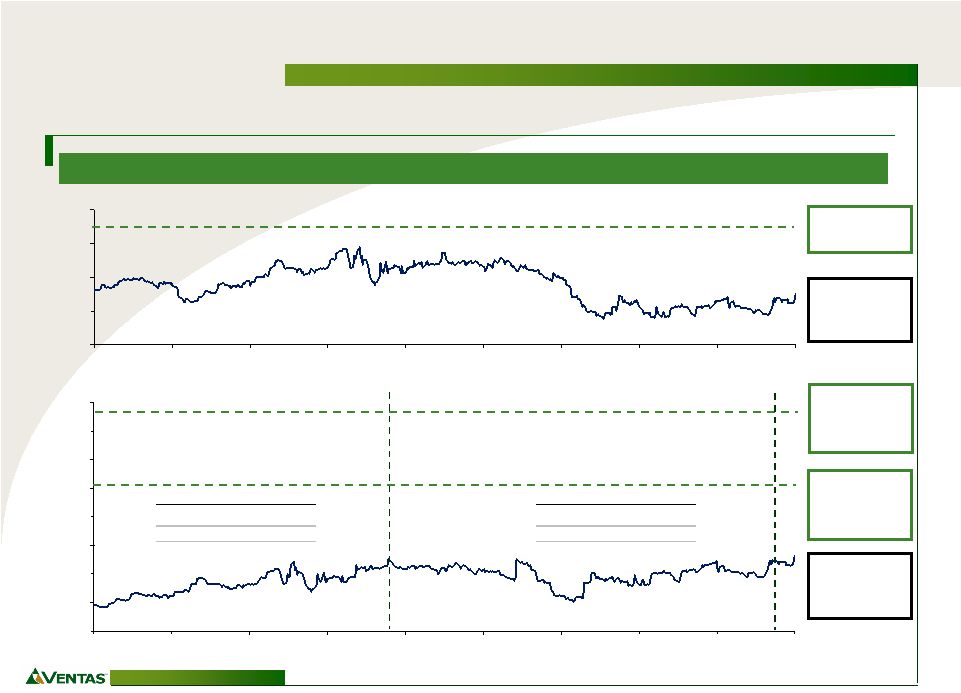

Positive Analyst Reaction to the Ventas Deal – Fully Values Sunrise REIT 10 ____________________ Source: Wall Street research. “Overall, we think VTR is paying a lot for the Sunrise portfolio, possibly at the high end of an acceptable range ” -BMO Capital Markets, 1/16/2007 “Given the premium and the challenges SZR was facing (high payout ratio, high leverage, difficulty in meeting consensus growth expectations, etc.), we believe the Ventas bid has a high probability of being approved by unitholders . Moreover, we believe the probability of receiving a higher bid is low, as we understand SZR ran a fairly full auction process ” - BMO Capital Markets, 1/15/2007 “The Ventas offer was supported by the boards of both Sunrise REIT and Ventas, and was agreed to following a competitive bid process in which HCP participated” - CIBC World Markets, 2/16/2007 “We believe the offer represents full value and reflects the strong institutional demand for high-quality seniors housing properties and portfolios, particularly lighter care, assisted and independent living segments The offer is attractive and fair an d should be accepted” - CIBC World Markets, 1/15/2007 “Ventas is paying Cdn$15 for shares of SZR, a 36% premium to Friday’s closing price, though the shares have underperformed since its IPO in December 2004 (went public at Cdn$10)” - Citigroup, 1/16/2007 “While the deal is expensive (initial cap of 6.2%, 36% premium to SZR stock price), it is in line with recent deals for Class A assets (i.e. the HCP/CNL deal )” -UBS, 1/16/2007 …. |