Dear Fellow Shareholders:

We are pleased to report a strong start to 2019.We ended our first quarter with record quarterly net income of$14.3 million, compared to $12.8 million for the first quarter of 2018, and diluted earnings per share of $0.91, an 11% increase from a year ago. Our financial performance was powered by steady loan and deposit growth, a positive return on investments and a stable credit environment.

Our primary source of revenues is net interest income and for the first quarter of 2019 totaled $31.9 million, an increase of nearly $3.0 million, or 10%, over the first quarter of 2018. Increased net interest income reflects major investments we made in our employees and in products and services to support loan and deposit growth.

We increased lending activity by leveraging digital platforms, such as MortgageTouch®, our online residential mortgage solution, and hiring experienced lenders within our growth markets. At March 31, 2019, total loans of $3.1 billion were up $252.5 million, or 9%, from a year ago. Residential mortgages grew 18% and commercial real estate grew 8%.

Total deposits grew 18% to $3.6 billion at March 31, 2019, compared to a year ago, led by checking, savings and money market deposit growth of $407.0 million, or 18%. Equipped with extensive training, our retail banking teams serve as experts and consultants to individuals, families and small businesses, and our corporate treasury management team offers online cash management and in-person guidance to commercial customers.

Our net interest margin for the first quarter of 2019 expanded to 3.18%, compared to 3.10% for the first quarter of 2018. Our asset yield increased 42 basis points to 4.20%, compared to the first quarter of 2018, while our cost of funds increased 35 basis points over the same period to 1.07%. More importantly, our loan-to-deposit ratio improved to 85% at March 31, 2019, compared to 92% at March 31, 2018. In comparison, the average loan-to-deposit ratio for all other Maine-based banks at December 31, 2018 was 104%.

Asset quality through the first quarter of 2019 remained strong with annualized average net charge offs of 0.03% of average loans, compared to 0.10% for the same period last year. Non-performing assets at March 31, 2019, were 0.33% of total assets, comparing favorably to 0.47% recorded a year prior.

We are closely monitoring changing economic conditions, including the overall level of interest rates and the yield curve. There is increased market concern of an inverted yield curve where short-term rates exceed long-term rates. One of our key elements of managing interest rate risk is a strong core deposit base, which we have expanded through product and service innovation. Over the past several years, we have also invested in resources to adopt the new accounting standard for loan loss reserves (commonly referred to as “CECL”) that goes into effect January 1, 2020.

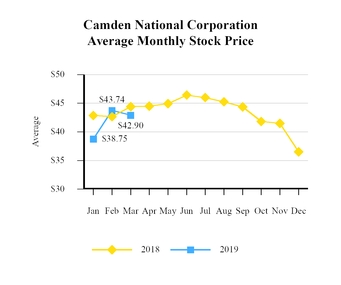

Our first quarter 2019 performance yielded strong financial metrics, including a return on average equity of 13.13%, a return on average assets of 1.33% and an efficiency ratio of 54.86%. During the first three months of 2019, we repurchased 55,557 shares of our common stock and provided a cash dividend of $0.30 per common share.

As a full-service community bank, social responsibility is core to our heritage and impact. We are proud to provide financial guidance and expertise to customers, make direct donations to nonprofit organizations and volunteer our time to support the people and organizations that make our towns and neighborhoods such amazing places to live and work. Through our Hope@Home program alone, we have donated over $385,000 in unrestricted funding to homeless shelters across our communities. In addition, this year we celebrated 10 years of supporting Maine’s High School Basketball State Championship games. Over the past decade, more than 10,000 students have been able to attend over 70 championship games through our support. We credit this company-wide tradition to our dedicated employees who have been inspired to help, knowing that many high school students cannot afford to purchase tickets to see their classmates compete.

Our financial performance and community impact result from a strong, talented team of employees, backed by shareholders who understand the unique value we bring to all of the people, communities and organizations we serve. We greatly appreciate your support.

Sincerely,

Gregory A. Dufour

President and Chief Executive Officer

First Quarter Report - 2019

First Quarter Report - 2019