SCHEDULE 14A

(RULE 14A – 101)

INFORMATION REQUIRED IN PROXY STATEMENT

SCHEDULE 14A INFORMATION

PROXY STATEMENT PURSUANT TO SECTION 14 (a) OF THE SECURITIES

EXCHANGE ACT OF 1934

(AMENDMENT NO. 5)

Filed by the Registrantþ Filed by a Party other than the Registrant¨

Check the appropriate box:

| ¨ | Preliminary Proxy Statement |

| ¨ | Definitive Proxy Statement |

| ¨ | Definitive Additional Materials |

| þ | Soliciting Material Pursuant to Rule 14a-11 (c) or Rule 14a-12 |

| ¨ | CONFIDENTIAL, FOR THE USE OF THE COMMISSION ONLY (AS PERMITTED BY RULE 14a-6 (e) (2) ) |

Ohio Casualty Corporation

(NAME OF REGISTRANT AS SPECIFIED IN ITS CHARTER)

(NAME OF PERSON (S) FILING PROXY STATEMENT, IF OTHER THAN THE REGISTRANT)

Payment of Filing Fee (Check the appropriate box):

| þ | No fee required. |

| ¨ | Fee computed on table below per Exchange Act Rules 14a-6 (i) (1) and 0-11. |

| (1) | Title of each class of securities to which transaction applies: |

| (2) | Aggregate number of securities to which transaction applies: |

| (3) | Per unit price or other underlying value of transaction computed pursuant to Exchange Act Rule 0-11 (Set forth the amount on which the filing fee is calculated and state how it was determined): |

| (4) | Proposed maximum aggregate value of transaction: |

| (5) | Total fee paid: |

| ¨ | Fee paid previously with preliminary materials. |

| ¨ | Check box if any part of the fee is offset as provided by Exchange Act Rule 0-11 (a) (2) and identify the filing for which the offsetting fee was paid previously. Identify the previous filing by registration statement number, or the Form or Schedule and the date of its filing. |

| (1) | Amount Previously Paid: |

| (2) | Form, Schedule or Registration Statement No.: |

| (3) | Filing Party: |

| (4) | Date Filed: |

Please Note

| · | Additional Information and Where to Find It |

This communication may be deemed to be solicitation material in respect of the proposed transaction. In connection with the proposed transaction, a proxy statement of Ohio Casualty and other materials have been filed with the SEC. WE URGE INVESTORS TO READ THE PROXY STATEMENT AND THESE OTHER MATERIALS CAREFULLY BECAUSE THEY CONTAIN IMPORTANT INFORMATION ABOUT OHIO CASUALTY CORPORATION AND THE PROPOSED TRANSACTION. Investors are able to obtain free copies of the proxy statement as well as other filed documents containing information about Ohio Casualty on the SEC’s website athttp://www.sec.gov. Free copies of Ohio Casualty’s SEC filings are also available from Ohio Casualty Corporation, 9450 Seward Road, Fairfield, Ohio 45014, Attention: Investor Relations.

| · | Participants in the Solicitation |

Ohio Casualty and its executive officers, directors, other members of management, employees and Liberty Mutual may be deemed, under SEC rules, to be participants in the solicitation of proxies from Ohio Casualty’s shareholders with respect to the proposed transaction. Information regarding the executive officers and directors of Ohio Casualty is set forth in its definitive proxy statement for its 2007 annual meeting filed with the SEC on April 4, 2007. More detailed information regarding the identity of potential participants, and their direct or indirect interests, by securities holdings or otherwise, is also set forth in the proxy statement filed with the SEC in connection with the proposed transaction and dated June 29, 2007.

Financial Highlights

[DOLLARS IN MILLIONS]

December 31, | 2006 | 2005 | 2004 | |||||||||||

Liberty Mutual | Revenues | $ | 23,520 | $ | 21,161 | $ | 19,641 | |||||||

Group | Pre-tax operating income | 1,640 | 399 | 766 | ||||||||||

| Net income | 1,626 | 1,027 | 1,245 | |||||||||||

| Cash Flow from operations | 3,895 | 3,464 | 3,237 | |||||||||||

| Total assets | 85,498 | 78,824 | 72,457 | |||||||||||

| GAAP combined ratio | 99.3 | % | 105.7 | % | 102.9 | % | ||||||||

Personal Markets | Revenues | $ | 6,695 | $ | 6,083 | $ | 5,931 | |||||||

| Pre-tax operating income | 782 | 636 | 613 | |||||||||||

| Cash Flow from operations, pre-tax | 1,551 | 869 | 990 | |||||||||||

| Total assets | 16,653 | 15,271 | 13,810 | |||||||||||

| GAAP combined ratio | 92.1 | % | 94.7 | % | 95.5 | % | ||||||||

Commercial Markets | Revenues | $ | 4,771 | $ | 4,437 | $ | 4,408 | |||||||

| Pre-tax operating income | 301 | 191 | 308 | |||||||||||

| Cash Flow from operations, pre-tax | 1,127 | 790 | 960 | |||||||||||

| Total assets | 23,646 | 22,354 | 21,428 | |||||||||||

| GAAP combined ratio | 105.4 | % | 108.7 | % | 105.3 | % | ||||||||

Agency Markets | Revenues | $ | 6,246 | $ | 5,830 | $ | 5,185 | |||||||

| Pre-tax operating income | 632 | 564 | 417 | |||||||||||

| Cash Flow from operations, pre-tax | 1,591 | 1,445 | 1,189 | |||||||||||

| Total assets | 15,893 | 14,471 | 13,281 | |||||||||||

| GAAP combined ratio | 97.8 | % | 98.3 | % | 100.6 | % | ||||||||

International | Revenues | $ | 4,900 | $ | 3,908 | $ | 3,620 | |||||||

| Pre-tax operating income | 467 | (244 | ) | 273 | ||||||||||

| Cash Flow from operations, pre-tax | 848 | 967 | 768 | |||||||||||

| Total assets | 17,687 | 14,515 | 12,680 | |||||||||||

| GAAP combined ratio | 97.2 | % | 117.0 | % | 97.9 | % | ||||||||

Other | Revenues | $ | 908 | $ | 903 | $ | 497 | |||||||

| Pre-tax operating income | (542 | ) | (748 | ) | (845 | ) | ||||||||

| Cash Flow from operations | (1,222 | ) | (607 | ) | (670 | ) | ||||||||

Pre-tax operating income is defined as net income in accordance with Generally Accepted Accounting Principles (GAAP) excluding net realized gains (losses), results from private equity investments, federal and foreign income taxes, extraordinary items, discontinued operations and cumulative effect of changes in accounting principles. Investment income is allocated to the major businesses on a total return basis and differs from the methodology utilized in the Company’s recent debt offering memorandum and its financial reporting on the Company’s website. Pre-tax operating income is the basis used by management for measuring operating performance internally. However, analysis of the Company’s results should be used only in conjunction with data presented in accordance with GAAP.

Other includes discontinued operations (including asbestos and environmental), interest expense, internal reinsurance programs, net investment income after allocations to business units, certain expenses not allocated to the business units, net realized gains and losses from domestic operations and other revenues from corporate subsidiaries.

Personal Markets reported above includes Individual Life, which differs from the financial reporting on the Company’s website where Individual Life is included in Corporate and Other. Each business unit is reported in accordance with GAAP.

Contents | Policyholder Message 3 | Company Overview 7 | Strategic Business Units 11 | Worldwide Office and Company Locations 26 | Financial Statements 27

If you were to ask Liberty Mutual employee Adriana Prado (on cover) or the other three individuals featured in this report about their actions, they’d say “we were just doing our jobs.” To their delighted customers, however, they far exceeded expectations. That’s what high-quality service is all about – honoring a promise of service even when the solution isn’t easy.

Thousands of Liberty Mutual employees put this belief into action every day – going that extra mile to make sure that we meet our policyholders’ needs. Why? Because it’s our responsibility, and it’s the right thing to do.

1

2

LIBERTY MUTUAL GROUP | POLICYHOLDER MESSAGE

What a difference a year–and the weather–makes. One year ago, I wrote you about the negative effect of a devastating Atlantic and Gulf Coast hurricane season. In 2006, except for a few smaller, but locally costly, hailstorm events, we had a mild year as far as natural catastrophes went. The result: Liberty Mutual Group and its industry peers reported record profits.

Ironically, the lack of storms in 2006 may have a more significant, long-term impact on the industry than a hurricane-heavy year – more on that later.

Looking at the numbers, 2006 was a very, very successful year for Liberty Mutual Group. While we felt some competitive pressure on prices, we grew all lines of business, experiencing 11 percent growth in total revenue, a growth rate well ahead of the industry. While growing substantially, we produced net income of $1.6 billion, a number that exceeds last year’s total by 58 percent, and the company’s previous record by 31 percent. Contributing significantly to these results, as it has for several years now, was our investment activity, as our private equity and energy investments continued to produce exceptional results.

While pleased with our earnings, our primary emphasis continued to be the quality of our balance sheet, which is rock solid. Nothing is more important to our policyholders, and the longer-term health of the company, than the confidence that our reserves are sufficient to satisfy all legitimate claims.

While our aggregate numbers were over-and-above expectations, perhaps more revealing are the numbers for our Strategic Business Units: Personal Markets, Agency Markets, Commercial Markets and Liberty International.

In Personal Markets, which sells direct under the Liberty Mutual brand, we were a major beneficiary of the lack of significant storm events, and reported very satisfactory earnings. We expanded our affinity marketing programs and continued to be the leader in this good source of high-quality business. Voluntary policies inforce grew by 2.5 and 3.5 percent in auto and homeowners, respectively.

3

LIBERTY MUTUAL GROUP | POLICYHOLDER MESSAGE

Looking longer term, we began to surgically reduce our exposure in areas of more extreme weather risk. We refrained, however, from widespread cancellations, staying consistent with our philosophy of carefully managing risk, and providing affordable insurance to our policyholders while maintaining our profit levels.

In Agency Markets, our organization of regional and national property and casualty insurers that distribute their products and services through brokers and agents, each of the franchises had a successful year. Our more than 6,600 independent agency partners continue to demonstrate an ability to meet customer needs, particularly those of small to mid-size businesses.

In 2005, lacking a heavy concentration of property business in hurricane-prone areas, Agency Markets was for the most part sheltered from major weather events. That was not the case in 2006, as the hailstorms and similar events in the Midwest affected our Agency Markets’ policyholders. Still, Agency Markets had an exceptional year overall, with revenue growth of 7 percent and a 12 percent increase in pre-tax operating income.

In Commercial Markets, each operating unit had an excellent year. Liberty Mutual Property benefited from the combination of solid underwriting, strong pricing and lack of significant storm events. Business Market, which sells to the middle market, added significantly to its direct sales force and showed great growth and retention. Despite some downward pressure on prices, we are extremely pleased with business quality, as exceptional coverage and service continue to sell well in the market. The National Market, focused on large companies with more than $2.5 million in annual cost of risk, now has 20 Fortune 100 accounts. Overall, Commercial Markets grew revenue and pre-tax operating income by 8 and 58 percent, respectively.

Liberty International’s country-by-country operations continued to expand. We received a general insurance license in Vietnam, and established a branch of our Spanish company in Poland. We expect to begin issuing our first policies by mid-year 2007. We also entered Turkey with the acquisition of Seker Sigorta A.S. Overall, our existing country operations in Europe, South America and Southeast Asia continued to thrive with overall growth and pre-tax operating income of 15 percent and $239 million, respectively.

4

Liberty International’s global specialty lines insurance and reinsurance business, Liberty International Underwriters (LIU), produced growth and pre-tax operating income of 42 percent and $228 million, respectively. In London, we are significantly reducing our writings of U.S. property catastrophe insurance, as the pricing for the risk is not adequate, even with a significant increase over the prior year. Elsewhere, we opportunistically grew LIU, which opened new offices in Houston, Los Angeles, Puerto Rico, Dubai and Hong Kong, and now operates 31 offices worldwide.

Earlier I said the long-term impact of a “no-hurricane” year may prove more detrimental to the industry than a year with multiple hurricanes. The challenge involves regulatory politics. While rate increases in Florida, for example, have been substantial, they are still inadequate for the risk. However, because of the lack of storms, the political process only looked at the industry’s 2006 profit, not the huge cumulative losses for prior years. The upshot has been the legislature putting the risk on the taxpayer, a vast increase in scope for the state-run Citizens Property Insurance Corp., and a mandated rate rollback. All in all, not a recipe for long-term stability and availability of insurance. In Connecticut, legislation that would bar insurers from requiring that policyholders institute certain risk reduction measures, such as the installation of hurricane shutters, is under consideration.

We will continue to grapple with these and other legislative and regulatory matters, as we see somewhat a reemergence of legislative behaviors that led to a crisis in insurance availability and cost in the 1980s. This trend obviously bears some watching.

On the competitive front, the market has been surprisingly benign. Downward pressure on prices clearly exists, although we anticipated more pressure than has actually emerged. This downward pressure will increase as the industry has plenty of capital and many of our competitors missed their growth targets in 2006, and we will monitor our pricing and underwriting standards carefully. For our policyholders in aggregate, we must not let marginal risks negatively impact the company’s overall financial position. That said, we are very optimistic that we can grow our book of business in 2007 while maintaining an acceptable level of quality.

A very public change in 2006 was the introduction of our new advertising campaign. Its “responsibility” theme, drawn from interviews with Liberty Mutual employees at all levels of the organization, has struck a chord with our customers, our employees and the broader community. We are very pleased with the response to this theme, which captures our feeling about our business and the people with whom we deal every day.

As part of the responsibility positioning, we established, in conjunction with the College Football Hall of Fame, the Liberty Mutual Coach of the Year Award. This award recognizes, not just a coach’s professional competence and achievement on the field, but also a coach’s commitment to the well-being and development of athletes, high ethical standards, and civic and charitable stewardship. I want to congratulate Coach Greg Schiano of Rutgers University, the first recipient of this annual honor.

5

LIBERTY MUTUAL GROUP | POLICYHOLDER MESSAGE

I would also like to highlight the 2006 Liberty Mutual National Firemark Award recipients. In October, Oscar-winning actress Marcia Gay Harden, who experienced a personal fire-related tragedy, presented the awards to firefighters Bonnie Lopez of Acton, Mass., and Omar Shareef and Albert Jason Boyd of Baltimore, Md.

This year also marked the launch of the Liberty Mutual Chairman’s Community Service Award, which recognizes the great work of so many Liberty employees with not-for-profit agencies around the country. While I was aware that many of our employees are involved in community activities, I was astounded, while reviewing the nominations, at how much, and how deeply, our employees commit themselves to improving the communities in which they live and work.

In closing, it is with some sadness that I say goodbye to Liberty Mutual board member Glenn Strehle, Treasurer Emeritus of the Massachusetts Institute of Technology, after 28 years of service. Glenn has been a great advisor and, as chair of the Audit Committee, has helped us immeasurably as we voluntarily (not being a public company) adopted an internal control attestation process consistent with public companies’ Sarbanes-Oxley attestations. We are a better company for Glenn’s service. We wish Glenn and his wife Kathie well, and we thank him again for all he has done for Liberty.

I also thank our board of directors for their continued guidance, our various distribution partners—affinity, independent agents, brokers—for their support, and our 39,000 employees worldwide for their expertise and dedication to our policyholders and our company.

Most importantly, I thank our policyholders and customers for their business, and for continuing to place your confidence in us.

|

| Edmund F. Kelly |

| Chairman, President and Chief Executive Officer |

6

LIBERTY MUTUAL GROUP | COMPANY OVERVIEW

Liberty Mutual Group is a diversified global insurer whose largest line of business is private passenger auto, based on 2006 net written premium.

On December 31, 2006, Liberty Mutual Group had $85.5 billion in consolidated assets. Liberty Mutual is the 8th-largest personal lines writer and 4th-largest commercial lines writer in the U.S. based on 2006 direct written premium.

| REVENUE GROWTH | PRE-TAX INCOME GROWTH | |

| IN BILLIONS | IN MILLIONS | |

|  | |

7

LIBERTY MUTUAL GROUP | COMPANY OVERVIEW

Headquartered in Boston, Mass., Liberty Mutual Group employs more than 39,000 people in nearly 900 offices in 24 countries throughout the world.

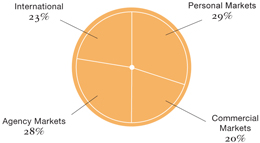

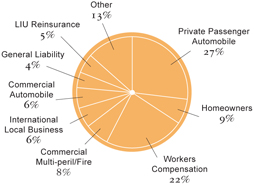

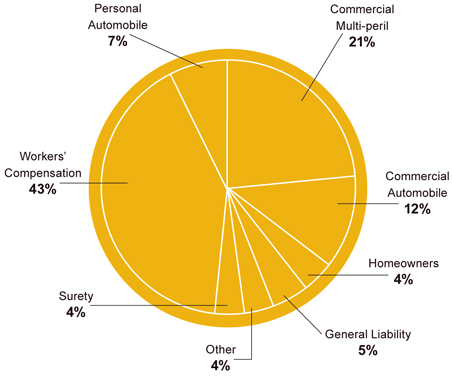

Liberty Mutual Group has four strategic business units – Personal Markets, Commercial Markets, Agency Markets and Liberty International – with no single unit contributing more than 30 percent of net written premium. The company offers a wide range of insurance products and services, including private passenger automobile, homeowners, workers compensation, commercial multiple peril/fire, commercial automobile, general liability, assumed reinsurance, global specialty products, group disability and surety.

Liberty Mutual Group’s revenue for 2006 was $23.5 billion, an increase of $2.4 billion from 2005. Net investment income increased by $234 million to $2.3 billion, and cash flow from operations was $3.9 billion. Pre-tax operating income for 2006 was $1.6 billion, an increase of $1.2 billion from 2005. The Group’s GAAP property and casualty combined ratio decreased to 99.3 percent in 2006 from 105.7 percent in 2005, and policyholders’ equity increased by over $2.0 billion to $10.9 billion.

| David H. LongPresident, | J. Paul Condrin IIIPresident, | |

| Commercial Markets | Personal Markets | |

|  | |

8

| STRATEGIC BUSINESS UNITS | SIGNIFICANT LINES OF BUSINESS | |

| $20.6 B NET WRITTEN PREMIUM | $20.6 B NET WRITTEN PREMIUM | |

|  | |

| DIVERSIFICATION BY DISTRIBUTION CHANNEL | MIX OF BUSINESS | |

|  | |

| Gary R. GreggPresident, | Thomas C. RameyPresident, | A. Alexander FontanesExecutive | ||

| Agency Markets | Liberty International | Vice President & Chief Investment Officer | ||

|  |  | ||

9

10

PERSONAL MARKETS | SALT LAKE CITY, UTAH

Beyond the Call

The storm seemed to take aim that morning at Erna Huck’s home at the base of the Wasatch Range, overlooking Salt Lake City. One moment the sun was shining; the next, pitch darkness. Within 15 minutes, the mini-storm’s winds destroyed her deck, downed trees and ripped out electrical service.

The damage was bad enough but, coming just days before Erna’s long-planned 95th birthday celebration, with 100 friends and family arriving from around the world, it was a personal catastrophe. Or so she thought.

In tears, the normally plucky woman – she stopped skiing at age 94 – called her son Rainer, also a Liberty Mutual policyholder, who lived nearby. “Call the insurance company and see if they can help,” she pleaded.

“I called Liberty Mutual, but I didn’t expect much to happen. Perhaps a check to cover damage expenses, but that’s about all,” said Rainer, who had rushed over to console his mother. “She had planned this party down to the smallest detail and cleaned the house top to bottom. She was even picking up individual leaves from the lawn!”

Rainer quickly found himself speaking with Andy Low, a Liberty Mutual claims adjuster. “I explained the situation to Andy and, amazingly, he had a crew of seven working that afternoon,” he said. “They removed all the crushed materials, cut the fallen trees to pieces and worked until 11 p.m. installing new electrical service. All this was clearly beyond the call of duty.”

But not to Andy. “I didn’t do anything out of the ordinary with this claim,” he said. “The timing of the storm was unfortunate, and I just lined up someone who could accelerate the repairs. Nothing I wouldn’t do for any insured. We simply provided the service she paid for, and deserved, and it was nice to know her birthday party proceeded as planned.”

11

12

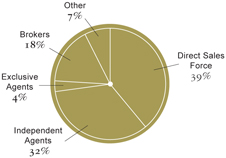

PERSONAL MARKETS | AT A GLANCE

PRODUCT MIX (% 2006 NET WRITTEN PREMIUM) |  |

Liberty Mutual’s Personal Markets provides full lines of coverage for private passenger automobile, homeowners, valuable possessions, identity theft and personal liability through its own sales force in more than 350 offices throughout the U.S., two direct response centers, appointed Prudential agents and the internet. It also offers a wide range of traditional and variable life insurance and annuity products. Personal Markets’ largest source of new business is its more than 9,800 sponsored affinity group relationships, including employers, credit unions, and professional and alumni associations. Liberty Mutual’s affinity program is the industry’s most-sponsored voluntary auto and home insurance benefit.

Financial Results

| 2006 | 2005 | 2004 | ||||||||||

Revenues | $ | 6.7 billion | $ | 6.1 billion | $ | 5.9 billion | ||||||

Pre-tax operating income | $ | 782 million | $ | 636 million | $ | 613 million | ||||||

Cash flow from operations | $ | 1.6 billion | $ | 869 million | $ | 990 million | ||||||

GAAP combined ratio | 92.1 | % | 94.7 | % | 95.5 | % | ||||||

Policies in force | 4,812,921 | 4,670,548 | 4,563,142 | |||||||||

Distribution Channels

| • | Direct Sales Force |

| • | Direct Response Centers |

| • | Internet |

| • | Prudential Agents |

By The Numbers

| • | 4.4 million auto and home policies |

| • | 11,200 employees |

| • | 9,800 affinity relationships |

| • | 1,600 field sales representatives |

| • | 370 telesales counselors |

| • | 1,260 Prudential insurance agents |

13

COMMERCIAL MARKETS | GLENDALE, CALIFORNIA

What Matters Most

Kaleen Osendorf, a Liberty Mutual account service representative in Glendale, Calif., wasn’t out to save the environment. But in her own small way, that’s what she did.

Her story begins in Fall 2006 when San Bernardino County asked one of Kaleen’s customers, Anaheim-based West Coast Arborists (WCA), to clear bark beetle-infested trees in the county forest. The 34-year-old business provides various forestry services, such as tree pruning, removal and planting.

Over the past three years, drought and bark beetles had destroyed hundreds of thousands of trees, primarily on government-owned land, to such a degree that then-Governor Gray Davis proclaimed a State of Emergency in three counties. To help contain future fires, San Bernardino County asked WCA to create a firebreak to spare the healthy trees.

For WCA to proceed with the work, the County required proof of insurance, including an endorsement document called a “Loggers Broad Form.” “This was not a commonly used form, at least in California, and nobody knew what it included,” Kaleen said. To track it down, she contacted her local and national counterparts in underwriting, county and state forestry departments, and the International Risk Management Institute, but to no avail. “Nobody had heard of it,” she said.

But that didn’t stop her. After more than 50 phone calls and 90-plus emails, Kaleen gathered enough information for underwriting to draft an acceptable endorsement that incorporated elements from forms used in other states. And she did this while handling her regular $20 million customer service workload, whether it be renewing business, rolling out a new system or sitting in on claims meetings.

Meanwhile, the customer, WCA, which began work in December, had little knowledge of the lengths Kaleen went to in order to provide the required document. “That’s fine with me,” she said. “What matters most is they were able to begin work.”

14

15

16

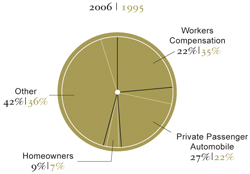

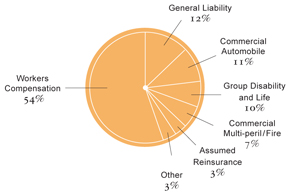

COMMERCIAL MARKETS | AT A GLANCE

PRODUCT MIX (% 2006 NET WRITTEN PREMIUM) |  |

Liberty Mutual’s Commercial Markets provides risk and disability management and risk transfer products and services to buyers and buyers’ representatives through five business units:

| • | National Market, which serves the complex needs of large companies; |

| • | Business Market, which serves mid-sized businesses that prefer a direct relationship; |

| • | Liberty Mutual Property, which provides property insurance programs, loss control and claims services for both large and mid-sized companies; |

| • | Group Market, which provides short- and long-term disability products, integrated disability management, group life insurance, AD&D and FMLA administration for large and mid-sized businesses; and, |

| • | Liberty Mutual Reinsurance, which provides property and casualty reinsurance to insurance carriers worldwide. |

Financial Results

| 2006 | 2005 | 2004 | ||||||||||

Revenues | $ | 4.8 billion | $ | 4.4 billion | $ | 4.4 billion | ||||||

Pre-tax operating income | $ | 301 million | $ | 191 million | $ | 308 million | ||||||

Cash flow from operations | $ | 1.1 billion | $ | 0.8 billion | $ | 1.0 billion | ||||||

GAAP combined ratio | 105.4 | % | 108.7 | % | 105.3 | % | ||||||

Distribution Channels

| • | Direct Sales Force |

| • | National and Regional Brokers |

| • | Benefit and Risk Management Consulting Firms |

By The Numbers

| • | 8,960 employees |

| • | 540 account executives |

| • | 546,000 claims call center calls |

| • | 1,780 national customers |

| • | 8,100 middle-market customers |

| • | 370 loss prevention consultants |

| • | $1.2 billion in medical bill review savings |

17

AGENCY MARKETS | COLDWATER, OHIO

No Brainer

It was an exciting time for the Coldwater, Ohio, village school system. A long-awaited, $35 million renovation and expansion of the rural town’s K-12 public school, serving 1,500 students from a 40-square-mile area, was soon to begin.

But Sherry Shaffer, the school’s Treasurer and Chief Financial Officer (pictured on opposite page with Carolee Roberts, a senior loss prevention consultant with Indiana Insurance, a Liberty Mutual Agency Markets company), had a nagging concern. How do you hold classes safely during the school’s anticipated, three-year construction period? “We couldn’t just stop teaching,” she said, “but we had to make sure we drew on all of our resources so that staff and students were safe.”

For help, Sherry turned to the school’s insurance agency, Phelan Insurance of nearby Versailles, Ohio, one of the independent insurance agencies that distributes Indiana Insurance products and services. They put Sherry in touch with Carolee for expert construction loss prevention advice. “Construction safety can be both exciting and challenging,” Carolee said. “Whenever you deal with human behavior, especially a seven- or eight-year-old’s behavior, you have to be ready for anything.”

During the next two years of construction, Carolee visited the school regularly, meeting with Sherry, the architect, and the contractor. Nothing escaped her notice, from the need to install exterior barricading and fencing to the proper placement of gas shut-off switches in the science labs. She even helped one of the school’s maintenance professionals earn Playground Safety Inspector certification. “She didn’t just do the inspections,” Shaffer said. “She took it as a personal mission to ensure that no one would get hurt during construction.”

Coldwater completed its school renovation in the fall of 2006, with no severe, or even reportable, injuries. Today, Carolee, at Sherry Shaffer’s request, continues her regular visits, making sure the school follows her recommendations, and even testing the school’s preparedness for an incidence of school violence.

When it came time to put the school’s insurance coverage out for bid, as required by the Board of Education, the final decision was a “no brainer.” “Carolee made that decision easy,” Sherry said.

18

19

20

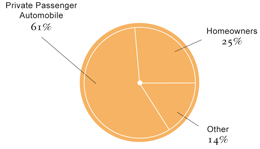

AGENCY MARKETS | AT A GLANCE

PRODUCT MIX (% 2006 NET WRITTEN PREMIUM) |  |

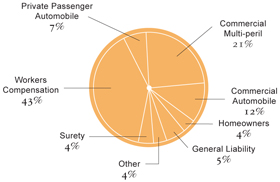

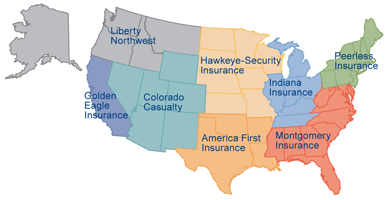

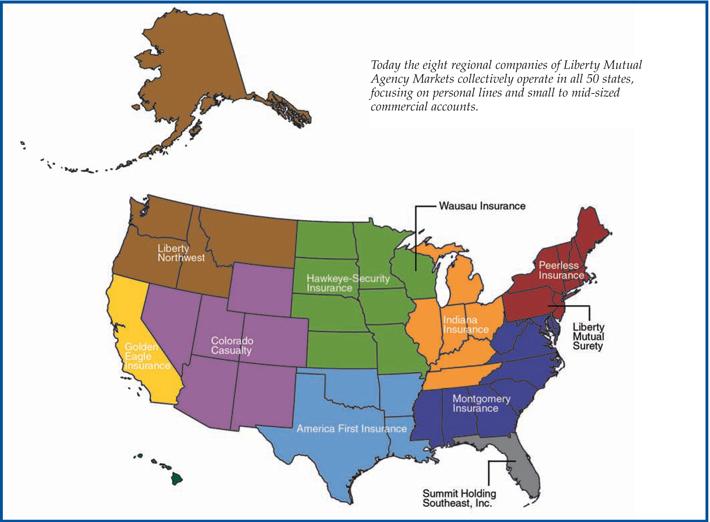

Liberty Mutual Agency Markets consists of property and casualty, and specialty insurance carriers that distribute their products and services through agents and brokers.

Core Property and Casualty Products

Core property and casualty products, including a comprehensive set of personal and commercial coverages, are available in most states from the following companies:

| • | America First Insurance (Gulf Region) |

| • | Colorado Casualty (Mountain Region) |

| • | Golden Eagle Insurance (Pacific Region) |

| • | Hawkeye-Security Insurance (North Central Region) |

| • | Indiana Insurance (Midwest Region) |

| • | Liberty Northwest (Pacific Northwest Region) |

| • | Montgomery Insurance (Southeast Region) |

| • | Peerless Insurance (Northeast Region) |

| • | Wausau Insurance Companies (National) |

Agency Markets also includes Summit Holding Southeast, Inc., a specialty insurer offering workers compensation products and services in Florida and nine Southeast states, and Liberty Mutual Surety, offering contract surety bonds for construction firms, manufacturers and suppliers, and commercial surety bonds for corporations and individuals.

Financial Results

| 2006 | 2005 | 2004 | ||||||||||

Revenues | $ | 6.2 billion | $ | 5.8 billion | $ | 5.2 billion | ||||||

Pre-tax operating income | $ | 632 million | $ | 564 million | $ | 417 million | ||||||

Cash flow from operations | $ | 1.6 billion | $ | 1.4 billion | $ | 1.2 billion | ||||||

GAAP combined ratio | 97.8 | % | 98.3 | % | 100.6 | % | ||||||

By The Numbers

| • | More than 6,900 employees |

| • | More than 6,600 appointed independent agents and brokers |

| • | 822,600 personal lines and 474,500 commercial lines Regional Company policies in force, with average premium of $900 and $5,900, respectively |

| • | 24,500 Summit policies in force with average premium of $34,300 |

| • | 11,800 Wausau Insurance accounts in force, averaging $156,000 in account size |

21

22

LIBERTY INTERNATIONAL | UBERLANDIA, BRAZIL

Being Human

It was a vacation turned nightmare. That’s how Liberty Seguros (Brazil) policyholder Joao Klinger Ribeiro describes what happened on March 1, 2006, as he and two family members were driving about 550 miles from home in the Bahia region of Brazil.

“One moment I’m changing the CD, the next we’re off the road and bouncing down a steep hillside,” he said. When the car hit a pole and finally came to rest, he knew he and his sister, judging from her screams, were badly injured. “Passersby could do little more than cool us off with towels. They knew they shouldn’t move us.”

With no cellphone service in rural northeast Brazil, someone flagged down a passing army truck, which radioed for an ambulance. Surgeons at a nearby hospital operated on his lower back, and placed him in a cast that jutted his legs away in a V shape. Eight days after the accident, the doctor wanted to release him.

But there was a problem: transport out of rural, uneven terrain with a broken back would not be easy. “Mr. Ribeiro called his auto insurance agent at Romap Seguros, which sells Liberty Seguros policies, in his hometown of Uberlandia, and the agent soon called me for help,” said Adriana Corsari Prado in Sao Paulo, who manages external service providers for Liberty Seguros.

Compounding the problem, according to Adriana, was that Mr. Ribeiro’s policy entitled him to an economy class plane ticket home but, because of his cast, a commercial jet’s seating couldn’t accommodate him. An ambulance was also out of the question as the bumpy, 500-mile ride home could cause more serious harm, even paralysis.

“I knew we had to get him home, and after analyzing all potential risk to our company and the policyholder, I researched other transport options, including private jets,” Adriana said. Finally, working with Mondial Assistance, she negotiated the release of an ambulance plane to transport Mr. Ribeiro and his sister, who had suffered two broken vertebrae, home to Uberlandia.

After four months in a cast and two months of physical therapy, a grateful Mr. Ribeiro (pictured outside his home on the opposite page) is fully recovered. Writing to Liberty Seguros, he said: “In one of the most difficult moments of my life, you were there. Please, go on with this beautiful professionalism but, above all, go on being human.”

23

24

LIBERTY INTERNATIONAL | AT A GLANCE

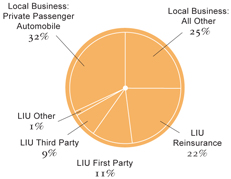

PRODUCT MIX (% 2006 NET WRITTEN PREMIUM) |  |

Liberty International provides personal and small commercial lines insurance through operations in 14 countries. Additionally, Liberty International Underwriters, a global specialty commercial lines insurance and reinsurance business, provides casualty, specialty casualty, marine, energy, engineering and aviation insurance products through 31 offices in Asia, Australia, Europe, the Middle East and North America. Liberty Syndicate 4472 at Lloyd���s of London writes on a worldwide basis.

Financial Results

| 2006 | 2005 | 2004 | ||||||||||

Revenues | $ | 4.9 billion | $ | 3.9 billion | $ | 3.6 billion | ||||||

Pre-tax operating income | $ | 467 million | $ | (244) million | $ | 273 million | ||||||

Cash flow from operations | $ | 848 million | $ | 967 million | $ | 768 million | ||||||

GAAP combined ratio | 97.2 | % | 117.0 | % | 97.9 | % | ||||||

By The Numbers

| • | 2nd largest U.S.-based international property and casualty insurance company |

| • | 7,300 employees worldwide |

| • | offices in 24 countries |

| • | number one ranking in Colombia and Venezuela |

| • | a top ten property and casualty company in Argentina, Chile, Portugal, Spain, Singapore and Thailand |

| • | net written premium grew 24 percent in 2006 with sustained compound annual growth rate of 18 percent since 1998 |

Country Operations(57 percent of International Net Written Premium)

Asia

Liberty Mutual Insurance Company (China), Liberty International Insurance Ltd. (Hong Kong), Liberty Insurance Pte. Ltd. (Singapore), LMG Insurance (Thailand), Liberty Insurance Ltd. (Vietnam)

Europe

Liberty Direct (Poland), Liberty Seguros (Portugal), Liberty Seguros and Genesis (Spain), Seker Sigorta A.S. (Turkey)

Latin America

Liberty ART S.A. (Argentina), Liberty Seguros Argentina S.A., Liberty Paulista Seguros (Brazil), Liberty Seguros (Chile), Liberty Seguros (Colombia), Seguros Caracas de Liberty Mutual C.A. (Venezuela)

Liberty International Underwriters

(LIU) (43 percent of International Net Written Premium)

Liberty Syndicate Management (Lloyd’s), Liberty Mutual Insurance Europe, LIU Australia, LIU Canada, LIU Dubai, LIU Hong Kong, LIU Singapore, LIU U.S.

25

LIBERTY MUTUAL GROUP | WORLDWIDE PRESENCE

26

LIBERTY MUTUAL HOLDING COMPANY INC.

Financial Statements

Consolidated Statements of Income 28 | Consolidated Balance Sheets 29 | Consolidated Statements of Cash Flows 30 | Consolidated Statements of Changes in Policyholders’ Equity 31 | Notes to Consolidated Financial Statements 32 | Report of Independent Auditors 54 | Report of Management 55 | Independent Auditors’ Opinion on Management’s Assessment 56 | Board of Directors 57 | Officers 57 | Operating Management 58 | Advisory Boards 60 | Annual Meeting Inside Back Cover

27

LIBERTY MUTUAL HOLDING COMPANY INC.

Consolidated Statements of Income

[DOLLARS IN MILLIONS]

Years Ended December 31, | 2006 | 2005 | 2004 | ||||||||

Revenues | |||||||||||

Premiums earned | $ | 19,867 | $ | 17,631 | $ | 16,563 | |||||

Net investment income | 2,548 | 2,247 | 2,102 | ||||||||

Net realized investment gains | 343 | 523 | 312 | ||||||||

Fee and other revenues | 762 | 760 | 664 | ||||||||

Total revenues | 23,520 | 21,161 | 19,641 | ||||||||

Claims, Benefits and Expenses | |||||||||||

Benefits, claims and claim adjustment expenses | 14,609 | 14,272 | 13,084 | ||||||||

Insurance operating costs and expenses | 3,425 | 2,912 | 2,666 | ||||||||

Amortization of deferred policy acquisition costs | 2,827 | 2,480 | 2,349 | ||||||||

Other expenses | 401 | 367 | 323 | ||||||||

Total claims, benefits and expenses | 21,262 | 20,031 | 18,422 | ||||||||

Income from continuing operations before income tax expense | 2,258 | 1,130 | 1,219 | ||||||||

Federal and foreign income tax expense | 632 | 91 | — | ||||||||

Income from continuing operations before extraordinary loss and discontinued operations | 1,626 | 1,039 | 1,219 | ||||||||

Extraordinary loss, net of tax | — | — | (3 | ) | |||||||

Discontinued operations, net of tax | — | (12 | ) | 29 | |||||||

Net income | $ | 1,626 | $ | 1,027 | $ | 1,245 | |||||

See accompanying notes to the audited consolidated financial statements.

28

LIBERTY MUTUAL HOLDING COMPANY INC.

Consolidated Balance Sheets

[DOLLARS IN MILLIONS]

December 31, | 2006 | 2005 | ||||

Assets: | ||||||

Investments: | ||||||

Fixed maturities, available for sale, at fair value (amortized cost of $40,981 and $36,962) | $ | 41,102 | $ | 37,391 | ||

Equity securities, available for sale, at fair value (cost of $1,664 and $1,077) | 2,619 | 1,812 | ||||

Trading securities, at fair value (cost of $14 and $13) | 22 | 20 | ||||

Other investments | 1,646 | 1,220 | ||||

Short-term investments | 1,550 | 1,430 | ||||

Mortgage loans | 322 | — | ||||

Total investments | 47,261 | 41,873 | ||||

Cash and cash equivalents | 3,512 | 3,155 | ||||

Premium and other receivables (net of allowance of $ 101 and $131) | 6,075 | 5,976 | ||||

Reinsurance recoverables (net of allowance of $315 and $324) | 15,564 | 16,302 | ||||

Deferred income taxes (net of valuation allowance of $101 and $99) | 1,490 | 1,627 | ||||

Deferred policy acquisition costs | 1,662 | 1,476 | ||||

Goodwill and intangible assets | 907 | 810 | ||||

Prepaid reinsurance premiums | 1,230 | 1,224 | ||||

Property, plant and equipment, net | 1,660 | 1,109 | ||||

Other assets | 3,088 | 2,702 | ||||

Separate account assets | 3,049 | 2,570 | ||||

Total assets | $ | 85,498 | $ | 78,824 | ||

Liabilities: | ||||||

Unpaid claims and claim adjustment expenses and future policy benefits: | ||||||

Property and casualty | $ | 38,606 | $ | 38,067 | ||

Life | 5,591 | 4,751 | ||||

Other policyholder funds and benefits payable | 2,658 | 2,491 | ||||

Unearned premiums | 9,343 | 8,454 | ||||

Funds held under reinsurance treaties | 1,823 | 1,826 | ||||

Short-term debt | 171 | 145 | ||||

Long-term debt | 3,175 | 2,555 | ||||

Other liabilities | 10,187 | 9,107 | ||||

Separate account liabilities | 3,049 | 2,570 | ||||

Total liabilities | 74,603 | 69,966 | ||||

Policyholders’ equity: | ||||||

Unassigned equity | 10,092 | 8,466 | ||||

Accumulated other comprehensive income | 803 | 392 | ||||

Total policyholders’ equity | 10,895 | 8,858 | ||||

Total liabilities and policyholders’ equity | $ | 85,498 | $ | 78,824 | ||

See accompanying notes to the audited consolidated financial statements.

29

LIBERTY MUTUAL HOLDING COMPANY INC.

Consolidated Statements of Cash Flows

[DOLLARS IN MILLIONS]

Years Ended December 31, | 2006 | 2005 | 2004 | |||||||||

Cash flows from operating activities: | ||||||||||||

Net income from continuing operations | $ | 1,626 | $ | 1,039 | $ | 1,219 | ||||||

Adjustments to reconcile net income to net cash provided by operating activities: | ||||||||||||

Depreciation and amortization | 238 | 217 | 191 | |||||||||

Realized investment gains | (343 | ) | (523 | ) | (312 | ) | ||||||

Undistributed private equity investment gains | (275 | ) | (208 | ) | (141 | ) | ||||||

Premium, other receivables, and reinsurance recoverables | 669 | (2,545 | ) | (2,586 | ) | |||||||

Deferred policy acquisition costs and distribution costs | (154 | ) | (144 | ) | (232 | ) | ||||||

Liabilities for insurance reserves | 1,865 | 5,153 | 5,187 | |||||||||

Taxes payable, net of deferred | 169 | (195 | ) | (233 | ) | |||||||

Other, net | 100 | 912 | 114 | |||||||||

Total adjustments | 2,269 | 2,667 | 1,988 | |||||||||

Net cash provided by operating activities | 3,895 | 3,706 | 3,207 | |||||||||

Cash flows from investing activities: | ||||||||||||

Purchases of investments | (20,952 | ) | (20,273 | ) | (21,467 | ) | ||||||

Sales and maturities of investments | 16,508 | 16,955 | 18,858 | |||||||||

Property and equipment purchased, net | (762 | ) | (306 | ) | (208 | ) | ||||||

Payment for purchase of companies, net of cash acquired | (48 | ) | (13 | ) | — | |||||||

Other investing activities | 317 | (143 | ) | (253 | ) | |||||||

Net cash from acquisitions and dispositions | — | (15 | ) | (79 | ) | |||||||

Net cash used in investing activities | (4,937 | ) | (3,795 | ) | (3,149 | ) | ||||||

Cash flows from financing activities: | ||||||||||||

Net activity in policyholder accounts | 69 | 20 | 109 | |||||||||

Debt financing, net | 646 | 373 | 534 | |||||||||

Net securities lending activity and other financing activities | 684 | 297 | (146 | ) | ||||||||

Net cash provided by financing activities | 1,399 | 690 | 497 | |||||||||

Net cash (used in) provided by discontinued operations, principally operating activities | — | (36 | ) | 36 | ||||||||

Net increase in cash and cash equivalents | 357 | 565 | 591 | |||||||||

Cash and cash equivalents, beginning of year | 3,155 | 2,590 | 1,999 | |||||||||

Cash and cash equivalents, end of year | $ | 3,512 | $ | 3,155 | $ | 2,590 | ||||||

Supplemental disclosure of cash flow information: | ||||||||||||

Income taxes paid | $ | 496 | $ | 264 | $ | 185 | ||||||

See accompanying notes to the audited consolidated financial statements.

30

LIBERTY MUTUAL HOLDING COMPANY INC.

Consolidated Statements of Changes in Policyholders’ Equity

[DOLLARS IN MILLIONS]

| Unassigned Equity | Accumulated Other Comprehensive Income | Policyholders’ Equity | |||||||||

Balance, January 1, 2004 | $ | 6,194 | $ | 1,187 | $ | 7,381 | |||||

Comprehensive income | |||||||||||

Net income | 1,245 | — | 1,245 | ||||||||

Other comprehensive income, net of taxes: | |||||||||||

Unrealized gains on securities | — | 189 | 189 | ||||||||

Less: reclassification adjustment for gains and losses included in net income | — | (203 | ) | (203 | ) | ||||||

Minimum pension liability | — | (1 | ) | (1 | ) | ||||||

Foreign currency translation adjustments | — | 86 | 86 | ||||||||

Other comprehensive income, net of taxes | — | 71 | 71 | ||||||||

Total comprehensive income | 1,316 | ||||||||||

Balance, December 31, 2004 | $ | 7,439 | $ | 1,258 | $ | 8,697 | |||||

Comprehensive income | |||||||||||

Net income | 1,027 | — | 1,027 | ||||||||

Other comprehensive loss, net of taxes: | |||||||||||

Unrealized losses on securities | — | (171 | ) | (171 | ) | ||||||

Less: reclassification adjustment for gains and losses included in net income | — | (340 | ) | (340 | ) | ||||||

Minimum pension liability | — | (306 | ) | (306 | ) | ||||||

Foreign currency translation adjustments | — | (49 | ) | (49 | ) | ||||||

Other comprehensive loss, net of taxes | — | (866 | ) | (866 | ) | ||||||

Total comprehensive income | 161 | ||||||||||

Balance, December 31, 2005 | $ | 8,466 | $ | 392 | $ | 8,858 | |||||

Comprehensive income | |||||||||||

Net income | 1,626 | — | 1,626 | ||||||||

Other comprehensive income, net of taxes: | |||||||||||

Unrealized gains on securities | — | 211 | 211 | ||||||||

Less: reclassification adjustment for gains and losses included in net income | — | (223 | ) | (223 | ) | ||||||

Minimum pension liability | — | 312 | 312 | ||||||||

Foreign currency translation adjustments | — | 111 | 111 | ||||||||

Other comprehensive income, net of taxes | — | 411 | 411 | ||||||||

Total comprehensive income | 2,037 | ||||||||||

Balance, December 31, 2006 | $ | 10,092 | $ | 803 | $ | 10,895 | |||||

See accompanying notes to the audited consolidated financial statements.

31

LIBERTY MUTUAL HOLDING COMPANY INC.

Notes to Consolidated Financial Statements

[DOLLARS IN MILLIONS]

(1) SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

Basis of Presentation

The accompanying consolidated financial statements include the accounts of Liberty Mutual Holding Company Inc. and its subsidiaries (collectively “LMHC” or the “Company”). Certain reclassifications have been made to the 2005 and 2004 consolidated financial statements to conform with the 2006 presentation. All material intercompany transactions and balances have been eliminated.

The accompanying consolidated financial statements have been prepared in conformity with accounting principles generally accepted in the United States (“GAAP”). The preparation of financial statements in conformity with GAAP requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities and disclosure of contingent assets and liabilities at the date of the financial statements, and the reported amounts of revenues and expenses during the reporting period. The Company’s principal estimates include (1) unpaid losses and loss expense reserves, including asbestos and environmental reserves, (2) allowance for uncollectible reinsurance and policyholder receivables, (3) other than temporary impairments in the fair value of the investment portfolio, (4) deferred acquisition costs, (5) the valuation of goodwill and intangible assets, and (6) valuation allowance on deferred taxes. While management believes that the amounts included in the consolidated financial statements reflect their best estimates and assumptions, these amounts could ultimately be materially different from the amounts currently provided for in the consolidated financial statements.

Nature of Operations

The Company conducts substantially all of its business through four strategic business units: Personal Markets, Commercial Markets, Agency Markets and International.

The Company’s Personal Markets business unit writes virtually all types of property and casualty insurance covering personal risks, primarily personal automobile and homeowners.

The Commercial Markets business unit is organized into separate marketing and underwriting groups, each of which focuses on a particular customer base, product grouping, or distribution channel to provide tailored products and services that specifically address customers’ needs. The Commercial Markets business unit includes National Market, Business Market, Liberty Mutual Property and Group Market. The Commercial Markets coverages include workers compensation, commercial automobile, general liability, including product liability, multiple peril, group disability and life insurance, property, and a variety of other coverages. Commercial Markets is also a servicing carrier for workers compensation and commercial automobile involuntary market pools.

Agency Markets is composed of eight regionally-branded insurance companies that focus on the small commercial market and personal market. It also includes Wausau Insurance, which specializes in larger, commercial accounts, and the specialty operations, Liberty Mutual Surety (nationwide contract and commercial surety) and Summit Holding Southeast, Inc., (mono-line workers compensation in the Southeast, primarily Florida). Agency Markets companies distribute their products and services primarily through independent agents and brokers.

The Company’s International business unit consists of the global specialty business, known as Liberty International Underwriters (“LIU”), and local personal and commercial businesses, primarily property and casualty. LIU is composed of global specialty commercial insurance and reinsurance with operations principally based in the U.S., Canada, Australia, Singapore, Hong Kong, Dubai, London and European markets. London and European operations consist of Liberty Mutual Insurance Europe Ltd. with branches in Dublin, Paris and Cologne and Lloyd’s of London, Syndicate 4472, (formerly known as Syndicates 190 and 282) with branches in Paris and Cologne. International distributes its LIU global specialty commercial insurance and reinsurance products exclusively through brokers. LIU provides a variety of specialty products including casualty, marine, engineering, energy, directors and officers, errors and omissions, aviation, property and professional liability insurance together with multi-line insurance and reinsurance including property catastrophe reinsurance, written through Lloyd’s of London. International also operates local insurance operations consisting of local companies selling traditional property, casualty and life insurance products to individuals and businesses in nations with a large and growing middle class, primarily in South America, Asia and Southern Europe.

32

Adoption of New Accounting Standards

In January 2003, the FASB issued Interpretation No. 46,“Consolidation of Variable Interest Entities, an Interpretation of ARB No. 51” (“FIN 46”). FIN 46 requires certain variable interest entities (“VIEs”) to be consolidated by the primary beneficiary of the entity if the equity investors in the entity do not have the characteristics of a controlling financial interest or the entity does not have sufficient equity at risk for the entity to finance its activities without additional subordinated financial support from other parties. FIN 46 was revised in late 2003 (FIN 46(R)) and was effective January 1, 2004 for the Company for all new VIEs created or acquired after December 31, 2003. The provisions of FIN 46 were applied in 2005 for VIEs created or acquired by the Company prior to December 31, 2003 and they did not materially impact the Company’s financial position or results of operations.

Effective January 1, 2006, the Company adopted Financial Accounting Standards Board (FASB) Statement of Position No. FAS 115-1 and FAS 124-1,“Meaning of Other-Than-Temporary Impairments and Its Application to Certain Investments”(“FSP FAS 115-1 and FAS 124-1”),which provides guidance on determining whether investment impairment is other-than-temporary regardless of the intent to sell and when a security is impaired due to fluctuations in interest rates. The adoption of the statement did not have a material impact on the Company’s consolidated financial statements.

Effective April 1, 2006, the Company adopted Statement of Financial Accounting Standards No. 123(R),“Share-Based Payments” (“SFAS 123(R)”). The Company has elected to continue to measure its awards at their intrinsic value. Compensation cost related to these plans is determined in accordance with plan formulas and recorded ratably over the years the employee service is provided. The adoption of SFAS 123(R) did not impact the Company’s consolidated financial statements.

Future Adoption of New Accounting Standards

In September 2005, the Accounting Standards Executive Committee of the American Institute of Certified Public Accountants (“AcSEC”) issued Statement of Position No. 05-1,“Accounting by Insurance Enterprises for Deferred Acquisition Costs in Connection with Modifications or Exchanges of Insurance Contracts” (“SOP 05-1”). This SOP provides guidance on accounting by insurance enterprises for deferred acquisition costs on internal replacements of insurance and investment contracts other than those specifically described in FASB Statement No. 97,“Accounting and Reporting by Insurance Enterprises for Certain Long-Duration Contracts and for Realized Gains and Losses from the Sale of Investments” (“FAS 97”). As defined by the SOP, an internal replacement is a modification in product benefits, features, rights, or coverage that occurs by exchange of a contract for a new contract, or by amendment, endorsement, rider, or by election of a feature or coverage within an existing contract. The guidance in this SOP is effective for internal replacements occurring in fiscal years beginning after December 15, 2006, with earlier adoption encouraged. This statement is effective for the Company on January 1, 2007, and its adoption is not expected to materially impact the Company’s consolidated financial statements.

In June 2006, the FASB issued Interpretation No. 48,“Accounting for Uncertainty in Income Taxes, an Interpretation of FASB Statement No. 109” (“FIN 48”). The interpretation requires companies to recognize the tax benefits of uncertain tax positions only where the position is “more likely than not” to be sustained assuming examination by tax authorities. The amount recognized would be the amount that represents the largest amount of tax benefit that is greater than 50% likely of being ultimately realized. A liability would be recognized for any benefit claimed, or expected to be claimed, in a tax return in excess of the benefit recorded in the financial statements, along with any interest and penalty (if applicable) on the excess. FIN 48 will require a tabular reconciliation of the change in the aggregate unrecognized tax benefits claimed, or expected to be claimed, in tax returns and disclosure relating to accrued interest and penalties for unrecognized tax benefits. Discussion will also be required for those uncertain tax positions where it is reasonably possible that the estimate of the tax benefit will change significantly in the next 12 months. The Company is required to adopt FIN 48 effective January 1, 2007. Adoption of FIN 48 is not expected to have a material impact on the Company’s consolidated financial statements.

In February 2006, the FASB released Statement of Financial Accounting Standards No. 155,“Accounting for Certain Hybrid Financial Instruments - an Amendment of FASB Statements No. 133 and 140” (“SFAS 155”). SFAS 155 nullifies the guidance in the FASB’s Derivatives Implementation Group Issue D1“Application of Statement 133 to Beneficial Interests in Securitized Assets”, which had deferred the bifurcation requirements of Statement of Financial Accounting Standards No. 133, “Accounting for Derivative Instruments and Hedging Activities” (“SFAS 133”), for certain beneficial interests in securitized financial assets. SFAS 155 requires beneficial interests in securitized financial assets be analyzed to determine whether they are freestanding derivatives or hybrid instruments that contain an embedded derivative requiring bifurcation. SFAS 155 is effective for all financial instruments acquired, issued or subject to a re-measurement (new basis) event occurring after the beginning of an entity’s fiscal year that begins after September 15, 2006. The Company is required to adopt SFAS 155 effective January 1, 2007. In January 2007, the FASB issued Derivative Implementation Group Issue No. B40,“Embedded Derivatives: Application of Paragraph 13(b) to Securitized Interests in Prepayable Financial Assets” (“DIG B40”). DIG B40 provided limited exemption from bifurcation of embedded derivatives as required by paragraph 13(b) of SFAS 133. Management has concluded the exemption applies for the Company’s investment in its mortgage backed securities and as a result, SFAS 155 is not expected to have a material impact to the Company’s consolidated financial statements.

33

| Notes to Consolidated Financial Statements | LIBERTY MUTUAL HOLDING COMPANY INC. | |

[CONTINUED] |

In September 2006, the FASB issued SFAS No. 157,“Fair Value Measurements” (“SFAS 157”). This statement defines fair value, establishes a framework for measuring fair value under accounting principles generally accepted in the United States, and enhances disclosures about fair value measurements. SFAS 157 provides guidance on how to measure fair value when required under existing accounting standards. The statement establishes a fair value hierarchy that prioritizes the inputs to valuation techniques used to measure fair value into three broad levels (“Level 1, 2 and 3”). Level 1 inputs are observable inputs that reflect quoted prices for identical assets or liabilities in active markets the Company has the ability to access at the measurement date. Level 2 inputs are observable inputs, other than quoted prices included in Level 1, for the asset or liability. Level 3 inputs are unobservable inputs reflecting the reporting entity’s estimates of the assumptions that market participants would use in pricing the asset or liability (including assumptions about risk). Quantitative and qualitative disclosures will focus on the inputs used to measure fair value for both recurring and non-recurring fair value measurements and the effects of the measurements in the financial statements. The Company is required to adopt SFAS 157 effective January 1, 2008. The Company is in the process of evaluating the impact of adoption.

In September 2006, the FASB issued SFAS No. 158,“Employers’ Accounting for Defined Benefit Pension and Other Post-retirement Plans, an Amendment of FASB Statements No. 87, 88, 106 and 132(R)” (“SFAS 158”). This statement requires an entity to: (a) recognize an asset for the funded status of defined benefit plans that are over-funded and a liability for plans that are under-funded, measured as of the employer’s fiscal year end; and (b) recognize changes in the funded status of defined benefit plans, other than for the net periodic benefit cost included in net income, in accumulated other comprehensive income. For pension plans the funded status must be based on the projected benefit obligation, which includes an assumption for future salary increases. For postretirement plans the funded status is based on the accumulated postretirement benefit obligation. The Company is required to adopt SFAS 158 effective December 31, 2007. The actual impact to the Company will depend on the discount rate, other valuation assumptions, and the actual value of plan assets as of December 31, 2007. The impact is expected to be less than 5% of equity.

In February 2007, the FASB issued SFAS No. 159,“The Fair Value Option for Financial Assets and Financial Liabilities, Including an Amendment of SFAS 115” (“SFAS 159”). SFAS 159 permits all entities to choose, at specified election dates, to measure eligible items at fair value (the “fair value option”). An entity shall report unrealized gains and losses on items for which the fair value option has been elected in earnings at each subsequent reporting date eliminating complex hedge accounting provisions. The decision about whether to elect the fair value option is applied on an instrument by instrument basis and is irrevocable unless a new election date occurs and is applied only to an entire instrument. SFAS 159 also provides guidance on disclosure requirements designed to facilitate comparisons between entities that choose different measurement attributes for similar types of assets and liabilities. SFAS 159 is effective for the Company January 1, 2008. The Company is in the process of evaluating the impact of adoption.

In September 2006, the Emerging Issues Task Force (EITF) released, issue No. 06-4,“Accounting for Deferred Compensation and Postretirement Benefit Aspects of Endorsement Split-Dollar Life Insurance Arrangements” (“EITF 06-4”). This issue requires a company to recognize a liability for future life insurance benefits in accordance with SFAS 106 or Opinion 12. EITF 06-4 is effective for the Company for fiscal years beginning after December 15, 2007. The Company is in the process of evaluating the impact of adoption but it is not expected to be material.

Investments

Fixed maturity securities classified as available for sale are debt securities that have fixed or variable principal payment schedules, held for indefinite periods of time, and are used as a part of the Company’s asset/liability strategy or sold in response to risk/reward characteristics, liquidity needs or similar economic factors. These securities are carried at fair value with the corresponding unrealized investment gains or losses, net of deferred income taxes, reported in accumulated other comprehensive income.

Equity securities classified as available for sale include common equities and non-redeemable preferred stocks and are reported at quoted market values. Changes in the market values of these securities, net of deferred income taxes, are reflected as unrealized investment gains or losses in accumulated other comprehensive income.

Trading securities are securities bought principally for the purpose of sale in the near term and are reported at market value. Changes in market value are recognized in income as realized gains or losses in the current period.

Realized gains and losses on sales of investments are recognized in income using the specific identification method. Unrealized losses that are other-than-temporary are recognized as realized losses. The Company reviews fixed income and public equity securities for impairment on a quarterly basis and private equity and co-investment securities on a semi-annual basis. Securities are reviewed for both quantitative and qualitative considerations including, but not limited to, (1) the

34

extent of the decline in fair value below book value, (2) the duration of the decline, (3) significant adverse changes in the financial condition or near term prospects for the investment or issuer, (4) significant changes in the business climate or credit ratings of the issuer, (5) general market conditions and volatility, (6) industry factors, and (7) the past impairment history of the security holding or the issuer. All mortgage-backed securities and asset-backed securities are reviewed for other-than-temporary impairment treatment in accordance with the guidance of EITF Issue No. 99-20,“Recognition of Interest Income and Impairment on Purchased and Retained Beneficial Interests in Securitized Financial Assets”. In addition, for securities expected to be sold, an other-than-temporary impairment charge is recognized if the Company does not expect the fair value of a security to recover to cost or amortized cost prior to the expected date of sale.

For mortgage-backed fixed maturity securities, the Company recognizes income using a constant effective yield based on anticipated prepayments over the economic life of the security. The mortgage-backed portfolio is accounted for under the retrospective method and prepayment assumptions are based on market expectations. When actual prepayments differ significantly from anticipated prepayments, the effective yield is recalculated to reflect actual payments to date and anticipated future payments and any resulting adjustment is included in net investment income.

Cash equivalents are short-term, highly liquid investments that are both readily convertible into known amounts of cash and so near to maturity that they present insignificant risk of changes in value due to changing interest rates. The Company’s cash equivalents include debt securities purchased with maturities of three months or less at acquisition and are carried at amortized cost that approximates fair value.

Short-term investments are debt securities with maturities at acquisition between three months and one year, are considered available for sale and are carried at amortized cost, which approximates fair value.

All Variable Interest Entities (VIEs) for which the Company is the primary beneficiary are consolidated into the Company’s financial statements.

Other investments, principally investments in limited partnerships, are accounted for using the equity method. Equity investments in privately held businesses are accounted for under the cost method where market value data is unavailable for the underlying investment.

Mortgage loans are stated at amortized cost less a valuation allowance for potentially uncollectible amounts.

Derivatives

All derivatives are recognized on the balance sheet at fair value. On the date a contract is entered into, the Company designates the derivative as either (1) a hedge of a fair value of a recognized asset (“fair value hedge”) or (2) an economic hedge (“non-designated derivative”). Changes in the fair value of a derivative that is highly effective and is designated and qualifies as a fair value hedge, along with the loss or gain on the hedged asset attributable to the hedged risk, are recorded in current period operations as a component of net investment income. Changes in the fair value of non-designated derivatives are reported in current period operations as a component of net realized gains and losses and the derivative is included in other assets or liabilities. The Company owns fixed maturity securities which have an option to convert to equity. The derivative features embedded are ancillary to the overall investment. This type of activity is unrelated to hedging. The Company uses various derivative instruments to hedge exposure against interest rates and equity market returns guaranteed by certain life products. In addition, there may be call, put or conversion options embedded in certain bonds it has purchased. The fair value of these derivative instruments is based on broker quotations. These derivatives are not material to the Company’s financial statements.

Securities Lending

The Company participates in a securities lending program to generate additional income, whereby certain domestic fixed income securities are loaned for a short period of time from the Company’s portfolio to qualifying third parties via a lending agent. Terms of the agreement are for borrowers of these securities to provide collateral of at least 102% of the market value of the loaned securities. Acceptable collateral may be in the form of cash or U.S. government securities. The market value of the loaned securities is monitored and additional collateral is obtained if the market value of the collateral falls below 100% of the market value of the loaned securities. Under the terms of the securities lending program, the lending agent indemnifies the Company against borrower defaults. The loaned securities remain a recorded asset of the Company; however, the Company records a liability for the amount of cash collateral held, representing its obligation to return the collateral related to the loaned securities.

Goodwill and Intangible Assets

Goodwill and intangible assets are tested for impairment at least annually using a two-step process. The first step is performed to identify potential impairment and, if necessary, the second step is performed for the purpose of measuring the amount of impairment, if any. Impairment is recognized only if the carrying amount is not recoverable from its undiscounted cash flows and is measured as the difference between the carrying amount and the implied fair value. Other changes in the carrying amount of goodwill are primarily caused as a result of foreign currency translation adjustments and adjustments to valuation allowances for acquired tax losses. Intangible assets are amortized over their useful lives.

35

| Notes to Consolidated Financial Statements | LIBERTY MUTUAL HOLDING COMPANY INC. | |

[CONTINUED] |

Deferred Policy Acquisition Costs

Costs that vary with and are primarily related to the acquisition of new insurance and investment contracts are deferred and amortized over the respective policy terms. Deferred policy acquisition costs are reviewed annually for recoverability. Investment income is considered in the recoverability assessment. For short-duration contracts, acquisition costs include commissions, underwriting expenses and premium taxes. For long-duration insurance contracts, these costs include first year commissions in excess of annual renewal commissions and variable sales, underwriting and administrative expenses.

For short-duration contracts, acquisition costs are amortized in proportion to earned premiums. For traditional long-duration contracts, acquisition costs are amortized over the premium paying period of the related policies using assumptions consistent with those used in computing policy benefit reserves. For universal life insurance, annuity, and investment products, acquisition costs are amortized in relation to expected gross profits.

For long-duration contracts, to the extent unrealized gains or losses on fixed income securities carried at fair value would result in an adjustment of estimated gross profits had those gains or losses actually been realized, the related unamortized deferred policy acquisition costs are recorded net of tax as a reduction of the unrealized capital gains or losses and included in accumulated other comprehensive income.

Real Estate and Other Fixed Assets

The costs of buildings, furniture, and equipment are depreciated, principally on a straight-line basis, over their estimated useful lives (a maximum of 39.5 years for buildings, 10 years for furniture, and 5 years for equipment). Expenditures for maintenance and repairs are charged to income as incurred while expenditures for improvements are capitalized and depreciated.

Separate Account Assets and Liabilities

Separate and variable accounts represent funds for which investment income and investment gains and losses accrue directly to the policyholders who predominantly bear the investment risk. Each account has specific investment objectives, and the assets are carried at fair value. The assets of each account are legally segregated and are not subject to claims that arise out of any other business of the Company. The liabilities of these accounts are equal to the account assets. Investment income, realized investment gains (losses), and policyholder account deposits and withdrawals related to separate accounts are excluded from the consolidated statements of income. The fees earned for administrative and contract holder maintenance services performed for these separate accounts are included in fee and other revenue.

Insurance Liabilities and Reserves

For short-duration contracts, the Company establishes reserves for unpaid insurance claims and claim adjustment expenses covering events that occurred in 2006 and prior years. These reserves reflect estimates of the total cost of claims reported but not yet paid and the cost of claims not yet reported, as well as the estimated expenses necessary to settle the claims. Reserve estimates are based on past loss experience modified for current claim trends, as well as prevailing social, economic and legal conditions. Final claim payments, however, may ultimately differ from the established reserves, since these payments might not occur for several years. Reserve estimates are continually reviewed and updated, and any resulting adjustments are reflected in current operating results. The Company does not discount reserves other than tabular discounting on the long-term indemnity portion of workers compensation claims, the long-term disability portion of group accident and health claims as permitted by insurance regulations in certain states, and specific asbestos structured settlements. Reserves are reduced for estimated amounts of salvage and subrogation and deductibles recoverable from policyholders.

For long-duration contracts, measurement of liabilities is based on generally accepted actuarial techniques but requires assumptions about mortality, lapse rates, and assumptions about future returns on related investments. Annuity and structured settlement contracts without significant mortality or morbidity risk are accounted for as investment contracts, whereby the premium received plus interest credited less policyholder withdrawals represents the investment contract liability. Implied credited interest rates for domestic structured settlement contracts in force averaged 5.9%, 6.2%, and 6.3% for 2006, 2005, and 2004, respectively. Implied credited interest rates for foreign structured settlement contracts in force were between 2.5% and 6.0% in 2006, 2005 and 2004. Credited rates for domestic universal life contracts in force were between 4.0% and 6.3% in 2006, 3.5% and 7.0% in 2005, and 4.0% and 8.0% in 2004. Credited rates for foreign universal life contracts in force were between 2.0% and 6.0% in 2006 and 1.0% and 6.0% in 2005 and 2004. Liabilities for future policy benefits for traditional life policies have been computed using the net level premium method based upon estimated future investment yields (between 4.5% and 10.3% in 2006 and 2005 and 4.1% and 10.3% in 2004), mortality assumptions (based on the Company’s experience relative to standard industry mortality tables) and withdrawal assumptions (based on the Company’s experience).

36

Policyholder Dividends

Policyholder dividends are accrued using an estimate of the ultimate amount to be paid in relation to premiums earned based on the underlying contractual obligations.

For domestic property-casualty insurance, certain insurance contracts, primarily workers compensation policies, are issued with dividend plans to be paid subject to approval by the insurer’s board of directors. Such policies approximated 2% of domestic property-casualty insurance premiums written for the years ended December 31, 2006, 2005, and 2004.

For life insurance, dividends to participating policyholders are calculated as the sum of the difference between the assumed mortality, interest and loading, and the actual experience of the Company relating to participating policyholders. As a result of statutory regulations, the major portion of earnings from participating policies inures to the benefit of the participating policy-holders and is excluded from the consolidated net income and policyholders’ equity. Participating policies approximate 36% of ordinary life insurance in force at December 31, 2006, and 2005, and 37% of premium for the years ended December 31, 2006, and 2005.

Long-Term Incentive and Performance Based Incentive Plans

The Company maintains short-and long-term incentive compensation plans. Long-term plans that vest over the requisite service period and are based upon notional units are accounted for under SFAS 123(R). Additionally, the Company provides various performance based incentive compensation to the majority of employees meeting the participation requirements of the respective plans. Compensation cost related to these plans is determined in accordance with plan formulas and recorded ratably over the years the employee service is provided.

Revenue Recognition

For short-duration insurance contracts, premiums are reported as earned income generally on a pro-rata basis over the terms of the related policies. For retrospectively rated policies and contracts, premium estimates are continually reviewed and updated and any resulting adjustments are reflected in current operating results. For traditional long-duration insurance contracts (including term and whole life contracts and annuities), premiums are earned when due. For annuities and structured settlements without significant mortality or morbidity risk (investment contracts) and universal life contracts (long-duration contracts with terms that are not fixed or guaranteed), revenues represent investment income earned on the related assets. Universal life and annuity contract revenues also include mortality, surrender, and administrative fees charged to policyholders.

Reinsurance

All assets and liabilities related to reinsurance ceded contracts are reported on a gross basis in the consolidated balance sheets. Prospective reinsurance premiums, losses, and loss adjustment expenses are accounted for on a basis consistent with the terms of the reinsurance contracts. The consolidated statements of income reflect premiums, benefits, and settlement expenses net of reinsurance ceded.

Transactions that do not transfer risk are included in other assets or other liabilities. Ceded transactions that transfer risk but are retroactive are included in reinsurance recoverables. The excess of estimated liabilities for claims and claim costs over the consideration paid net of experience adjustments is established as a deferred credit at inception. The deferred amounts are subsequently amortized using the effective interest method over the expected settlement period. The periodic amortization is reflected in the accompanying consolidated statements of income through operating costs and expenses.

Amounts recoverable from reinsurers are estimated in a manner consistent with the claim liabilities associated with the reinsured business. The Company evaluates reinsurance collectibility and a provision for uncollectible reinsurance is recorded.

Translation of Foreign Currencies