Exhibit 99.1

Barrick’s strategy is focused on maximizing risk-adjusted returns and free cash flow to position the company to return more capital to shareholders over time.

| | 2012 | | 2011 | | 2010 | |

| | | | | | | |

(In millions of US dollars, except per share data) | | | | | | | |

(Based on IFRS) | | | | | | | |

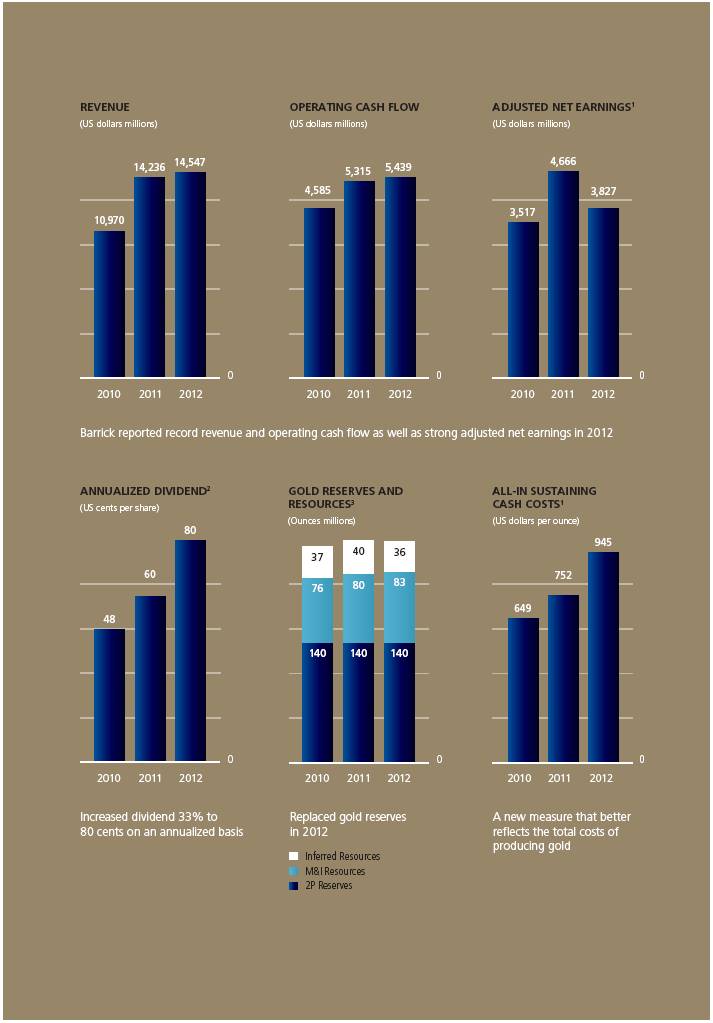

Revenues | | $ | 14,547 | | $ | 14,236 | | $ | 10,970 | |

Net earnings (loss) | | (665 | ) | 4,484 | | 3,582 | |

per share | | (0.66 | ) | 4.49 | | 3.63 | |

Adjusted net earnings1 | | 3,827 | | 4,666 | | 3,517 | |

per share1 | | 3.82 | | 4.67 | | 3.56 | |

Operating cash flow | | 5,439 | | 5,315 | | 4,585 | |

Adjusted operating cash flow1 | | 5,156 | | 5,680 | | 5,241 | |

Adjusted EBITDA1 | | 7,457 | | 8,611 | | 6,448 | |

Cash and equivalents | | 2,093 | | 2,745 | | 3,968 | |

Dividends paid per share | | 0.75 | | 0.51 | | 0.44 | |

Annualized dividend per share2 | | 0.80 | | 0.60 | | 0.48 | |

| | | | | | | |

Gold production (000s oz) | | 7,421 | | 7,676 | | 7,765 | |

Average realized gold price per ounce1 | | $ | 1,669 | | $ | 1,578 | | $ | 1,228 | |

All-in sustaining cash costs per ounce1 | | $ | 945 | | $ | 752 | | $ | 649 | |

Total cash costs per ounce1 | | $ | 584 | | $ | 460 | | $ | 409 | |

| | | | | | | | | | |

Copper production (M lbs) | | 468 | | 451 | | 368 | |

Average realized copper price per pound1 | | $ | 3.57 | | $ | 3.82 | | $ | 3.41 | |

C1 cash costs per pound1 | | $ | 2.17 | | $ | 1.71 | | $ | 1.08 | |

C3 fully allocated costs per pound1 | | $ | 2.97 | | $ | 2.30 | | $ | 1.40 | |

(1) Non-GAAP financial measure – see pages 79–87 of the 2012 Financial Report.

(2) Calculation based on annualizing the last dividend paid in the respective year.

(3) See pages 163–170 of the 2012 Annual Report for additional information on Barrick’s reserves and resources.

Fellow Shareholders,

2012 was a year of both successes and disappointments for Barrick and our shareholders, as the company transitioned to new leadership and adopted an entirely new approach to managing the business.

We recorded adjusted net earnings of $3.8 billion, along with the company’s highest ever operating cash flows of $5.4 billion.

This reflects the quality and potential of our global portfolio to generate earnings and cash flow on an unprecedented scale and allowed us to increase our quarterly dividend by 33 percent last year. Although this is merely the beginning of our new and redoubled commitment to maximize the return of capital to shareholders, it is a start which we expect to accelerate once our major, new projects are completed.

In 2012, we also poured first gold at Pueblo Viejo in the Dominican Republic on schedule, and completed it — with a construction cost of nearly $4 billion — within capital guidance. This is a truly exceptional operation that will be part of a rare, elite class of mines producing in excess of one million ounces of gold annually and with a mine life of more than 25 years. Also, once again, we replaced our gold reserves, which remain by far the largest in our industry in absolute terms. Significantly, we continued to grow our major Goldrush discovery in Nevada, which has the potential to become one of the world’s largest new gold deposits. Importantly, it is also located in one of the world’s best jurisdictions for mining, and next door to the huge, existing facilities and infrastructure at our world-class Cortez mine. This discovery, like others to come in Nevada, will benefit from billions of dollars of investment in mining infrastructure in the state, all of which is fully operational and available to us today.

Meanwhile, the price of gold remains near historically high levels and the secular outlook for the metal remains strong. Despite periodic short-term optimism, the fundamental and structural causes for fear and uncertainty over the world economy remain, and will continue to weigh on the long-term macroeconomic environment. At the same time, gold supply from mines will remain constrained due to a variety of factors, including significantly higher capital costs and ever-longer lead times to permit and build new mines, along with increasingly complex regulatory requirements in nearly every jurisdiction.

Despite a supportive gold price environment and our achievements in 2012, we faced a number of serious challenges last year. We suffered a significant delay and a major cost overrun at our flagship Pascua-Lama project on the border of

Barrick Gold Corporation | Annual Report 2012

2

MESSAGE FROM THE FOUNDER AND CHAIRMAN

Chile and Argentina. Since that fact surfaced — so unexpectedly — the main focus of our company, at every level, has been directed at ensuring that this project will meet its new cost and schedule estimate. At the same time, we made identifying the root causes of this major setback a priority, so that we can apply those lessons in the future. Our other major disappointment in 2012 was related to the Lumwana copper mine in Zambia, where we have taken a $3.8 billion after-tax impairment charge, resulting primarily from our inability to realize the potential we saw in this asset in the short term. We are determined to do what it takes to extract the maximum value we can from Lumwana, which holds exceptional future potential with its dominant holdings on one of the world’s major copper belts. These negative surprises disappointed our investors, and understandably so. In some ways, Barrick’s setbacks mirrored similar challenges across the broader mining industry, and while that in no way excuses our shortfalls, it does point to the need for some fundamental changes in corporate behavior and strategy.

Our dismal share performance last year clearly reflected these setbacks, yet there are other new realities in our industry that also played a significant role. In the years leading up to the global financial crisis, rising gold prices and booming equity markets created a mood of euphoria among investors, rewarding gold producers that delivered aggressive production growth, no matter what the cost. The industry as a whole, and Barrick in particular, delivered. In fact, between 1986 and 2006, as Barrick expanded its operations around the world, our shares increased in value by approximately 4,000 percent, or about 20 percent compounded annually. In order to sustain that kind of growth, gold mining companies and others began to make ever-larger, unprecedented capital investments in new projects to deliver more ounces. Many came from lower-grade ore bodies, erroneously justified by expectations of higher gold prices, and yielded ever more expensive ounces, at ever-growing capital costs. These growing capital commitments virtually eliminated free cash flow generation. Yet that was what investors expected to be available to them — in direct proportion to increased gold prices. It didn’t happen — and the disappointment of investors was severe.

As a result, investor confidence was roiled and wealth managers began to shun gold shares. At the same time, most investors looking for full participation in the rise of gold prices moved vast sums of money from gold equities, where they perceived risks but little return, to gold ETFs. These — of course — offered full participation in gold price movements, without any operational risks. The numbers tell the story: since the creation of the gold ETFs some eight years ago, their value has reached an incredible $140 billion! Meanwhile, gold mining company multiples have suffered an unprecedented contraction, particularly when measured against the performance of their sole product, gold itself.

Recognizing the above facts, it is clear that a new approach — indeed a whole paradigm shift — is required so that an investment in Barrick becomes desirable, rewarding and viable — a demonstrably superior alternative to investing in gold itself. This major shift requires a continuation of asset rationalization, the exploring and realizing of available operational and administrative synergies, a rigorous application of capital discipline, and other measures enhancing our ability to increase payouts to our shareholders. These are all clearly options available to Barrick — with its size and scale — and will make our shares a realistic alternative to ETFs.

Accordingly, Barrick is leading the change from a focus on growth, in favor of maximizing free cash flow and growing rates of return: a significant paradigm shift for our industry. In June of last year, following Jamie Sokalsky’s appointment as CEO, I was proud that his first message to shareholders was a commitment that has become nearly universally accepted throughout the industry: “Returns will drive production, production will not drive returns.” Each and every CEO has phrased it differently, but the end result is the same.

We believe this is the right approach for us and the only one that will deliver results and rekindle shareholder interest in Barrick and the industry at large. Yet we must also realize that repositioning Barrick — a company of considerable size and operational diversity — to deliver against this paradigm cannot happen overnight. Large ships take longer to turn around. I can assure our shareholders that at all levels within Barrick — be it at our Board or at the executive management level — we are united in our commitment to effect the significant change needed and which our investors clearly demand.

We have already made good progress. Last year alone we cut or deferred over $4 billion in capital spending plans and reduced our long-term production targets to focus on only the most

3

profitable ounces. At the same time, we are adding about 1.5 million ounces of annual production from Pueblo Viejo and Pascua Lama at costs significantly below the company’s current average. Also, as part of the new paradigm, we put on hold all plans to build any new mines. In the future, before we approve any projects and allocate capital, they must meet the new standards of our disciplined capital allocation framework and a threshold of exceptional free cash flow returns. In the same vein, and as part of this new paradigm shift, we are also actively pursuing a variety of asset disposals — those that do not support our objectives in terms of operating performance, reserve life, free cash flow generation, or that are otherwise non-core for the company.

Barrick Gold Corporation’s Founder and Chairman

Peter Munk and Co-Chairman John L. Thornton.

These actions are all aimed at positioning Barrick with an improved and growing capacity for free cash flow generation from a balanced portfolio of world-class assets (even if a reduced number), and the ability to return more value to shareholders through growing dividends and capital appreciation.

And as always, we are committed to strengthening our corporate social responsibility practices. This is not about paying lip service, but about doing what’s right, reducing our business risks and maintaining our license to operate around the world.

As we reposition the company to deliver against these objectives, it is also appropriate that we consider a path to new leadership at our Board level. I have taken great pride in my role over more than a quarter century as the Founder and Chairman of Barrick, focused throughout on the various stages of our company’s development with the primary aim of creating value for our investors. This approach worked in building the company from a penny stock to an industry leading position. Yet while we have achieved much, equally there is much more to be done. Accordingly, standing still and perpetuating the status quo is not an option. A vital prerequisite for the future is a new generation of qualified and developed leadership.

I, together with my colleagues on the Board, have been searching for someone with the drive, the ambition, the ability, the global experience and the contacts to lead our Board. Most importantly, I have been looking for someone to share my optimism about the unlimited opportunities available to Barrick as we chart our path forward. In 2011, John Thornton joined our International Advisory Board, and was subsequently appointed Co-Chairman of our main Board in 2012. It is indeed our great fortune that John has reached a point in his spectacular career at the same time when our need for someone of his exceptional qualifications, credentials and experience also reached a decision point.

Over the past year, John and I have been working in lock-step with the entire Board and our management team, focused on the singular and exclusive goal of setting the stage for Barrick’s long-term success. We remain convinced that Barrick is on the cusp of a new era, poised to deliver the shareholder returns that will again define us — in every aspect of our global activities — as a highly successful and respected public company.

Finally, on behalf of the Board of Directors, I would like to extend my sincere gratitude to Nathaniel Rothschild, who has recently resigned from our Board. We are grateful for his many contributions to the company. And most importantly, I would like to thank Barrick’s committed workforce of more than 25,000 employees around the world who are putting our plans to create shareholder value into action daily. They are the heart of the company, and without them, we could not succeed.

Sincerely,

/s/ Peter Munk | |

Peter Munk, Founder and Chairman | |

4

Over the past decade, our industry has been focused on increasing gold production, often without regard for the cost. In essence, this was growth for growth’s sake, without a focus on rates of return. Today, we find ourselves in a very different environment, a new paradigm for the gold industry.

Jamie C. Sokalsky

President and

Chief Executive Officer

Rising capital and operating costs, longer lead times for projects, increasing resource nationalism and a lack of large new discoveries have altered investor perceptions of gold equity risk. In addition, the industry’s track record on capital allocation has been poor. As a result, gold mining shares have continued to under-perform gold itself, and equity multiples across the sector have compressed significantly. At the same time, exchange traded funds continue to offer a popular alternative for those seeking exposure to gold.

While we believe the fundamental factors supporting the price of gold remain firmly in place, and our outlook remains bullish, we cannot simply rely on an ever-rising gold price to generate higher returns. The message from investors has been clear: something has to change. It’s a message we have embraced at Barrick. The past year marked a significant turning point for the company. We began to reposition Barrick around a new paradigm of disciplined capital allocation, one that prioritizes shareholder value creation through a focus on maximizing free cash flow and risk-adjusted rates of return. My overriding objective, and that of everyone at Barrick today, is to translate our company’s strengths and results into higher shareholder returns.

We are driving this change guided by a simple mantra: returns will drive production, production will not drive returns. This represents a fundamental shift for our company and our industry, but we are fully committed to this approach and have already implemented significant changes. All capital allocation options, including returns to shareholders, organic investment, acquisitions and other expenditures, will be ranked and prioritized against each other. Our framework includes the following key objectives:

· Returns Driving Production: Production decisions to be made based on generating appropriate risk-adjusted rates of return and free cash flow.

· Returns to Shareholders: A commitment to pass through the benefits of this model to shareholders.

· Aggressive Cost Management: Reducing costs and an ongoing review of our cost structure is an integral part of the management of our business.

· Portfolio Optimization: Divesting assets that do not meet specific criteria, including return thresholds, free cash flow generation, operating performance and reserve life, and investing in assets that do meet these criteria.

· Reduction of Geopolitical Risk: Focusing on high return, low-cost assets in less risky geopolitical jurisdictions through portfolio optimization.

5

We made considerable progress on the implementation of this framework in the second half of 2012. After evaluating our production profile with the objective of maximizing returns and free cash flow, we cut or deferred approximately $4 billion in previously budgeted capital spending. As a result, we recalibrated our long-term gold production forecast to a higher quality, more profitable base of eight million ounces by 2016 and copper production levels to 600 million pounds by 2015. We also announced that in today’s challenging environment, we have no plans to build any new mines. The company has a number of world-class ore bodies with significant economic potential, but which do not currently meet our investment criteria. We will spend the minimum amount of capital required to maintain their economic potential but we will continue to advance our opportunities in Nevada, particularly Goldrush.

Additionally, as part of our broad approach to cost control, we have cut budgeted overhead for 2013, and expect to make further reductions as a result of an ongoing company-wide review. We have also begun reporting costs using an all-in sustaining cash cost measure that better represents the total cost of producing gold and is consistent with our goal of generating higher returns and free cash flow.

Ultimately, the implementation of this framework is a dynamic and continuous process that will guide every decision we make going forward.

In 2012, the company performed well against its key operating objectives. We met our gold production guidance for the tenth consecutive year, producing 7.4 million ounces at all-in sustaining cash costs of $945 per ounce and total cash costs of $584 per ounce. The company also produced 468 million pounds of copper at C1 cash costs of $2.17 per pound and C3 fully allocated costs of $2.97 per pound.

Adjusted net earnings for the year were the second highest in Barrick’s history at $3.83 billion and the company reported record operating cash flow of $5.44 billion. Our robust financial results allowed us to increase our quarterly dividend by 33 percent in 2012.

Once again, Barrick successfully replaced gold reserves, which now stand at 140 million ounces, with an additional 83 million ounces in measured and indicated gold resources. Barrick also has one billion ounces of silver contained within gold reserves and 14 billion pounds of copper reserves.

Our exploration focus for 2012 was in Nevada, where we doubled and upgraded the resource base at our world-class Goldrush discovery near our Cortez mine. The project is advancing through prefeasibility and we expect to further expand the resource base in this highly prospective area.

We poured first gold at our world-class, 60 percent-owned Pueblo Viejo mine in the Dominican Republic in August, on schedule and within capital guidance. This long-life, low-cost operation achieved commercial production in January 2013 and is expected to ramp up to full capacity in the second half of the year. Pueblo Viejo is expected to contribute an average of 625,000 — 675,000 ounces of gold per year to Barrick in its first full five years of production at all-in sustaining cash costs of $500 — $600 per ounce. With an estimated mine life of more

6

than 25 years, Pueblo Viejo will be a significant contributor to Barrick’s earnings and cash flow.

During 2012, we experienced some significant challenges at Pascua-Lama, our other large development project under construction on the border of Chile and Argentina. These challenges led to a significant increase in capital costs, which are now expected to be $8.0 — $8.5 billion, with first gold targeted for the second half of 2014. This was a highly disappointing outcome for the company and our shareholders, and since being appointed CEO, I have made the successful completion of Pascua-Lama among my top personal priorities.

In late July, we recognized that the complexity of this project exceeded the capabilities of the in-house construction team. We immediately initiated a comprehensive schedule and cost review, and subsequently transferred construction management responsibilities to Fluor, a world leader in engineering, procurement and construction management.

Although we were disappointed by the increased capital costs and extended schedule, Pascua-Lama will be one of the world’s truly great gold mines with an anticipated mine life of 25 years. Once in production, it will be a significant free cash flow generator, with average annual production of 800,000 — 850,000 ounces of gold in its first full five years of operation, at all-in sustaining cash costs of $50 — $200 per ounce.

Once at full capacity, Pueblo Viejo and Pascua-Lama together are expected to contribute about 1.5 million low-cost ounces of gold to Barrick’s production profile, underpinning our high-quality, profitable production base for the long term.

The Lumwana copper mine in Zambia represented our other significant challenge in 2012. During the year, we completed an updated life-of-mine plan which reflects new data from the drilling program that was completed late in 2012. Unfortunately, the new mine plan indicates mining costs will be higher than we anticipated, and as a result, we recorded an after-tax asset and goodwill impairment charge of $3.8 billion in 2012. This was clearly an unfortunate result. Our 2013 guidance reflects realistic expectations for an improvement over 2012; however, we need to implement a significant change in the mine’s future performance to realize its potential. Long-term, Lumwana has an enormous mineral inventory and tremendous leverage to higher copper prices. As copper becomes more difficult to find and demand increases, we stand to benefit substantially from having this asset in our portfolio.

Maintaining and strengthening our commitment to corporate responsibility is another critical component of our strategy to deliver superior returns to our shareholders. It is also one of my personal commitments as CEO and one shared by our entire management team. We must earn support for our activities by living up to our commitments on safety and the environment, while ensuring that communities and society at large see mutual, long-term benefits from our operations. Improving our social and environmental performance is a continuous process, and one we remain fully committed to.

Looking ahead to 2013, we remain focused on delivering against a number of key priorities to drive shareholder value. First and foremost, we must meet our production and cost guidance. With respect to projects, we are focused on ramping up Pueblo Viejo to full capacity, advancing Pascua-Lama in line with our cost and schedule estimates, and advancing our Goldrush discovery in Nevada. Improving Lumwana’s performance is another key goal for the year, and one that our new copper leadership team is pursuing aggressively. During 2013, we will also be actively pursuing opportunities to optimize our portfolio, along with seeking further cost reductions across the company. And as always, further strengthening our corporate social responsibility performance is a top priority.

In conclusion, I would like to express my gratitude to our Founder and Chairman Peter Munk, Co-Chairman John Thornton and the rest of the Board of Directors for entrusting me with the role of Chief Executive Officer at this critical juncture in Barrick’s history. I would also like to thank Peter Kinver and Igor Gonzales for their many years of service with the company.

Delivering returns for our shareholders is my number one objective, and it’s something I intend to keep in laser-sharp focus as we move forward. Through our disciplined and rigorous approach to capital allocation, I believe we have the industry’s best platform to deliver profitable production while positioning Barrick as a significant generator of free cash flow. This should enable us to return more capital to shareholders, and ultimately drive superior shareholder returns over the long term.

/s/ Jamie C. Sokalsky | |

Jamie C. Sokalsky, President and Chief Executive Officer | |

7

As the gold price recorded its 12th straight year of increases, Barrick reported record operating cash flow of $5.44 billion and the second highest adjusted net earnings in its history of $3.83 billion or $3.82 per share. Barrick continues to demonstrate exceptional leverage to the gold price on a per share basis. Since the launch of the gold exchange traded fund in 2004, the company’s adjusted net earnings and adjusted operating cash flow per share have increased about 700 percent1 and 450 percent1, respectively, compared to a 280 percent1 rise in the gold price over the same period. The 2012 net loss of $0.7 billion primarily reflects after-tax impairment charges of $3.8 billion for Lumwana. While we increased reserves and defined significant new mineralization at Lumwana in 2012, the mining costs in the new life-of-mine plan were higher than anticipated. Lumwana has tremendous leverage to higher copper prices, but our focus is on reducing mining costs to unlock its potential.

TRACK RECORD OF DIVIDEND GROWTH

Our robust cash flow generation and positive gold price outlook enabled the company to raise the quarterly dividend in 2012 by 33 percent to

(1) 2004–2012. All EPS are adjusted except 2004 is on a US GAAP basis and all CFPS are on a US GAAP basis except 2009–2012 are adjusted. 2004–2009 are on a US GAAP basis and 2010–2012 are on an IFRS basis.

8

“We can’t rely on stronger gold prices to deliver higher returns and free cash flow. We are managing our costs on an all-in sustaining cash cost basis and have significantly reduced budgeted company-wide overhead costs.”

Ammar Al-Joundi, Executive Vice President and Chief Financial Officer

$0.20 per share, or $0.80 per share on an annualized basis. Over the last six years, Barrick has had a consistent track record of returning more capital to shareholders, increasing its dividend by approximately 260 percent2 during this period, or a 24 percent compound annual growth rate.

DISCIPLINED APPROACH TO COST CONTROL

Costs are a key driver of Barrick’s financial performance and an integral part of our disciplined capital allocation strategy. Barrick continues to utilize risk management strategies, including currency and commodity hedging, to help manage our cost exposures. The company has also adopted a new cost measure — all-in sustaining cash costs per ounce — that is a more meaningful metric and better reflects the total costs of producing gold. This measure also reflects how we manage our business and is consistent with our goal of generating higher returns and increased free cash flow. While our expected 2013 all-in sustaining cash costs of $1,000 — $1,100 per ounce3 are competitive, we continue to evaluate a broad spectrum of ways to meaningfully reduce them.

ANNUALIZED DIVIDEND

US cents per share

In 2012, we initiated a review of company-wide overhead costs and an ongoing portfolio review that ranked our assets on their ability to meet our two primary investment metrics — free cash flow and risk-adjusted returns. As a result of these steps, we have reduced budgeted 2013 company-wide overhead by more than $100 million and we also identified approximately $4 billion of previously planned capital expenditures that do not meet our investment criteria. This capital was cut or deferred from our future plans.

Although we can’t rely on higher gold prices to deliver free cash flow growth, supportive supply/demand fundamentals appear to be in place for the foreseeable future. We expect gold to remain attractive as a de facto currency and a store of value as many developed nations continue to struggle with elevated debt levels and respond with accommodative monetary policies.

Central banks continue to purchase gold to diversify their portfolios, and recorded net purchases for the third year in a row. The growing middle class in emerging economies such as China and India is providing a further backstop to gold prices, and is also anticipated to benefit copper prices through infrastructure and consumer demand. Mine supply for both gold and copper is expected to be limited by the scarcity of new discoveries, which should positively impact prices.

(2) Calculation based on converting the 2006 semi-annual dividend of $0.11 per share to a quarterly dividend.

(3) Non-GAAP financial measure, see pages 79–87 of the 2012 Financial Report.

9

GLOBAL PORTFOLIO OF PREMIER ASSETS

Barrick’s portfolio of 27 operating mines, advanced exploration and development projects and extensive land positions on five continents around the globe includes some of the world’s premier gold assets. Once Pueblo Viejo is at full capacity, Barrick will operate three of the world’s six mines that are one million ounce or more per year producers. Our top four mines — Cortez, Goldstrike, Lagunas Norte and Veladero — together produced 4.1 million ounces in 2012 at an average total cash cost of $406 per ounce.

These mines, plus Pueblo Viejo and Pascua-Lama, form an unmatched core group of six high quality assets with long lives and low costs, that alone would be the world’s largest gold producer. The goal of our ongoing portfolio review process, launched in mid-2012, is to further optimize the quality of our entire portfolio. Assets that do not generate acceptable risk-adjusted returns or free cash flow will be deferred, shelved or divested.

Barrick met its gold production guidance in 2012 for the tenth year in a row with an industry-leading

10

7.4 million ounces of gold. All-in sustaining cash costs were $945 per ounce and total cash costs of $584 per ounce were the lowest among the senior gold producers. These strong results reflect the high quality of our assets. Going forward, Barrick’s cost structure is expected to benefit from combined average annual production of about 1.5 million1 new ounces from Pueblo Viejo and Pascua-Lama at average all-in sustaining cash costs of $250 — $350 per ounce2 and average total cash costs of $100 — $200 per ounce2.

GOLD BUSINESS

Our North America unit is the company’s largest producing region and generated 3.5 million ounces, or 47 percent of total 2012 production, at total cash costs of $500 per ounce. Nevada is home to seven of the region’s nine mines and contributed 3.1 million ounces or 42 percent of total production in 2012. Cortez remains our lowest cost mine and exceeded expectations for the third straight year with production of 1.37 million ounces at total cash costs of $282 per ounce. Significant exploration

(1) About 1.5 million ounces is based on the estimated cumulative annual average production in the first full five years once both mines are at full capacity.

(2) Based on first full five year averages once both mines are at full capacity.

11

WORLD CLASS ASSETS

success at the nearby Goldrush discovery has further demonstrated the potential of this truly world-class district.

At Goldstrike, construction advanced on the thiosulfate project to enable continued production from the autoclaves, which were originally expected to cease operations in 2012. Modifications to the autoclave circuit will accelerate about 3.5 million ounces in the mine plan and contribute an average of about 350,000 — 400,000 ounces annually in the first full five years. First gold production is expected in mid-2014. The North America region contains a number of excellent prospects for future production, including Goldrush and the Lower Zone underground expansion at Cortez.

The Cortez mine in Nevada exceeded expectations for the third straight year. The processing facilities are shown in the foreground.

The three mines in South America produced 1.6 million ounces, or 22 percent of the company’s total 2012 production, at total cash costs of $467 per ounce. The Lagunas Norte mine had another strong year, contributing 754,000 ounces at low total cash costs of $318 per ounce, while Veladero produced 766,000 ounces at total cash costs of $510 per ounce. Both mines have significantly exceeded feasibility study expectations for production since they began operations in 2005. Lagunas Norte has outperformed original estimates for the last seven years and, on a cumulative basis, has produced more than 50 percent above expectations. Veladero has outpaced feasibility estimates for the last four years and cumulatively has produced about 20 percent more than anticipated.

Australia Pacific’s eight mines produced 1.8 million ounces in 2012, or 25 percent of total production, at total cash costs of $803 per ounce. The Porgera mine in Papua New Guinea continued to lead production in the region with production of 436,000 ounces at total cash costs of $955 per ounce.

Barrick’s 73.9 percent share of production from the four mines within African Barrick Gold Plc (ABG) was 0.5 million ounces, or 6 percent of total production, at total cash costs of $949 per ounce.

12

INVESTING IN HIGH RETURN PROJECTS

Barrick added another world-class operation to its portfolio in 2012 with the successful completion of its 60 percent-owned Pueblo Viejo mine in the Dominican Republic. Pueblo Viejo is one of only a handful of mines globally that will produce more than one million ounces of gold per year and its state-of-the-art processing facility houses four of the largest autoclaves in the world. Based on reserves of 25.0 million ounces3 (100 percent basis), this mine is anticipated to be a major contributor of low-cost production to Barrick for many years to come. Completed at a capital cost of $3.7 billion, Pueblo Viejo is expected to provide 1,900 jobs and 10,000 indirect jobs over its anticipated 25+ year mine life.

Pueblo Viejo poured its first gold in August 2012 and is scheduled to ramp up to full capacity in the second half of 2013 with expected production of 500,000 — 650,000 ounces4 in 2013. In the first

(3) See pages 163–170 of the 2012 Annual Report for additional information on reserves and resources.

(4) Actual production may vary depending on the progress of the ramp-up.

Pueblo Viejo’s state-of-the-art processing facility houses four of the largest autoclaves in the world.

13

full five years of operation, Barrick’s share of annual production is anticipated to be 625,000 — 675,000 ounces at all-in sustaining cash costs of $500 — $600 per ounce5 and total cash costs of $300 — $350 per ounce5.

The Pascua-Lama project on the border of Chile and Argentina is expected to be one of the world’s lowest operating cost gold mines and will generate significant free cash flow for Barrick once it ramps up to full production. First production is targeted for the second half of 2014 and mine construction capital is estimated at $8.0 — $8.5 billion. The project is expected to generate 1,600 direct jobs and 4,000 indirect jobs over its 25 year mine life and Barrick is providing skills training programs, opportunities for local businesses and investing in

Assembly of the grinding building at Pascua-Lama is well advanced; the covered ore stockpile building is shown in the background.

14

communities around the project. The project hosts a large gold reserve of nearly 18 million ounces and 676 million ounces of silver contained within the gold reserves.

In its first full five years of operation, Pascua-Lama is expected to produce an annual average of 800,000 —850,000 ounces of gold at all-in sustaining cash costs of $50 — $200 per ounce6 and total cash costs of $0 to negative $150 per ounce6. The mine will also be one of the world’s top silver producers, with average annual production of about 35 million ounces over the same period. At the end of 2012, construction was approximately 40 percent complete.

COPPER BUSINESS UNIT

Barrick strengthened the management of its Global Copper Business Unit (CBU) in 2012 to exclusively focus on optimizing this business, which includes the Zaldívar mine in Chile, the Lumwana mine in Zambia, and the Jabal Sayid project in Saudi Arabia.

Total 2012 copper production was 468 million pounds at C1 cash costs of $2.17 per pound and C3 fully allocated costs of $2.97 per pound. The Zaldívar mine produced 289 million pounds at C1 cash costs of $1.62 per pound and Lumwana contributed 179 million pounds at C1 cash costs of $3.07 per pound.

Our focus at Lumwana is on significant cost reduction in order to realize its potential. With an enhanced understanding based on drilling completed in 2012 and an updated mine plan, the company is in a better position to identify necessary changes that will improve free cash flow over the life of the mine. Higher utilization and productivity of the mining fleet and a full transition to owner maintenance have been identified as major opportunities to improve value.

The leach pad at Zaldívar is refreshed with ore in a constant cycle of delivery and reclaim.

At Jabal Sayid, production is expected to commence in 2014 once the mine is compliant with Saudi Arabia standards for safety and security. Average annual production from Jabal Sayid is anticipated to be 100 — 130 million pounds at C1 cash costs of $1.50 — $1.70 per pound7 in its first full five years of operation.

(5) Based on first full five year averages and gold and oil price assumptions of $1,700/oz and $90/bbl, respectively. Does not include escalation for future inflation.

(6) Based on first full five year averages and gold, silver and oil price assumptions of $1,700/oz, $30/oz and $90/bbl, respectively, and assuming a Chilean peso f/x rate of 475:1. Does not include escalation for future inflation.

(7) Does not include escalation for future inflation.

15

Barrick replaced proven and probable gold reserves in 2012 for the seventh year in a row, ending the year with an industry-leading 140 million ounces. In addition, the company has measured and indicated resources of 83 million ounces and inferred resources of 36 million ounces.

The company has an excellent track record of finding new gold reserves dating back nearly to its inception. Since 1990, we have spent about $2.9 billion on exploration1 with an overall finding cost of about $18 per ounce. During that time, we have mined 127 million ounces of gold, acquired 110 million ounces and found 157 million ounces of gold through exploration.

Copper reserves grew by 1.2 million pounds to 13.9 million pounds in 2012 following the completion of an extensive 18-month drill program at Lumwana. The company also had measured and indicated copper resources of 10.3 million pounds at the end of 2012.

(1) Barrick’s exploration programs are designed and conducted under the supervision of Robert Krcmarov, Senior Vice President, Global Exploration of Barrick. For information on the geology, exploration activities generally, and drilling and analysis procedures on Barrick’s material properties, see Barrick’s most recent Annual Information Form/Form 40-F.

16

The 2012 exploration program was focused largely in Nevada, which received about 40 percent of the exploration budget. Extensive drill programs were conducted at Goldrush to upgrade resources and test the limits and regional potential of this large discovery near the Cortez mine.

Infill drilling joined the Red Hill and Goldrush deposits (renamed Goldrush), doubled and upgraded the resource base and more than doubled the footprint of the mineralized corridor to over seven kilometers in length. Measured and indicated resources grew by more than 500 percent from 2011 to 8.4 million ounces. In addition, there are 5.7 million ounces in the inferred category. Goldrush remains open in multiple directions to the north, east and south.

Stepping out from Goldrush, the greater Cortez camp contains a wealth of long-term, district-scale exploration opportunities. The purchase of the Mill Canyon property in 2012 brought the entire Cortez camp under Barrick management and will permit

17

CORTEZ DISTRICT POTENTIAL

The Cortez district contains substantial exploration opportunities, including a new parallel trend west of Goldrush.

a systematic exploration of high quality targets that will be drill tested. These include a parallel trend identified to the west of Goldrush, and the northern, eastern and southern extensions of the Goldrush system. A scoping study has been completed, and a prefeasibility study is underway in parallel with continuing exploration work and technical studies. A number of development options are being considered, including open pit mining, underground mining, or a combination of both.

At the 75 percent-owned Turquoise Ridge mine, drilling in 2012 added 0.7 million ounces to reserves, 2.6 million ounces to measured and indicated resources and 1.9 million ounces to inferred resources (all 100 percent basis).

The 2013 exploration budget of $400 — $440 million will focus on quality priority projects aligned with our objective of “returns driving production.”

About half of the 2013 budget is allocated to North America, primarily Nevada, while Australia Pacific will receive about 18 percent of the budget, copper will be allocated about 16 percent and South America about 14 percent, with the balance being for African Barrick Gold.

18

HISTORY OF GOLD RESERVE | RESOURCE GROWTH

Ounces Added Since Discovery or Acquisition (millions)

Reserves and Resources Summary

at December 31, 2012 | | Proven and | | Measured and | | Inferred | |

(Barrick’s equity share) | | Probable Reserves | | Indicated Resources | | Resources | |

Gold (000s oz) | | 140,248 | | 83,008 | | 35,591 | |

North America | | 59,478 | | 59,139 | | 19,064 | |

South America | | 51,689 | | 10,338 | | 6,447 | |

Australia Pacific | | 16,609 | | 6,150 | | 6,772 | |

Africa | | 12,271 | | 7,379 | | 3,291 | |

Other | | 201 | | 2 | | 17 | |

Other Metals | | | | | | | |

Copper (M lbs) | | 13,881 | | 10,308 | | 506 | |

Nickel (M lbs) | | — | | 1,080 | | 596 | |

Other Metals Contained in:

| | Proven and Probable | | Measured and Indicated | | Inferred | |

| | Gold Reserves | | Gold Resources | | Gold Resources | |

Silver (000s oz) | | 1,051,680 | | 255,633 | | 60,162 | |

Copper (M lbs) | | 5,761 | | 1,335 | | 1,639 | |

19

We believe our commitment to responsible mining is the right way to operate and vital to achieving our business objectives. Our priority is to deliver superior returns to our shareholders and at the same time create value for the communities and countries where we operate.

Around the world, the economic, social and political context of the mining industry continues to evolve at a rapid pace, bringing with it changing risks and heightened expectations. Barrick’s approach to corporate responsibility helps us identify and manage emerging risks to ensure we can continue to create value for our investors and stakeholders.

We do this by conducting our activities to high operational, social, environmental and safety standards and by developing respectful and collabor-ative relationships with communities, governments, civil society and others, wherever we operate.

We recognize that our ongoing success is tied to the success and stability of our host communities, and to our reputation as a responsible partner in resource development. In all locations, we work diligently to manage the impacts of our operations, provide a safe workplace for our employees, and ensure that communities and society derive long-term benefits from our mining activities.

20

This approach helps us sustain broad support for our operations. As a result, we are able to develop a quality portfolio of assets that generates strong returns for our shareholders.

ECONOMIC AND COMMUNITY DEVELOPMENT

Barrick’s operations are a powerful engine of economic development and can drive positive social change. Our operations contribute billions of dollars annually to local and national economies in the form of wages, taxes and royalties, procurement of goods and services and community investments. In 2011 alone (the most recent year for which figures are available) these contributions totaled approximately $13 billion. Through local hiring and purchasing, we seek to maximize the benefits of our operations in ways that are good for the community and good for our business.

The issues facing our host communities are diverse and often complex. In developing countries, where many new deposits are located, poverty, limited infrastructure and services, and a lack of educational opportunities are a reality. To help our host communities address these challenges, we work with them to invest in the right development initiatives that reflect local priorities. These initiatives

21

help to foster longer-term socio-economic development and contribute to greater stability where we operate.

Investing in Communities

Barrick invests in every community where we operate. Some examples of the numerous initiatives we are supporting are highlighted below:

IN CHILE | Barrick helped 125 families move into new homes as part of an initiative aimed at alleviating poverty in Chile’s Atacama Region. Barrick’s partners in the program were “A Roof for Chile,” a non-governmental organization (NGO) dedicated to eradi-cating slums, and the Chilean Ministry of Housing.

Barrick partnered with A Roof for Chile and the Chilean government to enable 125 Chilean families living in poverty to become homeowners. Pictured above, the families outside their new homes.

IN THE DOMINICAN REPUBLIC | The company has invested in numerous community projects around the Pueblo Viejo mine to improve health care, housing, infrastructure and literacy. Additional funding has been allocated to conduct the clean-up of a former mining operation and remediate its impacts outside the current Pueblo Viejo mine site, helping to improve the local living environment.

IN ZAMBIA | Barrick invested in a wide range of sustainable development initiatives in 2012. These included funding for infrastructure, such as schools and health centers, literacy and agricultural programs, community sports and recreation, and an initiative to provide microcredit and small business loans to women.

IN ARGENTINA | At the end of 2012, Barrick’s operations in Argentina generated employment for a total of 15,800 people, including direct employees and third-party contractors. The company is providing skills training programs, purchasing from local suppliers and investing in host communities. These investments in agribusinesses, health, tourism, and internet connectivity further leverage the positive socio-economic impact of our business.

IN THE UNITED STATES | A long-time supporter of education at all levels in Nevada, Barrick recently signed a four-year sponsorship agreement with the NGO Communities in Schools that is helping at-risk students at two Nevada middle schools stay in school and succeed academically.

22

Relationship-Building

Our goal is to build strong relationships with a broad range of stakeholders, including governments, NGOs, civil society and others. By working together, we are better able to address the issues facing our host communities and countries and achieve more sustainable outcomes, while continuously improving our performance. Some examples of our efforts in 2012 are provided below.

CSR ADVISORY BOARD: Barrick established an external CSR Advisory Board in 2012 to provide advice and guidance to the company’s senior leadership team on our social and environmental performance. The inaugural Board met twice over the course of the year and included five highly distinguished individuals — Aron Cramer, Elizabeth Dowdeswell, Robert Fowler, Edward Liebow, and Gare Smith — as well as Professor John Ruggie, who served as a Special Consultant to the Advisory Board. This third-party feedback and counsel is one of the many ways we are working to improve our performance and deliver on our commitment to mining responsibly.

COMMUNITIES: In 2012, Barrick began implementing its Community Relations Management System (CRMS) at all of its mines worldwide. The CRMS sets minimum performance requirements that are aligned with international best practice to ensure community relations activities are carried out in a systematic and professional manner. Grievance mechanisms were one of the priorities for implementation in 2012, which provide local stakeholders with an accessible, transparent mechanism to voice their concerns to the company.

In 2012, Barrick’s inaugural CSR Advisory Board included, from left to right, Ed Liebow, Gare Smith, Aron Cramer, Elizabeth Dowdeswell, John Ruggie (Special Consultant to the Advisory Board) and Robert Fowler.

NGOs: Barrick unveiled the Alto Chicama Commitment, an initiative involving NGOs and governments working together with Barrick on sustainable development projects in northern Peru. This collaborative model, which follows on the success of the Atacama Commitment in Chile, features alliances with such respected NGOs as CARE and World Vision.

Government Relations

Barrick’s government relations program is critical to achieving our business goals and is a significant strength for the company in managing our operations and the political risk inherent in complex jurisdictions. We ensure that we are trusted partners with all levels of government where we have

23

projects and operations. We build and maintain productive relationships with regulators and public policy makers that underscore our role as a responsible operator. We conduct our activities in a transparent way and commit to rigorous implementtation of the standards set out by our home and host countries. Our collaborative approach to working with governments helps us to secure necessary approvals and stability agreements, negotiate permit requirements and supports project financing.

As a Canadian multinational company, we endeavor to ensure our investments are protected through multilateral and bilateral investment and free trade agreements and advocate for the creation of such where none exists. Finally, we work closely with our international and domestic peers through the World Gold Council, the International Council on Mining and Metals, the Mining Association of Canada, the National Mining Association of the United States, and other national associations in countries where we operate. Through these associations, we advocate for best practices, participate in the creation of industry standards, communicate and document the economic and social benefits of resource development to host countries, and collaborate on managing collective risks.

The First Lady of Zambia, Dr. Christine Kaseba (center), celebrates International Women’s Day at the Lumwana mine.

ENVIRONMENTAL RESPONSIBILITY

In the mining industry today, there is a stronger focus on environmental responsibility than ever before. From exploration to reclamation, we are working to identify, control and mitigate the impacts of our activities on land, air and water. Our programs that lead to energy savings and reduce water consumption and emissions keep us competitive and protect our ability to operate.

In 2012, Barrick completed implementation of its Environmental Management System (EMS) at all operations, which is designed to improve environmental performance across the company. Barrick’s EMS is aligned with high international standards, including ISO 14001 and the International Council on Mining and Metals Framework for Sustainable Development. All North American operations and business units and South American operations are now ISO 14001 certified, with further certifications achieved or underway in

24

Australia Pacific. Our most recent operation to achieve certification is the Porgera Joint Venture in Papua New Guinea.

We recognize the risk that climate change poses to society and to our long-term success. To mitigate these risks, we set energy efficiency and greenhouse gas emissions targets that lead to improvements against business as usual. Our focus is to improve processes across the organization — at mine sites and in office settings. Barrick is also continuing its efforts to use more renewable energy, building on the success of our Punta Colorada wind farm in Chile and our solar farm in Nevada. All Barrick mines reuse water, and we continually seek new ways to reduce the amount of water used for mining activities.

MEETING OUR RESPONSIBILITY TO OUR EMPLOYEES

Barrick’s reputation as a safe operator reflects our values and makes us an employer of choice. Our Safety and Health Policy outlines the company’s goal of a zero-incident work environment to achieve our safety vision, which is “Every person going home safe and healthy every day.” The Barrick Safety and Health Management System is our framework to reach that objective.

During 2012, Barrick reduced its Total Reportable Injury Frequency Rate to 0.76, an 18 percent reduction from 0.92 achieved in 2011. Across the company, more diligent implementation of safety standards is making a difference on the front line. Ongoing installation of in-vehicle driver mentoring systems is helping us coach drivers and reduce light vehicle incidents. Barrick has also developed a management standard to prevent fatigue-related incidents, which is now being piloted at several sites.

Barrick will continue to increase management presence in the field, focusing on compliance with standards related to critical risks. In addition, the company has implemented a rigorous approach to investigate “near miss” incidents, engaging in specialized training and analysis. The involvement of leaders in these processes promotes quality investigations and leads to better corrective actions and more diligent follow up. Through these actions, we continue to create a safety culture at Barrick that is fundamental to how we work every day.

Barrick maintains emergency response teams at all its sites around the world. These highly trained professionals are the first responders to any mine emergency, and often assist communities in times of need.

25

Our company is built on a foundation of doing the right thing in every situation. We guide our conduct by the highest standards of honesty, integrity, and ethical behavior. Nothing is more important to our success as a company than these values, which are vital to securing and maintaining respect from our employees, the communities and governments where we operate, and our shareholders.

We have several global policies and processes in place to guide our employees and help ensure compliance with our core values. These values, policies and processes, combined with our commitment to comply with all applicable national and international laws, help guide our day-to-day work as a responsible and honest company.

CODE OF BUSINESS CONDUCT AND ETHICS

Barrick’s Code of Business Conduct and Ethics embodies our commitment to conduct our business in accordance with all applicable laws, rules and regulations and to the highest ethical standards throughout our worldwide organization. Adopted by Barrick’s Board of Directors, the Code of Conduct applies to every Barrick employee. We ensure that all employees are aware of and follow the obligations contained in the Code through training, certifications, communications, and other methods. We also maintain an anonymous hotline where

26

concerns about adherence to the Code can be reported and we investigate all reports that are made.

HUMAN RIGHTS

Barrick recognizes the equality and dignity of all people, and respects human rights in every location in which we operate. We believe that responsible resource development can and should improve human rights. In 2012, we continued to implement a global cross-functional human rights compliance program aligned with the UN Guiding Principles on Business and Human Rights. As part of that program, in 2012 we provided human rights training in some capacity to more than 10,000 employees. We began conducting human rights risk and impact assessments at key sites and projects. We strengthened human rights due diligence in our hiring practices and instituted human rights requirements in agreements with third parties.

We also initiated a human rights remediation framework at the Porgera Joint Venture in Papua New Guinea to address claims of sexual violence committed by employees. In late 2012, after 18 months of designing the remedy framework, including consultations with leading human rights experts, experts in violence against women, and prominent local stakeholders, the program — which is administered independently of the company — began to accept claims. In 2012, Barrick also assisted its affiliate African Barrick Gold in seeking to remediate past human rights violations at the North Mara mine in Tanzania.

Barrick also engages broadly in human rights initiatives and partnerships. We serve on the Board of Directors of the Voluntary Principles on Security and Human Rights and, in 2012, entered into new partnerships with leading human rights organizations, including:

· A two-year partnership with the Danish Institute for Human Rights to develop human rights tools for business and further enhance Barrick’s human rights performance globally.

· Assisted in founding a Human Rights Working Group with Business for Social Responsibility, which now involves some two dozen leading companies.

· Helping to lead the effort to establish a UN Global Compact Network within Canada, serving as one of the network’s core member companies.

ANTI-CORRUPTION AND FRAUD

As part of ensuring we operate ethically at all times, Barrick maintains a cross-functional global anticorruption compliance program. In 2012, we continued to enhance this program, which includes training and due diligence on prospective employees and third-party contractors. Barrick also seeks to engage with leading entities and experts and promote global anticorruption efforts. Barrick is a member of Transparency International and the Extractive Industries Transparency Initiative. In 2012, we became a member of the World Economic Forum’s Partnership Against Corruption Initiative and became a lead member of Trace International Inc.’s TRAC program, a global supply chain due diligence and transparency tool.

COMPLIANCE

Maintaining Barrick’s license to operate requires adherence to consistent standards and policies that are applied on a global basis. We actively seek to ensure that our policies and procedures are followed through training, communication, reporting, investigations, and other means. We conduct regular audits to ensure our operations are adequately identifying social, safety, security, environmental and other risks and have appropriate plans in place to address them. These assessments ensure appropriate compliance with our requirements and identify areas where our processes can be strengthened.

27

Financial Report

Management’s Discussion and Analysis | 29 |

Financial Statements | 93 |

Notes to Consolidated Financial Statements | 98 |

Mineral Reserves and Mineral Resources | 163 |

Corporate Governance and Committees of the Board | 171 |

Shareholder Information | 172 |

Board of Directors and Senior Officers | 174 |

Management’s Discussion and Analysis (“MD&A”)

Management’s Discussion and Analysis (“MD&A”) is intended to help the reader understand Barrick Gold Corporation (“Barrick”, “we”, “our” or the “Company”), our operations, financial performance and present and future business environment. This MD&A, which has been prepared as of February 13, 2013, should be read in conjunction with our audited consolidated financial statements for the year ended December 31, 2012. Unless otherwise indicated, all amounts are presented in US dollars.

For the purposes of preparing our MD&A, we consider the materiality of information. Information is considered material if: (i) such information results in, or would reasonably be expected to result in, a significant change in the market price or value of our shares; or (ii) there is a substantial likelihood that a reasonable investor would consider it important in making an investment decision; or (iii) it would significantly alter the total mix of information available to investors. We evaluate materiality with reference to all relevant circumstances, including potential market sensitivity.

Continuous disclosure materials, including our most recent Form 40-F/Annual Information Form, annual MD&A, audited consolidated financial statements, and Notice of Annual Meeting of Shareholders and Proxy Circular will be available on our website at www.barrick.com, on SEDAR at www.sedar.com and on EDGAR at www.sec.gov. For an explanation of terminology unique to the mining industry, readers should refer to the glossary on page 88.

Cautionary Statement on Forward-Looking Information

Certain information contained or incorporated by reference in this MD&A, including any information as to our strategy, projects, plans or future financial or operating performance, constitutes “forward-looking statements”. All statements, other than statements of historical fact, are forward-looking statements. The words “believe”, “expect”, “anticipate”, “contemplate”, “target”, “plan”, “intend”, “continue”, “budget”, “estimate”, “may”, “will”, “schedule” and similar expressions identify forward-looking statements. Forward-looking statements are necessarily based upon a number of estimates and assumptions that, while considered reasonable by the Company, are inherently subject to significant business, economic and competitive uncertainties and contingencies. Known and unknown factors could cause actual results to differ materially from those projected in the forward-looking statements. Such factors include, but are not limited to: fluctuations in the spot and forward price of gold and copper or certain other commodities (such as silver, diesel fuel and electricity); diminishing quantities or grades of reserves; the impact of inflation; changes in national and local government legislation, taxation, controls, regulations, expropriation or nationalization of property and political or economic developments in Canada, the United States, Dominican Republic, Australia, Papua New Guinea, Chile, Peru, Argentina, Tanzania, Zambia, Saudi Arabia, United Kingdom, Pakistan or Barbados or other countries in which we do or may carry on business in the future; the impact of global liquidity and credit availability on the timing of cash flows and the values of assets and liabilities based on projected future cash flows; increased costs, delays and technical challenges associated with the construction of capital projects; fluctuations in the currency markets (such as Canadian and Australian dollars, Chilean and Argentinean peso, British pound, Peruvian sol, Zambian kwacha, South African rand, Tanzanian shilling, and Papua New Guinean kina versus the US dollar); changes in US dollar interest rates that could impact the mark-to-market value of outstanding derivative instruments and ongoing payments/receipts under interest rate swaps and variable rate debt

29

obligations; risks arising from holding derivative instruments (such as credit risk, market liquidity risk and mark-to-market risk); risk of loss due to acts of war, terrorism, sabotage and civil disturbances; business opportunities that may be presented to, or pursued by, the Company; our ability to successfully integrate acquisitions or complete divestitures; operating or technical difficulties in connection with mining or development activities; employee relations; availability and increased costs associated with mining inputs and labor; litigation; the speculative nature of mineral exploration and development, including the risks of obtaining necessary licenses and permits; adverse changes in our credit rating; contests over title to properties, particularly title to undeveloped properties; and the organization of our previously held African gold operations and properties under a separate listed company. In addition, there are risks and hazards associated with the business of mineral exploration, development and mining, including environmental hazards, industrial accidents, unusual or unexpected formations, pressures, cave-ins, flooding and gold bullio or copper cathode losses (and the risk of inadequate insurance, or inability to obtain insurance, to cover these risks). Many of these uncertainties and contingencies can affect our actual results and could cause actual results to differ materially from those expressed or implied in any forward-looking statements made by, or on behalf of, us. Readers are cautioned that forward-looking statements are not guarantees of future performance. All of the forward-looking statements made in this MD&A are qualified by these cautionary statements. Specific reference is made to the most recent Form 40-F/Annual Information Form on file with the SEC and Canadian provincial securities regulatory authorities for a discussion of some of the factors underlying forward-looking statements. We disclaim any intention or obligation to update or revise any forward-looking statements whether as a result of new information, future events or otherwise, except as required by applicable law.

Changes in Presentation of Non-GAAP Financial Performance Measures

We use certain non-GAAP financial performance measures in our MD&A. These new measures are intended to provide additional information only and do not have any standardized meaning prescribed by IFRS and should not be considered in isolation or as substitutes for measures of performance prepared in accordance with IFRS. Other companies may calculate these measures differently. For a detailed description of each of the non-GAAP measures used in this MD&A, please see the discussion under “Non-GAAP Financial Performance Measures” beginning on page 79 of our MD&A. In 2012, we added or made changes to the following non-GAAP performance measures:

Total Cash Costs per pound, C1 Cash Costs per pound and C3 Fully Allocated Costs per pound

In 2012, we replaced the non-GAAP measure “total cash costs per pound” for our copper business with “C1 cash costs per pound”. We believe that this change will enable investors to better understand the performance of our global copper segment in comparison to other copper producers who present results on a similar basis. As part of this change, we also introduced “C3 fully allocated costs per pound”. The primary difference between total cash costs and C1 cash costs is that royalties and non-routine charges are excluded from C1 cash costs as they are not direct production costs. C3 fully allocated costs per pound include C1 cash costs, depreciation, royalties, exploration and evaluation expense, administration expense and non-routine charges.

Adjusted Operating Cash Flow

In 2012, we have adjusted our operating cash flow to remove the effect of the “settlement of currency contracts”. This settlement activity is not reflective of the underlying capacity of our operations to generate operating cash flow on a recurring basis, and therefore this adjustment will result in a more meaningful operating cash flow measure for investors and analysts to evaluate our performance in the period and assess our future operating cash flow generating capability.

Adjusted EBITDA

Starting in this MD&A, we are introducing “Adjusted EBITDA” as a non-GAAP measure. We have adjusted our EBITDA to remove the effect of “impairment charges”. These charges are not reflective of our ability to generate liquidity by producing operating cash flow and therefore this adjustment will result in a more meaningful valuation measure for investors and analysts to evaluate our performance in the period and assess our future ability to generate liquidity.

All-in Sustaining Cash Costs per ounce

Beginning in 2013, we are adopting an all-in sustaining cash costs measure. The Company believes that current operating measures commonly used in the gold industry do not capture all of the sustaining expenditures incurred

30

in order to produce gold, and therefore they do not present a complete picture of a company’s operating performance or its ability to generate free cash flow from its current operations. Similarly, they do not reflect all of the expenditures that would be included in the valuation of a gold mining company. For these reasons, the Company is working with the members of the World Gold Council (“WGC”) to define an all-in sustaining cash costs measure that better represents the total costs associated with producing gold. We believe this measure will better meet the needs of analysts, investors and other stakeholders of the Company in assessing its operating performance, its ability to generate free cash flow from current operations and its overall value.

The WGC project to define all-in sustaining cash costs is ongoing and a final standard is expected in the middle of 2013. We expect to conform our disclosure of all-in sustaining cash costs to the measure that is ultimately approved by the WGC. Our current definition of all-in sustaining cash costs commences with total cash costs and then adds sustaining capital expenditures, corporate general and administrative costs, mine site exploration and evaluation costs and environmental rehabilitation costs. This measure seeks to represent the total costs of producing gold from current operations, and therefore it does not include capital expenditures attributable to projects or mine expansions, exploration and evaluation costs attributable to growth projects, income tax payments, interest costs or dividend payments. Consequently, this measure is not representative of all of the Company’s cash expenditures. In addition, our calculation of all-in sustaining cash costs does not include depreciation expense as it does not reflect the impact of expenditures incurred in prior periods. Therefore, it is not indicative of the Company’s overall profitability. All-in sustaining cash costs for 2012 are outlined in the table below:

($ per ounce) | | | |

For the year ended December 31 | | 2012 | |

Total cash costs | | $ | 584 | |

Minesite sustaining capital expenditures | | 155 | |

Mine development expenditures | | 114 | |

Corporate administration applicable to gold segments | | 51 | |

Exploration and evaluation | | 21 | |

Environmental rehabilitation costs | | 20 | |

All-in sustaining cash costs | | $ | 945 | |

Please refer to pages 81 to 84 of this MD&A for a detailed reconciliation of all-in sustaining cash costs.

Index

32 | | Overview |

| | 32 | Our Business and Strategy |

| | 34 | Review of 2012 Results |

| | 36 | Key Business Developments |

| | 39 | Outlook for 2013 |

| | 43 | Exploration and Mineral Reserves and Mineral Resources Update |

| | 45 | Enterprise Risk Management Approach |

| | 45 | Market Overview |

52 | | Review of Annual Financial Results |

| | 52 | Revenues |

| | 52 | Production Costs |

| | 53 | Corporate Administration |

| | 53 | Other Expense/Other Income |

| | 53 | Exploration and Evaluation |

| | 53 | Capital Expenditures |

| | 54 | Finance Cost/Finance Income |

| | 54 | Impairment Charges |

| | 54 | Income Tax |

| | 56 | Operational Overview |

| | 57 | Review of Operating Segments Performance |

63 | | Financial Condition Review |

| | 63 | Balance Sheet Review |

| | 64 | Financial Position and Liquidity |

| | 67 | Financial Instruments |

| | 69 | Commitments and Contingencies |

70 | | Review of Quarterly Results |

71 | | IFRS Critical Accounting Policies and Estimates |

79 | | Non-GAAP Financial Performance Measures |

88 | | Glossary of Technical Terms |

| | | | |

31

Overview

Our Business and Strategy

Our Business

Barrick’s vision is to be the world’s best gold mining company by operating in a safe, profitable and responsible manner. We sell our production in the world market through the following distribution channels: gold bullion is sold in the gold spot market; gold and copper concentrate is sold to independent smelting companies; and copper cathode is sold to various manufacturers and traders.

Barrick’s market capitalization, annual gold production and gold reserves are the largest in the industry. We also produce significant amounts of copper and have significant silver reserves contained within our gold reserves at our Pascua-Lama project. Our large mineral inventory provides significant optionality to metal prices, which supports mine life extension and expansion investment opportunities where the risk-adjusted returns are appropriate.

MARKET CAPITALIZATION as at December 31, 2012

(USD billions)

2012 GOLD PRODUCTION1

(millions of ounces)

(1) Based on fiscal 2012 results publicly available as of February 13, 2013.

We manage our business through seven primary business units: four regional gold businesses, a global copper business, an oil & gas business and a Capital Projects business. This structure enables each business unit to customize corporate strategies to meet the unique conditions in which they operate.

For gold, we manage our operations using a geographical business unit approach, with producing mines concentrated in three regional business units (“RBUs”): North America, South America and Australia Pacific, each of which is led by its own Regional President. We also hold a 73.9% equity interest in African Barrick Gold plc (“ABG”), a publicly traded company, which includes our previously held African gold mines and exploration properties.

Our Global Copper business unit manages our copper business with a view towards maximizing the value of our copper and non-gold assets. The global copper business unit manages the Zaldívar and Lumwana mines and Jabal Sayid project.

32

Our oil & gas business, managed by Barrick Energy, provides an economic hedge against our exposure to oil prices and also provides support for energy-saving initiatives undertaken by our other business units. In January 2013, we confirmed that we have commenced a process to potentially divest Barrick Energy as part of our ongoing global portfolio optimization in accordance with our disciplined capital allocation framework.

Our Capital Projects business, distinct from our other business units, focuses on managing feasibility studies and construction of our major capital projects, while our operating business units manage feasibility studies and construction of mine expansion projects at existing operating mines.

Our business unit structure adds value by enabling the realization of operational efficiencies, allocating resources to individual mines/projects more effectively and understanding and better managing the local business environment, including labor, consumable costs and supply and government and community relations.

We have operating mines or projects in Canada, the United States, the Dominican Republic, Australia, Papua New Guinea, Peru, Chile, Argentina, Zambia, Saudi Arabia, Pakistan and Tanzania. The geographic split of gold production for the year ended December 31, 2012 was as follows:

GOLD PRODUCTION BY REGION IN 2012

Our Strategy

Our actions are driven by our core values reflecting the guiding principles used to run the Company and these values provide the foundation for our strategy. Our core values are:

· Integrity

· Respect and open communication

· Responsibility and accountability

· Teamwork

· Create shareholder value

In 2012, we renewed our focus on maximizing shareholder value and reemphasized our commitment to a disciplined capital allocation framework to guide our decision making. Under this approach, all capital allocation options, which include organic investment in exploration and projects, and acquisitions or divestitures to improve the quality of our portfolio, will be assessed on the basis of maximizing risk-adjusted returns. Our increased emphasis on free cash flow should position the Company, in the future, with the potential to return more capital to shareholders, repay debt, and make additional attractive return investments to upgrade our portfolio. We will seek to optimize the overall returns from our portfolio of assets and projects. Consequently, investments in existing assets that do not generate target returns or long-term free cash flow will be deferred, shelved or divested to improve the overall quality of our portfolio. Our strategy and approach to capital allocation has been summed up as follows:

RETURNS WILL DRIVE PRODUCTION;

PRODUCTION WILL NOT DRIVE RETURNS.

33

Review of 2012 Results

2012 Fourth Quarter and Year-End Results

| | For the three months ended | | For the years ended | |

| | December 31 | | December 31 | |

($ millions, except where indicated) | | 2012 | | 2011 | | 2012 | | 2011 | |

Financial Data | | | | | | | | | |

Revenue | | $ | 4,189 | | $ | 3,761 | | $ | 14,547 | | $ | 14,236 | |

Net earnings/(loss)1 | | (3,062 | ) | 959 | | (665 | ) | 4,484 | |

Per share (“EPS”)2 | | (3.06 | ) | 0.96 | | (0.66 | ) | 4.49 | |

Adjusted net earnings3 | | 1,108 | | 1,166 | | 3,827 | | 4,666 | |

Per share (“adjusted EPS”)2,3 | | 1.11 | | 1.17 | | 3.82 | | 4.67 | |

EBITDA3 | | (4,023 | ) | 1,998 | | 987 | | 8,376 | |

Adjusted EBITDA3 | | 2,173 | | 2,210 | | 7,457 | | 8,611 | |

Total consolidated project capital expenditures | | 697 | | 663 | | 2,616 | | 2,275 | |

Total capital expenditures — expansion, sustaining and mine development | | 1,000 | | 652 | | 3,206 | | 2,316 | |

Operating cash flow | | 1,672 | | 1,224 | | 5,439 | | 5,315 | |

Adjusted operating cash flow3 | | 1,752 | | 1,299 | | 5,156 | | 5,680 | |

Adjusted operating cash flow before working capital changes3 | | 1,696 | | 1,405 | | 5,392 | | 5,819 | |

Free cash flow3 | | $ | (66 | ) | $ | 68 | | $ | (838 | ) | $ | 1,082 | |