UNITED STATES SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 10-Q

QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF

THE SECURITIES EXCHANGE ACT OF 1934

For the Quarterly Period Ended MARCH 31, 2013

Commission File No. 000-13580

SUFFOLK BANCORP

(Exact Name of Registrant as Specified in Its Charter)

| NEW YORK | | 11-2708279 |

| (State or Other Jurisdiction of Incorporation or Organization) | | (I.R.S. Employer Identification No.) |

4 WEST SECOND STREET, RIVERHEAD, NEW YORK 11901

(Address of Principal Executive Offices) (Zip Code)

(631) 208-2400

(Registrant’s Telephone Number, Including Area Code)

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

Yes x No o

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files).

Yes x No o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

| | Large accelerated filer o | Accelerated filer x | |

| | Non-accelerated filer o | Smaller reporting company o | |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act).

Yes o No x

As of April 25, 2013, there were 11,566,347 shares of registrant’s Common Stock outstanding.

SUFFOLK BANCORP

Form 10-Q

For the Quarterly Period Ended March 31, 2013

| | | Page |

| | PART I | |

| | | |

| Item 1. | Financial Statements | |

| | | |

| | | 2 |

| | | |

| | | 3 |

| | | |

| | | 4 |

| | | |

| | | 4 |

| | | |

| | | 5 |

| | | |

| | | 6 |

| | | |

| Item 2. | | 27 |

| | | |

| Item 3. | | 38 |

| | | |

| Item 4. | | 39 |

| | | |

| | PART II | |

| | | |

| Item 1. | | 39 |

| | | |

| Item 1A. | | 40 |

| | | |

| Item 2. | | 40 |

| | | |

| Item 3. | | 40 |

| | | |

| Item 4. | | 40 |

| | | |

| Item 5. | | 40 |

| | | |

| Item 6. | | 40 |

| | | |

| | | 41 |

PART I

ITEM 1. – FINANCIAL STATEMENTS

SUFFOLK BANCORP AND SUBSIDIARIES

CONDENSED CONSOLIDATED STATEMENTS OF CONDITION (UNAUDITED) March 31, 2013 and December 31, 2012

(dollars in thousands except per share data)

| | | | | | | |

| ASSETS | | | | | | |

| Cash and cash equivalents | | | | | | |

| Cash and non-interest bearing deposits due from banks | | $ | 35,292 | | | $ | 80,436 | |

| Interest bearing deposits due from banks | | | 267,237 | | | | 304,220 | |

| Federal funds sold | | | 1,150 | | | | 1,150 | |

| Total cash and cash equivalents | | | 303,679 | | | | 385,806 | |

| Federal Reserve Bank, Federal Home Loan Bank and other stock | | | 3,043 | | | | 3,043 | |

| Investment securities: | | | | | | | | |

| Available for sale, at fair value | | | 413,277 | | | | 402,353 | |

| Held to maturity (fair value of $8,662 and $8,861, respectively) | | | 7,871 | | | | 8,035 | |

| Total investment securities | | | 421,148 | | | | 410,388 | |

| | | | | | | | | |

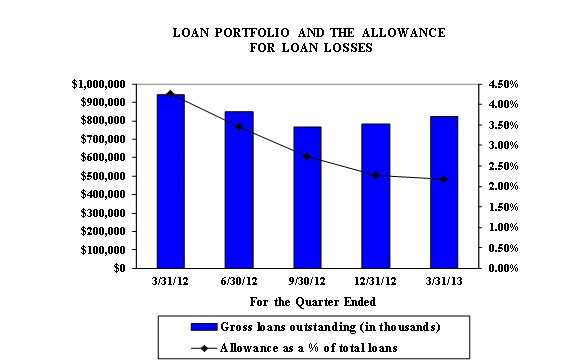

| Loans | | | 824,399 | | | | 780,780 | |

| Allowance for loan losses | | | 17,834 | | | | 17,781 | |

| Net loans | | | 806,565 | | | | 762,999 | |

| | | | | | | | | |

| Loans held-for-sale | | | 2,494 | | | | 907 | |

| Premises and equipment, net | | | 27,299 | | | | 27,656 | |

| Deferred taxes | | | 11,656 | | | | 11,385 | |

| Income tax receivable | | | 5,349 | | | | 5,406 | |

| Other real estate owned ("OREO") | | | 372 | | | | 1,572 | |

| Accrued interest and loan fees receivable | | | 5,746 | | | | 4,883 | |

| Goodwill and other intangibles | | | 2,853 | | | | 2,670 | |

| Other assets | | | 3,722 | | | | 5,749 | |

| TOTAL ASSETS | | $ | 1,593,926 | | | $ | 1,622,464 | |

| | | | | | | | | |

| LIABILITIES & STOCKHOLDERS' EQUITY | | | | | | | | |

| Demand deposits | | $ | 557,712 | | | $ | 615,120 | |

| Saving, N.O.W. & money market deposits | | | 596,230 | | | | 572,263 | |

| Time certificates of $100,000 or more | | | 173,918 | | | | 165,731 | |

| Other time deposits | | | 75,898 | | | | 78,000 | |

| Total deposits | | | 1,403,758 | | | | 1,431,114 | |

| | | | | | | | | |

| Unfunded pension liability | | | 7,765 | | | | 7,781 | |

| Capital leases | | | 4,675 | | | | 4,688 | |

| Accrued interest payable | | | 235 | | | | 237 | |

| Other liabilities | | | 11,937 | | | | 14,659 | |

| TOTAL LIABILITIES | | | 1,428,370 | | | | 1,458,479 | |

| COMMITMENTS AND CONTINGENT LIABILITIES | | | | | | | | |

| STOCKHOLDERS' EQUITY | | | | | | | | |

| Common stock (par value $2.50; 15,000,000 shares authorized;13,732,085 shares issued; 11,566,347 shares outstanding at March 31, 2013 and December 31, 2012) | | | 34,330 | | | | 34,330 | |

| Surplus | | | 42,710 | | | | 42,628 | |

| Retained earnings | | | 92,264 | | | | 89,555 | |

| Treasury stock at par (2,165,738 shares at March 31, 2013 and December 31, 2012) | | | (5,414 | ) | | | (5,414 | ) |

| Accumulated other comprehensive income net of tax | | | 1,666 | | | | 2,886 | |

| TOTAL STOCKHOLDERS' EQUITY | | | 165,556 | | | | 163,985 | |

| TOTAL LIABILITIES & STOCKHOLDERS' EQUITY | | $ | 1,593,926 | | | $ | 1,622,464 | |

See accompanying notes to unaudited condensed consolidated financial statements.

SUFFOLK BANCORP AND SUBSIDIARIES

For the Three Months Ended March 31, 2013 and 2012

(dollars in thousands except per share data)

| | | Three Months Ended | |

| | | March 31, | |

| | | 2013 | | | 2012 | |

| INTEREST INCOME | | | | | | |

| Loans and Loan Fees | | $ | 11,082 | | | $ | 12,394 | |

| U.S. Government Agency Obligations | | | 333 | | | | - | |

| Obligations of States & Political Subdivisions | | | 1,500 | | | | 1,526 | |

| Collateralized Mortgage Obligations | | | 835 | | | | 1,194 | |

| Mortgage-Backed Securities | | | 365 | | | | 7 | |

| Corporate Bonds | | | 117 | | | | - | |

| Federal Funds Sold & Interest Bearing Deposits Due from Banks | | | 173 | | | | 77 | |

| Dividends | | | 39 | | | | 46 | |

| Total Interest Income | | | 14,444 | | | | 15,244 | |

| INTEREST EXPENSE | | | | | | | | |

| Saving, N.O.W. & Money Market Deposits | | | 286 | | | | 317 | |

| Time Certificates of $100,000 or More | | | 300 | | | | 439 | |

| Other Time Deposits | | | 182 | | | | 280 | |

| Total Interest Expense | | | 768 | | | | 1,036 | |

| | | | | | | | | |

| Net Interest Income | | | 13,676 | | | | 14,208 | |

| Provision for Loan Losses | | | - | | | | - | |

| Net Interest Income After Provision for Loan Losses | | | 13,676 | | | | 14,208 | |

| NON-INTEREST INCOME | | | | | | | | |

| Service Charges on Deposit Accounts | | | 924 | | | | 950 | |

| Other Service Charges, Commissions & Fees | | | 710 | | | | 750 | |

| Fiduciary Fees | | | 273 | | | | 201 | |

| Net Gain on Sale of Securities Available for Sale | | | 359 | | | | - | |

| Net Gain on Sale of Portfolio Loans | | | 442 | | | | - | |

| Net Gain on Sale of Mortgage Loans Originated for Sale | | | 526 | | | | 197 | |

| Other Operating Income | | | 83 | | | | 157 | |

| Total Non-Interest Income | | | 3,317 | | | | 2,255 | |

| OPERATING EXPENSES | | | | | | | | |

| Employee Compensation and Benefits | | | 8,582 | | | | 8,584 | |

| Occupancy Expense | | | 1,544 | | | | 1,454 | |

| Equipment Expense | | | 572 | | | | 512 | |

| Consulting and Professional Services | | | 570 | | | | 897 | |

| FDIC Assessments | | | 517 | | | | 70 | |

| Data Processing | | | 467 | | | | 369 | |

| Accounting and Audit Fees | | | 21 | | | | 584 | |

| Other Operating Expense | | | 1,528 | | | | 2,135 | |

| Total Operating Expenses | | | 13,801 | | | | 14,605 | |

| | | | | | | | | |

| Income Before Income Tax Expense | | | 3,192 | | | | 1,858 | |

| Income Tax Expense | | | 483 | | | | 690 | |

| | | | | | | | | |

| NET INCOME | | $ | 2,709 | | | $ | 1,168 | |

| | | | | | | | | |

| EARNINGS PER COMMON SHARE - BASIC | | $ | 0.23 | | | $ | 0.12 | |

| EARNINGS PER COMMON SHARE - DILUTED | | $ | 0.23 | | | $ | 0.12 | |

| WEIGHTED AVERAGE NUMBER OF COMMON SHARES - BASIC | | | 11,566,347 | | | | 9,726,814 | |

| WEIGHTED AVERAGE NUMBER OF COMMON SHARES - DILUTED | | | 11,566,347 | | | | 9,726,814 | |

See accompanying notes to unaudited condensed consolidated financial statements.

SUFFOLK BANCORP AND SUBSIDIARIES

CONDENSED CONSOLIDATED STATEMENTS OF COMPREHENSIVE INCOME (LOSS) (UNAUDITED) For the Three Months Ended March 31, 2013 and 2012

(dollars in thousands)

| | | Three Months Ended | |

| | | March 31, | |

| | | 2013 | | | 2012 | |

| Net Income | | $ | 2,709 | | | $ | 1,168 | |

| Other Comprehensive Loss, Net of Taxes and Reclassification Adjustments: | | | | | | | | |

| Decrease in Unrealized Gain on Securities Available for Sale Arising During the Period | | | (1,220 | ) | | | (1,573 | ) |

| Pension and Post-Retirement Plan Benefit Obligation | | | - | | | | (255 | ) |

| Total Other Comprehensive Loss, Net of Taxes | | | (1,220 | ) | | | (1,828 | ) |

| Total Comprehensive Income (Loss) | | $ | 1,489 | | | $ | (660 | ) |

See accompanying notes to unaudited condensed consolidated financial statements.

SUFFOLK BANCORP AND SUBSIDIARIES

CONDENSED CONSOLIDATED STATEMENTS OF STOCKHOLDERS' EQUITY (UNAUDITED) For the Three Months Ended March 31, 2013 and 2012

(in thousands except for share data)

| | | Three Months Ended | |

| | | March 31, | |

| | | 2013 | | | 2012 | |

| Common Stock | | | | | | |

| Balance, January 1 | | $ | 34,330 | | | $ | 34,330 | |

| Ending Balance | | | 34,330 | | | | 34,330 | |

| Surplus | | | | | | | | |

| Balance, January 1 | | | 42,628 | | | | 24,010 | |

| Stock-based compensation | | | 82 | | | | 27 | |

| Ending Balance | | | 42,710 | | | | 24,037 | |

| Retained Earnings | | | | | | | | |

| Balance, January 1 | | | 89,555 | | | | 91,303 | |

| Net income | | | 2,709 | | | | 1,168 | |

| Ending Balance | | | 92,264 | | | | 92,471 | |

| Treasury Stock | | | | | | | | |

| Balance, January 1 | | | (5,414 | ) | | | (10,013 | ) |

| Ending Balance | | | (5,414 | ) | | | (10,013 | ) |

| Accumulated Other Comprehensive Income (Loss), Net of Tax | | | | | | | | |

| Balance, January 1 | | | 2,886 | | | | (3,070 | ) |

| Other comprehensive loss | | | (1,220 | ) | | | (1,828 | ) |

| Ending Balance | | | 1,666 | | | | (4,898 | ) |

| Total Stockholders' Equity | | $ | 165,556 | | | $ | 135,927 | |

See accompanying notes to unaudited condensed consolidated financial statements.

SUFFOLK BANCORP AND SUBSIDIARIES

For the Three Months Ended March 31, 2013 and 2012

(in thousands)

| | | Three Months Ended | |

| | | March 31, | |

| | | 2013 | | | 2012 | |

| | | | | | | |

| NET INCOME | | $ | 2,709 | | | $ | 1,168 | |

| ADJUSTMENTS TO RECONCILE NET INCOME TO NET CASH PROVIDED BY OPERATING ACTIVITIES | | | | | | | | |

| Depreciation and Amortization | | | 684 | | | | 648 | |

| Stock-Based Compensation | | | 82 | | | | 27 | |

| Net Amortization of Premiums | | | 317 | | | | 504 | |

| Originations of Mortgage Loans for Sale | | | (20,461 | ) | | | (8,195 | ) |

| Proceeds from Sale of Mortgage Loans Originated for Sale | | | 23,073 | | | | 8,392 | |

| Gain on Sale of Mortgage Loans Originated for Sale | | | (526 | ) | | | (197 | ) |

| Gain on Sale of Portfolio Loans | | | (442 | ) | | | - | |

| (Increase) Decrease in Other Intangibles | | | (183 | ) | | | 23 | |

| Deferred Tax Expense (Benefit) | | | 425 | | | | (11 | ) |

| Decrease in Income Tax Receivable | | | 57 | | | | 700 | |

| (Increase) Decrease in Accrued Interest and Loan Fees Receivable | | | (863 | ) | | | 752 | |

| Decrease in Other Assets | | | 2,028 | | | | 206 | |

| Adjustment to Unfunded Pension Liability | | | (16 | ) | | | 791 | |

| Decrease in Accrued Interest Payable | | | (2 | ) | | | - | |

| Decrease in Other Liabilities | | | (2,722 | ) | | | (1,373 | ) |

| Gain on Sale of Securities Available for Sale - Net | | | (359 | ) | | | - | |

| Net Cash Provided by Operating Activities | | | 3,801 | | | | 3,435 | |

| | | | | | | | | |

| CASH FLOWS FROM INVESTING ACTIVITIES | | | | | | | | |

| Principal Payments on Investment Securities | | | 19,831 | | | | 8,100 | |

| Proceeds from Sale of Investment Securities - Available for Sale | | | 10,475 | | | | - | |

| Maturities of Investment Securities - Available for Sale | | | 6,025 | | | | 30,406 | |

| Purchases of Investment Securities - Available for Sale | | | (49,129 | ) | | | (30,000 | ) |

| Maturities of Investment Securities - Held to Maturity | | | 163 | | | | 143 | |

| Purchases of Investment Securities - Held to Maturity | | | - | | | | (25 | ) |

| Proceeds from Sale of Portfolio Loans | | | 1,349 | | | | - | |

| Loan (Originations) Repayments - Net | | | (48,146 | ) | | | 29,968 | |

| Proceeds from Sale of OREO | | | 1,200 | | | | - | |

| Purchases of Premises and Equipment - Net | | | (327 | ) | | | (518 | ) |

| Net Cash (Used in) Provided by Investing Activities | | | (58,559 | ) | | | 38,074 | |

| | | | | | | | | |

| CASH FLOWS FROM FINANCING ACTIVITIES | | | | | | | | |

| Net Decrease in Deposit Accounts | | | (27,356 | ) | | | (596 | ) |

| Decrease in Capital Lease Payable | | | (13 | ) | | | (18 | ) |

| Net Cash Used in Financing Activities | | | (27,369 | ) | | | (614 | ) |

| | | | | | | | | |

| Net (Decrease) Increase in Cash and Cash Equivalents | | | (82,127 | ) | | | 40,895 | |

| Cash and Cash Equivalents Beginning of Period | | | 385,806 | | | | 172,559 | |

| | | | | | | | | |

| Cash and Cash Equivalents End of Period | | $ | 303,679 | | | $ | 213,454 | |

| Supplemental Disclosure: | | | | | | | | |

| Cash Paid During the Period for: | | | | | | | | |

| Interest | | $ | 770 | | | $ | 1,249 | |

See accompanying notes to unaudited condensed consolidated financial statements.

NOTES TO UNAUDITED CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

1. FINANCIAL STATEMENT PRESENTATION AND SIGNIFICANT ACCOUNTING POLICIES

The unaudited interim condensed consolidated financial statements include the accounts of Suffolk Bancorp (the “Company”) and its wholly owned subsidiary, the Suffolk County National Bank of Riverhead and its subsidiaries (the “Bank”). The Bank formed Suffolk Greenway, Inc., a real estate investment trust, and owns 100% of an insurance agency and two corporations used to acquire foreclosed real estate. The insurance agency and the two corporations used to acquire foreclosed real estate are immaterial to the Company’s operations. Suffolk Bancorp and subsidiaries are collectively referred to hereafter as the “Company.” All material intercompany accounts and transactions have been eliminated in consolidation.

In the opinion of the Company’s management, the preceding unaudited interim condensed consolidated financial statements contain all adjustments, consisting of normal accruals, necessary for a fair presentation of its condensed consolidated statements of condition as of March 31, 2013 and December 31, 2012, its condensed consolidated statements of operations for the three months ended March 31, 2013 and 2012, its condensed consolidated statements of comprehensive income (loss) for the three months ended March 31, 2013 and 2012, its condensed consolidated statements of stockholders’ equity for the three months ended March 31, 2013 and 2012 and its condensed consolidated statements of cash flows for the three months ended March 31, 2013 and 2012. The preceding unaudited interim condensed consolidated financial statements have been prepared in accordance with accounting principles generally accepted in the United States of America (“U.S. GAAP”) for interim financial information and with the instructions to Form 10-Q and Article 10 of Regulation S-X, as well as in accordance with predominant practices within the banking industry. They do not include all of the information and footnotes required by U.S. GAAP for complete financial statements. The results of operations for the three months ended March 31, 2013 are not necessarily indicative of the results of operations to be expected for the remainder of the year. For further information, please refer to the audited consolidated financial statements and footnotes thereto included in the Company’s 2012 Annual Report on Form 10-K.

Loans and Loan Interest Income Recognition - Loans that management has the intent and ability to hold for the foreseeable future or until maturity or payoff are reported at the principal balance outstanding, net of unearned discounts, deferred loan fees and costs. Unearned discounts on installment loans are credited to income using methods that result in a level yield. Loan origination fees, net of certain direct origination costs, are deferred and recognized in interest income over the respective term of the loan without anticipating prepayments.

Interest income is accrued on the unpaid loan principal balance. Recognition of interest income is discontinued when reasonable doubt exists as to whether principal or interest due can be collected. For all classes of loans, loans generally no longer accrue interest when over 90 days past due unless the loan is well-secured and in process of collection. When a loan is placed on non-accrual status, all interest previously accrued, but not collected, is reversed against current-year interest income. Interest received on such loans is applied against principal or interest, according to management’s judgment as to the collectability of the principal, until qualifying for return to accrual status. Loans start accruing interest again when they become current as to principal and interest for at least six months, and when, in the opinion of management, the loans can be collected in full. For all classes of loans, an impaired loan is defined as a loan for which it is probable that the lender will not collect all amounts due under the contractual terms of the loan agreement. Loans for which the terms have been modified resulting in a concession, and for which the borrower is experiencing financial difficulties are considered troubled debt restructurings (“TDRs”) and are classified as impaired. Generally, TDRs are initially classified as non-accrual until sufficient time has passed to assess whether the restructured loan will continue to perform. For impaired, accruing loans, interest income is recognized on an accrual basis with cash offsetting the recorded accruals upon receipt. Interest received on non-accrual, impaired loans is applied against principal or interest according to management’s judgment as to the collectibility of the principal.

Allowance for Loan Losses - The allowance for loan losses is a valuation allowance for probable incurred losses, increased by the provision for loan losses and recoveries, and decreased by loan charge-offs. For all classes of loans, when a loan, in full or in part, is deemed uncollectible, it is charged against the allowance for loan losses. This happens when the loan is past due and the borrower has not shown the ability or intent to make the loan current, or the borrower does not have sufficient assets to pay the debt, or the value of the collateral is less than the balance of the loan and is not considered likely to improve soon. The allowance for loan losses is determined by a continuous analysis of the loan portfolio. Such analysis includes changes in the size and composition of the portfolio, the Company’s own historical loan losses, industry-wide losses, current and anticipated economic trends, and details about individual loans. It also includes estimates of the actual value of collateral, other possible sources of repayment and estimates that are susceptible to significant changes due to changes in appraisal values of collateral, national and regional economic conditions and other relevant factors. All non-accrual loans over $250 thousand in the commercial and industrial, commercial real estate and real estate construction loan classes and all TDRs are evaluated individually for impairment. Management will use judgment to determine if there are other loans outside of these two categories that fit the definition of impaired. All other loans are generally evaluated as homogeneous pools with similar risk characteristics. In assessing the adequacy of the allowance for loan losses, management reviews the loan portfolio by separate classes that have similar risk and collateral characteristics; e.g., commercial and industrial, commercial real estate, real estate construction, residential mortgages (1st and 2nd liens), home equity and consumer loans.

The allowance for loan losses consists of specific and general components. The specific component relates to loans that are individually classified as impaired. Specific reserves are established based on an analysis of the most probable sources of repayment and liquidation of collateral. Impaired loans that are collateral dependent are reviewed based on their collateral and the estimated time required to recover the Company’s investment in the loans, as well as the cost of doing so, and the estimate of the recovery. Non-collateral dependent impaired loans are reviewed based on the present value of estimated future cash flows, including balloon payments, if any, using the loan’s effective interest rate. While every non-performing loan is evaluated individually, not every loan requires a specific reserve. Specific reserves fluctuate based on changes in the underlying loans, anticipated sources of repayment, and charge-offs. The general component covers non-impaired loans and is based on historical loss experience for each loan class from a rolling twelve quarter period and modifying those percentages, if necessary, after adjusting for current qualitative and environmental factors that reflect changes in the collectability of the loan class not captured by historical loss data. These factors augment actual loss experience and help estimate the probability of loss within the loan portfolio based on emerging or inherent risk trends. These qualitative factors are applied as an adjustment to historical loss rates and require judgments that cannot be subjected to exact mathematical calculation. There are no formulas for translating them into a specific basis point adjustment of the Company’s historical loss rate for a pool of loans having similar risk characteristics. These adjustments reflect management’s overall estimate of the extent to which current losses on a pool of loans will differ from historical loss experience. These adjustments are subjective estimates and management reviews them on a quarterly basis. TDRs are also considered impaired with impairment generally measured at the present value of estimated future cash flows using the loan’s effective interest rate at inception or using the fair value of collateral, less estimated costs to sell, if repayment is expected solely from the collateral.

Loans Held-For-Sale – Loans held-for-sale are carried at the lower of aggregate cost or fair value, as determined by outstanding commitments from investors. Changes in fair value of loans held-for-sale are recognized in earnings.

Dividend Restriction - Banking regulations and the Bank's formal agreement (the “Agreement”) with the Office of the Comptroller of the Currency (“OCC”) require maintaining certain capital levels and impose limitations on dividends paid by the Bank to the Company and by the Company to stockholders. (See also Regulatory Matters footnote contained herein.)

Recent Accounting Guidance - In February 2013, the Financial Accounting Standards Board (“FASB”) issued Accounting Standards Update (“ASU”) 2013-02, Comprehensive Income (Topic 220), “Reporting of Amounts Reclassified Out of Accumulated Other Comprehensive Income.” ASU 2013-02 does not change the current requirements for reporting net income or other comprehensive income in financial statements. However, the amendments require an entity to provide information about the amounts reclassified out of accumulated other comprehensive income by component. In addition, an entity is required to present, either on the face of the statement where net income is presented or in the notes, significant amounts reclassified out of accumulated other comprehensive income by the respective line items of net income but only if the amount reclassified is required under U.S. GAAP to be reclassified to net income in its entirety in the same reporting period. For other amounts that are not required under U.S. GAAP to be reclassified in their entirety to net income, an entity is required to cross-reference to other disclosures required under U.S. GAAP that provide additional detail about those amounts. This standard is effective prospectively for public entities for annual and interim reporting periods beginning after December 15, 2012. Being disclosure-related only, the Company’s adoption of ASU 2013-02 on January 1, 2013 did not have a material effect on the Company’s results of operations or financial condition.

Reclassifications — Certain reclassifications have been made to prior period information in order to conform to the current period’s presentation. Such reclassifications had no impact on the Company’s results of operations or financial condition.

2. ACCUMULATED OTHER COMPREHENSIVE INCOME (“AOCI”)

The changes in the Company’s AOCI by component, net of tax, for the three months ended March 31, 2013 and 2012 follow (in thousands).

| | | Three Months Ended March 31, 2013 | | | Three Months Ended March 31, 2012 | |

| | | Unrealized Gains and Losses on Available-for-Sale Securities | | | Pension and Post- Retirement Plan Items | | | Total | | | Unrealized Gains and Losses on Available-for-Sale Securities | | | Pension and Post- Retirement Plan Items | | | Total | |

| Beginning balance | | $ | 10,553 | | | $ | (7,667 | ) | | $ | 2,886 | | | $ | 11,873 | | | $ | (14,943 | ) | | $ | (3,070 | ) |

| Other comprehensive loss before reclassifications | | | (991 | ) | | | - | | | | (991 | ) | | | (1,573 | ) | | | (255 | ) | | | (1,828 | ) |

| Amounts reclassified from AOCI | | | (229 | ) | | | - | | | | (229 | ) | | | - | | | | - | | | | - | |

| Net current-period other comprehensive loss | | | (1,220 | ) | | | - | | | | (1,220 | ) | | | (1.573 | ) | | | (255 | ) | | | (1,828 | ) |

| Ending balance | | $ | 9,333 | | | $ | (7,667 | ) | | $ | 1,666 | | | $ | 10,300 | | | $ | (15,198 | ) | | $ | (4,898 | ) |

The table below presents reclassifications out of AOCI for the three months ended March 31, 2013 (in thousands).

Three Months Ended March 31, 2013 Details about AOCI Components | | Amount Reclassified from AOCI | | Affected Line Item in the Statement Where Net Income is Presented |

| Unrealized Gains and Losses on Available-for-Sale Securities | | $ | 359 | | Net Gain on Sale of Securities Available for Sale |

| | | | | | |

| | | | (130 | ) | Income Tax Expense |

| | | | | | |

| Total reclassifications, net of tax | | $ | 229 | | |

3. INVESTMENT SECURITIES

At the time of purchase of a security, the Company designates the security as either available for sale or held to maturity, depending upon investment objectives, liquidity needs and intent. Securities held to maturity are stated at cost, adjusted for premium amortized or discount accreted, if any. The Company has the positive intent and ability to hold such securities to maturity. Securities available for sale are stated at estimated fair value. Unrealized gains and losses are excluded from income and reported net of tax as accumulated other comprehensive income (loss) as a separate component of stockholders’ equity until realized. Interest earned on securities is included in interest income. Realized gains and losses on the sale of securities are reported in the consolidated statements of operations and determined using the adjusted cost of the specific security sold.

The amortized cost, estimated fair value and gross unrealized gains and losses of the Company’s investment securities available for sale and held to maturity at March 31, 2013 and December 31, 2012 follow (in thousands).

| | | March 31, 2013 | | | December 31, 2012 | |

| | | | | | Gross | | | Gross | | | Estimated | | | | | | Gross | | | Gross | | | Estimated | |

| | | Amortized | | | Unrealized | | | Unrealized | | | Fair | | | Amortized | | | Unrealized | | | Unrealized | | | Fair | |

| | | Cost | | | Gains | | | Losses | | | Value | | | Cost | | | Gains | | | Losses | | | Value | |

| Available for sale: | | | | | | | | | | | | | | | | | | | | | | | | |

| U.S. Treasury securities | | $ | - | | | $ | - | | | $ | - | | | $ | - | | | $ | 500 | | | $ | - | | | $ | - | | | $ | 500 | |

| U.S. government agency securities | | | 75,533 | | | | 59 | | | | (204 | ) | | | 75,388 | | | | 65,085 | | | | 70 | | | | (77 | ) | | | 65,078 | |

| Obligations of states and political subdivisions | | | 153,701 | | | | 12,851 | | | | - | | | | 166,552 | | | | 155,121 | | | | 13,314 | | | | - | | | | 168,435 | |

| Collateralized mortgage obligations | | | 64,724 | | | | 1,449 | | | | (69 | ) | | | 66,104 | | | | 87,624 | | | | 2,148 | | | | (80 | ) | | | 89,692 | |

| Mortgage-backed securities | | | 86,156 | | | | 500 | | | | (277 | ) | | | 86,379 | | | | 61,750 | | | | 766 | | | | (66 | ) | | | 62,450 | |

| Corporate bonds | | | 18,507 | | | | 362 | | | | (15 | ) | | | 18,854 | | | | 15,701 | | | | 497 | | | | - | | | | 16,198 | |

| Total available for sale securities | | | 398,621 | | | | 15,221 | | | | (565 | ) | | | 413,277 | | | | 385,781 | | | | 16,795 | | | | (223 | ) | | | 402,353 | |

| Held to maturity: | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Obligations of states and political subdivisions | | | 7,871 | | | | 791 | | | | - | | | | 8,662 | | | | 8,035 | | | | 826 | | | | - | | | | 8,861 | |

| Total investment securities | | $ | 406,492 | | | $ | 16,012 | | | $ | (565 | ) | | $ | 421,939 | | | $ | 393,816 | | | $ | 17,621 | | | $ | (223 | ) | | $ | 411,214 | |

At March 31, 2013 and December 31, 2012, investment securities carried at $278 million and $286 million, respectively, were pledged to secure trust deposits and public funds on deposit.

The amortized cost, contractual maturities and estimated fair value of the Company’s investment securities at March 31, 2013 (in thousands) are presented in the table below. Collateralized mortgage obligations (“CMOs”) and mortgage-backed securities (“MBS”) assume maturity dates pursuant to average lives.

| | | March 31, 2013 | |

| | | Amortized | | | Estimated | |

| | | Cost | | | Fair Value | |

| Securities available for sale: | | | | | | |

| Due in one year or less | | $ | 42,434 | | | $ | 43,232 | |

| Due from one to five years | | | 116,217 | | | | 123,531 | |

| Due from five to ten years | | | 209,792 | | | | 216,357 | |

| Due after ten years | | | 30,178 | | | | 30,157 | |

| Total securities available for sale | | | 398,621 | | | | 413,277 | |

| Securities held to maturity: | | | | | | | | |

| Due in one year or less | | | 1,535 | | | | 1,545 | |

| Due from one to five years | | | 5,938 | | | | 6,672 | |

| Due from five to ten years | | | 398 | | | | 445 | |

| Total securities held to maturity | | | 7,871 | | | | 8,662 | |

| Total investment securities | | $ | 406,492 | | | $ | 421,939 | |

The proceeds from sales of securities available for sale and the associated net realized gains follow (in thousands):

| | | Three Months Ended | |

| | | March 31, | |

| | | 2013 | | | 2012 | |

| Proceeds | | $ | 10,475 | | | $ | - | |

| | | | | | | | | |

| Gross realized gains | | | 359 | | | | - | |

| Gross realized losses | | | - | | | | - | |

| Net realized gains | | $ | 359 | | | $ | - | |

The table below indicates the length of time individual securities, both held to maturity and available for sale, have been held in a continuous unrealized loss position at the date indicated (in thousands).

| | | | | | Less than 12 months | | | 12 months or longer | | | Total | |

| As of March 31, 2013 | | Number of | | | Estimated | | | Unrealized | | | Estimated | | | Unrealized | | | Estimated | | | Unrealized | |

| Type of securities | | Securities | | | Fair value | | | Losses | | | Fair value | | | Losses | | | Fair value | | | Losses | |

| U.S. government agency securities | | | 8 | | | $ | 38,820 | | | $ | 204 | | | $ | - | | | $ | - | | | $ | 38,820 | | | $ | 204 | |

| Collateralized mortgage obligations | | | 3 | | | | 10,177 | | | | 69 | | | | - | | | | - | | | | 10,177 | | | | 69 | |

| Mortgage-backed securities | | | 9 | | | | 30,696 | | | | 277 | | | | - | | | | - | | | | 30,696 | | | | 277 | |

| Corporate bonds | | | 2 | | | | 5,520 | | | | 15 | | | | - | | | | - | | | | 5,520 | | | | 15 | |

| Total | | | 22 | | | $ | 85,213 | | | $ | 565 | | | $ | - | | | $ | - | | | $ | 85,213 | | | $ | 565 | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | Less than 12 months | | | 12 months or longer | | | Total | |

| As of December 31, 2012 | | Number of | | | Estimated | | | Unrealized | | | Estimated | | | Unrealized | | | Estimated | | | Unrealized | |

| Type of securities | | Securities | | | Fair value | | | Losses | | | Fair value | | | Losses | | | Fair value | | | Losses | |

| U.S. government agency securities | | | 6 | | | $ | 28,958 | | | $ | 77 | | | $ | - | | | $ | - | | | $ | 28,958 | | | $ | 77 | |

| Collateralized mortgage obligations | | | 2 | | | | 7,878 | | | | 80 | | | | - | | | | - | | | | 7,878 | | | | 80 | |

| Mortgage-backed securities | | | 4 | | | | 14,098 | | | | 66 | | | | - | | | | - | | | | 14,098 | | | | 66 | |

| Total | | | 12 | | | $ | 50,934 | | | $ | 223 | | | $ | - | | | $ | - | | | $ | 50,934 | | | $ | 223 | |

The Company’s management evaluates securities for other-than-temporary impairment (“OTTI”) at least on a quarterly basis, and more frequently when economic or market conditions warrant such an evaluation. All of the Company’s investment securities classified as available-for-sale or held-to-maturity are evaluated for OTTI under ASC 320, “Accounting for Certain Investments in Debt and Equity Securities.” In determining OTTI under ASC 320, management considers many factors, including: (1) the length of time and the extent to which the fair value has been less than amortized cost, (2) the financial condition and near-term prospects of the issuer, (3) whether the market decline was affected by macroeconomic conditions, and (4) whether the Company has the intent to sell the debt security or more likely than not will be required to sell the debt security before its anticipated recovery. The assessment of whether an OTTI decline exists involves a high degree of subjectivity and judgment and is based on information available to management at a point in time. An OTTI is deemed to have occurred if there has been an adverse change in the remaining expected future cash flows.

When an OTTI occurs, the amount of the OTTI recognized in earnings depends on whether an entity intends to sell the security or more likely than not will be required to sell the security before recovery of its amortized cost basis less any current-period credit loss. If an entity intends to sell or more likely than not will be required to sell the security before recovery of its amortized cost basis less any current-period credit loss, the OTTI is recognized in earnings equal to the entire difference between the investment’s amortized cost and its estimated fair value at the balance sheet date. If an entity does not intend to sell the security and it is not more likely than not that the entity will be required to sell the security before recovery of its amortized cost less any current-period loss, the OTTI is separated into the amount representing the credit loss and the amount related to all other factors. The amount of the total OTTI related to the credit loss is determined based on the present value of cash flows expected to be collected and is recognized in earnings. The amount of the total OTTI related to other factors is recognized in other comprehensive income, net of applicable tax benefit. The previous amortized cost basis less the OTTI recognized in earnings becomes the new amortized cost basis of the investment.

Upon review of the considerations mentioned here, no OTTI was deemed to be warranted at March 31, 2013.

4. LOANS

At March 31, 2013 and December 31, 2012, net loans disaggregated by class consisted of the following (in thousands):

| | | March 31, | | | December 31, | |

| | | 2013 | | | 2012 | |

| Commercial and industrial | | $ | 187,775 | | | $ | 168,709 | |

| Commercial real estate | | | 399,270 | | | | 369,271 | |

| Real estate construction | | | 14,075 | | | | 15,469 | |

| Residential mortgages (1st and 2nd liens) | | | 146,967 | | | | 146,575 | |

| Home equity | | | 63,463 | | | | 66,468 | |

| Consumer | | | 12,849 | | | | 14,288 | |

| Gross loans | | | 824,399 | | | | 780,780 | |

| Allowance for loan losses | | | (17,834 | ) | | | (17,781 | ) |

| Net loans at end of period | | $ | 806,565 | | | $ | 762,999 | |

For the three months ended March 31, 2013 and 2012, the activity in the allowance for loan losses disaggregated by class is shown below (in thousands).

| | | Commercial and industrial | | | Commercial real estate | | | Real estate construction | | | Residential mortgages (1st and 2nd liens) | | | Home equity | | | Consumer | | | Unallocated | | | Total | |

| | | | | | | | | | | | | | | | | | | | | | | | | |

| Three months ended March 31, 2013 | | | | | | | | | | | | | | | | | | | | | | | | |

| Balance at beginning of period | | $ | 6,181 | | | $ | 6,149 | | | $ | 141 | | | $ | 1,576 | �� | | $ | 907 | | | $ | 189 | | | $ | 2,638 | | | $ | 17,781 | |

| Charge-offs | | | (348 | ) | | | - | | | | - | | | | - | | | | - | | | | (11 | ) | | | - | | | | (359 | ) |

| Recoveries | | | 299 | | | | 72 | | | | - | | | | 1 | | | | 1 | | | | 39 | | | | - | | | | 412 | |

| Provision for loan losses | | | (787 | ) | | | 349 | | | | 704 | | | | 864 | | | | 16 | | | | 28 | | | | (1,174 | ) | | | - | |

| Balance at end of period | | $ | 5,345 | | | $ | 6,570 | | | $ | 845 | | | $ | 2,441 | | | $ | 924 | | | $ | 245 | | | $ | 1,464 | | | $ | 17,834 | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | Commercial and industrial | | | Commercial real estate | | | Real estate construction | | | Residential mortgages (1st and 2nd liens) | | | Home equity | | | Consumer | | | Unallocated | | | Total | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Three months ended March 31, 2012 | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Balance at beginning of period | | $ | 25,047 | | | $ | 11,029 | | | $ | 623 | | | $ | 2,401 | | | $ | 512 | | | $ | 313 | | | $ | 33 | | | $ | 39,958 | |

| Charge-offs | | | (337 | ) | | | - | | | | - | | | | (395 | ) | | | (61 | ) | | | (32 | ) | | | - | | | | (825 | ) |

| Recoveries | | | 855 | | | | - | | | | - | | | | 1 | | | | - | | | | 19 | | | | - | | | | 875 | |

| Provision for loan losses | | | (1,772 | ) | | | (2,150 | ) | | | (44 | ) | | | 28 | | | | 804 | | | | 54 | | | | 3,080 | | | | - | |

| Balance at end of period | | $ | 23,793 | | | $ | 8,879 | | | $ | 579 | | | $ | 2,035 | | | $ | 1,255 | | | $ | 354 | | | $ | 3,113 | | | $ | 40,008 | |

The allowance for loan losses is a valuation allowance for probable incurred credit losses. Loan losses are charged against the allowance when management believes the uncollectibility of a loan balance is confirmed. Subsequent recoveries, if any, are credited to the allowance. Management estimates the allowance balance required using past loan loss experience, the nature and volume of the portfolio, information about specific borrower situations and estimated collateral values, economic conditions, and other factors. Allocations of the allowance may be made for specific loans, but the entire allowance is available for any loan that, in management’s judgment, should be charged off. The allowance consists of specific and general components. The specific component relates to loans that are individually classified as impaired.

A loan is impaired when, based on current information and events, it is probable that the Company will be unable to collect all amounts due according to the contractual terms of the loan agreement. Loans for which the terms have been modified resulting in a concession, and for which the borrower is experiencing financial difficulties, are considered TDRs and classified as impaired. Generally, TDRs are initially classified as non-accrual until sufficient time has passed to assess whether the restructured loan will continue to perform. Generally, the Company returns a TDR to accrual status upon six months of performance under the new terms.

Factors considered by management in determining impairment include payment status, collateral value, and the probability of collecting scheduled principal and interest payments when due. Loans that experience insignificant payment delays and payment shortfalls generally are not classified as impaired. Management determines the significance of payment delays and payment shortfalls on a case-by-case basis, taking into consideration all of the circumstances surrounding the loan and the borrower, including the length of the delay, the reasons for the delay, the borrower’s prior payment record, and the amount of the shortfall in relation to the principal and interest owed.

Management has determined that all TDRs and all non-accrual loans are impaired; however, non-accrual loans with an impaired balance of $250 thousand or less will be evaluated under ASC 450 with other groups of smaller or homogeneous loans with similar risk characteristics. Management will use judgment to determine if there are other loans outside of these two categories that fit the definition of impaired. If a loan is impaired, a specific reserve is recorded so that the loan is reported, net, at the present value of estimated future cash flows including balloon payments, if any, using the loan’s existing rate or at the fair value of collateral if repayment is expected solely from the collateral. Large groups of homogeneous loans with smaller individual balances, such as consumer and residential real estate loans, are generally evaluated collectively for impairment, and accordingly, are not separately identified for impairment disclosures. TDRs are separately identified for impairment disclosures and are measured at the present value of estimated future cash flows using the loan’s effective rate at inception. If a TDR is considered to be “collateral-dependent,” the loan is reported at the fair value of the collateral net of estimated costs to sell. For TDRs that subsequently default, the Company determines the allowance amount in accordance with its accounting policy for the allowance for loan losses.

The general component of the allowance covers non-impaired loans and is based on historical loss experience, adjusted for qualitative factors. The historical loss experience is determined by loan class, and is based on the actual loss history experienced by the Company over a rolling twelve quarter period. This actual loss experience is supplemented with other qualitative factors based on the risks present for each loan class. These qualitative factors include consideration of the following: levels of and trends in delinquencies and impaired loans; levels of and trends in charge-offs and recoveries; trends in volume and terms of loans; effects of any changes in risk selection and underwriting standards; other changes in lending policies, procedures and practices; experience, ability, and depth of lending management and other relevant staff; local, regional and national economic trends and conditions; industry conditions; and effects of changes in credit concentrations. The following loan classes have been identified: commercial and industrial, commercial real estate, real estate construction, residential mortgages (1st and 2nd liens), home equity and consumer. For performing loans, an estimate of adequacy is made by applying qualitative factors specific to the portfolio to the period-end balances. Consideration is also given to the type and collateral of the loans with particular attention paid to commercial real estate construction loans, due to the inherent risk of this type of loan. Specific and general reserves are available for any identified loss.

The Company recorded no consolidated provision for loan losses for the three months ended March 31, 2013 and 2012. For the three months ended March 31, 2013, the Company decreased its allowance for loan losses allocated to commercial and industrial (“C&I”) loans by $787 thousand, while increasing its allowance allocation to commercial real estate (“CRE”), real estate construction and residential mortgages (1st and 2nd liens) by $349 thousand, $704 thousand and $864 thousand, respectively.

The decrease in the allowance for loan losses allocated to C&I loans during the first quarter of 2013 reflected a 0.94% reduction in the ASC 450-20 historical loss factors rate on unimpaired pass rated C&I loans. Partially offsetting the loss factors rate reduction was a $20 million increase in the balance of unimpaired pass rated C&I loans during the first quarter of 2013, coupled with an increase of $97 thousand in specific reserves for C&I loans as computed under ASC 310-10 at March 31, 2013 as compared to December 31, 2012.

The increase in the allowance for loan losses allocated to CRE loans was primarily due to a $39 million increase in the balance of unimpaired pass rated CRE loans, mainly due to growth in multi-family lending, versus December 31, 2012. The increases to the allowance allocated to real estate construction and residential mortgages was largely due to increases in the ASC 450-20 historical loss factors for such loans of 5.68% and 0.56%, respectively, when compared to December 31, 2012.

The changes in the ASC 450-20 loss factors rates were primarily due to an expansion of the look back period used in calculating historical losses to a rolling twelve quarter period (from an eight quarter period) for each loan segment. This change results from the Company’s effort to improve the granularity of its individual loan segment charge-off history effective with the March 31, 2013 calculation. Additionally, the expansion of the look back period reduces the volatility associated with improperly weighting short-term trends in this calculation. These changes more accurately represent the Company’s incurred and expected losses at March 31, 2013 by individual loan segment.

At March 31, 2013 and December 31, 2012, the ending balance in the allowance for loan losses disaggregated by class and impairment methodology follows below (in thousands). Also shown below are total loans at March 31, 2013 and December 31, 2012 disaggregated by class and impairment methodology (in thousands).

| March 31, 2013 | | Commercial and industrial | | | Commercial real estate | | | Real estate construction | | | Residential mortgages (1st and 2nd liens) | | | Home equity | | | Consumer | | | Unallocated | | | Total | |

| Allowance for loan losses: | | | | | | | | | | | | | | | | | | | | | | | | |

| Ending balance: individually evaluated for impairment | | $ | 437 | | | $ | - | | | $ | - | | | $ | 618 | | | $ | 165 | | | $ | 56 | | | $ | - | | | $ | 1,276 | |

| Ending balance: collectively evaluated for impairment | | | 4,908 | | | | 6,570 | | | | 845 | | | | 1,823 | | | | 759 | | | | 189 | | | | 1,464 | | | | 16,558 | |

| Ending balance | | $ | 5,345 | | | $ | 6,570 | | | $ | 845 | | | $ | 2,441 | | | $ | 924 | | | $ | 245 | | | $ | 1,464 | | | $ | 17,834 | |

| Loan balances: | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Ending balance: individually evaluated for impairment | | $ | 10,545 | | | $ | 8,238 | | | $ | 840 | | | $ | 4,976 | | | $ | 750 | | | $ | 324 | | | $ | - | | | $ | 25,673 | |

| Ending balance: collectively evaluated for impairment | | | 177,230 | | | | 391,032 | | | | 13,235 | | | | 141,991 | | | | 62,713 | | | | 12,525 | | | | - | | | | 798,726 | |

| Ending balance | | $ | 187,775 | | | $ | 399,270 | | | $ | 14,075 | | | $ | 146,967 | | | $ | 63,463 | | | $ | 12,849 | | | $ | - | | | $ | 824,399 | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| December 31, 2012 | | Commercial and industrial | | | Commercial real estate | | | Real estate construction | | | Residential mortgages (1st and 2nd liens) | | | Home equity | | | Consumer | | | Unallocated | | | Total | |

| Allowance for loan losses: | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Ending balance: individually evaluated for impairment | | $ | 340 | | | $ | 22 | | | $ | 1 | | | $ | 575 | | | $ | 86 | | | $ | - | | | $ | - | | | $ | 1,024 | |

| Ending balance: collectively evaluated for impairment | | | 5,841 | | | | 6,127 | | | | 140 | | | | 1,001 | | | | 821 | | | | 189 | | | | 2,638 | | | | 16,757 | |

| Ending balance | | $ | 6,181 | | | $ | 6,149 | | | $ | 141 | | | $ | 1,576 | | | $ | 907 | | | $ | 189 | | | $ | 2,638 | | | $ | 17,781 | |

| Loan balances: | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Ending balance: individually evaluated for impairment | | $ | 10,369 | | | $ | 9,443 | | | $ | 1,961 | | | $ | 4,660 | | | $ | 502 | | | $ | 21 | | | $ | - | | | $ | 26,956 | |

| Ending balance: collectively evaluated for impairment | | | 158,340 | | | | 359,828 | | | | 13,508 | | | | 141,915 | | | | 65,966 | | | | 14,267 | | | | - | | | | 753,824 | |

| Ending balance | | $ | 168,709 | | | $ | 369,271 | | | $ | 15,469 | | | $ | 146,575 | | | $ | 66,468 | | | $ | 14,288 | | | $ | - | | | $ | 780,780 | |

The following table presents certain information pertaining to the Company’s impaired loans disaggregated by class at March 31, 2013 and December 31, 2012 (in thousands):

| | | March 31, 2013 | | | December 31, 2012 | |

| | | Impaired Loans | | | Impaired Loans | |

| | | Unpaid Principal Balance | | | Recorded Balance | | | Allowance Allocated | | | Unpaid Principal Balance | | | Recorded Balance | | | Allowance Allocated | |

| With no allowance recorded: | | | | | | | | | | | | | | | | | | |

| Commercial and industrial | | $ | 8,887 | | | $ | 8,887 | | | $ | - | | | $ | 7,913 | | | $ | 7,492 | | | $ | - | |

| Commercial real estate | | | 9,223 | | | | 8,238 | | | | - | | | | 8,859 | | | | 7,282 | | | | - | |

| Real estate construction | | | 840 | | | | 840 | | | | - | | | | 1,334 | | | | 1,305 | | | | - | |

| Residential mortgages (1st and 2nd liens) | | | 2,335 | | | | 2,206 | | | | - | | | | 1,918 | | | | 1,788 | | | | - | |

| Home equity | | | 572 | | | | 572 | | | | - | | | | 418 | | | | 416 | | | | - | |

| Consumer | | | 166 | | | | 166 | | | | - | | | | 21 | | | | 21 | | | | - | |

| Subtotal | | | 22,023 | | | | 20,909 | | | | - | | | | 20,463 | | | | 18,304 | | | | - | |

| | | | | | | | | | | | | | | | | | | | | | | | | |

| With an allowance recorded: | | | | | | | | | | | | | | | | | | | | | | | | |

| Commercial and industrial | | | 1,960 | | | | 1,658 | | | | 437 | | | | 2,884 | | | | 2,877 | | | | 340 | |

| Commercial real estate | | | - | | | | - | | | | - | | | | 2,161 | | | | 2,161 | | | | 22 | |

| Real estate construction | | | - | | | | - | | | | - | | | | 656 | | | | 656 | | | | 1 | |

| Residential mortgages (1st and 2nd liens) | | | 2,896 | | | | 2,770 | | | | 618 | | | | 3,015 | | | | 2,872 | | | | 575 | |

| Home equity | | | 178 | | | | 178 | | | | 165 | | | | 86 | | | | 86 | | | | 86 | |

| Consumer | | | 158 | | | | 158 | | | | 56 | | | | - | | | | - | | | | - | |

| Subtotal | | | 5,192 | | | | 4,764 | | | | 1,276 | | | | 8,802 | | | | 8,652 | | | | 1,024 | |

| Total | | $ | 27,215 | | | $ | 25,673 | | | $ | 1,276 | | | $ | 29,265 | | | $ | 26,956 | | | $ | 1,024 | |

The following table presents additional information pertaining to the Company’s impaired loans disaggregated by class for the three months ended March 31, 2013 and 2012 (in thousands):

| | | Three Months Ended March 31, 2013 | | | Three Months Ended March 31, 2012 | |

| | | Impaired Loans | | | Impaired Loans | |

| | | Average recorded investment in impaired loans | | | Interest income recognized on impaired loans | | | Interest income recognized on a cash basis on impaired loans | | | Average recorded investment in impaired loans | | | Interest income recognized on impaired loans | | | Interest income recognized on a cash basis on impaired loans | |

| Commercial and industrial | | $ | 10,947 | | | $ | 57 | | | $ | - | | | $ | 29,678 | | | $ | 265 | | | $ | - | |

| Commercial real estate | | | 11,090 | | | | 69 | | | | - | | | | 73,791 | | | | 325 | | | | - | |

| Real estate construction | | | 1,401 | | | | - | | | | - | | | | 12,609 | | | | 181 | | | | - | |

| Residential mortgages (1st and 2nd liens) | | | 5,004 | | | | 42 | | | | - | | | | 8,463 | | | | - | | | | - | |

| Home equity | | | 751 | | | | 3 | | | | - | | | | 3,993 | | | | - | | | | - | |

| Consumer | | | 318 | | | | 5 | | | | - | | | | 675 | | | | - | | | | - | |

| Total | | $ | 29,511 | | | $ | 176 | | | $ | - | | | $ | 129,209 | | | $ | 771 | | | $ | - | |

TDRs involve modifications or renewals where the Company has granted a concession to a borrower in financial distress. The Company reviews all modifications and renewals for determination of TDR status. The Company allocated $1 million and $800 thousand of specific reserves to customers whose loan terms have been modified in TDRs as of March 31, 2013 and December 31, 2012, respectively. These loans involved the restructuring of terms to allow customers to mitigate the risk of foreclosure by meeting a lower payment requirement based upon their current cash flow. These may also include loans that renewed at existing contractual rates, but below market rates for comparable credit.

A total of $38 thousand and $35 thousand were committed to be advanced in connection with TDRs as of March 31, 2013 and December 31, 2012, respectively, representing the amount the Company is legally required to advance under existing loan agreements. These loans are not in default under the terms of the loan agreements and are accruing. It is the Company’s policy to evaluate advances on such loans on a case by case basis. Absent a legal obligation to advance pursuant to the terms of the loan agreement, the Company generally will not advance funds for which it has outstanding commitments, but may do so in certain circumstances.

The following tables present certain information regarding outstanding TDRs at March 31, 2013 and December 31, 2012 (dollars in thousands), TDRs executed during the three months ended March 31, 2013 and 2012 (dollars in thousands) and TDRs with payment defaults of 90 days or more within twelve months of restructuring during the three months ended March 31, 2013 and 2012 (dollars in thousands):

| | | March 31, 2013 | | | December 31, 2012 | |

| Total Troubled Debt Restructurings | | Number of Loans | | | Outstanding Recorded Balance | | | Number of Loans | | | Outstanding Recorded Balance | |

| | | | | | | | | | | | | |

| Commercial and industrial | | | 42 | | | $ | 6,400 | | | | 41 | | | $ | 6,468 | |

| Commercial real estate | | | 8 | | | | 5,072 | | | | 9 | | | | 6,238 | |

| Residential mortgages (1st and 2nd liens) | | | 18 | | | | 4,441 | | | | 15 | | | | 3,587 | |

| Consumer | | | 5 | | | | 324 | | | | 5 | | | | 311 | |

| | | | 73 | | | $ | 16,237 | | | | 70 | | | $ | 16,604 | |

| | | Three months ended | | | Three months ended | |

| | | March 31, 2013 | | | March 31, 2012 | |

| | | | | | Pre-Modification | | | Post-Modification | | | | | | Pre-Modification | | | Post-Modification | |

| | | Number | | | Outstanding | | | Outstanding | | | Number | | | Outstanding | | | Outstanding | |

| New Troubled Debt | | of | | | Recorded | | | Recorded | | | of | | | Recorded | | | Recorded | |

| Restructurings | | Loans | | | Balance | | | Balance | | | Loans | | | Balance | | | Balance | |

| | | | | | | | | | | | | | | | | | | |

| Commercial and industrial | | | 2 | | | $ | 320 | | | $ | 320 | | | | 9 | | | $ | 3,316 | | | $ | 3,316 | |

| Residential mortgages (1st and 2nd liens) | | | 3 | | | | 905 | | | | 905 | | | | - | | | | - | | | | - | |

| Consumer | | | 1 | | | | 17 | | | | 17 | | | | - | | | | - | | | | - | |

| | | | 6 | | | $ | 1,242 | | | $ | 1,242 | | | | 9 | | | $ | 3,316 | | | $ | 3,316 | |

| | | Three months ended | | | Three months ended | |

| | | March 31, 2013 | | | March 31, 2012 | |

| | | | | | Outstanding | | | | | | Outstanding | |

| | | Number | | | Recorded | | | Number | | | Recorded | |

| Defaulted Troubled Debt Restructurings | | of Loans | | | Balance | | | of Loans | | | Balance | |

| | | | | | | | | | | | | |

| Commercial and industrial | | | - | | | $ | - | | | | 1 | | | $ | 15 | |

| Residential mortgages (1st and 2nd liens) | | | - | | | | - | | | | 1 | | | | 494 | |

| | | | - | | | $ | - | | | | 2 | | | $ | 509 | |

Not all loan modifications are TDRs. In some cases, the Company might provide a concession, such as a reduction in interest rate, but the borrower is not experiencing financial distress. This could be the case if the Company is matching a competitor’s interest rate.

The following table presents information regarding modifications and renewals executed during the three months ended March 31, 2013 and 2012 that are not considered TDRs (dollars in thousands):

| | | Three months ended | | | Three months ended | |

| | | March 31, 2013 | | | March 31, 2012 | |

| | | | | | Outstanding | | | | | | Outstanding | |

| | | Number | | | Recorded | | | Number | | | Recorded | |

| Modifications Not Considered TDRs | | of Loans | | | Balance | | | of Loans | | | Balance | |

| | | | | | | | | | | | | |

| Commercial and industrial | | | - | | | $ | - | | | | 1 | | | $ | 580 | |

| Commercial real estate | | | 11 | | | | 19,703 | | | | 2 | | | | 3,179 | |

| | | | 11 | | | $ | 19,703 | | | | 3 | | | $ | 3,759 | |

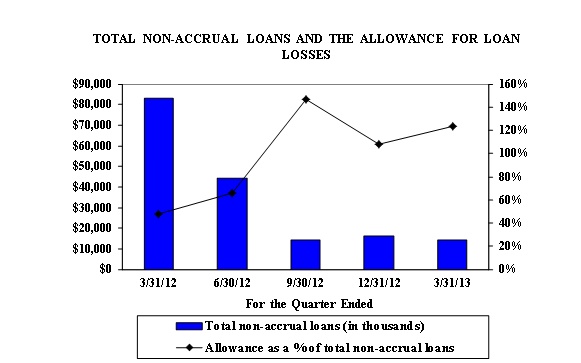

The following is a summary of information pertaining to non-performing assets at March 31, 2013 and December 31, 2012 (in thousands):

| | | March 31, | | | December 31, | |

| | | 2013 | | | 2012 | |

| Non-accrual loans | | $ | 14,420 | | | $ | 16,435 | |

| Non-accrual loans held-for-sale | | | - | | | | 907 | |

| Loans 90 days past due and still accruing | | | - | | | | - | |

| OREO | | | 372 | | | | 1,572 | |

| Total non-performing assets | | $ | 14,792 | | | $ | 18,914 | |

| TDRs accruing interest | | $ | 10,247 | | | $ | 9,954 | |

| TDRs nonaccruing | | $ | 5,990 | | | $ | 6,650 | |

The following table summarizes non-accrual loans by loan class at March 31, 2013 and December 31, 2012 (dollars in thousands):

| | | Non-accrual Loans | |

| | | | | | Total | | | % of | | | | | | Total | | | % of | |

| | | | | | % of | | | Loans | | | Total | | | | | | % of | | | Loans | | | Total | |

| | | 3/31/2013 | | | Total | | | 3/31/2013 | | | Loans | | | 12/31/2012 | | | Total | | | 12/31/2012 | | | Loans | |

| Commercial and industrial | | $ | 6,746 | | | | 46.8 | % | | $ | 187,775 | | | | 0.8 | % | | $ | 6,529 | | | | 39.8 | % | | $ | 168,709 | | | | 0.8 | % |

| Commercial real estate | | | 3,972 | | | | 27.5 | | | | 399,270 | | | | 0.5 | | | | 5,192 | | | | 31.6 | | | | 369,271 | | | | 0.7 | |

| Real estate construction | | | 840 | | | | 5.8 | | | | 14,075 | | | | 0.1 | | | | 1,961 | | | | 11.9 | | | | 15,469 | | | | 0.3 | |

| Residential mortgages (1st and 2nd liens) | | | 2,336 | | | | 16.2 | | | | 146,967 | | | | 0.3 | | | | 2,466 | | | | 15.0 | | | | 146,575 | | | | 0.3 | |

| Home equity | | | 514 | | | | 3.6 | | | | 63,463 | | | | - | | | | 266 | | | | 1.6 | | | | 66,468 | | | | - | |

| Consumer | | | 12 | | | | 0.1 | | | | 12,849 | | | | - | | | | 21 | | | | 0.1 | | | | 14,288 | | | | - | |

| Total non-accrual loans | | $ | 14,420 | | | | 100.0 | % | | $ | 824,399 | | | | 1.7 | % | | $ | 16,435 | | | | 100.0 | % | | $ | 780,780 | | | | 2.1 | % |

For the non-accrual loans outstanding at the end of the reported periods, additional interest income of approximately $406 thousand and $1.4 million would have been recorded on non-accrual loans during the three months ended March 31, 2013 and 2012, respectively, if the loans had performed in accordance with their original terms.

The following table details the collateral value securing non-accrual loans at March 31, 2013 and December 31, 2012 (in thousands):

| | | March 31, 2013 | | | December 31, 2012 | |

| | | Non-accrual Loans | | | Non-accrual Loans | |

| | | Principal Balance | | | Collateral Value | | | Principal Balance | | | Collateral Value | |

| Commercial and industrial (1) | | $ | 6,746 | | | $ | 5,163 | | | $ | 6,529 | | | $ | 4,400 | |

| Commercial real estate | | | 3,972 | | | | 10,490 | | | | 5,192 | | | | 12,675 | |

| Real estate construction | | | 840 | | | | 3,310 | | | | 1,961 | | | | 3,661 | |

| Residential mortgages (1st and 2nd liens) | | | 2,336 | | | | 3,511 | | | | 2,466 | | | | 5,141 | |

| Home equity | | | 514 | | | | 1,436 | | | | 266 | | | | 849 | |

| Consumer | | | 12 | | | | - | | | | 21 | | | | - | |

| Total | | $ | 14,420 | | | $ | 23,910 | | | $ | 16,435 | | | $ | 26,726 | |

(1) Repayment of commercial and industrial loans is expected primarily from the cash flow of the business. The collateral typically securing these loans is a lien on all corporate assets via a blanket UCC filing and does not usually include real estate. For purposes of this disclosure, the Company has ascribed no value to the non-real estate collateral for this class of loans.

At March 31, 2013 and December 31, 2012, past due loans disaggregated by class were as follows (in thousands):

| | | Past Due | | | | | | | |

| March 31, 2013 | | 30 - 59 days | | | 60 - 89 days | | | 90 days and over | | | Total | | | Current | | | Total | |

| Commercial and industrial | | $ | 382 | | | $ | 370 | | | $ | 6,746 | | | $ | 7,498 | | | $ | 180,277 | | | $ | 187,775 | |

| Commercial real estate | | | 1,339 | | | | - | | | | 3,972 | | | | 5,311 | | | | 393,959 | | | | 399,270 | |

| Real estate construction | | | - | | | | - | | | | 840 | | | | 840 | | | | 13,235 | | | | 14,075 | |

| Residential mortgages | | | | | | | | | | | | | | | | | | | | | | | | |

| (1st and 2nd liens) | | | 2,540 | | | | - | | | | 2,336 | | | | 4,876 | | | | 142,091 | | | | 146,967 | |

| Home equity | | | 1,356 | | | | 496 | | | | 514 | | | | 2,366 | | | | 61,097 | | | | 63,463 | |

| Consumer | | | 79 | | | | 1 | | | | 12 | | | | 92 | | | | 12,757 | | | | 12,849 | |

| Total | | $ | 5,696 | | | $ | 867 | | | $ | 14,420 | | | $ | 20,983 | | | $ | 803,416 | | | $ | 824,399 | |

| | | | | | | | | | | | | | | | | | | | | | | | | |

| | | Past Due | | | | | | | | | |

| December 31, 2012 | | 30 - 59 days | | | 60 - 89 days | | | 90 days and over | | | Total | | | Current | | | Total | |

| Commercial and industrial | | $ | 6,591 | | | $ | 1,274 | | | $ | 6,529 | | | $ | 14,394 | | | $ | 154,315 | | | $ | 168,709 | |

| Commercial real estate | | | 1,145 | | | | 329 | | | | 5,192 | | | | 6,666 | | | | 362,605 | | | | 369,271 | |

| Real estate construction | | | 1,382 | | | | - | | | | 1,961 | | | | 3,343 | | | | 12,126 | | | | 15,469 | |

| Residential mortgages | | | | | | | | | | | | | | | | | | | | | | | | |

| (1st and 2nd liens) | | | 2,867 | | | | 6 | | | | 2,466 | | | | 5,339 | | | | 141,236 | | | | 146,575 | |

| Home equity | | | 261 | | | | 100 | | | | 266 | | | | 627 | | | | 65,841 | | | | 66,468 | |

| Consumer | | | 189 | | | | 18 | | | | 21 | | | | 228 | | | | 14,060 | | | | 14,288 | |

| Total | | $ | 12,435 | | | $ | 1,727 | | | $ | 16,435 | | | $ | 30,597 | | | $ | 750,183 | | | $ | 780,780 | |

The Bank utilizes an eight-grade risk-rating system for commercial and industrial loans, commercial real estate and construction loans. Loans in risk grades 1- 4 are considered “pass” loans. The Bank’s risk grades are as follows:

Risk Grade 1 – Excellent. Loans secured by liquid collateral such as certificates of deposit, reputable bank letters of credit, or other cash equivalents; loans that are guaranteed or otherwise backed by the full faith and credit of the United States government or an agency thereof, such as the Small Business Administration; or loans to any publicly held company with a current long-term debt rating of A or better.

Risk Grade 2 – Good. Loans to businesses that have strong financial statements containing an unqualified opinion from a CPA firm and at least three consecutive years of profits; loans supported by un-audited financial statements containing strong balance sheets, five consecutive years of profits, a five-year satisfactory relationship with the Bank, and key balance sheet and income statement trends that are either stable or positive; loans secured by publicly traded marketable securities where there is no impediment to liquidation; loans to individuals backed by liquid personal assets, established credit history, and unquestionable character; or loans to publicly held companies with current long-term debt ratings of Baa or better.

Risk Grade 3 – Satisfactory. Loans supported by financial statements (audited or un-audited) that indicate average or slightly below average risk and having some deficiency or vulnerability to changing economic conditions; loans with some weakness but offsetting features of other support are readily available; loans that are meeting the terms of repayment, but which may be susceptible to deterioration if adverse factors are encountered. Loans may be graded Satisfactory when there is no recent information on which to base a current risk evaluation and the following conditions apply:

| | · | At inception, the loan was properly underwritten, did not possess an unwarranted level of credit risk, and the loan met the above criteria for a risk grade of Excellent, Good, or Satisfactory. |

| | · | At inception, the loan was secured with collateral possessing a loan value adequate to protect the Bank from loss. |

| | · | The loan has exhibited two or more years of satisfactory repayment with a reasonable reduction of the principal balance. |

| | · | During the period that the loan has been outstanding, there has been no evidence of any credit weakness. Some examples of weakness include slow payment, lack of cooperation by the borrower, breach of loan covenants, or |

| | · | The borrower is in an industry known to be experiencing problems. If any of these credit weaknesses is observed, a lower risk grade may be warranted. |

Risk Grade 4 - Satisfactory/Monitored. Loans in this category are considered to be of acceptable credit quality, but contain greater credit risk than satisfactory loans due to weak balance sheets, marginal earnings or cash flow, or other uncertainties. These loans warrant a higher than average level of monitoring to ensure that weaknesses do not advance. The level of risk in a Satisfactory/Monitored loan is within acceptable underwriting guidelines so long as the loan is given the proper level of management supervision.

Risk Grade 5 - Special Mention. Loans which possess some credit deficiency or potential weakness which deserves close attention. Such loans pose an unwarranted financial risk that, if not corrected, could weaken the loan by adversely impacting the future repayment ability of the borrower. The key distinctions of a Special Mention classification are that (1) it is indicative of an unwarranted level of risk and (2) weaknesses are considered “potential,” not “defined,” impairments to the primary source of repayment.

Risk Grade 6 – Substandard. One or more of the following characteristics may be exhibited in loans classified Substandard:

| | · | Loans which possess a defined credit weakness. The likelihood that a loan will be paid from the primary source of repayment is uncertain. Financial deterioration is under way and very close attention is warranted to ensure that the loan is collected without loss. |

| | · | Loans are inadequately protected by the current net worth and paying capacity of the obligor. |

| | · | The primary source of repayment is gone, and the Bank is forced to rely on a secondary source of repayment, such as collateral liquidation or guarantees. |

| | · | Loans have a distinct possibility that the Bank will sustain some loss if deficiencies are not corrected. |

| | · | Unusual courses of action are needed to maintain a high probability of repayment. |

| | · | The borrower is not generating enough cash flow to repay loan principal; however, it continues to make interest payments. |

| | · | The lender is forced into a subordinated or unsecured position due to flaws in documentation. |

| | · | Loans have been restructured so that payment schedules, terms, and collateral represent concessions to the borrower when compared to the normal loan terms. |

| | · | The lender is seriously contemplating foreclosure or legal action due to the apparent deterioration in the loan. |

| | · | There is a significant deterioration in market conditions to which the borrower is highly vulnerable. |

Risk Grade 7 – Doubtful. One or more of the following characteristics may be present in loans classified Doubtful:

| | · | Loans have all of the weaknesses of those classified as Substandard. However, based on existing conditions, these weaknesses make full collection of principal highly improbable. |

| | · | The primary source of repayment is gone, and there is considerable doubt as to the quality of the secondary source of repayment. |

| | · | The possibility of loss is high but because of certain important pending factors which may strengthen the loan, loss classification is deferred until the exact status of repayment is known. |

Risk Grade 8 – Loss. Loans are considered uncollectible and of such little value that continuing to carry them as assets is not feasible. Loans will be classified Loss when it is neither practical nor desirable to defer writing off or reserving all or a portion of a basically worthless asset, even though partial recovery may be possible at some time in the future.

At March 31, 2013 and December 31, 2012, based upon the most recent analysis performed, the following table presents the Company’s loan portfolio credit risk profile by internally assigned grade disaggregated by class of loan (in thousands):

| | | Credit Risk Profile By Internally Assigned Grade | |

| March 31, 2013 | | Commercial and industrial | | | Commercial real estate | | | Real estate construction | | | Residential mortgages (1st and 2nd liens) | | | Home equity | | | Consumer | | | Total | |

| Grade: | | | | | | | | | | | | | | | | | | | | | |

| Pass | | $ | 163,819 | | | $ | 353,080 | | | $ | 5,283 | | | $ | 141,991 | | | $ | 62,949 | | | $ | 12,530 | | | $ | 739,652 | |

| Special mention | | | 4,969 | | | | 25,627 | | | | - | | | | - | | | | - | | | | - | | | | 30,596 | |

| Substandard | | | 18,987 | | | | 20,563 | | | | 8,792 | | | | 4,976 | | | | 514 | | | | 319 | | | | 54,151 | |

| Total | | $ | 187,775 | | | $ | 399,270 | | | $ | 14,075 | | | $ | 146,967 | | | $ | 63,463 | | | $ | 12,849 | | | $ | 824,399 | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | Credit Risk Profile By Internally Assigned Grade | |

| December 31, 2012 | | Commercial and industrial | | | Commercial real estate | | | Real estate construction | | | Residential mortgages (1st and 2nd liens) | | | Home equity | | | Consumer | | | Total | |

| Grade: | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Pass | | $ | 143,804 | | | $ | 311,123 | | | $ | 4,790 | | | $ | 141,915 | | | $ | 65,966 | | | $ | 14,267 | | | $ | 681,865 | |

| Special mention | | | 5,995 | | | | 38,670 | | | | - | | | | - | | | | - | | | | - | | | | 44,665 | |

| Substandard | | | 18,910 | | | | 19,478 | | | | 10,679 | | | | 4,660 | | | | 502 | | | | 21 | | | | 54,250 | |

| Total | | $ | 168,709 | | | $ | 369,271 | | | $ | 15,469 | | | $ | 146,575 | | | $ | 66,468 | | | $ | 14,288 | | | $ | 780,780 | |

The Bank annually reviews the ratings on all commercial and industrial, commercial real estate and real estate construction loans greater than $1 million. Semi-annually, the Bank engages an independent third-party to review a significant portion of loans within these loan classes. Management uses the results of these reviews as part of its ongoing review process.

5. RETIREMENT PLAN

The Company’s retirement plan is noncontributory and covers substantially all eligible employees. The plan conforms to the provisions of the Employee Retirement Income Security Act of 1974, as amended, and the Pension Protection Act of 2006, which requires certain funding rules for defined benefit plans. The Company’s policy is to accrue for all pension costs and to fund the maximum amount allowable for tax purposes. Actuarial gains and losses that arise from changes in assumptions concerning future events are amortized over a period that reflects the long-term nature of pension expense used in estimating pension costs.

The Company accounts for its retirement plan in accordance with ASC 715, “Compensation – Retirement Benefits” and ASC 960, “Plan Accounting – Defined Benefit Pension Plans,” which require an employer that is a business entity and sponsors one or more single-employer defined benefit plans to recognize the funded status of a benefit plan in its statement of financial position; recognize as a component of other comprehensive income, net of tax, the gains or losses and prior service costs or credits that arise during the period but are not recognized as components of net periodic benefit cost; measure defined benefit plan assets and obligation as of the date of fiscal year-end statement of financial position (with limited exceptions); and disclose in the notes to financial statements additional information about certain effects of net periodic benefit cost for the next fiscal year that arise from delayed recognition of the gains or losses, prior service costs or credits, and transition asset and obligation. Plan assets and benefit obligations shall be measured as of the date of its statement of financial position and in determining the amount of net periodic benefit cost. The codification also requires an employer to use the same date for the measurement of plan assets as for the statement of condition.

On December 31, 2012, certain provisions of the Company’s retirement plan were changed which affected all participants in this plan and froze the participation of new entrants into the pension plan for all remaining employees in 2012. These changes froze the plan such that no additional pension benefits would accumulate.

The following table presents information concerning net periodic defined benefit pension (income) expense for the three months ended March 31, 2013 and 2012 (in thousands):

| | | Three Months Ended | |

| | | March 31, 2013 | | | March 31, 2012 | |

| Service cost | | $ | - | | | $ | 603 | |

| Interest cost | | | 498 | | | | 555 | |

| Expected return on plan assets | | | (575 | ) | | | (527 | ) |

| Net amortization | | | 61 | | | | 160 | |

| Net periodic benefit (income) expense | | $ | (16 | ) | | $ | 791 | |

In December 2012, the Company made an annual minimum contribution of $1 million for the plan year ending September 30, 2013. There is no additional minimum required contribution for the plan year ending September 30, 2013.

6. STOCK-BASED COMPENSATION