UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Form N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act File Number: 811-04015

Eaton Vance Mutual Funds Trust

(Exact Name of Registrant as Specified in Charter)

Two International Place, Boston, Massachusetts 02110

(Address of Principal Executive Offices)

Maureen A. Gemma

Two International Place, Boston, Massachusetts 02110

(Name and Address of Agent for Services)

(617) 482-8260

(Registrant’s Telephone Number)

January 31

Date of Fiscal Year End

January 31, 2021

Date of Reporting Period

| Item 1. | Reports to Stockholders |

Eaton Vance

Emerging Markets Debt Fund

Annual Report

January 31, 2021

Commodity Futures Trading Commission Registration. The Commodity Futures Trading Commission (“CFTC”) has adopted regulations that subject registered investment companies and advisers to regulation by the CFTC if a fund invests more than a prescribed level of its assets in certain CFTC-regulated instruments (including futures, certain options and swap agreements) or markets itself as providing investment exposure to such instruments. The adviser is registered with the CFTC as a commodity pool operator with respect to its management of the Fund. As the commodity pool operator of the Fund, the adviser has claimed relief under the Commodity Exchange Act from certain reporting and recordkeeping requirements. The adviser is also registered as a commodity trading advisor.

Fund shares are not insured by the FDIC and are not deposits or other obligations of, or guaranteed by, any depository institution. Shares are subject to investment risks, including possible loss of principal invested.

This report must be preceded or accompanied by a current summary prospectus or prospectus. Before investing, investors should consider carefully the investment objective, risks, and charges and expenses of a mutual fund. This and other important information is contained in the summary prospectus and prospectus, which can be obtained from a financial intermediary. Prospective investors should read the prospectus carefully before investing. For further information, please call 1-800-262-1122.

Annual Report January 31, 2021

Eaton Vance

Emerging Markets Debt Fund

Eaton Vance

Emerging Markets Debt Fund

January 31, 2021

Management’s Discussion of Fund Performance1

Economic and Market Conditions

The 12-month period that began on February 1, 2020, was dominated by a black swan event: the outbreak of a new coronavirus in China that became known as COVID-19. As the virus turned into a global pandemic in February and March, it ended the longest-ever U.S. economic expansion and triggered a global economic slowdown. Credit markets along with equity markets plunged in value amid unprecedented volatility.

Emerging market (EM) economies were particularly hard-hit as many workers in those nations could not work remotely and were part of an informal economy with few government supports. In contrast with developed nations where many workers shifted to working safely from home, most workers in EMs faced the choice of going to work despite COVID-19, or losing their income. Oil-exporting EM nations suffered the additional shock of plunging prices for their exports as demand for transportation fuels slowed to a trickle. Tourism and remittances from family members overseas — additional sources of income for many EM economies — also declined dramatically during the period.

In response to the pandemic slowdown, the U.S. Federal Reserve announced two emergency rate cuts in March 2020 — lowering the federal funds rate to 0.00%-0.25% — along with other measures designed to shore up the markets. Across the globe, other central banks and governments launched aggressive monetary and fiscal responses to help mitigate the economic effects of COVID-19. These actions provided liquidity to the global economy that, in turn, helped calm investment markets and initiated a fixed-income rally that began in April and lasted through most of the summer.

For EM bond issuers specifically, this combination also helped to re-open the market for new debt issues and provide the much-needed ability to refinance maturing bonds. As economies started to emerge from COVID-19 lockdowns, factories resumed production and global market indexes reflected investor optimism.

In September and October, however, the fixed-income rally stalled as the pandemic appeared to increase its drag on the global economy. Across Europe, nations that seemed to have beaten back the coronavirus during the summer initiated new lockdowns to combat a second wave of infections. In the U.S., coronavirus cases were on the rise in virtually every state. Reflecting an increasingly grim economic outlook for fall and winter, EM fixed-income indexes, along with many of their developed-market counterparts, reported negative returns in September and October.

In the closing months of 2020, however, bonds reversed course again. Joe Biden’s victory in the November U.S. presidential election eased political uncertainties that had dogged investment markets through much of the fall. Additionally, the announcement that two COVID-19 vaccine candidates had proven more than 90% effective in late-stage trials — and the initial distribution of those vaccines in December — boosted investor optimism and powered a global market rally. But in the final month of the period, bond returns turned negative amid concerns over variant strains of the virus as well as an increase in real yields in the U.S.

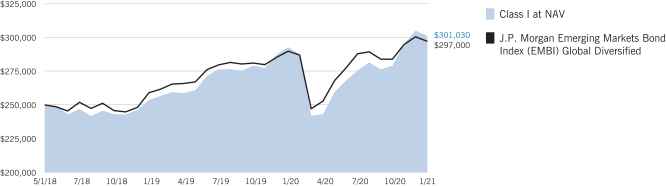

Nonetheless, the EM debt asset class ended the period solidly in positive territory for the period, although it lagged developed-market returns. For the 12 tumultuous months ended January 31, 2021, the J.P. Morgan Emerging Markets Bond Index (EMBI) Global Diversified (the Index), a broad measure of the asset class, returned 2.55%, while the Bloomberg Barclays U.S. Aggregate Bond Index, a broad measure of the U.S. fixed-income market, returned 4.72%.

Fund Performance

For the 12-month period ended January 31, 2021, Eaton Vance Emerging Markets Debt Fund (the Fund) returned 2.81% for Class I shares at net asset value (NAV), outperforming its benchmark, the Index, which returned 2.55%.

On a regional basis, the largest contributors to Fund performance versus the Index were the Fund’s allocations to the Middle East, Eastern Europe, and Asia. In the Middle East, concerns about the potential effects of the nascent COVID-19 outbreak led the Fund to sell its position in Bahrain government bonds in mid-February 2020, after a strong rally during the prior 18 months sparked by fiscal reforms and the repair of relations with Bahrain’s neighbor Saudi Arabia. Prices of Bahraini bonds plunged during the pandemic market downturn, and not owning them in March was a further boost to relative returns. Beginning in April, however, the Fund then acquired an overweight position relative to the Index in Bahraini debt, which subsequently rallied and contributed to Fund performance versus the Index during the period.

In Eastern Europe, the Fund’s overweight position in Ukrainian sovereign debt also helped performance versus the Index. Despite considerable volatility during the period, prices of Ukrainian debt ended the period about where they began, while the debt delivered a notably higher yield than the Index throughout the period. In Asia, not owning Sri Lankan debt, an Index component, contributed to relative returns as well. Sri Lankan debt levels had been high entering the period, and the virtual absence of tourism — a key driver of the nation’s economy — during the pandemic led Sri Lankan bond prices to decline substantially to distressed levels.

In contrast, the Fund’s U.S. duration positioning and exposure to Latin American debt detracted from performance versus the Index. The Fund’s average duration, or sensitivity to interest rate changes, was generally less than that of the Index. As a result, the Fund benefited less than the Index when interest rates declined during the period.

In Latin America, the Fund’s overweight positions in Costa Rican, El Salvadoran and Ecuadorian sovereign debt negatively impacted relative returns. As tourism — a mainstay of the Costa Rican economy — virtually disappeared during the pandemic, the country’s debt declined in value and was sold from the Fund. In El Salvador, a new president elected on a reform platform in 2019 appeared to turn more authoritarian in the face of the pandemic, and El Salvadoran debt lost value and was also sold from the Fund.

See Endnotes and Additional Disclosures in this report.

Past performance is no guarantee of future results. Returns are historical and are calculated by determining the percentage change in net asset value (NAV) or offering price (as applicable) with all distributions reinvested. Investment return and principal value will fluctuate so that shares, when redeemed, may be worth more or less than their original cost. Performance for periods less than or equal to one year is cumulative. Performance is for the stated time period only; due to market volatility, current Fund performance may be lower or higher than the quoted return. For performance as of the most recent month-end, please refer to eatonvance.com.

Eaton Vance

Emerging Markets Debt Fund

January 31, 2021

Management’s Discussion of Fund Performance1 — continued

The Fund’s Ecuador debt position was initiated in early February 2020 in response to an improving political environment. But as falling oil prices during the pandemic hurt Ecuador’s oil-dependent economy, its bonds declined in price and were sold from the Fund. After the bonds subsequently defaulted, the Fund initiated a new Ecuador position in October as the debt was restructured.

As a whole, the Fund’s use of derivatives contributed to returns versus the Index. Interest rate futures and swaps, which were used to manage interest rate exposures, positively impacted performance. Sovereign credit default swaps also contributed to performance versus the Index during the period. However, currency forwards, generally used to hedge euro exposure in the Fund’s euro-denominated holdings, detracted from performance relative to the Index.

See Endnotes and Additional Disclosures in this report.

Past performance is no guarantee of future results. Returns are historical and are calculated by determining the percentage change in net asset value (NAV) or offering price (as applicable) with all distributions reinvested. Investment return and principal value will fluctuate so that shares, when redeemed, may be worth more or less than their original cost. Performance for periods less than or equal to one year is cumulative. Performance is for the stated time period only; due to market volatility, current Fund performance may be lower or higher than the quoted return. For performance as of the most recent month-end, please refer to eatonvance.com.

Eaton Vance

Emerging Markets Debt Fund

January 31, 2021

Performance2,3

Portfolio Managers John R. Baur, Michael A. Cirami, CFA and Eric A. Stein, CFA

| | | | | | | | | | | | | | | | | | | | |

| % Average Annual Total Returns | | Class

Inception Date | | | Performance

Inception Date | | | One Year | | | Five Years | | | Since

Inception | |

| | | | | |

Class I at NAV | | | 05/01/2018 | | | | 05/01/2018 | | | | 2.81 | % | | | — | | | | 6.97 | % |

|

| |

| | | | | |

J.P. Morgan Emerging Markets Bond Index (EMBI) Global Diversified | | | — | | | | — | | | | 2.55 | % | | | 6.88 | % | | | 6.45 | % |

| | | | | |

| % Total Annual Operating Expense Ratios4 | | | | | | | | | | | | | | Class I | |

| | | | | |

Gross | | | | | | | | | | | | | | | | | | | 2.73 | % |

Net | | | | | | | | | | | | | | | | | | | 0.85 | |

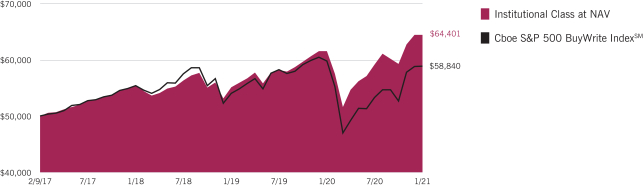

Growth of $250,000

This graph shows the change in value of a hypothetical investment of $250,000 in Class I of the Fund for the period indicated. For comparison, the same investment is shown in the indicated index.

See Endnotes and Additional Disclosures in this report.

Past performance is no guarantee of future results. Returns are historical and are calculated by determining the percentage change in net asset value (NAV) or offering price (as applicable) with all distributions reinvested. Investment return and principal value will fluctuate so that shares, when redeemed, may be worth more or less than their original cost. Performance for periods less than or equal to one year is cumulative. Performance is for the stated time period only; due to market volatility, current Fund performance may be lower or higher than the quoted return. For performance as of the most recent month-end, please refer to eatonvance.com.

Eaton Vance

Emerging Markets Debt Fund

January 31, 2021

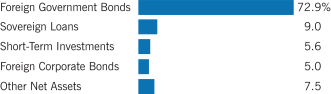

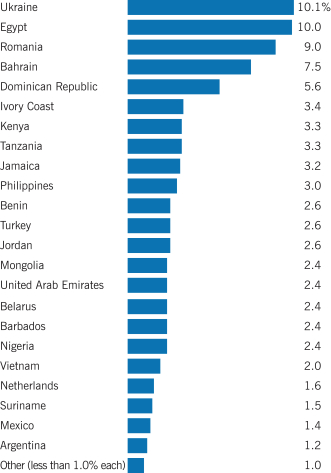

Fund Profile

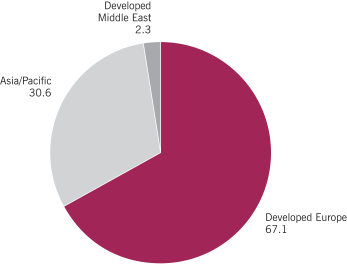

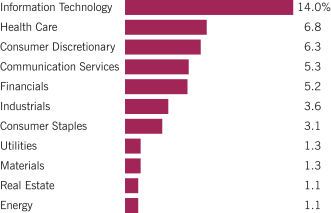

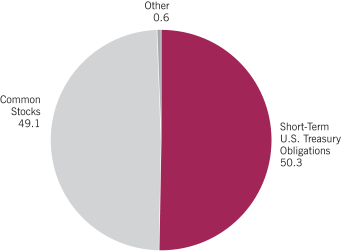

Asset Allocation (% of net assets)5

Country Allocation (% of net assets)6

See Endnotes and Additional Disclosures in this report.

Eaton Vance

Emerging Markets Debt Fund

January 31, 2021

Endnotes and Additional Disclosures

| 1 | The views expressed in this report are those of the portfolio manager(s) and are current only through the date stated at the top of this page. These views are subject to change at any time based upon market or other conditions, and Eaton Vance and the Fund(s) disclaim any responsibility to update such views. These views may not be relied upon as investment advice and, because investment decisions are based on many factors, may not be relied upon as an indication of trading intent on behalf of any Eaton Vance fund. This commentary may contain statements that are not historical facts, referred to as “forward-looking statements.” The Fund’s actual future results may differ significantly from those stated in any forward-looking statement, depending on factors such as changes in securities or financial markets or general economic conditions, the volume of sales and purchases of Fund shares, the continuation of investment advisory, administrative and service contracts, and other risks discussed from time to time in the Fund’s filings with the Securities and Exchange Commission. |

| 2 | J.P. Morgan Emerging Markets Bond Index (EMBI) Global Diversified is a market-cap weighted index that measures USD-denominated Brady Bonds, Eurobonds, and traded loans issued by sovereign entities. Information has been obtained from sources believed to be reliable but J.P. Morgan does not warrant its completeness or accuracy. The Index is used with permission. The Index may not be copied, used, or distributed without J.P. Morgan’s prior written approval. Copyright 2021, J.P. Morgan Chase & Co. All rights reserved. Unless otherwise stated, index returns do not reflect the effect of any applicable sales charges, commissions, expenses, taxes or leverage, as applicable. It is not possible to invest directly in an index. |

| 3 | Class I shares are offered at net asset value (NAV). Total Returns are historical and are calculated by determining the percentage change in NAV with all distributions reinvested. Unless otherwise stated, performance does not reflect the deduction of taxes on Fund distributions or redemptions of Fund shares. Performance since inception for an index, if presented, is the performance since the Fund’s or oldest share class’ inception, as applicable. |

| 4 | Source: Fund prospectus. Net expense ratio reflects a contractual expense reimbursement that continues through 5/31/21. Without the reimbursement, performance would have been lower. The expense ratios for the current reporting period can be found in the Financial Highlights section of this report. |

| 5 | Other Net Assets represents other assets less liabilities and includes any investment type that represents less than 1% of net assets. |

| 6 | Excludes cash and cash equivalents. |

Fund profile subject to change due to active management.

Additional Information

Bloomberg Barclays U.S. Aggregate Bond Index is an unmanaged index of domestic investment-grade bonds, including corporate, government and mortgage-backed securities.

Duration is a measure of the expected change in price of a bond — in percentage terms — given a one percent change in interest rates, all else being constant. Securities with lower durations tend to be less sensitive to interest rate changes.

Important Notice to Shareholders

Effective April 1, 2021, the portfolio management team for the Fund will be John R. Baur and Michael A. Cirami.

Eaton Vance

Emerging Markets Debt Fund

January 31, 2021

Fund Expenses

Example: As a Fund shareholder, you incur two types of costs: (1) transaction costs, including sales charges (loads) on purchases and redemption fees (if applicable); and (2) ongoing costs, including management fees; and other Fund expenses. This Example is intended to help you understand your ongoing costs (in dollars) of Fund investing and to compare these costs with the ongoing costs of investing in other mutual funds. The Example is based on an investment of $1,000 invested at the beginning of the period and held for the entire period (August 1, 2020 – January 31, 2021).

Actual Expenses: The first section of the table below provides information about actual account values and actual expenses. You may use the information in this section, together with the amount you invested, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number in the first section under the heading entitled “Expenses Paid During Period” to estimate the expenses you paid on your account during this period.

Hypothetical Example for Comparison Purposes: The second section of the table below provides information about hypothetical account values and hypothetical expenses based on the actual Fund expense ratio and an assumed rate of return of 5% per year (before expenses), which is not the actual Fund return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing costs of investing in your Fund and other funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of the other funds.

Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any transactional costs, such as sales charges (loads) or redemption fees (if applicable). Therefore, the second section of the table is useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds. In addition, if these transactional costs were included, your costs would be higher.

| | | | | | | | | | | | | | | | |

| | | Beginning

Account Value

(8/1/20) | | | Ending

Account Value

(1/31/21) | | | Expenses Paid

During Period*

(8/1/20 – 1/31/21) | | | Annualized

Expense

Ratio | |

| | | | |

Actual | | | | | | | | | | | | | | | | |

Class I | | $ | 1,000.00 | | | $ | 1,092.50 | | | $ | 4.47 | ** | | | 0.85 | % |

| | | | | |

Hypothetical* | | | | | | | | | | | | | | | | |

(5% return per year before expenses) | | | | | | | | | | | | | | | | |

Class I | | $ | 1,000.00 | | | $ | 1,020.90 | | | $ | 4.32 | ** | | | 0.85 | % |

| * | Expenses are equal to the Fund’s annualized expense ratio for the indicated Class, multiplied by the average account value over the period, multiplied by 184/366 (to reflect the one-half year period). The Example assumes that the $1,000 was invested at the net asset value per share determined at the close of business on July 31, 2020. |

| ** | Absent an allocation of certain expenses to an affiliate, expenses would be higher. |

Eaton Vance

Emerging Markets Debt Fund

January 31, 2021

Portfolio of Investments

| | | | | | | | | | |

| Foreign Corporate Bonds — 5.0% | |

| Security | | | | Principal

Amount*

(000’s omitted) | | | Value | |

|

| Brazil — 1.6% | |

| | | |

Petrobras Global Finance BV, 6.90%, 3/19/49 | | | | | 120 | | | $ | 144,602 | |

| |

Total Brazil | | | $ | 144,602 | |

|

| Mexico — 1.4% | |

| | | |

Petroleos Mexicanos, 6.75%, 9/21/47 | | | | | 142 | | | $ | 124,270 | |

| |

Total Mexico | | | $ | 124,270 | |

|

| Vietnam — 2.0% | |

| | | |

Debt and Asset Trading Corp., 1.00%, 10/10/25(1) | | | | | 200 | | | $ | 175,500 | |

| |

Total Vietnam | | | $ | 175,500 | |

| |

Total Foreign Corporate Bonds

(identified cost $404,406) | | | $ | 444,372 | |

|

| Foreign Government Bonds — 72.9% | |

| Security | | | | Principal

Amount*

(000’s omitted) | | | Value | |

|

| Argentina — 1.2% | |

| | | |

Republic of Argentina, 0.125% to 3/15/21, 7/9/35(2) | | | | | 187 | | | $ | 64,421 | |

| | | |

Republic of Argentina, 0.125% to 3/15/21, 7/9/41(2) | | | | | 43 | | | | 15,695 | |

| | | |

Republic of Argentina, 0.125% to 3/15/21, 7/9/46(2) | | | | | 71 | | | | 24,637 | |

| |

Total Argentina | | | $ | 104,753 | |

|

| Bahrain — 7.5% | |

| | | |

Bahrain Government International Bond, 5.45%, 9/16/32(1) | | | | | 200 | | | $ | 203,648 | |

| | | |

Bahrain Government International Bond, 7.00%, 1/26/26(1) | | | | | 200 | | | | 231,979 | |

| | | |

CBB International Sukuk Programme Co., 6.25%, 11/14/24(1) | | | | | 200 | | | | 221,344 | |

| |

Total Bahrain | | | $ | 656,971 | |

|

| Barbados — 2.4% | |

| | | |

Government of Barbados, 6.50%, 10/1/29(3) | | | | | 206 | | | $ | 207,656 | |

| |

Total Barbados | | | $ | 207,656 | |

|

| Belarus — 2.4% | |

| | | |

Republic of Belarus, 6.875%, 2/28/23(1) | | | | | 200 | | | $ | 208,694 | |

| |

Total Belarus | | | $ | 208,694 | |

|

| Benin — 2.6% | |

| | | |

Benin Government International Bond, 6.875%, 1/19/52(1) | | EUR | | | 180 | | | $ | 231,184 | |

| |

Total Benin | | | $ | 231,184 | |

| | | | | | | | | | |

| Security | | | | Principal

Amount*

(000’s omitted) | | | Value | |

|

| Dominican Republic — 5.6% | |

| | | |

Dominican Republic, 4.50%, 1/30/30(1) | | | | | 220 | | | $ | 230,835 | |

| | | |

Dominican Republic, 5.875%, 1/30/60(1) | | | | | 250 | | | | 263,000 | |

| |

Total Dominican Republic | | | $ | 493,835 | |

|

| Ecuador — 0.7% | |

| | | |

Republic of Ecuador, 0.50% to 6/20/21, 7/31/40(1)(2) | | | | | 182 | | | $ | 62,426 | |

| |

Total Ecuador | | | $ | 62,426 | |

|

| Egypt — 10.0% | |

| | | |

Arab Republic of Egypt, 8.15%, 11/20/59(1) | | | | | 200 | | | $ | 213,244 | |

| | | |

Arab Republic of Egypt, 8.50%, 1/31/47(1) | | | | | 400 | | | | 441,393 | |

| | | |

Arab Republic of Egypt, 8.875%, 5/29/50(1) | | | | | 200 | | | | 227,108 | |

| |

Total Egypt | | | $ | 881,745 | |

|

| Ivory Coast — 3.4% | |

| | | |

Ivory Coast Government International Bond, 4.875%, 1/30/32(1) | | EUR | | | 100 | | | $ | 125,208 | |

| | | |

Ivory Coast Government International Bond, 6.625%, 3/22/48(1) | | EUR | | | 131 | | | | 172,925 | |

| |

Total Ivory Coast | | | $ | 298,133 | |

|

| Jamaica — 3.2% | |

| | | |

Jamaica Government International Bond, 7.875%, 7/28/45 | | | | | 200 | | | $ | 282,500 | |

| |

Total Jamaica | | | $ | 282,500 | |

|

| Jordan — 2.6% | |

| | | |

Jordan Government International Bond, 7.375%, 10/10/47(1) | | | | | 200 | | | $ | 228,453 | |

| |

Total Jordan | | | $ | 228,453 | |

|

| Lebanon — 0.3% | |

| | | |

Lebanese Republic, 6.25%, 11/4/24(1)(4) | | | | | 33 | | | $ | 4,322 | |

| | | |

Lebanese Republic, 6.40%, 5/26/23(4) | | | | | 33 | | | | 4,328 | |

| | | |

Lebanese Republic, 6.65%, 4/22/24(1)(4) | | | | | 33 | | | | 4,363 | |

| | | |

Lebanese Republic, 6.65%, 11/3/28(1)(4) | | | | | 14 | | | | 1,876 | |

| | | |

Lebanese Republic, 6.85%, 3/23/27(1)(4) | | | | | 26 | | | | 3,456 | |

| | | |

Lebanese Republic, 6.85%, 5/25/29(4) | | | | | 45 | | | | 6,007 | |

| | | |

Lebanese Republic, 7.00%, 12/3/24(4) | | | | | 15 | | | | 1,964 | |

| | | |

Lebanese Republic, 7.00%, 3/20/28(1)(4) | | | | | 11 | | | | 1,465 | |

| | | |

Lebanese Republic, 7.05%, 11/2/35(1)(4) | | | | | 5 | | | | 663 | |

| |

Total Lebanon | | | $ | 28,444 | |

| | | | |

| | 8 | | See Notes to Financial Statements. |

Eaton Vance

Emerging Markets Debt Fund

January 31, 2021

Portfolio of Investments — continued

| | | | | | | | | | |

| Security | | | | Principal

Amount*

(000’s omitted) | | | Value | |

|

| Mongolia — 2.4% | |

| | | |

Mongolia Government International Bond, 5.125%, 4/7/26(1) | | | | | 200 | | | $ | 214,484 | |

| |

Total Mongolia | | | $ | 214,484 | |

|

| Philippines — 3.0% | |

| | | |

Republic of the Philippines, 2.95%, 5/5/45 | | | | | 255 | | | $ | 264,761 | |

| |

Total Philippines | | | $ | 264,761 | |

|

| Romania — 9.0% | |

| | | |

Romanian Government International Bond, 2.625%, 12/2/40(1) | | EUR | | | 13 | | | $ | 16,495 | |

| | | |

Romanian Government International Bond, 2.75%, 2/26/26(1) | | EUR | | | 30 | | | | 40,312 | |

| | | |

Romanian Government International Bond, 3.375%, 1/28/50(1) | | EUR | | | 177 | | | | 242,521 | |

| | | |

Romanian Government International Bond, 3.624%, 5/26/30(1) | | EUR | | | 50 | | | | 72,367 | |

| | | |

Romanian Government International Bond, 4.625%, 4/3/49(1) | | EUR | | | 261 | | | | 425,710 | |

| |

Total Romania | | | $ | 797,405 | |

|

| Suriname — 1.5% | |

| | | |

Republic of Suriname, 9.25%, 10/26/26(1) | | | | | 205 | | | $ | 134,623 | |

| |

Total Suriname | | | $ | 134,623 | |

|

| Turkey — 2.6% | |

| | | |

Republic of Turkey, 7.625%, 4/26/29 | | | | | 200 | | | $ | 231,179 | |

| |

Total Turkey | | | $ | 231,179 | |

|

| Ukraine — 10.1% | |

| | | |

Ukraine Government International Bond, 0.00%, GDP-Linked, 5/31/40(1)(3)(5) | | | | | 144 | | | $ | 163,054 | |

| | | |

Ukraine Government International Bond, 9.75%, 11/1/28(1) | | | | | 600 | | | | 729,783 | |

| |

Total Ukraine | | | $ | 892,837 | |

|

| United Arab Emirates — 2.4% | |

| | | |

Abu Dhabi Government International Bond, 3.125%, 9/30/49(1) | | | | | 200 | | | $ | 210,196 | |

| |

Total United Arab Emirates | | | $ | 210,196 | |

| |

Total Foreign Government Bonds

(identified cost $5,811,940) | | | $ | 6,430,279 | |

| | | | | | | | | | |

| Sovereign Loans — 9.0% | |

| Borrower | | | | Principal

Amount

(000’s omitted) | | | Value | |

|

| Kenya — 3.3% | |

| | | |

Government of Kenya, Term Loan, 6.71%, (6 mo. USD LIBOR + 6.45%), Maturing June 29, 2025(6) | | | | $ | 293 | | | $ | 294,984 | |

| |

Total Kenya | | | $ | 294,984 | |

|

| Nigeria — 2.4% | |

| | | |

Bank of Industry Limited, Term Loan, 6.22%, (3 mo. USD LIBOR + 6.00%), Maturing December 14, 2023(6)(7) | | | | $ | 205 | | | $ | 207,334 | |

| |

Total Nigeria | | | $ | 207,334 | |

|

| Tanzania — 3.3% | |

| | | |

Government of the United Republic of Tanzania, Term Loan, 5.46%, (6 mo. USD LIBOR + 5.20%), Maturing May 23, 2023(6) | | | | $ | 286 | | | $ | 288,080 | |

| |

Total Tanzania | | | $ | 288,080 | |

| |

Total Sovereign Loans

(identified cost $781,308) | | | $ | 790,398 | |

|

| Short-Term Investments — 5.6% | |

| Description | | | | Units | | | Value | |

| | | |

Eaton Vance Cash Reserves Fund, LLC, 0.11%(8) | | | | | 499,206 | | | $ | 499,206 | |

| |

Total Short-Term Investments

(identified cost $499,206) | | | $ | 499,206 | |

| |

Total Investments — 92.5%

(identified cost $7,496,860) | | | $ | 8,164,255 | |

| |

Other Assets, Less Liabilities — 7.5% | | | $ | 658,487 | |

| |

Net Assets — 100.0% | | | $ | 8,822,742 | |

The percentage shown for each investment category in the Portfolio of Investments is based on net assets.

| | * | In U.S. dollars unless otherwise indicated. |

| | (1) | Security exempt from registration under Regulation S of the Securities Act of 1933, as amended, which exempts from registration securities offered and sold outside the United States. Security may not be offered or sold in the United States except pursuant to an exemption from, or in a transaction not subject to, the registration requirements of the Securities Act of 1933, as amended. At January 31, 2021, the aggregate value of these securities is $5,502,631 or 62.4% of the Fund’s net assets. |

| | (2) | Step coupon security. Interest rate represents the rate in effect at January 31, 2021. |

| | | | |

| | 9 | | See Notes to Financial Statements. |

Eaton Vance

Emerging Markets Debt Fund

January 31, 2021

Portfolio of Investments — continued

| | (3) | Security exempt from registration under Rule 144A of the Securities Act of 1933, as amended. These securities may be sold in certain transactions in reliance on an exemption from registration (normally to qualified institutional buyers). At January 31, 2021, the aggregate value of these securities is $370,710 or 4.2% of the Fund’s net assets. |

| | (4) | Issuer is in default with respect to interest payments. |

| | (5) | Amounts payable in respect of the security are contingent upon and determined by reference to Ukraine’s GDP and Real GDP Growth Rate. Principal amount represents the notional amount used to calculate payments due to the security holder and does not represent an entitlement for payment. |

| | (6) | Variable rate security. The stated interest rate represents the rate in effect at January 31, 2021. |

| | (7) | Loan is subject to scheduled mandatory prepayments. Maturity date shown reflects the final maturity date. |

| | (8) | Affiliated investment company, available to Eaton Vance portfolios and funds, which invests in high quality, U.S. dollar denominated money market instruments. The rate shown is the annualized seven-day yield as of January 31, 2021. |

| | | | | | | | | | | | | | | | | | | | | | | | | | |

| Centrally Cleared Forward Foreign Currency Exchange Contracts | |

| | | | | |

| Currency Purchased | | | | | | Currency Sold | | | | | | Settlement

Date | | | Value/Unrealized

Appreciation

(Depreciation) | |

| | | | | | | |

| EUR | | | 171,832 | | | | | | | USD | | | 208,759 | | | | | | | | 2/2/21 | | | $ | (232 | ) |

| | | | | | | |

| EUR | | | 130,000 | | | | | | | USD | | | 158,045 | | | | | | | | 2/2/21 | | | | (284 | ) |

| | | | | | | |

| EUR | | | 130,000 | | | | | | | USD | | | 158,029 | | | | | | | | 3/2/21 | | | | (268 | ) |

| | | | | | | |

| USD | | | 157,937 | | | | | | | EUR | | | 130,000 | | | | | | | | 2/2/21 | | | | 176 | |

| | | | | | | |

| USD | | | 208,902 | | | | | | | EUR | | | 171,832 | | | | | | | | 2/2/21 | | | | 376 | |

| | | | | | | |

| USD | | | 208,880 | | | | | | | EUR | | | 171,832 | | | | | | | | 3/2/21 | | | | 226 | |

| | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | | | $ | (6 | ) |

| | | | | | | | | | | | | | | | | | | | | | | | |

| Forward Foreign Currency Exchange Contracts | |

| | | | | |

| Currency Purchased | | | Currency Sold | | | Counterparty | | Settlement

Date | | | Unrealized

Appreciation | | | Unrealized

(Depreciation) | |

| | | | | | | |

| USD | | | 712,749 | | | EUR | | | 578,427 | | | Standard Chartered Bank | | | 2/8/21 | | | $ | 10,710 | | | $ | — | |

| | | | | | | |

| USD | | | 291,470 | | | EUR | | | 236,540 | | | Standard Chartered Bank | | | 2/8/21 | | | | 4,380 | | | | — | |

| | | | | | | |

| USD | | | 171,511 | | | EUR | | | 139,188 | | | Standard Chartered Bank | | | 2/8/21 | | | | 2,577 | | | | — | |

| | | | | | | |

| USD | | | 96,864 | | | EUR | | | 80,000 | | | UBS AG | | | 2/8/21 | | | | — | | | | (232 | ) |

| | | | | | | |

| | | | | | | | | | | | | | | | | | | $ | 17,667 | | | $ | (232 | ) |

| | | | | | | | | | | | | | | | | | | | |

| Futures Contracts | |

| | | | | |

| Description | | Number of

Contracts | | | Position | | | Expiration

Date | | | Notional

Amount | | | Value/Unrealized

Appreciation

(Depreciation) | |

| | | | | |

Interest Rate Futures | | | | | | | | | | | | | | | | | | | | |

| | | | | |

| U.S. Long Treasury Bond | | | 1 | | | | Long | | �� | | 3/22/21 | | | $ | 168,719 | | | $ | (96 | ) |

| | | | | |

| U.S. Ultra-Long Treasury Bond | | | 8 | | | | Long | | | | 3/22/21 | | | | 1,637,750 | | | | (53,424 | ) |

| | | | | |

| Euro-Bobl | | | (1 | ) | | | Short | | | | 3/8/21 | | | | (164,133 | ) | | | 11 | |

| | | | | |

| Euro-Bund | | | (4 | ) | | | Short | | | | 3/8/21 | | | | (860,407 | ) | | | 903 | |

| | | | | |

| | | | | | | | | | | | | | | | | | | $ | (52,606 | ) |

| | | | |

| | 10 | | See Notes to Financial Statements. |

Eaton Vance

Emerging Markets Debt Fund

January 31, 2021

Portfolio of Investments — continued

| | | | | | | | | | | | | | | | | | | | | | | | |

| Centrally Cleared Interest Rate Swaps | | | | | | | | | |

| | | | | | | |

Notional

Amount

(000’s omitted) | | | Fund Pays/

Receives

Floating Rate | | Floating Rate | | Annual Fixed Rate | | Termination

Date | | Value | | | Unamortized

Upfront

Receipts

(Payments) | | | Unrealized

Appreciation

(Depreciation) | |

| | | | | | | | |

| EUR | | | 19 | | | Receives | | 6-month EURIBOR (pays semi-annually) | | 0.37%

(pays annually) | | 2/12/50 | | $ | (1,804 | ) | | $ | — | | | $ | (1,804 | ) |

| | | | | | | | |

| EUR | | | 19 | | | Receives | | 6-month EURIBOR (pays semi-annually) | | 0.39%

(pays annually) | | 2/13/50 | | | (1,866 | ) | | | — | | | | (1,866 | ) |

| | | | | | | | |

| EUR | | | 5 | | | Receives | | 6-month EURIBOR (pays semi-annually) | | 0.38%

(pays annually) | | 2/13/50 | | | (485 | ) | | | — | | | | (485 | ) |

| | | | | | | | |

| EUR | | | 16 | | | Receives | | 6-month EURIBOR (pays semi-annually) | | 0.38%

(pays annually) | | 2/13/50 | | | (1,557 | ) | | | — | | | | (1,557 | ) |

| | | | | | | | |

| EUR | | | 8 | | | Receives | | 6-month EURIBOR (pays semi-annually) | | 0.39%

(pays annually) | | 2/14/50 | | | (814 | ) | | | — | | | | (814 | ) |

| | | | | | | | |

| EUR | | | 7 | | | Receives | | 6-month EURIBOR (pays semi-annually) | | 0.34%

(pays annually) | | 2/20/50 | | | (583 | ) | | | — | | | | (583 | ) |

| | | | | | | | |

| EUR | | | 58 | | | Receives | | 6-month EURIBOR (pays semi-annually) | | 0.32%

(pays annually) | | 2/21/50 | | | (4,392 | ) | | | — | | | | (4,392 | ) |

| | | | | | | | |

| EUR | | | 62 | | | Receives | | 6-month EURIBOR (pays semi-annually) | | 0.26%

(pays annually) | | 2/25/50 | | | (3,375 | ) | | | — | | | | (3,375 | ) |

| | | | | | | | |

| EUR | | | 16 | | | Receives | | 6-month EURIBOR (pays semi-annually) | | 0.21%

(pays annually) | | 2/26/50 | | | (571 | ) | | | — | | | | (571 | ) |

| | | | | | | | |

| EUR | | | 49 | | | Receives | | 6-month EURIBOR (pays semi-annually) | | 0.12%

(pays annually) | | 6/8/50 | | | (104 | ) | | | — | | | | (104 | ) |

| | | | | | | | |

| USD | | | 200 | | | Receives | | 3-month USD-LIBOR (pays quarterly) | | 0.55%

(pays semi-annually) | | 3/12/23 | | | (1,864 | ) | | | — | | | | (1,864 | ) |

| | | | | | | | |

| USD | | | 1,605 | | | Pays | | 3-month USD-LIBOR (pays quarterly) | | 0.61%

(pays semi-annually) | | 3/16/25 | | | 16,734 | | | | — | | | | 16,734 | |

| | | | | | | | |

| USD | | | 169 | | | Receives | | 3-month USD-LIBOR (pays quarterly) | | 0.33%

(pays semi-annually) | | 5/12/25 | | | 601 | | | | — | | | | 601 | |

| | | | | | | | |

| USD | | | 147 | | | Receives | | 3-month USD-LIBOR (pays quarterly) | | 1.74%

(pays semi-annually) | | 12/16/26 | | | (9,586 | ) | | | — | | | | (9,586 | ) |

| | | | | | | | |

| USD | | | 140 | | | Receives | | 3-month USD-LIBOR (pays quarterly) | | 0.57%

(pays semi-annually) | | 4/17/27 | | | 928 | | | | — | | | | 928 | |

| | | | | | | | |

| USD | | | 209 | | | Pays | | 3-month USD-LIBOR (pays quarterly) | | 2.34%

(pays semi-annually) | | 5/17/29 | | | 24,230 | | | | — | | | | 24,230 | |

| | | | | | | | |

| USD | | | 438 | | | Receives | | 3-month USD-LIBOR (pays quarterly) | | 2.09%

(pays semi-annually) | | 7/15/29 | | | (40,367 | ) | | | 126 | | | | (40,241 | ) |

| | | | | | | | |

| USD | | | 150 | | | Receives | | 3-month USD-LIBOR (pays quarterly) | | 0.69%

(pays semi-annually) | | 4/17/30 | | | 4,576 | | | | — | | | | 4,576 | |

| | | | | | | | |

| USD | | | 10 | | | Receives | | 3-month USD-LIBOR (pays quarterly) | | 0.74%

(pays semi-annually) | | 6/18/30 | | | 296 | | | | — | | | | 296 | |

| | | | | | | | |

| USD | | | 95 | | | Receives | | 3-month USD-LIBOR (pays quarterly) | | 2.88%

(pays semi-annually) | | 1/31/49 | | | (28,979 | ) | | | (47 | ) | | | (29,026 | ) |

| | | | |

| | 11 | | See Notes to Financial Statements. |

Eaton Vance

Emerging Markets Debt Fund

January 31, 2021

Portfolio of Investments — continued

| | | | | | | | | | | | | | | | | | | | | | | | |

| Centrally Cleared Interest Rate Swaps (continued) | | | | | | | | | |

| | | | | | | |

Notional

Amount

(000’s omitted) | | | Fund Pays/

Receives

Floating Rate | | Floating Rate | | Annual Fixed Rate | | Termination

Date | | Value | | | Unamortized

Upfront

Receipts

(Payments) | | | Unrealized

Appreciation

(Depreciation) | |

| | | | | | | | |

| USD | | | 121 | | | Receives | | 3-month USD-LIBOR (pays quarterly) | | 2.54% (pays semi-annually) | | 5/17/49 | | $ | (28,048 | ) | | $ | 14,178 | | | $ | (13,870 | ) |

| | | | | | | | |

| USD | | | 99 | | | Receives | | 3-month USD-LIBOR (pays quarterly) | | 1.65%

(pays semi-annually) | | 9/9/49 | | | (1,940 | ) | | | — | | | | (1,940 | ) |

| | | | | | | | |

| USD | | | 7 | | | Receives | | 3-month USD-LIBOR (pays quarterly) | | 1.70%

(pays semi-annually) | | 9/12/49 | | | (219 | ) | | | — | | | | (219 | ) |

| | | | | | | | |

| USD | | | 110 | | | Receives | | 3-month USD-LIBOR (pays quarterly) | | 1.87%

(pays semi-annually) | | 10/25/49 | | | (7,910 | ) | | | — | | | | (7,910 | ) |

| | | | | | | | |

| USD | | | 37 | | | Receives | | 3-month USD-LIBOR (pays quarterly) | | 1.97%

(pays semi-annually) | | 11/15/49 | | | (3,493 | ) | | | — | | | | (3,493 | ) |

| | | | | | | | |

| USD | | | 130 | | | Receives | | 3-month USD-LIBOR (pays quarterly) | | 0.84%

(pays semi-annually) | | 3/30/50 | | | 23,649 | | | | — | | | | 23,649 | |

| | | | | | | | |

| USD | | | 160 | | | Receives | | 3-month USD-LIBOR (pays quarterly) | | 0.83%

(pays semi-annually) | | 4/29/50 | | | 29,725 | | | | — | | | | 29,725 | |

| | | | | | | | |

| USD | | | 50 | | | Receives | | 3-month USD-LIBOR (pays quarterly) | | 0.93%

(pays semi-annually) | | 5/26/50 | | | 8,102 | | | | — | | | | 8,102 | |

| | | | | | | | |

| USD | | | 100 | | | Receives | | 3-month USD-LIBOR (pays quarterly) | | 0.97%

(pays semi-annually) | | 6/17/50 | | | 15,272 | | | | — | | | | 15,272 | |

| | | | | | | | |

Total | | | | | | | | | | | | | | $ | (13,844 | ) | | $ | 14,257 | | | $ | 413 | |

| | | | | | | | | | | | | | | | | | | | | | | | |

| Centrally Cleared Credit Default Swaps — Sell Protection | |

| | | | | | | |

| Reference Entity | | Notional

Amount*

(000’s omitted) | | | Contract Annual

Fixed Rate** | | Termination

Date | | Current

Market Annual

Fixed Rate*** | | | Value | | | Unamortized

Upfront

Receipts

(Payments) | | | Unrealized

Appreciation (Depreciation) | |

| | | | | | | |

| Brazil | | $ | 130 | | | 1.00% (pays quarterly)(1) | | 12/20/25 | | | 1.72 | % | | $ | (4,298 | ) | | $ | 6,787 | | | $ | 2,489 | |

| | | | | | | |

| Colombia | | | 275 | | | 1.00% (pays quarterly)(1) | | 12/20/25 | | | 1.13 | | | | (1,359 | ) | | | 4,175 | | | | 2,816 | |

| | | | | | | |

| Indonesia | | | 320 | | | 1.00% (pays quarterly)(1) | | 12/20/25 | | | 0.76 | | | | 4,055 | | | | — | | | | 4,055 | |

| | | | | | | |

| Mexico | | | 290 | | | 1.00% (pays quarterly)(1) | | 12/20/30 | | | 1.56 | | | | (14,278 | ) | | | 14,658 | | | | 380 | |

| | | | | | | |

| South Africa | | | 150 | | | 1.00% (pays quarterly)(1) | | 6/20/21 | | | 0.50 | | | | 477 | | | | 685 | | | | 1,162 | |

| | | | | | | |

| Turkey | | | 137 | | | 1.00% (pays quarterly)(1) | | 6/20/21 | | | 1.35 | | | | (26 | ) | | | 2,540 | | | | 2,514 | |

| | | | |

| | 12 | | See Notes to Financial Statements. |

Eaton Vance

Emerging Markets Debt Fund

January 31, 2021

Portfolio of Investments — continued

| | | | | | | | | | | | | | | | | | | | | | | | |

| Centrally Cleared Credit Default Swaps — Sell Protection (continued) | |

| | | | | | | |

| Reference Entity | | Notional

Amount*

(000’s omitted) | | | Contract Annual

Fixed Rate** | | Termination

Date | | Current

Market Annual

Fixed Rate*** | | | Value | | | Unamortized

Upfront

Receipts

(Payments) | | | Unrealized

Appreciation (Depreciation) | |

| | | | | | | |

| Turkey | | $ | 90 | | | 1.00% (pays quarterly)(1) | | 6/20/25 | | | 2.98 | % | | $ | (7,210 | ) | | $ | 14,122 | | | $ | 6,912 | |

| | | | | | | |

Total | | $ | 1,392 | | | | | | | | | | | $ | (22,639 | ) | | $ | 42,967 | | | $ | 20,328 | |

| * | If the Fund is the seller of credit protection, the notional amount is the maximum potential amount of future payments the Fund could be required to make if a credit event, as defined in the credit default swap agreement, were to occur. At January 31, 2021, such maximum potential amount for all open credit default swaps in which the Fund is the seller was $1,392,000. |

| ** | The contract annual fixed rate represents the fixed rate of interest received by the Fund (as a seller of protection) on the notional amount of the credit default swap contract. |

| *** | Current market annual fixed rates, utilized in determining the net unrealized appreciation or depreciation as of period end, serve as an indicator of the market’s perception of the current status of the payment/performance risk associated with the credit derivative. The current market annual fixed rate of a particular reference entity reflects the cost, as quoted by the pricing vendor, of selling protection against default of that entity as of period end and may include upfront payments required to be made to enter into the agreement. The higher the fixed rate, the greater the market perceived risk of a credit event involving the reference entity. A rate identified as “Defaulted” indicates a credit event has occurred for the reference entity. |

| (1) | Upfront payment is exchanged with the counterparty as a result of the standardized trading coupon. |

Abbreviations:

| | | | |

| | |

| EURIBOR | | – | | Euro Interbank Offered Rate |

| | |

| GDP | | – | | Gross Domestic Product |

| | |

| LIBOR | | – | | London Interbank Offered Rate |

Currency Abbreviations:

| | | | |

| | |

| EUR | | – | | Euro |

| | |

| USD | | – | | United States Dollar |

| | | | |

| | 13 | | See Notes to Financial Statements. |

Eaton Vance

Emerging Markets Debt Fund

January 31, 2021

Statement of Assets and Liabilities

| | | | |

| Assets | | January 31, 2021 | |

| |

Unaffiliated investments, at value (identified cost, $6,997,654) | | $ | 7,665,049 | |

| |

Affiliated investment, at value (identified cost, $499,206) | | | 499,206 | |

| |

Deposits for derivatives collateral — | | | | |

| |

Financial futures contracts | | | 81,673 | |

| |

Centrally cleared derivatives | | | 491,743 | |

| |

Foreign currency, at value (identified cost, $41,238) | | | 41,191 | |

| |

Interest receivable | | | 138,721 | |

| |

Dividends receivable from affiliated investment | | | 28 | |

| |

Receivable for investments sold | | | 591,908 | |

| |

Receivable for variation margin on open centrally cleared derivatives | | | 11,401 | |

| |

Receivable for open forward foreign currency exchange contracts | | | 17,667 | |

| |

Receivable from affiliate | | | 5,319 | |

| |

Total assets | | $ | 9,543,906 | |

|

| Liabilities | |

| |

Payable for investments purchased | | $ | 394,913 | |

| |

Payable for variation margin on open financial futures contracts | | | 9,912 | |

| |

Payable for open forward foreign currency exchange contracts | | | 232 | |

| |

Due to custodian | | | 204,998 | |

| |

Payable to affiliate: | | | | |

| |

Investment adviser and administration fee | | | 4,890 | |

| |

Accrued expenses | | | 106,219 | |

| |

Total liabilities | | $ | 721,164 | |

| |

Net Assets | | $ | 8,822,742 | |

|

| Sources of Net Assets | |

| |

Paid-in capital | | $ | 8,620,718 | |

| |

Distributable earnings | | | 202,024 | |

| |

Total | | $ | 8,822,742 | |

|

| Class I Shares | |

| |

Net Assets | | $ | 8,822,742 | |

| |

Shares Outstanding | | | 852,310 | |

| |

Net Asset Value, Offering Price and Redemption Price Per Share | | | | |

| |

(net assets ÷ shares of beneficial interest outstanding) | | $ | 10.35 | |

| | | | |

| | 14 | | See Notes to Financial Statements. |

Eaton Vance

Emerging Markets Debt Fund

January 31, 2021

Statement of Operations

| | | | |

| Investment Income | | Year Ended January 31, 2021 | |

| |

Interest | | $ | 480,012 | |

| |

Dividends from affiliated investment | | | 2,634 | |

| |

Total investment income | | $ | 482,646 | |

| |

| Expenses | | | | |

| |

Investment adviser and administration fee | | $ | 54,610 | |

| |

Trustees’ fees and expenses | | | 937 | |

| |

Custodian fee | | | 94,481 | |

| |

Transfer and dividend disbursing agent fees | | | 478 | |

| |

Legal and accounting services | | | 60,827 | |

| |

Printing and postage | | | 12,493 | |

| |

Registration fees | | | 23,784 | |

| |

Interest expense | | | 754 | |

| |

Miscellaneous | | | 11,122 | |

| |

Total expenses | | $ | 259,486 | |

| |

Deduct — | | | | |

| |

Allocation of expenses to affiliate | | $ | 187,115 | |

| |

Total expense reductions | | $ | 187,115 | |

| |

Net expenses | | $ | 72,371 | |

| |

Net investment income | | $ | 410,275 | |

| |

| Realized and Unrealized Gain (Loss) | | | | |

| |

Net realized gain (loss) — | | | | |

| |

Investment transactions | | $ | (461,640 | ) |

| |

Investment transactions — affiliated investment | | | (19 | ) |

| |

Financial futures contracts | | | 484,385 | |

| |

Swap contracts | | | (280,332 | ) |

| |

Foreign currency transactions | | | (3,760 | ) |

| |

Forward foreign currency exchange contracts | | | (101,078 | ) |

| |

Net realized loss | | $ | (362,444 | ) |

| |

Change in unrealized appreciation (depreciation) — | | | | |

| |

Investments | | $ | 85,571 | |

| |

Investments — affiliated investment | | | (35 | ) |

| |

Financial futures contracts | | | (144,808 | ) |

| |

Swap contracts | | | 140,921 | |

| |

Foreign currency | | | 372 | |

| |

Forward foreign currency exchange contracts | | | 17,100 | |

| |

Net change in unrealized appreciation (depreciation) | | $ | 99,121 | |

| |

Net realized and unrealized loss | | $ | (263,323 | ) |

| |

Net increase in net assets from operations | | $ | 146,952 | |

| | | | |

| | 15 | | See Notes to Financial Statements. |

Eaton Vance

Emerging Markets Debt Fund

January 31, 2021

Statements of Changes in Net Assets

| | | | | | | | |

| | | Year Ended January 31, | |

| Increase (Decrease) in Net Assets | | 2021 | | | 2020 | |

| | |

From operations — | | | | | | | | |

| | |

Net investment income | | $ | 410,275 | | | $ | 421,165 | |

| | |

Net realized gain (loss) | | | (362,444 | ) | | | 40,324 | |

| | |

Net change in unrealized appreciation (depreciation) | | | 99,121 | | | | 728,203 | |

| | |

Net increase in net assets from operations | | $ | 146,952 | | | $ | 1,189,692 | |

| | |

Distributions to shareholders — | | | | | | | | |

| | |

Class I | | $ | (446,396 | ) | | $ | (562,574 | ) |

| | |

Total distributions to shareholders | | $ | (446,396 | ) | | $ | (562,574 | ) |

| | |

Transactions in shares of beneficial interest — | | | | | | | | |

| | |

Proceeds from sale of shares | | $ | 1,796,027 | | | $ | 23,743 | |

| | |

Net asset value of shares issued to shareholders in payment of distributions declared | | | 32,636 | | | | 654 | |

| | |

Cost of shares redeemed | | | (1,236,464 | ) | | | — | |

| | |

Net increase in net assets from Fund share transactions | | $ | 592,199 | | | $ | 24,397 | |

| | |

Net increase in net assets | | $ | 292,755 | | | $ | 651,515 | |

|

| Net Assets | |

| | |

At beginning of year | | $ | 8,529,987 | | | $ | 7,878,472 | |

| | |

At end of year | | $ | 8,822,742 | | | $ | 8,529,987 | |

| | | | |

| | 16 | | See Notes to Financial Statements. |

Eaton Vance

Emerging Markets Debt Fund

January 31, 2021

Financial Highlights

| | | | | | | | | | | | |

| | | Class I | |

| | | Year Ended January 31, | | | Period Ended

January 31, 2019(1) | |

| | | 2021 | | | 2020 | |

| | | | |

Net asset value — Beginning of period | | $ | 10.620 | | | $ | 9.840 | | | $ | 10.000 | |

| | | |

| Income (Loss) From Operations | | | | | | | | | | | | |

| | | |

Net investment income(2) | | $ | 0.476 | | | $ | 0.526 | | | $ | 0.286 | |

| | | |

Net realized and unrealized gain (loss) | | | (0.229 | ) | | | 0.956 | | | | (0.151 | ) |

| | | |

Total income from operations | | $ | 0.247 | | | $ | 1.482 | | | $ | 0.135 | |

| | | |

| Less Distributions | | | | | | | | | | | | |

| | | |

From net investment income | | $ | (0.517 | ) | | $ | (0.577 | ) | | $ | (0.219 | ) |

| | | |

From net realized gain | | | — | | | | (0.125 | ) | | | (0.076 | ) |

| | | |

Total distributions | | $ | (0.517 | ) | | $ | (0.702 | ) | | $ | (0.295 | ) |

| | | |

Net asset value — End of period | | $ | 10.350 | | | $ | 10.620 | | | $ | 9.840 | |

| | | |

Total Return(3)(4) | | | 2.81 | % | | | 15.57 | % | | | 1.34 | %(5) |

| | | |

| Ratios/Supplemental Data | | | | | | | | | | | | |

| | | |

Net assets, end of period (000’s omitted) | | $ | 8,823 | | | $ | 8,530 | | | $ | 7,878 | |

| | | |

Ratios (as a percentage of average daily net assets): | | | | | | | | | | | | |

| | | |

Expenses(4) | | | 0.86 | %(6) | | | 0.85 | % | | | 0.85 | %(7) |

| | | |

Net investment income | | | 4.88 | % | | | 5.12 | % | | | 3.92 | %(7) |

| | | |

Portfolio Turnover | | | 220 | % | | | 187 | % | | | 82 | %(5) |

| (1) | For the period from the start of business, May 1, 2018, to January 31, 2019. |

| (2) | Computed using average shares outstanding. |

| (3) | Returns are historical and are calculated by determining the percentage change in net asset value with all distributions reinvested. |

| (4) | The investment adviser and administrator reimbursed certain operating expenses (equal to 2.23%, 1.88% and 2.24% of average daily net assets for the years ended January 31, 2021, 2020 and the period ended January 31, 2019, respectively). Absent this reimbursement, total return would be lower. |

| (6) | Includes interest expense of 0.01% for the year ended January 31, 2021. |

| | | | |

| | 17 | | See Notes to Financial Statements. |

Eaton Vance

Emerging Markets Debt Fund

January 31, 2021

Notes to Financial Statements

1 Significant Accounting Policies

Eaton Vance Emerging Markets Debt Fund (the Fund) is a non-diversified series of Eaton Vance Mutual Funds Trust (the Trust). The Trust is a Massachusetts business trust registered under the Investment Company Act of 1940, as amended (the 1940 Act), as an open-end management investment company. The Fund’s investment objective is total return. The Fund offers Class I shares, which are sold at net asset value and are not subject to a sales charge.

The following is a summary of significant accounting policies of the Fund. The policies are in conformity with accounting principles generally accepted in the United States of America (U.S. GAAP). The Fund is an investment company and follows accounting and reporting guidance in the Financial Accounting Standards Board (FASB) Accounting Standards Codification Topic 946.

A Investment Valuation — The following methodologies are used to determine the market value or fair value of investments.

Debt Obligations. Debt obligations are generally valued on the basis of valuations provided by third party pricing services, as derived from such services’ pricing models. Inputs to the models may include, but are not limited to, reported trades, executable bid and ask prices, broker/dealer quotations, prices or yields of securities with similar characteristics, interest rates, anticipated prepayments, benchmark curves or information pertaining to the issuer, as well as industry and economic events. The pricing services may use a matrix approach, which considers information regarding securities with similar characteristics to determine the valuation for a security. Short-term debt obligations purchased with a remaining maturity of sixty days or less for which a valuation from a third party pricing service is not readily available may be valued at amortized cost, which approximates fair value.

Derivatives. Financial futures contracts are valued at the closing settlement price established by the board of trade or exchange on which they are traded. Forward foreign currency exchange contracts are generally valued at the mean of the average bid and average ask prices that are reported by currency dealers to a third party pricing service at the valuation time. Such third party pricing service valuations are supplied for specific settlement periods and the Fund’s forward foreign currency exchange contracts are valued at an interpolated rate between the closest preceding and subsequent settlement period reported by the third party pricing service. Swaps are normally valued using valuations provided by a third party pricing service. Such pricing service valuations are based on the present value of fixed and projected floating rate cash flows over the term of the swap contract, and in the case of credit default swaps, based on credit spread quotations obtained from broker/dealers and expected default recovery rates determined by the pricing service using proprietary models. Future cash flows on swaps are discounted to their present value using swap rates provided by electronic data services or by broker/dealers.

Foreign Securities and Currencies. Foreign securities and currencies are valued in U.S. dollars, based on foreign currency exchange rate quotations supplied by a third party pricing service. The pricing service uses a proprietary model to determine the exchange rate. Inputs to the model include reported trades and implied bid/ask spreads.

Affiliated Fund. The Fund may invest in Eaton Vance Cash Reserves Fund, LLC (Cash Reserves Fund), an affiliated investment company managed by Eaton Vance Management (EVM). While Cash Reserves Fund is not a registered money market mutual fund, it conducts all of its investment activities in accordance with the requirements of Rule 2a-7 under the 1940 Act. Investments in Cash Reserves Fund are valued at the closing net asset value per unit on the valuation day. Cash Reserves Fund generally values its investment securities based on available market quotations provided by a third party pricing service.

Fair Valuation. Investments for which valuations or market quotations are not readily available or are deemed unreliable are valued at fair value using methods determined in good faith by or at the direction of the Trustees of the Fund in a manner that most fairly reflects the security’s “fair value”, which is the amount that the Fund might reasonably expect to receive for the security upon its current sale in the ordinary course. Each such determination is based on a consideration of relevant factors, which are likely to vary from one pricing context to another. These factors may include, but are not limited to, the type of security, the existence of any contractual restrictions on the security’s disposition, the price and extent of public trading in similar securities of the issuer or of comparable companies or entities, quotations or relevant information obtained from broker/dealers or other market participants, information obtained from the issuer, analysts, and/or the appropriate stock exchange (for exchange-traded securities), an analysis of the company’s or entity’s financial statements, and an evaluation of the forces that influence the issuer and the market(s) in which the security is purchased and sold.

B Investment Transactions — Investment transactions for financial statement purposes are accounted for on a trade date basis. Realized gains and losses on investments sold are determined on the basis of identified cost.

C Income — Interest income is recorded on the basis of interest accrued, adjusted for amortization of premium or accretion of discount. Dividend income is recorded on the ex-dividend date for dividends received in cash and/or securities.

D Federal Taxes — The Fund’s policy is to comply with the provisions of the Internal Revenue Code applicable to regulated investment companies and to distribute to shareholders each year substantially all of its net investment income, and all or substantially all of its net realized capital gains. Accordingly, no provision for federal income or excise tax is necessary.

As of January 31, 2021, the Fund had no uncertain tax positions that would require financial statement recognition, de-recognition, or disclosure. The Fund files a U.S. federal income tax return annually after its fiscal year-end, which is subject to examination by the Internal Revenue Service for a period of three years from the date of filing.

Eaton Vance

Emerging Markets Debt Fund

January 31, 2021

Notes to Financial Statements — continued

E Foreign Currency Translation — Investment valuations, other assets, and liabilities initially expressed in foreign currencies are translated each business day into U.S. dollars based upon current exchange rates. Purchases and sales of foreign investment securities and income and expenses denominated in foreign currencies are translated into U.S. dollars based upon currency exchange rates in effect on the respective dates of such transactions. Recognized gains or losses on investment transactions attributable to changes in foreign currency exchange rates are recorded for financial statement purposes as net realized gains and losses on investments. That portion of unrealized gains and losses on investments that results from fluctuations in foreign currency exchange rates is not separately disclosed.

F Unfunded Loan Commitments — The Fund may enter into certain loan agreements all or a portion of which may be unfunded. The Fund is obligated to fund these commitments at the borrower’s discretion. These commitments, if any, are disclosed in the accompanying Portfolio of Investments.

G Use of Estimates — The preparation of the financial statements in conformity with U.S. GAAP requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities at the date of the financial statements and the reported amounts of income and expense during the reporting period. Actual results could differ from those estimates.

H Indemnifications — Under the Trust’s organizational documents, its officers and Trustees may be indemnified against certain liabilities and expenses arising out of the performance of their duties to the Fund. Under Massachusetts law, if certain conditions prevail, shareholders of a Massachusetts business trust (such as the Trust) could be deemed to have personal liability for the obligations of the Trust. However, the Trust’s Declaration of Trust contains an express disclaimer of liability on the part of Fund shareholders and the By-laws provide that the Trust shall assume, upon request by the shareholder, the defense on behalf of any Fund shareholders. Moreover, the By-laws also provide for indemnification out of Fund property of any shareholder held personally liable solely by reason of being or having been a shareholder for all loss or expense arising from such liability. Additionally, in the normal course of business, the Fund enters into agreements with service providers that may contain indemnification clauses. The Fund’s maximum exposure under these arrangements is unknown as this would involve future claims that may be made against the Fund that have not yet occurred.

I Financial Futures Contracts — Upon entering into a financial futures contract, the Fund is required to deposit with the broker, either in cash or securities, an amount equal to a certain percentage of the contract amount (initial margin). Subsequent payments, known as variation margin, are made or received by the Fund each business day, depending on the daily fluctuations in the value of the underlying security, and are recorded as unrealized gains or losses by the Fund. Gains (losses) are realized upon the expiration or closing of the financial futures contracts. Should market conditions change unexpectedly, the Fund may not achieve the anticipated benefits of the financial futures contracts and may realize a loss. Futures contracts have minimal counterparty risk as they are exchange traded and the clearinghouse for the exchange is substituted as the counterparty, guaranteeing counterparty performance.

J Forward Foreign Currency Exchange Contracts — The Fund may enter into forward foreign currency exchange contracts for the purchase or sale of a specific foreign currency at a fixed price on a future date. The forward foreign currency exchange contracts are adjusted by the daily exchange rate of the underlying currency and any gains or losses are recorded as unrealized until such time as the contracts have been closed. While forward foreign currency exchange contracts are privately negotiated agreements between the Fund and a counterparty, certain contracts may be “centrally cleared”, whereby all payments made or received by the Fund pursuant to the contract are with a central clearing party (CCP) rather than the original counterparty. The CCP guarantees the performance of the original parties to the contract. Upon entering into centrally cleared contracts, the Fund is required to deposit with the CCP, either in cash or securities, an amount of initial margin determined by the CCP, which is subject to adjustment. For centrally cleared contracts, the daily change in valuation is recorded as a receivable or payable for variation margin and settled in cash with the CCP daily. Risks may arise upon entering these contracts from the potential inability of counterparties to meet the terms of their contracts and from movements in the value of a foreign currency relative to the U.S. dollar. In the case of centrally cleared contracts, counterparty risk is minimal due to protections provided by the CCP.

K Interest Rate Swaps — Pursuant to interest rate swap agreements, the Fund either makes floating-rate payments to the counterparty (or CCP in the case of centrally cleared swaps) based on a benchmark interest rate in exchange for fixed-rate payments or the Fund makes fixed-rate payments to the counterparty (or CCP in the case of a centrally cleared swap) in exchange for payments on a floating benchmark interest rate. Payments received or made, including amortization of upfront payments/receipts, are recorded as realized gains or losses. During the term of the outstanding swap agreement, changes in the underlying value of the swap are recorded as unrealized gains or losses. For centrally cleared swaps, the daily change in valuation is recorded as a receivable or payable for variation margin and settled in cash with the CCP daily. The value of the swap is determined by changes in the relationship between two rates of interest. The Fund is exposed to credit loss in the event of non-performance by the swap counterparty. In the case of centrally cleared swaps, counterparty risk is minimal due to protections provided by the CCP. Risk may also arise from movements in interest rates.

L Credit Default Swaps — When the Fund is the buyer of a credit default swap contract, the Fund is entitled to receive the par (or other agreed-upon) value of a referenced debt obligation (or basket of debt obligations) from the counterparty (or CCP in the case of a centrally cleared swap) to the contract if a credit event by a third party, such as a U.S. or foreign corporate issuer or sovereign issuer, on the debt obligation occurs. In return, the Fund pays the counterparty a periodic stream of payments over the term of the contract provided that no credit event has occurred. If no credit event occurs, the Fund would have spent the stream of payments and received no proceeds from the contract. When the Fund is the seller of a credit default swap contract, it receives the stream of payments, but is obligated to pay to the buyer of the protection an amount up to the notional amount of the swap and in certain instances take delivery of securities of the reference entity upon the occurrence of a credit event, as defined under the terms of that particular swap agreement. Credit events are contract specific but may include bankruptcy, failure to pay, restructuring, obligation acceleration and repudiation/moratorium. If the Fund is a seller of protection and a credit event occurs, the maximum potential amount of future payments that the Fund could be required to make would be an amount equal to the notional amount of the agreement. This potential amount would be partially offset by any recovery value

Eaton Vance

Emerging Markets Debt Fund

January 31, 2021

Notes to Financial Statements — continued

of the respective referenced obligation, or net amount received from the settlement of a buy protection credit default swap agreement entered into by the Fund for the same referenced obligation. As the seller, the Fund may create economic leverage to its portfolio because, in addition to its total net assets, the Fund is subject to investment exposure on the notional amount of the swap. The interest fee paid or received on the swap contract, which is based on a specified interest rate on a fixed notional amount, is accrued daily as a component of unrealized appreciation (depreciation) and is recorded as realized gain upon receipt or realized loss upon payment. The Fund also records an increase or decrease to unrealized appreciation (depreciation) in an amount equal to the daily valuation. For centrally cleared swaps, the daily change in valuation is recorded as a receivable or payable for variation margin and settled in cash with the CCP daily. For financial reporting purposes, unamortized upfront payments or receipts, if any, are netted with unrealized appreciation or depreciation on swap contracts to determine the market value of swaps as presented in Notes 6 and 10. The Fund segregates assets in the form of cash or liquid securities in an amount equal to the notional amount of the credit default swaps of which it is the seller. The Fund segregates assets in the form of cash or liquid securities in an amount equal to any unrealized depreciation of the credit default swaps of which it is the buyer, marked-to-market on a daily basis. These transactions involve certain risks, including the risk that the seller may be unable to fulfill the transaction. In the case of centrally cleared swaps, counterparty risk is minimal due to protections provided by the CCP.

2 Distributions to Shareholders and Income Tax Information

It is the present policy of the Fund to make monthly distributions of all or substantially all of its net investment income and to distribute annually all or substantially all of its net realized capital gains. Distributions to shareholders are recorded on the ex-dividend date. Shareholders may reinvest income and capital gain distributions in additional shares of the Fund at the net asset value as of the ex-dividend date or, at the election of the shareholder, receive distributions in cash. Distributions to shareholders are determined in accordance with income tax regulations, which may differ from U.S. GAAP. As required by U.S. GAAP, only distributions in excess of tax basis earnings and profits are reported in the financial statements as a return of capital. Permanent differences between book and tax accounting relating to distributions are reclassified to paid-in capital. For tax purposes, distributions from short-term capital gains are considered to be from ordinary income.

The tax character of distributions declared for the years ended January 31, 2021 and January 31, 2020 was as follows:

| | | | | | | | |

| | | Year Ended January 31, | |

| | | 2021 | | | 2020 | |

| | |

Ordinary income | | $ | 446,396 | | | $ | 510,625 | |

| | |

Long-term capital gains | | $ | — | | | $ | 51,949 | |

As of January 31, 2021, the components of distributable earnings (accumulated loss) on a tax basis were as follows:

| | | | |

| | |

Undistributed ordinary income | | $ | 13,564 | |

| |

Deferred capital losses | | $ | (410,899 | ) |

| |

Net unrealized appreciation | | $ | 599,359 | |

At January 31, 2021, the Fund, for federal income tax purposes, had deferred capital losses of $410,899 which would reduce its taxable income arising from future net realized gains on investment transactions, if any, to the extent permitted by the Internal Revenue Code, and thus would reduce the amount of distributions to shareholders, which would otherwise be necessary to relieve the Fund of any liability for federal income or excise tax. The deferred capital losses are treated as arising on the first day of the Fund’s next taxable year and retain the same short-term or long-term character as when originally deferred. Of the deferred capital losses at January 31, 2021, $410,899 are short-term.

The cost and unrealized appreciation (depreciation) of investments, including open derivative contracts, of the Fund at January 31, 2021, as determined on a federal income tax basis, were as follows:

| | | | |

| |

Aggregate cost | | $ | 7,581,269 | |

| |

Gross unrealized appreciation | | $ | 657,666 | |

| |

Gross unrealized depreciation | | | (58,985 | ) |

| |

Net unrealized appreciation | | $ | 598,681 | |

Eaton Vance

Emerging Markets Debt Fund

January 31, 2021

Notes to Financial Statements — continued

3 Investment Adviser and Administration Fee and Other Transactions with Affiliates

The investment adviser and administration fee is earned by EVM, a wholly-owned subsidiary of Eaton Vance Corp., as compensation for investment advisory and administrative services rendered to the Fund. The fee is computed at an annual rate of 0.65% of the Fund’s average daily net assets up to $500 million and is payable monthly. On net assets of $500 million and over, the annual fee is reduced. For the year ended January 31, 2021, the investment adviser and administration fee amounted to $54,610 or 0.65% of the Fund’s average daily net assets. The Fund invests its cash in Cash Reserves Fund. EVM does not currently receive a fee for advisory services provided to Cash Reserves Fund.

EVM has agreed to reimburse the Fund’s expenses to the extent that total annual operating expenses (relating to ordinary operating expenses only and excluding such expenses as borrowing costs, taxes or litigation expenses) exceed 0.85% of the Fund’s average daily net assets for Class I. This agreement may be changed or terminated after May 31, 2021. Pursuant to this agreement, EVM was allocated $187,115 of the Fund’s operating expenses for the year ended January 31, 2021.

EVM provides sub-transfer agency and related services to the Fund pursuant to a Sub-Transfer Agency Support Services Agreement. For the year ended January 31, 2021, EVM earned $120 from the Fund pursuant to such agreement, which is included in transfer and dividend disbursing agent fees on the Statement of Operations.

Trustees and officers of the Fund who are members of EVM’s organization receive remuneration for their services to the Fund out of the investment adviser and administration fee. Trustees of the Fund who are not affiliated with EVM may elect to defer receipt of all or a percentage of their annual fees in accordance with the terms of the Trustees Deferred Compensation Plan. For the year ended January 31, 2021, no significant amounts have been deferred. Certain officers and Trustees of the Fund are officers of EVM.

4 Purchases and Sales of Investments

Purchases and sales of investments, other than short-term obligations, aggregated $16,608,344 and $15,980,675, respectively, for the year ended January 31, 2021.

5 Shares of Beneficial Interest

The Trust’s Declaration of Trust permits the Trustees to issue an unlimited number of full and fractional shares of beneficial interest (without par value) in one or more series (such as the Fund). Transactions in Fund shares were as follows:

| | | | | | | | |

| | | Year Ended January 31, | |

| | | 2021 | | | 2020 | |

| | |

Sales | | | 180,018 | | | | 2,254 | |

| | |

Issued to shareholders electing to receive payments of distributions in Fund shares | | | 3,429 | | | | 63 | |

| | |

Redemptions | | | (134,224 | ) | | | — | |

| | |

Net increase | | | 49,223 | | | | 2,317 | |

At January 31, 2021, EVM owned 93.8% of the outstanding shares of the Fund.

6 Financial Instruments

The Fund may trade in financial instruments with off-balance sheet risk in the normal course of its investing activities. These financial instruments may include forward foreign currency exchange contracts, financial futures contracts and swap contracts and may involve, to a varying degree, elements of risk in excess of the amounts recognized for financial statement purposes. The notional or contractual amounts of these instruments represent the investment the Fund has in particular classes of financial instruments and do not necessarily represent the amounts potentially subject to risk. The measurement of the risks associated with these instruments is meaningful only when all related and offsetting transactions are considered. A summary of obligations under these financial instruments at January 31, 2021 is included in the Portfolio of Investments. At January 31, 2021, the Fund had sufficient cash and/or securities to cover commitments under these contracts.

In the normal course of pursuing its investment objective, the Fund is subject to the following risks:

Credit Risk: The Fund enters into credit default swap contracts to enhance total return and/or as a substitute for the purchase or sale of securities.

Foreign Exchange Risk: The Fund engages in forward foreign currency exchange contracts to enhance total return and/or to seek to hedge against fluctuations in currency exchange rates.

Eaton Vance

Emerging Markets Debt Fund

January 31, 2021

Notes to Financial Statements — continued

Interest Rate Risk: The Fund utilizes various interest rate derivatives including interest rate futures contracts and interest rate swaps to enhance total return, to seek to hedge against fluctuations in interest rates, and/or to change the effective duration of its portfolio.