1

PG&E Corporation:

Preparing For the Future

Peter A. Darbee, Chairman, CEO and President

Sanford Bernstein Strategic Decisions Conference

May 30 - June 1, 2007, New York, NY

2

This presentation contains forward-looking statements regarding management’s guidance for PG&E Corporation’s 2007 and 2008 earnings per share from operations, targeted

average annual growth rate for earnings per share from operations, anticipated dividend growth, as well as management’s projections regarding Pacific Gas and Electric

Company’s (Utility) capital expenditures, rate base and rate base growth, future electricity resources, and energy efficiency funding levels. These statements are based on

current expectations and various assumptions which management believes are reasonable, including that substantial capital investments are made in Utility business over the

2007-2011 period, Utility rate base averages $17 billion in 2007 and $18.7 billion in 2008, that the Utility earns at least its authorized rate of return on equity, and that theUtility’s ratemaking capital structure is maintained at 52 percent equity. These statements and assumptions are necessarily subject to various risks and uncertainties, the

realization or resolution of which are outside of management's control. Actual results may differ materially. Factors that could cause actual results to differ materially include:

•Utility’s ability to timely recover costs through rates;

•the outcome of regulatory proceedings, including ratemaking proceedings pending at the California Public Utilities Commission (CPUC) and the Federal Energy Regulatory

Commission;

•the adequacy and price of electricity and natural gas supplies, and the ability of the Utility to manage and respond to the volatility of the electricity and natural gas markets;

•the effect of weather, storms, earthquakes, fires, floods, disease, other natural disasters, explosions, accidents, mechanical breakdowns, acts of terrorism, and other events or

hazards that could affect the Utility’s facilities and operations, its customers, and third parties on which the Utility relies;

•the potential impacts of climate change on the Utility’s electricity and natural gas business;

•changes in customer demand for electricity and natural gas resulting from unanticipated population growth or decline, general economic and financial market conditions,

changes in technology including the development of alternative energy sources, or other reasons;

•operating performance of the Utility’s Diablo Canyon nuclear generating facilities (Diablo Canyon), the occurrence of unplanned outages at Diablo Canyon, or the temporary

or permanent cessation of operations at Diablo Canyon;

•the ability of the Utility to recognize benefits from its initiatives to improve its business processes and customer service;

•the ability of the Utility to timely complete its planned capital investment projects;

•the impact of changes in federal or state laws, or their interpretation, on energy policy and the regulation of utilities and their holding companies;

•the impact of changing wholesale electric or gas market rules, including the California Independent System Operator’s new rules to restructure the California wholesale

electricity market;

•how the CPUC administers the conditions imposed on PG&E Corporation when it became the Utility’s holding company;

•the extent to which PG&E Corporation or the Utility incur costs and liabilities in connection with pending litigation that are not recoverable through rates, from third parties, or

through insurance recoveries;

•thee ability of PG&E Corporation and/or the Utility to access capital markets and other sources of credit;

•the impact of environmental laws and regulations and the costs of compliance and remediation;

•the effect of municipalization, direct access, community choice aggregation, or other forms of bypass, and

•other risks and factors disclosed in PG&E Corporation’s and Pacific Gas and Electric Company’s SEC reports.

Cautionary Statement Regarding Forward-Looking

Information

3

Key Takeaways From Today’s Discussion

•PCG is a core utility holding, delivering strong investment

opportunities and low regulatory risk.

•Potential earnings “upsides” in 2008 and beyond are not

included in guidance.

•Emerging growth strategies present additional business

opportunities.

4

Agenda For Today

•PG&E Corporation overview

•Regulatory business drivers

•Core investment - focus and strategy

•PCG earnings outlook

•Energy policy and emerging opportunities

5

Business Unit | 2006 Rate Base ($B) | Regulation |

Electric and gas distribution | $10.3 | CPUC |

Electric generation | $1.8 | CPUC |

Gas transmission | $1.5 | CPUC |

Electric transmission | $2.3 | FERC |

PCG Total Business | $15.9 | 85% CPUC/15% FERC |

Pacific Gas and Electric Company (PG&E)

•$12.5 B in Revenues

•$34.8 B in Assets

•5.1 MM Electric/4.2 MM Gas Customers

•$18 B+ Market Capitalization

6

We act with integrity and communicate honestly and openly.

We are passionate about meeting our customers’ needs

and delivering for our shareholders.

We are accountable for all of our own actions: these include

safety, protecting the environment, and supporting our communities.

We work together as a team and are committed to excellence and innovation.

We respect each other and celebrate our diversity.

The

leading

utility in the

United States

Delighted Energized Rewarded

customers employees shareholders

Our values

Operational excellence

Transformation

Our strategies

Our goals

Our vision

PG&E Vision

7

Our Business Strategy

•Competitive customer focus

•Operational excellence

•Regulatory alignment

•Environmental leadership

•Community involvement

8

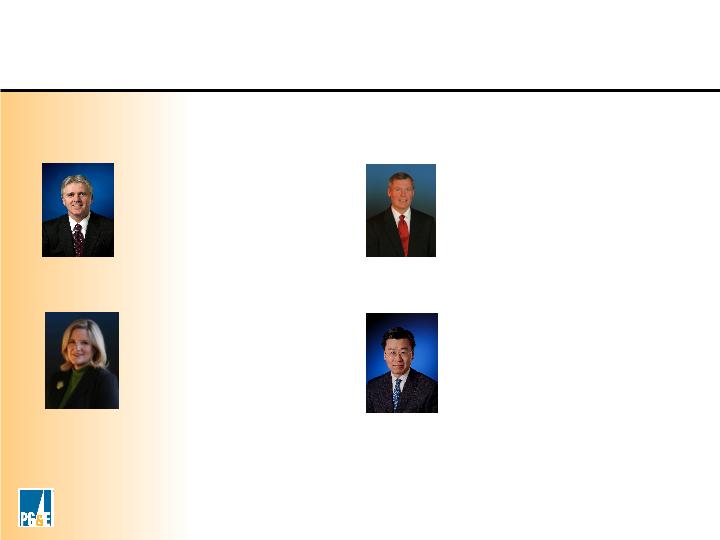

Experienced leaders joined the team in 2006:

Hyun Park

SVP & General Counsel

PG&E Corporation

Jack Keenan

SVP, Generation & Chief Nuclear Officer

Pacific Gas and Electric Company

Helen Burt

SVP & Chief Customer Officer

Pacific Gas and Electric Company

Bill Morrow

President & Chief Operating Officer

Pacific Gas and Electric Company

A Diverse Leadership Team

9

Regulated Business Drivers

•Statewide Energy Strategy

- California Energy Action Plan

- Renewable Portfolio Standard

- AB32 Greenhouse Gas Legislation

•Constructive Regulatory Environment

- Decoupling/Balancing Account Treatment

- Purchased Power and Fuel Costs Pass-Through

- Pre-Approved CapEx

10

Core Business Investment Opportunities

•Electric and gas distribution

•Electric transmission

- System reliability

- Growth to reach renewable resources

•Natural gas transmission and storage

•Electric resource requirements

- Energy efficiency

- Renewables

- Conventional generation

11

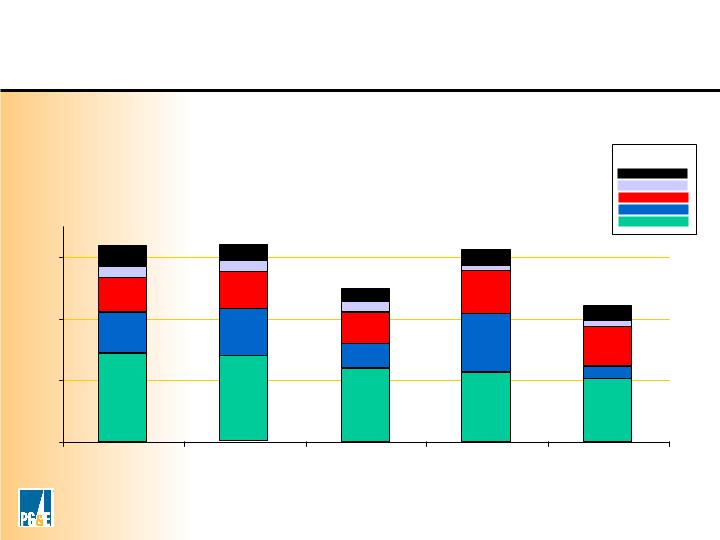

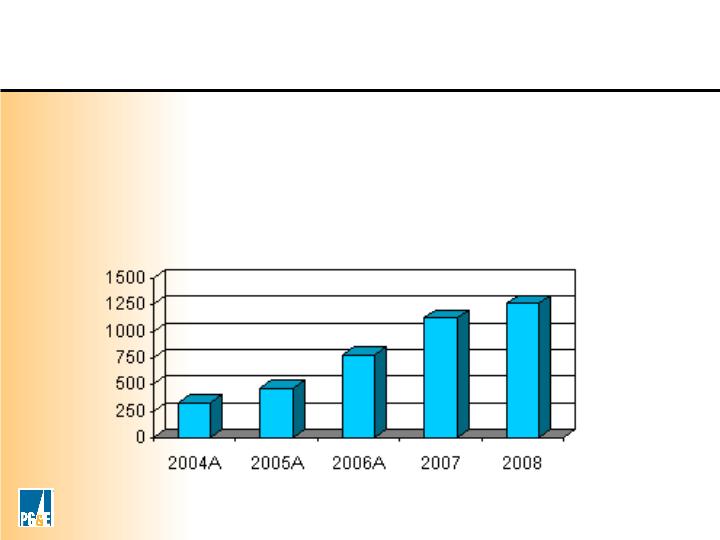

Capital Expenditures ($MM)

Common Plant

Gas Trans.

Electric Trans.

Generation

Distribution

Chart Key

0

$1,000

$2,000

$3,000

2007

2008

2009

2010

2011

$3,200

$3,200

$2,500

$3,100

$2,200

Capital Expenditure Outlook

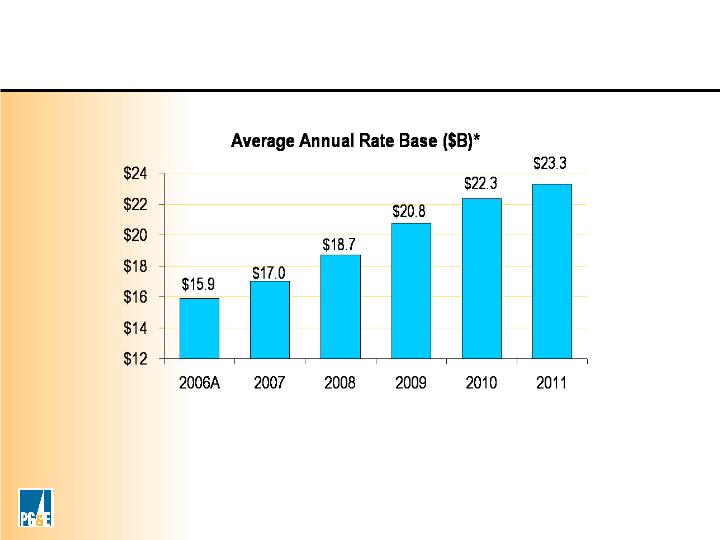

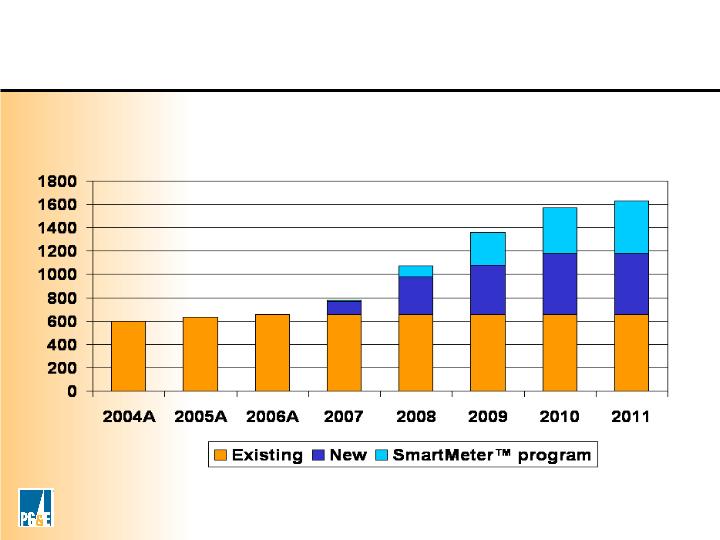

12

* Projected 2007-2011 rate base is not adjusted for the impact of the carrying cost credit that primarily results from

the second series of the Energy Recovery Bonds. Earnings will be reduced by an amount equal to the deferred tax

balance associated with the Energy Recovery Bonds regulatory asset, multiplied by the utility's equity ratio and by its

equity return. The carrying cost credit declines to zero when the taxes are fully paid in 2012.

Rate Base Growth

13

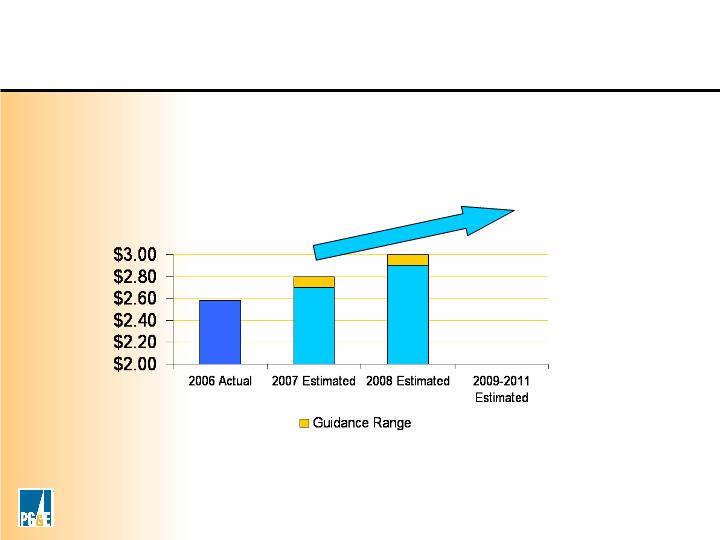

*Reg G reconciliation to GAAP for 2006 EPS from Operations and 2007 and 2008

EPS Guidance available in Appendix and at www.pge-corp.com

EPS from Operations*

EPS Guidance

EPS from Operations*:2007 guidance of $2.70-$2.80 per share 2008

guidance of $2.90-$3.00 per share

14

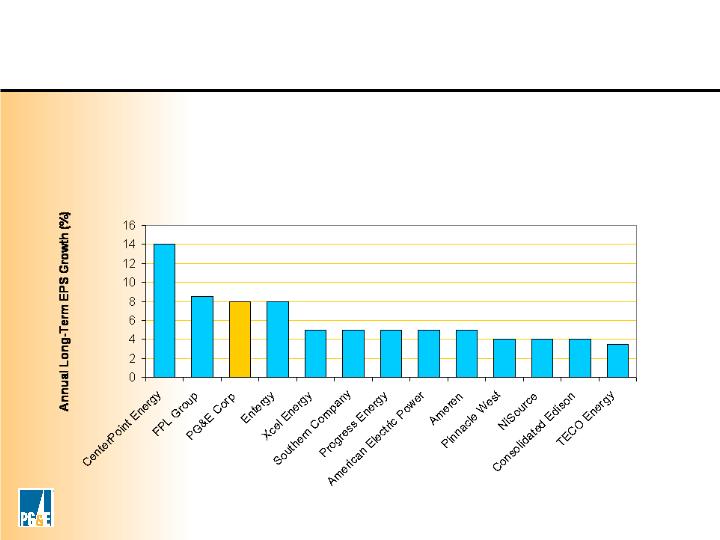

Survey of analyst estimates of EPS growth:

Source: Thomson IBIS long-term EPS Growth Consensus Estimate Median May 8, 2007

EPS Growth - Comparator Group

EPS from operations annual growth targeted to average 8% for

2007 - 2011

15

Potential Earnings Upsides

•Transformation benefits

•Energy efficiency incentives

•Additional transmission and generation investments

16

California Energy Policy

PG&E’s resource investment strategy is aligned with

California’s Energy Action Plan “preferred loading order”:

1.Energy Efficiency

2.Demand Response

3.Renewable Resources

4.Distributed Generation

5.Conventional Resources

17

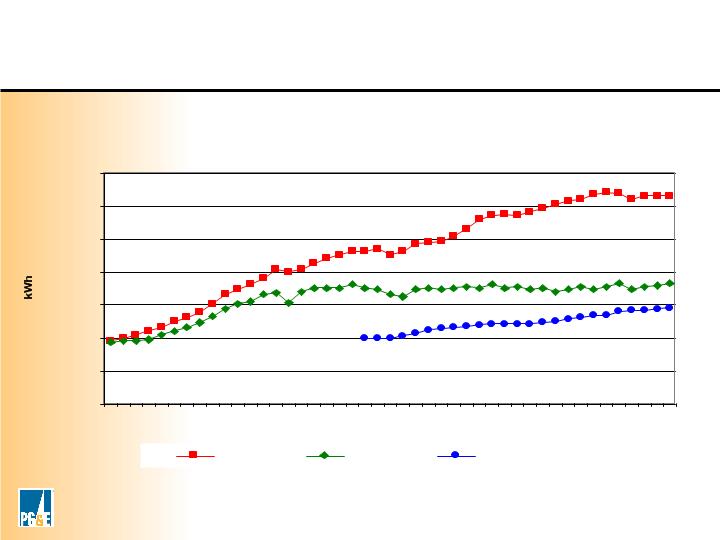

Over the past 30 years, California per capita energy use has remained relatively

flat compared to the 50% increase in U.S. per capita energy use.

Source: California Energy Commission

California’s Success With Energy Efficiency

-

2,000

4,000

6,000

8,000

10,000

12,000

14,000

1960

1965

1970

1975

1980

1985

1990

1995

2000

US

CA

Western Europe

18

Changing Legislative Environment for GHG

Recent greenhouse gas legislation:

•California global warming legislation enacted in 2006

•Federal legislation expected in 2 to 4 years

PG&E supports:

•Mandatory market-based approach

•Encouraging early action toward goals before full regulatory

implementation

•Recognition of prior actions

•Pursuit of all cost-effective reductions in greenhouse gases

•International cooperation

19

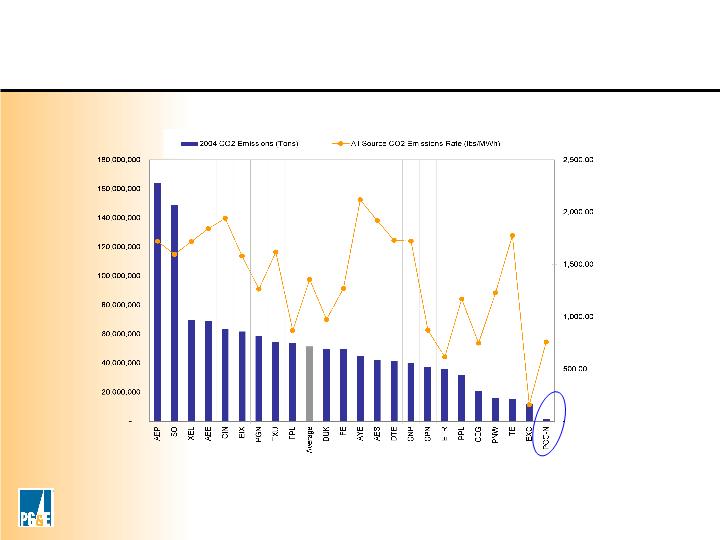

* Comparison companies selected by Innovest. Data include emissions of regulated and unregulated plants.

2004 is the most recent data available.

2004 CO2 Emissions and Emission Rates*

Source: Innovest

Relative CO2 Emissions Rates - Generation

20

Industry Leadership and Emerging Growth

PG&E is looking ahead to the future of utility services

•Clean/renewable fuel technologies

•Smart Energy Web

•Plug-in anywhere technologies

•Sustainable Energy Communities

21

PCG Investment Opportunity Summary

•First quartile EPS growth

- Approved infrastructure investment

•Potential upsides

- Transformation benefits

- Energy efficiency incentives

- Additional transmission and generation investment

•New Products and Services

- Diverse management team with a competitive mindset

- Record of innovation, well-positioned for industry change

22

Conference Notes

23

Appendix

Sanford Bernstein Strategic Decisions Conference

May 30 - June 1, 2007

24

•About half of expected load growth will be met by energy efficiency

•PG&E’s budget and goals for 2006-2008:

Overall energy efficiency budget:$975 million

PG&E filed goals:3,063 GWh; 47 MM therms

GWh Savings: Historic and Target

PG&E’s Energy Efficiency Programs

25

MWs

Demand response impacts expected to double from 2007

Actual and Projected Capacity Savings from Demand Response

Programs

Demand Response Programs

26

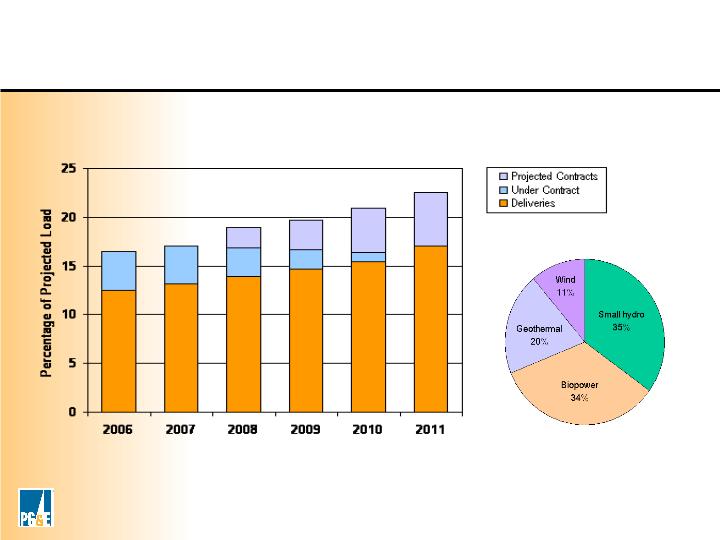

* 2008 to 2011 estimates are based on forecasted construction schedules and

additional contracted resources

Projected Deliveries Plus Contracts*

2006 deliveries comprised of:

Renewable Portfolio Standard target is 20% by 2010

Renewable Resource Procurement

27

PPAs Counterparty/Facility | Size (MW) | Target Operational Date | Contract Term (years) |

Calpine Hayward | 601 | 2010 | 10 |

EIF Firebaugh | 399 | 2009 | 20 |

Starwood Firebaugh | 118 | 2009 | 15 |

EIF Fresno | 196 | 2009 | 20 |

Tierra Energy Hayward | 116 | 2009 | 20 |

Total | 1,430 |

Facility | Size (MW) | Status | Target Operational Date | Estimated Capital Costs |

Gateway | 530 | broken ground | 2009 | $370 million |

Humboldt Bay | 163 | permitting | 2009 | $239 million |

Colusa | 657 | permitting | 2010 | $673 million |

Total | 1,350 | $1,282 million |

New Generation Resources: Utility-Owned &

Conventional Power Purchase Agreements

28

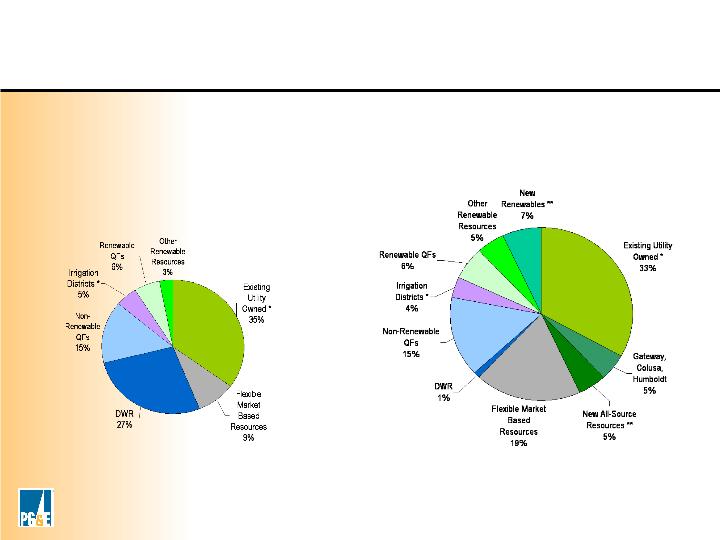

*Over 20% of total retail sales expected to be eligible renewable resources coming from

utility-owned, QFs, Irrigation Districts, and other sources.

**May include utility-owned resources.

* Approximately 13% of total retail sales expected to be eligible renewable resources

coming from utility-owned, QFs, Irrigation Districts and other sources.

2007 Projected Sources of Energy

85,500 GWh

2012 Projected Sources of Energy

89,900 GWh

•Energy efficiency expected to meet half of future load growth

•Growth in renewable resources and resources with operating flexibility

•Growth in utility ownership

Long-Term Electric Resources

29

Balancing Accounts = | •Cost of procuring energy •Sales volume •Selected other elements of operating costs such as energy conservation programs |

Rate Base = | Net Plant (in service) -deferred taxes from accelerated depreciation +/- net working capital (may exclude many balance sheet assets or liabilities) |

Ratemaking = | Projected Test Year With Attrition adjustments |

Ratemaking Summary

30

Credit Profile

•Current Ratings

- Utility issuer rating: BBB (S&P) and Baa1 (Moody’s)

- Utility unsecured debt: BBB (S&P) and Baa1 (Moody’s)

•Average Utility Metrics (2007-2011)*

- S&P Business Profile Rating: 5

- Total Debt to capitalization (EOY): 53.6%

- Funds from Operations Cash Interest Coverage: 5.1x

- Funds from Operations to Average Total Debt: 22%

*Metrics include debt equivalents for long-term power purchase contracts

31

Dividend Policy

•Objectives:

- Flexibility

- Sustainability

- Comparability

•Payout ratio range of 50% - 70%

•Growth balanced with funding for additional investment

opportunities

•Dividend growth is expected to be generally in line with the

growth in EPS from Operations

32

2006

EPS on an Earnings from Operations Basis* Items Impacting Comparability: Scheduling Coordinator Cost Recovery Environmental Remediation Liability Recovery of Interest on PX Liability Severance Costs EPS on a GAAP Basis | $2.57 0.21 (0.05) 0.08 (0.05) $2.76 |

* Earnings per share from operations is a non-GAAP measure. This non-GAAP measure is used because it allows investors to compare the core underlying financial performance from one period to another, exclusive of items that do not reflect the normal course of operations | |

2006 EPS - Reg G Reconciliation

33

2007 EPS Guidance on an Earnings from Operations Basis* Estimated Items Impacting Comparability EPS Guidance on a GAAP Basis 2008 EPS Guidance on an Earnings from Operations Basis* Estimated Items Impacting Comparability EPS Guidance on a GAAP Basis | Low $2.70 0.00 $2.70 Low $2.90 0.00 $2.90 | High $2.80 0.00 $2.80 High $3.00 0.00 $3.00 |

* Earnings per share from operations is a non-GAAP measure. This non-GAAP measure is used because it allows investors to compare the core underlying financial performance from one period to another, exclusive of items that do not reflect the normal course of operations | ||

EPS Guidance - Reg G Reconciliation