Exhibit 99.1

SECOND QUARTER REPORT 2017

All amounts expressed in U.S. dollars unless otherwise indicated

Barrick Reports Second Quarter 2017 Results

| | ● | | Barrick reported second quarter net earnings attributable to equity holders (“net earnings”) of $1.084 billion ($0.93 per share), and adjusted net earnings1 of $261 million ($0.22 per share). |

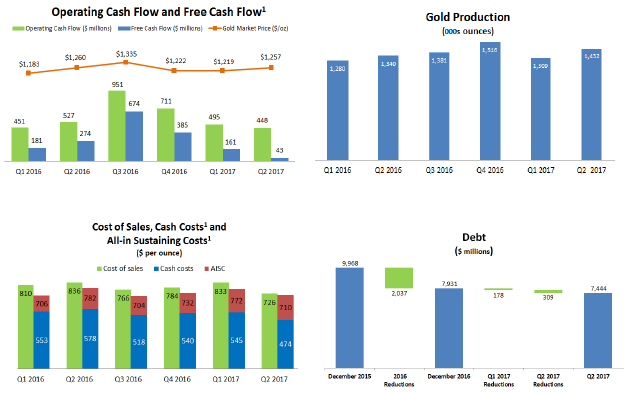

| | ● | | The Company reported second quarter revenues of $2.160 billion, net cash provided by operating activities (“operating cash flow”) of $448 million, and free cash flow2 of $43 million. |

| | ● | | Gold production in the second quarter was 1.432 million ounces, at a cost of sales applicable to gold3 of $726 per ounce, andall-in sustaining costs4 of $710 per ounce. |

| | ● | | Total debt was reduced by $309 million in the second quarter. |

| | ● | | We continue to expect full-year gold production of5.3-5.6 million ounces, at a cost of sales3 of$780-$820 per ounce, andall-in sustaining costs4 of$720-$770 per ounce. |

| | ● | | Normal leaching operations, including the addition of cyanide, have resumed at the Veladero mine in Argentina, following the anticipated ramp up and testing of upgraded leach pad systems. |

| | ● | | We completed the formation of our strategic partnership with Shandong Gold, a landmark agreement with the potential to create fundamental long-term value for our respective owners, as well as our community and government partners in Argentina. |

| | ● | | Barrick will begin discussions with the Government of Tanzania next week concerning the concentrate export ban and other issues impacting Acacia Mining plc’s operations in the country. |

TORONTO, July 26, 2017 — Barrick Gold Corporation (NYSE:ABX)(TSX:ABX) (“Barrick” or the “Company”) today reported second quarter results for the period ending June 30, 2017.

Our portfolio delivered higher gold production and a 10 percent decrease in direct mining costs compared to the prior-year period, resulting in lower cost of sales andall-in sustaining costs for the second quarter. A number of factors contributed to lower cash flow over the same period, including higher cash taxes paid, an increase in working capital, and a planned increase in capital expenditures focused on sustaining and growing the value of our operations over the long term. We expect higher cash flow in the second half of the year as a number of these factors abate.

Reflecting our drive to maximize the productivity and efficiency of our operations, we have completed the unification of our Cortez and Goldstrike operations, and we are accelerating the implementation of our digital transformation in Nevada, which will support unit cost improvements, increased throughput, and expanding margins. During the quarter we continued to optimize our portfolio for long-term value creation, completing the formation of a strategic partnership with

Shandong that has the potential to unlock the untapped mineral wealth of the El Indio Belt—a highly prospective district on the border of Argentina and Chile that is home to the Veladero mine, Pascua-Lama, Alturas, and other projects.

By applying strict capital discipline, leveraging innovation and digital technologies, and building distinctive partnerships, we are positioning Barrick to grow free cash flow per share over the long term. We continue to advance a deep organic project pipeline that provides our owners with exceptional leverage to gold prices, built on a foundation of core mines that are among the longest-life, lowest-cost gold operations in the industry.

FINANCIAL HIGHLIGHTS

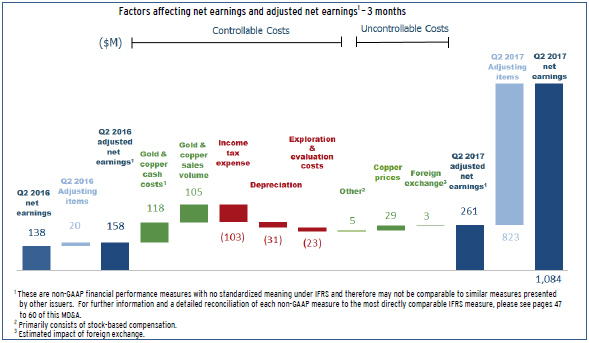

Second quarter net earnings were $1.084 billion ($0.93 per share), compared to $138 million ($0.12 per share) in the prior-year period. This significant increase in net earnings was primarily due to $882 million in gains related to the sale of a 50 percent interest in the Veladero mine, and the sale of a 25 percent interest in the Cerro Casale project.

Adjusted net earnings1 for the second quarter were $261 million ($0.22 per share), compared to $158 million ($0.14 per share) in the prior-year period. Higher adjusted net earnings were primarily the result of a 10 percent decrease in direct mining costs, driven by lower costs at Barrick Nevada and Pueblo Viejo, higher sales from ourlow-cost operations at Barrick Nevada, and lower relative sales from Acacia and Turquoise Ridge compared to the prior-year period. Higher gold and copper sales volumes and higher copper prices also contributed to stronger adjusted net earnings. This was partially offset by an increase in tax expense, higher depreciation, and an increase in exploration and evaluation costs.

Significant adjusting items(pre-tax andnon-controlling interest effects) in the second quarter of 2017 include:

| | ● | | $689 million in a gain relating to the sale of a 50 percent interest in the Veladero mine; |

| | ● | | $193 million in a gain relating to the sale of a 25 percent interest in the Cerro Casale project; partially offset by |

| | ● | | $32 million in foreign currency translation losses primarily related to the devaluation of the Argentine Peso on VAT receivables; and |

| | ● | | $26 million in losses on debt extinguishment. |

Refer to page 48 of Barrick’s second quarter MD&A for a full list of reconciling items between net earnings and adjusted net earnings for the current and prior-year periods.

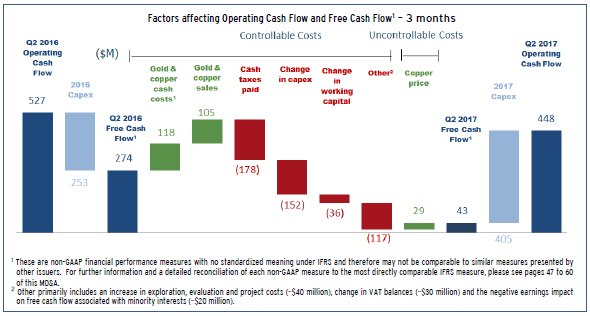

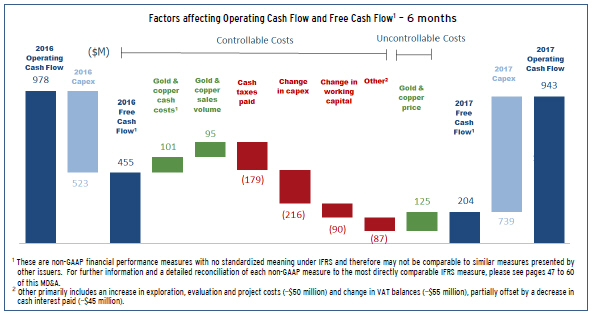

Operating cash flow was $448 million, compared to $527 million in the second quarter of 2016. Lower operating cash flow was primarily due to higher cash taxes paid at Pueblo Viejo. During the quarter we made our final 2016 tax payment in the Dominican Republic, in addition to our first tax payment for 2017. Based on our current estimates, this should result in nominal tax payments at Pueblo Viejo for the remainder of the year. Operating cash flow was further impacted by the concentrate export ban affecting Acacia’s operations in Tanzania, an increase in working capital primarily related to leach pad inventories at Veladero, and an increase in exploration, evaluation, and project costs. These decreases were partially offset by higher gold and copper sales volumes and higher copper prices, combined with lower direct mining costs, as described above.

| | | | |

| BARRICK SECOND QUARTER 2017 | | 2 | | PRESS RELEASE |

Free cash flow2 for the second quarter was $43 million, compared to $274 million in the second quarter of 2016. The decrease primarily reflects higher capital expenditures, combined with lower operating cash flows. On a cash basis, capital expenditures for the second quarter were $405 million, compared to $253 million in the second quarter of 2016. This primarily reflects a planned increase in minesite sustaining capital expenditures at Barrick Nevada, relating to higher capitalized stripping costs and the timing of minesite sustaining projects in the current period, as well as greater spending at Veladero relating to phase 4B and 5B of the leach pad expansion and equipment purchases. The increase in capital expenditures also includes a $31 million increase in project capital, primarily at Barrick Nevada. This includes the Robertson property acquisition, development of Crossroads and the Cortez Hills Lower Zone, and the Goldrush project, partially offset by a decrease in pre-production stripping at the Arturo pit, which entered commercial production in August 2016. These increases reflect high-confidence investments in our most attractive opportunities to sustain and grow the value of our operations over the long term.

RESTORING A STRONG BALANCE SHEET

Achieving and maintaining a strong balance sheet remains a top priority. We intend to reduce our total debt from $7.9 billion at the start of 2017, to $5 billion by the end of 2018—at least half of which we are targeting this year. We will achieve this by using cash flow from operations, further portfolio optimization, and the creation of new joint ventures and partnerships. We will continue to pursue debt reduction with discipline, taking only those actions that make sense for the business, on terms we consider favorable to our shareholders.

We reduced our total debt by $309 million in the second quarter, or a total of $487 million year to date. On June 30, the Company completed the sale of a 50 percent interest in the Veladero mine in Argentina to Shandong for $960 million, which will be allocated to debt reduction.

At the end of the second quarter, Barrick had a consolidated cash balance of approximately $2.9 billion.5 The Company has less than $200 million6 in debt due before 2020. About $5 billion, ortwo-thirds of our outstanding total debt of $7.4 billion, does not mature until after 2032.

OPERATING HIGHLIGHTS AND OUTLOOK

Barrick produced 1.432 million ounces of gold in the second quarter at a cost of sales3 of $726 per ounce. This compares to 1.340 million ounces at a cost of sales3 of $836 per ounce in the prior-year period. After removingnon-controlling interests, cost of sales declined by 13 percent on aper-ounce basis compared to the second quarter of 2016, primarily driven by a 10 percent reduction in direct mining costs, and higher ounces sold.

All-in sustaining costs4 in the second quarter were $710 per ounce, compared to $782 per ounce in the second quarter of 2016. A nine percent reduction inall-in sustaining costs was primarily driven by lower cost of sales per ounce, combined with lower general and administrative expenses, partially offset by an increase in minesite sustaining capital expenditures. Cash costs3 also decreased by 18 percent, from $578 per ounce in the second quarter of 2016, to $474 per ounce in the second quarter of 2017.

| | | | |

| BARRICK SECOND QUARTER 2017 | | 3 | | PRESS RELEASE |

We continue to expect full-year gold production of5.3-5.6 million ounces, at a cost of sales3 of$780-$820 per ounce, andall-in sustaining costs4 of$720-$770 per ounce. This does not include any revisions to Acacia’s annual output as a result of the export ban on concentrates currently impacting Acacia’s operations (see “Tanzania Concentrate Export Ban Update” on page 5 for additional details). We expect production for the remainder of the year to be weighted towards the fourth quarter. Based on sales mix and our current expectations for the timing of capital expenditures, we expect costs to be higher in the third quarter.

The Company produced 104 million pounds of copper in the second quarter, at a cost of sales3 of $1.85 per pound, andall-in sustaining costs7 of $2.38 per pound. This compares to 103 million pounds, at a cost of sales3 of $1.43 per pound, andall-in sustaining costs7 of $2.14 per pound in the second quarter of 2016.

Cost of sales applicable to copper increased by 28 percent compared to the prior-year period, primarily due to higher depreciation expense, and higher power and processing costs at Lumwana. Copperall-in sustaining costs, adjusted to include our proportionate share of equity method investments at Zaldívar and Jabal Sayid, were 10 percent higher in the second quarter. This primarily reflects the higher cost of sales applicable to copper combined with higher minesite sustaining capital expenditures at Jabal Sayid, which only began incurring sustaining capital expenditures upon entering commercial production in July 2016, as well as higher capitalized stripping at Lumwana.

We continue to expect full-year copper production of400-450 million pounds, at a cost of sales3 of$1.50-$1.70 per pound, andall-in sustaining costs7 of$2.10-$2.40 per pound.

As part of our ongoing efforts to increase transparency and strengthen our disclosures, we intend topre-release production and sales figures ahead of our quarterly earnings releases, beginning in the third quarter of 2017.

Please see page 32 of Barrick’s second quarter MD&A for individual operating segment performance details. Detailed mine site guidance information can be found in Appendix 1 of this press release.

| | | | | | | | | | | | |

| Gold | | Second Quarter

2017 | | | Current

2017 Guidance | | | Original

2017 Guidance | |

| | | |

Production8(000s of ounces) | | | 1,432 | | | | 5,300-5,600 | | | | 5,600-5,900 | |

| | | |

Cost of sales applicable to gold3($ per ounce) | | | 726 | | | | 780-820 | | | | 780-820 | |

| | | |

All-in sustaining costs4($ per ounce) | | | 710 | | | | 720-770 | | | | 720-770 | |

| | | |

Copper | | | | | | | | | | | | |

| | |

| | | |

Production8(millions of pounds) | | | 104 | | | | 400-450 | | | | 400-450 | |

| | | |

Cost of sales applicable to copper3($ per pound) | | | 1.85 | | | | 1.50-1.70 | | | | 1.50-1.70 | |

| | | |

All-in sustaining costs7($ per pound) | | | 2.38 | | | | 2.10-2.40 | | | | 2.10-2.40 | |

| | |

Total Attributable Capital Expenditures9($ millions) | | | 393 | | | | 1,300-1,500 | | | | 1,300-1,500 | |

| | |

| | | | |

| BARRICK SECOND QUARTER 2017 | | 4 | | PRESS RELEASE |

Veladero Operational Update

On June 15, San Juan provincial government and judicial authorities lifted operating restrictions that had been imposed at the Veladero heap leach facility in March 2017. Following the lifting of restrictions, Veladero completed a gradualramp-up of the mine’s upgraded leach pad systems, testing the safety and integrity of the new infrastructure. Normal leaching operations at Veladero, including the addition of new cyanide to the heap leach circuit, resumed inmid-July.

On a 100 percent basis, we continue to expect full-year production at Veladero of630,000-730,000 ounces of gold, at a cost of sales3 of$740-$790 per ounce, andall-in sustaining costs4 of$890-$990 per ounce. Barrick’s share of full-year production, reflecting 50 percent ownership from July 1, is expected to be430,000-480,000 ounces of gold.

Tanzania Concentrate Export Ban Update

Barrick holds a 63.9 percent equity interest in Acacia Mining plc, a publicly traded company listed on the London Stock Exchange that is operated independently of Barrick. At this time, Acacia continues to evaluate the impact of Tanzania’s concentrate export ban, as well as recently enacted legislation, on its 2017 production guidance. Acacia has not revised its full-year production guidance to reflect any change to annual output as a result of the concentrate export ban currently in place, but has stated that it is now targeting the lower end of its guidance range. Acacia has also indicated that, given the rate of cash outflow, it does not believe continued operations are sustainable at its Bulyanhulu mine beyond September 30. Barrick continues to monitor the situation, and should Acacia revise its full-year outlook, Barrick will evaluate the impact to its own guidance at that time. Any impact will depend, in large part, on the duration of the concentrate export ban. Acacia operations impacted by the current ban on concentrate exports (Bulyanhulu and Buzwagi) account for approximately six per cent of Barrick’s 2017 gold production guidance. In total, Acacia accounts for approximately 10 percent of Barrick’s 2017 gold production guidance.

In an effort to seek a resolution that is in the best interests of all parties, including the Government of Tanzania, Barrick, and Acacia, Barrick will begin direct discussions with the Government of Tanzania concerning the concentrate export ban and other issues next week. Barrick is doing so in its capacity as Acacia’s largest shareholder. Acacia is not participating directly in the discussions at this stage, however it intends to work with Barrick as necessary to support the process. Any potential resolution arising from these discussions will be subject to approval by Acacia.

STRATEGIC COOPERATION AGREEMENT WITH SHANDONG

On June 30, we completed the formation of our strategic partnership with Shandong. The sale of a 50 percent interest in the Veladero mine in San Juan province, Argentina to Shandong Gold Mining Co., Ltd, for $960 million was the first of three steps outlined in a strategic cooperation agreement signed by Barrick and Shandong Gold Group Co., Ltd. on April 6. In keeping with the second step in the agreement, the two companies have also formed a working group to explore the joint development of the Pascua-Lama deposit. As a third step, Barrick and Shandong will evaluate additional investment opportunities on the highly prospective El Indio Gold Belt on the border of Argentina and Chile, home to Pascua-Lama, Alturas, and other projects.

Following the closing of the transaction, senior Shandong leaders traveled to Argentina to kick off the new partnership, participating in town hall meetings and welcome ceremonies with employees at the Veladero mine and San Juan offices. The delegation also met with San Juan Governor Sergio

| | | | |

| BARRICK SECOND QUARTER 2017 | | 5 | | PRESS RELEASE |

Uñac, San Juan Mining Minister Alberto Hensel, and other provincial and federal government officials. Our first joint venture planning and integration meeting was held on July 11.

PORTFOLIO OPTIMIZATION

Cerro Casale Joint Venture

On June 9, Barrick completed the sale of a 25 percent interest in the Cerro Casale project in Chile to Goldcorp Inc., resulting in the formation of a new 50/50 joint venture to manage the project. Following the completion of Goldcorp’s acquisition of Exeter Resource Corporation, the Joint Venture will control more than 20,000 hectares of land in the Maricunga District, including the Caspiche and Cerro Casale deposits.

Robertson Property Acquisition

On June 8, Barrick completed the acquisition of the Robertson property and other claims in Nevada from Coral Gold Resources. The Robertson property is adjacent to Cortez, located just six kilometers north of the Pipeline mill. If successfully brought into production, ore from the project would provide an additional feed for the Cortez mill, with the potential to extend open pit operations in the Cortez District. Robertson also has processing synergies with the Deep South underground expansion project at Cortez. In addition, the land package contains a number of promising near-mine exploration opportunities, as well potential new exploration targets in this highly prospective and prolific district.

ALTURAS PROJECT UPDATE

The Alturas project, located on the border between Argentina and Chile on the El Indio Belt, is a Barrick greenfield discovery with 6.8 million ounces of inferred gold resources (211 million tonnes, grading 1.0 grams per tonne) as of December 31, 2016.10 We have completed a scoping study for a conventional open pit heap leach operation at Alturas. We believe we can add more value by applying innovative new mining and processing solutions to the project, and through additional reverse circulation (RC) drilling. We are now carrying out further studies to evaluate the feasibility of these potential enhancements. Establishing a more accurate grade model using RC drilling will be one of our objectives for the next drilling season. Our Investment Committee will continue to scrutinize the project as it advances, applying a high degree of consistency and rigor—as we do for all capital allocation decisions at the Company—before further review by Barrick’s Executive Committee and our Board of Directors at each stage of advancement.

TECHNICAL INFORMATION

The scientific and technical information contained in this press release has been reviewed and approved by Steven Haggarty, P. Eng., Senior Director, Metallurgy of Barrick, Rick Sims, Registered Member SME, Senior Director, Resources and Reserves of Barrick, and Patrick Garretson, Registered Member SME, Senior Director, Life of Mine Planning of Barrick, each a “Qualified Person” as defined in National Instrument43-101Standards of Disclosure for Mineral Projects.

| | | | |

| BARRICK SECOND QUARTER 2017 | | 6 | | PRESS RELEASE |

APPENDIX 1 – 2017 Updated Operating and Capital Expenditure Guidance

GOLD PRODUCTION AND COSTS

| | | | | | | | |

| | | Production

(millions of ounces) | | Cost of sales3

($ per ounce) | | All-in

sustaining costs4

($ per ounce) | | Cash costs4

($ per ounce) |

Barrick Nevada | | 2.270-2.350 | | 790-830 | | 630-680 | | 440-480 |

Pueblo Viejo (60%) | | 0.625-0.650 | | 650-680 | | 540-570 | | 420-440 |

Veladero (50%) | | 0.430-0.480 | | 740-790 | | 890-990 | | 550-590 |

Lagunas Norte | | 0.380-0.420 | | 660-730 | | 490-550 | | 430-470 |

| |

Sub-total | | 3.700-3.900 | | 750-790 | | 650-700 | | 450-480 |

| |

Acacia (63.9%) | | 0.545-0.575 | | 860-910 | | 880-920 | | 580-620 |

KCGM (50%) | | 0.375-0.425 | | 680-770 | | 665-715 | | 585-635 |

Turquoise Ridge (75%) | | 0.230-0.250 | | 700-750 | | 750-830 | | 570-600 |

Porgera (47.5%) | | 0.240-0.260 | | 780-840 | | 900-970 | | 650-700 |

Hemlo | | 0.205-0.220 | | 880-940 | | 940-1,040 | | 720-770 |

Golden Sunlight | | 0.035-0.050 | | 1,200-1,500 | | 1,200-1,300 | | 1,100-1,200 |

| |

Total Gold | | 5.300-5.60011 | | 780-820 | | 720-770 | | 510-535 |

| |

COPPER PRODUCTION AND COSTS

| | | | | | | | |

| | | Production

(millions of pounds) | | Cost of sales3

($ per pound) | | All-in

sustaining costs7

($ per pound) | | C1 cash costs7

($ per pound) |

Zaldívar (50%) | | 120-135 | | 2.00-2.20 | | 1.90-2.10 | | ~1.50 |

Lumwana | | 250-275 | | 1.20-1.40 | | 2.10-2.30 | | 1.40-1.60 |

Jabal Sayid (50%) | | 35-45 | | 2.10-2.80 | | 2.10-2.60 | | 1.50-1.90 |

Total Copper | | 400-45011 | | 1.50-1.70 | | 2.10-2.40 | | 1.40-1.60 |

CAPITAL EXPENDITURES

| | | | |

| | | ($ millions) | |

Mine site sustaining | | | 1,050-1,200 | |

Project | | | 250-300 | |

| | |

Total Attributable | | | 1,300-1,500 | |

Capital Expenditures9 | | | | |

| | |

| | | | |

| BARRICK SECOND QUARTER 2017 | | 7 | | PRESS RELEASE |

APPENDIX 2 – 2017 Outlook Assumptions and Economic Sensitivity Analysis

| | | | | | | | | | |

| | | 2017 Guidance

Assumption | | Hypothetical

Change | | Impact on

Revenue

(millions) | | Impact on

Cost of sales3

(millions) | | Impact on

All-in sustaining

costs4,7 |

Gold revenue, net of royalties | | $1,050/oz | | +/- $100/oz | | +/- $271 | | +/- $8 | | +/- $3/oz |

Copper revenue, net of royalties12 | | $2.25/lb | | + $0.50/lb | | + $113 | | + $7 | | + $0.03/lb |

Copper revenue, net of royalties12 | | $2.25/lb | | - $0.50/lb | | - $100 | | - $6 | | - $0.03/lb |

|

Goldall-in sustaining costs4 | | | | | | | | | | |

WTI crude oil price13 | | $55/bbl | | +/- $10/bbl | | n/a | | +/- $9 | | +/- $3/oz |

Australian dollar exchange rate | | 0.75 : 1 | | +/- 10% | | n/a | | +/- $15 | | +/- $6/oz |

Canadian dollar exchange rate | | 1.32 : 1 | | +/- 10% | | n/a | | +/- $16 | | +/- $6/oz |

|

Copperall-in sustaining costs7 | | | | | | | | | | |

WTI crude oil price13 | | $55/bbl | | +/- $10/bbl | | n/a | | +/- $3 | | +/- $0.01/lb |

Chilean peso exchange rate | | 675 : 1 | | +/- 10% | | n/a | | +/- $3 | | +/- $0.01/lb |

|

ENDNOTE 1

“Adjusted net earnings” and “adjusted net earnings per share” arenon-GAAP financial performance measures. Adjusted net earnings excludes the following from net earnings: certain impairment charges (reversals) related to intangibles, goodwill, property, plant and equipment, and investments; gains (losses) and otherone-time costs relating to acquisitions or dispositions: foreign currency translation gains (losses); significant tax adjustments not related to current period earnings; unrealized gains (losses) onnon-hedge derivative instruments; and the tax effect andnon-controlling interest of these items. The Company uses this measure internally to evaluate our underlying operating performance for the reporting periods presented and to assist with the planning and forecasting of future operating results. Barrick believes that adjusted net earnings is a useful measure of our performance because these adjusting items do not reflect the underlying operating performance of our core mining business and are not necessarily indicative of future operating results. Adjusted net earnings and adjusted net earnings per share are intended to provide additional information only and do not have any standardized meaning under IFRS and may not be comparable to similar measures of performance presented by other companies. They should not be considered in isolation or as a substitute for measures of performance prepared in accordance with IFRS. Further details on thesenon-GAAP measures are provided in the MD&A accompanying Barrick’s financial statements filed from time to time on SEDAR at www.sedar.com and on EDGAR at www.sec.gov.

Reconciliation of Net Earnings to Net Earnings per Share, Adjusted Net Earnings and Adjusted Net Earnings per Share

| | | | | | | | | | | | | | | | |

| ($ millions, except per share amounts in dollars) | | For the three months ended June 30 | | | For the six months ended June 30 | |

| | | 2017 | | | 2016 | | | 2017 | | | 2016 | |

Net earnings (loss) attributable to equity holders of the Company | | | $ 1,084 | | | | $138 | | | | $ 1,763 | | | | $55 | |

Impairment charges (reversals) related to intangibles, goodwill, property, plant and equipment, and investments1 | | | (5) | | | | 4 | | | | (1,130) | | | | 5 | |

Acquisition/disposition (gains)/losses2 | | | (880) | | | | (11) | | | | (877) | | | | (2) | |

Foreign currency translation (gains)/losses | | | 32 | | | | 23 | | | | 35 | | | | 162 | |

Significant tax adjustments | | | 12 | | | | 3 | | | | 9 | | | | 54 | |

Other expense adjustments | | | 21 | | | | 6 | | | | 27 | | | | 74 | |

Unrealized gains onnon-hedge derivative instruments | | | - | | | | (5) | | | | 3 | | | | (11) | |

Tax effect andnon-controlling interest3 | | | (3) | | | | - | | | | 593 | | | | (52) | |

| | |

Adjusted net earnings | | | $ 261 | | | | $158 | | | | $ 423 | | | | $285 | |

| | |

Net earnings (loss) per share4 | | | 0.93 | | | | 0.12 | | | | 1.51 | | | | 0.05 | |

Adjusted net earnings per share4 | | | 0.22 | | | | 0.14 | | | | 0.36 | | | | 0.24 | |

| | |

| 1 | Net impairment reversals for six month period ended June 30, 2017 primarily relate to impairment reversals at the Cerro Casale project upon reclassification of the project’s net assets as held-for-sale as at March 31, 2017. |

| 2 | Disposition gains for the three and six month periods ended June 30, 2017 primarily relates to the sale of a 50% interest in the Veladero mine and the gain related to the sale of a 25% interest in the Cerro Casale project. |

| 3 | Tax effect and non-controlling interest for the six month period ended June 30, 2017 primarily relates to the impairment reversals at the Cerro Casale project discussed above. |

| 4 | Calculated using weighted average number of shares outstanding under the basic method of earnings per share. |

| | | | |

| BARRICK SECOND QUARTER 2017 | | 8 | | PRESS RELEASE |

ENDNOTE 2

“Free cash flow” is anon-GAAP financial performance measure which excludes capital expenditures from net cash provided by operating activities. Barrick believes this to be a useful indicator of our ability to operate without reliance on additional borrowing or usage of existing cash. Free cash flow is intended to provide additional information only and does not have any standardized meaning under IFRS and may not be comparable to similar measures of performance presented by other companies. Free cash flow should not be considered in isolation or as a substitute for measures of performance prepared in accordance with IFRS. Further details on thesenon-GAAP measures are provided in the MD&A accompanying Barrick’s financial statements filed from time to time on SEDAR at www.sedar.com and on EDGAR at www.sec.gov.

Reconciliation of Net Cash Provided by Operating Activities to Free Cash Flow

| | | | | | | | | | | | | | | | |

| ($ millions) | | For the three months ended June 30 | | | For the six months ended June 30 | |

| | | 2017 | | | 2016 | | | 2017 | | | 2016 | |

Net cash provided by operating activities | | | $ 448 | | | | $ 527 | | | | $ 943 | | | | $ 978 | |

Capital expenditures | | | (405) | | | | (253) | | | | (739) | | | | (523) | |

| | |

Free cash flow | | | $ 43 | | | | $ 274 | | | | $ 204 | | | | $ 455 | |

| | |

ENDNOTE 3

Cost of sales applicable to gold per ounce is calculated using cost of sales applicable to gold on an attributable basis (removing thenon-controlling interest of 40% Pueblo Viejo and 36.1% Acacia from cost of sales), divided by attributable gold ounces. Cost of sales applicable to copper per pound is calculated using cost of sales applicable to copper including our proportionate share of cost of sales attributable to equity method investments (Zaldívar and Jabal Sayid), divided by consolidated copper pounds (including our proportionate share of copper pounds from our equity method investments).

ENDNOTE 4

“Cash costs” per ounce and“All-in sustaining costs” per ounce arenon-GAAP financial performance measures. “Cash costs” per ounce starts with cost of sales applicable to gold production, but excludes the impact of depreciation, thenon-controlling interest of cost of sales, and includesby-product credits.“All-in sustaining costs” per ounce begin with “Cash costs” per ounce and add further costs which reflect the additional costs of operating a mine, primarily sustaining capital expenditures, general & administrative costs, minesite exploration and evaluation costs, and reclamation cost accretion and amortization. Barrick believes that the use of “cash costs” per ounce and“all-in sustaining costs” per ounce will assist investors, analysts and other stakeholders in understanding the costs associated with producing gold, understanding the economics of gold mining, assessing our operating performance and also our ability to generate free cash flow from current operations and to generate free cash flow on an overall Company basis. “Cash costs” per ounce and“All-in sustaining costs” per ounce are intended to provide additional information only and do not have any standardized meaning under IFRS. Although a standardized definition ofall-in sustaining costs was published in 2013 by the World Gold Council (a market development organization for the gold industry comprised of and funded by 18 gold mining companies from around the world, including Barrick), it is not a regulatory organization, and other companies may calculate this measure differently. These measures should not be considered in isolation or as a substitute for measures prepared in accordance with IFRS. Further details on thesenon-GAAP measures are provided in the MD&A accompanying Barrick’s financial statements filed from time to time on SEDAR at www.sedar.com and on EDGAR at www.sec.gov.

Reconciliation of Gold Cost of Sales to Cash costs,All-in sustaining costs andAll-in costs, including on a per ounce basis

| | | | | | | | | | | | | | | | | | | | |

| ($ millions, except per ounce information in dollars) | | | | | For the three months ended June 30 | | | For the six months ended June 30 | |

| | | Footnote | | | 2017 | | | 2016 | | | 2017 | | | 2016 | |

Cost of sales applicable to gold production | | | | | | | $ 1,159 | | | | $ 1,229 | | | | $ 2,397 | | | | $ 2,431 | |

Depreciation | | | | | | | (383) | | | | (367) | | | | (768) | | | | (735) | |

By-product credits | | | 1 | | | | (32) | | | | (46) | | | | (73) | | | | (84) | |

Realized (gains)/losses on hedge andnon-hedge derivatives | | | 2 | | | | 10 | | | | 26 | | | | 10 | | | | 57 | |

Non-recurring items | | | 3 | | | | - | | | | - | | | | - | | | | (10) | |

Other | | | 4 | | | | (27) | | | | (6) | | | | (47) | | | | (15) | |

| | | | |

| BARRICK SECOND QUARTER 2017 | | 9 | | PRESS RELEASE |

| | | | | | | | | | | | | | | | | | |

Non-controlling interests (Pueblo Viejo and Acacia) | | 5 | | | (64) | | | | (90) | | | | (145) | | | | (175) | |

Cash costs | | | �� | | $ 663 | | | | $ 746 | | | | $ 1,374 | | | | $ 1,469 | |

General & administrative costs | | | | | 45 | | | | 88 | | | | 117 | | | | 146 | |

Minesite exploration and evaluation costs | | 6 | | | 16 | | | | 8 | | | | 23 | | | | 16 | |

Minesite sustaining capital expenditures | | 7 | | | 320 | | | | 235 | | | | 582 | | | | 410 | |

Rehabilitation - accretion and amortization (operating sites) | | 8 | | | 20 | | | | 14 | | | | 37 | | | | 25 | |

Non-controlling interest, copper operations and other | | 9 | | | (71) | | | | (82) | | | | (132) | | | | (132) | |

All-in sustaining costs | | | | | $ 993 | | | | $ 1,009 | | | | $ 2,001 | | | | $ 1,934 | |

Project exploration and evaluation and project costs | | 6 | | | 65 | | | | 48 | | | | 133 | | | | 95 | |

Community relations costs not related to current operations | | | | | 1 | | | | 3 | | | | 2 | | | | 5 | |

Project capital expenditures | | 7 | | | 83 | | | | 49 | | | | 139 | | | | 89 | |

Rehabilitation - accretion and amortization(non-operating sites) | | 8 | | | 9 | | | | 3 | | | | 13 | | | | 5 | |

Non-controlling interest and copper operations | | 9 | | | (1) | | | | (15) | | | | (6) | | | | (31) | |

All-in costs | | | | | $ 1,150 | | | | $ 1,097 | | | | $ 2,282 | | | | $ 2,097 | |

Ounces sold - equity basis (000s ounces) | | 10 | | | 1,398 | | | | 1,292 | | | | 2,703 | | | | 2,598 | |

Cost of sales per ounce | | 11,12 | | | $ 726 | | | | $ 836 | | | | $ 778 | | | | $ 823 | |

Cash costs per ounce | | 12 | | | $ 474 | | | | $ 578 | | | | $ 508 | | | | $ 565 | |

Cash costs per ounce (on aco-product basis) | | 12,13 | | | $ 488 | | | | $ 605 | | | | $ 527 | | | | $ 591 | |

All-in sustaining costs per ounce | | 12 | | | $ 710 | | | | $ 782 | | | | $ 739 | | | | $ 744 | |

All-in sustaining costs per ounce (on aco-product basis) | | 12,13 | | | $ 724 | | | | $ 809 | | | | $ 758 | | | | $ 770 | |

All-in costs per ounce | | 12 | | | $ 823 | | | | $ 849 | | | | $ 844 | | | | $ 807 | |

All-in costs per ounce (on aco-product basis) | | 12,13 | | | $ 837 | | | | $ 876 | | | | $ 863 | | | | $ 833 | |

Revenues include the sale ofby-products for our gold and copper mines for the three and six months ended June 30, 2017 of $32 million and $73 million, respectively, (2016: $32 million and $60 million, respectively) and energy sales from the Monte Rio power plant at our Pueblo Viejo mine for the three and six months ended June 30, 2017 of $nil and $nil, respectively, (2016: $14 million and $24 million, respectively) up until its disposition on August 18, 2016.

| 2 | Realized (gains)/losses on hedge andnon-hedge derivatives |

Includes realized hedge losses of $8 million and $14 million, respectively, for the three and six month periods ended June 30, 2017 (2016: $20 million and $44 million, respectively), and realizednon-hedge losses of $2 million and gains of $4 million, respectively, for the three and six month periods ended June 30, 2017 (2016: losses of $6 million and $13 million, respectively). Refer to Note 5 of the Financial Statements for further information.

Non-recurring items in the first half of 2016 consist of $10 million in abnormal costs at Veladero relating to the administrative fine in connection with the cyanide incident that occurred in 2015. These costs are not indicative of our cost of production and have been excluded from the calculation of cash costs.

Other adjustments for the three and six month periods ended June 30, 2017 include adding the net margins related to power sales at Pueblo Viejo of $nil and $nil, respectively, (2016: $2 million and $4 million, respectively) adding the cost of treatment and refining charges of ($1 million) and $1 million, respectively, (2016: $4 million and $9 million, respectively) and the removal of cash costs andby-product credits associated with our Pierina mine, which is mining incidental ounces as it enters closure, of $27 million and $48 million, respectively (2016: $12 million and $28 million, respectively).

| 5 | Non-controlling interests (Pueblo Viejo and Acacia) |

Non-controlling interests includenon-controlling interests applicable to gold production of $98 million and $214 million, respectively, for the three and six month periods ended June 30, 2017 (2016: $131 million and $257 million, respectively). Refer to Note 5 of the Financial Statements for further information.

| 6 | Exploration and evaluation costs |

Exploration, evaluation and project expenses are presented as minesite sustaining if it supports current mine operations and project if it relates to future projects. Refer to page 28 of Barrick’s Second Quarter 2017 MD&A.

Capital expenditures are related to our gold sites only and are presented on a 100% accrued basis. They are split between minesite sustaining and project capital expenditures. Project capital expenditures are distinct projects designed to increase the net present value of the mine and are not related to current production. Significant projects in the current year are stripping at Cortez Crossroads, underground development at Cortez Hills Lower Zone and the range front declines, Lagunas Norte Refractory Ore Project and Goldrush. Refer to page 28 of Barrick’s Second Quarter 2017 MD&A.

| 8 | Rehabilitation - accretion and amortization |

Includes depreciation on the assets related to rehabilitation provisions of our gold operations and accretion on the rehabilitation provision of our gold operations, split between operating andnon-operating sites.

| | | | |

| BARRICK SECOND QUARTER 2017 | | 10 | | PRESS RELEASE |

| 9 | Non-controlling interest and copper operations |

Removes general & administrative costs related tonon-controlling interests and copper based on a percentage allocation of revenue. Also removes exploration, evaluation and project costs, rehabilitation costs and capital expenditures incurred by our copper sites and thenon-controlling interest of our Acacia and Pueblo Viejo operating segment and Arturo. Figures remove the impact of Pierina. The impact is summarized as the following:

| | | | | | | | | | | | | | | | |

| ($ millions) | | For the three months ended

June 30 | | | For the six months ended

June 30 | |

| Non-controlling interest, copper operations and other | | 2017 | | | 2016 | | | 2017 | | | 2016 | |

General & administrative costs | | | $ 1 | | | | ($ 12) | | | | ($ 8) | | | | ($ 22) | |

Minesite exploration and evaluation costs | | | (5) | | | | (2) | | | | (7) | | | | (4) | |

Rehabilitation - accretion and amortization (operating sites) | | | (4) | | | | (2) | | | | (6) | | | | (3) | |

Minesite sustaining capital expenditures | | | (63) | | | | (66) | | | | (111) | | | | (103) | |

All-in sustaining costs total | | | ($ 71) | | | | ($ 82) | | | | ($ 132) | | | | ($ 132) | |

Project exploration and evaluation and project costs | | | (1) | | | | (2) | | | | (6) | | | | (5) | |

Project capital expenditures | | | - | | | | (13) | | | | - | | | | (26) | |

All-in costs total | | | ($ 1) | | | | ($ 15) | | | | ($ 6) | | | | ($ 31) | |

| 10 | Ounces sold - equity basis |

Figures remove the impact of Pierina as the mine is currently going through closure.

| 11 | Cost of sales per ounce |

Figures remove the cost of sales impact of Pierina of $47 million and $81 million, respectively, for the three and six month periods ended June 30, 2017 (2016: $16 million and $35 million, respectively), as the mine is currently going through closure. Cost of sales per ounce excludesnon-controlling interest related to gold production. Cost of sales applicable to gold per ounce is calculated using cost of sales on an attributable basis (removing thenon-controlling interest of 40% Pueblo Viejo and 36.1% Acacia from cost of sales), divided by attributable gold ounces.

Cost of sales per ounce, cash costs per ounce,all-in sustaining costs per ounce andall-in costs per ounce may not calculate based on amounts presented in this table due to rounding.

| 13 | Co-product costs per ounce |

Cash costs per ounce,all-in sustaining costs per ounce andall-in costs per ounce presented on aco-product basis removes the impact ofby-product credits of our gold production (net ofnon-controlling interest) calculated as:

| | | | | | | | | | | | | | | | |

| ($ millions) | | For the three months ended

June 30 | | | For the six months ended

June 30 | |

| | | 2017 | | | 2016 | | | 2017 | | | 2016 | |

By-product credits | | | $ 32 | | | | $ 46 | | | | $ 73 | | | | $ 84 | |

Non-controlling interest | | | (9) | | | | (13) | | | | (17) | | | | (26) | |

| | |

By-product credits (net ofnon-controlling interest) | | | $ 23 | | | | $ 33 | | | | $ 56 | | | | $ 58 | |

| | |

ENDNOTE 5

Includes $552 million of cash primarily held at Acacia and Pueblo Viejo, which may not be readily deployed outside of Acacia and/or Pueblo Viejo.

ENDNOTE 6

Amount excludes capital leases and includes project financing payments at Pueblo Viejo (60% basis) and Acacia (100% basis).

ENDNOTE 7

“C1 cash costs” per pound and“All-in sustaining costs” per pound arenon-GAAP financial performance measures. “C1 cash costs” per pound is based on cost of sales but excludes the impact of depreciation and royalties and includes treatment and refinement charges.“All-in sustaining costs” per pound begins with “C1 cash costs” per pound and adds further costs which reflect the additional costs of operating a mine, primarily sustaining capital expenditures, general & administrative costs and royalties. Barrick believes that the use of “C1 cash costs” per pound and“all-in sustaining costs” per pound will assist investors, analysts, and other stakeholders in understanding the costs associated with producing copper, understanding the economics of copper mining, assessing our operating performance, and also our ability to generate free cash flow from current operations and to generate free cash flow on an overall Company basis. “C1 cash costs” per pound and“All-in sustaining costs” per pound are intended to provide additional information only, do not have any standardized meaning under IFRS, and may not

| | | | |

| BARRICK SECOND QUARTER 2017 | | 11 | | PRESS RELEASE |

be comparable to similar measures of performance presented by other companies. These measures should not be considered in isolation or as a substitute for measures of performance prepared in accordance with IFRS. Further details on thesenon-GAAP measures are provided in the MD&A accompanying Barrick’s financial statements filed from time to time on SEDAR at www.sedar.com and on EDGAR at www.sec.gov.

Reconciliation of Copper Cost of Sales to C1 cash costs andAll-in sustaining costs, including on a per pound basis

| | | | | | | | | | | | | | | | |

| ($ millions, except per pound information in dollars) | | For the three months ended June 30 | | | For the six months ended June 30 | |

| | | 2017 | | | 2016 | | | 2017 | | | 2016 | |

Cost of sales | | | $ 102 | | | | $ 80 | | | | $ 184 | | | | $ 169 | |

Depreciation/amortization1 | | | (19) | | | | (9) | | | | (33) | | | | (20) | |

Treatment and refinement charges | | | 35 | | | | 38 | | | | 67 | | | | 84 | |

Cash cost of sales applicable to equity method investments2 | | | 62 | | | | 43 | | | | 123 | | | | 84 | |

Less: royalties | | | (8) | | | | (11) | | | | (15) | | | | (25) | |

By-product credits | | | (3) | | | | - | | | | (3) | | | | - | |

| | |

C1 cash cost of sales | | | $ 169 | | | | $ 141 | | | | $ 323 | | | | $ 292 | |

| | |

General & administrative costs | | | 3 | | | | 5 | | | | 6 | | | | 12 | |

Rehabilitation - accretion and amortization | | | 3 | | | | 2 | | | | 5 | | | | 3 | |

Royalties | | | 8 | | | | 10 | | | | 15 | | | | 25 | |

Minesite exploration and evaluation costs | | | 1 | | | | - | | | | 1 | | | | - | |

Minesite sustaining capital expenditures | | | 50 | | | | 41 | | | | 87 | | | | 70 | |

| | |

All-in sustaining costs | | | $ 234 | | | | $ 199 | | | | $ 437 | | | | $ 402 | |

| | |

Pounds sold - consolidated basis (millions pounds) | | | 98 | | | | 93 | | | | 191 | | | | 196 | |

| | |

Cost of sales per pound3,4 | | | $ 1.85 | | | | $ 1.43 | | | | $ 1.79 | | | | $ 1.39 | |

| | |

C1 cash cost per pound3 | | | $ 1.72 | | | | $ 1.52 | | | | $ 1.69 | | | | $ 1.49 | |

| | |

All-in sustaining costs per pound3 | | | $ 2.38 | | | | $ 2.14 | | | | $ 2.29 | | | | $ 2.05 | |

| | |

| 1 | For the three and six months ended June 30, 2017, depreciation excludes $17 million and $35 million, respectively, (2016: $11 million and $19 million, respectively) of depreciation applicable to equity method investments. |

| 2 | For the three and six months ended June 30, 2017, figures include $41 million and $87 million, respectively, (2016: $43 million and $84 million, respectively) of cash costs related to our 50% share of Zaldívar and $21 million and $36 million, respectively, (2016: $nil and $nil, respectively) of cash costs related to our 50% share of Jabal Sayid due to their accounting as equity method investments. |

| 3 | Cost of sales per pound, C1 cash costs per pound and all-in sustaining costs per pound may not calculate based on amounts presented in this table due to rounding. |

| 4 | Cost of sales applicable to copper per pound is calculated using cost of sales including our proportionate share of cost of sales attributable to equity method investments (Zaldívar and Jabal Sayid), divided by consolidated copper pounds (including our proportionate share of copper pounds from our equity method investments). |

ENDNOTE 8

Barrick’s share.

ENDNOTE 9

Includes our 60% share of Pueblo Viejo and Arturo, our 63.9% share of Acacia, and our 50% share of Zaldívar and Jabal Sayid and our share of joint operations. 2017 guidance includes our 50% sale of Veladero which closed on June 30, 2017.

ENDNOTE 10

Estimated in accordance with National Instrument43-101 as required by Canadian securities regulatory authorities. Estimates are as of December 31, 2016, unless otherwise noted. For United States reporting purposes, Industry Guide 7 under the Securities and Exchange Act of 1934 (as interpreted by Staff of the SEC), applies different standards in order to classify mineralization as a reserve. All mineral resources referenced in this press release are exclusive of mineral reserves and mineral resources which are not mineral reserves do not have demonstrated economic viability. Complete mineral reserve and mineral resource data for all mines and projects referenced in this press release, including tonnes, grades, and ounces, can be found on pages25-35 of Barrick’s most recent Form40-F/Annual Information Form.

| | | | |

| BARRICK SECOND QUARTER 2017 | | 12 | | PRESS RELEASE |

ENDNOTE 11

Operating unit guidance ranges for production reflect expectations at each individual operating unit, but do not necessarily add up to the corporate-wide guidance range total.

ENDNOTE 12

As at June 30, 2017, utilizing option collar strategies, the Company has protected the downside on approximately 36 million pounds of expected remaining 2017 copper production at an average floor price of $2.39 per pound and can participate in the upside on the same amount up to an average of $3.01 per pound. Subsequent toquarter-end, we have put in place an additional 25 million pounds of option collar strategies, so that we are now protecting the downside on approximately 61 million pounds of expected remaining 2017 copper production at an average floor price of $2.39 per pound and can participate in the upside on the same amount to an average of $2.97 per pound. Our remaining copper production is subject to market prices.

ENDNOTE 13

Due to our hedging activities, which are reflected in these sensitivities, we are partially protected against changes in these factors.

| | | | |

| BARRICK SECOND QUARTER 2017 | | 13 | | PRESS RELEASE |

Key Statistics

| | | | | | | | | | | | | | | | |

Barrick Gold Corporation | | | | | | | | | | | | | | | | |

| (in United States dollars) | | Three months ended June 30 | | | Six months ended June 30 | |

| | | 2017 | | | 2016 | | | 2017 | | | 2016 | |

Financial Results (millions) | | | | | | | | | | | | | | | | |

Revenues | | | $ 2,160 | | | | $ 2,012 | | | | $ 4,153 | | | | $ 3,942 | |

Cost of sales | | | 1,277 | | | | 1,336 | | | | 2,619 | | | | 2,660 | |

Net earnings1 | | | 1,084 | | | | 138 | | | | 1,763 | | | | 55 | |

Adjusted net earnings2 | | | 261 | | | | 158 | | | | 423 | | | | 285 | |

Adjusted EBITDA2 | | | 1,114 | | | | 895 | | | | 2,033 | | | | 1,765 | |

Total capital expenditures - sustaining3 | | | 320 | | | | 234 | | | | 582 | | | | 409 | |

Total project capital expenditures3 | | | 83 | | | | 50 | | | | 139 | | | | 90 | |

Net cash provided by operating activities | | | 448 | | | | 527 | | | | 943 | | | | 978 | |

Free cash flow2 | | | 43 | | | | 274 | | | | 204 | | | | 455 | |

| | | | |

Per share data (dollars) | | | | | | | | | | | | | | | | |

Net earnings (basic and diluted) | | | 0.93 | | | | 0.12 | | | | 1.51 | | | | 0.05 | |

Adjusted net earnings (basic)2 | | | 0.22 | | | | 0.14 | | | | 0.36 | | | | 0.24 | |

Weighted average diluted common shares (millions) | | | 1,166 | | | | 1,165 | | | | 1,166 | | | | 1,165 | |

| | |

| | | | |

Operating Results | | | | | | | | | | | | | | | | |

Gold production (thousands of ounces)4 | | | 1,432 | | | | 1,340 | | | | 2,741 | | | | 2,620 | |

Gold sold (thousands of ounces)4 | | | 1,398 | | | | 1,292 | | | | 2,703 | | | | 2,598 | |

| | | | |

Per ounce data | | | | | | | | | | | | | | | | |

Average spot gold price | | | $ 1,257 | | | | $ 1,260 | | | | $ 1,238 | | | | $ 1,221 | |

Average realized gold price2 | | | 1,258 | | | | 1,259 | | | | 1,239 | | | | 1,219 | |

Cost of sales (Barrick’s share)5 | | | 726 | | | | 836 | | | | 778 | | | | 823 | |

All-in sustaining costs2 | | | 710 | | | | 782 | | | | 739 | | | | 744 | |

| | | | |

Copper production (millions of pounds)6 | | | 104 | | | | 103 | | | | 199 | | | | 214 | |

Copper sold (millions of pounds)6 | | | 98 | | | | 93 | | | | 191 | | | | 196 | |

| | | | |

Per pound data | | | | | | | | | | | | | | | | |

Average spot copper price | | | $ 2.57 | | | | $ 2.14 | | | | $ 2.61 | | | | $2.13 | |

Average realized copper price2 | | | 2.60 | | | | 2.14 | | | | 2.68 | | | | 2.16 | |

Cost of sales (Barrick’s share)7 | | | 1.85 | | | | 1.43 | | | | 1.79 | | | | 1.39 | |

C1 cash costs2 | | | 1.72 | | | | 1.52 | | | | 1.69 | | | | 1.49 | |

All-in sustaining costs2 | | | 2.38 | | | | 2.14 | | | | 2.29 | | | | 2.05 | |

| | |

| | | | |

| | | | | | | | | As at June 30, | | | As at December 31, | |

| | | | | | | | | 2017 | | | 2016 | |

Financial Position(millions) | | | | | | | | | | | | | | | | |

Cash and equivalents | | | | | | | | | | | $2,926 | | | | $ 2,389 | |

Working capital (excluding cash) | | | | | | | | | | | 1,490 | | | | 1,155 | |

| | |

| | 1 | Net earnings represents net earnings attributable to the equity holders of the Company. |

| | 2 | Adjusted net earnings, adjusted EBITDA, free cash flow, adjusted net earnings per share, realized gold price, all-in sustaining costs and realized copper price are non-GAAP financial performance measures with no standardized meaning under IFRS and therefore may not be comparable to similar measures presented by other issuers. For further information and a detailed reconciliation of each non-GAAP measure to the most directly comparable IFRS measure, please see pages 47 to 60 of this MD&A. |

| | 3 | Amounts presented on a 100% accrued basis. Project capital expenditures are included in our calculation of all-in costs, but not included in our calculation of all-in sustaining costs. |

| | 4 | Includes Acacia on a 63.9% basis, Pueblo Viejo on a 60% basis, and South Arturo on a 60% basis, which reflects our equity share of production and sales. 2016 includes production and sales from Bald Mountain and Round Mountain up to January 11, 2016, the effective date of sale of the assets. |

| | 5 | Cost of sales per ounce (Barrick’s share) is calculated as cost of sales - gold on an attributable basis excluding Pierina divided by gold ounces sold. |

| | 6 | Amounts reflect production and sales from Jabal Sayid and Zaldívar on a 50% basis, which reflects our equity share of production, and Lumwana. |

| | 7 | Cost of sales per pound (Barrick’s share) is calculated as cost of sales - copper plus our equity share of cost of sales attributable to Zaldívar and Jabal Sayid divided by copper pounds sold. |

| | | | |

| BARRICK SECOND QUARTER 2017 | | 14 | | SUMMARY INFORMATION |

Production and Cost Summary

| | | | | | | | | | | | | | | | |

| | | Production | |

| | | Three months ended June 30, | | | Six months ended June 30, | |

| | | 2017 | | | 2016 | | | 2017 | | | 2016 | |

Gold (equity ounces (000s)) | | | | | | | | | | | | | | | | |

Barrick Nevada1 | | | 741 | | | | 511 | | | | 1,262 | | | | 1,007 | |

Pueblo Viejo2 | | | 171 | | | | 150 | | | | 314 | | | | 322 | |

Lagunas Norte | | | 90 | | | | 124 | | | | 178 | | | | 224 | |

Veladero | | | 72 | | | | 119 | | | | 223 | | | | 251 | |

Turquoise Ridge | | | 24 | | | | 79 | | | | 79 | | | | 129 | |

Acacia3 | | | 134 | | | | 141 | | | | 274 | | | | 263 | |

Other Mines - Gold4 | | | 200 | | | | 216 | | | | 411 | | | | 424 | |

| | |

Total | | | 1,432 | | | | 1,340 | | | | 2,741 | | | | 2,620 | |

| | |

| |

| | |

Copper (equity pounds (millions))5 | | | 104 | | | | 103 | | | | 199 | | | | 214 | |

| | |

| |

| | | Cost of Sales per unit (Barrick’s share) | |

| | | Three months ended June 30, | | | Six months ended June 30, | |

| | | 2017 | | | 2016 | | | 2017 | | | 2016 | |

Gold Cost of Sales per ounce ($/oz)6 | | | | | | | | | | | | | | | | |

Barrick Nevada | | $ | 723 | | | $ | 904 | | | $ | 804 | | | $ | 923 | |

Pueblo Viejo | | | 586 | | | | 739 | | | | 635 | | | | 667 | |

Lagunas Norte | | | 615 | | | | 663 | | | | 595 | | | | 664 | |

Veladero | | | 628 | | | | 838 | | | | 770 | | | | 840 | |

Turquoise Ridge | | | 853 | | | | 582 | | | | 728 | | | | 641 | |

Acacia | | | 756 | | | | 836 | | | | 792 | | | | 872 | |

| | |

Total | | $ | 726 | | | $ | 836 | | | $ | 778 | | | $ | 823 | |

| | |

| |

| | |

Copper Cost of Sales per pound ($/lb)7 | | $ | 1.85 | | | $ | 1.43 | | | $ | 1.79 | | | $ | 1.39 | |

| | |

| |

| | | All-in sustaining costs8 | |

| | | Three months ended June 30, | | | Six months ended June 30, | |

| | | 2017 | | | 2016 | | | 2017 | | | 2016 | |

GoldAll-in Sustaining Costs ($/oz) | | | | | | | | | | | | | | | | |

Barrick Nevada | | $ | 541 | | | $ | 649 | | | $ | 605 | | | $ | 615 | |

Pueblo Viejo | | | 475 | | | | 634 | | | | 505 | | | | 559 | |

Lagunas Norte | | | 472 | | | | 585 | | | | 451 | | | | 571 | |

Veladero | | | 1,315 | | | | 744 | | | | 1,038 | | | | 709 | |

Turquoise Ridge | | | 965 | | | | 621 | | | | 784 | | | | 668 | |

Acacia | | | 835 | | | | 926 | | | | 893 | | | | 941 | |

| | |

Total | | $ | 710 | | | $ | 782 | | | $ | 739 | | | $ | 744 | |

| | |

| |

| | |

CopperAll-in Sustaining Costs ($/lb) | | $ | 2.38 | | | $ | 2.14 | | | $ | 2.29 | | | $ | 2.05 | |

| | |

| | 1 | Reflects production from South Arturo on a 60% basis, which reflects our equity share of production, Goldstrike and Cortez. |

| | 2 | Reflects production from Pueblo Viejo on a 60% basis, which reflects our equity share of production. |

| | 3 | Reflects production from Acacia on a 63.9% basis, which reflects our equity share of production. |

| | 4 | In 2017, Other Mines - Gold includes Golden Sunlight, Hemlo, Porgera on a 47.5% basis and Kalgoorlie on a 50% basis. In 2016, Other Mines - Gold includes Golden Sunlight, Hemlo, Porgera on a 47.5% basis, Kalgoorlie on a 50% basis and production from Bald Mountain and Round Mountain up to January 11, 2016, the effective date of sale of the assets. |

| | 5 | Reflects production from Jabal Sayid and Zaldívar on a 50% basis, which reflects our equity share of production, and Lumwana. |

| | 6 | Cost of sales per ounce (Barrick’s share) is calculated as cost of sales - gold on an attributable basis excluding Pierina divided by gold ounces sold. |

| | 7 | Cost of sales per pound (Barrick’s share) is calculated as cost of sales - copper plus our equity share of cost of sales attributable to Zaldívar and Jabal Sayid divided by copper pounds sold. |

| | 8 | All-in sustaining costs is a non-GAAP financial performance measure with no standardized meaning under IFRS and therefore may not be comparable to similar measures presented by other issuers. For further information and a detailed reconciliation of this non-GAAP measure to the most directly comparable IFRS measure, please see pages 47 to 60 of this MD&A. |

| | | | |

| BARRICK SECOND QUARTER 2017 | | 15 | | SUMMARY INFORMATION |

MANAGEMENT’S DISCUSSION AND ANALYSIS (“MD&A”)

This portion of the Quarterly Report provides management’s discussion and analysis (“MD&A”) of the financial condition and results of operations, to enable a reader to assess material changes in financial condition and results of operations as at, and for the three and six month periods ended June 30, 2017, in comparison to the corresponding prior–year periods. The MD&A is intended to help the reader understand Barrick Gold Corporation (“Barrick”, “we”, “our” or the “Company”), our operations, financial performance and present and future business environment. This MD&A, which has been prepared as of July 26, 2017, is intended to supplement and complement the condensed unaudited interim consolidated financial statements and notes thereto, prepared in accordance with International Accounting Standard 34 Interim Financial Reporting (“IAS 34”) as issued by the International Accounting Standards Board (“IASB”), for the three and six month periods ended June 30, 2017 (collectively, the “Financial Statements”), which are included in this Quarterly Report on pages 62 to 81. You are encouraged to review the Financial Statements in conjunction with your review of this MD&A. This MD&A should be read in conjunction with both the annual audited consolidated financial statements for the two years ended December

31, 2016, the related annual MD&A included in the 2016 Annual Report, and the most recent Form 40–F/Annual Information Form on file with the U.S. Securities and Exchange Commission (“SEC”) and Canadian provincial securities regulatory authorities. These documents and additional information relating to the Company are available on SEDAR at www.sedar.com and EDGAR at www.sec.gov. Certain notes to the Financial Statements are specifically referred to in this MD&A and such notes are incorporated by reference herein. All dollar amounts in this MD&A are in millions of United States dollars (“$” or “US$”), unless otherwise specified.

For the purposes of preparing our MD&A, we consider the materiality of information. Information is considered material if: (i) such information results in, or would reasonably be expected to result in, a significant change in the market price or value of our shares; or (ii) there is a substantial likelihood that a reasonable investor would consider it important in making an investment decision; or (iii) it would significantly alter the total mix of information available to investors. We evaluate materiality with reference to all relevant circumstances, including potential market sensitivity.

CAUTIONARY STATEMENT ON FORWARD-LOOKING INFORMATION

Certain information contained or incorporated by reference in this MD&A, including any information as to our strategy, projects, plans or future financial or operating performance, constitutes “forward-looking statements”. All statements, other than statements of historical fact, are forward-looking statements. The words “believe”, “expect”, “anticipate”, “target”, “plan”, “objective”, “assume”, “intend”, “project”, “goal”, “continue”, “budget”, “estimate”, “potential”, “may”, “will”, “can”, “could”, “would” and similar expressions identify forward-looking statements. In particular, this MD&A contains forward-looking statements including, without limitation, with respect to: (i) Barrick’s forward-looking production guidance; (ii) estimates of future cost of sales per ounce for gold and per pound for copper,all-in-sustaining costs per ounce/pound, cash costs per ounce and C1 cash costs per pound; (iii) cash flow forecasts; (iv) projected capital, operating and exploration expenditures; (v) targeted debt and cost reductions; (vi) mine life and production rates; (vii) potential mineralization and metal or mineral recoveries; (viii) savings from our improved capital management program; (ix) Barrick’sBest-in-Class

program (including potential improvements to financial and operating performance that may result from certainBest-in-Class initiatives); (x) the prefeasibility study at Pascua-Lama; (xi) our pipeline of high confidence projects at or near existing operations; (xii) the benefits of unifying the Cortez and Goldstrike operations; (xiii) asset sales, joint ventures and partnerships; and (xiv) expectations regarding future price assumptions, financial performance and other outlook or guidance.

Forward-looking statements are necessarily based upon a number of estimates and assumptions including material estimates and assumptions related to the factors set forth below that, while considered reasonable by the Company as at the date of this MD&A in light of management’s experience and perception of current conditions and expected developments, are inherently subject to significant business, economic and competitive uncertainties and contingencies. Known and unknown factors could cause actual results to differ materially from those projected in the forward-looking statements and undue reliance should not be placed on such statements and information. Such factors include,

| | | | |

| BARRICK SECOND QUARTER 2017 | | 16 | | MANAGEMENT’S DISCUSSION AND ANALYSIS |

but are not limited to: fluctuations in the spot and forward price of gold, copper or certain other commodities (such as silver, diesel fuel, natural gas and electricity); the speculative nature of mineral exploration and development; changes in mineral production performance, exploitation and exploration successes; risks associated with the fact that certainBest-in-Class initiatives are still in the early stages of evaluation and additional engineering and other analysis is required to fully assess their impact; the benefits expected from recent transactions being realized; diminishing quantities or grades of reserves; increased costs, delays, suspensions and technical challenges associated with the construction of capital projects; operating or technical difficulties in connection with mining or development activities, including geotechnical challenges and disruptions in the maintenance or provision of required infrastructure and information technology systems; failure to comply with environmental and health and safety laws and regulations; timing of receipt of, or failure to comply with, necessary permits and approvals; uncertainty whether some or all of theBest-in-Class initiatives and targeted investments will meet the Company’s capital allocation objectives; the impact of global liquidity and credit availability on the timing of cash flows and the values of assets and liabilities based on projected future cash flows; adverse changes in our credit ratings; the impact of inflation; fluctuations in the currency markets; changes in U.S. dollar interest rates; risks arising from holding derivative instruments; changes in national and local government legislation, taxation, controls or regulations and/or changes in the administration of laws, policies and practices, expropriation or nationalization of property and political or economic developments in Canada, the United States and other jurisdictions in which the Company or its affiliates do or may carry on business in the future; the duration of the Tanzanian ban on mineral concentrate exports; the outcome of discussions between Barrick (on behalf of its 63.9%-owned subsidiary, Acacia Mining plc (“Acacia”)) and the Government of Tanzania to resolve a dispute relating to the imposition of the concentrate export ban and allegations by the Government of Tanzania that Acacia under-declared the metal content of concentrate exports from Tanzania; the manner in which amendments to the 2010 Mining Act (Tanzania) increasing the royalty rate applicable to metallic minerals such as gold, copper and silver to 6% (from 4%), and the new Finance Act (Tanzania) imposing a 1% clearing fee on the value of all minerals exported from Tanzania from July 1, 2017 will be implemented and the impact of these and other legislative changes on Acacia;

lack of certainty with respect to foreign legal systems, corruption and other factors that are inconsistent with the rule of law; damage to the Company’s reputation due to the actual or perceived occurrence of any number of events, including negative publicity with respect to the Company’s handling of environmental matters or dealings with community groups, whether true or not; risk of loss due to acts of war, terrorism, sabotage and civil disturbances; litigation; contests over title to properties, particularly title to undeveloped properties, or over access to water, power and other required infrastructure; business opportunities that may be presented to, or pursued by, the Company; our ability to successfully integrate acquisitions or complete divestitures; risks associated with working with partners in jointly controlled assets; employee relations including loss of key employees; increased costs and physical risks, including extreme weather events and resource shortages, related to climate change; availability and increased costs associated with mining inputs and labor; and the organization of our previously held African gold operations and properties under a separate listed Company. In addition, there are risks and hazards associated with the business of mineral exploration, development and mining, including environmental hazards, industrial accidents, unusual or unexpected formations, pressures,cave-ins, flooding and gold bullion, copper cathode or gold or copper concentrate losses (and the risk of inadequate insurance, or inability to obtain insurance, to cover these risks).

Many of these uncertainties and contingencies can affect our actual results and could cause actual results to differ materially from those expressed or implied in any forward-looking statements made by, or on behalf of, us. Readers are cautioned that forward-looking statements are not guarantees of future performance. All of the forward-looking statements made in this MD&A are qualified by these cautionary statements. Specific reference is made to the most recent Form40-F/Annual Information Form on file with the SEC and Canadian provincial securities regulatory authorities for a more detailed discussion of some of the factors underlying forward-looking statements and the risks that may affect Barrick’s ability to achieve the expectations set forth in the forward-looking statements contained in this MD&A. We disclaim any intention or obligation to update or revise any forward-looking statements whether as a result of new information, future events or otherwise, except as required by applicable law.

| | | | |

| BARRICK SECOND QUARTER 2017 | | 17 | | MANAGEMENT’S DISCUSSION AND ANALYSIS |

USE OFNON-GAAP FINANCIAL PERFORMANCE MEASURES

We use the followingnon-GAAP financial performance measures in our MD&A:

| | ● | | “adjusted net earnings” |

| | ● | | “C1 cash costs per pound” |

| | ● | | “all-in sustaining costs per ounce/pound” |

| | ● | | “all-in costs per ounce” and |

For a detailed description of each of thenon-GAAP measures used in this MD&A and a detailed reconciliation to the most directly comparable measure under International Financial Reporting Standards (“IFRS”), please refer to theNon-GAAP Financial Performance Measures section of this MD&A on pages 47 to 60. Eachnon-GAAP financial performance measure has been annotated with a reference to an endnote on page 61. Thenon-GAAP financial performance measures set out in this MD&A are intended to provide additional information to investors and do not have any standardized meaning under IFRS, and therefore may not be comparable to other issuers, and should not be considered in isolation or as a substitute for measures of performance prepared in accordance with IFRS.

Changes in presentation ofnon-GAAP financial performance measures

Adjusted EBITDA

Starting with this second quarter 2017 MD&A, we have begun including additional adjusting items in the Adjusted EBITDA reconciliation to provide a greater level of consistency with the adjusting items included in our Adjusted Net Earnings reconciliation. These new items include: acquisition/disposition gains/losses; foreign currency translation gains/losses; other expense adjustments; and unrealized gains onnon-hedge derivative instruments. These amounts are adjusted to remove any impact on finance costs/income, income tax expense and/or depreciation as they do not affect EBITDA. The prior periods have been restated to reflect the change in presentation. We believe this additional information will assist analysts, investors and other stakeholders of Barrick in better understanding our ability to generate liquidity from operating cash flow, by excluding these amounts from the calculation as they are not indicative of the performance of our core mining

business and not necessarily reflective of the underlying operating results for the periods presented.

| | | | |

| | | |

| INDEX | | page | | |

| | | |

Overview | | | | |

| | | |

Financial and Operating Results | | 19 | | |

Key Business Developments | | 24 | | |

Full Year 2017 Outlook | | 25 | | |

| | | |

Review of Financial Results | | | | |

| | | |

Revenue | | 26 | | |

Production Costs | | 27 | | |

Capital Expenditures | | 28 | | |

General and Administrative Expenses | | 28 | | |

Exploration, Evaluation and Project Costs | | 28 | | |

Finance Costs, Net | | 29 | | |

Additional Significant Statement of Income Items | | 29 | | |

Income Tax Expense | | 29 | | |

| | | |

Financial Condition Review | | | | |

| | | |

Balance Sheet Review | | 30 | | |

Shareholders’ Equity | | 30 | | |

Financial Position and Liquidity | | 30 | | |

Summary of Cash Inflow (Outflow) | | 31 | | |

| | | |

Operating Segments Performance | | 32 | | |

| | | |

Barrick Nevada | | 33 | | |

Pueblo Viejo | | 35 | | |

Lagunas Norte | | 36 | | |

Veladero | | 37 | | |

Turquoise Ridge | | 40 | | |

Acacia Mining plc | | 41 | | |

Pascua-Lama | | 44 | | |

| | | |

Commitments and Contingencies | | 45 | | |

| | | |

Review of Quarterly Results | | 46 | | |

| | | |

| Internal Control over Financial Reporting and Disclosure Controls and Procedures | | 46 | | |

| | | |

| IFRS Critical Accounting Policies and Accounting Estimates | | 47 | | |

| | | |

Non-GAAP Financial Performance Measures | | 47 | | |

| | | |

Technical Information | | 61 | | |

| | | |

Endnotes | | 61 | | |

| | | | |

| BARRICK SECOND QUARTER 2017 | | 18 | | MANAGEMENT’S DISCUSSION AND ANALYSIS |

OVERVIEW

FINANCIAL AND OPERATING HIGHLIGHTS

| | | | | | | | | | | | | | | | |

| ($ millions, except per share amounts in dollars) | | For the three months ended June 30 | | | For the six months ended June 30 | |

| | | 2017 | | | 2016 | | | 2017 | | | 2016 | |

Net earnings (loss) attributable to equity holders of the Company | | | $ 1,084 | | | | $ 138 | | | | $ 1,763 | | | | $ 55 | |

Per share (dollars)1 | | | 0.93 | | | | 0.12 | | | | 1.51 | | | | 0.05 | |

Adjusted net earnings2 | | | 261 | | | | 158 | | | | 423 | | | | 285 | |

Per share (dollars)1,2 | | | 0.22 | | | | 0.14 | | | | 0.36 | | | | 0.24 | |

Operating cash flow | | | 448 | | | | 527 | | | | 943 | | | | 978 | |

Free cash flow2 | | | $ 43 | | | | $ 274 | | | | $ 204 | | | | $ 455 | |

| | |

| 1 | Calculated using weighted average number of shares outstanding under the basic method of earnings per share of 1,166 million shares for the three and six months ended June 30, 2017 (2016: 1,165 million shares). |

| 2 | Adjusted net earnings and free cash flow are non-GAAP financial performance measures with no standardized meaning under IFRS and therefore may not be comparable to similar measures of performance presented by other issuers. For further information and a detailed reconciliation of the non-GAAP measures used in this section of the MD&A to the most directly comparable IFRS measure, please see pages 47 to 60 of this MD&A. |

| | | | |

| BARRICK SECOND QUARTER 2017 | | 19 | | MANAGEMENT’S DISCUSSION AND ANALYSIS |

Net Earnings, Adjusted Net Earnings, Operating Cash Flow and Free Cash Flow

Net earnings attributable to equity holders of Barrick (“net earnings”) for the second quarter of 2017 were $1,084 million compared with $138 million in the same prior year period. This significant improvement was largely due to a $689 million ($686 million net of tax) gain on the sale of a 50% interest in the Veladero mine and a $193 million ($192 million net of tax) gain on the sale of a 25% interest in the Cerro Casale project in the second quarter of 2017. After adjusting for items that are not indicative of future operating earnings, including these gains, adjusted net earnings1 were $261 million in the second quarter of 2017, 65% higher than the same prior year period. The increase in adjusted net earnings was primarily due to a decrease in direct mining costs driven by a change in sales mix with higher sales volume from the lower cost Barrick Nevada and lower relative sales volume from Acacia and Turquoise Ridge combined with the impact of higher gold and copper sales volume and copper prices. Further impacting lower direct mining costs were lower costs at Barrick Nevada and Pueblo Viejo compared to the same prior year period. These increases in net earnings were partially offset by an increase in tax expense, higher depreciation and an increase in exploration and evaluation costs.

Significant adjusting items(pre-tax andnon-controlling interest effects) in the second quarter of 2017 include:

| ● | | $689 million in a gain relating to the sale of a 50% interest in the Veladero mine; |

| ● | | $193 million in a gain related to the sale of a 25% interest in the Cerro Casale project; partially offset by |

| ● | | $32 million in foreign currency translation losses primarily related to the devaluation of the Argentine Peso on VAT receivables; and |

| ● | | $26 million in losses on debt extinguishment. |

Refer to page 48 for a full list of reconciling items between net earnings and adjusted net earnings for the current and prior year periods.

| | | | |

| BARRICK SECOND QUARTER 2017 | | 20 | | MANAGEMENT’S DISCUSSION AND ANALYSIS |

Net earnings for the first half of 2017 were $1,763 million compared with $55 million in the same prior year period. The significant increase was primarily due to a $1,120 million impairment reversal ($518 million net of tax andnon-controlling interest) recorded in the first quarter of 2017 as a result of the indicative fair value of the Cerro Casale project resulting from our divestment of 25%. This was combined with a $689 million ($686 million net of tax andnon-controlling interest) gain on the sale of a 50% interest in the Veladero mine and a $193 million ($192 million net of tax andnon-controlling interest) gain on the sale of a 25% interest in the Cerro Casale project during the second quarter of 2017. After adjusting for items that are not indicative of future operating earnings, adjusted net earnings1 of $423 million in the second quarter of 2017 were 48% higher than the same prior year period. The increase in adjusted net earnings was primarily due to a decrease in direct mining costs, as discussed above, combined with the impact of higher gold and copper sales volume and prices. These were partially offset by an increase in tax expense, higher depreciation and an increase in exploration and evaluation costs.

Significant adjusting items(pre-tax andnon-controlling interest effects) in the first half of 2017 include:

| ● | | $1,130 million in net impairment reversals primarily as a result of the indicative fair value of the Cerro Casale project resulting from our divestment of 25%; |

| ● | | $689 million in a gain relating to the sale of a 50% interest in the Veladero mine; |

| ● | | $193 million in a gain related to the sale of a 25% interest in the Cerro Casale project; partially offset by |

| ● | | $593 million in tax effects andnon-controlling interest impact mainly in relation to the Cerro Casale impairment reversal discussed above; |

| ● | | $35 million in foreign currency translation losses primarily related to the devaluation of the Argentine Peso on VAT receivables; and |

| ● | | $26 million in losses on debt extinguishment. |

Refer to page 48 for a full list of reconciling items between net earnings and adjusted net earnings for the current and prior year periods.

| | | | |

| BARRICK SECOND QUARTER 2017 | | 21 | | MANAGEMENT’S DISCUSSION AND ANALYSIS |