Exhibit D

Republic of Panama

This description of the Republic of Panama is dated as of September 27, 2004 and appears as Exhibit D to the Republic of Panama’s Annual Report on Form 18-K to the U.S. Securities and Exchange Commission for the fiscal year ended December 31, 2003.

TABLE OF CONTENTS

| | |

| | | Page

|

Recent Developments | | D-2 |

The Republic of Panama | | D-7 |

The Panamanian Economy | | D-11 |

Structure of the Panamanian Economy | | D-26 |

The Panama Canal | | D-38 |

The Colón Free Zone | | D-43 |

Employment and Labor | | D-44 |

Public Finance | | D-49 |

Financial System | | D-55 |

Foreign Trade and Balance of Payments | | D-62 |

Public Sector Debt | | D-69 |

Tables and Supplementary Information | | D-75 |

The fiscal year of the Government of the Republic of Panama (the “Government”) ends on December 31. The twelve-month period ended December 31, 2003 is referred to in this description of the Republic of Panama as “2003” and other years are referred to in a similar manner unless otherwise indicated. All references to “$” or “dollars” are to United States Dollars.

Totals in certain tables in this description of the Republic of Panama may differ from the sum of the respective individual items in such tables due to rounding.

INDEX OF TABLES

| | | | |

| | | | | Page

|

Table No. 1 – | | Selected Panamanian Economic Indicators | | D-6 |

Table No. 2 – | | Inflation | | D-21 |

Table No. 3 – | | Gross Domestic Product | | D-22 |

Table No. 4 – | | Sectoral Origin of Gross Domestic Product | | D-23 |

Table No. 5 – | | Percentage Change from Prior Year for Sectoral Origin of Gross Domestic Product | | D-24 |

Table No. 6 – | | Sectoral Origin of Gross Domestic Product | | D-25 |

Table No. 7 – | | Selected State-Owned Enterprises 2003 Financial Statistics | | D-28 |

Table No. 8 – | | Selected Completed Privatizations and Concessions | | D-35 |

Table No. 9 – | | Panama Canal Principal Statistics | | D-38 |

Table No. 10 – | | Labor Force and Employment | | D-45 |

Table No. 11 – | | Average Real Monthly Wages | | D-47 |

Table No. 12 – | | Expenditures of the Central Government by Function | | D-50 |

Table No. 13 – | | Central Government Operations | | D-52 |

Table No. 14 – | | Consolidated Non-Financial Public Sector Operations | | D-53 |

Table No. 15 – | | International Reserves | | D-54 |

Table No. 16 – | | Largest Banking Institutions | | D-56 |

Table No. 17 – | | The Banking Sector | | D-57 |

Table No. 18 – | | Banco Nacional de Panama Balance Sheet | | D-60 |

Table No. 19 – | | Composition of Merchandise Exports, F.O.B. | | D-64 |

Table No. 20 – | | Composition of Merchandise Imports, C.I.F. | | D-65 |

Table No. 21 – | | Direction of Merchandise Trade | | D-66 |

Table No. 22 – | | Balance of Payments | | D-68 |

Table No. 23 – | | Public Sector Internal Debt | | D-70 |

Table No. 24 – | | Public Sector External Debt | | D-71 |

Table No. 25 – | | Public Sector External Debt Amortization | | D-71 |

Table No. 26 – | | External Direct Debt of the Republic, Central Government | | D-75 |

Table No. 27 – | | External Debt Guaranteed by the Republic, Decentralized Institutions | | D-76 |

Table No. 28 – | | Internal Securities Debt of the Republic Outstanding on December 31, 2003 | | D-77 |

D-1

RECENT DEVELOPMENTS

Government

Mireya Moscoso (“Moscoso”) completed her term as the President of Panama on August 31, 2004. National elections were held on May 2, 2004, in which seven political parties participated. Martin Torrijos (“Torrijos”), leader of the Partido Revolucionario Democrático (“PRD”), was elected president for a five-year term with 47.4% of the vote, and took office on September 1, 2004. Torrijos’ coalition, consisting of the PRD and the Partido Popular (“PP”), won a majority of the 78 seats available in the National Assembly, with the PRD and the PP securing 38 and 3 seats, respectively. The Partido Arnulfista (“PA”) secured 17 seats and the Partido Solidaridad (“Solidarity Party”) secured 20 seats.

Torrijos has announced that under his initial development plan, Alianza para la Patria Nueva (or “Alliance for a New Country”), he intends to pursue wide-ranging reforms, including reforms to the Constitution, fiscal system, public sector and judiciary. Before assuming office, Torrijos also pledged to seek enhancements in consumer protection, to combat corruption and to promote sustainable economic and human development.

The Economy

Panama’s economy grew in virtually all sectors in the first and second quarters of 2004 compared to the same respective periods of 2003. Panama’s gross domestic product (“GDP”) registered a real increase of 6.7% in the first quarter of 2004 and 6.8% in the second quarter of 2004 compared to the same respective periods of 2003. Inflation, as measured by the consumer price index (“CPI”), was 1.5% in the first quarter and 2.0% in the second quarter of 2004.

In the first quarter of 2004, the primary sector grew 12.7% compared to the same period of 2003. In particular, the agriculture sector grew 6.7% in the first quarter of 2004 compared to the same period of 2003. This increase is primarily attributable to a growth in melon, pineapple and tuna exports. The transportation and telecommunications sector grew by 8.9% in the first quarter of 2004 compared to the same period of 2003, with particular growth in port activities due to an increase in the movement of containers, particularly those destined for China. Mining activities increased 26.1% in the first quarter of 2004 compared to the same period of 2003 due to the increased levels of construction activity. The construction industry grew by 26.6% in the first quarter of 2004 compared to the same period of 2003 due to low mortgage rates and a number of large construction projects, in both the private and public sectors, that are still underway. Activities of the Colón Free Trade Zone (or the “CFZ”) increased 13.2% in the first quarter of 2004 compared to the same period of 2003. This increase is primarily attributable to the economic recovery of the region. Panama Canal activities grew 6.8% in the first quarter of 2004 compared to the same period of 2003 due to an increase in canal traffic and volume of cargo. The manufacturing sector grew 1.1% in the first quarter of 2004 compared to the same period of 2003, due in part to an increase in the production of alcoholic beverages. The only sector that declined was the financial intermediation sector, which fell 1.4% in the first quarter of 2004 compared to the same period of 2003. This decrease is attributable to a reduction in external credit.

The sectors principally responsible for growth in the second quarter of 2004 were construction; transportation and telecommunications; the Colón Free Zone (“CFZ”); and electricity and water. The construction industry grew by 17.0% in the second quarter of 2004 compared to the same period of 2003, reflecting a substantial increase in the number of construction permits granted for construction projects in the private and public sectors. The transportation and telecommunications sector grew by 9.7% in the second quarter of 2004 compared to the same period of 2003, with particular growth in port and Panama Canal activities. Port activities grew by 17.1% for the same period due to an increase in the movement of containers, and Panama Canal activities grew by 13.2% for the same period due to an increase in the movement of containers and commercial cargo, particularly petroleum and petroleum products which are growing in demand in the United States. In the second quarter of 2004, activities of the CFZ experienced an increase of 23.0% compared to the same period of 2003, due in part to growth in international commerce and increased activity in the CFZ of petroleum-producing countries such as Ecuador, Venezuela and Colombia. The electricity and water sector grew by 21.9% in the second quarter of 2004 compared to the same period of 2003, reflecting an increase in government, residential and commercial hydroelectric consumption and an increase in water production. The only sector that declined was the fisheries sector, which dropped 6.6% in the second quarter of 2004 compared to the same period of 2003. This decline is attributable to a reduction in exports of fish, shrimp, fish oil and fishmeal.

Panama’s net exports of goods and services rose by 11.3% in the first quarter of 2004 and 13.7% in the second quarter of 2004 compared to the same respective periods of 2003. Import figures for 2004 are not yet available.

The current account with respect to operations of the Central Government registered a deficit of $440.1 million (or 3.2% of nominal GDP) in the first half of 2004, compared to a deficit of $266.7 million (or 2.0% of nominal GDP) in the first quarter of 2004 and a deficit of $395.1 million (or 3.1% of nominal GDP) in the first half of 2003. In the first half of 2004, Panama’s non-financial public sector balance registered a deficit of approximately $218.7 million (or 1.6% of nominal GDP), up from $155.0 million (or 1.1% of nominal GDP) in the first quarter of 2004, but down from $292.7 million (or 2.3% of nominal GDP) in the first half of 2003.

The Torrijos administration is currently reviewing the methodology used by the former Government to calculate the non-financial public sector deficit. On September 10, 2004, the Minister of Economy and Finance issued a press release with a non-financial public sector deficit estimate for 2004 of $700.0 million (or approximately 5.3% of nominal GDP). On September 15, 2004, the Minister of Economy and Finance announced a number of measures to limit the non-financial public sector deficit for 2004, including austerity measures to reduce government expenditures for electricity, insurance, transportation and telecommunications. Additionally, the Government has requested the Assembly to suspend in fiscal years 2004 and 2005 the mandate, set forth in Law No. 20 of May 7, 2002 (the “Fiscal Responsibility Law”), that the annual fiscal deficit not exceed 2% of GDP.

The National Assembly approved the 2004 budget on November 17, 2003. The 2004 budget contemplates total expenditures of $6.003 billion, with budget estimates based on an anticipated 3.0%

D-2

growth in real GDP and an anticipated consolidated non-financial public sector deficit of approximately $250 million (or approximately 2.0% of nominal GDP) for 2004.

There were no privatizations in 2003 or in the first half of 2004. Due to the absence of competitive bids, the effort to privatize Panama City’s Convention Center was terminated pursuant to Resolution No. 20 of February 13, 2004.

Law No. 41 of July 20, 2004 created a special economic zone at the former U.S. military base of Fort Howard in the district of Arraijan and established an independent agency responsible for administering the zone. The Area Económica Especial Panamá-Pacifico (“AEEPP”) is intended to attract foreign investment and to create jobs by granting preferential tax treatment to businesses involved in such areas as technology, airline repair and maintenance, maritime cargo and transportation logistics. The AEEPP is not expected to compete with the CFZ as a result of a prohibition in the legislation on the importation into and reexportation out of the AEEPP of finished products.

As of June 30, 2004, Panama’s external debt was equal to $6.639 billion, up from $6.504 billion as of December 31, 2003. The ratio of external debt to nominal GDP as of June 30, 2004 was 48.0%. Panama’s total public sector debt as of June 30, 2004 was $9.009 billion, up from $8.661 billion as of December 31, 2003.

On January 21, 2004, Panama launched an offer to purchase (“Offer to Purchase”) outstanding Brady Bonds, which offer was financed by a further issuance on February 3, 2004 of $326 million of its 9.375% Global Bonds Due 2023, of which $430 million principal amount had been previously issued and are outstanding. Pursuant to the settlement of the Offer to Purchase, which occurred on February 3, 2004, Panama repurchased approximately $406 million aggregate original principal amount of Brady Bonds, of which there were approximately $177 million aggregate original principal amount of Past-Due Interest Bonds Due 2016 (“PDIs”), approximately $221 million aggregate original principal amount of Interest Reduction Bonds Due 2014 (“IRBs”), approximately $5.5 million aggregate original principal amount of Par Bonds Due 2026 (“Par Bonds”) and approximately $2.5 million aggregate original principal amount of Discount Bonds Due 2026 (“Discount Bonds”). The consummation of the Offer to Purchase yielded a nominal net reduction of $57.0 million in Panama’s public sector debt balance and reduced the balance of outstanding Brady Bonds to $379.5 million aggregate original principal amount. As of June 30, 2004, outstanding Brady Bonds totaled $378.2 million, consisting of approximately $221.2 million aggregate principal amount of PDIs, approximately $134.1 million aggregate principal amount of IRBs, approximately $9.7 million aggregate principal amount of Par Bonds, and approximately $13.1 million aggregate principal amount of Discount Bonds. On January 28, 2004, Panama issued $250 million aggregate principal amount of its 8.125% Global Bonds Due 2034 containing collective action clauses. See “Public Sector Debt – Global Notes and Bonds.”

On August 19, 2004, the Government of Panama and the U.S. Government signed a debt-for-nature swap agreement, pursuant to which Panama and the United States agreed to restructure debt, aggregating approximately $9.4 million principal amount, owed by Panama to the United States in return for Panama’s commitment to fund, through 2016, a trust devoted to forest conservation activities in Panama’s Darién National Park. This follows a similar debt-for-nature swap agreement that Panama and the United States signed on July 10, 2003, pursuant to which the two countries agreed to restructure other debt owed by Panama to the United States in exchange for Panama’s commitment to fund, through 2016, a trust for conservation activities in Panama’s Chagres National Park. Under the 2003 debt-for-nature swap, approximately $16.1 principal amount million of debt was restructured.

In an effort to promote the development of Panama’s capital markets, the Government initiated, in July 2002, a program of Treasury Note issuances in the local market. In seven monthly auctions ending on February 4, 2003, Panama issued $250 million of 7.25% Treasury Notes due 2005; in ten monthly auctions from March 11, 2003 to December 2, 2003, Panama issued almost $250 million of 6.75% Treasury Notes due 2007. The Government completed its 2003 financing following the June 2003 auction, and proceeds from subsequent auctions in 2003 were used for debt management operations. In nine monthly auctions from January 13, 2004 to September 7, 2004, the Government issued $166.7 million of 5.25% Treasury Notes due 2009. Proceeds from monthly Treasury Note auctions through December 2004 will be allocated to the Government’s 2004 financing needs. In nine monthly auctions from January 20, 2004 to September 21, 2004,

D-3

Panama issued $250 million of zero-coupon Treasury Bills with six- and twelve-month maturities in Panama’s capital markets.

Law No. 4 of January 16, 2004 authorized the early retirement of certain qualifying teachers and is estimated to cost the Complementary Pension Fund for Civil Servants $18 million in 2005. The Complementary Pension Fund for Civil Servants is administered by Caja de Seguro Social, Panama’s social security agency.

International Trade

Panama is negotiating a bilateral trade agreement with the Dominican Republic that will enter into force after each country has ratified a negotiated list of products to be included in the agreement. Panama is currently negotiating similar bilateral protocols with each of Guatemala, Honduras, Costa Rica and Nicaragua. On August 21, 2003, Panama signed a free trade agreement with Taiwan. The agreement, which took effect on January 1, 2004, was ratified by Taiwan’s legislature on October 1, 2003 and by Panama’s National Assembly on October 13, 2003. Under the agreement, 95% of import tariffs will be phased out over 10 years. In July 2004, Panama concluded a second round of free trade negotiations with Singapore, which negotiations began in February 2004.

On November 18, 2003, the United States Trade Representative notified the United States Congress of his intent to initiate free trade negotiations with the Republic of Panama. Negotiations with the United States began in the second quarter of 2004 on a comprehensive agreement. Total trade between the two countries reached approximately $2.1 billion in 2003.

The Cabinet, by Decree No. 11 dated April 7, 2004, approved the elimination of import tariffs on certain raw and intermediate materials, such as linseed, corrugated steel bars and support rods for concrete, although the national 5% value-added tax on goods and services will continue to be assessed on such products at their time of entry into Panama.

IMF Relationship

Panama’s most recent standby agreement with the International Monetary Fund (“IMF”) expired in March 2002. The IMF and Government representatives met in April 2002, and the IMF concluded an Article IV review of Panama in July 2002. During 2002, the Government maintained ongoing conceptual discussions with the IMF about a possible new standby facility, but no such facility was arranged. In November 2003, the IMF initiated its most recent Article IV review of Panama and concluded such review in March 2004.

The Panama Canal

The Panama Canal Authority announced that total revenues for the quarter ending June 30, 2004 were $192.7 million, an increase of 18.1% over the same period in 2003. The increase is in part attributable to an increase in tonnage flow and increased movement of crude oil due to economic demand.

Toll revenues for fiscal year 2003 reached $666.0 million, an increase of 13.1% over fiscal year 2002. Toll revenues for fiscal year 2002 were $588.8 million, an increase of 1.6% over fiscal year 2001. In July 2002, the Panama Canal Authority announced changes to its tolls structure. The first phase of the changes (implemented in October 2002) raised tolls by an average of 8% and the second phase (implemented in July 2003) raised tolls by an average of 4.5%, with actual toll fees based on vessel type and tonnage, and a fee for locomotive usage based on the number of locomotive cables required. Currently, there is no toll increase programmed for fiscal years 2004 and 2005; however, in early 2004, tariffs for transit-related services such as reservations, towing and line handling were revised upward to reflect the rising cost associated with providing such services.

The Canal investment plan for fiscal years 2004 through 2006 contemplates investments of more than $497 million, and includes such projects as deepening and widening of the Gaillard Cut, the Gatun Lake and the Pacific and Atlantic entrances of the Canal; acquisition of tugboats and towing locomotives; rehabilitation of railways for towing locomotives; and an increase in the capacity of the potable water system. Discussions also have begun with regard to the construction of a third set of locks that will accomodate vessels too large to currently traverse the Canal. On July 3, 2003 and August 10, 2004, the National Assembly approved the Panama Canal

D-4

Authority’s budgets for fiscal years 2004 and 2005, respectively. The fiscal 2004 and 2005 budgets allocate $209.4 million and $190.7 million, respectively, to the Canal’s investment plan.

On May 13, 2004, the Panama Canal Authority’s Industrial Shipyard Division announced plans to construct a new barge built entirely in Panama. The assembly of the barge is part of the Canal’s investment plan and is expected to begin operating in February 2005. The new barge will facilitate projects, such as deepening Gatun Lake and widening the Gaillard Cut, that are intended to increase Canal capacity. Approximately $14.8 million is budgeted for the assembly of the barge.

On August 15, 2004, the span of the second bridge over the Panama Canal was completed at a total cost of $104.1 million, and work on the feeder roads continued.

D-5

TABLE NO. 1

Selected Panamanian Economic Indicators(1)

The following table sets forth Panama’s principal economic indicators for the years 1999 through 2003:

| | | | | | | | | | | | | | | | | | | | |

| | | 1999(R)

| | | 2000(R)

| | | 2001(R)

| | | 2002(R)

| | | 2003(E)

| |

Economic Data: | | | | | | | | | | | | | | | | | | | | |

GDP (millions, current dollars)(2) | | $ | 11,456 | | | $ | 11,621 | | | $ | 11,808 | | | $ | 12,216 | (P) | | $ | 12,888 | |

GDP (millions, constant dollars)(3) | | $ | 11,071 | | | | 11,375 | | | $ | 11,440 | | | $ | 11,697 | (P) | | $ | 12,172 | |

GDP (% change, constant dollars)(3) | | | 4.0 | % | | | 2.7 | % | | | 0.6 | % | | | 2.2 | %(P) | | | 4.1 | % |

Service Sector (% change, constant dollars)(3)(4) | | | 3.0 | % | | | 6.3 | % | | | 1.8 | % | | | 2.1 | % | | | 3.4 | % |

Other (% change, constant dollars)(3)(5) | | | 7.3 | % | | | (0.2 | )% | | | (5.5 | )% | | | (1.8 | )% | | | 6.0 | % |

Population (millions) | | | 2.81 | | | | 2.85 | | | | 2.90 | | | | 3.06 | | | | 3.12 | |

CPI (% change)(6) | | | 1.4 | % | | | 1.4 | % | | | 0.3 | % | | | 1.0 | % | | | 1.4 | % |

Unemployment | | | 11.8 | % | | | 13.5 | % | | | 14.0 | % | | | 13.5 | % | | | 12.8 | % |

Public Finance: | | | | | | | | | | | | | | | | | | | | |

Total Consolidated Non-Financial Public Sector Revenues (millions) | | $ | 2,802 | | | $ | 3,007 | | | $ | 3,014 | | | $ | 2,963 | | | $ | 2,995 | |

Total Consolidated Non-Financial Public Sector Expenditures (millions)(7) | | $ | 2,613 | | | $ | 2,587 | | | $ | 2,685 | | | $ | 2,764 | | | $ | 2,770 | |

Overall Surplus (Deficit)(millions) | | $ | (138 | ) | | $ | 54 | | | $ | (79 | ) | | $ | (244 | ) | | $ | (247 | ) |

As % of Current GDP(2) | | | (1.2 | )% | | | 0.5 | % | | | (0.7 | )% | | | (2.0 | )% | | | (1.9 | )% |

Central Government Surplus (Deficit) (millions) | | $ | (228 | ) | | $ | (128 | ) | | $ | (200 | ) | | | (238 | ) | | $ | (321 | ) |

As % of Current GDP(2) | | | (2.0 | )% | | | (1.1 | )% | | | (1.7 | )% | | | (1.9 | )% | | | (2.5 | )% |

Public Debt (at December 31): | | | | | | | | | | | | | | | | | | | | |

Internal Debt (millions) | | $ | 2,216 | | | $ | 2,128 | | | $ | 2,138 | | | $ | 2,172 | | | $ | 2,158 | |

External Debt (millions) | | $ | 5,568 | | | $ | 5,604 | | | $ | 6,263 | | | $ | 6,349 | | | $ | 6,504 | |

Total Public Debt (millions) | | $ | 7,784 | | | $ | 7,732 | | | $ | 8,401 | | | $ | 8,521 | | | $ | 8,661 | |

Public Debt (as % of Current GDP)(2) | | | | | | | | | | | | | | | | | | | | |

Internal Debt | | | 19.3 | % | | | 18.3 | % | | | 18.1 | % | | | 17.8 | % | | | 16.7 | % |

External Debt | | | 48.6 | % | | | 48.2 | % | | | 53.0 | % | | | 52.0 | % | | | 50.5 | % |

Trade Data: | | | | | | | | | | | | | | | | | | | | |

Exports (f.o.b.) Goods (millions)(8) | | $ | 5,288 | | | $ | 5,839 | | | $ | 5,992 | | | $ | 5,315 | | | $ | 5,051 | |

Imports (c.i.f.) Goods (millions)(8) | | $ | (6,628 | ) | | $ | (6,981 | ) | | $ | (6,689 | ) | | $ | (6,352 | ) | | $ | (6,143 | ) |

Merchandise Trade Balance (millions) | | $ | (1,340 | ) | | $ | (1,143 | ) | | $ | (696 | ) | | $ | (1,037 | ) | | $ | (1,092 | ) |

Current Account Surplus (Deficit) (millions) | | $ | (1,159 | ) | | $ | (689 | ) | | $ | (174 | ) | | $ | (92 | ) | | $ | (408 | ) |

Overall Balance of Payments Surplus (Deficit) (millions)(9) | | $ | 191 | | | $ | (77 | ) | | $ | 644 | | | $ | 60 | | | $ | (153 | ) |

Total Official Reserves (millions, at December 31)(10) | | $ | 838 | | | $ | 904 | | | $ | 1,156 | | | $ | 1,211 | | | $ | 1,005 | |

| (1) | All monetary amounts in millions of U.S. dollars at current prices, unless otherwise noted. |

| (2) | Nominal GDP figures reflect a revised base year of 1996. |

| (3) | Constant GDP figures are based on 1996 constant dollars. See “The Panamanian Economy—Economic Performance—1999 Through 2003.” |

| (4) | Including real estate, public administration, commerce, hotels and restaurants, financial services, the CFZ, Panama Canal, transportation and communications and public utilities. |

| (5) | Including manufacturing, agriculture and construction. |

| (7) | Excluding external interest. |

| (9) | Figures were calculated pursuant to the V Version of the Balance of Payments Manual prepared by the IMF. |

| (10) | See “Public Finance—International Reserves” for components. |

Sources: Directorate of Analysis and Economic Policies (as of May 31, 2003), Office of the Comptroller General, Banco Nacional de Panama (“BNP”) and Ministry of Economy and Finance.

D-6

THE REPUBLIC OF PANAMA

Area and Population

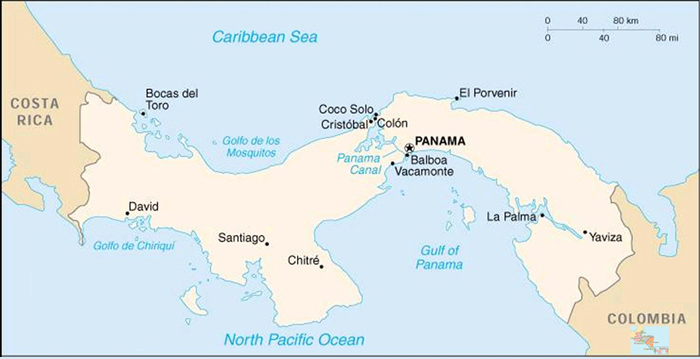

Panama is a republic located on the narrowest point of the Central American isthmus, which connects the continents of North America and South America. It has a coastline of approximately 1,868 miles on the Caribbean Sea and Pacific Ocean, and is bordered on the east by Colombia and on the west by Costa Rica. Panama has a national territory of approximately 29,157 square miles situated within its coastline and 345 miles of land borders, and includes numerous coastal islands. The Panama Canal, one of the most important commercial waterways in the world, which connects the Atlantic and Pacific Oceans, bisects the country running northwest to southeast. Panama’s climate is primarily tropical.

As of December 31, 2003, Panama had an estimated population of 3.12 million and a population density of 107.0 people per square mile. During the period 1999-2003, the population grew by an average of 2.7% per annum. Approximately 63.3% of Panama’s population lives in cities and towns with more than 1,500 inhabitants, and 10% of the population is indigenous, some of whom are seeking greater autonomy from the Government. Of the Panamanian population, 30.7% is under 15 years of age, 63.5% is between the ages of 15 and 64, and 5.8% is over the age of 65. Average life expectancy in Panama is 74.7 years. The infant mortality rate is estimated at 20.6 per 1,000 births. Panama’s official language is Spanish.

Panama’s per capita GDP for 2003, expressed in 1996 constant prices, was approximately $3,906. Education indicators show that Panama’s adult literacy rate is approximately 92.3%. During the period 1999-2003, the Government spent an average of 4.4% of GDP and 24.5% of Central Government expenditures on education. Estimates show that 40.5% of the population is considered to be living in poverty (which is defined as annual expenditure per capita below $905) while 26.5% is considered to be living in extreme poverty (annual expenditure per capita below $519).

Panama City, Panama’s capital and its largest city, is the political, financial, commercial, communications and cultural center of Panama. Panama City’s population is estimated to comprise 14.0% of Panama’s total population. Other principal cities are San Miguelito, a suburb of Panama City (estimated to comprise 10.5% of the total population), and Colón, located at the northern terminus of the Panama Canal (estimated to comprise 1.2% of the total population).

Historical Information

Panama gained its independence from Spain in 1821 and subsequently joined the Confederation of Greater Colombia, from which Panama declared its independence on November 3, 1903. Several weeks after independence, Panama signed the Hay/Bunau-Varilla Treaty with the United States (“U.S.”), which, among other things, granted the U.S. the right to occupy a ten-mile wide zone and a concession for the construction, maintenance, operation and protection of the Panama Canal (the “Canal Zone”). See “The Panama Canal—General.”

Panama adopted its first constitution in 1904, and, between 1904 and 1968, Panama generally experienced social and political stability and economic growth under a constitutional democracy. During the period immediately following World War II, the Panamanian military interfered with the civilian government, although this interference largely ended by the mid-1950s. Constitutional government continued until October 1968, when the National Guard successfully mounted a military coup and replaced the civilian government. Although the military made nominal efforts during the late 1970s to return to civilian government, the military generally remained in control of the Government until 1989.

Issues related to control of the Panama Canal and the Canal Zone caused considerable unrest in Panama. In 1977, following 13 years of negotiations, Panama signed treaties with the U.S. that provided

D-7

for abolishing the Canal Zone in 1979 and the eventual turnover of the Panama Canal to Panama in 1999. See “The Panama Canal—The Canal Treaty of 1977.”

In 1983, General Manuel Antonio Noriega (“Noriega”) became Commander of the National Guard and assumed effective control of the Government. In the spring of 1987, a political crisis galvanized Noriega opponents and resulted in the formation of a major civilian protest and opposition movement widely supported by civilian organizations, political parties and the business community. This political crisis evoked an economic crisis as well.

In response to the ensuing political crisis, in March 1988, the U.S. suspended its Agency for International Development (“AID”) programs to Panama and blocked preferential sugar quotas, causing further economic disruption. The U.S. imposed additional economic sanctions that year, including a freeze on all U.S. payments for the Panama Canal (at that time, approximately $6 million per month), an order prohibiting American citizens and companies from making payments to the Government and a freeze on all Government accounts (and certain additional assets) in the U.S.

In December 1989, relations between Panama and the U.S. deteriorated, culminating in a U.S. military intervention that resulted in the removal of Noriega. Guillermo Endara (“Endara”), who had been elected by a significant majority of the popular vote earlier in the year, was subsequently sworn in as President.

Since the end of 1989, Panama has enjoyed political and economic stability under democratically elected governments. Relations with the U.S. have been fully restored. Endara finished his presidential term, and in the spring of 1994, orderly national elections were held. Ernesto Pérez Balladares (“Pérez Balladares”), who was elected President with 33% of the vote in May 1994, finished his presidential term in August 1999. Mireya Moscoso, who was elected with 44.8% of the vote in May 1999, took office on September 1, 1999 and completed her presidential term on August 31, 2004. On May 2, 2004, Martin Torrijos was elected President. He took office on September 1, 2004.

The Panamanian military was disbanded in 1990, and, in 1994, by constitutional amendment, the military was abolished. Costa Rica, Panama’s western neighbor, also does not have a military. If Panama were attacked by a foreign force and the neutrality of the Panama Canal were jeopardized, the U.S. would have the right under treaties related to the Panama Canal to take measures to protect the neutrality of the Canal. The national police force of Panama also has certain defensive capabilities.

Form of Government and Political Parties

Panama is a republic with a representative form of government. In 1972, the original version of the current Constitution was adopted (the fourth in Panama’s history), setting forth the structure of the Government, individual and collective rights and duties, and the division of powers among the executive, legislative and judicial branches.

Executive power is vested in the President and the presidentially appointed Ministers, who constitute the Cabinet. The President, the First Vice-President and the Second Vice-President are each elected by direct, universal suffrage for a term of five years. The President and Vice-Presidents may not be reelected to the same office within ten years after the expiration of their term. In the event the President is unable to finish a term, the First Vice-President would succeed to the presidency.

National legislative power is vested in the National Assembly (“Assembly”), Panama’s unicameral legislative body. The number of electoral circuits, each comprising between 20,000 and 40,000 persons, determines the number of legislators; as of December 31, 2003, the Assembly consisted of 71 members. The full Assembly is elected by universal suffrage every five years. Members of the Assembly are not subject to limits on the number of terms in office to which they may be elected. The Assembly has, among other powers, the power to enact legislation, ratify treaties, approve the budget and ratify the appointment of the Comptroller General, the Attorney General and justices of the Supreme Court of Justice

D-8

(the “Supreme Court”). To be enacted, legislation must be approved after three separate readings by a majority of all legislators or by a majority of legislators present at the session, depending on the substance of the legislation being enacted. The President may veto bills adopted by the Assembly, but the Assembly may override presidential vetoes by a vote of two-thirds of its members. Pursuant to the Constitution, the Assembly may empower the President and the Cabinet to adopt legislation when the Assembly is not in session. The Assembly has the power to amend the Constitution. Amendments to the Constitution may be adopted either by a majority vote of all legislators in two different Assemblies or by a majority vote of all legislators in two sessions of the same Assembly and a public referendum.

In the 1999 national elections, during which Moscoso was elected president, twelve political parties participated. A seven-party coalition led by the PA won 36 of 71 seats in the Assembly (18 of such seats were held by PA members). This coalition was formed to support the legislative agenda of the Moscoso administration. The PRD won 34 seats in the 1999 elections, and the PRD has generally functioned in opposition to the PA’s coalition. On September 1, 2000, the PRD gained a majority in the Assembly when two legislators from the Christian Democratic Party and one legislator from the Solidarity Party joined the PRD. However, on September 1, 2002, the Moscoso coalition regained a working majority in the Assembly when five members of the PRD voted with the coalition on key economic issues. As of December 31, 2003, of the 71 seats then comprising the Assembly, the Moscoso coalition held 40, with the remaining 31 held by the PRD.

The most recent national elections, in which seven political parties participated, were held on May 2, 2004. Martin Torrijos, leader of the PRD, was elected president for a five-year term with 47.4% of the vote. Historically, there have been few material ideological differences among the significant political parties in Panama. To some extent, the PRD has tended to enjoy more support in urban areas while the PA has had more rural support. However, the primary distinctions among political parties have tended to be associated with the personalities involved in their leadership.

The next elections for President and the Assembly are scheduled for May 2009. Currently, there are constitutional provisions prohibiting the reelection of a president within ten years after the expiration of his or her term. The Moscoso administration, which served until August 31, 2004, oversaw the remaining reversion of facilities in the former Canal Zone, and, at the end of 1999, the return of the Canal itself to Panama under the 1977 Panama Canal treaties with the U.S. See “The Panama Canal.”

Judicial power is vested in the Supreme Court and various lower tribunals. The President appoints the nine justices of the Supreme Court for staggered ten-year terms, with two justices being selected every two years, subject to ratification by the Assembly. Lower court judges are appointed by the Supreme Court. The judicial branch prepares its own budget and sends it to the executive branch for inclusion in the general budget presented to the Assembly for approval. The Supreme Court is the final court of appeal and has the power to declare null and void laws, regulations or other acts of the executive or legislative branches that conflict with the Constitution.

Panama is administratively divided into nine provinces and three territories. In each province, executive power is exercised by a governor who is appointed by the President. There are no provincial legislative or judicial bodies. Provincial governments do not have their own independent budgets. Within each province are municipalities that are, in turn, divided into precincts. Each municipality has a municipal council and a mayor, who exercises executive power. Mayors and members of municipal councils are elected by direct, universal suffrage for five-year terms. Municipalities levy and collect municipal taxes and adopt their own budgets for financing local projects.

Foreign Affairs and International Organizations

Panama maintains diplomatic relations with 123 countries. Panama is a charter member of the United Nations (“U.N.”) and a member of various other international organizations, including the IMF and the Inter-American Development Bank (“IDB”). Panama is a founding member of the Organization of American States and is also a member of the International Bank for Reconstruction and Development (“World Bank”) and the World Bank affiliates, the International Finance Corporation (“IFC”) and the

D-9

Multilateral Investment Guaranty Agency (“MIGA”), as well as a member of the San José Pact. On October 2, 1996, Panama signed the World Trade Organization (“WTO”) accession protocol and submitted it to the Assembly for ratification. On June 18, 1997, the Assembly ratified the WTO accession protocol, and shortly thereafter the protocol was signed by the President. Panama’s WTO membership became effective on September 6, 1997.

Panama consults with various international agencies, such as the IDB, the World Bank and the IMF, regarding its economic program, objectives, projections and policies. In recent years, Panama has utilized the IDB, the World Bank and the IMF for significant external financing. See “Public Sector Debt—External Debt.”

D-10

THE PANAMANIAN ECONOMY

General

Panama’s unique geographic position, service economy (including the Panama Canal) and monetary regime anchored on the use of the U.S. dollar as legal tender are major factors in Panama’s economic performance.

Panama has used the U.S. dollar as its legal tender since shortly after gaining its independence. The national currency, the Balboa, is used primarily as a unit of account linked to the U.S. dollar at a ratio of one dollar per one Balboa. The Government does not print paper currency, although a limited amount of coinage is minted. Panama’s monetary system is based on its Constitution (beginning with the 1904 Constitution, which established the Balboa) and Panamanian laws expressly recognizing the U.S. dollar as legal tender. There are no Panamanian foreign exchange controls or reporting requirements, and capital moves freely in and out of the country, without local currency risk. Under Panama’s unique monetary system, foreign exchange reserves are not needed to support the currency.

The absence of a national printed currency and a Balboa exchange market causes the balance of payments to be less important than fiscal policy as an indicator of the Government’s external debt service capacity. Surpluses and deficits in the balance of payments have less effect than public sector fiscal surpluses and deficits on the accumulation and drawdown of Government reserves available for sovereign debt service. Moreover, this monetary system imposes considerable discipline on Panamanian authorities in the areas of monetary and fiscal policy. Panama is limited in its ability to conduct a stimulative monetary policy and can finance public sector deficits only through borrowing. From 1999 through 2003, the non-financial public sector’s deficits averaged 1.1% of GDP. Over the same period, Panama experienced an average annual rate of inflation, as measured by the CPI, of 1.1%.

The Panamanian economy is dominated by a large service sector, which in recent years has represented an average of over three-quarters of GDP. The manufacturing and agricultural sectors represent far smaller percentages. Historically, the Panamanian economy has been characterized by an imbalance between the open, internationally oriented service sector and the fairly closed manufacturing and agricultural sectors, where productivity has been considerably lower and government polices in recent decades have impeded efficient resource allocation. See “Structure of the Panamanian Economy—Principal Sectors of the Economy.”

While much of the service sector economic activity is represented by activities associated with public administration, commerce and real estate, the significant, internationally oriented activities of this sector distinguish the Panamanian economy. The Panama Canal has played a significant role in the economy, accounting for an average of 4.8% of GDP since 1999. In 1996, commercial oceangoing traffic registered 15,187 transits, the highest volume in the Canal’s history. In 2003, commercial oceangoing traffic registered 13,154 transits, and the Canal’s toll revenue was $666.0 million. The withdrawal of the U.S. military and reversion of facilities in the former Canal Zone, culminating with the reversion of the Canal itself at the end of 1999, have had, and can be expected to continue to have, substantial fiscal and macroeconomic impacts on Panama and its economy. See “The Panama Canal—Reversion of the Canal Area to Panama.”

Another significant and distinctive factor in the Panamanian economy is the CFZ, a tax-favored export and import trading zone located near the Atlantic entrance to the Canal, which has accounted for approximately 7.1% of GDP since 1999. See “The Colón Free Zone.” As a result of the dollar-based economy, the international trade associated with the Panama Canal, the CFZ and certain legislative initiatives, Panama has also developed an important banking sector that has represented an average of 9.2% of GDP since 1999. There is no lender of last resort or deposit insurance in Panama. See “Financial System—The Banking Sector.”

D-11

Reforms and Development Programs

In September 1994, the Pérez Balladares administration announced its development plan, Desarrollo Social con Eficiencia Económica, or “Social Development with Economic Efficiency” (the “Development Program”). The Development Program acknowledged that Panama’s public sector had imposed inefficiencies and rigidities on the economy that had significantly curtailed investment, including an inflexible labor code, various barriers to free trade, including high import duties and non-tariff measures, price controls, discriminatory tax policies and high cost public utility monopolies. These conditions, in turn, had adversely affected the social conditions and development of Panama. The principal initial objectives of the Pérez Balladares administration and the Development Program were: Panama’s accession to the WTO and the associated trade liberalization measures which accession would require; maintenance of fiscal discipline and internal savings; normalization of external debt; privatization; revision of Panama’s inflexible labor code; elimination of price controls; establishment of antitrust authorities; expansion of educational programs; development of health and housing programs to ease Panama’s severe poverty and unemployment; and infrastructure improvements. The Pérez Balladares administration achieved many of its legislative objectives in a number of these areas.

In September 1999, the Moscoso administration announced its initial development plan, Nuestro Compromiso para el Cambio, or “Our Commitment for Change.” In December 1999, the Moscoso administration proposed, as a complementary plan to Nuestro Compromiso para el Cambio, the development plan Desarollo Económico, Social y Financiero con Inversión en Capital Humano, or “Economic, Social and Financial Development with Investment in Human Capital” (the “Economic Development Plan”). The Economic Development Plan focused on implementing policies designed to help reduce the level of debt, implement a social investment program and reduce the level of poverty. The Economic Development Plan originally contemplated the sale of the Government’s remaining interest in Cable & Wireless (Panama) S.A. (“C&W Panama”) and the use of the Development Trust Fund, the trust fund created by the Government in 1995 to hold and manage proceeds generated from certain privatizations, to retire certain external debt of the Republic and finance certain social development programs. On June 27, 2000, the Assembly approved Law No. 22, which approved the use of the Development Trust Fund principal for social development programs (“Law No. 22”). See “Structure of the Panamanian Economy—The Role of the Government in the Economy” and “Public Finance—Central Government Budget.”

President Torrijos has announced his initial development plan, Alianza para la Patria Nueva, or “Alliance for a New Country.” A major focus of the plan is to pursue wide-ranging reforms, including reforms to the Constitution, fiscal system, public sector and judiciary. Before assuming office, Torrijos also pledged to seek enhancements in consumer protection, to combat corruption and to promote sustainable economic and human development.

Privatization. The Pérez Balladares administration pursued partial privatization of the sizable state sector of the economy. Generally, entities were slated for privatization based on whether they performed customary governmental functions and in order of the complexity that would be involved in the privatization process. More straightforward privatizations were undertaken first, while certain more complex transactions requiring special legislation and the restructuring of operations and organizations prior to completion were undertaken later. The scheduling of privatizations has been an evolving process since adoption of the first legislation. Most significantly, in the telecommunications area, in May 1997, the Pérez Balladares administration completed the partial privatization of the landline telephone company, INTEL, S.A. (“INTEL”), through the sale of a 49% interest and management control to C&W Panama. The Economic Development Plan originally included a proposal for the sale of the Government’s remaining 49% interest in the successor entity to INTEL, C&W Panama. However, after review, the Government decided to maintain its interest in C&W Panama. In February 1996, a $72.6 million concession was granted to a consortium that includes an affiliate of BellSouth International, Inc. (the “BellSouth Consortium”) for Panama’s first cellular telephone service.

In February 1995, the Assembly passed legislation allowing the electric utility, Instituto de Recursos Hidráulicos y de Electrificación (“IRHE”), to purchase energy from private suppliers. In

D-12

February 1997, legislation was approved by the Assembly authorizing the restructuring and privatization of IRHE. In October 1998, 51% of the stock of the three IRHE distribution companies was sold for an aggregate of $302 million, and in January 1999, the stock of the four IRHE generation companies was also sold for a total of $302 million. In May 1998, privatization legislation with respect to water and sewage utilities was revised and approved by the Cabinet pursuant to the Assembly’s delegation of legislative powers to the executive branch for this purpose. Operation of certain major Government-owned ports has been turned over to the private sector through concessions, while new port facilities are being built and managed by private sector concessionaires.

There have been no significant privatizations since 1999. See “Structure of the Panamanian Economy—The Role of the Government in the Economy.” In September 1999, the Moscoso administration announced that it would not privatize the national water and sewage utility, Instituto de Acueductos y Alcantarillados Nacionales (“IDAAN”). In September 2000, the Moscoso administration, acting through the Interoceanic Region Authority (“ARI”), entered into an agreement with the IFC to study investment opportunities for former U.S. military bases such as Forts Howard, Kobbe and Sherman. One proposal developed by the IFC was the conversion of the Fort Howard air base into a special economic zone. The Assembly adopted Law No. 41 of July 20, 2004 for this purpose.

In January 2003, Panama decided not to privatize the Tocumen International Airport, located outside Panama City. On January 29, 2003, the Assembly enacted legislation to create the Civil Aeronautic Authority, an autonomous state entity that will oversee civil aviation in Panama. The Assembly also approved accompanying legislation aimed at the development and maintenance of Panama’s airport facilities, including measures to improve operating efficiency. In June 2003, control over the airport was transferred from the Civil Aeronautic Authority to Aeropuerto Internacional de Tocumen, S.A., a state-owned corporation established to manage and operate the airport pursuant to Law No. 23, also enacted on January 29, 2003. The privatization of Panama City’s Convention Center was still under discussion as of December 31, 2003, but the effort was abandoned with the issuance of Resolution No. 20 of February 13, 2004.

Panama’s privatization efforts have resulted in the sale of interests in 17 enterprises and concessions since 1990, raising a total of $1.646 billion. With the exception of IDAAN and Caja de Seguro Social (Panama’s social security agency), there remain very few public institutions to privatize in Panama.

Trade Liberalization. Developments in trade liberalization received new impetus under the Pérez Balladares administration. On October 2, 1996, Panama signed the WTO’s accession protocol, the Assembly ratified the WTO’s accession protocol on June 18, 1997 and on July 15, 1997, the President signed the protocol making it law. The accession became effective September 6, 1997. Panama had begun lowering its duties and quantitative restrictions in anticipation of WTO accession, although significant duties permitted under WTO rules remain in place for certain products. On January 1, 1997, a series of measures became effective generally providing for the: (i) conversion of all existing quotas and import permits to ad valorem tariffs; (ii) conversion of all remaining specific or mixed tariffs to ad valorem tariffs; and (iii) setting of a tariff ceiling of 40% for industrial products and 50% for agri-industrial products. A major piece of legislation designed, in part, to remove barriers to Panama’s accession to the WTO, the Ley de Universalización de Incentivos Tributarios a la Producción (“LUIT”), was passed by the Assembly in June 1995. As of September 1, 1997, tariffs were reduced to 10% for components of bread, cooking oils and numerous construction industry inputs, including steel and cement. The Ministry of Planning and Economic Policy, now the Ministry of Economy and Finance, retained a consultant to study further lowering of duties, below those agreed to with the WTO, and on October 10, 1997, the Cabinet approved additional reductions of tariffs on certain specific products to 15%. The Moscoso administration has also increased tariffs; for example, it increased tariffs for certain agricultural products in October 1999. See “Foreign Trade and Balance of Payments—Tariffs and Other Trade Restrictions.”

In early 2002, Panama signed an agreement in principle (the “Free Trade Agreement”) with Costa Rica, El Salvador, Guatemala, Honduras and Nicaragua to work towards a Central American free trade zone by 2005. The agreement is aimed at diversifying the commercial market and services in the region, eliminating trade barriers and increasing investment. The National Assembly approved the Free Trade

D-13

Agreement in February 2003. Pursuant to the Free Trade Agreement, Panama and El Salvador signed a bilateral protocol, also approved by the National Assembly in February 2003, which covers approximately 85% of both countries’ output. Panama is also negotiating a list of products to be included in a bilateral trade agreement with the Dominican Republic. The agreement will enter into force after each country ratifies the list of products.

On August 21, 2003, Panama signed a free trade agreement with Taiwan. The agreement, which took effect on January 1, 2004, was ratified by Taiwan’s legislature on October 1, 2003 and by Panama’s National Assembly on October 13, 2003. Under the agreement, 95 percent of import tariffs will be phased out over ten years.

On November 18, 2003, the U.S. Trade Representative notified the U.S. Congress of his intent to initiate free trade negotiations with the Republic of Panama. Free trade negotiations with the U.S. began in the second quarter of 2004.

In May 2002, Panama announced the creation of the Baru Free Trade Zone, located in the District of Baru, in the western province of Chiriqui. The objective of the creation of the Baru Free Trade Zone is to facilitate commercial access to and from markets in the Pacific, Central America, Mexico and the West Coast of the United States.

Other Economic Reforms. Other areas of economic reform during the Pérez Balladares administration included elimination of virtually all price controls, adoption of a competition law addressing antitrust, consumer protection and other issues, establishment of a public utility regulatory body and adoption of securities laws. Under the Moscoso administration, reforms included strengthening anti-money laundering legislation, promoting investment in infrastructure and services in order to stimulate private investment in the interior and tightening Governmental fiscal responsibility and accountability. President Torrijos has announced his intention to pursue reforms to the Constitution, the judiciary, the public sector and the Fiscal Responsibility Law. See “Structure of the Panamanian Economy—The Role of the Government in the Economy.”

Fiscal Reforms. To enforce fiscal discipline and budgetary compliance, the Government has established special review procedures for public sector expenditures. See “Public Finance—Central Government Budget.” In addition, the LUIT removes some of the fiscal mechanisms used to disfavor foreign competition in the domestic economy and eliminates certain tax exemptions and fiscal incentives that are believed to have led to distortions in the economy. The LUIT reduces the maximum tax rate applicable to most corporations for non-CFZ income and reforms the tax subsidies and incentives regime by generally granting all enterprises, regardless of size, similar tax abatements on imports of manufacturing inputs and investments in capital goods. Previously, many of these subsidies and incentives were available only to a specified class of manufacturers. In addition, the LUIT authorized the gradual elimination by year-end 2003 of tax exemptions and subsidies, either direct or indirect, for activities that substitute imports. In December 2002, the Assembly approved tax reforms aimed at improving and streamlining tax collection processes, as well as creating a broader tax base. See “Public Finance—Taxation.” The approved tax reform legislation allowed the Government to raise the level of income required for exemption from income tax from $300 to $800 per month, crack down on tax evasion and increase the income tax on banks.

External Debt Normalization. In May 1995, Panama agreed to terms with its Bank Advisory Committee for a Brady Plan restructuring of its medium- and long-term commercial bank debt, and the restructuring was successfully closed in July 1996. Petroleum import debts to Mexico and Venezuela under the San José Pact were also settled in 1996. Panamanian public sector borrowers have restructured the external debt on which they defaulted in 1987 and normalized relations with their external creditors. See “Public Sector Debt—External Debt.”

Labor Code. In order to facilitate labor market flexibility, in August 1995, the Assembly adopted substantial amendments to Panama’s Labor Code, which eased restrictions in areas such as termination of employees and payment of incentives. Prior to these amendments, the Labor Code significantly and

D-14

adversely affected the development of the private sector economy and discouraged foreign investment. See “Employment and Labor—The Labor Code.”

Social Developments. Panama’s social spending generally does not involve income subsidies or other welfare benefits but instead focuses on spending in the social sectors of health, education and housing. Together, these areas represented 45.6% of 2003 government expenditures. In July 1995, a reform of the Organic Law of Education was adopted, which, among other things, changed the structure of the Ministry of Education, provided for increased expenditures on education and increased investment in infrastructure and teacher training. In the summer of 1997, a special session of the Assembly adopted and the President signed legislation authorizing a reorganization and decentralization of education programs. In July 1997, the IDB approved a $58.1 million loan aimed at improving the education sector. As of December 31, 2003, $10.6 million of this loan had been disbursed. In September 2000, the World Bank approved a $35 million loan to help fund a $59 million program aimed at improving basic education in rural and poor urban areas through, among other things, enhanced teacher training and technical assistance to decentralized offices of the Ministry of Education.

Panama entered into an agreement with the IDB in December 1999 pursuant to which the IDB provided a $48.8 million loan aimed at improving living conditions in certain poverty-stricken communities in Panama. As of December 31, 2003, $17.2 million of this loan had been disbursed. In August 1997, the World Bank provided a $28 million loan to fund a project, slated to operate through June 30, 2004, aimed at improving infrastructure in poor rural communities. The laws that currently govern the Development Trust Fund provide that up to $200 million may be drawn down from the Development Trust Fund to support infrastructure projects. The disbursements are to be made against invoices presented to the Ministry of Economy and Finance. See “Structure of the Panamanian Economy—The Role of the Government in the Economy.” For 2002 and 2003, funds were available in the following amounts: $70 million to water supply; $40 million to irrigation projects; and $90 million to road rehabilitation. In April 2001, Panama entered into a loan agreement with the World Bank whereby Panama received a $47.9 million loan. The loan will finance a land administration program, slated to operate through September 30, 2006, that will provide equitable access to land and provide land administration services in selected rural, semi-urban and urban areas. In March 2003, Panama entered into two loan agreements with the IDB for a total of $25.2 million to support a program for the sustainable development of the Bocas del Toro region and a program to strengthen the fiscal management of the public sector.

Environmental Law. In 1998, the Assembly enacted the Ley General del Ambiente y de los Recursos Naturales (the “Environmental Protection Law”). The Environmental Protection Law created the Autoridad Nacional del Ambiente y los Recursos Naturales (“ANAM”), an autonomous administrative agency, which regulates the use of natural resources in local areas and assists in protecting the environment on the local level. The Environmental Protection Law also created the Consejo Nacional del Ambiente (the “National Environmental Council”), a governmental agency headed by three government ministers. The National Environmental Council advises the Government on appropriate national environmental policy for Panama. In addition to creating the foregoing agencies, the Environmental Protection Law established standards, sanctions and other provisions to protect more effectively the environment in Panama. In December 1999, Panama entered into an agreement with the IDB pursuant to which the IDB provided a $15.8 million loan to ANAM to regulate and manage environmental projects in Panama.

Infrastructure. Through the privatization of major public utilities, the Government has sought significant improvements in Panama’s infrastructure. In 1994, with financial assistance from the World Bank and the IDB, the Government began two road construction and rehabilitation programs that have, as of December 31, 2003, both since concluded. The Government is also expanding the highway network through administrative concessions for toll road projects. See “Structure of the Panamanian Economy—The Role of the Government in the Economy.” The Government entered into an agreement to build more than a dozen highway overpasses in Panama City and entered into a financing arrangement for this construction, which has been guaranteed by Great Britain’s Export Credits Guarantee Department. In January 2000, a two-lane addition to the Pan American highway was completed, extending from La Chorrera to San Carlos, west of Panama City. In November 2000, the Government, with the assistance of a $72 million loan from the IDB, began a five-year program to install electrical transmission lines to

D-15

transmit electrical power generated by hydroelectric plants in the countryside to urban areas. In addition, plans were implemented in 2002 for the construction of a new bridge over the Panama Canal, together with feeder roads. The estimated total cost of the project, including the designs, inspections and construction of the bridge and feeder roads, was $204.1 million. As of December 31, 2003, construction continued and the bridge is expected to be complete by August 2004.

Puebla-Panama Plan. In June 2001, Panama, together with Mexico, Nicaragua, Guatemala, Honduras, El Salvador, Belize and Costa Rica signed the Puebla-Panama Plan, a development plan to be supported by $2 billion in loans from the IDB and other multilateral organizations. The development includes joint management of natural resources and infrastructure projects such as highways, roads, electricity, seaports, airports, gas pipelines and communications as well as a plan for environmental protection. In July 2003, the IDB approved an additional $37 million loan to Panama to rehabilitate and upgrade a highway on the Pacific Corridor, a component of the Puebla-Panama Plan’s network of Mesoamerican highways.

Prevention of Money Laundering and Other Crimes. The Pérez Balladares administration, with international encouragement and support, targeted certain illegal activities, including money laundering, corruption and drugs, for reduction and elimination. The Moscoso administration continued to target these illegal activities, and the Torrijos administration has pledged to follow suit. The Development Program itself was designed to reduce opportunities for corruption, and the Pérez Balladares administration took several significant actions in the area of money laundering. Legislation adopted in 1994 mandated forfeiture of proceeds derived from money laundering, while a decree issued that year by the Pérez Balladares administration required resident agents of corporations to know the identity of the corporation’s beneficial owners. In June 1995, the Financial Analysis Unit (“UAF”), an independent investigative unit reporting to the President, was created to monitor certain financial transactions. Banks, casinos, financial institutions, exporters and others are required to report to the UAF cash transactions exceeding $10,000. Additionally, new banking legislation was enacted which has tightened controls and supervision of various banking activities. The UAF has signed letters of understanding with regulatory bodies in twenty other countries in Latin America and the Caribbean to prevent money laundering. The letters of understanding are intended to pave the way for greater cooperation between countries by facilitating the exchange of information. See “Financial System—The Banking Sector.”

The Government has collaborated with other nations, including the U.S. and Canada, in several investigations and prosecutions related to drug smuggling and money laundering. On February 29, 2000, the U.S. certified Panama under applicable U.S. law as having adequately complied with the U.N. Convention Against Illicit Traffic in Narcotic Drugs and Psychotropic Substances. In June 2001, the Financial Action Task Force on Money Laundering (“FATF”) of the Organization for Economic Cooperation and Development (“OECD”) removed Panama from its list of countries and jurisdictions that are non-cooperative in the fight against money laundering. In April 2002, the OECD removed Panama from the list of countries that it considers uncooperative tax havens. As part of an agreement with the OECD, Panama has pledged to improve the transparency of its tax system and to provide certain tax information to the OECD member countries. In March 2003, Panama signed a cooperation agreement with Mexico that provides for the exchange of financial information to prevent and detect money laundering.

Economic Performance—1999 Through 2003

Revision of GDP Calculations. In 2002, the Directorate for Statistics and Census of the Comptroller General’s Office (“DEC”) revised its calculation of GDP by adopting a 1996 base year; the base year previously used was 1982. The calculation of Panama’s GDP now also includes, for example, figures from sectors that were previously unaccounted for under the previous methodology, takes into account indirect taxes paid by various sectors and adjusts national accounts figures to account for the offer and use of goods and services. The Government believes that the revised methodology produces a more accurate estimate of Panama’s GDP and is consistent with accounting methods espoused by various international organizations, including the Economic Commission for Latin America and the Caribbean (an economic commission of the U.N. that, along with Panama’s Ministry of Economy and Finance, provided technical assistance to the DEC in

D-16

its recalculations). The revised methodology has been applied retroactively to, and thus adjusts, economic statistics from fiscal year 1999 onward.

Economic Performance in 1999. Real GDP increased by 4.0% in 1999. The sectors of the economy primarily responsible for such growth in 1999 were agriculture; mining; construction; transportation and communications; financial intermediation; commerce, restaurants and hotels; and real estate. Agricultural activities increased by 1.8% in 1999, accounting for 6.6% of GDP. This increase was primarily attributable to increased exports of cattle and pork, as well as non-traditional agriculture commodities such as melon, cashew seeds and hot pepper flakes. The contribution of mining activities to GDP grew 23.9% from 1998 as a result of an increase in the production of raw mining materials used in the construction sector. The construction sector grew 36.0% from 1998 to 1999, representing a contribution to GDP of 4.8% in 1999. This increase was principally the result of the increase in the construction and rehabilitation of highways, roads and housing projects. The contribution of transportation and communications to GDP was 9.1% in 1999 and represented an increase of 9.6% from 1998. This growth was due to an increase in the movement of containers in the nationwide port system, the merger of local airline companies with international airline companies, the privatization of a publicly owned communication company and increased investment in communication equipment and infrastructure. Financial intermediation activity in 1999 increased 5.3% from 1998, representing a contribution to GDP of 9.3% in 1999. This increase was principally the result of strong expansion in the domestic banking sector. Activity in the commerce, restaurants and hotels sector in 1999 increased 3.2% from 1998, representing a contribution to GDP of 10.2% in 1999, an increase that was primarily attributable to sales of housing and infrastructure in the former Canal Zone areas. Real estate activity represented 15.5% of GDP in 1999, reflecting an increase of 6.1% in the sector from 1998 resulting from an increase in construction of housing and other building projects and the enactment by the Assembly in October 1999 of an amendment to Law No. 3 of 1985 (the “Preferential Interest Rate Law”) that was intended to encourage the acquisition of new housing. The Canal’s contribution to GDP in 1999 reached 4.7%, reflecting a growth of 1.4% in the sector from 1998. The public administration sector experienced only a slight increase, growing 0.8% from 1998 as a result of budgetary restrictions to control the deficit; the public administration sector represented 9.5% of GDP in 1999.

Activity in the CFZ declined 13.6% from 1998 to 1999, primarily as a result of economic difficulties in South America triggered by, among other causes, the reduction of capital inflows after the Asian financial crisis. The CFZ’s contribution to GDP reached 6.3% in 1999.

Inflation for 1999, as measured by the CPI, increased 1.4%. This increase was primarily due to the increased cost of rental housing, health services and gasoline. The unemployment rate decreased from 13.6% in 1998 to 11.8% in 1999. In 1999, the Government’s current account had a surplus of $155 million (1.4% of GDP). The Government’s overall deficit decreased to $228 million in 1999, or 2.1% of GDP, from $461 million in 1998. This decrease in the Government’s overall deficit was primarily attributable to the decline in capital expenditures and the significant reduction of social security transfers. The overall non-financial public sector deficit also decreased to $138 million (or 1.2% of GDP) in 1999, primarily due to a cut in public expenditures.

The current account deficit with respect to Panama’s balance of payments increased from $1.016 billion in 1998 to $1.159 billion in 1999. The net balance of payments registered a surplus of $190.6 million in 1999, as compared to a net balance of payments deficit of $104.9 million in 1998.

On March 31, 1999, Panama issued $500 million principal amount of its 9.375% U.S. Dollar-Denominated Global Bonds due 2029. Panama repurchased approximately $203 million aggregate principal amount of Brady Bonds in June 1999.

Economic Performance in 2000. Real GDP increased by 2.7% in 2000. This represented a decrease from 1999’s 4.0% growth in real GDP. The principal sectors of the economy primarily responsible for such growth in 2000 were agriculture, construction, real estate, transportation and communications, public utilities, financial intermediation and public administration. The agricultural sector saw growth of 10.1% from 1999 to 2000 (reflecting a contribution to GDP of 7.0% in 2000)

D-17

primarily due to a recovery in fishing activities and exports of agricultural products. Construction activity grew 1.3% from 1999 to 2000 (reflecting a contribution to GDP of 4.7% in 2000) due to growth in housing construction. In 2000, the real estate sector also grew for the same reason, increasing 3.6% from 1999 and representing 15.6% of GDP. Transportation and communications activity in 2000 increased 17.8%, from 1999, representing a contribution to GDP of 10.5% in 2000 as compared to 9.1% in 1999. This increase was primarily due to port development permitting an increase in the number of containers handled, the privatization of INTEL and increased public and private sector investment in communications equipment, infrastructure and services. Public utilities activity increased 9.3% from 1999, representing a contribution to GDP of 3.3% in 2000, as compared to 3.1% in 1999. This increase is primarily attributable to a surplus of hydroelectric power. The financial intermediation sector grew 9.7% from 1999 to 2000, representing 9.9% of Panama’s GDP in 2000, due to an increase in credit extended by local banks in the domestic market. The value produced by the public administration sector increased 1.8% from 1999 to 2000, representing 9.4% of GDP in 2000.

The Panama Canal Authority’s activity in 2000 increased 2.3% from 1999, representing a contribution to GDP of 4.7% in 2000, as compared to a GDP contribution of 4.7% in 1999. CFZ activity in 2000 increased 16.0% from 1999, representing a contribution to GDP of 7.1% in 2000 as compared to 6.3% in 1999.

Inflation in 2000, as measured by the CPI, was 1.4%, the same rate as in 1999, remaining constant despite a slight increase in health care costs and increases in housing and energy costs. The unemployment rate increased from 11.8% in 1999 to 13.5% in 2000.

The Government’s current account for 2000 had a surplus of $148 million (1.3% of GDP), compared to a surplus of $155 million (1.4% of GDP) in 1999. The Government’s overall deficit decreased from $228 million in 1999 (2.0% of GDP) to $128 million in 2000 (1.1% of GDP). This decrease in the overall deficit was primarily attributable to increased revenues, relating to the payment of dividends to the Government by privatized companies and to improved tax collections. The overall non-financial public sector registered a surplus of $54 million in 2000, compared to a deficit of $138 million in the previous year, principally due to reductions of government spending and debt levels in 2000. The current account deficit with respect to Panama’s balance of payments decreased from $1.159 billion in 1999 to $689.4 million in 2000, resulting from an increase in the value added by exports and services in 2000.

On July 13, 2000, Panama issued $350 million principal amount of its 10.75% U.S. Dollar-Denominated Global Bonds Due 2020.

Economic Performance in 2001. Real GDP increased by an estimated 0.6% in 2001. This represented a decrease from the 2.7% growth in real GDP experienced in 2000. The sectors of the economy primarily responsible for such growth in 2001 were transportation and communications, the CFZ, public administration, agriculture and other services. Transportation and communications activity increased by 2.3% in 2001 (contributing 10.7% to GDP in 2001 compared to 10.5% to GDP in 2000). In the transportation sector, this increase was primarily due to modernization of the transportation infrastructure. In the communications sector, C&W Panama completed the first stage of an expansion project and modernized its communications equipment. The contribution of the CFZ to GDP rose from 7.1% in 2000 to 7.8% in 2001. This increase was primarily attributable to an increase in merchandise exports and imports, reflecting an increase in commercial activities in the CFZ. The public administration sector grew 5.8% in 2001, reflecting a contribution of 9.9% to GDP (an increase from 9.4% of GDP in 2000). This increase principally resulted from an increase in personnel in the health and education areas. The agricultural sector experienced an increase of 6.4% from 2000. Activity in other service sectors, including tourism, grew 0.7% in the aggregate in 2001, contributing 5.7% to 2001 GDP (compared to a contribution of 5.7% to 2000 GDP).

Activity in the construction sector fell 21.8% from 2000 to 2001 (compared to an increase of 1.3% from 1999 to 2000) and represented a contribution to GDP of 3.7% in 2001. This decline is attributable to the lack of new construction projects during the year and a slowdown in housing projects. Activities of the Panama Canal Authority continued to grow by increasing 3.1% from 2000 to 2001 (compared to an

D-18

increase of 2.3% from 1999 to 2000); the sector represented 4.8% of 2001 GDP (compared to 4.7% of 2000 GDP). The growth in Panama Canal Authority activities was attributable to increased Canal traffic.

Inflation in 2001, as measured by the CPI, rose 0.3% as compared with 1.4% in 2000. The inflation rate was affected by the cost of electric energy, gas and medical services. The unemployment rate increased from 13.5% in 2000 to 14.0% in 2001 due to an increase in the labor force, as well as job losses in the private sector. The economy had difficulty absorbing large numbers of unskilled workers, particularly those migrating from rural to urban areas.

The Government’s current account for 2001 had a surplus of $62 million (0.5% of GDP), compared to a surplus of $148 million (1.3% of GDP) in 2000. The Government’s overall deficit increased from $128 million in 2000 (1.1% of GDP) to $200 million in 2001 (1.7% of GDP). This increase in the overall deficit is primarily attributable to a decrease in federal income tax revenues and an increase in government current expenses, specifically an increase in external debt interest and wages. In 2001, the overall non-financial public sector registered a deficit of $79 million (or 0.7% of 2001 GDP), compared to a surplus of $54 million in 2000 (or 0.5% of 2000 GDP). The current account deficit with respect to Panama’s balance of payments decreased from $689.4 million in 2000 to $173.5 million in 2001, as a result of an increase in the value added by exports and services and a drop in import expenses in 2000.

On February 8, 2001, Panama issued $750 million principal amount of its 9.625% U.S. Dollar-Denominated Global Bonds due 2011. On July 13, 2001, Panama repurchased $158.4 million of its 7.25% Notes due 2002 for cash and warrants to purchase its 9.375% Global Bonds due 2012. On November 16 and December 11, 2001, Panama issued an aggregate $350 million principal amount of its 8.25% U.S. Dollar-Denominated Global Bonds due 2008 in reopenings of that issue.