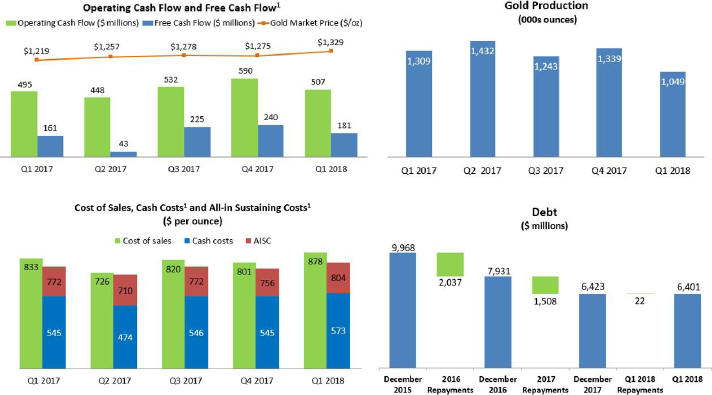

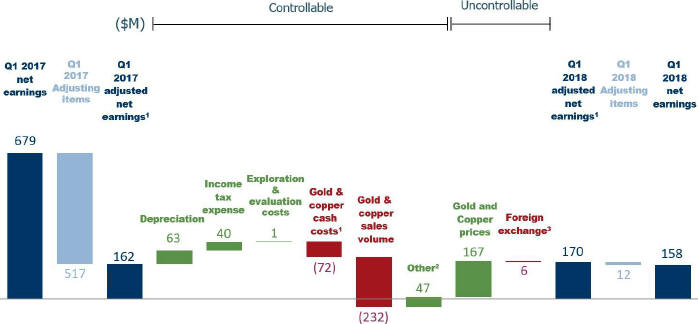

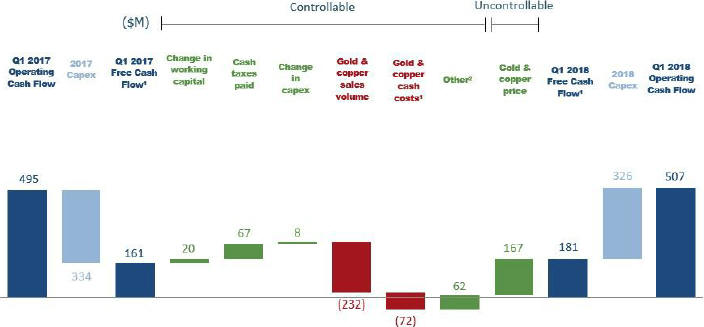

Operating cash flow for the first quarter was $507 million, compared to $495 million in the prior-year period. Higher operating cash flow was driven by higher realized gold prices9, lower cash taxes and interest paid, and lower general and administrative expenses related to stock-based compensation compared to the first quarter of 2017.

Free cash flow2 for the first quarter was $181 million, compared to $161 million in the prior-year period, reflecting slightly higher operating cash flows, combined with slightly lower capital expenditures. In the first quarter of 2018, capital expenditures on a cash basis were $326 million, compared to $334 million in the prior-year period.

BALANCE SHEET UPDATE

Over the past three years, we have reduced our total debt by more than 50 percent, from $13.1 billion at the end of 2014, to $6.4 billion by the end of 2017. In the first quarter of 2018, both S&P Global Ratings and Moody’s Investors Service upgraded Barrick’s credit rating, citing significant improvements in free cash flow generation and liquidity, supported by the Company’slow-cost portfolio and favorable geopolitical risk profile.

Our goal remains to reduce our total debt from $6.4 billion at present, to around $5 billion by the end of 2018. To achieve this, we will use cash flow from operations, and cash on hand. Having materially strengthened the balance sheet, Barrick does not intend to sell further assets for the purposes of debt repayment. Any proceeds resulting from additional portfolio optimization will be reinvested back into the business to enhance our project pipeline, or returned to shareholders.

At the end of the first quarter, Barrick had a consolidated cash balance of approximately $2.4 billion.10 The Company has less than $100 million in debt due before 2020.11 More than three-quarters of our outstanding total debt of $6.4 billion does not mature until after 2032.

OPERATING HIGHLIGHTS

Barrick produced 1.05 million ounces of gold in the first quarter of 2018 at a cost of sales3 of $878 per ounce, andall-in sustaining costs4 of $804 per ounce, in line with expectations. This compares to gold production of 1.31 million ounces in the first quarter of 2017, at a cost of sales3 of $833 per ounce, andall-in sustaining costs4 of $772 per ounce.

Lower gold production compared with the prior-year period was expected as a result of the sale of 50 percent of the Veladero mine on June 30, 2017, lower throughput at Acacia as a result of reduced operations at Bulyanhulu, lower grades processed through the oxide mill and roaster at Barrick Nevada, and lower throughput and grade at Hemlo and Lagunas Norte. An earthquake that damaged power infrastructure in Papua New Guinea also impacted production at Porgera during the quarter.

On a per ounce basis, cost of sales was five percent higher than the prior-year period due to the impact of fewer ounces sold, and higher royalty expenses as a result of an increase in realized gold prices.9 Cost of sales was also impacted by higher direct mining costs, primarily due to inflation in fuel, labor, and maintenance costs, partially offset byBest-in-Class operational and efficiency improvements. Higherall-in sustaining costs4 primarily reflect a planned increase in mine site sustaining capital expenditures on a per ounce basis, combined with higher direct mining costs.

The Company produced 85 million pounds of copper in the first quarter, at a cost of sales3 of $2.07 per pound, andall-in sustaining costs5 of $2.61 per pound. This compares to 95 million pounds, at a cost of sales of $1.73 per pound, andall-in sustaining costs5 of $2.19 per pound, in the first quarter of 2017.

| | | | |

BARRICK FIRST QUARTER 2018 | | 3 | | PRESS RELEASE |