UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number 811-4085

Fidelity Income Fund

(Exact name of registrant as specified in charter)

82 Devonshire St., Boston, Massachusetts 02109

(Address of principal executive offices) (Zip code)

Scott C. Goebel, Secretary

82 Devonshire St.

Boston, Massachusetts 02109

(Name and address of agent for service)

Registrant's telephone number, including area code: 617-563-7000

Date of fiscal year end: | August 31 |

|

|

Date of reporting period: | August 31, 2011 |

This report on Form N-CSR relates solely to the Registrant's Fidelity Total Bond Fund series (the "Fund").

Item 1. Reports to Stockholders

Fidelity®

Total Bond

Fund

Annual Report

August 31, 2011

(2_fidelity_logos) (Registered_Trademark)

Contents

Chairman's Message | The Chairman's message to shareholders. | |

Performance | How the fund has done over time. | |

Management's Discussion of Fund Performance | The Portfolio Manager's review of fundperformance and strategy. | |

Shareholder Expense Example | An example of shareholder expenses. | |

Investment Changes | A summary of major shifts in the fund's investments over the past six months. | |

Investments | A complete list of the fund's investments with their market values. | |

Financial Statements | Statements of assets and liabilities, operations, and changes in net assets, | |

Notes | Notes to the financial statements. | |

Report of Independent Registered Public Accounting Firm |

| |

Trustees and Officers |

| |

Distributions |

|

To view a fund's proxy voting guidelines and proxy voting record for the 12-month period ended June 30, visit http://www.fidelity.com/proxyvotingresults or visit the Securities and Exchange Commission's (SEC) web site at http://www.sec.gov. You may also call 1-800-544-8544 to request a free copy of the proxy voting guidelines.

Standard & Poor's, S&P and S&P 500 are registered service marks of The McGraw-Hill Companies, Inc. and have been licensed for use by Fidelity Distributors Corporation.

Other third party marks appearing herein are the property of their respective owners.

All other marks appearing herein are registered or unregistered trademarks or service marks of FMR LLC or an affiliated company.

This report and the financial statements contained herein are submitted for the general information of the shareholders of the fund. This report is not authorized for distribution to prospective investors in the fund unless preceded or accompanied by an effective prospectus.

A fund files its complete schedule of portfolio holdings with the SEC for the first and third quarters of each fiscal year on Form N-Q. Forms N-Q are available on the SEC's web site at http://www.sec.gov. A fund's Forms N-Q may be reviewed and copied at the SEC's Public Reference Room in Washington, DC. Information regarding the operation of the SEC's Public Reference Room may be obtained by calling 1-800-SEC-0330. For a complete list of a fund's portfolio holdings, view the most recent holdings listing, semiannual report, or annual report on Fidelity's web site at http://www.fidelity.com, http://www.advisor.fidelity.com, or http://www.401k.com, as applicable.

NOT FDIC INSURED • MAY LOSE VALUE • NO BANK GUARANTEE

Neither the fund nor Fidelity Distributors Corporation is a bank.

Annual Report

Chairman's Message

(photo_of_Abigail_P_Johnson)

Dear Shareholder:

U.S. equities remained in a significant midyear downturn that began in May and intensified in the final week of July and the early part of August, when Standard & Poor's announced it was lowering its long-term sovereign credit rating of the United States. The historic downgrade followed a political stalemate in which Congress struggled to address the debt ceiling issue before an early-August deadline, resulting in heightened investor anxiety and volatility across major financial markets. Financial markets are always unpredictable, of course, but there are several time-tested investment principles that can help put the odds in your favor.

One of the basic tenets is to invest for the long term. Over time, riding out the markets' inevitable ups and downs has proven much more effective than selling into panic or chasing the hottest trend. Even missing only a few of the markets' best days can significantly diminish investor returns. Patience also affords the benefits of compounding - of earning interest on additional income or reinvested dividends and capital gains. There can be tax advantages and cost benefits to consider as well. While staying the course doesn't eliminate risk, it can considerably lessen the effect of short-term declines.

You can further manage your investing risk through diversification. And today, more than ever, geographic diversification should be taken into account. Studies indicate that asset allocation is the single most important determinant of a portfolio's long-term success. The right mix of stocks, bonds and cash - aligned to your particular risk tolerance and investment objective - is very important. Age-appropriate rebalancing is also an essential aspect of asset allocation. For younger investors, an emphasis on equities - which historically have been the best-performing asset class over time - is encouraged. As investors near their specific goal, such as retirement or sending a child to college, consideration may be given to replacing volatile assets (e.g. common stocks) with more-stable fixed investments (bonds or savings plans).

A third principle - investing regularly - can help lower the average cost of your purchases. Investing a certain amount of money each month or quarter helps ensure you won't pay for all your shares at market highs. This strategy - known as dollar cost averaging - also reduces "emotion" from investing, helping shareholders avoid selling weak performers just prior to an upswing, or chasing a hot performer just before a correction.

We invite you to contact us via the Internet, through our Investor Centers or by phone. It is our privilege to provide you the information you need to make the investments that are right for you.

Sincerely,

(The chairman's signature appears here.)

Abigail P. Johnson

Annual Report

Performance: The Bottom Line

Average annual total return reflects the change in the value of an investment, assuming reinvestment of the class' distributions from dividend income and capital gains (the profits earned upon the sale of securities that have grown in value, if any) and assuming a constant rate of performance each year. The $10,000 table and the fund's returns do not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares. During periods of reimbursement by Fidelity, a fund's total return will be greater than it would be had the reimbursement not occurred. How a fund did yesterday is no guarantee of how it will do tomorrow.

Average Annual Total Returns

Periods ended August 31, 2011 | Past 1 | Past 5 | Life of |

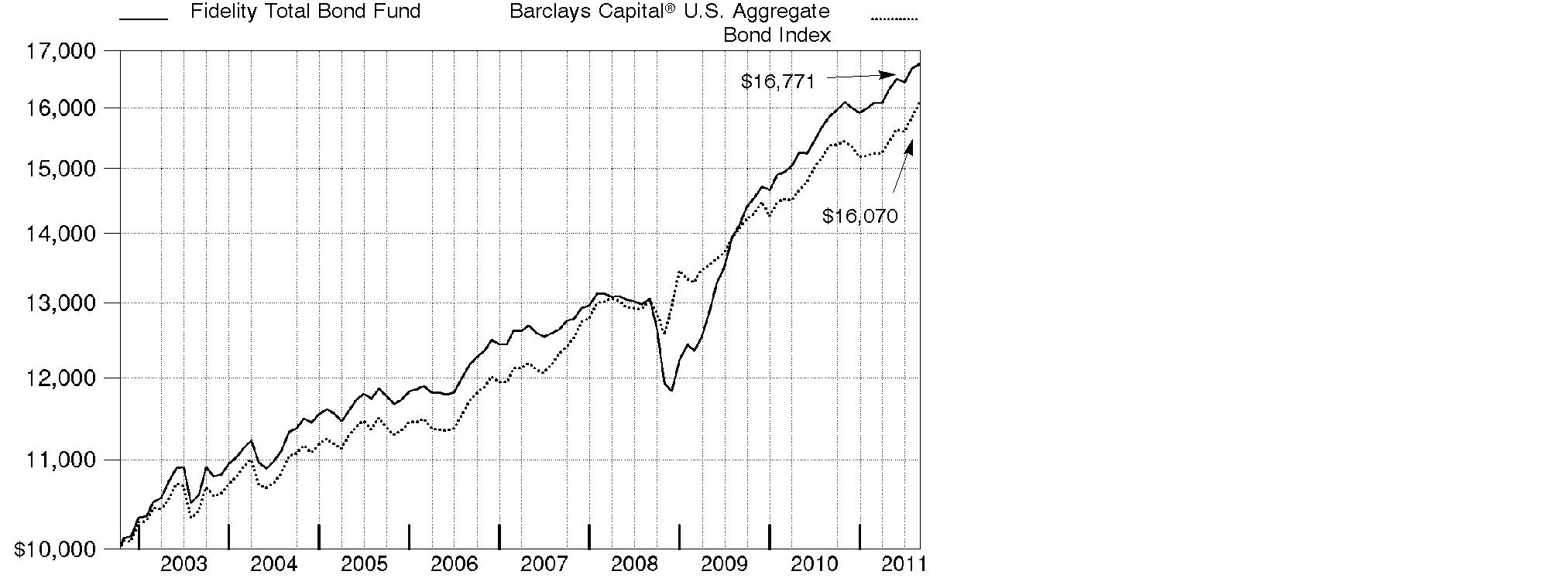

Fidelity® Total Bond Fund | 5.76% | 6.64% | 5.99% |

A From October 15, 2002.

$10,000 Over Life of Fund

Let's say hypothetically that $10,000 was invested in Fidelity® Total Bond Fund, a class of the fund, on October 15, 2002, when the fund started. The chart shows how the value of your investment would have changed, and also shows how the Barclays Capital® U.S. Aggregate Bond Index performed over the same period.

Annual Report

Management's Discussion of Fund Performance

Market Recap: Against the backdrop of ultra-low interest rates and heightened volatility, U.S. taxable investment-grade bonds generated moderate gains for the year ending August 31, 2011, as evidenced by the 4.62% advance of the Barclays Capital® U.S. Aggregate Bond Index. Among the sectors that comprise the index, the best performers were on the riskier end of the spectrum, bolstered by improving economic data. Buoyed by a strong first half, commercial mortgage-backed securities (CMBS) fared best, gaining 5.94% amid continued modest improvement in commercial real estate fundamentals. Investment-grade corporate bonds rose 4.98%, due in large part to increased corporate profitability, high cash balances, reduced debt levels and improved credit conditions. Residential mortgage-backed securities also rose 4.98%, supported by a combination of slower-than-expected prepayments and strong demand from investors seeking higher-yielding alternatives to government bonds. Meanwhile, U.S. Treasury bonds gained 4.17%. After underperforming in the first half, when economic data was strong, Treasuries performed exceedingly well in the second half, when the economy weakened, sovereign debt woes in Europe worsened, Congress wrangled over raising the federal debt ceiling and Standard & Poor's downgraded the long-term sovereign credit rating of the United States. U.S. Government agency securities returned 3.04%.

Comments from Ford O'Neil, Lead Portfolio Manager of Fidelity® Total Bond Fund: For the year, the fund's Retail Class shares returned 5.76%, outpacing the Barclays Capital® U.S. Aggregate Bond Index and the 4.81% return of the Barclays Capital U.S. Universal Bond Index. As I review performance, I'll address the aggregate of my direct investments and those I made in Fidelity's fixed-income central funds. Versus the Aggregate Bond index, sector allocation and security selection within the investment-grade portion of the fund provided the biggest boost. Specifically, an out-of-index stake in Treasury Inflation-Protected Securities (TIPS) contributed, as did a significant overweighting in commercial mortgage-backed securities (CMBS). Good picks among residential mortgage-backed securities worked to our advantage, making up for the unhelpful decision to underweight agency MBS. Out-of-index holdings in collateralized mortgage obligations (CMOs) contributed as well, along with allocations to high-yield corporate and emerging-markets bonds. However, the fund's positioning among high-grade corporates showed mixed results. An emphasis on financials detracted, although we had good security selection there and also benefited from overweighting utilities.

The views expressed above reflect those of the portfolio manager(s) only through the end of the period as stated on the cover of this report and do not necessarily represent the views of Fidelity or any other person in the Fidelity organization. Any such views are subject to change at any time based upon market or other conditions and Fidelity disclaims any responsibility to update such views. These views may not be relied on as investment advice and, because investment decisions for a Fidelity fund are based on numerous factors, may not be relied on as an indication of trading intent on behalf of any Fidelity fund.

Annual Report

Shareholder Expense Example

As a shareholder of the Fund, you incur two types of costs: (1) transaction costs, including sales charges (loads) on purchase payments or redemption proceeds, and (2) ongoing costs, including management fees, distribution and/or service (12b-1) fees and other Fund expenses. This Example is intended to help you understand your ongoing costs (in dollars) of investing in the Fund and to compare these costs with the ongoing costs of investing in other mutual funds.

The Example is based on an investment of $1,000 invested at the beginning of the period and held for the entire period (March 1, 2011 to August 31, 2011).

Actual Expenses

The first line of the accompanying table for each class of the Fund provides information about actual account values and actual expenses. You may use the information in this line, together with the amount you invested, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000.00 (for example, an $8,600 account value divided by $1,000.00 = 8.6), then multiply the result by the number in the first line for a class of the Fund under the heading entitled "Expenses Paid During Period" to estimate the expenses you paid on your account during this period. In addition, the Fund, as a shareholder in the underlying Fidelity Central Funds, will indirectly bear its pro-rata share of the fees and expenses incurred by the underlying Fidelity Central Funds. These fees and expenses are not included in the Fund's annualized expense ratio used to calculate the expense estimate in the table below.

Hypothetical Example for Comparison Purposes

The second line of the accompanying table for each class of the Fund provides information about hypothetical account values and hypothetical expenses based on a Class' actual expense ratio and an assumed rate of return of 5% per year before expenses, which is not the Class' actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing costs of investing in the Fund and other funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of the other funds. In addition, the Fund, as a shareholder in the underlying Fidelity Central Funds, will indirectly bear its pro-rata share of the fees and expenses incurred by the underlying Fidelity Central Funds. These fees and expenses are not included in the Fund's annualized expense ratio used to calculate the expense estimate in the table below.

Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any transaction costs. Therefore, the second line of the table is useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds. In addition, if these transactional costs were included, your costs would have been higher.

Annual Report

Shareholder Expense Example - continued

| Annualized Expense Ratio | Beginning | Ending | Expenses Paid |

Class A | .82% |

|

|

|

Actual |

| $ 1,000.00 | $ 1,040.90 | $ 4.22 |

HypotheticalA |

| $ 1,000.00 | $ 1,021.07 | $ 4.18 |

Class T | .77% |

|

|

|

Actual |

| $ 1,000.00 | $ 1,041.10 | $ 3.96 |

HypotheticalA |

| $ 1,000.00 | $ 1,021.32 | $ 3.92 |

Class B | 1.50% |

|

|

|

Actual |

| $ 1,000.00 | $ 1,037.30 | $ 7.70 |

HypotheticalA |

| $ 1,000.00 | $ 1,017.64 | $ 7.63 |

Class C | 1.49% |

|

|

|

Actual |

| $ 1,000.00 | $ 1,037.40 | $ 7.65 |

HypotheticalA |

| $ 1,000.00 | $ 1,017.69 | $ 7.58 |

Total Bond | .45% |

|

|

|

Actual |

| $ 1,000.00 | $ 1,042.80 | $ 2.32 |

HypotheticalA |

| $ 1,000.00 | $ 1,022.94 | $ 2.29 |

Institutional Class | .53% |

|

|

|

Actual |

| $ 1,000.00 | $ 1,041.50 | $ 2.73 |

HypotheticalA |

| $ 1,000.00 | $ 1,022.53 | $ 2.70 |

A 5% return per year before expenses

* Expenses are equal to each Class' annualized expense ratio, multiplied by the average account value over the period, multiplied by 184/365 (to reflect the one-half year period). The fees and expenses of the underlying Fidelity Central Funds in which the Fund invests are not included in the Fund's annualized expense ratio.

Annual Report

Investment Changes (Unaudited)

The information in the following tables is based on the combined investments of the Fund and its pro-rata share of its investments in each non-money market Fidelity Central Fund.

Quality Diversification (% of fund's net assets) | |||||||

As of August 31, 2011 | As of February 28, 2011 | ||||||

| U.S. Government |

| | U.S. Government |

| ||

| AAA 6.8% |

| | AAA 7.4% |

| ||

| AA 2.6% |

| | AA 3.0% |

| ||

| A 6.6% |

| | A 6.7% |

| ||

| BBB 11.3% |

| | BBB 11.2% |

| ||

| BB and Below 10.0% |

| | BB and Below 11.5% |

| ||

| Not Rated 0.9% |

| | Not Rated 0.8% |

| ||

| Equities 0.1% |

| | Equities 0.2% |

| ||

| Short-Term |

| | Short-Term |

| ||

We have used ratings from Moody's Investors Service, Inc. Where Moody's® ratings are not available, we have used S&P® ratings. All ratings are as of the date indicated and do not reflect subsequent changes. Securities rated BB or below were rated investment grade at the time of acquisition. |

Weighted Average Maturity as of August 31, 2011 | ||

|

| 6 months ago |

Years | 6.2 | 6.7 |

This is a weighted average of all the maturities of the securities held in a fund. Weighted Average Maturity (WAM) can be used as a measure of sensitivity to interest rate changes and markets changes. Generally, the longer the maturity, the greater the sensitivity to such changes. WAM is based on the dollar-weighted average length of time until principal payments must be paid. Depending on the types of securities held in a fund, certain maturity shortening devices (e.g., demand features, interest rate resets, and call options) may be taken into account when calculating the WAM. |

Duration as of August 31, 2011 | ||

|

| 6 months ago |

Years | 4.3 | 4.6 |

Duration estimates how much a bond fund's price will change with a change in comparable interest rates. If rates rise 1%, for example, a fund with a 5-year duration is likely to lose about 5% of its value. Other factors also can influence a bond fund's performance and share price. Accordingly, a bond fund's actual performance may differ from this example. Duration takes into account any call or put option embedded in the bonds. |

Asset Allocation (% of fund's net assets) | |||||||

As of August 31, 2011 * | As of February 28, 2011 ** | ||||||

| Corporate Bonds 23.1% |

| | Corporate Bonds 24.6% |

| ||

| U.S. Government |

| | U.S. Government |

| ||

| Asset-Backed |

| | Asset-Backed |

| ||

| CMOs and Other Mortgage Related Securities 7.6% |

| | CMOs and Other Mortgage Related Securities 8.3% |

| ||

| Municipal Bonds 0.2% |

| | Municipal Bonds 0.3% |

| ||

| Stocks 0.1% |

| | Stocks 0.2% |

| ||

| Other Investments 4.9% |

| | Other Investments 4.9% |

| ||

| Short-Term |

| | Short-Term |

| ||

* Foreign investments | 5.3% |

| ** Foreign investments | 6.2% |

| ||

* Futures and Swaps | 1.1% |

| ** Futures and Swaps | 1.4% |

| ||

† Short-Term Investments and Net Other Assets are not included in the pie chart.

A holdings listing for the Fund, which presents direct holdings as well as the pro-rata share of any securities and other investments held indirectly through its investment in underlying non-money market Fidelity Central Funds is available at fidelity.com and/or advisor.fidelity.com as applicable.

Annual Report

Investments August 31, 2011

Showing Percentage of Net Assets

Corporate Bonds - 23.0% | ||||

| Principal | Value | ||

Convertible Bonds - 0.0% | ||||

FINANCIALS - 0.0% | ||||

Real Estate Investment Trusts - 0.0% | ||||

Developers Diversified Realty Corp. 3% 3/15/12 | $ 270,000 | $ 270,000 | ||

Inland Real Estate Corp. 4.625% 11/15/26 | 233,000 | 232,720 | ||

| 502,720 | |||

Nonconvertible Bonds - 23.0% | ||||

CONSUMER DISCRETIONARY - 2.4% | ||||

Auto Components - 0.1% | ||||

DaimlerChrysler NA Holding Corp. 5.75% 9/8/11 | 6,978,000 | 6,979,968 | ||

Dana Holding Corp.: | ||||

6.5% 2/15/19 | 575,000 | 557,750 | ||

6.75% 2/15/21 | 1,370,000 | 1,328,900 | ||

Delphi Corp.: | ||||

5.875% 5/15/19 (d) | 990,000 | 960,300 | ||

6.125% 5/15/21 (d) | 920,000 | 892,400 | ||

Tenneco, Inc.: | ||||

6.875% 12/15/20 | 1,505,000 | 1,520,050 | ||

7.75% 8/15/18 | 1,400,000 | 1,400,000 | ||

| 13,639,368 | |||

Automobiles - 0.1% | ||||

Automotores Gildemeister SA 8.25% 5/24/21 (d) | 575,000 | 583,625 | ||

Chrysler Group LLC/CG Co-Issuer, Inc.: | ||||

8% 6/15/19 (d) | 2,160,000 | 1,863,000 | ||

8.25% 6/15/21 (d) | 1,070,000 | 912,175 | ||

Ford Motor Co. 7.45% 7/16/31 | 2,715,000 | 2,969,637 | ||

| 6,328,437 | |||

Distributors - 0.0% | ||||

AmeriGas Partners LP/AmeriGas Finance Corp.: | ||||

6.25% 8/20/19 | 1,255,000 | 1,220,488 | ||

6.5% 5/20/21 | 790,000 | 774,200 | ||

Ferrellgas LP/Ferrellgas Finance Corp. 6.5% 5/1/21 | 1,405,000 | 1,260,988 | ||

| 3,255,676 | |||

Diversified Consumer Services - 0.0% | ||||

Visant Corp. 10% 10/1/17 | 1,320,000 | 1,280,400 | ||

Corporate Bonds - continued | ||||

| Principal | Value | ||

Nonconvertible Bonds - continued | ||||

CONSUMER DISCRETIONARY - continued | ||||

Hotels, Restaurants & Leisure - 0.2% | ||||

Ameristar Casinos, Inc. 7.5% 4/15/21 (d) | $ 1,620,000 | $ 1,603,800 | ||

Chukchansi Economic Development Authority 8% 11/15/13 (d) | 765,000 | 558,450 | ||

CityCenter Holdings LLC/CityCenter Finance Corp.: | ||||

7.625% 1/15/16 (d) | 2,590,000 | 2,564,100 | ||

11.5% 1/15/17 pay-in-kind (d)(k) | 622,794 | 596,879 | ||

FelCor Escrow Holdings, LLC 6.75% 6/1/19 (d) | 2,675,000 | 2,507,813 | ||

GWR Operating Partnership LLP/Great Wolf Finance Corp. 10.875% 4/1/17 | 1,635,000 | 1,708,575 | ||

Host Marriott LP 6.375% 3/15/15 | 250,000 | 252,500 | ||

ITT Corp. 7.375% 11/15/15 | 250,000 | 276,250 | ||

MGM Mirage, Inc.: | ||||

6.625% 7/15/15 | 2,315,000 | 2,118,225 | ||

7.5% 6/1/16 | 2,160,000 | 1,965,600 | ||

7.625% 1/15/17 | 3,420,000 | 3,112,200 | ||

11.375% 3/1/18 | 1,490,000 | 1,571,950 | ||

MTR Gaming Group, Inc. 11.5% 8/1/19 pay-in-kind (d)(k) | 1,595,000 | 1,339,800 | ||

NCL Corp. Ltd. 9.5% 11/15/18 (d) | 1,125,000 | 1,164,375 | ||

Royal Caribbean Cruises Ltd.: | ||||

7.25% 3/15/18 | 465,000 | 479,508 | ||

yankee: | ||||

7.25% 6/15/16 | 3,985,000 | 4,064,700 | ||

7.5% 10/15/27 | 3,070,000 | 2,885,800 | ||

Times Square Hotel Trust 8.528% 8/1/26 (d) | 630,955 | 706,930 | ||

Universal City Development Partners Ltd./UCDP Finance, Inc. 8.875% 11/15/15 | 784,000 | 864,360 | ||

Wynn Las Vegas LLC/Wynn Las Vegas Capital Corp. 7.75% 8/15/20 | 970,000 | 1,050,025 | ||

| 31,391,840 | |||

Household Durables - 0.2% | ||||

Fortune Brands, Inc.: | ||||

5.375% 1/15/16 | 321,000 | 355,833 | ||

5.875% 1/15/36 | 14,352,000 | 14,650,766 | ||

6.375% 6/15/14 | 3,374,000 | 3,765,472 | ||

KB Home 7.25% 6/15/18 | 1,430,000 | 1,201,200 | ||

Lennar Corp. 6.95% 6/1/18 | 1,955,000 | 1,779,050 | ||

Reliance Intermediate Holdings LP 9.5% 12/15/19 (d) | 2,125,000 | 2,252,500 | ||

Corporate Bonds - continued | ||||

| Principal | Value | ||

Nonconvertible Bonds - continued | ||||

CONSUMER DISCRETIONARY - continued | ||||

Household Durables - continued | ||||

Standard Pacific Corp.: | ||||

8.375% 5/15/18 | $ 5,510,000 | $ 4,821,250 | ||

10.75% 9/15/16 | 2,370,000 | 2,346,300 | ||

| 31,172,371 | |||

Media - 1.7% | ||||

Allbritton Communications Co. 8% 5/15/18 | 2,630,000 | 2,603,700 | ||

AMC Networks, Inc. 7.75% 7/15/21 (d) | 1,045,000 | 1,092,025 | ||

AOL Time Warner, Inc. 7.625% 4/15/31 | 500,000 | 613,059 | ||

Cablevision Systems Corp.: | ||||

7.75% 4/15/18 | 1,440,000 | 1,483,200 | ||

8.625% 9/15/17 | 1,505,000 | 1,591,538 | ||

Catalina Marketing Corp. 10.5% 10/1/15 pay-in-kind (d)(k) | 2,835,000 | 2,835,000 | ||

Cequel Communications Holdings I LLC/Cequel Capital Corp. 8.625% 11/15/17 (d) | 8,280,000 | 8,611,200 | ||

Checkout Holding Corp. 0% 11/15/15 (d) | 800,000 | 472,000 | ||

Citadel Broadcasting Corp. 7.75% 12/15/18 (d) | 2,275,000 | 2,451,313 | ||

Comcast Corp.: | ||||

4.95% 6/15/16 | 2,344,000 | 2,632,778 | ||

5.15% 3/1/20 | 435,000 | 495,313 | ||

5.7% 5/15/18 | 14,629,000 | 16,943,483 | ||

6.4% 3/1/40 | 4,490,000 | 5,085,688 | ||

6.45% 3/15/37 | 2,196,000 | 2,433,486 | ||

6.55% 7/1/39 | 9,000,000 | 10,260,063 | ||

COX Communications, Inc. 4.625% 6/1/13 | 4,467,000 | 4,739,920 | ||

CSC Holdings LLC 8.625% 2/15/19 | 565,000 | 622,913 | ||

Discovery Communications LLC: | ||||

3.7% 6/1/15 | 7,129,000 | 7,614,556 | ||

6.35% 6/1/40 | 6,392,000 | 7,196,516 | ||

Globo Comunicacoes e Participacoes SA 6.25% (c)(d)(e) | 2,935,000 | 3,067,075 | ||

Houghton Mifflin Harcourt Publishing Co. 10.5% 6/1/19 (d) | 920,000 | 736,000 | ||

Insight Communications, Inc. 9.375% 7/15/18 (d) | 2,030,000 | 2,314,200 | ||

Kabel BW Erste Beteiligungs GmbH/Kabel Baden-Wurttemberg GmbH & Co. KG 7.5% 3/15/19 (d) | 660,000 | 646,800 | ||

NBCUniversal Media LLC: | ||||

3.65% 4/30/15 | 3,514,000 | 3,727,936 | ||

5.15% 4/30/20 | 11,614,000 | 12,863,573 | ||

Corporate Bonds - continued | ||||

| Principal | Value | ||

Nonconvertible Bonds - continued | ||||

CONSUMER DISCRETIONARY - continued | ||||

Media - continued | ||||

NBCUniversal Media LLC: - continued | ||||

6.4% 4/30/40 | $ 18,278,000 | $ 20,649,662 | ||

News America Holdings, Inc. 7.75% 12/1/45 | 170,000 | 200,205 | ||

News America, Inc.: | ||||

6.15% 3/1/37 | 2,970,000 | 3,101,366 | ||

6.15% 2/15/41 | 12,939,000 | 13,489,774 | ||

Nexstar Broadcasting, Inc./Mission Broadcasting, Inc. 8.875% 4/15/17 | 1,693,000 | 1,693,000 | ||

Nielsen Finance LLC/Nielsen Finance Co. 7.75% 10/15/18 | 2,770,000 | 2,880,800 | ||

ProQuest LLC/ProQuest Notes Co. 9% 10/15/18 (d) | 2,915,000 | 2,885,850 | ||

Quebecor Media, Inc.: | ||||

7.75% 3/15/16 | 4,032,000 | 3,991,680 | ||

7.75% 3/15/16 | 2,485,000 | 2,460,150 | ||

Time Warner Cable, Inc.: | ||||

5.4% 7/2/12 | 3,048,000 | 3,157,164 | ||

5.85% 5/1/17 | 7,607,000 | 8,571,918 | ||

6.2% 7/1/13 | 2,898,000 | 3,151,734 | ||

6.75% 7/1/18 | 13,763,000 | 16,193,670 | ||

Time Warner, Inc.: | ||||

3.15% 7/15/15 | 3,115,000 | 3,239,556 | ||

5.875% 11/15/16 | 368,000 | 428,377 | ||

6.2% 3/15/40 | 10,492,000 | 11,250,162 | ||

6.5% 11/15/36 | 9,243,000 | 10,310,945 | ||

TV Azteca SA de CV 7.5% 5/25/18 (Reg. S) | 850,000 | 843,625 | ||

Univision Communications, Inc. 6.875% 5/15/19 (d) | 1,300,000 | 1,202,500 | ||

Viacom, Inc.: | ||||

3.5% 4/1/17 | 7,993,000 | 8,264,538 | ||

6.75% 10/5/37 | 1,460,000 | 1,700,991 | ||

| 222,801,002 | |||

Multiline Retail - 0.0% | ||||

Sears Holdings Corp. 6.625% 10/15/18 | 2,375,000 | 1,965,313 | ||

Specialty Retail - 0.1% | ||||

AutoNation, Inc. 6.75% 4/15/18 | 1,105,000 | 1,143,675 | ||

Burlington Coat Factory Warehouse Corp. 10% 2/15/19 (d) | 2,564,000 | 2,390,930 | ||

J. Crew Group, Inc. 8.125% 3/1/19 | 2,249,000 | 1,956,630 | ||

PETCO Animal Supplies, Inc. 9.25% 12/1/18 (d) | 2,260,000 | 2,316,500 | ||

Corporate Bonds - continued | ||||

| Principal | Value | ||

Nonconvertible Bonds - continued | ||||

CONSUMER DISCRETIONARY - continued | ||||

Specialty Retail - continued | ||||

Staples, Inc. 7.375% 10/1/12 | $ 554,000 | $ 590,218 | ||

Toys 'R' Us, Inc. 7.375% 9/1/16 (d) | 1,200,000 | 1,164,000 | ||

| 9,561,953 | |||

TOTAL CONSUMER DISCRETIONARY | 321,396,360 | |||

CONSUMER STAPLES - 1.1% | ||||

Beverages - 0.1% | ||||

Anheuser-Busch InBev Worldwide, Inc.: | ||||

2.5% 3/26/13 | 8,433,000 | 8,660,387 | ||

5.375% 11/15/14 | 1,207,000 | 1,363,335 | ||

Cerveceria Nacional Dominicana C por A 8% 3/27/14 (Reg. S) | 225,000 | 231,750 | ||

Diageo Capital PLC 5.2% 1/30/13 | 1,037,000 | 1,100,343 | ||

FBG Finance Ltd. 5.125% 6/15/15 (d) | 3,662,000 | 4,052,626 | ||

| 15,408,441 | |||

Food & Staples Retailing - 0.1% | ||||

Albertsons, Inc.: | ||||

7.45% 8/1/29 | 155,000 | 122,450 | ||

8% 5/1/31 | 765,000 | 631,125 | ||

BFF International Ltd. 7.25% 1/28/20 (d) | 800,000 | 862,000 | ||

CVS Caremark Corp. 4.125% 5/15/21 | 4,050,000 | 4,101,192 | ||

Rite Aid Corp.: | ||||

9.375% 12/15/15 | 795,000 | 719,475 | ||

9.5% 6/15/17 | 1,590,000 | 1,391,250 | ||

SUPERVALU, Inc. 8% 5/1/16 | 865,000 | 865,000 | ||

Tops Markets LLC 10.125% 10/15/15 | 1,360,000 | 1,377,000 | ||

US Foodservice, Inc. 8.5% 6/30/19 (d) | 480,000 | 453,600 | ||

| 10,523,092 | |||

Food Products - 0.4% | ||||

Cargill, Inc. 6% 11/27/17 (d) | 9,457,000 | 11,245,413 | ||

Gruma SAB de CV 7.75% (Reg. S) | 985,000 | 980,075 | ||

Kraft Foods, Inc.: | ||||

5.375% 2/10/20 | 10,631,000 | 12,061,401 | ||

5.625% 11/1/11 | 588,000 | 592,200 | ||

6.125% 2/1/18 | 10,623,000 | 12,559,722 | ||

6.5% 8/11/17 | 10,238,000 | 12,365,303 | ||

Corporate Bonds - continued | ||||

| Principal | Value | ||

Nonconvertible Bonds - continued | ||||

CONSUMER STAPLES - continued | ||||

Food Products - continued | ||||

Kraft Foods, Inc.: - continued | ||||

6.75% 2/19/14 | $ 540,000 | $ 610,352 | ||

MHP SA 10.25% 4/29/15 (d) | 510,000 | 512,550 | ||

| 50,927,016 | |||

Personal Products - 0.0% | ||||

NBTY, Inc. 9% 10/1/18 | 2,065,000 | 2,147,600 | ||

Tobacco - 0.5% | ||||

Altria Group, Inc.: | ||||

8.5% 11/10/13 | 326,000 | 373,920 | ||

9.7% 11/10/18 | 23,631,000 | 31,203,838 | ||

Philip Morris International, Inc.: | ||||

4.875% 5/16/13 | 9,347,000 | 9,953,424 | ||

5.65% 5/16/18 | 7,161,000 | 8,438,852 | ||

Reynolds American, Inc.: | ||||

6.75% 6/15/17 | 3,719,000 | 4,378,542 | ||

7.25% 6/15/37 | 5,056,000 | 5,632,293 | ||

| 59,980,869 | |||

TOTAL CONSUMER STAPLES | 138,987,018 | |||

ENERGY - 3.3% | ||||

Energy Equipment & Services - 0.3% | ||||

Calfrac Holdings LP 7.5% 12/1/20 (d) | 1,570,000 | 1,522,900 | ||

DCP Midstream LLC 5.35% 3/15/20 (d) | 8,816,000 | 9,711,291 | ||

El Paso Pipeline Partners Operating Co. LLC: | ||||

4.1% 11/15/15 | 10,806,000 | 11,372,472 | ||

6.5% 4/1/20 | 738,000 | 837,136 | ||

Expro Finance Luxembourg SCA 8.5% 12/15/16 (d) | 3,230,000 | 3,068,500 | ||

Exterran Holdings, Inc. 7.25% 12/1/18 (d) | 2,250,000 | 2,160,000 | ||

Forbes Energy Services Ltd. 9% 6/15/19 (d) | 1,080,000 | 1,015,200 | ||

Hornbeck Offshore Services, Inc. 8% 9/1/17 | 1,450,000 | 1,435,500 | ||

Noble Holding International Ltd. 3.45% 8/1/15 | 632,000 | 669,750 | ||

Oil States International, Inc. 6.5% 6/1/19 (d) | 710,000 | 708,225 | ||

Precision Drilling Corp.: | ||||

6.5% 12/15/21 (d) | 170,000 | 171,700 | ||

6.625% 11/15/20 | 1,890,000 | 1,899,450 | ||

Corporate Bonds - continued | ||||

| Principal | Value | ||

Nonconvertible Bonds - continued | ||||

ENERGY - continued | ||||

Energy Equipment & Services - continued | ||||

Weatherford International Ltd.: | ||||

4.95% 10/15/13 | $ 2,173,000 | $ 2,310,583 | ||

5.15% 3/15/13 | 2,840,000 | 2,990,937 | ||

| 39,873,644 | |||

Oil, Gas & Consumable Fuels - 3.0% | ||||

Afren PLC 11.5% 2/1/16 (d) | 795,000 | 826,800 | ||

Alpha Natural Resources, Inc.: | ||||

6% 6/1/19 | 1,225,000 | 1,218,875 | ||

6.25% 6/1/21 | 835,000 | 826,650 | ||

Anadarko Petroleum Corp.: | ||||

5.95% 9/15/16 | 485,000 | 544,873 | ||

6.375% 9/15/17 | 19,790,000 | 22,837,799 | ||

Antero Resources Finance Corp.: | ||||

7.25% 8/1/19 (d) | 1,580,000 | 1,504,950 | ||

9.375% 12/1/17 | 2,915,000 | 3,089,900 | ||

BW Group Ltd. 6.625% 6/28/17 (d) | 3,688,000 | 3,452,886 | ||

Canadian Natural Resources Ltd.: | ||||

5.15% 2/1/13 | 5,610,000 | 5,916,216 | ||

5.7% 5/15/17 | 16,295,000 | 19,029,676 | ||

Chesapeake Energy Corp. 6.875% 11/15/20 | 635,000 | 669,925 | ||

ConocoPhillips: | ||||

4.6% 1/15/15 | 10,000,000 | 10,992,090 | ||

5.75% 2/1/19 | 2,930,000 | 3,489,952 | ||

CONSOL Energy, Inc.: | ||||

8% 4/1/17 | 2,320,000 | 2,447,600 | ||

8.25% 4/1/20 | 650,000 | 692,250 | ||

Crestwood Midstream Partners LP / Finance Corp. 7.75% 4/1/19 (d) | 800,000 | 764,000 | ||

Denbury Resources, Inc. 6.375% 8/15/21 | 1,710,000 | 1,662,975 | ||

Drummond Co., Inc.: | ||||

7.375% 2/15/16 | 6,015,000 | 6,075,150 | ||

9% 10/15/14 (d) | 3,045,000 | 3,143,963 | ||

DTEK Finance BV 9.5% 4/28/15 (d) | 600,000 | 610,500 | ||

Duke Capital LLC 6.25% 2/15/13 | 1,000,000 | 1,064,026 | ||

Duke Energy Field Services: | ||||

5.375% 10/15/15 (d) | 1,524,000 | 1,721,619 | ||

6.45% 11/3/36 (d) | 1,801,000 | 2,033,803 | ||

El Paso Natural Gas Co. 5.95% 4/15/17 | 1,166,000 | 1,347,769 | ||

Corporate Bonds - continued | ||||

| Principal | Value | ||

Nonconvertible Bonds - continued | ||||

ENERGY - continued | ||||

Oil, Gas & Consumable Fuels - continued | ||||

EnCana Holdings Finance Corp. 5.8% 5/1/14 | $ 3,602,000 | $ 3,974,094 | ||

Energy Transfer Equity LP 7.5% 10/15/20 | 2,155,000 | 2,208,875 | ||

Enterprise Products Operating LP: | ||||

5.6% 10/15/14 | 483,000 | 530,172 | ||

5.65% 4/1/13 | 697,000 | 739,976 | ||

EV Energy Partners LP/EV Energy Finance Corp. 8% 4/15/19 (d) | 1,650,000 | 1,617,000 | ||

Frontier Oil Corp.: | ||||

6.875% 11/15/18 | 485,000 | 499,550 | ||

8.5% 9/15/16 | 1,950,000 | 2,057,250 | ||

Gulf South Pipeline Co. LP 5.75% 8/15/12 (d) | 4,818,000 | 4,964,226 | ||

Gulfstream Natural Gas System LLC 6.95% 6/1/16 (d) | 221,000 | 263,393 | ||

KazMunaiGaz Finance Sub BV: | ||||

6.375% 4/9/21 (d) | 850,000 | 884,000 | ||

7% 5/5/20 (d) | 1,635,000 | 1,757,625 | ||

8.375% 7/2/13 (d) | 1,420,000 | 1,528,346 | ||

9.125% 7/2/18 (d) | 1,855,000 | 2,230,638 | ||

11.75% 1/23/15 (d) | 1,860,000 | 2,241,300 | ||

LINN Energy LLC/LINN Energy Finance Corp.: | ||||

6.5% 5/15/19 (d) | 1,790,000 | 1,709,450 | ||

7.75% 2/1/21 (d) | 1,950,000 | 1,940,250 | ||

8.625% 4/15/20 | 2,685,000 | 2,872,950 | ||

Marathon Petroleum Corp. 5.125% 3/1/21 (d) | 6,178,000 | 6,588,429 | ||

Midcontinent Express Pipeline LLC 5.45% 9/15/14 (d) | 10,834,000 | 11,653,256 | ||

Motiva Enterprises LLC: | ||||

5.75% 1/15/20 (d) | 4,187,000 | 4,862,422 | ||

6.85% 1/15/40 (d) | 5,937,000 | 7,564,914 | ||

Naftogaz of Ukraine NJSC 9.5% 9/30/14 | 1,450,000 | 1,547,875 | ||

Nakilat, Inc. 6.067% 12/31/33 (d) | 1,975,000 | 2,133,000 | ||

Nexen, Inc.: | ||||

5.2% 3/10/15 | 1,133,000 | 1,238,570 | ||

5.875% 3/10/35 | 240,000 | 226,592 | ||

6.2% 7/30/19 | 603,000 | 697,110 | ||

6.4% 5/15/37 | 13,102,000 | 13,443,622 | ||

NGPL PipeCo LLC 6.514% 12/15/12 (d) | 10,209,000 | 10,562,446 | ||

OGX Petroleo e Gas Participacoes SA 8.5% 6/1/18 (d) | 555,000 | 555,000 | ||

Overseas Shipholding Group, Inc.: | ||||

7.5% 2/15/24 | 500,000 | 353,750 | ||

8.125% 3/30/18 | 2,530,000 | 2,150,500 | ||

Corporate Bonds - continued | ||||

| Principal | Value | ||

Nonconvertible Bonds - continued | ||||

ENERGY - continued | ||||

Oil, Gas & Consumable Fuels - continued | ||||

Pacific Rubiales Energy Corp. 8.75% 11/10/16 | $ 1,093,000 | $ 1,218,695 | ||

Pan American Energy LLC 7.875% 5/7/21 (d) | 4,370,000 | 4,522,950 | ||

Pemex Project Funding Master Trust: | ||||

5.75% 3/1/18 | 645,000 | 715,950 | ||

6.625% 6/15/35 | 945,000 | 1,044,225 | ||

Petro-Canada: | ||||

6.05% 5/15/18 | 3,850,000 | 4,459,309 | ||

6.8% 5/15/38 | 8,950,000 | 10,476,297 | ||

Petrobras International Finance Co. Ltd.: | ||||

3.875% 1/27/16 | 10,192,000 | 10,447,962 | ||

5.75% 1/20/20 | 18,708,000 | 20,296,085 | ||

6.875% 1/20/40 | 470,000 | 531,100 | ||

7.875% 3/15/19 | 10,517,000 | 12,793,931 | ||

8.375% 12/10/18 | 470,000 | 583,014 | ||

Petrohawk Energy Corp.: | ||||

6.25% 6/1/19 (d) | 1,290,000 | 1,489,950 | ||

7.25% 8/15/18 | 1,330,000 | 1,556,100 | ||

Petroleos de Venezuela SA 144A: | ||||

4.9% 10/28/14 | 2,475,000 | 1,825,313 | ||

5.25% 4/12/17 | 1,385,000 | 834,463 | ||

5.375% 4/12/27 | 5,310,000 | 2,588,625 | ||

5.5% 4/12/37 | 2,670,000 | 1,241,550 | ||

8% 11/17/13 | 380,000 | 342,000 | ||

8.5% 11/2/17 (d) | 4,555,000 | 3,256,825 | ||

12.75% 2/17/22 (d) | 3,580,000 | 2,912,330 | ||

Petroleos Mexicanos: | ||||

5.5% 1/21/21 | 500,000 | 543,750 | ||

5.5% 1/21/21 (d) | 11,569,000 | 12,581,288 | ||

6% 3/5/20 | 1,108,000 | 1,249,270 | ||

6.5% 6/2/41 (d) | 350,000 | 375,884 | ||

6.625% (d)(e) | 2,025,000 | 2,030,063 | ||

8% 5/3/19 | 420,000 | 531,300 | ||

Petroleum Co. of Trinidad & Tobago Ltd. (Reg. S) 6% 5/8/22 | 522,500 | 522,500 | ||

Pioneer Natural Resources Co. 6.65% 3/15/17 | 4,605,000 | 4,996,425 | ||

Plains All American Pipeline LP/PAA Finance Corp.: | ||||

3.95% 9/15/15 | 5,869,000 | 6,212,307 | ||

4.25% 9/1/12 | 485,000 | 500,276 | ||

5% 2/1/21 | 3,410,000 | 3,623,797 | ||

Corporate Bonds - continued | ||||

| Principal | Value | ||

Nonconvertible Bonds - continued | ||||

ENERGY - continued | ||||

Oil, Gas & Consumable Fuels - continued | ||||

Plains All American Pipeline LP/PAA Finance Corp.: - continued | ||||

6.125% 1/15/17 | $ 6,185,000 | $ 7,086,754 | ||

PT Adaro Indonesia 7.625% 10/22/19 (d) | 925,000 | 1,008,250 | ||

PT Pertamina Persero: | ||||

5.25% 5/23/21 (d) | 815,000 | 845,563 | ||

6.5% 5/27/41 (d) | 595,000 | 627,725 | ||

Quicksilver Resources, Inc.: | ||||

7.125% 4/1/16 | 4,415,000 | 4,105,950 | ||

11.75% 1/1/16 | 2,255,000 | 2,508,688 | ||

Ras Laffan Liquefied Natural Gas Co. Ltd. 8.294% 3/15/14 (d) | 2,235,000 | 2,447,325 | ||

Ras Laffan Liquefied Natural Gas Co. Ltd. III: | ||||

4.5% 9/30/12 (d) | 4,773,000 | 4,940,055 | ||

5.5% 9/30/14 (d) | 6,670,000 | 7,353,675 | ||

5.832% 9/30/16 (d) | 1,407,838 | 1,541,582 | ||

6.332% 9/30/27 (d) | 1,840,000 | 2,056,108 | ||

6.75% 9/30/19 (d) | 4,366,000 | 5,239,200 | ||

Rockies Express Pipeline LLC 6.25% 7/15/13 (d) | 3,392,000 | 3,628,999 | ||

Ship Finance International Ltd. 8.5% 12/15/13 | 2,065,000 | 2,003,050 | ||

Southeast Supply Header LLC 4.85% 8/15/14 (d) | 367,000 | 394,186 | ||

Spectra Energy Capital, LLC 5.65% 3/1/20 | 308,000 | 344,357 | ||

Spectra Energy Partners, LP: | ||||

2.95% 6/15/16 | 2,061,000 | 2,119,697 | ||

4.6% 6/15/21 | 2,694,000 | 2,782,541 | ||

Suncor Energy, Inc. 6.1% 6/1/18 | 11,154,000 | 12,926,605 | ||

Targa Resources Partners LP/Targa Resources Partners Finance Corp.: | ||||

6.875% 2/1/21 (d) | 685,000 | 678,150 | ||

7.875% 10/15/18 | 2,205,000 | 2,160,900 | ||

Venoco, Inc. 8.875% 2/15/19 | 1,745,000 | 1,561,775 | ||

Western Gas Partners LP 5.375% 6/1/21 | 11,663,000 | 12,281,022 | ||

XTO Energy, Inc.: | ||||

4.9% 2/1/14 | 267,000 | 293,509 | ||

5% 1/31/15 | 1,749,000 | 1,987,369 | ||

Corporate Bonds - continued | ||||

| Principal | Value | ||

Nonconvertible Bonds - continued | ||||

ENERGY - continued | ||||

Oil, Gas & Consumable Fuels - continued | ||||

XTO Energy, Inc.: - continued | ||||

5.65% 4/1/16 | $ 1,200,000 | $ 1,423,384 | ||

YPF SA 10% 11/2/28 | 445,000 | 507,300 | ||

| 392,718,081 | |||

TOTAL ENERGY | 432,591,725 | |||

FINANCIALS - 9.7% | ||||

Capital Markets - 1.5% | ||||

Bear Stearns Companies, Inc. 5.3% 10/30/15 | 1,685,000 | 1,830,572 | ||

BlackRock, Inc. 4.25% 5/24/21 | 5,000,000 | 5,085,045 | ||

Equinox Holdings, Inc. 9.5% 2/1/16 (d) | 2,020,000 | 2,136,150 | ||

Goldman Sachs Group, Inc.: | ||||

3.7% 8/1/15 | 10,365,000 | 10,471,449 | ||

5.25% 7/27/21 | 27,721,000 | 28,069,425 | ||

5.625% 1/15/17 | 3,200,000 | 3,313,139 | ||

5.95% 1/18/18 | 4,975,000 | 5,289,261 | ||

6.75% 10/1/37 | 9,643,000 | 9,129,549 | ||

Janus Capital Group, Inc. 5.875% 9/15/11 (c) | 3,067,000 | 3,069,319 | ||

JPMorgan Chase Capital XX 6.55% 9/29/36 | 17,904,000 | 17,783,309 | ||

JPMorgan Chase Capital XXV 6.8% 10/1/37 | 7,405,000 | 7,355,327 | ||

Lazard Group LLC: | ||||

6.85% 6/15/17 | 4,817,000 | 5,416,317 | ||

7.125% 5/15/15 | 1,717,000 | 1,936,005 | ||

Merrill Lynch & Co., Inc.: | ||||

5.45% 2/5/13 | 13,533,000 | 13,883,518 | ||

6.4% 8/28/17 | 7,843,000 | 8,031,663 | ||

Morgan Stanley: | ||||

4% 7/24/15 | 9,153,000 | 9,105,185 | ||

4.75% 4/1/14 | 5,820,000 | 5,900,712 | ||

5.5% 7/28/21 | 10,909,000 | 10,878,706 | ||

5.625% 9/23/19 | 12,714,000 | 12,909,923 | ||

5.95% 12/28/17 | 5,186,000 | 5,359,866 | ||

6% 5/13/14 | 14,113,000 | 14,815,362 | ||

6% 4/28/15 | 1,414,000 | 1,479,342 | ||

6.625% 4/1/18 | 16,118,000 | 17,255,850 | ||

Northern Trust Corp. 3.375% 8/23/21 | 2,714,000 | 2,709,185 | ||

| 203,214,179 | |||

Corporate Bonds - continued | ||||

| Principal | Value | ||

Nonconvertible Bonds - continued | ||||

FINANCIALS - continued | ||||

Commercial Banks - 1.8% | ||||

African Export-Import Bank 8.75% 11/13/14 | $ 815,000 | $ 902,613 | ||

Akbank T.A.S. 5.125% 7/22/15 (d) | 1,265,000 | 1,246,025 | ||

Banco Bradesco SA 5.9% 1/16/21 (d) | 620,000 | 631,625 | ||

Banco de Credito del Peru 4.75% 3/16/16 (d) | 895,000 | 886,050 | ||

Banco Nacional de Desenvolvimento Economico e Social: | ||||

5.5% 7/12/20 (d) | 520,000 | 557,700 | ||

6.5% 6/10/19 (d) | 325,000 | 371,313 | ||

Banco Votorantim SA 5.25% 2/11/16 (d) | 1,035,000 | 1,050,525 | ||

Bank of America NA: | ||||

5.3% 3/15/17 | 6,339,000 | 6,200,803 | ||

6.1% 6/15/17 | 382,000 | 378,014 | ||

BB&T Capital Trust IV 6.82% 6/12/77 (k) | 2,330,000 | 2,332,913 | ||

BBVA Paraguay SA 9.75% 2/11/16 (d) | 1,145,000 | 1,213,700 | ||

CIT Group, Inc.: | ||||

7% 5/1/15 | 117 | 116 | ||

7% 5/4/15 (d) | 3,689,000 | 3,633,665 | ||

7% 5/1/16 | 861 | 848 | ||

7% 5/2/16 (d) | 2,651,000 | 2,597,980 | ||

7% 5/2/17 (d) | 3,534,000 | 3,454,485 | ||

Credit Suisse New York Branch 6% 2/15/18 | 16,785,000 | 17,674,571 | ||

DBS Bank Ltd. (Singapore) 0.5101% 5/16/17 (d)(k) | 4,686,000 | 4,615,710 | ||

Development Bank of Kazakhstan JSC 5.5% 12/20/15 (d) | 895,000 | 921,850 | ||

Development Bank of Philippines: | ||||

5.5% 3/25/21 | 510,000 | 512,550 | ||

8.375% (e)(k) | 1,655,000 | 1,837,050 | ||

Discover Bank 8.7% 11/18/19 | 12,480,000 | 14,692,192 | ||

Eastern and Southern African Trade and Development Bank 6.875% 1/9/16 (Reg. S) | 870,000 | 848,250 | ||

EXIM of Ukraine 7.65% 9/7/11 (Issued by Credit Suisse International for EXIM of Ukraine) | 4,935,000 | 4,910,325 | ||

Export-Import Bank of Korea: | ||||

5.25% 2/10/14 (d) | 565,000 | 602,015 | ||

5.5% 10/17/12 | 2,813,000 | 2,925,526 | ||

Fifth Third Bancorp: | ||||

3.625% 1/25/16 | 5,953,000 | 6,032,223 | ||

4.5% 6/1/18 | 798,000 | 796,299 | ||

8.25% 3/1/38 | 4,667,000 | 5,276,254 | ||

Corporate Bonds - continued | ||||

| Principal | Value | ||

Nonconvertible Bonds - continued | ||||

FINANCIALS - continued | ||||

Commercial Banks - continued | ||||

Fifth Third Bank 4.75% 2/1/15 | $ 1,329,000 | $ 1,418,495 | ||

Fifth Third Capital Trust IV 6.5% 4/15/67 (k) | 8,522,000 | 7,904,155 | ||

HBOS PLC 6.75% 5/21/18 (d) | 6,067,000 | 5,608,341 | ||

HSBK (Europe) BV: | ||||

7.25% 5/3/17 (d) | 1,435,000 | 1,467,288 | ||

9.25% 10/16/13 (d) | 1,170,000 | 1,254,825 | ||

Huntington Bancshares, Inc. 7% 12/15/20 | 2,851,000 | 3,261,573 | ||

Itau Unibanco Holding SA 6.2% 12/21/21 (d) | 590,000 | 609,175 | ||

JPMorgan Chase Bank 6% 10/1/17 | 11,313,000 | 12,672,517 | ||

KeyBank NA: | ||||

5.45% 3/3/16 | 3,939,000 | 4,270,018 | ||

5.8% 7/1/14 | 9,490,000 | 10,365,813 | ||

6.95% 2/1/28 | 1,977,000 | 2,205,328 | ||

KeyCorp. 5.1% 3/24/21 | 5,572,000 | 5,700,423 | ||

Korea Development Bank 4% 9/9/16 | 525,000 | 540,855 | ||

Manufacturers & Traders Trust Co. 1.7458% 4/1/13 (k) | 720,797 | 719,995 | ||

Marshall & Ilsley Bank: | ||||

4.85% 6/16/15 | 4,520,000 | 4,942,159 | ||

5% 1/17/17 | 13,700,000 | 14,720,075 | ||

5.25% 9/4/12 | 3,162,000 | 3,252,367 | ||

Regions Bank: | ||||

6.45% 6/26/37 | 10,658,000 | 9,085,945 | ||

7.5% 5/15/18 | 6,622,000 | 6,456,450 | ||

Regions Financial Corp.: | ||||

0.4165% 6/26/12 (k) | 338,000 | 330,870 | ||

5.75% 6/15/15 | 2,005,000 | 1,894,725 | ||

7.75% 11/10/14 | 6,404,000 | 6,355,970 | ||

RSHB Capital SA: | ||||

6% 6/3/21 (d) | 555,000 | 548,756 | ||

9% 6/11/14 (d) | 405,000 | 453,519 | ||

Standard Bank PLC 5.799% 2/9/16 (Issued by Standard Bank PLC for PrivatBank) (k) | 675,000 | 551,813 | ||

SunTrust Banks, Inc. 3.6% 4/15/16 | 9,501,000 | 9,538,377 | ||

The State Export-Import Bank of Ukraine JSC 5.7928% 2/9/16 (Issued by Credit Suisse First Boston International for The State Export-Import Bank of Ukraine JSC) (c) | 1,335,000 | 1,178,138 | ||

Trade & Development Bank of Mongolia LLC 8.5% 10/25/13 | 555,000 | 563,325 | ||

Corporate Bonds - continued | ||||

| Principal | Value | ||

Nonconvertible Bonds - continued | ||||

FINANCIALS - continued | ||||

Commercial Banks - continued | ||||

Turkiye Garanti Bankasi AS: | ||||

2.7513% 4/20/16 (d)(k) | $ 945,000 | $ 894,206 | ||

6.25% 4/20/21 (d) | 1,050,000 | 985,688 | ||

Turkiye Is Bankasi AS 5.1% 2/1/16 (d) | 910,000 | 882,700 | ||

UniCredit Luxembourg Finance SA 5.584% 1/13/17 (d)(k) | 2,162,000 | 1,933,704 | ||

UnionBanCal Corp. 5.25% 12/16/13 | 826,000 | 891,162 | ||

Vimpel Communications 8.25% 5/23/16 (Reg. S) (Issued by UBS Luxembourg SA for Vimpel Communications) | 2,325,000 | 2,432,531 | ||

Wachovia Bank NA: | ||||

4.8% 11/1/14 | 372,000 | 399,599 | ||

4.875% 2/1/15 | 1,756,000 | 1,871,317 | ||

Wachovia Corp.: | ||||

5.625% 10/15/16 | 4,239,000 | 4,639,009 | ||

5.75% 6/15/17 | 2,933,000 | 3,321,708 | ||

Wells Fargo & Co.: | ||||

3.625% 4/15/15 | 5,893,000 | 6,156,376 | ||

3.676% 6/15/16 | 4,301,000 | 4,544,101 | ||

3.75% 10/1/14 | 4,016,000 | 4,270,602 | ||

| 238,197,183 | |||

Consumer Finance - 0.8% | ||||

Ally Financial, Inc.: | ||||

3.4784% 2/11/14 (k) | 2,895,000 | 2,692,350 | ||

6.25% 12/1/17 | 1,300,000 | 1,241,500 | ||

Capital One Financial Corp. 5.7% 9/15/11 | 5,251,000 | 5,257,133 | ||

Discover Financial Services: | ||||

6.45% 6/12/17 | 10,366,000 | 11,658,184 | ||

10.25% 7/15/19 | 11,672,000 | 15,060,417 | ||

Ford Motor Credit Co. LLC: | ||||

5% 5/15/18 | 2,120,000 | 2,055,637 | ||

5.875% 8/2/21 | 2,230,000 | 2,234,658 | ||

12% 5/15/15 | 3,440,000 | 4,196,800 | ||

General Electric Capital Corp.: | ||||

2.25% 11/9/15 | 314,000 | 315,669 | ||

4.625% 1/7/21 | 5,706,000 | 5,875,394 | ||

5.625% 9/15/17 | 5,858,000 | 6,503,358 | ||

5.625% 5/1/18 | 25,000,000 | 27,680,175 | ||

6.375% 11/15/67 (k) | 9,000,000 | 8,910,000 | ||

Corporate Bonds - continued | ||||

| Principal | Value | ||

Nonconvertible Bonds - continued | ||||

FINANCIALS - continued | ||||

Consumer Finance - continued | ||||

Household Finance Corp. 6.375% 10/15/11 | $ 2,320,000 | $ 2,333,094 | ||

HSBC Finance Corp. 5.9% 6/19/12 | 578,000 | 598,420 | ||

SLM Corp. 0.483% 10/25/11 (k) | 12,343,000 | 12,314,414 | ||

| 108,927,203 | |||

Diversified Financial Services - 2.0% | ||||

Aquarius Investments Luxemburg 8.25% 2/18/16 | 1,025,000 | 1,076,250 | ||

Bank of America Corp. 5.75% 12/1/17 | 27,955,000 | 29,039,738 | ||

Biz Finance PLC 8.375% 4/27/15 (Reg. S) | 700,000 | 703,500 | ||

BP Capital Markets PLC: | ||||

3.125% 10/1/15 | 10,828,000 | 11,325,059 | ||

3.625% 5/8/14 | 711,000 | 749,814 | ||

4.5% 10/1/20 | 650,000 | 702,434 | ||

4.742% 3/11/21 | 8,800,000 | 9,628,705 | ||

Capital One Capital V 10.25% 8/15/39 | 5,267,000 | 5,467,673 | ||

CCO Holdings LLC/CCO Holdings Capital Corp.: | ||||

6.5% 4/30/21 | 635,000 | 620,713 | ||

7% 1/15/19 | 3,335,000 | 3,368,350 | ||

7% 1/15/19 (d) | 725,000 | 728,625 | ||

7.25% 10/30/17 | 3,055,000 | 3,123,738 | ||

7.875% 4/30/18 | 865,000 | 899,600 | ||

CDW LLC/CDW Finance Corp. 8% 12/15/18 (d) | 2,230,000 | 2,196,550 | ||

Citigroup, Inc.: | ||||

3.953% 6/15/16 | 11,847,000 | 12,098,405 | ||

4.75% 5/19/15 | 32,881,000 | 34,276,601 | ||

5.5% 4/11/13 | 13,549,000 | 14,115,497 | ||

6.125% 5/15/18 | 8,677,000 | 9,464,438 | ||

6.5% 8/19/13 | 13,174,000 | 14,012,775 | ||

City of Buenos Aires 12.5% 4/6/15 (d) | 2,725,000 | 2,963,438 | ||

Fibria Overseas Finance Ltd. 6.75% 3/3/21 (d) | 520,000 | 520,000 | ||

General Motors Financial Co., Inc. 6.75% 6/1/18 (d) | 1,500,000 | 1,477,500 | ||

Icahn Enterprises LP/Icahn Enterprises Finance Corp.: | ||||

7.75% 1/15/16 | 4,100,000 | 4,141,000 | ||

8% 1/15/18 | 4,960,000 | 5,009,600 | ||

ILFC E-Capital Trust II 6.25% 12/21/65 (d)(k) | 1,250,000 | 925,000 | ||

Indo Energy Finance BV 7% 5/7/18 (d) | 525,000 | 532,875 | ||

JPMorgan Chase & Co.: | ||||

3.15% 7/5/16 | 13,000,000 | 13,271,193 | ||

3.4% 6/24/15 | 642,000 | 661,252 | ||

Corporate Bonds - continued | ||||

| Principal | Value | ||

Nonconvertible Bonds - continued | ||||

FINANCIALS - continued | ||||

Diversified Financial Services - continued | ||||

JPMorgan Chase & Co.: - continued | ||||

4.95% 3/25/20 | $ 17,148,000 | $ 18,271,743 | ||

LBI Escrow Corp. 8% 11/1/17 (d) | 2,545,000 | 2,824,950 | ||

NSG Holdings II, LLC 7.75% 12/15/25 (d) | 9,115,000 | 8,841,550 | ||

Offshore Group Investment Ltd.: | ||||

11.5% 8/1/15 | 3,155,000 | 3,344,300 | ||

11.5% 8/1/15 (d) | 320,000 | 339,200 | ||

ORIX Corp. 5.48% 11/22/11 | 385,000 | 387,846 | ||

Prime Property Funding, Inc.: | ||||

5.125% 6/1/15 (d) | 2,806,000 | 2,974,742 | ||

5.5% 1/15/14 (d) | 867,000 | 926,528 | ||

5.7% 4/15/17 (d) | 2,115,000 | 2,261,504 | ||

Rearden G Holdings Eins GmbH 7.875% 3/30/20 (d) | 915,000 | 933,300 | ||

Reynolds Group Issuer, Inc./Reynolds Group Issuer LLC/Reynolds Group Issuer (Luxembourg): | ||||

7.875% 8/15/19 (d) | 685,000 | 674,725 | ||

9.875% 8/15/19 (d) | 820,000 | 760,550 | ||

SB Capital SA 5.4% 3/24/17 (Reg. S) | 540,000 | 558,225 | ||

Steel Capital SA Ln Partner Net Program 6.25% 7/26/16 (d) | 945,000 | 932,006 | ||

Sunwest Management, Inc. 7.9726% 2/10/15 | 364,436 | 320,703 | ||

T2 Capital Finance Co. SA 6.95% 2/6/17 (Reg. S) (c) | 778,000 | 779,945 | ||

TECO Finance, Inc.: | ||||

4% 3/15/16 | 2,562,000 | 2,740,628 | ||

5.15% 3/15/20 | 3,761,000 | 4,189,735 | ||

TMK Capital SA 7.75% 1/27/18 | 525,000 | 514,500 | ||

TransCapitalInvest Ltd. 5.67% 3/5/14 (d) | 4,317,000 | 4,525,986 | ||

Transportation Union LLC/Transportation Union Financing Corp. 11.375% 6/15/18 | 2,310,000 | 2,561,097 | ||

UPCB Finance III Ltd. 6.625% 7/1/20 (d) | 1,055,000 | 1,028,625 | ||

Vnesheconombank Via VEB Finance Ltd. 6.8% 11/22/25 (d) | 605,000 | 623,150 | ||

Wind Acquisition Holdings Finance SA 12.25% 7/15/17 pay-in-kind (d)(k) | 5,768,176 | 5,658,260 | ||

WM Finance Corp.: | ||||

9.5% 6/15/16 (d) | 270,000 | 274,050 | ||

11.5% 10/1/18 (d) | 1,595,000 | 1,467,400 | ||

ZFS Finance USA Trust II 6.45% 12/15/65 (d)(k) | 5,755,000 | 5,639,900 | ||

ZFS Finance USA Trust IV 5.875% 5/9/62 (d)(k) | 1,673,000 | 1,573,607 | ||

Corporate Bonds - continued | ||||

| Principal | Value | ||

Nonconvertible Bonds - continued | ||||

FINANCIALS - continued | ||||

Diversified Financial Services - continued | ||||

ZFS Finance USA Trust V 6.5% 5/9/67 (d)(k) | $ 3,125,000 | $ 2,984,375 | ||

Zhaikmunai Finance BV 10.5% 10/19/15 (d) | 1,735,000 | 1,730,663 | ||

| 263,744,116 | |||

Insurance - 1.4% | ||||

Allstate Corp.: | ||||

5.55% 5/9/35 | 7,505,000 | 7,528,971 | ||

6.2% 5/16/14 | 6,893,000 | 7,795,301 | ||

Aon Corp.: | ||||

3.125% 5/27/16 | 10,200,000 | 10,208,150 | ||

3.5% 9/30/15 | 4,451,000 | 4,617,494 | ||

5% 9/30/20 | 4,928,000 | 5,297,211 | ||

6.25% 9/30/40 | 3,160,000 | 3,479,666 | ||

Assurant, Inc. 5.625% 2/15/14 | 2,384,000 | 2,530,058 | ||

Axis Capital Holdings Ltd. 5.75% 12/1/14 | 558,000 | 608,128 | ||

Great-West Life & Annuity Insurance Co. 7.153% 5/16/46 (d)(k) | 1,859,000 | 1,770,698 | ||

Hartford Financial Services Group, Inc. 5.375% 3/15/17 | 194,000 | 199,962 | ||

Liberty Mutual Group, Inc.: | ||||

5% 6/1/21 (d) | 11,772,000 | 11,473,533 | ||

6.5% 3/15/35 (d) | 741,000 | 715,490 | ||

Marsh & McLennan Companies, Inc. 4.8% 7/15/21 | 7,090,000 | 7,228,858 | ||

MetLife, Inc.: | ||||

2.375% 2/6/14 | 6,865,000 | 7,014,733 | ||

4.75% 2/8/21 | 4,032,000 | 4,223,439 | ||

5% 6/15/15 | 1,163,000 | 1,284,040 | ||

5.875% 2/6/41 | 3,113,000 | 3,308,048 | ||

6.125% 12/1/11 | 990,000 | 1,002,847 | ||

6.75% 6/1/16 | 7,610,000 | 8,913,563 | ||

Metropolitan Life Global Funding I: | ||||

5.125% 4/10/13 (d) | 559,000 | 590,462 | ||

5.125% 6/10/14 (d) | 6,751,000 | 7,363,228 | ||

Monumental Global Funding III 5.5% 4/22/13 (d) | 2,746,000 | 2,914,917 | ||

New York Life Insurance Co. 6.75% 11/15/39 (d) | 3,590,000 | 4,231,673 | ||

Northwestern Mutual Life Insurance Co. 6.063% 3/30/40 (d) | 5,682,000 | 6,231,512 | ||

Pacific Life Global Funding 5.15% 4/15/13 (d) | 12,118,000 | 12,777,704 | ||

Pacific Life Insurance Co. 9.25% 6/15/39 (d) | 5,674,000 | 7,489,901 | ||

Corporate Bonds - continued | ||||

| Principal | Value | ||

Nonconvertible Bonds - continued | ||||

FINANCIALS - continued | ||||

Insurance - continued | ||||

Pacific LifeCorp 6% 2/10/20 (d) | $ 6,323,000 | $ 7,058,928 | ||

Prudential Financial, Inc.: | ||||

3.625% 9/17/12 | 11,000,000 | 11,260,370 | ||

4.75% 9/17/15 | 11,000,000 | 11,761,827 | ||

5.15% 1/15/13 | 2,966,000 | 3,106,019 | ||

7.375% 6/15/19 | 3,230,000 | 3,859,937 | ||

8.875% 6/15/38 (k) | 1,915,000 | 2,087,350 | ||

QBE Insurance Group Ltd. 5.647% 7/1/23 (d)(k) | 320,000 | 303,590 | ||

Symetra Financial Corp. 6.125% 4/1/16 (d) | 6,375,000 | 6,783,179 | ||

The Chubb Corp. 5.75% 5/15/18 | 4,035,000 | 4,714,744 | ||

Unum Group: | ||||

5.625% 9/15/20 | 5,753,000 | 6,274,987 | ||

7.125% 9/30/16 | 587,000 | 686,000 | ||

| 188,696,518 | |||

Real Estate Investment Trusts - 0.5% | ||||

AvalonBay Communities, Inc.: | ||||

4.95% 3/15/13 | 367,000 | 385,772 | ||

5.5% 1/15/12 | 2,071,000 | 2,104,409 | ||

BRE Properties, Inc. 5.5% 3/15/17 | 661,000 | 730,868 | ||

Camden Property Trust: | ||||

5.375% 12/15/13 | 4,073,000 | 4,356,122 | ||

5.875% 11/30/12 | 670,000 | 699,868 | ||

Developers Diversified Realty Corp.: | ||||

4.75% 4/15/18 | 7,559,000 | 7,173,083 | ||

5.375% 10/15/12 | 5,101,000 | 5,161,855 | ||

7.5% 4/1/17 | 5,574,000 | 6,196,421 | ||

7.875% 9/1/20 | 323,000 | 358,998 | ||

Duke Realty LP: | ||||

4.625% 5/15/13 | 1,106,000 | 1,146,652 | ||

5.875% 8/15/12 | 1,017,000 | 1,048,740 | ||

Equity One, Inc.: | ||||

5.375% 10/15/15 | 1,403,000 | 1,488,126 | ||

6% 9/15/17 | 890,000 | 927,998 | ||

6.25% 12/15/14 | 6,140,000 | 6,594,004 | ||

6.25% 1/15/17 | 494,000 | 530,686 | ||

Federal Realty Investment Trust: | ||||

5.4% 12/1/13 | 441,000 | 470,078 | ||

5.9% 4/1/20 | 2,504,000 | 2,707,250 | ||

Corporate Bonds - continued | ||||

| Principal | Value | ||

Nonconvertible Bonds - continued | ||||

FINANCIALS - continued | ||||

Real Estate Investment Trusts - continued | ||||

Federal Realty Investment Trust: - continued | ||||

6% 7/15/12 | $ 3,658,000 | $ 3,781,421 | ||

6.2% 1/15/17 | 620,000 | 703,185 | ||

HMB Capital Trust V 3.847% 12/15/36 (a)(d)(k) | 270,000 | 0 | ||

HRPT Properties Trust: | ||||

5.75% 11/1/15 | 2,386,000 | 2,554,914 | ||

6.25% 6/15/17 | 1,232,000 | 1,350,921 | ||

6.65% 1/15/18 | 867,000 | 976,737 | ||

MPT Operating Partnership LP/MPT Finance Corp. 6.875% 5/1/21 (d) | 1,760,000 | 1,654,400 | ||

Omega Healthcare Investors, Inc.: | ||||

6.75% 10/15/22 | 1,510,000 | 1,445,825 | ||

7% 1/15/16 | 3,060,000 | 3,128,850 | ||

Senior Housing Properties Trust: | ||||

6.75% 4/15/20 | 940,000 | 1,045,865 | ||

8.625% 1/15/12 | 250,000 | 255,583 | ||

UDR, Inc. 5.5% 4/1/14 | 5,222,000 | 5,593,859 | ||

Washington (REIT) 5.25% 1/15/14 | 322,000 | 343,968 | ||

| 64,916,458 | |||

Real Estate Management & Development - 1.4% | ||||

AMB Property LP 5.9% 8/15/13 | 2,580,000 | 2,673,907 | ||

Arden Realty LP 5.2% 9/1/11 | 1,670,000 | 1,670,000 | ||

BioMed Realty LP: | ||||

3.85% 4/15/16 | 11,000,000 | 11,098,659 | ||

6.125% 4/15/20 | 3,429,000 | 3,701,942 | ||

Brandywine Operating Partnership LP: | ||||

5.7% 5/1/17 | 7,049,000 | 7,374,960 | ||

5.75% 4/1/12 | 2,972,000 | 3,027,695 | ||

CB Richard Ellis Services, Inc. 6.625% 10/15/20 | 1,945,000 | 1,886,650 | ||

Colonial Properties Trust 6.875% 8/15/12 | 5,706,000 | 5,895,605 | ||

Colonial Realty LP 6.05% 9/1/16 | 2,000,000 | 2,100,000 | ||

Digital Realty Trust LP: | ||||

4.5% 7/15/15 | 4,981,000 | 5,158,030 | ||

5.25% 3/15/21 | 5,708,000 | 5,709,593 | ||

Duke Realty LP: | ||||

5.4% 8/15/14 | 5,561,000 | 5,881,870 | ||

5.95% 2/15/17 | 1,109,000 | 1,201,606 | ||

6.25% 5/15/13 | 14,494,000 | 15,325,463 | ||

Corporate Bonds - continued | ||||

| Principal | Value | ||

Nonconvertible Bonds - continued | ||||

FINANCIALS - continued | ||||

Real Estate Management & Development - continued | ||||

Duke Realty LP: - continued | ||||

6.5% 1/15/18 | $ 3,795,000 | $ 4,126,026 | ||

6.75% 3/15/20 | 10,379,000 | 11,116,719 | ||

8.25% 8/15/19 | 75,000 | 88,197 | ||

ERP Operating LP: | ||||

4.75% 7/15/20 | 7,700,000 | 7,977,993 | ||

5.25% 9/15/14 | 1,310,000 | 1,421,336 | ||

5.375% 8/1/16 | 2,768,000 | 3,076,779 | ||

5.5% 10/1/12 | 3,690,000 | 3,851,135 | ||

5.75% 6/15/17 | 14,407,000 | 16,276,366 | ||

Forest City Enterprises, Inc.: | ||||

6.5% 2/1/17 | 450,000 | 415,125 | ||

7.625% 6/1/15 | 100,000 | 97,500 | ||

Highwoods/Forsyth LP 5.85% 3/15/17 | 615,000 | 668,797 | ||

Host Hotels & Resorts, Inc.: | ||||

5.875% 6/15/19 (d) | 150,000 | 148,500 | ||

6% 11/1/20 | 205,000 | 199,363 | ||

Liberty Property LP: | ||||

4.75% 10/1/20 | 11,627,000 | 11,853,296 | ||

5.125% 3/2/15 | 1,405,000 | 1,540,997 | ||

5.5% 12/15/16 | 1,891,000 | 2,098,919 | ||

6.625% 10/1/17 | 4,835,000 | 5,696,752 | ||

Mack-Cali Realty LP 7.75% 8/15/19 | 700,000 | 872,428 | ||

Post Apartment Homes LP 6.3% 6/1/13 | 3,812,000 | 4,073,728 | ||

Realogy Corp. 7.875% 2/15/19 (d) | 2,920,000 | 2,423,600 | ||

Reckson Operating Partnership LP 6% 3/31/16 | 3,651,000 | 3,864,635 | ||

Regency Centers LP: | ||||

4.95% 4/15/14 | 611,000 | 649,858 | ||

5.25% 8/1/15 | 2,133,000 | 2,307,961 | ||

5.875% 6/15/17 | 1,089,000 | 1,237,372 | ||

Simon Property Group LP 4.2% 2/1/15 | 3,659,000 | 3,901,811 | ||

Tanger Properties LP: | ||||

6.125% 6/1/20 | 10,268,000 | 11,591,227 | ||

6.15% 11/15/15 | 1,777,000 | 2,002,862 | ||

Toys 'R' Us Property Co. II LLC 8.5% 12/1/17 | 1,455,000 | 1,480,463 | ||

Ventas Realty LP 6.75% 4/1/17 | 250,000 | 260,000 | ||

| 178,025,725 | |||

Corporate Bonds - continued | ||||

| Principal | Value | ||

Nonconvertible Bonds - continued | ||||

FINANCIALS - continued | ||||

Thrifts & Mortgage Finance - 0.3% | ||||

Bank of America Corp.: | ||||

3.75% 7/12/16 | $ 12,400,000 | $ 12,233,964 | ||

5.65% 5/1/18 | 7,555,000 | 7,702,738 | ||

6.5% 8/1/16 | 9,000,000 | 9,653,868 | ||

First Niagara Financial Group, Inc. 6.75% 3/19/20 | 7,993,000 | 8,875,323 | ||

Wrightwood Capital LLC 1.9% 4/20/20 | 112,350 | 35,952 | ||

| 38,501,845 | |||

TOTAL FINANCIALS | 1,284,223,227 | |||

HEALTH CARE - 0.5% | ||||

Biotechnology - 0.0% | ||||

Celgene Corp. 2.45% 10/15/15 | 613,000 | 623,433 | ||

Health Care Providers & Services - 0.4% | ||||

Community Health Systems, Inc. 8.875% 7/15/15 | 1,860,000 | 1,855,350 | ||

Coventry Health Care, Inc.: | ||||

5.95% 3/15/17 | 1,747,000 | 1,968,160 | ||

6.3% 8/15/14 | 3,618,000 | 3,997,492 | ||

DaVita, Inc.: | ||||

6.375% 11/1/18 | 2,085,000 | 2,032,875 | ||

6.625% 11/1/20 | 1,020,000 | 991,950 | ||

Express Scripts, Inc.: | ||||

3.125% 5/15/16 | 10,525,000 | 10,759,781 | ||

5.25% 6/15/12 | 7,157,000 | 7,385,072 | ||

6.25% 6/15/14 | 2,629,000 | 2,927,242 | ||

HCA, Inc.: | ||||

6.5% 2/15/20 | 2,705,000 | 2,718,525 | ||

7.25% 9/15/20 | 115,000 | 116,725 | ||

HealthSouth Corp. 7.25% 10/1/18 | 1,695,000 | 1,678,050 | ||

IASIS Healthcare LLC/IASIS Capital Corp. 8.375% 5/15/19 (d) | 4,395,000 | 3,856,613 | ||

Medco Health Solutions, Inc.: | ||||

2.75% 9/15/15 | 1,176,000 | 1,202,332 | ||

4.125% 9/15/20 | 7,486,000 | 7,502,170 | ||

Sabra Health Care LP/Sabra Capital Corp. 8.125% 11/1/18 | 2,580,000 | 2,463,900 | ||

Corporate Bonds - continued | ||||

| Principal | Value | ||

Nonconvertible Bonds - continued | ||||

HEALTH CARE - continued | ||||

Health Care Providers & Services - continued | ||||

Skilled Healthcare Group, Inc. 11% 1/15/14 | $ 164,000 | $ 168,510 | ||

Vanguard Health Holding Co. II LLC / Vanguard Holding Co. II, Inc. 8% 2/1/18 | 2,750,000 | 2,640,000 | ||

| 54,264,747 | |||

Health Care Technology - 0.0% | ||||

DJO Finance LLC/DJO Finance Corp.: | ||||

7.75% 4/15/18 (d) | 925,000 | 874,125 | ||

10.875% 11/15/14 | 4,115,000 | 4,228,163 | ||

| 5,102,288 | |||

Pharmaceuticals - 0.1% | ||||

Endo Pharmaceuticals Holdings, Inc.: | ||||

7% 7/15/19 (d) | 860,000 | 870,750 | ||

7.25% 1/15/22 (d) | 860,000 | 870,750 | ||

Giant Funding Corp. 8.25% 2/1/18 (d) | 1,210,000 | 1,222,100 | ||

Mylan, Inc.: | ||||

6% 11/15/18 (d) | 1,030,000 | 1,011,975 | ||

7.625% 7/15/17 (d) | 1,115,000 | 1,170,750 | ||

Valeant Pharmaceuticals International: | ||||

6.5% 7/15/16 (d) | 2,550,000 | 2,384,250 | ||

6.875% 12/1/18 (d) | 3,440,000 | 3,199,200 | ||

7% 10/1/20 (d) | 255,000 | 234,600 | ||

Watson Pharmaceuticals, Inc. 5% 8/15/14 | 720,000 | 786,716 | ||

| 11,751,091 | |||

TOTAL HEALTH CARE | 71,741,559 | |||

INDUSTRIALS - 0.9% | ||||

Aerospace & Defense - 0.1% | ||||

BAE Systems Holdings, Inc.: | ||||

4.95% 6/1/14 (d) | 572,000 | 617,972 | ||

6.375% 6/1/19 (d) | 8,071,000 | 9,448,615 | ||

6.4% 12/15/11 (d) | 818,000 | 830,906 | ||

BE Aerospace, Inc. 6.875% 10/1/20 | 1,120,000 | 1,142,400 | ||

Huntington Ingalls Industries, Inc. 6.875% 3/15/18 (d) | 380,000 | 355,300 | ||

| 12,395,193 | |||

Airlines - 0.2% | ||||

Air Canada 9.25% 8/1/15 (d) | 735,000 | 705,600 | ||

Corporate Bonds - continued | ||||

| Principal | Value | ||

Nonconvertible Bonds - continued | ||||

INDUSTRIALS - continued | ||||

Airlines - continued | ||||

American Airlines, Inc. 7.5% 3/15/16 (d) | $ 2,575,000 | $ 2,323,938 | ||

AMR Corp. 9% 8/1/12 | 485,000 | 490,755 | ||

Continental Airlines, Inc.: | ||||

pass-thru trust certificates 9.798% 4/1/21 | 356,704 | 369,188 | ||

6.648% 3/15/19 | 3,249,044 | 3,362,761 | ||

6.75% 9/15/15 (d) | 3,405,000 | 3,315,449 | ||

6.9% 7/2/19 | 942,455 | 980,154 | ||

Continental Airlines, Inc. 9.25% 5/10/17 | 2,736,965 | 2,736,965 | ||

Delta Air Lines, Inc. pass-thru trust certificates: | ||||

6.375% 1/2/16 | 1,515,000 | 1,424,100 | ||

6.75% 11/23/15 | 1,515,000 | 1,378,650 | ||

8.021% 8/10/22 | 1,444,844 | 1,444,844 | ||

8.954% 8/10/14 | 1,981,876 | 2,001,694 | ||

Northwest Airlines, Inc. pass-thru trust certificates 8.028% 11/1/17 | 759,696 | 729,308 | ||

U.S. Airways pass-thru trust certificates: | ||||

6.85% 7/30/19 | 1,905,565 | 1,867,454 | ||

8.36% 1/20/19 | 1,441,215 | 1,441,215 | ||

United Air Lines, Inc. 9.875% 8/1/13 (d) | 707,000 | 724,675 | ||

United Air Lines, Inc. pass-thru trust certificates: | ||||

Class B, 7.336% 7/2/19 | 806,507 | 725,856 | ||

9.75% 1/15/17 | 2,134,421 | 2,337,191 | ||

12% 1/15/16 (d) | 730,061 | 792,116 | ||

| 29,151,913 | |||

Building Products - 0.1% | ||||

Building Materials Corp. of America: | ||||

6.75% 5/1/21 (d) | 1,710,000 | 1,658,700 | ||

6.875% 8/15/18 (d) | 2,550,000 | 2,556,375 | ||

Griffon Corp. 7.125% 4/1/18 | 2,220,000 | 2,086,800 | ||

| 6,301,875 | |||

Commercial Services & Supplies - 0.2% | ||||

ARAMARK Corp. 3.754% 2/1/15 (k) | 5,440,000 | 5,168,000 | ||

ARAMARK Holdings Corp. 8.625% 5/1/16 pay-in-kind (d)(k) | 1,715,000 | 1,715,000 | ||

Covanta Holding Corp. 7.25% 12/1/20 | 1,190,000 | 1,210,798 | ||

International Lease Finance Corp.: | ||||

6.75% 9/1/16 (d) | 1,620,000 | 1,644,300 | ||

8.625% 9/15/15 | 2,745,000 | 2,813,625 | ||

Corporate Bonds - continued | ||||

| Principal | Value | ||

Nonconvertible Bonds - continued | ||||

INDUSTRIALS - continued | ||||

Commercial Services & Supplies - continued | ||||

International Lease Finance Corp.: - continued | ||||

8.75% 3/15/17 | $ 2,865,000 | $ 2,936,625 | ||

8.875% 9/1/17 | 1,665,000 | 1,710,788 | ||

WP Rocket Merger Sub, Inc. 10.125% 7/15/19 (d) | 1,695,000 | 1,678,050 | ||

| 18,877,186 | |||

Construction & Engineering - 0.0% | ||||

Amsted Industries, Inc. 8.125% 3/15/18 (d) | 2,535,000 | 2,623,725 | ||

Odebrecht Finance Ltd.: | ||||

7% 4/21/20 (d) | 560,000 | 611,800 | ||

7.5% (d)(e) | 935,000 | 935,000 | ||

| 4,170,525 | |||

Electrical Equipment - 0.0% | ||||

Sensata Technologies BV 6.5% 5/15/19 (d) | 2,060,000 | 1,977,600 | ||

Industrial Conglomerates - 0.2% | ||||

General Electric Co. 5.25% 12/6/17 | 17,730,000 | 19,862,795 | ||

Marine - 0.0% | ||||

Navios Maritime Acquisition Corp./Navios Acquisition Finance US, Inc.: | ||||

8.625% 11/1/17 | 260,000 | 217,100 | ||

8.625% 11/1/17 (d) | 550,000 | 466,125 | ||

Navios Maritime Holdings, Inc. 8.875% 11/1/17 | 1,020,000 | 938,400 | ||

SCF Capital Ltd. 5.375% 10/27/17 (d) | 480,000 | 471,600 | ||

| 2,093,225 | |||

Professional Services - 0.0% | ||||

CDRT Merger Sub, Inc. 8.125% 6/1/19 (d) | 1,610,000 | 1,513,400 | ||

FTI Consulting, Inc. 6.75% 10/1/20 | 2,515,000 | 2,464,700 | ||

| 3,978,100 | |||

Road & Rail - 0.1% | ||||

Avis Budget Car Rental LLC/Avis Budget Finance, Inc.: | ||||

7.625% 5/15/14 | 1,202,000 | 1,198,995 | ||

7.75% 5/15/16 | 1,935,000 | 1,942,160 | ||

Georgian Railway Ltd. 9.875% 7/22/15 | 475,000 | 508,250 | ||

Hertz Corp.: | ||||

6.75% 4/15/19 (d) | 2,170,000 | 2,023,525 | ||

7.5% 10/15/18 (d) | 6,965,000 | 6,825,700 | ||

Corporate Bonds - continued | ||||

| Principal | Value | ||

Nonconvertible Bonds - continued | ||||

INDUSTRIALS - continued | ||||

Road & Rail - continued | ||||

Kansas City Southern de Mexico SA de CV 12.5% 4/1/16 | $ 1,335,000 | $ 1,591,988 | ||

Swift Services Holdings, Inc. 10% 11/15/18 | 1,915,000 | 1,915,000 | ||

| 16,005,618 | |||

Trading Companies & Distributors - 0.0% | ||||

Aircastle Ltd. 9.75% 8/1/18 | 1,575,000 | 1,634,063 | ||

Transportation Infrastructure - 0.0% | ||||

Aeropuertos Argentina 2000 SA 10.75% 12/1/20 (d) | 861,420 | 930,334 | ||

TOTAL INDUSTRIALS | 117,378,427 | |||

INFORMATION TECHNOLOGY - 0.4% | ||||

Communications Equipment - 0.1% | ||||

Avaya, Inc.: | ||||

9.75% 11/1/15 | 1,670,000 | 1,444,550 | ||

10.125% 11/1/15 pay-in-kind (k) | 1,660,000 | 1,452,500 | ||

CommScope, Inc. 8.25% 1/15/19 (d) | 1,310,000 | 1,290,350 | ||

EH Holding Corp. 6.5% 6/15/19 (d) | 1,725,000 | 1,725,000 | ||

Lucent Technologies, Inc.: | ||||

6.45% 3/15/29 | 5,010,000 | 4,308,600 | ||

6.5% 1/15/28 | 1,240,000 | 1,066,400 | ||

| 11,287,400 | |||

Computers & Peripherals - 0.0% | ||||

CDW Escrow Corp. 8.5% 4/1/19 (d) | 2,855,000 | 2,626,600 | ||

Seagate HDD Cayman: | ||||

6.875% 5/1/20 | 740,000 | 706,700 | ||

7% 11/1/21 (d) | 855,000 | 760,950 | ||

| 4,094,250 | |||

Electronic Equipment & Components - 0.1% | ||||

Reddy Ice Corp. 11.25% 3/15/15 | 635,000 | 574,675 | ||

Sanmina-SCI Corp. 7% 5/15/19 (d) | 4,090,000 | 3,701,450 | ||

Tyco Electronics Group SA: | ||||

5.95% 1/15/14 | 3,835,000 | 4,189,860 | ||

6% 10/1/12 | 4,835,000 | 5,107,360 | ||

6.55% 10/1/17 | 1,383,000 | 1,645,435 | ||

| 15,218,780 | |||

Corporate Bonds - continued | ||||

| Principal | Value | ||

Nonconvertible Bonds - continued | ||||

INFORMATION TECHNOLOGY - continued | ||||

Internet Software & Services - 0.0% | ||||

Equinix, Inc. 8.125% 3/1/18 | $ 2,530,000 | $ 2,681,800 | ||

IT Services - 0.1% | ||||

Audatex North America, Inc. 6.75% 6/15/18 (d) | 795,000 | 787,050 | ||

Ceridian Corp.: | ||||

11.25% 11/15/15 | 1,110,000 | 1,029,525 | ||

12.25% 11/15/15 pay-in-kind (k) | 795,000 | 731,400 | ||

First Data Corp.: | ||||

9.875% 9/24/15 | 1,485,000 | 1,351,350 | ||

11.25% 3/31/16 | 1,565,000 | 1,314,600 | ||

SunGard Data Systems, Inc.: | ||||

7.375% 11/15/18 | 1,095,000 | 1,053,938 | ||

10.25% 8/15/15 | 1,765,000 | 1,791,475 | ||

| 8,059,338 | |||

Office Electronics - 0.0% | ||||

Xerox Corp.: | ||||

4.25% 2/15/15 | 368,000 | 395,962 | ||

5.5% 5/15/12 | 1,998,000 | 2,062,008 | ||

| 2,457,970 | |||

Semiconductors & Semiconductor Equipment - 0.1% | ||||

Advanced Micro Devices, Inc. 7.75% 8/1/20 | 1,300,000 | 1,313,000 | ||

Amkor Technology, Inc.: | ||||

6.625% 6/1/21 (d) | 1,405,000 | 1,320,700 | ||

7.375% 5/1/18 | 2,060,000 | 2,060,000 | ||

Freescale Semiconductor, Inc. 8.05% 2/1/20 | 4,585,000 | 4,355,750 | ||

Spansion LLC 7.875% 11/15/17 (d) | 3,465,000 | 3,534,300 | ||

STATS ChipPAC Ltd. 7.5% 8/12/15 (d) | 550,000 | 574,750 | ||

| 13,158,500 | |||

TOTAL INFORMATION TECHNOLOGY | 56,958,038 | |||

MATERIALS - 0.8% | ||||

Chemicals - 0.4% | ||||

Braskem America Finance Co. 7.125% 7/22/41 (d) | 735,000 | 714,788 | ||

Braskem Finance Ltd.: | ||||

5.75% 4/15/21 (d) | 515,000 | 515,000 | ||

7% 5/7/20 (d) | 460,000 | 492,200 | ||

Celanese US Holdings LLC 6.625% 10/15/18 | 1,935,000 | 2,031,750 | ||

Corporate Bonds - continued | ||||

| Principal | Value | ||

Nonconvertible Bonds - continued | ||||

MATERIALS - continued | ||||

Chemicals - continued | ||||

Dow Chemical Co.: | ||||

4.85% 8/15/12 | $ 11,805,000 | $ 12,238,125 | ||

7.6% 5/15/14 | 16,974,000 | 19,561,381 | ||

Huntsman International LLC 8.625% 3/15/20 | 1,160,000 | 1,206,400 | ||

Ineos Finance PLC 9% 5/15/15 (d) | 1,715,000 | 1,723,575 | ||

INEOS Group Holdings PLC 8.5% 2/15/16 (d) | 1,895,000 | 1,648,650 | ||

Inergy LP/Inergy Finance Corp.: | ||||

6.875% 8/1/21 (d) | 685,000 | 664,450 | ||

7% 10/1/18 | 1,865,000 | 1,809,050 | ||

Lyondell Chemical Co. 11% 5/1/18 | 2,595,000 | 2,896,669 | ||

NOVA Chemicals Corp. 3.542% 11/15/13 (k) | 2,720,000 | 2,652,000 | ||

| 48,154,038 | |||

Construction Materials - 0.0% | ||||

CRH America, Inc. 6% 9/30/16 | 2,286,000 | 2,525,045 | ||

Headwaters, Inc. 7.625% 4/1/19 | 1,580,000 | 1,295,600 | ||

| 3,820,645 | |||

Metals & Mining - 0.4% | ||||

Alrosa Finance SA: | ||||

(Reg. S) 8.875% 11/17/14 | 460,000 | 510,025 | ||

7.75% 11/3/20 (d) | 700,000 | 747,250 | ||

Anglo American Capital PLC 9.375% 4/8/14 (d) | 6,817,000 | 8,055,506 | ||

ArcelorMittal SA 3.75% 3/1/16 | 2,911,000 | 2,879,486 | ||

BHP Billiton Financial (USA) Ltd. 5.125% 3/29/12 | 1,975,000 | 2,026,788 | ||

Boart Longyear Management Pty Ltd. 7% 4/1/21 (d) | 930,000 | 920,700 | ||

Corporacion Nacional del Cobre (Codelco) 6.375% 11/30/12 (d) | 2,002,000 | 2,125,782 | ||

CSN Islands XII Corp. 7% (Reg. S) (e) | 1,880,000 | 1,847,100 | ||

Edgen Murray Corp. 12.25% 1/15/15 | 3,960,000 | 3,722,400 | ||

Essar Steel Algoma, Inc. 9.375% 3/15/15 (d) | 2,990,000 | 2,847,975 | ||

Evraz Group SA: | ||||

8.25% 11/10/15 (d) | 630,000 | 664,650 | ||

9.5% 4/24/18 (Reg. S) | 780,000 | 864,427 | ||

FMG Resources (August 2006) Pty Ltd.: | ||||

6.375% 2/1/16 (d) | 190,000 | 186,675 | ||

6.875% 2/1/18 (d) | 580,000 | 577,100 | ||

7% 11/1/15 (d) | 2,140,000 | 2,172,100 | ||

JMC Steel Group, Inc. 8.25% 3/15/18 (d) | 2,310,000 | 2,182,950 | ||

McJunkin Red Man Corp. 9.5% 12/15/16 | 3,950,000 | 3,969,750 | ||

Corporate Bonds - continued | ||||

| Principal | Value | ||

Nonconvertible Bonds - continued | ||||

MATERIALS - continued | ||||

Metals & Mining - continued | ||||

Metinvest BV 10.25% 5/20/15 (d) | $ 485,000 | $ 509,250 | ||

Severstal Columbus LLC 10.25% 2/15/18 | 3,790,000 | 3,922,650 | ||

Southern Copper Corp. 6.75% 4/16/40 | 1,690,000 | 1,785,823 | ||

Tube City IMS Corp. 9.75% 2/1/15 | 1,700,000 | 1,695,750 | ||

United States Steel Corp. 6.65% 6/1/37 | 2,349,000 | 1,908,563 | ||

Vale Overseas Ltd. 6.25% 1/23/17 | 5,581,000 | 6,331,600 | ||

Vedanta Resources PLC: | ||||

6.75% 6/7/16 (d) | 3,090,000 | 2,873,700 | ||

8.25% 6/7/21 (d) | 1,600,000 | 1,504,000 | ||

Votorantim Cimentos SA 7.25% 4/5/41 (d) | 515,000 | 507,275 | ||

| 57,339,275 | |||

Paper & Forest Products - 0.0% | ||||

ABI Escrow Corp. 10.25% 10/15/18 (d) | 795,000 | 834,750 | ||

Sino-Forest Corp. 6.25% 10/21/17 (d) | 890,000 | 240,300 | ||

| 1,075,050 | |||

TOTAL MATERIALS | 110,389,008 | |||

TELECOMMUNICATION SERVICES - 1.7% | ||||

Diversified Telecommunication Services - 1.0% | ||||

Alestra SA de RL de CV 11.75% 8/11/14 | 1,635,000 | 1,823,025 | ||

AT&T, Inc.: | ||||

2.5% 8/15/15 | 7,670,000 | 7,853,927 | ||

5.35% 9/1/40 | 4,006,000 | 4,068,277 | ||

6.3% 1/15/38 | 16,665,000 | 18,595,057 | ||

BellSouth Capital Funding Corp. 7.875% 2/15/30 | 742,000 | 960,405 | ||

CenturyLink, Inc.: | ||||

6.15% 9/15/19 | 4,793,000 | 4,722,715 | ||

6.45% 6/15/21 | 12,933,000 | 12,579,593 | ||

7.6% 9/15/39 | 2,067,000 | 1,901,055 | ||

Clearwire Communications LLC/Clearwire Finance, Inc. 12% 12/1/15 (d) | 3,720,000 | 3,515,400 | ||

Embarq Corp. 7.995% 6/1/36 | 3,924,000 | 3,721,726 | ||

Frontier Communications Corp.: | ||||

7.875% 4/15/15 | 1,045,000 | 1,085,442 | ||

8.125% 10/1/18 | 1,810,000 | 1,873,350 | ||

Global Crossing Ltd. 9% 11/15/19 (d) | 1,820,000 | 2,184,000 | ||

Intelsat Ltd. 11.25% 6/15/16 | 1,635,000 | 1,700,400 | ||

Corporate Bonds - continued | ||||

| Principal | Value | ||

Nonconvertible Bonds - continued | ||||

TELECOMMUNICATION SERVICES - continued | ||||

Diversified Telecommunication Services - continued | ||||

Intelsat Luxembourg SA: | ||||

11.25% 2/4/17 | $ 1,215,000 | $ 1,178,550 | ||

11.5% 2/4/17 pay-in-kind (d)(k) | 1,860,000 | 1,790,250 | ||

11.5% 2/4/17 pay-in-kind (k) | 7,388,205 | 7,074,206 | ||

Sprint Capital Corp.: | ||||

6.875% 11/15/28 | 10,465,000 | 9,366,175 | ||

6.9% 5/1/19 | 1,140,000 | 1,122,900 | ||

8.75% 3/15/32 | 905,000 | 927,625 | ||

Telefonica Emisiones SAU: | ||||

5.134% 4/27/20 | 10,522,000 | 9,991,197 | ||

5.462% 2/16/21 | 6,967,000 | 6,730,582 | ||

6.421% 6/20/16 | 1,162,000 | 1,220,549 | ||

Telemar Norte Leste SA 5.5% 10/23/20 (d) | 530,000 | 526,025 | ||

U.S. West Communications 7.5% 6/15/23 | 3,760,000 | 3,703,600 | ||

Verizon Communications, Inc.: | ||||

6.1% 4/15/18 | 6,000,000 | 7,132,584 | ||

6.25% 4/1/37 | 2,348,000 | 2,660,068 | ||

6.9% 4/15/38 | 6,295,000 | 7,655,312 | ||

Verizon New York, Inc. 6.875% 4/1/12 | 3,309,000 | 3,419,990 | ||

Wind Acquisition Finance SA: | ||||