Interchange

Financial Services

Corporation

America’s Community Bankers Conference

San Francisco, February 21-22, 2006

1

Forward Looking Statement

In addition to discussing historical information, certain statements included in or incorporated into

this report relating to the financial condition, results of operations and business of the Company,

which are not historical facts may be deemed “forward-looking statements” within the meaning of the

Private Securities Litigation Reform Act of 1995. When used herein, the words “anticipate,”

“believe,” “estimate,” “expect” and other similar expressions (including when preceded or followed by

the word “not”) are generally intended to identify such forward-looking statements. Such statements

are intended to be covered by the safe harbor provisions for forward-looking statements contained in

such Act, and we are including this statement for purposes of invoking these safe harbor provisions.

Such forward-looking statements include, but are not limited to, statements about the operations of

the Company, the adequacy of the Company’s allowance for losses associated with the loan and lease

portfolio, the quality of the loan and lease portfolio, the prospects of continued loan and deposit

growth, and improved credit quality. The forward-looking statements in this report involve certain

estimates or assumptions, known and unknown risks and uncertainties, many of which are beyond the

control of the Company, and reflect what we currently anticipate will happen in each case. What

actually happens could differ materially from what we currently anticipate will happen due to a

variety of factors, including, among others, (i) increased competitive pressures among financial

services companies; (ii) adverse changes in Government-Sponsored Enterprises (the “GSE”) status or

financial condition impacting the GSE’s guarantees or ability to pay or issue debt; (iii) changes in

the interest rate yield curve such as flat, inverted or steep yield curves, or interest rate

environment which impact interest margins and may impact prepayments on the mortgage-backed securities

portfolio; (iv) changes in consumer spending, borrowing and saving habits; (v) technological changes,

(vi) deterioration in general economic conditions, internationally, nationally, or in the State of New

Jersey; (vii) disruptions caused by terrorism, such as the events of September 11, 2001, or military

actions in the Middle East or other areas; (viii) legislation or regulatory requirements or changes

adversely affecting the business of the Company; and (ix) other risks detailed in reports filed by the

Company with the Securities and Exchange Commission. Readers should not place undue expectations on

any forward-looking statements. We are not promising to make any public announcement when we consider

forward-looking statements in this document to be no longer accurate, whether as a result of new

information, what actually happens in the future or for any other reason.

2

A diversified financial services holding company:

Principal subsidiary is Interchange Bank (since 1969)

Total Assets: $1.6 Billion

Total Loans and leases: $1.1 Billion

Market Cap: $378 million (As of 2/14/05)

Book Value per Share: $8.89

3

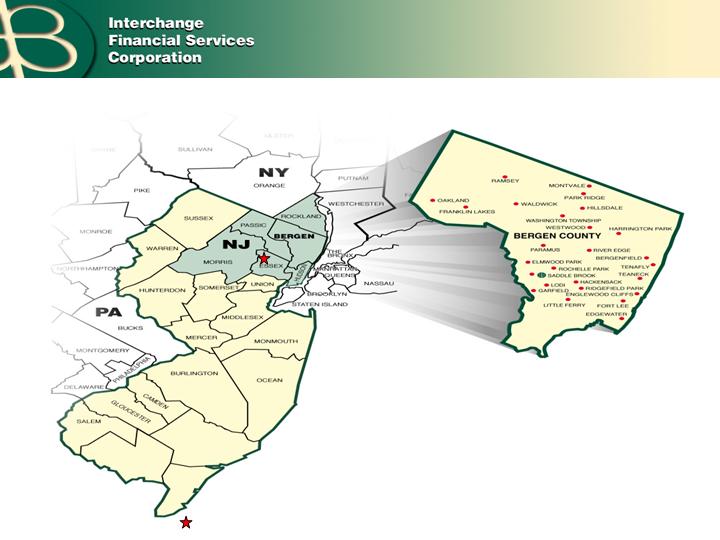

Markets Served

Bergen County Demographics

Total Population: 901,514

Businesses: 42,785

Households: 337,645

Median Household Income: $ 70,957

Median House Price: $448,100

Franklin Bank acquisition in Nutley, NJ

4

Strategic Goals

Premier Business Bank in New Jersey

To rank in the Top 100 banks in the US

(based on total assets)

Strong and consistent profitability

Continue to build shareholder value

5

Business Lending contributes approximately

40% of the Company’s pretax earnings

Planned growth of 15% to 20% annually

Restructured and expanded our Business

Banking platform

Streamlined lending and credit administration

Implemented specialized lending units and

lending teams

Business development programs

Attract and retain talented loan officers

Focus on Business Banking

6

Business Banking

Commercial

Real Estate

Capital

Financing

Commercial &

Industrial Loans

SBA/ EDA

Loans

Small

Business

Loans

Equipment

Leasing

Compensating

Balances

Construction

Lending

Business

Banking

Asset Based

Lending

7

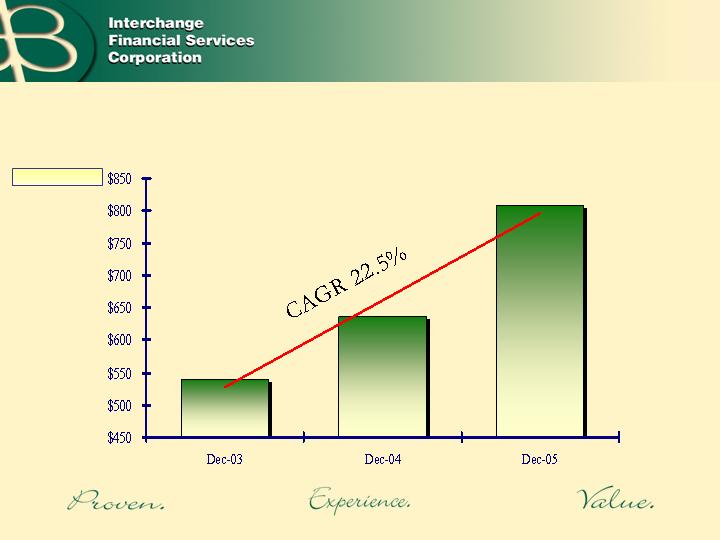

Business Banking

(In Millions)

Commercial loans represents 73% of total loans at 12/05 as compared to

45% at 12/98 (Objective 70%)

8

A strong core deposit base drives profitability

87% of earning assets are funded by deposits

Strong core deposit mix…low cost of funds

Non-interest bearing demand 21%

Non-maturity deposits 75%

Creates a competitive advantage

Loyal core customer base

Balance Sheet (Funding)

9

On average, our customers have been with us for 12-13 years

65% of the Bank’s customer households have been with us

over 5 years

81% of current customers consider us their primary bank

77% of our customers rated us in the top 30th percentile

Bank customers rated us much higher than non-customers

rated their own banks

The majority (81%) of our customers felt that Interchange

was a stable and solid financial company and was a one stop

shop for all their banking needs.

Customer Loyalty

10

Core Deposit Advantage

Funding Cost Advantage To Peers

Spread benefit to peers: Interest expense as a % of total assets / Peer source: UPBR

11

Our focus remains on:

Innovating the customer experience

1.

Distinction in customer service

2.

Value of relationship

3.

Convenience

Disciplined pricing (Marginal Cost Pricing)

Core Deposit Strategies

12

Strategic Growth

Acquire whole financial companies

Purchase branches

Pursue de novo branching

Projected new denovo branches in 2006

Potential denovo branches in 2007 & 2008

Nutley, NJ

Corporate Offices (Saddle Brook, NJ)

LEGEND

13

RISK MANAGEMENT

AND FINANCIAL

OVERVIEW

14

Risk Management

We are highly focused on risk -- evaluating it to ensure that

it is either mitigated or well-balanced with the reward.

Credit Risk

Strong credit culture and policy

Independent credit administration function.

Validated by strong loan growth with minimal Commercial Loan

charge-offs.

Interest Rate Risk

Emphasis on total return

Risks are commensurate with rewards

Understanding the dynamic nature of interest rates and the effects

of prudent balance sheet management on current and future

earnings.

15

2005

Commercial loan growth of 28%

Loans to interest earning assets of 75%

ROA 1.28%

ROTE 20.37%

Financial Overview

16

Balance Sheet

($ in thousands)

17

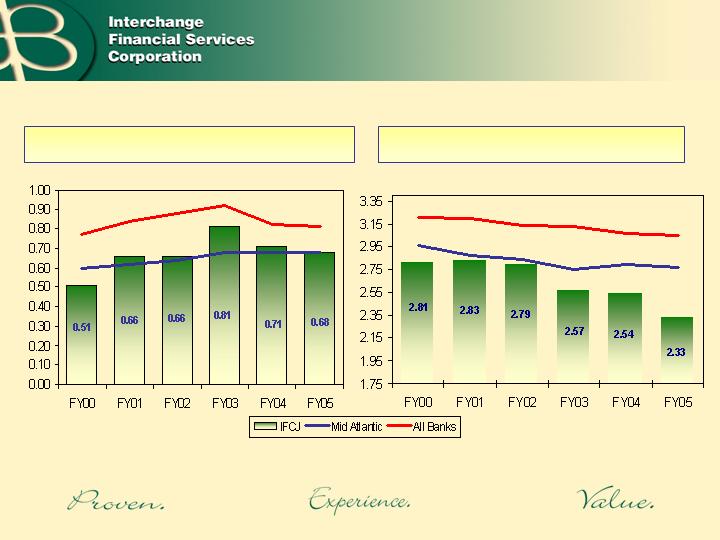

Net Interest Margin (%)

Competitive advantage: 21bp to All Banks

and 40bp to Mid Atlantic Banks

Mid Atlantic and All Banks

Data Source: SNL 9/05

18

Non-interest Income &

Expense /Average Assets (%)

Non-interest income

Non-interest expense

19

Net charge-offs % of loans

Credit Quality

20

NPA’s % of assets

Credit Quality

21

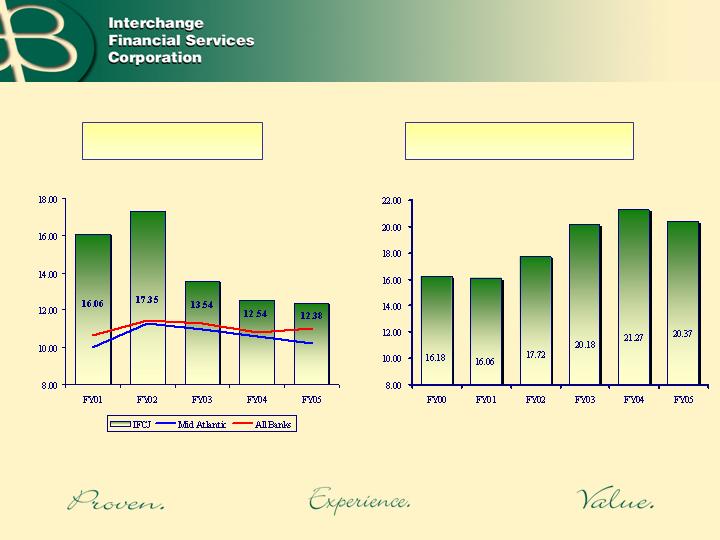

Return On Assets (%)

22

Total Equity

Tangible Equity

Return On Equity (%)

23

Diluted EPS

24

Valuable franchise in a superior market

Consistently Strong Profitability Through Varying

Economic Cycles

Uninterrupted Dividend for over 20 years

IFCJ’s value proposition has significantly exceeded major

market indices

Returning Shareholder Value

25

IFCJ – 10 Year Total

Return on Investment

8

%

1

5

As of 02/10/2006

Annual

Equivalent

of 20%.

26