PG&E Corporation

Edison Electric Institute

Financial Conference

Financial Conference

November 9-12, 2008

Phoenix, Arizona

Exhibit 99

2

This presentation contains forward-looking statements regarding management’s guidance for PG&E Corporation’s 2008 and 2009 earnings per share (“EPS”) from

operations, targeted compound annual growth rate for EPS from operations over the 2007-2011 outlook period, and financing plans, as well as management’s

projections of Pacific Gas and Electric Company’s (Utility) capital expenditures, rate base, rate base growth, and financing plans. These statements and the underlying

assumptions are based on current expectations which management believes are reasonable. The realization of these statements and assumptions are subject to

various risks and uncertainties and actual results may differ materially. Factors that could cause actual results to differ materially include:

operations, targeted compound annual growth rate for EPS from operations over the 2007-2011 outlook period, and financing plans, as well as management’s

projections of Pacific Gas and Electric Company’s (Utility) capital expenditures, rate base, rate base growth, and financing plans. These statements and the underlying

assumptions are based on current expectations which management believes are reasonable. The realization of these statements and assumptions are subject to

various risks and uncertainties and actual results may differ materially. Factors that could cause actual results to differ materially include:

§ the Utility’s ability to manage capital expenditures and operating costs within authorized levels and recover costs through rates in a timely manner;

§ the outcome of regulatory proceedings, including pending and future ratemaking proceedings at the California Public Utilities Commission (CPUC) and

the Federal Energy Regulatory Commission;

the Federal Energy Regulatory Commission;

§ the adequacy and price of electricity and natural gas supplies, and the ability of the Utility to manage and respond to the volatility of the electricity and

natural gas markets;

natural gas markets;

§ the effect of weather, storms, earthquakes, fires, floods, disease, other natural disasters, explosions, accidents, mechanical breakdowns, acts of

terrorism, and other events or hazards on the Utility’s facilities and operations, its customers, and third parties on which the Utility relies;

terrorism, and other events or hazards on the Utility’s facilities and operations, its customers, and third parties on which the Utility relies;

§ the potential impacts of climate change on the Utility’s electricity and natural gas business;

§ changes in customer demand for electricity and natural gas resulting from unanticipated population growth or decline, general economic and financial

market conditions, changes in technology including the development of alternative energy sources, or other reasons;

market conditions, changes in technology including the development of alternative energy sources, or other reasons;

§ operating performance of the Utility’s Diablo Canyon nuclear generating facilities (Diablo Canyon), the occurrence of unplanned outages at Diablo

Canyon, or the temporary or permanent cessation of operations at Diablo Canyon;

Canyon, or the temporary or permanent cessation of operations at Diablo Canyon;

§ whether the Utility can maintain the cost savings it has recognized from operating efficiencies it has achieved and identify and successfully implement

additional sustainable cost-saving measures;

additional sustainable cost-saving measures;

§ whether the Utility incurs substantial unanticipated expense to improve the safety and reliability of its electric and natural gas distribution systems;

§ whether the Utility achieves the CPUC’s energy efficiency targets and recognizes any incentives the Utility may earn in a timely manner;

§ the impact of changes in federal or state laws, or their interpretation, on energy policy and the regulation of utilities and their holding companies;

§ the impact of changing wholesale electric or gas market rules, including the California Independent System Operator’s new rules to restructure the

California wholesale electricity market;

California wholesale electricity market;

§ how the CPUC administers the conditions imposed on PG&E Corporation when it became the Utility’s holding company;

§ the extent to which PG&E Corporation or the Utility incurs costs and liabilities in connection with litigation that are not recoverable through rates, from

third parties, or through insurance recoveries;

third parties, or through insurance recoveries;

§ the ability of PG&E Corporation and/or the Utility to access capital markets and other sources of credit in a timely manner on favorable terms; especially

given the recent deteriorating conditions in the economy and financial markets

given the recent deteriorating conditions in the economy and financial markets

§ the impact of environmental laws and regulations and the costs of compliance and remediation;

§ the effect of municipalization, direct access, community choice aggregation, or other forms of bypass;

§ the impact of changes in federal or state tax laws, policies or regulations; and

§ other risks and factors disclosed in PG&E Corporation’s and the Utility’s 2007 Annual Report on Form 10-K and other reports filed with the SEC.

Cautionary Language Regarding

Forward-Looking Statements

Forward-Looking Statements

3

PCG: Investment Case

§ PCG’s investment case remains solid in turbulent

financial times:

financial times:

§ Decoupled revenues

§ Ratemaking mechanisms mitigate exposure to commodity price volatility

§ 11.45% weighted ROE on 52% equity

§ Successful execution and timely completion on large scale projects

§ Sustainable dividend, growing in-line with EPS

4

2008 Business Priorities

§ Deliver on Financial Objectives

§ Focus on Customer Service and Satisfaction

§ Identify and Capture Operating Efficiencies

§ Ensure Workforce Readiness and Alignment

§ Improve System Reliability

5

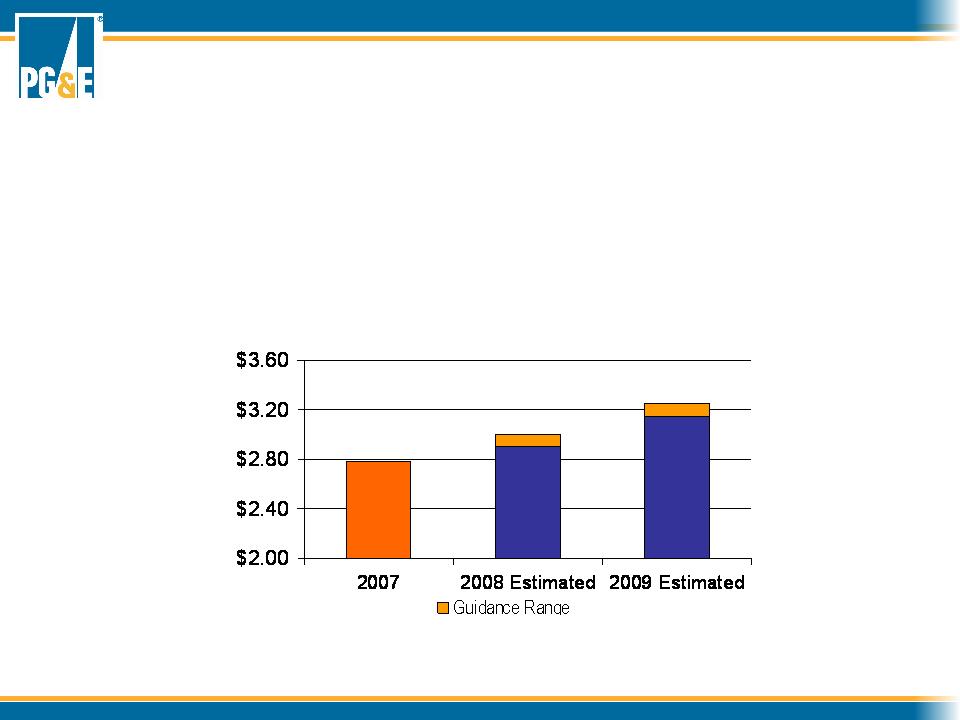

EPS from Operations*

* Reg G reconciliation to GAAP for 2007 EPS from Operations, and 2008 and 2009 EPS Guidance available in Appendix and at

www.pgecorp.com

www.pgecorp.com

Confirming EPS Guidance

§ EPS from Operations Guidance:

§ 2008 guidance of $2.90-$3.00 per share

§ 2009 guidance of $3.15-$3.25 per share

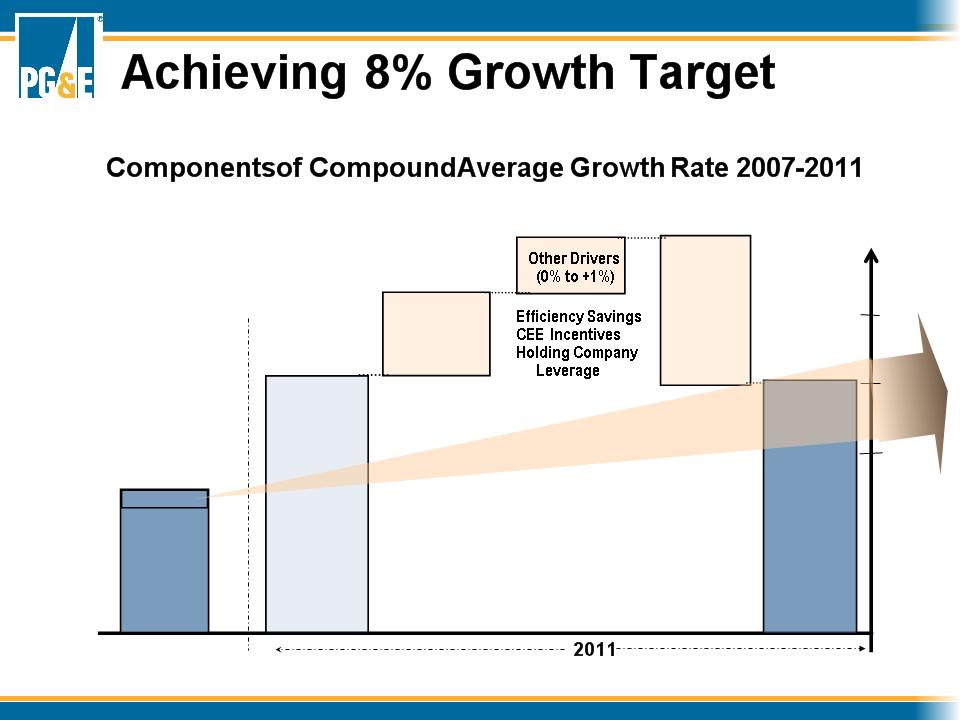

§ 8% targeted CAGR 2007-2011

6

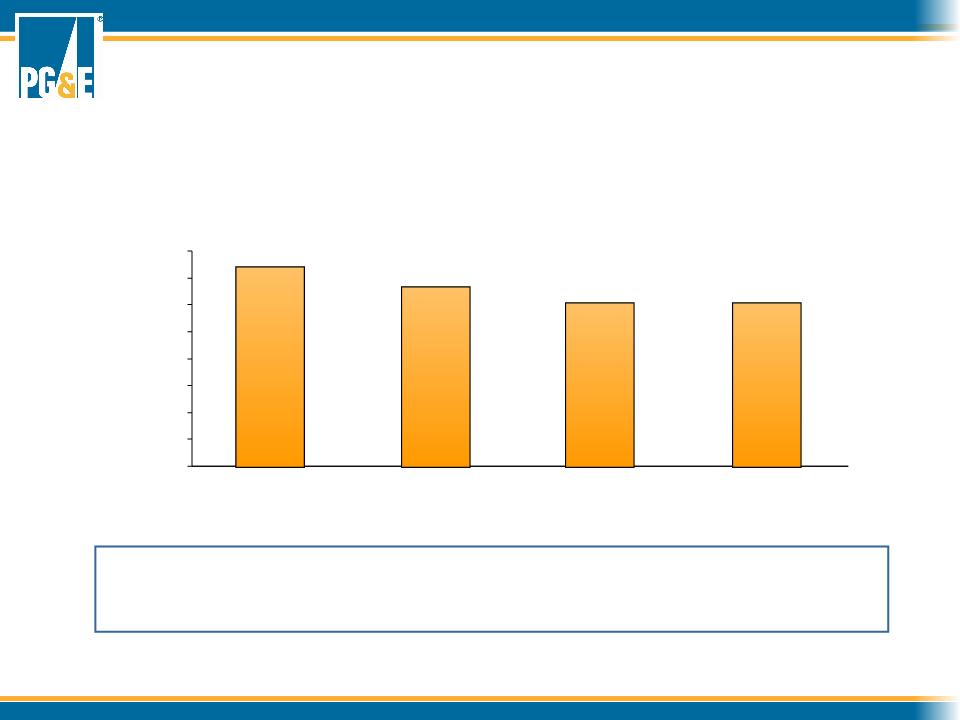

2007

Base

Forecast

Rate Base

Forecast

Rate Base

Growth

(+9% to 10%)

Add’l CapEx

(+1% to 3%)

New Shares

(-3% to- 5%)

$2.70-

$2.80

$2.80

8% CAGR

2007- 2011

8%

10%

6%

2007

Guidance {

Guidance {

Range

% CAGR

2007-2011

7

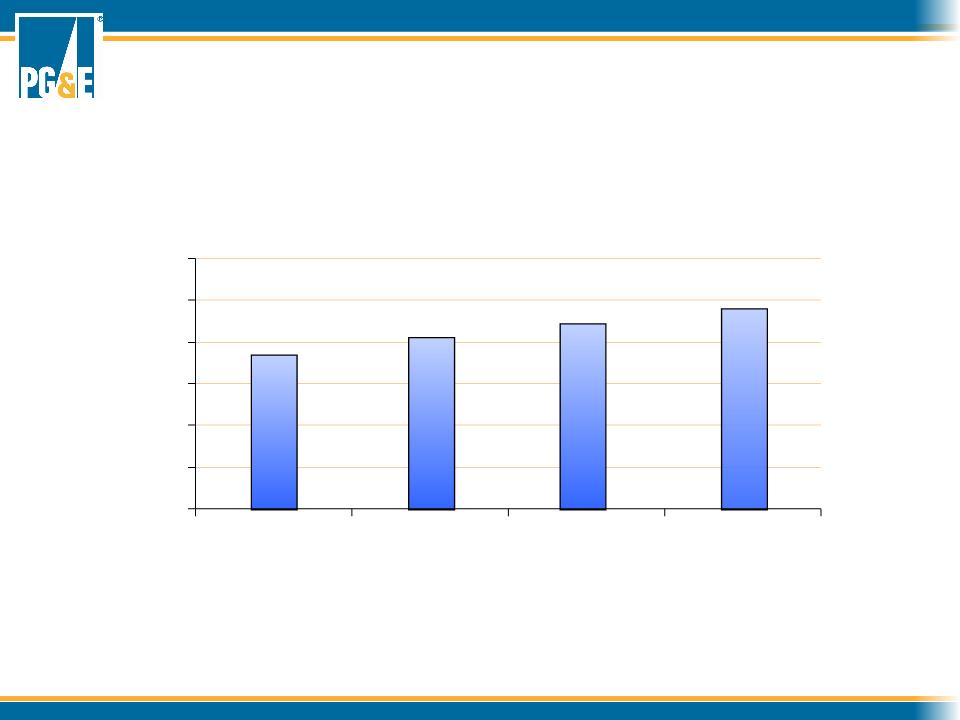

$ MM

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

2008

2009

2010

2011

Projects not included in base forecast include: SmartMeterTM Upgrade, Cornerstone

Improvement Program, additional generation and gas pipeline investments, and BC

Transmission

Improvement Program, additional generation and gas pipeline investments, and BC

Transmission

$3.6 B

$3.3 B

$3.0 B

$3.0 B

Capital Expenditure Outlook

8

* Projected 2008-2011 rate base is not adjusted for the impact of the carrying cost credit that primarily results from the second series of the Energy

Recovery Bonds. Earnings will be reduced by an amount equal to the deferred tax balance associated with the Energy Recovery Bonds regulatory

asset, multiplied by the Utility's equity ratio and by its equity return. This rate base offset carrying cost declines to zero when the taxes are fully paid

in 2012.

Recovery Bonds. Earnings will be reduced by an amount equal to the deferred tax balance associated with the Energy Recovery Bonds regulatory

asset, multiplied by the Utility's equity ratio and by its equity return. This rate base offset carrying cost declines to zero when the taxes are fully paid

in 2012.

Weighted Average Annual Rate Base*

$18.3

$20.4

$22.1

$23.9

0.0

5.0

10.0

15.0

20.0

25.0

30.0

2008

2009

2010

2011

$ B

Rate Base Growth

9

§ Steam Generator Replacement

§ $700 MM approved capital investment

§ Unit 2 replacement completed in 69 days earlier this year

§ Unit 1 replacement scheduled for early 2009

Current Rate Base:

Diablo Steam Generator Replacement

Diablo Steam Generator Replacement

10

Current Rate Base:

Gateway Generating Station

Gateway Generating Station

§ More than 90% complete

§ Testing phase begun

§ On budget, on time

§ Begins operations 1Q 2009

11

Colusa

657 MW

Gateway

530 MW

Humboldt

163 MW

Current Rate Base:

New Generation - Colusa & Humboldt

New Generation - Colusa & Humboldt

§ Colusa Generating Station

§ All permits received and cleared

§ Construction started in early October

§ Cost cap is $673 MM

§ Humboldt Repowering Project

§ Final approvals for site demolition received

§ Construction began early November

§ Cost cap is $239 MM

§ Strategy for execution on both projects

mirrors successes at Gateway

mirrors successes at Gateway

§ Experienced project teams in place

12

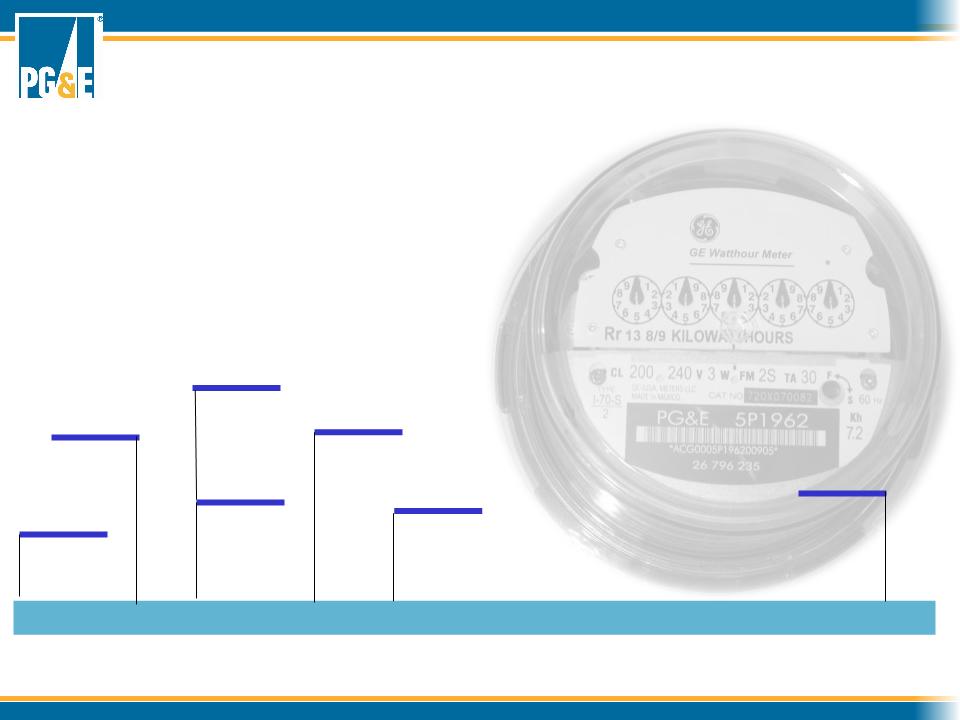

* 2008 to 2011 estimates are based on forecasted construction schedules and additional contracted resources

2007 2008 2009 2010 2011 2012

1st meter

installed

11/06

11/06

Billing IT infrastructure

live 2Q 2007

Live AMI billing

12/07

SmartMeterTM

Upgrade Filing

12/07

12/07

Demand Response

Interval Billing Live

05/08

05/08

Upgrade technology

installation 4Q 08

Deployment (incl.upgrade)

complete 1Q 2012

Current Rate Base: SmartMeterTM Program

§ Year-end 2008 target: 1.5 million meters installed

- 1,300,000 meters currently installed

- Over 1 million meters being read electronically

13

Additional CapEx

Proposed Projects Above 2008-2011 Base CapEx

Forecast

Forecast

§ SmartMeterTM Program Upgrade

§ $460 MM capital

§ Approval expected around year-end 2008

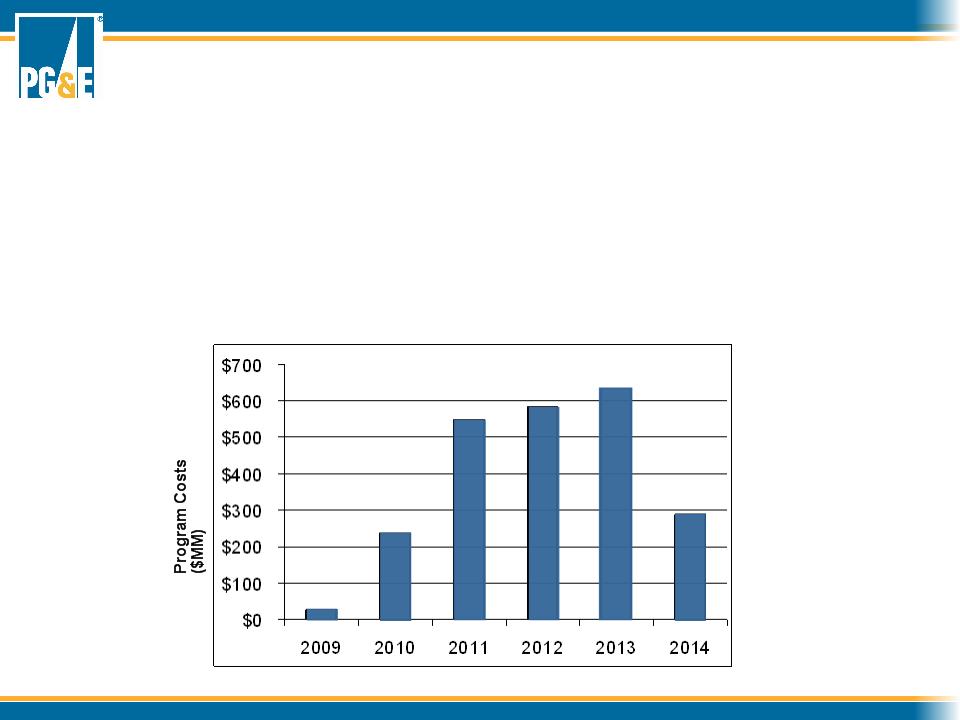

§ Cornerstone Improvement Program (Enhanced Reliability Investment)

§ $800 MM capital 2008-2011

§ $1.5 B capital investment beyond 2011

§ BC Transmission

§ Recovery of costs approved by FERC

§ Working on multi-utility partnership for development of the project

§ $5+ B in forecasted capital costs, with PG&E’s share at 51% or greater

§ New Generation

§ RFO for 2006-2016 period issued April 2008 for 800 - 1200 MW

§ Renewable investment opportunities

§ Pacific Connector LNG Pipeline

§ ~$50 MM capital 2008-2011

§ FERC approval expected by 3Q 2009

14

Additional CapEx:

SmartMeterTM Program Upgrade

SmartMeterTM Program Upgrade

§ Funding request of $572 MM

- $463 MM additional capital

§ CPUC decision expected around year-end

§ New capabilities

- Integrated connect/disconnect switches

- Solid state meter technology

- Home area network gateway device

15

PG&E seeking CPUC approval for a six-year program to improve

reliability of our electric distribution system.

reliability of our electric distribution system.

§ Enhances overall reliability of energy delivery

§ Increases grid flexibility to mitigate outages

§ Sets higher performance expectations as measured by a proposed set of metrics

$2.3B total capital investment with revenue requirement true-up

Additional CapEx:

Cornerstone Improvement Program

Cornerstone Improvement Program

16

(1) Pacific Gas and Electric Company issued $600 million of senior notes in March 2008 and an additional $600 million of senior notes in October 2008

Financing Plan 2008-2011

Objective: Ensure adequate liquidity to fund operations and capital growth

• Strong financial profile that will support growth plan

• Ensure adequate liquidity

Pacific Gas and Electric Company Financings

• Maintain authorized capital structure with 48% debt/preferred and 52% equity components

• Additional(1) $3.5 - $4.0 billion of long-term debt projected through 2011

• Total equity contribution of $1.1 - $1.7 billion by PG&E Corporation projected from 2009 through

2011

2011

PG&E Corporation Financings

• Estimate that PG&E Corporation partially funds equity contributions by issuing $100-$200

million of common stock annually through internal programs (e.g. DRSPP and 401k)

million of common stock annually through internal programs (e.g. DRSPP and 401k)

• Balance of equity contributions funded through additional equity issuances and incremental

parent debt

parent debt

• Additional parent debt capacity: $300 - - $500 million, depending on market conditions

17

Financial Assumptions 2008-2011

§ Capital expenditure base forecast reflects projects that

are highly likely or already approved

are highly likely or already approved

§ CPUC authorized ROE is 11.35% and Utility earns at

least 12% at FERC on projected rate base

least 12% at FERC on projected rate base

§ Ratemaking capital structure maintained at 52% equity

§ Additional capital expenditures, CEE incentives, and

operational efficiencies consistent with earnings targets

operational efficiencies consistent with earnings targets

§ Resolution of FERC generator claims in 2009-2011

results in financing needs

results in financing needs

§ Timely return to stable capital markets

18

2008

Business

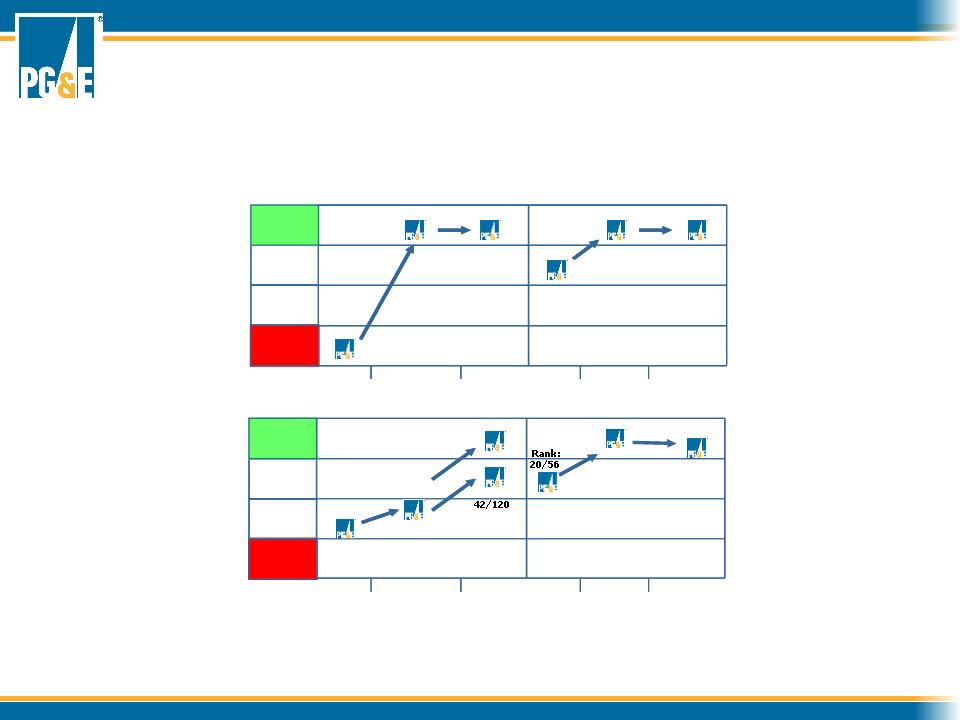

Overall Customer

Satisfaction Index

Note: Residential data released in July (Electric) and September (Gas); Business data released in February (Electric) and March (Gas)

* Residential Electric Study switched from a telephone to an online survey in 2008 and expanded to cover 120 utilities that serve 125,000 or more residential electric customers.

JD Power also provided rankings for a subset of the 58 large utilities that serve at least 500,000 residential electric customers

JD Power also provided rankings for a subset of the 58 large utilities that serve at least 500,000 residential electric customers

Residential

Overall Customer

Satisfaction Index

Electric Customers

Gas Customers

3

rd

Quartile

2

nd

Quartile

2006

2007

2006

2007

2008

2008

Rank:

2/55

Rank:

46/51

Rank:

4/38

Rank:

11/37

Rank:

2/40

Rank:

11/56

3

rd

Quartile

2

nd

Quartile

Rank:

51/76

Rank:

43/76

Rank:

5/56

2006

2007

2006

2007

2008

2008

Rank:

15/58

Rank:

*

Electric Customers

Gas Customers

Bottom

Quartile

3

rd

Quartile

2

nd

Quartile

Top

Quartile

2006

2007

2006

2007

2008

2008

Rank:

2/55

Rank:

46/51

Rank:

4/38

Rank:

11/37

Rank:

2/40

Rank:

11/56

Bottom

Quartile

3

rd

Quartile

2

nd

Quartile

Top

Quartile

Rank:

51/76

Rank:

43/76

Rank:

5/58

2006

2007

2006

2007

2008

Rank:

15/58

Rank:

*

Rank:

11/60

Customer Satisfaction Performance

19

Case | Docket # | Expected Decision Date |

CEMA | A. 08-03-017 | Q4 2008 |

SmartMeterTM Upgrade Program | A. 07-12-009 | Q4 2008 |

Energy Efficiency Programs | R.06-04-010 D. 07-09-043 D.08-01-042 | Q4 2008 |

Direct Access § Phase 1 - Legal Issues § Phase 2a - DWR Contracts § Phase 2b - Merit § Phase 3 - Rules | OIR: Q2 2007 | 2/29/08 Q4 2008 TBD TBD |

AB 32 Implementation • CARB Scoping Plan • Implementation (regulations in effect) | AB 32 signed 9/2006 | 1/1/2009 1/1/2012 |

Hydro Divestiture | A. 08-05-023 | 2009 |

Transmission Owners Rate Case 11 | ER08-1318-000 | Q3 2009 |

Reserve Margin | R. 08-04-012 | Q3 2009 |

2011 General Rate Case | August 2009 (NOI) | Q4 2010 |

Cornerstone Improvement Program | A. 08-05-023 | TBD |

Key Regulatory Proceedings

Appendix

21

(1) Authorized revenues = operating costs + (rate of return x rate base)

Rate base = net plant ± adjustments to approximate invested capital

Business Scope |

§ Retail electricity and natural gas distribution service (construction, operations and maintenance) § Customer services (call centers, meter reading, billing) § 5.1 million electric and 4.3 million gas customer accounts |

Primary Assets |

§ $11.0 billion of rate base (2007 wtd. avg.) |

Regulation |

§ California state regulation (CPUC) § Cost of service ratemaking (1) |

Electric And Gas Distribution

22

Midway

Los Banos

Moss Landing

Diablo Canyon

Gates

Dixon

Malin

Round Mt

Vaca

Business Scope |

§ Wholesale electric transmission services (construction, maintenance) § Operation by CA Independent System Operator |

Primary Assets |

§ $2.6 billion of rate base (2007 wtd. avg.) |

Regulation |

§ Federal regulation (FERC) § Cost of service ratemaking § Revenues vary with system load |

23

Business Scope |

§ Natural gas transportation, storage, parking and lending services § Customers: PG&E natural gas distribution and electric generation businesses, industrial customers, California electric generators |

Primary Assets |

§ $1.5 billion of rate base (2007 wtd. avg.) |

Regulation |

§ California state regulation (CPUC) § Incentive ratemaking framework (“Gas Accord”) § Revenues vary with throughput |

Natural Gas Transmission

24

Business Scope |

§ Electricity and ancillary services from owned and controlled resources § Energy procurement program |

Primary Assets |

§ $1.7 billion of rate base (2007 wtd. avg.) § Diablo Canyon nuclear power plant (2,240 MW) § Largest privately owned hydro system (3,896 MW) § Funded nuclear plant decommissioning trusts of $1.8 billion |

Regulation |

§ Cost of service ratemaking for utility-owned generation § Pass through of power procurement costs |

Electric Procurement & Owned Generation

25

Year Signed | Project | Max GWh/yr | Technology |

2006 | Military Pass Rd. | 840 | Geothermal |

2006 | HFI Silvan | 142 | Biomass |

2006 | Liberty Biofuels | 70 | Biofuels |

2006 | Bottle Rock USRG | 385 | Geothermal |

2006 | IAE Truckhaven | 366 | Geothermal |

2006 | Global Common - Chowchilla | 72 | 2006 |

2006 | Global Common - El Nido | 72 | Biomass |

2006 | Newberry | 840 | Geothermal |

2006 | Calpine Geysers | 922 | Geothermal |

2006 | Tunnel Hydro | 2.1 | Hydro |

2006 | Buckeye Hydro | 1.4 | Hydro |

2006 | Eden Vale Dairy | 1.3 | Biogas |

2006 | Microgy | TBD | Biogas |

2006 | Bio_Energy LLC | TBD | Biogas |

2006 | Palco | 36 | Biomass |

Year Signed | Project | Max GWh/yr | Technology |

2007 | Solel | 1388 | Solar Thermal |

2007 | PPM-Klondike | 265 | Wind |

2007 | CalRenew | 9 | PV |

2007 | Green Volts | 5 | PV |

2007 | enXco | 509 | Wind |

2007 | Ausra | 388 | Solar Thermal |

2008 | Calpine | 500 | Geothermal |

2008 | Wadham | 141 | Biomass |

2008 | BrightSource | 1230 | Solar Thermal |

2008 | San Joaquin Solar | 700 | Solar Thermal- Biofuel Hybrid |

2008 | Arlington Wind (Horizon) | 240 | Wind |

2008 | OptiSolar | 1148 | PV |

2008 | SunPower | 594 | PV |

2008 | Iberdrola / BPA Klla | 260 | Wind |

* Based on contracts signed through October 2008

1) Average delivered energy over multiple years: pre-RPS baseline

Over 24% of Projected Load Currently Signed*

Renewable Contracts Signed

26

* Earnings per share from operations is a non-GAAP measure. This non-GAAP measure is used because it allows

investors to compare the core underlying financial performance from one period to another, exclusive of items that do not

reflect the normal course of operations.

investors to compare the core underlying financial performance from one period to another, exclusive of items that do not

reflect the normal course of operations.

EPS on an Earnings from Operations Basis | $2.78 |

Items Impacting Comparability | 0.00 |

EPS on a GAAP Basis | $2.78 |

2007

2007 EPS - Reg G Reconciliation

27

2008 | ||

Low | High | |

EPS Guidance on an Earnings from Operations Basis* Estimated Items Impacting Comparability** Estimated EPS on a GAAP Basis | $2.90 0.66 $3.56 | $3.00 0.69 $3.69 |

2009 | ||

Low | High | |

EPS Guidance on an Earnings from Operations Basis* Estimated Items Impacting Comparability Estimated EPS on a GAAP Basis | $3.15 0.00 $3.15 | $3.25 0.00 $3.25 |

* Earnings per share from operations is a non-GAAP measure. This non-GAAP measure is used because it allows investors to compare the core underlying financial performance from one period to another, exclusive of items that do not reflect the normal course of operations. ** Estimated amount of income to be recognized in the fourth quarter of 2008 in connection with the recent settlement of 2001-2004 tax audits. | ||

Guidance Range

Guidance Range

EPS Guidance -Reg G Reconciliation