UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 10-K

| x | Annual Report Pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 |

For the year ended December 31, 2008

| ¨ | Transition Report Pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 |

For the transition period from to

Commission File Number 1-9810

OWENS & MINOR, INC.

(Exact name of registrant as specified in its charter)

| | |

| Virginia | | 54-1701843 |

(State or other jurisdiction of incorporation or organization) | | (I.R.S. Employer Identification No.) |

| |

| 9120 Lockwood Boulevard, Mechanicsville, Virginia | | 23116 |

| (Address of principal executive offices) | | (Zip Code) |

Registrant’s telephone number, including area code (804) 723-7000

Securities registered pursuant to Section 12(b) of the Act:

| | |

Title of each class | | Name of each exchange on which registered |

| Common Stock, $2 par value | | New York Stock Exchange |

| Preferred Stock Purchase Rights | | New York Stock Exchange |

| 6.35% Senior Notes due 2016 | | Not Listed |

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer (as defined in Rule 405 of the Securities Act). Yes x No ¨

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 12(d) of the Act. Yes ¨ No x

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No ¨

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. x

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, or a non-accelerated filer. See definition of “accelerated filer and large accelerated filer” in Rule 12b-2 of the Exchange Act.

| | | | |

| Large accelerated filer x | | Accelerated filer ¨ | | Non-accelerated filer ¨ |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ¨ No x

The aggregate market value of Common Stock held by non-affiliates (based upon the closing sales price) was approximately $1,890,330,999 as of June 30, 2008.

The number of shares of the Company’s common stock outstanding as of February 23, 2009 was 41,418,080 shares.

Documents Incorporated by Reference

The proxy statement for the annual meeting of shareholders on April 24, 2009, is incorporated by reference for Part III.

Form 10-K Table of Contents

“Corporate Officers,” located on page 8 of the company’s printed Annual Report, can be found at the end of the electronic filing of this Form 10-K.

2

Part I

Item 1. Business

The Company

Owens & Minor, Inc. and subsidiaries (Owens & Minor, O&M or the company) is a leading national distributor of medical and surgical supplies to the acute-care market and a healthcare supply-chain management company. In its acute-care supply distribution business, the company distributes over 220,000 finished medical and surgical products produced by over 1,600 suppliers to approximately 4,500 healthcare provider customers from 55 distribution and service centers nationwide. The company’s primary distribution customers are acute-care hospitals. Many of these hospital customers are represented by integrated healthcare networks (IHNs) or group purchasing organizations (GPOs) that negotiate pricing with suppliers and contract for distribution services with the company. Other customers include the federal government, for which Owens & Minor serves as a prime vendor for medical and surgical supply distribution services for the U.S. Department of Defense. On a more limited basis, the company serves alternate care providers including ambulatory surgery centers, physicians’ practices, clinics, home healthcare organizations, nursing homes and rehabilitation facilities. The company typically provides its distribution services under contractual arrangements with terms ranging from three to five years. Most of O&M’s sales consist of consumable goods such as disposable gloves, dressings, endoscopic products, intravenous products, needles and syringes, sterile procedure trays, surgical products and gowns, urological products and wound closure products.

Founded in 1882 and incorporated in 1926 in Richmond, Virginia, as a wholesale drug company, the company sold the wholesale drug division in 1992 to concentrate on medical and surgical supply distribution. Since then, O&M has significantly expanded and strengthened its national presence through internal growth and acquisitions, including the October 1, 2008, acquisition of certain assets and liabilities of The Burrows Company, a Chicago-based, privately-held distributor of medical and surgical supplies to the acute-care market. Additional information regarding the acquisition and the company’s other acquisition activity is included in Note 3 of the consolidated financial statements.

The Acute-Care Supply Distribution Industry

Distributors of medical and surgical supplies provide a wide variety of products and services to healthcare providers, including hospitals and hospital-based systems, and alternate care providers. The company contracts with these providers directly under terms negotiated with GPOs and IHNs. The medical/surgical supply distribution industry continues to grow as the aging population in the United States requires more healthcare services and as emerging medical technology leads to the development of new products and procedures. Over the years, healthcare providers have adapted their health systems to meet the evolving needs of the markets they serve. In order to manage supply procurement and distribution challenges, these providers have increasingly forged strategic relationships with national medical and surgical supply distributors. The traditional role of distributors in warehousing and delivering medical and surgical supplies to customers continues to evolve into the role of assisting customers in efficiently managing the entire supply chain.

Consolidation trends in the overall healthcare market have led to the creation of larger and more sophisticated healthcare providers, which increasingly seek methods to lower the total cost of delivering healthcare services. These healthcare providers face a variety of financial challenges, including the cost of purchasing, receiving, storing and tracking medical and surgical supplies. The competitive nature of the medical/surgical supply distribution industry mitigates distributors’ ability to influence pricing, keeping profit margins relatively modest. However, distributors have opportunities to help reduce healthcare providers’ costs by offering services designed to streamline the supply chain through inventory management, activity-based pricing, consulting and outsourcing services. These trends have driven significant consolidation within the medical/surgical supply distribution industry due to the competitive advantages enjoyed by larger distributors, which include, among other things, the ability to serve nationwide customers, buy inventory in large volume, and develop technology platforms and decision support systems.

3

The Acute-Care Supply Distribution Business

Through its healthcare provider distribution business, the company purchases a large volume of medical and surgical products from suppliers, stores these items at its distribution centers, and provides delivery services to its customers. The company has 55 distribution centers located throughout the continental United States, three of which are integrated service centers serving the needs of specific healthcare systems; additional warehouse space in nine locations near the company’s distribution centers; and one warehousing arrangement in Hawaii. The company’s distribution centers generally serve hospitals and other customers within a 200-mile radius, delivering most customer orders with a fleet of leased trucks. Almost all of O&M’s delivery personnel are employees of the company, thereby increasing the consistency of customer service. Contract carriers and parcel services are used in situations where it is more cost-effective. The company customizes its product pallets, truckloads and delivery schedules according to the customers’ needs, thus enabling increased efficiency in receiving and storing the product. Sales, logistics, credit management and operations teammates are located at or near distribution centers to manage service to healthcare provider customers.

O&M strives to make the supply chain more efficient through the use of advanced warehousing, delivery and purchasing techniques, enabling customers to order and receive products using just-in-time and stockless services. A key component of this strategy is a significant investment in information technology infrastructure and services. O&M uses a variety of enterprise systems to support its business needs and efficiently manage its business growth, including warehouse management systems, customer service functions, and demand forecasting programs. The company employs a number of customer-facing technology solutions, including OMDirectSM, an Internet-based product catalog and direct ordering system that facilitates commerce with customers and suppliers. O&M also uses its technology and logistics experience to offer customers supply-chain management solutions, including outsourcing and logistics services through its OMSolutionsSMprofessional services unit.

Products & Services

The distribution of medical and surgical supplies to healthcare providers, including O&M’s MediChoice® private label product line, accounts for over 95% of the company’s revenues.

The company also offers its customers a number of supply-chain management services, including inventory management; information management; strategic, logistical and clinical inventory management consulting; materials management outsourcing; and resource management. Examples are as follows:

| | • | | OMSolutionsSM is comprised of O&M’s supply-chain consulting, customer technology and resource management teams. OMSolutionsSM implements customized healthcare supply chain solutions through the integration of people, processes and technologies. Services offered by OMSolutionsSM create value by decreasing supply chain costs while increasing operating efficiency. For example, OMSolutionsSM provides clinician consultants who work one-on-one with hospital staff to standardize and efficiently utilize products, processes and technologies. Other examples of OMSolutionsSM services are in-depth value analysis and cost management, receiving and storeroom redesign, conducting physical inventories, and configuration of automatic inventory replenishment systems. |

| | • | | PANDAC® is O&M’s operating room-focused inventory management program that helps healthcare providers reduce and control suture and endo-mechanical inventory. Detailed analysis and ongoing reporting decreases redundancy and obsolescence, and increases inventory turns, which in turn reduces investment in these high-cost products. |

| | • | | SurgiTrack® is O&M’s customizable surgical supply service that includes the assembly and delivery, in procedure-based totes, of supplies based on the operating room’s surgical schedule. Through in-depth assessment, O&M provides customers with information in order to standardize products, reduce inventory and streamline workflow. |

4

| | • | | WISDOM GoldSM is O&M’s Internet-based spend management, data normalization and contract management solution. WISDOM GoldSM is supported by analysts, either on-site or remote, who identify cost saving opportunities for our customers. WISDOM GoldSM enables customers to gain deeper understanding and control over their supply procurement and contracting efforts. WISDOM GoldSM consists of three components: WISDOMSM; a standard product master file (“Gold” file) that includes industry standard information, including catalog numbers, names and product codes; and an Internet-based contract management system that digitizes local and GPO contracts, maintains contract details in a central database, and synchronizes customers’ item files to their contract portfolios. |

| | • | | Clinical Supply SolutionsSM (CSS) is an Internet-based order, inventory, contract, revenue, resource and utilization management service that enables healthcare providers to reduce expenses by accurately tracking and managing physician-preference products and medical/surgical inventories in high-cost clinical specialty departments, such as cardiac catheterization labs, radiology and operating rooms. CSS is a service offering that is enabled by O&M’s proprietary technology QSightand WISDOM GoldSMand is supported by an analyst resource center. |

Customers

The company currently provides distribution, consulting and outsourcing services to approximately 4,500 healthcare providers, including hospitals, the federal government and alternate care providers, contracting with them directly and through IHNs and GPOs. The company also provides logistics services to manufacturers of medical and surgical products.

GPOs and IHNs

GPOs are entities that act on behalf of a group of healthcare providers to obtain better pricing and other benefits than may be available to individual providers. Hospitals, physicians and other types of healthcare providers have joined GPOs to take advantage of improved economies of scale and to obtain services from medical and surgical supply distributors ranging from discounted product pricing to logistical and clinical support. GPOs negotiate directly with medical and surgical product suppliers and distributors on behalf of their members, establishing exclusive or multi-supplier relationships; however, GPOs cannot ensure that members will purchase their supplies from a particular distributor. O&M is a distributor for Novation, a GPO which represents the purchasing interests of more than 2,400 healthcare organizations. The company has a five-year agreement with Novation expiring in 2011. Sales to Novation members represented approximately 38% of the company’s revenue in 2008 and 41% in 2007. The company is also party to a distribution agreement with Premier, a GPO representing more than 2,100 hospitals. Premier provides resources to support healthcare services, including group purchasing activities. Sales to Premier members represented approximately 20% of O&M’s revenue in both 2008 and 2007. Effective January 1, 2009, the company executed a new three-year agreement with Premier. The company is also a distributor for Broadlane, a GPO providing national contracting for more than 900 acute-care hospitals and more than 2,600 sub-acute-care facilities, including Tenet Healthcare Corporation, one of the largest for-profit hospital chains in the nation. The company has a five-year agreement with Broadlane expiring in 2012. Sales to Broadlane members represented approximately 12% of O&M’s revenue in both 2008 and 2007.

IHNs are typically networks of commonly owned or managed healthcare providers that seek to offer a broad spectrum of healthcare services and geographic coverage to a particular market. IHNs are significant in the acute-care market because of their expanding role in healthcare delivery and cost containment and their reliance upon the hospital as a key component of their organizations. Because IHNs frequently rely on cost containment as a competitive advantage, IHNs have become an important source of demand for O&M’s enhanced inventory management and other value-added services.

5

Individual Providers

In addition to contracting with healthcare providers at the IHN level and through GPOs, O&M contracts directly with individual healthcare providers and smaller networks of healthcare providers that have joined to negotiate terms.

Sales and Marketing

O&M’s healthcare provider sales and marketing function is organized to support field sales teams throughout the United States. Local sales teams are positioned to respond to customer needs quickly and efficiently. National account directors work closely with IHNs and GPOs to meet their needs and coordinate activities with individual members. The company also has an enterprise sales team that operates centrally and coordinates the company’s service offerings for large customers. The company’s integrated sales and marketing strategy offers customers value-added services in supplier management, distribution and logistics, analytics, resource management and consulting, and clinical supply management. O&M provides special training and support tools to help its sales teams promote the value of its cost saving portfolio of programs and services.

Pricing

Industry practice is for healthcare providers, or their IHNs or GPOs, to negotiate product pricing directly with suppliers and then negotiate distribution pricing terms with distributors.

The majority of O&M’s distribution arrangements compensate the company on a cost-plus percentage basis, under which a negotiated fixed-percentage distribution fee is added to the product cost agreed to by the customer and the supplier or the cost to O&M of procuring the product. The determination of this percentage distribution fee is typically based on purchase volume, as well as other factors, and usually remains constant for the life of the contract. In many cases, distribution contracts in the medical/surgical supply industry specify a minimum volume of product to be purchased and are terminable by either party upon relatively short notice.

In some cases, the company may offer pricing that varies during the life of the contract depending upon purchase volume, and, as a result, the negotiated fixed-percentage distribution fee may increase or decrease over time. Under these contracts, customers’ distribution fees may be reset after a measurement period to either more or less favorable pricing based on significant changes in purchase volume. If a customer’s distribution fee percentage is adjusted, the modified percentage distribution fee applies only to purchases made following the change. Because customer sales volumes typically change gradually, changes in distribution fee percentages for individual customers under this type of arrangement have an insignificant effect on total company results.

Pricing under O&M’s CostTrackSM activity-based pricing model differs from pricing under a traditional cost-plus model. With CostTrackSM, the pricing of services is based on the costs to O&M of providing the services required by the customer. As a result, this pricing model more accurately aligns distribution fees charged with the costs of the individual services provided.

O&M also has arrangements under which incremental fees are charged for enhanced inventory management services, such as more frequent deliveries and distribution of products in small units of measure.

OMSolutionsSM pricing is based on professional rates and costs of managing and providing a team or individual to provide specific services. Additionally, technology costs are based on the structure and complexity of the customer engagement, including spending level, contracts, system interfacing and, as applicable, number of facilities. The company has certain contracts for its OMSolutionsSM services under which the company is obligated to make payments if performance targets specified by the contract are not achieved.

6

Suppliers

O&M believes that its size, strength and long-standing relationships enable it to obtain attractive terms from suppliers, and the company has well-established relationships with virtually all major suppliers of medical and surgical supplies. The company works with its largest suppliers to create operating efficiencies in the supply-chain through a number of programs which drive product standardization and consolidation for the company and its healthcare provider customers. By increasing the volume of purchases from the company’s most efficient suppliers, the company provides operational benefits and cost savings throughout the supply-chain.

The company works very closely with its branded supplier base to enlist their participation in a variety of O&M supplier program offerings. O&M supplier programs provide for enhanced levels of support that are closely aligned with annual supplier objectives in the areas of product market share and sales growth attainment. O&M receives incentives from these suppliers, including cash discounts for prompt payment, operational efficiency funding and performance-based incentives. Operational incentives are negotiated annually and are based on improved end-to-end supply-chain expenses realized by the suppliers. Sales of products from suppliers participating in the company’s supply-chain efficiency programs represented 45% of O&M’s 2008 revenue.

The company offers MediChoice®, O&M’s private label brand of medical and surgical products and equipment. O&M partners with a select group of manufacturers known for their quality and high service levels for the MediChoice® products to provide cost savings alternatives on over 1,800 mostly commodity products. MediChoice® supports a savings value and a comprehensive product portfolio for healthcare provider customers in combination with branded supplier partner offerings.

Sales of products of Covidien accounted for approximately 14% and 13% for 2008 and 2007, respectively, of the company’s revenue. Sales of products of Johnson & Johnson Health Care Systems, Inc. were approximately 11% of the company’s revenue for 2008 and 2007.

Information Technology

To support its strategic efforts, the company has implemented information systems to manage all aspects of operations, including order fulfillment, customer service, warehouse and inventory management, asset management, electronic commerce, and financial management. O&M believes its investment in and use of technology in the management of operations provides the company with a significant competitive advantage.

O&M has an agreement with Perot Systems Corporation through 2014 to outsource its information technology operations. This agreement includes the management and operation of information technology and infrastructure, as well as support, development and enhancement of all key business systems.

The company’s technology strategy and expenditures focus on customer service, electronic commerce, data warehousing, decision support, supply-chain management, warehousing management, and sales and marketing programs, as well as significant enhancements to back office systems and overall technology infrastructure. O&M uses electronic commerce technology to conduct business transactions with customers, suppliers and other trading partners. These capabilities in technology include the award-winning OMDirectSM Internet Order Fulfillment system, and the WISDOM GoldSM knowledge management and decision support system.

Asset Management

In the medical/surgical supply distribution industry, a significant investment in inventory and accounts receivable is required to meet the rapid delivery requirements of customers and provide high-quality service. As a result, efficient asset management is essential to the company’s profitability. O&M is focused on effective processes to optimize inventory and collect accounts receivable.

7

Inventory

The significant and ongoing emphasis on cost control in the healthcare industry puts pressure on suppliers, distributors and healthcare providers to manage their inventory more efficiently. O&M’s response to these ongoing challenges has been to develop inventory management capabilities based upon proven planning techniques; to utilize a highly flexible client/server warehouse management system; to standardize product whenever possible; and to collaborate with supply-chain partners on inventory productivity initiatives, including vendor-managed inventory, freight optimization and lead-time reductions.

During 2008, the company invested in certain infrastructure initiatives designed to improve operational efficiency in its operating units. The company installed automation equipment in certain large distribution centers where the high volume of low unit of measure business is expected to benefit the most from the use of such equipment. The company believes it will achieve productivity improvements, such as an increase in the number of lines-picked-per-hour, by adding automation equipment. In addition, the company launched a pilot project for voice-pick technology in selected distribution centers. This hands-free communication technology will enable warehouse teammates to improve speed and accuracy as they compile customer orders in the warehouse setting. Over time, the company intends to install this voice-pick technology, as appropriate, throughout its distribution network.

Accounts Receivable

The company believes its credit practices are consistent with those of other acute-care medical and surgical supply distributors. O&M actively manages its accounts receivable to minimize credit risk and days sales outstanding (DSO). The company maintains reserves for estimated credit losses.

Competition

The acute-care medical/surgical supply distribution industry in the United States is highly competitive. The sector includes two major nationwide distributors: O&M and Cardinal Health, Inc. The company also competes with a smaller national distributor of medical and surgical supplies, Medline, Inc., and a number of regional and local distributors.

Competitive factors within the medical/surgical supply distribution industry include total delivered product cost, product availability, the ability to fill and invoice orders accurately, delivery time, range of services provided, inventory management, information technology, electronic commerce capabilities, and the ability to meet customer-specific requirements. O&M believes its emphasis on technology, combined with a customer-focused approach to distribution and value-added services, enables it to compete effectively with both larger and smaller distributors.

Direct-to-Consumer Supply Distribution Business

Starting in 2005, with the acquisition of Access Diabetic Supply, LLC, O&M operated a direct-to-consumer supply distribution business (DTC business) under the trade name AOM Healthcare Solutions (AOM). AOM primarily marketed blood glucose monitoring devices, test strips and other ancillary products used by diabetic consumers for self-testing, mainly through direct-response advertising using a variety of media. AOM shipped products directly to approximately 178,000 customers’ homes throughout the United States by mail or parcel service and managed the documentation and insurance claims-filing process for its customers, collecting most of its revenue directly from Medicare or private insurance providers, and billing the customer for any remainder. As a result, pricing was almost wholly dependent upon the reimbursement rates set by Medicare and private insurers. AOM did not manufacture products, but purchased its products from a number of suppliers.

In December 2008, O&M made a decision to exit the DTC business and entered into a definitive agreement to sell certain assets of the business, including customer data and intellectual property, to Liberty Healthcare

8

Group, Inc., a subsidiary of Medco Health Solutions, Inc., for $63 million. The transaction closed on January 2, 2009. O&M retained the remaining assets and liabilities, including accounts receivable. Additional information regarding this discontinued operation is included in Note 4 of the consolidated financial statements.

Other Matters

Regulation

The medical/surgical supply distribution industry is subject to regulation by federal, state and local government agencies. Each of O&M’s distribution centers is licensed to distribute medical and surgical supplies, as well as certain pharmaceutical and related products. The company must comply with laws and regulations, including those addressing operating, storage, transport, safety and security standards for each of its distribution centers, of the Food and Drug Administration, the Department of Transportation, the Department of Homeland Security, the Occupational Safety and Health Administration, state boards of pharmacy, or similar state licensing boards and regulatory agencies. The company also is subject to various federal and state laws intended to protect the privacy of health or other personal information and prevent healthcare fraud and abuse. In addition, the DTC business must comply with Medicare regulations regarding billing practices. O&M believes it is in material compliance with all statutes and regulations applicable to distributors of medical and surgical supply products and pharmaceutical and related products, including the Healthcare Insurance Portability and Accountability Act of 1996 (HIPAA), Medicare, Medicaid, as well as applicable general employment and employee health and safety laws and regulations.

Employees

At the end of 2008, the company had approximately 5,300 full- and part-time teammates. O&M believes that ongoing teammate training is critical to performance, using Owens & Minor University, an in-house training facility, to offer classes in leadership, management development, finance, operations and sales. Management believes that relations with teammates are good.

Available Information

The company makes its Forms 10-K, Forms 10-Q and Forms 8-K (and all amendments to these reports) available free of charge through the “SEC Filings” link in the Investor Relations content section on the company’s website located at www.owens-minor.com as soon as reasonably practicable after they are filed with or furnished to the SEC. Information included on the company’s website is not incorporated by reference into this Annual Report on Form 10-K.

Additionally, the company has adopted a written Code of Honor that applies to all of the company’s directors, officers and teammates, including its principal executive officer and senior financial officers. This Code of Honor (including any amendment to or waiver of a provision thereof) and the company’s Corporate Governance Guidelines are available on the company’s website at www.owens-minor.com.

Item 1A. Certain Risk Factors

Set forth below are certain risk factors that the company believes could affect its business and prospects. These risk factors are in addition to those mentioned in other parts of this report.

Competition

The medical/surgical supply distribution industry in the United States is highly competitive. The company competes with other national distributors and a number of regional and local distributors. Competitive factors within the medical/surgical supply distribution industry include total delivered product cost, product availability,

9

the ability to fill and invoice orders accurately, delivery time, range of services provided, inventory management, information technology, electronic commerce capabilities, and the ability to meet special requirements of customers. The company’s success is dependent on its ability to compete on the above factors and to continually bring greater value to customers at a lower cost. These competitive pressures could have a material adverse effect on the company’s results of operations.

Dependence on Significant Customers

In 2008, the company’s top ten customers represented approximately 20% of its revenue. In addition, in 2008, approximately 70% of the company’s revenue was from sales to member hospitals under contract with its three largest GPOs: Novation, Premier and Broadlane. The company could lose a significant customer or GPO relationship if an existing contract expires without being replaced or is terminated by the customer or GPO prior to its expiration (if permitted by the applicable contract). Although the termination of the company’s relationship with a given GPO would not necessarily result in the loss of all of the member hospitals as customers, any such termination of a GPO relationship or a significant individual customer relationship could have a material adverse effect on the company’s results of operations.

The company has a contract with Defense Supply Center, Philadelphia (DSCP) under which the U.S. Department of Defense, the company’s largest customer, and other federal agencies purchase supplies and services. The DSCP contract expires in October 2010. A significant decline in volume of sales under this contract or a failure to renew the contract upon expiration could have a material adverse effect on the company’s results of operations.

Dependence on Significant Suppliers

The company distributes approximately 220,000 products from over 1,600 suppliers and is dependent on these suppliers for the supply of products. In 2008, sales of products of the company’s ten largest suppliers accounted for approximately 56% of revenue. The company relies on suppliers to provide agreeable purchasing and delivery terms and sales performance incentives. The company’s ability to sustain adequate gross margins has been, and will continue to be, partially dependent upon its ability to obtain favorable terms and incentives from suppliers, as well as suppliers’ continuing use of third-party distributors to sell and deliver their products. A change in terms by a significant supplier, or the decision of such a supplier to distribute its products directly to hospitals rather than through third-party distributors, could have a material adverse effect on the company’s results of operations.

Bankruptcy, Insolvency or other Credit Failure of Customers

The company provides credit, in the normal course of business, to its customers. The company performs initial and ongoing credit evaluations of its customers and maintains reserves for credit losses. The bankruptcy, insolvency or other credit failure of one or more customers with substantial balances due to the company could have a material adverse effect on the company’s results of operations.

Changes in the Healthcare Environment

O&M, its customers and its suppliers are subject to extensive federal and state regulations relating to healthcare, as well as the policies and practices of the private healthcare insurance industry. In recent years, there have been a number of government and private initiatives to reduce healthcare costs and government spending. These changes have included an increased reliance on managed care; consolidation of competitors, suppliers and customers; and the development of larger, more sophisticated purchasing groups. All of these changes place additional pressure on healthcare providers, who in turn seek to reduce the costs and pricing of products and services provided by the company. The company expects the healthcare industry to continue to change significantly and these potential changes, which may include a reduction in government support of healthcare

10

services, adverse changes in legislation or regulations, and reductions in healthcare reimbursement practices, could have a material adverse effect on the company’s results of operations.

Operating Margin Initiatives

Competitive pricing pressure has been a significant factor in recent years and management expects this trend to continue. In addition, suppliers continue to seek more restrictive agreements with distributors, resulting in lower product margins and reduced profitability. The company is working to counteract the effects of these trends through several margin initiatives, including consulting and outsourcing services, through the OMSolutionsSM business unit, and MediChoice®, the company’s private label brand of select medical/surgical products. In addition, the company offers customers a wide range of value-added services, including PANDAC®, Wisdom GoldSM, Clinical Supply SolutionsSM and others, all of which enhance profitability. The company also works with suppliers on programs to enhance gross margin. If these margin initiatives fail to produce anticipated results, the company’s results of operations could be materially adversely affected.

Reliance on Information Systems and Technological Advancement

The company relies on information systems to receive, process, analyze and manage data in distributing thousands of inventory items to customers from numerous distribution centers across the country. These systems are also relied on for billings and collections from customers, as well as the purchase of and payment for inventory and related transactions from hundreds of suppliers. The company’s business and results of operations may be adversely affected if these systems are interrupted or damaged by unforeseen events or if they fail for any extended period of time. In addition, the success of the company’s long-term growth strategy is dependent upon its ability to continually monitor and upgrade its information systems to provide better service to customers. A third-party service provider, Perot Systems Corporation, is responsible for managing a significant portion of the company’s information systems, including key operational and financial systems. The company’s business and results of operations may be materially adversely affected if the third-party service provider does not perform satisfactorily.

Regulatory Requirements

The company must comply with numerous laws and regulations, including those of the Food and Drug Administration, the Department of Transportation, the Department of Homeland Security, the Occupational Safety and Health Administration, state boards of pharmacy, or similar state licensing boards, and other regulatory agencies. Also, the company is subject to various federal and state laws intended to protect the privacy of health or other personal information and prevent healthcare fraud and abuse. Although the company believes it is in material compliance with all applicable laws and regulations, any failure to comply with existing laws and regulations or the imposition of any additional laws and regulations could have a material adverse effect on the company’s business.

Strategic Initiatives

The company has made and is continuing to make substantial investments in the development and implementation of certain strategic initiatives designed to drive long-term growth in profitability and shareholder value as well as continued improvement in results of operations. There can be no assurance that the company will be able to successfully implement its strategic initiatives or that they will produce the desired results, which could have a material adverse effect on the company’s business and financial performance.

General Economic Climate

Recent deterioration in the financial and economic climate has expanded and intensified, having a negative impact on most sectors of the U.S. economy. This deterioration in the financial and economic climate could

11

reduce patient demand for healthcare services, intensify pressures on healthcare providers to reduce both costs and purchases of products and services of the company and compromise customers’ ability to timely pay for their purchases. These and other possible consequences of financial and economic changes, including but not limited to the ability of banks to honor commitments under the company’s credit facility, could materially and adversely affect the company’s business and financial results.

Item 1B. Unresolved Staff Comments

None.

Item 2. Properties

The company owns its corporate headquarters building, and adjacent acreage, in Mechanicsville, Virginia, a suburb of Richmond, Virginia. The company owns nine distribution centers, all of which were acquired from The Burrows Company and are being offered for sale. Three of these distribution centers were closed as of December 31, 2008. The company leases office and warehouse space from unaffiliated third parties for 49 distribution centers across the United States, of which three are integrated service centers. The company also leases additional warehouse space in nine locations near the company’s distribution centers; one distribution center that is closed; offices and shipping facilities for its DTC supply distribution business in southern Florida; and small offices for sales and consulting personnel across the United States. In addition, the company has a warehousing arrangement in Honolulu, Hawaii, with an unaffiliated third party, and leases space on a temporary basis from time to time to meet its inventory storage needs.

The company regularly assesses its business needs and makes changes to the capacity and location of distribution centers. The company believes that its facilities are adequate to carry on its business as currently conducted. A number of leases are scheduled to terminate within the next several years. The company believes that, if necessary, it could find facilities to replace these leased premises without suffering a material adverse effect on its business.

Item 3. Legal Proceedings

The company is subject to various legal actions that are ordinary and incidental to its business, including contract disputes, employment, workers’ compensation, product liability, regulatory and other matters. The company establishes reserves from time to time based upon periodic assessment of the potential outcomes of pending matters. In addition, the company believes that any potential liability arising from employment, product liability, workers’ compensation and other personal injury litigation matters would be adequately covered by the company’s insurance coverage, subject to policy limits, applicable deductibles and insurer solvency. While the outcome of legal actions cannot be predicted with certainty, the company believes, based on current knowledge and the advice of counsel, that the outcome of these currently pending matters, individually or in the aggregate, will not have a material adverse effect on the company’s financial condition or results of operations.

Item 4. Submission of Matters to a Vote of Security Holders

During the fourth quarter of 2008, no matters were submitted to a vote of security holders.

12

Part II

Item 5. Marketfor Registrant’s Common Equity and Related Stockholder Matters

Owens & Minor, Inc.’s common stock trades on the New York Stock Exchange under the symbol OMI. As of February 23, 2009, there were approximately 4,200 common shareholders of record. The company believes there are an estimated additional 39,800 beneficial holders of its common stock. See “Quarterly Financial Information” under Item 15 for high and low closing sales prices of the company’s common stock.

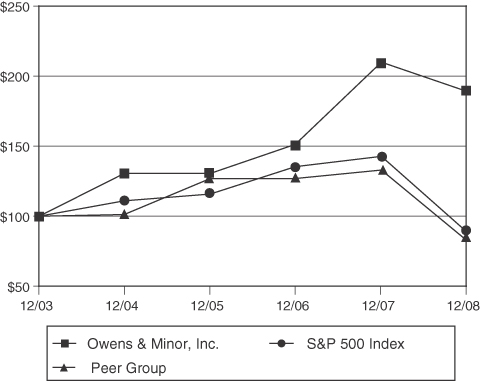

The following performance graph compares the performance of the company’s common stock to the S&P 500 Index and an Industry Peer Group (which includes the companies listed below) for the last five years.

5-Year Total Shareholder Return

This graph assumes that the value of the investment in the common stock and each index was $100 on December 31, 2003, and that all dividends were reinvested.

(Data provided by Standard & Poor’s)

| | | | | | | | | | | | | | | | | | |

| | | Base Period

12/2003 | | 12/2004 | | 12/2005 | | 12/2006 | | 12/2007 | | 12/2008 |

Owens & Minor, Inc. | | $ | 100 | | $ | 130.75 | | $ | 130.09 | | $ | 150.62 | | $ | 208.07 | | $ | 188.14 |

S&P 500 Index | | | 100 | | | 110.88 | | | 116.33 | | | 134.70 | | | 142.10 | | | 89.53 |

Peer Group | | | 100 | | | 101.17 | | | 126.85 | | | 126.69 | | | 133.16 | | | 83.86 |

The Industry Peer Group, weighted by market capitalization, consists of companies engaged in the business of healthcare product distribution. The Peer Group includes pharmaceutical distribution companies: AmerisourceBergen Corporation, Cardinal Health, Inc., and McKesson Corporation; and medical product distribution companies: Henry Schein, Inc., Patterson Companies, Inc., and PSS World Medical, Inc.

13

Item 6. Selected Consolidated Financial Data

(in thousands, except ratios and per share data)

| | | | | | | | | | | | | | | | | | | | |

| | | At or for the Year Ended December 31,(1) (2) | |

| | | 2008 | | | 2007 | | | 2006 | | | 2005 | | | 2004 | |

Summary of Operations: | | | | | | | | | | | | | | | | | | | | |

Revenue | | $ | 7,243,237 | | | $ | 6,694,596 | | | $ | 5,441,266 | | | $ | 4,763,183 | | | $ | 4,525,105 | |

Income from continuing operations | | $ | 101,257 | | | $ | 71,411 | | | $ | 53,953 | | | $ | 60,343 | | | $ | 60,500 | |

Income (loss) from discontinued operations, net of tax | | | (7,930 | ) | | | 1,299 | | | | (5,201 | ) | | | 4,077 | | | | — | |

| | | | | | | | | | | | | | | | | | | | |

Net income | | $ | 93,327 | | | $ | 72,710 | | | $ | 48,752 | | | $ | 64,420 | | | $ | 60,500 | |

| | | | | | | | | | | | | | | | | | | | |

Per Common Share: | | | | | | | | | | | | | | | | | | | | |

Income (loss) per share—basic: | | | | | | | | | | | | | | | | | | | | |

Continuing operations | | $ | 2.48 | | | $ | 1.77 | | | $ | 1.35 | | | $ | 1.53 | | | $ | 1.55 | |

Discontinued operations | | | (0.19 | ) | | | 0.04 | | | | (0.13 | ) | | | 0.10 | | | | — | |

| | | | | | | | | | | | | | | | | | | | |

Net income per share—basic | | $ | 2.29 | | | $ | 1.81 | | | $ | 1.22 | | | $ | 1.63 | | | $ | 1.55 | |

| | | | | | | | | | | | | | | | | | | | |

Income (loss) per share—diluted: | | | | | | | | | | | | | | | | | | | | |

Continuing operations | | $ | 2.44 | | | $ | 1.76 | | | $ | 1.33 | | | $ | 1.51 | | | $ | 1.53 | |

Discontinued operations | | | (0.19 | ) | | | 0.03 | | | | (0.13 | ) | | | 0.10 | | | | — | |

| | | | | | | | | | | | | | | | | | | | |

Net income per share—diluted | | $ | 2.25 | | | $ | 1.79 | | | $ | 1.20 | | | $ | 1.61 | | | $ | 1.53 | |

| | | | | | | | | | | | | | | | | | | | |

Cash dividends | | $ | 0.80 | | | $ | 0.68 | | | $ | 0.60 | | | $ | 0.52 | | | $ | 0.44 | |

Stock price at year end | | $ | 37.65 | | | $ | 42.43 | | | $ | 31.27 | | | $ | 27.53 | | | $ | 28.17 | |

Book value at year end(3) | | $ | 16.63 | | | $ | 15.03 | | | $ | 13.60 | | | $ | 12.84 | | | $ | 11.65 | |

Summary of Financial Position: | | | | | | | | | | | | | | | | | | | | |

Total assets | | $ | 1,776,190 | | | $ | 1,528,003 | | | $ | 1,697,044 | | | $ | 1,245,522 | | | $ | 1,136,428 | |

Long-term debt, excluding current portion | | $ | 359,237 | | | $ | 283,845 | | | $ | 433,133 | | | $ | 204,418 | | | $ | 207,476 | |

Shareholders’ equity(4)(5) | | $ | 689,051 | | | $ | 614,359 | | | $ | 547,454 | | | $ | 511,998 | | | $ | 460,256 | |

Selected Ratios: | | | | | | | | | | | | | | | | | | | | |

Gross margin as a percent of revenue | | | 9.90 | % | | | 9.71 | % | | | 9.90 | % | | | 10.02 | % | | | 10.24 | % |

Selling, general and administrative expense

as a percent of revenue | | | 7.20 | % | | | 7.39 | % | | | 7.64 | % | | | 7.43 | % | | | 7.54 | % |

Operating earnings as a percent of revenue | | | 2.50 | % | | | 2.10 | % | | | 2.05 | % | | | 2.33 | % | | | 2.43 | % |

Days sales outstanding(6) | | | 24.5 | | | | 23.6 | | | | 29.5 | | | | 25.5 | | | | 27.2 | |

Average annual inventory turnover(7) | | | 10.4 | | | | 9.7 | | | | 8.9 | | | | 9.8 | | | | 9.9 | |

Days payables outstanding(7) | | | 28.9 | | | | 28.6 | | | | 40.3 | | | | 33.0 | | | | 30.9 | |

Debt to equity(8) | | | 0.52 | | | | 0.46 | | | | 0.79 | | | | 0.40 | | | | 0.45 | |

(1) | In December 2008, the company committed to plans to exit its direct-to-consumer business (the “DTC business”), thereby meeting criteria for classification of the business as a discontinued operation in accordance with generally accepted accounting principles. Accordingly, the DTC business is presented as discontinued operations for all periods presented. For additional information regarding discontinued operations, see Note 4 of “Notes to Consolidated Financial Statements.” |

(2) | Certain adjustments have been made to conform to current year presentation. See Note 1 of “Notes to Consolidated Financial Statements.” |

(3) | Represents shareholders’ equity divided by year-end common shares outstanding. |

(4) | The company adopted FASB Interpretation No. 48, “Accounting for Uncertainty in Income Taxes,” on January 1, 2007. As a result, the company recognized an increase of $0.8 million to the January 1, 2007, balance of retained earnings. See Note 1 of “Notes to Consolidated Financial Statements.” |

14

(5) | On December 31, 2006, the company adopted Statement of Financial Accounting Standards No. 158, “Employers’ Accounting for Defined Benefit Pension and Other Postretirement Plans” and recognized an increase of $3.1 million as a direct adjustment to accumulated other comprehensive loss. See Note 1 of “Notes to Consolidated Financial Statements.” |

(6) | Based on revenues for the fourth quarter of the year. |

(7) | Based on cost of goods sold for the preceding 12 months. |

(8) | Represents long-term debt, less current portion, divided by shareholders’ equity. |

Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations

2008 Financial Results

Overview. In 2008, the company earned net income of $93.3 million, increased from $72.7 million in 2007, and $48.8 million in 2006. Net income per diluted share was $2.25 in 2008, as compared with $1.79 in 2007, and $1.20 in 2006. Operating earnings, which were $180.7 million in 2008, improved from $140.8 million in 2007 and $111.4 million in 2006. As a percentage of revenue, operating earnings were 2.50%, 2.10% and 2.05% in 2008, 2007 and 2006. Operating earnings in 2008 reflect the cost of integrating a portion of the acquired acute-care distribution business of The Burrows Company. Operating earnings in both 2007 and 2006 were affected by the cost of integrating the acquired acute-care distribution business of McKesson Medical-Surgical Inc. Operating earnings for 2007 and 2006 include $6.7 million and $19.3 million of service fees paid to McKesson for operational support during the transition period.

Acquisitions. The company acquired certain assets and liabilities of The Burrows Company (“Burrows”), a Chicago-based distributor of medical and surgical supplies to the acute-care market, on October 1, 2008. The purchase price, net of a $7.0 million purchase price adjustment receivable at December 31, 2008, and including transaction costs, was approximately $17.2 million in cash, plus $56.1 million of assumed debt. The acquisition included inventory valued at $58.2 million, accounts receivable of $37.5 million, and acute-care customer relationships. The acquisition was financed with borrowings under the company’s revolving credit facility. In connection with the acquisition, the company recorded $6.6 million of estimated involuntary termination and lease exit costs. The company also purchased real property associated with the Burrows business for $17.0 million in December 2008. This property was classified as held for sale at December 31, 2008.

Effective September 30, 2006, the company acquired certain assets of the acute-care medical and surgical supply distribution business of McKesson Medical-Surgical Inc. (“McKesson”), a subsidiary of McKesson Corporation. The adjusted purchase price, including transaction costs, was approximately $152.1 million. The acquisition included inventory valued at $105.4 million, acute-care customer relationships, certain fixed assets, and the assumption of facility leases. The acquisition was financed with borrowings under the company’s revolving credit facility and available cash. In connection with the acquisition, the company recorded $6.2 million of estimated involuntary termination and lease exit costs. During 2007, the company completed its allocation of the purchase price, including its determination of the fair value of acquired intangibles. As a result, intangible assets, which are comprised of customer relationships and a non-compete agreement, were reduced by $8.8 million from the amounts recorded at the date of acquisition. These adjustments resulted in an increase to recorded goodwill. At the effective date of the acquisition, McKesson and the company entered into a transition services agreement, pursuant to which McKesson provided operational support to the company during a transition period. Under this agreement, which ended in March 2007, the company paid McKesson revenue-based service fees.

Divestitures. In December 2008, the company announced its intention to exit its direct-to-consumer distribution business (the “DTC business”), dispose of certain remaining assets, and terminate substantially all of the employees of the business, and the company entered into a definitive agreement to sell certain assets of the business. Accordingly, the DTC business is presented as discontinued operations in the company’s consolidated financial statements, and all prior period information has been reclassified to be consistent with the current period presentation.

15

Results of Operations

The following table presents highlights from the company’s consolidated statements of income on a percentage of revenue basis:

| | | | | | | | | |

Year ended December 31, | | 2008 | | | 2007 | | | 2006 | |

Gross margin | | 9.90 | % | | 9.71 | % | | 9.90 | % |

Selling, general and administrative expenses | | 7.20 | | | 7.39 | | | 7.64 | |

Operating earnings | | 2.50 | | | 2.10 | | | 2.05 | |

Income from continuing operations | | 1.40 | | | 1.07 | | | 0.99 | |

Revenue. Revenue was $7.2 billion for 2008, $6.7 billion for 2007 and $5.4 billion for 2006, representing an increase of 8.2% for 2008 compared to 2007 and an increase of 23.0% for 2007 compared to 2006. Approximately 90% of the increase in revenues for 2008 compared to 2007 was due to greater sales from existing customers. Sales to net new customers, including customers acquired from Burrows, partially offset by expected decreases in revenue from the acquired McKesson business, represented approximately 10% of the increase. Approximately 60% of the increase for 2007 compared to 2006 was due to the acquired McKesson business, which contributed $1.05 billion of revenue in 2007, as compared with $281.5 million in 2006. In addition, greater sales volumes to existing healthcare provider customers accounted for an additional 25% of the increase in 2007, while the remaining 15% resulted from sales to new customers.

Gross margin.Gross margin as a percentage of revenue was 9.90% in 2008, 9.71% in 2007 and 9.90% in 2006. Gross margin dollars were $717.3 million in 2008, as compared with $650.0 million in 2007, and $538.8 million in 2006. The increase in gross margin as a percentage of revenue of 19 basis points for 2008 compared to 2007 resulted from: (i) improved gross margin from the acquired McKesson business as this business transitioned to O&M systems; (ii) additional sales of programs and services; (iii) greater supplier incentives; and (iv) greater impact of manufacturers’ price increases. These increases were partially offset by a decrease in gross margin as a percentage of revenue from the acquired Burrows business and an increase in the reserve for last-in, first-out (LIFO) inventory valuation. The decrease in gross margin as a percentage of revenue of 19 basis points from 2006 to 2007 resulted primarily from the effects of certain contract renewals with major group purchasing organizations under which the company offers more favorable pricing to customers as they purchase in greater volume, as well as increased sales to existing customers under these and other contracts. Additionally, the acquired McKesson business experienced lower gross margins as a percentage of sales until this business was transitioned to O&M systems and pricing files were brought to O&M standards.

The company values inventory for its healthcare provider distribution business under the LIFO method. Had inventory been valued under the first-in, first-out (FIFO) method, gross margin would have been higher by 0.2% of revenue in 2008, and 0.1% in 2007 and 2006.

Selling, general and administrative (SG&A) expense.SG&A expenses as a percentage of revenue were 7.20% in 2008, 7.39% in 2007, and 7.64% in 2006. SG&A expenses were $521.4 million in 2008, $494.5 million in 2007, and $415.6 million in 2006. SG&A expense dollars increased in 2008 from 2007, primarily as a result of an increase in incentive and share-based compensation expenses of $18.1 million, reflecting improved achievement against certain performance-based measures, as well as the impact of an increase in the price of the company’s common stock factored into the compensation cost of share-based awards granted in 2008. Also contributing to the increase were increases in personnel expenses of $10.1 million, distribution center occupancy expenses of $3.4 million resulting from sales growth, as well as the acquired Burrows business, and increased information technology outsourcing expenses of $3.8 million. These increases were partially offset by non-recurring costs incurred in 2007 associated with the integration of the acquired McKesson business and service fees of $6.7 million paid to McKesson for operational support during the transition period, a decrease in consulting expenses of $1.1 million, and a $3.4 million lower provision for losses on accounts and notes receivable.

16

SG&A expenses in 2007 and 2006 include $6.7 million and $19.3 million of transition service fees paid to McKesson for operational support during the transition period which ended in March 2007. The remaining decline in SG&A, as a percent of revenue, resulted from lower infrastructure costs, as the company leveraged its costs over greater revenues, partially offset by higher delivery costs and higher teammate benefit costs.

Depreciation and amortization expense. Depreciation and amortization expense increased from $20.9 million in 2007 to $22.0 million in 2008. This increase was primarily due to greater depreciation expense from warehouse equipment purchased in 2008 to accommodate increased sales volume. Depreciation and amortization expense increased from $15.5 million in 2006 to $20.9 million in 2007. This increase was driven by an increase in the amortization of intangibles of $2.1 million related to the McKesson acquisition and approximately $1.0 million of additional depreciation expense from certain information technology assets capitalized pursuant to an amended outsourcing agreement effective during the latter half of 2006. The remainder resulted from greater depreciation expense from capital additions to accommodate the acquired McKesson business.

Other operating income and expense, net. Other operating income and expense, net, was $6.8 million, $6.2 million and $3.7 million of income in 2008, 2007 and 2006, including finance charge income of $4.4 million, $4.4 million and $3.2 million.

Interest expense, net. Interest expense, net, was $16.0 million for 2008, as compared with $23.1 million in 2007 and $13.4 million in 2006. The decrease of $7.1 million from 2007 to 2008 is primarily due to lower balances outstanding under the company’s revolving credit agreement, as the company has significantly reduced borrowings under this facility during 2008. Interest expense also decreased in 2008 due to a more favorable interest rate environment. These decreases were partially offset by interest expense recognized during 2008 on the borrowings related to the Burrows acquisition and interest rate swaps hedging a portion of the company’s $200 million fixed-rate debt. These swaps were designated as a fair value hedge until Lehman Brothers Holdings Inc., guarantor of one of the swaps, declared bankruptcy in September 2008. The company determined at that date that the swaps were no longer expected to be effective in offsetting interest rate risk. The company discontinued accounting for the swaps as a fair value hedge as of that date and realized a loss of $3.1 million, representing the difference between the fair value of the swaps as of the date that hedge accounting was discontinued and the proceeds received on termination of the swaps of $3.8 million. The fair value adjustment of $6.9 million to the carrying value of the related debt is being recognized as an offset to interest expense using the interest method over the remaining life of the debt.

Of the $9.7 million increase in interest expense from 2006 to 2007, $7.3 million was due to the company’s borrowings under its revolving credit facility to finance the McKesson acquisition and its related working capital needs. The remainder of the increase was due to lower cash balances available to invest, partially offset by a decrease in interest expense due to the refinancing of long-term debt at lower rates in April 2006.

In April 2006, the company completed its offering of $200 million of 6.35% Senior Notes maturing in 2016 (Senior Notes) and retired substantially all of its $200 million of 8.5% Senior Subordinated Notes due 2011. The company expects to continue to manage its financing costs by managing working capital levels. Future financing costs will be affected primarily by changes in short-term interest rates, and funds used for working capital requirements, capital improvements and for acquisitions.

In 2008, the company’s effective interest rate was 6.2%, excluding interest expense recognized related to the interest rate swaps, on average borrowings of $215.8 million, compared to 6.8% on average borrowings of $346.3 million in 2007, and 7.2% on average borrowings of $234.4 million in 2006.

Income taxes. The provision for income taxes was $63.5 million in 2008, compared with $46.2 million in 2007, and $32.6 million in 2006. The company’s effective tax rate was 38.5% in 2008, as compared with 39.3% in 2007, and 37.7% in 2006. The lower effective tax rates for 2008 and 2006 were due to decreases in tax accruals as a result of the resolution of outstanding tax issues.

Income from continuing operations. Income from continuing operations increased to $101.3 million for 2008, from $71.4 million for 2007, and $54.0 million for 2006. The increases for 2008 compared to 2007, and

17

2007 compared to 2006, are primarily due to increases in revenues from existing customers. In addition, the company experienced revenue growth from new customers in 2007 and 2008 from its 2006 acquisition of the McKesson business and, in 2008, from its acquisition of the Burrows business in the fourth quarter.

Income (loss) from discontinued operations, net of tax. Loss from discontinued operations, net of tax, was $7.9 million in 2008, compared to income of $1.3 million in 2007 and loss of $5.2 million in 2006. The decrease of $9.2 million for 2008 compared to 2007 was primarily due to pre-tax charges associated with the exit from the DTC business, including losses recognized for abandoned software, employee severance and accrued contract termination costs totaling $7.8 million. The increase of $6.5 million for 2007 compared to 2006 is primarily due to pre-tax charges for uncollectible accounts receivable of $9.3 million recognized in 2006.

Net income. Net income was $93.3 million in 2008, compared to $72.7 million in 2007 and $48.8 million in 2006. The increase of $20.6 million for 2008 compared to 2007 is a result of an increase in revenue of $548.6 million, primarily due to increased sales to existing customers and the acquired Burrows business, which contributed to an increase of $39.9 million in operating earnings. The increase of $24.0 million for 2007 compared to 2006 is due to an increase in revenue of $1.25 billion, primarily due to an increase in sales to existing customers and the acquired McKesson business, which contributed to an increase of $29.4 million in operating earnings. Net income for 2006 included a pre-tax charge of $11.4 million related to a loss on the early retirement of debt, as the company refinanced $200 million in debt.

Financial Condition, Liquidity and Capital Resources

The following table summarizes the Company’s Consolidated Statements of Cash Flows for the years ended December 31, 2008, 2007 and 2006:

(in millions)

| | | | | | | | | | | | |

| | | 2008 | | | 2007 | | | 2006 | |

Net cash provided by (used in)—continuing operations: | | | | | | | | | | | | |

Operating activities | | $ | 62.9 | | | $ | 210.3 | | | $ | (70.9 | ) |

Investing activities | | | (123.3 | ) | | | (11.8 | ) | | | (193.8 | ) |

Financing activities | | | 65.3 | | | | (202.7 | ) | | | 216.9 | |

Liquidity. During 2008, cash and cash equivalents decreased from $10.4 million at December 31, 2007, to $7.9 million at December 31, 2008. In 2008, the company generated $62.9 million of cash from continuing operations, compared with cash from continuing operations of $210.3 million in 2007 and cash used for continuing operations of $70.9 million in 2006. Cash from continuing operations in 2008 was negatively affected by increases in accounts receivable and inventories largely as a result of the Burrows acquisition. Strong operating cash flows in 2007 were primarily driven by decreases in accounts receivable and inventory which had increased at the end of 2006 as a result of the acquisition of the McKesson business. Accounts receivable days sales outstanding (DSO) at December 31, 2008, based on three months’ sales, were 24.5 days, compared with 23.6 days at December 31, 2007, and 29.5 days at December 31, 2006. In 2006, DSO was negatively affected by the McKesson acquisition. Average annual inventory turnover was 10.4, 9.7, and 8.9 in 2008, 2007, and 2006. Average annual inventory turnover for 2008 compared to 2007, and for 2007 compared to 2006, increased as a result of growth in sales at a higher rate than the increase in average inventory for the corresponding period.

Cash used for investing activities increased to $123.3 million in 2008 from $11.8 million in 2007, which decreased from $193.8 million in 2006. Cash used for investing activities in 2008 and 2006 was largely due to acquisitions, as the company invested $96.8 million in 2008 and $170.7 million in 2006 on acquisitions of businesses, including intangible assets. The company acquired certain assets and liabilities of Burrows, in exchange for cash consideration of $17.2 million, net of a $7.0 million purchase price adjustment receivable at December 31, 2008, and including transaction costs, plus $56.1 million of assumed debt. The assumed debt was satisfied in full on the acquisition date, October 1, 2008. The company borrowed approximately $80 million under its revolving credit facility to fund this acquisition. In connection with the acquisition, the company also

18

acquired real property from Burrows in December 2008 for $17.0 million. In 2008, the company invested $27.0 million in capital expenditures, primarily for software, warehouse equipment and additional land near the corporate headquarters building. Cash provided by investing activities in 2007 includes $15.4 million related to acquisitions, which is primarily due to approximately $16.5 million received from McKesson, as the company finalized the determination of the value of inventory transferred. Investing cash flows also included $27.5 million of capital expenditures in 2007 primarily to accommodate the acquired McKesson and other new business. In 2006, $26.5 million of capital expenditures included spending on construction of the new corporate headquarters building.

The company’s financing activities provided $65.3 million in cash in 2008, used $202.7 million of cash in 2007, and provided $216.9 million of cash in 2006. In 2008, cash provided by financing activities was primarily due to net borrowings under the revolving credit facility of $73.7 million used to partially fund the Burrows acquisition, and the related payment of assumed debt, partially offset by the use of funds for the payment of dividends of $33.0 million. In 2007, the company reduced net borrowings under its revolving credit facility by $152.6 million, which partially funded the McKesson acquisition and its related working capital needs. An additional $27.6 million of cash was used to fund dividends and $34.6 million to reduce drafts payable. In 2006, cash provided by financing activities was primarily due to borrowings under the revolving credit facility of $229.1 million used to partially fund the McKesson acquisition and to fund working capital requirements during the integration of the acquired business, and an increase of $17.1 million in drafts payable. Proceeds from financing activities in 2006 were partially offset by the use of funds for the payment of dividends of $24.1 million and the refinancing of long-term debt.

In April 2006, the company issued $200 million of 6.35% Senior Notes maturing April 15, 2016. The net proceeds from the Senior Notes, together with available cash, were used to retire substantially all of the company’s $200 million of 8.5% Senior Subordinated Notes. Interest on the Senior Notes is paid semi-annually on April 15 and October 15, beginning October 15, 2006. The company has an investment grade rating of “BBB-” from Standard & Poor’s and Fitch Ratings and a rating of “Ba2” from Moody’s.

In conjunction with the Senior Notes, the company entered into interest rate swap agreements, under which the company paid counterparties variable rates based on LIBOR, and the counterparties paid the company a fixed interest rate of 6.35% on a notional amount of $100 million, effectively converting one-half of the Senior Notes to variable-rate debt. These swaps were designated as fair value hedges and were assumed to have no ineffectiveness. During 2008, the company terminated these interest rate swap agreements and received cash proceeds totaling $4.7 million, of which $3.8 million related to the fair value of the swaps is included in cash provided by financing and $0.9 million related to accrued interest is included in cash provided by operating activities.

The company has a $306 million revolving credit facility which expires on May 3, 2011. In July 2008, the credit agreement was amended to improve the company’s flexibility by changing certain restrictions and by releasing certain guarantors. The interest rate on the facility is based on, at the company’s discretion, LIBOR, the Federal Funds Rate or the Prime Rate, plus an adjustment based on the company’s leverage ratio, as defined by the credit agreement. The company is charged a commitment fee of between 0.05% and 0.15% on the unused portion of the facility, which includes a 0.05% reduction in the fee based on the company’s investment grade rating. The terms of the agreement limit the amount of indebtedness that the company may incur, require the company to maintain certain levels of net worth, leverage ratio and fixed charge coverage ratio, and restrict the ability of the company to materially alter the character of the business through consolidation, merger, or purchase or sale of assets. At December 31, 2008, the company was in compliance with these covenants. The company had total borrowing capacity under the facility of $350 million; however, on October 1, 2008, Lehman Brothers, Inc. defaulted on its commitment under the facility, thereby decreasing the company’s total borrowing capacity to $306 million. At December 31, 2008, the following financial institutions had commitments under the facility: Bank of America, N.A., Citibank N.A., SunTrust Bank, Wachovia Bank, National Association, Comerica Bank, KeyBank National Association, Union Bank of California, N.A., U.S. Bank, National Association, The Bank of New York and Fifth Third Bank. At December 31, 2008, Owens & Minor had $159.3 million outstanding under

19

the facility, including outstanding letters of credit, leaving $146.7 million available for borrowing as of December 31, 2008.

On December 22, 2008, the company entered into a definitive agreement to sell certain assets of its DTC business for $63 million in cash. The sale of these assets was completed on January 2, 2009, and the proceeds were used to reduce borrowings under the revolving credit facility.

The company believes its available financing sources will be sufficient to fund working capital needs and long-term strategic growth, although this cannot be assured, as economic conditions may impact the ability of financial institutions to meet their contractual commitments to the company or may impact O&M’s customers’ ability to meet their obligations to the company. Based on the company’s leverage ratio at December 31, 2008, the company’s interest rate under its revolving credit facility, which is subject to adjustment quarterly, will remain unchanged at LIBOR plus 62.5 basis points at the next adjustment date.

The following is a summary of the company’s significant contractual obligations as of December 31, 2008:

(in millions)

| | | | | | | | | | | | | | | |

Contractual obligations | | Total | | Less than

1 year | | 1-3 years | | 4-5 years | | After 5 years |

Long-term debt, including interest payments(1) | | $ | 448.2 | | $ | 14.6 | | $ | 178.6 | | $ | 25.4 | | $ | 229.6 |

Purchase obligations(2) | | | 193.0 | | | 39.3 | | | 68.1 | | | 66.4 | | | 19.2 |

Operating leases(2) | | | 162.4 | | | 41.3 | | | 65.7 | | | 38.9 | | | 16.5 |

Capital lease obligations(1) | | | 3.8 | | | 1.7 | | | 1.8 | | | 0.3 | | | — |

FIN 48 liability(3) | | | 21.2 | | | 0.4 | | | — | | | — | | | — |

Other long-term liabilities(4) | | | 39.2 | | | 4.9 | | | 7.4 | | | 8.5 | | | 18.4 |

| | | | | | | | | | | | | | | |

Total contractual obligations(5) | | $ | 867.8 | | $ | 102.2 | | $ | 321.6 | | $ | 139.5 | | $ | 283.7 |

| | | | | | | | | | | | | | | |

(1) | See Note 10 to the consolidated financial statements. Debt is assumed to be held to maturity with interest paid at the stated rate. |

(2) | See Note 17 to the consolidated financial statements. |

(3) | Total FIN 48 liability includes $20.8 million, for which the company cannot reasonably estimate the timing of cash settlement. |

(4) | Other long-term liabilities include obligations for retirement plans. Expected timing of payments is based on actuarial assumptions; actual timing of payments could vary significantly from amounts projected. See Note 13 to the consolidated financial statements. |

(5) | Excludes certain contingent contractual obligations that are required to be paid in the event that performance targets specified by customer contracts are not achieved. See Note 17 to the consolidated financial statements. |

Capital expenditures. Capital expenditures were $27.0 million in 2008, compared to $27.5 million in 2007 and $26.5 million in 2006. Capital expenditures in 2008, 2007 and 2006 reflect additions to equipment and software to accommodate the growth in the business. Capital expenditures in 2008 also include the purchase of land for possible future expansion of the company’s headquarters for $5.4 million.

Critical Accounting Policies

The company’s consolidated financial statements and accompanying notes have been prepared in accordance with U.S. generally accepted accounting principles. The preparation of financial statements requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities, the disclosure of contingent assets and liabilities at the date of the financial statements, and the reported amounts of revenues and expenses during the reporting periods. The company continually evaluates the accounting policies and estimates it uses to prepare its financial statements. Management’s estimates are generally based on

20

historical experience and various other assumptions that are judged to be reasonable in light of the relevant facts and circumstances. Because of the uncertainty inherent in such estimates, actual results may differ.

Critical accounting policies are defined as those policies that relate to estimates that require a company to make assumptions about matters that are highly uncertain at the time the estimate is made and could have a material impact on the company’s results due to changes in the estimate or the use of different estimates that could reasonably have been used. Management believes its critical accounting policies and estimates include its allowances for losses on accounts and notes receivable, inventory valuation, accounting for goodwill, and self-insurance liabilities.

Allowances for losses on accounts and notes receivable. The company maintains valuation allowances based upon the expected collectibility of accounts and notes receivable. The allowances include specific amounts for accounts that are likely to be uncollectible, such as customer bankruptcies and disputed amounts, allowances to contractual amounts expected to be collected from Medicare and other third-party insurers, and general allowances for accounts that may become uncollectible. These allowances are estimated based on a number of factors, including industry trends, current economic conditions, creditworthiness of customers, age of the receivables, changes in customer payment patterns, and historical experience. At December 31, 2008, the company had accounts and notes receivable of $521.3 million, net of allowances of $14.8 million. An unexpected bankruptcy or other adverse change in the financial condition of a customer could result in increases in these allowances, which could have a material effect on net income. The company actively manages its accounts receivable to minimize credit risk.