Table of Contents

| Page |

|

|

About the Company................................................................................................... | 1 |

|

|

Awards and Recognition.......................................................................................... | 2 |

|

|

Sound Governance..................................................................................................... | 3 |

|

|

Developing Social and Human Capital...................................................................... | 6 |

|

|

Managing Environmental Risks................................................................................ | 16 |

|

|

About This Report

This report provides a comprehensive review of how BancFirst Corporation is addressing sustainability, including environmental, social and governance (ESG) and other matters important to our business, as well as to our various stakeholders and the communities we serve. Throughout the report we refer to other sources for more information, including our annual report, our proxy statement, and our investor relations website. The information presented is as of or proximate to September 30, 2021, unless otherwise stated.

About the Company

History

The Company was organized in 1984, and has grown from a multibank holding company with $450 million in assets serving seven communities, to a regional financial holding company with over $11 billion in assets serving 60 communities in Oklahoma and Texas. We operate as a “super community bank”, managing our community banking offices on a decentralized basis, which permits them to be responsive to local customer needs. Its two subsidiary banks are BancFirst in Oklahoma and Pegasus Bank in Dallas, Texas. Our strategy focuses on providing a full range of banking services to retail customers and small to medium-sized businesses. More information about the Company’s business and its strategies can be found in its Annual Report.

Core Values

Our core values govern how we do business and also inform our approach to sustainability.

Asset Quality – Superior asset quality is the cornerstone of our strong balance sheet that supports consistent, long-term profitability.

Community Leadership – By being a leading corporate citizen we impact the success of our communities and their quality of life.

Customer Care – A high level of customer care and service differentiates us from our competitors, contributing to retention and growth of our customer base.

Employee Development – Highly trained and motivated employees are critical to our success.

Integrity – Integrity and unquestionable business ethics are the foundation for meeting the needs and expectations of our stakeholders.

Profitability – Sustainable profitability is fundamental to creating long-term value.

Sustainability

The essence of BancFirst Corporation’s mission statement is creating long-term value. We view “sustainability” as the activities that maintain or enhance the ability of the Company to create enterprise value over the long-term. Sustainability is accomplished through:

Sound Governance

Developing Social and Human Capital

Managing Environmental Risk

How the Company addresses each of these elements of sustainability is presented in the remainder of this report.

1

Awards and Recognition

BancFirst Corporation has received numerous awards and recognition, demonstrating its financial strength, consistent performance, service to its customers and communities, and commitment to building long-term value.

For the 9th consecutive year, BancFirst was included on the KBW Bank Honor Roll. Keefe, Bruyette & Woods, Inc., is a full‐service, boutique investment bank that names U.S. banking institutions to its coveted “Bank Honor Roll” of superior performers every year

BancFirst is included in the Dividend Achievers Index for having increased its dividend payments for 28 consecutive years

BancFirst has been named the top volume SBA lender in Oklahoma for over 28 years

BancFirst was the largest producer of PPP loans in Oklahoma with $1.14 billion going to small businesses

o

We made 15,119 loans through two rounds of funding, with an average loan balance of $75,000

2

Sound Governance

Overview

Sound governance is essential to long-term sustainable growth. The Company complies with all federal and state laws regulating corporate governance and disclosures, as well as various governance best practices. This report is not a comprehensive review of our corporate governance. Disclosures regarding governance matters required by SEC rules and regulations, the Sarbanes-Oxley Act of 2002, and the Nasdaq Stock Market rules are included in the Proxy Statement for our Annual Meeting of Shareholders issued April 7, 2021 and our Annual Report on Form 10-K for the year ended December 31, 2020. Additional information regarding corporate governance is available on the Company’s investor relations page of its website at www.BancFirst.bank/Investor-Relations. This report addresses other aspects of governance not directly required by laws and regulations, but are nonetheless key elements of governance related to sustainability.

Sustainability Committee

The Company has formed a Sustainability Committee comprised of executive risk managers, the CEO and an independent director. Its purpose is to develop a strategy for enhancing sustainability and to incorporate environmental, social and governance factors into the Company’s business processes. The Sustainability Committee reports to the Board of Directors.

Board Composition

The Company’s Proxy Statement provides detailed information regarding its Board of Directors, including:

Independence – A majority of the directors meet the independence requirements.

Refreshment and Assessment – All directors serve a one-year term, and must be nominated and stand for election each year. There is an ongoing process to assess the skills and performance of continuing directors, and to identify and consider new director candidates. The Company’s age limit for directors is 79 years old.

Skillset of Directors – The directors possess a wide range of skills and experiences representing a number of industries that are prevalent in the Company’s market areas. A Directors Skills Matrix is included in our Proxy Statement.

Diversity - The Board includes three women, one of whom identifies as African American, another member who identifies as Hispanic, and a member who identifies as Native American.

Business Ethics

Our core value of Integrity encompasses the business ethics under which we operate. The Company’s Code of Conduct addresses various ethical and legal matters, and is available on the Investor Relations page of our website. All directors, officers and employees are required to confirm in writing that they have read, understand, and agree to comply with the Code. In addition, our Corporate Policies address certain ethical and legal matters, such as:

3

Confidential Nature of Customer Affairs – Requires that information and affairs of customers be kept private.

Conflicts of Interest – Prohibits conflicts of interest between directors, officers and employees and the Company, including:

o

directly doing business as a vendor to the Company;

o

holding a substantial financial interest in, or serving as a director or officer of, any vendor to the Company;

o

competing with the Company;

o

having outside employment, unless approved in advance;

o

using inside information for personal gain; and

o

accepting gifts, payments, extravagant entertainment, services or loans from any vendor soliciting or already doing business with the Company.

Government and Community Relations – Provides guidance for political, community development and community relations activities, and prohibits the Company from making contributions or expenditures related to a political campaign or election, or to a political action committee.

Insider Trading – Prohibits use of inside information, insider trading and hedging of Company securities, and we impose blackout periods when appropriate.

Self-Dealing Transactions – Prohibits employees from conducting and processing transactions with the Company for their own benefit.

Compliance with Laws and Regulations – Various policies that require compliance with laws and regulations, including lending and consumer compliance.

Antitrust Laws – The Company prohibits anti-competitive practices such as cartels and abuse of dominant market power. It complies with antitrust laws and has never faced an antitrust charge or allegation.

Anti-Money Laundering – The Company has an extensive policy, program and procedures for compliance with the Bank Secrecy Act and anti-money laundering laws and regulations.

Legal Proceedings and Enforcement Actions

The Company is a defendant in legal actions arising from normal business activities. The amount of losses and legal fees that the Company has incurred has been immaterial. Most of the litigation has related to lending, largely arising from collection counterclaims, and other transactional disputes with individual customers. The Company has never been the subject of an enforcement action by a governmental regulatory authority.

Whistleblower Policies and Procedures

The Company’s Code of Conduct provides for a whistleblower program using EthicsPoint, a comprehensive, anonymous Internet and telephone based reporting system that allows management and employees to work together to address financial reporting issues, fraud, inappropriate conduct, harassment, discrimination, or other matters in the workplace. All EthicsPoint reports are reviewed, investigated, and addressed, as applicable, by the Company’s Audit Committee Chairman, Chief Internal

Auditor, Executive Chairman, Chief Executive Officer, or Director of Human Resources. Retaliation or harassment against any reporting person through EthicsPoint, or any whistleblower to a regulatory agency, is explicitly prohibited. Any incidents of potential retaliation are to be reported directly to the Director of Human Resources for investigation and corrective action, in order to protect the confidentiality of the reporting person. This program is intended to comply with the requirements of the Sarbanes-Oxley Act and the Consumer Financial Protection Act. The Company has not been accused of any violations of whistleblower regulations.

4

The telephone number and Internet address to access the EthicsPoint system are provided in the Code of Conduct, the Employee Handbook and on the Company’s intranet. Instructions for how to file a report, and questions and answers are also provided to employees on the intranet.

Shareholder Participation/Voting

To facilitate shareholder participation in meetings, the Company provides for voting on proxy resolutions by mail, internet, and telephone. In addition, shareholders may participate in the meetings in person or by conference call. Proxy statements and voting instructions are provided by mail, on the Company’s investor relations website, or by electronic delivery if requested by the shareholder. Shareholders may submit proposals in advance to be considered for inclusion in the Annual Meeting.

The Company has only common stock outstanding and each share is entitled to one vote. It has Senior Preferred Stock that is authorized that may be issued with voting rights. There are no existing voting right restrictions.

Compliance

As a publicly traded financial holding company, BancFirst Corporation operates in a highly regulated environment. Compliance programs, procedures, and training are necessary for sustaining its legal, regulatory and ethical compliance. Each year, banking regulatory agencies conduct examinations that assess the Company’s governance processes and compliance programs. The more significant elements of its compliance processes are summarized below.

Corporate Governance Risk Report – Each year the Chief Risk Officer prepares a report assessing the Company’s governance processes and the related risks.

Code of Conduct Training – Annual training for the Code of Conduct is required.

Compliance Training Program – An extensive compliance training program is conducted covering a wide range of laws and regulations.

Conflicts of Interest Review – The Chief Risk Officer conducts quarterly reviews for possible conflicts of interest.

Related Party Transactions Audit – The Internal Audit Department performs an audit of related party transactions annually.

Annual Assessment of Corporate Governance – The Internal Audit Department assesses the Company’s corporate governance as part of the entity level controls over financial reporting.

5

Developing Social and Human Capital

Overview

Developing social and human capital enhances sustainability. We develop social and human capital through:

Leading and investing in our communities

Providing financial services accessible to everyone

Fair and ethical conduct in serving our customers

Maintaining privacy and information security

Developing a diverse, well-trained and motivated workforce

Community Leadership and Investment

Community Leadership is one of our core values. Our success depends on the growth and development of our communities. Employees are encouraged to act as effective and responsible citizens by taking part in community and political activities that enhance the quality of life. Examples of these community development activities include:

Serving on the boards of industrial authorities and economic development foundations

Using their financial expertise to review and approve grant monies and provide assistance to new businesses and businesses moving into their communities

Serving on the boards or committees of various affordable housing authorities

Teaching financial literacy courses in schools in their communities where over 50 percent of the students receive free and reduced cost lunches

Providing financial education and literacy resources on our website

The Company supports and funds, on an ongoing long-term basis, the following history, arts and educational programs to enrich the lives of students in our communities:

Preservation Oklahoma – PlanFirst Grant Program – a “grass-roots preservation matching funds” grant program to provide funding for historic preservation initiatives

Oklahoma Historical Society – Oklahoma History Center Traveling Program – a program which brings the Oklahoma History Center museum to the classroom, including lesson plans, hands-on activities, and artifacts for the students to handle

o

Our sponsorship targets rural elementary and secondary schools and is free to teachers

Oklahoma Children’s Theatre – BancFirst Tour – annual performances of the Oklahoma Children’s Theatre in rural BancFirst communities, targeted to elementary school students

Oklahoma Arts Institute - Teacher Workshops – provides 15 teacher scholarships to attend the Oklahoma Fall Arts Institute, where four-day workshops are taught by nationally renowned artists in areas such as creative writing, photography, film, painting, and vocal music

6

Habitat for Humanity’s Affordable Housing Program – BancFirst administers payments for Habitat’s Affordable Housing Program grants for down payment assistance to new homeowners

Greenwood Chamber of Commerce – BancFirst is a member of the Greenwood Chamber of Commerce in Tulsa, and provided a grant for plans to redevelop the “Black Wall Street” area

Local School Programs – Our community banks fund programs through their local public schools

Charitable Contributions – During 2020, the Company made contributions of over $1,360,000.

Access to Financial Services

The Company provides a wide range of financial services that are available for access by all persons in its communities. Its extensive branch network and other delivery systems help ensure that its products and services are available to all segments of its communities, including low to moderate income areas. According to a 2017 FDIC survey, within the Company’s primary market area of Oklahoma, 7.3% of the households were unbanked and 21.7% of the households were considered underbanked. Several of the Company’s delivery systems, products and services are available to benefit these households, including:

108 banking locations in 59 communities throughout Oklahoma and three locations in Dallas

o

Over 26% of its banking locations are in low-to-moderate-income census tracts

o

20 counties out of the 29 counties in Oklahoma where the Company has banking locations have median household income below the state and national averages

240 ATMs, 28% of which are located in low-to-moderate-income census tracts

Free online and mobile banking services

Online services, such as deposit account opening, consumer loan applications, credit card applications, small business loan applications, and mortgage loan requests

Products such as money orders and check cashing services

Deposit Services

The Company has a leading market share of deposit customers in Oklahoma. Below is a summary of deposit accounts for individuals and small businesses.

| Number of Accounts | Balance |

Personal |

|

|

Demand Deposit | 256,650 | $1,914,516,000 |

Savings | 91,069 | $994,916,000 |

Treasury Fund | 20,183 | $1,656,171,000 |

Small Business |

|

|

Demand Deposit | 38,564 | $805,944,000 |

Savings | 2,205 | $51,141,000 |

7

Over 86% of the Company’s personal demand deposit accounts are no cost accounts that provide core banking services without extra fees or minimum balance requirements.

| Number of Accounts | Balance |

No Cost Accounts | 222,140 | $1,258,819,000 |

Credit Services

The Company is committed to meeting the credit needs of all segments of the communities that it serves. We provide a wide range of credit products to individuals and small businesses, as well as corporate customers. Below is a summary of BancFirst’s loans by broad segment (excluding real estate loans).

| Number of Accounts | Balance |

Personal | 29,522 | $382,615,000 |

Small business | 14,563 | $765,918,000 |

Corporate | 674 | $1,071,804,000 |

A significant number of the Company’s loans are made to borrowers in low to moderate income (LMI) areas. For 2020:

21.3% of home mortgage loans made were to LMI applicants

20.6% of small business loans made were to applicants in LMI areas

10.4% of small farm loans made were to applicants in LMI areas

In addition to the lending activities described under its Community Reinvestment Act program below, the Company has the following special programs to ensure access to credit services for potentially underserved segments in its markets.

BancFirst pursues outreach programs in its larger communities to better serve majority minority areas, such as:

In the Oklahoma City metropolitan area, a program for lending to non-citizens to reach more Hispanic borrowers, maintaining bilingual staff, and advertising in media serving Black and Hispanic communities

In the Tulsa metropolitan area, specific action plans, developed by management of six bank locations, to increase applications from majority minority areas

In the Lawton metropolitan area, a Business Development Team tasked with increasing the bank’s presence in the Black community and increasing applications from Black borrowers

BancFirst also maintains a unique Flexible Home Loan Program (FHLP) that benefits minority loan applicants who do not otherwise meet the bank’s standards of creditworthiness. The FHLP is authorized by Regulation B, which is enforced by the Consumer Financial Protection Bureau. Applicants who meet the criteria of the program have their applications forwarded to FHLP underwriting for consideration

under the more flexible terms of the program. During 2020, 18% of the loans submitted to the program were subsequently approved under the more accommodative terms of the FHLP. The approval percentage was 22% for the first nine months of 2021. Since inception in 2011, a total of 264 loans have been approved under the program.

8

Pegasus Bank is implementing a program to develop consumer and small business credit products to deliver to minorities and low-to-moderate income borrowers within its market area, by partnering with community service groups targeting those market segments.

Community Reinvestment Act Performance

BancFirst is subject to the Community Reinvestment Act (CRA). The most recent CRA examination was conducted by the FDIC in 2021. The examination and the resulting Performance Evaluation cover three tests: Lending Test, Investment Test, and Service Test. These three tests were evaluated for performance since the previous examination in 2018. The Lending Test was rated High Satisfactory, and overall performance was rated Satisfactory. Also, the examination did not identify any evidence of discriminatory or other illegal credit practices for the bank as a whole. Overall conclusions and significant factors for the three tests were:

Lending –

o

An excellent record regarding its lending activity, supported by market rankings of 4th for home mortgage loans, 3rd for small business loans, and 1st for small farm loans

o

Excellent responsiveness to its market areas’ community development needs

Originated 173 community development loans totaling $805,018,000 (15.2% of average net loans)

o

Innovative and flexible lending practices in order to serve assessment area credit needs

Originated 3,081 innovative or flexible loans totaling $419,402,000 (7.9% of average net loans)

Investment –

o

The bank had 105 qualified investments totaling $48,723,000

Service –

o

The Company’s branch network and delivery systems are accessible to essentially all portions of its market areas

o

Employees provided a total of 383 community development services, including affordable housing, community, economic development, and revitalization services

o

Community services also included employees teaching financial literacy courses in schools where over 50 percent of the students receive free and reduced lunches.

The results of CRA examinations are considered in enhancing our strategies to further develop or expand products and services, and to improve access to financial services by all persons in our communities.

Consumer Protection

The Company is committed to fair and ethical conduct in serving its customers. Its core value of Customer Care encompasses issues of customer and product responsibility, sales practices, marketing

and the treatment of customers in financial distress. The Company maintains a Product Development group that oversees new product and service offerings, and evaluates the related customer, marketing, sales, and compliance considerations. This group is also responsible for:

9

Periodically reviewing all marketing information, disclosures and agreements for consumer products and services to ensure that:

o

the information is easily understandable, not misleading, comprehensive, and accurate;

o

there is transparency of all costs and conditions; and

o

there is limited use of “fine print”

Reviewing pricing of products and services to ensure fair and competitive pricing

Reviewing sales practices and incentives to ensure that they don’t encourage abuse

Maintaining compliance with consumer protection laws and regulations, such as the Truth in Savings Act

As a financial holding company, the Company is subject to various consumer protection laws and regulations, and is examined for compliance by the Federal Reserve and the FDIC. Responsibility for maintaining consumer compliance is assigned to lending and operational compliance officers. Our Corporate Policies cover many aspects of consumer protection and compliance, such as:

Compliance Program – Establishes a comprehensive compliance program encompassing consumer protection, fair lending, and community credit activities

Compliance Training Program – Provides employee training for consumer compliance and lending compliance

Truth in Savings – Requires compliance with regulations regarding account disclosures and advertising of accounts

Tying Restrictions – Prohibits tying extensions of credit to use of other products or services

Fair Lending – Ensures that all persons receive fair and consistent treatment throughout the credit function of the bank, without discriminatory practices

Americans With Disabilities Act – Requires that we make banking services accessible for customers with disabilities, such as through ADA compliant banking facilities, drive through lanes, ATMs, and online services

The Company is subject to the Truth in Savings Act (Regulation DD), the purpose of which is to enable consumers to make informed decisions about bank deposit services. It requires banks to provide consumers detailed disclosures regarding terms and costs of deposit accounts, and imposes requirements for advertisements. The Company is in full compliance with Regulation DD.

To ensure adherence to the policies, laws and regulations listed above, the Asset Quality and Internal Audit Departments conduct periodic compliance audits. The Company is also examined by banking regulatory agencies for consumer compliance.

The Company is also committed to maintaining responsible sales practices, and has several measures to ensure that unethical or inappropriate behavior is discouraged or prevented, such as:

A limited number of employees who are significantly compensated through sales commissions (primarily insurance agents and mortgage loan officers), and sales incentives for promoting certain products are modest

o

Commissions and sales incentives are only approximately 6.2% of total compensation

10

Internal audits of sales and incentive programs to monitor for inappropriate sales practices, such as opening of accounts or enrollment in services that were not requested by the customer

Maintaining a mystery shopper program

Monitoring, evaluation and follow-up for customer complaints received

To assist customers who incur significant overdraft fees, we notify them of less costly services that are available and provide financial education resources. Customers who continue to experience a high level of overdrafts may also be offered the assistance of a banker and a plan to keep the account active, while suspending overdrafts and repaying the overdrawn position over time.

Customers who become past due on their home loans are provided with homeowner counseling resources. Furthermore, past due notices provide information to borrowers who have protections under the Servicemembers Civil Relief Act.

Pandemic Response

The COVID-19 pandemic caused financial distress for many of our customers, including families and small business. In response, the Company took several proactive steps to provide relief to our customers, such as:

Reducing fees for returning checks – We reduced our fee for returning checks by $10.

Eliminating Mobile Deposit fee – We eliminated the fee for making mobile deposits; the service is now free.

Allowing customers to defer loan payments – Through our skip-a-payment program, individuals deferred 18,665 payments for 9,832 loans.

Eliminating late fees – The Company temporarily ceased charging late fees on past due loan payments beginning in early 2020 through the second quarter of 2021.

Participating in the Paycheck Protection Program – BancFirst was Oklahoma’s largest producer of PPP loans, making 15,119 loans with an average balance of $75,000 totaling $1.14 billion.

Privacy and Information Security

Ensuring the privacy and security of both our customers’ and the Company’s information is essential to maintaining confidence in our Company, and our reputation. We have strict policies regarding privacy, and we maintain a robust Information Security Program. The Program follows the guidelines of section 501(b) of the Gramm-Leach-Bliley Act and sections 621 and 628 of the Fair Credit Reporting Act. The Company also maintains an Identity Theft Program that complies with sections 114 and 315 of the Fair and Accurate Credit Transaction Act (FACT Act). In addition, we provide resources on our website for our customers regarding protecting personal information and bank accounts.

Our policy is to comply with all laws and regulations requiring the prompt notification and disclosure of breaches of sensitive private information to affected customers and to regulatory authorities, including the Interagency Guidance Response Programs for Unauthorized Access to Consumer Information and Customer Notice. The Company has not experienced any significant data breaches requiring public disclosure or notification of regulatory authorities.

11

Approach

The Company has an Information Security Committee, comprised of the Chief Information Officer, the Chief Technology Officer, the Information Security Officer, the Chief Risk Officer, the Chief Operations Officer, and the EVP of Financial Services. The Committee oversees the Information Security Program and strategy. The Program includes risk assessments, processes to manage and control risks, training for all employees, and monitoring of systems and controls, to accomplish the following objectives:

Ensure the security and confidentiality of sensitive information

Protect against threats or hazards to the security or integrity of such information

Protect against unauthorized access to or use of such information that could result in substantial harm or inconvenience to any customer

Ensure the proper disposal of sensitive information

The Program relies on well-proven principles of information security by:

Maintaining a risk assessment process that identifies areas that are required to be protected, and to determine if effective controls are used to safeguard the bank against threats and vulnerabilities

Assigning ratings to identify priorities that need additional controls

Providing training on cybersecurity to all employees and to customers to address the ever changing technology and tactics of malicious actors

Monitoring security controls and the use of systems and networks

Conducting security review meetings to discuss monitoring activities and relevant security events

Assessments by Internal Auditors of our controls, design, and monitoring capabilities

Engaging external parties at least annually to perform security assessments that further test and review the effectiveness of our security

Providing for response to information security events and management of any such events by the Information Security Committee

The Company also maintains an extensive Vendor Management Program to ensure vendors adequately protect information. This program includes:

Initial risk assessments for new vendors and identification of red flags

Due diligence procedures such as reviews of financial information, reputation, qualifications and experience, complaints, regulatory actions, information security processes and audits, certifications, and business contingency plans

Review and negotiation of contract terms, including requirements regarding information security, use of third parties, insurance coverage, indemnifications, performance standards, and monitoring of contract compliance

Ongoing monitoring and annual formal reviews of vendor information, performance and contract compliance

12

Human Capital

The Company’s approach to developing human capital resources focuses on objectives that include, but are not limited to, providing fair and equitable compensation, training employees to reach heightened skill sets and standards of motivation, identifying and developing the proficiencies of all employees, and enhancing ongoing diversity, equity and inclusion initiatives. Human capital is developed through a variety of strategies, including:

Diversity, equity, and inclusion - affirmatively recruiting (in some instances, through specialized recruitment platforms), promoting, and developing an increasingly diverse group of current and prospective employees

Equal employment opportunity – the Company is an affirmative action employer, and its policies prohibit discrimination in hiring, training, promotion, compensation or in any other aspect of employment based on race, religion, sex, sexual orientation, national origin, ancestry, marital status, disability, medical condition, age, genetic information, military service, or any other basis prohibited by state and local law

Freedom of association and collective bargaining – by policy, the Company recognizes employees’ rights and protections, as provided by the National Labor Relations Act, to choose or not choose to affiliate with legally sanctioned organizations or associations without unlawful interference; none of the Company’s employees are represented by collective bargaining agreements

Limited use of temporary employment – The vast majority (98.9%) of the Company’s workforce are considered permanent employees and temporary employment is only used for short-term staffing needs, with 1.1% of employees on temporary contracts

Support for human rights – by policy, the Company is committed to human rights in the workplace, and is committed to the principles outlined in the United States Department of State Human Rights and Democracy Policy Statement, and prohibits the use of forced labor and child labor

Confidential channels for reporting – publicizing and promoting, through policy, employees’ ability to anonymously report workplace, off-duty, and Code of Conduct matters through EthicsPoint

Competitive compensation practices – paying competitive wages, including a minimum wage of $12.50/hr., a comprehensive health plan, a 401(k) plan, and an employee stock ownership plan

Opportunities to earn variable pay – a bonus plan, various sales and referral incentive programs, and individual performance-based bonuses are available

Training – providing an extensive in-house training program with specific programs provided for key supervisory and non-supervisory positions

Education Assistance Program – providing reimbursements for job-related outside education, including college level courses

Annual performance development reviews – written performance development reviews and coaching sessions conducted each year for every employee

Career development - identifying high potential candidates and providing specifically tailored plans developing their careers

Management Succession Plan – annually identifying high potential employees for development and opportunities for internal promotions

13

Employee appreciation and recognition – conducting monthly anniversary lunches in celebration of work anniversaries, holding annual employee appreciation events, and providing specific written and other recognition to employees who have gone “above and beyond”

Anti-harassment policy and training – prohibiting harassment, discrimination and retaliation, and providing annual training on anti-harassment, anti-retaliation, and anti-discrimination policies

Employee health and safety – promoting health and safety, including: a smoke free, drug free and weapon free workplace; an Employee Assistance Program for mental health and other counseling; a Smoker Cessation Program; and subsidies for gym memberships

Employee Assistance Program – providing personal counseling and a variety of resources for mental and emotional well-being, healthy lifestyles, family and relationships, legal and financial issues, and work/life balance and transitions; the program is available to all full-time employees

Special leave – providing paid short-term leave for personal or family illnesses and other personal reasons, military leave, long-term leaves of absences for medical, parental, family care, or personal reasons, available to all full-time employees

Dependent Care Benefit – providing a dependent care benefit under its Flexible Benefit Plan, available to all full-time employees

COVID-19 Pandemic response - providing moral and economic support to employees through plans for maintaining safe operations, constant and consistent communication, and a variety of compensation and incentive strategies for employees affected by the pandemic, including but not limited to subsidies for child care obligations for employees affected by distance learning and school closures

Employee Engagement

We conduct a survey of all employees biennially to measure and promote employee engagement and satisfaction with a variety of other workforce matters including training, development, compensation and work environment. For the most recent survey conducted in 2018, favorable responses to the survey categories ranged from a high of 93% to a low of 68%, and 62% of the questions measured above the industry norm. Survey participants can also provide comments and suggestions for consideration.

Gender Diversity

The Company promotes fair and equitable treatment of women in its workforce. The Company has an inclusive culture, holding an annual event celebrating and promoting the accomplishments of its women. It also strictly prohibits gender bias and discrimination, and sexual harassment. A majority of the Company’s employees are women and there is significant representation of women in management and the executive team.

Percentage of women in the overall workforce | 75.0% |

Percentage of women in management positions | 67.6% |

Percentage of women in the executive team | 15.7% |

14

Government and Community Relations

BancFirst Corporation operates only within the United States, in Oklahoma and Texas. Also, the Company does not engage in offering offshore banking services, or other activities enabling tax base erosion and profit shifting to other jurisdictions. In compliance with the Bank Secrecy Act, the Company reports numerous Suspicious Activity Reports to the Treasury Department regarding possible money laundering or other criminal activities, and it cooperates with law enforcement agencies in their investigations of such activities. It has policies regarding government and community relations, addressing and restricting political activities of the Company and its employees, but encouraging support of community development activities. By policy and law, the Company is prohibited from making contributions or expenditures related to a political campaign or election, or to a political action committee. Also, the Company has not received any grants, tax relief, or other types of financial benefits such as assistance payments or bailouts, from any government. Additionally, the Company did not borrow from the Federal Reserve’s Paycheck Protection Program Liquidity Facility to fund the PPP loans that it made.

15

Managing Environmental Risk

Overview

Managing environmental risk supports long-term value creation. Environmental risks, such as pollution, changing climate and exploitation of natural resources, can adversely affect the Company, our customers, and our communities. The impacts of Government regulation of environmental risks must also be considered. The Company has responded to certain environmental risks to its business for many years, but we are developing processes to assess and respond to new and emerging risks on a more comprehensive basis.

Environmental Impact of Financing Activities

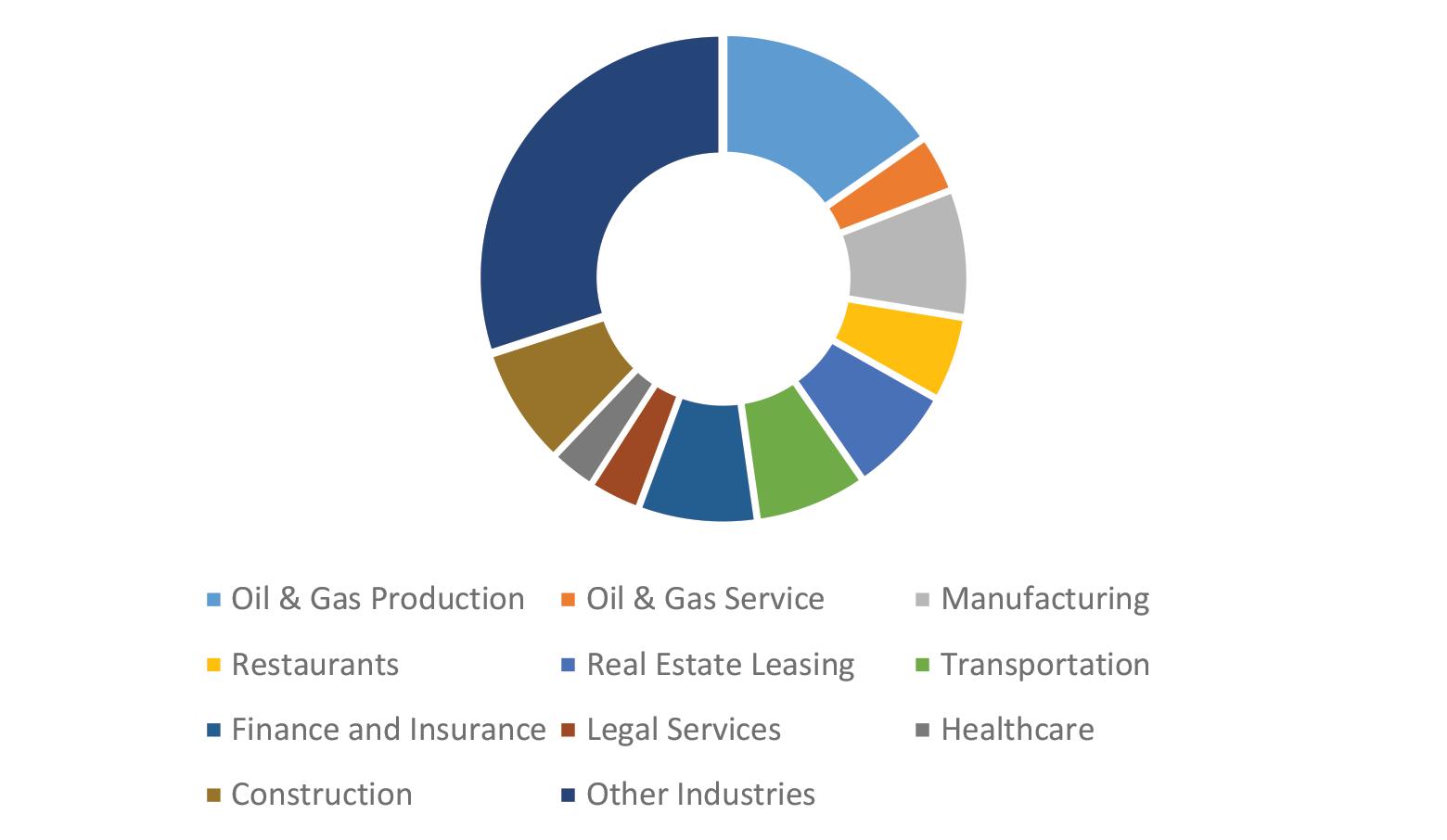

The Company operates in Oklahoma and Texas, which have economies that are significantly influenced by the energy industry and other industries that could be impacted by environmental risks. Below is a schedule listing the top 10 industries represented in the Company’s commercial and industrial loans.

Industry | Number of Loans | Balance |

Oil & Gas Production | 346 | $219,200,000 |

Oil & Gas Service | 258 | $54,390,000 |

Manufacturing | 710 | $121,565,000 |

Construction | 1,449 | $112,992,000 |

Finance & Insurance | 144 | $112,937,000 |

Transportation | 675 | $106,281,000 |

Real Estate Leasing | 393 | $102,921,000 |

Restaurants | 560 | $80,324,000 |

Legal Services | 485 | $49,264,000 |

Health Care | 358 | $43,341,000 |

Other Industries | 4,793 | $430,234,000 |

Total Commercial & Industrial | 10,171 | $1,433,449,000 |

16

The Company’s loan policies limit its exposure to oil & gas industry related collateral by setting the maximum amount of loans secured by oil & gas production and equipment at 55% of its equity capital, and the actual percentage is well below this limit at approximately 22%. The aggregate balance of all the Company’s loans related to the oil & gas industry is approximately $369 million, which is only 6.1% of its total loan portfolio.

The Company does not participate in any significant project financing that would have environmental considerations.

Energy and Paper Efficiency

The Company has several initiatives to improve its energy efficiency and use of paper. These initiatives include:

Converting lighting systems to LED

Installing geothermal heat pumps in new facilities

Using building automation systems to better manage HVAC systems

Building Intelligent Teller Machine (ITM) facilities rather than larger manned facilities

Upgrading systems in its new headquarters building to energy efficient systems, including completely replacing the glass exterior with thermal glass and adding motion sensor light switches

Purchasing EPEAT registered information technology equipment (85% of the equipment is Energy Star compliant)

Reducing paper usage through increased utilization of digital systems and processes

Shredding and recycling of most of its paper waste

17