May 31, 2008, the fund utilized $4,968,000 of capital loss carryforwards. As of May 31, 2008, unused capital loss carryforwards expire as follows: $117,000 in fiscal 2009, $447,000 in fiscal 2012, $4,473,000 in fiscal 2013, $6,329,000 in fiscal 2014, and $3,014,000 in fiscal 2015. Additionally, $1,544,000 of the fund’s unused capital loss carryforwards acquired through tax-free reorganizations is subject to certain limitations on amount and/or timing of use.

NOTE 5 - ACQUISITION

On June 19, 2006, the fund acquired substantially all of the assets of the Short-Term Government Security Fund (the acquired fund), pursuant to the Agreement and Plan of Reorganization dated February 15, 2006, and approved by shareholders of the acquired fund on June 9, 2006. The acquisition was accomplished by a tax-free exchange of 4,106,357 shares of the fund (with a value of $19,053,000) for all 1,980,654 shares of the acquired fund outstanding on June 16, 2006 with the same value. The net assets of the acquired fund at that date included $269,000 of unrealized depreciation and $3,052,000 of net realized losses carried forward for tax purposes to offset distributable gains realized by the fund in the future. Net assets of the acquired fund were combined with those of the fund, resulting in aggregate net assets of $1,458,228,000 immediately after the acquisition.

NOTE 6 - RELATED PARTY TRANSACTIONS

The fund is managed by T. Rowe Price Associates, Inc. (the manager or Price Associates), a wholly owned subsidiary of T. Rowe Price Group, Inc. The investment management agreement between the fund and the manager provides for an annual investment management fee, which is computed daily and paid monthly. The fee consists of an individual fund fee, equal to 0.10% of the fund’s average daily net assets, and a group fee. The group fee rate is calculated based on the combined net assets of certain mutual funds sponsored by Price Associates (the group) applied to a graduated fee schedule, with rates ranging from 0.48% for the first $1 billion of assets to 0.285% for assets in excess of $220 billion. The fund’s group fee is determined by applying the group fee rate to the fund’s average daily net assets. At May 31, 2008, the effective annual group fee rate was 0.30%.

The Investor Class and Advisor Class are also subject to a contractual expense limitation through the limitation dates indicated in the table below. During the limitation period, the manager is required to waive its management fee and/or reimburse expenses, excluding interest, taxes, brokerage commissions, and extraordinary expenses, that would otherwise cause the class’s ratio of annualized total expenses to average net assets (expense ratio) to exceed its expense limitation. For a period of three years after the date of any reimbursement or waiver, each class is required to repay the manager for expenses previously reimbursed and management fees waived to the extent the class’s net assets have grown or expenses have declined sufficiently to allow repayment without causing the class’s expense ratio to exceed its expense limitation.

Pursuant to this agreement, management fees in the amount of $172,000 were waived and expenses in the amount of $485,000 were reimbursed by the manager during the year ended May 31, 2008. Including these amounts, management fees waived and expenses previously reimbursed by the manager in the amount of $2,921,000 remain subject to repayment at May 31, 2008.

In addition, the fund has entered into service agreements with Price Associates and two wholly owned subsidiaries of Price Associates (collectively, Price). Price Associates computes the daily share prices and provides certain other administrative services to the fund. T. Rowe Price Services, Inc., provides shareholder and administrative services in its capacity as the fund’s transfer and dividend disbursing agent. T. Rowe Price Retirement Plan Services, Inc., provides subaccounting and recordkeeping services for certain retirement accounts invested in the Investor Class. For the year ended May 31, 2008, expenses incurred pursuant to these service agreements were $176,000 for Price Associates, $764,000 for T. Rowe Price Services, Inc., and $116,000 for T. Rowe Price Retirement Plan Services, Inc. The total amount payable at period-end pursuant to these service agreements is reflected as Due to Affiliates in the accompanying financial statements.

Additionally, the fund is one of several mutual funds in which certain college savings plans managed by Price Associates may invest. As approved by the fund’s Board of Directors, shareholder servicing costs associated with each college savings plan are borne by the fund in proportion to the average daily value of its shares owned by the college savings plan. For the year ended May 31, 2008, the fund was charged $315,000 for shareholder servicing costs related to the college savings plans, of which $290,000 was for services provided by Price. The amount payable at period-end pursuant to this agreement is reflected as Due to Affiliates in the accompanying financial statements. At May 31, 2008, approximately 9% of the outstanding shares of the Investor Class were held by college savings plans.

The fund is also one of several mutual funds sponsored by Price Associates (underlying Price funds) in which the T. Rowe Price Spectrum Funds (Spectrum Funds) may invest and T. Rowe Price Retirement Funds (Retirement Funds) have invested. Neither the Spectrum Funds nor the Retirement Funds invest in the underlying Price funds for the purpose of exercising management or control. Pursuant to separate special servicing agreements, expenses associated with the operation of the Spectrum and Retirement Funds are borne by each underlying Price fund to the extent of estimated savings to it and in proportion to the average daily value of its shares owned by the Spectrum and Retirement Funds, respectively. Expenses allocated under these agreements are reflected as shareholder servicing expenses in the accompanying financial statements. For the year ended May 31, 2008, the fund was allocated $643,000 of Spectrum Funds’ expenses and was reimbursed $23,000 of overaccrued Retirement Funds’ expenses. Of these amounts, $472,000 related to services provided by Price. The amount payable at period-end pursuant to this agreement is reflected as Due to Affiliates in the accompanying financial statements. At May 31, 2008, approximately 29% of the outstanding shares of the Investor Class were held by the Spectrum Funds and none were held by the Retirement Funds.

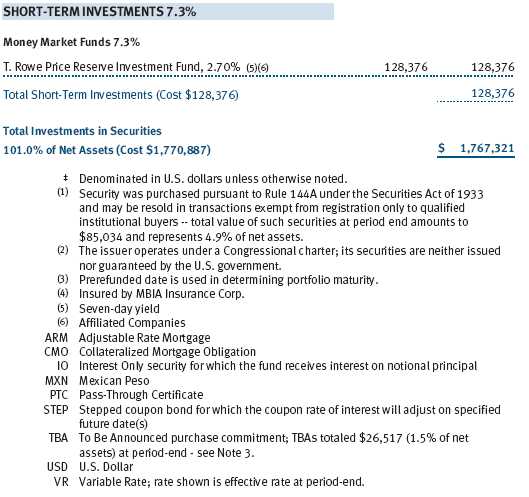

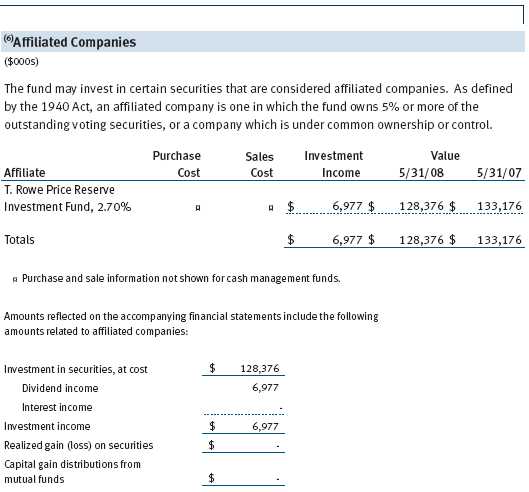

The fund may invest in the T. Rowe Price Reserve Investment Fund and the T. Rowe Price Government Reserve Investment Fund (collectively, the T. Rowe Price Reserve Investment Funds), open-end management investment companies managed by Price Associates and considered affiliates of the fund. The T. Rowe Price Reserve Investment Funds are offered as cash management options to mutual funds, trusts, and other accounts managed by Price Associates and/or its affiliates and are not available for direct purchase by members of the public. The T. Rowe Price Reserve Investment Funds pay no investment management fees.

As of May 31, 2008, T. Rowe Price Group, Inc., and/or its wholly owned subsidiaries owned 9,560,627 shares of the Investor Class, representing 3% of the fund’s net assets.

| REPORT OF INDEPENDENT REGISTERED PUBLIC ACCOUNTING FIRM |

To the Board of Directors and Shareholders of T. Rowe Price Short-Term Bond Fund, Inc.

In our opinion, the accompanying statement of assets and liabilities, including the portfolio of investments, and the related statements of operations and of changes in net assets and the financial highlights present fairly, in all material respects, the financial position of T. Rowe Price Short-Term Bond Fund, Inc. (the “Fund”) at May 31, 2008, the results of its operations for the year then ended, the changes in its net assets for each of the two years in the period then ended and the financial highlights for each of the fiscal periods presented, in conformity with accounting principles generally accepted in the United States of America. These financial statements and financial highlights (hereafter referred to as “financial statements”) are the responsibility of the Fund’s management; our responsibility is to express an opinion on these financial statements based on our audits. We conducted our audits of these financial statements in accordance with the auditing standards of the Public Company Accounting Oversight Board (United States). Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free of material misstatement. An audit includes examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements, assessing the accounting principles used and significant estimates made by management, and evaluating the overall financial statement presentation. We believe that our audits, which included confirmation of securities at May 31, 2008 by correspondence with the custodian and brokers, and confirmation of the underlying fund by correspondence with the transfer agent, provide a reasonable basis for our opinion.

PricewaterhouseCoopers LLP

Baltimore, Maryland

July 11, 2008

| TAX INFORMATION (UNAUDITED) FOR THE TAX YEAR ENDED 5/31/08 |

We are providing this information as required by the Internal Revenue Code. The amounts shown may differ from those elsewhere in this report because of differences between tax and financial reporting requirements.

The fund’s distributions to shareholders included $112,000 from short-term capital gains.

| INFORMATION ON PROXY VOTING POLICIES, PROCEDURES, AND RECORDS |

A description of the policies and procedures used by T. Rowe Price funds and portfolios to determine how to vote proxies relating to portfolio securities is available in each fund’s Statement of Additional Information, which you may request by calling 1-800-225-5132 or by accessing the SEC’s Web site, www.sec.gov. The description of our proxy voting policies and procedures is also available on our Web site, www.troweprice.com. To access it, click on the words “Company Info” at the top of our homepage for individual investors. Then, in the window that appears, click on the “Proxy Voting Policy” navigation button in the top left corner.

Each fund’s most recent annual proxy voting record is available on our Web site and through the SEC’s Web site. To access it through our Web site, follow the directions above, then click on the words “Proxy Voting Record” at the bottom of the Proxy Voting Policy page.

| HOW TO OBTAIN QUARTERLY PORTFOLIO HOLDINGS |

The fund files a complete schedule of portfolio holdings with the Securities and Exchange Commission for the first and third quarters of each fiscal year on Form N-Q. The fund’s Form N-Q is available electronically on the SEC’s Web site (www.sec.gov); hard copies may be reviewed and copied at the SEC’s Public Reference Room, 450 Fifth St. N.W., Washington, DC 20549. For more information on the Public Reference Room, call 1-800-SEC-0330.

| APPROVAL OF INVESTMENT MANAGEMENT AGREEMENT |

On March 4, 2008, the fund’s Board of Directors (Board) unanimously approved the investment advisory contract (Contract) between the fund and its investment manager, T. Rowe Price Associates, Inc. (Manager). The Board considered a variety of factors in connection with its review of the Contract, also taking into account information provided by the Manager during the course of the year, as discussed below:

Services Provided by the Manager

The Board considered the nature, quality, and extent of the services provided to the fund by the Manager. These services included, but were not limited to, management of the fund’s portfolio and a variety of related activities, as well as financial and administrative services, reporting, and communications. The Board also reviewed the background and experience of the Manager’s senior management team and investment personnel involved in the management of the fund. The Board concluded that it was satisfied with the nature, quality, and extent of the services provided by the Manager.

Investment Performance of the Fund

The Board reviewed the fund’s average annual total returns over the 1-, 3-, 5-, and 10-year periods as well as the fund’s year-by-year returns and compared these returns with a wide variety of previously agreed upon comparable performance measures and market data, including those supplied by Lipper and Morningstar, which are independent providers of mutual fund data. On the basis of this evaluation and the Board’s ongoing review of investment results, the Board concluded that the fund’s performance was satisfactory.

Costs, Benefits, Profits, and Economies of Scale

The Board reviewed detailed information regarding the revenues received by the Manager under the Contract and other benefits that the Manager (and its affiliates) may have realized from its relationship with the fund, including research received under “soft dollar” agreements. The Board noted that soft dollars were not used to pay for third-party, non-broker research. The Board also received information on the estimated costs incurred and profits realized by the Manager and its affiliates from advising T. Rowe Price mutual funds, as well as estimates of the gross profits realized from managing the fund in particular. The Board concluded that the Manager’s profits were reasonable in light of the services provided to the fund. The Board also considered whether the fund or other funds benefit under the fee levels set forth in the Contract from any economies of scale realized by the Manager. Under the Contract, the fund pays a fee to the Manager composed of two components—a group fee rate based on the aggregate assets of certain T. Rowe Price mutual funds (including the fund) that declines at certain asset levels and an individual fund fee rate that is assessed on the assets of the fund. The Board concluded that the advisory fee structure for the fund continued to provide for a reasonable sharing of benefits from economies of scale with the fund’s investors.

Fees

The Board reviewed the fund’s management fee rate, operating expenses, and total expense ratio (for both the Investor Class and Advisor Class) and compared them with fees and expenses of other comparable funds based on information and data supplied by Lipper. The information provided to the Board showed that the fund’s management fee (including any applicable fee waivers or expenses paid by the Manager or reimbursements by the fund) was above the median for certain groups of comparable funds but at or below the median for other groups of comparable funds. The information also showed that the fund’s expense ratio for the Investor Class was above the median for certain groups of comparable funds but below the median for other groups of funds, and that the fund’s expense ratio for the Advisor Class was at or below the median for comparable funds. The Board also reviewed the fee schedules for comparable privately managed accounts of the Manager and its affiliates. Management informed the Board that the Manager’s responsibilities for privately managed accounts are more limited than its responsibilities for the fund and other T. Rowe Price mutual funds that it or its affiliates advise. On the basis of the information provided, the Board concluded that the fees paid by the fund under the Contract were reasonable.

Approval of the Contract

As noted, the Board approved the continuation of the Contract. No single factor was considered in isolation or to be determinative to the decision. Rather, the Board concluded, in light of a weighting and balancing of all factors considered, that it was in the best interests of the fund to approve the continuation of the Contract, including the fees to be charged for services thereunder.

| ABOUT THE FUND’S DIRECTORS AND OFFICERS |

Your fund is governed by a Board of Directors (Board) that meets regularly to review a wide variety of matters affecting the fund, including performance, investment programs, compliance matters, advisory fees and expenses, service providers, and other business affairs. The Board elects the fund’s officers, who are listed in the final table. At least 75% of Board members are independent of T. Rowe Price Associates, Inc. (T. Rowe Price), and T. Rowe Price International, Inc. (T. Rowe Price International); “inside” or “interested” directors are employees or officers of T. Rowe Price. The business address of each director and officer is 100 East Pratt Street, Baltimore, Maryland 21202. The Statement of Additional Information includes additional information about the fund directors and is available without charge by calling a T. Rowe Price representative at 1-800-225-5132.

| Independent Directors | |

| Name | |

| (Year of Birth) | Principal Occupation(s) During Past Five Years and Directorships of |

| Year Elected* | Other Public Companies |

| Jeremiah E. Casey | Director, National Life Insurance (2001 to 2005); Director, The Rouse |

| (1940) | Company, real estate developers (1990 to 2004) |

| 2006 | |

| Anthony W. Deering | Chairman, Exeter Capital, LLC, a private investment firm (2004 to |

| (1945) | present); Director, Vornado Real Estate Investment Trust (3/04 to |

| 1983 | present); Director, Mercantile Bankshares (2002 to 2007); Member, |

| Advisory Board, Deutsche Bank North America (2004 to present); | |

| Director, Chairman of the Board, and Chief Executive Officer, The | |

| Rouse Company, real estate developers (1997 to 2004) | |

| Donald W. Dick, Jr. | Principal, EuroCapital Advisors, LLC, an acquisition and management |

| (1943) | advisory firm (10/95 to present); Chairman, The Haven Group, a cus- |

| 2001 | tom manufacturer of modular homes (1/04 to present) |

| David K. Fagin | Chairman and President, Nye Corporation (6/88 to present); Chair- |

| (1938) | man, Canyon Resources Corp. (8/07 to 3/08); Director, Golden Star |

| 2001 | Resources Ltd. (5/92 to present); Director, Pacific Rim Mining Corp. |

| (2/02 to present); Director, B.C. Corporation (3/08 to present) | |

| Karen N. Horn | Director, Federal National Mortgage Association (9/06 to present); |

| (1943) | Director, Norfolk Southern (2/08 to present); Director, Eli Lilly and |

| 2003 | Company (1987 to present); Director, Simon Property Group (2004 |

| to present); Managing Director and President, Global Private Client | |

| Services, Marsh Inc. (1999 to 2003); Director, Georgia Pacific (5/04 | |

| to 12/05) | |

| Theo C. Rodgers | President, A&R Development Corporation (1977 to present) |

| (1941) | |

| 2005 | |

| John G. Schreiber | Owner/President, Centaur Capital Partners, Inc., a real estate invest- |

| (1946) | ment company (1991 to present); Partner, Blackstone Real Estate |

| 1992 | Advisors, L.P. (10/92 to present) |

| *Each independent director oversees 123 T. Rowe Price portfolios and serves until retirement, resignation, | |

| or election of a successor. | |

| Inside Directors | |

| Name | |

| (Year of Birth) | |

| Year Elected* | |

| [Number of T. Rowe Price | Principal Occupation(s) During Past Five Years and Directorships of |

| Portfolios Overseen] | Other Public Companies |

| Edward C. Bernard | Director and Vice President, T. Rowe Price; Vice Chairman of the Board, |

| (1956) | Director, and Vice President, T. Rowe Price Group, Inc.; Chairman of |

| 2006 | the Board, Director, and President, T. Rowe Price Investment Services, |

| [123] | Inc.; Chairman of the Board and Director, T. Rowe Price Global Asset |

| Management Limited, T. Rowe Price Global Investment Services | |

| Limited, T. Rowe Price Retirement Plan Services, Inc., T. Rowe Price | |

| Savings Bank, and T. Rowe Price Services, Inc.; Director, T. Rowe Price | |

| International, Inc.; Chief Executive Officer, Chairman of the Board, | |

| Director, and President, T. Rowe Price Trust Company; Chairman of | |

| the Board, all funds | |

| Mary J. Miller, CFA | Director, T. Rowe Price Trust Company; Director and Vice President, |

| (1955) | T. Rowe Price; Vice President, T. Rowe Price Group, Inc. |

| 2004 | |

| [38] | |

| *Each inside director serves until retirement, resignation, or election of a successor. | |

| Officers | |

| Name (Year of Birth) | |

| Title and Fund(s) Served | Principal Occupation(s) |

| Brian J. Brennan, CFA (1964) | Vice President, T. Rowe Price, T. Rowe Price |

| Vice President, Short-Term Bond Fund | Group, Inc., and T. Rowe Price Trust Company |

| Steven G. Brooks, CFA (1954) | Vice President, T. Rowe Price and T. Rowe Price |

| Vice President, Short-Term Bond Fund | Group, Inc. |

| Bridget A. Ebner (1970) | Vice President, T. Rowe Price |

| Assistant Vice President, Short-Term | |

| Bond Fund | |

| Roger L. Fiery III, CPA (1959) | Vice President, T. Rowe Price, T. Rowe Price |

| Vice President, Short-Term Bond Fund | Group, Inc., T. Rowe Price International, Inc., |

| and T. Rowe Price Trust Company | |

| John R. Gilner (1961) | Chief Compliance Officer and Vice President, |

| Chief Compliance Officer, Short-Term | T. Rowe Price; Vice President, T. Rowe Price |

| Bond Fund | Group, Inc., and T. Rowe Price Investment |

| Services, Inc. | |

| Gregory S. Golczewski (1966) | Vice President, T. Rowe Price and T. Rowe Price |

| Vice President, Short-Term Bond Fund | Trust Company |

| Michael J. Grogan, CFA (1971) | Vice President, T. Rowe Price |

| Assistant Vice President, Short-Term | |

| Bond Fund | |

| Geoffrey M. Hardin (1971) | Vice President, T. Rowe Price; formerly Invest- |

| Assistant Vice President, Short-Term | ment Analyst, Morgan Stanley’s Alternative |

| Bond Fund | Investment Partners (to 2007); Associate |

| Portfolio Manager, Smith Breeden Associates | |

| (to 2005) | |

| Charles B. Hill, CFA (1961) | Vice President, T. Rowe Price and T. Rowe Price |

| Vice President, Short-Term Bond Fund | Group, Inc. |

| Gregory K. Hinkle, CPA (1958) | Vice President, T. Rowe Price and T. Rowe |

| Treasurer, Short-Term Bond Fund | Price Group, Inc.; formerly Partner, |

| PricewaterhouseCoopers, LLP (to 2007) | |

| Keir R. Joyce, CFA (1972) | Vice President, T. Rowe Price |

| Assistant Vice President, Short-Term | |

| Bond Fund | |

| Patricia B. Lippert (1953) | Assistant Vice President, T. Rowe Price and |

| Secretary, Short-Term Bond Fund | T. Rowe Price Investment Services, Inc. |

| Andrew McCormick (1960) | Vice President, T. Rowe Price and T. Rowe Price |

| Vice President, Short-Term Bond Fund | Group, Inc.; formerly Chief Investment Officer, |

| IMPAC Mortgage Holdings (to 2006); Senior | |

| Portfolio Manager, Avenue Capital Group, and | |

| Senior Vice President, Portfolio Transactions, | |

| Federal National Mortgage Association (to 2005) | |

| Robert L. McWilliam (1970) | Vice President, T. Rowe Price; formerly Portfolio |

| Assistant Vice President, Short-Term | Manager, Sailfish Capital Partners (to 2006); |

| Bond Fund | Vice President, Merrill Lynch (to 2006) |

| Cheryl A. Mickel, CFA (1967) | Vice President, T. Rowe Price and T. Rowe Price |

| Vice President, Short-Term Bond Fund | Group, Inc. |

| David Oestreicher (1967) | Director and Vice President, T. Rowe Price |

| Vice President, Short-Term Bond Fund | Investment Services, Inc., and T. Rowe Price Trust |

| Company; Vice President, T. Rowe Price, T. Rowe | |

| Price Global Asset Management Limited, T. Rowe | |

| Price Global Investment Services Limited, | |

| T. Rowe Price Group, Inc., and T. Rowe Price | |

| International, Inc. | |

| Vernon A. Reid, Jr. (1954) | Vice President, T. Rowe Price and T. Rowe Price |

| Vice President, Short-Term Bond Fund | Group, Inc. |

| Daniel O. Shackelford, CFA (1958) | Vice President, T. Rowe Price, T. Rowe Price |

| Vice President, Short-Term Bond Fund | Group, Inc., and T. Rowe Price Trust Company |

| Julie L. Waples (1970) | Vice President, T. Rowe Price |

| Vice President, Short-Term Bond Fund | |

| John D. Wells (1960) | Vice President, T. Rowe Price, T. Rowe Price |

| Vice President, Short-Term Bond Fund | Group, Inc., and T. Rowe Price Savings Bank |

| Edward A. Wiese, CFA (1959) | Vice President, T. Rowe Price, T. Rowe Price |

| President, Short-Term Bond Fund | Group, Inc., and T. Rowe Price Trust Company; |

| Chief Investment Officer, Director, and Vice | |

| President, T. Rowe Price Savings Bank | |

| Unless otherwise noted, officers have been employees of T. Rowe Price or T. Rowe Price International | |

| for at least five years. | |

Item 2. Code of Ethics.

The registrant has adopted a code of ethics, as defined in Item 2 of Form N-CSR, applicable to its principal executive officer, principal financial officer, principal accounting officer or controller, or persons performing similar functions. A copy of this code of ethics is filed as an exhibit to this Form N-CSR. No substantive amendments were approved or waivers were granted to this code of ethics during the period covered by this report.

Item 3. Audit Committee Financial Expert.

The registrant’s Board of Directors/Trustees has determined that Ms. Karen N. Horn qualifies as an audit committee financial expert, as defined in Item 3 of Form N-CSR. Ms. Horn is considered independent for purposes of Item 3 of Form N-CSR.

Item 4. Principal Accountant Fees and Services.

(a) – (d) Aggregate fees billed to the registrant for the last two fiscal years for professional services rendered by the registrant’s principal accountant were as follows:

Audit fees include amounts related to the audit of the registrant’s annual financial statements and services normally provided by the accountant in connection with statutory and regulatory filings. Audit-related fees include amounts reasonably related to the performance of the audit of the registrant’s financial statements and specifically include the issuance of a report on internal controls and, if applicable, agreed-upon procedures related to fund acquisitions. Tax fees include amounts related to services for tax compliance, tax planning, and tax advice. The nature of these services specifically includes the review of distribution calculations and the preparation of Federal, state, and excise tax returns. All other fees include the registrant’s pro-rata share of amounts for agreed-upon procedures in conjunction with service contract approvals by the registrant’s Board of Directors/Trustees.

(e)(1) The registrant’s audit committee has adopted a policy whereby audit and non-audit services performed by the registrant’s principal accountant for the registrant, its investment adviser, and any entity controlling, controlled by, or under common control with the investment adviser that provides ongoing services to the registrant require pre-approval in advance at regularly scheduled audit committee meetings. If such a service is required between regularly scheduled audit committee meetings, pre-approval may be authorized by one audit committee member with ratification at the next scheduled audit committee meeting. Waiver of pre-approval for audit or non-audit services requiring fees of a de minimis amount is not permitted.

(2) No services included in (b) – (d) above were approved pursuant to paragraph (c)(7)(i)(C) of Rule 2-01 of Regulation S-X.

(f) Less than 50 percent of the hours expended on the principal accountant’s engagement to audit the registrant’s financial statements for the most recent fiscal year were attributed to work performed by persons other than the principal accountant’s full-time, permanent employees.

(g) The aggregate fees billed for the most recent fiscal year and the preceding fiscal year by the registrant’s principal accountant for non-audit services rendered to the registrant, its investment adviser, and any entity controlling, controlled by, or under common control with the investment adviser that provides ongoing services to the registrant were $1,529,000 and $1,201,000, respectively, and were less than the aggregate fees billed for those same periods by the registrant’s principal accountant for audit services rendered to the T. Rowe Price Funds.

(h) All non-audit services rendered in (g) above were pre-approved by the registrant’s audit committee. Accordingly, these services were considered by the registrant’s audit committee in maintaining the principal accountant’s independence.

Item 5. Audit Committee of Listed Registrants.

Not applicable.

Item 6. Investments.

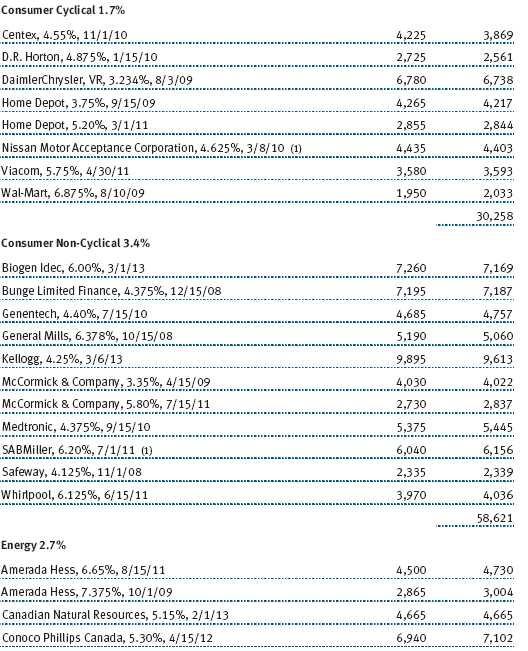

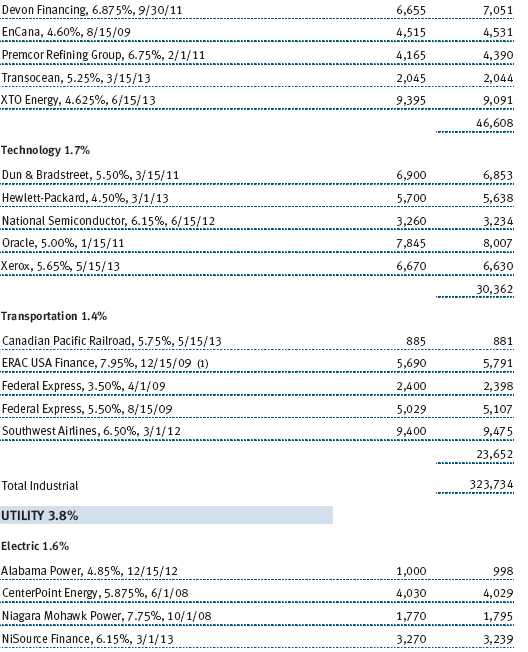

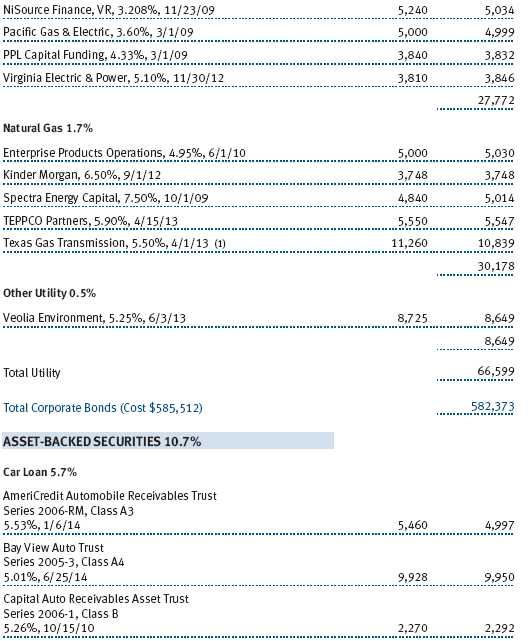

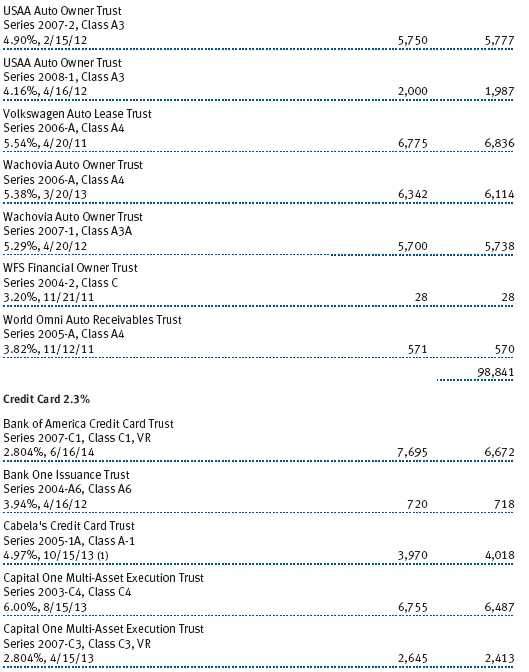

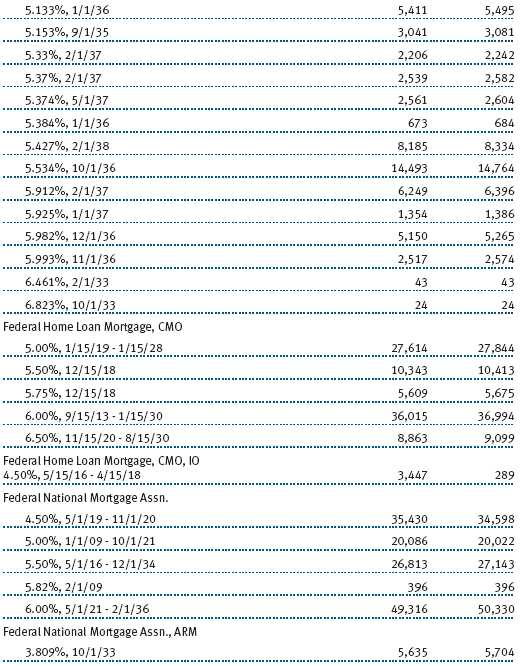

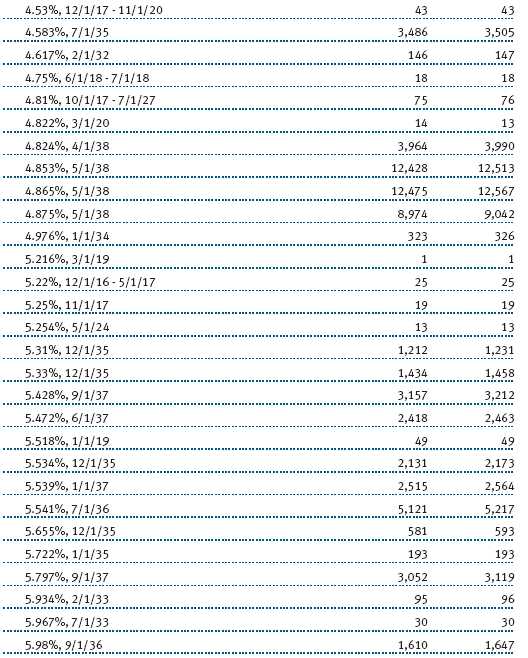

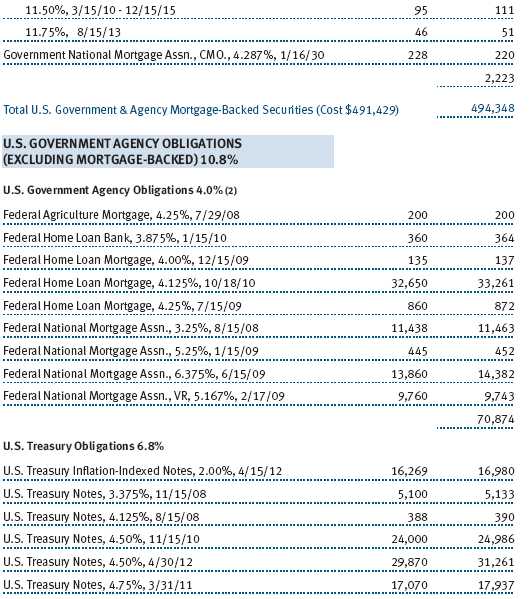

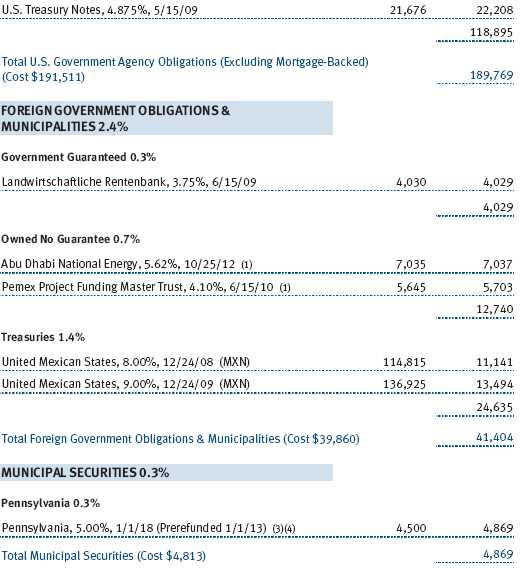

(a) Not applicable. The complete schedule of investments is included in Item 1 of this Form N-CSR.

(b) Not applicable.

Item 7. Disclosure of Proxy Voting Policies and Procedures for Closed-End Management Investment Companies.

Not applicable.

Item 8. Portfolio Managers of Closed-End Management Investment Companies.

Not applicable.

Item 9. Purchases of Equity Securities by Closed-End Management Investment Company and Affiliated Purchasers.

Not applicable.

Item 10. Submission of Matters to a Vote of Security Holders.

Not applicable.

Item 11. Controls and Procedures.

(a) The registrant’s principal executive officer and principal financial officer have evaluated the registrant’s disclosure controls and procedures within 90 days of this filing and have concluded that the registrant’s disclosure controls and procedures were effective, as of that date, in ensuring that information required to be disclosed by the registrant in this Form N-CSR was recorded, processed, summarized, and reported timely.

(b) The registrant’s principal executive officer and principal financial officer are aware of no change in the registrant’s internal control over financial reporting that occurred during the registrant’s second fiscal quarter covered by this report that has materially affected, or is reasonably likely to materially affect, the registrant’s internal control over financial reporting.

Item 12. Exhibits.

(a)(1) The registrant’s code of ethics pursuant to Item 2 of Form N-CSR is attached.

(2) Separate certifications by the registrant's principal executive officer and principal financial officer, pursuant to Section 302 of the Sarbanes-Oxley Act of 2002 and required by Rule 30a-2(a) under the Investment Company Act of 1940, are attached.

(3) Written solicitation to repurchase securities issued by closed-end companies: not applicable.

(b) A certification by the registrant's principal executive officer and principal financial officer, pursuant to Section 906 of the Sarbanes-Oxley Act of 2002 and required by Rule 30a-2(b) under the Investment Company Act of 1940, is attached.

SIGNATURES | |

| Pursuant to the requirements of the Securities Exchange Act of 1934 and the Investment | |

| Company Act of 1940, the registrant has duly caused this report to be signed on its behalf by the | |

| undersigned, thereunto duly authorized. | |

| T. Rowe Price Short-Term Bond Fund, Inc. | |

| By | /s/ Edward C. Bernard |

| Edward C. Bernard | |

| Principal Executive Officer | |

| Date | July 22, 2008 |

| Pursuant to the requirements of the Securities Exchange Act of 1934 and the Investment | |

| Company Act of 1940, this report has been signed below by the following persons on behalf of | |

| the registrant and in the capacities and on the dates indicated. | |

| By | /s/ Edward C. Bernard |

| Edward C. Bernard | |

| Principal Executive Officer | |

| Date | July 22, 2008 |

| By | /s/ Gregory K. Hinkle |

| Gregory K. Hinkle | |

| Principal Financial Officer | |

| Date | July 22, 2008 |