A Leading National Supplier of a Wide Variety of

Components for RV’s and Manufactured Homes

Drew Industries (NYSE:DW)

2003

Forward Looking Statements

This presentation contains certain “forward-looking statements” within the meaning of the Private Securities

Litigation Reform Act of 1995 with respect to financial condition, results of operations, business strategies,

operating efficiencies or synergies, competitive position, growth opportunities for existing products, plans and

objectives of management, markets for the Company’s common stock and other matters. Statements in this

presentation that are not historical facts are “forward-looking statements” for the purpose of the safe harbor

provided by Section 21E of the Exchange Act and Section 27A of the Securities Act. Forward-looking statements,

including, without limitation those relating to our future business prospects, revenues, expenses and income,

wherever they occur in this presentation, are necessarily estimates reflecting the best judgment of our senior

management, at the time such statements were made, and involve a number of risks and uncertainties that could

cause actual results to differ materially from those suggested by forward-looking statements. The Company does

not undertake to update forward-looking statements to reflect circumstances or events that occur after the date the

forward-looking statements are made. You should consider forward-looking statements, therefore, in light of

various important factors, including those set forth in this presentation and the Company’s SEC filings.

There are a number of factors, many of which are beyond the Company’s control, which could cause actual results

and events to differ materially from those described in the forward-looking statements. These factors include pricing

pressures due to domestic and foreign competition, costs and availability of raw materials (particularly steel and

related components, vinyl, aluminum, glass and ABS resin), availability of retail and wholesale financing for

manufactured homes, availability and costs of labor, inventory levels of retailers and manufacturers, levels of

repossessed manufactured homes, the disposition into the market by FEMA by sale or otherwise of RVs or

manufactured homes purchased by FEMA in connection with natural disasters, changes in zoning regulations for

manufactured homes, the decline in the manufactured housing industry, the financial condition of our customers,

retention of significant customers, interest rates, oil and gasoline prices, the outcome of litigation, and adverse

weather conditions impacting retail sales. In addition, national and regional economic conditions and consumer

confidence may affect the retail sale of recreational vehicles and manufactured homes.

Page 2

About Drew Industries

A leading national

manufacturer of

quality components

for Recreational

Vehicles (RV) and

Manufactured

Homes (MH)

Page 3

Headquartered in White

Plains, New York – 10

employees

41 manufacturing facilities in

the U.S.

Approximately 4,000

employees nationwide

Organic growth from 2001

through 6/30/07 was over

$180 million or a 10%

average annual growth,

excluding price increases,

acquisitions, and FEMA

business

Company Overview

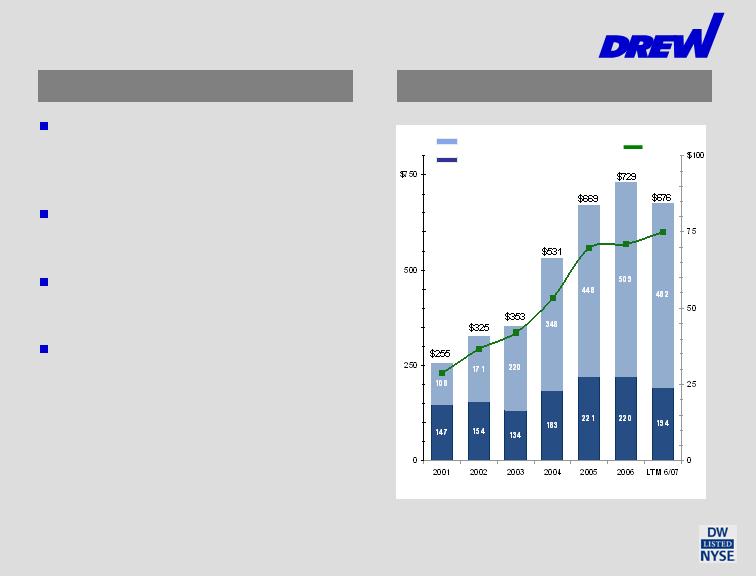

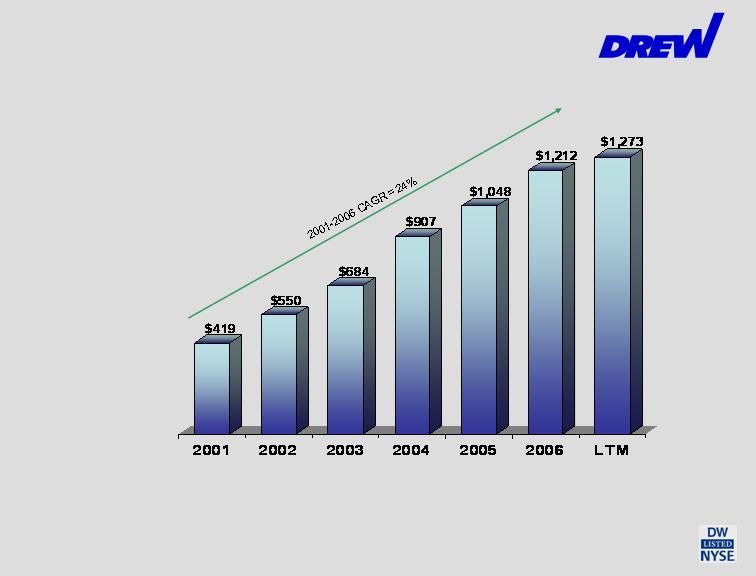

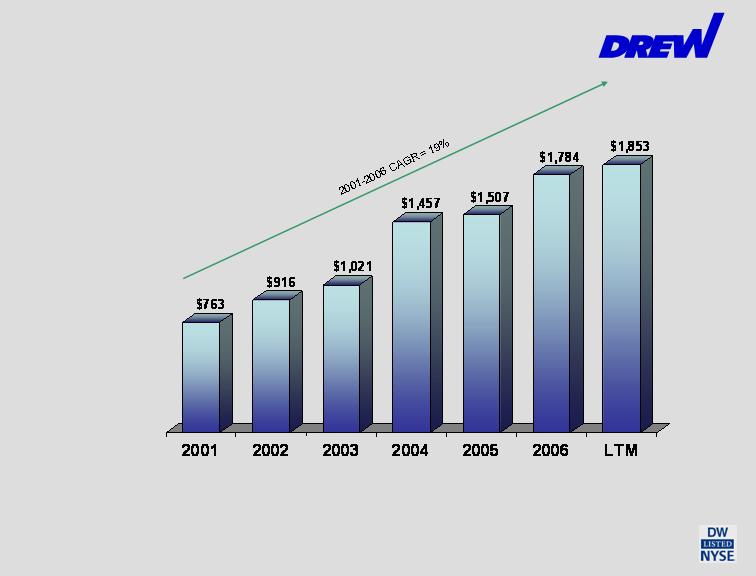

Financial Performance

Sales and EBITDA (in millions)

MH segment sales

RV segment sales

EBITDA(1)

(1)

2001- June 2007 EBIDTA CAGR = 19%. EBITDA is

operating profit plus depreciation and amortization

Page 4

Drew’s Companies

Kinro, Inc. – Acquired 1980

Aluminum windows for RVs

Doors for RVs and MHs

Aluminum and vinyl windows and screens for MHs

Bath and shower units, and sinks for MHs and RVs

Exterior panels for RVs

Lippert Components, Inc. – Acquired 1997

Chassis and chassis parts for RVs and MHs

Slide-out mechanisms and leveling devices for RVs

Axles for towable RVs, MHs and specialty trailers

Bed lifts and ramp doors for “toy-hauler” RVs

Steps for RVs

Suspension systems

Specialty trailers for boats, personal watercraft and

hauling equipment

Page 5

Drew’s Segments – LTM 6/30/07

MH = $16 million

23%

RV = $52 million

77%

Revenues - $676 million

90% of RV segment revenues

are for towable RVs

Segment Operating Profit - $68 million

MH = $194 million

29%

RV = $482 million

71%

Page 6

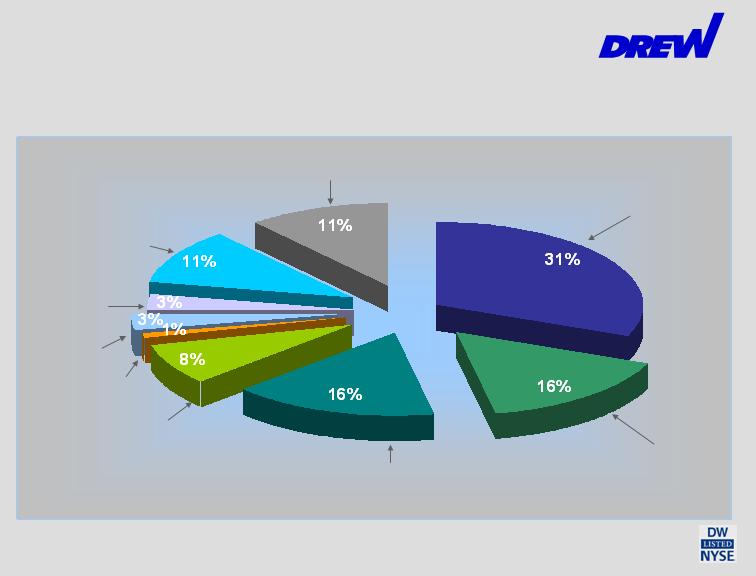

Drew’s Products

RV Chassis and Chassis Parts:

$200 million

RV Windows and Doors:

$109 million

12 Months Ended June 30, 2007

Sales - $676 million

Other: $7 million

MH and RV

Bath Products:

$23 million

Specialty

Trailers:

$20 million

RV Slide-out mechanisms:

$107 million

RV and MH Axles and

Tires: $57 million

Page 7

MH Chassis and Chassis

Parts: $76 million

MH Windows, Doors and

Screens: $77 million

Supplier to Industry Leaders

Outstanding customer service and national coverage, with 41

production facilities (more than 3 million sq. ft.), make us a key

partner with our customers.

Supply most of the Leading Producers of RVs and MHs:

Both RV and MH

Fleetwood (NYSE:FLE)

Skyline (NYSE: SKY)

RV

Coachmen (NYSE: COA)

Forest River (owned by Berkshire Hathaway)

Monaco Coach (NYSE: MNC)

Starcraft (privately owned)

Thor (NYSE:THO)

MH

Champion (NYSE: CHB)

Clayton (owned by Berkshire Hathaway)

Oakwood Homes and Southern Energy Homes

(owned by Clayton)

Palm Harbor (Nasdaq: PHHM)

Page 8

Business Strategy

Increase sales and profitability through:

Market share growth

New product introductions

Strategic acquisitions

This strategy accomplished through:

Outstanding customer service

Motivating management through profit incentives and training

programs

Maintaining highly efficient factories by optimizing production

efficiencies through state-of-the-art manufacturing technology, and

stringent cost controls

Extensive R & D efforts

Disciplined and patient acquirer

Page 9

Content Per Vehicle - RV

Peak potential is $2,500 to $2,800 per RV

(a)

Excludes sales of specialty trailers.

(b)

Excludes sales of Emergency Living Units (“ELU’s”) purchased by FEMA.

90% of RV segment sales are for Towable RVs

See Page 17 for Industry Information

Page 10

Operating

profit margin 8.6% 9.4% 11.3% 9.2% 9.6% 8.6% 10.8%

6/30/07

(a)(b)

(a)(b)

(a)

(a)

Content Per Home - MH

Peak potential is $3,300 to $3,600 per home

Operating

Profit margin 10.8% 11.0% 10.7% 10.1% 10.2% 9.5% 8.2%

See Page 21 for Industry Information

Page 11

6/30/07

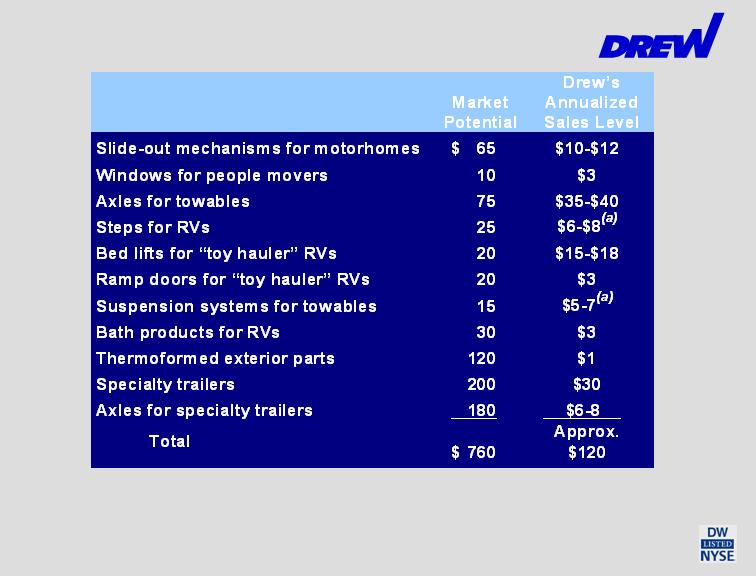

New Product Introductions

Annualized sales of these products increased from about $100 million in the

2nd quarter of 2006.

(in millions)

Page 12

(a)

Including recent acquisitions.

Acquisition Criteria

Drew is a disciplined and patient

acquirer

Target less than 6 times pro forma EBITDA

Immediately accretive

Complementary to our core RV and MH markets

Strategic

Acquisitions

Seek to acquire products or technologies that we can

introduce through our nationwide customer base and

factory network

Become a more extensive supplier to our customers

Page 13

Acquisition History

Strategic

Acquisitions

May 2004

Zieman

RV, MH and

specialty trailers.

Annual sales of over

$40 million

Each of our RV and MH acquisitions has

expanded geographic markets or

broadened product lines

July 2007

Extreme Engineering

Custom boat trailers.

Annual Sales of $12

million

2001

Better Bath

Bath and shower

products for MH.

Annual sales of

$20 million

14 Acquisitions

1980 – 2003

Including Kinro (1980)

and Lippert

Components (1997)

March 2006

Steelco

MH & RV Chassis.

Annual sales

of $8 million

May 2007

Coach Step

Electric steps

for motorhomes.

Annual sales of

$2 million

Page 14

May 2005

Venture Welding

MH Chassis. Annual

sales of $18 million

June 2006

Happijac

Bed lifts for

“toy haulers”.

Annualized sales

of $15 million

January 2007

Trailair/Equa-Flex

RV Suspension Systems.

Annual sales of $3 million

Drew’s Management Team

Highly respected and experienced

management:

Drew

Leigh Abrams, CEO, 35+ years

Fred Zinn, CFO, 25+ years

Kinro

David Webster, CEO, Chairman,

30+ years

Lippert

Jason Lippert, CEO, Chairman

12+ years

Excellent management training

and incentive programs

Innovative &

Experienced

Management

Leigh Abrams

David Webster

Page 15

Jason Lippert

Investments

Kinro and Lippert have

extensive R&D departments

Since January 1997:

Invested over $157 million in

plant and equipment

Invested nearly $179 million

for acquisitions

Invested $40 million for stock repurchases at an average

price of $5.37 per share

These investments have been accretive to earnings

Page 16

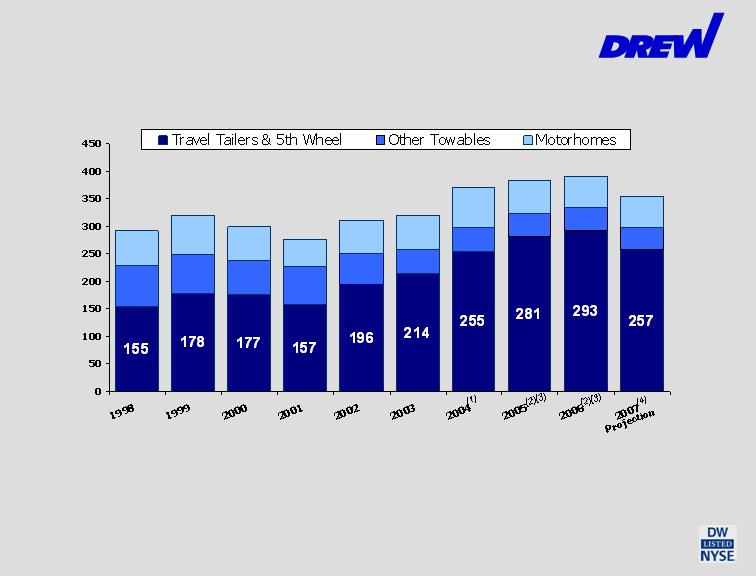

RVs - Industry Wholesale Shipments

(Thousands of Vehicles)

90% of Drew’s current RV product sales are for Travel Trailers and 5th Wheel RVs

(1)

Includes approximately 13,500 RVs purchased by FEMA for emergency housing for 2004 hurricane victims.

(2)

Excludes 38,900 ELU’s in 2005 and 31,400 ELU’s in 2006 purchased by FEMA. A total of 70,300 ELU’s were

purchased by FEMA for the period 9/05 to 4/06. The Company’s sales content per ELU was significantly less

than that of a typical travel trailer.

(3)

Starting in September 2005, about 27,000 towable RVs were purchased by FEMA from dealers which were

replaced by the dealers in 2005 and 2006.

(4)

Projection by RVIA. A portion of decline is attributable to FEMA units produced in 2006.

293

321

257

311

321

370

391

300

384

Page 17

41

57

42

56

355

RV Market

86% of industry 2006 unit sales

50% of wholesale dollar sales

Retail cost $4,000 to $100,000

per unit. Average about $20,000

From 1998 to 2006 the travel

trailer and 5th wheel market grew

at an annual rate of

approximately 8%, compared to

a 2% annual decrease in

motorhome shipments.

14% of industry 2006 unit sales

50% of wholesale dollar sales

Retail cost $41,000 to $400,000+

per unit. Average about $100,000

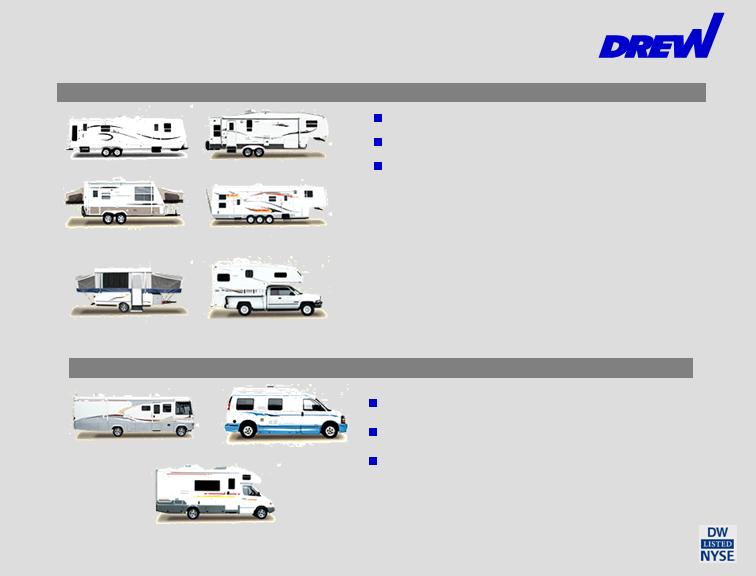

TOWABLE RVS (90% of Drew’s RV revenues)

MOTORHOMES

Travel trailer with

expandable ends

Type A Motorhomes

Type B Motorhomes

Type C Motorhomes

Folding camping trailer

Travel trailer

Folding camping trailer

Sport utility RV

Fifth wheel travel trailer

Truck camper

Page 18

Growth In RV Market

Positive Demographic

Trends

Primary owners of RVs are

50 and over

According to census

projections, there are

expected to be 20 million

more people over 50 by 2014

Strong Growth

Prospects

Industry Advertising Campaign

Target Market 30 and over

Post 9/11 security concerns and high airline ticket

prices increase RV travel use

Fifth Wheel RV

Page 19

How RVs Are Used

Shift in U.S. culture

toward more RV-related

activities

NASCAR events

College and NFL football

games

“Toy Haulers”

More economical family

vacations

Typical RV family vacation

up to 74% less expensive

Strong Growth

Prospects

Many RVs are “parked”over the long-term

as second homes

Travel Trailer

Page 20

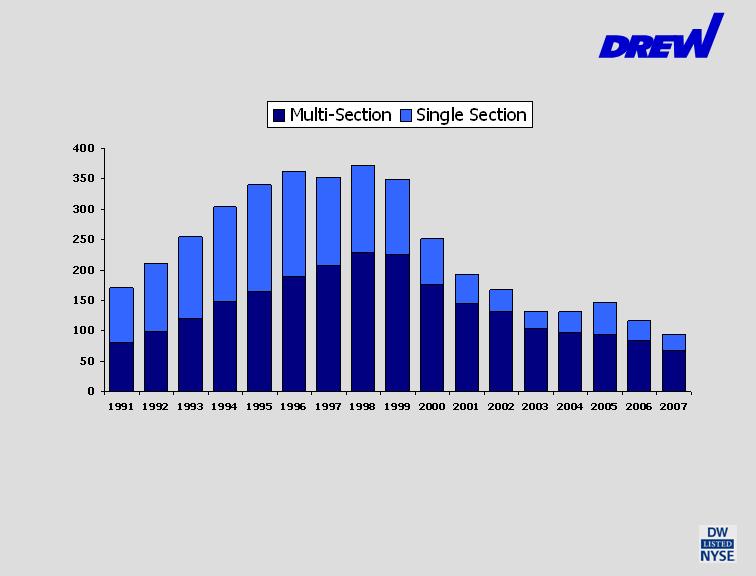

MH - Industry Production

171

211

254

304

340

363

353

373

349

(Thousands of Homes)

131

168

193

251

(1)

131

(1)

Includes approximately 3,500, 15,000 and 3,000 for 2004, 2005 and 2006, respectively,

MHs purchased by FEMA for emergency housing for hurricane victims.

(2)

Estimate by Company management.

(1)

147

(1)

117

Drew’s MH segment remained profitable every quarter since 1998.

47%

61%

59%

52%

49%

49%

47%

47%

75%

70%

65%

78%

74%

80%

72%

64%

Page 21

95

71%

Estimate (2)

Manufactured Housing (MH) Market

Cost per sq. ft. is $39 for MH vs.

$91 for site-built homes

Average retail price of $62,300

for a 1,595 sq. ft. MH

9 million manufactured homes

across the U.S.

Strong Growth

Prospects

Improved quality, appearance and safety

Studies have shown that MH built since 1995 sustain no more

damage in hurricanes than site-built homes

Industry production was down 69% from 1998 to 2006, but

Drew’s MH sales were up 13% and segment operating profit was

down only 20%

Page 22

MH: Industry Financing

Trends

Improved lending practices

Conventional financing more common than

chattel; improves collateral

Recent increase in loan applications

Recent increase in manufacturer order

backlogs

Subprime market woes could help MH

Pressure on Fannie Mac/Freddie Mac to

support MH loans

Strong Growth

Prospects

Page 23

MH: Other Favorable Factors

Baby Boomers retiring in

increasing numbers

Appropriate inventory

levels

Affordability and quality

New HUD code

Potential for rebuilding

the Gulf Coast

Strong

Growth

Prospects

Page 24

Improved industry image

Advertising campaign being developed

Berkshire investments

Drew’s Ownership and Governance

Executives and Directors currently own 11%.

Drew’s Corporate Governance Program –

ranked in the 87th percentile of all Russell 3000

Companies by Institutional Shareholder

Services.

Added to S&P SmallCap 600 Index in October

2005

Page 25

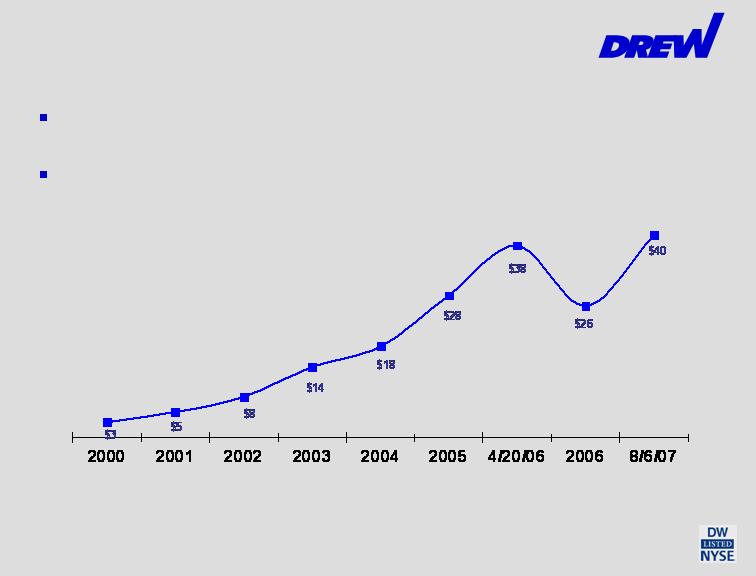

Financial Performance

The price of Drew’s common stock is nearly 14 times the price

as of December 31, 2000

Drew has 21.8 million shares outstanding and a market

capitalization of more than $850 million as of August 6, 2007

(December 31 unless noted)

Stock Price History

Drew effected a 2-for-1 stock split on 9/7/05 to holders of record on 8/19/05

Page 26

Operating Results

Year Ended December 31, (except as noted)

Financial

Performance

(1)

Excluding the estimated impact of hurricane-related sales from both 2006 and 2005, the Company

estimates that diluted EPS would have been approximately $1.33 in 2006, compared to approximately

$1.40 in 2005.

(2)

Sales during the latter part of 2006 and the first half of 2007 were negatively impacted by weakness in

both the RV and MH industries.

(3)

Adjusted for 2 for 1 stock split on 9/7/05.

(4)

EBITDA is operating profit plus depreciation and amortization (see page 37).

Page 27

($ in millions, except EPS)

2004

2005

200

6

(2)

LTM

6/07

(2)

LTM

6/07 vs

2006

Sales

$

531

$

669

$

7

29

$

676

-

7%

Operating Profit

$

44.0

$

57.7

$

55.3

$

57.4

+4%

% of Sales

8.3

%

8

.

6

%

7

.

6

%

8.5%

Net Income

$

25.1

$

33.6

$

3

1.0

$

32.7

+6%

Diluted EPS

(1

)

(3

)

$

1

.18

$

1

.56

$

1

.42

$

1.49

+5%

EBITDA

(4

)

$

53.3

$

69.7

$

71.0

$

74.7

+5%

Results By Segment

Year Ended December 31, (except as noted)

Financial

Performance

Page 28

(a)

After a charge of $1.4 million and $0.8 million for 2004 and 2005, respectively, related to legal

proceedings, net of related incentive compensation.

(b)

After a gain of $0.8 million related to the sale of closed facilities, net of related incentive compensation.

(c)

Sales during the latter part of 2006 and first half of 2007 were negatively impacted by weakness in both the

RV and MH industries.

See Form 10-K filed March 13, 2007 for a reconciliation to 2004 through 2006 consolidated results.

See page 38 for reconciliation to LTM 6/07 consolidated results.

10.8%

8.2%

8.6%

9.5%

9.6%

10.2%

9.4%

9.6%

Operating Profit as a

Percentage of Net sales

RV Segment

MH Segment

$ 52.1

$ 15.8

$ 43.9

$ 21.0 (b)

$ 43.1

$ 22.6(a)

$ 32.6

$ 17.7(a)

Operating Profit

RV Segment

MH Segment

$ 482.5

$ 193.7

$ 508.8

$ 220.4

$ 447.7

$ 221.5

$ 346.2

$ 184.7

Net Sales

RV Segment

MH Segment

LTM 6/07(c)

2006(c)

2005

2004

($ in Millions)

Operating Results

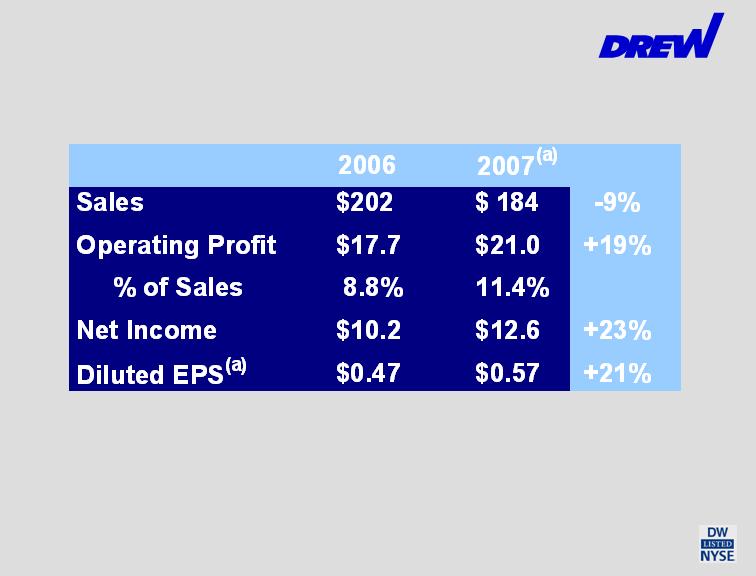

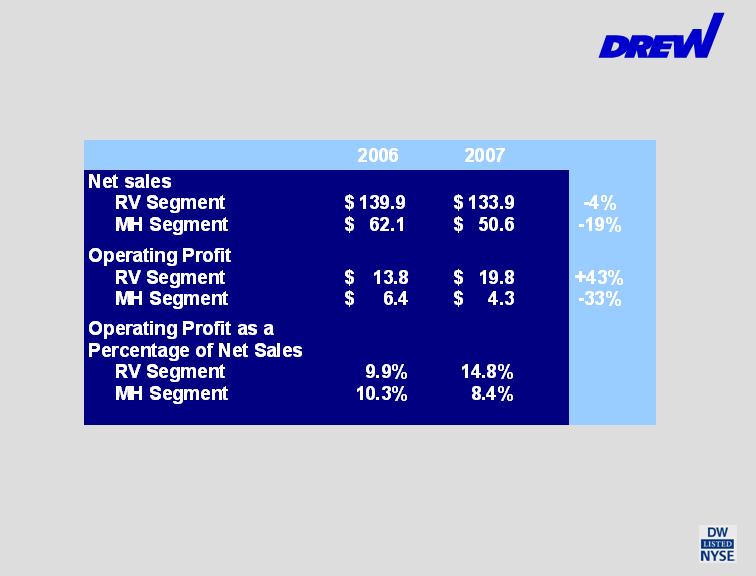

Three Months Ended June 30,

Financial

Performance

($ in millions, except EPS)

Page 29

(a)

Sales during the second quarter of 2007 were negatively impacted by weakness in both the RV

and MH industries.

Results By Segment

Three Months Ended June 30,

Financial

Performance

($ in millions)

Page 30

See Press Release dated July 31, 2007 for a reconciliation to consolidated results.

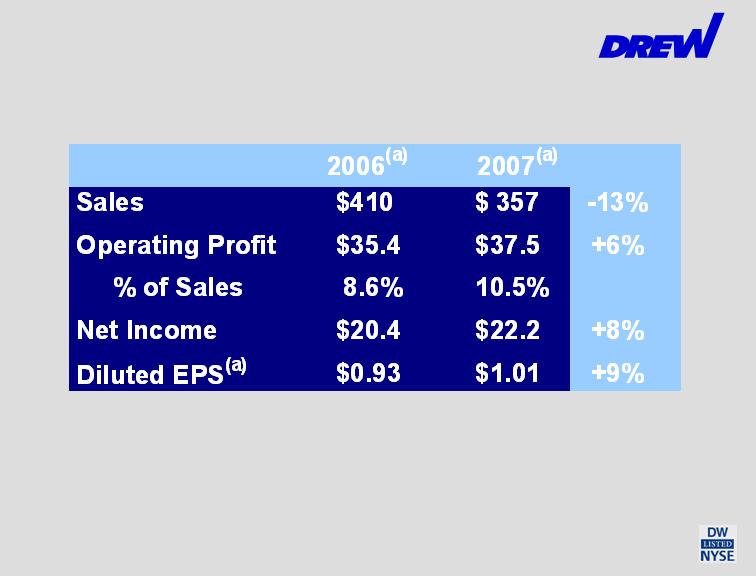

Operating Results

Six Months Ended June 30,

Financial

Performance

($ in millions, except EPS)

Page 31

(a)

Sales during the first six months of 2007 were negatively impacted by weakness in both the RV

and MH industries, while sales in the first six months of 2006 included approximately $20 million

of hurricane-related sales.

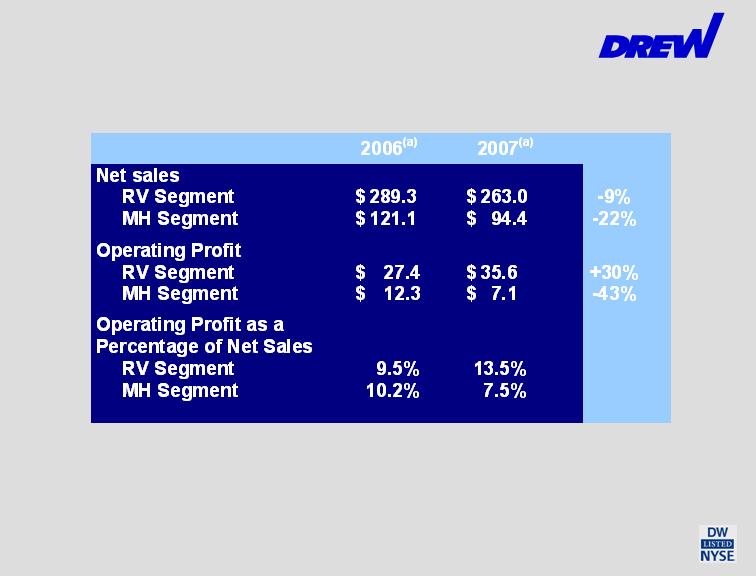

Results By Segment

Six Months Ended June 30,

Financial

Performance

($ in millions)

Page 32

See Press Release dated July 31, 2007 for a reconciliation to consolidated results.

(a)

Sales during the first six months of 2007 were negatively impacted by weakness in both the RV

and MH industries, while sales in the first six months of 2006 included approximately $20 million

of hurricane-related sales.

Balance Sheet

Financial

Performance

(1)

Days sales in accounts receivable is the most recent month’s net sales divided by accounts receivable, net,

at the end of the period.

(2)

Inventory turns is cost of goods sold for the last twelve months divided by average inventory for the last

twelve months.

Page 33

($ in millions)

Financial Strength

Financial

Performance

Page 34

(1) EBITDA is operating profit plus depreciation and amortization (see page 37).

12/31/04

12/31/05

12/31/06

LTM 6

/07

Return on Equity

23%

24%

16

%

16

%

Return on Assets

12%

12%

9

%

10

%

Total Debt to Equity

0.6

0.4

0.

3

0.

2

Total Debt to EBITDA

(1)

1

.3

1

.1

0.

8

0.

6

Peer Comparison

20%

13%

10.7

19.1

Spartan (SPAR)

(69%)

(4%)

28.7

N/A

Fleetwood (FLE)

16%

11%

19.0

27.4

Drew (DW)

ROE

ROA

Forward

P/E

Trailing

P/E

(1%)

1%

16.0

N/A

Monaco (MNC)

18%

11%

15.5

19.2

Thor (THO)

16.8

25.1

Winnebago (WGO)

16%

8%

Source: Capital IQ, August 7, 2007, except forward P/E, which is provided by

Thomson Financial and is based on fiscal 2007 analyst projections.

Financial

Performance

Page 35

Thank You

Analyst coverage:

Avondale Partners, LLC:

Kathryn Thompson (615) 467-5637

BB&T Capital Markets:

John Diffendal (615) 340-8284

Ferris, Baker Watts, Inc.

John T. G. Rogers (410) 659-4645

Sidoti & Company LLC:

Scott Stember (212) 453-7017

Susquehanna Financial Group, LLP:

Cheryl Cortez (312) 427-5236

For more information contact:

Leigh J. Abrams, President and CEO

914-428-9098

leigh@drewindustries.com

Fredric M. Zinn, Executive VP and CFO

914-428-9098

fred@drewindustries.com

Or visit: www.drewindustries.com

Page 36

Reconciliation of Operating Profit

to EBITDA

Financial

Performance

Page 37

($ in millions)

2001

2002

2003

2004

2005

2006

LTM

6

/07

Operating Profit

$20.3

$29.2

$34.3

$44.0

$57.7

$55.3

$57

.

4

Depreciation and

Amortization

$8.4

$7.3

$7.8

$9.3

$12.0

$15.7

$

1

7

.

3

EBITDA

$28.7

$36.5

$42.1

$53.3

$69.7

$71.0

$7

4

.

7

Capital Expenditures

$8.2

$

10.5

$5.1

$27.1

$26.1

$22.3

$

1

1

.

3

Results By Segment

Financial

Performance

Page 38

($ in millions)

Last

12

Months Ended

June 30,

2007

2006

Net sales

RV Segment

MH Segment

$

482.5

193.7

$

520.8

241.2

Total

Net Sales

$

676.2

$

762.0

Operating Profit

RV Segment

MH Segment

$

52.1

15.8

$

50.6

25.4

Total Segment

Operating Profits

67.9

76.0

Amortization of intangibles

(

3.5

)

(

1.7

)

Corporate and other

(

7.7

)

(

7.4

)

Other income

0.

7

0.

7

Total

Operating

P

rofit

$

57.4

$

67.6