January 30, 2012

Ms. Tia L. Jenkins

Senior Assistant Chief Accountant

Securities and Exchange Commission

Washington, D.C. 20549

| RE: | Owens & Minor, Inc. |

Form 10-K for Fiscal Year Ended December 31, 2010

Filed February 25, 2011

File No. 001-09810

Dear Ms. Jenkins:

The responses of Owens & Minor, Inc. (the “company”) to your letter dated January 19, 2012, regarding the above-referenced filing of the company, are set forth below.

For convenience, the comments contained in your letter are presented beginning on page 4 of this letter, followed by the company’s response.

Exhibits Provided to Staff

Reference is made in this letter to certain supplemental materials (referred to as Exhibits 1, 2 and 3) that we are providing to the Staff under separate cover with our request for confidential treatment pursuant to the provisions of Commission Rule 83 and return of the materials upon completion of your review pursuant to Securities Exchange Act Rule 12b-4. The supplemental materials include examples of reports and internal financial information regularly reviewed and considered by our chief operating decision maker (“CODM”) to evaluate operating performance and allocate resources, including a sample report provided to our Board of Directors, as well as internal organizational information.

Background Information

The following information is presented to assist the Staff in assessing the responses presented below to the questions presented.

Our Business and Segment Reporting Under U.S. GAAP

In our response dated January 6, 2012, we indicated that the following three components of our business comprise one reporting segment:

| • | Traditional distribution of products bought and re-sold (“Core Distribution”); |

| • | Supply-chain management services (“OMSolutions”); and, |

| • | Distribution of products under the third-party logistics model (“OM HCL”). |

All three components are focused on providing supply chain and distribution services to the same pool of healthcare providers or vendors of healthcare providers.

1

Under U.S. GAAP, reportable segments are operating segments or aggregations of operating segments that meet specified criteria. Operating segments are components of an entity about which separate financial information is available that is evaluated regularly by the CODM in deciding how to allocate resources and in assessing performance. Financial information is required to be reported externally on the same basis that the company reports internally for evaluating operating segment performance and deciding how to allocate resources to operating segments. However, operating segments can be aggregated for external reporting purposes if they have similar economic characteristics.

Our conclusion that the three components of our business comprise one reporting segment is based on the following:

| • | The Core Distribution and OMSolutions components are operationally integrated and rely on shared administrative and management services as well as share a customer base. Further, while certain separate financial information is reviewed by our President and Chief Executive Officer (our CODM), it is not reviewed for the purpose of allocating resources and assessing performance, as that allocation and assessment is performed at a level of financial results that includes the performance of both components. Accordingly, Core Distribution and OMSolutions comprise one operating segment (together “Distribution”). |

| • | The Distribution and OM HCL operating segments have similar economic characteristics and are therefore aggregated into one reportable segment. |

We would also like to emphasize that Core Distribution represents 99% of our revenue and essentially all of our operating earnings as both OMSolutions and OM HCL have generated inconsequential operating losses to-date (see Exhibit 1 of the supplemental materials).

The fee-based services provided by OMSolutions and OM HCL are primarily for facilitating revenue growth and help retain or secure new distribution business. Moreover, our internal financial information for OMSolutions and OM HCL (which is set forth in Exhibit 1 of the supplemental materials) does not include a full allocation of costs for services rendered to them by Core Distribution (including Home Office costs) or the cost associated with the value or “brand” of Core Distribution used by OMSolutions and OM HCL to get new business from vendors and customers of Core Distribution. Accordingly, the internal financial information for OMSolutions and OM HCL does not represent stand-alone results and neither of these components would be viable operations on their own.

The integrated and synergistic services offering of Core Distribution and OMSolutions mean that the allocation of resources and assessment of performance must be accomplished together and not separately. Most healthcare providers want their distributor to provide not only distribution services but complementary savings opportunities via supply chain efficiencies, inventory management and overall cost management. As a result, most of our prospective customers ask about supply chain services such as OMSolutions, and many of those consider it a favorable factor for awarding integrated distribution service contracts due to the additional savings opportunities OMSolutions often provides. Accordingly, OMSolutions offerings are included in nearly all request-for-proposal (“RFP”) responses to existing or substantial new customers. The local Core Distribution and OMSolutions teammates work with teammates in the Home Office to strategize and create comprehensive RFP responses. We believe that this has had a positive influence on winning Core Distribution business at many large customers.

2

OM HCL is a late-stage start-up initiative that provides distribution opportunities for high-dollar value products that cannot economically be distributed using the buy-sell and cost-plus model currently used in the Core Distribution model. The first full year of operations for OM HCL was in 2009. In contrast to the cost-plus percentage pricing methodology used in Core Distribution, OM HCL distribution agreements are based on activity-based pricing since the cost-plus method would result in an uncompetitive distribution fee due to the high-dollar value of the products distributed by OM HCL. Accordingly, different information systems capabilities are needed under the buy-sell versus the third-party logistics models, and much of the start-up investment and losses for OM HCL shown in Exhibit 1 of the supplemental materials are related to developing systems and the related infrastructure needed for third-party logistics.

In addition, we believe that the interrelationship between our management structure, our strategic goals and our internal reporting of financial information will help to further respond to your comments.

Our Leadership Team

Our CEO is the CODM with six direct reports that have responsibilities for the activities required for providing supply chain and distribution services to healthcare providers or vendors of healthcare providers and achieving our strategic plan goals. Exhibit 2 of the supplemental materials provides information regarding our present organizational structure.

Our Strategic Plan

Our strategic plan is built around the following four goal areas:

Goal Area 1: Modernize Core Infrastructure and Customer Capacity

Goal Area 2: Enhance Strategic Sourcing and Product Management

Goal Area 3: Ensure Success of OM Healthcare Logistics

Goal Area 4: Expand into Non-Acute Markets

Goal Areas 1, 2 and 4, which are further described herein and in Exhibit A attached to this letter, are entirely related to Core Distribution. Exhibit A attached to this letter includes the chart of the four goal areas that is placed in highly visible locations throughout our Home Office and our distribution centers across the country. Consequently, our goals are very well known to our teammates.

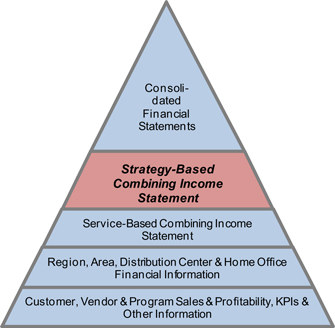

Our Financial Information Hierarchy

We have aligned our strategic plan goal areas with our internal financial reporting. The hierarchy of our financial information and metrics is based on our assessment of the relative importance of the information and is included in Exhibit B attached to this letter. We provide monthly financial information to the Board of Directors which includes the top three levels of information shown in Exhibit B, with the third level including the serviced-based combining income statements that include Core Distribution, OMSolutions, OM HCL and Home Office costs. While our consolidated financial statements are the most important measure of performance, our strategy-based combining income statement indicated in level 2 of Exhibit B is the information that top management uses to monitor and measure performance since it is aligned with our goal areas.

3

Exhibit 3 of the supplemental materials provides the format for the strategy-based combining income statement included in the monthly financial information provided to our Board of Directors. Management uses several layers of financial information for each goal area to monitor and measure performance as several sub-goals must be achieved for the overall goal to be accomplished.

Securities and Exchange Commission’s Comments

Notes to Consolidated Financial Statements, page 34

Note 1 – Summary of Significant Accounting Policies, page 34

Segment

| 1. | We note in your response to comment three of our letter dated December 8, 2011 that while separate financial information for your Core Distribution and OMSolutions components is reviewed by your CODM, it is not reviewed for the purpose of allocating resources and assessing performance, as that allocation and assessment is performed at a level of financial results that includes the performance of both components. Please explain to us in sufficient detail the purpose of the CODM’s review of the separate financial information for your Core Distribution and OMSolutions components. In this regard, the CODM identifies a function and not necessarily a person; and that function is to allocate resources to and assess the performance of the operating segments. |

Owens & Minor’s Response

As previously discussed, our CODM does receive information regarding all of our components as part of a comprehensive set of information provided to him. More importantly, the strategy-based combining income statement in Exhibit 3 of the supplemental materials is the primary report that the CODM and other top management use to measure and monitor performance. In this report OMSolutions is included in Goal Area 1 on a combined basis with other elements of Core Distribution. Moreover, Core Distribution and OMSolutions are an integrated and synergistic services offering which means that the allocation of resources and assessment of performance must be accomplished together, not separately, and this would apply to the CODM or any other senior leader in our organization or function.

OMSolutions is managed by an operating vice president that reports along with 11 other vice presidents to the Executive Vice President and Chief Operating Officer (“COO”) (see Exhibit 2 of the supplemental materials). In addition, 50% of the incentive compensation for OMSolutions teammates is tied to total company consolidated income from continuing operations, and the OMSolutions qualifier to participate in any incentive compensation is dependent on achieving a specified minimum level of total company consolidated income from continuing operations. The incentive compensation program for OM HCL currently has no link to total company results as we want our teammates involved in this start-up initiative (many of which had been part of Core Distribution) to be focused on making this venture a successful extended offering of Core Distribution.

4

| 2. | We note in your response to comment three of our letter dated December 8, 2011 that the Core Distribution and OMSolutions components sell and provide distribution and related supply chain services on an integrated basis, rely on shared administrative and management services and share a customer base. Please tell us if there is a separate manager responsible for each of these components who is directly accountable to and who maintains regular contact with the CODM to discuss operating activities, financial results, forecasts, or plans for the component. Also tell us if you present separate financial information for each component to the board of directors. |

Owens & Minor’s Response

As indicated in our response to your first comment, both our Core Distribution and OMSolutions components are managed by our COO who is directly accountable to and maintains regular contact with our CODM for all aspects of our business. Similar to the information presented to our CODM, our Board of Directors receives information in a number of formats. The focus point for our discussions with the Board of Directors is progress made against our four key strategic goals and the financial information that measures this progress (see Exhibit 3 of the supplemental materials).

| 3. | We note in your response to comment three of our letter dated December 8, 2011 that Core Distribution represents over 99% and OMSolutions and OM HCL each represent less than 0.5% of consolidated net revenues in 2010. Please also provide us with the gross margins, sales trends and absolute profit for each of these components in fiscal 2009 and 2010, and the nine months ended September 30, 2011, along with the long-term average gross margins and sales trends of each. |

Owens & Minor’s Response

Exhibit 1 of the supplemental materials provides selected internal financial information for Core Distribution, OMSolutions, OM HCL and the total company for all of 2009 and 2010 and the first nine months of 2011. For both OMSolutions and OM HCL, revenue and gross margin are the same since there are no cost of goods sold as the cost of services provided are included in selling, general and administrative (“SG&A”), depreciation and amortization (“D&A”) and other operating expenses.

As mentioned in the background information, our internal financial information for OMSolutions and OM HCL does not include a full allocation of costs for services rendered to them by Core Distribution (including Home Office costs) or the cost associated with the value or “brand” of Core Distribution used by OMSolutions and OM HCL to get new business from vendors and customers of Core Distribution. Accordingly, the internal financial information for OMSolutions and OM HCL does not represent stand-alone results and neither of these components would be viable operations on their own. The level of integration and synergy between these components is further described in the background information and our responses to your first and second comments above.

5

The internal financial information for OMSolutions essentially shows a break-even operation as it is a supporting operation for Core Distribution.

We eventually see our Distribution business and OM HCL converging into one distribution offering as OM HCL evolves from the late-stage start-up that it is today to a profitable and synergistic component. We believe break-even operating results can be achieved for OM HCL in 2012, which is reflected in our 2012 budget. We also believe that a reasonably achievable level of scale will generate variable earnings contribution in excess of the fixed costs inherent in this new business which will result in operating earnings for OM HCL that are comparable to Core Distribution at the equivalent level of throughput. While Distribution and OM HCL each qualify as separate operating segments currently (and OM HCL classified as such only because of the level of attention given to it by the CODM to make it a successful extended offering of Distribution), both are aggregated into one reporting segment as they both provide medical/surgical product distribution and supply chain services to healthcare providers and vendors of healthcare providers in a highly competitive environment that drives the potential for comparable profitability. Consequently, we believe Distribution and OM HCL, which as previously indicated, we believe will ultimately converge into one distribution offering, have similar long-term economic characteristics.

We have disclosed, and will continue to disclose, in management’s discussion and analysis in our Form 10-Q and Form 10-K filings, any significant impact of our operating components on consolidated net revenue, gross margin, selling, general and administrative, depreciation and amortization and other expenses.

We will continue to monitor our operating components as our business environment and strategies change to ensure that we are complying with segment reporting requirements under U.S. GAAP and will revise future filings if and as necessary.

Owens & Minor understands that (i) it is responsible for the adequacy and accuracy of the disclosure in its filings, (ii) staff comments or changes to disclosure in response to staff comments do not foreclose the Commission from taking any action with respect to the filings, and (iii) the company may not assert staff comments as a defense in any proceeding initiated by the Commission or any person under the federal securities laws of the United States.

Should you have any questions or require further information, please feel free to contact me at (804) 723-7566 or James L. Bierman at (804) 723-7500.

Sincerely,

/s/ D. Andrew Edwards

D. Andrew Edwards

Vice President, Controller

& Chief Accounting Officer

6

Exhibit A: Strategic Plan Goal Areas

7

Exhibit B: Hierarchy of Financial Information and Metrics

8