UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, DC 20549

FORM 10-K

(Mark One)

ý ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended December 31, 2006

o TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

Commission File Number 0-16761

HIGHLANDS BANKSHARES, INC.

(Exact name of registrant as specified in its charter)

| West Virginia | 55-0650743 |

| (State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) |

| P.O. Box 929 Petersburg, WV | 26847 |

| (Address of principal executive offices) | (Zip Code) |

Registrant’s telephone number, including area code: 304-257-4111

Securities registered pursuant to Section 12(b) of the Act: None

Securities registered pursuant to Section 12(g) of the Act: Common Stock, $5 par

Indicate by check mark if the registrant is a well-know seasoned issuer, as defined in Rule 405 or the Securities Act o Yes ý No

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act o Yes ý No

Indicate by check mark whether the registrant has (1) filed all reports required to be filed by Section 13 or 15(d) of the Exchange Act during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ý No o

Indicate by check mark if disclosure of delinquent filers in response to Item 405 of Regulation S-K is not contained in this form, and will not be contained, to the best of registrant's knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ý

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, or a non-accelerated filer. o Large Accelerated Filer o Accelerated Filer ý Non-accelerated filer

Indicate by check mark whether the registrant is a shell company (as defined in rule 126-2 of the Act) Yes o No ý

State the aggregate market value of the voting and non-voting common equity held by non-affiliates computed by reference to the price at which the common equity was last sold, or the average bid and asked price of such common equity, as of the last business day of the registrant’s most recently completed second fiscal quarter:

The aggregate market value of the 1,319,381 shares of common stock of the registrant issued and outstanding held by nonaffiliates on June 30, 2006 was approximately $42,880,000 based on the closing sales price of $32.50 on June 30, 2006. For the purposes of this calculation, the term “affiliate” refers to all directors and executive officers of the registrant.

Indicate the number of shares outstanding of each of the registrant’s classes of common stock as of the last practicable date: As of March 15, 2007: 1,436,874 shares of common stock.

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the Proxy Statement for the 2007 Annual Shareholders’ Meeting are incorporated by reference into Part III, Items 10,11,12,13 and 14.

|

| | Page |

| Business | 1 |

| Risk Factors | 5 |

| Unresolved Staff Comments | 8 |

| Properties | 8 |

| Legal Proceedings | 8 |

| Submission of Matters to a Vote of Security Holders | 8 |

| | | |

| | |

| Market for Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities | 8 |

| Selected Financial Data | 10 |

| Management’s Discussion and Analysis of Financial Condition and Results of Operations | 11 |

| Quantitative and Qualitative Disclosures About Market Risk | 31 |

| Financial Statements and Supplementary Data | 33 |

| Changes in and Disagreements with Accountants on Accounting and Financial Disclosure | 62 |

| Controls and Procedures | 62 |

| Other Information | 62 |

| | | |

| | |

| Directors and Officers of Registrant | 62 |

| Executive Compensation | 62 |

| Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters | 63 |

| Certain Relationships and Related Transactions | 63 |

| Principal Accounting Fees and Services | 63 |

| | | |

| | |

| Exhibits and Financial Statement Schedules | 64 |

| | | |

| 65 |

General

Highlands Bankshares, Inc. (hereinafter referred to as “Highlands,” or the “Company”), incorporated under the laws of West Virginia in 1985, is a multi bank holding company subject to the provisions of the Bank Holding Company Act of 1956, as amended, and owns 100% of the outstanding stock of its subsidiary Banks, The Grant County Bank and Capon Valley Bank (hereinafter referred to as the “Banks” or “Capon” and/or “Grant”), and its life insurance subsidiary, HBI Life Insurance Company (hereinafter referred to as “HBI Life”).

The Grant County Bank was chartered on August 6, 1902, and Capon Valley Bank was chartered on July 1, 1918. Both are state banks chartered under the laws of the State of West Virginia. HBI Life was chartered in April 1988 under the laws of the State of Arizona.

Services Offered by the Banks

The Banks offer all services normally offered by a full service commercial bank, including commercial and individual demand and time deposit accounts, commercial and individual loans, drive in banking services and automated teller machines. No material portion of the Banks' deposits have been obtained from a single or small group of customers and the loss of the deposits of any one customer or of a small group of customers would not have a material adverse effect on the business of the Banks. Credit life and accident and health insurance are sold to customers of the subsidiary Banks through HBI Life.

Employees

As of December 31, 2006, The Grant County Bank had 72 full time equivalent employees, Capon Valley Bank had 49 full time equivalent employees and Highlands had 3 full time equivalent employees. No person is employed by HBI Life on a full time basis.

Competition

The Banks' primary trade area is generally defined as Grant, Hardy, Mineral, Randolph, Pendleton and Tucker Counties in West Virginia, the western portion of Frederick County in Virginia and portions of Western Maryland. This area includes the towns of Petersburg, Wardensville, Moorefield and Keyser and several rural towns. The Banks' secondary trade area includes portions of Hampshire County in West Virginia. The Banks primarily compete with four state chartered banks, three national banks and three credit unions. In addition, the Banks compete with money market mutual funds and investment brokerage firms for deposits in their service area. No financial institution has been chartered in the area within the last five years although branches of state and nationally chartered banks have located in this area within this time period. Competition for new loans and deposits in the Banks' service area is quite intense.

Regulation and Supervision

The Company, as a registered bank holding company, and its subsidiary Banks, as insured depository institutions, operate in a highly regulated environment and are regularly examined by federal and state regulators. The following description briefly discusses certain provisions of federal and state laws and regulations and the potential impact of such provisions to which the Company and subsidiary are subject. These federal and state laws and regulations are designed to reduce potential loss exposure to the depositors of such depository institutions and to the Federal Deposit Insurance Corporation’s insurance fund and are not intended to protect the Company’s security holders. Proposals to change the laws and regulations governing the banking industry are frequently raised in Congress, in state legislatures, and before the various bank regulatory agencies. The likelihood and timing of any changes and the impact such changes might have on the Company are impossible to determine with any certainty. A change in applicable laws or regulations, or a change in the way such laws or regulations are interpreted by regulatory agencies or courts, may have a material impact on the business, operations and earnings of the Company. To the extent that the following information describes statutory or regulatory provisions, it is qualified entirely by reference to the particular statutory or regulatory provision.

As a bank holding company registered under the Bank Holding Company Act of 1956, as amended (the “BHCA”), the Company is subject to regulation by the Federal Reserve Board. Federal banking laws require a bank holding company to serve as a source of financial strength to its subsidiary depository institutions and to commit resources to support such institutions in circumstances where it might not do so otherwise. Additionally, the Federal Reserve Board has jurisdiction under the BHCA to approve any bank or non-bank acquisition, merger or consolidation proposed by a bank holding company. The BHCA generally limits the activities of a bank holding company and its subsidiaries to that of banking, managing or controlling banks as to be a proper incident thereto. The BHCA also prohibits a bank holding company, with certain exceptions, from acquiring more than 5% of the voting shares of any company and from engaging in any business other than banking or managing or controlling banks. The Federal Reserve Board has by regulation determined that certain activities are closely related to banking within the meaning of the BHCA. These activities include: operating a mortgage company, finance company, credit card company or factoring company; performing certain data processing operations; providing investment and financial advice; and acting as an insurance agent for certain types of credit-related insurance.

The Gramm-Leach-Bliley Act (“Gramm-Leach”) became law in November 1999. Gramm-Leach established a comprehensive framework to permit affiliations among commercial banks, investment banks, insurance companies, securities firms, and other financial service providers. Gramm-Leach permits qualifying bank holding companies to register with the Federal Reserve Board as “financial holding companies” and allows such companies to engage in a significantly broader range of financial activities than were historically permissible for bank holding companies. Although the Federal Reserve Board provides the principal regulatory supervision of financial services permitted under Gramm-Leach, the Securities and Exchange Commission and state regulators also provide substantial supervisory oversight. In addition to broadening the range of financial services a bank holding company may provide, Gramm-Leach also addressed customer privacy and information sharing issues and set forth certain customer disclosure requirements. The Company has no current plans to petition the Federal Reserve Board for consideration as a financial holding company.

The Riegle-Neal Interstate Banking and Branching Efficiency Act of 1994 (“Riegle-Neal”) permits bank holding companies to acquire banks located in any state. Riegle-Neal also allows national banks and state banks with different home states to merge across state lines and allows branch banking across state lines, unless specifically prohibited by state laws.

The International Money Laundering Abatement and Anti-Terrorist Financing Act of 2001 (USA “Patriot Act”) was adopted in response to the September 11, 2001 terrorist attacks. The Patriot Act provides law enforcement with greater powers to investigate terrorism and prevent future terrorist acts. Among the broad-reaching provisions contained in the Patriot Act are several designed to deter terrorists’ ability to launder money in the United States and provide law enforcement with additional powers to investigate how terrorists and terrorist organizations are financed. The Patriot Act creates additional requirements for banks, which were already subject to similar regulations. The Patriot Act authorizes the Secretary of Treasury to require financial institutions to take certain “special measures” when the Secretary suspects that certain transactions or accounts are related to money laundering. These special measures may be ordered when the Secretary suspects that a jurisdiction outside of the United States, a financial institution operating outside of the United States, a class of transactions involving a jurisdiction outside of the United States or certain types of accounts are of “primary money laundering concern.” The special measures include the following: (a) require financial institutions to keep records and report on transactions or accounts at issue; (b) require financial institutions to obtain and retain information related to the beneficial ownership of any account opened or maintained by foreign persons; (c) require financial institutions to identify each customer who is permitted to use the account; and (d) prohibit or impose conditions on the opening or maintaining of correspondence or payable-through accounts. Failure of a financial institution to maintain and implement adequate programs to combat money laundering and terrorist financing, or to comply with all of the relevant laws or regulations, could have serious legal and reputational consequences for the institution.

The operations of the insurance subsidiary are subject to the oversight and review of State of Arizona Department of Insurance.

On July 30, 2002, the United States Congress enacted the Sarbanes-Oxley Act of 2002, a law that addresses corporate governance, auditing and accounting, executive compensation and enhanced timely disclosure of corporate information. As Sarbanes-Oxley directs, the Company’s Chief Executive Officer and Chief Financial Officer are each required to certify that the Company’s quarterly and annual reports do not contain any untrue statement of a material fact. Additionally, these individuals must certify that: they are responsible for establishing, maintaining and regularly evaluating the effectiveness of the Company’s internal controls; they have made certain disclosures to the Company’s auditors and the Audit Committee of the Board of Directors about the Company’s internal controls; and they have included information in the Company’s quarterly and annual reports about their evaluation and whether there have been significant changes in the Company’s internal controls or in other factors that could significantly affect internal controls subsequent to the evaluations. Effective in 2007, Section 404 of Sarbanes-Oxley will become applicable to the Company.

Capital Adequacy

Federal banking regulations set forth capital adequacy guidelines, which are used by regulatory authorities to assess the adequacy of capital in examining and supervising a bank holding company and its insured depository institutions. The capital adequacy guidelines generally require bank holding companies to maintain total capital equal to at least 8% of total risk-adjusted assets, with at least one-half of total capital consisting of core capital (i.e., Tier I capital) and the remaining amount consisting of “other” capital-eligible items (i.e., Tier II capital), such as perpetual preferred stock, certain subordinated debt, and, subject to limitations, the allowance for loan losses. Tier I capital generally includes common stockholders’ equity plus, within certain limitations, perpetual preferred stock and trust preferred securities. For purposes of computing risk-based capital ratios, bank holding companies must meet specific capital guidelines that involve quantitative measures of assets, liabilities and certain off-balance sheet items, calculated under regulatory accounting practices. The Company’s and its subsidiaries’ capital accounts and classifications are also subject to qualitative judgments by the regulators about components, risk weightings, and other factors.

In addition to total and Tier I capital requirements, regulatory authorities also require bank holding companies and insured depository institutions to maintain a minimum leverage capital ratio of 3%. The leverage ratio is determined as the ratio of Tier I capital to total average assets, where average assets exclude goodwill, other intangibles, and other specifically excluded assets. Regulatory authorities have stated that minimum capital ratios are adequate for those institutions that are operationally and financially sound, experiencing solid earnings, have high levels of asset quality and are not experiencing significant growth. The guidelines also provide that banking organizations experiencing internal growth or making acquisitions will be expected to maintain strong capital positions substantially above the minimum supervisory levels. In those instances where these criteria are not evident, regulatory authorities expect, and may require, bank holding companies and insured depository institutions to maintain higher than minimum capital levels.

Additionally, federal banking laws require regulatory authorities to take “prompt corrective action” with respect to depository institutions that do not satisfy minimum capital requirements. The extent of these powers depends upon whether the institutions in question are “well capitalized”, “adequately capitalized”, “undercapitalized”, “significantly undercapitalized” or “critically undercapitalized”, as such terms are defined under uniform regulations defining such capital levels issued by each of the federal banking agencies. As an example, a depository institution that is not well capitalized is generally prohibited from accepting brokered deposits and offering interest rates on deposits higher than the prevailing rate in its market. Additionally, a depository institution is generally prohibited from making any capital distribution (including payment of a dividend) or paying any management fee to its holding company, may be subject to asset growth limitations and may be required to submit capital restoration plans if the depository institution is considered undercapitalized.

The Company’s and its subsidiaries’ regulatory capital ratios are presented in the following table:

| | Actual Ratio | Actual Ratio | Regulatory |

| | December 31, 2006 | December 31, 2005 | Minimum |

Total Risk Based Capital | | | |

| Highlands Bankshares | 13.45% | 13.85% | |

| The Grant County Bank | 12.63% | 13.67% | 8.00% |

| Capon Valley Bank | 14.56% | 13.45% | 8.00% |

| | | | |

Tier 1 Leverage Ratio | | | |

| Highlands Bankshares | 9.26% | 9.45% | |

| The Grant County Bank | 8.85% | 8.81% | 4.00% |

| Capon Valley Bank | 9.53% | 8.87% | 4.00% |

| | | | |

Tier 1 Risk Based Capital Ratio | | | |

| Highlands Bankshares | 12.21% | 12.60% | |

| The Grant County Bank | 11.39% | 12.47% | 4.00% |

| Capon Valley Bank | 13.30% | 12.20% | 4.00% |

Dividends and other Payments

The Company is a legal entity separate and distinct from its subsidiaries. Dividends and management fees from Grant County Bank and Capon Valley Bank are essentially the sole source of cash for the Company, although HBI Life will periodically pay dividends to the Company. The right of the Company, and shareholders of the Company, to participate in any distribution of the assets or earnings of Grant County Bank and Capon Valley Bank through the payment of such dividends or otherwise is necessarily subject to the prior claims of creditors of Grant County Bank and Capon Valley Bank, except to the extent that claims of the Company in its capacity as a creditor may be recognized. Moreover, there are various legal limitations applicable to the payment of dividends to the Company as well as the payment of dividends by the Company to its shareholders. Under federal law, Grant County Bank and Capon Valley Bank may not, subject to certain limited expectations, make loans or extensions of credit to, or invest in the securities of, or take securities of the Company as collateral for loans to any borrower. Grant County Bank and Capon Valley Bank are also subject to collateral security requirements for any loans or extensions of credit permitted by such exceptions.

Grant County Bank and Capon Valley Bank are subject to various statutory restrictions on their ability to pay dividends to the Company. Specifically, the approval of the appropriate regulatory authorities is required prior to the payment of dividends by Grant County Bank and Capon Valley Bank in excess of earnings retained in the current year plus retained net profits for the preceding two years. The payment of dividends by the Company, Grant County Bank and Capon Valley Bank may also be limited by other factors, such as requirements to maintain adequate capital above regulatory guidelines. The Federal Reserve Board and the Federal Deposit Insurance Corporation have the authority to prohibit any bank under their jurisdiction from engaging in an unsafe and unsound practice in conducting its business. Depending upon the financial condition of Grant County Bank and Capon Valley Bank, the payment of dividends could be deemed to constitute such an unsafe or unsound practice. The Federal Reserve Board and the FDIC have indicated their view that it generally would be an unsafe and unsound practice to pay dividends except out of current operating earnings. The Federal Reserve Board has stated that, as a matter of prudent banking, a bank or bank holding company should not maintain its existing rate of cash dividends on common stock unless (1) the organization’s net income available to common shareholders over the past year has been sufficient to fund fully the dividends and (2) the prospective rate or earnings retention appears consistent with the organization’s capital needs, asset quality, and overall financial condition. Moreover, the Federal Reserve Board has indicated that bank holding companies should serve as a source of managerial and financial strength to their subsidiary banks. Accordingly, the Federal Reserve Board has stated that a bank holding company should not maintain a level of cash dividends to its shareholders that places undue pressure on the capital of bank subsidiaries, or that can be funded only through additional borrowings or other arrangements that may undermine the bank holding company’s ability to serve as a source of strength.

Governmental Policies

The Federal Reserve Board regulates money and credit and interest rates in order to influence general economic conditions. These policies have a significant influence on overall growth and distribution of bank loans, investments and deposits and affect interest rates charged on loans or paid for time and savings deposits. Federal Reserve monetary policies have had a significant effect on the operating results of commercial banks in the past and are expected to continue to do so in the future.

Various other legislation, including proposals to overhaul the banking regulatory system and to limit the investments that a depository institution may make with insured funds, are from time to time introduced in Congress. The Company cannot determine the ultimate effect that such potential legislation, if enacted, would have upon its financial condition or operations.

Available Information

The Company files annual, quarterly and current reports, proxy statements and other information with the SEC. The Company’s SEC filings are filed electronically and are available to the public via the internet at the SEC’s website, www.sec.gov. In addition, any document filed by the Company with the SEC can be read and copies obtained at the SEC’s public reference facilities at 100 F Street, NE, Washington, DC 20549. Copies of documents can be obtained at prescribed rates by writing to the Public Reference Section of the SEC at 100 F Street NE, Washington, DC 20549. The public may obtain information on the operation of the Public Reference Room by calling the SEC at 1-800-SEC-0330. Copies of documents can also be obtained free of charge by writing to Highlands Bankshares, Inc., P.O. Box 929, Petersburg, WV 26847.

Executive Officers

Name | Age | Position with the Company | Principal Occupation (Past Five Years) |

Clarence E. Porter | 58 | President & Chief Executive Officer; Treasurer | CEO of Highlands since 2004; President of The Grant County Bank since 1991 |

R. Alan Miller | 37 | Finance Officer | Finance Officer of Highlands since 2002; Senior Manager of Finance, Cable & Wireless USA prior to 2002 |

| Alan L. Brill | 52 | Secretary; President of Capon Valley Bank | President of Capon Valley Bank since 2001 |

Due to Increased Competition, the Company May Not Be Able to Attract and Retain Banking Customers At Current Levels.

If, due to competition from competitors in the Company’s market area, the Company is unable to attract new and retain current customers, loan and deposit growth could decrease causing the Company’s results of operations and financial condition to be negatively impacted. The Company faces competition from the following:

| | · | Local, regional and national banks; |

| | · | Brokerage firms serving the Company’s market areas. |

The Company’s Lending Limit May Prevent It from Making Large Loans.

In the future, the Company may not be able to attract larger volume customers because the size of loans that the company can offer to potential customers is less than the size of the loans that many of the Company’s larger competitors can offer. We anticipate that our lending limit will continue to increase proportionately with the Company’s growth in earnings; however, the Company may not be able to successfully attract or maintain larger customers.

Certain Loans That the Banks Make Are Riskier than Loans for Real Estate Lending.

The Banks make loans that involve a greater degree of risk than loans involving residential real estate lending. Commercial business loans may involve greater risks than other types of lending because they are often made based on varying forms of collateral, and repayment of these loans often depends on the success of the commercial venture. Consumer loans may involve greater risk because adverse changes in borrowers’ incomes and employment after funding of the loans may impact their abilities to repay the loans.

The Company Is Subject to Interest Rate Risk.

Aside from credit risk, the most significant risk resulting from the Company’s normal course of business, extending loans and accepting deposits, is interest rate risk. If market interest rate fluctuations cause the Company’s cost of funds to increase faster than the yield of its interest-earning assets, then its net interest income will be reduced. The Company’s results of operations depend to a large extent on the level of net interest income, which is the difference between income from interest-earning assets, such as loans and investment securities, and interest expense on interest-bearing liabilities, such as deposits and borrowings. Interest rates are highly sensitive to many factors that are beyond the Company’s control, including general economic conditions and the policies of various governmental and regulatory authorities.

The Company May Not Be Able to Retain Key Members of Management.

The departure of one or more of the Company’s officers or other key personnel could adversely affect the Company’s operations and financial position. The Company’s management makes most decisions that involve the Company’s operations.

An Economic Slowdown in the Company’s Market Area Could Hurt Our Business.

An economic slowdown in our market area could hurt our business. An economic slowdown could have the following consequences:

| · | Loan delinquencies may increase; |

| · | Problem assets and foreclosures may increase; |

| · | Demand for the products and services of the Company may decline; and |

| · | Collateral (including real estate) for loans made by the company may decline in value, in turn reducing customers’ borrowing power and making existing loans less secure. |

The Company and the Bank are Extensively Regulated.

The operations of the Company are subject to extensive regulation by federal, state and local governmental authorities and are subject to various laws and judicial and administrative decisions imposing requirements and restrictions on them. Policies adopted or required by these governmental authorities can affect the Company’s business operations and the availability, growth and distribution of the Company’s investments, borrowings and deposits. Proposals to change the laws governing financial institutions are frequently raised in Congress and before bank regulatory authorities. Changes in applicable laws or policies could materially affect the Company’s business, and the likelihood of any major changes in the future and their effects are impossible to determine.

The Company’s Allowance for Loan Losses May Not Be Sufficient.

In the future, the Company could experience negative credit quality trends that could lead to a deterioration of asset quality. Such deterioration could require the company to incur loan charge-offs in the future and incur additional loan loss provision, both of which would have the effect of decreasing earnings. The Company maintains an allowance for possible loan losses which is a reserve established through a provision for possible loan losses charged to expense that represents management’s best estimate of probable losses that have been incurred within the existing portfolio of loans. Any increases in the allowance for possible loan losses will result in a decrease in net income and, possibly, capital, and may not have a material adverse effect on the Company’s financial condition and results of operation.

A Shareholder May Have Difficulty Selling Shares.

Because a very limited public market exists for the Company’s common stock, a shareholder may have difficulty selling his or her shares in the secondary market. We cannot predict when, if ever, we could meet the listing qualifications of the Nasdaq Stock Market’s National Market Tier or any exchange. We cannot assure investors that there will be a more active public market for the shares in the near future.

Shares of the Company’s Common Stock Are Not FDIC Insured.

Neither the Federal Deposit Insurance Corporation nor any other governmental agency insures the shares of the Company’s common stock. Therefore, the value of investors’ shares in the Company will be based on their market value and may decline.

Customers May Default on the Repayment of Loans.

The Bank’s customers may default on the repayment of loans, which may negatively impact the Company’s earnings due to loss of principal and interest income. Increased operating expenses may result from the allocation of management time and resources to the collection and workout of the loan. Collection efforts may or may not be successful causing the Company to write off the loan or repossess the collateral securing the loan, which may or may not exceed the balance of the loan.

The Company’s Controls and Procedures May Fail or Be Circumvented.

Management regularly reviews and updates the Company’s internal controls, disclosure controls and procedures, and corporate governance policies and procedures. Any system of controls, no matter how well designed and operated, is based in part on certain assumptions and can provide only reasonable, not absolute, assurances that the objectives of the system are met. Any failure or circumvention of the Company’s controls and procedures or failure to comply with regulations related to controls and procedures could have a material adverse effect on the Company’s business, results of operations and financial conditions.

| Unresolved Staff Comments |

None

Location | | Description |

| 3 N. Main Street, Petersburg, WV 26847 | | Primary Office, The Grant County Bank |

| Route 33, Riverton, WV 26814 | | Branch Office, The Grant County Bank |

| 500 S. Main Street, Moorefield, WV 26836 | | Branch Office, The Grant County Bank |

| Route 220 & Josie Dr., Keyser, WV 26726 | | Branch Office, The Grant County Bank |

| Main Street, Harman, WV 26270 | | Branch Office, The Grant County Bank |

| William Avenue, Davis, WV 26260 | | Branch Office, The Grant County Bank |

| Route 32 & Cortland Rd., Davis, WV 26260 | | Branch Office, The Grant County Bank |

| 2 W. Main Street, Wardensville, WV 26851 | | Primary Office, Capon Valley Bank |

| 717 N. Main Street, Moorefield, WV 26836 | | Branch Office, Capon Valley Bank |

| Route 55, Baker, WV 26801 | | Branch Office, Capon Valley Bank |

| 6701 Northwestern Pike, Gore, VA 22637 | | Branch Office, Capon Valley Bank |

All facilities are owned by the Company.

Management is not aware of any material pending or threatened litigation in which Highlands or its subsidiaries may be involved as a defendant. In the normal course of business, the Banks periodically must initiate suits against borrowers as a final course of action in collecting past due loans.

| Submission of Matters to a Vote of Security Holders |

Highlands Bankshares, Inc. did not submit any matters to a vote of security holders during the fourth quarter of 2006.

| Market for Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities |

The Company had approximately 1,100 shareholders of record as of December 31, 2006. This amount includes all shareholders, whether titled individually or held by a brokerage firm or custodian in street name. The Company's stock is not traded on any national or regional stock exchange although brokers may occasionally initiate or be a participant in a trade. The Company’s stock is listed on the Over The Counter Bulletin Board. Terms of an exchange between individual parties may not be known to the Company.

The following table outlines the dividends paid and market prices of the Company's stock based on prices disclosed to management. Prices have been provided using a nationally recognized online stock quote system. Such prices may not include retail mark-ups, mark-downs or commissions. Dividends are subject to the restrictions described in Note 10 to the Financial Statements.

| | | | Estimated Market Price Range |

2006 | | Dividends Per Share | High | Low |

| First Quarter | | .23 | 32.25 | 31.00 |

| Second Quarter | | .23 | 32.50 | 31.15 |

| Third Quarter | | .23 | 32.50 | 31.03 |

| Fourth Quarter | | .25 | 32.75 | 31.50 |

| | | | | |

2005 | | | | |

| First Quarter | | .20 | 28.90 | 24.80 |

| Second Quarter | | .20 | 29.10 | 26.74 |

| Third Quarter | | .20 | 30.79 | 28.11 |

| Fourth Quarter | | .22 | 32.00 | 30.79 |

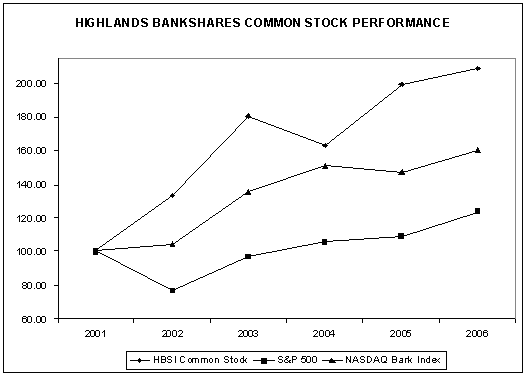

Set forth below is a line graph comparing the cumulative total return of Highlands Bankshares’ common stock from December 31, 2000 assuming reinvestment of dividends, with that of the Standard & Poor's 500 Index ("S&P 500") and the the Nasdaq Bank Index.

| | | Years Ending December 31, | |

| | | (in thousands of dollars, except for per share amounts) | |

| | | 2006 | | 2005 | | 2004 | | 2003 | | 2002 | |

| Total Interest Income | | $ | 23,894 | | $ | 19,813 | | $ | 17,729 | | $ | 18,283 | | $ | 18,970 | |

| Total Interest Expense | | | 7,909 | | | 5,761 | | | 4,711 | | | 6,338 | | | 7,705 | |

| Net Interest Income | | | 15,985 | | | 14,052 | | | 13,018 | | | 11,945 | | | 11,265 | |

| | | | | | | | | | | | | | | | | |

| Provision for Loan Losses | | | 682 | | | 875 | | | 920 | | | 1,820 | | | 820 | |

| | | | | | | | | | | | | | | | | |

| Net Interest Income After Provision for Loan Losses | | | 15,303 | | | 13,177 | | | 12,098 | | | 10,125 | | | 10,445 | |

| | | | | | | | | | | | | | | | | |

| Other Income | | | 1,997 | | | 1,669 | | | 1,597 | | | 1,367 | | | 1,304 | |

| Other Expenses | | | 10,394 | | | 9,128 | | | 8,938 | | | 8,247 | | | 8,048 | |

| | | | | | | | | | | | | | | | | |

| Income Before Income Taxes | | | 6,906 | | | 5,718 | | | 4,757 | | | 3,245 | | | 3,701 | |

| | | | | | | | | | | | | | | | | |

| Income Tax Expense | | | 2,391 | | | 1,916 | | | 1,551 | | | 1,012 | | | 1,179 | |

| | | | | | | | | | | | | | | | | |

| Net Income | | $ | 4,515 | | $ | 3,802 | | $ | 3,206 | | $ | 2,233 | | $ | 2,522 | |

| | | | | | | | | | | | | | | | | |

| Total Assets at Year End | | $ | 357,316 | | $ | 337,573 | | $ | 299,992 | | $ | 301,168 | | $ | 296,672 | |

| Long Term Debt at Year End | | $ | 14,992 | | $ | 15,063 | | $ | 8,377 | | $ | 5,295 | | $ | 4,030 | |

| | | | | | | | | | | | | | | | | |

| Net Income Per Share of Common Stock | | $ | 3.14 | | $ | 2.65 | | $ | 2.23 | | $ | 1.55 | | $ | 1.73 | |

| Dividends Per Share of Common Stock | | $ | .94 | | $ | .82 | | $ | .63 | | $ | .56 | | $ | .51 | |

| | | | | | | | | | | | | | | | | |

| Return on Average Assets | | | 1.29 | % | | 1.21 | % | | 1.07 | % | | .73 | % | | .89 | % |

| Return on Average Equity | | | 12.67 | % | | 11.53 | % | | 10.36 | % | | 7.60 | % | | 8.87 | % |

| Dividend Payout Ratio | | | 29.91 | % | | 30.99 | % | | 28.23 | % | | 36.03 | % | | 29.26 | % |

| Year End Equity to Assets Ratio | | | 10.38 | % | | 10.07 | % | | 10.55 | % | | 9.81 | % | | 9.69 | % |

| | | | | | | | | | | | | | | | | |

| 2002 per share figures restated to reflect stock split effected in form of dividend in 2002 |

| Management’s Discussion and Analysis of Financial Condition and Results of Operations |

Forward Looking Statements

Certain statements in this report may constitute “forward-looking statements” within the meaning of the Private Securities Litigation Reform Act of 1995. Forward-looking statements are statements that include projections, predictions, expectations or beliefs about future events or results or otherwise are not statements of historical fact. Such statements are often characterized by the use of qualified words (and their derivatives) such as “expect,” “believe,” “estimate,” “plan,” “project,” “anticipate” or other similar words. Although the Company believes that its expectations with respect to certain forward-looking statements are based upon reasonable assumptions within the bounds of its existing knowledge of its business and operations, there can be no assurance that actual results, performance or achievements of the Company will not differ materially from any future results, performance or achievements expressed or implied by such forward-looking statements. Actual future results and trends may differ materially from historical results or those anticipated depending on a variety of factors, including, but not limited to, the effects of and changes in: general economic conditions, the interest rate environment, legislative and regulatory requirements, competitive pressures, new products and delivery systems, inflation, changes in the stock and bond markets, technology, downturns in the trucking and timber industries, effects of mergers and/or downsizing in the poultry industry in Hardy County, and consumer spending and savings habits. Additionally, actual future results and trends may differ from historical or anticipated results to the extent: (1) any significant downturn in certain industries, particularly the trucking and timber and coal extraction industries are experienced; (2) loan demand decreases from prior periods; (3) the Company may make additional loan loss provisions due to negative credit quality trends in the future that may lead to a deterioration of asset quality; (4) the Company may not continue to experience significant recoveries of previously charged-off loans or loans resulting in foreclosure; (5) increased liquidity needs may cause an increase in funding costs; and, (6) the Company is unable to control costs and expenses as anticipated. The Company does not update any forward-looking statements that may be made from time to time by or on behalf of the Company.

Introduction

The following discussion focuses on significant results of the Company’s operations and significant changes in our financial condition or results of operations for the periods indicated in the discussion. This discussion should be read in conjunction with the preceding financial statements and related notes. Current performance does not guarantee, and may not be indicative of, similar performance in the future.

Critical Accounting Policies

The Company’s financial statements are prepared in accordance with accounting principles generally accepted in the United States (“GAAP”). The financial statements contained within these statements are, to a significant extent, financial information that is based on measures of the financial effects of transactions and events that have already occurred. A variety of factors could affect the ultimate value that is obtained either when earning income, recognizing an expense, recovering an asset or relieving a liability. In addition, GAAP itself may change from one previously acceptable method to another method. Although the economics of these transactions would be the same, the timing of events that would impact these transactions could change.

Allowance for Loan Losses

The allowance for loan losses is an estimate of the losses in the loan portfolio. The allowance is based on two basic principles of accounting: (i) SFAS No. 5, Accounting for Contingencies, which requires that losses be accrued when they are probable of occurring and estimable and (ii) SFAS No. 114, Accounting by Creditors for Impairment of a Loan, which requires that losses be accrued based on the differences between the value of collateral, present value of future cash flows or values that are observable in the secondary market and the loan balance.

The Company’s allowance for loan losses is the accumulation of various components that are calculated based on independent methodologies. All components of the allowance represent an estimation performed pursuant to either SFAS No. 5 or SFAS No. 114. Management’s estimate of each SFAS No. 5 component is based on certain observable data that management believes are most reflective of the underlying credit losses being estimated. This evaluation includes credit quality trends; collateral values; loan volumes; geographic, borrower and industry concentrations; seasoning of the loan portfolio; the findings of internal credit quality assessments and results from external bank regulatory examinations. These factors, as well as historical losses and current economic and business conditions, are used in developing estimated loss factors used in the calculations.

Reserves for commercial loans are determined by applying estimated loss factors to the portfolio based on management’s evaluation and “risk grading” of the commercial loan portfolio. Reserves are provided for noncommercial loan categories using estimated loss factors applied to the total outstanding loan balance of each loan category. Specific reserves are typically provided on all impaired commercial loans in excess of a defined threshold that are classified in the Special Mention, Substandard or Doubtful risk grades. The specific reserves are determined on a loan-by-loan basis based on management’s evaluation the Company’s exposure for each credit, given the current payment status of the loan and the value of any underlying collateral.

While management uses the best information available to establish the allowance for loan and lease losses, future adjustments to the allowance may be necessary if economic conditions differ substantially from the assumptions used in making the valuations or, if required by regulators, based upon information available to them at the time of their examinations. Such adjustments to original estimates, as necessary, are made in the period in which these factors and other relevant considerations indicate that loss levels may vary from previous estimates.

Post Retirement Benefits and Life Insurance Investments

The Company has invested in and owns life insurance polices on key officers. The policies are designed so that the company recovers the interest expenses associated with carrying the policies and the officer will, at the time of retirement, receive any earnings in excess of the amounts earned by the Company. The Company recognizes as an asset the net amount that could be realized under the insurance contract as of the balance sheet date. This amount represents the cash surrender value of the policies less applicable surrender charges. The portion of the benefits, which will be received by the executives at the time of their retirement, is considered, when taken collectively, to constitute a retirement plan. Therefore the Company accounts for these policies using guidance found in Statement of Financial Accounting Standards No. 106, "Employers' Accounting for Post Retirement Benefits Other Than Pensions.” SFAS No. 106 requires that an employers' obligation under a deferred compensation agreement be accrued over the expected service life of the employee through their normal retirement date.

Assumptions are used in estimating the present value of amounts due officers after their normal retirement date. These assumptions include the estimated income to be derived from the investments and an estimate of the Company’s cost of funds in these future periods. In addition, the discount rate used in the present value calculation will change in future years based on market conditions.

Intangible Assets

Generally accepted accounting principles were applied to allocate the intangible components of the purchase of the National Bank of Davis in November 2005. This excess was allocated between identifiable intangibles (i.e. core deposit intangibles) and unidentified intangibles (i.e. goodwill). Goodwill is required to be evaluated for impairment on an annual basis, and the value of the goodwill adjusted accordingly, should impairment be found. As of December 31, 2006, the Company did not identify an impairment of this intangible.

Recent Accounting Pronouncements

In September 2006, the FASB issued Statement of Financial Accounting Standards No. 158, “Employers Accounting for Defined Benefit Pension and Other Postretirement Plans—an amendment of FASB Statements No. 87, 88, 106 and 132R” (SFAS 158). SFAS 158 requires an employer to recognize the over-funded or under-funded status of a defined benefit postretirement plan as an asset or liability in its statement of financial position and to recognize changes in that funded status, through comprehensive income, in the year in which the changes occur. The funded status of a benefit plan will be measured as the difference between plan assets at fair value and benefit obligation. For any other postretirement plan, the benefit obligation is the accumulated postretirement benefit obligation. SFAS 158 also requires an employer to measure the funded status of a plan as of the date of its year-end statement of financial position. The Statement also requires additional disclosures in the notes to financial statements about certain effects on net periodic benefit cost for the next fiscal year that arise from delayed recognition of the gains or losses, prior service costs or credits, and transition asset or obligation. Under SFAS 158 a company is required to initially recognize the funded status of a defined benefit postretirement plan to provide the required disclosures as of the end of the fiscal year ending after December 15, 2006. The requirement to measure plan assets and benefit obligations as of the date of the employer’s fiscal year end statement of financial position is effective for fiscal years ending after December 15, 2008. The Grant County Bank is a member of the West Virginia Bankers' Association Retirement Plan, a defined benefit plan under SFAS 158.

No other recent accounting pronouncements had a material impact on the Company’s consolidated financial statements.

Overview of 2006 Results

Highlands Bankshares experienced an 18.75% increase in net income for 2006 as compared to 2005. Increases in net interest income, driven by balance sheet increases and a net interest margin of 5.05%, and an increase of $328,000 in non-interest income offset increases in non-interest expense. Return on Average Assets (ROAA) for 2006 was 1.29% compared to an ROAA in 2005 of 1.21%. Return on Average Equity (ROAE) for the year was 12.67% compared to ROAE of 11.53% for 2005. Earnings per share increased from $2.65 in 2005 to $3.14 in 2006.

Total assets grew 5.85% from December 31, 2005 to December 31, 2006. Average earning assets were 8.72% greater in 2006 than during 2005. Loan balances continue to make up the bulk of earning assets. During 2006 average loan balances represented 87.47% of total average balances of earning assets.

The Company’s provision for loan losses during 2006 was $193,000 less than that taken in 2005. In spite of the decrease in provision, the ratio of the allowance for loan losses to gross loans increased from 1.16 at December 31, 2005 to 1.19 at December 31, 2006 as net loan charge-offs, as a percentage of gross loans, fell from .17% in 2005 to .11% in 2006.

Due largely to an increase in service fees on deposit accounts, non-interest income increased 19.65%. In addition to the increase in service fees, the Company experienced an increase in earnings on investments in life insurance policies, mainly as the result of a $155,000 one-time gain from the settlement of two of these policies. Insurance earnings declined significantly from 2005 to 2006, as over the past several years the volume of new consumer installment loans, the primary market for the Company’s insurance products, has declined.

Due largely to the general increase in operational size, and, to a lesser degree, due to normal inflationary pressures on costs, non-interest expense increased 13.87% in 2006 as compared to 2005. Of the increase in non-interest expense, the majority was an increase in the cost of salaries and employee benefits, though occupancy and equipment expense and data processing expense also experienced year over year increases.

Highlands' results of operations are discussed in greater detail following this overview.

The following table illustrates Highlands’ quarterly financial results for the year ended December 31, 2006 (in thousands of dollars):

| Quarterly Financial Results | |

| For The Year Ended December 31, 2006 | |

| (in thousands, except per share amounts) | |

| | |

| | | Fourth Quarter | | Third Quarter | | Second Quarter | | First Quarter | |

| Total Interest Income | | $ | 6,477 | | $ | 6,140 | | $ | 5,735 | | $ | 5,542 | |

| Total Interest Expense | | | 2,338 | | | 2,047 | | | 1,831 | | | 1,693 | |

| Net Interest Income | | | 4,139 | | | 4,093 | | | 3,904 | | | 3,849 | |

| | | | | | | | | | | | | | |

| Provision for Loan Losses | | | 173 | | | 155 | | | 176 | | | 177 | |

| | | | | | | | | | | | | | |

| Net Interest Income After Provision for Loan Losses | | | 3,966 | | | 3,938 | | | 3,728 | | | 3,671 | |

| | | | | | | | | | | | | | |

| Other Income | | | 442 | | | 469 | | | 647 | | | 439 | |

| Other Expenses | | | 2,619 | | | 2,619 | | | 2,615 | | | 2,541 | |

| | | | | | | | | | | | | | |

| Income Before Income Taxes | | | 1,789 | | | 1,788 | | | 1,760 | | | 1,569 | |

| | | | | | | | | | | | | | |

| Income Tax Expense | | | 635 | | | 632 | | | 559 | | | 565 | |

| | | | | | | | | | | | | | |

| Net Income | | $ | 1,154 | | $ | 1,156 | | $ | 1,201 | | $ | 1,004 | |

| | | | | | | | | | | | | | |

| Net Income Per Share of Common Stock | | $ | .80 | | $ | .80 | | $ | .84 | | $ | .70 | |

| Dividends Per Share of Common Stock | | $ | .25 | | $ | .23 | | $ | .23 | | $ | .23 | |

The following table illustrates Highlands’ quarterly financial results for the year ended December 31, 2006 (in thousands of dollars):

| Quarterly Financial Results | |

| For The Year Ended December 31, 2005 | |

| (in thousands, except per share amounts) | |

| | |

| | | Fourth Quarter | | Third Quarter | | Second Quarter | | First Quarter | |

| Total Interest Income | | $ | 5,406 | | $ | 5,008 | | $ | 4,783 | | $ | 4,616 | |

| Total Interest Expense | | | 1,612 | | | 1,493 | | | 1,392 | | | 1,264 | |

| Net Interest Income | | | 3,794 | | | 3,515 | | | 3,391 | | | 3,352 | |

| | | | | | | | | | | | | | |

| Provision for Loan Losses | | | 185 | | | 255 | | | 210 | | | 225 | |

| | | | | | | | | | | | | | |

| Net Interest Income After Provision for Loan Losses | | | 3,609 | | | 3,260 | | | 3,181 | | | 3,127 | |

| | | | | | | | | | | | | | |

| Other Income | | | 415 | | | 445 | | | 445 | | | 364 | |

| Other Expenses | | | 2,390 | | | 2,299 | | | 2,229 | | | 2,210 | |

| | | | | | | | | | | | | | |

| Income Before Income Taxes | | | 1,634 | | | 1,406 | | | 1,397 | | | 1,281 | |

| | | | | | | | | | | | | | |

| Income Tax Expense | | | 542 | | | 463 | | | 479 | | | 432 | |

| | | | | | | | | | | | | | |

| Net Income | | $ | 1,092 | | $ | 943 | | $ | 918 | | $ | 849 | |

| | | | | | | | | | | | | | |

| Net Income Per Share of Common Stock | | $ | .76 | | $ | .66 | | $ | .64 | | $ | .59 | |

| Dividends Per Share of Common Stock | | $ | .22 | | $ | .20 | | $ | .20 | | $ | .20 | |

Impact of Acquisition on Operational Results

During the fourth quarter of 2005, the Company acquired two additional branches through the purchase of the National Bank of Davis. Further information regarding this purchase can be found in the Company’s Annual Report on Form 10-K for 2005. This acquisition has significantly impacted the results of operations for 2006, both in revenues and costs.

The acquisition added significant balances of both earning assets and interest bearing liabilities to the Company’s operations. The addition of these assets and liabilities has impacted the asset/liability management strategy of the Company, specifically The Grant County Bank into which the branches were integrated. Because of the full integration of these assets and liabilities, determination of the exact dollar amount of the impact on the Company’s net interest income is difficult to determine. However, the addition has increased net interest income as compared to 2005 both because of the increased balances of earning assets and interest bearing liabilities and because of the increased options for asset/liability management resulting from the purchase.

The addition of two branches and eleven full time equivalent employees as the result of the purchase of the National Bank of Davis has also caused an increase in non-interest expense. Specifically, occupancy and equipment expense has increased because of the added physical locations. Salary and benefits expense have increased because of the additional employees, and data processing expense has increased because of the additional loan and deposit customers. Additionally, certain other non-interest expenses have increased because of the acquisition.

Non-interest income has also been impacted by the acquisition, but to a lesser degree than the impact of the acquisition on net interest income and non-interest expense.

Net Interest Income

2006 Compared to 2005

The acquisition of the branches, as discussed earlier, has had significant impact on the Company’s net interest income. The following discussion highlights recent trends in the Company’s management of its net interest margin. The comparison of net interest income in 2006 as compared to 2005, as discussed below, should be considered in conjunction with the comments relating to the impact on net interest income of the acquisition of the National Bank of Davis, found earlier in Management’s Discussion and Analysis under the heading of “Impact of Acquisition on Operational Results.”

Net interest income, on a fully taxable equivalent basis, increased 13.73% from 2005 to 2006. This increase is both attributable to a general growth in the Company’s net interest balance sheet and also to increases in rates. Though the relative mix of earning assets and earning liabilities and also the ratio of earning assets to earning liabilities was roughly similar from 2005 to 2006 and therefore changes in the mix of these assets and liabilities or the ratio of the same did not contribute greatly to the increase in net interest income, the ratio of assets to liabilities and the percentage of earning assets made up of higher earning loan balances continues to be favorable to the Company’s net interest income and also its net interest margin.

Average balances of earning assets increased 8.72% from 2005 to 2006 and the ratio of earning assets to earning liabilities remained steady, 1.24 in 2006 and 1.25 in 2005. Average balances of interest bearing liabilities increased 9.26%.

As the Federal Reserve Board (“the Fed”) continued to increase rates into the early portions of 2006, the Company continued to experience average rate increases on both earnings of assets and on the costs of interest bearing liabilities. The increase in the average rates earned on interest earning assets of 74 basis points outpaced the average rates paid on interest bearing liabilities, which experienced a 64 basis point increase. Due to the rate increases by the Fed, rates earned on new loan balances continue to increase and due to the volume of adjustable rate mortgages in the Company’s portfolio, a significant portion of existing loan balances continue to reprice upward. This increase in rates earned on loans has been offset to some extent by higher rates paid on new time deposits, and as older time deposits mature and are renewed, higher rates are paid on the renewed balances.

During the later portions of 2006, the Fed halted its increases in the target rate for Federal Funds and rates have flattened as a result. If the Fed continues its pattern into the coming periods of holding rates constant, the Company expects average rates on loans and deposits to continue to increase as new loans and deposits are made and older loans and deposits mature or are repriced at higher rates. However, management anticipates that a Fed pattern of constant rates will cause the increase in average rates to slow somewhat.

During the past several years, management has undertaken a strategy of funding loan growth by reductions in balances of comparatively lower earning assets such as federal funds sold and securities, rather than pay above market rates to obtain new deposits. Management weighed the relative cost of these deposits versus earning on certain assets in making this decision. During 2006, the relative earnings of federal funds sold and securities as compared to loans increased. This increase, coupled with strong loan demand created a need for a change in the funding strategy. During the later portions of 2006, the Company began offering competitive rates to attract new deposit balances with which to fund new loan growth. The resulting increase in interest bearing liabilities has not negatively impacted net interest margin. Although significant loan growth may create a need for corresponding deposit growth, and to obtain this growth, the Company may be required to pay above market rates to obtain new deposit balances. Management anticipates that net interest income will continue to not be adversely impacted, though net interest margin percentages may decline.

The table below sets forth an analysis of net interest income for the years ended December 31, 2006 and 2005 (average balances and interest income/expense shown in thousands of dollars):

| | | 2006 | | 2005 | |

| | | Average Balance | | Income /Expense | | Yield /Rate | | Average Balance | | Income /Expense | | Yield /Rate | |

| | | | | | | | | | | | | | |

| Earning Assets | | | | | | | | | | | | | | | | | | | |

| Loans | | $ | 277,871 | | $ | 22,118 | | | 7.96 | % | $ | 254,700 | | $ | 18,622 | | | 7.31 | % |

| Taxable investment securities | | | 24,970 | | | 1,095 | | | 4.39 | % | | 23,313 | | | 707 | | | 3.03 | % |

| Nontaxable investment securities | | | 2,987 | | | 173 | | | 5.79 | % | | 2,951 | | | 163 | | | 5.52 | % |

| Interest bearing deposits | | | 1,576 | | | 72 | | | 4.57 | % | | 1,268 | | | 38 | | | 3.00 | % |

| Federal funds sold | | | 10,287 | | | 500 | | | 4.87 | % | | 9,970 | | | 343 | | | 3.44 | % |

| Total Earning Assets | | | 317,691 | | | 23,958 | | | 7.54 | % | | 292,202 | | | 19,873 | | | 6.80 | % |

| | | | | | | | | | | | | | | | | | | | |

| Allowance for loan losses | | | (3,283 | ) | | | | | | | | (2,807 | ) | | | | | | |

| Other non-earning assets | | | 28,648 | | | | | | | | | 25,291 | | | | | | | |

| | | | | | | | | | | | | | | | | | | | |

| Total Assets | | $ | 343,056 | | | | | | | | $ | 314,686 | | | | | | | |

| | | | | | | | | | | | | | | | | | | | |

| Interest Bearing Liabilities | | | | | | | | | | | | | | | | | | | |

| Demand deposits | | $ | 25,658 | | $ | 224 | | | .87 | % | $ | 23,554 | | $ | 189 | | | .80 | % |

| Savings deposits | | | 50,235 | | | 549 | | | 1.09 | % | | 49,391 | | | 437 | | | .88 | % |

| Time deposits | | | 164,005 | | | 6,429 | | | 3.92 | % | | 146,211 | | | 4,504 | | | 3.08 | % |

| Borrowed money | | | 15,643 | | | 707 | | | 4.52 | % | | 14,728 | | | 631 | | | 4.28 | % |

| Total Interest Bearing Liabilities | | | 255,541 | | | 7,909 | | | 3.10 | % | | 233,884 | | | 5,761 | | | 2.46 | % |

| | | | | | | | | | | | | | | | | | | | |

| Demand deposits | | | 48,056 | | | | | | | | | 41,360 | | | | | | | |

| Other liabilities | | | 3,810 | | | | | | | | | 6,459 | | | | | | | |

| Stockholders’ equity | | | 35,649 | | | | | | | | | 32,983 | | | | | | | |

| | | | | | | | | | | | | | | | | | | | |

| Total Liabilities and Stockholders’ Equity | | $ | 343,056 | | | | | | | | $ | 314,686 | | | | | | | |

| | | | | | | | | | | | | | | | | | | | |

| Net Interest Income | | | | | $ | 16,049 | | | | | | | | $ | 14,112 | | | | |

| Net Yield on Earning Assets | | | | | | | | | 5.05 | % | | | | | | | | 4.83 | % |

| | | | | | | | | | | | | | | | | | | | |

| Notes: | | | | | | | | | | | | | | | | | | | |

| (1) Yields are computed on a taxable equivalent basis using a 37% tax rate |

| (2) Average balances are based upon daily balances |

| (3) Includes loans in non-accrual status |

| (4) Income on loans includes fees |

The table below illustrates the effects on net interest income of changes in average volumes of interest bearing liabilities and earning assets from 2005 to 2006 and changes in average rates on interest bearing liabilities and earning assets from 2005 to 2006 (in thousands of dollars):

| EFFECT OF RATE-VOLUME CHANGES ON NET INTEREST INCOME | |

| (On a fully taxable equivalent basis) | |

| (In thousands of dollars) | |

| | | | | | | | |

| Increase (Decrease) 2006 Compared to 2005 | |

| | | | | | | | |

| | | Due to change in: | | | |

| | | Average Volume | | Average Rate | | Total Change | |

| Interest Income | | | | | | | | | | |

| Loans | | $ | 1,694 | | $ | 1,802 | | $ | 3,496 | |

| Taxable investment securities | | | 50 | | | 338 | | | 388 | |

| Nontaxable investment securities | | | 2 | | | 8 | | | 10 | |

| Interest bearing deposits | | | 9 | | | 25 | | | 34 | |

| Federal funds sold | | | 11 | | | 146 | | | 157 | |

| Total Interest Income | | | 1,766 | | | 2,319 | | | 4,085 | |

| | | | | | | | | | | |

| Interest Expense | | | | | | | | | | |

| Demand deposits | | | 17 | | | 18 | | | 35 | |

| Savings deposits | | | 7 | | | 105 | | | 112 | |

| Time deposits | | | 548 | | | 1,377 | | | 1,925 | |

| Borrowed money | | | 39 | | | 37 | | | 76 | |

| Total Interest Expense | | | 611 | | | 1,537 | | | 2,148 | |

| | | | | | | | | | | |

| Net Interest Income | | $ | 1,155 | | $ | 782 | | $ | 1,937 | |

Changes in volume are calculated based on the difference in average balance multiplied by the prior year average rate. Changes due to rate changes are calculated by subtracting the change due to volume from the total change.

2005 Compared to 2004

Net interest income, on a fully taxable equivalent basis, increased 7.81% in 2005 as compared to 2004. As the Federal Reserve Board (the “Fed”) continued to increase the target rates for federal funds, both interest rates paid on deposits and interest earned on assets increased. The increases by the Fed had the greatest impact on the rates earned on federal funds sold, deposits in other banks and on interest bearing deposits. Average balances of earning assets increased $12.39 million while average balances of interest bearing liabilities increased only $5.68 million. This relative increase, coupled with increases in loan balances, (a comparatively higher earning asset as a percentage of total average earning assets) had the greatest impact in the increase in net interest income and the increase of 15 basis points in net interest margin.

Throughout 2004 and into the early part of 2005, the Company chose to fund loan growth through the reduction of balances of federal funds sold, deposits in other banks and securities (relatively low earning assets) rather than pay above market rates to attract new deposits. This strategy caused overall average balances of interest bearing deposits to decrease slightly, investments in securities to decrease moderately and federal funds sold to decrease substantially. Average rates paid on interest bearing liabilities increased 40 basis points from 2004 to 2005 compared to the slightly larger 44 basis point increase experienced with interest earning assets.

While the rate increases enacted by the Fed had an immediate impact on the yields of federal funds sold and interest bearing deposits, continued heavy competition for new loans caused a more subdued increase in average rates earned on loans.

In addition to funding loan growth through reductions in balances of relatively lower earning assets, the Company also chose to utilize its borrowing capacity from the Federal Home Loan Bank (“FHLB”) more in 2005 than in the past. The lending options offered by the FHLB allowed the subsidiary Banks to borrow in certain instances at favorable rates and/or favorable repayment terms and assist in the Company’s management of its assets and liabilities.

Average balances of many of the categories of both earning assets and interest bearing liabilities were increased by the purchase of The National Bank of Davis (“Davis”). However, because this purchase occurred late in 2005, and because of the relatively small size of Davis compared to Highlands Bankshares, the impact on net interest margin for 2005 was not significant. At the time of purchase, Davis had a comparatively conservative balance sheet. Davis’ loan to deposit ratio at the time of purchase was 33.14% and Davis’ ratio of earning assets to interest bearing liabilities was 84.45% compared to a Highlands 2005 average ratio of earning assets to interest bearing liabilities of 124.93%.

The table below sets forth an analysis of net interest income for the years ended December 31, 2005 and 2004 (average balances and interest income/expense shown in thousands of dollars):

| | | 2005 | | 2004 | |

| | | Average Balance | | Income /Expense | | Yield /Rate | | Average Balance | | Income /Expense | | Yield /Rate | |

| | | | | | | | | | | | | | |

| Earning Assets | | | | | | | | | | | | | | | | | | | |

| Loans | | $ | 254,700 | | $ | 18,622 | | | 7.31 | % | $ | 235,023 | | $ | 16,752 | | | 7.13 | % |

| Taxable investment securities | | | 23,313 | | | 707 | | | 3.03 | % | | 25,944 | | | 674 | | | 2.60 | % |

| Nontaxable investment securities | | | 2,951 | | | 163 | | | 5.52 | % | | 3,298 | | | 194 | | | 5.89 | % |

| Interest bearing deposits | | | 1,268 | | | 38 | | | 3.00 | % | | 1,430 | | | 18 | | | 1.26 | % |

| Federal funds sold | | | 9,970 | | | 343 | | | 3.44 | % | | 14,119 | | | 163 | | | 1.15 | % |

| Total Earning Assets | | | 292,202 | | | 19,873 | | | 6.80 | % | | 279,814 | | | 17,801 | | | 6.36 | % |

| | | | | | | | | | | | | | | | | | | | |

| Allowance for loan losses | | | (2,807 | ) | | | | | | | | (2,418 | ) | | | | | | |

| Other non-earning assets | | | 25,291 | | | | | | | | | 23,024 | | | | | | | |

| | | | | | | | | | | | | | | | | | | | |

| Total Assets | | $ | 314,686 | | | | | | | | $ | 300,420 | | | | | | | |

| | | | | | | | | | | | | | | | | | | | |

| Interest Bearing Liabilities | | | | | | | | | | | | | | | | | | | |

| Demand deposits | | $ | 23,554 | | $ | 189 | | | .80 | % | $ | 24,031 | | $ | 95 | | | .40 | % |

| Savings deposits | | | 49,391 | | | 437 | | | .88 | % | | 52,079 | | | 296 | | | .57 | % |

| Time deposits | | | 146,211 | | | 4,504 | | | 3.08 | % | | 145,834 | | | 4,042 | | | 2.77 | % |

| Borrowed money | | | 14,728 | | | 631 | | | 4.28 | % | | 6,264 | | | 278 | | | 4.44 | % |

| Total Interest Bearing Liabilities | | | 233,884 | | | 5,761 | | | 2.46 | % | | 228,208 | | | 4,711 | | | 2.06 | % |

| | | | | | | | | | | | | | | | | | | | |

| Demand deposits | | | 41,360 | | | | | | | | | 37,325 | | | | | | | |

| Other liabilities | | | 6,459 | | | | | | | | | 3,954 | | | | | | | |

| Stockholders’ equity | | | 32,983 | | | | | | | | | 30,933 | | | | | | | |

| | | | | | | | | | | | | | | | | | | | |

| Total Liabilities and Stockholders’ Equity | | $ | 314,686 | | | | | | | | $ | 300,420 | | | | | | | |

| | | | | | | | | | | | | | | | | | | | |

| Net Interest Income | | | | | $ | 14,112 | | | | | | | | $ | 13,090 | | | | |

| Net Yield on Earning Assets | | | | | | | | | 4.83 | % | | | | | | | | 4.68 | % |

| | | | | | | | | | | | | | | | | | | | |

| Notes: | | | | | | | | | | | | | | | | | | | |

| (1) Yields are computed on a taxable equivalent basis using a 37% tax rate |

| (2) Average balances are based upon daily balances |

| (3) Includes loans in non-accrual status |

| (4) Income on loans includes fees |

The table below illustrates the effects on net interest income of changes in average volumes of interest bearing liabilities and earning assets from 2004 to 2005 and changes in average rates on interest bearing liabilities and earning assets from 2004 to 2005 (in thousands of dollars):

| EFFECT OF RATE-VOLUME CHANGES ON NET INTEREST INCOME | |

| (On a fully taxable equivalent basis) | |

| (In thousands of dollars) | |

| | | | | | | | |

| Increase (Decrease) 2005 Compared to 2004 | |

| | | | | | | | |

| | | Due to change in: | | | |

| | | Average Volume | | Average Rate | | Total Change | |

| Interest Income | | | | | | | | | | |

| Loans | | $ | 1,402 | | $ | 468 | | $ | 1,870 | |

| Taxable investment securities | | | (68 | ) | | 101 | | | 33 | |

| Nontaxable investment securities | | | (20 | ) | | (11 | ) | | (31 | ) |

| Interest bearing deposits | | | (2 | ) | | 22 | | | 20 | |

| Federal funds sold | | | (48 | ) | | 228 | | | 180 | |

| Total Interest Income | | | 1,264 | | | 808 | | | 2,012 | |

| | | | | | | | | | | |

| Interest Expense | | | | | | | | | | |

| Demand deposits | | | (2 | ) | | 96 | | | 94 | |

| Savings deposits | | | (15 | ) | | 156 | | | 141 | |

| Time deposits | | | 10 | | | 452 | | | 462 | |

| Borrowed money | | | 376 | | | (23 | ) | | 353 | |

| Total Interest Expense | | | 369 | | | 681 | | | 1,050 | |

| | | | | | | | | | | |

| Net Interest Income | | $ | 895 | | $ | 127 | | $ | 1,022 | |

Changes in volume are calculated based on the difference in average balance multiplied by the prior year average rate. Changes due to rate changes are calculated by subtracting the change due to volume from the total change.

Loan Portfolio

The Company is an active residential mortgage and construction lender and extends commercial loans to small and medium sized businesses within its primary service area. The Company’s commercial lending activity extends across its primary service areas of Grant, Hardy, Hampshire, Mineral, Randolph, Tucker and Pendleton counties in West Virginia and Frederick County, Virginia. Consistent with its focus on providing community-based financial services, the Company does not attempt to diversify its loan portfolio geographically by making significant amounts of loans to borrowers outside of its primary service area.

The following table summarizes the Company’s loan portfolio at December 31, 2006, 2005, 2004, 2003 and 2002 (in thousands of dollars):

| | | At December 31, | |

| | | 2006 | | 2005 | | 2004 | | 2003 | | 2002 | |

| Real estate mortgage | | $ | 164,243 | | $ | 153,646 | | $ | 140,762 | | $ | 129,671 | | $ | 121,558 | |

| Real estate construction | | | 14,828 | | | 12,201 | | | 8,850 | | | 7,552 | | | 6,813 | |

| Commercial | | | 70,408 | | | 57,908 | | | 52,813 | | | 42,911 | | | 47,089 | |

| Installment | | | 43,337 | | | 46,265 | | | 46,092 | | | 46,501 | | | 50,294 | |

| Total Loans | | | 292,816 | | | 270,020 | | | 248,517 | | | 226,635 | | | 225,754 | |

| | | | | | | | | | | | | | | | | |

| Allowance for loan losses | | | (3,482 | ) | | (3,129 | ) | | (2,530 | ) | | (2,463 | ) | | (1,793 | ) |

| | | | | | | | | | | | | | | | | |

| Net Loans | | $ | 289,334 | | $ | 266,891 | | $ | 245,987 | | $ | 224,172 | | $ | 223,961 | |

Commercial loan balances include certain loans secured by commercial real estate. As of December 31, 2006 the Company maintained balances of loans secured by real estate of $226,310,000.

There were no foreign loans outstanding during any of the above periods.

The following table illustrates the Company’s loan maturity distribution as of December 31, 2006 (in thousands of dollars):

| | | Maturity Range | |

| | | Less than 1 Year | | 1-5 Years | | Over 5 Years | | Total | |

Loan Type | | | | | | | | | | | | | |

| Commercial | | $ | 46,937 | | $ | 12,379 | | $ | 11,092 | | $ | 70,408 | |

| Real estate mortgage and construction | | | 60,347 | | | 52,802 | | | 65,922 | | | 179,071 | |

| Installment | | | 15,760 | | | 26,726 | | | 851 | | | 43,337 | |

| Total Loans | | $ | 123,044 | | $ | 91,907 | | $ | 77,865 | | $ | 292,816 | |

Credit Quality

The principal economic risk associated with each of the categories of loans in the Company’s portfolio is the creditworthiness of its borrowers. Within each category, such risk is increased or decreased depending on prevailing economic conditions. The risk associated with the real estate mortgage loans and installment loans to individuals varies based upon employment levels, consumer confidence, fluctuations in value of residential real estate and other conditions that affect the ability of consumers to repay indebtedness. The risk associated with commercial, financial and agricultural loans varies based upon the strength and activity of the local economies of the Company’s market areas. The risk associated with real estate construction loans varies based upon the supply of and demand for the type of real estate under construction.

An inherent risk in the lending of money is that the borrower will not be able to repay the loan under the terms of the original agreement. The allowance for loan losses (see subsequent section) provides for this risk and is reviewed periodically for adequacy. This review also considers concentrations of loans in terms of geography, business type or level of risk. While lending is geographically diversified within the service area, the Company does have some concentration of loans in the area of agriculture (primarily poultry farming), and the timber and coal extraction industries. Management recognizes these concentrations and considers them when structuring its loan portfolio.

Nonperforming loans include non-accrual loans, loans 90 days or more past due and restructured loans. Non-accrual loans are loans on which interest accruals have been discontinued. Loans are typically placed in non-accrual status when the collection of principal or interest is 90 days past due and collection is uncertain based on the net realizable value of the collateral and/or the financial strength of the borrower. Also, the existence of any guaranties by federal or state agencies is given consideration in this decision. The policy is the same for all types of loans. Restructured loans are loans for which a borrower has been granted a concession on the interest rate or the original repayment terms because of financial difficulties. Nonperforming loans do not represent or result from trends or uncertainties which management reasonably expects will materially impact future operating results, liquidity, or capital resources. Nonperforming loans are listed in the table below.

Nonperforming loans decreased 11.96% from December 31, 2005 to December 31, 2006, but still remain below the Company’s 5-year average. At December 31, 2006, nonperforming loans represented .58% of the Company’s balances of gross loans as compared to .72% at December 31, 2005.

The following table summarizes the Company’s nonperforming loans (in thousands of dollars):

| | | At December 31, | |

| | | 2006 | | 2005 | | 2004 | | 2003 | | 2002 | |

| Loans accounted for on a non-accrual basis | | | | | | | | | | | | | | | | |

| Consumer | | $ | 83 | | $ | 124 | | $ | 252 | | $ | 228 | | $ | 9 | |

| Real estate | | | 161 | | | 619 | | | 278 | | | 1,436 | | | 290 | |

| Total Non-accrual Loans | | | 244 | | | 743 | | | 530 | | | 1,664 | | | 299 | |

| | | | | | | | | | | | | | | | | |

| Restructured Loans | | | 0 | | | 0 | | | 0 | | | 631 | | | 662 | |

| | | | | | | | | | | | | | | | | |

| Loans delinquent 90 days or more | | | | | | | | | | | | | | | | |

| Consumer | | | 122 | | | 74 | | | 140 | | | 25 | | | 161 | |

| Commercial | | | 0 | | | 966 | | | 355 | | | 1,255 | | | 1,312 | |

| Real estate | | | 1,335 | | | 149 | | | 40 | | | 318 | | | 445 | |