UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number: 811-04032

Sit Money Market Fund, Inc.

(Exact name of registrant as specified in charter)

3300 IDS Center

80 South Eighth Street

Minneapolis, MN 55402

(Address of principal executive offices)

Paul E. Rasmussen, VP Treasurer

Sit Mutual Funds, Inc.

3300 IDS Center

80 South Eighth Street

Minneapolis, MN 55402

(Name and address of agent for service)

Copy to:

Mike Radmer, Esq.

Dorsey & Whitney

Suite 1500

50 South Sixth Street

Minneapolis, MN 55402-1498

Registrant’s telephone number, including area code:

(612) 334-5888

Date of fiscal year end: March 31, 2007

Date of reporting period: March 31, 2007

Item 1: Reports to Stockholders.

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number: 811-04995

Sit U.S. Government Securities Fund, Inc.

(Exact name of registrant as specified in charter)

3300 IDS Center

80 South Eighth Street

Minneapolis, MN 55402

(Address of principal executive offices)

Paul E. Rasmussen, VP Treasurer

Sit Mutual Funds, Inc.

3300 IDS Center

80 South Eighth Street

Minneapolis, MN 55402

(Name and address of agent for service)

Copy to:

Mike Radmer, Esq.

Dorsey & Whitney

Suite 1500

50 South Sixth Street

Minneapolis, MN 55402-1498

Registrant’s telephone number, including area code:

(612) 334-5888

Date of fiscal year end: March 31, 2007

Date of reporting period: March 31, 2007

Item 1: Reports to Stockholders.

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number: 811-04033

Sit Mutual Funds II, Inc.

(Exact name of registrant as specified in charter)

3300 IDS Center

80 South Eighth Street

Minneapolis, MN 55402

(Address of principal executive offices)

Paul E. Rasmussen, VP Treasurer

Sit Mutual Funds, Inc.

3300 IDS Center

80 South Eighth Street

Minneapolis, MN 55402

(Name and address of agent for service)

Copy to:

Mike Radmer, Esq.

Dorsey & Whitney

Suite 1500

50 South Sixth Street

Minneapolis, MN 55402-1498

Registrant’s telephone number, including area code:

(612) 334-5888

Date of fiscal year end: March 31, 2007

Date of reporting period: March 31, 2007

Item 1: Reports to Stockholders.

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number: 811-21447

Sit Mutual Funds Trust

(Exact name of registrant as specified in charter)

3300 IDS Center

80 South Eighth Street

Minneapolis, MN 55402

(Address of principal executive offices)

Paul E. Rasmussen, VP Treasurer

Sit Mutual Funds, Inc.

3300 IDS Center

80 South Eighth Street

Minneapolis, MN 55402

(Name and address of agent for service)

Copy to:

Mike Radmer, Esq.

Dorsey & Whitney

Suite 1500

50 South Sixth Street

Minneapolis, MN 55402-1498

Registrant’s telephone number, including area code:

(612) 334-5888

Date of fiscal year end: March 31, 2007

Date of reporting period: March 31, 2007

Item 1: Reports to Stockholders.

Sit Mutual Funds

Bond Funds

Annual Report

March 31, 2007

Money Market Fund

U.S. Government Securities Fund

Tax-Free Income Fund

Minnesota Tax-Free Income Fund

Florida Tax-Free Income Fund

|

Sit Mutual Funds |

BOND FUNDS ANNUAL REPORT |

TABLE OF CONTENTS |

|

This document must be preceded or accompanied by a Prospectus.

| | | | | |

|

| | | | |

| | | | |

| | Sit Mutual Funds | | |

| | One Year Ended March 31, 2007 | | |

| | | | |

| | Chairman’s Letter

| | |

| | | | |

| | | | |

Dear fellow shareholders:

The Federal Reserve increased short-term interest rates twice more during the second calendar quarter of 2006, bringing the federal funds rate to 5.25%. Treasury yields rose approximately 30 basis points to above 5.0% across the maturity spectrum, reflecting continued concerns over inflation and creating an almost flat yield curve. The Fed’s rate increase on June 29, 2006 was its 17th and latest move in the 425 basis points of tightening that began two years earlier. Weaker economic data in the third quarter of 2006 led intermediate and longer term yields to decline as investors believed that the current cycle of Fed tightening might be done. Treasury yields have been relatively stable since then, with the front end of the curve inverted as short term yields remain higher than longer term yields. The 3-month Treasury bill yield ended the 12-month period 0.40% higher at around 5.0% while the 5-year and 30-year Treasury yields declined -0.27% and -0.04% to 4.54% and 4.85%, respectively. The Fed has maintained a bias against inflationary risks since its May 2006 meeting.

The final estimate of U.S. fourth quarter 2006 real GDP growth was +2.5%, and total real GDP growth measured on a year-over-year basis in the fourth quarter remained a healthy +3.1%. We expect real GDP growth rate to moderate to a +2.7% average rate for 2007. Real personal consumption expenditures (PCE), which represent two-thirds of GDP, are on pace to exceed +3.0% for the first calendar quarter of 2007 and could approach +4.0%. While this rate of spending growth represents a slowdown from the +4.2% rate posted in the fourth quarter, it is still quite solid and counters the recession prospects that an inverted yield curve environment might suggest. The strong employment data released on April 5th, which saw the unemployment rate dip slightly to 4.4%, was also supportive of sustained consumer spending. The domestic economy could also see strength from other sectors. The inventory sector, which is notoriously volatile and remained a major drag in the fourth quarter, could eventually rebound to provide a solid underpinning to growth. In addition, real business spend-

ing remains a positive factor and, despite some softening, grew at approximately twice the rate of the total economy on a year-over-year basis in the fourth quarter.

The headline Consumer Price Index for All Urban Consumers (CPI) increased +0.4% in February, and core CPI, which excludes the volatile food and energy sectors, rose +0.2%. These monthly increases resulted in year-over-year figures of +2.4% and +2.7% for the headline and core CPIs, respectively. Over the next few months, the year-over-year CPI data are likely to decrease from February levels as a result of easy comparisons from the same period a year ago. However, in the second half of the year, the opposite effect will occur as even just moderate increases in the monthly inflation figures will boost the year-over-year measurements. Despite the intermediate volatility, we expect the average CPI figure for the year to fall in a range between +2.0% and +2.5%.

Although the dollar has been weak recently, it has stayed within its trading range of the past two years. We expect the dollar to remain in this range as pressure from the budget and trade deficits is, at least partially, offset by the relative attractiveness of U.S. equity and fixed-income markets.

The domestic fiscal environment has shown steady improvement and we continue to expect the deficit to be less than $200 billion for the current fiscal year. For the first five months of fiscal 2007 through February, the U.S. budget deficit stands at $162.2 billion, which is almost a $56 billion improvement over the $217.7 billion deficit for the comparable period last year. Receipt growth for the first half of fiscal year 2007 is estimated to have increased +8% versus the comparable period in fiscal 2006 due to higher tax payments, while outlays are estimated to have grown just +2%. Factoring in similarly positive Congressional Budget Office (CBO) estimates for March, estimates from CBO and the Office of Management and Budget (OMB) for the fiscal year 2007 budget deficit remain unchanged at $177 billion and $244 billion, respectively.

2

| | | | |

| | |

| |

| | |

| | |

|

| |

| | | | |

Strategy Summary

We continue to expect that the U.S. economy will successfully transition to a more moderate growth environment, with real GDP growth averaging approximately +2.7% in 2007, as indications are that the key consumer spending sector remains intact. Elevated energy prices and a slowdown in the housing market are providing dual headwinds. Factors in the housing market, generally, and the subprime market, specifically, will continue to create pressures on consumer spending. However, we believe the bottoming phase in the housing market correction is underway and that the spillover effects from the difficulties in the subprime lending market will be manageable. While the price of crude oil rose in March, it remains well below the highs of last spring and summer and is close to flat with this period last year. Looking forward, inflation could provide a surprise on the upside later in the year as the easy comparisons from prior periods roll off. Nonetheless, we expect the CPI figure to average between +2.0% and +2.5% for the year.

The yield curve steepened in March, reflecting increased investor anticipation of a cut in the federal funds rate later this year in response to weaker economic data. The slowing housing market and problems within the subprime mortgage market have added to the list of justifications for the Fed to reduce its hawkish stance on interest rates. The Fed dropped its tightening bias at its meeting on March 21st, 2007 while maintaining an inflationary risk assessment. We expect further steepening in the yield curve later in the year as shorter and intermediate term rates decline while longer term yields should be relatively stable. However, longer term yields could shift slightly higher if an inflation surprise materializes and the Fed decides to maintain short term rates around current levels. Taxable bond portfolio durations are being maintained modestly longer than related benchmarks, with an emphasis on attractively yielding securities that will outperform in a steepening yield curve environment.

Municipal issuance volume remains high. New issuance volume in calendar 2007 is estimated to be around $375 billion, compared to $383 billion in 2006 and the record $408 billion in 2005. Approximately $80 billion of issuance is expected to come from voter-approved funding measures passed in November, of which $43 billion will come from California alone. Relative yield comparisons of short to intermediate duration municipals to similar duration Treasuries have cheapened as supply has kept shorter and intermediate municipal yields from declining. For example, the ratio of 10-year maturity municipal-to-Treasury yields increased from approximately 80% to 85% in March, returning to the higher end of its historical range in recent years. Longer term municipal bonds are fairly valued when compared to taxable bonds on a relative yield basis. We expect improving underwriting profitability for insurers to help demand for municipals remain robust, despite yields remaining near historic lows. Durations on our municipal portfolios are being extended closer to their benchmark levels in anticipation of the steepening yield curve environment we expect later in 2007. We remain focused on securities that offer attractive after-tax income, but are cautious as incremental yields provided by higher yielding sectors are historically narrow.

Fixed-income investments are an important component of a well-diversified, long term portfolio. We believe the Sit Bond Funds, with their dual objectives of high income and stability of principal, offer attractive risk/reward profiles to complement equity holdings. We appreciate your continued interest in Sit Mutual Funds and look forward to assisting you in achieving your long-term investment goals.

With best wishes,

Eugene C. Sit, CFA

Chairman and Chief Investment Officer

3

| | | | |

| Sit Mutual Funds | | | |

| One Year Ended March 31, 2007 | | | |

| | | | |

| Performance Summary - Bond Funds

| | | |

| | | | |

The Federal Reserve increased short term rates twice more on May 10th and June 29th, 2006, bringing the federal funds rate to 5.25%. The rate increase in June was the Fed’s 17th and latest move in the 425 basis points round of tightening that began two years earlier. The 3-month Treasury bill yield rose from 4.60% in March 2006 to 5.00% by June 2006 while Treasury bond yields rose approximately +0.30%, creating an almost flat yield curve. Since June, Treasury bill yields have been relatively stable while intermediate and longer term Treasury yields have fallen by approximately -0.60% and -0.35%, respectively, to create an inverted yield curve. Longer term bond yields ended the 12-month period little changed as 5-year and 30-year Treasury yields declined just - -0.27% and -0.04%, respectively, to 4.54% and 4.85% on March 31, 2007. The Fed has maintained a bias against inflationary risks since its May 2006 meeting.

Taxable bonds provided attractive returns for the 12-month period as short-term securities earned high current income and longer term securities benefited from price appreciation resulting from the decline in yields. The corporate sector outperformed due to its longer duration, despite recent widening in yield spreads as economic growth has moderated. The mortgage sector, with its yield advantage, also outperformed. The Treasury sector lagged due to its lower yields while the asset-backed sector lagged due to its shorter duration.

Shorter term municipals were fairly stable during the 12-month period while intermediate and longer term yields fell. Demand for municipals has remained robust despite a continued heavy pace of new issuance. The Bond Buyer 40-Bond Index yield rose to almost 5.0% in June and then declined to 4.61% to end the fiscal year-0.19% lower. As of March 31, 2007, longer term municipals were fairly valued compared to Treasury bonds on a relative yield basis while valuations on shorter and intermediate municipals were at the cheaper end of their recent historical range. The higher yielding industrial revenue and health care sectors outperformed during the period, while shorter duration municipal sectors lagged.

Fixed-income portfolios are being positioned to take advantage of the steepening yield curve environment we expect later in 2007, and we remain focused on securities that offer attractive incremental yield.

| | | | | | | | | | | |

SIT FIXED-INCOME FUNDS | | Three

Month* | | Six

Month* | |

U.S. Government Securities SNGVX | | | | 1.67 | | | | | 2.96 | | |

Lehman Inter. Govt. Bond Index | | | | 1.53 | | | | | 2.43 | | |

Tax-Free Income SNTIX | | | | 0.81 | | | | | 1.81 | | |

Lehman 5-Year Municipal Bond Index | | | | 0.93 | | | | | 1.56 | | |

Minnesota Tax-Free Income SMTFX | | | | 0.84 | | | | | 1.98 | | |

Lehman 5-Year Municipal Bond Index | | | | 0.93 | | | | | 1.56 | | |

Florida Tax-Free Income SFLIX | | | | 0.82 | | | | | 1.64 | | |

Lehman 5-Year Municipal Bond Index | | | | 0.93 | | | | | 1.56 | | |

| | | | | | | | | | | |

| | | | | | | | | | | |

SIT MONEY MARKET FUND | | | | | | | | | | | |

Money Market Fund(1) SNIXX | | | | 1.20 | | | | | 2.43 | | |

3-Month Treasury Bill | | | | 1.28 | | | | | 2.56 | | |

| | | | | | | | | | | |

*3- and 6-month returns not annualized. | | | | | | | | | | | |

| | | | | | | | | | | |

| | | | | |

| | 1997 | | 1998 | |

U.S. Government Securities SNGVX | | | | 8.19 | % | | | | 6.52 | % | |

Lehman Interm. Govt. Bond Index | | | | 7.72 | | | | | 8.49 | | |

Tax-Free Income SNTIX | | | | 9.87 | | | | | 6.29 | | |

Lehman 5-Year Municipal Bond Index | | | | 6.38 | | | | | 5.84 | | |

Minnesota Tax-Free Income SMTFX | | | | 8.19 | | | | | 6.14 | | |

Lehman 5-Year Municipal Bond Index | | | | 6.38 | | | | | 5.84 | | |

Florida Tax-Free Income SFLIX | | | | — | | | | | — | | |

Lehman 5-Year Municipal Bond Index | | | | — | | | | | — | | |

| | | | | | | | | | | |

Money Market Fund(1) SNIXX | | | | 5.22 | | | | | 5.17 | | |

3-Month Treasury Bill | | | | 5.32 | | | | | 5.01 | | |

Performance figures are historical and do not guarantee future results. Investment returns and principal value will vary, and you may have a gain or loss when you sell shares. Average annual returns include reinvestment of all dividends and capital gains. For any returns less than one year, the returns are cumulative. Investors should consider the investment objectives, risks, charges and expenses of the Funds carefully before investing. This and other information is contained in the Funds’ prospectus, which may be obtained by calling or visiting www.sitfunds.com. Please read the prospectus carefully before you invest or send money. An investment in the Money Market Fund is not insured or guaranteed by the Federal Deposit Insurance Corporation or any other government agency. Although the Money Market Fund seeks to preserve the value of your investment at $1.00 per share, it is possible to lose money by investing in the Fund.

| |

(1) | Converted from Sit Investment Reserve Fund to Sit Money Market Fund on 11/1/93 |

(2) | Based on the last 12 monthly distributions of net investment income and average NAV as of 3/31/07. |

(3) | For individuals in the 25%, 28%, 33% and 35% federal tax brackets, the federal tax equivalent yields are 5.72%, 5.96%, 6.40% and 6.60%, respectively. (Income subject to state tax, if any.) |

(4) | For Minnesota residents in the 25%, 28%, 33% and 35% federal tax brackets, the double exempt tax equivalent yields are 6.28%, 6.54%, 7.03% and 7.25%, respectively. (Assumes the maximum Minnesota tax bracket of 7.85%.) |

(5) | For individuals in the 25%, 28%, 33% and 35% federal tax brackets, the tax equivalent yields are 5.40%, 5.63%, 6.04% and 6.23%, respectively. (Income subject to state tax, if any.) |

(6) | The yield quotation more closely reflects the current earnings of the Money Market Fund than the total return quotation which refers to a specific past holding period. |

4

| | | | | | | | | | | | | | | | |

AVERAGE ANNUAL RETURNS FOR PERIODS ENDED MARCH 31, 2007 | |

| | |

One

Year | | Three

Year | | Five

Year | | Ten

Year | | Since

Inception | | Inception

Date | |

5.81 | | | 3.38 | | | 3.58 | | | 5.21 | | | 6.62 | | | 6/2/87 | |

5.75 | | | 2.39 | | | 4.29 | | | 5.64 | | | 6.77 | | | | |

4.00 | | | 3.30 | | | 3.93 | | | 4.52 | | | 5.85 | | | 9/29/88 | |

4.28 | | | 2.22 | | | 4.12 | | | 4.79 | | | 5.78 | | | | |

5.17 | | | 4.10 | | | 4.88 | | | 4.89 | | | 5.18 | | | 12/1/93 | |

4.28 | | | 2.22 | | | 4.12 | | | 4.79 | | | 4.77 | | | | |

3.97 | | | 3.12 | | | — | | | — | | | 3.21 | | | 12/31/03 | |

4.28 | | | 2.22 | | | — | | | — | | | 2.44 | | | | |

| | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | |

4.80 | | | 3.10 | | | 2.20 | | | 3.48 | | | 3.80 | | | 11/1/93 | |

5.18 | | | 3.56 | | | 2.63 | | | 3.70 | | | 4.05 | | | | |

| | | | |

AS OF 3/31/2007 |

| | | | |

30-Day

SEC Yield | | Distribution

Rate(2) |

4.98 | % | |

4.61

| % |

| | | | |

4.29 | (3) | | 3.93 | |

| | | | |

4.34 | (4) | | 4.17 | |

| | | | |

4.05 | (5) | | 3.60 | |

| | | | |

| | | | |

| | | | |

7-Day

Yield(6) | | 7-Day

Effective

Yield(6) |

4.97 | % | | 5.09 | % |

| | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | | | |

TOTAL RETURN BY CALENDAR YEAR |

1999 | | | 2000 | | | 2001 | | | 2002 | | | 2003 | | | 2004 | | | 2005 | | | 2006 | | | YTD 2007 |

1.37 | % | | 9.15 | % | | 8.56 | % | | 5.79 | % | | 1.19 | % | | 3.35 | % | | 2.49 | % | | 4.13 | % | | 1.67 | % |

0.49 | | | 10.47 | | | 8.42 | | | 9.64 | | | 2.29 | | | 2.33 | | | 1.68 | | | 3.84 | | | 1.53 | |

-4.01 | | | 8.32 | | | 5.84 | | | 5.69 | | | 2.87 | | | 3.96 | | | 3.30 | | | 3.54 | | | 0.81 | |

0.74 | | | 7.72 | | | 6.21 | | | 9.27 | | | 4.13 | | | 2.72 | | | 0.95 | | | 3.34 | | | 0.93 | |

-3.82 | | | 8.09 | | | 5.85 | | | 7.06 | | | 4.42 | | | 3.68 | | | 4.44 | | | 4.92 | | | 0.84 | |

0.74 | | | 7.72 | | | 6.21 | | | 9.27 | | | 4.13 | | | 2.72 | | | 0.95 | | | 3.34 | | | 0.93 | |

— | | | — | | | — | | | — | | | — | | | 2.58 | | | 3.22 | | | 3.82 | | | 0.82 | |

— | | | — | | | — | | | — | | | — | | | 2.72 | | | 0.95 | | | 3.34 | | | 0.93 | |

4.79 | | | 6.03 | | | 3.67 | | | 1.25 | | | 0.65 | | | 0.88 | | | 2.77 | | | 4.59 | | |

1.20

| |

4.88 | | | 6.16 | | | 3.50 | | | 1.67 | | | 1.03 | | | 1.41 | | | 3.26 | | | 5.00 | | | 1.28 | |

5

| | | | |

|

| Sit Mutual Funds | | | |

| | | | |

| Average Annual Total Returns for Periods Ended December 31, 2006

| | | |

| | | | |

The tables on the next page show the Funds’ average annual total returns (before and after taxes) and the change in value of a broad-based market index over various periods ended December 31, 2006. The index information is intended to permit you to compare each Fund’s performance to a broad measure of market performance. The after-tax returns are intended to show the impact of federal income taxes on an investment in a Fund. The highest individual federal marginal income tax rate in effect during the specified period is assumed, and the state and local tax impact is not reflected.

A Fund’s “Return After Taxes on Distributions” shows the effect of taxable distributions (dividends and capital gain distributions), but assumes that you still hold the Fund shares at the end of the period and so do not have any taxable gain or loss on your investment in the Fund.

A Fund’s “Return After Taxes on Distributions and Sale of Fund Shares” shows the effect of both taxable distributions and any taxable gain or loss that would be realized if the Fund shares were purchased at the beginning and sold at the end of the specified period.

The Funds’ past performance, before and after taxes, is not an indication of how the Funds will perform in the future. Your actual after-tax returns depend on your own tax situation and may differ from those shown. After-tax returns reflect past tax effects and are not predictive of future tax effects. After-tax returns are not relevant to investors who hold their Fund shares in a tax-deferred account (including a 401(k) or IRA account).

6

| | | |

Sit U.S. Government Securities Fund | 1 Year | 5 Years | 10 Years |

Return Before Taxes | 4.1% | 3.4% | 5.0% |

Return After Taxes on Distributions | 2.5% | 2.0% | 3.1% |

Return After Taxes on Distributions and Sale of Fund Shares | 2.6% | 2.1% | 3.1% |

Lehman Intermediate Government Bond Index | 3.8% | 3.9% | 5.5% |

| | | |

Sit Tax-Free Income Fund | 1 Year | 5 Years | 10 Years |

Return Before Taxes | 3.5% | 3.9% | 4.5% |

Return After Taxes on Distributions | 3.5% | 3.9% | 4.5% |

Return After Taxes on Distributions and Sale of Fund Shares | 3.6% | 3.9% | 4.5% |

Lehman 5-Year Municipal Bond Index | 3.3% | 4.1% | 4.7% |

| | | |

Sit Minnesota Tax-Free Income Fund | 1 Year | 5 Years | 10 Years |

Return Before Taxes | 4.9% | 4.9% | 4.8% |

Return After Taxes on Distributions | 4.9% | 4.9% | 4.8% |

Return After Taxes on Distributions and Sale of Fund Shares | 4.8% | 4.8% | 4.8% |

Lehman 5-Year Municipal Bond Index | 3.3% | 4.1% | 4.7% |

| | | |

Sit Florida Tax-Free Income Fund | 1 Year | 5 Years | Since Inception* |

Return Before Taxes | 3.8% | n/a | 3.2% |

Return After Taxes on Distributions | 3.8% | n/a | 3.2% |

Return After Taxes on Distributions and Sale of Fund Shares | 3.8% | n/a | 3.2% |

Lehman 5-Year Municipal Bond Index | 3.3% | n/a | 2.3% |

*Inception date 12/31/03

7

| | | | |

| Sit Money Market Fund | | | |

| One Year Ended March 31, 2007 | | | |

| | | | |

| Michael C. Brilley, Senior Portfolio Manager

Mark H. Book, CFA, Portfolio Manager | | | |

The Sit Money Market Fund returned +4.80% net of fees for the twelve months ended March 31, 2007 compared to +5.18% for the 3-month U.S. Treasury bill. As of March 31, the Fund’s 7-day compound yield was 4.97% and its average maturity was 25 days.

The Fed raised the federal funds rate target to 5.25% in June 2006, which was its latest increase in the tightening cycle that began two years earlier in June 2004. Short-term yields rose during the 12-month period while yields on intermediate and longer maturities declined. Yields on intermediate maturities fell the most, creating an inverted yield curve at the front end of the maturity spectrum and an upward sloping curve at the long end. Because investors in longer maturity Treasuries believe the Fed will be successful in its efforts to contain inflation, they have been willing to buy intermediate and long maturity Treasuries at lower yields. The steepening in the yield curve reflects investor anticipation of a cut in the federal funds rate later in 2007, in response to recent weaker economic data and the Federal Reserve’s decision to drop its tightening bias at its most recent FOMC meeting on March 21, 2007. While market levels currently suggest that the Fed will begin reducing rates in the third quarter of 2007, we believe that easing may not occur that soon, as the Fed is still focused on containing inflation. It is unclear when the Fed will begin easing monetary policy but action will continue to be largely dependent on various metrics including the rate of inflation and economic growth.

The Fund has maintained its average maturity near the short end of its customary 20 to 40 day range as the 3-month Treasury bill yield increased 43 basis points over the past twelve months. The Fund has begun to extend its average maturity as the current cycle of Fed tightening may be complete. Corporate credit quality remains strong in general, but some sectors have slowed along with the economy. The Fund has no direct exposure to sub-prime mortgages, which has become a concern in the Corporate market. We continue to focus on issuers with top-tier credit quality.

INVESTMENT OBJECTIVE AND STRATEGY |

The objective of the Fund is to achieve maximum current income to the extent consistent with the preservation of capital and maintenance of liquidity. The Fund pursues this objective by investing in short-term debt instruments which mature in 397 days or less and by maintaining a dollar-weighted portfolio maturity of 90 days or less.

An investment in the Fund is neither insured nor guaranteed by the U.S. Government and there can be no assurance that the Fund will be able to maintain a stable net asset value of $1.00 per share.

| | |

Net Asset Value 3/31/07: | | $1.00 Per Share |

3/31/06: | | $1.00 Per Share |

| | |

Total Net Assets: | | $52.5 Million |

PORTFOLIO STRUCTURE

(% OF TOTAL NET ASSETS) |

8

| | | | |

| | |

| |

| | |

| | |

|

| |

| | | | |

| | | | | | | | |

AVERAGE ANNUAL TOTAL RETURNS* | |

| | | | | | | |

| | Sit Money

Market Fund | | 3-Month

U.S.

Treasury Bill | | Lipper

Money

Market | |

| | | | | | | | | | |

3 Month** | | | 1.20 | % | | | 1.28 | % | | | 1.17 | % |

6 Month** | | | 2.43 | | | | 2.56 | | | | N/A | |

1 Year | | | 4.80 | | | | 5.18 | | | | 4.72 | |

5 Years | | | 2.20 | | | | 2.63 | | | | 2.13 | |

10 Years | | | 3.48 | | | | 3.70 | | | | 3.44 | |

Inception | | | 3.80 | | | | 4.05 | | | | 3.75 | |

(11/1/93) | | | | | | | | | | | | |

| | | | | | | | | | | | |

CUMULATIVE TOTAL RETURNS* |

| | | | | | | | | | | | |

| | Sit Money

Market Fund | | 3-Month

U.S.

Treasury Bill | | Lipper

Money

Market |

| | | | | | | | | | | | |

1 Year | | | 4.80 | % | | | 5.18 | % | | | 4.72 | % |

5 Year | | | 11.49 | | | | 13.83 | | | | 11.10 | |

10 Year | | | 40.83 | | | | 43.83 | | | | 40.24 | |

Inception | | | 64.96 | | | | 70.45 | | | | 63.91 | |

(11/1/93) | | | | | | | | | | | | |

| | | | | | | | | | | | |

*As of 3/31/07 | **Not annualized. |

| |

Performance is historical and assumes reinvestment of all dividends and capital gains. Money Market funds are neither insured nor guaranteed by the U.S. Government. There is no assurance that a fund will maintain a $1 share value. Yield fluctuates. Past performance is not a guarantee of future results. Management fees and administrative expenses are included in the Fund’s performance; however, fees and expenses are not incorporated in the 3-Month U.S. Treasury Bill. The Lipper returns are obtained from Lipper Analytical Services, Inc., a large independent evaluator of mutual funds.

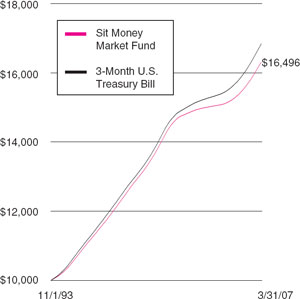

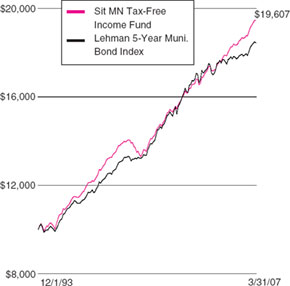

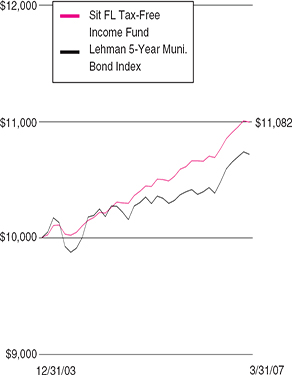

The sum of $10,000 invested at inception (11/1/93) and held until 3/31/07 would have grown to $16,496 in the Fund or $17,045 in the 3-Month U.S. Treasury Bill assuming reinvestment of all dividends and capital gains.

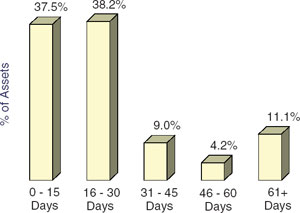

SIT MONEY MARKET MATURITY RANGES |

9

| | | | |

| Sit Money Market Fund | | | |

| March 31, 2007 | | | |

| | | | |

| Portfolio of Investments | | | |

| | | | |

| | | | | |

Quantity ($) | Name of Issuer | | Market Value ($)(1) | |

| | | | | |

| | | | |

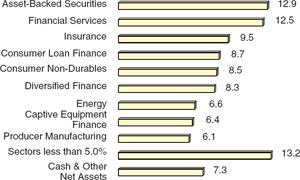

Commercial Paper (92.7%) (2) | | | |

| | | |

Asset-Backed (12.9%) | | | |

| | Daimler-Chrysler Auto Conduit: | | | |

700,000 | | 5.25%, 6/1/07 | | 693,695 | |

1,500,000 | | 5.25%, 6/1/07 | | 1,486,438 | |

1,000,000 | | FCAR Owner Trust Series I, | | | |

| | 5.25%, 4/24/07 | | 996,500 | |

1,300,000 | | FCAR Owner Trust Series II, | | | |

| | 5.27%, 4/5/07 | | 1,299,048 | |

2,300,000 | | New Center Asset Trust, | | | |

| | 5.23%, 4/27/07 | | 2,290,978 | |

| | | | | |

| | | | 6,766,659 | |

| | | | | |

| | | | | |

Captive Equipment Finance (6.4%) | | | |

1,200,000 | | Caterpillar Financial Services, | | | |

| | 5.24%, 4/2/07 | | 1,199,651 | |

| | Pitney Bowes Inc.: | | | |

1,175,000 | | 5.22%, 4/2/07 | | 1,174,659 | |

1,000,000 | | 5.25%, 4/17/07 | | 997,521 | |

| | | | | |

| | | | 3,371,831 | |

| | | | | |

Consumer Durables (4.8%) | | | |

2,500,000 | | American Honda Finance, | | | |

| | 5.23%, 4/16/07 | | 2,494,189 | |

| | | | | |

| | | | | |

Consumer Loan Finance (8.7%) | | | |

| | American Express Credit Corp.: | | | |

1,000,000 | | 5.24%, 4/3/07 | | 999,563 | |

1,300,000 | | 5.22%, 4/4/07 | | 1,299,246 | |

2,300,000 | | American General Financial Corp., | | | |

| | 5.23%, 4/23/07 | | 2,292,315 | |

| | | | | |

| | | | 4,591,124 | |

| | | | | |

Consumer Non-Durables (8.5%) | | | |

2,300,000 | | Coca Cola Company, | | | |

| | 5.20%, 4/10/07 | | 2,296,678 | |

| | Coca Cola Enterprises: | | | |

1,200,000 | | 5.26%, 4/13/07(5) | | 1,197,721 | |

1,000,000 | | 5.26%, 5/9/07(5) | | 994,302 | |

| | | | | |

| | | | 4,488,701 | |

| | | | | |

Diversified Finance (8.3%) | | | |

| | GE Capital Corp.: | | | |

1,300,000 | | 5.23%, 4/9/07 | | 1,298,300 | |

900,000 | | 5.23%, 6/8/07 | | 890,978 | |

2,200,000 | | GE Capital Services, | | | |

| | 5.23%, 5/29/07 | | 2,181,143 | |

| | | | | |

| | | | 4,370,421 | |

| | | | | |

Electronic Technology (4.2%) | | | |

| | IBM Corp.: | | | |

1,300,000 | | 5.20%, 4/17/07 | | 1,296,808 | |

900,000 | | 5.22%, 5/8/07 | | 895,041 | |

| | | | | |

| | | | 2,191,849 | |

| | | | | |

| | | | |

Quantity ($) | Name of Issuer | | Market Value ($)(1) |

| | | | | | |

| | | | | | |

Energy (6.6%) | | | | |

1,470,000 | | BP Capital Markets, | | | | |

| | 5.40%, 4/2/07 | | | 1,469,559 | |

2,000,000 | | Chevron Funding Corp., | | | | |

| | 5.23%, 5/4/07 | | | 1,990,121 | |

| | | | | | |

| | | | | 3,459,680 | |

| | | | | | |

Financial Services (12.5%) | | | | |

2,300,000 | | Citigroup Funding, Inc., | | | | |

| | 5.24%, 4/20/07 | | | 2,293,304 | |

2,300,000 | | Deutsche Bank Financial, | | | | |

| | 5.26%, 4/12/07 | | | 2,295,967 | |

| | UBS Finance Corp.: | | | | |

1,400,000 | | 5.25%, 4/19/07 | | | 1,396,121 | |

600,000 | | 5.23%, 4/19/07 | | | 598,337 | |

| | | | | | |

| | | | | 6,583,729 | |

| | | | | | |

Insurance (9.5%) | | | | |

2,200,000 | | AIG Funding, Inc., | | | | |

| | 5.24%, 4/18/07 | | | 2,194,236 | |

2,800,000 | | American Family Financial, | | | | |

| | 5.21%, 6/15/07 | | | 2,769,203 | |

| | | | | | |

| | | | | 4,963,439 | |

| | | | | | |

Producer Manufacturing (6.1%) | | | | |

1,000,000 | | Caterpillar, Inc, | | | | |

| | 5.30%, 4/9/07 | | | 998,675 | |

| | Siemens Capital: | | | | |

1,282,000 | | 5.24%, 4/9/07 | | | 1,280,321 | |

900,000 | | 5.25%, 4/11/07 | | | 898,556 | |

| | | | | | |

| | | | | 3,177,552 | |

| | | | | | |

Retail Trade (4.2%) | | | | |

| | Wal-Mart Stores Inc.: | | | | |

775,000 | | 5.20%, 4/24/07(5) | | | 772,313 | |

562,000 | | 5.20%, 4/24/07(5) | | | 560,052 | |

900,000 | | 5.21%, 5/8/07(5) | | | 895,051 | |

| | | | | | |

| | | | | 2,227,416 | |

| | | | | | |

| | | | | | |

Total Commercial Paper | | 48,686,590 | |

| | | | | | |

(cost: $48,686,590) | | | |

| | | | | | |

U.S. Government Securities (7.7%) (2) | | | | |

2,000,000 | | FHLB Discount Note, 5.16%, 4/25/07 | | | 1,992,833 | |

1,706,000 | | FHLMC Discount Note, 5.15%, 4/3/07 | | | 1,705,268 | |

350,000 | | FHLMC Discount Note, 5.15%, 4/5/07 | | | 349,750 | |

| | | | | | |

| | | | | 4,047,851 | |

| | | | | | |

| | | | | | |

(cost: $4,047,851) | | | | |

| | | | | | |

Total investments in securities | | | |

(cost: $52,734,441) (6) | $ | 52,734,441 | |

| | | | | | |

| |

10 | See accompanying notes to portfolios of investments on page 62. |

This page has been left blank intentionally.

11

| | | | |

| Sit U.S. Government Securities Fund | | | |

| One Year Ended March 31, 2007 | | | |

| | | | |

| Senior Portfolio Managers, Michael C. Brilley and Bryce A. Doty, CFA

Portfolio Manager, Mark H. Book, CFA

| | | |

| | | | |

The Sit U.S. Government Securities Fund returned +5.81% during the fiscal year ending March 31, 2007, compared to the return of the Lehman Intermediate Government Bond Index of +5.75%. The Fund’s 30-day SEC yield was 4.98% and its 12-month distribution rate was 4.61%.

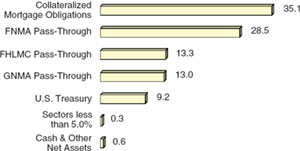

The return for the Fund was most positively influenced by its holdings in collateralized mortgage obligations, which exceeded the returns of the Lehman Intermediate Government Bond Index due to their income advantage. The Fund’s weighting in U.S. Treasury obligations detracted from performance, as these securities did not experience price appreciation in line with the bond market as a whole.

The last twelve months experienced two raises by the Federal Reserve in its target short-term lending rate to a level of 5.25%, each occurring in the first two meetings of the fiscal year, May 10th and June 29th. Mid-year 2006, the Federal Reserve ended its consistent tightening pace as inflation came to a more measured level. The Federal Reserve is still mindful of inflation risk, while monitoring the potential for an economic slowdown. We believe a decrease in the Federal Reserve’s short term borrowing rate sometime in the second half of the year is likely, as concern of slower economic growth builds. However, we believe that fears of higher inflation will potentially result in higher yields and price depreciation for longer maturity fixed income securities. As such, we expect the price stability of the Fund’s high coupon mortgage securities, coupled with their high level of income, to drive the Fund’s return, which has consistently been the case since the Fund’s inception.

INVESTMENT OBJECTIVE AND STRATEGY |

The objective of the U.S. Government Securities Fund is to provide high current income and safety of principal, which it seeks to attain by investing solely in debt obligations issues, guaranteed or insured by the U.S. government or its agencies or its instrumentalities.

Agency mortgage securities and U.S. Treasury securities will be the principal holdings in the Fund. The mortgage securities that the Fund will purchase consist of pass-through securities including those issued by Government National Mortgage Association (GNMA), Federal National Mortgage Asociation (FNMA), and Federal Home Loan Mortgage Corporation (FHLMC).

| | |

Net Asset Value 3/31/07: | | $10.56 Per Share |

3/31/06: | | $10.45 Per Share |

Total Net Assets: | | $198.4 Million |

30-day SEC Yield: | | 4.98% |

12-Month Distribution Rate: | | 4.61% |

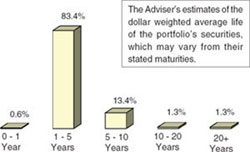

Average Maturity: | | 21.8 Years |

Effective Duration: | | 3.0 Years(1) |

(1) See next page

PORTFOLIO STRUCTURE

(% OF TOTAL NET ASSETS) |

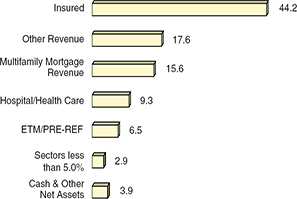

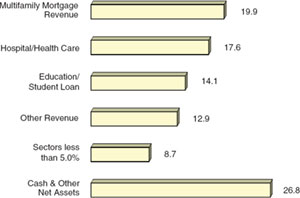

Portfolio Structure by Sector

12

| | | | |

| | |

| |

| | |

| | |

|

| |

| | | | |

| | | | | | | | |

AVERAGE ANNUAL TOTAL RETURNS* | |

| | | | | | | |

| | Sit

U.S. Gov’t

Securities

Fund | | Lehman

Inter. Gov’t

Bond Index | | Lipper

U.S. Gov’t

Fund Index | |

3 Month** | | | 1.67 | % | | | 1.53 | % | | | 1.38 | % |

6 Month** | | | 2.96 | | | | 2.43 | | | | n/a | |

1 Year | | | 5.81 | | | | 5.75 | | | | 5.66 | |

5 Years | | | 3.58 | | | | 4.29 | | | | 4.47 | |

10 Years | | | 5.21 | | | | 5.64 | | | | 5.52 | |

Inception | | | 6.62 | | | | 6.77 | | | | 6.36 | |

(6/2/87) | | | | | | | | | | | | |

| | | | | | | | | | | | |

CUMULATIVE TOTAL RETURNS* |

| | | | | | | | | | | | |

| | Sit

U.S. Gov’t

Securities

Fund | | Lehman

Inter. Gov’t

Bond Index | | Lipper

U.S. Gov’t

Fund Index |

1 Year | | | 5.81 | % | | | 5.75 | % | | | 5.66 | % |

5 Year | | | 19.24 | | | | 23.36 | | | | 24.42 | |

10 Year | | | 66.24 | | | | 73.09 | | | | 71.14 | |

Inception | | | 256.56 | | | | 266.64 | | | | 239.85 | |

(6/2/87) | | | | | | | | | | | | |

| | | | | | | | | | | | |

*As of 3/31/07.

| **Not annualized.

|

| |

Performance figures are historical and do not guarantee future results. Investment returns and principal value will vary, and you may have a gain or loss when you sell shares. Average annual total returns include changes in share price as well as reinvestment of all dividends and capital gains. Management fees and administrative expenses are included in the Fund’s performance; however, fees and expenses are not incorporated in the Lehman Intermediate Government Bond Index. The Lipper returns are obtained from Lipper Analytical Services, Inc., a large independent evaluator of mutual funds.

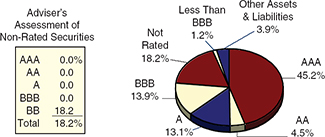

(1) Effective duration is a measure which reflects estimated price sensitivity to a given change in interest rates. For example, for an interest rate change of 1.0%, a portfolio with a duration of 5 years would be expected to experience a price change of 5%. Effective duration is based on current interest rates and the Adviser’s assumptions regarding the expected average life of individual securities held in the portfolio.

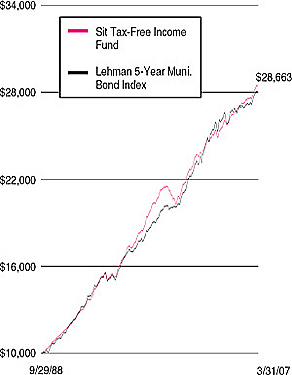

The sum of $10,000 invested at inception (6/2/87) and held until 3/31/07 would have grown to $35,656 in the Fund or $36,664 in the Lehman Intermediate Government Bond Index assuming reinvestment of all dividends and capital gains.

ESTIMATED AVERAGE LIFE PROFILE |

13

| | | | |

| Sit U.S. Government Securities Fund

March 31, 2007 | | | |

| | | | |

| Portfolio of Investments

| | | |

| | | | |

| | | | | | | |

Mortgage Pass-Through Securities (54.8%) (2) | |

Federal Home Loan Mortgage Corporation (13.3%): | |

|

Par ($) | | Coupon | | Maturity | | Market Value ($)(1) | |

| | | | | | | | |

49,067 | | 5.50% | | 8/1/17 | | 49,714 | |

215,209 | | 6.38% | | 12/1/26 | | 218,903 | |

76,705 | | 6.38% | | 8/1/27 | | 78,852 | |

120,448 | | 6.38% | | 12/1/27 | | 123,819 | |

716,104 | | 6.50% | | 8/1/29 | | 730,284 | |

86,532 | | 7.00% | | 6/1/19 | | 90,030 | |

1,291,476 | | 7.00% | | 10/1/31 | | 1,327,959 | |

302,211 | | 7.38% | | 12/17/24 | | 312,999 | |

31,993 | | 7.50% | | 2/1/17 | | 33,636 | |

152,221 | | 7.50% | | 1/1/23 | | 159,324 | |

153,518 | | 7.50% | | 8/1/23 | | 160,453 | |

528,320 | | 7.50% | | 1/1/27 | | 553,381 | |

807,403 | | 7.50% | | 7/1/29 | | 836,260 | |

62,881 | | 7.50% | | 1/1/30 | | 65,775 | |

108,899 | | 7.50% | | 9/1/30 | | 114,200 | |

1,004,654 | | 7.50% | | 1/1/31 | | 1,043,542 | |

1,261,305 | | 7.50% | | 10/1/31 | | 1,326,131 | |

2,310,626 | | 7.50% | | 4/1/32 | | 2,393,207 | |

1,557,914 | | 7.50% | | 7/1/32 | | 1,628,589 | |

613,789 | | 7.50% | | 6/1/35 | | 643,410 | |

68,541 | | 7.95% | | 10/1/25 | | 71,780 | |

73,019 | | 7.95% | | 10/1/25 | | 77,003 | |

51,753 | | 7.95% | | 11/1/25 | | 54,577 | |

22,149 | | 8.00% | | 5/1/17 | | 23,011 | |

69,905 | | 8.00% | | 1/1/21 | | 73,014 | |

430,893 | | 8.00% | | 12/1/23 | | 449,417 | |

267,411 | | 8.00% | | 9/15/24 | | 281,860 | |

41,650 | | 8.00% | | 12/1/26 | | 44,095 | |

143,956 | | 8.00% | | 6/1/30 | | 152,176 | |

9,595 | | 8.25% | | 12/1/08 | | 9,629 | |

48,339 | | 8.25% | | 12/1/17 | | 51,147 | |

5,092 | | 8.50% | | 1/1/17 | | 5,419 | |

25,388 | | 8.50% | | 2/1/17 | | 26,950 | |

27,710 | | 8.50% | | 3/1/17 | | 29,486 | |

75,882 | | 8.50% | | 4/1/17 | | 80,315 | |

77,077 | | 8.50% | | 5/1/17 | | 82,018 | |

25,689 | | 8.50% | | 5/1/17 | | 27,336 | |

72,045 | | 8.50% | | 10/1/19 | | 77,108 | |

39,172 | | 8.50% | | 7/1/21 | | 41,924 | |

410,489 | | 8.50% | | 12/1/29 | | 440,070 | |

485,271 | | 8.50% | | 2/1/31 | | 520,241 | |

22,526 | | 8.75% | | 1/1/17 | | 23,535 | |

6,762 | | 9.00% | | 5/1/09 | | 6,859 | |

3,781 | | 9.00% | | 6/1/09 | | 4,076 | |

11,059 | | 9.00% | | 7/1/09 | | 11,217 | |

12,541 | | 9.00% | | 7/1/09 | | 12,784 | |

| | | | | | | |

Par ($) | | Coupon | | Maturity | | Market Value ($)(1) | |

| | | | | | | | |

|

1,093 | | 9.00% | | 8/1/09 | | 1,114 | |

24,161 | | 9.00% | | 12/1/09 | | 24,507 | |

4,475 | | 9.00% | | 9/1/10 | | 4,501 | |

12,437 | | 9.00% | | 10/1/13 | | 13,201 | |

146,480 | | 9.00% | | 11/1/15 | | 158,920 | |

8,779 | | 9.00% | | 5/1/16 | | 9,391 | |

177,031 | | 9.00% | | 5/1/16 | | 192,065 | |

90,842 | | 9.00% | | 7/1/16 | | 97,173 | |

50,545 | | 9.00% | | 10/1/16 | | 53,566 | |

14,277 | | 9.00% | | 1/1/17 | | 15,238 | |

3,161 | | 9.00% | | 1/1/17 | | 3,381 | |

31,854 | | 9.00% | | 2/1/17 | | 32,697 | |

89,269 | | 9.00% | | 2/1/17 | | 95,490 | |

31,391 | | 9.00% | | 4/1/17 | | 32,064 | |

647,509 | | 9.00% | | 4/1/17 | | 691,334 | |

25,536 | | 9.00% | | 6/1/17 | | 27,270 | |

33,159 | | 9.00% | | 6/1/17 | | 35,556 | |

85,947 | | 9.00% | | 10/1/17 | | 92,158 | |

45,704 | | 9.00% | | 6/1/18 | | 48,512 | |

184,199 | | 9.00% | | 6/1/19 | | 196,666 | |

131,796 | | 9.00% | | 6/1/19 | | 140,716 | |

90,499 | | 9.00% | | 10/1/19 | | 97,401 | |

277,159 | | 9.00% | | 10/1/19 | | 297,189 | |

234,221 | | 9.00% | | 6/1/21 | | 243,608 | |

20,522 | | 9.00% | | 7/1/21 | | 22,171 | |

28,941 | | 9.00% | | 10/1/21 | | 30,176 | |

233,394 | | 9.00% | | 11/1/25 | | 252,786 | |

3,002,334 | | 9.00% | | 5/1/31 | | 3,243,641 | |

2,775 | | 9.25% | | 7/1/08 | | 2,836 | |

8,153 | | 9.25% | | 8/1/08 | | 8,334 | |

2,578 | | 9.25% | | 8/1/09 | | 2,621 | |

18,063 | | 9.25% | | 7/1/10 | | 18,482 | |

13,022 | | 9.25% | | 3/1/11 | | 13,107 | |

23,279 | | 9.25% | | 6/1/16 | | 25,080 | |

18,934 | | 9.25% | | 3/1/17 | | 20,399 | |

235,923 | | 9.25% | | 2/1/18 | | 247,901 | |

6,481 | | 9.25% | | 1/1/19 | | 6,523 | |

82,123 | | 9.25% | | 3/1/19 | | 86,884 | |

96,538 | | 9.25% | | 3/1/19 | | 99,909 | |

12,414 | | 9.50% | | 10/1/08 | | 12,708 | |

29,842 | | 9.50% | | 2/1/10 | | 30,501 | |

10,198 | | 9.50% | | 5/1/10 | | 10,609 | |

7,188 | | 9.50% | | 6/1/10 | | 7,346 | |

5,229 | | 9.50% | | 1/1/11 | | 5,514 | |

11,769 | | 9.50% | | 6/1/16 | | 12,748 | |

5,442 | | 9.50% | | 7/1/16 | | 5,895 | |

31,179 | | 9.50% | | 10/1/16 | | 33,775 | |

5,962 | | 9.50% | | 6/1/17 | | 6,479 | |

46,171 | | 9.50% | | 4/1/18 | | 50,309 | |

14

| | | | |

| | |

| |

| | |

| | |

|

| |

| | | | |

| | | | | | | |

Par ($) | | Coupon | | Maturity | | Market Value ($)(1) | |

| | | | | | | | |

|

6,062 | | 9.50% | | 10/1/18 | | 6,588 | |

256,507 | | 9.50% | | 6/17/19 | | 276,905 | |

1,116,650 | | 9.50% | | 12/17/21 | | 1,210,629 | |

15,451 | | 9.75% | | 12/1/08 | | 15,797 | |

4,048 | | 9.75% | | 12/1/08 | | 4,139 | |

18,176 | | 9.75% | | 11/1/09 | | 18,583 | |

9,034 | | 9.75% | | 6/1/11 | | 9,236 | |

159,879 | | 9.75% | | 12/1/16 | | 170,395 | |

40,524 | | 9.75% | | 6/1/17 | | 44,417 | |

145,456 | | 9.75% | | 12/1/17 | | 158,491 | |

30,341 | | 10.00% | | 11/1/10 | | 31,068 | |

34,117 | | 10.00% | | 11/1/11 | | 37,826 | |

169,314 | | 10.00% | | 9/1/20 | | 187,390 | |

1,065,875 | | 10.00% | | 3/15/25 | | 1,173,907 | |

12,396 | | 10.25% | | 6/1/10 | | 13,006 | |

32,188 | | 10.25% | | 2/1/17 | | 33,773 | |

43,791 | | 10.29% | | 9/1/16 | | 46,675 | |

54,015 | | 10.50% | | 10/1/13 | | 58,916 | |

73,804 | | 10.50% | | 5/1/14 | | 77,625 | |

25,688 | | 10.50% | | 9/1/15 | | 28,338 | |

17,437 | | 10.50% | | 1/1/19 | | 19,495 | |

298,524 | | 10.50% | | 6/1/19 | | 330,363 | |

6,434 | | 11.00% | | 12/1/11 | | 7,025 | |

22,675 | | 11.00% | | 6/1/15 | | 24,799 | |

12,689 | | 11.00% | | 2/1/16 | | 13,887 | |

12,127 | | 11.00% | | 5/1/19 | | 13,076 | |

14,549 | | 11.00% | | 7/1/19 | | 16,078 | |

731,189 | | 11.00% | | 8/15/20 | | 805,156 | |

6,464 | | 11.25% | | 10/1/09 | | 6,849 | |

17,122 | | 11.25% | | 8/1/11 | | 18,898 | |

19,123 | | 13.00% | | 5/1/17 | | 21,665 | |

| | | | | | | |

| | | | | | 26,308,962 | |

| | | | | | | |

| | | | | | | |

Federal National Mortgage Association (28.5%): | |

| | | | | | | |

Par ($) | | Coupon | | Maturity | | Market Value ($)(1) | |

| | | | | | | | |

197,759 | | 3.66% | | 8/1/33 | | 194,162 | |

282,401 | | 3.70% | | 8/1/33 | | 277,867 | |

76,769 | | 5.76% | | 3/1/33 | | 77,033 | |

26,518 | | 6.49% | | 3/1/19 | | 26,730 | |

88,018 | | 6.49% | | 2/1/32 | | 90,472 | |

72,321 | | 6.49% | | 4/1/32 | | 74,337 | |

55,757 | | 6.91% | | 11/1/26 | | 58,255 | |

186,614 | | 6.91% | | 8/1/27 | | 194,977 | |

322,624 | | 6.95% | | 8/1/21 | | 332,126 | |

14,190 | | 7.00% | | 2/1/17 | | 14,794 | |

24,115 | | 7.00% | | 4/1/27 | | 25,318 | |

553,460 | | 7.00% | | 1/1/29 | | 570,883 | |

27,161 | | 7.00% | | 10/1/29 | | 28,308 | |

1,882,962 | | 7.00% | | 11/1/29 | | 1,962,496 | |

274,094 | | 7.00% | | 5/1/31 | | 285,650 | |

| | | | | | | |

Par ($) | | Coupon | | Maturity | | Market Value ($)(1) | |

| | | | | | | | |

|

49,003 | | 7.00% | | 9/1/31 | | 51,114 | |

383,182 | | 7.00% | | 2/1/32 | | 395,245 | |

353,836 | | 7.00% | | 6/1/32 | | 371,284 | |

45,141 | | 7.00% | | 7/1/32 | | 47,041 | |

624,615 | | 7.00% | | 9/1/32 | | 650,897 | |

489,642 | | 7.00% | | 4/1/34 | | 505,056 | |

1,313,829 | | 7.45% | | 6/1/16 | | 1,417,833 | |

345,269 | | 7.50% | | 11/1/12 | | 348,470 | |

781,563 | | 7.50% | | 6/1/22 | | 818,055 | |

873,600 | | 7.50% | | 8/1/22 | | 918,794 | |

38,145 | | 7.50% | | 7/1/23 | | 39,948 | |

17,987 | | 7.50% | | 7/1/23 | | 18,852 | |

1,022,524 | | 7.50% | | 5/1/24 | | 1,059,824 | |

48,046 | | 7.50% | | 9/1/27 | | 50,860 | |

740,224 | | 7.50% | | 5/1/29 | | 767,227 | |

63,017 | | 7.50% | | 11/1/29 | | 66,092 | |

804,487 | | 7.50% | | 1/1/31 | | 843,289 | |

180,378 | | 7.50% | | 6/1/31 | | 185,905 | |

232,616 | | 7.50% | | 3/1/32 | | 242,827 | |

78,198 | | 7.50% | | 8/1/32 | | 80,647 | |

138,011 | | 7.50% | | 9/1/32 | | 142,315 | |

328,215 | | 7.50% | | 12/1/34 | | 340,188 | |

1,550,573 | | 7.50% | | 7/1/36 | | 1,607,163 | |

920,171 | | 7.50% | | 8/1/36 | | 953,754 | |

1,856,164 | | 7.50% | | 12/1/36 | | 1,923,908 | |

644,288 | | 7.95% | | 9/15/20 | | 679,623 | |

18,660 | | 8.00% | | 8/1/09 | | 18,955 | |

219,589 | | 8.00% | | 4/1/16 | | 231,085 | |

523,425 | | 8.00% | | 7/1/21 | | 555,309 | |

150,908 | | 8.00% | | 1/1/22 | | 159,092 | |

97,475 | | 8.00% | | 5/1/23 | | 102,574 | |

75,085 | | 8.00% | | 9/1/23 | | 79,214 | |

841,909 | | 8.00% | | 7/1/24 | | 891,251 | |

378,630 | | 8.00% | | 9/1/27 | | 401,338 | |

596,387 | | 8.00% | | 5/1/29 | | 628,579 | |

363,919 | | 8.00% | | 2/1/31 | | 383,563 | |

423,386 | | 8.00% | | 12/1/31 | | 446,240 | |

744,380 | | 8.00% | | 9/1/32 | | 788,544 | |

971,086 | | 8.00% | | 5/1/36 | | 1,023,457 | |

669,513 | | 8.00% | | 6/1/36 | | 705,646 | |

313,445 | | 8.00% | | 7/1/36 | | 330,349 | |

49,183 | | 8.25% | | 4/1/22 | | 51,454 | |

578,945 | | 8.33% | | 7/15/20 | | 628,782 | |

287,046 | | 8.38% | | 7/20/28 | | 307,998 | |

2,643,911 | | 8.45% | | 5/31/35 | | 2,847,894 | |

38,545 | | 8.50% | | 11/1/10 | | 39,518 | |

201,373 | | 8.50% | | 9/1/13 | | 203,662 | |

489,698 | | 8.50% | | 2/1/16 | | 523,016 | |

64,832 | | 8.50% | | 6/1/17 | | 65,679 | |

| |

See accompanying notes to portfolios of investments on page 62. | 15 |

| | | | |

| Sit U.S. Government Securities Fund

March 31, 2007 | | | |

| | | | |

| Portfolio of Investments

| | | |

| | | | |

| | | | | | | |

Par ($) | | Coupon | | Maturity | | Market Value ($)(1) | |

| | | | | | | | |

|

20,757 | | 8.50% | | 9/1/17 | | 21,758 | |

95,837 | | 8.50% | | 8/1/18 | | 102,201 | |

27,287 | | 8.50% | | 7/1/22 | | 29,355 | |

18,067 | | 8.50% | | 5/1/24 | | 19,449 | |

150,574 | | 8.50% | | 7/1/26 | | 160,602 | |

797,577 | | 8.50% | | 11/1/26 | | 857,229 | |

400,082 | | 8.50% | | 11/1/28 | | 430,319 | |

821,054 | | 8.50% | | 12/1/28 | | 882,462 | |

271,344 | | 8.50% | | 1/1/30 | | 290,765 | |

64,142 | | 8.50% | | 11/1/30 | | 68,700 | |

13,727 | | 8.50% | | 1/1/31 | | 14,702 | |

295,184 | | 8.52% | | 9/15/30 | | 315,635 | |

602,718 | | 8.71% | | 7/20/30 | | 647,989 | |

112,910 | | 8.87% | | 12/15/25 | | 125,305 | |

51,012 | | 9.00% | | 1/1/09 | | 52,095 | |

11,092 | | 9.00% | | 5/1/09 | | 11,306 | |

22,300 | | 9.00% | | 5/1/09 | | 22,505 | |

18,739 | | 9.00% | | 5/1/09 | | 19,101 | |

39,300 | | 9.00% | | 3/1/11 | | 40,611 | |

26,244 | | 9.00% | | 9/1/17 | | 28,192 | |

39,176 | | 9.00% | | 2/1/18 | | 42,084 | |

17,355 | | 9.00% | | 10/1/19 | | 18,516 | |

48,062 | | 9.00% | | 12/15/19 | | 51,218 | |

208,368 | | 9.00% | | 6/15/25 | | 228,100 | |

29,414 | | 9.00% | | 7/1/31 | | 31,987 | |

6,921,551 | | 9.00% | | 3/1/32 | | 7,501,400 | |

25,770 | | 9.25% | | 10/1/09 | | 26,371 | |

14,517 | | 9.25% | | 7/1/10 | | 14,980 | |

52,033 | | 9.25% | | 10/1/16 | | 56,267 | |

59,256 | | 9.25% | | 12/1/16 | | 64,078 | |

125,268 | | 9.25% | | 2/1/17 | | 134,937 | |

217,025 | | 9.34% | | 8/20/27 | | 242,433 | |

35,390 | | 9.50% | | 12/1/09 | | 36,654 | |

21,988 | | 9.50% | | 11/1/18 | | 24,086 | |

46,819 | | 9.50% | | 5/1/19 | | 51,425 | |

52,567 | | 9.50% | | 10/1/19 | | 56,930 | |

768,629 | | 9.50% | | 3/1/20 | | 860,865 | |

845,844 | | 9.50% | | 7/1/20 | | 927,179 | |

100,848 | | 9.50% | | 9/1/20 | | 110,062 | |

144,673 | | 9.50% | | 10/15/20 | | 156,251 | |

25,385 | | 9.50% | | 12/15/20 | | 27,408 | |

101,731 | | 9.50% | | 12/15/20 | | 110,317 | |

40,938 | | 9.50% | | 3/1/21 | | 44,701 | |

35,326 | | 9.50% | | 4/15/21 | | 38,476 | |

193,639 | | 9.50% | | 5/1/27 | | 214,012 | |

884,114 | | 9.50% | | 4/1/30 | | 967,075 | |

4,057,404 | | 9.50% | | 8/1/31 | | 4,455,927 | |

1,171,970 | | 9.55% | | 8/20/25 | | 1,295,110 | |

114,462 | | 9.75% | | 1/15/13 | | 123,876 | |

| | | | | | | |

Par ($) | | Coupon | | Maturity | | Market Value ($)(1) | |

| | | | | | | | |

|

113,392 | | 9.75% | | 1/1/21 | | 124,911 | |

202,885 | | 9.75% | | 10/1/21 | | 225,184 | |

240,150 | | 9.75% | | 4/1/25 | | 266,544 | |

32,732 | | 10.00% | | 5/1/11 | | 34,252 | |

94,142 | | 10.00% | | 7/1/13 | | 101,211 | |

507,930 | | 10.00% | | 2/1/15 | | 553,177 | |

711,803 | | 10.00% | | 3/1/15 | | 788,330 | |

66,241 | | 10.00% | | 11/1/16 | | 72,393 | |

41,947 | | 10.00% | | 9/1/19 | | 46,283 | |

15,970 | | 10.00% | | 11/1/20 | | 17,777 | |

35,201 | | 10.00% | | 1/1/21 | | 39,301 | |

85,525 | | 10.00% | | 1/1/24 | | 94,544 | |

429,518 | | 10.00% | | 2/1/28 | | 477,707 | |

293,216 | | 10.18% | | 7/1/20 | | 321,689 | |

212,650 | | 10.25% | | 8/15/13 | | 230,583 | |

26,331 | | 10.50% | | 5/1/15 | | 28,281 | |

181,917 | | 10.50% | | 1/1/16 | | 202,592 | |

58,964 | | 10.50% | | 12/1/17 | | 65,456 | |

97,309 | | 10.50% | | 4/1/22 | | 106,041 | |

11,301 | | 10.75% | | 11/1/10 | | 11,678 | |

3,877 | | 11.00% | | 4/1/14 | | 4,264 | |

20,766 | | 11.00% | | 8/1/15 | | 22,050 | |

19,062 | | 11.00% | | 4/1/17 | | 20,487 | |

306,132 | | 11.27% | | 8/15/20 | | 343,000 | |

187,256 | | 11.75% | | 10/20/22 | | 211,210 | |

| | | | | | | |

| | | | | | 56,614,769 | |

| | | | | | | |

| | | | | | | |

Government National Mortgage Association (13.0%) (3): | |

|

Par ($) | | Coupon | | Maturity | | Market Value ($)(1) | |

| | | | | | | | |

411,929 | | 5.50% | | 9/15/25 | | 412,487 | |

133,964 | | 5.76% | | 3/20/33 | | 134,642 | |

82,234 | | 5.76% | | 3/20/33 | | 82,650 | |

110,080 | | 5.76% | | 3/20/33 | | 110,637 | |

351,547 | | 5.76% | | 5/20/33 | | 353,325 | |

115,179 | | 5.76% | | 5/20/33 | | 115,762 | |

93,405 | | 5.76% | | 6/20/33 | | 93,877 | |

107,491 | | 5.76% | | 6/20/33 | | 108,035 | |

69,502 | | 6.00% | | 9/15/18 | | 70,310 | |

82,393 | | 6.05% | | 3/20/33 | | 83,263 | |

239,101 | | 6.25% | | 5/15/13 | | 243,041 | |

343,187 | | 6.25% | | 12/15/23 | | 352,172 | |

231,606 | | 6.25% | | 1/15/24 | | 237,676 | |

218,040 | | 6.38% | | 12/15/27 | | 223,645 | |

297,444 | | 6.38% | | 4/15/28 | | 305,122 | |

248,907 | | 6.49% | | 11/20/31 | | 255,619 | |

48,567 | | 6.49% | | 12/20/31 | | 49,876 | |

257,399 | | 6.49% | | 4/20/32 | | 264,103 | |

74,406 | | 6.49% | | 6/20/32 | | 76,343 | |

55,047 | | 6.49% | | 6/20/32 | | 56,480 | |

88,040 | | 6.49% | | 12/20/32 | | 90,332 | |

16

| | | | |

| | |

| |

| | |

| | |

|

| |

| | | | |

| | | | | | | | | |

| Par ($) | | Coupon | | | Maturity | | Market Value ($)(1) |

| | | | | | | |

| | | | | | | | | |

| 39,347 | | 6.57% | | | 9/20/32 | | | 40,508 |

| 65,957 | | 6.57% | | | 1/20/33 | | | 67,915 |

| 83,858 | | 6.57% | | | 3/20/33 | | | 86,347 |

| 77,858 | | 6.75% | | | 9/15/15 | | | 80,561 |

| 342,657 | | 6.75% | | | 8/15/28 | | | 355,972 |

| 192,538 | | 6.75% | | | 6/15/29 | | | 200,003 |

| 132,520 | | 6.75% | | | 6/15/29 | | | 137,658 |

| 527,295 | | 6.91% | | | 7/20/26 | | | 548,637 |

| 32,899 | | 7.00% | | | 9/20/16 | | | 33,973 |

| 493,822 | | 7.00% | | | 2/15/28 | | | 513,245 |

| 851,976 | | 7.00% | | | 7/15/29 | | | 891,320 |

| 953,684 | | 7.00% | | | 10/15/32 | | | 997,558 |

| 765,486 | | 7.00% | | | 11/15/32 | | | 800,658 |

| 16,964 | | 7.05% | | | 2/15/23 | | | 17,504 |

| 133,469 | | 7.05% | | | 9/20/26 | | | 137,352 |

| 80,648 | | 7.05% | | | 11/20/26 | | | 82,995 |

| 68,048 | | 7.05% | | | 1/20/27 | | | 70,022 |

| 144,318 | | 7.05% | | | 4/20/27 | | | 148,504 |

| 91,966 | | 7.15% | | | 12/20/26 | | | 94,885 |

| 76,082 | | 7.15% | | | 3/20/27 | | | 78,490 |

| 245,992 | | 7.15% | | | 4/20/27 | | | 253,778 |

| 17,873 | | 7.25% | | | 8/15/10 | | | 18,210 |

| 130,330 | | 7.25% | | | 5/15/29 | | | 135,252 |

| 64,113 | | 7.27% | | | 7/20/22 | | | 66,212 |

| 61,183 | | 7.38% | | | 1/15/29 | | | 63,690 |

| 451,959 | | 7.38% | | | 3/15/31 | | | 464,047 |

| 74,054 | | 7.50% | | | 5/15/16 | | | 77,427 |

| 293,359 | | 7.50% | | | 6/15/36 | | | 305,497 |

| 69,383 | | 7.55% | | | 7/20/22 | | | 72,579 |

| 83,749 | | 7.55% | | | 10/20/22 | | | 87,606 |

| 94,718 | | 7.63% | | | 10/15/29 | | | 99,611 |

| 88,535 | | 7.65% | | | 10/20/21 | | | 92,779 |

| 87,214 | | 7.65% | | | 7/20/22 | | | 91,456 |

| 180,911 | | 7.75% | | | 6/15/20 | | | 190,784 |

| 188,268 | | 7.75% | | | 7/15/20 | | | 198,543 |

| 141,766 | | 7.75% | | | 8/15/20 | | | 149,503 |

| 180,364 | | 7.75% | | | 8/15/20 | | | 190,208 |

| 83,199 | | 7.75% | | | 11/15/20 | | | 87,740 |

| 495,749 | | 7.75% | | | 10/15/22 | | | 527,824 |

| 44,163 | | 7.90% | | | 1/20/21 | | | 46,557 |

| 32,302 | | 7.90% | | | 1/20/21 | | | 34,053 |

| 29,481 | | 7.90% | | | 4/20/21 | | | 31,079 |

| 96,903 | | 7.95% | | | 2/15/20 | | | 102,679 |

| 42,471 | | 7.95% | | | 5/20/25 | | | 44,827 |

| 120,747 | | 7.95% | | | 7/20/25 | | | 127,447 |

| 48,590 | | 7.95% | | | 8/20/25 | | | 51,286 |

| 165,992 | | 7.95% | | | 9/20/25 | | | 175,202 |

| 27,243 | | 7.95% | | | 10/20/25 | | | 28,755 |

| 37,639 | | 7.95% | | | 10/20/25 | | | 39,727 |

| | | | | | | | | |

| Par ($) | | Coupon | | | Maturity | | Market Value ($)(1) |

| | | | | | | |

| | | | | | | | | |

| 31,980 | | 7.95% | | | 10/20/25 | | | 33,755 |

| 72,579 | | 7.95% | | | 1/20/26 | | | 76,649 |

| 82,324 | | 7.95% | | | 1/20/26 | | | 86,941 |

| 120,000 | | 7.95% | | | 4/20/26 | | | 126,729 |

| 23,148 | | 7.95% | | | 6/20/26 | | | 24,446 |

| 32,215 | | 7.95% | | | 9/20/26 | | | 34,022 |

| 39,079 | | 7.95% | | | 9/20/26 | | | 41,271 |

| 26,824 | | 7.95% | | | 11/20/26 | | | 28,328 |

| 35,452 | | 7.95% | | | 12/20/26 | | | 37,440 |

| 46,342 | | 7.95% | | | 3/20/27 | | | 48,938 |

| 49,593 | | 7.99% | | | 2/20/21 | | | 52,392 |

| 60,056 | | 7.99% | | | 4/20/21 | | | 63,446 |

| 133,838 | | 7.99% | | | 7/20/21 | | | 141,392 |

| 102,218 | | 7.99% | | | 9/20/21 | | | 107,988 |

| 102,253 | | 7.99% | | | 10/20/21 | | | 108,025 |

| 231,009 | | 7.99% | | | 1/20/22 | | | 244,280 |

| 359,958 | | 7.99% | | | 6/20/22 | | | 380,636 |

| 24,899 | | 8.00% | | | 10/15/12 | | | 26,156 |

| 432,160 | | 8.00% | | | 10/15/14 | | | 457,357 |

| 60,607 | | 8.00% | | | 5/15/16 | | | 64,425 |

| 223,533 | | 8.00% | | | 6/15/16 | | | 237,616 |

| 63,342 | | 8.00% | | | 9/15/16 | | | 67,333 |

| 81,701 | | 8.00% | | | 11/20/16 | | | 85,746 |

| 42,216 | | 8.00% | | | 7/20/23 | | | 44,553 |

| 25,717 | | 8.00% | | | 12/20/23 | | | 27,141 |

| 3,631 | | 8.00% | | | 2/20/24 | | | 3,835 |

| 119,831 | | 8.00% | | | 2/20/26 | | | 126,712 |

| 22,772 | | 8.00% | | | 12/20/26 | | | 24,079 |

| 56,988 | | 8.00% | | | 9/15/29 | | | 60,527 |

| 18,364 | | 8.00% | | | 1/20/32 | | | 19,422 |

| 260,218 | | 8.10% | | | 5/20/19 | | | 275,749 |

| 34,054 | | 8.10% | | | 6/20/19 | | | 36,087 |

| 121,365 | | 8.10% | | | 7/20/19 | | | 128,609 |

| 162,913 | | 8.10% | | | 9/20/19 | | | 172,637 |

| 80,809 | | 8.10% | | | 9/20/19 | | | 85,632 |

| 81,899 | | 8.10% | | | 10/20/19 | | | 86,787 |

| 73,363 | | 8.10% | | | 1/20/20 | | | 77,847 |

| 90,963 | | 8.10% | | | 7/20/20 | | | 96,523 |

| 103,222 | | 8.25% | | | 12/15/11 | | | 108,529 |

| 20,010 | | 8.25% | | | 1/15/12 | | | 21,158 |

| 54,056 | | 8.25% | | | 8/15/15 | | | 57,572 |

| 383,366 | | 8.25% | | | 4/15/19 | | | 409,181 |

| 131,803 | | 8.25% | | | 2/15/20 | | | 140,885 |

| 19,567 | | 8.25% | | | 4/15/27 | | | 20,899 |

| 39,387 | | 8.25% | | | 6/15/27 | | | 42,067 |

| 42,231 | | 8.38% | | | 10/15/19 | | | 45,198 |

| 106,535 | | 8.40% | | | 2/15/19 | | | 114,099 |

| 31,445 | | 8.40% | | | 4/15/19 | | | 33,677 |

| 116,429 | | 8.40% | | | 6/15/19 | | | 124,696 |

| |

See accompanying notes to portfolios of investments on page 62. | 17 |

| | | | |

| Sit U.S. Government Securities Fund | | | |

| March 31, 2007 | | | |

| | | | |

| Portfolio of Investments

| | | |

| | | | |

| | | | | | | | | |

| Par ($) | | Coupon | | | Maturity | | Market Value ($)(1) |

| | | | | | | |

| | | | | | | | | |

| 40,199 | | 8.40% | | | 9/15/19 | | | 43,054 |

| 55,384 | | 8.40% | | | 9/15/19 | | | 59,317 |

| 55,257 | | 8.40% | | | 2/15/20 | | | 59,275 |

| 27,341 | | 8.50% | | | 12/15/11 | | | 28,850 |

| 98,052 | | 8.50% | | | 1/15/12 | | | 104,101 |

| 12,317 | | 8.50% | | | 4/15/15 | | | 13,182 |

| 59,817 | | 8.50% | | | 4/15/15 | | | 64,020 |

| 176,447 | | 8.50% | | | 9/15/16 | | | 189,399 |

| 84,645 | | 8.50% | | | 1/15/17 | | | 91,445 |

| 105,749 | | 8.50% | | | 12/15/21 | | | 113,879 |

| 82,685 | | 8.50% | | | 12/15/21 | | | 88,932 |

| 12,752 | | 8.50% | | | 7/20/22 | | | 13,699 |

| 82,373 | | 8.50% | | | 10/20/22 | | | 88,495 |

| 43,253 | | 8.50% | | | 9/20/24 | | | 46,572 |

| 77,941 | | 8.50% | | | 3/20/25 | | | 83,948 |

| 221,365 | | 8.50% | | | 12/20/26 | | | 236,958 |

| 26,408 | | 8.50% | | | 8/15/30 | | | 28,376 |

| 54,752 | | 8.60% | | | 5/15/18 | | | 58,276 |

| 49,256 | | 8.60% | | | 6/15/18 | | | 52,426 |

| 56,597 | | 8.63% | | | 10/15/18 | | | 60,185 |

| 24,720 | | 8.75% | | | 11/15/09 | | | 25,880 |

| 30,980 | | 8.75% | | | 6/15/11 | | | 32,907 |

| 150,662 | | 8.75% | | | 11/15/11 | | | 160,033 |

| 28,446 | | 8.75% | | | 12/15/11 | | | 30,216 |

| 95,558 | | 8.75% | | | 10/15/30 | | | 103,151 |

| 3,784 | | 9.00% | | | 10/15/07 | | | 3,879 |

| 8,399 | | 9.00% | | | 9/15/08 | | | 8,552 |

| 3,336 | | 9.00% | | | 9/15/08 | | | 3,396 |

| 5,937 | | 9.00% | | | 11/15/08 | | | 6,045 |

| 11,341 | | 9.00% | | | 12/15/08 | | | 11,548 |

| 1,528 | | 9.00% | | | 2/15/09 | | | 1,575 |

| 6,852 | | 9.00% | | | 4/15/09 | | | 7,128 |

| 1,048 | | 9.00% | | | 5/15/09 | | | 1,080 |

| 9,889 | | 9.00% | | | 8/15/09 | | | 10,287 |

| 10,513 | | 9.00% | | | 9/15/09 | | | 10,936 |

| 4,450 | | 9.00% | | | 10/15/09 | | | 4,585 |

| 18,431 | | 9.00% | | | 11/15/09 | | | 19,341 |

| 2,929 | | 9.00% | | | 12/15/09 | | | 3,047 |

| 42,924 | | 9.00% | | | 7/15/10 | | | 44,656 |

| 77,463 | | 9.00% | | | 5/15/11 | | | 82,573 |

| 33,966 | | 9.00% | | | 5/15/11 | | | 36,207 |

| 55,172 | | 9.00% | | | 6/15/11 | | | 58,812 |

| 57,295 | | 9.00% | | | 7/15/11 | | | 61,074 |

| 72,787 | | 9.00% | | | 8/15/11 | | | 77,588 |

| 20,717 | | 9.00% | | | 8/15/11 | | | 22,043 |

| 79,528 | | 9.00% | | | 9/15/11 | | | 84,775 |

| 74,260 | | 9.00% | | | 9/15/11 | | | 79,159 |

| 45,507 | | 9.00% | | | 9/15/11 | | | 48,509 |

| 44,350 | | 9.00% | | | 10/15/11 | | | 47,276 |

| | | | | | | | | |

| Par ($) | | Coupon | | | Maturity | | Market Value ($)(1) |

| | | | | | | |

|

| 12,665 | | 9.00% | | | 1/15/12 | | | 13,585 |

| 43,044 | | 9.00% | | | 5/20/15 | | | 45,788 |

| 112,938 | | 9.00% | | | 7/15/15 | | | 120,590 |

| 33,273 | | 9.00% | | | 8/15/15 | | | 35,528 |

| 91,439 | | 9.00% | | | 12/20/15 | | | 97,269 |

| 14,409 | | 9.00% | | | 5/20/16 | | | 15,378 |

| 393,076 | | 9.00% | | | 12/15/16 | | | 421,078 |

| 107,350 | | 9.00% | | | 1/15/17 | | | 117,098 |

| 9,985 | | 9.00% | | | 3/20/17 | | | 10,662 |

| 317,754 | | 9.00% | | | 7/15/17 | | | 346,608 |

| 187,869 | | 9.00% | | | 8/20/17 | | | 200,608 |

| 2,569 | | 9.00% | | | 7/20/21 | | | 2,762 |

| 1,281 | | 9.00% | | | 10/20/21 | | | 1,377 |

| 261,829 | | 9.00% | | | 11/15/24 | | | 281,890 |

| 36,603 | | 9.00% | | | 7/20/25 | | | 39,509 |

| 126,918 | | 9.00% | | | 4/15/26 | | | 137,428 |

| 22,864 | | 9.10% | | | 5/15/18 | | | 24,719 |

| 50,450 | | 9.25% | | | 11/15/09 | | | 53,426 |

| 22,733 | | 9.25% | | | 1/15/10 | | | 24,276 |

| 28,278 | | 9.25% | | | 4/15/10 | | | 30,197 |

| 23,637 | | 9.25% | | | 11/15/10 | | | 25,241 |

| 56,819 | | 9.25% | | | 11/15/11 | | | 61,176 |

| 10,710 | | 9.25% | | | 4/15/12 | | | 11,609 |

| 11,325 | | 9.50% | | | 9/15/09 | | | 11,708 |

| 68,871 | | 9.50% | | | 10/15/09 | | | 71,201 |

| 15,544 | | 9.50% | | | 10/15/09 | | | 16,070 |

| 4,377 | | 9.50% | | | 10/15/09 | | | 4,525 |

| 21,360 | | 9.50% | | | 11/15/09 | | | 22,672 |

| 55,713 | | 9.50% | | | 1/15/10 | | | 59,673 |

| 12,535 | | 9.50% | | | 2/15/10 | | | 13,080 |

| 35,297 | | 9.50% | | | 4/15/10 | | | 37,428 |

| 18,132 | | 9.50% | | | 8/15/10 | | | 19,421 |

| 30,234 | | 9.50% | | | 11/15/10 | | | 32,383 |

| 9,931 | | 9.50% | | | 1/15/11 | | | 10,730 |

| 72,903 | | 9.50% | | | 3/15/11 | | | 78,771 |

| 14,730 | | 9.50% | | | 3/20/16 | | | 15,915 |

| 42,645 | | 9.50% | | | 11/20/16 | | | 46,074 |

| 3,283 | | 9.50% | | | 8/20/17 | | | 3,558 |

| 3,836 | | 9.50% | | | 12/20/17 | | | 4,158 |

| 5,007 | | 9.50% | | | 4/20/18 | | | 5,442 |

| 1,696 | | 9.50% | | | 5/20/18 | | | 1,843 |

| 36,605 | | 9.50% | | | 6/20/18 | | | 39,785 |

| 30,632 | | 9.50% | | | 7/20/18 | | | 33,294 |

| 21,914 | | 9.50% | | | 8/20/18 | | | 23,818 |

| 73,127 | | 9.50% | | | 9/20/18 | | | 79,481 |

| 42,918 | | 9.50% | | | 9/20/18 | | | 46,647 |

| 12,352 | | 9.50% | | | 9/20/18 | | | 13,425 |

| 30,453 | | 9.50% | | | 8/20/19 | | | 33,178 |

| 2,932 | | 9.50% | | | 10/20/19 | | | 3,194 |

18

| | | | |

| | |

| |

| | |

| | |

|

| |

| | | | |

| | | | | | | | | |

| Par ($) | | Coupon | | | Maturity | | Market Value ($)(1) |

| | | | | | | |

| | | | | | | | | |

| 35,896 | | 9.75% | | | 8/15/09 | | | 38,429 |

| 36,946 | | 9.75% | | | 9/15/09 | | | 39,553 |

| 101,825 | | 9.75% | | | 8/15/10 | | | 110,530 |

| 27,784 | | 9.75% | | | 11/15/10 | | | 30,160 |

| 136,166 | | 9.75% | | | 12/15/10 | | | 147,807 |

| 101,286 | | 9.75% | | | 1/15/11 | | | 111,081 |

| 76,120 | | 9.75% | | | 1/15/11 | | | 83,481 |

| 22,558 | | 9.75% | | | 10/15/12 | | | 24,942 |

| 9,064 | | 9.75% | | | 10/15/12 | | | 10,021 |

| 8,677 | | 9.75% | | | 10/15/12 | | | 9,593 |

| 8,390 | | 9.75% | | | 11/15/12 | | | 9,276 |

| 29,185 | | 9.75% | | | 11/15/12 | | | 32,268 |

| 24,482 | | 9.75% | | | 11/15/12 | | | 27,069 |

| 25,765 | | 9.75% | | | 11/15/12 | | | 28,487 |

| 14,965 | | 10.00% | | | 11/15/08 | | | 15,775 |

| 1,242 | | 10.00% | | | 11/15/09 | | | 1,302 |

| 4,038 | | 10.00% | | | 6/15/10 | | | 4,397 |

| 58,425 | | 10.00% | | | 6/15/10 | | | 63,609 |

| 18,985 | | 10.00% | | | 7/15/10 | | | 20,670 |

| 8,247 | | 10.00% | | | 7/15/10 | | | 8,979 |

| 7,787 | | 10.00% | | | 10/15/10 | | | 8,478 |

| 44,490 | | 10.00% | | | 11/15/10 | | | 48,437 |

| 31,138 | | 10.00% | | | 3/20/16 | | | 34,380 |

| 17,342 | | 10.00% | | | 11/15/17 | | | 19,274 |

| 31,531 | | 10.00% | | | 2/15/19 | | | 35,059 |

| 19,689 | | 10.00% | | | 2/20/19 | | | 21,814 |

| 21,181 | | 10.00% | | | 3/20/19 | | | 23,467 |

| 16,022 | | 10.00% | | | 5/20/19 | | | 17,751 |

| 173,439 | | 10.00% | | | 10/15/19 | | | 197,095 |

| 39,830 | | 10.00% | | | 11/15/19 | | | 44,287 |

| 31,523 | | 10.00% | | | 12/15/20 | | | 35,095 |

| 103,611 | | 10.00% | | | 6/15/21 | | | 115,483 |

| 23,765 | | 10.25% | | | 5/15/09 | | | 25,192 |

| 17,333 | | 10.25% | | | 11/15/11 | | | 18,790 |

| 19,962 | | 10.25% | | | 1/15/12 | | | 21,885 |

| 7,757 | | 10.25% | | | 2/15/12 | | | 8,504 |

| 7,593 | | 10.25% | | | 7/15/12 | | | 8,324 |

| 24,334 | | 10.50% | | | 6/15/09 | | | 25,855 |

| 4,699 | | 10.50% | | | 7/15/10 | | | 5,044 |

| 9,344 | | 10.50% | | | 9/15/15 | | | 10,368 |

| 12,218 | | 10.50% | | | 11/15/15 | | | 13,557 |

| 3,176 | | 10.50% | | | 8/20/17 | | | 3,530 |

| 46,928 | | 10.50% | | | 11/15/18 | | | 52,445 |

| 41,723 | | 10.50% | | | 6/15/19 | | | 46,768 |

| 213,229 | | 10.50% | | | 2/15/20 | | | 238,036 |

| 161,804 | | 10.50% | | | 8/15/21 | | | 183,866 |

| 2,721 | | 10.75% | | | 1/15/10 | | | 2,952 |

| 1,227 | | 10.75% | | | 7/15/11 | | | 1,340 |

| 19,728 | | 11.25% | | | 6/15/10 | | | 21,579 |

| | | | | | | | | |

| Par ($) | | Coupon | | | Maturity | | Market Value ($)(1) |

| | | | | | | |

| | | | | | | | | |

| 30,520 | | 11.25% | | | 9/15/10 | | | 33,384 |

| 3,811 | | 11.25% | | | 9/15/10 | | | 4,168 |

| 16,813 | | 11.25% | | | 3/15/11 | | | 18,514 |

| 7,582 | | 11.25% | | | 3/15/11 | | | 8,349 |

| 37,416 | | 11.25% | | | 4/15/11 | | | 41,200 |

| 8,652 | | 11.25% | | | 5/15/11 | | | 9,527 |

| 28,197 | | 11.25% | | | 7/15/11 | | | 31,049 |

| 6,050 | | 11.25% | | | 7/15/11 | | | 6,661 |

| 4,748 | | 11.25% | | | 7/15/11 | | | 5,229 |

| 13,242 | | 11.25% | | | 9/15/11 | | | 14,581 |

| 10,147 | | 11.25% | | | 10/15/11 | | | 11,174 |

| 88,714 | | 11.50% | | | 8/15/18 | | | 97,441 |

| | | | | | | | |

| | | | | | | | | 25,760,558 |

| | | | | | | | |

Total mortgage pass-through securities

(cost: $108,934,932) | | | | 108,684,289 |

| | | | | |

Taxable Municipal Securities (0.3%) (2)

| | | | | |

205,000 | | Bernalillo Multifamily Rev. Series | | | |

| | 1998A, 7.50%, 9/20/20 | | | 217,156 |

20,000 | | Cuyahoga County Multifamily Rev. | | | |

| | Series 2000B, 7.00%, 1/20/08 | | | 20,182 |

30,000 | | Louisiana Comm. Dev. Auth Rev. | | | |

| | Series 2002B, 5.25%, 12/20/07 | | | 29,918 |

370,000 | | Maplewood Multifamily Rev. | | | |

| | Series 1998B, 6.75%, 7/20/15 | | | 371,765 |

| | | | |

Total taxable municipal securities

(cost: $625,000) | | | 639,021 |

| | | | |

U.S. Treasury / Federal Agency Securities (9.2%) (2)

| | | | | |

5,000,000 | | FNMA Strip, zero coupon, | | | |

| | 4.88% effective yield, 11/15/30 | | | 1,475,985 |

3,000,000 | | U.S. Treasury Bond, 4.50%, 11/30/11 | | | 2,995,194 |

2,800,000 | | U.S. Treasury Note, 3.375%, 9/15/09 | | | 2,722,672 |

3,750,000 | | U.S. Treasury Note, 4.50%, 11/15/10 | | | 3,747,071 |

| | U.S. Treasury Strips, Zero Coupon: | | | |

3,500,000 | | 5.45% Effective Yield, 5/15/30 | | | 1,132,628 |

2,200,000 | | 4.60% Effective Yield, 8/15/16 | | | 2,234,890 |

3,734,024 | | U.S. Treasury inflation-protected security, | |

| | 3.375%, 1/15/12 (*) | | | 3,961,419 |

| | | | |

Total U.S. Treasury / Federal Agency securities

(cost: $18,316,378) | | | 18,269,859 |

| | |

Collateralized Mortgage Obligations (35.1%) (2)

Federal Home Loan Mortgage Corp.:

| | | | | | | | | |

| Par ($) | | Coupon | | | Maturity | | Market Value ($)(1) |

| | | | | | | |

| 597,577 | | 3.00% | | | 2/15/23 | | | 552,486 |

| |

See accompanying notes to portfolios of investments on page 62. | 19 |

| | | | |

| Sit U.S. Government Securities Fund | | | |

| March 31, 2007 | | | |

| | | | |

| Portfolio of Investments

| | | |

| | | | |

| | | | | | | | | |

| Par ($) | | Coupon | | | Maturity | | Market Value ($)(1) |

| | | | | | | |

| | | | | | | | | |

| 3,103,713 | | 3.25% | | | 4/15/32 | | | 2,895,825 |

| 632,671 | | 3.50% | | | 5/15/29 | | | 599,516 |

| 601,552 | | 4.00% | | | 11/15/14 | | | 584,093 |

| 2,683,573 | | 4.00% | | | 5/31/25 | | | 2,481,647 |

| 325,074 | | 4.00% | | | 12/15/32 | | | 308,626 |

| 1,028,473 | | 4.50% | | | 5/15/32 | | | 1,011,838 |

| 500,000 | | 5.50% | | | 7/15/31 | | | 502,204 |

| 5,000,000 | | 5.50% | | | 3/15/32 | | | 4,996,275 |

| 789,287 | | 6.95% | | | 3/15/28 | | | 815,885 |

| 517,644 | | 7.50% | | | 6/15/17 | | | 543,433 |

| 263,930 | | 7.50% | | | 9/15/30 | | | 269,875 |

| 17,335 | | 7.75% | | | 3/18/25 | | | 17,506 |

| 242,502 | | 8.00% | | | 11/25/22 | | | 250,857 |

| 89,052 | | 8.00% | | | 3/15/23 | | | 92,728 |

| 106,583 | | 8.00% | | | 4/25/24 | | | 113,979 |

| 31,024 | | 9.15% | | | 10/15/20 | | | 32,572 |

| 1,451,361 | | 9.50% | | | 2/15/20 | | | 1,516,227 |

| | | | | | | | | |

| | | | | | | | | 17,585,572 |

| | | | | | | | | |

| | | | | | |

Federal National Mortgage Association: | | |

| | | | | | |

| Par ($) | | Coupon | | | Maturity | | Market Value ($)(1) |

| | | | | | | |

| 3,348,105 | | 3.50% | | | 2/25/33 | | | 3,073,145 |

| 733,927 | | 3.50% | | | 3/25/33 | | | 698,911 |

| 352,963 | | 3.50% | | | 8/25/33 | | | 321,523 |

| 1,454,425 | | 3.50% | | | 6/25/35 | | | 1,400,242 |

| 921,103 | | 3.75% | | | 5/25/33 | | | 853,931 |

| 1,186,248 | | 4.00% | | | 11/25/32 | | | 1,143,830 |

| 345,454 | | 4.00% | | | 1/25/33 | | | 330,780 |

| 1,503,851 | | 4.00% | | | 3/25/33 | | | 1,424,399 |

| 1,725,186 | | 4.00% | | | 5/25/33 | | | 1,652,313 |

| 226,244 | | 5.00% | | | 8/25/22 | | | 222,951 |

| 1,700,000 | | 5.00% | | | 12/25/31 | | | 1,642,976 |

| 5,125,203 | | 5.50% | | | 5/25/25 | | | 5,099,363 |

| 3,787,251 | | 6.50% | | | 10/25/17 | | | 3,886,778 |

| 86,047 | | 6.85% | | | 12/18/27 | | | 88,786 |

| 106,788 | | 7.00% | | | 1/25/21 | | | 109,778 |

| 46,290 | | 7.70% | | | 3/25/23 | | | 48,789 |

| 230,864 | | 8.00% | | | 7/25/22 | | | 245,217 |

| 275,013 | | 8.00% | | | 7/25/22 | | | 284,250 |

| 100,000 | | 8.00% | | | 7/18/27 | | | 111,798 |

| 407,469 | | 8.00% | | | 7/25/44 | | | 428,368 |

| 78,745 | | 8.20% | | | 4/25/25 | | | 81,118 |

| 37,810 | | 8.50% | | | 1/25/21 | | | 40,340 |

| 41,112 | | 8.50% | | | 4/25/21 | | | 42,333 |

| 333,459 | | 8.50% | | | 9/25/21 | | | 358,705 |

| 94,415 | | 8.50% | | | 1/25/25 | | | 99,712 |

| 416,109 | | 8.50% | | | 6/25/30 | | | 496,204 |

| 73,019 | | 8.75% | | | 9/25/20 | | | 75,999 |

| 179,757 | | 8.95% | | | 10/25/20 | | | 193,489 |

| 547,169 | | 9.00% | | | 7/25/19 | | | 585,412 |

| | | | | | | | | |

| Par ($) | | Coupon | | | Maturity | | Market Value ($)(1) |

| | | | | | | |

| | | | | | | | | |

| 290,146 | | 9.00% | | | 12/25/19 | | | 311,754 |

| 105,093 | | 9.00% | | | 5/25/20 | | | 110,985 |

| 71,327 | | 9.00% | | | 6/25/20 | | | 76,733 |

| 162,344 | | 9.00% | | | 6/25/20 | | | 172,013 |

| 28,014 | | 9.00% | | | 7/25/20 | | | 30,369 |

| 150,528 | | 9.00% | | | 9/25/20 | | | 161,988 |

| 97,813 | | 9.00% | | | 10/25/20 | | | 105,598 |

| 212,876 | | 9.00% | | | 3/1/24 | | | 230,473 |

| 1,354,206 | | 9.00% | | | 11/25/28 | | | 1,498,387 |

| 157,260 | | 9.25% | | | 1/25/20 | | | 169,933 |

| 148,721 | | 9.50% | | | 12/25/18 | | | 161,548 |

| 272,344 | | 9.50% | | | 3/25/20 | | | 297,870 |

| 67,504 | | 9.50% | | | 4/25/20 | | | 71,754 |