Second Quarter FY 2012 Earnings Presentation Bristow Group Inc. November 8, 2011 Exhibit 99.1 |

2 Second quarter earnings call agenda Introduction CEO remarks and operational highlights Current and future financial performance - FY12 Q2 Financial discussion - Update on capital return Closing remarks Questions and answers Linda McNeill, Director Investor Relations Bill Chiles, President and CEO Jonathan Baliff, SVP and CFO Bill Chiles, President and CEO |

3 Forward-looking statements This presentation may contain “forward-looking statements” within the meaning of the Private Securities Litigation Reform Act of 1995. Forward-looking statements include statements about our future business, operations, capital expenditures, fleet composition, capabilities and results; modeling information, earnings guidance, expected operating margins and other financial projections; future dividends, share repurchase and other uses; plans, strategies and objectives of our management, including our plans and strategies to grow earnings and our business, our general strategy going forward and our business model; expected actions by us and by third parties, including our customers, competitors and regulators; share repurchase and other uses of excess cash; the valuation of our company and its valuation relative to relevant financial indices; assumptions underlying or relating to any of the foregoing, including assumptions regarding factors impacting our business, financial results and industry; and other matters. Our forward-looking statements reflect our views and assumptions on the date of this presentation regarding future events and operating performance. They involve known and unknown risks, uncertainties and other factors, many of which may be beyond our control, that may cause actual results to differ materially from any future results, performance or achievements expressed or implied by the forward-looking statements. These risks, uncertainties and other factors include those discussed under the captions “Risk Factors” and “Management’s Discussion and Analysis of Financial Condition and Results of Operations” in our Annual Report on Form 10-K for the fiscal year ended March 31, 2011 and our Quarterly Report on Form 10-Q for the quarter ended September 30, 2011. We do not undertake any obligation, other than as required by law, to update or revise any forward- looking statements, whether as a result of new information, future events or otherwise. |

4 Chief Executive comments Bill Chiles, President and CEO |

5 Operational safety review 0.33 0.34 0.34 0.31 0.28 0.43 0.00 0.00 0.25 0.18 0.27 0.22 0.00 0.50 1.00 O N D J F M A M J J A S 1.17 0.78 0.78 0.00 0.00 1.02 0.54 0.00 1.00 2.00 2006 2007 2008 2009 2010 2011 YTD 2012 * Includes consolidated commercial operations only 0.16 0.13 0.16 0.14 0.13 0.15 0.14 0.13 0.23 0.18 0.20 0.17 0.00 0.10 0.20 0.30 0.40 0.50 O N D J F M A M J J A S Total Reportable Injury Rate per 200,000 man- hours (cumulative) Lost Work Case Rate per 200,000 man-hours (cumulative) Air Accident Rate* per 100,000 Flight Hours (Fiscal Year) FY11 FY12 FY11 FY12 |

6 Q2 FY12 highlights • Quarterly performance was negatively affected by a non-cash inventory write down, a decrease in earnings from unconsolidated affiliates, an impairment charge resulting from a base closure, and the loss on the disposal of a fixed wing aircraft • Strong cash flow generation allows us to deliver on commitment to create a balanced return as evidenced by (up to) $100 million share buyback program • Bristow revises earnings per share guidance for the full FY12 to $3.05 - $3.30 • Q2 operating revenue of $297.1M (4% increase from Q2 FY11, 4% increase from Q1 FY12) • Q2 GAAP EPS of $0.07 (93% decrease from Q2 FY11, 88% decrease from Q1 FY12) • Q2 adjusted EPS * of $0.63 (38% decrease from Q2 FY11, 17% increase from Q1 FY12) • Q2 operating income of $9.6M (82% decrease from Q2 FY11, 74% decrease from Q1 FY12) • Q2 adjusted operating income * of $38.5M (25% decrease from Q2 FY11, 10% increase from Q1 FY12) • Q2 adjusted EBITDA * of $62.1M (15% decrease from Q2 FY11, 7% increase from Q1 FY12) • Q2 operating cash flow of $64.1M (51% increase from Q2 FY11, 21% increase from Q1 FY12) * Adjusted EPS, adjusted operating income and adjusted EBITDA amounts exclude gains and losses on dispositions of assets and any special items during the period. See reconciliation of these items to GAAP measures in appendix and our earnings release for the quarter ended September 30, 2011 |

7 • Brent remains above $100 in the face of weak global economy. OPEC expected to defend $90/b - $100/b Brent • Momentum continues to build in the U.S. Gulf of Mexico with restart of deepwater drilling • International oil service up-cycle is continuing to steadily unfold; however costs to fulfill growth are impacting many providers this quarter • Strong helicopter activity returning to pre-recession levels with increasing tender activity and tightening helicopter availability • Today we are bidding for contracts requiring 20-25 new large aircraft starting in 2012 and 2013. Bidding activity over the next six months is expected to double requiring over 40 new large aircraft • 81% of our consolidated operating revenue and 94% of our business unit operating income came from international markets this quarter Current market environment Source: Barclays Capital Research and PFC Energy October 2011 |

8 • Europe represents 38% of total Bristow operating revenue in Q2FY12 and 52% of operating income • Operating margin of 20.7% vs 22.1% in prior year quarter • Increased oil and gas revenue and flying hours primarily from customers in Southern North Sea and Aberdeen • Higher salary and benefit costs in Norway and increased maintenance costs • Search and Rescue (SAR) UK Gap bid submitted; Norwegian SAR pre-qualified Outlook: • Continued high tender activity • New incremental work starting, including two large aircraft in Norway continuing market share gains • FBH was awarded Dutch Antilles SAR contract for two large aircraft FY12 operating margin expected to be ~low twenties Europe (EBU) UK Netherlands Norway Norwich Aberdeen Scasta Stavanger Den Helder Bergen Hammerfest Esbjerg Humberside Kristiansund |

9 West Africa (WASBU) Nigeria Lagos Escravos Port Harcourt Warri Osubi Eket Calabar • Nigeria represents 19% of total Bristow operating revenue in Q2 FY12 and 36% of operating income • Operating revenue of $61.1M increased from $56.2M in Q2 FY11 with operating income decreased slightly to $16.1M from $17.2M from prior year quarter • Operating margin of 26.4% vs 30.5% in prior year quarter due to increase in maintenance, depreciation, training and travel expense • $1.1M loss on fixed wing aircraft damaged in incident • Record flight hours due to competitor aircraft model type grounding; however, not expected to continue Outlook: • Incremental contracts at attractive rates • Focus on Client Promise and reducing working capital • Organizational restructuring continues FY12 operating margin expected to be ~ low to mid twenties Warri Texaco |

10 Exmouth Varanus Is Barrow Is Australia (AUSBU) Australia Perth Dongara Essendon Tooradin Broome Truscott Darwin BDI provide support to the Republic of Singapore Air Force Oakey • Australia represented 12% of total Bristow operating revenue in Q2 FY12 and 1% of operating income • Operating revenue of $30.5M decreased from $34.2M Q2 prior year primarily due to continued delayed activity • Operating income decreased from $6.1M in Q2 FY11 to $0.6M in Q2 FY12 due to reduced overall volume of work combined with relatively high overhead • Operating margin decreased to 1.9% vs 17.8% for the prior year quarter due to continued labor costs associated with lost contract Outlook: • Additional new technology work confirmed in FY12 with two key operators • Other first half work delayed until late FY12, early FY13 FY12 operating margin expected to be ~ mid teens Karratha |

11 Other International (OIBU) Consolidated in OIBU Unconsolidated Affiliate • OIBU represented 12% of total Bristow operating revenue and 5% of operating income for Q2 FY12 • Operating revenue of $35.2M slightly lower than Q2 FY11 of $36M; Operating income, excluding Lider, is $9M same as Q2 prior year • Operating margin, excluding Lider, remained relatively flat at ~ 25% over the prior year quarter • Although operationally on plan, Lider equity earnings had a negative impact of $6.6M for Q2 due to foreign exchange impact associated with US GAAP accounting • No work in Libya Outlook: • Incremental contracted work for nine helicopters in Equatorial Guinea, Bangladesh, Trinidad and Brazil is not reflected in this quarter’s numbers although some costs have been incurred • Lider will have 13 additional helicopters on contract in Q3 • Q3 will see two large aircraft move from Malaysia back to Australia FY12 operating margin expected to be ~ low twenties |

12 North America (NABU) • • Operating revenue of $47.9M represents 16% of total Bristow operating revenue • Operating income decreased to $2.6M vs. $8.9M in the prior year quarter • Operating margin of 5.4% compared to 16.4% prior year quarter, which was higher due to increased flying associated with oil spill work • Adjusted operating margin, excluding special items, of 11% compared to 3.6% prior year quarter, due to better flight hours and focused cost management • Creole base in Louisiana closed Outlook: • GoM drilling permits continue to be issued but at a slow rate • Two new technology large aircraft S-92s to arrive GoM Q3 for contracted work FY12 operating margin expected to be ~ single digit |

13 Financial discussion Jonathan Baliff, SVP and CFO |

14 Financial highlights: Adjusted EPS & EBITDA Summary Q2 FY11 to Q2 FY12 adjusted EPS bridge Q2 FY11 to Q2 FY12 adjusted EBITDA bridge (in millions) * Adjusted EPS, adjusted operating income and adjusted EBITDA amounts exclude gains and losses on dispositions of assets and any special items during the period. See reconciliation of these items to GAAP in our earnings release for the quarter ended September 30th, 2011. |

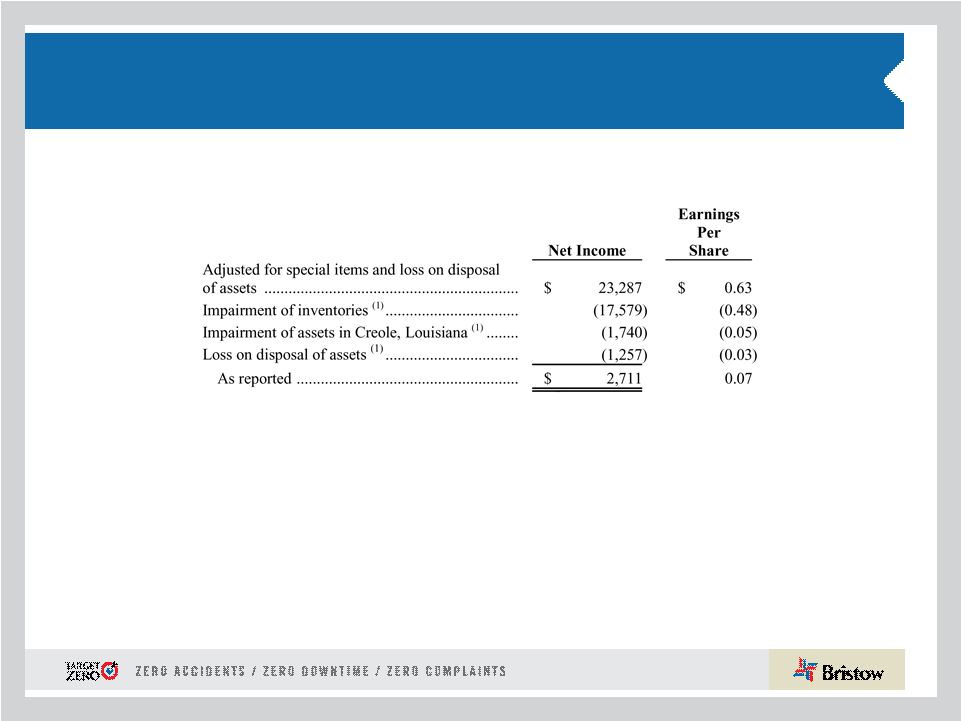

15 Financial highlights: Inventory write-down and special items • There has been a marked acceleration in our client’s desire for newer equipment in FY12 • Bristow will continue to be proactive with new technology as the premier service provider following through on the Client Promise • So in 2QFY12, our fleet management led to a shortening of certain aircraft lives and subsequent inventory write-down • Other operational non-cash items lead to adjusted 2Q EPS of $0.63 Reconciliation of Non-GAAP Net Income and Earnings Per Share September 2011 Quarter 1) These amounts are presented after applying the appropriate tax effect to each item and dividing earnings per share by the weighted average shares outstanding during the related period. |

16 Absolute BVA – Six Quarters Sequential quarterly improvement needs to continue Absolute BVA Q1FY11 - Q2FY12 -15.4 0.0 -3.6 -1.1 +4.2 -8.6 -20 -15 -10 -5 0 5 10 Q1 FY11 Q2 FY11 Q3 FY11 Q4 FY11 Q1 FY12 Q2 FY12 |

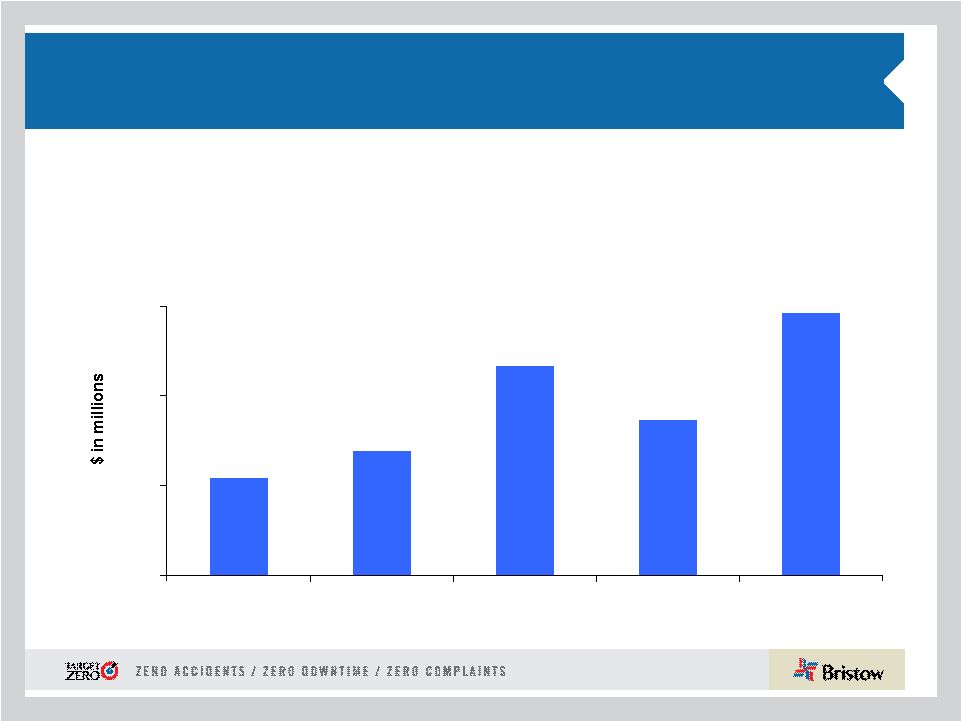

17 43 55 94 69 117 - 40 80 120 1HFY08 1HFY09 1HFY10 1HFY11 1HFY12 Financial highlights: Strong operating cash flow generation We generated 69% more operating cash flow in the first half of FY12 compared to the same period last year |

18 Commitment to balanced shareholder returns: Up to $100 million share repurchase authorization • We are confident in the underlying ability of Bristow to generate cash flow while growing the business across the globe and maintaining a prudent financial profile • The $100 million share buyback authorization represents approximately 5% of today’s outstanding shares based on current stock price • Bristow intends to complete the share repurchase as soon as practical, depending on conditions discussed in 10Q • There are a number of commonly used execution tactics and Bristow will employ one or a combination to provide the best value/certainty for our shareholders |

19 Financial highlights: Revising and narrowing of FY12 guidance Phase I Revision • EPS guidance range (as of November 8, 2011) $3.05 - $3.30, excluding aircraft sales and special items • Depreciation and amortization expense ~$87 – $93 million • SG & A expense ~ $135 - $140 million • Interest expense ~ $37 - $42 million • Tax ~ 20% - 24% (assuming revenue earned in same regions and same mix) Phase II Revision • LACE* (Large Aircraft Equivalent) = 158 • Revenue/LACE Rate* ~ $7.20 - 7.50 million per LACE aircraft per year * Excludes Bristow Academy, A/C held for sale, CIP, and reimbursable revenue. |

20 Conclusions • Client Promise is advancing and will have far reaching impacts on growth, fleet management and our valuable service offerings • Operating expenses this quarter were incurred in anticipation of future revenue growth, and resulted in disappointing 2QFY12 performance • We are revising our annual FY12 EPS guidance to $3.05 - $3.30 • Cash flow generation in FY12 is strong due to continued focus on BVA enhancing actions • Bristow is determined to appropriately balance growth and cash returns for our shareholders Analyst Day on November 10, 2011 in New York |

21 Appendix |

22 Organizational Chart - as of September 30, 2011 Business Unit (* % of Q2 FY12 Operating Revenue) Corporate Region ( # of Aircraft / # of Locations) Joint Venture (No. of aircraft) Key Operated Aircraft Bristow owns and/or operates 366 aircraft as of September 30, 2011 Affiliated Aircraft Bristow affiliates and joint ventures operate 186 aircraft as of September 30, 2011 |

23 Aircraft Fleet – Medium and Large As of September 30, 2011 Next Generation Aircraft Medium capacity 12-16 passengers Large capacity 18-25 passengers Mature Aircraft Models Aircraft Type No. of PAX Engine Consl Unconsl Total Ordered Large Helicopters AS332L Super Puma 18 Twin Turbine 30 - 30 - Bell 214ST 18 Twin Turbine - - - - EC225 25 Twin Turbine 18 - 18 2 Mil MI 8 20 Twin Turbine 7 - 7 - Sikorsky S-61 18 Twin Turbine 2 - 2 - Sikorsky S-92 19 Twin Turbine 25 2 27 8 82 2 84 10 LACE 76 Medium Helicopters AW139 12 Twin Turbine 7 5 12 - Bell 212 12 Twin Turbine 3 22 25 - Bell 412 13 Twin Turbine 36 35 71 - EC155 13 Twin Turbine 4 - 4 - Sikorsky S-76 A/A++ 12 Twin Turbine 20 6 26 - Sikorsky S-76 C/C++ 12 Twin Turbine 54 28 82 - 124 96 220 - LACE 57 |

24 Training Helicopters AS355 4 Twin Turbine 2 - 2 - Bell 206B 6 Single Engine 8 - 8 - Robinson R22 2 Piston 11 - 11 - Robinson R44 2 Piston 2 - 2 - Sikorsky 300CB/Cbi 2 Piston 46 - 46 - AS350BB 4 Turbine - 36 36 - Fixed Wing 1 - 1 - 70 36 106 - - Fixed Wing 3 38 41 - Total 366 186 552 10 TOTAL LACE (Large Aircraft Equivalent)* 154 10 Aircraft Fleet – Small, Training and Fixed As of September 30, 2011 (continued) Next Generation Aircraft Mature Aircraft Models Small capacity 4-7 passengers Training capacity 2-6 passengers •LACE does not include held for sale, training and fixed wing helicopters Aircraft Type No. of PAX Engine Consl Unconsl Total Ordered Small Helicopters Bell 206B 4 Turbine 2 2 4 - Bell 206 L-3 6 Turbine 4 6 10 - Bell 206 L-4 6 Turbine 30 1 31 - Bell 407 6 Turbine 41 - 41 - BK 117 7 Twin Turbine 2 - 2 - BO-105 4 Twin Turbine 2 - 2 - EC135 7 Twin Turbine 6 3 9 - Agusta 109 8 Twin Turbine - 2 2 - 87 14 101 - LACE 21 |

25 Consolidated Fleet Changes and Aircraft Sales for Q2 FY12 Q 1 FY12 Q 2 FY12 YTD Fleet Count Beginning Period 373 372 373 Delivered EC225 2 2 4 S-92 1 1 Total Delivered 2 3 5 Removed Sales (3) (5) (8) Other* (4) (4) Total Removed (3) (9) (12) 372 366 366 * Includes net lease returns and commencements # of A/C Sold Cash Received* Gain/ Loss* Q1 FY 12 3 2,478 1,525 Q2 FY 12 5 13,152 3,004 Totals 8 15,630 4,529 * Amounts stated in thousands Aircraft held for sale by BU EBU WASBU AUSBU OIBU NABU Total Large 3 - 3 - - 6 Medium 2 1 4 2 2 11 Small - 2 - - - 2 Total 5 3 7 2 2 19 |

26 # Helicopter Class Delivery Date Location Contracted # Helicopter Class Delivery Date Location 2 Large December 2011 NABU 2 of 2 2 Medium December 2012 EBU 1 Large December 2011 EBU 1 of 1 3 Large December 2012 EBU 1 Large March 2012 EBU 1 of 1 2 Medium June 2013 EBU 2 Large June 2012 EBU 2 of 2 1 Large September 2013 AUSBU 4 Large September 2012 EBU 1 Medium December 2013 OIBU 6 of 10 4 Large December 2013 EBU 1 Large December 2013 OIBU 1 Medium March 2014 OIBU 1 Large March 2014 OIBU 2 Medium June 2014 OIBU 1 Large June 2014 EBU 1 Medium September 2014 OIBU 1 Medium September 2014 AUSBU 1 Large September 2014 AUSBU 2 Medium December 2014 AUSBU 1 Large December 2014 AUSBU 1 Large March 2015 AUSBU 1 Large June 2015 AUSBU 1 Large September 2015 EBU 1 Large December 2015 EBU 1 Large March 2016 OIBU 1 Large June 2016 EBU 1 Large September 2016 OIBU 1 Large December 2016 EBU 1 Large March 2017 OIBU 1 Large June 2017 EBU 1 Large September 2017 OIBU 1 Large December 2017 OIBU 37 ORDER BOOK OPTIONS BOOK Order and options book as of September 30, 2011 Our order and options book reflects future contracted and line-of-sight work for the next five years with 10 large aircraft ordered and 25 large and 12 medium aircraft on option. * Subsequent to September 30, 2011, we entered into agreements to purchase or lease 8 new technology large aircraft for approximately $144 million that are not reflected in the table above. Fair market value of our fleet is ~$1.9 billion as of September 30, 2011. |

27 Operating margin trend 2008 2009 As Reported Full Year Full Year Q1 Q2 Q3 Q4 FY Q1 Q2 Q3 Q4 FY Q1 Q2 EBU 23.6% 19.3% 17.2% 16.7% 16.1% 18.1% 17.0% 18.0% 18.4% 19.6% 18.8% 18.8% 17.3% 16.8% WASBU 17.9% 21.5% 24.9% 29.3% 25.4% 34.7% 28.5% 26.5% 29.5% 29.8% 24.0% 27.4% 20.6% 25.2% NABU 14.5% 12.1% 8.9% 9.7% 3.3% 2.2% 6.1% 10.1% 16.1% 4.2% -4.0% 7.5% 3.6% 5.3% AUSBU 17.2% 5.9% 20.1% 23.1% 24.5% 24.5% 23.2% 22.5% 16.3% 17.2% 17.4% 18.2% 10.0% 1.7% OIBU 17.3% 27.0% 21.8% 35.1% 15.5% 1.8% 19.2% 6.9% 30.6% 27.7% 45.8% 28.4% 33.6% 5.8% Consolidated 16.0% 17.8% 15.4% 18.4% 13.1% 15.2% 15.5% 13.6% 17.1% 14.7% 16.1% 15.4% 11.3% 2.9% New methodology (operating income/operating revenue) 2008 2009 Revised * Full Year Full Year Q1 Q2 Q3 Q4 FY Q1 Q2 Q3 Q4 FY Q1 Q2 EBU 29.2% 24.3% 20.9% 20.5% 19.8% 22.4% 20.8% 21.4% 22.1% 25.4% 23.6% 23.6% 21.5% 20.7% WASBU 19.4% 22.8% 26.8% 30.0% 27.3% 35.7% 29.9% 27.1% 30.5% 30.4% 26.1% 28.6% 21.5% 26.4% NABU 14.5% 12.2% 8.9% 9.7% 3.3% 2.2% 6.2% 10.2% 16.4% 4.2% -4.0% 7.6% 3.6% 11.0% AUSBU 17.9% 6.3% 21.0% 24.5% 25.5% 25.6% 24.3% 23.6% 17.8% 18.8% 19.1% 19.8% 11.1% 1.9% OIBU 17.4% 27.3% 21.9% 35.9% 15.3% 1.9% 19.4% 6.9% 30.9% 28.2% 47.1% 28.8% 34.5% 5.9% Consolidated ** 16.4% 14.7% 15.9% 17.4% 14.2% 13.9% 15.3% 14.0% 18.0% 15.3% 18.3% 16.4% 12.2% 13.0% * - All amounts revised to exclude reimbursable revenue from denominator. ** - Revised to exclude aircraft sales from numerator. 2012 2010 2011 2012 2010 2011 |

28 EBIDTAR reconciliation ($ in millions) 2000 2001 2002 2003 2004 Income from continuing operations $8.8 $27.9 $42.5 $40.3 $49.6 Income tax expense 3.8 13.3 19.1 17.5 18.5 Interest expense 18.5 18.4 15.8 14.9 16.8 Depreciation and amortization 32.0 33.1 33.9 37.5 39.4 EBITDA Subtotal 63.1 92.7 111.4 110.2 124.3 Aircraft rental expense – – – – – EBITDAR $63.1 $92.7 $111.4 $110.2 $124.3 ($ in millions) 2005 2006 2007 2008 2009 Income from continuing operations $49.2 $54.5 $72.5 $107.7 $125.5 Income tax expense $20.4 $14.7 $38.8 $44.5 $50.5 Interest expense $15.7 $14.7 $10.9 $23.8 $35.1 Gain on disposal of assets ($0.1) ($10.6) ($9.4) ($9.1) Depreciation and amortization 40.5 42.1 42.5 54.1 65.5 EBITDA Subtotal 125.8 125.8 154.1 220.7 267.6 Aircraft rental expense – 2.1 6.3 6.3 8.2 EBITDAR $125.8 $127.9 $160.4 $227.0 $275.8 March 31, March 31, |

29 EBIDTAR reconciliation (continued) ($ in millions) 2010 2011 Income from continuing operations $113.5 $133.3 Income tax expense $29.0 $7.1 Interest expense $42.4 $46.2 Gain on disposal of assets (18.7) (10.2) Depreciation and amortization 74.7 90.9 EBITDA Subtotal 240.9 267.3 Aircraft rental expense 9.1 5.9 EBITDAR $250.1 $273.2 ($ in millions) YTD FY11 YTD FY12 TTM as of 9/30/2010 9/30/2011 9/30/2011 Income from continuing operations $59.8 $24.2 $97.7 Income tax expense 11.9 4.7 (0.1) Interest expense 22.5 18.4 42.1 Gain on disposal of assets (3.6) 0.2 (6.4) Depreciation and amortization 40.3 48.1 98.7 EBITDA Subtotal 130.8 95.6 232.1 Aircraft rental expense 3.0 2.8 5.8 EBITDAR $133.7 $98.4 $237.9 March 31, |

30 GAAP reconciliation |

31 Bristow Group Inc. (NYSE: BRS) 2000 West Sam Houston Parkway South Suite 1700, Houston, Texas 77042 t 713.267.7600 f 713.267.7620 bristowgroup.com Contact Us |