Bristow Group Inc. Investor Relations Presentation August 2012 Exhibit 99.1 |

2 Forward-looking statements This presentation may contain “forward-looking statements” within the meaning of the Private Securities Litigation Reform Act of 1995. Forward-looking statements include statements about our future business, operations, capital expenditures, fleet composition, capabilities and results; modeling information, earnings guidance, expected operating margins and other financial projections; future dividends, share repurchase and other uses of excess cash; plans, strategies and objectives of our management, including our plans and strategies to grow earnings and our business, our general strategy going forward and our business model; expected actions by us and by third parties, including our customers, competitors and regulators; the valuation of our company and its valuation relative to relevant financial indices; assumptions underlying or relating to any of the foregoing, including assumptions regarding factors impacting our business, financial results and industry; and other matters. Our forward-looking statements reflect our views and assumptions on the date of this presentation regarding future events and operating performance. They involve known and unknown risks, uncertainties and other factors, many of which may be beyond our control, that may cause actual results to differ materially from any future results, performance or achievements expressed or implied by the forward-looking statements. These risks, uncertainties and other factors include those discussed under the captions “Risk Factors” and “Management’s Discussion and Analysis of Financial Condition and Results of Operations” in our Annual Report on Form 10-K for the fiscal year-ended March 31, 2012 and our Quarterly Report on Form 10-Q for the quarter ended June 30, 2012. We do not undertake any obligation, other than as required by law, to update or revise any forward-looking statements, whether as a result of new information, future events or otherwise. |

3 Bristow is the leading provider of helicopter services and is a unique investment in oil field services • ~20 countries • 551 aircraft • ~3,400 employees • Ticker: BRS • Stock price * : $45.77/share • Market cap * : ~$1.7 billion • Quarterly dividend of $0.20/share $67 Bristow flies crews and light cargo to production platforms, vessels and rigs * Based on 36.4 million fully diluted weighted average shares outstanding for the three months ended 06/30/2012 and stock price as of July 31, 2012 |

4 • Safety is our primary core value • Bristow’s ‘Target Zero’ program is now the leading example emulated industry-wide • Safety Performance accounts for 25% of management incentive compensation • 2011 National Ocean Industries Association (NOIA) Safety in Seas Award Winner our industry leading safety program, creates differentiation and client loyalty , TARGET ZERO |

5 Bristow services are utilized in every phase of offshore oil and gas activity, especially production • Largest share of revenues (>60%) relates to oil and gas production, providing stability and growth opportunities • There are ~ 8,000 offshore production installations worldwide — compared with >600 exploratory drilling rigs • ~ 1,700 helicopters are servicing the worldwide oil and gas industry of which Bristow’s fleet is approximately one-third • Bristow revenues are primarily driven by operating expenditures Typical revenues by segment PRODUCTION Exploration 20% Development 10% Production 60% Other 10% SEISMIC EXPLORATION DEVELOPMENT ABANDONMENT H e l i c o p t e r t r a n s p o r t a t i o n s e r v i c e s |

6 Bristow’s contract and operations structure generates more predictable income with significant operating leverage Revenue sources • Two tiered contract structure includes both: – Fixed or monthly standing charge to reserve helicopter capacity – Variable fees based on hours flown with fuel pass through • Bristow contracts earn 65% of revenue without flying Operating income Fixed monthly 70% Variable hourly 30% Fixed monthly 65% Variable hourly 35% |

7 Why Bristow? $275 • Bristow has changed its client and capital allocation approach (Client Promise/Bristow Value Added) to generate better cash returns and fund it’s growth • Bristow is enjoying improved pricing for its services with better utilization especially in North America • Bristow is growing with demand not dependent on economic or commodity cycles • Bristow’s asset values continue to be resilient even in depressed economic times as there is strong demand for helicopters outside of exploration and production (E&P) • Bristow cash flow has increased 53% since FY11 and is more than 2 times higher than our next four competitors* combined * Four competitors are CHC, ERA, Inaer Aviation, and PHI. Data from latest filings as of July 29, 2012. ERA based on S-1 pro-forma. |

8 CHANGE: Bristow’s Client Promise initiative is gaining traction and is behind our margin improvement Target Zero accidents, downtime and complaints programs deliver value to operators. More zero-accident flight hours than anyone, more uptime than anyone, and hassle-free service creates confidence in flight. Worldwide. Lowers client’s offshore operating costs and improves productivity. Earns us more business to improve BVA. |

9 CHANGE: Bristow Value Added (BVA) makes employees treat the cost of capital like any other expense • BVA is the key measure to define Bristow’s financial success and charges managers for the capital they use every day • BVA has changed i) the way working capital is managed, and ii) has led to our operating lease initiative * Reconciliation for these items is in the appendix ** Quarterly capital charge of 2.625% is based on annual capital charge of 10.5% BRISTOW VALUE ADDED CALCULATION SAMPLE BVA =Gross Cash Flow – (Gross Operating Assets X Capital Charge) BVA = GCF - ( GOA X 10.5%** ) Bristow Value Added calculation for Q1 FY12 ($15.4) = $60* - ( $2,874* X 2.625%** ) Bristow Value Added calculation for Q1 FY13 $1.9 = $80* - ( $2,976* X 2.625%** ) |

10 • Of the 56 aircraft currently leased in our fleet, 30 are training and 26 are commercial (18 LACE) • 18 LACE aircraft represent approximately 12% of our commercial fleet • Our goal is for commercial fleet operating leases to account for 20-30% of our LACE Leased aircraft as of June 30, 2012 Large Medium Small Total Leased LACE Total LACE % Leased EBU 8 - - 8 8 47 17% WASBU - 1 - 1 1 22 2% NABU 2 11 1 14 8 30 26% AUSBU 1 - 2 3 2 18 11% OIBU - - - - - 32 0% Total 11 12 3 26 18 147 12% amount of capital needed to grow Operating lease initiative: lowering the cost and |

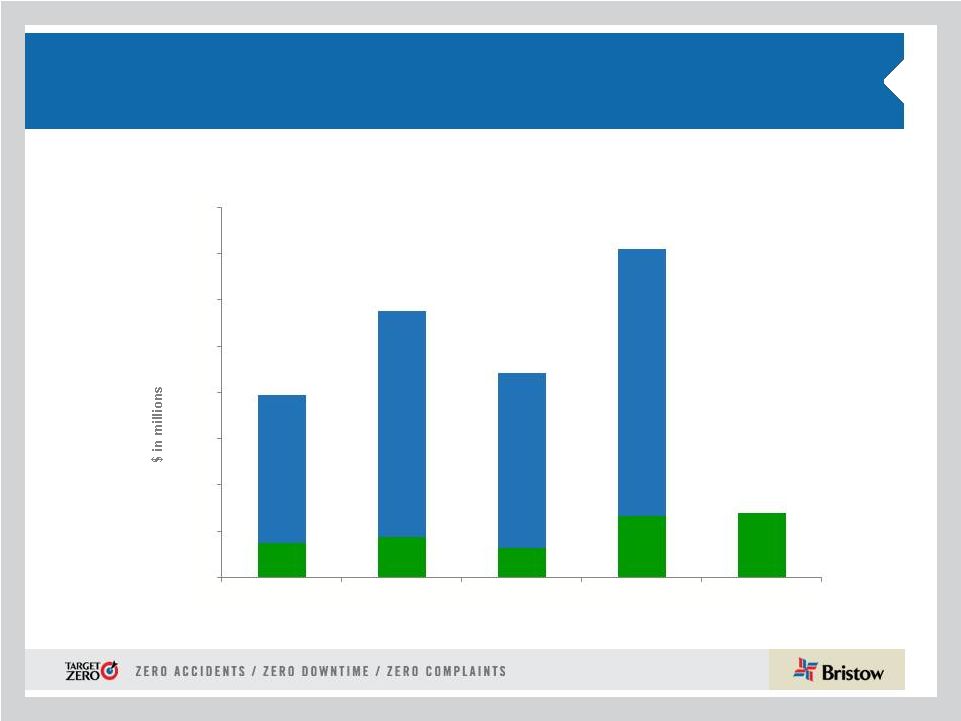

11 Net cash provided by operating activities See June 30, 2012 10-Q for more information on cash flow provided by operating activities Our focus on BVA has yielded much higher operating 29.6 35.0 25.7 52.9 55.4 127.9 195.4 151.4 231.3 0 40 80 120 160 200 240 280 320 FY09 FY10 FY11 FY12 Q1 FY13 cash flow generation . . . |

12 . . . And when combined with leasing, creates a significantly higher cash and liquidity position Total Liquidity 178 261 100 145 140 160 78 116 262 227 0 50 100 150 200 250 300 350 400 450 31-Mar-10 31-Mar-11 31-Mar-12 30-Jun-12 Undrawn borrowing capacity Cash 402 387 |

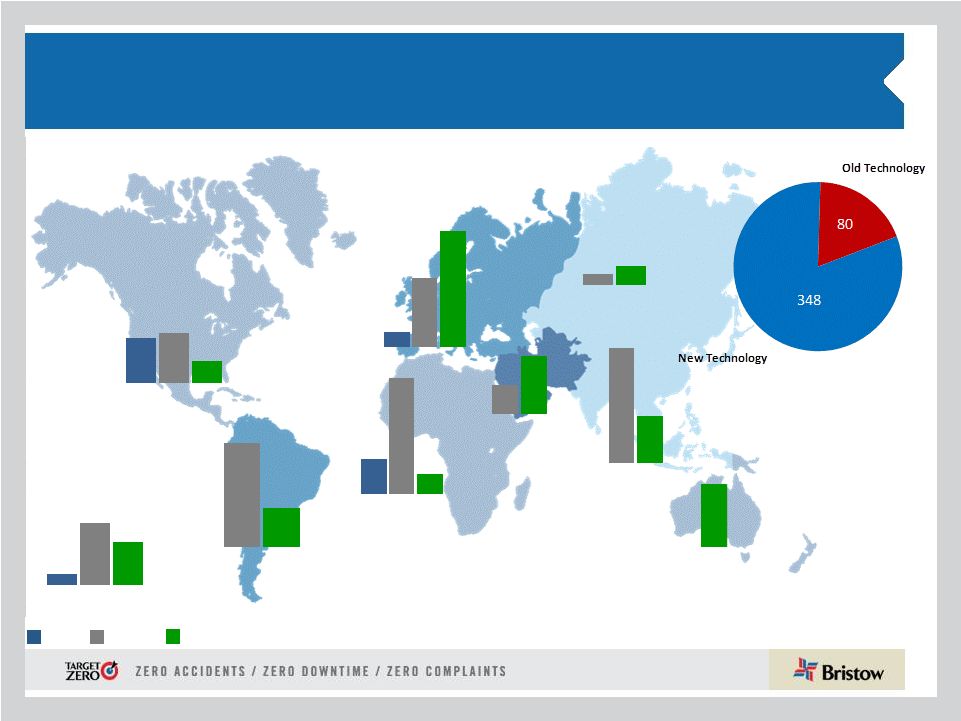

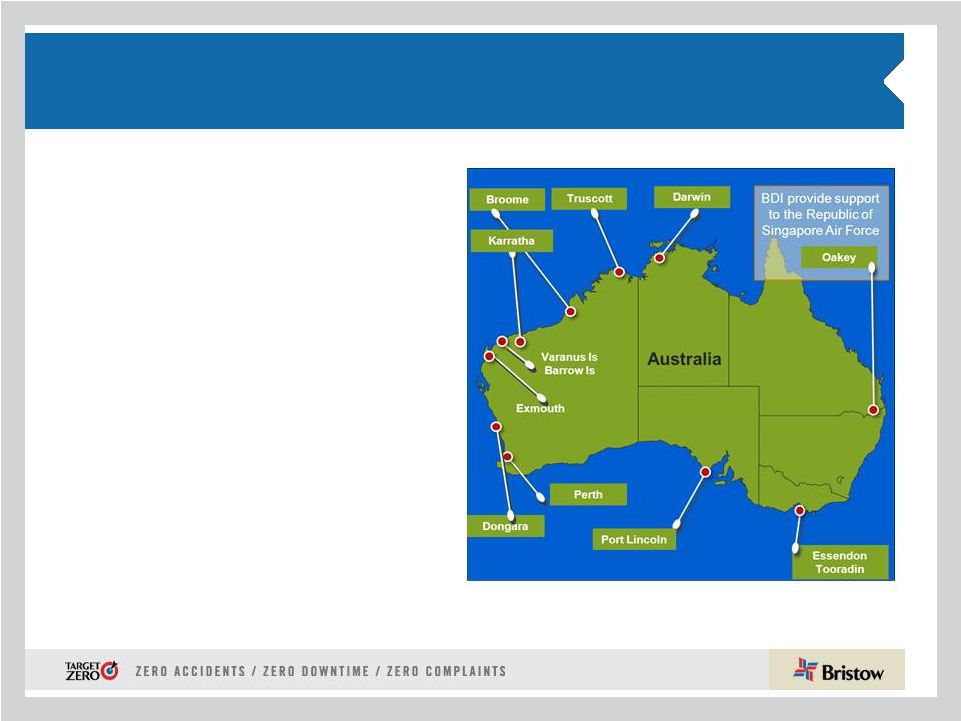

13 56 9 5 109 40 8 5 North America Brazil, Peru, Trinidad Gulf of Guinea Mid East, East Africa, India, Bangladesh Malaysia, Thailand Indonesia Australia Small Medium Large Total Opportunities * . . . Which allows us to pursue the larger scope of growth opportunities identified between FY13 and FY17 30 40 228 160 11 31 24 27 12 7 Europe Russia / Caspian 69 20 10 33 3 5 |

14 Overall activity above pre- 2008 levels • The overall market both in terms of tender activity and pricing is improving • North Sea tender activity remains at historic levels • Aircraft supply is tightening with significant search and rescue (SAR) requirements (both governmental and O&G) and faster Brazilian expansion Brazil growth accelerates NABU market returning • Petrobras board approved 52 incremental aircraft through FY15 with a focus on heavy aircraft. First ten were awarded, of which Lider will provide five, and a new bid is expected later this year for the next tranche. • International demand outside of Brazil expected to be at least equal to Brazilian demand suggesting further tightening of supply/demand for large a/c • Most clients increasing activity in USGoM as rigs go back to work • Eastern Canada new drilling activity increasing with Statoil, ExxonMobil and Chevron . . . With the market outlook even better in FY13 |

15 CONCLUSION: Bristow enjoys the strongest balance sheet in our industry with ample liquidity, cash flow and asset value Ample Liquidity with underlying asset value Significant Cash Flow generation • Bristow generated 53% more operating cash flow in FY12 compared to FY11. Operating cash flow in Q1 FY13 was 5% higher than Q1 FY12 and 48% higher than the sequential Q4 FY12 • Bristow closed Q1 FY13 with almost $400 million of liquidity • Fair market value of aircraft is well above share price at June 30, 2012 Prudent Balance Sheet management • Adjusted Debt/Capital Ratio less than 45% with a BBB- rating from Standard & Poor’s for secured debt • Operating lease strategy used to finance growth with a competitive cost of capital |

16 The “Growth Price Signal” is provided by the commercial markets and outlook for ANNUAL EPS Growth Cash Flow Yield = OCF + A/C sales – Depreciation Market Capitalization We can provide a balanced return, but some years we will “Go Faster” depending on price signals The “Capital Return Price Signal” is provided by the financial markets and our current free cash flow yield Today this equals 13.5 %* FY13 EPS Guidance: $3.25 - $3.55 FY12 – FY13 EPS Midpoint Growth 9.0 % = *Trailing twelve months as of June 30, 2012 Conclusion: Bristow provides investors with unique combination of growth and balanced return |

17 Appendix |

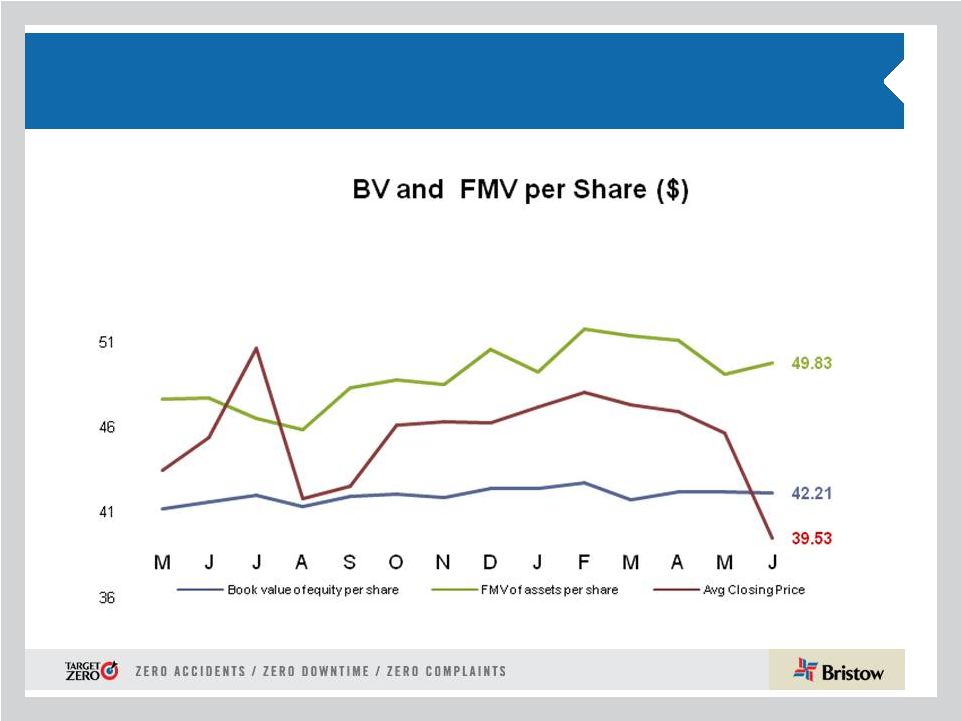

18 Bristow’s asset values are resilient as there is strong demand for helicopters outside of oil field services |

19 • Europe represented 39% of Bristow operating revenue and 42% of adjusted EBITDAR* in Q1 FY13 • Operating revenue increased to $123.2M in Q1 FY13 from $108.3M in Q1 FY12 with the addition of four large aircraft and increased activity with new and existing contracts in the UK and Norway • Adjusted EBITDAR increased to $39.7M in Q1 FY13 from $35.7M in Q1 FY12, while adjusted EBITDAR margin remained relatively flat at 32.2% in Q1 FY13 versus 33.0% in Q1 FY12 • Outlook: • Bristow is shortlisted for UK SAR program with results to be announced in early 2013 • High activity continues as demonstrated by new awards for nine aircraft recently announced. Additional awards are anticipated next quarter. FY13 adjusted EBITDAR margin expected to be ~ low thirties Europe (EBU) * Operating revenue and adjusted EBITDAR percentages exclude corporate and other. |

20 West Africa (WASBU) • Nigeria represented 21% of Bristow operating revenue and 22% of adjusted EBITDAR* in Q1 FY13 • Operating revenue of $66.4M in Q1 FY13 increased 27% from $52.3M in Q1 FY12 due to strong activity and a 12% increase in flight hours compared to Q1 FY12 • Adjusted EBITDAR increased to $21.2M in Q1 FY13 from $15.4M in Q1 FY12 with adjusted EBITDAR margin of 32% in Q1 FY13 vs 30% in Q1 FY12 Outlook: • Improved service through Client Promise initiative continues to drive strong results: Two existing contracts extended with better pricing and terms • Upcoming heavy maintenance on several aircraft will impact Q2 and Q3 FY13 • We continue to work on optimizing the operating model in this business unit as part of the local content initiative FY13 adjusted EBITDAR margin expected to be ~ low thirties * Operating revenue and adjusted EBITDAR percentages exclude corporate and other. |

21 • • North America represented 17% of Bristow operating revenue and 13% of adjusted EBITDAR* in Q1 FY13 • Adjusted EBITDAR doubled to $12.2M in Q1 FY13 vs. $6.3M in Q1 FY12 and adjusted EBITDAR margin was 23.2% in Q1 FY13 versus 14.3% in Q1 FY12 • Sequential improvement of almost 50% in adjusted EBITDAR from $8.2M in Q4 FY12 to $12.2M in the current quarter • Business model performed with key parameters significantly better; several mid-teen price increases; large aircraft working and costs contained Outlook: • Our business is improving in FY13 similar to other oil service sector recoveries - more rigs, more people, and more investment • Client Promise initiative continues to deliver positive results FY13 adjusted EBITDAR expected to be ~ low twenties North America (NABU) * Operating revenue and adjusted EBITDAR percentages exclude corporate and other. |

22 Australia (AUSBU) • Australia represented 12% of Bristow operating revenue and 11% of adjusted EBITDAR* in Q1 FY13 • Operating revenue of $38.2M in Q1 FY13 decreased from $40.9M in Q1 FY12 due to a decrease in overall flight activity • Adjusted EBITDAR increased to $10.3M in Q1 FY13 from $8.3M in Q1 FY12 and adjusted EBITDAR margin increased to 27.0% in Q1 FY13 from 20.2% in Q1 FY12 reflecting better asset utilization along with lower operating costs Outlook: • INPEX award of a ten-year contract for up to six large aircraft with an option to add a long term SAR aircraft with the start date in FY14 • Aircraft will be redeployed as short- term contracts roll off; will impact performance in Q2 and Q3 FY13 • An additional medium aircraft contract award with improved terms * Operating revenue and adjusted EBITDAR percentages exclude corporate and other. FY13 adjusted EBITDAR margin expected to be ~ mid to high twenties |

23 Other International (OIBU) • Other International represented 11% of Bristow operating revenue and 12% of adjusted EBITDAR* in Q1 FY13 • Operating revenue decreased to $33.2M in Q1 FY13 vs. $34.5M in Q1 FY12 due to decrease in activity in Ghana and the end of a contract in the Baltic Sea • Adjusted EBITDAR margin of 36.2% in Q1 FY13 decreased from 48.1% in Q1 FY12 due primarily to decreased earnings from unconsolidated affiliates (particularly Lider in Brazil), activity reduction in Mexico, and increased operating costs in Trinidad • Lider equity earnings decreased to $0.0M in Q1 FY13 compared to $2.7M in Q1 FY12 * Operating revenue and adjusted EBITDAR percentages exclude corporate and other. Outlook: • • • FY13 adjusted EBITDAR margin expected to be ~ low to mid forties Potential new opportunities in Caspian, East Africa, Southeast Asia and the Caribbean Petrobras awarded Lider contracts for five new large aircraft, with one leased by Bristow to Lider, with operations scheduled to commence starting in August 2012 through April 2013 Lider’s second half of the year is expected to be better than the first half as operations under new contracts begin. Currency fluctuations make it difficult to predict if this will translate into higher equity earnings |

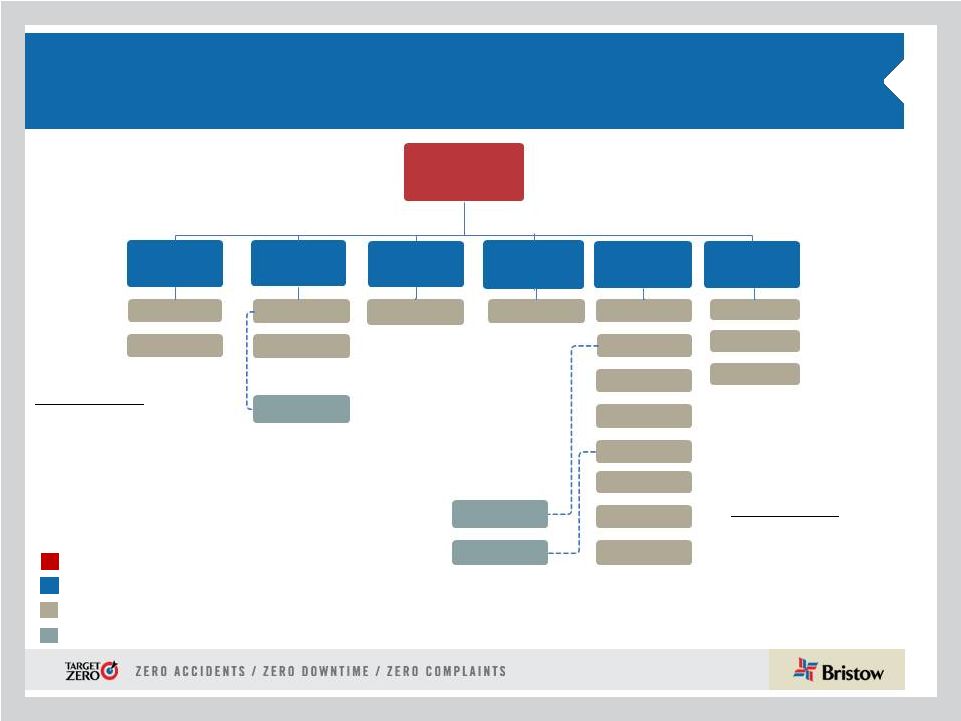

24 Organizational chart - as of June 30, 2012 Business Unit (% of FY13 Operating Revenue) Corporate Region ( # of Aircraft / # of Locations) Joint Venture (# of aircraft) Key Operated Aircraft Bristow owned and/or operated 357 aircraft as of June 30, 2012 Affiliated Aircraft Bristow affiliates and joint ventures operated 194 aircraft as of June 30, 2012 Bristow NABU 16% U.S. GoM – 79/7 Trinidad – 10 /1 Alaska – 12/3 Mexico – 12/5 Brazil –10/9 Lider - 85 UK –32/4 Norway – 26/3 FBH - 64 Nigeria – 45/7 Australia –28/10 Other – 12/1 Russia – 7/3 Egypt – –/– Turkmenistan – 2/1 PAS - 45 AUSBU 12% EBU 39% Florida – 58/1 Louisiana – 14/1 U.K. – 5/1 Malaysia – 5/2 WASBU 21% OIBU 10% BRS Academy 2% |

25 Aircraft fleet – medium and large as of June 30, 2012 Next Generation Aircraft Medium capacity 12-16 passengers Large capacity 18-25 passengers Mature Aircraft Models Aircraft Type No. of PAX Engine Consl Unconsl Total Ordered Large Helicopters AS332L Super Puma 18 Twin Turbine 23 - 23 - AW189 16 Twin Turbine - - - 6 EC225 25 Twin Turbine 18 - 18 - Mil MI 8 20 Twin Turbine 7 - 7 - Sikorsky S-61 18 Twin Turbine 2 - 2 - Sikorsky S-92 19 Twin Turbine 32 4 36 11 82 4 86 17 LACE 76 Medium Helicopters AW139 12 Twin Turbine 7 2 9 - Bell 212 12 Twin Turbine 1 14 15 - Bell 412 13 Twin Turbine 34 20 54 - EC155 13 Twin Turbine 3 - 3 - Sikorsky S-76A/A++ 12 Twin Turbine 15 5 20 - Sikorsky S-76C/C++ 12 Twin Turbine 52 31 83 - 112 72 184 - LACE 51 |

26 Aircraft fleet – small, training and fixed as of June 30, 2012 (continued) Next Generation Aircraft Mature Aircraft Models Small capacity 4-7 passengers Training capacity 2-6 passengers •LACE does not include held for sale, training and fixed wing helicopters Aircraft Type No. of PAX Engine Consl Unconsl Total Ordered Small Helicopters Bell 206B 4 Turbine 1 2 3 - Bell 206 L-3 6 Turbine 4 6 10 - Bell 206 L-4 6 Turbine 29 1 30 - Bell 407 6 Turbine 39 - 39 - BK 117 7 Twin Turbine 2 - 2 - BO-105 4 Twin Turbine 2 - 2 - EC135 7 Twin Turbine 6 3 9 - 83 12 95 - LACE 21 Training Helicopters AW139 12 Twin Turbine - 3 3 - Bell 412 13 Twin Turbine - 8 8 - Bell 212 12 Twin Turbine - 15 15 - AS355 4 Twin Turbine 5 - 5 - AS350BB 4 Turbine - 36 36 - Agusta 109 8 Twin Turbine - 2 2 - Bell 206B 6 Single Engine 12 - 12 - Robinson R22 2 Piston 12 - 12 - Robinson R44 2 Piston 2 - 2 - Sikorsky 300CB/Cbi 2 Piston 45 - 45 - Fixed Wing 1 - 1 - 77 64 141 - Fixed Wing 3 42 45 - Total 357 194 551 17 TOTAL LACE (Large Aircraft Equivalent) 147 |

27 # Helicopter Class Delivery Date Location Contracted # Helicopter Class Delivery Date 3 Large December 2012 EBU 3 1 Large September 2013 2 Large December 2012 WASBU 0 1 Large December 2013 2 Large March 2013 EBU 2 1 Large March 2014 1 Large September 2013 EBU 0 1 Large June 2014 1 Large September 2013 NABU 0 1 Large September 2014 2 Large December 2013 OIBU 0 1 Large December 2014 1 Large September 2014 NABU 0 1 Large March 2015 1 Large December 2014 OIBU 0 2 Large June 2015 1 Large March 2015 OIBU 0 2 Large September 2015 1 Large June 2015 EBU 0 2 Large December 2015 1 Large March 2016 EBU 0 1 Large March 2016 1 Large June 2016 AUSBU 0 2 Large June2016 17 5 2 Large September 2016 2 Large December 2016 * Six large ordered aircraft expected to enter service beginning 1 Large March 2017 in calendar year 2014 are subject to the successful development 1 Large June 2017 and certification of the aircraft. 1 Large September 2017 1 Large December 2017 1 Medium June 2013 4 Medium December 2013 3 Medium June 2014 2 Medium September 2014 2 Medium June 2015 36 ORDER BOOK* OPTIONS BOOK Order and options book as of June 30, 2012 |

28 Consolidated fleet changes and aircraft sales for Q1 FY13 Q 1 FY13 Fleet Count Beginning Period 361 Delivered S-92 2 Total Delivered 2 Removed Sales (4) Other* (2) Total Removed (6) 357 * Includes destroyed aircraft, lease returns and commencements Fleet changes EBU WASBU NABU AUSBU OIBU Total Large 3 - - 3 - 6 Medium 2 1 - 1 7 11 Small - - - - - - Total 5 1 - 4 7 17 Aircraft held for sale by BU Large 8 - 2 1 - - 11 Medium - 1 11 - - - 12 Small - - 1 2 - - 3 Fixed - - - - - - - Training - - - - - 30 30 Total 8 1 14 3 - 30 56 Leased aircraft in consolidated fleet EBU WASBU NABU AUSBU OIBU BA Total # of A/C Sold Received* Q1 FY13 4 19 $ Totals 4 19 $ * $ in millions |

29 Operating revenue LACE LACE Rate 2, 3 EBU $123.2 47 $10.60 WASBU 66.4 22 12.35 NABU 52.6 30 7.05 AUSBU 38.2 18 8.48 OIBU 4 33.2 32 4.22 Total $313.6 147 $8.55 Operating Revenue, LACE, and LACE Rate by BU as of June 30, 2012 Operating Revenue, LACE and LACE Rate by BU 1) $ in millions 2) LACE Rate is annualized 3) $ in millions per LACE 4) OIBU LACE rate is lower than other business units’ LACE rate due to a large proportion of revenue being from dry leases 1 |

30 Adjusted EBITDAR margin* trend Q1 Q2 Q3 Q4 Full Year Q1 Q2 Q3 Q4 Full Year EBU 31.2% 31.7% 31.9% 28.0% 30.8% 29.8% 31.5% 34.6% 34.4% 32.7% WASBU 31.7% 36.8% 33.7% 39.1% 36.0% 33.7% 36.9% 35.8% 34.3% 35.2% NABU 18.3% 20.0% 14.9% 17.7% 17.8% 20.8% 25.8% 15.9% 8.5% 18.5% AUSBU 26.5% 36.7% 34.4% 31.3% 32.4% 33.2% 26.1% 27.0% 31.1% 29.3% OIBU 34.4% 37.6% 25.9% 25.1% 31.0% 18.3% 40.2% 37.4% 59.4% 39.3% Consolidated 24.7% 27.8% 24.7% 23.9% 25.3% 23.8% 27.5% 25.9% 29.6% 26.7% 2013 Q1 Q2 Q3 Q4 Full Year Q1 EBU 33.0% 31.4% 30.7% 36.1% 32.9% 32.2% WASBU 29.5% 35.5% 37.2% 36.6% 35.0% 31.9% NABU 14.3% 20.6% 14.8% 19.4% 17.3% 23.2% AUSBU 20.2% 14.4% 23.5% 35.6% 24.3% 27.0% OIBU 48.1% 19.1% 47.8% 42.9% 39.5% 36.2% Consolidated 23.4% 24.0% 27.6% 31.2% 26.6% 26.3% 2010 2011 2012 * Adjusted EBITDAR excludes special items and asset dispositions and calculated by taking adjusted EBITDAR divided by operating revenue |

31 Adjusted EBITDAR* reconciliation * Adjusted EBITDAR excludes special items and asset dispositions ($ in millions) Q1 Q2 Q3 Q4 Full Year Q1 Q2 Q3 Q4 Full Year Net income $24.0 $33.7 $27.1 $28.7 $113.5 $20.9 $38.8 $42.3 $31.2 $133.3 Income tax expense 9.5 11.2 5.7 2.6 29.0 8.5 3.3 -11.8 7.1 7.1 Interest expense 10.0 10.6 11.0 10.8 42.4 11.0 11.5 13.8 9.9 46.2 Gain on disposal of assets -6.0 -4.9 -2.4 -5.3 -18.7 -1.7 -1.9 0.0 -5.1 -8.7 Depreciation and amortization 18.2 18.5 20.7 17.4 74.7 19.3 21.0 21.3 27.7 89.4 Special items 2.6 -2.5 -1.1 1.0 0.0 0.0 0.0 -1.2 2.4 1.2 EBITDA Subtotal 58.2 66.7 60.9 55.1 240.9 58.1 72.7 64.4 73.3 268.5 Rental expense 7.0 7.0 7.2 6.3 27.3 6.6 6.1 8.7 7.7 29.2 Adjusted EBITDAR $65.2 $73.6 $68.1 $61.3 $268.2 $64.7 $78.8 $73.1 $81.1 $297.7 3/31/2013 ($ in millions) Q1 Q2 Q3 Q4 Full Year Q1 Net income $21.2 $3.0 $26.5 $14.6 $65.2 $24.2 Income tax expense 6.6 -1.9 7.1 2.4 14.2 6.2 Interest expense 9.0 9.5 9.8 10.0 38.1 8.8 Gain on disposal of assets -1.4 1.6 2.9 28.6 31.7 5.3 Depreciation and amortization 22.7 25.4 22.7 25.3 96.1 21.4 Special items 0.0 24.6 0.0 3.4 28.1 2.2 EBITDA Subtotal 58.1 62.1 68.9 84.3 273.4 68.0 Rental expense 9.0 9.1 12.8 15.1 46.0 16.3 Adjusted EBITDAR $67.0 $71.2 $81.8 $99.5 $319.5 $84.3 3/31/2010 3/31/2011 3/31/2012 Fiscal year ended Fiscal year ended |

32 Bristow Value Added (BVA) Sample calculation * Reconciliation for these items on following two pages ** Quarterly capital charge of 2.625% is based on annual capital charge of 10.5% Bristow Value Added = Gross Cash Flow – (Gross Operating Assets X Capital Charge) BVA = GCF - ( GOA X 10.5%** ) Bristow Value Added calculation for Q1 FY12 ($15.4) = $60* - ( $2,874* X 2.625%** ) Bristow Value Added calculation for Q1 FY13 $1.9 = $80* - ( $2,976* X 2.625%** ) |

33 Gross cash flow presentation ($ in millions) Gross Cash Flow Reconciliation Q1 FY12 Q1 FY13 Net Income $21 $24 Depreciation and Amortization 23 21 Interest Expense 9 9 Interest Income (0) (0) Rent 9 16 Other Income/expense-net (0) 1 Gain/loss on Asset Sale (1) 5 Special Items 0 2 Tax Effect from Special Items 0 (2) Earnings (losses) from Unconsolidated Affiliates, Net (6) (2) Non-controlling Interests 0 1 Gross Cash Flow before Lider $54 $75 Gross Cash Flow - Lider proportional 6 5 Gross Cash Flow after Lider $60 $80 Special items: FY13 includes: $2.2m special charge for severance costs related to the termination of a contract in the Southern North Sea |

34 Gross operating asset presentation ($ in millions) Adjusted Gross Operating Assets Reconciliation Q1 FY12 Q1 FY13 Total Assets $2,701 $2,740 Accumulated Depreciation 463 468 Capitalized Operating Leases 136 194 Cash and Cash Equivalents (117) (227) Investment in Unconsolidated Entities (210) (201) Goodwill (30) (29) Intangibles (7) (4) Assets Held for Sale: Net (34) (18) Assets Held for Sale: Gross 77 86 Adj. for gains & losses on assets sales (0) 116 Accounts Payable (51) (58) Accrued Maintenance and Repairs (11) (16) Other Accrued Taxes (4) (7) Accrued Wages, Benefits and Related Taxes (33) (43) Other Accrued Liabilities (18) (27) Income Taxes Payable (16) (10) Deferred Revenue (9) (13) ST Deferred Taxes (10) (15) LT Deferred Taxes (155) (142) Adjusted Gross Operating Assets before Lider $2,672 $2,794 Adjusted Gross Operating Assets - Lider proportional 202 182 Adjusted Gross Operating Assets after Lider $2,874 $2,976 |

35 GAAP reconciliation (i) These amounts are presented after applying the appropriate tax effect to each item and dividing by the weighted average shares outstanding during the related period to calculate the earnings per share impact. Three Months Ended June 30, 2012 2011 (In thousands, except per share amounts) Adjusted operating income Gain (loss) on disposal of assets Severance costs for termination of a contract Operating income Adjusted EBITDAR Gain (loss) on disposal of assets Severance costs for termination of a contract Depreciation and amortization Rent expense Interest expense Provision for income taxes Net income Adjusted net income $ Gain (loss) on disposal of assets (i) Severance costs for termination of a contract (i) Net income attributable to Bristow Group $ Adjusted diluted earnings per share Gain (loss) on disposal of assets (i) Severance costs for termination of a contract (i) Diluted earnings per share $ 47,470 $ 34,989 (5,315) 1,416 (2,162) $ 84,273 $ 67,025 (5,315) 1,416 (2,162) (21,372) (22,708) (16,274) (8,953) (8,774) (8,955) (6,180) (6,606) $ $ $ 39,993 $ 36,405 24,196 21,219 29,618 $ 19,878 (4,234) 1,167 (1,722) $ 23,662 21,045 $ 0.81 (0.12) (0.05) 0.65 $ 0.54 0.03 — 0.57 — — — |

36 Leverage reconciliation *Adjusted EBITDAR exclude gains and losses on dispositions of assets Debt Investment Capital Leverage (a) (b) (c) = (a) + (b) (a) / (c) (in millions) As of June 30, 2012 736.3 $ 1,540.7 $ 2,277.0 $ 32.3% Adjust for: Unfunded pension liability 109.8 109.8 NPV of all lease obligations 217.0 217.0 Letters of credit 1.5 1.5 Adjusted 1,064.6 $ (d) 1,540.7 $ 2,605.3 $ 40.9% Calculation of debt to adjusted EBITDAR multiple Adjusted EBITDAR*: FY 2012 336.8 $ (e) Annualized 449.1 $ = (d) / (e) 3.16:1 |

37 Bristow Group Inc. (NYSE: BRS) 2103 City West Blvd., 4 Floor Houston, Texas 77042 t 713.267.7600 f 713.267.7620 bristowgroup.com Contact us th |