1

Exhibit 99

PG&E Corporation:

Opportunities in Renewable Energy

Investor Meetings

Morgan Stanley

Electric Utilities Corporate Access Day

October 9, 2007 - Chicago, IL

2

This presentation contains forward-looking statements regarding management’s guidance for PG&E Corporation’s 2007 and 2008 earnings per share from operations, targeted average annual

growth rate for earnings per share from operations, as well as management’s projections regarding Pacific Gas and Electric Company’s (Utility) capital expenditures, rate base and rate base

growth, future electricity resources, and potential investments in transmission, generation and renewable energy resources. These statements are based on current expectations and various

assumptions which management believes are reasonable, including that substantial capital investments are made in Utility business over the 2007-2011 period, Utility rate base averages $17

billion in 2007 and $18.7 billion in 2008, that the Utility earns at least its authorized rate of return on equ ity, and that the Utility’s ratemaking capital structure is maintained at 52 percent equity.

These statements and assumptions are necessarily subject to various risks and uncertainties, the realization or resolution of which are outside of management's control. Actual results may

differ materially. Factors that could cause actual results to differ materially include:

•Utility’s ability to timely recover costs through rates;

•the outcome of regulatory proceedings, including ratemaking proceedings pending at the California Public Utilities Commission (CPUC) and the Federal Energy Regulatory

Commission;

•the adequacy and price of electricity and natural gas supplies, and the ability of the Utility to manage and respond to the volatility of the electricity and natural gas markets;

•the effect of weather, storms, earthquakes, fires, floods, disease, other natural disasters, explosions, accidents, mechanical breakdowns, acts of terrorism, and other events or hazards

that could affect the Utility’s facilities and operations, its customers, and third parties on which the Utility relies;

•the potential impacts of climate change on the Utility’s electricity and natural gas business;

•changes in customer demand for electricity and natural gas resulting from unanticipated population growth or decline, general economic and financial market conditions, changes in

technology including the development of alternative energy sources, or other reasons;

•operating performance of the Utility’s Diablo Canyon nuclear generating facilities (Diablo Canyon), the occurrence of unplanned outages at Diablo Canyon, or the temporary or

permanent cessation of operations at Diablo Canyon;

•the ability of the Utility to recognize benefits from its initiatives to improve its business processes and customer service;

•the ability of the Utility to timely complete its planned capital investment projects;

•the impact of changes in federal or state laws, or their interpretation, on energy policy and the regulation of utilities and their holding companies;

•the impact of changing wholesale electric or gas market rules, including the California Independent System Operator’s new rules to restructure the California wholesale electricity

market;

•how the CPUC administers the conditions imposed on PG&E Corporation when it became the Utility’s holding company;

•the extent to which PG&E Corporation or the Utility incur costs and liabilities in connection with pending litigation that are not recoverable through rates, from third parties, or through

insurance recoveries;

•the ability of PG&E Corporation and/or the Utility to access capital markets and other sources of credit;

•the impact of environmental laws and regulations and the costs of compliance and remediation;

•the effect of municipalization, direct access, community choice aggregation, or other forms of bypass, and

•other risks and factors disclosed in PG&E Corporation’s SEC reports.

Cautionary Statement Regarding Forward-Looking

Information

3

Key Takeaways From Today’s Discussion

•PCG is a core utility holding delivering 1st quartile

earnings growth at low risk.

•PG&E is aligned with regulators/policy leaders to

increase the supply of cost-effective renewable

generation.

•Evolving renewables policy creates attractive

investment opportunities.

4

Agenda for Today

•PG&E’s core investment strategy and upside earnings

outlook

•PG&E’s position on renewable energy

-Current position

-Future investment opportunities

5

Investment Driver | Cap Ex | Notable Projects |

Common Plant | ~$1.3 Billion | •Building Investment •Technology Infrastructure •General Use Fleet |

Electric and Gas Transmission | ~$3.8 Billion | •Central California Clean Energy Transmission Line ( formerly Midway-Gregg) •Line Upgrades for Renewables •McDonald Island Gas Storage Pipeline |

Generation | ~$2.9 Billion | •Gateway Generating Station •Humboldt Power Plant •Colusa Power Plant •DCPP Steam Generator Replacement |

Distribution | ~$6.2 Billion | •Distribution maintenance and upgrades •New Customer Connections •AMI |

2007-2011 Estimated CapEx totals more than $14 B (~$2.8 B/yr.)

Capital Expenditures Drive Core Growth

6

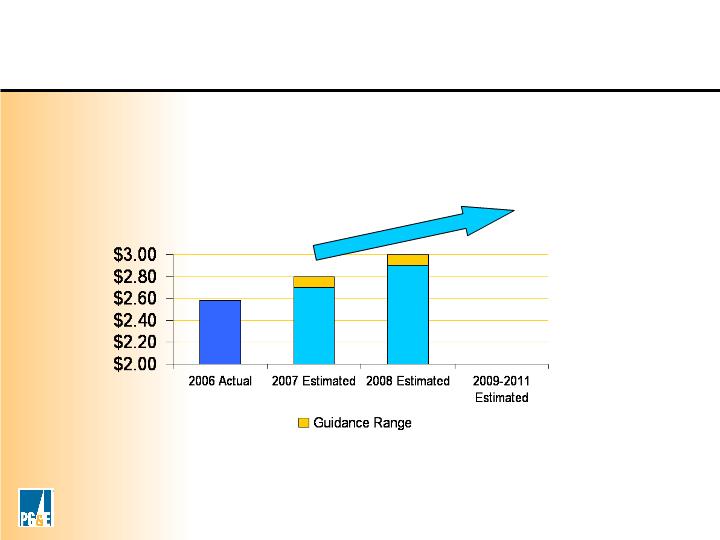

* Reg G reconciliation to GAAP for 2006 EPS from Operations and 2007 and 2008

EPS Guidance available in Appendix and at www.pgecorp.com

EPS from Operations*

EPS Guidance

EPS from Operations*: 2007 guidance of $2.70-$2.80 per share

2008 guidance of $2.90-$3.00 per share

8%

7

Additional Investment Opportunities Provide Upside

•Proposed Pacific Connector Gas Pipeline (PCGP)

-1.0 -1.5 Bcf/d, 230 mile LNG pipeline

-$1.1 B (33% PG&E share)

•2006 Long Term Procurement Plan

-Up to 2,300 MW proposed post-2011

•Potential BC Renewables Transmission Project

-$14 M approved to study feasibility

-Coordination between BC, WA, OR, CA

-Q1 2008 - Report to CPUC

•PG&E Owned Renewables

8

Biomass Energy

Wind Energy

Small Hydropower (<30MW)

Geothermal Energy

RPS Eligible Renewable Resources - Traditional

9

Biogas

Ocean Power

Central Solar Energy

~

Eligible Renewables - Emerging

10

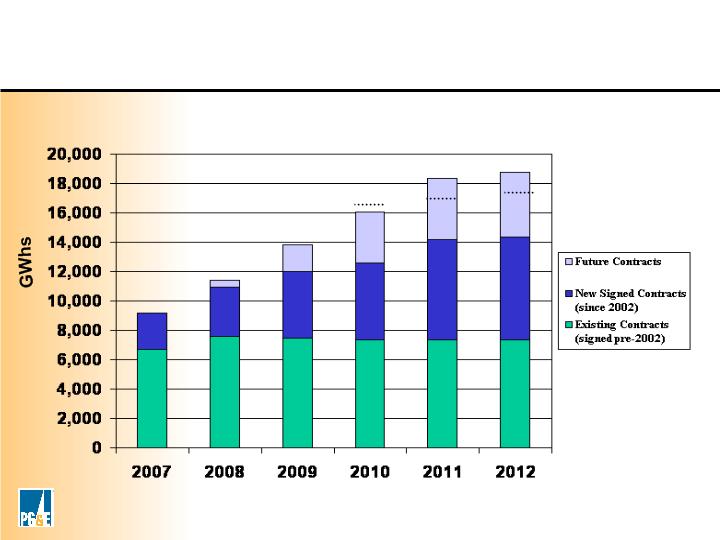

Year Signed | Project | Max GWh/yr | Technology |

Pre 2002 | Various Projects | ~7500 1 | Various |

2002 | Calpine Geysers 13 & 20 | 722 | Geothermal |

2002 | Wheelabrator #4 | 25 | Biomass |

2003 | CBEA Projects (3) | 305 | Biomass |

2004 | Big Valley Lumber | 41 | Biomass |

2004 | Diablo Winds | 65 | Wind |

2005 | FPL Energy-Montezuma Winds | 102 | Wind |

2005 | Buena Vista Energy LLC | 108 | Wind |

2005 | Pacific Renewable Energy | 280 | Wind |

2005 | Shiloh 1 Wind Project LLC | 225 | Wind |

2006 | Military Pass Rd. | 840 | Geothermal |

2006 | HFI Silvan | 142 | Biomass |

2006 | Liberty Biofuels | 70 | Biofuels |

2006 | Bottle Rock USRG | 385 | Geothermal |

2006 | IAE Truckhaven | 366 | Geothermal |

2006 | Global Common - Chowchilla | 72 | Biomass |

Year Signed | Project | Max GWh/yr | Technology |

2006 | Global Common - El Nido | 72 | Biomass |

2006 | Newberry | 840 | Geothermal |

2006 | Calpine Geysers | 922 | Geothermal |

2006 | Tunnel Hydro | 2.1 | Hydro |

2006 | Buckeye Hydro | 1.4 | Hydro |

2006 | Eden Vale Dairy | 1.3 | Biogas |

2006 | Microgy | TBD | Biogas |

2006 | Bio_Energy LLC | TBD | Biogas |

2006 | Palco | 36 | Biomass |

2007 | Solel | 1388 | Solar Thermal |

2007 | Western GeoPower | 212 | Geothermal |

2007 | PPM-Klondike | 265 | Wind |

2007 | CalRenew | 9 | PV |

2007 | Green Volts | 5 | PV |

18% of Projected 2010 Load Currently Signed*

*Based on contracts signed through August 2007

1) Average delivered energy over multiple years: pre-RPS baseline

PG&E’s Renewable Contracts Signed

11

Year

18%

15%

12%

19%

Expected Deliveries From Contracts

20%

20%

Renewable Portfolio Standard target is 20% by 2010*

* See Appendix for further description of RPS requirements

PG&E’s RPS Compliance Outlook

12

Challenges to Meeting RPS Goal

•Increasing competition for renewables projects from other

states/countries/utilities

•Many renewable resources are located in areas requiring either

new transmission or transmission upgrades

•Uncertain whether contracts will perform as projected

•System integration of intermittent resources becomes more

challenging at higher volumes

13

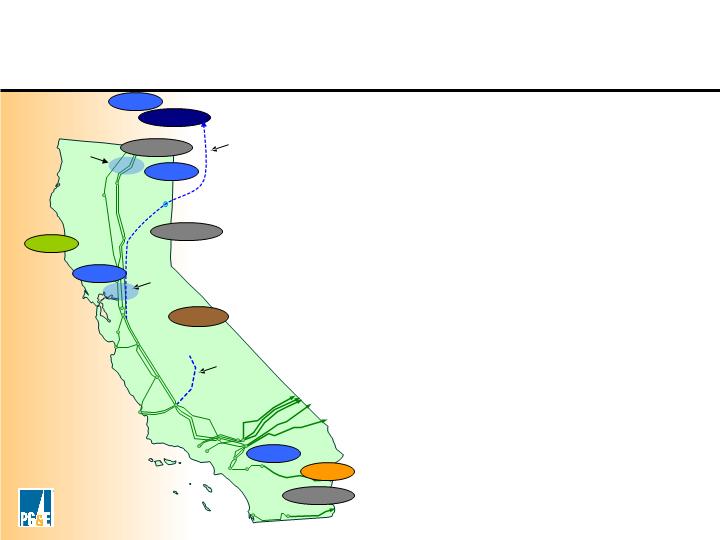

Wind

Transmission Line Project | Renewable Resources | |

1 | Central California Clean Energy Transmission (previously Midway-Gregg) | Resources to the south |

2 | Vaca Dixon - Contra Costa Upgrade | Solano County wind resources |

3 | California - Oregon Upgrade | Renewable resources from the Pacific Northwest |

4 | B.C. Renewable Line (possible) | Proposed to bring British Columbia renewable resource energy to California |

4

1

3

2

Bioenergy

Ocean

Solar

Geothermal

Geothermal

Geothermal

Small Hydro

Wind

Wind

Wind

New Transmission Investment is Necessary

14

Increasing opportunities for utilities in renewable development

Renewable Investment Landscape

•Renewable Provisions in Federal Energy Bill

-PTC (Wind, Biomass, Geothermal, Hydro, Solid Waste)

-ITC (Solar, Geothermal, Distributed Generation)

-Federal Renewable Portfolio Standard (RPS)

•PG&E’s 2007/2008 solicitation open to offers for utility

ownership

•CPUC provides incentive ROE on utility-owned renewables

15

PG&E Investment Opportunities

•PG&E is in the early stages of feasibility analysis

•Includes system-wide survey of land holdings and

assets for renewable potential

•Technologies include wind, solar and small hydro

16

PCG Value Summary

•PG&E is a core holding, delivering strong

investment opportunities and low risk.

•Renewables and related transmission investments

provide potential earnings “upsides” in 2008 and

beyond which are not currently included in long-term

guidance.

17

Appendix

18

Business Unit | 2006 Rate Base ($B) | Regulation |

Electric and gas distribution | $10.3 | CPUC |

Electric generation | $1.8 | CPUC |

Gas transmission | $1.5 | CPUC |

Electric transmission | $2.3 | FERC |

PCG Total Business | $15.9 | 85% CPUC/15% FERC |

Pacific Gas and Electric Company (PG&E)

•$12.5 B in Revenues

•$34.8 B in Assets

•5.1 MM Electric/4.2 MM Gas Customers

•$16 B+ Market Capitalization

19

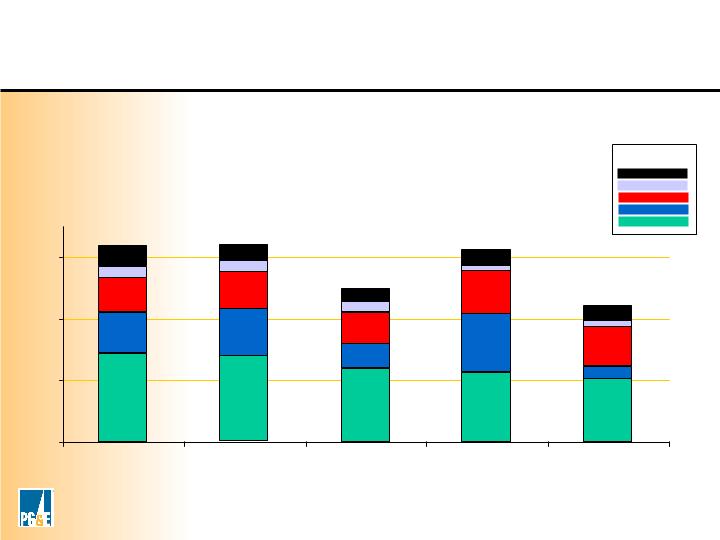

Projected Capital Expenditures ($MM)

Common Plant

Gas Trans.

Electric Trans.

Generation

Distribution

Chart Key

0

$1,000

$2,000

$3,000

2007

2008

2009

2010

2011

$3,200

$3,200

$2,500

$3,100

$2,200

Capital Expenditure Outlook

20

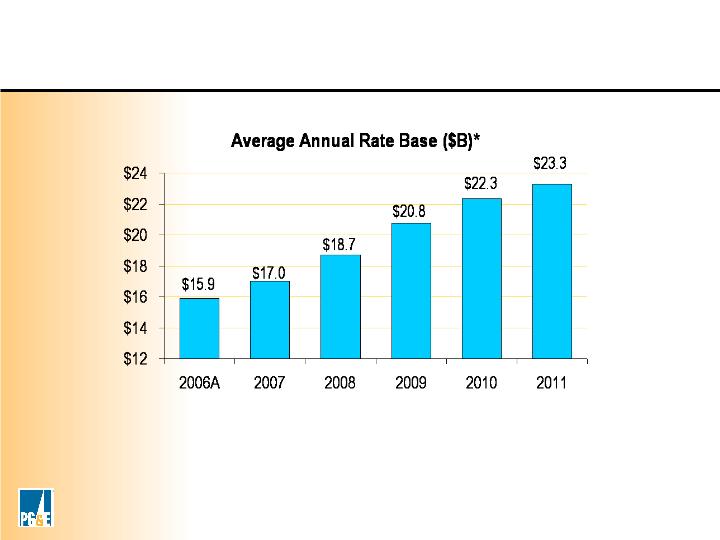

* Projected 2007-2011 rate base is not adjusted for the impact of the carrying cost credit that primarily results from

the second series of the Energy Recovery Bonds. Earnings will be reduced by an amount equal to the deferred tax

balance associated with the Energy Recovery Bonds regulatory asset, multiplied by the utility's equity ratio and by its

equity return. The carrying cost credit declines to zero when the taxes are fully paid in 2012.

Rate Base Growth

21

2006 | |

EPS on an Earnings from Operations Basis* | $2.57 |

Items Impacting Comparability: | |

Scheduling Coordinator Cost Recovery Environmental Remediation Liability Recovery of Interest on PX Liability Severance Costs EPS on a GAAP Basis | 0.21 (0.05) 0.08 (0.05) $2.76 |

*Earnings per share from operations is a non-GAAP measure. This non-GAAP measure is used

because it allows investors to compare the core underlying financial performance from one period to

another, exclusive of items that do not reflect the normal course of operations

2006 EPS - Reg G Reconciliation

22

2007 EPS Guidance on an Earnings from Operations Basis* Estimated Items Impacting Comparability EPS Guidance on a GAAP Basis | Low $2.70 0.00 $2.70 | High $2.80 0.00 $2.80 |

2008 EPS Guidance on an Earnings from Operations Basis* Estimated Items Impacting Comparability EPS Guidance on a GAAP Basis | Low $2.90 0.00 $2.90 | High $3.00 0.00 $3.00 |

* Earnings per share from operations is a non-GAAP measure. This non-GAAP measure is used because it allows

investors to compare the core underlying financial performance from one period to another, exclusive of items that do not

reflect the normal course of operations.

EPS Guidance - Reg G Reconciliation

23

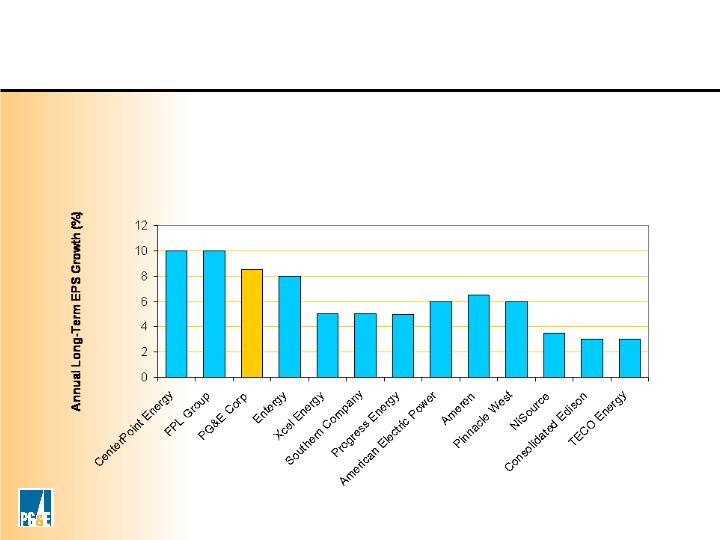

Consensus of analyst estimates of EPS growth:

Source: Thomson IBIS long-term EPS Growth Consensus Estimate Median October 1, 2007

EPS Growth - Comparator Group

EPS from operations annual growth targeted to average 8% for

2007 - 2011

24

Mandate | •Deliveries of 20% of load from eligible renewables by 2010. Large hydro (>30 MW) doesn’t qualify. |

Purpose | •Fuel Diversity •GHG Reduction •Economic Development |

Penalty | •$50/MWhr, up to $25 million per year |

Exceptions | 1)Contract failure 2)Insufficient public goods funds 3)Insufficient offers 4)Lack of transmission |

Flexible Compliance | •Allows shortfalls to be made up within following three years. |

California’s RPS Program

25

RPS Procurement Process

•PG&E conducts annual renewable RFOs, targeting 1 - 2% increases in

supply

•Projects are evaluated on:

§Market value

§Creditworthiness

§Transmission availability

§Portfolio fit

§Commercial and technical feasibility

•Bilateral contracts allow PG&E to negotiate unique renewable

opportunities outside the RFO process. Projects are evaluated against the

same metrics.

•PG&E continually examines new opportunities for utility ownership both via

the RFO process and outside it.

26

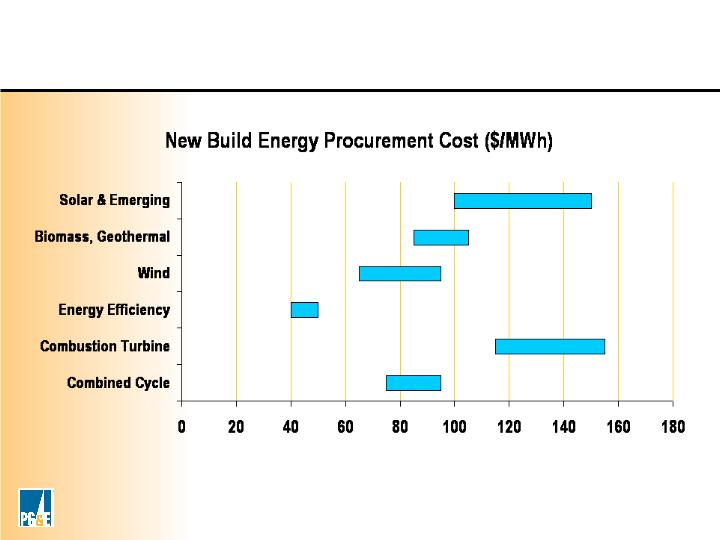

Illustrative Energy Procurement Costs

27

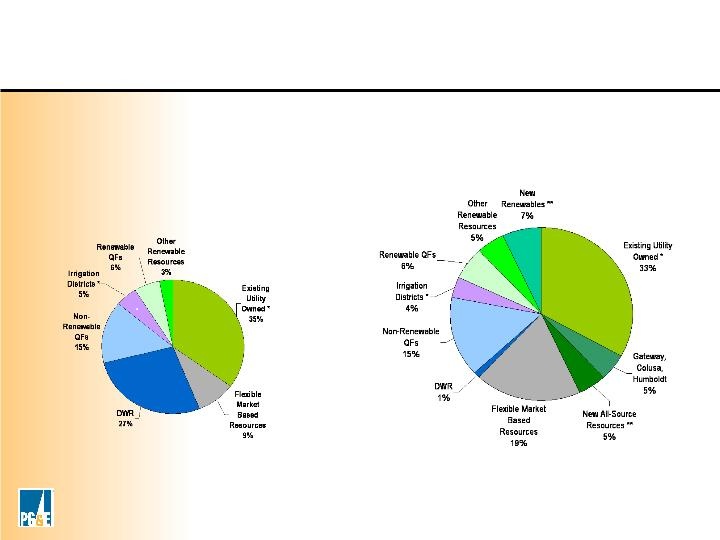

* Over 20% of total retail sales expected to be eligible renewable resources coming from

utility-owned, QFs, Irrigation Districts, and other sources.

** May include utility-owned resources.

* Approximately 13% of total retail sales expected to be eligible renewable resources

coming from utility-owned, QFs, Irrigation Districts and other sources.

2007 Projected Sources of Energy

85,500 GWh

2012 Projected Sources of Energy

89,900 GWh

•Energy efficiency expected to meet half of future load growth

•Growth in renewable resources and resources with operating flexibility

•Growth in utility ownership

Long-Term Electricity Resources