1st Quarter 2009 Earnings

May 4, 2009

This presentation may contain “Forward-Looking Statements”. All

statements other than statements of historical facts made in this

presentation regarding the prospects of our industry and our

prospects, plans, financial position and business strategy may

constitute forward-looking statements. We can give no assurance

that these expectations will prove to be correct. Factors and risks

that could cause actual results to differ materially from our

expectations are described in the most recent SkyTerra Forms 10-Q

and 10-K, on file with the SEC.

Outline of Presentation

Alex Good – Chairman & CEO

Chipset Technology Update

Satellite Construction

Customer Sales Activity

Regulatory Initiatives and Filings

Market and Industry Perspectives

Scott Macleod – Chief Financial Officer

1Q09 Financial Results

April 1, 2009 Funding

Ownership and Capital Structure

Next-Generation Satellite System Costs

Chipset Technology Update (1)

1.

We are making steady progress on our goal of integrating satellite

capability into a range of mass-market, terrestrial-capable handsets

2.

Qualcomm’s first handset-capable LTE chipset, the MSM8960 will include our satellite air interface instead of the MSM8660

The industry is adopting the LTE protocol

The MSM8660 will not support LTE, while the MSM8960 will support LTE

The MSM8960 includes legacy CDMA and GSM-based 3G and 2G protocols

The MDM9600 will support LTE and a broad range of 3G and 2G protocols

3.

Alcatel-Lucent has been selected to develop the Satellite Base Station

Subsystem compatible with the planned Qualcomm chipsets

Chipset Development Program (2)

1.

We have added a second technology path with Infineon

2.

The Infineon/Hughes Network Systems platform:

Combines GSM-based technologies with HNS’ GMR1-3G satellite air interface

The chipset platform (the XMM SDR210) is based on Infineon’s Software

Defined Radio architecture

HNS will develop and deliver GMR1-3G Satellite Base Station Subsystem

3.

Key advantages of the two-vendor approach:

Technology flexibility

Strengthens strategic position in delivering next-generation solutions to the

broadest range of partners and market segments

Sharing costs with other ATC providers increases cost-effectiveness

Satellite Construction Program

1.

The surface for the 22-meter reflector has been fully assembled and

successfully completed several stow and deploy sequences

2.

The payload module testing has been completed and the payload module has been mated with the spacecraft bus

3.

The development and testing of the GBBF systems is continuing

4.

The launch window for SkyTerra 1 is expected to be open from March

2010 through May 2010

Customer Sales Activity

1.

As we have done with the SMARTTM talkgroup program, we continue to develop reference customers and models of operation that will be a

framework for our next-generation system

2.

Shelby County, Tennessee

In late April, we closed a significant MSAT-G2 sales order to Shelby County,

Tennessee

The buy was facilitated through Federal funding, specifically, the Urban Area

Security Initiative grant program

This model of pairing fixed installations with mobile kits is very attractive to

local governments

3.

We are focused on finalizing plans to transition current customers to our next-generation system and expect to announce shortly several

transition initiatives

4.

As we have already done with a number of private network customers,

we recently extended our existing satellite data communications services contract with Wireless Matrix

Regulatory Initiatives and Filings

1.

On March 4, 2009, Harbinger and SkyTerra asked the FCC to separate the request

for authority to transfer control of SkyTerra from the request for approval of the

possible business combination between SkyTerra and Inmarsat

2.

SkyTerra filed on April 29, 2009, an amendment to its earlier filing with the FCC

to implement ATC Reconsideration and Cooperation Agreement

3.

We continue the formal satellite coordination process with the relevant ITU-

sanctioned operators and governments

Market and Industry Perspectives

1.

Smartphone penetration is driving growth in data services revenue

2.

The significant increase in data devices and usage requires significantly more

network capacity

3.

The CTIA and third-party analysts note that mobile Internet services require

significantly more spectrum

4.

There is limited new mobile spectrum that could be cleared in the medium term,

and existing spectrum positions lack uniform availability of 10 MHz carriers

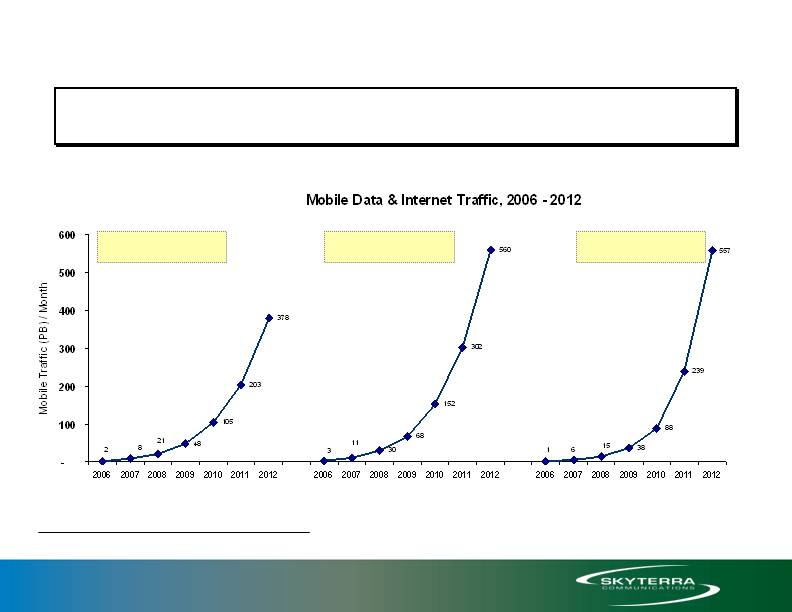

Wireless Data Usage Is Growing Exponentially

Source: Cisco IP Traffic Forecast, August 2008.

North America Europe & Japan Rest of World

Global wireless data is forecast to increase at 157% CAGR

between 2006 and 2012

2006 – 2012 CAGR

North America: 140%

2006 – 2012 CAGR

Europe & Japan: 130%

2006 – 2012 CAGR

Rest of World: 187%

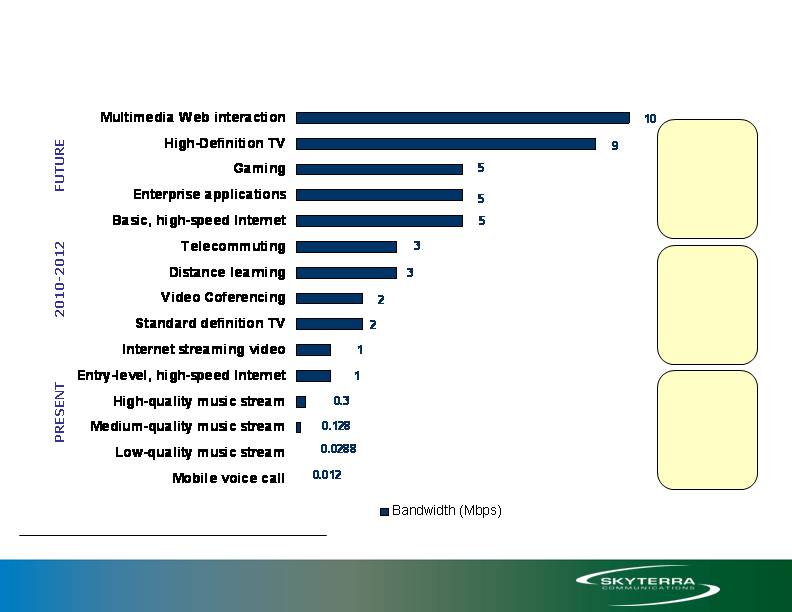

Large Bandwidth Will Be Needed to Support Next-

Generation Business Models

Mobile Access

Fixed-Mobile

Bundled Offerings

Web 2.0

Rysavy - Mobile Broadband Spectrum Demand, Dec. 2008

Fixed

Access

Fixed Mobile

Convergence

Embedded

Device Model

Industry Take-Aways

1.

We believe the backdrop of limited supply and rapidly increasing demand for

mobile bandwidth bodes well for our ATC spectrum opportunity

2.

Smartphone penetration and an emerging class of newly connected devices are

driving unprecedented growth in the use of mobile bandwidth

3.

Carriers, device manufacturers and consumers are increasingly dependent upon

data services for revenue or utility

4.

There is limited mobile spectrum available in the near term from traditional

sources

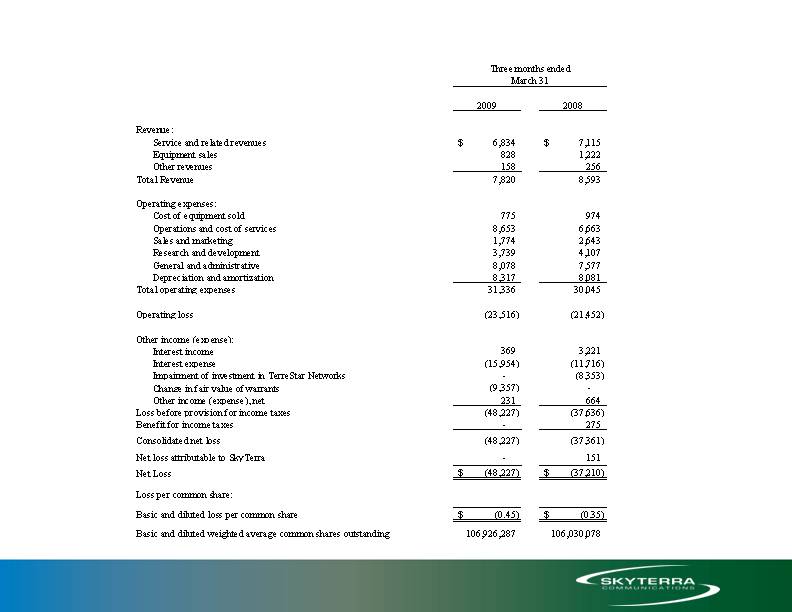

SkyTerra Consolidated Income Statement

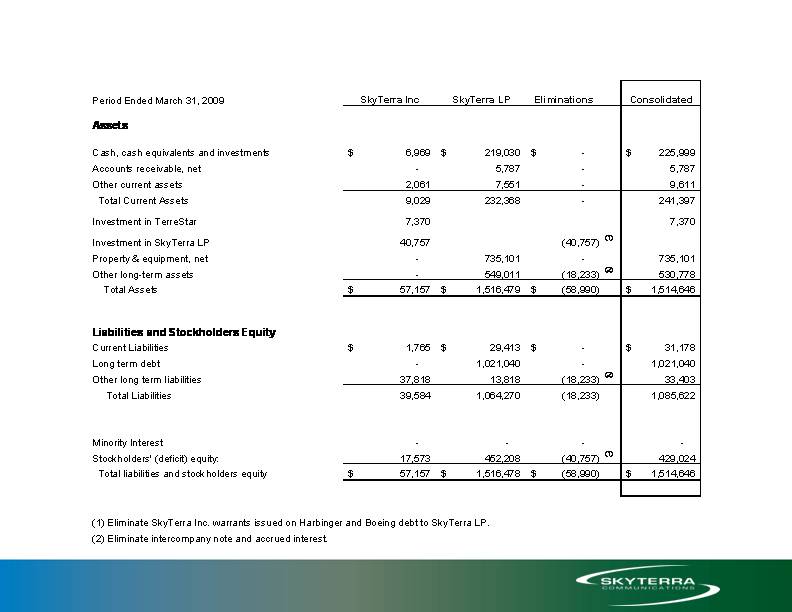

SkyTerra Consolidated Balance Sheet

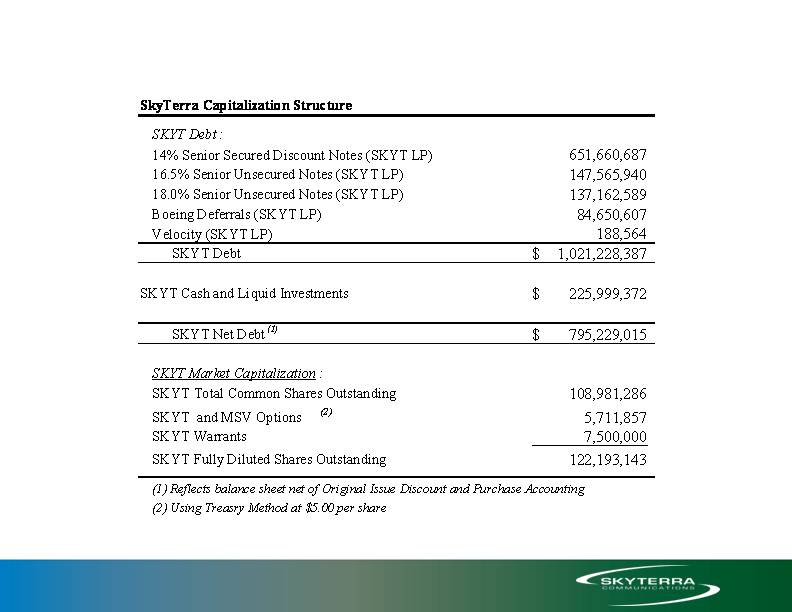

SkyTerra Capital Structure (1)

April 1, 2009 Funding

1.

Closed on the second of four funding tranches from Harbinger:

January 4, 2009: $150 million

April 1, 2009: $175 million

July 1, 2009: $ 75 million

January 4, 2010: $100 million

Total $500 million

2.

SKYT issued 21.25 million penny warrants for SKYT common stock as per the closing of the April funding tranche

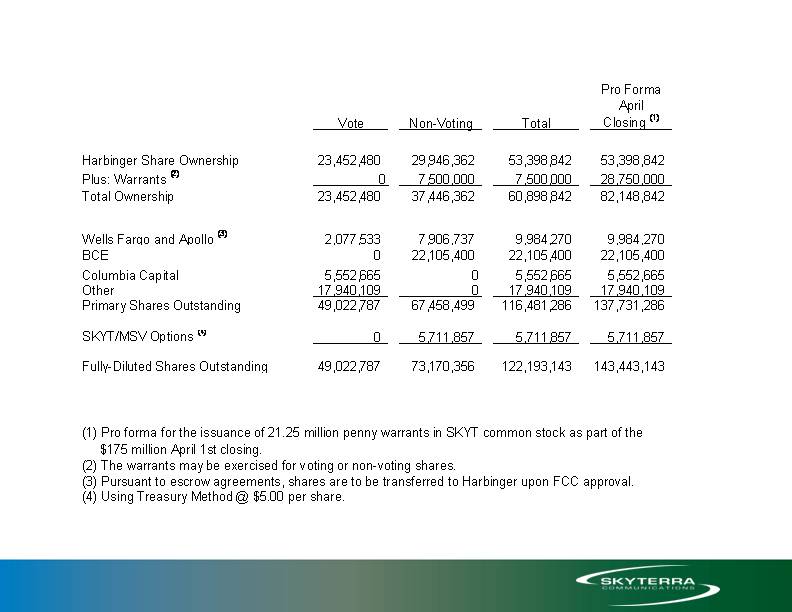

SkyTerra Ownership

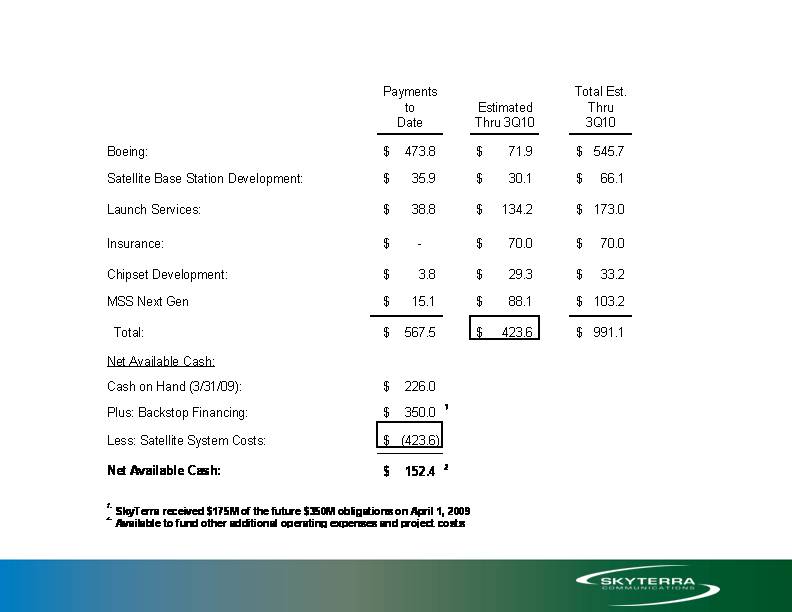

Next-Generation Satellite System Costs ($ in mm’s)