Exhibit 99.1

| | Focus on Value Creation | 9 |

| Strategy of Increasing Net Asset Value, Production, | |

| Reserves and Earnings – All on a Per Share Basis | |

| | |

| Exceptional Gold Price Leverage | 10 |

| Generating Record Earnings and Cash Flow · | |

| Nine Million Ounce Production Target within Five Years | |

| | |

| Financial Strength and Flexibility | 11 |

| ‘A’ Credit Rating and Strong Balance Sheet to | |

| Support Our Objectives | |

| | |

| Operational Excellence | 12 |

| Consistent Track Record of Achieving Targets | |

| | |

| Project Development Expertise | 15 |

| Cortez Hills Built on Time and Budget · World-Class | |

| Pueblo Viejo and Pascua-Lama Projects in Construction | |

| | |

| Surfacing Hidden Value | 19 |

| Optimizing Our High Quality, Diversified Portfolio | |

| of Assets | |

| | |

| Industry’s Largest Gold Reserves | 21 |

| Replaced or Grown for the Last Five Straight Years | |

| | |

| Strong Focus on Responsible Mining | 23 |

| Relisted on Dow Jones World Sustainability Index · | |

| Added to NASDAQ Global Sustainability Index | |

Barrick’s strategy is focused on maximizing shareholder value by building gold and copper reserves through exploration, investing in high return development projects, realizing the potential of existing mines, pursuing disciplined acquisitions and strengthening our social and environmental performance.

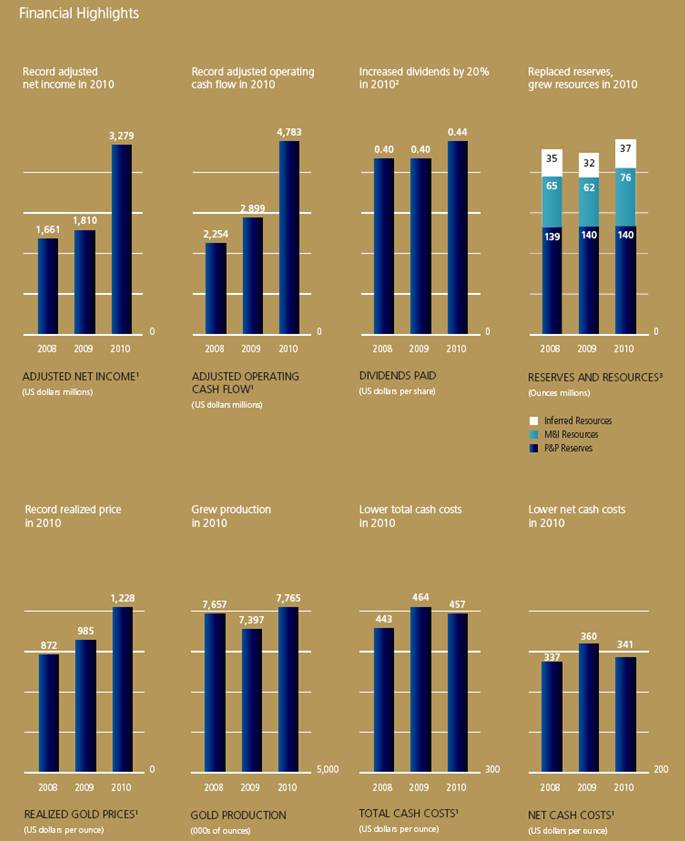

Barrick delivered a strong operating performance in 2010 with higher gold production and lower total cash costs, and achieved record financial results as the gold price reached new highs.

(in millions of US dollars, except per share data) | | | | | | | |

(US GAAP basis) | | 2010 | | 2009 | | 2008 | |

Sales | | $ | 10,924 | | $ | 8,136 | | $ | 7,613 | |

Net income (loss) | | 3,274 | | (4,274 | ) | 785 | |

per share | | 3.32 | | (4.73 | ) | 0.90 | |

Adjusted net income(1) | | 3,279 | | 1,810 | | 1,661 | |

per share | | 3.32 | | 2.00 | | 1.90 | |

Operating cash flow | | 4,127 | | (2,322 | ) | 2,254 | |

Adjusted operating cash flow(1) | | 4,783 | | 2,899 | | 2,254 | |

Cash and equivalents | | 3,968 | | 2,564 | | 1,437 | |

Dividends paid per share(2) | | 0.44 | | 0.40 | | 0.40 | |

| | | | | | | |

Operating Highlights | | | | | | | |

Gold production (000s oz) | | 7,765 | | 7,397 | | 7,657 | |

Average realized gold price per ounce(1) | | $ | 1,228 | | $ | 985 | | $ | 872 | |

Total cash costs per ounce(1) | | $ | 457 | | $ | 464 | | $ | 443 | |

Net cash costs per ounce(1) | | $ | 341 | | $ | 360 | | $ | 337 | |

Copper production (M lbs) | | 368 | | 393 | | 370 | |

Average realized copper price per pound(1) | | $ | 3.41 | | $ | 3.16 | | $ | 3.39 | |

Total cash costs per pound(1) | | $ | 1.11 | | $ | 1.17 | | $ | 1.19 | |

(1) Non-GAAP financial measure – see pages 78–85 of the 2010 Financial Report.

(2) In July 2010, Barrick increased its dividend by 20% to $0.12 per share on a quarterly basis; based on converting the previous semi-annual dividend of $0.20 per share to a quarterly equivalent.

(3) See page 22 of the 2010 Annual Report for additional information on Barrick’s reserves and resources.

Message from the Chairman

Message from the Chairman

Peter Munk

Founder and Chairman

Fellow shareholders,

There are countless theories that attempt to explain why gold prices behave the way they do. At its core, however, the gold market is not all that complicated: generally speaking, when people feel secure, gold prices fall; when people feel insecure, prices rise.

There was a time not that long ago – for about a decade, between 1988 and 2000 – that most of us in the West felt not just secure, but exuberant. The Berlin Wall came down. The Cold War ended. American power was at its zenith. In short, our confidence was unsurpassed. In his best-selling book of 1992, The End of History and the Last Man, Francis Fukuyama declared that in the long struggle between political ideologies, liberal democracy and market capitalism had clearly won the day. What was there to be worried about?

During this period of euphoria, gold prices dropped in half, from about $500 per ounce to a low of around $250 per ounce by 1999. You know what happened next. First, in 2000, the “dot-com” bubble burst and the stock market collapsed. One year later, on September 11, 2001, the whole world changed. We were not so secure, after all.

What has followed would have been unthinkable only a few years earlier: two intractable wars in the Middle East; a massive global economic recession; the collapse of the U.S. housing market; the bankruptcy of Lehman Brothers and the demise of Bear Stearns; and on and on. Investors lost faith in the world’s two most powerful currencies – the U.S. dollar and the new Euro. Then came fears of sovereign default in Europe, where governments, desperate to restore confidence in their rattled markets, were forced to intervene.

As I write this letter, amid spreading chaos and violence in the Mideast and North Africa, there continues to be little news to stir the confidence of investors. Our world is uncertain. More and more people are afraid of the future. The optimism of the 1990s has faded into an era of global pessimism.

With their confidence shaken, an ever-growing number of investors are moving into gold, and have been now for some 10 years. As a result, of course, the price of gold has climbed continually, increasing more than 400% in a decade. This, even while the S&P 500 Index has fallen by 5%.

Given how strongly gold has performed, it’s not surprising that some people now wonder if we’re in a bubble. They suggest we’re at a moment not unlike 1980, when gold prices, having reached unprecedented and historic highs, suddenly plummeted.

I don’t think we are in a bubble today; not at all. For one thing, the situation today could not be more different than it was in the late 1970s and early 1980s. What happened 30 years ago was clearly a kind of mania: in a single year, the price of gold shot up by more

2

Barrick Annual Report 2010 | Message from the Chairman

than 250%, hitting an all-time record of $850 per ounce in January 1980. It was madness! People around the world lined up outside banks to buy a few ounces of the metal, as prices rose daily. Then, almost as quickly as it had soared, gold collapsed.

By contrast, the past decade’s rise in gold prices has displayed neither extreme volatility nor irrationality; instead, the ascent of gold since 2001 has been steady, measured, and rational. What’s more, when compared to other commodities such as copper and oil, gold prices have not appreciated disproportionately. A simple glance at a chart comparing gold’s frenzied rise in 1979 to the gradual build-up of the past 10 years tells the story graphically: to me, it clearly suggests that the behavior of gold today has none of the attributes of a “bubble.”

If the last decade, fraught with insecurity, has driven up demand for gold, the question is, what happens next? None of us has a crystal ball, but all of us are determined to protect the assets we own or manage – and for the moment at least there is little doubt that gold is one of the best ways to protect the value of those assets.

While equities, debt markets, property and currencies – to name some of the more obvious forms of investment alternatives – have begun to recover in the past 18 months or so, there remain many ominous clouds on the geopolitical front. New risks continue to emerge, from growing political instability in the Middle East to the continued threat of terrorism. Meanwhile, excessive sovereign debt, huge unfunded government entitlement programs, an ever-greater use of quantitative easing, stalled economic growth in developed countries, stubbornly high unemployment, and an aging population are just some of the problems we have yet to resolve.

As we embark on a new decade, I can only conclude that the world is a long way from feeling secure. In fact, I believe we in the developed world have more reason today to be concerned and pessimistic than at any time in recent history – and with the outlook gloomy, there is, in my mind, no doubt that investors will continue to turn to gold as a rare safe haven.

Having made the case for gold generally, I’d like to comment on the past year at our Company, the world’s biggest gold producer. In 2010, Barrick recorded the most profitable year in its 27-year history, earning just under $3.3 billion. We increased production to 7.8 million ounces last year – and, despite the fact that currencies in most countries where we operate have appreciated against the U.S. dollar, our cash costs decreased to $457 per ounce.

Barrick’s remarkable performance led not only to record earnings, but also to record margins and cash flow. Thanks to the strength of our balance sheet, we were able to increase our dividend by 20%. Barrick’s share

3

Message from the Chairman

price, up 35% in 2010, outperformed both the price of gold and our peer group.

Meanwhile, our gold reserves now total 140 million ounces. And as the price of gold climbs, those reserves become increasingly valuable. Our new Cortez Hills mine in Nevada, for example, produced over 1.1 million ounces of gold in its first full year of operation – at a total cash cost of only $312 per ounce. Our Pueblo Viejo and Pascua-Lama projects, both of which we inherited through past acquisitions, will soon be contributing significant quantities of gold to our total production, again at low cash costs. Looking further ahead, our next generation of projects, including Cerro Casale and Donlin Creek, represent some of the most valuable gold assets in the world.

Whether it’s a question of financial strength or fiscal responsibility, basic operations or long-term strategic execution, Barrick’s track record is unmatched. For eight years in a row we have met or surpassed our annual targets. I’m also proud that we have achieved these extraordinary results while maintaining the highest commitment to corporate responsibility and integrity. We believe firmly in supporting the communities in which we operate, respecting the environment, and treating our employees and their families with dignity. From our senior management team to the individuals who work in our mines, from our directors to our support staff, Barrick’s team is composed of the most motivated and passionate people I have ever known. I am grateful to them all.

The newest member of our Board of Directors, Nathaniel Rothschild, represents yet another invaluable addition to Barrick’s brain trust. Nat is not only a member of one of Europe’s most prominent banking families, he is also an enormously successful financier and entrepreneur in his own right. Already, Nat’s knowledge of and experience in mining and resources have proven to be great assets to Barrick.

I noted earlier that I, unfortunately, don’t have a crystal ball. For one thing, I can’t promise that gold prices will keep rising. However, I can, with confidence, assure you that whatever happens in the world, Barrick will continue to lead the industry, always acting in the best interest of its shareholders. For nearly 30 years now, regardless of the price of gold, we’ve done just that.

/s/ Peter Munk | |

Peter Munk | |

Founder and Chairman | |

4

Barrick Annual Report 2010 | Message from the President and CEO

Message from the President and CEO

Aaron Regent

President and Chief Executive Officer

2010 was a record-breaking year for the gold industry. The appeal of gold as an investment grew significantly, reflecting persistent concerns about the global economy, geopolitical uncertainties and the outlook for global currencies. In many respects, the factors that have propelled gold prices to new highs intensified, pushing the metal to a new record of $1,431 per ounce.

The macroeconomic environment continues to be price supportive for gold. Expansionary monetary policies and quantitative easing programs have continued in order to stimulate economic growth and address high unemployment. In 2010, new sovereign debt concerns also emerged. The European Union announced bailouts for Greece and Ireland, while Spain and Portugal were also subject to credit concerns. The response to the bailouts has also led to a continued bias towards expansionary monetary policies. Global trade imbalances continue and a rebalancing will have an impact on the value of global currencies. As a monetary asset, gold’s value is determined relative to the value of other currencies. With downward pressure on currencies, gold’s relative value should continue to perform well. Meanwhile, geopolitical concerns have intensified with civil unrest and the potential for regime change throughout the Middle East, creating an increased environment of uncertainty and unpredictability.

Against this backdrop, investment demand for gold reached new records in 2010 and physical buying was strong. Central banks became net purchasers of gold after 21 years of selling. Physical demand, particularly from India and China, has also been very strong and is expected to continue. All of these factors underpin our positive outlook for gold prices going forward.

Our efforts to position Barrick as a prime beneficiary of a rising gold price, including the elimination of the Company’s gold hedges in 2009, helped to deliver record results for shareholders in 2010.

Operating results for the year met expectations, with higher gold production at lower cash costs compared to 2009. Gold production increased to 7.8 million ounces at total cash costs of $457 per ounce, or $341 per ounce on a net cash cost basis. Barrick also produced 368 million pounds of copper at total cash costs of $1.11 per pound. Strong operational results and consistent execution reflect the quality of the Company’s diversified portfolio, with 25 mines on four continents.

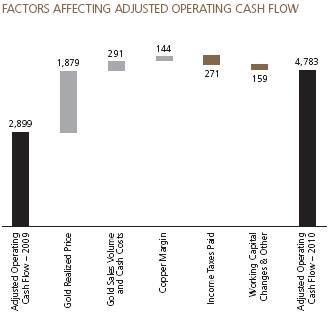

Our solid operational performance, combined with the increase in the gold price, resulted in record financial results. Adjusted net income for the year was $3.3 billion, an increase of 81% over 2009. This resulted in a return on equity of 19%. Adjusted cash flow from operations was $4.8 billion, up 65% from 2009.

Our leverage to the gold price was reflected in our financial results. While the gold price increased by 26% last year, Barrick realized record cash margins, which rose 48% to $771 per ounce, or $887 per ounce on a net cash cost basis. The Company’s earnings and cash flows per share have also significantly outpaced gold prices over the last six years, demonstrating the leverage we offer investors. While gold was up just over 200% in this period, Barrick’s cash flows per share have increased by over 400%, and earnings per share are up over 600%.

With record operating cash flows and expanding margins, Barrick continues to have the financial strength

5

Message from the President and CEO

to continue to invest in the business and meet our capital requirements while at the same time maintaining a strong balance sheet and returning capital back to shareholders. At year-end, the Company had about $4.0 billion in cash and a further $1.5 billion available through an undrawn line of credit, and we continue to have the gold industry’s only ‘A’ rated balance sheet. Given our financial position and the positive outlook for the Company, the Board of Directors authorized a 20% increase in the common share dividend in 2010. Over the past five years, the dividend has increased by about 120%.

Underpinning our annual production is a high quality and growing resource base. Targeted global exploration programs delivered excellent results, allowing Barrick to replace gold reserves in 2010 and grow gold resources. The Company has consistently replaced its reserves in each of the last five years, and we did so again in 2010. Gold reserves now stand at about 140 million ounces, the largest in the industry. In addition, measured and indicated gold resources grew 24% to 76 million ounces and inferred gold resources increased by 18% to 37 million ounces. Complementing our gold reserves and resources are 6.5 billion pounds of copper reserves, 13.0 billion pounds of measured and indicated copper resources and 9.1 billion pounds of inferred copper resources, plus 1.1 billion ounces of silver contained within gold reserves.

We continued to turn our resources into producing ounces with the advancement of our project pipeline. The Cortez Hills project in Nevada exceeded expectations in its first full year of production, boosting output at the Cortez property to 1.14 million ounces of gold in 2010.

We continued to make significant progress on our 60%-owned Pueblo Viejo project, located in the Dominican Republic. On a 100% basis, the project has gold reserves of over 23 million ounces. Barrick’s share of annual gold production in the first full five years of production is expected to average 625,000–675,000 ounces at total cash costs of $275–$300 per ounce. Work continues toward achieving key milestones.

What We Did in 2010

· Generated record net income and cash flow

· Return on equity increased to 19% from 12%

· Met targets to increase production at lower cash costs

· Completed Cortez Hills project on time and budget; ramp-up exceeded expectations

· Significantly advanced high return Pueblo Viejo and Pascua-Lama projects

· Acquired additional 25% ownership of Cerro Casale, a high quality, long life asset in a key region

· Identified significant new organic growth opportunities such as the potential to transform Turquoise Ridge into a large open pit operation

· Increased dividend by 20%

· Maintained license to operate:

· Achieved 22% improvement in total reportable injury frequency rate to 0.93

· Retained listings on the Dow Jones World and North America Sustainability Indexes and named to NASDAQ Global Sustainability Index

· First Canadian mining company to join the Voluntary Principles on Security and Human Rights

· Implemented Environmental Management System at all sites

· Maintained strong financial position and the industry’s only ‘A’ credit rating

· Replaced reserves and grew resources

· Completed IPO of African Barrick Gold

6

Barrick Annual Report 2010 | Message from the President and CEO

Construction at the Pascua-Lama project in Chile and Argentina is also progressing well, with initial production expected in 2013. This large, world-class project has approximately 18 million ounces of gold in reserves and 671 million ounces of contained silver. Once in operation, average annual production in the first full five years is expected to be 750,000–800,000 ounces of gold at total cash costs of $20–$50 per ounce, making Pascua-Lama one of the lowest cost gold mines in the world.

Looking further into the future, we continue to advance our next-generation projects, including Cerro Casale, Donlin Creek, Reko Diq and Kabanga. We have completed bankable feasibility studies for both Cerro Casale and Reko Diq, and we continue to work on improving the Donlin Creek feasibility study with the evaluation of a natural gas pipeline option for the project. In 2010, we also completed the acquisition of an additional 25% of Cerro Casale in Chile, which enabled us to gain control over this project and increase our metal exposure on a per share basis at attractive rates of return.

A greater emphasis on internal value creation has also surfaced some excellent opportunities within the Company’s existing portfolio. Combined with the production from our new mines under construction, this has positioned us to increase our production target to nine million ounces within five years. Beyond that horizon, we are currently evaluating an opportunity to transform the Turquoise Ridge Joint Venture in Nevada from a small underground mine to a large open pit operation. This would add another world-class asset to our portfolio.

The progress we made last year and the current position of the Company have been recognized by the market, as reflected by our strong share price performance in 2010. Barrick shares appreciated 35% last year, outperforming our peer group, and importantly, the gold price.

Our ability to meet our operating targets and advance our project pipeline is dependent upon maintaining a strong social license to operate. This means maintaining a strong safety culture, respecting the environment and achieving high standards of corporate and social responsibility.

What We Plan to Do in 2011

· Continue focus on increasing shareholder returns

· Meet production and cash cost targets

· Advance construction of Pueblo Viejo and Pascua-Lama and progress Cerro Casale towards a construction decision

· Continue to grow the net asset value of the Company and increase metal exposure per share by:

· maximizing free cash flow from existing operations

· growing reserves and resources

· advancing our pipeline of low cost, high quality projects

· pursuing selective acquisitions which are accretive to shareholder value

· Advance plans to achieve nine million ounce production target within five years

· Ensure license to operate through expanded CSR initiatives

· Preserve financial strength and the industry’s highest-rated balance sheet

· Continue trend of strong earnings and cash flow generation

7

Message from the President and CEO

As such, we continue to focus our efforts on enhancing and improving our performance in these areas.

At Barrick, we announced several initiatives in 2010 to further strengthen the Company’s corporate social responsibility (CSR) performance. We became the first Canadian mining company to join the Voluntary Principles on Security and Human Rights, a set of guidelines by which companies in the extractive sector can maintain the safety and security of their operations while ensuring respect for human rights and fundamental freedoms.

We also announced a plan to establish an external CSR Advisory Board that will provide advice and guidance to Barrick on challenging social and environmental issues and encourage further innovation and leadership in CSR. Consistent with these objectives, Barrick will also appoint an independent Director to its Board of Directors to support our commitment to CSR.

Our efforts in this area continue to be recognized. Barrick was once again listed on the Dow Jones World Sustainability Index, and the Company was added to the NASDAQ Global Sustainability Index, which tracks the world’s top 100 companies in this area.

Improving our safety performance will continue to be a priority in 2011. We achieved a significant reduction in total reportable injuries in 2010, however, the success we achieved was overshadowed by six fatalities during the year. This is unacceptable to me, and to everyone at Barrick. We will not rest in our efforts to improve until every person goes home safe and healthy every day. We have redoubled our efforts and have intensified our focus on critical risks, Visible Felt Leadership and incident investigation.

Looking ahead, the outlook for Barrick and our industry continues to be very bright. We expect the gold price will continue to be well supported. Our production levels in 2011 should be comparable to 2010 and will continue to trend higher as we make progress towards reaching our nine million ounce target. We have made considerable progress in controlling our operating costs but they will be higher in 2011 as we mine lower grade material, however, the impact is expected to be more than offset by higher gold prices. As a result, we should have another strong year of financial performance. Looking beyond 2011, Barrick’s cost profile should be stable as we benefit from the contribution of our new, low cost projects, including Pueblo Viejo and Pascua-Lama. In addition to these, we have a deep pipeline of other projects which will be augmented over time as a result of exploration success and the acquisition of new properties. Our focus on value creation, leveraging Barrick’s expertise and capabilities, has yielded significant results and I am confident that more can be done in this area to create further value for our shareholders.

In conclusion, I want to finish by recognizing the more than 20,000 employees around the world who work tirelessly to achieve the results that drive our performance. When I joined Barrick, I visited the Company’s mines and offices on four continents, and one thing struck me everywhere I went: the exceptional quality of our people. Two years later, my initial impressions have only intensified, and I want to thank the entire Barrick team for making this a great Company. Finally, I would also like to extend my gratitude to our Founder and Chairman, Peter Munk, and to the Board of Directors and our shareholders for their continued support and advice over the past year.

/s/ Aaron Regent | |

Aaron Regent | |

President and Chief Executive Officer | |

8

Barrick Annual Report 2010 | Focus on Value Creation

Focus on Value Creation

At Barrick, our primary goal is to maximize the value of the Company in a socially responsible way for the benefit of all our stakeholders. Our strategy is focused on increasing net asset value, production, reserves and earnings – all on a per share basis.

Barrick has a strong track record of creating value at its existing mines and projects. In 2010, our regional business units were given a clear mandate to unlock the full potential of our assets and took a fresh look at their portfolios to identify value creation opportunities and maximize free cash flow. This has resulted in our target to profitably increase production to nine million ounces within five years(1), and has uncovered some exciting prospects, including the open pit potential at Turquoise Ridge and other options to surface hidden value at our existing mines.

In support of this sharpened focus on value creation, our strategy is centered on investing in high return development projects such as Pueblo Viejo and Pascua-Lama, increasing our gold and copper reserves through both exploration and selective, accretive acquisitions, maximizing the value of our existing mines and leveraging our technical skills and regional infrastructure to commercialize new deposits. We recognize that our ability to be successful in the long run depends on a high standard of corporate social responsibility, and while Barrick has a strong social license, we continually strive to improve our social and environmental performance.

Our efforts are supported by our ‘A’ rated balance sheet, our management bench strength and the high quality of our employees, all of which position us to meet our goals. Barrick is focused on building long life, high return projects and is one of the few companies with the expertise and broad set of resources to develop large scale mines that are expected to provide lower cost ounces to the Company for the next several decades. The quality of these projects also enables us to be highly disciplined with respect to external opportunities, which are consistently benchmarked against our existing pipeline.

Our commitment to creating value should not only help us achieve our targeted production growth in what we expect to be a strong gold price environment, but also enable the Company to continue returning additional value to our shareholders.

From left: Jamie Sokalsky, Kelvin Dushnisky, Peter Kinver and Aaron Regent.

(1) The target of nine million ounces of annual production within five years reflects a current assessment of the expected production and timeline to complete and commission Barrick’s projects currently in construction (Pueblo Viejo and Pascua-Lama); and the Company’s current assessment of existing mine site opportunities, some of which are sensitive to metal price and various capital and input cost assumptions.

9

Exceptional Gold Price Leverage

Exceptional Gold Price Leverage

Gold surged to record-breaking highs in 2010 above $1,430 per ounce, recording its tenth straight year of price gains. Bullion continues to benefit from a myriad of price supportive factors which have driven robust investment demand, including a macroeconomic environment reflecting accommodative fiscal policies and ongoing monetary reflation, persistent sovereign debt issues in Europe and significant global trade and current account imbalances.

The global fiscal and monetary policies designed to stimulate economic recovery have had the dual effect of reducing the value of the world’s major currencies and affirming gold’s role in global portfolios. Central banks became net buyers of gold in 2010 for the first time in 21 years in an effort to diversify their holdings and address excessive foreign exchange reserves. Investor demand in the emerging economies of China and India is just beginning to ramp up, particularly following further measures to liberalize the Chinese gold market in 2010. We expect these trends to continue, along with a longer term contraction in mine supply as new discoveries become scarcer and as permitting timelines and requirements to bring new production on line have lengthened and become more complex.

Against this positive backdrop, Barrick offers investors a compelling combination of exceptional leverage through the benefits of active management relative to the gold ETF and lower risk compared to less diversified gold producers through our global portfolio of operations, as well as a competitive dividend yield. This leverage is backed by the industry’s largest gold reserves and production, a disciplined focus on value creation, and a strong balance sheet that enables us to pursue our strategy and goals.

10

Barrick Annual Report 2010 | Financial Strength and Flexibility

Financial Strength and Flexibility

In 2010, Barrick successfully grew its production and lowered its cash costs, bucking the industry trend to higher costs. The Company achieved its fifth straight year of margin expansion with record cash margins of $771 per ounce(1) or $887 per ounce(1) on a net cash cost basis, reflecting cash margin growth of 48% versus gold’s 26% rise. Combined with higher production of 7.8 million ounces, this resulted in record 2010 adjusted earnings and adjusted operating cash flow of $3.3 billion and $4.8 billion, respectively, as well as significant free cash flow of $1.5 billion(1), despite making substantial investments in our projects. Our ‘A’ credit rating and robust financial position – including cash of $4.0 billion, a $1.5 billion undrawn line of credit and strong operating cash flow – position us to continue executing on our project development plans and give us the flexibility to pursue other high return value creation opportunities within our portfolio.

Our excellent financial results have driven growth in our return on equity to 19% and enabled us to return additional capital to shareholders, while continuing to invest in our high return projects. Barrick has raised its dividend by nearly 120% in the past five years as gold prices have appreciated, including a 20% increase in 2010. This steady dividend growth reflects both the Company’s continued financial strength and our favorable outlook for gold.

Going forward, we expect to increase Barrick’s superior leverage to gold as our long life, high quality projects in construction – Pueblo Viejo and Pascua-Lama – begin contributing substantial new low cost production in the coming years. Beyond this, we see tremendous potential in our feasibility stage projects such as Cerro Casale, Donlin Creek and Reko Diq and in value creation opportunities underway at operating mines such as Turquoise Ridge and Zaldívar.

(1) Non-GAAP financial measure – see pages 78–85 of the 2010 Financial Report.

“Barrick generated record earnings and cash flow in 2010 as we increased production at lower cash costs, while continuing to invest in our high return projects. We were also able to return more capital to shareholders, raising the dividend by 20%.” Jamie Sokalsky, Executive Vice President and Chief Financial Officer |

|

11

Operational Excellence

Operational Excellence

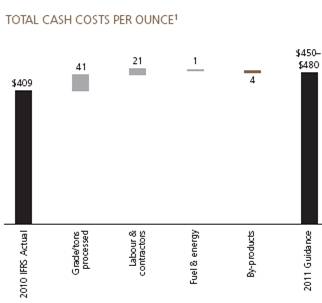

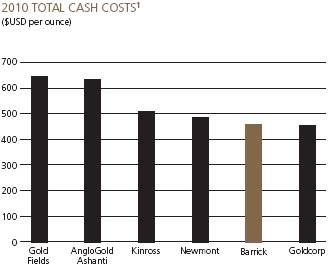

Our high quality, diversified asset base is a key driver that enables us to consistently meet targets and expectations. Barrick produced 7.8 million ounces of gold in 2010 at total cash costs of $457 per ounce or net cash costs of $341 per ounce, remaining the industry production leader at competitive cash costs. The Company delivered on its production target and, despite higher royalties and taxes associated with a year of record gold prices, was able to maintain cash costs in line with guidance, illustrating the flexibility of our 25-mine portfolio, the active management of our input costs and another year of strong operating performance from our regional business units.

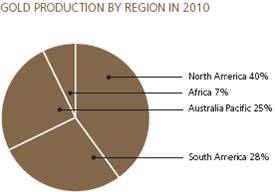

Our largest operating region, North America, contributed 3.11 million ounces of gold in 2010, primarily from its cluster of seven mines in Nevada. The expanded Cortez mine had an excellent year, producing 1.14 million ounces of gold at total cash costs of $312 per ounce with nearly a full year of production from Cortez Hills, which had a smooth ramp-up from both the open pit and underground operations. We expect to receive a Record of Decision in early 2011, allowing the mine to revert to its original scope. Barrick has added significant value to the Cortez

The Cortez Hills underground operation had a smooth ramp-up.

12

Barrick Annual Report 2010 | Operational Excellence

Cortez Case Study – Value Added Since Acquisition

2006 | | 2010 | | Future Value Creation Opportunities |

| | | | |

6.3 M oz of reserves(1) | | 14.5 M oz of reserves(1) | | Cortez Hills Middle and Lower |

60% interest | | 100% interest | | Zone extensions |

Pipeline: declining, | | Cortez: 1.1 M oz low cost | | Significant regional opportunities |

higher cost mine | | mine generating significant | | on underexplored 1,080 square |

| | cash flow | | mile property |

(1) 2006 and 2010 reserves reflect Barrick’s 60% and 100% interest, respectively. See page 22 of the 2010 Annual Report for additional information on Barrick’s reserves.

property since its acquisition in 2006 (see case study) by consolidating 100% ownership, expanding reserves and resources and bringing the world-class Cortez Hills deposit into production. We expect to create additional value through exploration success on this highly prospective property.

Our low cost South America region contributed 2.12 million ounces in 2010. The Veladero mine in Argentina had an outstanding year, producing more than 1.1 million ounces at total cash costs of $256 per ounce on higher grades and expanded throughput, while the Lagunas Norte mine in Peru contributed over 0.8 million ounces at total cash costs of $182 per ounce after producing more than one million ounces for four straight years. As a result of higher gold prices, the Pierina mine in Peru is now expected to continue operations until the end of 2014.

Led by the Porgera mine in Papua New Guinea, which celebrated its 20th year of production, our Australia Pacific business unit produced 1.94 million ounces in 2010. As of year-end 2010, the Company is 92% hedged on all of its Australian operating and capital expenditures for 2011 at an average rate of $0.79, 84% hedged for 2012 at an average rate of $0.75, and has substantial coverage for the following two years at rates at or below $0.75.

African Barrick Gold produced 0.56 million equity ounces to Barrick as issues with transitional oxide ore and the impact of actions taken in

“ Our diverse portfolio of operations enabled us to meet guidance for the eighth straight year in 2010. We also made excellent progress advancing our high quality projects – Cortez Hills had a successful ramp-up and we expect Pueblo Viejo and Pascua-Lama to contribute significant new low cost ounces in the coming years.” Peter Kinver, Executive Vice President and Chief Operating Officer | |

|

13

Operational Excellence

response to the fuel theft at Buzwagi resulted in lower than expected production for the year. The Company was admitted to the benchmark FTSE 100 Index during the year, signaling its stature among the most highly capitalized London-listed companies.

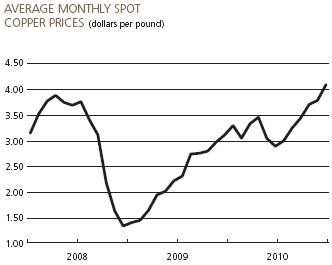

Barrick’s core gold business continued to profit from the reinvestment of strong cash flow from our two copper operations in 2010 as copper prices strengthened. Production from the large Zaldívar operation in Chile and the smaller Osborne mine in Australia, which was sold during the year, was 368 million pounds at total cash costs of $1.11 per pound, generating cash margins of 67%.

For 2011, Barrick forecasts equity production comparable to 2010 in the range of 7.6–8.0 million ounces at total cash costs and net cash costs of $450–$480 per ounce and $340–$380 per ounce(1), respectively. The Cortez Hills and Goldstrike mines in Nevada, the Veladero mine in Argentina and Porgera in Papua New Guinea are anticipated to make strong contributions.

Beyond 2011, the Company is targeting organic production growth to nine million ounces within five years and total cash costs to benefit from the start-up of its low cost Pueblo Viejo and Pascua-Lama projects.

(1) Net cash costs assume a realized copper price of $3.75 per pound for 2011.

14

Barrick Annual Report 2010 | Project Development Expertise

Project Development Expertise

One of Barrick’s distinctive hallmarks is its industry-leading technical expertise and strong track record of commercializing deposits from its pipeline of world-class development projects. Having delivered seven new mines in the past five years, Barrick has a reputation for successful mine development and a history of extracting further value from its assets post discovery or acquisition. This tradition of excellence and value creation is built on decades of experience acquired in building and operating a diverse set of mines in remote and often challenging operating environments around the globe.

The Cortez Hills project in Nevada is Barrick’s newest achievement, completed on time and budget in early 2010.

Our two world-class projects in construction, Pueblo Viejo in the Dominican Republic and Pascua-Lama on the border of Chile and Argentina, are forecast to contribute an average annual total of 1.4 million ounces(1) at low total cash costs when in full production, illustrating the significant impact these mega projects will have in strengthening the quality of Barrick’s portfolio.

As of February 2011, the 24,000 tonne per day Pueblo Viejo project was about 50% complete, with approximately 75% of its pre-production capital budget of about $3.3–$3.5 billion (100% basis) committed and first production expected in Q1 2012. All four autoclaves, the gold industry’s largest, have been installed and are in the process of being bricklined, and the main columns for the 4,000 tonne per day oxygen plant have been erected. In December

(1) Based on average production for both projects in their first full five years once both are at full capacity.

15

Project Development Expertise

2010, the Environmental Impact Assessment for the 240 kV power transmission line was approved, allowing associated construction activities to commence. Barrick’s 60% share of gold production from Pueblo Viejo in the first full five years of operation is expected to average 625,000–675,000 ounces at total cash costs of $275–$300 per ounce(2). Barrick has added considerable value to Pueblo Viejo since acquiring it in the 2006 Placer Dome transaction (see case study), expanding reserves by more than 75% and transforming this asset into a high return project with a mine life of more than 25 years. Applying in-house expertise, Barrick’s metallurgists dramatically improved silver and copper recoveries and the overall flowsheet, creating a significantly more robust project. A circuit to recover about three billion pounds of contained zinc is under evaluation, and the Company continues to explore options for longer term, lower cost power options.

Major progress was made in 2010 on advancing construction of the world-class Pascua-Lama gold-silver project on the border of Chile and Argentina, which is expected to enter production in the first half of 2013. As of February 2011, approximately 40% of the pre-production budget of about $3.3–$3.6 billion had been committed. Anticipated average annual production of 750,000–800,000 ounces at

High purity oxygen from the plant will be injected into the Pueblo Viejo autoclaves to release the gold.

Pueblo Viejo Case Study – Value Added Since Acquisition

2006 | | 2010 | | Future Value Creation Opportunities |

13.4 M oz of reserves(3) | | 23.7 M oz of reserves(3) | | Circuit to recover ~three billion |

Modest economics | | Robust economics | | pounds of contained zinc |

Technical challenges, | | Improved flowsheet, | | Longer term, lower cost |

low recoveries | | increased recoveries | | power options |

Au: 92% | | Au: 92% | | Reserve/resource upside |

Ag: 5% | | Ag: 87% | | |

Cu: 0% | | Cu: 79% | | |

(2) Based on gold and oil price assumptions of $1,100 per ounce and $85 per barrel, respectively.

(3) 100% basis. Barrick has a 60% interest in Pueblo Viejo. See page 22 of the 2010 Annual Report for additional information on Barrick’s reserves.

16

Barrick Annual Report 2010 | Project Development Expertise

total cash costs of $20–$50 per ounce(4) in the first full five years illustrates the positive impact this mega project will have on the Company’s overall portfolio. Each $1 per ounce increase in the price of silver is expected to reduce total cash costs by about $35 per ounce over this period.

As of February 2011, detailed engineering had been advanced to more than 90% completion. The four kilometer long ore tunnel connecting the mine in Chile with the processing plant in Argentina has been collared from both sides and is expected to be completed in the second half of 2012. Construction of the power transmission line is underway and the new access road is about 75% complete. With 17.8 million ounces of gold reserves and 671 million ounces of silver contained within the gold reserves, Pascua-Lama is expected to contribute very low cost ounces to Barrick over a mine life in excess of 25 years.

At the large Cerro Casale gold-copper project in Chile’s Maricunga district, detailed engineering was about 30% complete as of February 2011.

An excavator preparing the pebble crusher platform frames the tunnel portal in Argentina.

(4) Based on gold and oil price assumptions of $1,100 per ounce and $85 per barrel, respectively, and applying silver credits assuming a by-product silver price of $16 per ounce and assuming a Chilean peso f/x rate of 500:1.

17

Project Development Expertise

The review and timing of additional permitting requirements to accommodate changes to project design before considering a construction decision are being assessed alongside consultation with local communities and indigenous peoples.

A review is currently underway to determine the impact of a stronger Chilean peso and higher labor costs in Chile on expected capital and operating costs. An update will be provided by the end of the second quarter.

Next Generation of Projects

Barrick’s next tier of projects includes the Donlin Creek gold project in Alaska, the Reko Diq project in Pakistan and the Kabanga nickel project in Tanzania, all of which have progressed to the feasibility stage and represent significant option value within our portfolio.

The Donlin Creek 50-50 joint venture is one of the largest undeveloped gold projects in the world, with nearly 39 million ounces of measured and indicated gold resources and the potential to produce more than one million ounces per year (100% basis). Additional optimization work to evaluate the use of natural gas to reduce operating costs is expected to be completed in the third quarter of 2011.

At the 37.5% -owned Reko Diq copper-gold project in Pakistan, the initial mine development feasibility study and the environmental and social impact assessment are both complete. A copy of the feasibility study has been delivered to the government of Balochistan in accordance with the terms of the joint venture agreement with the government. The project company, Tethyan Copper, made an application for a mining lease on February 15, 2011(1).

A feasibility study and environmental and social impact assessment for the Kabanga nickel project in Tanzania, one of the world’s largest undeveloped nickel sulfide deposits, is expected to be completed in the first half of 2011. Acquired through an earlier gold acquisition, the project is a 50-50 joint venture with operator Xstrata Plc and hosts a measured and indicated resource of 2.2 billion pounds of nickel (100% basis). Barrick will consider how to extract the best value from this high quality asset for its shareholders.

Barrick’s 75%-owned Cerro Casale project in Chile is one of the world’s largest undeveloped gold-copper deposits and is located in a core region for the Company.

(1) As of February 2011, the Supreme Court of Pakistan was hearing several constitutional petitions relating to the Reko Diq project, which, among other things, challenge the government’s right to grant a mining lease to Tethyan Copper.

18

Barrick Annual Report 2010 | Surfacing Hidden Value

Surfacing Hidden Value

In addition to the world-class Pueblo Viejo and Pascua-Lama projects, which are expected to contribute significant new ounces at costs substantially lower than our current profile, we are focused on maximizing the value of our existing mines where we see new potential to organically grow production and extend mine life. With a strong mandate to create value, our regions carried out a rigorous re-evaluation of their portfolios in 2010 and identified a number of exciting options to surface hidden value.

The most significant of these came to light with a fresh look at our 75%-owned Turquoise Ridge mine in Nevada, which unearthed the potential to develop a large scale open pit to mine the lower grade halo around the high grade core. An open pit operation could conceptually quadruple total annual production to up to about 800,000 ounces a year from current annual production of 150,000–200,000 ounces based on 2010 reserves of 5.6 million ounces, measured and indicated resources of 11.2 million ounces and inferred resources of 6.9 million ounces(1). A scoping study and Phase 2 infill drill program is currently underway in support of a prefeasibility study which is expected to be completed in 2012, followed by a feasibility study in 2013. Early metallurgical testing indicates strong recoveries using acid autoclaving. While this project is beyond our nine million ounce target production timeframe, it provides excellent potential to make substantial contributions to production in the future.

At the Goldstrike Complex in Nevada, our metallurgists have been successful in piloting a thiosulphate leaching flow sheet after the autoclave process that enables treatment of mixed carbonaceous material previously routed to the roaster. We expect this will extend the life of the autoclaves and help support production rates at Goldstrike. There is good potential to apply this process and enhance efficiencies at other mines.

(1) 100% basis. Assumes a gold price of $975 per ounce. Feasibility, permitting and construction are estimated to take ~8 years. Key permits and approvals needed include: Environmental Impact Statement, Plan of Operations Approval, Clean Water Act Section 404 Permitting, Mercury Control Permits, Water Pollution Control Permit.

19

Surfacing Hidden Value

With the receipt of permits in 2010, a significant expansion commenced at the Bald Mountain mine in Nevada and is expected to be complete by late 2011, increasing annual production from 100,000 ounces to 150,000–200,000 ounces per year and extending the mine life by 10 years. The unified plan includes expanded process facilities, the merger of the North pits and the inclusion of several satellite pits. A proposed layback at the Hemlo mine in Ontario may also significantly extend the mine life at this operation.

The Lagunas Norte mine in Peru is one of the Company’s lowest cost producers, and has consistently outperformed our expectations since its start-up in 2005. We have defined some viable targets around the mine site, including the deeper sulfide ore, which have good potential to extend the mine life by four years with an additional two million ounces.

At Zaldívar, our large copper producer in Chile, where there are existing reserves of 6.5 billion pounds of copper plus a measured and indicated resource of 1.3 billion pounds, the deeper primary sulfides underneath the current open pit potentially offer an additional six billion pounds of copper containing about 2.4 million ounces of gold. The sulfides potentially represent an additional one billion tonnes that could overlap with the existing operation and extend the mine life by about 16 years(2). A prefeasibility study is expected to commence in the second quarter of 2011.

Our 2010 review also identified other brownfield opportunities which could increase production or extend the mine lives at the Kalgoorlie, Cowal, Granny Smith, and Porgera mines in our Australia Pacific region.

(2) Additional exploration and engineering is required to define the deep sulfide potential and it is uncertain whether Barrick will be able to define this potential resource. Development of Zaldívar deep sulfides assumes copper and gold prices of $2.50 per pound and $900 per ounce, respectively.

20

Barrick Annual Report 2010 | Industry’s Largest Gold Reserves

Industry’s Largest Gold Reserves

Barrick has a strong history of finding new ounces to replenish its gold reserves and resources, and we continued this tradition in 2010 by replacing our industry leading reserves of about 140 million ounces, despite reducing our equity interest in African Barrick Gold. Just as importantly, we strengthened our underlying resources, growing measured and indicated ounces by 24% to over 76 million ounces and increasing inferred resources by 18% to over 37 million ounces.

Our success at maintaining the industry’s largest reserve base can be largely attributed to our sustained approach to funding exploration, our deep technical expertise and disciplined approach to pipeline management, and an integrated alignment with corporate development. This strategy(1) has resulted in Barrick’s significant land positions on many of the world’s most prospective gold and copper trends, including the underexplored El Indio belt in Chile and Argentina and the Cortez Trend in Nevada. Barrick’s reserves continue to be largely situated in lower risk areas, with about 65% located in investment grade countries(2) including Chile, Australia, the United States and Canada.

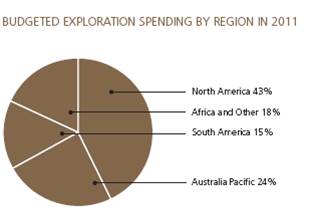

As a result of exploration success in 2010, our 2011 exploration budget is expected to increase by over 50% to $320–$340 million. Of the total, about 43% will be allocated to North America, with the majority targeted for Nevada to upgrade resources at Turquoise Ridge, where drilling continues in support of the scoping study, and to outline additional resources at Cortez. The Cortez property remains highly prospective, with excellent potential to add new ounces to the current 14.5 million ounce reserve from the Cortez Hills Middle and Lower Zones and from regional targets on our 1,080 square mile land position. The 2011 budget continues to be heavily weighted towards brown-field exploration around our existing operations, while still supporting substantial generative efforts to explore for large deposits, particularly in highly endowed, underexplored areas such as Papua New Guinea and El Indio. Activities in the El Indio area have been refocused to explore for gold-copper porphyry targets and have outlined 19 high priority targets, several of which will be drilled in 2011.

Over the past 20 years, Barrick’s exploration group has had excellent success at finding high quality, lower

(1) Barrick’s exploration programs are designed and conducted under the supervision of Robert Krcmarov, Senior Vice President, Global Exploration of Barrick. For information on the geology, exploration activities generally, and drilling and analysis procedures on Barrick’s material properties, see Barrick’s most recent Annual Information Form/Form 40-F on file with Canadian provincial securities regulatory authorities and the U.S. Securities and Exchange Commission.

(2) BBB- or higher as rated by Standard and Poor’s.

“Our exploration group is aligned with Barrick’s business needs and understands how to maximize the chances of success. In 2010, Barrick successfully replaced its reserves, marking the fifth straight year we have done so, and substantially grew resources. It’s a testament to the depth and quality of our project pipeline and people.” Rob Krcmarov, Senior Vice President, Global Exploration | |

|

21

Industry’s Largest Gold Reserves

cost ounces, identifying and delivering notable increases at Pascua-Lama, Lagunas Norte, Veladero, Pueblo Viejo, Cortez, Turquoise Ridge, and Donlin Creek.

Our key mines and projects continue to demonstrate strong exploration potential, positioning the Company to extract further value from its high quality portfolio through the drill bit.

Night drilling tests regional targets on Barrick’s highly prospective Nevada land package.

Reserves and Resources Summary(1),(2),(3)

at December 31, 2010 | | Proven and | | Measured and | | Inferred | |

(Barrick’s equity share) | | Probable Reserves | | Indicated Resources | | Resources | |

Gold (000s oz) | | 139,786 | | 76,319 | | 37,202 | |

North America | | 56,783 | | 45,573 | | 16,772 | |

South America | | 53,922 | | 10,265 | | 6,284 | |

Australia Pacific | | 16,568 | | 16,464 | | 11,331 | |

Africa | | 12,429 | | 3,967 | | 2,748 | |

Other | | 84 | | 50 | | 67 | |

| | | | | | | |

Other Metals | | | | | | | |

Copper (M lbs) | | 6,514 | | 13,014 | | 9,149 | |

Nickel (M lbs) | | — | | 1,080 | | 596 | |

Other Metals Contained in:

| | Proven and | | Measured and | | Inferred | |

| | Probable Gold Reserves | | Indicated Gold Resources | | Gold Resources | |

Silver (000s oz) | | 1,066,332 | | 232,890 | | 61,647 | |

Copper (M lbs) | | 5,735 | | 1,164 | | 1,563 | |

(1) Mineral reserves (“reserves”) and mineral resources (“resources”) have been calculated as at December 31, 2010 in accordance with National Instrument 43-101 as required by Canadian securities regulatory authorities. For United States reporting purposes, Industry Guide 7, (under the Securities and Exchange Act of 1934), as interpreted by Staff of the SEC, applies different standards in order to classify mineralization as a reserve. Accordingly, for U.S. reporting purposes, Cerro Casale is classified as mineralized material. In addition, while the terms “measured”, “indicated” and “inferred” mineral resources are required pursuant to National Instrument 43-101, the U.S. Securities and Exchange Commission does not recognize such terms. Canadian standards differ significantly from the requirements of the U.S. Securities and Exchange Commission, and mineral resource information contained herein is not comparable to similar information regarding mineral reserves disclosed in accordance with the requirements of the U.S. Securities and Exchange Commission. U.S. investors should understand that “inferred” mineral resources have a great amount of uncertainty as to their existence and great uncertainty as to their economic and legal feasibility. In addition, U.S. investors are cautioned not to assume that any part or all of Barrick’s mineral resources constitute or will be converted into reserves. Calculations have been prepared by employees of Barrick, its joint venture partners or its joint venture operating companies, as applicable, under the supervision of Rick Sims, Senior Director, Resources and Reserves of Barrick, Chris Woodall, Senior Director, Mining of Barrick and John Lindsay, Senior Director Metallurgy, of Barrick. Except as noted below, reserves have been calculated using an assumed long-term average gold price of $US 1,000 ($Aus. 1,180) per ounce, a silver price of $US 16.00 per ounce, a copper price of $US 2.00 per pound and exchange rates of $1.05 $Can/$US and $0.85 $US/$Aus. Reserves at Round Mountain have been calculated using an assumed long-term average gold price of $US 900. Reserve calculations incorporate current and/or expected mine plans and cost levels at each property. Varying cut-off grades have been used depending on the mine and type of ore contained in the reserves. Barrick’s normal data verification procedures have been employed in connection with the calculations. Resources as at December 31, 2010 have been estimated using varying cut-off grades, depending on both the type of mine or project, its maturity and ore types at each property. For a breakdown of reserves and resources by category and for a more detailed description of the key assumptions, parameters and methods used in calculating Barrick’s reserves and resources, see Barrick’s most recent Annual Information Form/Form 40-F on file with Canadian provincial securities regulatory authorities and the U.S. Securities and Exchange Commission.

(2) 2009 reserves and resources for the Cerro Casale project reflect Barrick’s then 50% interest. In March 2010, Barrick acquired an additional 25% of Cerro Casale. 2010 reserves and resources reflect Barrick’s 75% interest.

(3) In March 2010, Barrick created African Barrick Gold plc to hold its African gold mines, gold projects and gold exploration properties. As of April 2010, Barrick owns approximately 73.9% of African Barrick Gold plc.

22

Barrick Annual Report 2010 | Strong Focus on Responsible Mining

Strong Focus on Responsible Mining

Corporate Social Responsibility

As public expectations of the mining industry continue to rise, corporate social responsibility has never been more important. Barrick renewed and increased its focus on CSR in 2010. Efforts were aimed at further strengthening Barrick’s global performance in such areas as community relations, environmental management, security and human rights, and corporate governance.

Barrick works with governments and NGOs to ensure the provision of basic health services and improve community health.

Barrick’s CSR performance and alignment with international standards continue to be recognized. We are proud to be listed for the third consecutive year as a world leader in social and environmental responsibility by the Dow Jones World Sustainability Index. This also marks the first year that the Company has earned a place on the NASDAQ Global Sustainability Index of the top 100 companies worldwide. In addition, the Carbon Disclosure Project named Barrick a climate disclosure leader for the Company’s climate change strategy and reporting practices.

Strengthening Corporate Governance

To enhance expertise in CSR at the most senior level of the Company, Barrick announced a plan to establish an external CSR Advisory Board that will provide advice and guidance to Barrick on challenging social and environmental issues and encourage further innovation and leadership. Barrick will also appoint an independent Director to its Board of Directors to support our commitment to CSR. A search is underway to fill this position in 2011.

Commitment to Human Rights

Since 2005, Barrick has invested more than $33 million to build schools and improve education around the world.

Barrick is committed to protecting human rights and dignity at its operations around the world. In 2010, Barrick became the first Canadian mining company to be admitted to formally join the Voluntary Principles on Security and Human Rights, a set of guidelines by which companies in the extractive sector can maintain the safety and security of their operations while ensuring respect for human rights. We are advancing the implementation of the Voluntary Principles, engaging in the tripartite process with NGOs, extractive sector companies and government members, while working closely with local communities. This is particularly important in the complex environments in

23

Strong Focus on Responsible Mining

which Barrick operates and faces ongoing challenges, and where it is further strengthening its policies and compliance with these human rights principles.

Effective Engagement with our Stakeholders

At Barrick, we understand the value of relationships. Our ability to be successful as a company depends on being able to engage effectively with governments, civil society and our host communities. By being responsive to the issues and expectations of our stakeholders, we build trust and reduce business risks over the long term.

In 2010, Barrick completed a third-party assurance process of our performance and alignment with the International Council on Mining and Metals Sustainable Development Framework. While the overall results of this evaluation were positive, we also received constructive feedback and recommendations for improvements.

More than 5,000 people have participated in Barrick’s adult literacy program in Papua New Guinea.

For example, based on the input received, we have enhanced communications on issues of concern to our external stakeholders. Going forward, this assurance process will be conducted on an annual basis. We are also further strengthening our grievance mechanisms at all sites to ensure communities have a voice and a systematic way to resolve complaints, while building the capacity of the Company’s community relations function.

Creating a Positive Legacy

Barrick continues to make significant investments in community programs that take into account local development needs and priorities. As the Company has grown, our investments in such areas as health and education continue to expand. Our community programs are wide-ranging: from

24

Barrick Annual Report 2010 | Strong Focus on Responsible Mining

fighting HIV/AIDS and bringing electricity to towns in Tanzania to improving child nutrition and maternal health in Peru, assisting local farmers and suppliers in Chile and Argentina and providing adult literacy programs in Papua New Guinea and the Dominican Republic.

Globally, our operations are a catalyst for social and economic development and contribute to a higher standard of living. A study of the impact of the Pierina mine in Peru documented a decline in the poverty rate from 80% to 31% in one local district from 1993–2007. In developing regions, large-scale skills training programs are conducted to enable thousands of local people to join our workforce, while entrepreneurs can receive training to become suppliers to our operations. These are just some of the ways Barrick is maximizing the positive benefits of our operations and improving our CSR performance globally.

Environmental Stewardship

Around the world, Barrick operates to high environmental standards and is committed to continuous improvement. Consistent with this commitment, Barrick’s Environmental Management System (EMS) was implemented at all sites in 2010 and underwent a third-party review to identify possible areas of improvement. The Company also completed a three-year risk assessment to review the safety of tailings impoundments at all operations and closed sites. A tailings guidance manual was developed to ensure the Company is meeting or exceeding industry best practice in this area.

Pursuing Industry Leadership

In 2010, the Company also set its sights on industry-wide issues, such as addressing water use, safeguarding biodiversity, and reducing energy use and greenhouse gas (GHG) emissions.

Water conservation is an area where Barrick is demonstrating leadership, reflected in improved, more systematic management and monitoring of water use at our operations. Three industry-leading water conservation pilot projects are now underway at sites in Australia, Tanzania and North America. Eighteen Barrick mines are zero water discharge operations, with all water recycled and reused for mining processes on site. In 2011, Barrick will participate in the Water Disclosure Project to contribute to greater understanding of global industrial water use.

“Barrick made significant strides in its approach to responsible mining in 2010. We recognize the importance of proactively engaging with communities, governments and other stakeholders to ensure we maintain strong support for our operations. By challenging ourselves to improve, we have become a stronger and better company, positioned for even greater success in the future.” Kelvin Dushnisky, Executive Vice President, Corporate and Legal Affairs |

|

25

Strong Focus on Responsible Mining

In the area of biodiversity, Barrick is pursuing new territory for the industry. The Company is engaging with leading experts to put our biodiversity standard into practice and better manage, mitigate and offset biodiversity impacts. At the Kanowna Belle mine in Australia, Barrick is piloting the Nature Conservancy’s Development by Design strategy, a science-based approach to conservation planning and mitigation. In the Dominican Republic, a second pilot project to protect local species near the Pueblo Viejo project is also underway.

For the second year, the Company has established regional targets to improve energy and carbon efficiency at all operations. Overall, Barrick has improved ore processes, resulting in less GHG emissions per tonne of ore processed. Using this measure, Barrick’s emissions decreased 15% from 2006 to 2009. Barrick is also now completing a mercury abatement program which aims to control and reduce mercury emissions from processing facilities at our operations.

Barrick has long been a leading advocate of the International Cyanide Management Code, having achieved Code certification at 20 operations – more than any other gold producer. Code recertification of six operations has already been completed. In collaboration with the Mining Association of Canada, the Company is taking this commitment one step further by publicly advocating that Code safety standards and certification become standard practice within the gold mining industry.

Environmental Leadership from Within

Looking ahead, Barrick also plans to participate in a World Wildlife Fund (WWF) internship program that will provide future company leaders with an unparalleled opportunity to participate in the environmental programs of this respected organization around the world. Participants will work with WWF’s world-class scientists to gain a greater appreciation of the need to manage environmental impacts as well as the significance of company decision-making on the environment. This internship program complements new employee awards to acknowledge environmental leadership. Finally, in 2011, Barrick will begin a process to make annual

26

Barrick Annual Report 2010 | Strong Focus on Responsible Mining

environmental data at each operation publicly available.

Safety and Health

Barrick’s safety vision is every person going home safe and healthy every day. During 2010, Barrick continued to implement initiatives to reinforce a zero incident culture.

Barrick’s Courageous Leadership for Safety and Health training continues to be the catalyst for improved performance. During 2010, more than 8,000 employees and contractors participated in Courageous Leadership safety training. Through its concerted safety systems and implementation of standards in 2010, the Company’s overall reportable injury frequency rate decreased from 1.02 to 0.93. The Australia Pacific region improved significantly, with a 70% reduction in its lost-time injury frequency rate. A notable achievement was reached at the Pueblo Viejo project, when it exceeded 22 million hours without a lost-time incident. Three additional sites accumulating over 16 million hours also worked through 2010 without a lost-time injury. Sadly, our 2010 progress was overshadowed by six fatalities – which is unacceptable.

Nearly half of all high potential incidents are related to driving and mobile equipment. In recent years, Barrick has introduced a Mobile Equipment Operating Policy, Drive First education modules and the use of training simulators. In 2010, Barrick began installing WaySmartTM driver monitors in all vehicles. These devices monitor driver behavior and alert drivers if they are speeding, driving aggressively, or not wearing a seatbelt. If the driver does not correct the undesired behavior, the unit records the data and alerts the supervisor. By the end of 2010, more than 2,200 of these units had been installed and further installations will ensue in 2011.

North Mara’s Josephine Mkono receives the new CSR Champion Award.

In addition to these initiatives, Barrick continues to be an active member of the Earth Moving Equipment Safety Round Table (EMESRT). Since 2006, Barrick has been one of 10 major mining companies working directly with original equipment manufacturers to develop safe design

| “At Barrick, the values that define us as a company include a commitment to upholding human rights wherever we operate. That means respecting people — respecting our fellow employees and respecting those in the communities in which we work.” Sybil Veenman, Senior Vice President and General Counsel |

27

Strong Focus on Responsible Mining

philosophies for heavy equipment. In September 2010, EMESRT met again with major equipment manufacturers to review progress to mitigate risks defined by the EMESRT design philosophies.

Barrick’s efforts in 2011 will focus on three key areas: risk management of high potential risks, Visible Felt Leadership, and incident investigation. The Safety group has conducted an assessment of incidents to define the highest priority risks. Standards exist to mitigate each of these risks, and efforts will focus on ensuring effective implementation and compliance at every site. Barrick continues to invest in training to maintain a pool of Barrick Certified Investigators who conduct thorough investigations to determine the root cause of any failure of these existing controls and recommend mitigating actions. In 2011, efforts will focus on ensuring that final recommended mitigating actions from these investigations be implemented company-wide.

“Achieving zero incidents requires people to stop and think before undertaking any task to determine what risks are involved and how to eliminate or mitigate them. We reinforce this field level risk assessment process to make it part of our safety culture.” Don Ritz, Senior Vice President, Safety and Leadership |

|

28

Financial Report

Management’s Discussion and Analysis | 30 |

| |

Financial Statements | 104 |

| |

Notes to Consolidated Financial Statements | 108 |

| |

Mineral Reserves and Resources | 163 |

| |

Corporate Governance and Committees of the Board | 171 |

| |

Shareholder Information | 172 |

| |

Board of Directors and Senior Officers | 174 |

29

Management’s Discussion and Analysis

Management’s Discussion and Analysis (“MD&A”)

Management’s Discussion and Analysis (“MD&A”) is intended to help the reader understand Barrick Gold Corporation (“Barrick”, “we”, “our” or the “Company”), our operations, financial performance and present and future business environment. This MD&A, which has been prepared as of February 16, 2011, should be read in conjunction with our audited consolidated financial statements for the year ended December 31, 2010. Unless otherwise indicated, all amounts are presented in US dollars.

For the purposes of preparing our MD&A, we consider the materiality of information. Information is considered material if: (i) such information results in, or would reasonably be expected to result in, a significant change in the market price or value of our shares; or (ii) there is a substantial likelihood that a reasonable investor would consider it important in making an investment decision; or (iii) if it would significantly alter the total mix of information available to investors. We evaluate materiality with reference to all relevant circumstances, including potential market sensitivity.

Continuous disclosure materials, including our most recent Form 40-F/Annual Information Form, annual MD&A, audited consolidated financial statements, and Notice of Annual Meeting of Shareholders and Proxy Circular will be available on our website at www.barrick.com, on SEDAR at www.sedar.com and on EDGAR at www.sec.gov. For an explanation of terminology unique to the mining industry, readers should refer to the glossary on page 99.

Cautionary Statement On Forward-Looking Information

Certain information contained or incorporated by reference in this MD&A, including any information as to our strategy, plans or future financial or operating performance, constitutes “forward-looking statements”. All statements, other than statements of historical fact, are forward-looking statements. The words “believe”, “expect”, “anticipate”, “contemplate”, “target”, “plan”, “intend”, “continue”, “budget”, “estimate”, “may”, “will”, “schedule” and similar expressions identify forward-looking statements. Forward-looking statements are necessarily based upon a number of estimates and assumptions that, while considered reasonable by us, are inherently subject to significant business, economic and competitive uncertainties and contingencies. Known and unknown factors could cause actual results to differ materially from those projected in the forward-looking statements. Such factors include, but are not limited to: fluctuations in the market and forward price of gold and copper or certain other commodities (such as silver, diesel fuel and electricity); the impact of global liquidity and credit availability on the timing of cash flows and the values of assets and liabilities based on projected future cash flows; fluctuations in the currency markets (such as Canadian and Australian dollars, South African rand, Chilean peso, Argentinean peso, British pound, Peruvian sol and Papua New Guinean kina versus US dollar); changes in US dollar interest rates that could impact the mark-to-market value of outstanding derivative instruments and ongoing payments/receipts under interest rate swaps and variable rate debt obligations; risks arising from holding derivative instruments (such as credit risk, market liquidity risk and mark-to-market risk); changes in national and local government legislation, taxation, controls, regulations and political or economic developments

30

Barrick Financial Report 2010 | Management’s Discussion and Analysis

in Canada, the United States, Dominican Republic, Australia, Papua New Guinea, Chile, Peru, Argentina, South Africa, Tanzania, United Kingdom, Pakistan or Barbados or other countries in which we do or may carry on business in the future; business opportunities that may be presented to, or pursued by, us; our ability to successfully integrate acquisitions; operating or technical difficulties in connection with mining or development activities; employee relations; availability and increased costs associated with mining inputs and labor; litigation; the speculative nature of exploration and development, including the risks of obtaining necessary licenses and permits; diminishing quantities or reserve grades; adverse changes in our credit rating; and contests over title to properties, particularly title to undeveloped properties. In addition, there are risks and hazards associated with the business of exploration, development and mining, including environmental hazards, industrial accidents, unusual or unexpected formations, pressures, cave-ins, flooding and gold bullion or copper cathode losses (and the risk of inadequate insurance, or inability to obtain insurance, to cover these risks). Many of these uncertainties and contingencies can affect our actual results and could cause actual results to differ materially from those expressed or implied in any forward-looking statements made by, or on behalf of, us. Readers are cautioned that forward-looking statements are not guarantees of future performance. All of the forward-looking statements made in this MD&A are qualified by these cautionary statements. Specific reference is made to Barrick’s most recent Form 40-F/Annual Information Form on file with the SEC and Canadian provincial securities regulatory authorities for a discussion of some of the factors underlying forward-looking statements. We disclaim any intention or obligation to update or revise any forward-looking statements whether as a result of new information, future events or otherwise, except to the extent required by applicable law.

Changes in Presentation of Non-GAAP Financial Performance Measures

We use certain non-GAAP financial performance measures in our MD&A. For a detailed description of each of the non-GAAP measures used in this MD&A, please see the discussion under “Non-GAAP Financial Performance Measures” beginning on page 78 of our MD&A.

Adjusted Debt and Net Debt