EXHIBIT 99.1

SECOND QUARTER REPORT 2012

Based on IFRS and expressed in US dollars.

Barrick Announces Second Quarter 2012 Results

Pascua-Lama Cost Estimate Revised – First Production in Mid-2014

TORONTO, July 26, 2012 – Barrick Gold Corporation (NYSE: ABX, TSX: ABX) (Barrick or the “company”) today reported net earnings of $0.75 billion ($0.75 per share) compared to net earnings of $1.16 billion ($1.16 per share) in the same prior year quarter. Adjusted net earnings were $0.78 billion ($0.78 per share)1 compared to $1.12 billion ($1.12 per share) in the second quarter of 2011. Operating cash flow and adjusted operating cash flow of $0.76 billion1 compare to operating cash flow of $0.75 billion and adjusted operating cash flow of $0.94 billion, respectively, in the same prior year quarter.

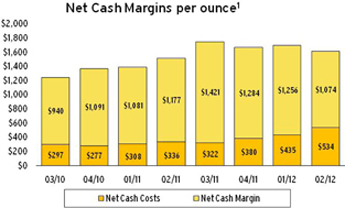

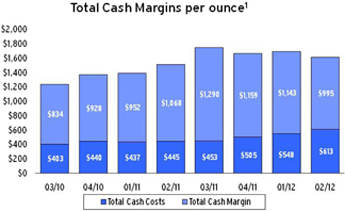

Operating Highlights • Gold and copper production of 1.74 million ounces and 109 million pounds, respectively • Gold total cash costs of $613 per ounce1 and net cash costs of $534 per ounce1 • Gold total cash margins of $995 per ounce1, and net cash margins of $1,074 per ounce1 • C1 copper cash costs of $2.28 per pound1 and C1 copper cash margins of $1.17 per pound1

Pascua-Lama Cost Increase • Due to lower than expected productivity and persistent inflationary and other cost pressures, as previously disclosed, the company initiated a detailed review of the cost and schedule estimates for Pascua-Lama in the second quarter. Preliminary results currently indicate an approximate 50-60 percent increase in capital costs from the top end of the previously announced estimate of $4.7-$5.0 billion, with first production expected in mid-2014. The company will provide a further progress update with third quarter results.

Pueblo Viejo Completion • Construction of the Pueblo Viejo and Jabal Sayid projects is essentially complete and capital costs for both projects are anticipated to be within guidance. First gold from Pueblo Viejo is expected in August and initial copper production from Jabal Sayid is anticipated in the third quarter.

2012 and Longer Term Outlook • Expected gold production for 2012 continues to be in the range of 7.3-7.8 million ounces. Total and net cash costs for gold are now anticipated to be slightly higher in the range of $550-$575 per ounce and $460-$500 per ounce2, respectively, primarily as a result of higher first half costs in Australia Pacific and at African Barrick Gold. Expected copper production for 2012 has been adjusted to 460-500 million pounds, primarily reflecting lower than expected production from Lumwana, and C1 cash costs are expected to be $2.10-$2.30 per pound. Total capital expenditures for 2012 are now anticipated to be $6.0-$6.3 billion.3 • In light of the current economic environment and Barrick’s increased rigor on disciplined capital allocation, the company has determined that various pipeline projects do not currently meet its investment hurdles. As a result, our gold and copper production base is now expected to be 8+ million ounces by 2015 and 600+ million pounds by 2013, respectively, representing a high quality and profitable core from which to expand further. |

| 1 | Adjusted net earnings, adjusted operating cash flow, gold total cash costs and net cash costs per ounce, gold total cash margins and net cash margins per ounce, C1 copper cash costs and C1 copper cash margins per pound are non-GAAP financial measures. See pages 44-48 of Barrick’s Q2 2012 Report. |

| 2 | Based on an assumed realized copper price of $3.50 per pound for the balance of 2012. |

| 3 | Reflects the increase in Pascua-Lama capital expenditures. |

| BARRICK SECOND QUARTER 2012 | 1 | PRESS RELEASE |

“Our second quarter earnings reflected lower gold production and higher operating costs as anticipated, but we continue to generate strong financial results and expect to have a stronger second half,” said Jamie Sokalsky, President and Chief Executive Officer. “We have announced a schedule delay and an increase in capital at Pascua-Lama, as well as some short term production challenges at Lumwana. These are disappointing developments but we are focused on addressing these challenges and they are my top priorities. We are taking immediate and strong action to get both on the right path.

I have also initiated a thorough review of our mines and projects to evaluate their rates of return and ability to generate free cash flow as part of a more disciplined capital allocation framework. In my view, rate of return should drive production, not the other way around. Our new Pueblo Viejo mine is an excellent example of an investment with an attractive rate of return that will generate free cash flow. I am very pleased to report that it has been completed on schedule and will begin contributing low cost ounces shortly.”

FINANCIAL AND OPERATING RESULTS

Reported net earnings were $0.75 billion or $0.75 per share compared to $1.16 billion or $1.16 per share in the same prior year quarter. Net adjusting items in the quarter totaled $34 million and significant components of this include:

| • | $29 million in tax adjustments related to a rate change in Canada and a foreign income tax assessment |

| • | $25 million in asset impairment charges (primarily related to available-for-sale investments) |

| • | $17 million in unrealized foreign currency translation losses |

| • | $12 million in severance costs |

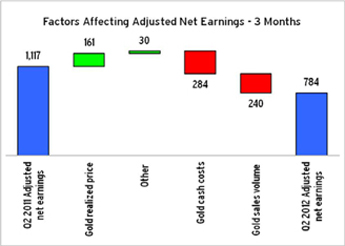

Second quarter 2012 adjusted net earnings were $0.78 billion or $0.78 per share compared to $1.12 billion or $1.12 per share in the same prior year period. The lower net earnings and adjusted net earnings primarily reflect higher cost of sales for gold and copper, lower gold sales volumes and lower realized copper prices, partially offset by higher realized gold prices, higher copper sales volumes and lower income tax expense.

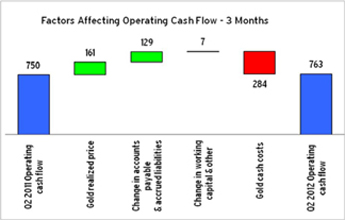

Operating cash flow and adjusted operating cash flow of $0.76 billion for the quarter compare to operating

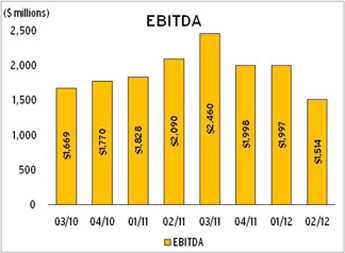

cash flow of $0.75 billion and adjusted operating cash flow of $0.94 billion, respectively, in the second quarter of 2011. The higher operating cash flow primarily reflects a decrease in net working capital outflows and income tax payments, as well as the impact of one-time acquisition related costs on operating cash flow in the second quarter of 2011, partially offset by lower net earnings. EBITDA for the second quarter was $1.51 billion4 compared to $2.09 billion in the same prior year period, reflecting the same factors affecting net earnings, except for income tax expense.

The second quarter realized gold price was $1,608 per ounce4, six percent higher than the same prior year period. Gold total cash margins and net cash margins were $995 per ounce and $1,074 per ounce compared to $1,068 per ounce and $1,177 per ounce in the second quarter of 2011. The realized copper price in the second quarter was $3.45 per pound4, 15 percent lower than the same prior year quarter.

PRODUCTION AND COSTS

Second quarter gold production was 1.74 million ounces at total cash costs of $613 per ounce and net cash costs of $534 per ounce. As previously disclosed, gold production in the second quarter was expected to be lower and total cash costs higher than the first quarter, with better results anticipated in the second half as lower cost mines contribute to a greater proportion of company production. Second quarter copper production of 109 million pounds at C1 cash costs of $2.28 per pound primarily reflects the impact of a waste stripping deficit accumulated in prior years as well as planned mill maintenance and the expected impact of the rainy season on ground conditions at Lumwana.

North America Regional Business Unit

North America produced 0.85 million ounces at total cash costs of $516 per ounce in the second quarter. Cortez production of 0.38 million ounces at total cash costs of $286 per ounce in the second quarter exceeded expectations on higher than expected underground grades and higher ore tons from the open pit.

Goldstrike produced 0.25 million ounces at total cash costs of $616 per ounce. As indicated with first quarter

| 4 | EBITDA and realized gold and copper prices per ounce/pound are non-GAAP financial measures. See pages 44-48 of Barrick’s Q2 2012 Report. |

| BARRICK SECOND QUARTER 2012 | 2 | PRESS RELEASE |

results, production in the second quarter was impacted by lower throughput capacity due to the planned shutdown of the roaster for maintenance. Goldstrike is expected to benefit in the second half of the year from increased throughput capacity following maintenance improvements implemented during the first half and from access to higher grades with completion of underground development. We continue to expect full year production for the region to be in the range of 3.425-3.60 million ounces at total cash costs of $475-$525 per ounce.

South America Regional Business Unit

South America produced 0.33 million ounces at total cash costs of $458 per ounce in the second quarter. The Veladero mine produced 0.16 million ounces at total cash costs of $397 per ounce. The mine experienced lower equipment availability as well as lower recoveries due to slower leach kinetics in addition to expected lower grades. At Lagunas Norte, production of 0.14 million ounces at total cash costs of $365 per ounce reflected mine sequencing and was also impacted by water management issues which restricted access to high grade areas of the open pit. Lagunas Norte is expected to return to higher production levels in the second half of the year with access to higher grades following the completion of pit dewatering. We continue to expect full year production for the region to be in the range of 1.55-1.70 million ounces at total cash costs of $430-$480 per ounce.

Australia Pacific Regional Business Unit

Australia Pacific produced 0.45 million ounces at total cash costs of $844 per ounce in the second quarter. The Porgera mine produced 0.10 million ounces at total cash costs of $1,014 per ounce, primarily reflecting lower underground tons mined. Expected full year production for Australia Pacific continues to be 1.80-1.95 million ounces. Total cash costs are now anticipated to be in the $770-$800 per ounce range in 2012 compared to the original guidance range of $700-$750 per ounce, primarily due to higher total cash costs in the first half of the year at Porgera and a similar outlook for the second half.

African Barrick Gold plc (ABG)

Second quarter attributable production from ABG was 0.11 million ounces at total cash costs of $950 per ounce, mainly reflecting lower grades from Buzwagi, as well as

higher energy costs. Barrick’s share of 2012 production continues to be expected at 0.500-0.535 million ounces. Total cash costs are expected to be at the top end of the original $790-$860 per ounce range.

Copper

The Zaldívar copper mine in Chile produced 73 million pounds at C1 cash costs of $1.56 per pound in the second quarter. The Lumwana mine in Zambia produced 36 million pounds of copper at C1 cash costs of $3.53 per pound.

Previous ownership at Lumwana planned and operated the mine with a view to maximizing short-term production. Production and C1 cash costs have been primarily constrained by a historical waste stripping deficit, and, as previously disclosed with our first quarter results, were expected to be impacted in the second quarter by planned mill maintenance and poor ground conditions from the wet season, which also led to lower than anticipated equipment availability. Barrick has determined it needs to advance a number of key initiatives at Lumwana in order to improve site performance and maximize longer-term returns and value. These initiatives include:

| • | increased waste stripping |

| • | migration to owner maintenance, currently underway, to improve maintenance practices and equipment availability |

| • | infrastructure improvements to mitigate the impact of the annual rainy season |

| • | key leadership changes at site, the majority of which were recently made |

In addition, the company will increasingly focus on advancing work around the large Chimiwungo deposit, which is the primary future ore supply for the operation.

As a result of a weaker than expected first half performance from the Malundwe pit and efforts to advance these key initiatives, we now expect 2012 production from Lumwana to be 145-165 million pounds at C1 cash costs of $3.30-$3.50 per pound. Overall higher grades are expected in 2013, with production anticipated to be about 250 million pounds at lower C1 cash costs. Beyond 2013, the scale of the Chimiwungo orebody is expected to allow for more productive mining. The expansion into the Chimiwungo deposit is on schedule. Commissioning of the crusher and overland conveyor system was completed in July and mill

| BARRICK SECOND QUARTER 2012 | 3 | PRESS RELEASE |

feed is expected in early August. About one million tonnes of ore have been stockpiled to date.

Exploration results to date continue to confirm the significant upside potential of Chimiwungo. We are also conducting a substantial infill drilling program to provide a more precise model of the ore body for mine planning purposes. These programs are expected to be completed at the end of the year and will form the basis for an updated resource base and life-of-mine plan. They will also be incorporated into a prefeasibility study on the expansion opportunity for Lumwana, which has the potential to double processing rates.

The company has floor protection on approximately 60 percent of its expected copper production for the remainder of 2012 at an average floor price of $3.75 per pound5 and has full participation to any upside in copper prices.

COST MANAGEMENT

Barrick continues to employ key risk management strategies which have helped manage our cost exposures, maximize margins and give predictability to our earnings.

The largest currency exposure for the company is the Australian dollar/US dollar exchange rate. Barrick is substantially hedged on its remaining Australian operating and administrative expenditures for 2012 at an effective average rate of $0.80. The company is also 94 percent hedged on expected Australian operating expenditures in 2013 at an effective average rate of $0.84. Additional hedge coverage is also in place for 2014-2016 at levels below current rates.

The company has also mitigated the impact of higher crude oil prices through the use of financial contracts and production from Barrick Energy. The Barrick Energy contribution, along with the financial contracts, provides hedge protection for approximately 70 percent of the expected remaining 2012 fuel consumption.

EXPLORATION UPDATE

The 2012 exploration budget is $450-$490 million6, of which over 40 percent is for major exploration programs at Goldrush, Lumwana and Turquoise Ridge. These are key projects with large drill programs which are expected

| 5 | The average realized price on total 2012 production is expected to be reduced by approximately $0.17 per pound as a result of the net premium paid for these positions. |

| 6 | Barrick’s exploration programs are designed and conducted under the supervision of Robert Krcmarov, Senior Vice President, Global Exploration of Barrick. |

to add to and upgrade gold and copper resources in 2012-2013 and directly contribute to various planned scoping, prefeasibility and expansion studies.

In Nevada, over 50 drill rigs are currently operating, 12 of which are located at Goldrush. Overall, the robustness and continuity of the Goldrush system continues to be demonstrated. The limits of the entire system still remain open in multiple directions. Based on results to date, a significant increase is expected by 2012 year end to the already defined indicated resource of 1.3 million ounces and inferred resource of 5.7 million ounces7.

At Lumwana, the full contingent of 23 exploration drill rigs is operating at Chimiwungo. Drilling to date has increased confidence in the ability to substantially upgrade resource categorization and has also demonstrated strong potential for resource expansion outside of current reserve and resource areas. Favorably thickened ore zones, grading 0.8 percent copper on average in the Equinox and Roan Shoots, are being intersected both within the current inferred resource areas as well as in areas of no previously defined resources, adjacent to and along the trend of these ore shoots.

Results have also identified strong mineralization between the shoots, typically grading 0.7-0.8 percent copper. This Intershoot zone appears to project to depths of less than 150 meters from surface, which could favorably impact near term development opportunities and offer significantly more operational flexibility.

These results are expected to significantly grow 2011 copper reserves and resources, which had already been increased by about 75 percent from the pre-acquisition copper inventory to 4.9 billion pounds of proven and probable reserves, 2.1 billion pounds of measured and indicated resources and 10.7 billion pounds of inferred resources7.

PROJECT UPDATE

Pueblo Viejo

Construction of the 60 percent-owned Pueblo Viejo project in the Dominican Republic has been essentially completed on schedule. Mine construction capital is expected to be within the previously disclosed guidance of $3.6-$3.8 billion (100 percent basis) or $2.2-$2.3 billion

| 7 | Calculated in accordance with National Instrument 43-101 as required by Canadian securities regulatory authorities. For a breakdown of reserves and resources by category and additional information relating to reserves and resources, see pages 161-166 of Barrick’s 2011 Year-End Report. |

| BARRICK SECOND QUARTER 2012 | 4 | PRESS RELEASE |

(Barrick’s 60 percent share). First gold is expected in August and commercial production continues to be anticipated in the fourth quarter of 2012. Pueblo Viejo is expected to contribute approximately 100,000-125,000 ounces of gold to Barrick at total cash costs of $400-$500 per ounce8 in 2012 as it ramps up to full production in 2013. Barrick’s 60 percent share of annual gold production in the first full five years of operation is expected to average 625,000-675,000 ounces at total cash costs of $300-$350 per ounce9.

About 16.4 million tonnes of ore, representing approximately 1.9 million contained gold ounces, has been stockpiled to date. During the quarter, construction on the tailings starter dam advanced to in excess of 175 meters. The mine is now fully connected to the national grid and has also secured additional supplemental onsite power. Major systems completed and commissioned include: the water supply system, main switch yard and harmonic filters, ore and limestone crushing and grinding, the first two of four autoclaves, the oxygen plant (with the first of two trains in production) and the first of three lime kilns.

Construction is well advanced on a 215 MW dual fuel power plant at an estimated net incremental cost of approximately $300 million (100 percent basis) or $180 million (Barrick’s 60 percent share). The power plant is expected to commence operations in 2013 utilizing heavy fuel oil, but have the ability to subsequently transition to lower cost liquid natural gas.

Pascua-Lama

Pascua-Lama is expected to be one of the world’s largest, lowest cost mines and, once in production, is expected to contribute significant free cash flow to Barrick for many years to come. As previously disclosed with our first quarter results, due to lower than expected productivity and persistent inflationary and other cost pressures, the company initiated a detailed review of Pascua-Lama’s schedule and cost estimate in the second quarter.

While the review is not yet complete, preliminary results currently indicate that initial gold production is now expected in mid-2014, with an approximate 50-60 percent increase in capital costs from the top end of the

| 8 | Based on a WTI oil price assumption of $90/bbl. The 2012 total cash cost estimate is dependent on the rate at which production ramps up after commercial levels of production are achieved. A change in the efficiency of the ramp up could have a significant impact on this estimate. |

| 9 | Based on gold and WTI oil price assumptions of $1,300/oz and $90/bbl, respectively. Does not include escalation for future inflation. |

previously announced estimate of $4.7-$5.0 billion. Approximately $3 billion has been spent to date. Inflationary pressures have also had an impact on total cash costs, which are now expected to be $0 to negative $150 per ounce based on a silver price of $25 per ounce10.

Based on information gathered to date, it is apparent that the challenges of building a project of this scale and complexity were greater than we anticipated. We also determined that we needed to re-align the project management structure between Barrick and our EPCM partners, Fluor and Techint. We have taken immediate actions to address these issues. We are strengthening the project management structure by seeking to have Fluor take over a greater proportion of the construction management of the project. Barrick is also working with Fluor and Techint to develop an integrated action plan that ensures the scope of remaining work is well planned and executed and has also engaged a leading EPCM organization to provide an independent assessment of the status of the project. We will provide a further progress update with third quarter results.

The key factors contributing to the capital cost increase are:

| • | lower than expected contractor productivity (~30%) |

| • | engineering and planning gaps (~25%) |

| • | cost escalation (~25%) |

| • | schedule extension (~20%) |

The delay to the schedule arises primarily from delays to completing the camps, tunnel and process plant.

In addition to the major change being made to construction management, we are also taking a series of other steps to mitigate the schedule and cost pressures. We have expedited procurement of key equipment and supplies to protect against adverse forward price movements and expanded procurement efforts in local markets. We have had notable successes with the fabrication and procurement of tanks and power transformers which are now being sourced in Argentina. We have also been ensuring since last year that, to the extent possible, new contracts for major work packages are done on a fixed fee basis, which should help mitigate significant labor cost increases.

| 10 | First full five year average. Based on gold, silver and WTI oil price assumptions of $1,300/oz, $25/oz and $90/bbl, respectively, and assuming a Chilean Peso assumption of 475:1. Inflation escalation assumptions are as of Q2 2012, and do not include escalation for future inflation. |

| BARRICK SECOND QUARTER 2012 | 5 | PRESS RELEASE |

During the second quarter, the project achieved critical milestones with completion of Phase 1 of the pioneering road and also the water management system in Chile, both of which enabled the commencement of pre-stripping activities. At the end of the second quarter, the tunnel was about 40 percent complete, the power-line in Chile was about 50 percent complete, and approximately 75 percent of the targeted 10,000 beds were available.

While Pascua-Lama has some unique challenges, it is a world-class resource with nearly 18 million ounces of proven and probable gold reserves plus silver contained within gold reserves of 676 million ounces7. Annual gold and silver production in the first full five years of a 25 year mine life is expected to average 800,000-850,000 ounces and 35 million ounces, respectively.

Jabal Sayid

Construction of the Jabal Sayid copper project in Saudi Arabia has been essentially completed and total project capital expenditures are expected to be approximately $400 million11, in line with expectations. Current efforts are focused on completing pre-commissioning testing. The ore crushing circuit is complete and ore is expected to be processed in the third quarter.

The mine has received approval of the Environmental and Social Impact Assessment (ESIA) permit relating to construction and project commissioning. Additional safety and security design engineering is being completed to enable shipments of concentrates to commence by mid-2013.

Approximately 320,000 tons of underground ore had been mined at the end of the second quarter, representing about 17.2 million contained pounds of copper. Jabal Sayid is expected to produce 25-35 million pounds of copper in 2012, slightly below original guidance as plant commissioning has been delayed by one month. This production will be included within finished goods inventory until the project is in receipt of authorization to enable the shipment of concentrates. Average annual production from Jabal Sayid is expected to be 100-130 million pounds over the first full five years of operation at C1 cash costs of $1.50-$1.70 per pound12.

| 11 | Includes approximately $125 million in incurred costs prior to Barrick’s acquisition of Equinox Minerals in 2011. |

| 12 | Does not include escalation for future inflation. |

PROJECTS IN FEASIBILITY AND PERMITTING

Barrick is evaluating its next tier of projects. Cerro Casale and Donlin Gold do not currently meet our investment criteria, primarily due to their large initial capital investments, and under our disciplined capital allocation framework we would not make a decision to construct them at this time. However, they contain large, long life mineral resources in stable jurisdictions, have significant leverage to the price of gold, and therefore represent valuable long-term opportunities for the company. We will maintain and enhance the option value of these projects by advancing permitting activities at reasonable costs which, in the case of Donlin Gold, will take a number of years. During this time, we will monitor the attractiveness of these projects and evaluate alternatives to improve their economics. This will provide the company with the option to make construction decisions in the future should investment conditions warrant.

2012 OUTLOOK

Barrick maintains its full year gold production guidance of 7.3-7.8 million ounces. As previously indicated, production is expected to be higher in the second half of 2012 compared to the first half as production commences at Pueblo Viejo and as Goldstrike and Lagunas Norte contribute to a greater proportion of production.

Total and net cash costs for gold are now expected to be slightly higher in the range of $550-$575 per ounce and $460-$500 per ounce, respectively, mainly due to higher costs in Australia Pacific and at African Barrick Gold in the first half of the year. Total cash costs are expected to be lower in the second half as a result of significantly higher overall production levels and lower cost mines contributing to a greater share of total company production.

Full year copper production is now expected to be 460-500 million pounds, primarily as a result of lower than anticipated production from Lumwana, at C1 cash costs of $2.10-$2.30 per pound.

CAPITAL ALLOCATION FRAMEWORK

Barrick’s renewed focus on maximizing shareholder value will be achieved through a disciplined approach to capital allocation based on maximizing returns on investment and free cash flow within the context of the prevailing

| BARRICK SECOND QUARTER 2012 | 6 | PRESS RELEASE |

economic and political environment. Under this approach, all capital allocation options, which include organic investment in exploration and projects, and acquisitions or divestitures to improve the quality of our portfolio, will be assessed on the basis of maximizing risk-adjusted returns. Our increased emphasis on free cash flow will position the company with the potential to return more capital to shareholders, repay debt, and make additional attractive return investments to upgrade our portfolio.

The company has recently launched a full review of its operations and projects to ensure they meet our objective of delivering appropriate risk-adjusted returns and maximizing free cash flow generation. In light of the current economic environment and this increased rigor on disciplined capital allocation, we have determined that various pipeline projects do not currently meet our investment criteria.

As a result, our annual gold production base is now expected to be 8+ million ounces by 2015 once Pueblo Viejo and Pascua-Lama are in full production. Our annual base copper production is expected to be 600+ million pounds by 2013, with the opportunity to increase to more than 1 billion pounds should the company decide to proceed with the Zaldívar Sulfides expansion and the Lumwana expansion. This production base represents a high quality and profitable core on which to expand further.

* * * *

Barrick’s vision is to be the world’s best gold company by finding, acquiring, developing and producing quality reserves in a safe, profitable and socially responsible manner. Barrick’s shares are traded on the Toronto and New York stock exchanges.

| BARRICK SECOND QUARTER 2012 | 7 | PRESS RELEASE |

Key Statistics

Barrick Gold Corporation (in United States dollars) | Three months ended June 30, | Six months ended June 30, | ||||||||||||||

| (Unaudited) | 2012 | 2011 | 2012 | 2011 | ||||||||||||

Operating Results | ||||||||||||||||

Gold production (thousands of ounces)1 | 1,742 | 1,977 | 3,623 | 3,934 | ||||||||||||

Gold sold (thousands of ounces) | 1,690 | 1,915 | 3,473 | 3,778 | ||||||||||||

Per ounce data | ||||||||||||||||

Average spot gold price | $ 1,609 | $1,506 | $1,651 | $1,445 | ||||||||||||

Average realized gold price2 | 1,608 | 1,513 | 1,651 | 1,452 | ||||||||||||

Net cash costs2 | 534 | 336 | 483 | 322 | ||||||||||||

Total cash costs2 | 613 | 445 | 580 | 441 | ||||||||||||

Depreciation3 | 185 | 152 | 182 | 147 | ||||||||||||

Other4 | 12 | 17 | 13 | 16 | ||||||||||||

Total production costs | 810 | 614 | 775 | 604 | ||||||||||||

Copper credits | 79 | 109 | 97 | 119 | ||||||||||||

Copper production (millions of pounds) | 109 | 93 | 226 | 168 | ||||||||||||

Copper sold (millions of pounds) | 116 | 82 | 234 | 162 | ||||||||||||

Per pound data | ||||||||||||||||

Average spot copper price | $ 3.57 | $4.14 | $3.67 | $4.26 | ||||||||||||

Average realized copper price2 | 3.45 | 4.07 | 3.62 | 4.16 | ||||||||||||

C1 cash costs2 | 2.28 | 1.54 | 2.18 | 1.39 | ||||||||||||

Depreciation3 | 0.55 | 0.26 | 0.50 | 0.25 | ||||||||||||

Other5 | 0.14 | 0.29 | 0.14 | 0.14 | ||||||||||||

C3 fully allocated costs2 | 2.97 | 2.09 | 2.82 | 1.78 | ||||||||||||

Financial Results (millions) | ||||||||||||||||

Revenues | $ 3,278 | $3,416 | $6,922 | $6,503 | ||||||||||||

Net earnings6 | 750 | 1,159 | 1,779 | 2,160 | ||||||||||||

Adjusted net earnings2 | 784 | 1,117 | 1,870 | 2,121 | ||||||||||||

EBITDA2 | 1,514 | 2,090 | 3,511 | 3,918 | ||||||||||||

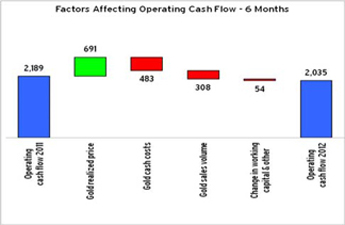

Operating cash flow | 763 | 750 | 2,035 | 2,189 | ||||||||||||

Adjusted operating cash flow2 | 763 | 938 | 2,137 | 2,377 | ||||||||||||

Per Share Data (dollars) | ||||||||||||||||

Net earnings (basic) | 0.75 | 1.16 | 1.78 | 2.16 | ||||||||||||

Adjusted net earnings (basic)2 | 0.78 | 1.12 | 1.87 | 2.12 | ||||||||||||

Net earnings (diluted) | 0.75 | 1.16 | 1.78 | 2.16 | ||||||||||||

Weighted average basic common shares (millions) | 1,000 | 999 | 1,000 | 999 | ||||||||||||

Weighted average diluted common shares (millions)7 | 1,001 | 1,001 | 1,001 | 1,001 | ||||||||||||

Return on equity2 | 13% | 21% | 16% | 21% | ||||||||||||

| As at | As at | |||||||||||||||

| June 30, | December 31, | |||||||||||||||

| 2012 | 2011 | |||||||||||||||

Financial Position (millions) | ||||||||||||||||

Cash and equivalents | $ 2,330 | $ 2,745 | ||||||||||||||

Non-cash working capital | 2,902 | 2,335 | ||||||||||||||

Adjusted debt2 | 13,667 | 13,058 | ||||||||||||||

Net debt2 | 11,354 | 10,320 | ||||||||||||||

Average shareholders’ equity | 24,031 | 21,418 | ||||||||||||||

| 1 | Production includes our equity share of gold production at Highland Gold up to April 26, 2012, the effective date of our sale of Highland Gold. |

| 2 | Realized price, net cash costs, total cash costs, C1 cash costs, C3 fully allocated costs, adjusted net earnings, EBITDA, adjusted operating cash flow, adjusted debt, net debt, and return on equity are non-GAAP financial performance measures with no standard definition under IFRS. See pages 44-48 of the Company’s MD&A. |

| 3 | Represents equity amortization expense divided by equity ounces of gold sold or pounds of copper sold. |

| 4 | Represents the Barrick Energy gross margin divided by equity ounces of gold sold. |

| 5 | For a breakdown, see reconciliation of cost of sales to C1 cash costs and C3 fully allocated costs per pound on page 46 of the Company’s MD&A. |

| 6 | Net earnings represents net income attributable to the equity holders of the Company. |

| 7 | Fully diluted includes dilutive effect of stock options. |

| BARRICK SECOND QUARTER 2012 | 8 | SUMMARY INFORMATION |

Production and Cost Summary

| Gold Production (attributable ounces) (000’s) | Total Cash Costs ($/oz) | |||||||||||||||||||||||||||||||

|

|

|

| |||||||||||||||||||||||||||||

Three months ended June 30, | Six months ended June 30, | Three months ended June 30, | Six months ended June 30, | |||||||||||||||||||||||||||||

|

|

|

|

|

|

|

| |||||||||||||||||||||||||

| (Unaudited) | 2012 | 2011 | 2012 | 2011 | 2012 | 2011 | 2012 | 2011 | ||||||||||||||||||||||||

|

|

|

|

|

|

| ||||||||||||||||||||||||||

North America | 854 | 923 | 1,742 | 1,785 | $ 516 | $404 | $ 505 | $ 400 | ||||||||||||||||||||||||

South America | 327 | 453 | 778 | 951 | 458 | 373 | 435 | 358 | ||||||||||||||||||||||||

Australia Pacific | 445 | 463 | 871 | 922 | 844 | 611 | 798 | 597 | ||||||||||||||||||||||||

African Barrick Gold1 | 113 | 127 | 220 | 256 | 950 | 652 | 938 | 655 | ||||||||||||||||||||||||

Other2 | 3 | 11 | 12 | 20 | - | - | - | - | ||||||||||||||||||||||||

| ||||||||||||||||||||||||||||||||

Total | 1,742 | 1,977 | 3,623 | 3,934 | $ 613 | $445 | $ 580 | $ 441 | ||||||||||||||||||||||||

| ||||||||||||||||||||||||||||||||

| Copper Production (attributable pounds) (Millions) |

| C1 Cash Costs ($/lb) | ||||||||||||||||||||||||||||||||

| Three months ended June 30, | Six months ended June 30, | Three months ended June 30, | Six months ended June 30, | |||||||||||||||||||||||||||||||

|

|

|

|

|

|

|

| |||||||||||||||||||||||||||

(Unaudited) | 2012 | 2011 | 2012 | 2011 | 2012 | 2011 | 2012 | 2011 | ||||||||||||||||||||||||||

| ||||||||||||||||||||||||||||||||||

Total | 109 | 93 | 226 | 168 | $ 2.28 | $ 1.54 | $ 2.18 | $ 1.39 | ||||||||||||||||||||||||||

| Total Gold Production Costs ($/oz) | ||||||||||||||||

| Three months ended June 30, | Six months ended June 30, | |||||||||||||||

|

|

|

| |||||||||||||

(Unaudited) | 2012 | 2011 | 2012 | 2011 | ||||||||||||

Direct mining costs at market foreign exchange rates | $ 642 | $ 501 | $ 619 | $ 489 | ||||||||||||

Gains realized on currency hedge and commodity hedge/economic hedge contracts | (40 | ) | (57 | ) | (49 | ) | (51 | ) | ||||||||

Other3 | (12 | ) | �� | (17 | ) | (13 | ) | (16 | ) | |||||||

By-product credits | (18 | ) | (19 | ) | (17 | ) | (18 | ) | ||||||||

Copper credits | (79 | ) | (109 | ) | (97 | ) | (119 | ) | ||||||||

Cash operating costs, net basis | 493 | 299 | 443 | 285 | ||||||||||||

Royalties | 41 | 37 | 40 | 37 | ||||||||||||

Net cash costs4 | 534 | 336 | 483 | 322 | ||||||||||||

Copper credits | 79 | 109 | 97 | 119 | ||||||||||||

Total cash costs4 | 613 | 445 | 580 | 441 | ||||||||||||

Depreciation | 185 | 152 | 182 | 147 | ||||||||||||

Other3 | 12 | 17 | 13 | 16 | ||||||||||||

Total production costs | $ 810 | $ 614 | $ 775 | $ 604 | ||||||||||||

| Total Copper Production Costs ($/lb) | ||||||||||||||||

| Three months ended June 30, | Six months ended June 30, | |||||||||||||||

|

|

|

| |||||||||||||

(Unaudited) | 2012 | 2011 | 2012 | 2011 | ||||||||||||

C1 cash costs4 | $ 2.28 | $ 1.54 | $ 2.18 | $ 1.39 | ||||||||||||

Depreciation | 0.55 | 0.26 | 0.50 | 0.25 | ||||||||||||

Other5 | 0.14 | 0.29 | 0.14 | 0.14 | ||||||||||||

C3 fully allocated costs4 | $ 2.97 | $ 2.09 | $ 2.82 | $ 1.78 | ||||||||||||

| ||||||||||||||||

| 1 | Figures relating to African Barrick Gold are presented on a 73.9% basis, which reflects our equity share of production. |

| 2 | Includes our equity share of gold production at Highland Gold up to April 26, 2012, the effective date of our sale of Highland Gold. |

| 3 | Represents the Barrick Energy gross margin divided by equity ounces of gold sold. |

| 4 | Total cash costs, net cash costs, C1 cash costs and C3 fully allocated costs are non-GAAP financial performance measures with no standard meaning under IFRS. See page 45 of the Company’s MD&A. |

| 5 | For a breakdown, see reconciliation of cost of sales to C1 cash costs and C3 fully allocated costs per pound on page 45 of the Company’s MD&A. |

| BARRICK SECOND QUARTER 2012 | 9 | SUMMARY INFORMATION |

MANAGEMENT’S DISCUSSION AND ANALYSIS (“MD&A”)

This portion of the Quarterly Report provides management’s discussion and analysis (“MD&A”) of the financial condition and results of operations to enable a reader to assess material changes in financial condition and results of operations as at and for the three and six month periods ended June 30, 2012, in comparison to the corresponding prior–year periods. The MD&A is intended to help the reader understand Barrick Gold Corporation (“Barrick”, “we”, “our” or the “Company”), our operations, financial performance and present and future business environment. This MD&A, which has been prepared as of July 25, 2012, is intended to supplement and complement the condensed unaudited interim consolidated financial statements and notes thereto, prepared in accordance with international Accounting Standard 34 Interim Financial Reporting (“IAS 34”) as issued by the International Accounting Standards Board (“IASB”), for the three and six month periods ended June 30, 2012 (collectively, the “Financial Statements”), which are included in this Quarterly Report on pages 49 to 71. You are encouraged to review the Financial Statements in conjunction with your review of this MD&A. This MD&A should be read in conjunction with both the annual

audited consolidated financial statements for the two years ended December 31, 2011, the related annual MD&A included in the 2011 Annual Report, and the most recent Form 40–F/Annual Information Form on file with the US Securities and Exchange Commission (“SEC”) and Canadian provincial securities regulatory authorities. Certain notes to the Financial Statements are specifically referred to in this MD&A and such notes are incorporated by reference herein. All dollar amounts in this MD&A are in millions of US dollars, unless otherwise specified.

For the purposes of preparing our MD&A, we consider the materiality of information. Information is considered material if: (i) such information results in, or would reasonably be expected to result in, a significant change in the market price or value of our shares; or (ii) there is a substantial likelihood that a reasonable investor would consider it important in making an investment decision; or (iii) it would significantly alter the total mix of information available to investors. We evaluate materiality with reference to all relevant circumstances, including potential market sensitivity.

CAUTIONARY STATEMENT ON FORWARD-LOOKING INFORMATION

Certain information contained or incorporated by reference in this MD&A, including any information as to our strategy, projects, plans or future financial or operating performance, constitutes “forward-looking statements”. All statements, other than statements of historical fact, are forward-looking statements. The words “believe”, “expect”, “anticipate”, “contemplate”, “target”, “plan”, “intend”, “continue”, “budget”, “estimate”, “may”, “will”, “schedule” and similar expressions identify forward-looking statements. Forward-looking statements are necessarily based upon a number of estimates and assumptions that, while considered reasonable by the Company, are inherently subject to significant business, economic and competitive uncertainties and contingencies. Known and unknown factors could cause actual results to differ materially from those projected in the forward-looking statements. Such factors include, but are not limited to: fluctuations in the spot and forward price of gold and copper or certain other commodities (such as silver, diesel fuel and electricity); diminishing quantities or grades of reserves; the impact of inflation; changes in national and local government legislation, taxation, controls, regulations, expropriation or nationalization of property and political or economic developments in Canada, the United States, Dominican Republic, Australia, Papua New Guinea, Chile, Peru, Argentina, Tanzania, Zambia, Saudi Arabia, United Kingdom, Pakistan or Barbados or other countries in

which we do or may carry on business in the future; the impact of global liquidity and credit availability on the timing of cash flows and the values of assets and liabilities based on projected future cash flows; fluctuations in the currency markets (such as Canadian and Australian dollars, Chilean and Argentinean peso, British pound, Peruvian sol, Zambian kwacha, South African rand, Tanzanian schilling, and Papua New Guinean kina versus the US dollar); changes in US dollar interest rates that could impact the mark-to-market value of outstanding derivative instruments and ongoing payments/receipts under interest rate swaps and variable rate debt obligations; risks arising from holding derivative instruments (such as credit risk, market liquidity risk and mark-to-market risk); risk of loss due to acts of war, terrorism, sabotage and civil disturbances; business opportunities that may be presented to, or pursued by, the Company; our ability to successfully integrate acquisitions; operating or technical difficulties in connection with mining or development activities; employee relations; availability and increased costs associated with mining inputs and labor; increased costs and technical challenges associated with the construction of capital projects; litigation; the speculative nature of mineral exploration and development, including the risks of obtaining necessary licenses and permits; adverse changes in our credit rating; contests over title to properties, particularly title to undeveloped properties;

| BARRICK SECOND QUARTER 2012 | 10 | MANAGEMENT’S DISCUSSION AND ANALYSIS |

and the organization of our previously held African gold operations and properties under a separate listed company. In addition, there are risks and hazards associated with the business of mineral exploration, development and mining, including environmental hazards, industrial accidents, unusual or unexpected formations, pressures, cave-ins, flooding and gold bullion or copper cathode losses (and the risk of inadequate insurance, or inability to obtain insurance, to cover these risks). Many of these uncertainties and contingencies can affect our actual results and could cause actual results to differ materially from those expressed or implied in any forward-looking statements made by, or on

behalf of, us. Readers are cautioned that forward-looking statements are not guarantees of future performance. All of the forward-looking statements made in this MD&A are qualified by these cautionary statements. Specific reference is made to the most recent Form 40-F/Annual Information Form on file with the SEC and Canadian provincial securities regulatory authorities for a discussion of some of the factors underlying forward-looking statements. We disclaim any intention or obligation to update or revise any forward-looking statements whether as a result of new information, future events or otherwise, except as required by applicable law.

| INDEX | ||||

| page | ||||

Financial and Operating Highlights | ||||

2012 Second Quarter Results | 12 | |||

Business Overview, Outlook and Market Review | 14 | |||

Financial and Operating Results | ||||

Summary of Operating Results | 23 | |||

Summary Cash Flow Performance | 24 | |||

Key Operating Performance Metrics | 25 | |||

Mining Overview | 28 | |||

Review of Operating Segment Results | 29 | |||

Financial Condition Review | ||||

Balance Sheet Review | 36 | |||

Liquidity and Cash Flow | 37 | |||

Financial Instruments | 40 | |||

Commitments and Contingencies | 41 | |||

Review of Quarterly Results | 42 | |||

IFRS Critical Accounting Policies and Accounting Estimates | 42 | |||

Non-GAAP Financial Performance Measures | 44 | |||

| BARRICK SECOND QUARTER 2012 | 11 | MANAGEMENT’S DISCUSSION AND ANALYSIS |

FINANCIAL AND OPERATING HIGHLIGHTS

Summary of Financial and Operating Data

| For the three months ended June 30 | For the six months ended June 30 | |||||||||||||||

| ($ millions, except where indicated) | 2012 | 2011 | 2012 | 2011 | ||||||||||||

Financial Data | ||||||||||||||||

Revenue | $ 3,278 | $3,416 | $ 6,922 | $6,503 | ||||||||||||

Net earnings1 | 750 | 1,159 | 1,779 | 2,160 | ||||||||||||

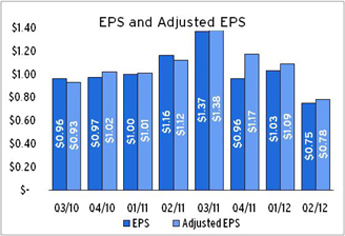

Per share (“EPS”)2 | 0.75 | 1.16 | 1.78 | 2.16 | ||||||||||||

Adjusted net earnings3 | 784 | 1,117 | 1,870 | 2,121 | ||||||||||||

Per share (“adjusted EPS”)2,3 | 0.78 | 1.12 | 1.87 | 2.12 | ||||||||||||

EBITDA3 | 1,514 | 2,090 | 3,511 | 3,918 | ||||||||||||

Total consolidated project capital expenditures | 805 | 630 | 1,494 | 1,205 | ||||||||||||

Total capital expenditures – expansion, sustaining, and open pit & underground mine development | 777 | 438 | 1,403 | 934 | ||||||||||||

Operating cash flow | 763 | 750 | 2,035 | 2,189 | ||||||||||||

Adjusted operating cash flow3 | 763 | 938 | 2,137 | 2,377 | ||||||||||||

Adjusted operating cash flow before working capital changes3 | 817 | 926 | 2,396 | 2,471 | ||||||||||||

Free cash flow3 | (746 | ) | (24 | ) | (606 | ) | 441 | |||||||||

| ||||||||||||||||

Operating Data | ||||||||||||||||

Gold | ||||||||||||||||

Gold produced (000s ounces)4 | 1,742 | 1,977 | 3,623 | 3,934 | ||||||||||||

Gold sold (000s ounces) | 1,690 | 1,915 | 3,473 | 3,778 | ||||||||||||

Realized price ($ per ounce)3 | $ 1,608 | $1,513 | $ 1,651 | $1,452 | ||||||||||||

Net cash costs ($ per ounce)3 | $534 | $336 | $483 | $322 | ||||||||||||

Total cash costs ($ per ounce)3 | $613 | $445 | $580 | $441 | ||||||||||||

Copper | ||||||||||||||||

Copper produced (millions of pounds) | 109 | 93 | 226 | 168 | ||||||||||||

Copper sold (millions of pounds) | 116 | 82 | 234 | 162 | ||||||||||||

Realized price ($ per pound)3 | $ 3.45 | $4.07 | $ 3.62 | $4.16 | ||||||||||||

C1 cash costs ($ per pound)3 | $ 2.28 | $1.54 | $ 2.18 | $1.39 | ||||||||||||

| 1 | Net earnings represent net income attributable to the equity holders of the Company. |

| 2 | Calculated using weighted average number of shares outstanding under the basic method. |

| 3 | Adjusted net earnings, adjusted EPS, EBITDA, adjusted operating cash flow, adjusted operating cash flow before working capital changes, free cash flow, realized price, net cash costs, total cash costs and C1 cash costs are non-GAAP financial performance measures with no standardized definition under IFRS. For further information and a detailed reconciliation, please see pages 44 – 48 of this MD&A. |

| 4 | We sold our 20.4% investment in Highland Gold with an effective date of April 26, 2012. Production includes our equity share of gold production at Highland Gold up to that date. |

SECOND QUARTER FINANCIAL AND OPERATING HIGHLIGHTS

| • | Net earnings and adjusted net earnings for the second quarter 2012 were $750 million and $784 million, respectively, down $409 million and $333 million from the same prior year period. The decrease in net earnings and adjusted net earnings was largely driven by higher cost of sales applicable to gold and copper, lower gold sales volumes and lower realized copper prices, partially offset by higher realized gold prices, higher copper sales volumes and lower income tax expense. These results were in line with our expectations, as second quarter 2012 was expected to be our lowest production and highest cost quarter of 2012. The magnitude of the decrease also reflects the fact that second quarter 2011 was our highest production quarter for that year. |

| • | EPS and adjusted EPS for the second quarter 2012 were $0.75 and $0.78, respectively, down 35% and 30%, over the same prior year period. The changes reflect the decrease in both net earnings and adjusted net earnings. |

| • | EBITDA for the second quarter 2012 was $1,514 million, down 28% over the same prior year period, reflecting the same factors affecting net earnings, except for income tax expense. |

| BARRICK SECOND QUARTER 2012 | 12 | MANAGEMENT’S DISCUSSION AND ANALYSIS |

| • | Operating cash flow for the second quarter 2012 was $763 million, up slightly compared to the same prior year period. The increase in operating cash flow primarily reflects a decrease in income tax payments of $130 million and a decrease in net working capital outflows of $309 million, partially offset by lower net earnings. Income tax payments in second quarter 2012 were $606 million, compared to the income tax payments of $736 million made in 2011, which included about $420 million in payments related to 2010. Free cash flow for the second quarter of 2012 decreased by $722 million compared to the same prior year period, reflecting primarily higher capital expenditures on our projects in construction. |

| • | Significant adjusting items (net of tax effects) in the second quarter include: $25 million in asset impairment charges, primarily related to our available-for-sale investments, $17 million in unrealized foreign currency translation losses, $12 million in severance costs, $4 million in unrealized losses on non-hedge derivative instruments, $29 million in tax adjustments related to a rate change in Canada and a foreign income tax assessment and $6 million in gains from the sale of assets. |

| • | Gold production and sales volumes for the second quarter 2012 were 1.742 million ounces and 1.690 million ounces, respectively, both down 12% over the same prior year period, primarily due to lower production at Veladero, Goldstrike and Cortez. Gold production in second quarter 2012 was in line with our expectations as we anticipated this quarter to be our lowest producing quarter of the year. |

| • | Total cash costs for the second quarter 2012 were $613 per ounce, up 38% over the same prior year period. The increase reflects increases in direct mining costs, including higher labor, energy, maintenance and consumable costs across all our regions as well as the impact of lower production levels. Net cash costs for second quarter 2012 were $534 per ounce, an increase of $198 per ounce or 59% compared to the same prior year period, due to higher total cash costs and lower copper credits. Total cash costs are expected to be the highest in the second quarter 2012 and are expected to be lower in the second half of 2012 as a result of higher production levels and lower cost mines contributing to a greater share of production. |

| • | Copper production and C1 cash costs for the second quarter 2012 were 109 million pounds and $2.28 per pound respectively, compared to production of 93 million pounds at C1 cash costs of $1.54 per pound in the same prior year period. Copper production and C1 cash costs increased in second quarter 2012 primarily due to the inclusion of a full quarter of higher cost production from Lumwana, acquired as part of the Equinox acquisition which closed on June 1, 2011. Copper production and C1 cash costs in second quarter 2012 also reflect poorer than expected performance at Lumwana. |

FIRST SIX MONTHS 2012 vs. FIRST SIX MONTHS 2011

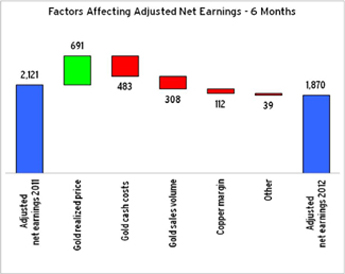

| • | Net earnings and adjusted net earnings for the first half of 2012 were $1,779 million and $1,870 million, respectively, compared to the net earnings of $2,160 million and adjusted net earnings of $2,121 million recorded in the first half of 2011. The decrease in net earnings and adjusted net earnings was largely driven by lower gold sales volumes, higher cost of sales applicable to gold and copper and lower market copper prices, partially offset by higher copper sales volumes, higher market gold prices and lower income tax expense. We expect production levels to be higher during the second half of 2012. The decreases in net earnings and adjusted net earnings were magnified by the fact that the first half of 2011 experienced higher production levels at lower cash costs compared to full 2011 results. |

| • | EPS and adjusted EPS for the first half of 2012 were $1.78 and $1.87, respectively, down 18% and 12%, respectively, compared to EPS of $2.16 and adjusted EPS of $2.12 for the first half of 2011. The decreases were due to the decrease in both net earnings and adjusted net earnings. |

| • | EBITDA for the first half of 2012 was $3,511 million, compared to EBITDA of $3,918 million for the first half of 2011. The decrease in EBITDA reflects the same factors affecting net earnings, except for income tax expense. |

| • | Operating cash flow was $2,035 million, compared to operating cash flow of $2,189 million for the first half of 2011. Adjusted operating cash flow was $2,137 million compared to $2,377 million for the first half of 2011. The decreases in operating cash flow and adjusted operating cash flow primarily reflects lower net earnings levels, partially offset by a decrease in income tax payments of $57 million and a decrease in net working capital outflows of $28 million. Income tax payments in first half 2012 were $967 million, compared to the income tax payments of $1,024 million made in 2011, which included about $470 million in payments related to 2010. Free cash flow for the first half of 2012 decreased by $1,047 million compared to the same prior year period primarily reflecting higher capital expenditures on our projects in construction. |

| • | Significant adjusting items (net of tax effects) in the first half of 2012 include: $118 million in asset impairment charges, which include a write-down of our investment in Highland Gold ($85 million) and write-downs on our available-for-sale |

| BARRICK SECOND QUARTER 2012 | 13 | MANAGEMENT’S DISCUSSION AND ANALYSIS |

investments ($31 million), $12 million in unrealized foreign currency translation losses, $12 million in severance costs, $29 million in tax adjustments related to a rate change in Canada and a foreign income tax assessment, $19 million in unrealized gains on non-hedge derivative instruments and $14 million in gains from the sale of assets. |

| • | Gold production and sales volumes for first half of 2012 were 3.62 million ounces and 3.47 million ounces, respectively. In first half of 2011, gold production and sales volumes were 3.93 million and 3.78 million ounces, respectively. The decrease in production and sales volumes compared to the prior year period is primarily due to lower production across all our regions, particularly at Veladero, Goldstrike and Porgera. |

| • | Total cash costs for gold were $580 per ounce, up $139 per ounce or 32% compared to the first half of 2011. The increase reflects increases in direct mining costs, including higher labor, energy, maintenance and consumable costs across all our regions as well as the impact of lower production levels. Net cash costs were $483 per ounce in first half of 2012, an increase of $161 per ounce or 50% compared to the same prior year period. The increase in net cash costs reflects higher total cash costs and lower copper credits. Total cash costs per ounce are expected to be lower in the second half of 2012. |

| • | Copper production and C1 cash costs for the first half of 2012 were 226 million pounds at C1 direct cash costs of $2.18 per pound respectively, compared to production of 168 million pounds at C1 direct cash cost of $1.39 per pound for the first half of 2011. Copper production and C1 cash costs increased for the first half of 2012 primarily due to the inclusion of a full six months of higher cost production from Lumwana, as well as poorer than expected first half performance at Lumwana. |

Business Overview

Senior Management Team Changes and Capital Allocation Framework

On June 6, 2012 Jamie Sokalsky, our long-serving Chief Financial Officer, was appointed as President and Chief Executive Officer, replacing Aaron Regent, the previous CEO of Barrick. Ammar Al-Joundi, an experienced finance executive within the mining industry, joined the Company as Chief Financial Officer. Our Chief Operating Officer, Peter Kinver, retired from his position at the end of the second quarter, and was succeeded by Igor Gonzales, previously President of our South American Business Unit. We appointed Guillermo Calo as President for Barrick’s South America Business Unit.

We are confident that these leadership changes will enable us to renew our focus on maximizing shareholder value. Our strategic objectives will be achieved through a disciplined approach to capital allocation with a view to maximizing return on investment within the context of the prevailing economic and political environment and maximizing the generation of free cash flow. Under this approach, all capital allocation options, which include organic investment in exploration and projects and acquisitions or divestitures to improve the quality of our asset portfolio, will be assessed on the basis of maximizing risk-adjusted returns. Our increased emphasis on free cash flow will position the company with the potential to return more capital to shareholders, repay debt, and make additional attractive return investments to upgrade our portfolio.

In the second quarter of 2012, we launched a full review of the operations and projects in our portfolio to ensure that

they meet our objective of delivering appropriate risk adjusted returns and maximizing our free cash flow generation. In light of the current economic environment and this increased rigor on disciplined capital allocation, we have determined that various pipeline projects, while contributing to the targeted increase in our gold production to nine million ounces by 2016, do not currently meet our investment hurdles. As a result, our annual gold production base is now expected to be 8+ million ounces by 2015 once Pueblo Viejo and Pascua-Lama are in full production. Our annual base copper production is expected to be 600+ million pounds by 2013, with the opportunity to increase to more than 1 billion pounds should the company decide to proceed with the Zaldívar Sulfides expansion and the Lumwana expansion. This production base represents a high quality and profitable core on which to expand further.

Projects in Construction

Pueblo Viejo

Construction of the 60 percent-owned Pueblo Viejo project in the Dominican Republic has been essentially completed on schedule. Mine construction capital is expected to be within the previously disclosed guidance of $3.6-$3.8 billion (100 percent basis) or $2.2-$2.3 billion (Barrick’s 60 percent share). First gold is expected in August and commercial production continues to be anticipated in the fourth quarter of 2012. Pueblo Viejo is expected to contribute approximately 100,000-125,000 ounces of gold to Barrick at total cash costs of $400-$500

| BARRICK SECOND QUARTER 2012 | 14 | MANAGEMENT’S DISCUSSION AND ANALYSIS |

per ounce1 in 2012 as it ramps up to full production in 2013. Barrick’s 60 percent share of annual gold production in the first full five years of operation is expected to average 625,000-675,000 ounces at total cash costs of $300-$350 per ounce2.

About 16.4 million tonnes of ore, representing approximately 1.9 million contained gold ounces, has been stockpiled to date. During the quarter, construction on the tailings starter dam advanced to in excess of 175 meters. The mine is now fully connected to the national grid and has also secured additional supplemental onsite power. Major systems completed and commissioned include: the water supply system, main switch yard and harmonic filters, ore and limestone crushing and grinding, the first two of four autoclaves, the oxygen plant (with the first of two trains in production) and the first of three lime kilns.

Construction is well advanced on a 215 MW dual fuel power plant at an estimated net incremental cost of approximately $300 million (100 percent basis) or $180 million (Barrick’s 60 percent share). The power plant is expected to commence operations in 2013 utilizing heavy fuel oil, but have the ability to subsequently transition to lower cost liquid natural gas.

Jabal Sayid

Construction of the Jabal Sayid copper project in Saudi Arabia has been essentially completed and total project capital expenditures are expected to be approximately $400 million3, in line with expectations. Current efforts are focused on completing pre-commissioning testing. The ore crushing circuit is complete and ore is expected to be processed in the third quarter.

The mine has received approval of the Environmental and Social Impact Assessment (ESIA) permit relating to construction and project commissioning. Additional safety and security design engineering is being completed to enable shipments of concentrates to commence by mid-2013.

Approximately 320,000 tons of underground ore had been mined at the end of the second quarter, representing about 17.2 million contained pounds of copper. Jabal Sayid is expected to produce 25-35 million pounds of copper in 2012, slightly below original guidance, as plant

| 1 | Based on a WTI oil price assumption of $90/bbl. The 2012 total cash cost estimate is dependent on the rate at which production ramps up after commercial levels of production are achieved. A change in the efficiency of the ramp up could have a significant impact on this estimate. |

| 2 | Based on gold and WTI oil price assumptions of $1,300/oz and $90/bbl, respectively. Does not include escalation for future inflation. |

| 3 | Includes approximately $125 million in incurred costs prior to Barrick’s acquisition of Equinox Minerals in 2011. |

commissioning has been delayed by one month. This production will be included within finished goods inventory until the project is in receipt of authorization to enable the shipment of concentrates. Average annual production from Jabal Sayid is expected to be 100-130 million pounds over the first full five years of operation at C1 cash costs of $1.50-$1.70 per pound4.

Pascua-Lama

Pascua-Lama is expected to be one of the world’s largest, lowest cost mines and, once in production, is expected to contribute significant free cash flow to Barrick for many years to come. As previously disclosed with our first quarter results, due to lower than expected productivity and persistent inflationary and other cost pressures, the company initiated a detailed review of Pascua-Lama’s schedule and cost estimate in the second quarter.

While the review is not yet complete, preliminary results currently indicate that initial gold production is now expected in mid-2014, with an approximate 50-60 percent increase in capital costs from the top end of the previously announced estimate of $4.7-$5.0 billion. Approximately $3 billion has been spent to date. Inflationary pressures have also had an impact on total cash costs, which are now expected to be $0 to negative $150 per ounce based on a silver price of $25 per ounce5.

Based on information gathered to date, it is apparent that the challenges of building a project of this scale and complexity were greater than we anticipated. We also determined that we needed to re-align the project management structure between Barrick and our EPCM partners, Fluor and Techint. We have taken immediate actions to address these issues. We are strengthening the project management structure by seeking to have Fluor take over a greater proportion of the construction management of the project. Barrick is also working with Fluor and Techint to develop an integrated action plan that ensures the scope of remaining work is well planned and executed and has also engaged a leading EPCM organization to provide an independent assessment of the status of the project. We will provide a further progress update with third quarter results.

| 4 | Does not include escalation for future inflation. |

| 5 | First full five year average. Based on gold, silver and WTI oil price assumptions of $1,300/oz, $25/oz and $90/bbl, respectively, and assuming a Chilean Peso assumption of 475:1. Inflation escalation assumptions are as of Q2 2012, and do not include escalation for future inflation. |

| BARRICK SECOND QUARTER 2012 | 15 | MANAGEMENT’S DISCUSSION AND ANALYSIS |

The key factors contributing to the capital cost increase are:

| • | lower than expected contractor productivity (~30%) |

| • | engineering and planning gaps (~25%) |

| • | cost escalation (~25%) |

| • | schedule extension (~20%) |

The delay to the schedule arises primarily from delays to completing the camps, tunnel and process plant.

In addition to the major change being made to construction management, we are also taking a series of other steps to mitigate the schedule and cost pressures. We have expedited procurement of key equipment and supplies to protect against adverse forward price movements and expanded procurement efforts in local markets. We have had notable successes with the fabrication and procurement of tanks and power transformers which are now being sourced in Argentina. We have also been ensuring since last year that, to the extent possible, new contracts for major work packages are done on a fixed fee basis, which should help mitigate significant labor cost increases.

During the second quarter, the project achieved critical milestones with completion of Phase 1 of the pioneering road and also the water management system in Chile, both of which enabled the commencement of pre-stripping activities. At the end of the second quarter, the tunnel was about 40 percent complete, the power-line in Chile was about 50 percent complete and approximately 75 percent of the targeted 10,000 beds were available.

While Pascua-Lama has some unique challenges, it is a world-class resource with nearly 18 million ounces of proven and probable gold reserves plus silver contained within gold reserves of 676 million ounces6. Annual gold and silver production in the first full five years of a 25 year mine life is expected to average 800,000-850,000 ounces and 35 million ounces, respectively.

Goldstrike Thiosulfate Technology

Construction of the thiosulfate technology project, including the retrofitting of the existing plant, as well as new installations, commenced in the first quarter. This project allows for continued production from the autoclaves, which were originally expected to cease operations in 2012, and brings forward production of about 3.5 million ounces in the mine plan. First gold

| 6 | Calculated in accordance with National Instrument 43-101 as required by Canadian securities regulatory authorities. For a breakdown of reserves and resources by category and additional information relating to reserves and resources, see pages 161-166 of Barrick’s 2011 Year-End Report. |

production is expected in the fourth quarter of 2013, with an average annual contribution of about 350 to 400 thousand ounces over the first full five years. Project costs are expected to be about $350 million.

Projects at Feasibility/Permitting Stage

Barrick is evaluating its next tier of projects. Cerro Casale and Donlin Gold do not currently meet our investment criteria, primarily due to their large initial capital investments, and under our disciplined capital allocation framework we would not make a decision to construct them at this time. However, they contain large, long life mineral resources in stable jurisdictions, have significant leverage to the price of gold, and therefore represent valuable long-term opportunities for the company. We will maintain and enhance the option value of these projects by advancing permitting activities at reasonable costs which, in the case of Donlin Gold, will take a number of years. During this time, we will monitor the attractiveness of these projects and evaluate alternatives to improve their economics. This will provide the company with the option to make construction decisions in the future should investment conditions warrant.

Cerro Casale

At the Cerro Casale project in Chile, the Environmental Impact Assessment (EIA) permitting process is currently underway. We have initiated a review of the project’s upfront initial capital and are also evaluating options to improve the project’s economics. Options being evaluated include differential processing options, alternative sources of power supply, assessment of the results of exploration drilling on satellite ore bodies that could potentially be included in the project plan, and pursuing potential synergies relating to infrastructure requirements. We expect to have the exploration drilling and results of the review of other options completed by mid 2013, at which point we will re-evaluate whether the project meets our investment criteria.

Cerro Casale, on a 100 percent basis, has total proven and probable gold and copper mineral reserves of 23 million ounces of gold and 5.8 billion pounds of copper. Barrick’s 75 percent share of average annual production from Cerro Casale has the potential to be 750,000-825,000 ounces of gold and 190-210 million pounds of copper in the first full five years of operation at total cash costs of $200-$250 per ounce7. Estimated mine construction capital, based on the present mine design, which excludes the impact of the options that are under review, is approximately $6.0 billion (100 percent basis)8.

| 7 | Based on gold, copper and oil prices of $1,300/oz, $3.25/lb and $100/bbl, respectively and assuming a Chilean peso f/x rate of 475:1. Does not include escalation for inflation. |

| 8 | Does not include escalation for inflation. |

| BARRICK SECOND QUARTER 2012 | 16 | MANAGEMENT’S DISCUSSION AND ANALYSIS |

Donlin Gold

At the 50 percent-owned Donlin Gold project in Alaska, the Board of Donlin Gold LLC formally approved the revised feasibility study (FSU2) in July and during the third quarter the project will submit a Plan of Operations (PoO) and a wetlands permit application to federal regulators, formally initiating the permitting process under the National Environmental Policy Act (NEPA) and leading to the development of an Environmental Impact Statement (EIS). Additionally, the project’s management team is also working to conclude negotiations to amend the mining surface land use agreement. Donlin Gold has indicated resource potential of approximately 39 million ounces of gold (100 percent basis) and has the potential to produce about 1.5 million ounces of gold annually (100 percent basis) in its first full five years of operation. The project does not presently meet our investment criteria, primarily due to its initial capital investment of about $6.7 billion (100 percent basis). However, Donlin Gold contains a large, long life mineral resource in a stable jurisdiction and is significantly leveraged to the price of gold, and therefore represents a valuable long-term opportunity for the company. We will maintain and enhance the option value of this project by advancing the permitting process, at reasonable costs, which will take a number of years. During this time, we will monitor the attractiveness of the project and evaluate alternatives to improve the economics with the objective of defining a project that satisfies our investment criteria. This will provide the company with the option to make a construction decision in the future should investment conditions warrant.

Kabanga

At the 50 percent-owned Kabanga nickel project in Tanzania, the Environment Impact Statement (EIS) was submitted to the National Environment Management Council (NEMC) in the first quarter, with a review meeting held in the second Quarter. In the second Quarter, the draft Mine Development Agreement (MDA) was lodged with the Ministry of Energy and Minerals (MEM) and the resettlement working group was reactivated to begin engaging those families that will need to relocate once the project is approved. The rest of the year efforts are focused on obtaining approval of the EIS and granting of the Environmental Certificate (EC), and finalizing the feasibility study. Additionally, the project will be pursuing the receipt of a Special Mining License (SML) and negotiating the MDA with the Tanzanian government.

Projects at Scoping/Pre-Feasibility Stage

Lagunas Norte Sulfides Expansion

A scoping study has been completed on the Lagunas Norte deep sulfide potential and the project is undergoing metallurgical and geotechnical work that will be completed

in fourth quarter 2012 before a decision to proceed with a prefeasibility study is made in 2013. This expansion opportunity has the potential to add 3.3 million ounces to life of mine production starting as early as 2018. Following a review of this project in second quarter 2012, we determined that the project does not presently meet our investment criteria and consequently we plan to evaluate options to improve the project’s economic returns with the objective of defining a project that satisfies our investment criteria.

Zaldívar Sulfides Expansion

A scoping study has been completed on the Zaldívar deep sulfides, and a prefeasibility study is now expected by fourth quarter 2013. This expansion opportunity has the potential to significantly increase annual mine production starting as early as 2018 and could significantly increase copper reserves/resources and extend the mine life. Following a review of this project in second quarter 2012, we determined that the project presently meets our investment criteria, subject to the impact of finalizing a prefeasibility and later a full feasibility study.

Cortez Hills Lower Zone

At the Cortez Hills Lower Zone Expansion project in Nevada, advancement continues on the exploration decline. Two exploration rigs continue to delineate the ore body in the lower zone. Infill drilling continues in the upper zone to convert resource to reserve classification. The expansion provides an opportunity to increase production and extend the mine life. A prefeasibility study has been completed and a feasibility study is expected to commence in the second half of 2012. Following a review of this project in second quarter 2012, we determined that the project presently meets our investment criteria, subject to the impact of finalizing a full feasibility study.

Hemlo Expansion

We have identified an opportunity at the Hemlo mine to expand the open pit and extend the mine life by up to 7 years from 2018, adding about 1 million ounces of gold to the life of mine plan. We are currently working on a feasibility study for the expansion, which is expected to be completed in the second half of 2012. Following a review of this project in second quarter 2012, we determined that the project does not presently meet our investment criteria and consequently in conjunction with the finalization of the feasibility study we plan to evaluate options to improve the project’s economic returns with the objective of defining a project that satisfies our investment criteria.

| BARRICK SECOND QUARTER 2012 | 17 | MANAGEMENT’S DISCUSSION AND ANALYSIS |

Exploration Update

The 2012 exploration budget is $450-$490 million9, of which over 40 percent is for major exploration programs at Goldrush, Lumwana and Turquoise Ridge. These are key projects with large drill programs which are expected to add to and upgrade gold and copper resources in 2012-2013 and directly contribute to various planned scoping, prefeasibility and expansion studies.

Goldrush

In Nevada, over 50 drill rigs are currently operating, 12 of which are located at Goldrush. Overall, the robustness and continuity of the Goldrush system continues to be demonstrated. The limits of the entire system still remain open in multiple directions. Based on results to date, a significant increase is expected by 2012 year end to the already defined indicated resource of 1.3 million ounces and inferred resource of 5.7 million ounces10.

Lumwana

At Lumwana, the full contingent of 23 exploration drill rigs is operating at Chimiwungo. Drilling to date has increased confidence in the ability to substantially upgrade resource categorization and has also demonstrated strong potential for resource expansion outside of current reserve and resource areas. Favorably thickened ore zones, grading 0.8 percent copper on average in the Equinox and Roan Shoots, are being intersected both within the current inferred resource areas as well as in areas of no previously defined resources, adjacent to and along the trend of these ore shoots.

Results have also identified strong mineralization between the shoots, typically grading 0.7-0.8 percent copper. This Intershoot zone appears to project to depths of less than 150 meters from surface, which could favorably impact near term development opportunities and offer significantly more operational flexibility.

These results are expected to significantly grow 2011 copper reserves and resources, which had already been increased by about 75 percent from the pre-acquisition copper inventory, to 4.9 billion pounds of proven and probable reserves, 2.1 billion pounds of measured and indicated resources and 10.7 billion pounds of inferred resources10.