Exhibit 13

| | | | | | |

FINANCIAL HIGHLIGHTS | | (dollar and share amounts in thousands, except per share data) |

| | | | | | | | | | | | | | | | |

| | | | | 2014 | | | | | 2013 | | | % CHANGE | |

FOR THE YEAR | | | | | | | | | | | | | | | | |

| | | | | |

Net sales | | | | $ | 21,105,141 | | | | | $ | 19,052,046 | | | | 11% | |

| | | | | |

Earnings: | | | | | | | | | | | | | | | | |

| | | | | |

Earnings before income taxes and noncontrolling interests | | | | | 1,204,577 | | | | | | 791,123 | | | | 52% | |

| | | | | |

Provision for income taxes | | | | | 388,787 | | | | | | 205,594 | | | | 89% | |

| | | | | | | | | | | | | | | | |

| | | | | |

Net earnings | | | | | 815,790 | | | | | | 585,529 | | | | 39% | |

| | | | | |

Earnings attributable to noncontrolling interests | | | | | 101,844 | | | | | | 97,504 | | | | 4% | |

| | | | | | | | | | | | | | | | |

| | | | | |

Net earnings attributable to Nucor stockholders | | | | | 713,946 | | | | | | 488,025 | | | | 46% | |

| | | | | |

Per share: | | | | | | | | | | | | | | | | |

| | | | | |

Basic | | | | | 2.22 | | | | | | 1.52 | | | | 46% | |

| | | | | |

Diluted | | | | | 2.22 | | | | | | 1.52 | | | | 46% | |

| | | | | |

Dividends declared per share | | | | | 1.4825 | | | | | | 1.4725 | | | | 1% | |

| | | | | |

Percentage of net earnings to net sales | | | | | 3.4% | | | | | | 2.6% | | | | | |

| | | | | |

Return on average stockholders’ equity | | | | | 9.3% | | | | | | 6.4% | | | | | |

| | | | | |

Capital expenditures | | | | | 568,867 | | | | | | 1,230,418 | | | | -54% | |

| | | | | |

Depreciation | | | | | 652,000 | | | | | | 535,852 | | | | 22% | |

| | | | | |

Acquisitions (net of cash acquired) | | | | | 768,581 | | | | | | — | | | | not meaningful | |

| | | | | |

Sales per employee | | | | | 921 | | | | | | 859 | | | | 7% | |

AT YEAR END | | | | | | | | | | | | | | | | |

| | | | | |

Working capital | | | | $ | 4,344,112 | | | | | $ | 4,449,830 | | | | -2% | |

| | | | | |

Property, plant and equipment, net | | | | | 5,287,639 | | | | | | 4,917,024 | | | | 8% | |

| | | | | |

Long-term debt (including current maturities) | | | | | 4,376,935 | | | | | | 4,380,200 | | | | — | |

| | | | | |

Total Nucor stockholders’ equity | | | | | 7,772,470 | | | | | | 7,645,769 | | | | 2% | |

| | | | | |

Per share | | | | | 24.36 | | | | | | 24.02 | | | | 1% | |

| | | | | |

Shares outstanding | | | | | 319,033 | | | | | | 318,328 | | | | — | |

| | | | | |

Employees | | | | | 23,600 | | | | | | 22,300 | | | | 6% | |

FORWARD-LOOKING STATEMENTS Certain statements made in this annual report are forward-looking statements that involve risks and uncertainties. The words “believe,” “expect,” “project,” “will,” “should,” “could” and similar expressions are intended to identify those forward-looking statements. These forward-looking statements reflect the Company’s best judgment based on current information, and although we base these statements on circumstances that we believe to be reasonable when made, there can be no assurance that future events will not affect the accuracy of such forward-looking information. As such, the forward-looking statements are not guarantees of future performance, and actual results may vary materially from the projected results and expectations discussed in this report. Factors that might cause the Company’s actual results to differ materially from those anticipated in forward-looking statements include, but are not limited to: (1) the sensitivity of the results of our operations to prevailing steel prices and changes in the supply and cost of raw materials, including pig iron, iron ore and scrap steel; (2) availability and cost of electricity and natural gas which could negatively affect our cost of steel production or could result in a delay or cancelation of existing or future drilling within our natural gas working interest drilling programs; (3) critical equipment failures and business interruptions; (4) market demand for steel products, which, in the case of many of our products, is driven by the level of nonresidential construction activity in the U.S.; (5) competitive pressure on sales and pricing, including pressure from imports and substitute materials; (6) impairment in the recorded value of inventory, equity investments, fixed assets, goodwill or other long-lived assets; (7) uncertainties surrounding the global economy, including the severe economic downturn in construction markets and excess world capacity for steel production; (8) fluctuations in currency conversion rates; (9) U.S. and foreign trade policies affecting steel imports or exports; (10) significant changes in laws or government regulations affecting environmental compliance, including legislation and regulations that result in greater regulation of greenhouse gas emissions that could increase our energy costs and our capital expenditures and operating costs or cause one or more of our permits to be revoked or make it more difficult to obtain permit modifications; (11) the cyclical nature of the steel industry; (12) capital investments and their impact on our performance; and (13) our safety performance.

| | | | |

22 | | | | MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS |

OVERVIEW

STEEL INDUSTRY CONDITIONS

After five years of recession, the worst the United States had experienced in decades, we began to see modest improvement in general economic indicators and manufacturing activity during 2014. There have been some recent positive trends in nonresidential construction markets (the sector to which we are most closely tied and the largest end market for steel), most likely due to a rise in consumer spending and the cautious realization of previously postponed business investment. The domestic automotive market, which is the second largest end market for steel, experienced its strongest year since the recession with over 16 million cars and light trucks sold in 2014 and further growth anticipated in 2015. Also contributing to the improvement in recent years was significant growth in domestic energy-related steel, which is the third largest end market for steel in the United States. With the global collapse in oil prices in the fourth quarter of 2014, activity in the energy sector has slowed dramatically. Long-term, we believe that lower energy prices will be good for the domestic economy.

Although both Nucor’s earnings and the markets we serve improved in 2014, we remain greatly constrained by the impact of global overcapacity. Weakening conditions in Europe, slowing growth in China and the strengthening of the dollar against other foreign currencies have made the U.S. markets a prime target for foreign imports. While the steel industry has historically been characterized by periods of overcapacity and intense competition for sales among producers, we are currently experiencing an era of global overcapacity that is unprecedented. Despite the bankruptcies of numerous domestic steel companies and ongoing global steel industry consolidation, the extraordinary increase in China’s steel production in the last decade, together with the excess capacity from other countries that have state-owned enterprises (SOEs) or export-focused steel industries, have exacerbated this overcapacity issue domestically as well as globally. According to the American Iron and Steel Institute, global steel overcapacity in 2014 was estimated at over 630 million tons per year, with China’s overcapacity being the largest piece at over 370 million tons. The Chinese overcapacity alone is estimated to be three times greater than the entire U.S. annual demand for steel.

Imported steel and steel products continue to present unique challenges for us because foreign producers often benefit from government subsidies, either directly through SOEs or indirectly through government-owned or controlled financial institutions. Foreign imports of finished and semi-finished steel increased 38% over 2013 and now account for approximately 34% of the U.S. steel market, despite significant unused cost-competitive domestic capacity. Products that we produce that experienced the most significant increases in imports by percentage include: cold-rolled and galvanized sheet, plate in coils and cut lengths and heavy structural shapes. Countries that had the largest increase in imports in 2014 include Russia, Turkey, China and South Korea.

China continues to pose a major challenge in particular. It is the world’s largest producer and exporter of steel, making more than 49% of the steel produced globally. We believe Chinese producers, many of which are government-owned in whole or in part, continue to benefit from their government’s manipulation of foreign currency exchange rates and from the receipt of government subsidies, which allows them to sell steel into our markets at artificially low prices.

China is not only selling steel at artificially low prices into our domestic market but also across the globe. When it does so, steel products that would otherwise have been consumed by the local steel customers in other countries are displaced into global markets, compounding the issue. In a more indirect manner, but still significant, is the import of fabricated steel products, such as oil country tubular goods, wind towers and other construction components that were produced in China.

Domestic steel industry markets are improving, allowing Nucor to deliver solid improvement in our performance in 2014. The steel industry has always been cyclical in nature, but North American producers of steel and steel products have been facing and are continuing to face some of the most arduous global market conditions they have experienced in history. The average capacity utilization rate of U.S. steel mills was at a historically unprecedented low of 52% in 2009. Since then, the average industry capacity utilization rate increased to approximately 77% in both 2014 and 2013. These rates, though improved, still compare unfavorably to capacity utilization rates of 81% and 87% in 2008 and 2007, respectively. Although domestic demand for steel and steel products is expected to improve further in 2015, it is unlikely that average capacity utilization rates will increase significantly due to the onslaught of steel imports into the U.S. The average utilization rates of all operating facilities in our steel mills, steel products and raw materials segments were approximately 78%, 64% and 63%, respectively, in 2014, compared with 74%, 58% and 62%, respectively, in 2013.

Macro-level uncertainties in world markets will almost certainly continue to weigh on global and domestic growth in 2015. We believe our net sales and financial results will be similar to 2014, but they will continue to be adversely affected by these general global economic factors as well as the global steel production overcapacity issue.

OUR CHALLENGES AND RISKS

Sales of many of our products are largely dependent upon capital spending in the nonresidential construction markets in the United States, including in the industrial and commercial sectors, as well as capital spending on infrastructure that is publicly funded, such as bridges, schools, prisons and hospitals. Unlike recoveries from past recessions, the recovery from the recession of 2008-2009 has not yet included a strong recovery in the severely depressed nonresidential construction market. Only recently has capital spending on nonresidential construction projects shown any real signs of life. We do not expect to see strong growth in our net sales until we see a more sustained increase in capital spending on these types of construction projects.

The significant recent surge in artificially cheap exports by some of our major foreign competitors into the United States and elsewhere reduces our net sales and adversely impacts our financial results. Aggressive enforcement of trade rules by the World Trade Organization to limit unfairly traded imports remains uncertain, although it is critical to our ability to remain competitive. We have been encouraged by recent trade enforcement actions the U.S. government recently completed, including terminating its suspension agreement with Russia for hot-rolled steel imports, assessing duties on oil country tubular goods from South Korea and five other countries and ruling that the domestic rebar industry has been materially injured as a result of dumped and subsidized rebar imports from Turkey and Mexico. We continue to believe that assertive enforcement of world trade rules must be one of the highest priorities of the United States government.

A major uncertainty we continue to face in our business is the price of our principal raw material, ferrous scrap, which is volatile and often increases or decreases rapidly in response to changes in domestic demand, unanticipated events that affect the flow of scrap into scrap yards and changes in foreign demand for scrap. In periods of rapidly increasing raw material prices in the industry, which is often also associated with periods of strong or rapidly improving steel market conditions, being able to increase our prices for the products we sell quickly enough to offset increases in the prices we pay for ferrous scrap is challenging but critical to maintaining our profitability. We attempt to mitigate the scrap price risk by managing scrap inventory levels at the steel mills to match the anticipated demand over the next several weeks for various steel products. Certain scrap substitutes, including pig iron, have longer lead times for delivery than scrap, which can make this inventory management strategy difficult to achieve. Continued successful implementation of our raw material strategy, including key investments in direct reduced iron (DRI) production coupled with the scrap brokerage and processing services performed by our team at The David J. Joseph Company (DJJ), give us greater control over our metallic inputs and thus also help us to mitigate this risk.

During periods of stronger or improving steel market conditions, we are more likely to be able to pass through to our customers, relatively quickly, the increased costs of ferrous scrap and scrap substitutes and to protect our gross margins from significant erosion. During weaker or rapidly deteriorating steel market conditions, including the global steel market environment of the past several years, weak steel demand, low industry utilization rates, and the impact of imports create an even more intensified competitive environment. All of those factors, to some degree, impact pricing, which increases the likelihood that Nucor will experience lower gross margins.

Although the majority of our steel sales are to spot market customers who place their orders each month based on their business needs and our pricing competitiveness compared to both domestic and global producers and trading companies, we also sell contract tons, primarily in our sheet operations. Approximately 50% of our sheet sales were to contract customers in 2014 (65% in both 2013 and 2012), with the balance in the spot market at the prevailing prices at the time of sale. Steel contract sales outside of our sheet operations are not significant. The amount of tons sold to contract customers depends on the overall market conditions at the time, how the end-use customers see the market moving forward and the strategy that Nucor management believes is appropriate to the upcoming period. Nucor management considerations include maintaining an appropriate balance of spot and contract tons based on market projections and appropriately supporting our diversified customer base. The percentage of tons that is placed under contract also depends on the overall market dynamics and customer negotiations. In years of strengthening demand, we typically see an increase in the percentage of sheet sales sold under contract as our customers have an expectation that transaction prices will rapidly rise and available capacity will quickly be sold out. To mitigate this risk, customers prefer to enter into contracts in order to obtain committed volumes of supply from the mills. Our contracts include a method of adjusting prices on a periodic basis to reflect changes in the market pricing for steel and/ or scrap. Market indices for steel generally trend with scrap pricing changes but during periods of steel market weakness, including the market conditions of the past several years, the more intensified competitive steel market environment can cause the sales price indices to result in reduced gross margins and profitability. Furthermore, since the selling price adjustments are not immediate, there will always be a timing difference between changes in the prices we pay for raw materials and the adjustments we make to our contract selling prices. Generally, in periods of increasing scrap prices, we experience a short-term margin contraction on contract tons. Conversely, in periods of decreasing scrap prices, we typically experience a short-term margin expansion. Contract sales typically have terms ranging from six to twelve months.

Another significant uncertainty we face is the cost of energy. The availability and prices of electricity and natural gas are influenced today by many factors including changes in supply and demand, advances in drilling technology and, increasingly, by changes in public policy relating to energy production and use. Proposed regulation of greenhouse gas emissions from new and refurbished power plants could increase our cost of electricity in future years, particularly if they are adopted in a form that requires deep reductions in greenhouse gas emissions. Adopting these regulations in an onerous form could lead to foreign producers that are not affected by them gaining a competitive advantage over us. We are monitoring these regulatory developments closely and will seek to educate public policy makers during the adoption process about their potential impact on our business and the U.S. manufacturing base.

Finally, due to our natural gas working interest drilling programs with Encana, a substantial or extended decline in natural gas prices could have a material adverse effect on these programs and, by extension, us. In the fourth quarter of 2013, we announced a joint decision with Encana to temporarily suspend drilling new wells until there is a sustained improvement in natural gas pricing. In the fourth quarter of 2014, Nucor and Encana agreed to further suspend drilling through calendar 2015 except for a de minimis number of wells that are necessary in order to retain leasehold rights. A substantial or extended decline in the price of natural gas could result in further delays or cancelation of existing or future drilling programs or curtailment in production at some properties, all of which could have an adverse

effect on our revenues, profitability and cash flows. In addition, natural gas drilling and production are subject to intense federal and state regulation as well as to public interest in environmental protection. Such regulation and interest, when coupled, could result in these drilling programs being forced to comply with certain future regulations, resulting in unknown impacts on the programs’ ability to achieve the cost and hedge benefits we expect from the programs.

OUR STRENGTHS AND OPPORTUNITIES

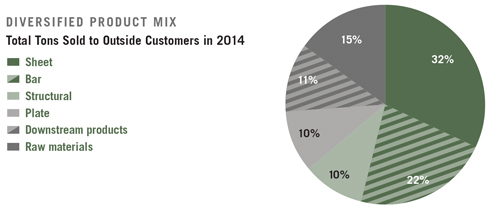

We are North America’s most diversified steel producer. As a result, our short-term performance is not tied to any one market. Since 2009 we have made investments of nearly $6 billion on projects that are not only diversifying our product offerings but also the markets that we serve. These investments will grow our long-term earnings power by expanding our product portfolio into higher value-added offerings that are less vulnerable to imports, improving our cost structure and further building upon our market leadership positions. The pie chart below shows the diversity of our product mix by total tons sold to outside customers in 2014.

Nucor’s raw material supply chain is another important strength. Our investment in DRI production facilities and scrap yards, as well as our access to international raw materials markets, provides Nucor with significant flexibility in optimizing our raw materials costs. Additionally, having a significant portion of our raw materials supply under our control minimizes risk associated with the global sourcing of raw materials, particularly since a good deal of scrap substitutes comes from regions of the world that have historically experienced greater political turmoil.

Our highly variable low-cost structure, combined with our financial strength and liquidity, has allowed us to successfully navigate cyclical severely depressed steel industry market conditions in the past. In such times, our incentive-based pay system reduces our payroll costs, both hourly and salary, which helps to offset lower selling prices. Our pay-for-performance system that is closely tied to our levels of production also allows us to keep our work force intact and to continue operating our facilities when some of our competitors with greater fixed costs are forced to shut down some of their facilities. Because we use electric arc furnaces to produce our steel, we can easily vary our production levels to match short-term changes in demand, unlike our integrated competitors. We believe these strengths also provide us further opportunities to gain market share during such times.

EVALUATING OUR OPERATING PERFORMANCE

We report our results of operations in three segments: steel mills, steel products and raw materials. Most of the steel we produce in our mills is sold to outside customers, but a significant percentage is used internally by some of the facilities in our steel products segment.

We begin measuring our performance by comparing our net sales, both in total and by individual segment, during a reporting period with our net sales in the corresponding period in the prior year. In doing so, we focus on changes in and the reasons for such changes in the two key variables that have the greatest influence on our net sales: average sales price per ton during the period and total tons shipped to outside customers.

We also focus on both dollar and percentage changes in gross margins, which are key drivers of our profitability, and the reasons for such changes. There are many factors from period to period that can affect our gross margins. One consistent area of focus for us is changes in “metal margins,” which is the difference between the selling price of steel and the cost of scrap and scrap substitutes. Increases in the cost of scrap and scrap substitutes that are not offset by increases in the selling price of steel can quickly compress our margins and reduce our profitability.

Another factor affecting our gross margins in any given period is the application of the last-in, first-out (LIFO) method of accounting to a substantial portion of our inventory (43% of total inventories as of December 31, 2014). LIFO charges or credits for interim periods are based on management’s interim period-end estimates, after considering current and anticipated market conditions, of both inventory costs and quantities at fiscal year end. The actual year end amounts may differ significantly from these estimated interim amounts.

Annual LIFO charges or credits are largely based on the relative changes in cost and quantities year over year, primarily with raw material inventory in the steel mills segment.

Because we are such a large user of energy, material changes in energy costs per ton can significantly affect our gross margins as well. Lower energy costs per ton increase our gross margins. Generally, our energy costs per ton are lower when the average utilization rates of all operating facilities in our steel mills segment are higher.

Changes in marketing, administrative and other expenses, particularly profit sharing costs, can have a material effect on our results of operations for a reporting period as well. Profit sharing costs vary significantly from period to period as they are based upon changes in our pre-tax earnings and are a reflection of our pay-for-performance system that is closely tied to our levels of production.

EVALUATING OUR FINANCIAL CONDITION

We evaluate our financial condition each reporting period by focusing primarily on the amounts of and reasons for changes in cash provided by operating activities, our current ratio, the turnover rate of our accounts receivable and inventories, the amount and reasons for changes in cash used in or provided by investing activities and financing activities and our cash and cash equivalents and short-term investments position at period end. Our conservative financial practices have served us well in the past and are serving us well today. As a result, our financial position remains strong despite the negative effects on our business of global overcapacity and the continued weakness in the global economy.

COMPARISON OF 2014 TO 2013

RESULTS OF OPERATIONS

NET SALES

Net sales to external customers by segment for 2014 and 2013 were as follows:

| | | | | | | | | | | | |

Year Ended December 31, | | 2014 | | | 2013 | | | % Change | |

| | | |

Steel mills | | $ | 14,723,642 | | | $ | 13,311,948 | | | | 11% | |

Steel products | | | 4,032,385 | | | | 3,607,333 | | | | 12% | |

Raw materials | | | 2,349,114 | | | | 2,132,765 | | | | 10% | |

| | | | | | | | | | | | |

Total net sales to external customers | | $ | 21,105,141 | | | $ | 19,052,046 | | | | 11% | |

| | | | | | | | | | | | |

| | | |

| | | | | | | | | | | | | |

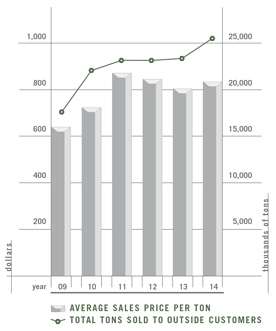

Net sales for 2014 increased 11% from the prior year. The average sales price per ton increased 3% from $803 in 2013 to $830 in 2014, while total tons shipped to outside customers increased 7% in 2014 as compared to 2013.

In the steel mills segment, production and sales tons were as follows:

| | | | | | | | | | | | |

Year Ended December 31, | | 2014 | | | 2013 | | | % Change | |

| | | |

Steel production | | | 21,135 | | | | 19,900 | | | | 6% | |

| | | | | | | | | | | | |

| | | |

Outside steel shipments | | | 18,681 | | | | 17,733 | | | | 5% | |

Inside steel shipments | | | 3,286 | | | | 2,917 | | | | 13% | |

| | | | | | | | | | | | |

Total steel shipments | | | 21,967 | | | | 20,650 | | | | 6% | |

| | | | | | | | | | | | |

| | | |

| | | | | | | | | | | | | |

Net sales to external customers in the steel mills segment increased 11% due to a 5% increase in the average sales price per ton from $751 in 2013 to $788 in 2014 and a 5% increase in tons sold to outside customers.

The sheet, bar, structural and plate product groups all experienced an increase in average sales price per ton compared with 2013 due to stronger demand and new product offerings. The strongest markets for the steel mills segment were manufactured goods, including automotive, energy and heavy truck. Steel mills segment sales were positively impacted by favorable trends in nonresidential construction markets during 2014. Energy markets were strong for the steel mills segment for 2013 and most of 2014. However, the collapse in oil prices in late 2014 triggered inventory reductions among pipe and tube producers which negatively impacted volumes and pricing at our sheet mills late in the year. Though average sales prices increased for the steel mills segment in 2014 compared with 2013, high levels of finished and semi-finished steel imports, which increased 38% compared to 2013, continued to apply pressure on pricing during 2014.

Tonnage data for the steel products segment is as follows:

| | | | | | | | | | | | |

Year Ended December 31, | | 2014 | | | 2013 | | | % Change | |

| | | |

Joist sales | | | 421 | | | | 342 | | | | 23% | |

Deck sales | | | 396 | | | | 334 | | | | 19% | |

Cold finished sales | | | 504 | | | | 474 | | | | 6% | |

Fabricated concrete reinforcing steel sales | | | 1,185 | | | | 1,065 | | | | 11% | |

| | | |

| | | | | | | | | | | | | |

Net sales to external customers in the steel products segment increased 12% from 2013 due to an 11% increase in tons sold to outside customers and a 1% increase in the average sales price per ton from $1,375 in 2013 to $1,383 in 2014. Particularly strong volume growth was achieved in our joist, decking and rebar fabrication products. Shipments to external customers decreased 17% in the fourth quarter of 2014 from the third quarter of 2014 because of typical seasonality in nonresidential construction markets. The increase in the quantity of steel products sold in 2014 as compared to 2013 is largely due to the continued improvement in nonresidential construction markets. As measured by square footage, U.S. nonresidential construction activity increased by approximately 7% in 2014.

Sales for the raw materials segment increased 10% from 2013 primarily due to increased volumes in DJJ’s brokerage and recycling businesses and our natural gas drilling activities, partially offset by decreased pricing at DJJ. Approximately 81% of outside sales in the raw materials segment in 2014 were from brokerage operations of DJJ and approximately 12% of the outside sales were from the scrap processing facilities (83% and 12%, respectively, in 2013). Sales for DJJ in the fourth quarter of 2014 decreased from the third quarter of 2014 due primarily to decreased volumes at our brokerage and processing businesses. Sales in the fourth quarter of 2014 decreased from the fourth quarter of 2013 due to decreased average sales prices and volumes at the brokerage and processing businesses.

GROSS MARGIN

In 2014, Nucor recorded gross margins of $1.91 billion (9%) compared to $1.41 billion (7%) in 2013. The year-over-year dollar and gross margin percentage increases were primarily the result of the 3% increase in the average sales price per ton and 7% increase in tons shipped to outside customers, along with the following factors:

| | | | |

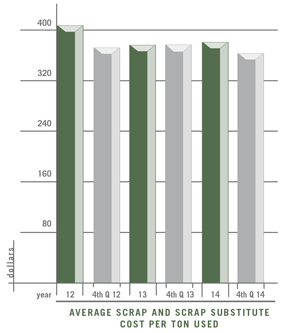

· | | In the steel mills segment, the average scrap and scrap substitute cost per ton used increased 1% from $376 in 2013 to $381 in 2014; however, metal margins also increased for our sheet, bar, structural and plate products from 2013. The increase in metal margins more than offset the increase in the average scrap and scrap substitute cost per ton used in 2014 compared to 2013. Metal margins in the fourth quarter of 2014 were higher than in the fourth quarter of 2013, but were lower compared to the third quarter of 2014. |

| | Scrap prices are driven by the global supply and demand for scrap and other iron-based raw materials used to make steel. We experienced more quarterly volatility in scrap costs during 2014 than in 2013. We believe that the current domestic scrap market is significantly overpriced compared with iron ore and global scrap markets. Based on increased imported steel penetration, slack international demand for domestic scrap, the strength of the U.S. dollar and moderating domestic demand for scrap, we expect scrap prices to fall significantly in early 2015. | |

|

· | | Nucor’s gross margins are significantly impacted by the application of the LIFO method of accounting. LIFO charges or credits are largely based on the relative changes in cost and quantities year over year, primarily within raw material inventory in the steel mills segment. The average scrap and scrap substitute cost per ton in ending inventory within our steel mills segment at December 31, 2014 decreased 11% as compared to December 31, 2013. As a result, Nucor recorded a LIFO credit of $57.3 million in 2014 (a LIFO charge of $17.4 million in 2013). The decreases in cost per ton were driven by market conditions at the end of 2014, which experienced weaker demand for steel and raw materials than market conditions at the end of 2013. | |

· | | Total steel mill energy costs increased approximately $2 per ton from 2013 to 2014 primarily due to higher unit costs for natural gas and electricity. Total steel mill energy costs per ton for the year reached a peak in the first quarter of 2014 due to harsh winter weather conditions that drove up energy demand and costs. Due to the efficiency of Nucor’s steel mills, energy costs remained less than 6% of the sales dollar in 2014 and 2013. | |

· | | Nucor’s 2014 gross margins were negatively impacted by $8.9 million in inventory-related purchase accounting adjustments associated with our acquisition of Nucor Steel Gallatin in the fourth quarter of 2014 (none in 2013). |

· | | Gross margins in the steel products segment increased significantly in 2014 compared to 2013 due in large part to the improving conditions in the nonresidential construction markets. Our joist, deck, rebar, cold finish and building systems operations all experienced margin improvement in 2014 compared to 2013. |

· | | Our Nucor Steel Louisiana DRI facility, which began production operations in December 2013, experienced significant operational losses, including start-up costs of $87.8 million in 2014 and $35.2 million in 2013, that negatively impacted gross margins. |

| | The start-up costs in 2013 and the first three quarters of 2014 were primarily due to yield loss, which in our experience is not unusual when a new facility is in the early stage of production. Although Nucor Steel Louisiana has had significant operational losses, it achieved excellent quality and volume levels. In the fourth quarter of 2014, an equipment failure occurred at Nucor Steel Louisiana related to the process gas heater. There were no injuries, no environmental impact and no damage to any other part of the DRI facility as a result of this incident. Production operations were suspended after the failure and have not restarted. As Nucor Steel Louisiana was not operational for almost the entire fourth quarter of 2014, we classified the facility’s fourth quarter operating loss of approximately $35 million, the majority of which impacts gross margin, as start-up costs. We are in the process of making the necessary repairs and adjustments to the process gas heater. Nucor Steel Louisiana is estimated to resume operations late in the first quarter of 2015. We expect a small reduction in the operating loss of Nucor Steel Louisiana in the first quarter of 2015 as compared to the fourth quarter of 2014. |

· | | Gross margins related to DJJ’s scrap processing and brokerage operations increased during 2014 compared to 2013. The brokerage group benefited from stronger domestic scrap sales. Though the gross margin for the scrap processing group improved during 2014 compared to 2013, the group experienced a decline in gross margin from the third quarter of 2014 to the fourth quarter of 2014. |

MARKETING, ADMINISTRATIVE AND OTHER EXPENSES

A major component of marketing, administrative and other expenses is profit sharing and other incentive compensation costs. These costs, which are based upon and fluctuate with Nucor’s financial performance, increased from 2013 to 2014. In 2014, profit sharing costs consisted of $110.1 million of contributions, including the Company’s matching contribution, made to the Company’s Profit Sharing and Retirement Savings Plan for qualified employees ($71.7 million in 2013). Other bonus costs also fluctuate based on Nucor’s achievement of certain financial performance goals, including comparisons of Nucor’s financial performance to peers in the steel industry and other companies. Stock-based compensation included in marketing, administrative and other expenses decreased by 4% to $21.9 million in 2014 compared with $22.9 million in 2013 and includes costs associated with vesting of stock awards granted in prior years.

Included in marketing, administrative and other expenses in 2014 is a $9.0 million charge related to the disposal of assets and a $12.5 million charge related to the partial write-down of assets, both in the steel mills segment.

In the third quarter of 2013, one of three iron ore storage domes collapsed at Nucor Steel Louisiana in St. James Parish. As a result, Nucor recorded a partial write-down of assets at the facility, including $21.0 million of property, plant and equipment, and $7.0 million of inventory, offset by a $14.0 million insurance receivable that was based on management’s best estimate of probable insurance recoveries. The associated net charge of $14.0 million was included in marketing, administrative and other expenses in 2013. As of December 31, 2014, Nucor has received initial payments of $10.3 million related to the insurance receivable. The two remaining storage domes have a carrying value of approximately $20 million. Nucor continues to assess these two domes and the assets associated with them. As a result of the ongoing assessment, it is possible that Nucor will make operational decisions that could impact the carrying value of the domes and the associated assets and the amount of insurance proceeds claimed by and payable to us.

EQUITY IN (EARNINGS) LOSSES OF UNCONSOLIDATED AFFILIATES

Equity method investment earnings, including amortization expense and other purchase accounting adjustments, were $13.5 million in 2014 and $9.3 million in 2013. The increase in equity method investment earnings from 2014 to 2013 is primarily due to greater equity method earnings at NuMit and a decrease in losses at Duferdofin Nucor.

INTEREST EXPENSE (INCOME)

Net interest expense is detailed below:

| | | | | | | | |

Year Ended December 31, | | 2014 | | | 2013 | |

| | |

Interest expense | | $ | 174,142 | | | $ | 151,986 | |

Interest income | | | (4,886 | ) | | | (5,091 | ) |

| | | | | | | | |

Interest expense, net | | $ | 169,256 | | | $ | 146,895 | |

| | | | | | | | |

| | |

| | | | | | | | | |

The 15% increase in gross interest expense from 2013 is primarily attributable to a 13% increase in average debt outstanding. Gross interest income decreased 4% due to a 13% decrease in average investments, partially offset by an increase in the average interest rate on investments.

EARNINGS BEFORE INCOME TAXES AND NONCONTROLLING INTERESTS

Earnings before income taxes and noncontrolling interests by segment for 2014 and 2013 are as follows:

| | | | | | | | |

Year Ended December 31, | | 2014 | | | 2013 | |

| | |

Steel mills | | $ | 1,594,352 | | | $ | 1,156,715 | |

Steel products | | | 166,323 | | | | 82,129 | |

Raw materials | | | (29,053 | ) | | | 13,686 | |

Corporate/eliminations | | | (527,045 | ) | | | (461,407 | ) |

| | | | | | | | |

Earnings before income taxes and noncontrolling interests | | $ | 1,204,577 | | | $ | 791,123 | |

| | | | | | | | |

| | |

| | | | | | | | | |

Earnings before income taxes and noncontrolling interests in the steel mills segment for 2014 increased significantly from 2013 due to higher sales volume, higher average sales prices and higher metal margins resulting from factors discussed above. Our recent capital project expansions have allowed us to broaden our product offerings and market share, particularly in the special bar quality, cold-rolled and galvanized sheet and plate steel products. These higher-value product offerings, which tend to be less vulnerable to imports, benefited the profitability of the steel mills segment in 2014. The improved results of the steel mills segment were achieved despite imports being at levels not seen since 2006. The strongest markets for the steel mills segment continued to be manufactured goods, including automotive, energy and heavy truck. Energy markets were strong for the steel mills segment for 2013 and most of 2014. However, the collapse in oil prices in late 2014 triggered inventory reductions among pipe and tube producers that negatively impacted volumes and pricing at our sheet mills late in the year. The steel mills segment profitability in 2014 also benefited from improving conditions in nonresidential construction markets. Negatively impacting the steel mills segment profitability in 2014 were the $12.5 million charge related to the partial write-down of assets, $9.0 million charge related to the disposal of assets, and $8.9 million of inventory-related purchase accounting adjustments at newly acquired Nucor Steel Gallatin. The steel mills segment profitability benefited from improved results at NuMit and Duferdofin Nucor.

In the steel products segment, earnings before income taxes and noncontrolling interests increased significantly in 2014 compared to 2013. The largest increases in profitability in 2014 compared to 2013 were at our joist, deck, and building systems operations, while the profitability of our rebar and cold finish operations also increased. The steel products segment has benefited from improving conditions in nonresidential construction markets. However, 2014 nonresidential construction starts, a measure of nonresidential building activity, represented only about 56% of 2007’s peak activity level. Backlog tons for the steel products segment were approximately 10% higher at the end of 2014 than at the end of 2013, including a record level of backlog tons since 2008 for our rebar fabrication businesses at the end of 2014.

The decrease in profitability of our raw materials segment for 2014 as compared to 2013 is due primarily to operating losses, which include start-up costs, of approximately $135 million at our Louisiana DRI facility (production did not begin at the facility until late December 2013). Production operations at the Louisiana DRI facility were suspended in the fourth quarter of 2014 due to an equipment failure related to the process gas heater. Prior to that, production outages in June, July and September of 2014 were necessary to implement changes intended to improve consistency in the production process and yield performance at Nucor Steel Louisiana. An additional factor affecting the performance of Nucor Steel Louisiana in 2014 was the impact of consuming higher-cost iron ore purchased earlier in the year under a quarterly lag pricing mechanism. Earnings before income taxes and noncontrolling interest in the raw materials segment in 2013 was impacted by the charges related to the net $14.0 million write-down of inventory and property, plant and equipment as a result of the dome collapse at Nucor Steel Louisiana that occurred in the third quarter of 2013.

Partially offsetting the losses at the Louisiana DRI plant was increased profitability from DJJ’s brokerage and scrap processing operations due to increased volumes and margin improvement, and increased profitability from our natural gas working interest drilling investment. The DRI facility in Trinidad also experienced an increase in profitability.

NONCONTROLLING INTERESTS

Noncontrolling interests represent the income attributable to the minority interest partners of Nucor’s joint ventures, primarily Nucor-Yamato Steel Company (NYS) of which Nucor owns 51%. The 4% increase in earnings attributable to noncontrolling interests was primarily due to increased average sales prices and increased metal margins, partially offset by decreased volumes and the impact of a planned three week outage associated with a capital project in the second quarter of 2014. Under the NYS limited partnership agreement, the minimum amount of cash to be distributed each year to the partners is the amount needed by each partner to pay applicable U.S. federal and state income taxes.

PROVISION FOR INCOME TAXES

The effective tax rate in 2014 was 32.3% compared with 26.0% in 2013. The increase in the rate between 2013 and 2014 is primarily due to a $21.3 million favorable non-cash out-of-period adjustment to deferred tax balances in 2013 compared to a $13.2 million favorable non-cash out-of-period adjustment to tax balances in 2014, the change in the relative proportions of net earnings attributable to noncontrolling interests and the foreign rate differential to total pre-tax earnings between the periods. The out-of-period items did not have a material impact to periods in which the corrections were recorded or in any previously reported period individually and in the aggregate. The Internal Revenue Service (IRS) is examining Nucor’s 2012 federal income tax return. Management believes that the Company has adequately provided for any adjustments that may arise from this audit. The 2011 and 2013 tax years are also open to examination by the IRS. U.S. federal income tax matters have been concluded for years through 2010. The Canada Revenue Agency is examining the 2012 Canadian returns for Harris Steel Group Inc. and certain related affiliates. Tax years 2009 through 2013 remain open to examination by other major taxing jurisdictions to which Nucor is subject (primarily Canada and other state and local jurisdictions).

NET EARNINGS AND RETURN ON EQUITY

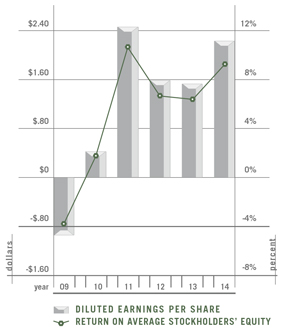

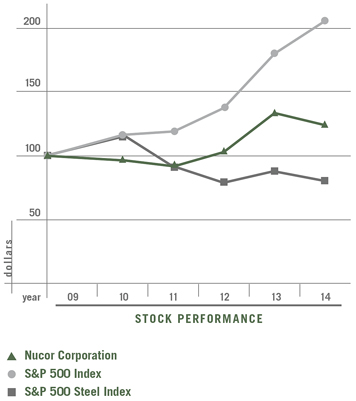

Nucor reported net earnings of $713.9 million, or $2.22 per diluted share, in 2014, compared to net earnings of $488.0 million, or $1.52 per diluted share, in 2013. Net earnings attributable to Nucor stockholders as a percentage of net sales were 3% in both 2014 and 2013. Return on average stockholders’ equity was 9% and 6% in 2014 and 2013, respectively.

COMPARISON OF 2013 TO 2012

RESULTS OF OPERATIONS

NET SALES

Net sales to external customers by segment for 2013 and 2012 were as follows:

| | | | | | | | | | | | |

| | | | | | | | | (in thousands) | |

| Year Ended December 31, | | 2013 | | | 2012 | | | % Change | |

| | | |

Steel mills | | | $13,311,948 | | | | $13,781,797 | | | | -3% | |

Steel products | | | 3,607,333 | | | | 3,738,381 | | | | -4% | |

Raw materials | | | 2,132,765 | | | | 1,909,095 | | | | 12% | |

| | | | | | | | | | | | |

Total net sales to external customers | | | $19,052,046 | | | | $19,429,273 | | | | -2% | |

| | | | | | | | | | | | |

| | | |

| | | | | | | | | | | | | |

Net sales for 2013 decreased 2% from the prior year. The average sales price per ton decreased 5% from $841 in 2012 to $803 in 2013, while total tons shipped to outside customers increased 3% in 2013 as compared to 2012.

In the steel mills segment, production and sales tons were as follows:

| | | | | | | | | | | | |

| | | | | | | | | (in thousands) | |

| Year Ended December 31, | | 2013 | | | 2012 | | | % Change | |

| | | |

Steel production | | | 19,900 | | | | 19,865 | | | | — | |

| | | | | | | | | | | | |

| | | |

Outside steel shipments | | | 17,733 | | | | 17,473 | | | | 1% | |

Inside steel shipments | | | 2,917 | | | | 2,769 | | | | 5% | |

| | | | | | | | | | | | |

Total steel shipments | | | 20,650 | | | | 20,242 | | | | 2% | |

| | | | | | | | | | | | |

| | | |

| | | | | | | | | | | | | |

Net sales to external customers in the steel mills segment decreased 3% due to a 5% decrease in the average sales price per ton from $792 in 2012 to $751 in 2013, partially offset by a 1% increase in tons sold to outside customers.

Tonnage data for the steel products segment is as follows:

| | | | | | | | | | | | |

| | | | | | | | | (in thousands) | |

| Year Ended December 31, | | 2013 | | | 2012 | | | % Change | |

| | | |

Joist sales | | | 342 | | | | 291 | | | | 18% | |

Deck sales | | | 334 | | | | 308 | | | | 8% | |

Cold finished sales | | | 474 | | | | 492 | | | | -4% | |

Fabricated concrete reinforcing steel sales | | | 1,065 | | | | 1,180 | | | | -10% | |

Net sales to external customers in the steel products segment decreased 4% from 2012 due to a 3% decrease in tons sold to outside customers and a 1% decrease in the average sales price per ton from $1,393 in 2012 to $1,375 in 2013.

Sales for the raw materials segment increased 12% from 2012 primarily due to increased volumes in DJJ’s brokerage and processing operations, partially offset by decreased pricing experienced by DJJ as well as increased volumes at our natural gas drilling working interests. Approximately 83% of outside sales in the raw materials segment in 2013 were from brokerage operations of DJJ and approximately 12% of the outside sales were from the scrap processing facilities (85% and 13%, respectively, in 2012).

GROSS MARGIN

In 2013, Nucor recorded gross margins of $1.41 billion (7%) compared to $1.51 billion (8%) in 2012. The year-over-year dollar and gross margin percentage decreases were primarily the result of the 5% decrease in the average sales price per ton, partially offset by the 3% increase in tons shipped to outside customers. Additionally, gross margins were impacted by the following factors:

| | | | | | |

| · | | | | In the steel mills segment, the average scrap and scrap substitute cost per ton used decreased 8% from $407 in 2012 to $376 in 2013; however, metal margins also decreased for our sheet, bar and plate products from 2012. |

| · | | | | The average scrap and scrap substitute cost per ton in ending inventory within our steel mills segment at December 31, 2013 increased 3% as compared to December 31, 2012. Ending inventory quantities also increased as compared to December 31, 2012. As a result of these factors, Nucor recorded a LIFO charge of $17.4 million in 2013 (a LIFO credit of $155.9 million in 2012). |

| · | | | | Nucor’s 2012 gross margins were negatively impacted by $48.8 million in inventory-related purchase accounting adjustments associated with our acquisition of Skyline (none in 2013). |

| · | | | | Gross margins at our rebar fabrication businesses increased significantly in 2013 as compared to 2012 due to higher average sales prices and the effects of management initiatives that resulted in lower costs, better selling strategies and improved supplier relationships. |

| · | | | | Total steel mill energy costs decreased approximately $1 per ton from 2012 to 2013 primarily due to the negative impact of natural gas hedge settlements on our overall natural gas costs in 2012. |

| · | | | | Gross margins related to DJJ’s scrap processing operations decreased significantly during 2013 compared to 2012 due to excess shredding capacity increasing DJJ’s cost of scrap purchases and weather-related effects in the first quarter of 2013 that reduced the flow of scrap into our scrap processing operations. |

MARKETING, ADMINISTRATIVE AND OTHER EXPENSES

Profit sharing costs decreased from 2012 to 2013. In 2013, profit sharing costs consisted of $71.7 million of contributions, including the Company’s matching contribution, made to the Company’s Profit Sharing and Retirement Savings Plan for qualified employees ($77.7 million in 2012). Stock-based compensation included in marketing, administrative and other expenses decreased 8% to $22.9 million in 2013 compared with $25.0 million in 2012 and includes costs associated with vesting of stock awards granted in prior years.

Of the $27.0 million increase in marketing, administrative and other expenses in 2013 as compared to 2012, $15.3 million was due to the inclusion of Skyline’s results for the entire year in 2013 as compared to only being included after its June 2012 acquisition date during 2012. Additionally, in the third quarter of 2013, a storage dome collapsed at Nucor Steel Louisiana in St. James Parish. As a result, Nucor recorded a partial write-down of assets at the facility, including $7.0 million of inventory and $21.0 million of property, plant and equipment, offset by a $14.0 million insurance receivable that was based on management’s best estimate of probable insurance recoveries. Included in marketing, administrative and other expenses in 2012 was a $17.6 million loss on the sale of the assets of Nucor Wire Products Pennsylvania, Inc.

EQUITY IN LOSSES OF UNCONSOLIDATED AFFILIATES

Nucor recorded equity method investment earnings of $9.3 million in 2013 and losses of $13.3 million in 2012. The improvement in the equity method investment earnings from 2013 to 2012 is primarily due to greater equity method earnings at NuMit, a decrease in losses at Duferdofin Nucor, and earnings at Hunter Ridge (acquired in November 2012).

IMPAIRMENT OF NON-CURRENT ASSETS

In 2013, Nucor incurred no charges for impairment of non-current assets compared to $30.0 million in 2012. In the second quarter of 2012, Nucor recorded a $30.0 million impairment charge related to its equity method investment in Duferdofin Nucor (see Note 10 to the Consolidated Financial Statements).

INTEREST EXPENSE (INCOME)

Net interest expense is detailed below:

| | | | | | | | |

| Year Ended December 31, | | 2013 | | | 2012 | |

| | |

Interest expense | | $ | 151,986 | | | $ | 173,503 | |

Interest income | | | (5,091 | ) | | | (11,128 | ) |

| | | | | | | | |

Interest expense, net | | $ | 146,895 | | | $ | 162,375 | |

| | | | | | | | |

| | |

| | | | | | | | | |

The 12% decrease in gross interest expense from 2012 is primarily attributable to a 6% decrease in average debt outstanding and a 2% decrease in the average interest rate. Gross interest income decreased 54% due to a 50% decrease in average investments and a 45% decrease in the average interest rate on investments.

EARNINGS BEFORE INCOME TAXES AND NONCONTROLLING INTERESTS

Earnings before income taxes and noncontrolling interests by segment for 2013 and 2012 are as follows:

| | | | | | | | |

| Year Ended December 31, | | 2013 | | | 2012 | |

| | |

Steel mills | | $ | 1,156,715 | | | $ | 1,162,270 | |

Steel products | | | 82,129 | | | | (17,140 | ) |

Raw materials | | | 13,686 | | | | 55,264 | |

Corporate/eliminations | | | (461,407 | ) | | | (347,454 | ) |

| | | | | | | | |

Earnings before income taxes and noncontrolling interests | | $ | 791,123 | | | $ | 852,940 | |

| | | | | | | | |

| | |

| | | | | | | | | |

Earnings before income taxes and noncontrolling interests in the steel mills segment in 2013 decreased slightly from 2012. Gross margin was negatively affected in 2013 by lower metal margin dollars resulting from factors discussed above. The steel mills segment’s profitability in 2013 benefited from improved results from the NuMit and Duferdofin Nucor equity method investments as compared to 2012. Other factors impacting the profitability of the steel mills segment in 2012 that did not occur in 2013 were the $30.0 million impairment charge related to Duferdofin Nucor and the $48.8 million of inventory-related purchase accounting adjustments related to Skyline.

The steel products segment had earnings before income taxes and noncontrolling interests in 2013 as compared to a loss in 2012. Although the average sales price and volume for the segment were lower in 2013 than 2012, profitability in our joist, cold finish and rebar fabrication businesses improved from 2012. The steel products segment’s 2012 loss was impacted by the $17.6 million loss on the sale of assets of Nucor Wire Products Pennsylvania, Inc. in the third quarter of 2012. The steel products segment’s 2013 profitability was the first profitable year since 2008.

The profitability of our raw materials segment decreased significantly from 2012. Difficult conditions in the scrap processing industry had a negative impact on the profitability of the scrap processing operations of DJJ since the first quarter of 2012. During this time, excess shredding capacity increased competition for raw materials while the selling price of scrap decreased in 2013 as compared to 2012. Also negatively affecting profitability in the raw materials segment in 2013 were the charges related to the net $14.0 million write-down of

inventory and property, plant and equipment as a result of the dome collapse at Nucor Steel Louisiana. Nucor Steel Louisiana also had increased start-up costs in 2013 over 2012 as it began production in late December. An unplanned 18-day outage at our Trinidad DRI facility in early 2013 also contributed to lower profitability for the raw materials segment in 2013 as compared to 2012.

The decrease in results in Corporate/eliminations in 2013 was primarily due to a LIFO charge of $17.4 million in 2013 compared to a $155.9 million LIFO credit in 2012.

NONCONTROLLING INTERESTS

The 10% increase in noncontrolling interests from 2012 to 2013 was primarily attributable Nucor-Yamato Steel’s increased margins, which were primarily due to changes in product mix.

PROVISION FOR INCOME TAXES

The effective tax rate in 2013 was 26.0% compared with 30.5% in 2012. The change in the rate between 2012 and 2013 was primarily due to a $21.3 million out-of-period adjustment to the deferred tax balances recorded in 2013.

NET EARNINGS AND RETURN ON EQUITY

Nucor reported net earnings of $488.0 million, or $1.52 per diluted share, in 2013 compared to net earnings of $504.6 million, or $1.58 per diluted share, in 2012. Net earnings attributable to Nucor stockholders as a percentage of net sales were 3% in both 2013 and 2012. Return on average stockholders’ equity was 6% and 7% in 2013 and 2012, respectively.

LIQUIDITY AND CAPITAL RESOURCES

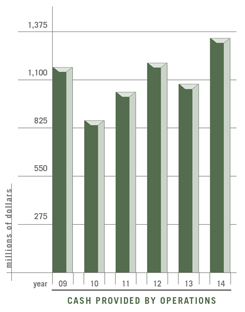

Nucor’s cash and cash equivalents and short-term investments position remained strong at $1.12 billion at the end of 2014. Approximately $156.1 million and $173.2 million of the cash and cash equivalents position at December 31, 2014 and December 31, 2013, respectively, was held by our majority-owned joint ventures. Cash flows provided by operating activities provide us with a significant source of liquidity. When needed, we have external short-term financing sources available, including the issuance of commercial paper and borrowings under our bank credit facilities. We also issue long-term debt from time to time.

In 2013, Nucor’s $1.5 billion revolving credit facility was amended and restated to extend the maturity date to August 2018, and the facility was undrawn at December 31, 2014. We believe our financial strength is a key strategic advantage among domestic steel producers, particularly during recessionary business cycles. We carry the highest credit ratings of any metals and mining company in North America, with an A rating from Standard and Poor’s and a Baa1 rating from Moody’s. Our credit ratings are dependent, however, upon a number of factors, both qualitative and quantitative, and are subject to change at any time. The disclosure of our credit ratings is made in order to enhance investors’ understanding of our sources of liquidity and the impact of our credit ratings on our cost of funds.

Based upon these factors, we expect to continue to have adequate access to the capital markets at a reasonable cost of funds for liquidity purposes when needed. This was evidenced when, during the fourth quarter of 2014, we issued approximately $300 million of commercial paper to partially fund the acquisition of Gallatin Steel Company. By the end of 2014, we had reduced the amount of commercial paper outstanding to approximately $151 million. Drawing from Nucor’s strong cash provided by operations, we expect to retire the remaining commercial paper in 2015. The next significant debt maturity is not until December 2017.

| | | | | | | | |

Selected Measures of Liquidity and Capital Resources | | | | | | |

| |

| | | (dollars in thousands) | |

| December 31, | | 2014 | | | 2013 | |

| | |

Cash and cash equivalents | | $ | 1,024,144 | | | $ | 1,483,252 | |

Short-term investments | | | 100,000 | | | | 28,191 | |

Working capital | | | 4,344,112 | | | | 4,449,830 | |

Current ratio | | | 3.1 | | | | 3.3 | |

| | |

| | | | | | | | | |

The current ratio was 3.1 at year end 2014 compared with 3.3 at year end 2013. The current ratio was negatively impacted by a 26% decrease from 2013 in cash and cash equivalents and short-term investments. The decrease in cash and cash equivalents and short-term investments was primarily due to cash paid for acquisitions of other companies, capital expenditures and dividends, partially offset by increased cash generated by operations. In addition, the $178.3 million increase in short-term debt from 2013, which was due mainly to the issuance of commercial paper, negatively affected the current ratio.

The current ratio benefited from a 14% increase in accounts receivable, a 5% increase in inventory and an 11% decrease in accounts payable as compared to year end 2013. The increase in accounts receivable was due primarily to the acquisition of Nucor Steel Gallatin, as well as a 2% increase in net sales in the fourth quarter of 2014 compared with the prior year fourth quarter. The net sales increase was the result of a 1% increase in both outside shipments and average sales price per ton in the fourth quarter of 2014 as compared with the fourth quarter of 2013. The increase in inventory from the previous year was mainly due to the addition of Nucor Steel Gallatin and an increase in inventory volumes on hand, partially offset by a decrease in scrap and iron ore prices in inventory from year end 2013. The decrease in scrap and iron ore prices was also a main driver of the decrease in accounts payable. In 2014, total accounts receivable turned approximately every five weeks and inventories turned approximately every seven weeks. These turnover rates are comparable to Nucor’s historical performance.

Funds provided by operations, cash and cash equivalents, short-term investments and new borrowings under existing credit facilities are expected to be adequate to meet future capital expenditure and working capital requirements for existing operations for at least the next 24 months.

| | |

| We have a simple capital structure with no off-balance sheet arrangements or relationships with unconsolidated special purpose entities that we believe could have a material impact on our financial condition or liquidity. | |  |

OPERATING ACTIVITIES Cash provided by operating activities was $1.34 billion, an increase of 25% compared with cash provided by operating activities of $1.08 billion in 2013. The primary reason for the change was higher net earnings, which included increased levels of depreciation expense due to significant capital projects being placed in service during 2014. Partially offsetting the increase in cash generated from higher earnings were changes in operating assets and liabilities that were ($400.2) million in 2014 compared with ($235.2) million in 2013. The funding of our working capital increased over the prior year period due mainly to increases in cash used to fund federal income taxes and accounts payable, somewhat offset by a decrease in cash used to fund the purchase of inventory. Federal income tax payments have increased due to Nucor’s increased profitability. The increased levels of cash used for accounts payable is due in large part to the change in accrued plant and equipment purchases. The decrease in cash used to fund the purchase of inventory is due to the decrease in scrap prices in inventory from year end 2013. | |

INVESTING ACTIVITIES

Our business is capital intensive; therefore, cash used in investing activities primarily represents capital expenditures for new facilities, the expansion and upgrading of existing facilities and the acquisition of other companies. Nucor invested $668.0 million in new facilities and expansion or upgrading of existing facilities in 2014 compared with $1.20 billion in 2013, a decrease of 44%. The decrease in capital expenditures is in large part due to the completion of our Louisiana DRI facility and reduced spending on our natural gas working interest drilling program. Additionally, Nucor invested $768.6 million in the acquisition of other companies in 2014, primarily Nucor Steel Gallatin (there were no acquisitions in 2013). Another factor contributing to the increase in cash used in investing activities was the net decrease of $421.0 million in proceeds from the sale of investments and restricted investments (net of purchases) and changes in restricted cash from 2013.

FINANCING ACTIVITIES

Cash used in financing activities in 2014 was $359.0 million compared with cash provided by financing activities of $196.0 million in 2013. In 2013, Nucor issued $500.0 million of 4.00% notes due in 2023 and $500.0 million of 5.2% notes due in 2043. Net of discounts, the prior year debt issuance increased cash provided by financing activities by $999.1 million. There were no issuances of long-term debt in 2014. However, mainly due to the issuance of commercial paper in 2014, the net change in short-term debt provided cash of $178.3 million compared with ($0.7) million in 2013. Additionally, cash used to repay debt maturities was only $5.4 million in 2014 compared to $250.0 million in the prior year.

In 2014, Nucor increased its quarterly base dividend, resulting in dividends paid of $475.1 million in 2014 ($471.0 million in 2013).

Although there were no repurchases in 2014 or 2013, approximately 27.2 million shares remain authorized for repurchase under the Company’s stock repurchase program.

Our credit facility includes only one financial covenant, which is a limit of 60% on the ratio of funded debt to total capitalization. In addition, the credit facility contains customary non-financial covenants, including a limit on Nucor’s ability to pledge the Company’s assets and a limit on consolidations, mergers and sales of assets. Our funded debt to total capital ratio was 36% at the end of 2014 and 2013, and we were in compliance with all other covenants under our credit facility.

MARKET RISK

Nucor’s largest exposure to market risk is in our steel mills and steel products segments. Our utilization rates for the steel mills and steel products facilities for the fourth quarter of 2014 were 76% and 61%, respectively. A significant portion of our steel and steel products segments sales are into the commercial, industrial and municipal construction markets. While we did see some improvement in some of these markets in 2014, they continue to be depressed when compared to historical levels. Our largest single customer in 2014 represented approximately 5% of sales and consistently pays within terms. In the raw materials segment, we are exposed to price fluctuations related to the purchase of scrap steel and iron ore. Our exposure to market risk is mitigated by the fact that our steel mills use a significant portion of the products of this segment.

Nucor’s tax-exempt industrial revenue bonds (IDRBs), including the Gulf Opportunity Zone bonds, have variable interest rates that are adjusted weekly. These IDRBs represent 23% of Nucor’s long-term debt outstanding at December 31, 2014. The remaining 77% of Nucor’s long-term debt is at fixed rates. Future changes in interest rates are not expected to significantly impact earnings. From time to time, Nucor makes use of interest rate swaps to manage interest rate risk. As of December 31, 2014, there were no such contracts outstanding. Nucor’s investment practice is to invest in securities that are highly liquid with short maturities. As a result, we do not expect changes in interest rates to have a significant impact on the value of our investment securities recorded as short-term investments.

Nucor also uses derivative financial instruments from time to time to partially manage its exposure to price risk related to natural gas purchases used in the production process as well as scrap, copper and aluminum purchased for resale to its customers. In addition, Nucor uses forward foreign exchange contracts from time to time to hedge cash flows associated with certain assets and liabilities, firm commitments and anticipated transactions. Nucor generally does not enter into derivative instruments for any purpose other than hedging the cash flows associated with specific volumes of commodities that will be purchased and processed or sold in future periods and hedging the exposures related to changes in the fair value of outstanding fixed-rate debt instruments and foreign currency transactions. Nucor recognizes all material derivative instruments in the consolidated balance sheets at fair value.

The Company is exposed to foreign currency risk primarily through its operations in Canada, Europe and Trinidad. We periodically use derivative contracts to mitigate the risk of currency fluctuations.

CONTRACTUAL OBLIGATIONS AND OTHER COMMERCIAL COMMITMENTS

The following table sets forth our contractual obligations and other commercial commitments as of December 31, 2014 for the periods presented:

| | | | | | | | | | | | | | | | | | | | |

| | | Payments Due By Period | |

| Contractual Obligations | | Total | | | 2015 | | | 2016 - 2017 | | | 2018 - 2019 | | | 2020 and thereafter | |

| | | | | |

Long-term debt | | | $ 4,376,900 | | | | $ 16,300 | | | | $ 600,000 | | | | $ 500,000 | | | | $3,260,600 | |

Estimated interest on long-term debt(1) | | | 2,308,005 | | | | 178,318 | | | | 353,684 | | | | 241,220 | | | | 1,534,783 | |

Capital leases | | | 27,648 | | | | 3,072 | | | | 6,144 | | | | 6,144 | | | | 12,288 | |

Operating leases | | | 85,389 | | | | 25,085 | | | | 32,113 | | | | 15,624 | | | | 12,567 | |

Raw material purchase commitments(2) | | | 2,958,520 | | | | 1,200,863 | | | | 1,204,309 | | | | 351,058 | | | | 202,290 | |

Utility purchase commitments(2) | | | 923,298 | | | | 261,918 | | | | 176,707 | | | | 117,932 | | | | 366,741 | |

Natural gas drilling commitments | | | 4,857,599 | | | | 18,600 | | | | 691,455 | | | | 724,860 | | | | 3,422,684 | |

Other unconditional purchase obligations(3) | | | 118,781 | | | | 100,800 | | | | 4,527 | | | | 3,386 | | | | 10,068 | |

Other long-term obligations(4) | | | 462,606 | | | | 295,995 | | | | 46,001 | | | | 32,744 | | | | 87,866 | |

| | | | | | | | | | | | | | | | | | | | |

Total contractual obligations | | | $16,118,746 | | | | $2,100,951 | | | | $3,114,940 | | | | $1,992,968 | | | | $8,909,887 | |

| | | | | | | | | | | | | | | | | | | | |

| | | | | |

| | | | | | | | | | | | | | | | | | | | | |

| | |

| (1) | | Interest is estimated using applicable rates at December 31, 2014 for Nucor’s outstanding fixed and variable rate debt. |

| (2) | | Nucor enters into contracts for the purchase of scrap and scrap substitutes, iron ore, electricity, natural gas and other raw materials and related services. These contracts include multi-year commitments and minimum annual purchase requirements and are valued at prices in effect on December 31, 2014, or according to the contract language. These contracts are part of normal operations and are reflected in historical operating cash flow trends. We do not believe such commitments will adversely affect our liquidity position. |

| (3) | | Purchase obligations include commitments for capital expenditures on operating machinery and equipment. |

| (4) | | Other long-term obligations include amounts associated with Nucor’s early-retiree medical benefits, management compensation and guarantees. |

| Note: | | In addition to the amounts shown in the table above, $63.0 million of unrecognized tax benefits have been recorded as liabilities, and we are uncertain as to if or when such amounts may be settled. Related to these unrecognized tax benefits, we have also recorded a liability for potential penalties and interest of $28.2 million at December 31, 2014. |

DIVIDENDS

Nucor has increased its base cash dividend every year since it began paying dividends in 1973. Nucor paid dividends of $1.48 per share in 2014 compared with $1.47 per share in 2013. In December 2014, the Board of Directors increased the base quarterly dividend to $0.3725 per share. The base quarterly dividend has more than tripled since the end of 2007. In February 2015, the Board of Directors declared Nucor’s 168th consecutive quarterly cash dividend of $0.3725 per share payable on May 11, 2015 to stockholders of record on March 31, 2015.

OUTLOOK

In 2015, we will continue to take advantage of our position of strength to grow Nucor’s long-term earnings power and shareholder value despite a U.S. economy burdened by a challenging regulatory and overall business environment. We have invested significant capital into our business since the last cyclical peak in 2008. We have done so over a broad range of strategic investments that will further enhance our ability to grow Nucor’s long-term earnings power by expanding our product portfolios into higher value-added offerings that are less vulnerable to imports, improving our highly variable low-cost structure and building upon our market leadership positions. With many of these capital projects completed and ready to yield results, we will focus on execution in order to generate strong returns on these investments.

Although macro-level uncertainties in world markets will almost certainly affect both global and domestic growth, we anticipate sales and profitability on par with 2014. Utilization rates, which grew slightly in 2014 compared to 2013, have slowed in early 2015. Although we expect the first quarter operating results to be similar to the first quarter 2014 results, they will be in the face of significant headwinds that developed for the steel industry late in 2014. The collapse in global oil prices has triggered inventory reductions among pipe and tube producers serving energy markets, an important customer group for Nucor as well as the domestic steel industry. Also, given the relative health of the domestic steel markets, imports have increased dramatically as we have entered 2015. We are anticipating a more positive trend in earnings as we enter into the second quarter and then into the second half of the year. We are therefore cautiously optimistic regarding full-year volume, pricing and profitability. We are encouraged by an improvement of approximately 10% in backlog tons at our downstream steel products segment over 2013 and we believe several end-use markets such as automotive, energy and nonresidential construction will experience some real demand improvement that will gain momentum throughout 2015. However, the effect this improvement in demand will have on our operating rates will be challenged by excess foreign steel capacity and the threat of continued increases in imported steel. We expect scrap prices to fall significantly in early 2015 and that we will continue to experience fluctuations in raw material costs throughout the year. We have made significant investments in our raw material segment and will continue to utilize our unmatched global supply chain to optimize our raw material costs.

We are committed to executing on the opportunities we see ahead to reward Nucor shareholders with very attractive long-term returns on their valuable capital invested in our company. Nucor is the only steel producer in North America with the extremely important competitive advantage of an investment-grade credit rating. Our industry-leading financial strength allows us to support investments in our facilities that will prepare us for increased profitability as we enter into more favorable market conditions. In 2015, as we have in our past, we will allocate capital to investments that build our long-term earnings power. Capital expenditures are currently projected to be approximately $500 million in 2015, approximating our spend in 2014 but significantly lower than in 2013. This decrease is mainly due to the joint agreement with Encana to suspend drilling new natural gas wells through the end of 2015. Included in this $500 million total are primarily investments in our core operations to expand our product offerings and keep them state-of-the-art and globally competitive.

CRITICAL ACCOUNTING POLICIES AND ESTIMATES

Our discussion and analysis of our financial condition and results of operations are based upon our consolidated financial statements, which have been prepared in accordance with accounting principles generally accepted in the United States of America. The preparation of these financial statements requires us to make estimates and assumptions that affect the reported amounts of assets and liabilities, the disclosure of contingent assets and liabilities at year end and the reported amount of revenues and expenses during the year. On an ongoing basis, we evaluate our estimates, including those related to the valuation allowances for receivables, the carrying value of non-current assets, reserves for environmental obligations and income taxes. Our estimates are based on historical experience and various other assumptions that we believe to be reasonable under the circumstances, the results of which form the basis for making judgments about the carrying values of assets and liabilities that are not readily apparent from other sources. Accordingly, actual costs could differ materially from these estimates under different assumptions or conditions. We believe the following critical accounting policies affect our significant judgments and estimates used in the preparation of our consolidated financial statements.

ALLOWANCES FOR DOUBTFUL ACCOUNTS

We maintain allowances for doubtful accounts for estimated losses resulting from the inability of our customers to make required payments. If the financial condition of our customers were to deteriorate, resulting in an impairment of their ability to make payments, additional allowances may be required.

INVENTORIES

Inventories are stated at the lower of cost or market. All inventories held by the parent company and Nucor-Yamato Steel Company are valued using the LIFO method of accounting except for supplies that are consumed indirectly in the production process, which are valued using the first-in, first-out (FIFO) method of accounting. All inventories held by the parent company’s other subsidiaries are valued using the FIFO method of accounting. The Company records any amount required to reduce the carrying value of inventory to net realizable value as a charge to cost of products sold.