Exhibit 99.1

December

2010

2010

1

During the course of this presentation the Company will be making forward-looking statements (as

such term is defined in the Private Securities Litigation Reform Act of 1995) that are based on our

current expectations, beliefs and assumptions about the industry and markets in which US

Ecology, Inc. and its subsidiaries operate. Because such statements include risks and

uncertainties, actual results may differ materially from what is expressed herein and no assurance

can be given that the Company will meet its 2010 earnings estimates, successfully execute its

growth strategy, or declare or pay future dividends. For information on other factors that could

cause actual results to differ materially from expectations, please refer to US Ecology, Inc.’s

(formally known as American Ecology Corporation) December 31, 2009 Annual Report on Form 10

- -K and other reports file with the Securities and Exchange Commission. Many of the factors that

will determine the Company’s future results are beyond the ability of management to control or

predict. Participants should not place undue reliance on forward-looking statements, reflect

management’s views only as of the date hereof. The Company undertakes no obligation to revise

or update any forward-looking statements, or to make any other forward-looking statements,

whether as a result of new information, future events or otherwise.

such term is defined in the Private Securities Litigation Reform Act of 1995) that are based on our

current expectations, beliefs and assumptions about the industry and markets in which US

Ecology, Inc. and its subsidiaries operate. Because such statements include risks and

uncertainties, actual results may differ materially from what is expressed herein and no assurance

can be given that the Company will meet its 2010 earnings estimates, successfully execute its

growth strategy, or declare or pay future dividends. For information on other factors that could

cause actual results to differ materially from expectations, please refer to US Ecology, Inc.’s

(formally known as American Ecology Corporation) December 31, 2009 Annual Report on Form 10

- -K and other reports file with the Securities and Exchange Commission. Many of the factors that

will determine the Company’s future results are beyond the ability of management to control or

predict. Participants should not place undue reliance on forward-looking statements, reflect

management’s views only as of the date hereof. The Company undertakes no obligation to revise

or update any forward-looking statements, or to make any other forward-looking statements,

whether as a result of new information, future events or otherwise.

Important assumptions and other important factors that could cause actual results to differ

materially from those set forth in the forward-looking information include a loss of a major

customer, compliance with and changes to applicable laws and regulations, market conditions,

pricing and production rates for the thermal recycling service at our Texas facility, access to cost

effective transportation services, access to insurance and other financial assurances, loss of key

personnel, lawsuits, adverse economic conditions including a tightened credit market, the timing

or level of government funding or competitive conditions, incidents that could limit or suspend

specific operations, our ability to perform under required contracts, our willingness or ability to pay

dividends and our ability to integrate Stablex or any other potential acquisitions.

materially from those set forth in the forward-looking information include a loss of a major

customer, compliance with and changes to applicable laws and regulations, market conditions,

pricing and production rates for the thermal recycling service at our Texas facility, access to cost

effective transportation services, access to insurance and other financial assurances, loss of key

personnel, lawsuits, adverse economic conditions including a tightened credit market, the timing

or level of government funding or competitive conditions, incidents that could limit or suspend

specific operations, our ability to perform under required contracts, our willingness or ability to pay

dividends and our ability to integrate Stablex or any other potential acquisitions.

2

} Founded in 1952 and headquartered in Boise, ID

} Own & operate hazardous and radioactive waste

treatment and disposal facilities

treatment and disposal facilities

} Provide safe, secure & cost-effective hazardous

and radioactive materials solutions to industry &

government

and radioactive materials solutions to industry &

government

3

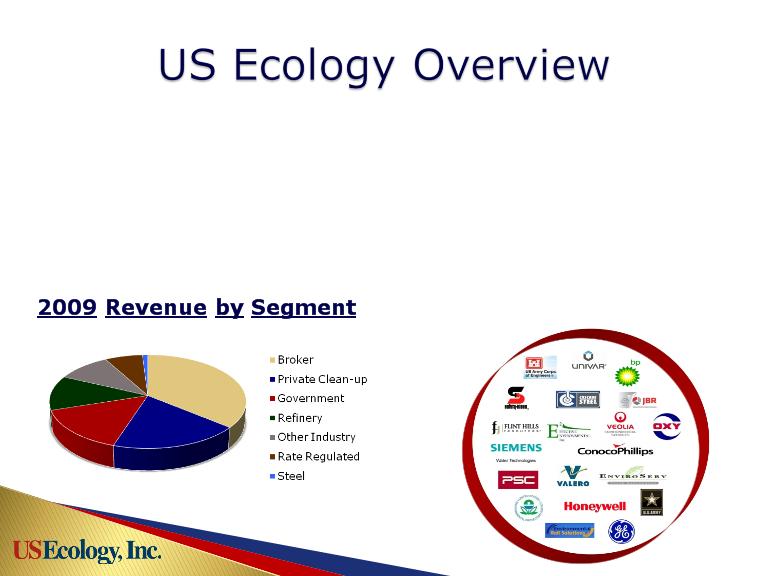

Large & Loyal Customer Base

4

Market Cap | $300 million* |

Recent Price: | $16.37* |

52 Wk. Range: | $12.98 - $17.67 |

Shares Out./Float: | 18.2 / 15.5 million |

Dividend/Yield: | $0.72 / 4.4% |

Revenue TTM | $89 million** |

SG&A % of Revenue: | 17% ** |

Cash/Investments: | $30.4 million** |

Term Debt: | -0- |

Avail. line of credit: | $16 million |

* At 11-22-2010 ** at 9-30-2010

5

6

4 Sites: US Ecology

5 Sites: Waste Management

7 Sites: Clean Harbors

5 Sites: Others *

2 Sites: Energy Solutions

3 Commercial Nuclear Waste Sites in US

21 Hazardous Waste Sites in US & Canada

Grand View, ID

Robstown, TX

Blainville, QC

2008 disposed volume, not capacity based on

Various Industry Sources

Various Industry Sources

} Estimated $5 billion per year market

} Landfill revenue represents

14% of market

14% of market

} Historically ~3.5M tons/year

◦ Down in 2009 due to economy

◦ Stronger in 2010, but still sluggish

} Volumes Fluctuate

◦ Clean-up projects (Events)

◦ Industrial production levels (Base)

} Regulatory Drivers

◦ Increased enforcement

◦ Changes in laws, regulation, and rules

◦ Court orders

} Commercial Drivers

◦ Alternative Use (e.g. real estate development)

◦ Plant expansion

◦ Compliance

} Government sponsored clean-ups

◦ Department of Defense, States, EPA

9

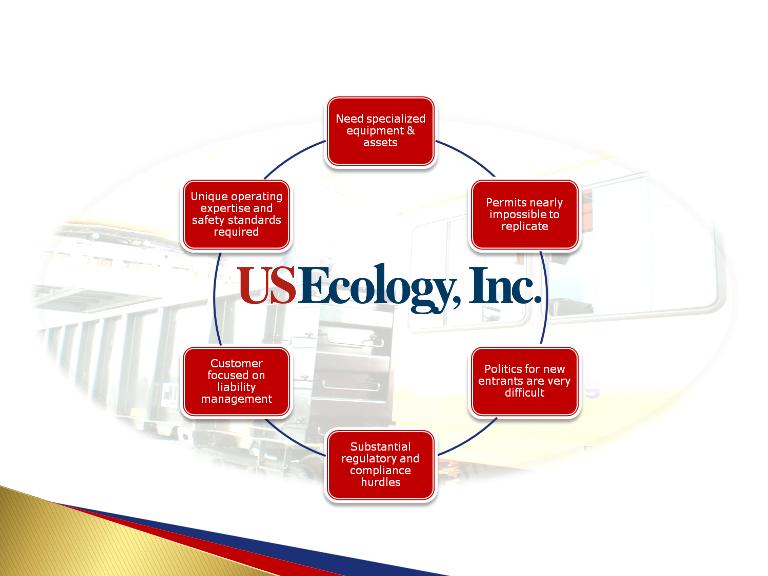

High Barriers to Entry

10

} Remote, geologically superior

desert site

desert site

} Rail served

} Specializes in high volume

treatment or direct disposal

projects

treatment or direct disposal

projects

} “Hybrid” site accepts low-activity

radioactive and hazardous waste

radioactive and hazardous waste

} Years of permitted capacity

Premier US Hazardous Waste Site

} Specializes in difficult to treat

waste streams

waste streams

} Adding waste handling

infrastructure to improve

operating efficiencies & service

infrastructure to improve

operating efficiencies & service

◦ Added disposal space in 2010

◦ Constructing new treatment and

drum handling building

drum handling building

} 10+ years of permitted capacity

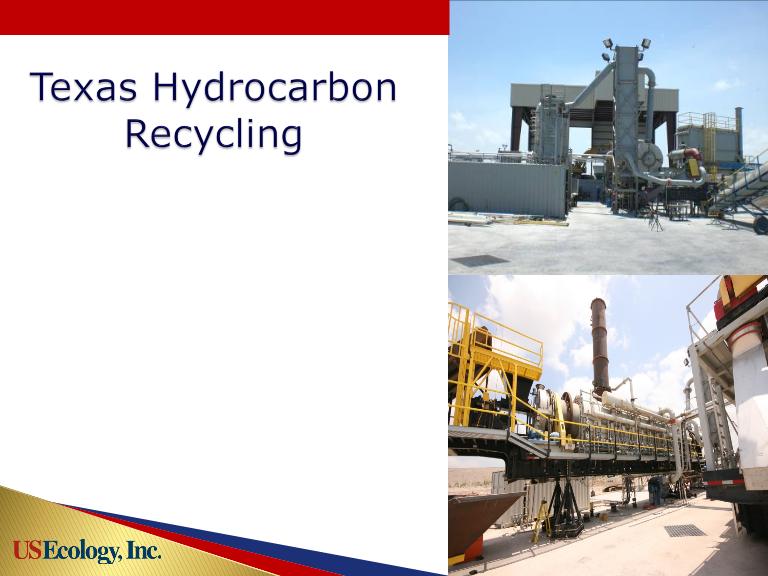

Serving the Gulf Coast Oil & Gas Market

} Recycles refinery tank

bottoms, cracking catalyst &

other oil bearing wastes

bottoms, cracking catalyst &

other oil bearing wastes

◦ Industrial reuse of catalyst

◦ Used oil resold into market

} Key advantage: Internalize

costs of recycling residuals:

ash & liquids

costs of recycling residuals:

ash & liquids

} Constructing new catalyst

handling system

handling system

Nationwide Recycling

} Superb natural conditions for

disposal

disposal

} Specializing in containers and

difficult to treat waste streams

difficult to treat waste streams

} State-of-the-art treatment

building with high capacity drum

handling capability

building with high capacity drum

handling capability

} New disposal space under

construction - Q1 2011 est.

completion

construction - Q1 2011 est.

completion

Great Desert Location Serving CA/AZ

Markets

Markets

} Regulated monopoly for low-

level radioactive waste in 11

western states

level radioactive waste in 11

western states

} Market pricing for certain

naturally occurring radioactive

material

naturally occurring radioactive

material

} Company’s “Cash Cow” -

limited growth potential

limited growth potential

Steady, Rate-Regulated Earnings

} Superb natural conditions

for disposal

for disposal

} Specializing in difficult to

treat waste streams

treat waste streams

} State-of-the-art treatment

building and proprietary

process

building and proprietary

process

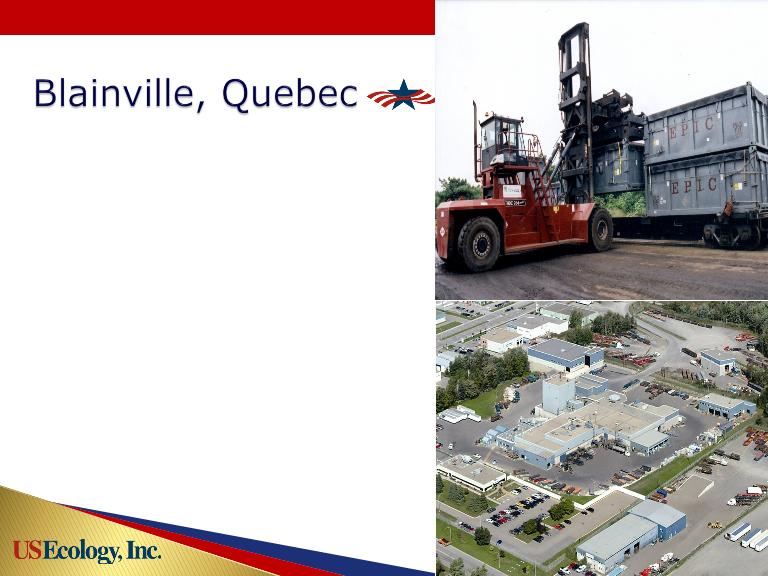

Stablex - Serving NE U.S., Canada

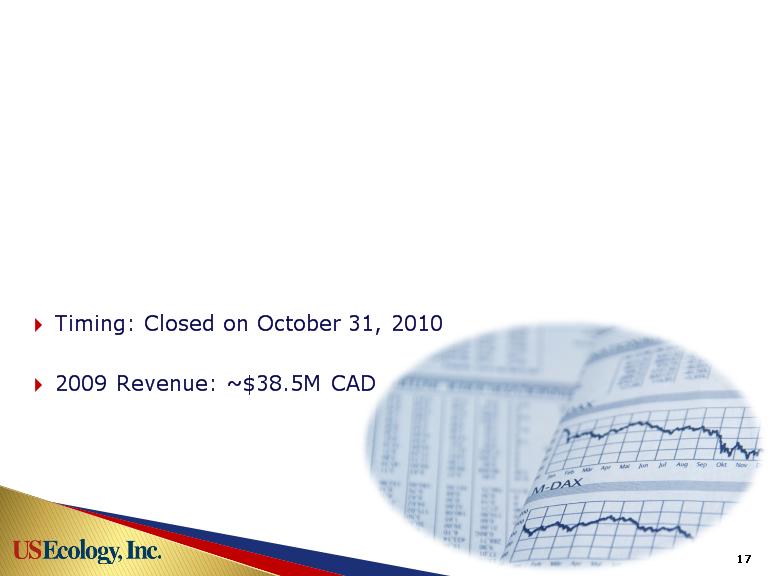

} Purchase price: $80 million Canadian dollars ($77.3M USD)

} Purchased from Marsulex Inc. (TSX: MLX)

} Form of transaction: Stock Purchase

} Financing: Cash on hand and bank financing

◦ $75 million USD Acquisition Credit Facility

} Non-recurring closing costs: $2.6 million or $0.13 per diluted

share

share

} 2009 EBITDA: ~$9.9M CAD

Transaction Summary

} Leverage Stablex diverse base

of blue-chip customers in North

America

of blue-chip customers in North

America

} More than 1,000 customer

relationships

relationships

Business Rationale

} Add physical presence in the

Northeastern U.S. & eastern

Canada

Northeastern U.S. & eastern

Canada

} Expand service offerings and

penetration of national accounts

penetration of national accounts

} Optimize Event opportunities

◦ Combined bids using Stablex

with other USE facilities and

transportation assets

with other USE facilities and

transportation assets

} Opportunity to increase revenue

and improve efficiencies

and improve efficiencies

◦ Transportation, brokering,

permit modifications

permit modifications

19

} Purchase Siemens Water

Technologies Vernon,

California permitted

hazardous liquids

processing facility

Technologies Vernon,

California permitted

hazardous liquids

processing facility

} Purchase Price: $8.65

Million

Million

} Structure: Asset

Purchase

Purchase

} Signed Definitive

Agreement August 27th

Agreement August 27th

} Closing: On Hold

*Treatment, Storage, Disposal Facility

20

21

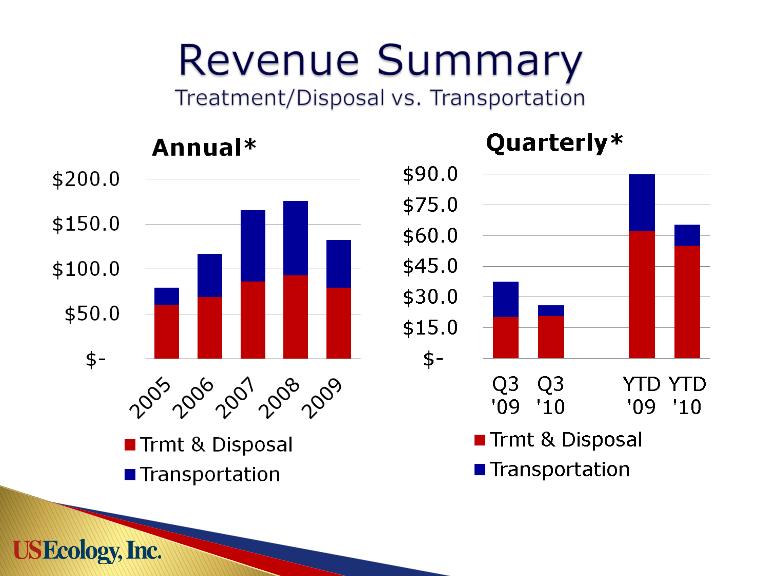

* - Dollars in millions

22

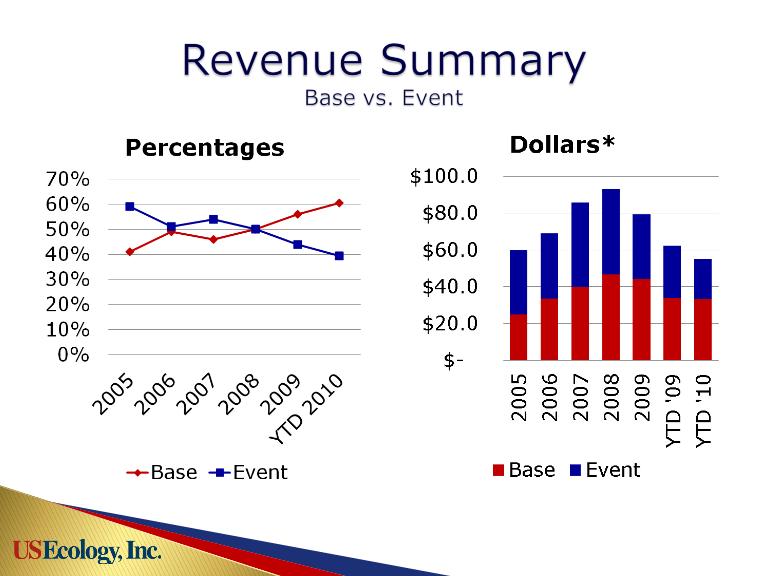

* - Dollars in millions

23

} Ongoing project delays/deferrals

◦ Event business still soft, but better than ‘09

} Pricing pressure for Thermal Recycling

services

services

} Accrual of regulatory fine

} Low rail car utilization in first half

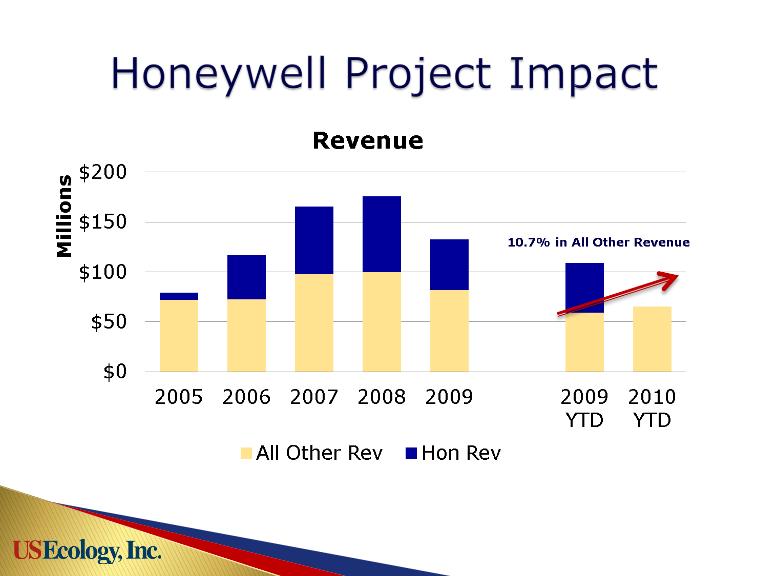

} Despite Challenges grew Non-Honeywell

related revenue by almost 11% vs. YTD

2009

related revenue by almost 11% vs. YTD

2009

24

} Still limited commercial project opportunities - few signs

of a quick or strong turnaround

of a quick or strong turnaround

} Government project opportunities up in 2010 (DOD,

EPA, State highway work), especially California

EPA, State highway work), especially California

} Recurring “Base Business” market has remained flat -

growth requires market share gains from competitors

growth requires market share gains from competitors

} National landfill overcapacity continues to pressure on

pricing

pricing

} Transportation costs rising; makes the distance to USE

West Coast sites vs. competition a more critical factor

West Coast sites vs. competition a more critical factor

25

General Market Trends

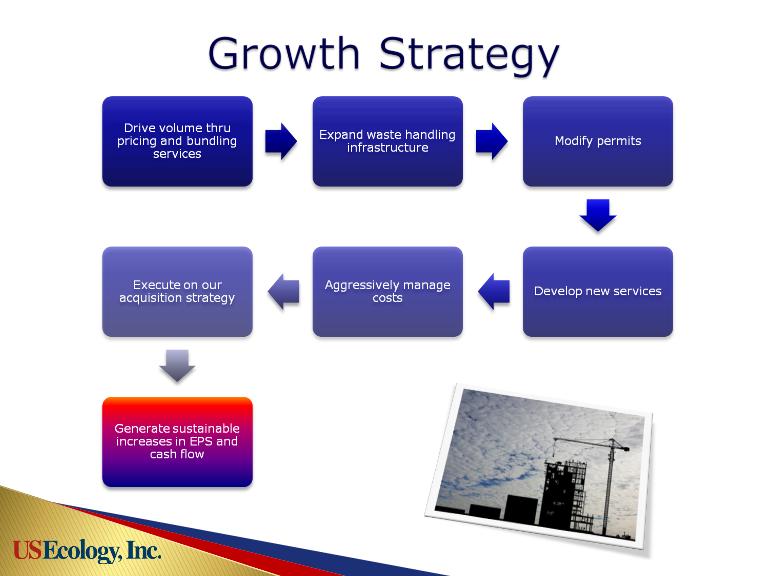

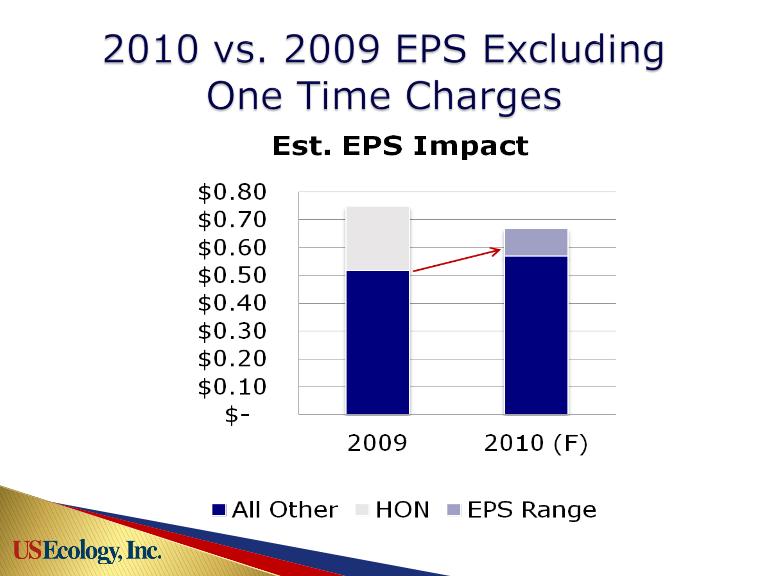

} 2010 EPS of $0.57 to $0.67 excluding one time transaction

and integration costs; reaffirmed October 2010

and integration costs; reaffirmed October 2010

} 2010 earnings will be impacted by $0.13 of non-recurring

transaction and integration costs

transaction and integration costs

} 2010 EPS growth of 10% to 29% over 2009 excluding

contributions from 2009 Honeywell and insurance

settlement and 2010 acquisition costs (“apples to apples”)

contributions from 2009 Honeywell and insurance

settlement and 2010 acquisition costs (“apples to apples”)

} Expect Q4 , while still relatively strong, to be sequentially

weaker than Q3 since most of GE waste was received in

Q3

weaker than Q3 since most of GE waste was received in

Q3

} Stablex 2009 Revenue of CAD$38.5 million, EBITDA of

CAD$9.9 million - expect EPS contribution in 2011

CAD$9.9 million - expect EPS contribution in 2011

26

Business Overview and Outlook

27

} Unique set of radioactive & hazardous services and assets

means high barriers to entry

means high barriers to entry

} Strong cash flow business with significant earnings upside

} Once fixed costs are covered, significant “fall thru” to

bottom line (i.e. high operating leverage)

bottom line (i.e. high operating leverage)

} Return on total capital: 13.8% ttm

} Attractive dividend yield of over 4.4%

} Seasoned, committed executive management team

} Large, loyal customer base

} Opportunity to leverage new

assets

assets

28