CERTIFIED SHAREHOLDER REPORT OF REGISTERED MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number:

(811-04178)

Exact name of registrant as specified in charter:

Putnam American Government Income Fund

Address of principal executive offices:

One Post Office Square, Boston, Massachusetts 02109

Name and address of agent for service:

Robert T. Burns, Vice President One Post Office Square Boston, Massachusetts 02109

Copy to:

Bryan Chegwidden, Esq. Ropes & Gray LLP 1211 Avenue of the Americas New York, New York 10036

Registrant’s telephone number, including area code:

(617) 292-1000

Date of fiscal year end:

September 30, 2015

Date of reporting period:

October 1, 2014 – March 31, 2015

Item 1. Report to Stockholders:

The following is a copy of the report transmitted to stockholders pursuant to Rule 30e-1 under the Investment Company Act of 1940:

Putnam American Government Income Fund

Semiannual report 3 | 31 | 15

Message from the Trustees

1

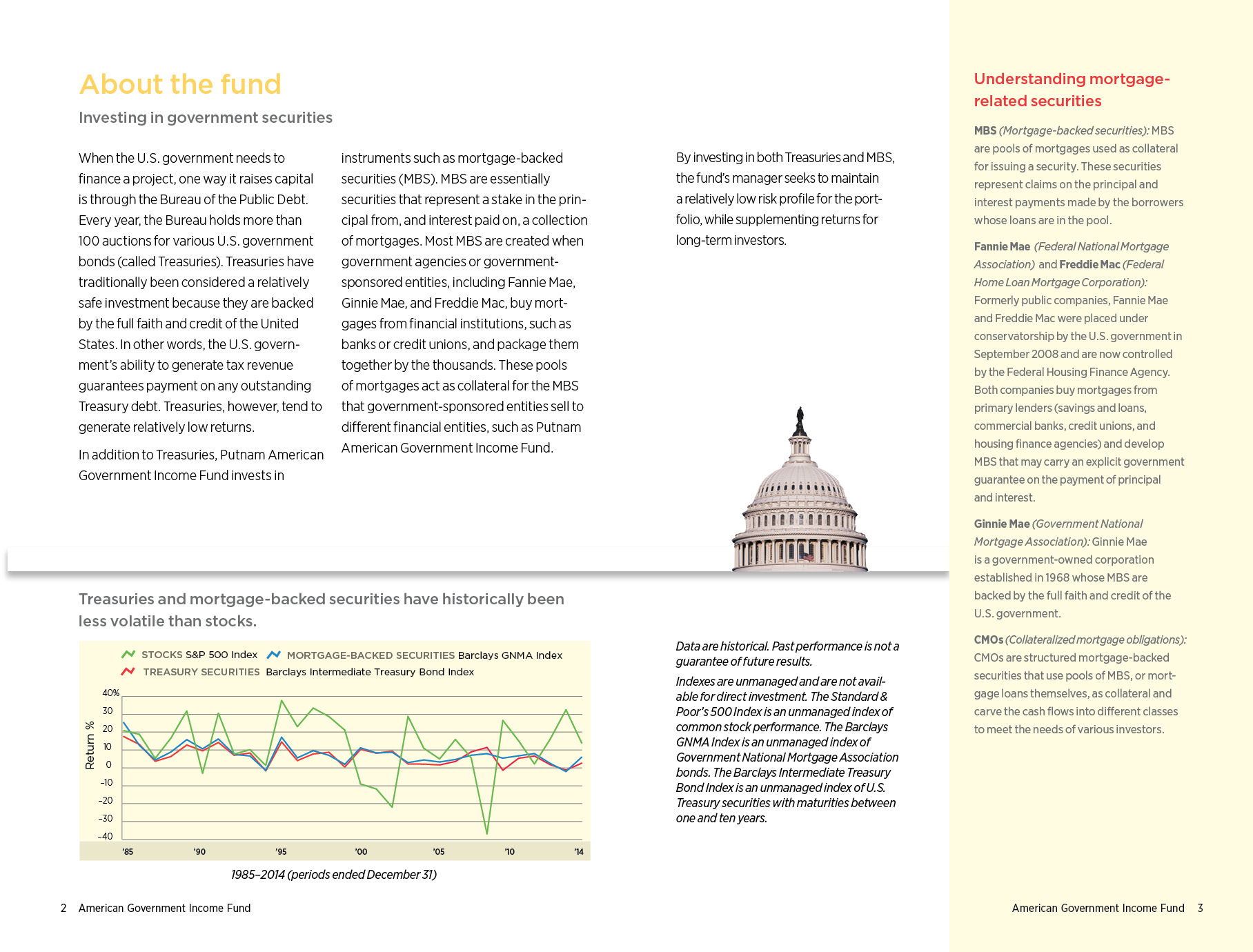

About the fund

2

Performance snapshot

4

Interview with your fund’s portfolio manager

5

Your fund’s performance

11

Your fund’s expenses

13

Terms and definitions

15

Other information for shareholders

16

Financial statements

17

Consider these risks before investing: Funds that invest in government securities are not guaranteed. Mortgage-backed securities are subject to prepayment risk and the risk that they may increase in value less when interest rates decline and decline in value more when interest rates rise. Bond investments are subject to interest-rate risk (the risk of bond prices falling if interest rates rise) and credit risk (the risk of an issuer defaulting on interest or principal payments). Interest-rate risk is greater for longer-term bonds, and credit risk is greater for below-investment-grade bonds. Risks associated with derivatives include increased investment exposure (which may be considered leverage) and, in the case of over-the-counter instruments, the potential inability to terminate or sell derivatives positions and the potential failure of the other party to the instrument to meet its obligations. Unlike bonds, funds that invest in bonds have fees and expenses. Bond prices may fall or fail to rise over time for several reasons, including general financial market conditions, changing market perceptions of the risk of default, changes in government intervention, and factors related to a specific issuer or industry. These factors may also lead to periods of high volatility and reduced liquidity in the bond markets. You can lose money by investing in the fund.

Message from the Trustees

Dear Fellow Shareholder:

The month of March 2015 marked the six-year milestone of the bull market in U.S. stocks, and this June will be the sixth anniversary of the beginning of the U.S. economic recovery as dated by the National Bureau of Economic Research, which has traced the chronology of U.S. business cycles back to 1854.

While six years is above the historical average on both counts, reaching these milestones does not necessarily indicate anything about the sustainability of the expansion or the market advance. However, we believe it is an unusually long period for the Federal Reserve to have refrained from raising interest rates. The Fed now appears poised to act, and speculation is mounting about where equity and fixed-income markets around the world could go from this point forward. Your portfolio manager provides a perspective in the following pages.

At this juncture of the market cycle, you might consult your financial advisor who can help you review your goals and risk profile, and explain the importance of timely adjustments to keep your portfolio equipped for all seasons.

As you make progress toward your long-term financial goals, markets may move in different directions. With Putnam, you are aligned with a group of portfolio managers and analysts who are experienced in navigating through changing markets with consistent strategies. They are dedicated to active, fundamental research and to helping you meet your financial needs.

As always, thank you for investing with Putnam.

Respectfully yours,

Robert L. Reynolds President and Chief Executive Officer Putnam Investments

Jameson A. Baxter Chair, Board of Trustees

May 8, 2015

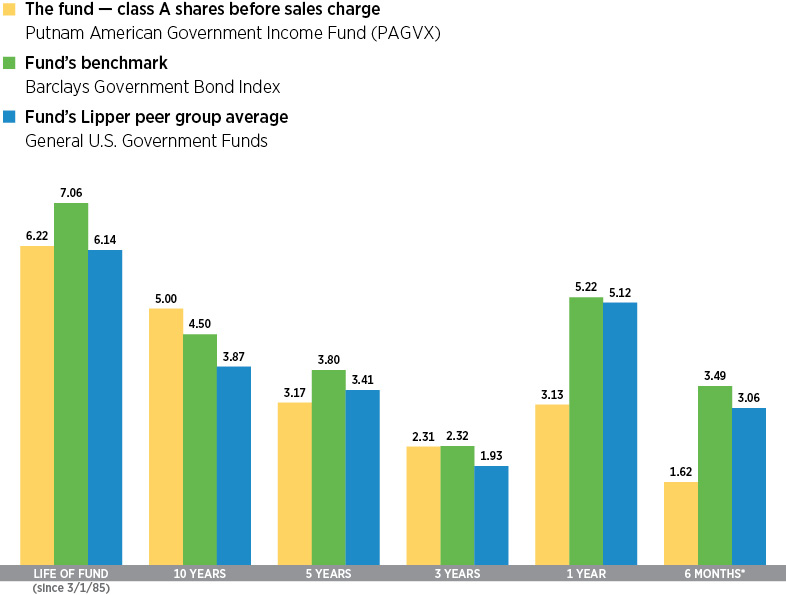

Performance snapshot

Annualized total return (%) comparison as of 3/31/15

Current performance may be lower or higher than the quoted past performance, which cannot guarantee future results. Share price, principal value, and return will fluctuate, and you may have a gain or a loss when you sell your shares. Performance of class A shares assumes reinvestment of distributions and does not account for taxes. Fund returns in the bar chart do not reflect a sales charge of 4.00%; had they, returns would have been lower. See pages 5 and 11–12 for additional performance information. For a portion of the periods, the fund had expense limitations, without which returns would have been lower. To obtain the most recent month-end performance, visit putnam.com.

*Returns for the six-month period are not annualized, but cumulative.

4 American Government Income Fund

Interview with your fund’s portfolio manager

Michael V. Salm

Mike, what was the bond market environment like during the six months ended March 31, 2015?

The period was punctuated by episodes of interest-rate volatility, but rates generally moved lower. We were not surprised to see some degree of rate volatility, given that the Federal Reserve ended its bond-buying program in October 2014 and the European Central Bank [ECB] officially announced its version of quantitative easing in January. Additionally, with U.S. gross domestic product growing at a 5% annual rate in the third quarter of 2014 — its strongest pace in 11 years — investors sought to fine-tune their forecasts as to when the Fed may begin raising its target for short-term interest rates.

In January, the combination of a stock market pullback, weaker-than-expected U.S. economic growth, and continued worries about deflation in Europe fueled investors’ appetite for government bonds. Against this backdrop, the yield on the benchmark 10-year U.S. Treasury fell to 1.68%, its low for the period. In February, concern that the Fed might start raising rates in June hampered Treasuries, causing prices to fall and yields to move higher. During March, however, dovish comments by Fed Chair Janet Yellen reassured investors that the central bank is likely to take a go-slow approach toward raising rates, which helped Treasuries modestly rebound during the final weeks of the period. The 10-year Treasury yield finished

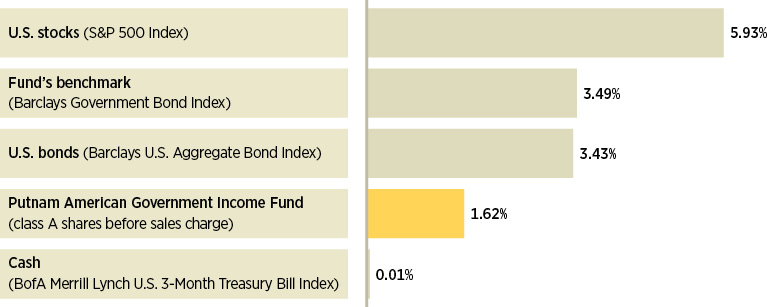

Broad market index and fund performance

This comparison shows your fund’s performance in the context of broad market indexes for the six months ended 3/31/15. See pages 4 and 11–12 for additional fund performance information. Index descriptions can be found on page 16.

American Government Income Fund 5

the period at 1.94%, down from 2.42% at the beginning of the period.

The fund lagged both its benchmark and the average return of its Lipper peer group during the reporting period. What factors hampered its relative performance?

Our interest-rate and yield-curve positioning worked against the fund’s relative performance and was the primary reason its performance lagged both the benchmark and the peer group average. The fund was defensively positioned for a rising-rate environment, resulting in an overall duration — a key measure of interest-rate sensitivity — that was shorter than that of the benchmark. Additionally, we positioned the portfolio to benefit from a steeper Treasury yield curve. During the period, however, rates declined and the yield curve flattened.

Which strategies helped performance versus the benchmark?

Various tactical trades that were designed to benefit from the difference between current mortgage rates and Treasury yields notably aided the fund’s relative performance.

Our prepayment strategies, which we implemented with securities such as government-agency interest-only collateralized mortgage obligations [IO CMOs] — which are outside the fund’s benchmark — slightly contributed to the fund’s relative return. During the early months of the period, even though interest rates were trending downward, their decline wasn’t severe enough to trigger substantial refinancing of the mortgages underlying our IO CMO holdings. Additionally, residential mortgage lending remained constrained, with banks generally willing to lend only to their most creditworthy customers. Consequently, prepayment speeds that continued to be

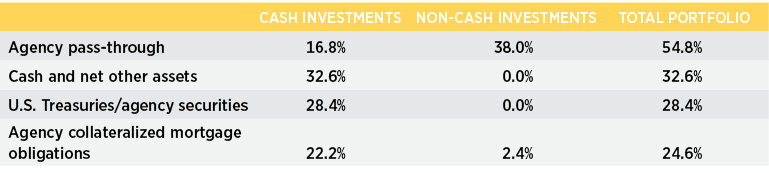

Sector weightings

Allocations are shown as a percentage of the fund’s net assets as of 3/31/15. Cash and net other assets, if any, represent the market value weights of cash, derivatives, short-term securities, and other unclassified assets in the portfolio. Summary information may differ from the portfolio schedule included in the financial statements due to the inclusion of derivative securities and any interest accruals. Percentages may not total 100% of net assets because cash may be set aside as collateral for certain securities holdings, such as to-be-announced (TBA) commitments. Holdings and allocations may vary over time.

6 American Government Income Fund

“We believe there are not enough homes being built in the United States to meet current demand.”

Michael Salm

slower than expected provided a tailwind to our IO CMO positions.

In January, however, the Obama administration announced that the Federal Housing Administration [FHA] would reduce the annual mortgage insurance premiums it charges to borrowers making small down payments. Investors reacted to this development by pricing in the possibility of faster mortgage prepayment speeds, which dampened the returns of existing prepayment-sensitive mortgage-backed securities. What’s more, this announcement came during a time when Treasury yields were sharply declining, compounding the negatives for IO CMOs. The asset class rebounded in February, but could not fully overcome January’s significant downturn.

What is your current view of the housing market?

Sales of newly built homes grew nearly 8% in February to an annual rate of 539,000, the highest level since early 2008, according to Commerce Department data. In our view, there needs to be roughly 1.2 million to 1.5 million new homes available each year to support normal population growth. So, we believe there are not enough homes being built in the United States to meet current demand, creating a supply/demand imbalance. While home prices continue to appreciate moderately, we believe housing affordability is somewhat better than it was two years ago. With an improving employment backdrop, continued low mortgage rates, and modestly easier mortgage-lending standards, we think demand-side fundamentals are positive. As a result, we

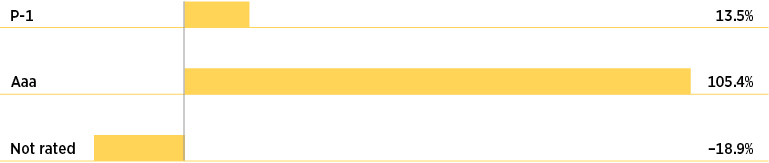

Credit quality overview

Credit qualities are shown as a percentage of the fund’s net assets as of 3/31/15. A bond rated Baa or higher (Prime-3 or higher, for short-term debt) is considered investment grade. The chart reflects Moody’s ratings; percentages may include bonds or derivatives not rated by Moody’s but rated by Standard & Poor’s (S&P) or, if unrated by S&P, by Fitch ratings, and then included in the closest equivalent Moody’s rating based on analysis of these agencies’ respective ratings criteria. Moody’s ratings are used in recognition of its prominence among rating agencies and breadth of coverage of rated securities. To-be-announced (TBA) mortgage commitments, if any, are included based on their issuer ratings. Ratings may vary over time.

Derivative instruments, including forward currency contracts, are only included to the extent of any unrealized gain or loss on such instruments and are shown in the not-rated category. Cash is also shown in the not-rated category. Derivative offset values are included in the not-rated category and may result in negative weights. The fund itself has not been rated by an independent rating agency.

American Government Income Fund 7

think new-home construction may pick up later this year.

How did you use derivatives during the period?

We used interest-rate swaps and “swaptions” — the latter of which give us the option to enter into a swap contract — to hedge the interest-rate and prepayment risks associated with our CMO and mortgage pass-through holdings, and to help manage overall downside risk. We also used interest-rate swaps and U.S. Treasury futures to help manage the fund’s yield-curve positioning.

What is your outlook for the months ahead, and how will it affect the fund’s positioning?

We remain positive on U.S. economic growth, but the recovery has reverted to a moderate pace after surging in the middle of last year. We believe this slowdown is partly because consumption hasn’t increased as much as was expected. During the past year, rising hourly wages and lower gasoline prices benefited lower-wage workers, which we thought would bolster personal consumption expenditures. However, rather than spending more, these consumers increased their savings. According to the Commerce Department, personal spending rose slightly in February, but was down in December and January. At the same time, the personal savings rate continued to climb, reaching 5.8% in February, its highest level since the end of 2012. As the effects of an unseasonably cold winter in the Northeast and Midwest dissipate, we think consumption will improve.

We believe the Fed is likely to begin raising rates during 2015, possibly in September. Many investors believe the Fed will wait until later in 2015, or even into 2016, before it begins hiking rates. Consequently, there appears to be a considerable disconnect between what the market is forecasting and the Fed’s own outlook, which could spark some volatility. In our view, however, once

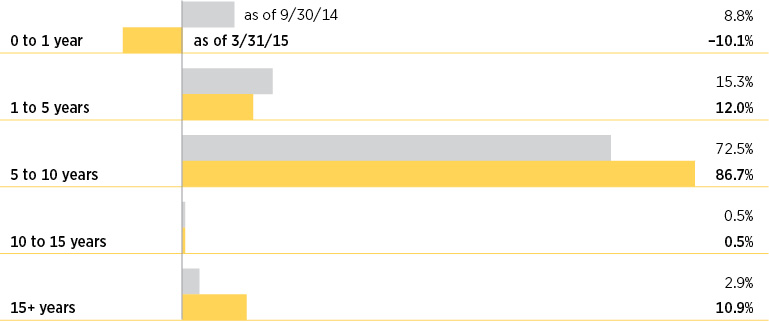

Comparison of maturity composition

This chart illustrates the fund’s composition by maturity, showing the percentage of holdings in different maturity ranges and how the composition has changed over the past six months. Holdings and maturity ranges may vary over time. A negative number represents cash to be allocated to to-be-announced (TBA) agency pass-through mortgage-backed securities, which the fund has agreed to purchase.

8 American Government Income Fund

the central bank begins to raise the federal funds rate, it will make every effort to do so in an orderly, well-communicated fashion in an effort to avoid major market disruption.

As for fund positioning, we plan to continue de-emphasizing interest-rate risk by keeping the portfolio’s duration shorter than the benchmark’s duration. We plan to maintain our holdings of IO CMOs since we do not believe the new FHA policy is likely to have a major impact on the overall pace of residential refinancing. Moreover, we continue to find prepayment risk attractive, given the potential for higher interest rates as the U.S. economic recovery matures.

Thanks, Mike, for your time and for bringing us up to date.

The views expressed in this report are exclusively those of Putnam Management and are subject to change. They are not meant as investment advice.

Please note that the holdings discussed in this report may not have been held by the fund for the entire period. Portfolio composition is subject to review in accordance with the fund’s investment strategy and may vary in the future. Current and future portfolio holdings are subject to risk.

Portfolio Manager Michael V. Salm is Co-Head of Fixed Income at Putnam. He has a B.A. from Cornell University. Michael joined Putnam in 1997 and has been in the investment industry since 1989.

ABOUT DERIVATIVES

Derivatives are an increasingly common type of investment instrument, the performance of which is derived from an underlying security, index, currency, or other area of the capital markets. Derivatives employed by the fund’s managers generally serve one of two main purposes: to implement a strategy that may be difficult or more expensive to invest in through traditional securities, or to hedge unwanted risk associated with a particular position.

For example, the fund’s managers might use currency forward contracts to capitalize on an anticipated change in exchange rates between two currencies. This approach would require a significantly smaller outlay of capital than purchasing traditional bonds denominated in the underlying currencies. In another example, the managers may identify a bond that they believe is undervalued relative to its risk of default, but may seek to reduce the interest-rate risk of that bond by using interest-rate swaps, a derivative through which two parties “swap” payments based on the movement of certain rates.

Like any other investment, derivatives may not appreciate in value and may lose money. Derivatives may amplify traditional investment risks through the creation of leverage and may be less liquid than traditional securities. And because derivatives typically represent contractual agreements between two financial institutions, derivatives entail “counterparty risk,” which is the risk that the other party is unable or unwilling to pay. Putnam monitors the counterparty risks we assume. For example, Putnam often enters into collateral agreements that require the counterparties to post collateral on a regular basis to cover their obligations to the fund. Counterparty risk for exchange-traded futures and centrally cleared swaps is mitigated by the daily exchange of margin and other safeguards against default through their respective clearinghouses.

American Government Income Fund 9

IN THE NEWS

Although the U.S. economy is showing positive trends, uneven growth in consumer spending remains a bit perplexing. Despite rising personal income and lower energy costs, consumer spending in the United States rose by only 0.1% in February after dropping 0.2% in January, according to the Commerce Department. Harsh winter weather during those months, with heavy snowfalls blanketing the Northeast and Midwest, may have discouraged millions of Americans from heading to stores. Amid weak spending, the pace of hiring also slowed to 126,000 new jobs in March, the lowest since December 2013. These soft readings, however, might be as temporary as the weather. The personal savings rate rose from 5.5% in January to 5.8% in February, with Americans reaching their highest levels in savings in more than two years. In short, consumers have money to spend, and a rebound in economic activity, along the lines of that seen in 2014, may be likely.

10 American Government Income Fund

Your fund’s performance

This section shows your fund’s performance, price, and distribution information for periods ended March 31, 2015, the end of the first half of its current fiscal year. In accordance with regulatory requirements for mutual funds, we also include expense information taken from the fund’s current prospectus. Performance should always be considered in light of a fund’s investment strategy. Data represent past performance. Past performance does not guarantee future results. More recent returns may be less or more than those shown. Investment return and principal value will fluctuate, and you may have a gain or a loss when you sell your shares. Performance information does not reflect any deduction for taxes a shareholder may owe on fund distributions or on the redemption of fund shares. For the most recent month-end performance, please visit the Individual Investors section at putnam.com or call Putnam at 1-800-225-1581. Class R, R5, R6, and Y shares are not available to all investors. See the Terms and Definitions section in this report for definitions of the share classes offered by your fund.

Fund performance Total return for periods ended 3/31/15

Class A

Class B

Class C

Class M

Class R

Class R5

Class R6

Class Y

(inception dates)

(3/1/85)

(5/20/94)

(7/26/99)

(2/14/95)

(4/1/03)

(7/2/12)

(7/2/12)

(7/2/01)

Before sales charge

After sales charge

Before CDSC

After CDSC

Before CDSC

After CDSC

Before sales charge

After sales charge

Net asset value

Net asset value

Net asset value

Net asset value

Annual average

(life of fund)

6.22%

6.08%

5.97%

5.97%

5.43%

5.43%

5.93%

5.81%

5.96%

6.35%

6.36%

6.35%

10 years

62.87

56.35

53.39

53.39

51.39

51.39

59.08

53.91

59.04

67.26

67.56

67.10

Annual average

5.00

4.57

4.37

4.37

4.23

4.23

4.75

4.41

4.75

5.28

5.30

5.27

5 years

16.86

12.19

12.57

10.78

12.64

12.64

15.49

11.74

15.46

18.40

18.61

18.28

Annual average

3.17

2.33

2.40

2.07

2.41

2.41

2.92

2.24

2.92

3.43

3.47

3.41

3 years

7.09

2.81

4.65

1.67

4.84

4.84

6.29

2.84

6.34

8.07

8.26

7.96

Annual average

2.31

0.93

1.53

0.55

1.59

1.59

2.05

0.94

2.07

2.62

2.68

2.59

1 year

3.13

–1.00

2.28

–2.72

2.37

1.37

2.83

–0.51

2.85

3.40

3.50

3.41

6 months

1.62

–2.45

1.15

–3.85

1.26

0.26

1.47

–1.83

1.48

1.76

1.80

1.76

Current performance may be lower or higher than the quoted past performance, which cannot guarantee future results. After-sales-charge returns for class A and M shares reflect the deduction of the maximum 4.00% and 3.25% sales charge, respectively, levied at the time of purchase. Class B share returns after contingent deferred sales charge (CDSC) reflect the applicable CDSC, which is 5% in the first year, declining over time to 1% in the sixth year, and is eliminated thereafter. Class C share returns after CDSC reflect a 1% CDSC for the first year that is eliminated thereafter. Class R, R5, R6, and Y shares have no initial sales charge or CDSC. Performance for class B, C, M, R, and Y shares before their inception is derived from the historical performance of class A shares, adjusted for the applicable sales charge (or CDSC) and the higher operating expenses for such shares, except for class Y shares, for which 12b-1 fees are not applicable. Performance for class R5 and R6 shares prior to their inception is derived from the historical performance of class Y shares and has not been adjusted for the lower investor servicing fees applicable to class R5 and R6 shares; had it, returns would have been higher.

For a portion of the periods, the fund had expense limitations, without which returns would have been lower.

Class B share performance reflects conversion to class A shares after eight years.

American Government Income Fund 11

Comparative index returns For periods ended 3/31/15

Barclays Government Bond Index

Lipper General U.S. Government Funds category average*

Annual average (life of fund)

7.06%

6.14%

10 years

55.24

47.10

Annual average

4.50

3.87

5 years

20.52

18.77

Annual average

3.80

3.41

3 years

7.12

6.00

Annual average

2.32

1.93

1 year

5.22

5.12

6 months

3.49

3.06

Index and Lipper results should be compared with fund performance before sales charge, before CDSC, or at net asset value.

*Over the 6-month, 1-year, 3-year, 5-year, 10-year, and life-of-fund periods ended 3/31/15, there were 108, 107, 102, 98, 74, and 7 funds, respectively, in this Lipper category.

Fund price and distribution information For the six-month period ended 3/31/15

Distributions

Class A

Class B

Class C

Class M

Class R

Class R5

Class R6

Class Y

Number

6

6

6

6

6

6

6

6

Income

$0.126

$0.093

$0.093

$0.114

$0.114

$0.138

$0.142

$0.138

Capital gains

—

—

—

—

—

—

—

—

Total

$0.126

$0.093

$0.093

$0.114

$0.114

$0.138

$0.142

$0.138

Share value

Before sales charge

After sales charge

Net asset value

Net asset value

Before sales charge

After sales charge

Net asset value

Net asset value

Net asset value

Net asset value

9/30/14

$9.08

$9.46

$9.01

$9.05

$9.16

$9.47

$9.10

$9.07

$9.06

$9.06

3/31/15

9.10

9.48

9.02

9.07

9.18

9.49

9.12

9.09

9.08

9.08

Current rate (end of period)

Before sales charge

After sales charge

Net asset value

Net asset value

Before sales charge

After sales charge

Net asset value

Net asset value

Net asset value

Net asset value

Current dividend rate 1

2.77%

2.66%

2.13%

2.12%

2.48%

2.40%

2.50%

3.04%

3.17%

3.04%

Current 30-day SEC yield 2

N/A

1.75

1.08

1.08

N/A

1.52

1.58

2.10

2.18

2.06

The classification of distributions, if any, is an estimate. Before-sales-charge share value and current dividend rate for class A and M shares, if applicable, do not take into account any sales charge levied at the time of purchase. After-sales-charge share value, current dividend rate, and current 30-day SEC yield, if applicable, are calculated assuming that the maximum sales charge (4.00% for class A shares and 3.25% for class M shares) was levied at the time of purchase. Final distribution information will appear on your year-end tax forms.

1 Most recent distribution, including any return of capital and excluding capital gains, annualized and divided by share price before or after sales charge at period-end.

2 Based only on investment income and calculated using the maximum offering price for each share class, in accordance with SEC guidelines.

12 American Government Income Fund

Your fund’s expenses

As a mutual fund investor, you pay ongoing expenses, such as management fees, distribution fees (12b-1 fees), and other expenses. Using the following information, you can estimate how these expenses affect your investment and compare them with the expenses of other funds. You may also pay one-time transaction expenses, including sales charges (loads) and redemption fees, which are not shown in this section and would have resulted in higher total expenses. For more information, see your fund’s prospectus or talk to your financial representative.

Expense ratios

Class A

Class B

Class C

Class M

Class R

Class R5

Class R6

Class Y

Total annual operating expenses for the fiscal year ended 9/30/14

0.88%

1.63%

1.63%

1.13%

1.13%

0.61%

0.54%

0.63%

Annualized expense ratio for the six-month period ended 3/31/15

0.87%

1.62%

1.62%

1.12%

1.12%

0.59%

0.52%

0.62%

Fiscal-year expense information in this table is taken from the most recent prospectus, is subject to change, and may differ from that shown for the annualized expense ratio and in the financial highlights of this report.

Expenses are shown as a percentage of average net assets.

Expenses per $1,000

The following table shows the expenses you would have paid on a $1,000 investment in the fund from October 1, 2014, to March 31, 2015. It also shows how much a $1,000 investment would be worth at the close of the period, assuming actual returns and expenses.

Class A

Class B

Class C

Class M

Class R

Class R5

Class R6

Class Y

Expenses paid per $1,000*†

$4.37

$8.12

$8.13

$5.63

$5.63

$2.97

$2.62

$3.12

Ending value (after expenses)

$1,016.20

$1,011.50

$1,012.60

$1,014.70

$1,014.80

$1,017.60

$1,018.00

$1,017.60

*Expenses for each share class are calculated using the fund’s annualized expense ratio for each class, which represents the ongoing expenses as a percentage of average net assets for the six months ended 3/31/15. The expense ratio may differ for each share class.

†Expenses are calculated by multiplying the expense ratio by the average account value for the period; then multiplying the result by the number of days in the period; and then dividing that result by the number of days in the year.

American Government Income Fund 13

Estimate the expenses you paid

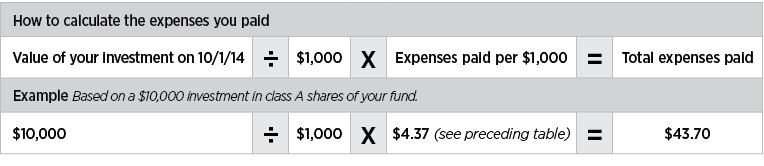

To estimate the ongoing expenses you paid for the six months ended March 31, 2015, use the following calculation method. To find the value of your investment on October 1, 2014, call Putnam at 1-800-225-1581.

Compare expenses using the SEC’s method

The Securities and Exchange Commission (SEC) has established guidelines to help investors assess fund expenses. Per these guidelines, the following table shows your fund’s expenses based on a $1,000 investment, assuming a hypothetical 5% annualized return. You can use this information to compare the ongoing expenses (but not transaction expenses or total costs) of investing in the fund with those of other funds. All mutual fund shareholder reports will provide this information to help you make this comparison. Please note that you cannot use this information to estimate your actual ending account balance and expenses paid during the period.

Class A

Class B

Class C

Class M

Class R

Class R5

Class R6

Class Y

Expenses paid per $1,000*†

$4.38

$8.15

$8.15

$5.64

$5.64

$2.97

$2.62

$3.13

Ending value (after expenses)

$1,020.59

$1,016.85

$1,016.85

$1,019.35

$1,019.35

$1,021.99

$1,022.34

$1,021.84

*Expenses for each share class are calculated using the fund’s annualized expense ratio for each class, which represents the ongoing expenses as a percentage of average net assets for the six months ended 3/31/15. The expense ratio may differ for each share class.

†Expenses are calculated by multiplying the expense ratio by the average account value for the six-month period; then multiplying the result by the number of days in the six-month period; and then dividing that result by the number of days in the year.

14 American Government Income Fund

Terms and definitions

Important terms

Total return shows how the value of the fund’s shares changed over time, assuming you held the shares through the entire period and reinvested all distributions in the fund.

Before sales charge, or net asset value, is the price, or value, of one share of a mutual fund, without a sales charge. Before-sales-charge figures fluctuate with market conditions, and are calculated by dividing the net assets of each class of shares by the number of outstanding shares in the class.

After sales charge is the price of a mutual fund share plus the maximum sales charge levied at the time of purchase. After-sales-charge performance figures shown here assume the 4.00% maximum sales charge for class A shares and 3.25% for class M shares.

Contingent deferred sales charge (CDSC) is generally a charge applied at the time of the redemption of class B or C shares and assumes redemption at the end of the period. Your fund’s class B CDSC declines over time from a 5% maximum during the first year to 1% during the sixth year. After the sixth year, the CDSC no longer applies. The CDSC for class C shares is 1% for one year after purchase.

Share classes

Class A shares are generally subject to an initial sales charge and no CDSC (except on certain redemptions of shares bought without an initial sales charge).

Class B shares are not subject to an initial sales charge and may be subject to a CDSC.

Class C shares are not subject to an initial sales charge and are subject to a CDSC only if the shares are redeemed during the first year.

Class M shares have a lower initial sales charge and a higher 12b-1 fee than class A shares and no CDSC (except on certain redemptions of shares bought without an initial sales charge).

Class R shares are not subject to an initial sales charge or CDSC and are available only to employer-sponsored retirement plans.

Class R5 and R6 shares are not subject to an initial sales charge or CDSC, and carry no 12b-1 fee. They are available only to employer-sponsored retirement plans.

Class Y shares are not subject to an initial sales charge or CDSC, and carry no 12b-1 fee. They are generally only available to corporate and institutional clients and clients in other approved programs.

Fixed-income terms

Current rate is the annual rate of return earned from dividends or interest of an investment. Current rate is expressed as a percentage of the price of a security, fund share, or principal investment.

Mortgage-backed security (MBS), also known as a mortgage “pass-through,” is a type of asset-backed security that is secured by a mortgage or collection of mortgages. The following are types of MBSs:

•Agency “pass-through” has its principal and interest backed by a U.S. government agency, such as the Federal National Mortgage Association (Fannie Mae), Government National Mortgage Association (Ginnie Mae), and Federal Home Loan Mortgage Corporation (Freddie Mac).

•Collateralized mortgage obligation (CMO) represents claims to specific cash flows from pools of home mortgages. The streams of principal and interest payments on the mortgages are distributed to the different classes of CMO interests in “tranches.” Each tranche may have different principal balances, coupon rates, prepayment risks, and maturity dates. A CMO is highly sensitive to changes in interest rates and any resulting change in the rate at which homeowners sell their properties, refinance, or otherwise prepay loans. CMOs are subject to prepayment, market, and liquidity risks.

•Interest-only (IO) security is a type of CMO in which the underlying asset is the interest portion of mortgage, Treasury, or bond payments.

•Non-agency residential mortgage-backed security (RMBS) is an MBS not backed by Fannie Mae, Ginnie Mae, or Freddie Mac. One type of RMBS is an Alt-A mortgage-backed security.

•Commercial mortgage-backed security (CMBS) is secured by the loan on a commercial property.

Yield curve is a graph that plots the yields of bonds with equal credit quality against their differing maturity dates, ranging from shortest to longest. It is used as a benchmark for other debt, such as mortgage or bank lending rates.

American Government Income Fund 15

Comparative indexes

Barclays Government Bond Index is an unmanaged index of U.S. Treasury and agency securities.

Barclays U.S. Aggregate Bond Index is an unmanaged index of U.S. investment-grade fixed-income securities.

BofA Merrill Lynch U.S. 3-Month Treasury Bill Index is an unmanaged index that seeks to measure the performance of U.S. Treasury bills available in the marketplace.

S&P 500 Index is an unmanaged index of common stock performance.

Indexes assume reinvestment of all distributions and do not account for fees. Securities and performance of a fund and an index will differ. You cannot invest directly in an index.

Lipper is a third-party industry-ranking entity that ranks mutual funds. Its rankings do not reflect sales charges. Lipper rankings are based on total return at net asset value relative to other funds that have similar current investment styles or objectives as determined by Lipper. Lipper may change a fund’s category assignment at its discretion. Lipper category averages reflect performance trends for funds within a category.

Other information for shareholders

Important notice regarding delivery of shareholder documents

In accordance with Securities and Exchange Commission (SEC) regulations, Putnam sends a single copy of annual and semiannual shareholder reports, prospectuses, and proxy statements to Putnam shareholders who share the same address, unless a shareholder requests otherwise. If you prefer to receive your own copy of these documents, please call Putnam at 1-800-225-1581, and Putnam will begin sending individual copies within 30 days.

Proxy voting

Putnam is committed to managing our mutual funds in the best interests of our shareholders. The Putnam funds’ proxy voting guidelines and procedures, as well as information regarding how your fund voted proxies relating to portfolio securities during the 12-month period ended June 30, 2014, are available in the Individual Investors section of putnam.com, and on the SEC’s website, www.sec.gov. If you have questions about finding forms on the SEC’s website, you may call the SEC at 1-800-SEC-0330. You may also obtain the Putnam funds’ proxy voting guidelines and procedures at no charge by calling Putnam’s Shareholder Services at 1-800-225-1581.

Fund portfolio holdings

The fund will file a complete schedule of its portfolio holdings with the SEC for the first and third quarters of each fiscal year on Form N-Q. Shareholders may obtain the fund’s Form N-Q on the SEC’s website at www.sec.gov. In addition, the fund’s Form N-Q may be reviewed and copied at the SEC’s Public Reference Room in Washington, D.C. You may call the SEC at 1-800-SEC-0330 for information about the SEC’s website or the operation of the Public Reference Room.

Trustee and employee fund ownership

Putnam employees and members of the Board of Trustees place their faith, confidence, and, most importantly, investment dollars in Putnam mutual funds. As of March 31, 2015, Putnam employees had approximately $494,000,000 and the Trustees had approximately $141,000,000 invested in Putnam mutual funds. These amounts include investments by the Trustees’ and employees’ immediate family members as well as investments through retirement and deferred compensation plans.

16 American Government Income Fund

Financial statements

A guide to financial statements

These sections of the report, as well as the accompanying Notes, constitute the fund’s financial statements.

The fund’s portfolio lists all the fund’s investments and their values as of the last day of the reporting period. Holdings are organized by asset type and industry sector, country, or state to show areas of concentration and diversification.

Statement of assets and liabilities shows how the fund’s net assets and share price are determined. All investment and non-investment assets are added together. Any unpaid expenses and other liabilities are subtracted from this total. The result is divided by the number of shares to determine the net asset value per share, which is calculated separately for each class of shares. (For funds with preferred shares, the amount subtracted from total assets includes the liquidation preference of preferred shares.)

Statement of operations shows the fund’s net investment gain or loss. This is done by first adding up all the fund’s earnings — from dividends and interest income — and subtracting its operating expenses to determine net investment income (or loss). Then, any net gain or loss the fund realized on the sales of its holdings — as well as any unrealized gains or losses over the period — is added to or subtracted from the net investment result to determine the fund’s net gain or loss for the fiscal period.

Statement of changes in net assets shows how the fund’s net assets were affected by the fund’s net investment gain or loss, by distributions to shareholders, and by changes in the number of the fund’s shares. It lists distributions and their sources (net investment income or realized capital gains) over the current reporting period and the most recent fiscal year-end. The distributions listed here may not match the sources listed in the Statement of operations because the distributions are determined on a tax basis and may be paid in a different period from the one in which they were earned. Dividend sources are estimated at the time of declaration. Actual results may vary. Any non-taxable return of capital cannot be determined until final tax calculations are completed after the end of the fund’s fiscal year.

Financial highlights provide an overview of the fund’s investment results, per-share distributions, expense ratios, net investment income ratios, and portfolio turnover in one summary table, reflecting the five most recent reporting periods. In a semiannual report, the highlights table also includes the current reporting period.

American Government Income Fund 17

The fund’s portfolio 3/31/15 (Unaudited)

U.S. GOVERNMENT AND AGENCY MORTGAGE OBLIGATIONS (78.2%)*

Principal amount

Value

U.S. Government Guaranteed Mortgage Obligations (9.7%)

Government National Mortgage Association Pass-Through Certificates

6s, January 15, 2029

$4

$5

5s, TBA, April 1, 2045

4,000,000

4,377,500

4 1/2s, with due dates from December 20, 2040 to January 20, 2045

9,298,393

10,319,296

4s, with due dates from March 20, 2044 to January 20, 2045

3,540,779

3,857,899

3 1/2s, with due dates from January 20, 2045 to March 20, 2045

10,094,609

10,655,937

3 1/2s, TBA, May 1, 2045

10,000,000

10,500,000

3s, TBA, June 1, 2045

6,000,000

6,150,937

3s, TBA, May 1, 2045

6,000,000

6,165,937

52,027,511

U.S. Government Agency Mortgage Obligations (68.5%)

Federal Home Loan Mortgage Corporation Pass-Through Certificates

7 1/2s, October 1, 2029

465,805

547,645

6s, September 1, 2021

5,951

6,530

5 1/2s, with due dates from July 1, 2019 to August 1, 2019

123,750

132,396

4 1/2s, with due dates from January 1, 2037 to May 1, 2044

4,205,854

4,693,034

3 1/2s, with due dates from August 1, 2043 to February 1, 2044

2,675,480

2,828,248

3 1/2s, TBA, April 1, 2045

2,000,000

2,096,719

3s, March 1, 2043

856,209

876,578

Federal National Mortgage Association Pass-Through Certificates

6 1/2s, with due dates from July 1, 2016 to February 1, 2017

12,532

12,990

6s, January 1, 2038

1,719,033

1,963,479

6s, with due dates from July 1, 2016 to August 1, 2022

724,652

792,956

6s, TBA, April 1, 2045

4,000,000

4,561,250

5 1/2s, with due dates from September 1, 2017 to February 1, 2021

205,147

220,191

5 1/2s, TBA, April 1, 2045

11,000,000

12,388,750

5s, March 1, 2021

11,625

12,529

4 1/2s, with due dates from March 1, 2039 to February 1, 2044

6,030,522

6,643,383

4 1/2s, TBA, May 1, 2045

39,000,000

42,436,875

4 1/2s, TBA, April 1, 2045

52,000,000

56,728,750

4s, with due dates from July 1, 2042 to February 1, 2045

36,880,614

39,976,032

4s, with due dates from May 1, 2019 to September 1, 2020

59,019

62,362

4s, TBA, April 1, 2045

27,000,000

28,871,016

3 1/2s, with due dates from March 1, 2043 to April 1, 2045

7,762,922

8,163,597

3 1/2s, TBA, May 1, 2045

17,000,000

17,816,133

3 1/2s, TBA, April 1, 2045

27,000,000

28,364,766

3s, February 1, 2043

890,074

912,465

3s, TBA, April 1, 2045

105,000,000

107,362,500

368,471,174

Total U.S. government and agency mortgage obligations (cost $417,462,630)

$420,498,685

18 American Government Income Fund

U.S. TREASURY OBLIGATIONS (28.3%)*

Principal amount

Value

U.S. Treasury Bonds

7 1/8s, February 15, 2023

$12,085,000

$16,876,985

6 1/4s, August 15, 2023

17,682,000

23,810,091

4 1/2s, August 15, 2039 Δ §

42,774,000

58,561,113

U.S. Treasury Notes 0 5/8s, May 31, 2017 Δ

52,927,000

52,927,000

Total U.S. treasury obligations (cost $140,935,582)

Total mortgage-backed securities (cost $119,343,444)

$118,082,709

PURCHASED SWAP OPTIONS OUTSTANDING (1.2%)* Counterparty Fixed right % to receive or (pay)/ Floating rate index/Maturity date

Expiration date/strike

Contract amount

Value

Bank of America N.A.

2.175/3 month USD-LIBOR-BBA/Apr-25

Apr-15/2.175

$35,832,400

$490,904

(2.0875)/3 month USD-LIBOR-BBA/Jul-25

Jul-15/2.0875

17,916,200

314,608

(2.685)/3 month USD-LIBOR-BBA/Sep-25

Sep-15/2.685

35,137,300

203,445

1.816/3 month USD-LIBOR-BBA/Apr-25

Apr-15/1.816

35,137,300

43,570

Barclays Bank PLC

(2.1625)/3 month USD-LIBOR-BBA/May-25

May-15/2.1625

35,137,300

294,099

(2.31)/3 month USD-LIBOR-BBA/Apr-45

Apr-15/2.31

7,027,460

232,820

2.31/3 month USD-LIBOR-BBA/Apr-45

Apr-15/2.31

7,027,460

82,573

Citibank, N.A.

2.20/3 month USD-LIBOR-BBA/May-25

May-15/2.20

35,216,800

631,789

2.172/3 month USD-LIBOR-BBA/Apr-25

Apr-15/2.172

17,916,200

244,556

2.043/3 month USD-LIBOR-BBA/May-25

May-15/2.043

17,568,650

183,241

1.4015/3 month USD-LIBOR-BBA/May-20

May-15/1.4015

70,274,600

182,714

(2.13)/3 month USD-LIBOR-BBA/Apr-25

Apr-15/2.13

35,137,300

140,901

1.294/3 month USD-LIBOR-BBA/May-20

May-15/1.294

70,274,600

103,304

1.3735/3 month USD-LIBOR-BBA/May-20

May-15/1.3735

35,137,300

79,410

1.266/3 month USD-LIBOR-BBA/May-20

May-15/1.266

35,137,300

44,273

1.802/3 month USD-LIBOR-BBA/Apr-25

Apr-15/1.802

35,137,300

38,300

Credit Suisse International

2.25/3 month USD-LIBOR-BBA/May-25

May-15/2.25

58,200,000

1,235,004

2.09125/3 month USD-LIBOR-BBA/Apr-25

Apr-15/2.09125

35,872,000

297,738

2.09/3 month USD-LIBOR-BBA/Apr-25

Apr-15/2.09

35,872,000

294,868

1.795/3 month USD-LIBOR-BBA/Apr-25

Apr-15/1.795

35,226,700

35,931

22 American Government Income Fund

PURCHASED SWAP OPTIONS OUTSTANDING (1.2%)* Counterparty Fixed right % to receive or (pay)/ Floating rate index/Maturity date cont.

Expiration date/strike

Contract amount

Value

Goldman Sachs International

2.655/3 month USD-LIBOR-BBA/May-45

May-15/2.655

$8,784,325

$551,831

(2.82)/3 month USD-LIBOR-BBA/Jan-46

Jan-16/2.82

11,904,425

449,392

1.84/3 month USD-LIBOR-BBA/Apr-25

Apr-15/1.84

26,353,000

56,659

1.76/3 month USD-LIBOR-BBA/Apr-25

Apr-15/1.76

26,353,000

31,097

Total purchased swap options outstanding (cost $5,571,717)

$6,263,027

PURCHASED OPTIONS OUTSTANDING (0.1%)*

Expiration date/strike price

Contract amount

Value

Federal National Mortgage Association 30 yr 3.0s TBA commitments (Put)

May-15/$102.57

$21,000,000

$189,294

Federal National Mortgage Association 30 yr 3.0s TBA commitments (Put)

Apr-15/103.07

18,000,000

139,032

Total purchased options outstanding (cost $621,563)

$328,326

SHORT-TERM INVESTMENTS (33.6%)*

Principal amount/shares

Value

Federal Home Loan Banks unsec. discount notes with an effective yield of 0.09%, May 1, 2015

$14,000,000

$13,998,892

Federal Home Loan Banks unsec. discount notes with an effective yield of 0.04%, April 15, 2015

8,000,000

7,999,860

Federal Home Loan Banks unsec. discount notes with an effective yield of 0.04%, April 6, 2015

17,000,000

16,999,906

Federal Home Loan Mortgage Corporation unsec. discount notes with an effective yield of 0.16%, April 10, 2015

1,800,000

1,799,928

Federal Home Loan Mortgage Corporation unsec. discount notes with an effective yield of 0.08%, April 27, 2015

16,000,000

15,999,076

Federal Home Loan Mortgage Corporation unsec. discount notes with an effective yield of 0.08%, April 6, 2015

1,000,000

999,988

Federal Home Loan Mortgage Corporation unsec. discount notes with an effective yield of 0.08%, April 9, 2015

1,800,000

1,799,966

Federal Home Loan Mortgage Corporation unsec. discount notes with effective yields ranging from 0.08% to 0.10%, May 13, 2015

4,200,000

4,199,557

Federal National Mortgage Association unsec. discount notes with an effective yield of 0.07%, April 6, 2015

4,000,000

3,999,963

Federal National Mortgage Association unsec. discount notes with an effective yield of 0.10%, May 1, 2015

3,800,000

3,799,683

Putnam Money Market Liquidity Fund 0.09% L

Shares 104,701,969

104,701,969

SSgA Prime Money Market Fund Class N 0.02% P

Shares 2,889,000

2,889,000

U.S. Treasury Bills with an effective yield of 0.03%, April 16, 2015 #

$50,000

49,999

U.S. Treasury Bills with an effective yield of 0.02%, April 23, 2015 #

243,000

242,997

U.S. Treasury Bills with an effective yield of 0.02%, April 9, 2015 #

175,000

174,999

U.S. Treasury Bills with an effective yield of 0.09%, June 11, 2015 #

108,000

107,996

American Government Income Fund 23

SHORT-TERM INVESTMENTS (33.6%)* cont.

Principal amount/shares

Value

U.S. Treasury Bills with an effective yield of 0.03%, May 21, 2015 #

$50,000

$49,998

U.S. Treasury Bills with an effective yield of 0.02%, May 7, 2015 #

570,000

569,988

Total short-term investments (cost $180,383,750)

$180,383,765

TOTAL INVESTMENTS

Total investments (cost $864,318,686)

$877,731,701

Key to holding’s abbreviations

FRB

Floating Rate Bonds: the rate shown is the current interest rate at the close of the reporting period

IFB

Inverse Floating Rate Bonds, which are securities that pay interest rates that vary inversely to changes in the market interest rates. As interest rates rise, inverse floaters produce less current income. The rate shown is the current interest rate at the close of the reporting period.

IO

Interest Only

PO

Principal Only

TBA

To Be Announced Commitments

Notes to the fund’s portfolio

Unless noted otherwise, the notes to the fund’s portfolio are for the close of the fund’s reporting period, which ran from October 1,2014 through March 31, 2015 (the reporting period). Within the following notes to the portfolio, references to “ASC 820” represent Accounting Standards Codification 820 Fair Value Measurements and Disclosures and references to “OTC”, if any, represent over-the-counter.

*

Percentages indicated are based on net assets of $537,634,896.

#

This security, in part or in entirety, was pledged and segregated with the broker to cover margin requirements for futures contracts at the close of the reporting period.

Δ

This security, in part or in entirety, was pledged and segregated with the custodian for collateral on certain derivative contracts at the close of the reporting period.

§

This security, in part or in entirety, was pledged and segregated with the custodian for collateral on the initial margin on certain centrally cleared derivative contracts at the close of the reporting period.

L

Affiliated company (Note 5). The rate quoted in the security description is the annualized 7-day yield of the fund at the close of the reporting period.

P

This security was pledged, or purchased with cash that was pledged, to the fund for collateral on certain derivative contracts. The rate quoted in the security description is the annualized 7-day yield of the fund at the close of the reporting period (Note 1).

At the close of the reporting period, the fund maintained liquid assets totaling $401,300,476 to cover certain derivative contracts and delayed delivery securities.

Debt obligations are considered secured unless otherwise indicated.

See Note 1 to the financial statements regarding TBA commitments.

The dates shown on debt obligations are the original maturity dates.

FUTURES CONTRACTS OUTSTANDING at 3/31/15 (Unaudited)

Number of contracts

Value

Expiration date

Unrealized appreciation/ (depreciation)

U.S. Treasury Bond 30 yr (Short)

44

$7,210,500

Jun-15

$(8,619)

U.S. Treasury Bond Ultra 30 yr (Long)

21

3,567,375

Jun-15

(15,261)

24 American Government Income Fund

FUTURES CONTRACTS OUTSTANDING at 3/31/15 (Unaudited) cont.

Number of contracts

Value

Expiration date

Unrealized appreciation/ (depreciation)

U.S. Treasury Note 2 yr (Long)

121

$26,517,906

Jun-15

$96,181

U.S. Treasury Note 5 yr (Long)

914

109,872,797

Jun-15

1,005,869

U.S. Treasury Note 10 yr (Long)

91

$11,730,469

Jun-15

74,288

Total

$1,152,458

WRITTEN SWAP OPTIONS OUTSTANDING at 3/31/15 (premiums $5,602,141) (Unaudited)

Counterparty Fixed Obligation % to receive or (pay)/ Floating rate index/Maturity date

Expiration date/strike

Contract amount

Value

Bank of America N.A.

2.916/3 month USD-LIBOR-BBA/Apr-25

Apr-15/2.916

$35,137,300

$35

(1.9125)/3 month USD-LIBOR-BBA/Apr-25

Apr-15/1.9125

35,832,400

52,674

2.955/3 month USD-LIBOR-BBA/Sep-25

Sep-15/2.955

70,274,600

184,119

(2.04375)/3 month USD-LIBOR-BBA/Apr-25

Apr-15/2.04375

35,832,400

197,795

1.66/3 month USD-LIBOR-BBA/Jul-20

Jul-15/1.66

35,832,400

310,309

Barclays Bank PLC

2.3775/3 month USD-LIBOR-BBA/May-25

May-15/2.3775

35,137,300

105,061

2.265/3 month USD-LIBOR-BBA/May-25

May-15/2.265

35,137,300

184,471

Citibank, N.A.

2.902/3 month USD-LIBOR-BBA/Apr-25

Apr-15/2.902

35,137,300

176

(1.602)/3 month USD-LIBOR-BBA/Apr-25

Apr-15/1.602

35,137,300

5,271

2.28/3 month USD-LIBOR-BBA/Apr-25

Apr-15/2.28

35,137,300

37,246

(1.932)/3 month USD-LIBOR-BBA/Apr-25

Apr-15/1.932

17,916,200

37,624

2.205/3 month USD-LIBOR-BBA/Apr-25

Apr-15/2.205

35,137,300

75,545

(2.052)/3 month USD-LIBOR-BBA/Apr-25

Apr-15/2.052

17,916,200

111,439

(1.481)/3 month USD-LIBOR-BBA/May-20

May-15/1.481

35,137,300

133,170

(2.223)/3 month USD-LIBOR-BBA/May-25

May-15/2.223

8,784,325

176,477

(1.509)/3 month USD-LIBOR-BBA/May-20

May-15/1.509

70,274,600

302,181

Credit Suisse International

2.895/3 month USD-LIBOR-BBA/Apr-25

Apr-15/2.895

35,226,700

35

(1.80)/3 month USD-LIBOR-BBA/Apr-25

Apr-15/1.80

35,872,000

16,142

(1.80125)/3 month USD-LIBOR-BBA/Apr-25

Apr-15/1.80125

35,872,000

16,501

(1.94)/3 month USD-LIBOR-BBA/Apr-25

Apr-15/1.94

35,872,000

81,429

(1.94125)/3 month USD-LIBOR-BBA/Apr-25

Apr-15/1.94125

35,872,000

82,506

Goldman Sachs International

(1.92)/3 month USD-LIBOR-BBA/Apr-25

Apr-15/1.92

26,353,000

99,087

(2.35)/3 month USD-LIBOR-BBA/May-45

May-15/2.35

8,784,325

194,485

(1.885)/3 month USD-LIBOR-BBA/Jan-46

Jan-16/1.885

11,904,425

270,492

(2.5025)/3 month USD-LIBOR-BBA/May-45

May-15/2.5025

8,784,325

343,291

JPMorgan Chase Bank N.A.

(6.00 Floor)/3 month USD-LIBOR-BBA/Mar-18

Mar-18/6.00

6,128,000

911,846

Total

$3,929,407

American Government Income Fund 25

WRITTEN OPTIONS OUTSTANDING at 3/31/15 (premiums $622,734) (Unaudited)

Expiration date/ strike price

Contract amount

Value

Federal National Mortgage Association 30 yr 3.0s TBA commitments (Put)

May-15/$101.57

$21,000,000

$92,778

Federal National Mortgage Association 30 yr 3.0s TBA commitments (Put)

May-15/100.57

21,000,000

36,393

Federal National Mortgage Association 30 yr 3.0s TBA commitments (Put)

Apr-15/102.07

18,000,000

37,692

Federal National Mortgage Association 30 yr 3.0s TBA commitments (Put)

Apr-15/101.07

18,000,000

3,222

Total

$170,085

FORWARD PREMIUM SWAP OPTION CONTRACTS OUTSTANDING at 3/31/15 (Unaudited)

Counterparty Fixed right or obligation % to receive or (pay)/ Floating rate index/ Maturity date

Expiration date/strike

Contract amount

Premium receivable/ (payable)

Unrealized appreciation/ (depreciation)

Goldman Sachs International

1.955/3 month USD-LIBOR-BBA/Apr-25 (Purchased)

Apr-15/1.955

$24,596,110

$(137,738)

$(6,149)

(2.155)/3 month USD-LIBOR-BBA/Apr-25 (Purchased)

Apr-15/2.155

24,596,110

(137,738)

(8,609)

JPMorgan Chase Bank N.A.

2.117/3 month USD-LIBOR-BBA/Feb-27 (Purchased)

Feb-17/2.117

8,784,325

(215,242)

61,051

2.035/3 month USD-LIBOR-BBA/Feb-27 (Purchased)

Feb-17/2.035

8,784,325

(223,201)

24,034

(3.035)/3 month USD-LIBOR-BBA/Feb-27 (Purchased)

Feb-17/3.035

8,784,325

(233,733)

(28,022)

(3.117)/3 month USD-LIBOR-BBA/Feb-27 (Purchased)

Feb-17/3.117

8,784,325

(245,961)

(58,987)

2.655/3 month USD-LIBOR-BBA/Feb-19 (Written)

Feb-17/2.655

38,475,300

254,899

72,295

2.56/3 month USD-LIBOR-BBA/Feb-19 (Written)

Feb-17/2.56

38,475,300

245,961

45,170

(1.56)/3 month USD-LIBOR-BBA/Feb-19 (Written)

Feb-17/1.56

38,475,300

221,514

(39,245)

(1.655)/3 month USD-LIBOR-BBA/Feb-19 (Written)

Feb-17/1.655

38,475,300

219,309

(73,487)

Total

$(251,930)

$(11,949)

TBA SALE COMMITMENTS OUTSTANDING at 3/31/15 (proceeds receivable $122,734,160) (Unaudited)

Agency

Principal amount

Settlement date

Value

Federal Home Loan Mortgage Corporation, 3 1/2s, April 1, 2045

$2,000,000

4/14/15

$2,096,719

Federal National Mortgage Association, 4 1/2s, April 1, 2045

52,000,000

4/14/15

56,728,750

Federal National Mortgage Association, 4s, April 1, 2045

11,000,000

4/14/15

11,762,266

Federal National Mortgage Association, 3 1/2s, April 1, 2045

27,000,000

4/14/15

28,364,766

26 American Government Income Fund

TBA SALE COMMITMENTS OUTSTANDING at 3/31/15 (proceeds receivable $122,734,160) (Unaudited) cont.

Agency

Principal amount

Settlement date

Value

Government National Mortgage Association, 4 1/2s, April 1, 2045

$7,000,000

4/22/15

$7,604,843

Government National Mortgage Association, 3 1/2s, April 1, 2045

10,000,000

4/22/15

10,525,000

Government National Mortgage Association, 3s, May 1, 2045

6,000,000

5/20/15

6,165,937

Total

$123,248,281

CENTRALLY CLEARED INTEREST RATE SWAP CONTRACTS OUTSTANDING at 3/31/15 (Unaudited)

OTC TOTAL RETURN SWAP CONTRACTS OUTSTANDING at 3/31/15 (Unaudited)

Swap counterparty/ Notional amount

Upfront premium received (paid)

Termination date

Payments received (paid) by fund per annum

Total return received by or paid by fund

Unrealized appreciation/ (depreciation)

Barclays Bank PLC

$1,940,184

$—

1/12/40

4.50% (1 month USD-LIBOR)

Synthetic MBX Index 4.50% 30 year Fannie Mae pools

$15,615

1,960,911

—

1/12/42

4.00% (1 month USD-LIBOR)

Synthetic TRS Index 4.00% 30 year Fannie Mae pools

(25,008)

3,713,889

—

1/12/38

(6.50%) 1 month USD-LIBOR

Synthetic MBX Index 6.50% 30 year Fannie Mae pools

(16,957)

3,434,440

—

1/12/40

5.00% (1 month USD-LIBOR)

Synthetic MBX Index 5.00% 30 year Fannie Mae pools

16,197

3,160,917

—

1/12/41

5.00% (1 month USD-LIBOR)

Synthetic MBX Index 5.00% 30 year Fannie Mae pools

15,894

9,704,970

—

1/12/38

(6.50%) 1 month USD-LIBOR

Synthetic MBX Index 6.50% 30 year Fannie Mae pools

(44,312)

8,493,241

—

1/12/41

5.00% (1 month USD-LIBOR)

Synthetic MBX Index 5.00% 30 year Fannie Mae pools

42,706

9,964,095

—

1/12/41

5.00% (1 month USD-LIBOR)

Synthetic MBX Index 5.00% 30 year Fannie Mae pools

50,102

384,623

—

1/12/40

4.00% (1 month USD-LIBOR)

Synthetic MBX Index 4.00% 30 year Fannie Mae pools

2,033

911,331

—

1/12/41

5.00% (1 month USD-LIBOR)

Synthetic MBX Index 5.00% 30 year Fannie Mae pools

4,582

1,149,703

—

1/12/41

5.00% (1 month USD-LIBOR)

Synthetic MBX Index 5.00% 30 year Fannie Mae pools

5,781

801,900

—

1/12/39

6.00% (1 month USD-LIBOR)

Synthetic TRS Index 6.00% 30 year Fannie Mae pools

5,653

8,309,222

—

1/12/38

(6.50%) 1 month USD-LIBOR

Synthetic MBX Index 6.50% 30 year Fannie Mae pools

(37,939)

10,404,814

—

1/12/41

5.00% (1 month USD-LIBOR)

Synthetic MBX Index 5.00% 30 year Fannie Mae pools

52,318

3,200,703

—

1/12/40

4.00% (1 month USD-LIBOR)

Synthetic MBX Index 4.00% 30 year Fannie Mae pools

16,922

79,164

—

1/12/38

6.50% (1 month USD-LIBOR)

Synthetic TRS Index 6.50% 30 year Fannie Mae pools

715

American Government Income Fund 31

OTC TOTAL RETURN SWAP CONTRACTS OUTSTANDING at 3/31/15 (Unaudited) cont.

Swap counterparty/ Notional amount

Upfront premium received (paid)

Termination date

Payments received (paid) by fund per annum

Total return received by or paid by fund

Unrealized appreciation/ (depreciation)

Barclays Bank PLC cont.

$704,002

$—

1/12/41

5.00% (1 month USD-LIBOR)

Synthetic MBX Index 5.00% 30 year Fannie Mae pools

$3,540

3,131,241

—

1/12/41

4.00% (1 month USD-LIBOR)

Synthetic TRS Index 4.00% 30 year Fannie Mae pools

(39,443)

763,225

—

1/12/41

5.00% (1 month USD-LIBOR)

Synthetic MBX Index 5.00% 30 year Ginnie Mae II pools

3,957

18,395,251

—

1/12/41

5.00% (1 month USD-LIBOR)

Synthetic MBX Index 5.00% 30 year Fannie Mae pools

92,496

3,507,147

—

1/12/38

(6.50%) 1 month USD-LIBOR

Synthetic MBX Index 6.50% 30 year Fannie Mae pools

(16,013)

587,688

—

1/12/41

4.00% (1 month USD-LIBOR)

Synthetic TRS Index 4.00% 30 year Fannie Mae pools

(7,403)

364,204

—

1/12/40

5.00% (1 month USD-LIBOR)

Synthetic MBX Index 5.00% 30 year Fannie Mae pools

1,718

1,677,179

—

1/12/40

4.50% (1 month USD-LIBOR)

Synthetic MBX Index 4.50% 30 year Fannie Mae pools

13,499

6,346,745

—

1/12/41

5.00% (1 month USD-LIBOR)

Synthetic MBX Index 5.00% 30 year Fannie Mae pools

31,913

91,695

—

1/12/40

5.00% (1 month USD-LIBOR)

Synthetic MBX Index 5.00% 30 year Fannie Mae pools

432

297,494

—

1/12/40

5.00% (1 month USD-LIBOR)

Synthetic MBX Index 5.00% 30 year Fannie Mae pools

1,403

215,586

—

1/12/40

5.00% (1 month USD-LIBOR)

Synthetic MBX Index 5.00% 30 year Fannie Mae pools

1,017

10,544,577

—

1/12/38

(6.50%) 1 month USD-LIBOR

Synthetic MBX Index 6.50% 30 year Fannie Mae pools

(48,146)

2,971,606

—

1/12/39

(6.00%) 1 month USD-LIBOR

Synthetic MBX Index 6.00% 30 year Fannie Mae pools

(17,898)

1,590,558

—

1/12/39

(5.50%) 1 month USD-LIBOR

Synthetic MBX Index 5.50% 30 year Fannie Mae pools

(8,417)

795,316

—

1/12/39

(5.50%) 1 month USD-LIBOR

Synthetic MBX Index 5.50% 30 year Fannie Mae pools

(4,209)

32 American Government Income Fund

OTC TOTAL RETURN SWAP CONTRACTS OUTSTANDING at 3/31/15 (Unaudited) cont.

Swap counterparty/ Notional amount

Upfront premium received (paid)

Termination date

Payments received (paid) by fund per annum

Total return received by or paid by fund

Unrealized appreciation/ (depreciation)

Barclays Bank PLC cont.

$795,316

$—

1/12/39

(5.50%) 1 month USD-LIBOR

Synthetic MBX Index 5.50% 30 year Fannie Mae pools

$(4,209)

1,596,037

—

1/12/39

(5.50%) 1 month USD-LIBOR

Synthetic MBX Index 5.50% 30 year Fannie Mae pools

(8,446)

4,145,240

—

1/12/39

(5.50%) 1 month USD-LIBOR

Synthetic MBX Index 5.50% 30 year Fannie Mae pools

(21,935)

1,596,037

—

1/12/39

(5.50%) 1 month USD-LIBOR

Synthetic MBX Index 5.50% 30 year Fannie Mae pools

(8,446)

1,343,638

—

1/12/38

6.50% (1 month USD-LIBOR)

Synthetic TRS Index 6.50% 30 year Fannie Mae pools

12,134

3,186,596

—

1/12/39

(5.50%) 1 month USD-LIBOR

Synthetic MBX Index 5.50% 30 year Fannie Mae pools

(16,862)

1,491,165

—

1/12/41

(5.00%) 1 month USD-LIBOR

Synthetic TRS Index 5.00% 30 year Fannie Mae pools

15,436

1,017,522

—

1/12/38

(6.50%) 1 month USD-LIBOR

Synthetic MBX Index 6.50% 30 year Fannie Mae pools

(4,646)

1,204,506

—

1/12/41

5.00% (1 month USD-LIBOR)

Synthetic MBX Index 5.00% 30 year Fannie Mae pools

6,057

Citibank, N.A.

1,399,189

—

1/12/41

5.00% (1 month USD-LIBOR)

Synthetic MBX Index 5.00% 30 year Fannie Mae pools

7,035

152,144

—

1/12/41

5.00% (1 month USD-LIBOR)

Synthetic MBX Index 5.00% 30 year Fannie Mae pools

765

Credit Suisse International

383,234

—

1/12/41

5.00% (1 month USD-LIBOR)

Synthetic MBX Index 5.00% 30 year Fannie Mae pools

1,927

2,177,538

—

1/12/41

(5.00%) 1 month USD-LIBOR

Synthetic TRS Index 5.00% 30 year Fannie Mae pools

22,542

4,208,197

—

1/12/41

4.00% (1 month USD-LIBOR)

Synthetic TRS Index 4.00% 30 year Fannie Mae pools

(53,009)

2,834,266

—

1/12/44

3.50% (1 month USD-LIBOR)

Synthetic TRS Index 3.50% 30 year Fannie Mae pools

(39,108)

American Government Income Fund 33

OTC TOTAL RETURN SWAP CONTRACTS OUTSTANDING at 3/31/15 (Unaudited) cont.

Swap counterparty/ Notional amount

Upfront premium received (paid)

Termination date

Payments received (paid) by fund per annum

Total return received by or paid by fund

Unrealized appreciation/ (depreciation)

Credit Suisse International cont.

$1,051,879

$12,984

1/12/43

3.50% (1 month USD-LIBOR)

Synthetic TRS Index 3.50% 30 year Fannie Mae pools

$(1)

2,577,618

43,095

1/12/43

3.50% (1 month USD-LIBOR)

Synthetic TRS Index 3.50% 30 year Fannie Mae pools

9,788

Goldman Sachs International

2,020,779

—

1/12/38

6.50% (1 month USD-LIBOR)

Synthetic TRS Index 6.50% 30 year Fannie Mae pools

18,249

1,558,880

—

1/12/38

6.50% (1 month USD-LIBOR)

Synthetic TRS Index 6.50% 30 year Fannie Mae pools

14,078

5,411,472

—

1/12/39

6.00% (1 month USD-LIBOR)

Synthetic TRS Index 6.00% 30 year Fannie Mae pools

38,151

1,958,024

—

1/12/38

6.50% (1 month USD-LIBOR)

Synthetic TRS Index 6.50% 30 year Fannie Mae pools

17,683

5,871,151

—

1/12/41

5.00% (1 month USD-LIBOR)

Synthetic MBX Index 5.00% 30 year Fannie Mae pools

29,522

4,865,927

—

1/12/42

4.00% (1 month USD-LIBOR)

Synthetic TRS Index 4.00% 30 year Fannie Mae pools

(62,057)

4,865,927

—

1/12/42

4.00% (1 month USD-LIBOR)

Synthetic TRS Index 4.00% 30 year Fannie Mae pools

(62,057)

2,892,465

—

1/12/38

(6.50%) 1 month USD-LIBOR

Synthetic MBX Index 6.50% 30 year Fannie Mae pools

(13,207)

1,086,633

—

1/12/38

(6.50%) 1 month USD-LIBOR

Synthetic MBX Index 6.50% 30 year Fannie Mae pools

(4,961)

1,131,987

—

1/12/40

4.00% (1 month USD-LIBOR)

Synthetic TRS Index 4.00% 30 year Fannie Mae pools

(15,496)

346,993

—

1/12/39

6.00% (1 month USD-LIBOR)

Synthetic TRS Index 6.00% 30 year Fannie Mae pools

2,446

2,380,717

—

1/12/39

6.00% (1 month USD-LIBOR)

Synthetic TRS Index 6.00% 30 year Fannie Mae pools

16,784

1,540,697

—

1/12/38

(6.50%) 1 month USD-LIBOR

Synthetic MBX Index 6.50% 30 year Fannie Mae pools

(7,035)

34 American Government Income Fund

OTC TOTAL RETURN SWAP CONTRACTS OUTSTANDING at 3/31/15 (Unaudited) cont.

Swap counterparty/ Notional amount

Upfront premium received (paid)

Termination date

Payments received (paid) by fund per annum

Total return received by or paid by fund

Unrealized appreciation/ (depreciation)

Goldman Sachs International cont.

$3,962,393

$—

1/12/38

(6.50%) 1 month USD-LIBOR

Synthetic MBX Index 6.50% 30 year Fannie Mae pools

$(18,092)

1,848,851

—

1/12/38

(6.50%) 1 month USD-LIBOR

Synthetic MBX Index 6.50% 30 year Fannie Mae pools

(8,442)

146,944

—

1/12/38

(6.50%) 1 month USD-LIBOR

Synthetic MBX Index 6.50% 30 year Fannie Mae pools

(671)

391,753

—

1/12/38

(6.50%) 1 month USD-LIBOR

Synthetic MBX Index 6.50% 30 year Fannie Mae pools

(1,789)

770,644

—

1/12/38

6.50% (1 month USD-LIBOR)

Synthetic TRS Index 6.50% 30 year Fannie Mae pools

6,960

2,214,585

—

1/12/38

6.50% (1 month USD-LIBOR)

Synthetic TRS Index 6.50% 30 year Fannie Mae pools

20,000

3,205,413

—

1/12/42

4.00% (1 month USD-LIBOR)

Synthetic TRS Index 4.00% 30 year Fannie Mae pools

(40,880)

3,578,511

—

1/12/42

4.00% (1 month USD-LIBOR)

Synthetic TRS Index 4.00% 30 year Fannie Mae pools

(45,638)

3,674,247

—

1/12/39

6.00% (1 month USD-LIBOR)

Synthetic TRS Index 6.00% 30 year Fannie Mae pools

25,904

3,972,814

—

1/12/42

4.00% (1 month USD-LIBOR)

Synthetic TRS Index 4.00% 30 year Fannie Mae pools

(50,667)

2,975,949

—

1/12/41

4.00% (1 month USD-LIBOR)

Synthetic TRS Index 4.00% 30 year Fannie Mae pools

(37,487)

2,925,611

—

1/12/41

(5.00%) 1 month USD-LIBOR

Synthetic TRS Index 5.00% 30 year Fannie Mae pools

30,286

JPMorgan Chase Bank N.A.

2,691,181

—

1/12/41

4.00% (1 month USD-LIBOR)

Synthetic TRS Index 4.00% 30 year Fannie Mae pools

(33,900)

2,975,949

—

1/12/41

4.00% (1 month USD-LIBOR)

Synthetic TRS Index 4.00% 30 year Fannie Mae pools

(37,487)

2,925,228

—

1/12/41

(5.00%) 1 month USD-LIBOR

Synthetic TRS Index 5.00% 30 year Fannie Mae pools

<

30,282

Total

$56,079

$(157,751)

American Government Income Fund 35

ASC 820 establishes a three-level hierarchy for disclosure of fair value measurements. The valuation hierarchy is based upon the transparency of inputs to the valuation of the fund’s investments. The three levels are defined as follows:

Level 1: Valuations based on quoted prices for identical securities in active markets.

Level 2: Valuations based on quoted prices in markets that are not active or for which all significant inputs are observable, either directly or indirectly.

Level 3: Valuations based on inputs that are unobservable and significant to the fair value measurement.

The following is a summary of the inputs used to value the fund’s net assets as of the close of the reporting period:

Valuation inputs

Investments in securities:

Level 1

Level 2

Level 3

Mortgage-backed securities

$—

$118,082,709

$—

Purchased options outstanding

—

328,326

—

Purchased swap options outstanding

—

6,263,027

—

U.S. government and agency mortgage obligations

—

420,498,685

—

U.S. treasury obligations

—

152,175,189

—

Short-term investments

107,590,969

72,792,796

—

Totals by level

$107,590,969

$770,140,732

$—

Valuation inputs

Other financial instruments:

Level 1

Level 2

Level 3

Futures contracts

$1,152,458

$—

$—

Written options outstanding

—

(170,085)

—

Written swap options outstanding

—

(3,929,407)

—

Forward premium swap option contracts

—

(11,949)

—

TBA sale commitments

—

(123,248,281)

—

Interest rate swap contracts

—

(3,033,738)

—

Total return swap contracts

—

(213,830)

—

Totals by level

$1,152,458

$(130,607,290)

$—

During the reporting period, transfers within the fair value hierarchy, if any, did not represent, in the aggregate, more than 1% of the fund’s net assets measured as of the end of the period.

The accompanying notes are an integral part of these financial statements.

36 American Government Income Fund

Statement of assets and liabilities 3/31/15 (Unaudited)

Receivable for sales of delayed delivery securities (Note 1)

66,525,017

Receivable for variation margin (Note 1)

2,010,289

Unrealized appreciation on forward premium swap option contracts (Note 1)

202,550

Unrealized appreciation on OTC swap contracts (Note 1)

704,522

Prepaid assets

73,147

Total assets

954,783,215

LIABILITIES

Payable to custodian

35,541

Payable for investments purchased

5,461,063

Payable for purchases of delayed delivery securities (Note 1)

276,015,973

Payable for shares of the fund repurchased

1,079,528

Payable for compensation of Manager (Note 2)

176,011

Payable for custodian fees (Note 2)

18,881

Payable for investor servicing fees (Note 2)

137,216

Payable for Trustee compensation and expenses (Note 2)

259,068

Payable for administrative services (Note 2)

1,898

Payable for distribution fees (Note 2)

315,493

Payable for variation margin (Note 1)

2,137,160

Unrealized depreciation on OTC swap contracts (Note 1)

862,273

Premium received on OTC swap contracts (Note 1)

56,079

Unrealized depreciation on forward premium swap option contracts (Note 1)

214,499

Written options outstanding, at value (premiums $6,224,875) (Notes 1 and 3)

4,099,492

TBA sale commitments, at value (proceeds receivable $122,734,160) (Note 1)

123,248,281

Collateral on certain derivative contracts, at value (Note 1)

2,889,000

Other accrued expenses

140,863

Total liabilities

417,148,319

Net assets

$537,634,896

REPRESENTED BY

Paid-in capital (Unlimited shares authorized) (Notes 1 and 4)

$560,135,375

Undistributed net investment income (Note 1)

7,198,829

Accumulated net realized loss on investments (Note 1)

(44,365,971)

Net unrealized appreciation of investments

14,666,663

Total — Representing net assets applicable to capital shares outstanding

$537,634,896

(Continued on next page)

The accompanying notes are an integral part of these financial statements.

American Government Income Fund 37

Statement of assets and liabilities (Continued)