Exhibit 99.1

Presentation on the

North America Chlor Alkali Industry

Prepared for

UBS Warburg

Grass Roots Chemical Conference

New Orleans, LA

February 16, 2005

By

John L. McIntosh

President, Chlor Alkali Products

Olin Corporation

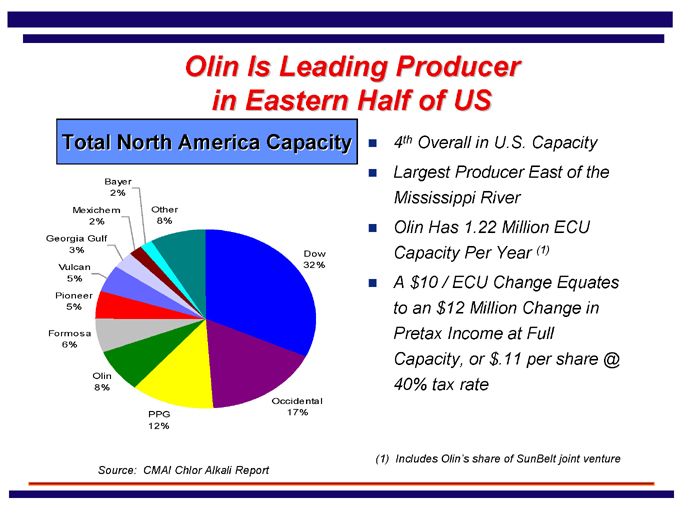

Olin Is Leading Producer

in Eastern Half of US

Source: CMAI Chlor Alkali Report

4th Overall in U.S. Capacity

Largest Producer East of the Mississippi River

Olin Has 1.22 Million ECU Capacity Per Year (1)

A $10 / ECU Change Equates to an $12 Million Change in Pretax Income at Full Capacity, or $.11 per share @ 40% tax rate

(1) Includes Olin’s share of SunBelt joint venture

Total North America Capacity

Bayer 2%

Other 8%

Dow 32%

Occidental 17%

PPG 12%

Olin 8%

Formosa 6%

Pioneer 5%

Vulcan 5%

Georgia Gulf 3%

Mexichem 2%

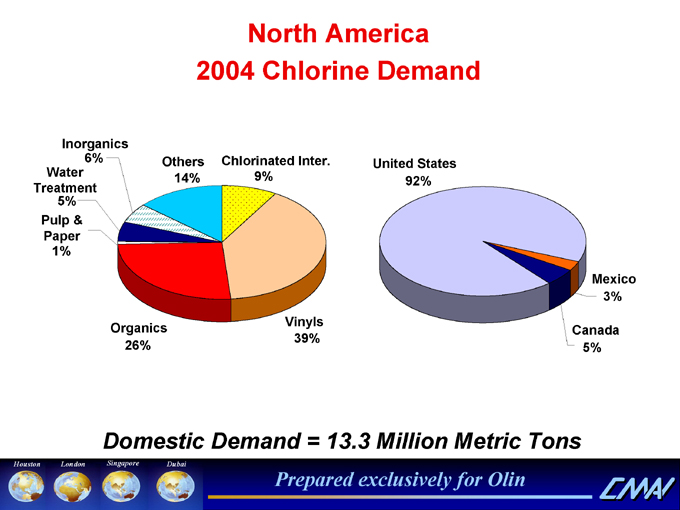

North America

2004 Chlorine Demand

United States 92%

Domestic Demand = 13.3 Million Metric Tons

Inorganics 6%

Others 14%

Chlorinated Inter.

9%

Vinyls 39%

Organics 26%

Pulp & Paper 1%

Water Treatment 5%

Mexico 3%

Canada 5%

Houston London Singapore Dubai

Prepared exclusively for Olin

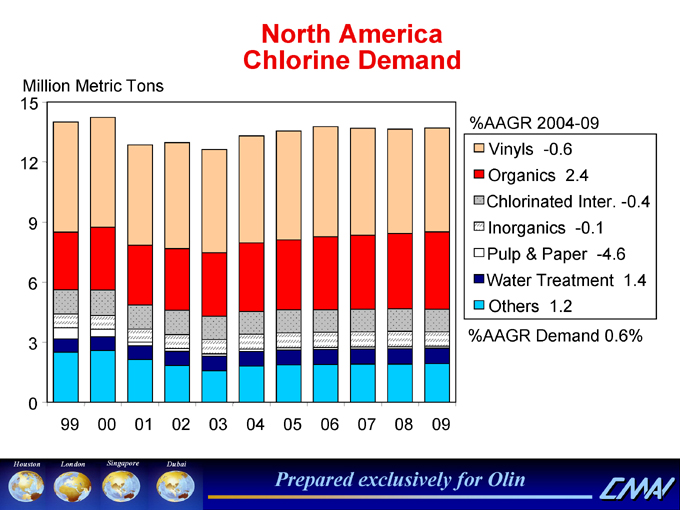

North America

Chlorine Demand

Million Metric Tons

15 12 9 6 3 0

99 00 01 02 03 04 05 06 07 08 09

Houston London Singapore Dubai

Prepared exclusively for Olin

%AAGR 2004-09

Vinyls -0.6

Organics 2.4

Chlorinated Inter. -0.4

Inorganics -0.1

Pulp & Paper -4.6

Water Treatment 1.4

Others 1.2

%AAGR Demand 0.6%

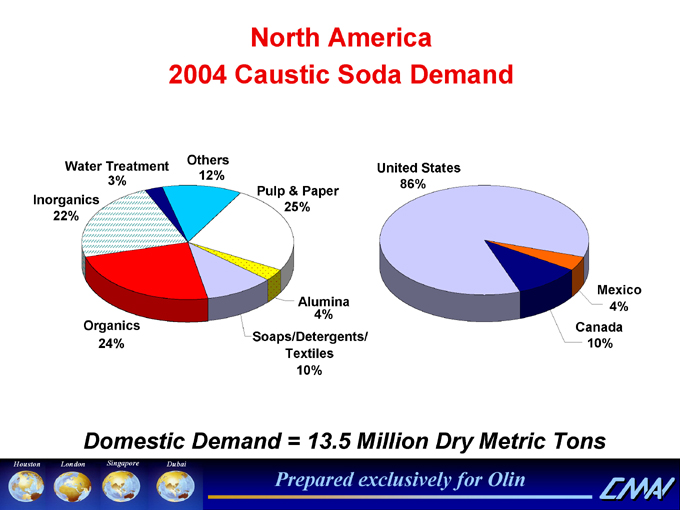

North America

2004 Caustic Soda Demand

Others 12%

Water Treatment 3%

United States 86%

Pulp & Paper 25%

Inorganics 22%

Alumina 4%

Mexico 4%

Organics 24%

Soaps/Detergents/Textiles 10%

Canada 10%

Domestic Demand = 13.5 Million Dry Metric Tons

Houston London Singapore Dubai

Prepared exclusively for Olin

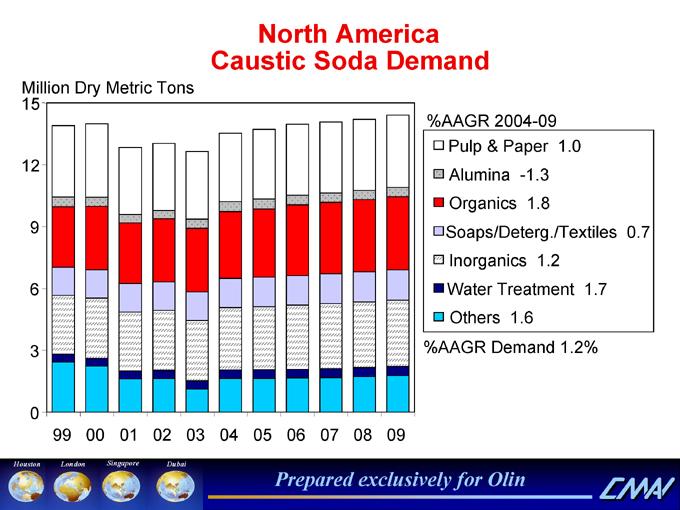

North America

Caustic Soda Demand

Million Dry Metric Tons

%AAGR 2004-09

Pulp & Paper 1.0

Alumina -1.3

Organics 1.8

Soaps/Deterg./Textiles 0.7 Inorganics 1.2

Water Treatment 1.7 Others 1.6

%AAGR Demand 1.2%

15 12 9 6 3 0

99 00 01 02 03 04 05 06 07 08 09

Houston London Singapore Dubai

Prepared exclusively for Olin

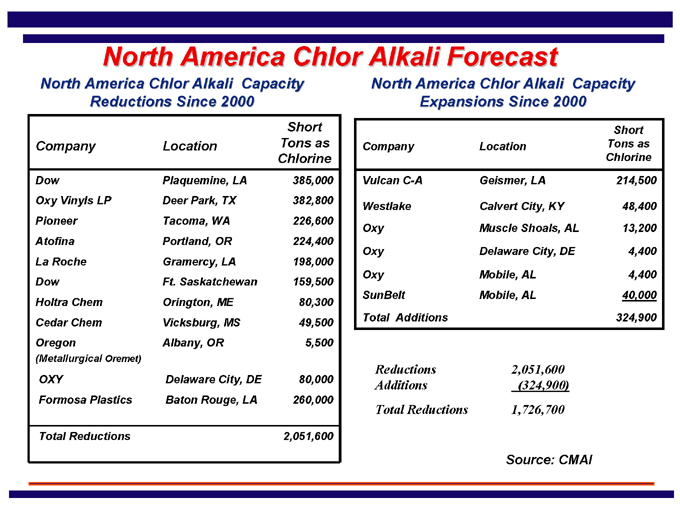

North America Chlor Alkali Forecast

North America Chlor Alkali Capacity Expansions Since 2000

Company Location Short Tons as Chlorine

Vulcan C-A Geismer, LA 214,500

Westlake Calvert City, KY 48,400

Oxy Muscle Shoals, AL 13,200

Oxy Delaware City, DE 4,400

Oxy Mobile, AL 4,400

SunBelt Mobile, AL 40,000

Total Additions 324,900

Reductions 2,051,600

Additions (324,900)

Total Reductions 1,726,700

Source: CMAI

North America Chlor Alkali Capacity

Reductions Since 2000

Company Location Short Tons as Chlorine

Dow Plaquemine, LA 385,000

Oxy Vinyls LP Deer Park, TX 382,800

Pioneer Tacoma, WA 226,600

Atofina Portland, OR 224,400

La Roche Gramercy, LA 198,000

Dow Ft. Saskatchewan 159,500

Holtra Chem Orington, ME 80,300

Cedar Chem Vicksburg, MS 49,500

Oregon Albany, OR 5,500

(Metallurgical Oremet)

OXY Delaware City, DE 80,000

Formosa Plastics Baton Rouge, LA 260,000

Total Reductions 2,051,600

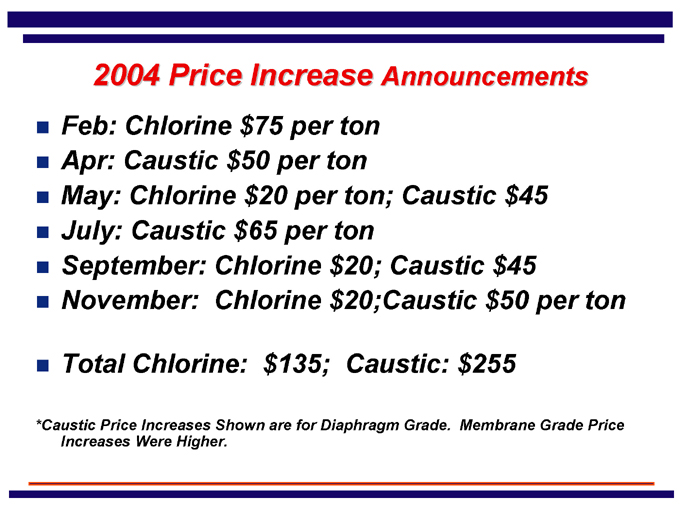

2004 Price Increase Announcements

Feb: Chlorine $75 per ton

Apr: Caustic $50 per ton

May: Chlorine $20 per ton; Caustic $45

July: Caustic $65 per ton

September: Chlorine $20; Caustic $45

November: Chlorine $20;Caustic $50 per ton

Total Chlorine: $135; Caustic: $255

*Caustic Price Increases Shown are for Diaphragm Grade. Membrane Grade Price Increases Were Higher.

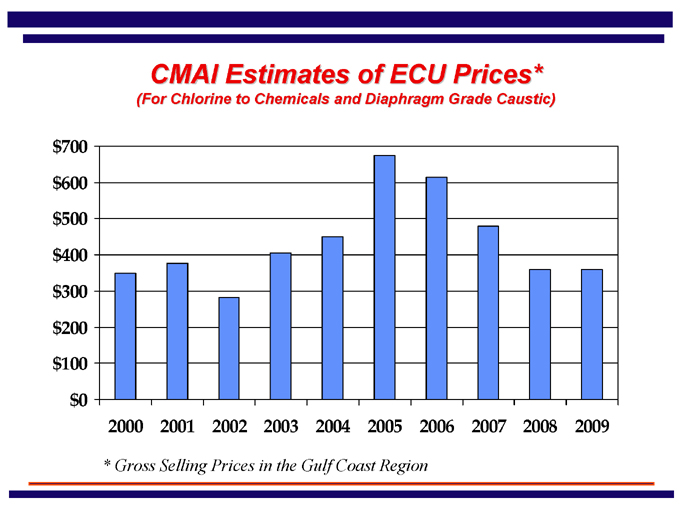

CMAI Estimates of ECU Prices*

(For Chlorine to Chemicals and Diaphragm Grade Caustic)

$700 $600 $500 $400 $300 $200 $100 $0

* Gross Selling Prices in the Gulf Coast Region

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009

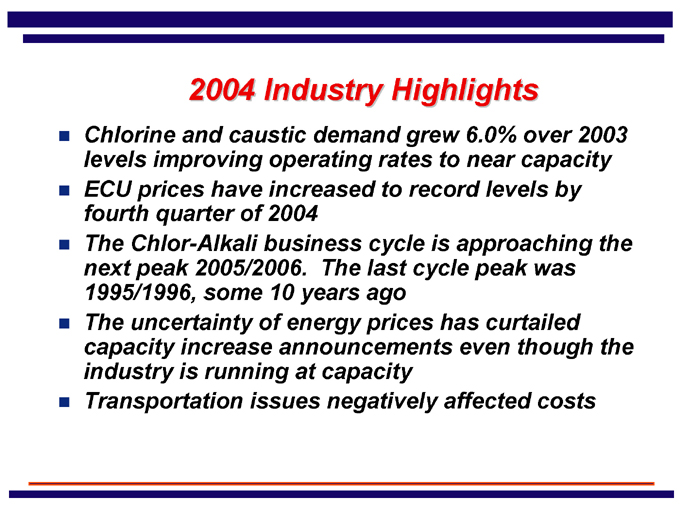

2004 Industry Highlights

Chlorine and caustic demand grew 6.0% over 2003 levels improving operating rates to near capacity

ECU prices have increased to record levels by fourth quarter of 2004

The Chlor-Alkali business cycle is approaching the next peak 2005/2006. The last cycle peak was 1995/1996, some 10 years ago

The uncertainty of energy prices has curtailed capacity increase announcements even though the industry is running at capacity

Transportation issues negatively affected costs

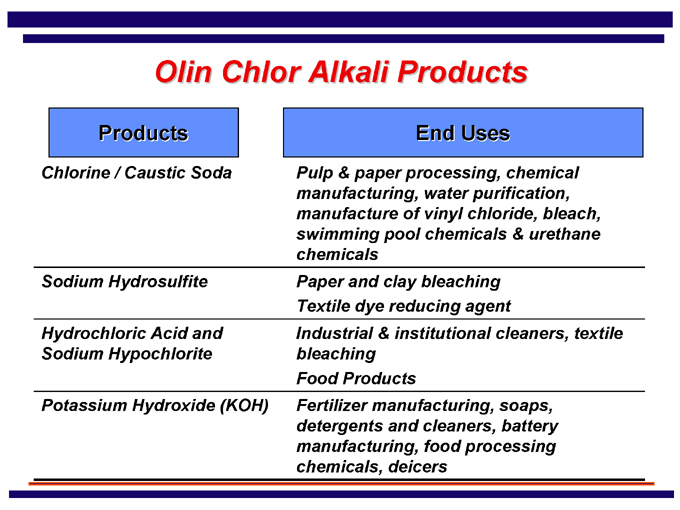

Olin Chlor Alkali Products

Products End Uses

Chlorine / Caustic Soda

Pulp & paper processing, chemical manufacturing, water purification, manufacture of vinyl chloride, bleach, swimming pool chemicals & urethane chemicals

Sodium Hydrosulfite

Paper and clay bleaching Textile dye reducing agent

Hydrochloric Acid and Sodium Hypochlorite

Industrial & institutional cleaners, textile bleaching Food Products

Potassium Hydroxide (KOH)

Fertilizer manufacturing, soaps, detergents and cleaners, battery manufacturing, food processing chemicals, deicers

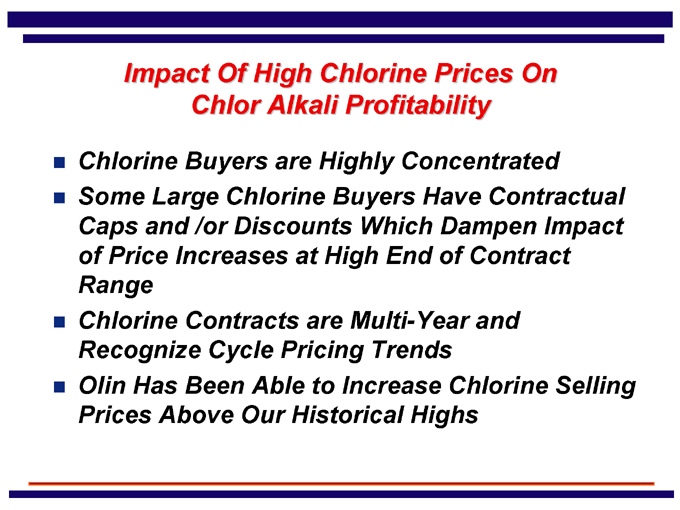

Impact Of High Chlorine Prices On

Chlor Alkali Profitability

Chlorine Buyers are Highly Concentrated

Some Large Chlorine Buyers Have Contractual Caps and /or Discounts Which Dampen Impact of Price Increases at High End of Contract Range

Chlorine Contracts are Multi-Year and Recognize Cycle Pricing Trends

Olin Has Been Able to Increase Chlorine Selling Prices Above Our Historical Highs

Caustic Price Increases Are A Key

to Higher ECU Values

Historically, Olin’s Chlor Alkali Business Has Seen Peak Earnings During Times of High Caustic Prices

Caustic Customers are Smaller and More Numerous

Caustic Demand Improvement Normally Lags Chlorine by Six Months

Olin Sells 10% More Caustic Than Chlorine

Proximity to Customers Creates a Freight Advantage

Olin’s Chlor Alkali Strategy

Be the Preferred Supplier to Non-Integrated Chlor Alkali Customers

Continue to Drive Cost Improvements Through Manufacturing and Logistic Optimization

Continue Our Partnership Philosophy With Our Customers

Significant Opportunities to Increase the Value of the Business at Modest Capital Cost

Be a Strong Cash Generator and Value Enhancer to Olin Corporation

Cautionary Language

This presentation includes estimates of future performance. These are forward-looking statements and results could differ materially from those projected. Some of the factors that could cause actual results to differ are described in the outlook section of our most recent 10-K and 10-Q, and our fourth quarter 2004 earnings release.