UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT

OF

REGISTERED MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number: 811-3916

Name of Registrant: Vanguard Specialized Funds

Address of Registrant:

P.O. Box 2600

Valley Forge, PA 19482

Name and address of agent for service:

Heidi Stam, Esquire

P.O. Box 876

Valley Forge, PA 19482

Registrant’s telephone number, including area code: (610) 669-1000

Date of fiscal year end: January 31

Date of reporting period: February 1, 2011 – July 31, 2011

Item 1: Reports to Shareholders

| Vanguard Energy Fund |

| Semiannual Report |

| July 31, 2011 |

|

> Vanguard Energy Fund returned about 4% for the six months ended July 31, 2011.

> The fund’s return beat that of its benchmark index and the average return of its peer funds.

> The top contributors to performance were companies that provide energy equipment and those engaged in oil and gas exploration and production.

| Contents | |

| Your Fund’s Total Returns. | 1 |

| Chairman’s Letter. | 2 |

| Advisors’ Report. | 6 |

| Fund Profile. | 10 |

| Performance Summary. | 12 |

| Financial Statements. | 13 |

| About Your Fund’s Expenses. | 27 |

| Trustees Approve Advisory Arrangements. | 29 |

| Glossary. | 31 |

Please note: The opinions expressed in this report are just that—informed opinions. They should not be considered promises or advice.

Also, please keep in mind that the information and opinions cover the period through the date on the front of this report. Of course, the risks of investing in your fund are spelled out in the prospectus.

See the Glossary for definitions of investment terms used in this report.

Cover photograph: Jean Maher.

Your Fund’s Total Returns

Six Months Ended July 31, 2011

| Total | |

| Returns | |

| Vanguard Energy Fund | |

| Investor Shares | 4.34% |

| Admiral™ Shares | 4.38 |

| MSCI ACWI Energy Index | 2.59 |

| Global Natural Resources Funds Average | 0.13 |

| Global Natural Resources Funds Average: Derived from data provided by Lipper Inc. | |

Admiral Shares carry lower expenses and are available to investors who meet certain account-balance requirements.

Your Fund’s Performance at a Glance

January 31, 2011 , Through July 31, 2011

| Distributions Per Share | ||||

| Starting | Ending | Income | Capital | |

| Share Price | Share Price | Dividends | Gains | |

| Vanguard Energy Fund | ||||

| Investor Shares | $69.20 | $71.69 | $0.018 | $0.503 |

| Admiral Shares | 129.93 | 134.64 | 0.043 | 0.944 |

1

Chairman’s Letter

Dear Shareholder,

Vanguard Energy Fund returned about 4% for the six months ended July 31, 2011. The fund outperformed both its benchmark index and the average return of global natural resources funds.

A surge in crude oil prices in the first half of the period helped energy stocks outpace the broad U.S. market. The Energy Fund also benefited from the advisors’ stock selection among oil and gas exploration companies and firms that provide energy equipment and services.

I want to note that on May 11, we lowered the minimum required investment for the Investor Shares of several Vanguard funds, including the Energy Fund, to $3,000. This was done as part of our ongoing effort to simplify the offering of Investor Shares and to increase the accessibility of our funds.

Stocks worldwide crept higher in a treacherous marketplace

Global stock markets struggled to find direction during the past six months, as every positive signal seemed to be paired with its negative. The good news included surprisingly strong corporate profits, which proved to be a source of investor optimism through much of the period.

The counterpoint was a series of increasingly glum economic reports. Expectations that the U.S. economic expansion would accelerate in the second half of the year gave way to anxiety about the possibility of recession.

2

The Dow Jones U.S. Total Stock Market Index finished the period with a return of 1.55%. Across the globe, stock returns were similarly modest.

Bonds rallied in the U.S. market as investors sought safety

Bond prices climbed amid the turbulence. Investors sought refuge from a collection of troubles: Europe’s debt dramas, economic shocks produced by the Japanese tsunami and its aftermath, and prolonged debate over raising the U.S. debt ceiling. For the full six months, the broad U.S. taxable bond market returned more than 4%. (Rising prices are a mixed blessing, of course; they imply lower yields on future investment.)

The yields on money market instruments such as Treasury bills remained near 0%, consistent with the Federal Reserve’s target for short-term interest rates.

The U.S. credit downgrade: a cause for concern, not panic

On August 5, after the close of our reporting period, Standard & Poor’s downgraded its credit rating of U.S. debt from AAA to AA+. S&P said its action was prompted, in large part, by concern about “the effectiveness, stability, and predictability of American policymaking and political institutions”— in other words, the political gridlock on vivid display during the debt-ceiling debate.

| Market Barometer | |||

| Total Returns | |||

| Periods Ended July 31, 2011 | |||

| Six | One | Five Years | |

| Months | Year | (Annualized) | |

| Stocks | |||

| Russell 1000 Index (Large-caps) | 1.62% | 20.68% | 2.80% |

| Russell 2000 Index (Small-caps) | 2.63 | 23.92 | 4.00 |

| Dow Jones U.S. Total Stock Market Index | 1.55 | 20.83 | 3.27 |

| MSCI All Country World Index ex USA (International) | 1.39 | 17.36 | 3.18 |

| Bonds | |||

| Barclays Capital U.S. Aggregate Bond Index (Broad | |||

| taxable market) | 4.23% | 4.44% | 6.57% |

| Barclays Capital Municipal Bond Index (Broad | |||

| tax-exempt market) | 6.27 | 3.24 | 4.90 |

| Citigroup Three-Month U.S. Treasury Bill Index | 0.05 | 0.13 | 1.78 |

| CPI | |||

| Consumer Price Index | 2.59% | 3.63% | 2.11% |

3

The downgrade was controversial, and the other major rating agencies reaffirmed their decision to continue giving the highest ratings to U.S. debt. At Vanguard, our credit analysts and economists regularly assess the financial strength of the United States and other sovereign borrowers. Our confidence in the “full faith and credit” of the U.S. government remains unshaken, and we have cautioned investors against overreacting to the S&P downgrade.

Oil and natural gas price volatility provided challenges, opportunities

Early in the semiannual period, investors grew fearful of supply disruptions resulting from conflicts in the Middle East and North Africa and the natural disasters in Japan. These concerns pushed up the price of West Texas Intermediate crude oil to more than $113 a barrel in April—its highest level since 2008.

Vanguard Energy Fund’s stocks climbed nearly 10% in the first three months of the period, but then retreated, losing half their gains by July. Steep gasoline prices led consumers to cut back their driving, and the faltering of the U.S. economic recovery further weakened demand, leading to a decline in crude oil prices.

The largest proportion of the Energy Fund’s assets—about 50%, on average—is invested in integrated oil and gas companies. Although many of these companies reported strong earnings for the second quarter of 2011, they

Expense Ratios

Your Fund Compared With Its Peer Group

| Investor | Admiral | Peer Group | |

| Shares | Shares | Average | |

| Energy Fund | 0.34% | 0.28% | 1.50% |

The fund expense ratios shown are from the prospectus dated May 26, 2011, and represent estimated costs for the current fiscal year. For the six months ended July 31, 2011, the fund’s annualized expense ratios were 0.34% for Investor Shares and 0.28% for Admiral Shares. The peer-group expense ratio is derived from data provided by Lipper Inc. and captures information through year-end 2010.

Peer group: Global Natural Resources Funds.

4

ended up contributing only about a fifth of the fund’s return for the fiscal six months. Several turned in negative returns, battered by the decline in oil prices and a slump in production caused by, among other factors, limited access to war-torn areas such as Libya and drilling restrictions in the Gulf of Mexico.

Exxon Mobil, the fund’s largest holding—representing about 8% of its assets, on average—had a flat return for the six months, in part because of costs associated with its aggressive push into the natural gas business, which has struggled with stagnant prices. Last year, Exxon acquired XTO Energy, making it the largest U.S. natural gas producer.

The Energy Fund’s top performers for the period were natural gas producers. Although natural gas prices declined slightly during the half-year, the fund held sizable shares of a few strong performers in that segment that helped boost its results above those of its benchmark index. One example was Cabot Oil & Gas, an independent natural gas producer, which represented about 2% of the fund’s assets on average but contributed more than a quarter of the overall return.

Providers of oil and gas equipment and services also were strong contributors. Several of these companies turned in double-digit returns for the period, as they have benefited from the drilling boom in natural gas shale formations throughout the United States.

Diversification and perspective are important in volatile markets

The volatility in the stock market in recent months has tested investors’ mettle. As an investor in the Energy Fund, you’re probably familiar with the market’s potential for sharp and unpredictable swings.

At Vanguard, our guidance is the same for all investment environments: We believe investors should pursue their long-term goals with a portfolio that includes stocks, bonds, and money market funds in proportions consistent with their personal risk tolerance and time horizon. This balanced approach has demonstrated its wisdom over decades.

Vanguard Energy Fund, with its wide exposure to global energy companies, can play a supporting role in such a well-balanced portfolio. And while its narrow focus can leave it vulnerable to notable share price fluctuations, in the context of a larger, well-diversified portfolio, the fund can help dampen overall volatility. That’s because one sector can behave very differently from other parts of the market.

As always, thank you for continuing to entrust your assets to Vanguard.

Sincerely,

F. William McNabb III

Chairman and Chief Executive Officer

August 10, 2011

5

Advisors’ Report

Vanguard Energy Fund returned 4.34% for Investor Shares and 4.38% for Admiral Shares in the six months ended July 31, 2011. Your fund is managed by two advisors, a strategy that enhances the fund’s diversification by providing exposure to distinct, yet complementary, investment approaches. It’s not uncommon for different advisors to have different views about individual securities or the broader investment environment.

The advisors, the amount and percentage of fund assets each manages, and brief descriptions of their investment strategies are presented in the table below. The advisors have also provided a discussion of the investment environment that existed during the year and of how their portfolio positioning reflects this assessment. These reports were prepared on August 17, 2011.

| Vanguard Energy Fund Investment Advisors | |||

| Fund Assets Managed | |||

| Investment Advisor | % | $ Million | Investment Strategy |

| Wellington Management | 95 | 13,549 | Emphasizes long-term total-return opportunities from |

| Company, LLP | the various energy subsectors: international oils, | ||

| foreign integrated oils and foreign producers, North | |||

| American producers, oil services and equipment, | |||

| transportation and distribution, and refining and | |||

| marketing. | |||

| Vanguard Quantitative Equity | 3 | 384 | Employs a quantitative fundamental management |

| Group | approach, using models that assess valuation, market | ||

| sentiment, earnings quality and growth, and | |||

| management decisions of companies relative to their | |||

| peers. | |||

| Cash Investments | 2 | 260 | These short-term reserves are invested by Vanguard in |

| equity index products to simulate investments in stock. | |||

| Each advisor may also maintain a modest cash | |||

| position. | |||

6

Wellington Management Company, LLP

Portfolio Manager:

Karl E. Bandtel, Senior Vice President

For the six months, U.S. equities returned a tepid 1.46% as measured by the S&P 500 Index. The broad equity market trailed energy stocks during a period marked by increasing risk aversion and heightened volatility. Ongoing sovereign-debt concerns and monetary-policy tightening in Europe, as well as the possibility of slower global economic growth, weighed on markets. The political uncertainty concerning the U.S. debt ceiling unnerved investors further as the half-year drew to a close.

Commodity prices fluctuated during the period. Unrest in the Middle East and North Africa contributed to increases in oil prices early on, but prices fell after Western governments decided to release strategic reserves. Crude oil finished the period higher than it started, closing at $96 a barrel (West Texas Intermediate).

The price of natural gas in the United States finished the period near $4.25 per million BTUs (Henry Hub), not far from where it started. Abundant U.S. shale formations continued to provide low-cost supplies. Abroad, rising demand from emerging markets and the aftermath of the natural and nuclear disasters in Japan kept prices higher in Europe and Asia.

Our position in shares of Cabot Oil & Gas, a producer that focuses on natural gas, contributed strongly to our portfolio’s performance. Wellhead results topped

the market’s expectations, increasing investors’ confidence in the quality of the firm’s resource base. We see a strong outlook for production growth as the completion of significant infrastructure projects unlocks constraints on natural gas production in the firm’s high-quality Marcellus shale acreage. We trimmed our position in Cabot as the stock rose.

Another notable contributor was Japan-based Inpex, an oil and gas exploration and production firm. The company’s stock advanced as the outlook for its Ichthys project improved. Inpex also benefited from the rising demand for liquefied natural gas.

On the other hand, our position in Total, a multinational integrated oil and gas company, detracted from six-month performance. The stock fell on declining production. Given the low valuation, we see attractive upside potential. The company also has a high dividend yield, an excellent balance sheet, and potential for good future production from new fields.

Shares of Petroleo Brasileiro, Brazil’s state-owned oil company, also declined during the period. Concerns about increased local-content requirements, high capital expenditures, and weak returns on downstream investments weighed on the stock. We continue to hold the company based on an attractive valuation and the firm’s high-quality project inventory, including its leverage in the offshore Brazil pre-salt layer, one of the most productive oil resources in the world.

7

Although our long-term outlook for the energy sector is favorable, we would urge caution regarding the near-term direction of commodity prices and the volatility that accompanies investing in energy stocks.

Looking ahead, we believe that crude oil prices will likely continue to vary in tandem with changes to the outlook for both supply and demand. While pricing for natural gas remains driven by regional factors, we think the wide price arbitrage with other fuels and changing views about nuclear power generation will drive global demand in the long term.

The portfolio remains focused on upstream companies—those engaged in exploration and production—and skewed in favor of low-cost producers with compelling valuations based on our assessment of their respective long-term resource bases. We believe many of these companies have the ability to create value absent generally rising commodity prices.

Our investment process remains steady in its emphasis on large-capitalization integrated oil firms as well as exploration and production companies. Maintaining a large-cap, low-turnover bias, this global portfolio remains diversified across the energy subsectors.

Vanguard Quantitative Equity Group

Portfolio Manager:

James D. Troyer, CFA, Principal

The energy stocks in our benchmark started the period strongly, extending the solid performance of the previous fiscal year. Along with equities in general, however, these stocks then reversed their trend and finished the half-year with a smaller gain.

Within the energy sector, emerging market stocks performed best, followed by stocks in the Pacific region. European energy companies continued to struggle, while U.S. companies slightly outperformed. These results underscore the point that strong corporate profit growth and earnings during the last two quarters alone have not been enough to convince investors that the economy is on a sustainable growth path, especially in view of the many unsettling political and economic events worldwide in recent months.

While portfolio performance is influenced by such macro factors, our strategy is not to maintain a view on the overall market for energy shares. We also avoid making calls on relative country performance. Rather, our investment process seeks to identify individual stocks that we believe

8

are undervalued or that have shown price improvement relative to peers on the basis of recent earnings pronouncements. Our risk-control process then neutralizes the portfolio’s exposure to market-capitalization, volatility, and industry risks in comparison with our energy benchmark. In our view, such risk exposures are not justified by the rewards available.

For the period, our most successful holdings represented regions across the globe: Halliburton (+22%) and Chesapeake Energy (+17%) in the United States; Petronas Dagangan (+52%) in Malaysia; and Tatneft (+44%) in Russia. Equally important to the portfolio’s performance was our ability to limit exposure to underperforming stocks such as Canada’s Cameco (–35%).

The portfolio’s results were dampened by our overweighting of Hess (–18%) and Arch Coal (–25%). Our underweighting of better-performing stocks such as China Shenhua Energy (+27%) also held back performance relative to the benchmark.

An analysis of the results from our stock selection model shows that, of the two core components described earlier, our valuation signal contributed most to the overall return, but our signal related to price and earnings improvements also had positive impact. This outcome strengthens our confidence in the diversified approach that we employ in constructing a portfolio, which we believe will prove its merit in the long term.

9

Energy Fund

Fund Profile

As of July 31, 2011

| Share-Class Characteristics | |||

| Investor | Admiral | ||

| Shares | Shares | ||

| Ticker Symbol | VGENX | VGELX | |

| Expense Ratio1 | 0.34% | 0.28% | |

| 30-Day SEC Yield | 1.35% | 1.41% | |

| Portfolio Characteristics | |||

| DJ | |||

| MSCI | U.S. Total | ||

| ACWI | Market | ||

| Fund | Energy | Index | |

| Number of Stocks | 135 | 168 | 3,753 |

| Median Market Cap | $47.4B | $80.3B | $31.4B |

| Price/Earnings Ratio | 15.5x | 13.0x | 16.3x |

| Price/Book Ratio | 1.9x | 1.8x | 2.2x |

| Return on Equity | 20.1% | 20.8% | 19.0% |

| Earnings Growth Rate | -5.4% | -2.2% | 6.3% |

| Dividend Yield | 1.8% | 2.4% | 1.8% |

| Foreign Holdings | 37.9% | 54.5% | 0.0% |

| Turnover Rate | |||

| (Annualized) | 19% | — | — |

| Short-Term Reserves | 1.0% | — | — |

| Volatility Measures | ||

| DJ | ||

| Spliced | U.S. Total | |

| Energy | Market | |

| Index | Index | |

| R-Squared | 0.90 | 0.77 |

| Beta | 1.13 | 1.09 |

| These measures show the degree and timing of the fund’s fluctuations compared with the indexes over 36 months. | ||

| Ten Largest Holdings (% of total net assets) | ||

| Exxon Mobil Corp. | Integrated Oil & | |

| Gas | 7.5% | |

| Chevron Corp. | Integrated Oil & | |

| Gas | 4.6 | |

| Royal Dutch Shell plc | Integrated Oil & | |

| Gas | 4.5 | |

| Occidental Petroleum | Integrated Oil & | |

| Corp. | Gas | 4.4 |

| BP plc | Integrated Oil & | |

| Gas | 3.6 | |

| Schlumberger Ltd. | Oil & Gas | |

| Equipment & | ||

| Services | 2.9 | |

| Baker Hughes Inc. | Oil & Gas | |

| Equipment & | ||

| Services | 2.7 | |

| Halliburton Co. | Oil & Gas | |

| Equipment & | ||

| Services | 2.7 | |

| Total SA | Integrated Oil & | |

| Gas | 2.6 | |

| Consol Energy Inc. | Coal & Consumable | |

| Fuels | 2.5 | |

| Top Ten | 38.0% | |

| The holdings listed exclude any temporary cash investments and equity index products. | ||

1 The expense ratios shown are from the prospectus dated May 26, 2011, and represent estimated costs for the current fiscal year. For the six months ended July 31, 2011, the annualized expense ratios were 0.34% for Investor Shares and 0.28% for Admiral Shares.

10

Energy Fund

| Subindustry Diversification (% of equity exposure) | ||

| MSCI | ||

| ACWI | ||

| Fund | Energy | |

| Coal & Consumable Fuels | 4.8% | 3.2% |

| Consumer Staples | 0.3 | 0.0 |

| Industrials | 0.9 | 0.0 |

| Integrated Oil & Gas | 47.1 | 56.7 |

| Oil & Gas Drilling | 1.6 | 1.9 |

| Oil & Gas Equipment & | ||

| Services | 11.2 | 10.3 |

| Oil & Gas Exploration & | ||

| Production | 29.3 | 20.4 |

| Oil & Gas Refining & | ||

| Marketing | 2.8 | 4.1 |

| Oil & Gas Storage & | ||

| Transportation | 1.2 | 3.4 |

| Other | 0.8 | 0.0 |

| Market Diversification (% of equity exposure) | ||

| Europe | ||

| United Kingdom | 11.1% | |

| France | 2.6 | |

| Norway | 1.4 | |

| Italy | 1.4 | |

| Other | 1.1 | |

| Subtotal | 17.6% | |

| Pacific | ||

| Japan | 1.9% | |

| Other | 0.2 | |

| Subtotal | 2.1% | |

| Emerging Markets | ||

| Russia | 2.8% | |

| China | 2.5 | |

| Brazil | 2.1 | |

| Other | 1.5 | |

| Subtotal | 8.9% | |

| North America | ||

| United States | 61.8% | |

| Canada | 9.6 | |

| Subtotal | 71.4% | |

11

Energy Fund

Performance Summary

All of the returns in this report represent past performance, which is not a guarantee of future results that may be achieved by the fund. (Current performance may be lower or higher than the performance data cited. For performance data current to the most recent month-end, visit our website at vanguard.com/performance.) Note, too, that both investment returns and principal value can fluctuate widely, so an investor’s shares, when sold, could be worth more or less than their original cost. The returns shown do not reflect taxes that a shareholder would pay on fund distributions or on the sale of fund shares.

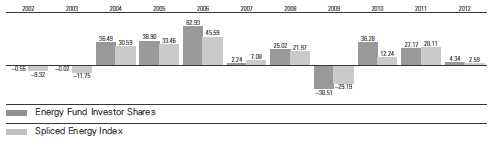

Fiscal-Year Total Returns (%): January 31, 2001, Through July 31, 2011

Note: For 2012, performance data reflect the six months ended July 31, 2011.

Average Annual Total Returns: Periods Ended June 30, 2011

This table presents returns through the latest calendar quarter—rather than through the end of the fiscal period.

Securities and Exchange Commission rules require that we provide this information.

| Inception | One | Five | Ten | |

| Date | Year | Years | Years | |

| Investor Shares | 5/23/1984 | 45.57% | 6.78% | 15.57% |

| Admiral Shares | 11/12/2001 | 45.66 | 6.85 | 16.601 |

| 1 Return since inception. | ||||

Vanguard fund returns do not reflect the 1% fee on redemptions of shares held for less than one year.

See Financial Highlights for dividend and capital gains information.

12

Energy Fund

Financial Statements (unaudited)

Statement of Net Assets

As of July 31, 2011

The fund reports a complete list of its holdings in regulatory filings four times in each fiscal year, at the quarter-ends. For the second and fourth fiscal quarters, the lists appear in the fund’s semiannual and annual reports to shareholders. For the first and third fiscal quarters, the fund files the lists with the Securities and Exchange Commission on Form N-Q. Shareholders can look up the fund’s Forms N-Q on the SEC’s website at sec.gov. Forms N-Q may also be reviewed and copied at the SEC’s Public Reference Room (see the back cover of this report for further information).

| Market | |||

| Value | |||

| Shares | ($000) | ||

| Common Stocks (97.6%)1 | |||

| United States (59.7%) | |||

| Energy Equipment & Services (11.1%) | |||

| Schlumberger Ltd. | 4,562,564 | 412,319 | |

| Baker Hughes Inc. | 4,970,650 | 384,629 | |

| Halliburton Co. | 7,006,162 | 383,447 | |

| * | Weatherford | ||

| International Ltd. | 5,535,900 | 121,347 | |

| National Oilwell | |||

| Varco Inc. | 1,431,876 | 115,366 | |

| SEACOR Holdings Inc. | 941,108 | 94,450 | |

| Noble Corp. | 1,728,325 | 63,723 | |

| Helmerich & Payne Inc. | 42,200 | 2,914 | |

| Transocean Ltd. | 6,210 | 382 | |

| 1,578,577 | |||

| Exchange-Traded Fund (0.5%) | |||

| ^,2 | Vanguard Energy ETF | 663,000 | 74,462 |

| Oil, Gas & Consumable Fuels (48.1%) | |||

| Coal & Consumable Fuels (3.7%) | |||

| Consol Energy Inc. | 6,611,200 | 354,360 | |

| Peabody Energy Corp. | 3,017,200 | 173,399 | |

| Arch Coal Inc. | 68,400 | 1,751 | |

| Integrated Oil & Gas (19.7%) | |||

| Exxon Mobil Corp. | 13,338,769 | 1,064,300 | |

| Chevron Corp. | 6,326,235 | 658,055 | |

| Occidental | |||

| Petroleum Corp. | 6,322,161 | 620,710 | |

| ConocoPhillips | 4,405,209 | 317,131 | |

| Hess Corp. | 1,835,839 | 125,865 | |

| Murphy Oil Corp. | 20,570 | 1,321 | |

| Oil & Gas Exploration & Production (22.3%) | |||

| EOG Resources Inc. | 3,371,986 | 343,943 | |

| Cabot Oil & Gas Corp. | 4,551,731 | 337,192 | |

| Anadarko | |||

| Petroleum Corp. | 3,204,930 | 264,599 | |

| Market | |||

| Value | |||

| Shares | ($000) | ||

| Noble Energy Inc. | 2,631,900 | 262,348 | |

| Devon Energy Corp. | 3,249,407 | 255,728 | |

| EQT Corp. | 3,475,900 | 220,650 | |

| Chesapeake Energy Corp. | 5,821,137 | 199,956 | |

| * | Denbury Resources Inc. | 9,771,344 | 188,782 |

| Apache Corp. | 1,515,300 | 187,473 | |

| Marathon Oil Corp. | 5,406,991 | 167,455 | |

| * | Ultra Petroleum Corp. | 3,113,236 | 145,762 |

| Range Resources Corp. | 2,029,100 | 132,216 | |

| Pioneer Natural | |||

| Resources Co. | 996,600 | 92,674 | |

| * | Newfield Exploration Co. | 1,320,203 | 89,008 |

| QEP Resources Inc. | 1,681,618 | 73,705 | |

| * | Southwestern Energy Co. | 1,642,000 | 73,168 |

| * | Whiting Petroleum Corp. | 821,300 | 48,128 |

| * | Gran Tierra Energy Inc. | 6,354,100 | 44,291 |

| * | Forest Oil Corp. | 1,221,500 | 31,759 |

| * | Plains Exploration & | ||

| Production Co. | 67,600 | 2,637 | |

| Oil & Gas Refining & Marketing (1.7%) | |||

| Valero Energy Corp. | 4,946,212 | 124,249 | |

| * | Marathon | ||

| Petroleum Corp. | 2,698,345 | 118,160 | |

| Oil & Gas Storage & Transportation (0.7%) | |||

| El Paso Corp. | 2,807,100 | 57,686 | |

| ^ | Nordic American | ||

| Tankers Ltd. | 1,894,515 | 38,800 | |

| Williams Cos. Inc. | 131,800 | 4,178 | |

| Spectra Energy Corp. | 2,100 | 57 | |

| 6,821,496 | |||

| Total United States | 8,474,535 | ||

| International (37.9%) | |||

| Argentina (0.5%) | |||

| YPF SA ADR | 1,800,200 | 76,634 | |

13

Energy Fund

| Market | |||

| Value | |||

| Shares | ($000) | ||

| Australia (0.2%) | |||

| Oil Search Ltd. | 3,897,262 | 29,242 | |

| Caltex Australia Ltd. | 136,558 | 1,597 | |

| Woodside Petroleum Ltd. | 26,520 | 1,118 | |

| 31,957 | |||

| Brazil (2.1%) | |||

| Petroleo Brasileiro | |||

| SA ADR | 7,729,505 | 262,571 | |

| Cosan Ltd. | 2,087,916 | 25,744 | |

| Petroleo Brasileiro | |||

| SA Prior Pfd. | 314,504 | 4,758 | |

| Petroleo Brasileiro SA | 222,022 | 3,722 | |

| Petroleo Brasileiro | |||

| SA ADR Type A | 44,920 | 1,380 | |

| 298,175 | |||

| Canada (9.5%) | |||

| Canadian Natural | |||

| Resources Ltd. | 7,430,318 | 299,368 | |

| Cenovus Energy Inc. | 6,204,800 | 237,954 | |

| Suncor Energy Inc. | 5,319,812 | 203,323 | |

| Encana Corp. | 3,543,100 | 103,777 | |

| Husky Energy Inc. | 2,980,200 | 83,437 | |

| Imperial Oil Ltd. | 1,736,477 | 76,457 | |

| Penn West | |||

| Petroleum Ltd. | 2,911,421 | 64,954 | |

| TransCanada Corp. | 1,472,896 | 61,879 | |

| Progress Energy | |||

| Resources Corp. | 3,943,800 | 57,210 | |

| Cameco Corp. | 1,814,500 | 48,193 | |

| Talisman Energy Inc. | 1,442,173 | 26,264 | |

| * | Legacy Oil & Gas Inc. | 1,633,200 | 19,333 |

| Niko Resources Ltd. | 237,550 | 16,337 | |

| * | MEG Energy Corp. | 277,517 | 14,947 |

| Suncor Energy Inc. | 220,134 | 8,437 | |

| Pacific Rubiales | |||

| Energy Corp. | 208,500 | 5,997 | |

| Petrominerales Ltd. | 183,000 | 5,838 | |

| Imperial Oil Ltd. | 71,500 | 3,143 | |

| Canadian Natural | |||

| Resources Ltd. | 75,378 | 3,044 | |

| ^ | PetroBakken Energy Ltd. | ||

| Class A | 140,400 | 2,066 | |

| Cenovus Energy Inc. | 27,139 | 1,043 | |

| ^ | Crescent Point Energy Corp. | 22,000 | 989 |

| Encana Corp. | 19,539 | 573 | |

| Enbridge Inc. | 17,100 | 561 | |

| * | Tourmaline Oil Corp. | 5,700 | 213 |

| 1,345,337 | |||

| China (2.5%) | |||

| PetroChina Co. Ltd. ADR | 1,308,000 | 186,037 | |

| China Shenhua | |||

| Energy Co. Ltd. | 16,317,000 | 81,815 | |

| Beijing Enterprises | |||

| Holdings Ltd. | 13,271,000 | 67,002 | |

| CNOOC Ltd. | 2,818,717 | 6,274 | |

| Market | |||

| Value | |||

| Shares | ($000) | ||

| PetroChina Co. Ltd. | 3,746,000 | 5,345 | |

| Yanzhou Coal | |||

| Mining Co. Ltd. | 742,000 | 2,843 | |

| China Oilfield | |||

| Services Ltd. | 1,164,000 | 2,036 | |

| 351,352 | |||

| France (2.6%) | |||

| Total SA ADR | 6,523,600 | 352,731 | |

| Total SA | 264,373 | 14,289 | |

| 367,020 | |||

| Hungary (0.0%) | |||

| * | MOL Hungarian | ||

| Oil and Gas plc | 21,197 | 2,275 | |

| India (0.8%) | |||

| Reliance Industries Ltd. | 5,975,772 | 111,758 | |

| Indonesia (0.0%) | |||

| Bumi Resources Tbk PT | 6,894,500 | 2,461 | |

| Italy (1.4%) | |||

| ENI SPA ADR | 3,860,350 | 167,076 | |

| ENI SPA | 1,223,968 | 26,598 | |

| Saipem SPA | 68,494 | 3,569 | |

| 197,243 | |||

| Japan (1.9%) | |||

| Inpex Corp. | 32,908 | 255,449 | |

| JX Holdings Inc. | 359,500 | 2,599 | |

| Idemitsu Kosan Co. Ltd. | 20,200 | 2,346 | |

| TonenGeneral Sekiyu KK | 176,000 | 2,211 | |

| Showa Shell Sekiyu KK | 227,500 | 2,190 | |

| Japan Petroleum | |||

| Exploration Co. | 15,200 | 774 | |

| Sumitomo Metal | |||

| Industries Ltd. | 69,000 | 165 | |

| 265,734 | |||

| Malaysia (0.0%) | |||

| Petronas Dagangan Bhd. | 399,000 | 2,395 | |

| Netherlands (0.3%) | |||

| Koninklijke Vopak NV | 719,642 | 35,916 | |

| SBM Offshore NV | 95,998 | 2,295 | |

| 38,211 | |||

| Norway (1.4%) | |||

| ^ | Statoil ASA ADR | 6,604,800 | 162,280 |

| * | Petroleum Geo- | ||

| Services ASA | 2,155,416 | 34,956 | |

| Statoil ASA | 47,651 | 1,175 | |

| 198,411 | |||

| Poland (0.0%) | |||

| * | Polski Koncern | ||

| Naftowy Orlen SA | 143,435 | 2,404 | |

| * | Grupa Lotos SA | 130,446 | 1,788 |

| 4,192 | |||

14

Energy Fund

| Market | ||

| Value | ||

| Shares | ($000) | |

| Russia (2.7%) | ||

| Gazprom OAO ADR | 19,718,615 | 282,167 |

| Rosneft Oil Co. GDR | 11,131,982 | 94,472 |

| Tatneft ADR | 78,772 | 3,289 |

| AK Transneft OAO | ||

| Prior Pfd. | 1,549 | 2,461 |

| Lukoil OAO ADR | 27,638 | 1,838 |

| NovaTek OAO GDR | 6,844 | 1,062 |

| Gazprom OAO | 124,674 | 883 |

| 386,172 | ||

| South Africa (0.0%) | ||

| Sasol Ltd. | 33,251 | 1,668 |

| South Korea (0.1%) | ||

| SK Innovation Co. Ltd. | 16,726 | 3,448 |

| S-Oil Corp. | 19,395 | 2,743 |

| GS Holdings | 31,530 | 2,702 |

| 8,893 | ||

| Spain (0.8%) | ||

| Repsol YPF SA | 3,504,087 | 110,513 |

| Thailand (0.1%) | ||

| PTT PCL (Foreign) | 267,500 | 3,100 |

| Banpu PCL | 95,150 | 2,323 |

| Thai Oil PCL (Foreign) | 872,600 | 2,234 |

| IRPC PCL (Foreign) | 10,783,200 | 2,071 |

| PTT Aromatics & | ||

| Refining PCL (Foreign) | 123,100 | 175 |

| 9,903 | ||

| Turkey (0.0%) | ||

| Tupras Turkiye | ||

| Petrol Rafinerileri AS | 89,761 | 2,179 |

| United Kingdom (11.0%) | ||

| BP plc ADR | 10,872,400 | 494,042 |

| Royal Dutch | ||

| Shell plc ADR | 6,426,600 | 472,741 |

| BG Group plc | 10,762,661 | 253,749 |

| Ensco plc ADR | 2,937,306 | 156,412 |

| Royal Dutch Shell plc | ||

| Class B | 4,226,315 | 154,751 |

| BP plc | 2,037,380 | 15,355 |

| Royal Dutch Shell plc | ||

| Class A | 330,410 | 12,103 |

| Royal Dutch Shell plc | ||

| Class A | ||

| (Amsterdam Shares) | 94,282 | 3,461 |

| Tullow Oil plc | 6,237 | 125 |

| 1,562,739 | ||

| Total International | 5,375,222 | |

| Total Common Stocks | ||

| (Cost $8,232,443) | 13,849,757 | |

| Market | |||

| Value | |||

| Shares | ($000) | ||

| Temporary Cash Investments (2.5%)1 | |||

| Money Market Fund (0.3%) | |||

| 3,4 | Vanguard Market | ||

| Liquidity Fund, 0.114% | 41,445,874 | 41,446 | |

| Face | |||

| Amount | |||

| ($000) | |||

| Repurchase Agreement (2.1%) | |||

| Deutsche Bank | |||

| Securities, Inc. | |||

| 0.200%, 8/1/11 | |||

| (Dated 7/29/11, | |||

| Repurchase Value | |||

| $296,705,000, | |||

| collateralized by | |||

| Government National | |||

| Mortgage Assn. | |||

| 4.000%–5.000%, | |||

| 7/15/39–7/15/41) | 296,700 | 296,700 | |

| U.S. Government and Agency Obligations (0.1%) | |||

| 5,6 | Fannie Mae Discount | ||

| Notes, 0.060%, 8/8/11 | 1,000 | 1,000 | |

| 5 | Federal Home Loan | ||

| Bank Discount Notes, | |||

| 0.250%, 9/7/11 | 5,000 | 4,999 | |

| 5,6 | Federal Home Loan | ||

| Bank Discount Notes, | |||

| 0.070%, 9/16/11 | 5,000 | 4,999 | |

| 5,6 | Federal Home Loan | ||

| Bank Discount Notes, | |||

| 0.100%, 10/11/11 | 1,000 | 1,000 | |

| 5,6 | Freddie Mac Discount | ||

| Notes, 0.050%, 10/3/11 | 2,000 | 1,999 | |

| 13,997 | |||

| Total Temporary Cash Investments | |||

| (Cost $352,144) | 352,143 | ||

| Total Investments (100.1%) | |||

| (Cost $8,584,587) | 14,201,900 | ||

| Other Assets and Liabilities (-0.1%) | |||

| Other Assets | 98,197 | ||

| Liabilities4 | (107,127) | ||

| (8,930) | |||

| Net Assets (100%) | 14,192,970 | ||

15

Energy Fund

| At July 31, 2011, net assets consisted of: | |

| Amount | |

| ($000) | |

| Paid-in Capital | 8,146,102 |

| Undistributed Net Investment Income | 92,815 |

| Accumulated Net Realized Gains | 337,165 |

| Unrealized Appreciation (Depreciation) | |

| Investment Securities | 5,617,313 |

| Futures Contracts | (1,078) |

| Forward Currency Contracts | 577 |

| Foreign Currencies | 76 |

| Net Assets | 14,192,970 |

| Investor Shares—Net Assets | |

| Applicable to 98,387,191 outstanding | |

| $.001 par value shares of beneficial | |

| interest (unlimited authorization) | 7,052,888 |

| Net Asset Value Per Share— | |

| Investor Shares | $71.69 |

| Admiral Shares—Net Assets | |

| Applicable to 53,032,725 outstanding | |

| $.001 par value shares of beneficial | |

| interest (unlimited authorization) | 7,140,082 |

| Net Asset Value Per Share— | |

| Admiral Shares | $134.64 |

See Note A in Notes to Financial Statements.

* Non-income-producing security.

^ Part of security position is on loan to broker-dealers. The total value of securities on loan is $33,777,000.

1 The fund invests a portion of its cash reserves in equity markets through the use of index futures contracts. After giving effect to futures investments, the fund’s effective common stock and temporary cash investment positions represent 98.8% and 1.3%, respectively, of net assets.

2 Considered an affiliated company of the fund as the issuer is another member of The Vanguard Group.

3 Affiliated money market fund available only to Vanguard funds and certain trusts and accounts managed by Vanguard. Rate shown is the 7-day yield.

4 Includes $35,165,000 of collateral received for securities on loan.

5 The issuer operates under a congressional charter; its securities are not backed by the full faith and credit of the U.S. government.

6 Securities with a value of $8,298,000 have been segregated as initial margin for open futures contracts.

ADR—American Depositary Receipt.

GDR—Global Depositary Receipt.

See accompanying Notes, which are an integral part of the Financial Statements.

16

Energy Fund

Statement of Operations

| Six Months Ended | |

| July 31, 2011 | |

| ($000) | |

| Investment Income | |

| Income | |

| Dividends1,2 | 130,016 |

| Interest2 | 436 |

| Security Lending | 5,022 |

| Total Income | 135,474 |

| Expenses | |

| Investment Advisory Fees—Note B | |

| Basic Fee | 10,010 |

| Performance Adjustment | 55 |

| The Vanguard Group—Note C | |

| Management and Administrative—Investor Shares | 6,012 |

| Management and Administrative—Admiral Shares | 4,083 |

| Marketing and Distribution—Investor Shares | 756 |

| Marketing and Distribution—Admiral Shares | 677 |

| Custodian Fees | 259 |

| Shareholders’ Reports—Investor Shares | 39 |

| Shareholders’ Reports—Admiral Shares | 10 |

| Trustees’ Fees and Expenses | 15 |

| Total Expenses | 21,916 |

| Expenses Paid Indirectly | (45) |

| Net Expenses | 21,871 |

| Net Investment Income | 113,603 |

| Realized Net Gain (Loss) | |

| Investment Securities Sold2 | 327,398 |

| Futures Contracts | 15,786 |

| Foreign Currencies and Forward Currency Contracts | (195) |

| Realized Net Gain (Loss) | 342,989 |

| Change in Unrealized Appreciation (Depreciation) | |

| Investment Securities | 136,330 |

| Futures Contracts | (6,195) |

| Foreign Currencies and Forward Currency Contracts | 624 |

| Change in Unrealized Appreciation (Depreciation) | 130,759 |

| Net Increase (Decrease) in Net Assets Resulting from Operations | 587,351 |

1 Dividends are net of foreign withholding taxes of $10,127,000.

2 Dividend income, interest income, and realized net gain (loss) from affiliated companies of the fund were $169,000, $204,000, and $25,901,000, respectively.

See accompanying Notes, which are an integral part of the Financial Statements.

17

Energy Fund

Statement of Changes in Net Assets

| Six Months Ended | Year Ended | |

| July 31, | January 31, | |

| 2011 | 2011 | |

| ($000) | ($000) | |

| Increase (Decrease) in Net Assets | ||

| Operations | ||

| Net Investment Income | 113,603 | 199,818 |

| Realized Net Gain (Loss) | 342,989 | 457,168 |

| Change in Unrealized Appreciation (Depreciation) | 130,759 | 2,204,352 |

| Net Increase (Decrease) in Net Assets Resulting from Operations | 587,351 | 2,861,338 |

| Distributions | ||

| Net Investment Income | ||

| Investor Shares | (1,784) | (90,181) |

| Admiral Shares | (2,298) | (94,977) |

| Realized Capital Gain1 | ||

| Investor Shares | (49,823) | (207,111) |

| Admiral Shares | (50,434) | (195,797) |

| Total Distributions | (104,339) | (588,066) |

| Capital Share Transactions | ||

| Investor Shares | 84,581 | (1,004,028) |

| Admiral Shares | 22,983 | 1,358,485 |

| Net Increase (Decrease) from Capital Share Transactions | 107,564 | 354,457 |

| Total Increase (Decrease) | 590,576 | 2,627,729 |

| Net Assets | ||

| Beginning of Period | 13,602,394 | 10,974,665 |

| End of Period2 | 14,192,970 | 13,602,394 |

1 Includes fiscal 2012 and 2011 short-term gain distributions totaling $22,102,000 and $62,911,000. Short-term gain distributions are treated as ordinary income dividends for tax purposes.

2 Net Assets—End of Period includes undistributed (overdistributed) net investment income of $92,815,000 and ($16,406,000).

See accompanying Notes, which are an integral part of the Financial Statements.

18

Energy Fund

Financial Highlights

Investor Shares

| Six Months | ||||||

| Ended | ||||||

| For a Share Outstanding | July 31, | Year Ended January 31, | ||||

| Throughout Each Period | 2011 | 2011 | 2010 | 2009 | 2008 | 2007 |

| Net Asset Value, Beginning of Period | $69.20 | $57.17 | $42.62 | $73.93 | $63.55 | $64.50 |

| Investment Operations | ||||||

| Net Investment Income | .502 | 1.053 | .910 | 1.2761 | 1.226 | 1.112 |

| Net Realized and Unrealized Gain (Loss) | ||||||

| on Investments | 2.509 | 14.103 | 14.591 | (28.853) | 14.639 | .405 |

| Total from Investment Operations | 3.011 | 15.156 | 15.501 | (27.577) | 15.865 | 1.517 |

| Distributions | ||||||

| Dividends from Net Investment Income | (.018) | (.977) | (.951) | (1.264) | (1.177) | (1.020) |

| Distributions from Realized Capital Gains | (.503) | (2.149) | — | (2.469) | (4.308) | (1.447) |

| Total Distributions | (.521) | (3.126) | (.951) | (3.733) | (5.485) | (2.467) |

| Net Asset Value, End of Period | $71.69 | $69.20 | $57.17 | $42.62 | $73.93 | $63.55 |

| Total Return2 | 4.34% | 27.17% | 36.28% | -38.51% | 25.02% | 2.24% |

| Ratios/Supplemental Data | ||||||

| Net Assets, End of Period (Millions) | $7,053 | $6,731 | $6,536 | $4,434 | $7,919 | $6,479 |

| Ratio of Total Expenses to | ||||||

| Average Net Assets | 0.34%3 | 0.34%3 | 0.38%3 | 0.28%3 | 0.25% | 0.25% |

| Ratio of Net Investment Income to | ||||||

| Average Net Assets | 1.57% | 1.74% | 1.73% | 1.84% | 1.67% | 1.71% |

| Portfolio Turnover Rate | 19% | 31% | 27% | 21% | 22% | 22% |

The expense ratio, net income ratio, and turnover rate for the current period have been annualized.

1 Calculated based on average shares outstanding.

2 Total returns do not include transaction or account service fees that may have applied in the periods shown. Fund prospectuses provide information about any applicable transaction and account service fees.

3 Includes performance-based investment advisory fee increases (decreases) of 0.00% for fiscal 2012, 0.00% for fiscal 2011, 0.03% for fiscal 2010, and 0.01% for fiscal 2009.

See accompanying Notes, which are an integral part of the Financial Statements.

19

Energy Fund

Financial Highlights

Admiral Shares

| Six Months | ||||||

| Ended | ||||||

| For a Share Outstanding | July 31, | Year Ended January 31, | ||||

| Throughout Each Period | 2011 | 2011 | 2010 | 2009 | 2008 | 2007 |

| Net Asset Value, Beginning of Period | $129.93 | $107.34 | $80.02 | $138.86 | $119.35 | $121.13 |

| Investment Operations | ||||||

| Net Investment Income | .981 | 2.045 | 1.780 | 2.4801 | 2.418 | 2.180 |

| Net Realized and Unrealized Gain (Loss) | ||||||

| on Investments | 4.716 | 26.479 | 27.395 | (54.203) | 27.505 | .757 |

| Total from Investment Operations | 5.697 | 28.524 | 29.175 | (51.723) | 29.923 | 2.937 |

| Distributions | ||||||

| Dividends from Net Investment Income | (.043) | (1.899) | (1.855) | (2.480) | (2.322) | (2.000) |

| Distributions from Realized Capital Gains | (.944) | (4.035) | — | (4.637) | (8.091) | (2.717) |

| Total Distributions | (.987) | (5.934) | (1.855) | (7.117) | (10.413) | (4.717) |

| Net Asset Value, End of Period | $134.64 | $129.93 | $107.34 | $80.02 | $138.86 | $119.35 |

| Total Return2 | 4.38% | 27.24% | 36.37% | -38.46% | 25.13% | 2.32% |

| Ratios/Supplemental Data | ||||||

| Net Assets, End of Period (Millions) | $7,140 | $6,871 | $4,439 | $2,889 | $5,214 | $3,612 |

| Ratio of Total Expenses to | ||||||

| Average Net Assets | 0.28%3 | 0.28%3 | 0.31%3 | 0.21%3 | 0.17% | 0.18% |

| Ratio of Net Investment Income to | ||||||

| Average Net Assets | 1.63% | 1.80% | 1.80% | 1.91% | 1.75% | 1.78% |

| Portfolio Turnover Rate | 19% | 31% | 27% | 21% | 22% | 22% |

The expense ratio, net income ratio, and turnover rate for the current period have been annualized.

1 Calculated based on average shares outstanding.

2 Total returns do not include transaction fees that may have applied in the periods shown. Fund prospectuses provide information about any applicable transaction fees.

3 Includes performance-based investment advisory fee increases (decreases) of 0.00% for fiscal 2012, 0.00% for fiscal 2011, 0.03% for fiscal 2010, and 0.01% for fiscal 2009.

See accompanying Notes, which are an integral part of the Financial Statements.

20

Energy Fund

Notes to Financial Statements

Vanguard Energy Fund is registered under the Investment Company Act of 1940 as an open-end investment company, or mutual fund. The fund invests in securities of foreign issuers, which may subject it to investment risks not normally associated with investing in securities of U.S. corporations. The fund offers two classes of shares: Investor Shares and Admiral Shares. Investor Shares are available to any investor who meets the fund’s minimum purchase requirements. Admiral Shares are designed for investors who meet certain administrative, service, and account-size criteria.

A. The following significant accounting policies conform to generally accepted accounting principles for U.S. mutual funds. The fund consistently follows such policies in preparing its financial statements.

1. Security Valuation: Securities are valued as of the close of trading on the New York Stock Exchange (generally 4 p.m., Eastern time) on the valuation date. Equity securities are valued at the latest quoted sales prices or official closing prices taken from the primary market in which each security trades; such securities not traded on the valuation date are valued at the mean of the latest quoted bid and asked prices. Securities for which market quotations are not readily available, or whose values have been affected by events occurring before the fund’s pricing time but after the close of the securities’ primary markets, are valued at their fair values calculated according to procedures adopted by the board of trustees. These procedures include obtaining quotations from an independent pricing service, monitoring news to identify significant market- or security-specific events, and evaluating changes in the values of foreign market proxies (for example, ADRs, futures contracts, or exchange-traded funds), between the time the foreign markets close and the fund’s pricing time. When fair-value pricing is employed, the prices of securities used by a fund to calculate its net asset value may differ from quoted or published prices for the same securities. Investments in Vanguard Market Liquidity Fund are valued at that fund’s net asset value. Temporary cash investments acquired over 60 days to maturity are valued using the latest bid prices or using valuations based on a matrix system (which considers such factors as security prices, yields, maturities, and ratings), both as furnished by independent pricing services. Other temporary cash investments are valued at amortized cost, which approximates market value.

2. Foreign Currency: Securities and other assets and liabilities denominated in foreign currencies are translated into U.S. dollars using exchange rates obtained from an independent third party as of the fund’s pricing time on the valuation date. Realized gains (losses) and unrealized appreciation (depreciation) on investment securities include the effects of changes in exchange rates since the securities were purchased, combined with the effects of changes in security prices. Fluctuations in the value of other assets and liabilities resulting from changes in exchange rates are recorded as unrealized foreign currency gains (losses) until the assets or liabilities are settled in cash, at which time they are recorded as realized foreign currency gains (losses).

3. Futures and Forward Currency Contracts: The fund uses index futures contracts to a limited extent, with the objective of maintaining full exposure to the stock market while maintaining liquidity. The fund may purchase or sell futures contracts to achieve a desired level of investment, whether to accommodate portfolio turnover or cash flows from capital share transactions. The primary risks associated with the use of futures contracts are imperfect correlation between changes in market values of stocks held by the fund and the prices of futures contracts, and the possibility of an illiquid market.

The fund also enters into forward currency contracts to provide the appropriate currency exposure related to any open futures contracts or to protect the value of securities and related receivables and payables against changes in foreign exchange rates. The primary risk associated with the fund’s use of these contracts is that a counterparty will fail to fulfill its obligation to pay gains due to the fund under the contracts. Counterparty risk is mitigated by entering into forward currency contracts only with highly rated counterparties, by a master netting arrangement between the fund and the counterparty,

21

Energy Fund

and by the posting of collateral by the counterparty. The forward currency contracts contain provisions whereby a counterparty may terminate open contracts if the fund’s net assets decline below a certain level, triggering a payment by the fund if the fund is in a net liability position at the time of the termination. The payment amount would be reduced by any collateral the fund has posted.

Any securities posted as collateral for open contracts are noted in the Statement of Net Assets.

Futures contracts are valued at their quoted daily settlement prices. Forward currency contracts are valued at their quoted daily prices obtained from an independent third party, adjusted for currency risk based on the expiration date of each contract. The aggregate principal amounts of the contracts are not recorded in the Statement of Net Assets. Fluctuations in the value of the contracts are recorded in the Statement of Net Assets as an asset (liability) and in the Statement of Operations as unrealized appreciation (depreciation) until the contracts are closed, when they are recorded as realized gains (losses) on futures or forward currency contracts.

4. Repurchase Agreements: The fund invests in repurchase agreements. Securities pledged as collateral for repurchase agreements are held by a custodian bank until the agreements mature. Each agreement requires that the market value of the collateral be sufficient to cover payments of interest and principal; however, in the event of default or bankruptcy by the other party to the agreement, retention of the collateral may be subject to legal proceedings.

5. Federal Income Taxes: The fund intends to continue to qualify as a regulated investment company and distribute all of its taxable income. Management has analyzed the fund’s tax positions taken for all open federal income tax years (January 31, 2008–2011), and for the period ended July 31, 2011, and has concluded that no provision for federal income tax is required in the fund’s financial statements.

6. Distributions: Distributions to shareholders are recorded on the ex-dividend date.

7. Security Lending: The fund may lend its securities to qualified institutional borrowers to earn additional income. Security loans are required to be secured at all times by collateral at least equal to the market value of securities loaned. The fund invests cash collateral received in Vanguard Market Liquidity Fund, and records a liability for the return of the collateral, during the period the securities are on loan. Security lending income represents fees charged to borrowers plus income earned on investing cash collateral, less expenses associated with the loan.

8. Other: Dividend income is recorded on the ex-dividend date. Interest income includes income distributions received from Vanguard Market Liquidity Fund and is accrued daily. Security transactions are accounted for on the date securities are bought or sold. Costs used to determine realized gains (losses) on the sale of investment securities are those of the specific securities sold. Fees assessed on redemptions of capital shares are credited to paid-in capital.

Each class of shares has equal rights as to assets and earnings, except that each class separately bears certain class-specific expenses related to maintenance of shareholder accounts (included in Management and Administrative expenses) and shareholder reporting. Marketing and distribution expenses are allocated to each class of shares based on a method approved by the board of trustees. Income, other non-class-specific expenses, and gains and losses on investments are allocated to each class of shares based on its relative net assets.

B. Wellington Management Company, LLP, provides investment advisory services to a portion of the fund for a fee calculated at an annual percentage rate of average net assets managed by the advisor.

The basic fee is subject to quarterly adjustments based on the fund’s performance for the preceding

22

Energy Fund

three years relative to a combined index composed of the S&P Citigroup BMI World Energy Index and the S&P 500 Energy Equal Weighted Blend Index through July 31, 2010, and the current benchmark, MSCI ACWI Energy Index, thereafter. The benchmark change will be fully phased in by July 2013.

The Vanguard Group provides investment advisory services to a portion of the fund on an at-cost basis; the fund paid Vanguard advisory fees of $164,000 for the six months ended July 31, 2011.

For the six months ended July 31, 2011, the aggregate investment advisory fee represented an effective annual basic rate of 0.14% of the fund’s average net assets, before an increase of $55,000 (0.00%) based on performance.

C. The Vanguard Group furnishes at cost corporate management, administrative, marketing, and distribution services. The costs of such services are allocated to the fund under methods approved by the board of trustees. The fund has committed to provide up to 0.40% of its net assets in capital contributions to Vanguard. At July 31, 2011, the fund had contributed capital of $2,235,000 to Vanguard (included in Other Assets), representing 0.02% of the fund’s net assets and 0.89% of Vanguard’s capitalization. The fund’s trustees and officers are also directors and officers of Vanguard.

D. The fund has asked its investment advisors to direct certain security trades, subject to obtaining the best price and execution, to brokers who have agreed to rebate to the fund part of the commissions generated. Such rebates are used solely to reduce the fund’s management and administrative expenses. For the six months ended July 31, 2011, these arrangements reduced the fund’s expenses by $45,000 (an annual rate of 0.00% of average net assets).

E. Various inputs may be used to determine the value of the fund’s investments. These inputs are summarized in three broad levels for financial statement purposes. The inputs or methodologies used to value securities are not necessarily an indication of the risk associated with investing in those securities.

Level 1—Quoted prices in active markets for identical securities.

Level 2—Other significant observable inputs (including quoted prices for similar securities, interest rates, prepayment speeds, credit risk, etc.).

Level 3—Significant unobservable inputs (including the fund’s own assumptions used to determine the fair value of investments).

The following table summarizes the fund’s investments as of July 31, 2011, based on the inputs used to value them:

| Level 1 | Level 2 | Level 3 | |

| Investments | ($000) | ($000) | ($000) |

| Common Stocks—United States | 8,474,535 | — | — |

| Common Stocks—International | 3,711,465 | 1,663,757 | — |

| Temporary Cash Investments | 41,446 | 310,697 | — |

| Futures Contracts—Liabilities1 | (1,108) | — | — |

| Forward Currency Contracts—Assets | — | 987 | — |

| Forward Currency Contracts—Liabilities | — | (410) | — |

| Total | 12,226,338 | 1,975,031 | — |

| 1 Represents variation margin on the last day of the reporting period. | |||

23

Energy Fund

F. At July 31, 2011, the fair values of derivatives were reflected in the Statement of Net Assets as follows:

| Foreign | |||

| Equity | Exchange | ||

| Contracts | Contracts | Total | |

| Statement of Net Assets Caption | ($000) | ($000) | ($000) |

| Other Assets | — | 987 | 987 |

| Liabilities1 | (1,108) | (410) | (1,518) |

| 1 Represents variation margin on the last day of the reporting period. | |||

Realized net gain (loss) and the change in unrealized appreciation (depreciation) on derivatives for the six months ended July 31, 2011, were:

| Foreign | |||

| Equity | Exchange | ||

| Contracts | Contracts | Total | |

| Realized Net Gain (Loss) on Derivatives | ($000) | ($000) | ($000) |

| Futures Contracts | 15,786 | — | 15,786 |

| Forward Currency Contracts | — | — | — |

| Realized Net Gain (Loss) on Derivatives | 15,786 | — | 15,786 |

| Change in Unrealized Appreciation (Depreciation) on Derivatives | |||

| Futures Contracts | (6,195) | — | (6,195) |

| Forward Currency Contracts | — | 577 | 577 |

| Change in Unrealized Appreciation (Depreciation) on Derivatives | (6,195) | 577 | (5,618) |

At July 31, 2011, the aggregate settlement value of open futures contracts and the related unrealized appreciation (depreciation) were:

| ($000) | ||||

| Aggregate | ||||

| Number of | Settlement | Unrealized | ||

| Long (Short) | Value | Appreciation | ||

| Futures Contracts | Expiration | Contracts | Long (Short) | (Depreciation) |

| E-mini S&P 500 Index | September 2011 | 2,059 | 132,640 | (1,264) |

| S&P 500 Index | September 2011 | 116 | 37,364 | 186 |

Unrealized appreciation (depreciation) on open futures contracts is required to be treated as realized gain (loss) for tax purposes.

24

Energy Fund

At July 31, 2011, the fund had open forward currency contracts to receive and deliver currencies as follows. Unrealized appreciation (depreciation) on open forward currency contracts is treated as realized gain (loss) for tax purposes.

| Unrealized | ||||||

| Contract | Appreciation | |||||

| Settlement | Contract Amount (000) | (Depreciation) | ||||

| Counterparty | Date | Receive | Deliver | ($000) | ||

| Bank of America NA | 9/16/11 | JPY | 1,308,379 | USD | 16,960 | 987 |

| Deutsche Bank AG | 9/16/11 | USD | 16,960 | JPY | 1,308,379 | (410) |

| JPY—Japanese yen. | ||||||

| USD—U.S. dollar. | ||||||

G. Distributions are determined on a tax basis and may differ from net investment income and realized capital gains for financial reporting purposes. Differences may be permanent or temporary. Permanent differences are reclassified among capital accounts in the financial statements to reflect their tax character. Temporary differences arise when certain items of income, expense, gain, or loss are recognized in different periods for financial statement and tax purposes; these differences will reverse at some time in the future. Differences in classification may also result from the treatment of short-term gains as ordinary income for tax purposes. The fund’s tax-basis capital gains and losses are determined only at the end of each fiscal year.

During the six months ended July 31, 2011, the fund realized net foreign currency losses of $195,000, which decreased distributable net income for tax purposes; accordingly, such losses have been reclassified from accumulated net realized gains to undistributed net investment income.

The fund realized gains on the sale of securities that were subject to capital gains tax in certain foreign countries. Capital gains taxes reduced realized gains for financial statement purposes but are treated as an expense for tax purposes. Accordingly, $105,000 of capital gains tax has been reclassified from accumulated net realized gains to undistributed net investment income.

At July 31, 2011, the cost of investment securities for tax purposes was $8,584,587,000. Net unrealized appreciation of investment securities for tax purposes was $5,617,313,000, consisting of unrealized gains of $5,699,422,000 on securities that had risen in value since their purchase and $82,109,000 in unrealized losses on securities that had fallen in value since their purchase.

H. During the six months ended July 31, 2011, the fund purchased $1,835,597,000 of investment securities and sold $1,340,344,000 of investment securities, other than temporary cash investments.

25

Energy Fund

I. Capital share transactions for each class of shares were:

| Six Months Ended | Year Ended | |||

| July 31, 2011 | January 31, 2011 | |||

| Amount | Shares | Amount | Shares | |

| ($000) | (000) | ($000) | (000) | |

| Investor Shares | ||||

| Issued | 752,324 | 10,514 | 993,363 | 16,506 |

| Issued in Lieu of Cash Distributions | 49,860 | 688 | 286,379 | 4,616 |

| Redeemed1 | (717,603) | (10,094) | (2,283,770) | (38,167) |

| Net Increase (Decrease)—Investor Shares | 84,581 | 1,108 | (1,004,028) | (17,045) |

| Admiral Shares | ||||

| Issued | 637,387 | 4,729 | 1,900,020 | 16,578 |

| Issued in Lieu of Cash Distributions | 48,506 | 356 | 261,084 | 2,235 |

| Redeemed1 | (662,910) | (4,934) | (802,619) | (7,281) |

| Net Increase (Decrease)—Admiral Shares | 22,983 | 151 | 1,358,485 | 11,532 |

| 1 Net of redemption fees for fiscal 2012 and 2011 of $1,035,000 and $2,317,000, respectively (fund totals). | ||||

J. The fund invested in a company that was considered to be an affiliated company of the fund because the fund owned more than 5% of the outstanding voting securities of the company. Transactions during the period in securities of this company were as follows:

| Current Period Transactions | |||||

| Jan. 31, 2011 | Proceeds from | July 31, 2011 | |||

| Market | Purchases | Securities | Dividend | Market | |

| Value | at Cost | Sold | Income | Value | |

| ($000) | ($000) | ($000) | ($000) | ($000) | |

| Cabot Oil & Gas Corp. | 266,816 | 4,965 | 100,718 | 169 | NA1 |

| 1 Not applicable—At July 31, 2011, the security was still held, but the issuer was no longer an affiliated company of the fund. | |||||

K. In preparing the financial statements as of July 31, 2011, management considered the impact of subsequent events for potential recognition or disclosure in these financial statements.

26

About Your Fund’s Expenses

As a shareholder of the fund, you incur ongoing costs, which include costs for portfolio management, administrative services, and shareholder reports (like this one), among others. Operating expenses, which are deducted from a fund’s gross income, directly reduce the investment return of the fund.

A fund’s expenses are expressed as a percentage of its average net assets. This figure is known as the expense ratio. The following examples are intended to help you understand the ongoing costs (in dollars) of investing in your fund and to compare these costs with those of other mutual funds. The examples are based on an investment of $1,000 made at the beginning of the period shown and held for the entire period.

The accompanying table illustrates your fund’s costs in two ways:

• Based on actual fund return. This section helps you to estimate the actual expenses that you paid over the period. The ”Ending Account Value“ shown is derived from the fund‘s actual return, and the third column shows the dollar amount that would have been paid by an investor who started with $1,000 in the fund. You may use the information here, together with the amount you invested, to estimate the expenses that you paid over the period.

To do so, simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number given for your fund under the heading ”Expenses Paid During Period.“

• Based on hypothetical 5% yearly return. This section is intended to help you compare your fund‘s costs with those of other mutual funds. It assumes that the fund had a yearly return of 5% before expenses, but that the expense ratio is unchanged. In this case—because the return used is not the fund’s actual return—the results do not apply to your investment. The example is useful in making comparisons because the Securities and Exchange Commission requires all mutual funds to calculate expenses based on a 5% return. You can assess your fund’s costs by comparing this hypothetical example with the hypothetical examples that appear in shareholder reports of other funds.

Note that the expenses shown in the table are meant to highlight and help you compare ongoing costs only and do not reflect transaction costs incurred by the fund for buying and selling securities. Further, the expenses do not include any purchase, redemption, or account service fees described in the fund prospectus. If such fees were applied to your account, your costs would be higher. Your fund does not carry a “sales load.”

The calculations assume no shares were bought or sold during the period. Your actual costs may have been higher or lower, depending on the amount of your investment and the timing of any purchases or redemptions.

You can find more information about the fund’s expenses, including annual expense ratios, in the Financial Statements section of this report. For additional information on operating expenses and other shareholder costs, please refer to your fund’s current prospectus.

27

| Six Months Ended July 31, 2011 | |||

| Beginning | Ending | Expenses | |

| Account Value | Account Value | Paid During | |

| Energy Fund | 1/31/2011 | 7/31/2011 | Period |

| Based on Actual Fund Return | |||

| Investor Shares | $1,000.00 | $1,043.43 | $1.72 |

| Admiral Shares | 1,000.00 | 1,043.76 | 1.42 |

| Based on Hypothetical 5% Yearly Return | |||

| Investor Shares | $1,000.00 | $1,023.11 | $1.71 |

| Admiral Shares | 1,000.00 | 1,023.41 | 1.40 |

The calculations are based on expenses incurred in the most recent six-month period. The fund’s annualized six-month expense ratios for that period are 0.34% for Investor Shares and 0.28% for Admiral Shares. The dollar amounts shown as “Expenses Paid” are equal to the annualized expense ratio multiplied by the average account value over the period, multiplied by the number of days in the most recent six-month period, then divided by the number of days in the most recent 12-month period.

28

Trustees Approve Advisory Arrangements

The board of trustees of Vanguard Energy Fund has renewed the fund’s investment advisory arrangements with The Vanguard Group, Inc., through its Quantitative Equity Group, and Wellington Management Company, LLP. The board determined that the retention of the fund’s advisors was in the best interests of the fund and its shareholders.

The board based its decision upon an evaluation of each advisor’s investment staff, portfolio management process, and performance. The trustees considered the factors discussed below, among others. However, no single factor determined whether the board approved the arrangements. Rather, it was the totality of the circumstances that drove the board’s decision.

Nature, extent, and quality of services

The board considered the quality of the fund’s investment management over both the short and long term, and took into account the organizational depth and stability of each advisor. The board noted the following:

Wellington Management Company, LLP. Founded in 1928, Wellington Management is among the nation’s oldest and most respected institutional investment managers. The investment team uses a bottom-up approach in which stocks are selected based on the advisor’s estimates of fundamental investment value. The advisor’s investment process emphasizes company fundamentals, management track record, and security valuation. The firm has advised the fund since the fund’s inception in 1984.

The Vanguard Group, Inc. Vanguard has been managing investments for more than three decades. The Quantitative Equity Group adheres to a sound, disciplined investment management process; the team has considerable experience, stability, and depth. Vanguard has managed a portion of the fund since 2005.

The board concluded that each advisor’s experience, stability, depth, and performance, among other factors, warranted the continuation of the advisory arrangements.

Investment performance

The board considered the short- and long-term performance of the fund, including any periods of outperformance or underperformance of a relevant benchmark and peer group. The board concluded that each advisor has carried out its investment strategy in disciplined fashion, and that performance results have been in line with expectations. Information about the fund’s most recent performance can be found in the Performance Summary section of this report.

Cost

The board concluded that the fund’s expense ratio was well below the average expense ratio charged by funds in its peer group and that the fund’s advisory fee rate was also well below its peer-group average. Information about the fund’s expenses appears in the About Your Fund’s Expenses section of this report as well as in the Financial Statements section, which also includes information about the fund’s advisory fee rate.

The board did not consider profitability of Wellington Management in determining whether to approve the advisory fee, because Wellington Management is independent of Vanguard, and the advisory fee is the result of arm’s-length negotiations. The board does not conduct a profitability analysis of Vanguard, because of Vanguard’s unique “at-cost” structure. Unlike most other mutual fund management companies, Vanguard is owned by the funds it oversees, and produces “profits” only in the form of reduced expenses for fund shareholders.

29

The benefit of economies of scale

The board concluded that the fund’s shareholders benefit from economies of scale because of breakpoints in the fund’s advisory fee schedule for Wellington Management. The breakpoints reduce the effective rate of the fee as the fund’s assets managed by Wellington Management increase. The board also concluded that the fund’s low-cost arrangement with Vanguard ensures that the fund will realize economies of scale as it grows, with the cost to shareholders declining as the fund’s assets managed by Vanguard increase.

The board will consider whether to renew the advisory arrangement again after a one-year period.

30

Glossary

30-Day SEC Yield. A fund’s 30-day SEC yield is derived using a formula specified by the U.S. Securities and Exchange Commission. Under the formula, data related to the fund’s security holdings in the previous 30 days are used to calculate the fund’s hypothetical net income for that period, which is then annualized and divided by the fund’s estimated average net assets over the calculation period. For the purposes of this calculation, a security’s income is based on its current market yield to maturity (in the case of bonds), its actual income (for asset-backed securities), or its projected dividend yield (for stocks). Because the SEC yield represents hypothetical annualized income, it will differ—at times significantly—from the fund’s actual experience. As a result, the fund’s income distributions may be higher or lower than implied by the SEC yield.

Beta. A measure of the magnitude of a fund’s past share-price fluctuations in relation to the ups and downs of a given market index. The index is assigned a beta of 1.00. Compared with a given index, a fund with a beta of 1.20 typically would have seen its share price rise or fall by 12% when the index rose or fell by 10%. For this report, beta is based on returns over the past 36 months for both the fund and the index. Note that a fund’s beta should be reviewed in conjunction with its R-squared (see definition). The lower the R-squared, the less correlation there is between the fund and the index, and the less reliable beta is as an indicator of volatility.

Dividend Yield. Dividend income earned by stocks, expressed as a percentage of the aggregate market value (or of net asset value, for a fund). The yield is determined by dividing the amount of the annual dividends by the aggregate value (or net asset value) at the end of the period. For a fund, the dividend yield is based solely on stock holdings and does not include any income produced by other investments.

Earnings Growth Rate. The average annual rate of growth in earnings over the past five years for the stocks now in a fund.

Equity Exposure. A measure that reflects a fund’s investments in stocks and stock futures. Any holdings in short-term reserves are excluded.

Expense Ratio. The percentage of a fund’s average net assets used to pay its annual administrative and advisory expenses. These expenses directly reduce returns to investors.

Foreign Holdings. The percentage of a fund represented by securities or depositary receipts of companies based outside the United States.

Inception Date. The date on which the assets of a fund (or one of its share classes) are first invested in accordance with the fund’s investment objective. For funds with a subscription period, the inception date is the day after that period ends. Investment performance is measured from the inception date.

Median Market Cap. An indicator of the size of companies in which a fund invests; the midpoint of market capitalization (market price x shares outstanding) of a fund’s stocks, weighted by the proportion of the fund’s assets invested in each stock. Stocks representing half of the fund’s assets have market capitalizations above the median, and the rest are below it.

Price/Book Ratio. The share price of a stock divided by its net worth, or book value, per share. For a fund, the weighted average price/book ratio of the stocks it holds.

31

Price/Earnings Ratio. The ratio of a stock’s current price to its per-share earnings over the past year. For a fund, the weighted average P/E of the stocks it holds. P/E is an indicator of market expectations about corporate prospects; the higher the P/E, the greater the expectations for a company’s future growth.

R-Squared. A measure of how much of a fund’s past returns can be explained by the returns from the market in general, as measured by a given index. If a fund’s total returns were precisely synchronized with an index’s returns, its R-squared would be 1.00. If the fund’s returns bore no relationship to the index’s returns, its R-squared would be 0. For this report, R-squared is based on returns over the past 36 months for both the fund and the index.

Return on Equity. The annual average rate of return generated by a company during the past five years for each dollar of shareholder’s equity (net income divided by shareholder’s equity). For a fund, the weighted average return on equity for the companies whose stocks it holds.

Short-Term Reserves. The percentage of a fund invested in highly liquid, short-term securities that can be readily converted to cash.

Turnover Rate. An indication of the fund’s trading activity. Funds with high turnover rates incur higher transaction costs and may be more likely to distribute capital gains (which may be taxable to investors). The turnover rate excludes in-kind transactions, which have minimal impact on costs.

32

This page intentionally left blank.

This page intentionally left blank.

This page intentionally left blank.

The People Who Govern Your Fund

The trustees of your mutual fund are there to see that the fund is operated and managed in your best interests since, as a shareholder, you are a part owner of the fund. Your fund’s trustees also serve on the board of directors of The Vanguard Group, Inc., which is owned by the Vanguard funds and provides services to them on an at-cost basis.