Exhibit 13.1

POPULAR®

CONTENTS/ÍNDICE 1 Popular, Inc. Year in Review 3 Fast Facts 5 Our Values 6 Puerto Rico In the Face of Change 8 Key Drivers Behind Solid Performance 9 Succeeding in a Challenging Regulatory Environment 10 A Transformative 2013 Supported By A Robust Infrastructure 11 Popular, Inc. Management 12 25-Year Historical Financial Summary 14 Our Creed/Our People 15 Popular, Inc. – Resumen del Año 17 Cifras a la Mano 19 Nuestros Valores 20 Puerto Rico de Cara al Cambio 22 Impulsores Claves de un Desempeño Sólido 23 Teniendo Éxito en un Ambiente Legal y Regulatorio Desafiante 24 Un 2013 Transformador Apoyado por una Infraestructura Robusta 25 Popular, Inc. Gerencia 26 Resumen Financiero Histórico – 25 Años 28 Nuestro Credo/Nuestra Gente Popular, Inc. (NASDAQ:BPOP) is a full-service, financial provider based in Puerto Rico with operations in Puerto Rico and the United States. In Puerto Rico, Popular is the leading banking institution by both assets and deposits and ranks among the largest 40 banks in the U.S. by assets. With 180 branches in Puerto Rico and the Virgin Islands, Popular offers retail and commercial banking services, as well as auto and equipment leasing and financing, mortgage loans, insurance, investment banking and broker-dealer services. In the United States, Popular has established a community-banking franchise, doing business as Popular Community Bank, providing a broad range of financial services and products with branches in New York, New Jersey, Illinois, Florida and California. Popular, Inc. (NASDAQ: BPOP) es un proveedor financiero de servicio completo con sede en Puerto Rico y operaciones en Puerto Rico y los Estados Unidos. En Puerto Rico es la institución bancaria líder tanto en activos como en depósitos y se encuentra entre los 40 bancos más grandes de Estados Unidos por total de activos. Con 180 sucursales en Puerto Rico y las Islas Vírgenes, Popular ofrece servicios bancarios a individuos y comercios, así como arrendamiento y financiamiento de autos y equipo, préstamos hipotecarios, seguros, banca de inversión y transacciones de corredores de valores. En los Estados Unidos, Popular ha establecido una franquicia bancaria de base comunitaria, que opera bajo el nombre de Popular Community Bank y provee una amplia gama de servicios y productos financieros, con sucursales en Nueva York, Nueva Jersey, Illinois, Florida y California.

POPULAR, INC. 2 01 3 A n n u a l R e p o r t Popular, Inc. Year In Review POPULAR, INC. 2 01 3 A n n u a l R e p o r t RICHARD L. CARRIÓN Chairman, President and Chief Executive Officer I am pleased to report that Popular generated strong financial results in 2013. Our financial performance was driven by robust revenues and improving credit trends, which helped offset the impact of low demand stemming from continued economic weakness in Puerto Rico, our main market. We made considerable progress in our primary areas of focus: credit quality, business growth, our U.S. operation, and efficiency and organizational excellence. CREDIT QUALITY Credit quality has been a particular area of intense focus for all financial institutions since the financial crisis of 2008, and we are no different. I am pleased by the steady progress we have made in recent years in improving our credit metrics. But 2013 was truly a turnaround year. • Non-performing assets declined dramatically, from $2 billion or 5.5 percent of assets in 2012 to $932 million or 2.6 percent of assets by the end of 2013. • This improvement was the result of a combination of strategies. During the year, we completed two bulk sales involving approximately $944 million in non-performing assets which included commercial, construction and mortgage loans as well as commercial and residential other real estate owned. In addition, our credit administration groups continued working diligently on our loss mitigation efforts and loan resolutions and restructurings. • Other encouraging results include significant reductions in net charge-offs, excluding the impact of the bulk sales, and a substantial decline in non-performing loan inflows when compared to 2012. Despite the continued weakness of the Puerto Rico economy, we have not seen significant signs of stress in our loan portfolio in Puerto Rico. We remain cautious, but are encouraged by ongoing stability in our credit quality indicators. Expanded Insights We have redesigned our annual report to provide you additional outlooks and insights into our operations and markets. In their own words, the managers who lead some of the most vital areas of our Corporation walk you through the drivers behind our strategies to maximize long-term shareholder value. In addition to our annual shareholders letter that outlines key performance indicators, we have included a deeper look into our financial performance, as well as viewpoints about our main market in Puerto Rico, our risk-management blueprint and the increasingly challenging regulatory environment. BUSINESS GROWTH In 2013, we continued to identify potential areas where we could grow our business to offset the impact of the challenging economic environment. Despite market conditions in Puerto Rico, we continued strengthening our competitive position on the island, increasing our market share in most product categories and further distancing ourselves from other financial providers. • Our total loan book increased by 4 percent in 2013, driven mainly by an increase in mortgage balances. The growth of our 1

POPULAR, INC. 2 01 3 A n n u a l R e p o r t Popular, Inc. POPULAR STOCK PRICE CHANGE VS PEERS (2013) Percent 60 50 40 30 20 10 0 -10 12/12 1/13 2/13 3/13 4/13 5/13 6/13 7/13 8/13 9/13 10/13 11/13 12/13 BPOP PR PEER AVG. US PEER AVG. KBW INDEX In 2013, we continued to identify potential areas where we could grow our business to offset the impact of the challenging economic environment. Despite market conditions in Puerto Rico, we continued strengthening our competitive position on the island, increasing our market share in most product categories and further distancing ourselves from other financial providers. mortgage portfolio was the result of strong origination volume, supplemented with several portfolio acquisitions amounting to approximately $761 million. • Initiatives to grow our auto financing business also yielded very positive results, leading to a 13 percent increase in this portfolio. • The commercial loan portfolio increased by 3 percent, with higher activity in the corporate segment offsetting lower demand in the small and middle segments, which are more susceptible to weak economic conditions. Though we are not expecting an improvement in market conditions in Puerto Rico in the short term, we have proved that we can generate healthy revenues, even in trying times, and are uniquely poised to benefit from an eventual economic recovery. POPULAR COMMUNITY BANK Popular Community Bank (PCB) has made significant progress in recent years. • Financial results have improved substantially as a result of lower credit costs and effective expense management. • However, slow demand for commercial loans remains the biggest challenge. As a result, we launched a series of niche lending initiatives to generate additional loan volume. While these efforts are still in a development stage, we have observed encouraging results in several of them. In addition, we took advantage of several opportunities to acquire loan portfolios, adding approximately $411 million in mortgages to our loan book. We still have a long way to go with regards to PCB. But these improvements put PCB in a better position and grant us greater flexibility as we evaluate strategic alternatives for our U.S. operation. Fundamental Resources And Skills Of course, the successful execution of current and future business strategies at Popular depends on the quality of our organization’s 2

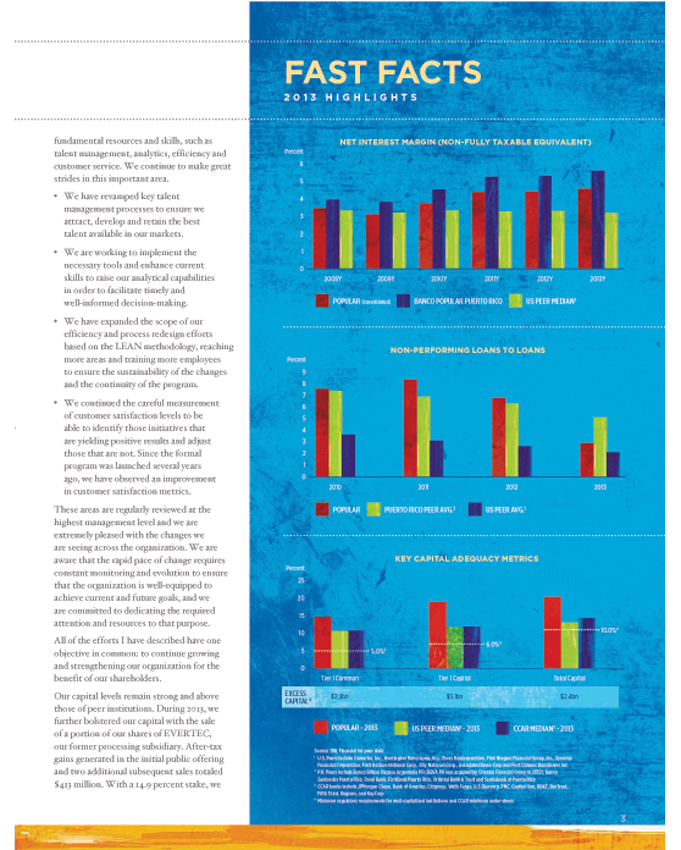

FAST FACTS 2 0 1 3 H I G H L I G H T S fundamental resources and skills, such as talent management, analytics, efficiency and customer service. We continue to make great strides in this important area. • We have revamped key talent management processes to ensure we attract, develop and retain the best talent available in our markets. • We are working to implement the necessary tools and enhance current Percent 6 5 4 3 2 1 0 NET INTEREST MARGIN (NON-FULLY TAXABLE EQUIVALENT) skills to raise our analytical capabilities in order to facilitate timely and 2008Y 2009Y 2010Y 2011Y 2012Y 2013Y well-informed decision-making. • We have expanded the scope of our efficiency and process redesign efforts POPULAR (consolidated) BANCO POPULAR PUERTO RICO US PEER MEDIAN1 based on the LEAN methodology, reaching more areas and training more employees to ensure the sustainability of the changes and the continuity of the program. • We continued the careful measurement of customer satisfaction levels to be able to identify those initiatives that are yielding positive results and adjust those that are not. Since the formal program was launched several years ago, we have observed an improvement Percent 9 8 7 6 5 4 3 2 1 0 NON-PERFORMING LOANS TO LOANS in customer satisfaction metrics. These areas are regularly reviewed at the highest management level and we are extremely pleased with the changes we are seeing across the organization. We are 2010 POPULAR 2011 PUERTO RICO PEER AVG.2 2012 US PEER AVG.1 2013 aware that the rapid pace of change requires constant monitoring and evolution to ensure that the organization is well-equipped to achieve current and future goals, and we are committed to dedicating the required attention and resources to that purpose. All of the efforts I have described have one objective in common: to continue growing and strengthening our organization for the Percent 25 20 15 10 5 0 5.0%4 KEY CAPITAL ADEQUACY METRICS 6.0%4 10.0%4 benefit of our shareholders. Our capital levels remain strong and above those of peer institutions. During 2013, we further bolstered our capital with the sale EXCESS CAPITAL 4 Tier 1 Common Tier 1 Capital Total Capital $2.3bn $3.1bn $2.4bn of a portion of our shares of EVERTEC, our former processing subsidiary. After-tax POPULAR - 2013 Source: SNL Financial for peer data US PEER MEDIAN1 - 2013 CCAR MEDIAN3 - 2013 gains generated in the initial public offering and two additional subsequent sales totaled $413 million. With a 14.9 percent stake, we 1 U.S. Peers include Comerica, Inc., Huntington Bancshares, Inc., Zions Bancorporation, First Niagara Financial Group, Inc., Synovus Financial Corporation, First Horizon National Corp., City National Corp., Associated Banc-Corp and First Citizens Bancshares Inc. ² P.R. Peers include Banco Bilbao Vizcaya Argentaria PR (BBVA PR was acquired by Oriental Financial Group in 2012), Banco Santander Puerto Rico, Doral Bank, FirstBank Puerto Rico, Oriental Bank & Trust and Scotiabank of Puerto Rico 3 CCAR banks include JPMorgan Chase, Bank of America, Citigroup, Wells Fargo, U.S. Bancorp, PNC, Capital One, BB&T, SunTrust, Fifth Third, Regions, and KeyCorp Minimum regulatory requirements for well-capitalized institutions and CCAR minimum under stress 3 POPULAR, INC. 2 01 3 A n n u a l R e p o r t

POPULAR, INC. 2 01 3 A n n u a l R e p o r t Popular, Inc. Year In Review If I have learned one thing in recent years, it is that our people, 8,000 strong, thrive in the most difficult of times and outdo themselves under challenging circumstances. remain a large shareholder of EVERTEC, which continues to be an important business partner and a source of income for Popular. Given our strong capital levels, there has been significant interest regarding the timing and structure of an eventual repayment of TARP funds. We are eager and ready to repay TARP. In October of 2013, we submitted a formal application to our regulators indicating our desire to repay and we remain in constant communication with them regarding this matter. While we cannot provide specific details on the repayment plan yet, let me reassure you that our objective is, and has always been, to repay these funds in a manner that is most beneficial for our shareholders. The upward trend in our stock price during 2012 continued in the early months of 2013, and the stock price had risen 65 percent by mid-August. However, the share price began to deteriorate as concerns with Puerto Rico’s fiscal and economic situation began to grow. Notwithstanding the decline in the second half of the year, BPOP closed 2013 at $28.73, an increase of 38 percent when compared with 2012. OUR ORGANIZATION As we announced in January of 2013, Jorge A. Junquera, who had served as our Chief Financial Officer (CFO) for 16 years, assumed the role of Vice-Chairman and Special Assistant to the CEO. Carlos J. Vázquez, who has held various important positions in our organization, succeeded Jorge as CFO. The transition was better than seamless, with both Jorge and Carlos growing into their new roles for the benefit of the organization. Our Board of Directors also received a significant inflow of talent and energy with the appointment of Joaquín E. Bacardí, III and John W. Diercksen. Mr. Bacardí is the President and Chief Executive Officer of Bacardi Corporation, a major producer and distributor of rum and other spirits. He brings extensive experience in the development and implementation of international marketing, sales and distribution strategies from more than 20 years of service at Bacardí. Mr. Diercksen was an Executive Vice President of Verizon Communications, Inc., responsible for key strategic initiatives related to the review and assessment of potential mergers, acquisitions and divestitures. Joaquín and John bring valuable skills and experience to Popular that will undoubtedly enrich our Board’s discussions and decisions. Popular has a first- rate Board of Directors and I consider it a privilege to have their guidance and support. I extend my most sincere gratitude to all of the Directors for their continued leadership. The year 2013 marked our 120th anniversary. Throughout 2013, we celebrated our history and reaffirmed our values, recognizing that they are at the core of everything we do. These values clearly spell out our commitment to our customers, our employees, our communities and our shareholders, as well as the principles that guide our behavior – innovation, integrity and excellence. In conclusion, we are proud of Popular’s achievements in 2013, but we are far from satisfied. The year 2014 brings its own set of challenges. The Puerto Rican economy has not recovered as we expected a year ago, and the island’s fiscal troubles will likely complicate matters going forward. Our operations in the U. S., while improving, are still not where we need them to be. Meanwhile, the regulatory environment and its requirements place increasing pressure on all financial institutions. Still, I am confident we are facing these challenges from a position of strength. Our revenue-generating capacity is formidable, thanks to our unique franchise in Puerto Rico. After a multi-year effort, credit quality is at or close to normalized levels. We continue to have a robust capital base, even as we seek to repay TARP. We are actively evaluating alternatives to improve the performance of our operations in the U.S. And we have buttressed those areas responsible for managing heightened regulatory requirements. If I have learned one thing in recent years, it is that our people, 8,000 strong, thrive in the most difficult of times and outdo themselves under challenging circumstances. We are aware of the headwinds we are facing, but we are also optimistic about the opportunities that lie ahead of us. We have clear objectives, the right team to pursue them and the determination to achieve them.I thank you for your continued support. Sincerely, RICHARD L. CARRIÓN CHAIRMAN, PRESIDENT AND CHIEF EXECUTIVE OFFICER 4

POPULAR, INC. 2 01 3 A n n u a l R e p o r t Our Values Social Commitment We work hand-in-hand with our communities. We are committed to actively promote the social and economic well-being of our communities. Customer We develop life-long relationships. Our relationship with the customer takes precedence over any particular transaction. We add value to each interaction by offering high quality personalized service, and efficient and innovative solutions. Integrity We live up to the trust placed in us. We adhere to the strictest ethical and moral standards through our daily decisions and action. Excellence We strive to excel each day. We believe there is only one way to do things: doing them right the first time while exceeding expectations. Innovation We are a driving force for progress. We foster a constant search for innovative ideas and solutions in everything we do, thus enhancing our competitive advantage. Our People Performance We have the best talent. We are leaders and work together as a team in a caring and disciplined environment. We are fully committed to our shareholders. We aim to attain a high level of efficiency, both individually and as a team, to achieve superior and consistent financial results based on a long-term vision. 5

POPULAR, INC. 2 01 3 A n n u a l R e p o r t Puerto Rico In the Face of Change The inauguration of the former art-deco headquarters of Banco Popular de Puerto Rico on April 11, 1939 sent a strong message of local resilience near the end of The Great Depression, from which Puerto Rico recovered to transform its economy from agrarian to industrial. Today, the building in the historic Old San Juan hosts the Banco Popular Foundation, a full-fledged branch and an exhibition hall where it explores socioeconomic issues of Puerto Rico. RicHARd cARRión Chairman, President and Chief Executive OfficerPUeRto Rico is on tHe cUsP oF An iMPoRtAnt tRAnsFoRMAtion. The legacy of decades of fiscal mismanagement and the toll of a prolonged recession have combined with a shifting global economy and a lower risk tolerance in the wake of the international financial crisis to create what some have called a perfect storm. 6 Without minimizing the extent of the challenges Puerto Rico faces, we remain optimistic about the prospects of Puerto Rico emerging from the current situation with a stronger and more vibrant economy. This optimism does not stem from blind faith. It comes from experience. The 120-year history of Popular has allowed us to witness events such as a change in sovereignty, two world wars, the Great Depression and devastating hurricanes. Throughout this history, we have seen Puerto Rico transform itself time and time again, a testament to our resilience and resourcefulness. The most important metamorphosis of the last century – the economy’s transformation from agrarian to industrial – produced a dramatic increase in standards of living, a gross domestic product per capita that, despite the recent years of stagnation, is the highest in Latin America and a manufacturing infrastructure that is recognized around the world for its leadership in pharmaceutical and medical- device products. We are now at the threshold of a second economic transformation – from an industrial to a knowledge-based and services economy. Readymade infrastructure, tested human capital, high enrollment in local universities, a modern communications and transportation infrastructure and a

POPULAR, INC. 2 01 3 A n n u a l R e p o r t solid legal and institutional framework are pillars Puerto Rico can build on. Leading institutional investors are taking notice. …we look forward to the opportunities that will arise from this important moment in our history, just as they have from past junctures… Stateside and local investors have purchased $1.6 billion in commercial and real estate assets in a span of three years. The local government has taken major steps toward addressing its fiscal issues and has enacted serious reforms to its public- pension system. We see a path of fiscal reconstruction similar to various countries with similar debt levels that, after serious fiscal reforms, have regained market access at favorable rates. Additional changes, however, are necessary to speed up an economic recovery and put the economy on a track of sustainable growth. Two areas we see as requiring urgent attention are energy and taxes. Reducing the high cost of energy on our island will liberate substantial capital for businesses and consumers and is critical to the long-term competitiveness of the island. Puerto Rico’s public electric utility sold energy to consumers, businesses and manufacturers at an average of 26 cents per kWh for the past three years. That is nearly three times more expensive than the average retail price of electricity per U.S. state (10.6 kWh). Opening energy generation to private and public-private partnerships can lower energy costs by generating competition and facilitate investment in natural gas and other clean sources of energy. Overhauling our tax system can generate greater stability in revenues, promote self-sufficiency and relieve workers and businesses from carrying the tax burden of a substantially large cash economy. New levies have generated additional revenues in the current fiscal year. While this has provided some relief to the government, we see it as only a short-term solution, not a long-term policy. There is room to maneuver into a more equitable and productive tax system. For example, while income taxes generated 30% of revenues in fiscal 2012, property taxes only accounted for about 4% of revenues. Most of the island’s residences are exempt from paying property taxes. Amid current economic pressures, Puerto Rico would be served best by a tax system that is more efficient to administer, simpler to comply with and better tuned to the island’s economic realities and persistent evasion. These actions are feasible. There is consensus across diverse circles that these two major issues need to be addressed. The private sector also has to adjust to these new economic realities by developing new products and services and finding untapped markets. Puerto Rican businesses can leverage our unique position in the hemisphere, which benefits from our relationship with the largest economy in the world as well as our cultural affinity with Latin America. We are encouraged by the healthy level of reinvention we see among the 1.5 million clients we serve at Banco Popular. We have financed acquisitions of nonoperational plants for local businesses that have successfully turned them into multipurpose operations serving local and regional markets. We are seeing new opportunities unfold in the tourism sector, which has recently drawn substantial investments from local and stateside investors, as it registered the highest number of hotel check-ins and occupancy rate in the last eight years. We are encouraged by plans to revitalize old industries with potential in the current global economy like the sugar cane industry, which can generate economic activity by helping lower the production costs of local rum distilleries that currently buy raw materials in international markets. We are inspired by the resolve of entrepreneurs and technicians who with hard work and careful study have expanded their local businesses to international markets. These are some pixels that form part of a larger emerging picture encouraging us to look beyond the current headlines. Popular has a privileged position with a broad view of the economy we have been an important part of for more than a century. We recognize and are prepared for the challenges ahead. But, more importantly, we look forward to the opportunities that will arise from this important moment in our history, just as they have from past junctures, and stand ready to actively support Puerto Rico in this new transformation.

POPULAR, INC. 2 01 3 A n n u a l R e p o r tKey Drivers Behind cARLos J. VAZQUeZ Executive Vice President Chief Financial Officer Popular, Inc. President Popular Community Bank2013 marked yet another set of notable improvements for Popular. With our third consecutive year of healthy profitability, our franchise continues to demonstrate its ability to yield reasonable returns even in a Percent 12 10 8 6 4 2 0 2009 tAnGiBLe coMMon eQUitY/tAnGiBLe Assets 2010 2011 2012 2013 BPOP 11.08 PEER AVG. 8.26 challenging economic environment. Credit quality improvements, strong earnings and healthy capital levels were key drivers of our solid performance and will surely be the cornerstones of our future results. Popular’s adjusted net income of $256 million was up 4% from 2012, as we remained focused on creating revenue opportunities while effectively managing credit and overhead costs. Our adjusted gross revenues Driving our earnings power are spread levels above our peers, which result from strong asset yields and funding costs that have improved every quarter for more than four years. and our minority ownership in Centro Financiero BHD, which includes one of the largest banks in the Dominican Republic, form the foundation of our capital management efforts. Specifically, we seek to maintain strong capital levels appropriate for Popular’s risk profile; strive toward our target of a for the year stayed strong at $1.9 billion while the loan loss provision, excluding bulk sales, double digit return on tangible equity; and eventually pursue – with the approval of fell by $124 million to a level comparable to our normalized target. Driving our earnings power are spread levels above our peers, which result from strong asset yields and funding costs that have improved every quarter for more than four years. Popular’s net interest margin (NIM) for 2013 increased to 4.52%, up 16 basis points from 2012 levels. Continued improvements in actual and projected cash flows from our covered portfolio (Westernbank) contributed to the stability of our NIM. While organic loan growth in Puerto Rico remains limited, we plan to offset this impact through selective loan portfolio purchases. Operating expenses stayed somewhat elevated due mainly to the expenses stemming from the workout of our covered loan portfolio. As credit continues to normalize, we expect additional savings in costs related to our credit management efforts, including reductions in legal fees, appraisals and OREO expenses. We are confident that these efforts, ahead of the 2015 expiration of our loss-sharing agreement of commercial loans with the FDIC, will lead to a lower cost base in the coming years. Managing the expense side of our operations is still a top priority, and we are committed to capturing every opportunity to do so. Our stress-testing and capital planning programs are robust, as we have permanently reallocated resources to bolster these important management and regulatory processes. The power of substantial internal capital generation from improved operating earnings, alongside additional sources of value in our remaining stake in EVERTEC our regulators – other capital management and distribution strategies, including the repayment of TARP. With two thirds of our managers holding Popular stock, our leadership continues to work with a great shared interest and a motivated ownership approach. Popular’s stock valuation is not immune to the uncertainties now confronting Puerto Rico – our principal market. Having said that, we are confident that our fundamental strengthening of Popular’s credit condition, liquidity, market share and capital base should result in a valuation that better reflects our tangible book value and underlying earning capacity. 8

Succeeding in a Challenging Regulatory Environment POPULAR, INC. 2 01 3 A n n u a l R e p o r t IGNACIO ÁLVAREZ Executive Vice President Chief Legal Officer General Counsel & Corporate Matters Group Popular, Inc.Like all financial institutions, we are working hard to address the challenges of succeeding in a rapidly evolving and increasingly demanding regulatory environment. Banking has always been a highly regulated industry, but today’s pace and sheer amount of regulatory and legal changes affecting the banking industry are unprecedented. The Dodd-Frank Wall Street Reform and CAPITAL During the financial crisis, the banking industry suffered a significant reduction in capital due to substantial credit losses. As a result, regulators continue to push for high capital ratios and enhanced stress testing processes. Our current robust capital levels, however, will allow us to comply with the additional requirements mandated under Basel III, without having to raise new capital. Notwithstanding that, as an institution, we will have to continue to review our balance sheet and product offerings carefully to determine proactively whether we should emphasize growth in certain asset classes and deemphasize it in others. substantial human and financial resources to conform our mortgage and other consumer products to these new CFPB requirements. We remain focused on these evolving regulations to make sure that our product and service offerings comply with all regulatory requirements as well as the needs of our clients. GOVERNANCE In this new environment, regulators expect greater involvement from senior management and the board of directors in overseeing regulatory and compliance issues. At Popular, we believe that good governance is a key element of our success, as evidenced by our strong governance Protection Act of 2010 (the “Dodd -Frank framework. As this area continues to Act”) is the most significant and far-reaching legislation affecting the banking industry since the Great Depression. Failure to comply with these new regulations can result not only in massive fines or other penalties, but can also trigger corrective actions that entail considerable financial expenditures and investment of human capital. In our case, the challenge is even greater due to the difficult economic environment in our principal market, Puerto Rico. The Puerto Rican government’s current fiscal problems will continue to challenge the local macro- economic environment, and we will seek more creative ways to meet the needs of our clients given this and other challenges. These regulatory changes will result in additional costs and administrative burdens that will undoubtedly lead to structural changes in how financial institutions develop and deliver products and services to their clients. At Popular, we are approaching this new reality as an opportunity to review and transform our processes and systems to better serve our clients. Some of the principal changes facing our institution will be in the areas of capital and compliance regulations: At Popular, we are approaching this new reality as an opportunity to review and transform our processes and systems to better serve our clients. COMPLIANCE As a bank with large retail operations, we have put a strong emphasis on compliance. Following the financial crisis, regulators have given greater weight to compliance issues and have found major compliance breakdowns at a number of large financial institutions that resulted in enforcement actions with significant fines and penalties. One important result was the creation of the Consumer Financial Protection Bureau (CFPB), which is the first federal regulatory agency dedicated exclusively to the protection of consumers of financial services and products. The CFPB has given particular attention to mortgage origination and servicing, as well as fair lending and consumer lending activities, such as credit cards and auto loans. We have dedicated evolve, we will continue to review our processes on a regular basis to identify further enhancements. In the last four years, we increased the diversity and skill set of our board with the addition of six new directors – better equipping the board to help us meet these new governance challenges. LOOKING AHEAD The regulatory environment is driving significant change in the banking industry, and it will have a major impact on how we structure the products and services we offer our clients. Banks that do a better job of rapidly adapting to this new paradigm will have a more favorable opportunity to grow their business. Those who fail to change face not only the loss of clients, but also enormous legal and reputational risks. At Popular, we are keenly aware of how much is at stake, and we are dedicating the time, resources and management focus to ensure that we continue to thrive in this new environment. 9

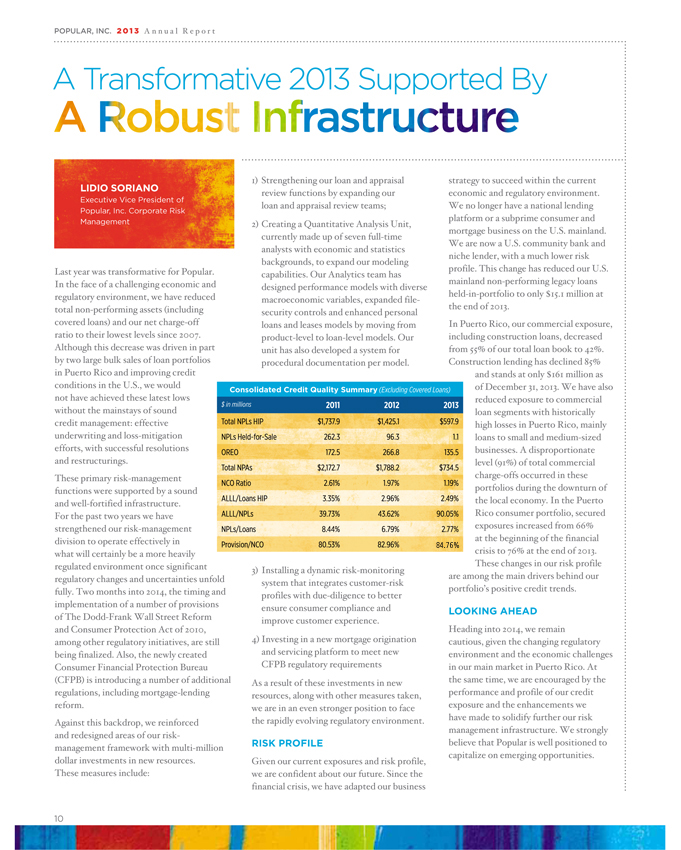

POPULAR, INC. 2 01 3 A n n u a l R e p o r tA Transformative 2013 Supported By A Robust Infrastructure LIDIO SORIANO Executive Vice President of Popular, Inc. Corporate Risk ManagementLast year was transformative for Popular. In the face of a challenging economic and regulatory environment, we have reduced total non-performing assets (including covered loans) and our net charge-off ratio to their lowest levels since 2007. Although this decrease was driven in part by two large bulk sales of loan portfolios in Puerto Rico and improving credit 1) Strengthening our loan and appraisal review functions by expanding our loan and appraisal review teams; 2) Creating a Quantitative Analysis Unit, currently made up of seven full-time analysts with economic and statistics backgrounds, to expand our modeling capabilities. Our Analytics team has designed performance models with diverse macroeconomic variables, expanded file-security controls and enhanced personal loans and leases models by moving from product-level to loan-level models. Our unit has also developed a system for procedural documentation per model. strategy to succeed within the current economic and regulatory environment. We no longer have a national lending platform or a subprime consumer and mortgage business on the U.S. mainland. We are now a U.S. community bank and niche lender, with a much lower risk profile. This change has reduced our U.S. mainland non-performing legacy loans held-in-portfolio to only $15.1 million at the end of 2013. In Puerto Rico, our commercial exposure, including construction loans, decreased from 55% of our total loan book to 42%. Construction lending has declined 85% and stands at only $161 million as conditions in the U.S., we would not have achieved these latest lows without the mainstays of sound credit management: effective underwriting and loss-mitigation efforts, with successful resolutions and restructurings. These primary risk-management functions were supported by a sound and well-fortified infrastructure. For the past two years we have strengthened our risk-management division to operate effectively in what will certainly be a more heavily regulated environment once significant CONSOLIDATED CREDIT QUALITY summary (Excluding Covered Loans)$ in millions 2011 2012 20133) Installing a dynamic risk-monitoring of December 31, 2013. We have also reduced exposure to commercial loan segments with historically high losses in Puerto Rico, mainly loans to small and medium-sized businesses. A disproportionate level (91%) of total commercial charge-offs occurred in these portfolios during the downturn of the local economy. In the Puerto Rico consumer portfolio, secured exposures increased from 66% 84.76% at the beginning of the financial crisis to 76% at the end of 2013. These changes in our risk profile regulatory changes and uncertainties unfold fully. Two months into 2014, the timing and implementation of a number of provisions of The Dodd-Frank Wall Street Reform and Consumer Protection Act of 2010, among other regulatory initiatives, are still being finalized. Also, the newly created Consumer Financial Protection Bureau (CFPB) is introducing a number of additional regulations, including mortgage-lending reform. Against this backdrop, we reinforced and redesigned areas of our risk-management framework with multi-million dollar investments in new resources. These measures include: system that integrates customer-risk profiles with due-diligence to better ensure consumer compliance and improve customer experience. 4) Investing in a new mortgage origination and servicing platform to meet new CFPB regulatory requirements As a result of these investments in new resources, along with other measures taken, we are in an even stronger position to face the rapidly evolving regulatory environment. RISK PROFILE Given our current exposures and risk profile, we are confident about our future. Since the financial crisis, we have adapted our business are among the main drivers behind our portfolio’s positive credit trends. LOOKING AHEAD Heading into 2014, we remain cautious, given the changing regulatory environment and the economic challenges in our main market in Puerto Rico. At the same time, we are encouraged by the performance and profile of our credit exposure and the enhancements we have made to solidify further our risk management infrastructure. We strongly believe that Popular is well positioned to capitalize on emerging opportunities. 10

POPULAR, INC. POPULAR, INC. 2 01 3 A n n u a l R e p o r t EXECUTIVE OFFICERS RICHARD L .. CARRIÓN Chairman, President and Chief Executive Officer Popular, Inc. CARLOS J. VÁZQUEZ Executive Vice President Chief Financial Officer Popular, Inc. President Popular Community Bank IGNACIO ÁLVAREZ Executive Vice President Chief Legal Officer General Counsel & Corporate Matters Group Popular, Inc. ILEANA GONZÁLEZ Executive Vice President Commercial Credit Administration Group Banco Popular de Puerto Rico JUAN GUERRERO Executive Vice President Financial & Insurance Services Group Banco Popular de Puerto Rico GILBERTO MONZÓN Executive Vice President Individual Credit Group Banco Popular de Puerto Rico EDUARDO J. NEGRÓN Executive Vice President Administration Group Popular, Inc. NÉSTOR O. RIVERA Executive Vice President Retail Banking and Operations Group Banco Popular de Puerto Rico ELI SEPÚLVEDA Executive Vice President Popular, Inc.Commercial Credit Group Banco Popular de Puerto Rico LIDIO SORIANO Executive Vice President Chief Risk Officer Corporate Risk Management Group Popular, Inc. BOARD OF DIRECTORS RICHARD L . CARRIÓN Chairman, President and Chief Executive Officer Popular, Inc. JOAQUÍN E. BACARDÍ, III President and Chief Executive Officer Bacardi Corporation ALEJANDRO M. BALLESTER President Ballester Hermanos, Inc. JOHN DIERCKSEN Principal Greycrest, LLC. MARÍA LUISA FERRE President and Chief Executive Officer Grupo Ferré Rangel DAVID E. GOEL Managing General Partner Matrix Capital Management Company, LLC C. KIM GOODWIN Private Investor WILLIAM J. TEUBER JR. Vice Chairman EMC Corporation CARLOS A. UNANUE President Goya de Puerto Rico 11

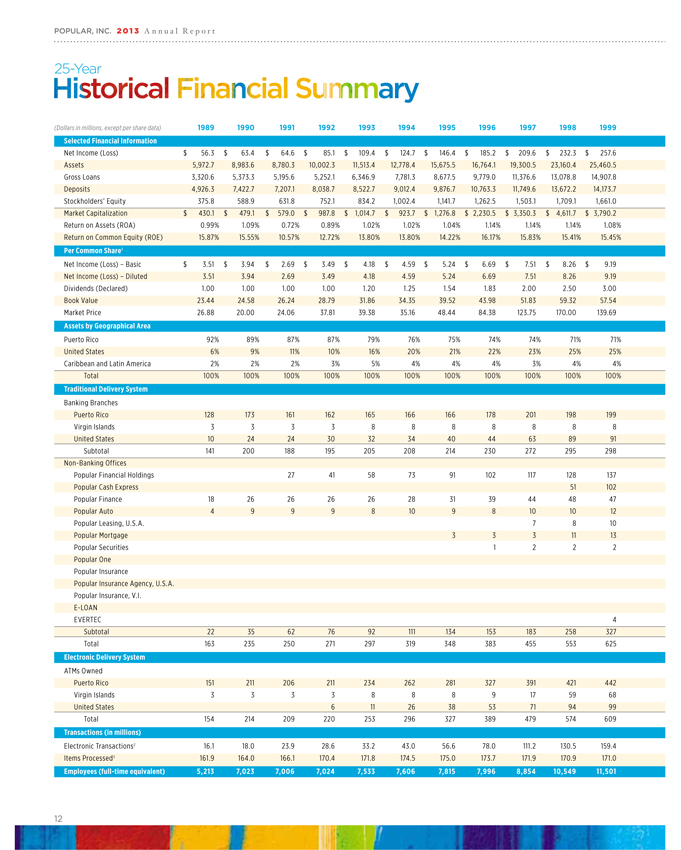

POPULAR, INC. 2 01 3 A n n u a l R e p o r t 25-Year Historical Financial Summary (Dollars in millions, except per share data) 1989 1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 Selected Financial Information Net Income (Loss) $ 56.3 $ 63.4 $ 64.6 $ 85.1 $ 109.4 $ 124.7 $ 146.4 $ 185.2 $ 209.6 $ 232.3 $ 257.6 Assets 5,972.7 8,983.6 8,780.3 10,002.3 11,513.4 12,778.4 15,675.5 16,764.1 19,300.5 23,160.4 25,460.5 Gross Loans 3,320.6 5,373.3 5,195.6 5,252.1 6,346.9 7,781.3 8,677.5 9,779.0 11,376.6 13,078.8 14,907.8 Deposits 4,926.3 7,422.7 7,207.1 8,038.7 8,522.7 9,012.4 9,876.7 10,763.3 11,749.6 13,672.2 14,173.7 Stockholders’ Equity 375.8 588.9 631.8 752.1 834.2 1,002.4 1,141.7 1,262.5 1,503.1 1,709.1 1,661.0 Market Capitalization $ 430.1 $ 479.1 $ 579.0 $ 987.8 $ 1,014.7 $ 923.7 $ 1,276.8 $ 2,230.5 $ 3,350.3 $ 4,611.7 $ 3,790.2 Return on Assets (ROA) 0.99% 1.09% 0.72% 0.89% 1.02% 1.02% 1.04% 1.14% 1.14% 1.14% 1.08% Return on Common Equity (ROE) 15.87% 15.55% 10.57% 12.72% 13.80% 13.80% 14.22% 16.17% 15.83% 15.41% 15.45% Per Common Share1 Net Income (Loss) – Basic $ 3.51 $ 3.94 $ 2.69 $ 3.49 $ 4.18 $ 4.59 $ 5.24 $ 6.69 $ 7.51 $ 8.26 $ 9.19 Net Income (Loss) – Diluted 3.51 3.94 2.69 3.49 4.18 4.59 5.24 6.69 7.51 8.26 9.19 Dividends (Declared) 1.00 1.00 1.00 1.00 1.20 1.25 1.54 1.83 2.00 2.50 3.00 Book Value 23.44 24.58 26.24 28.79 31.86 34.35 39.52 43.98 51.83 59.32 57.54 Market Price 26.88 20.00 24.06 37.81 39.38 35.16 48.44 84.38 123.75 170.00 139.69 Assets by Geographical Area Puerto Rico 92% 89% 87% 87% 79% 76% 75% 74% 74% 71% 71% United States 6% 9% 11% 10% 16% 20% 21% 22% 23% 25% 25% Caribbean and Latin America 2% 2% 2% 3% 5% 4% 4% 4% 3% 4% 4% Total 100% 100% 100% 100% 100% 100% 100% 100% 100% 100% 100% Traditional Delivery System Banking Branches Puerto Rico 128 173 161 162 165 166 166 178 201 198 199 Virgin Islands 3 3 3 3 8 8 8 8 8 8 8 United States 10 24 24 30 32 34 40 44 63 89 91 Subtotal 141 200 188 195 205 208 214 230 272 295 298 Non-Banking Offices Popular Financial Holdings 27 41 58 73 91 102 117 128 137 Popular Cash Express 51 102 Popular Finance 18 26 26 26 26 28 31 39 44 48 47 Popular Auto 4 9 9 9 8 10 9 8 10 10 12 Popular Leasing, U.S.A. 7 8 10 Popular Mortgage 3 3 3 11 13 Popular Securities 1 2 2 2 Popular One Popular Insurance Popular Insurance Agency, U.S.A. Popular Insurance, V.I. E-LOAN EVERTEC 4 Subtotal 22 35 62 76 92 111 134 153 183 258 327 Total 163 235 250 271 297 319 348 383 455 553 625 Electronic Delivery System ATMs Owned Puerto Rico 151 211 206 211 234 262 281 327 391 421 442 Virgin Islands 3 3 3 3 8 8 8 9 17 59 68 United States 6 11 26 38 53 71 94 99 Total 154 214 209 220 253 296 327 389 479 574 609 Transactions (in millions) Electronic Transactions2 16.1 18.0 23.9 28.6 33.2 43.0 56.6 78.0 111.2 130.5 159.4 Items Processed3 161.9 164.0 166.1 170.4 171.8 174.5 175.0 173.7 171.9 170.9 171.0 Employees (full-time equivalent) 5, 2 13 7,02 3 7,0 0 6 7,02 4 7, 533 7,6 0 6 7, 815 7,9 9 6 8 , 85 4 1 0, 5 49 11 , 5 01 12

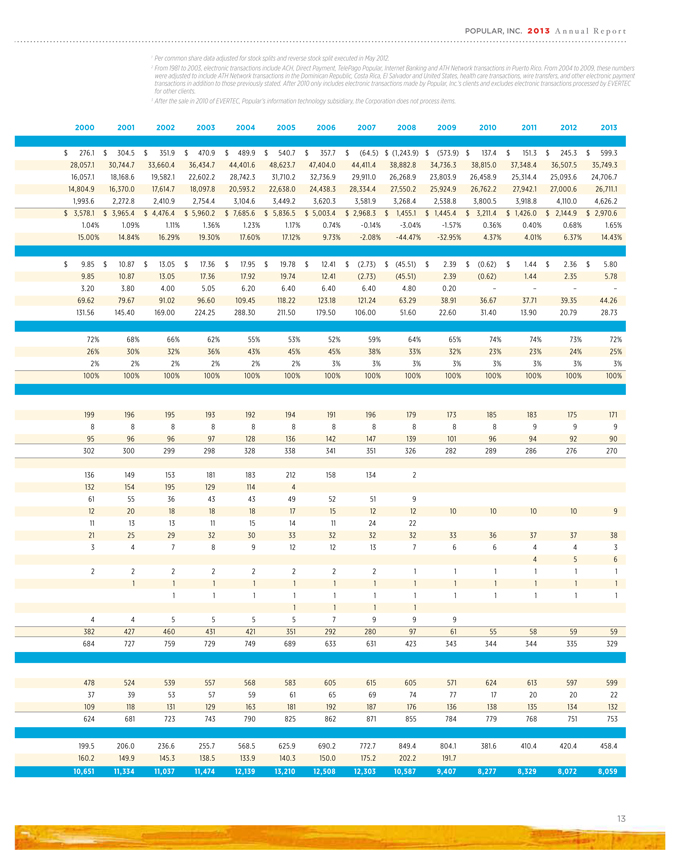

POPULAR, INC. 2 01 3 A n n u a l R e p o r t 1 Per common share data adjusted for stock splits and reverse stock split executed in May 2012. 2 From 1981 to 2003, electronic transactions include ACH, Direct Payment, TelePago Popular, Internet Banking and ATH Network transactions in Puerto Rico. From 2004 to 2009, these numbers were adjusted to include ATH Network transactions in the Dominican Republic, Costa Rica, El Salvador and United States, health care transactions, wire transfers, and other electronic payment transactions in addition to those previously stated. After 2010 only includes electronic transactions made by Popular, Inc.’s clients and excludes electronic transactions processed by EVERTEC for other clients. 3 After the sale in 2010 of EVERTEC, Popular’s information technology subsidiary, the Corporation does not process items. 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 $ 276.1 $ 304.5 $ 351.9 $ 470.9 $ 489.9 $ 540.7 $ 357.7 $ (64.5) $ (1,243.9) $ (573.9) $ 137.4 $ 151.3 $ 245.3 $ 599.3 28,057.1 30,744.7 33,660.4 36,434.7 44,401.6 48,623.7 47,404.0 44,411.4 38,882.8 34,736.3 38,815.0 37,348.4 36,507.5 35,749.3 16,057.1 18,168.6 19,582.1 22,602.2 28,742.3 31,710.2 32,736.9 29,911.0 26,268.9 23,803.9 26,458.9 25,314.4 25,093.6 24,706.7 14,804.9 16,370.0 17,614.7 18,097.8 20,593.2 22,638.0 24,438.3 28,334.4 27,550.2 25,924.9 26,762.2 27,942.1 27,000.6 26,711.1 1,993.6 2,272.8 2,410.9 2,754.4 3,104.6 3,449.2 3,620.3 3,581.9 3,268.4 2,538.8 3,800.5 3,918.8 4,110.0 4,626.2 $ 3,578.1 $ 3,965.4 $ 4,476.4 $ 5,960.2 $ 7,685.6 $ 5,836.5 $ 5,003.4 $ 2,968.3 $ 1,455.1 $ 1,445.4 $ 3,211.4 $ 1,426.0 $ 2,144.9 $ 2,970.6 1.04% 1.09% 1.11% 1.36% 1.23% 1.17% 0.74% -0.14% -3.04% -1.57% 0.36% 0.40% 0.68% 1.65% 15.00% 14.84% 16.29% 19.30% 17.60% 17.12% 9.73% -2.08% -44.47% -32.95% 4.37% 4.01% 6.37% 14.43% $ 9.85 $ 10.87 $ 13.05 $ 17.36 $ 17.95 $ 19.78 $ 12.41 $ (2.73) $ (45.51) $ 2.39 $ (0.62) $ 1.44 $ 2.36 $ 5.80 9.85 10.87 13.05 17.36 17.92 19.74 12.41(2.73) (45.51) 2.39 (0.62) 1.44 2.35 5.78 3.20 3.80 4.00 5.05 6.20 6.40 6.40 6.40 4.80 0.20 – – – – 69.62 79.67 91.02 96.60 109.45 118.22 123.18 121.24 63.29 38.91 36.67 37.71 39.35 44.26 131.56 145.40 169.00 224.25 288.30 211.50 179.50 106.00 51.60 22.60 31.40 13.90 20.79 28.73 72% 68% 66% 62% 55% 53% 52% 59% 64% 65% 74% 74% 73% 72% 26% 30% 32% 36% 43% 45% 45% 38% 33% 32% 23% 23% 24% 25% 2% 2% 2% 2% 2% 2% 3% 3% 3% 3% 3% 3% 3% 3% 100% 100% 100% 100% 100% 100% 100% 100% 100% 100% 100% 100% 100% 100% 199 196 195 193 192 194 191 196 179 173 185 183 175 171 8 8 8 8 8 8 8 8 8 8 8 9 9 9 95 96 96 97 128 136 142 147 139 101 96 94 92 90 302 300 299 298 328 338 341 351 326 282 289 286 276 270 136 149 153 181 183 212 158 134 2 132 154 195 129 114 4 61 55 36 43 43 49 52 51 9 12 20 18 18 18 17 15 12 12 10 10 10 10 9 11 13 13 11 15 14 11 24 22 21 25 29 32 30 33 32 32 32 33 36 37 37 38 3 4 7 8 9 12 12 13 7 6 6 4 4 3 4 5 6 2 2 2 2 2 2 2 2 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 4 4 5 5 5 5 7 9 9 9 382 427 460 431 421 351 292 280 97 61 55 58 59 59 684 727 759 729 749 689 633 631 423 343 344 344 335 329 478 524 539 557 568 583 605 615 605 571 624 613 597 599 37 39 53 57 59 61 65 69 74 77 17 20 20 22 109 118 131 129 163 181 192 187 176 136 138 135 134 132 624 681 723 743 790 825 862 871 855 784 779 768 751 753 199.5 206.0 236.6 255.7 568.5 625.9 690.2 772.7 849.4 804.1 381.6 410.4 420.4 458.4 160.2 149.9 145.3 138.5 133.9 140.3 150.0 175.2 202.2 191.7 1 0,651 11 , 33 4 11 ,037 11 ,474 12 ,139 13, 2 1 0 12 , 5 0 8 12 , 303 1 0, 5 87 9,4 07 8 , 2 7 7 8 , 3 2 9 8 ,07 2 8 ,059 13

POPULAR® P.O. Box 362708 San Juan, Puerto Rico 00936-2708

Financial Review and

Supplementary Information

| | | | | | |

| | Management’s Discussion and Analysis of | | | | |

| | Financial Condition and Results of Operations | | 2 | | |

| | | |

| | Statistical Summaries | | 107 | | |

| | | |

| | Financial Statements | | | | |

| | | |

| | Management’s Report to Stockholders | | 112 | | |

| | | |

| | Report of Independent Registered Public Accounting Firm | | 113 | | |

| | | |

| | Consolidated Statements of Financial Condition as of December 31, 2013 and 2012 | | 115 | | |

| | | |

| | Consolidated Statements of Operations for the years ended December 31, 2013, 2012 and 2011 | | 116 | | |

| | | |

| | Consolidated Statements of Comprehensive Income (Loss) for the years ended December 31, 2013, 2012 and 2011 | | 117 | | |

| | | |

| | Consolidated Statements of Changes in Stockholders’ Equity for the years ended December 31, 2013, 2012 and 2011 | | 118 | | |

| | | |

| | Consolidated Statements of Cash Flows for the years ended December 31, 2013, 2012 and 2011 | | 119 | | |

| | | |

| | Notes to Consolidated Financial Statements | | 121 | | |

Management’s Discussion and

Analysis of Financial Condition

and Results of Operations

| | | | | | |

| | | |

| | Forward-Looking Statements | | 3 | | |

| | | |

| | Overview | | 4 | | |

| | | |

| | Critical Accounting Policies / Estimates | | 10 | | |

| | | |

| | Statement of Operations Analysis | | 25 | | |

| | | |

| | Net Interest Income | | 25 | | |

| | | |

| | Provision for Loan Losses | | 30 | | |

| | | |

| | Non-Interest Income | | 30 | | |

| | | |

| | Operating Expenses | | 33 | | |

| | | |

| | Income Taxes | | 34 | | |

| | | |

| | Fourth Quarter Results | | 36 | | |

| | | |

| | Reportable Segment Results | | 37 | | |

| | | |

| | Statement of Financial Condition Analysis | | 41 | | |

| | | |

| | Assets | | 41 | | |

| | | |

| | Deposits and Borrowings | | 47 | | |

| | | |

| | Stockholders’ Equity | | 48 | | |

| | | |

| | Regulatory Capital | | 49 | | |

| | | |

| | Off-Balance Sheet Arrangements and Other Commitments | | 53 | | |

| | | |

| | Contractual Obligations and Commercial Commitments | | 53 | | |

| | | |

| | Guarantees | | 55 | | |

| | | |

| | Risk Management | | 59 | | |

| | | |

| | Market / Interest Rate Risk | | 60 | | |

| | | |

| | Liquidity | | 68 | | |

| | | |

| | Credit Risk Management and Loan Quality | | 75 | | |

| | | |

| | Enterprise Risk and Operational Risk Management | | 103 | | |

| | | |

| | Adoption of New Accounting Standards and Issued But Not Yet Effective Accounting Standards | | 104 | | |

| | | |

| | Statistical Summaries | | | | |

| | | |

| | Statements of Financial Condition | | 107 | | |

| | | |

| | Statements of Operations | | 108 | | |

| | | |

| | Average Balance Sheet and Summary of Net Interest Income | | 109 | | |

| | | |

| | Quarterly Financial Data | | 111 | | |

2

The following Management’s Discussion and Analysis (“MD&A”) provides information which management believes is necessary for understanding the financial performance of Popular, Inc. and its subsidiaries (the “Corporation” or “Popular”). All accompanying tables, consolidated financial statements, and corresponding notes included in this “Financial Review and Supplementary Information - 2013 Annual Report” (“the report”) should be considered an integral part of this MD&A.

FORWARD-LOOKING STATEMENTS

The information included in this report contains certain forward-looking statements within the meaning of the Private Securities Litigation Reform Act of 1995. These forward-looking statements may relate to the Corporation’s financial condition, results of operations, plans, objectives, future performance and business, including, but not limited to, statements with respect to expected earnings levels, the adequacy of the allowance for loan losses, delinquency trends, market risk and the impact of interest rate changes, capital market conditions, capital adequacy and liquidity, and the effect of legal proceedings and new accounting standards on the Corporation’s financial condition and results of operations. All statements contained herein that are not clearly historical in nature are forward-looking, and the words “anticipate,” “believe,” “continues,” “expect,” “estimate,” “intend,” “project” and similar expressions and future or conditional verbs such as “will,” “would,” “should,” “could,” “might,” “can,” “may,” or similar expressions are generally intended to identify forward-looking statements.

Forward-looking statements are not guarantees of future performance, are based on management’s current expectations and, by their nature, involve certain risks, uncertainties, estimates and assumptions by management that are difficult to predict. Various factors, some of which are beyond the Corporation’s control, could cause actual results to differ materially from those expressed in, or implied by, such forward-looking statements. Factors that might cause such a difference include, but are not limited to, the rate of growth in the economy and employment levels, as well as general business and economic conditions; changes in interest rates, as well as the magnitude of such changes; the fiscal and monetary policies of the federal government and its agencies; changes in federal bank regulatory and supervisory policies, including required levels of capital; the impact of the Dodd-Frank Wall Street Reform and Consumer Protection Act (Financial Reform Act) on the Corporation’s businesses, business practices and costs of operations; the relative strength or weakness of the consumer and commercial credit sectors and of the real estate markets in Puerto Rico and the other markets in which borrowers are located; the performance of the stock and bond markets; competition in the financial services industry; additional Federal Deposit Insurance Corporation (“FDIC”) assessments; and possible legislative, tax or regulatory changes. Other possible events or factors that could cause results or performance to differ materially from those expressed in such forward-looking statements include the following: negative economic conditions that adversely affect the general economy, housing prices, the job market, consumer confidence and spending habits which may affect, among other things, the level of non-performing assets, charge-offs and provision expense; changes in interest rates and market liquidity, which may reduce interest margins, impact funding sources and affect the ability to originate and distribute financial products in the primary and secondary markets; adverse movements and volatility in debt and equity capital markets; changes in market rates and prices, which may adversely impact the value of financial assets and liabilities; liabilities resulting from litigation and regulatory investigations; changes in accounting standards, rules and interpretations; increased competition; the Corporation’s ability to grow its core businesses; decisions to downsize, sell or close units or otherwise change the business mix of the Corporation; and management’s ability to identify and manage these and other risks. Moreover, the outcome of legal proceedings is inherently uncertain and depends on judicial interpretations of law and the findings of regulators, judges and juries.

All forward-looking statements included in this report are based upon information available to the Corporation as of the date of this report, and other than as required by law, including the requirements of applicable securities laws, management assumes no obligation to update or revise any such forward-looking statements to reflect occurrences or unanticipated events or circumstances after the date of such statements.

The description of the Corporation’s business and risk factors contained in Item 1 and 1A of its Form 10-K for the year ended December 31, 2013 discusses additional information about the business of the Corporation and the material risk factors that, in addition to the other information in this report, readers should consider.

3

OVERVIEW

The Corporation is a diversified, publicly-owned financial holding company subject to the supervision and regulation of the Board of Governors of the Federal Reserve System. The Corporation has operations in Puerto Rico, the United States (“U.S.”) mainland, and the U.S. and British Virgin Islands. In Puerto Rico, the Corporation provides retail, including residential mortgage loans originations, and commercial banking services through its principal banking subsidiary, Banco Popular de Puerto Rico (“BPPR”), as well as investment banking, broker-dealer, auto and equipment leasing and financing, and insurance services through specialized subsidiaries. Effective December 31, 2012, Popular Mortgage, which was a wholly-owned subsidiary of BPPR prior to that date, was merged with and into BPPR as part of an internal reorganization. The Corporation’s mortgage origination business continues to be conducted under the brand name Popular Mortgage, a division of BPPR. In the U.S. mainland, the Corporation operates Banco Popular North America (“BPNA”), including its wholly-owned subsidiary E-LOAN. The BPNA franchise operates under the brand name of Popular Community Bank. BPNA focuses efforts and resources on the core community banking business. BPNA operates branches in New York, California, Illinois, New Jersey and Florida. E-LOAN markets deposit accounts under its name for the benefit of BPNA. Note 41 to the consolidated financial statements presents information about the Corporation’s business segments.

The Corporation has several investments which accounts for under the equity method. These include the 14.9% interest in EVERTEC, a 19.99% interest in Centro Financiero BHD, a 24.9% interest in PR Asset Portfolio 2013-1 International, LLC and a 24.9% interest in PRLP 2011 Holdings LLP, among other investments in limited partnerships which mainly hold investment securities. EVERTEC provides transaction processing services throughout the Caribbean and Latin America, including servicing many of the Corporation’s system infrastructures and transaction processing businesses. Centro Financiero BHD is a diversified financial services institution operating in the Dominican Republic. PR Asset Portfolio 2013-1 International, LLC is a joint venture to which the Corporation sold construction and commercial loans and commercial and residential real estate owned assets, most of which were non-performing, with a fair value of $306 million during the year 2013. PRLP 2011 Holdings LLP is a joint venture to which the Corporation sold construction and commercial loans, most of which were non-performing, with a fair value of $148 million during the year 2011. For the year ended December 31, 2013, the Corporation recorded approximately $42.9 million in earnings from these investments on an aggregate basis. The carrying amounts of these investments as of December 31, 2013 were $197.0 million. Refer to Note 16 to the consolidated financial statements for additional information of the Corporation’s investments at equity.

The Corporation’s net income for the year ended December 31, 2013 amounted to $599.3 million, compared with net income of $245.3 million and $151.3 million for 2012 and 2011, respectively. The results for 2013 reflect the impact of two bulk sale of non-performing assets resulting in an aggregate after tax loss of $287.7 million, $412.8 million in after tax gains resulting from the initial and subsequent public offerings and related transactions completed by EVERTEC in which the Corporation participated as a selling stockholder and an income tax benefit of $197.5 million related to the change in the corporate tax rate from 30% to 39%. The results for 2012 reflect an income tax benefit of $72.9 million related to reduction of the deferred tax liability on the estimated gains for tax purposes related to the loans acquired from Westernbank as a result of the closing agreement with the Puerto Rico Department of Treasury, which established that these would be taxed at a capital gain rate. Also, the results from 2012 reflect a benefit of approximately $26.9 million from the Corporation’s share of a tax benefit from a grant received by EVERTEC from the Puerto Rico Government. During 2011, the Corporation recorded an income tax expense of $103.3 million as a result of the reduction in the marginal tax rate, which was partially offset by a benefit of $53.6 million recorded as a result of a closing agreement with the Puerto Rico Department of Treasury, which deferred the deduction of charge-offs taken during 2009 and 2010 until the years 2013-2016. Table 1 provides selected financial data for the past five years. For purposes of the discussions, assets subject to loss sharing agreements with the FDIC, including loans and other real estate owned, are referred to as “covered assets” or “covered loans” since the Corporation expects to be reimbursed for 80% of any future losses on those assets, subject to the terms of the FDIC loss sharing agreements.

Excluding the impact of the above mentioned transactions, the adjusted net income for the year ended December 31, 2013 was $256.2 million. Refer to Table 70 for the reconciliation to the adjusted, Non-GAAP net income.

During 2013, the Corporation maintained a strong net interest margin and reflected a reduction in its provision for loan losses, excluding the impact of the bulk sales of non performing assets. Net interest margin, on a taxable equivalent basis, increased 24 basis points from 2012 to 4.72%, mainly due to a higher yield from the covered loans portfolio, lower levels of non-performing assets and lower cost of funds. The Corporation made significant improvements in its overall credit metrics. Non-performing assets,

4

excluding covered assets, declined $1.1 billion as a result of the two bulk sales of non-performing assets during the first and second quarters as well as the continuation of aggressive asset resolution strategies. Excluding the impact of the bulk sales of non-performing assets, the provision for loan losses for the non-covered portfolio was down $119.0 million from the year ended December 31, 2012. Inflows of non-performing assets were down $492 million, or 42%, from 2012 and the net charge off ratio was 1.19%, compared to 1.97% in 2012 (excluding the impact of the bulk sales of non-performing assets).

While the Corporation has made improvements in the credit quality of its portfolios, the continued economic weakness in Puerto Rico, our principal market, continues to present challenges which are being considered in its overall reserve levels. In light of these economic conditions, which put pressure on loan growth, during 2013 the Corporation supplemented its organic growth with opportunistic loan purchases, particularly of residential mortgage loans.

The Corporation’s U.S. mainland operations were profitable during 2013 with net income of $116.6 million, compared to $46.0 million for 2012. The improvement is mainly related to improved credit performance which resulted in a reserve release of $14.7 million for 2013, compared to a provision of $52.0 million for 2012, a $66.7 million variance. The reserve release also reflects the impact of $10.8 million due to the enhancements to the allowance for loan losses methodology implemented during the second quarter of 2013. The U.S. operations have followed the general credit trends on the mainland demonstrating progressive improvement. Management remains focused on increasing BPNA’s customer base, as it continues its strategy to transition from a mainly Hispanic-focused bank to a more broad-based community bank. The biggest challenge for the BPNA reportable segment is achieving healthy loan growth in the markets it serves at an adequate risk-adjusted return.

Table 1 - Selected Financial Data

| | | | | | | | | | | | | | | | | | | | |

| |

| | | Year ended December 31, | |

| |

| (Dollars in thousands, except per common share data) | | 2013 | | | 2012 | | | 2011 | | | 2010 | | | 2009 | |

| |

CONDENSED STATEMENTS OF OPERATIONS | | | | | | | | | | | | | | | | | | | | |

Interest income | | $ | 1,748,456 | | | $ | 1,755,846 | | | $ | 1,941,161 | | | $ | 1,949,300 | | | $ | 1,854,997 | |

Interest expense | | | 315,876 | | | | 379,213 | | | | 505,816 | | | | 653,427 | | | | 753,744 | |

| |

Net interest income | | | 1,432,580 | | | | 1,376,633 | | | | 1,435,345 | | | | 1,295,873 | | | | 1,101,253 | |

| |

Provision for loan losses: | | | | | | | | | | | | | | | | | | | | |

Non-covered loans | | | 533,167 | | | | 334,102 | | | | 430,085 | | | | 1,011,880 | | | | 1,405,807 | |

Covered loans | | | 69,396 | | | | 74,839 | | | | 145,635 | | | | - | | | | - | |

Non-interest income | | | 810,569 | | | | 531,212 | | | | 625,426 | | | | 1,304,458 | | | | 896,501 | |

Operating expenses | | | 1,292,586 | | | | 1,280,032 | | | | 1,218,799 | | | | 1,342,820 | | | | 1,154,196 | |

Income tax (benefit) expense | | | (251,327) | | | | (26,403) | | | | 114,927 | | | | 108,230 | | | | (8,302) | |

| |

Income (loss) from continuing operations | | | 599,327 | | | | 245,275 | | | | 151,325 | | | | 137,401 | | | | (553,947) | |

Loss from discontinued operations, net of tax | | | - | | | | - | | | | - | | | | - | | | | (19,972) | |

| |

Net income (loss) | | $ | 599,327 | | | $ | 245,275 | | | $ | 151,325 | | | $ | 137,401 | | | $ | (573,919) | |

| |

Net income (loss) applicable to common stock | | $ | 595,604 | | | $ | 241,552 | | | $ | 147,602 | | | $ | (54,576) | | | $ | 97,377 | |

| |

PER COMMON SHARE DATA[1] | | | | | | | | | | | | | | | | | | | | |

Net income (loss): | | | | | | | | | | | | | | | | | | | | |

Basic: | | | | | | | | | | | | | | | | | | | | |

From continuing operations | | $ | 5.80 | | | $ | 2.36 | | | $ | 1.44 | | | $ | (0.62) | | | $ | 2.88 | |

From discontinued operations | | | - | | | | - | | | | - | | | | - | | | | (0.49) | |

| |

Total | | $ | 5.80 | | | $ | 2.36 | | | $ | 1.44 | | | $ | (0.62) | | | $ | 2.39 | |

| |

Diluted: | | | | | | | | | | | | | | | | | | | | |

From continuing operations | | $ | 5.78 | | | $ | 2.35 | | | $ | 1.44 | | | $ | (0.62) | | | $ | 2.88 | |

From discontinued operations | | | - | | | | - | | | | - | | | | - | | | | (0.49) | |

| |

Total | | $ | 5.78 | | | $ | 2.35 | | | $ | 1.44 | | | $ | (0.62) | | | $ | 2.39 | |

| |

Dividends declared | | $ | - | | | $ | - | | | $ | - | | | $ | - | | | $ | 0.20 | |

Book Value | | | 44.26 | | | | 39.35 | | | | 37.71 | | | | 36.67 | | | | 38.91 | |

Market Price | | | 28.73 | | | | 20.79 | | | | 13.90 | | | | 31.40 | | | | 22.60 | |

Outstanding shares: | | | | | | | | | | | | | | | | | | | | |

Average - basic | | | 102,693,685 | | | | 102,429,755 | | | | 102,179,393 | | | | 88,515,404 | | | | 40,822,950 | |

Average - assuming dilution | | | 103,061,475 | | | | 102,653,610 | | | | 102,289,496 | | | | 88,515,404 | | | | 40,822,950 | |

End of period | | | 103,397,699 | | | | 103,169,806 | | | | 102,590,457 | | | | 102,272,780 | | | | 63,954,011 | |

AVERAGE BALANCES | | | | | | | | | | | | | | | | | | | | |

5

| | | | | | | | | | | | | | | | | | | | |

Net loans[2] | | $ | 24,734,542 | | | $ | 24,845,494 | | | $ | 25,617,767 | | | $ | 25,821,778 | | | $ | 24,836,067 | |

Earning assets | | | 31,675,763 | | | | 31,569,702 | | | | 32,931,332 | | | | 34,154,021 | | | | 34,083,406 | |

Total assets | | | 36,266,993 | | | | 36,264,031 | | | | 38,066,268 | | | | 38,378,966 | | | | 36,569,370 | |

Deposits | | | 26,772,375 | | | | 26,903,933 | | | | 27,503,391 | | | | 26,650,497 | | | | 26,828,209 | |

Borrowings | | | 4,293,042 | | | | 4,415,624 | | | | 5,846,874 | | | | 7,448,021 | | | | 5,832,896 | |

Total stockholders’ equity | | | 4,176,349 | | | | 3,843,652 | | | | 3,732,836 | | | | 3,259,167 | | | | 2,852,065 | |

PERIOD END BALANCE | | | | | | | | | | | | | | | | | | | | |

Net loans[2] | | $ | 24,706,719 | | | $ | 25,093,632 | | | $ | 25,314,392 | | | $ | 26,458,855 | | | $ | 23,803,909 | |

Allowance for loan losses | | | 640,555 | | | | 730,607 | | | | 815,308 | | | | 793,225 | | | | 1,261,204 | |

Earning assets | | | 31,521,963 | | | | 31,906,198 | | | | 32,441,983 | | | | 33,507,582 | | | | 32,340,967 | |

Total assets | | | 35,749,333 | | | | 36,507,535 | | | | 37,348,432 | | | | 38,814,998 | | | | 34,736,325 | |

Deposits | | | 26,711,145 | | | | 27,000,613 | | | | 27,942,127 | | | | 26,762,200 | | | | 25,924,894 | |

Borrowings | | | 3,645,246 | | | | 4,430,673 | | | | 4,293,669 | | | | 6,946,955 | | | | 5,288,748 | |

Total stockholders’ equity | | | 4,626,150 | | | | 4,110,000 | | | | 3,918,753 | | | | 3,800,531 | | | | 2,538,817 | |

SELECTED RATIOS | | | | | | | | | | | | | | | | | | | | |

Net interest margin (taxable equivalent basis) | | | 4.72 | % | | | 4.48 | % | | | 4.48 | % | | | 3.82 | % | | | 3.47 % | |

Return on average total assets | | | 1.65 | | | | 0.68 | | | | 0.40 | | | | 0.36 | | | | (1.57) | |

Return on average common stockholders’ equity | | | 14.43 | | | | 6.37 | | | | 4.01 | | | | 4.37 | | | | (32.95) | |

Tier I Capital to risk-adjusted assets | | | 19.15 | | | | 17.35 | | | | 15.97 | | | | 14.52 | | | | 9.81 | |

Total Capital to risk-adjusted assets | | | 20.42 | | | | 18.63 | | | | 17.25 | | | | 15.79 | | | | 11.13 | |

| |

| | |

[1] Per share data is based on the average number of shares outstanding during the periods, except for the book value and market price which are based on the information at the end of the periods. All per share data has been adjusted to retroactively reflect the 1-for-10 reverse stock split effected on May 29, 2012. |

| [2] Includes loans held-for-sale and covered loans. |

|

The Corporation has strived to mitigate the decline in earning assets amid challenging economic conditions in Puerto Rico. During the first half of 2013, the Corporation completed two bulk purchases from Puerto Rico financial institutions acquiring $761.3 million in mortgage loans. Also, during 2012, the BPPR reportable segment purchased $265 million in consumer loans. During the first half of 2011, the Corporation completed two bulk purchases of residential mortgage loans from a Puerto Rico financial institution, adding $518 million in performing mortgage loans to its portfolio. In August 2011, the Corporation completed the purchase of Citibank’s AAdvantage co-branded credit card portfolio in Puerto Rico and the U.S. Virgin Islands, which represented approximately $131 million in balances. In addition, BPPR entered into an agreement with American Airlines, Inc. to become the exclusive issuer of AAdvantage co-branded credit cards in those two regions.

On April 30, 2010, BPPR acquired certain assets and assumed certain liabilities of Westernbank from the FDIC in an assisted transaction. Table 2 provides a summary of the gross revenues derived from the assets acquired in the FDIC-assisted transaction during 2013, 2012 and 2011.

Table 2 - Financial Information - Westernbank FDIC-Assisted Transaction

| | | | | | | | | | | | |

| | | Year ended December 31, | |

(In thousands) | | 2013 | | | 2012 | | | 2011 | |

| |

Interest income: | | | | | | | | | | | | |

Interest income on covered loans | | $ | 300,745 | | | $ | 301,441 | | | $ | 375,595 | |

Discount accretion on ASC 310-20 covered loans | | | - | | | | - | | | | 37,083 | |

| |

Total interest income on covered loans | | | 300,745 | | | | 301,441 | | | | 412,678 | |

| |

FDIC loss share (expense) income : | | | | | | | | | | | | |

Amortization of loss share indemnification asset | | | (161,635) | | | | (129,676) | | | | (10,855) | |

80% mirror accounting on credit impairment losses[1] | | | 60,454 | | | | 58,187 | | | | 110,457 | |

80% mirror accounting on reimbursable expenses | | | 50,985 | | | | 30,771 | | | | 5,093 | |

80% mirror accounting on recoveries on covered assets, including rental income on OREOs, subject to reimbursement to the FDIC | | | (16,057) | | | | (2,979) | | | | - | |

80% mirror accounting on amortization of contingent liability on unfunded commitments | | | (473) | | | | (969) | | | | (33,221) | |

Change in true-up payment obligation | | | (15,993) | | | | (13,178) | | | | (6,304) | |

Other | | | 668 | | | | 1,633 | | | | 1,621 | |

| |

Total FDIC loss share (expense) income | | | (82,051) | | | | (56,211) | | | | 66,791 | |

| |

6

| | | | | | | | | | | | |

| |

Fair value change in equity appreciation instrument | | | - | | | | - | | | | 8,323 | |

Amortization of contingent liability on unfunded commitments (included in other operating income) | | | 593 | | | | 1,211 | | | | 4,487 | |

| |

Total revenues | | | 219,287 | | | | 246,441 | | | | 492,279 | |

| |

Provision for loan losses | | | 69,396 | | | | 74,839 | | | | 145,635 | |

| |

Total revenues less provision for loan losses | | $ | 149,891 | | | $ | 171,602 | | | $ | 346,644 | |

| |

| [1] | Reductions in expected cash flows for ASC 310-30 loans, which may impact the provision for loan losses, may consider reductions in both principal and interest cash flow expectations. The amount covered under the FDIC loss sharing agreements for interest not collected from borrowers is limited under the agreements (approximately 90 days); accordingly, these amounts are not subject fully to the 80% mirror accounting. | |

| | | | | | | | | | |

|

| |

| Average balances | | | |

|

| | | Year ended December 31, |

| (In millions) | | 2013 | | | 2012 | | | |

|

Covered loans | | $ | 3,228 | | | $ | 4,050 | | | |

FDIC loss share asset | | | 1,310 | | | | 1,680 | | | |

|

Interest income on covered loans for the year 2013 amounted to $300.7 million vs. $301.4 million in 2012, reflecting a yield of 9.32% vs. 7.44%, for each year respectively. The increase in the yield was due to higher expected cash flows which are reflected in the accretable yield and recognized over the life of the loans and resolutions of loans during the year. This portfolio, due to its nature, should continue to decline as scheduled payments are received and workout arrangements are made. The yield improvement in 2013 reflects higher collections and estimated cash flows, which increase the accretable yield to be taken over the life of the loan pools. For 2011, net interest income reflects $37.1 million of discount accretion related to covered loans accounted for under ASC Subtopic 310-20. This discount was fully accreted into earnings during 2011.

The FDIC loss share reflected an expense of $82.1 million for 2013, compared to $56.2 million for 2012. This was the mainly the result of higher amortization of the indemnification asset by $32.0 million and higher recoveries on covered assets, including rental income, of $13.1 million, offset by higher mirror accounting on reimbursable expenses for $20.2 million. For 2012, when compared to 2011 this line reflected a negative variance of $123.0 million due to lower discount accretion on loans and unfunded commitments subject to ASC Subtopic 310-20, higher amortization of the FDIC loss share asset, lower mirror accounting on credit impairment losses and higher fair value adjustments to the true-up payment obligation, partially offset by the favorable mirror accounting on reimbursable expenses.

Although the increase in cash flows increases the accretable yield to be recognized over the life of the loans, it also has the effect of lowering the realizable value of the loss share asset since the Corporation would receive lower FDIC payments under the loss share agreements. This is reflected in the increased amortization of the loss share asset for 2013 and an increase in the fair value of the true-up payment obligation. The change in the amortization of the loss share asset from 2011 to 2012 also reflected higher expected cash flows from year to year.

The discussion that follows provides highlights of the Corporation’s results of operations for the year ended December 31, 2013 compared to the results of operations of 2012. It also provides some highlights with respect to the Corporation’s financial condition, credit quality, capital and liquidity. Table 3 presents a five-year summary of the components of net income (loss) as a percentage of average total assets.

| | | | | | | | | | | | | | | | | | | | |

| Table 3 - Components of Net Income (Loss) as a Percentage of Average Total Assets | |

| |

| | | | | |

| | | 2013 | | | 2012 | | | 2011 | | | 2010 | | | 2009 | |

| |

| | | | | |

Net interest income | | | 3.95 % | | | | 3.80 % | | | | 3.77 % | | | | 3.38 % | | | | 3.01 % | |

| | | | | |

Provision for loan losses | | | (1.66) | | | | (1.13) | | | | (1.51) | | | | (2.64) | | | | (3.84) | |

| | | | | |

Mortgage banking activities | | | 0.20 | | | | 0.24 | | | | (0.01) | | | | 0.04 | | | | 0.04 | |

| | | | | |

Net gain and valuation adjustments on investment securities | | | 0.02 | | | | - | | | | 0.03 | | | | 0.01 | | | | 0.60 | |

| | | | | |

Net (loss) gain on sale of loans, including valuation adjustments on loans held-for-sale | | | (0.14) | | | | (0.08) | | | | 0.01 | | | | 0.02 | | | | (0.03) | |

| | | | | |

Adjustments (expense) to indemnity reserves | | | (0.10) | | | | (0.06) | | | | (0.09) | | | | (0.19) | | | | (0.11) | |

| | | | | |

Trading account profit | | | (0.04) | | | | 0.01 | | | | 0.12 | | | | 0.09 | | | | 0.15 | |

7

| | | | | | | | | | | | | | | | | | | | |

FDIC loss share (expense) income | | | (0.23) | | | | (0.16) | | | | 0.18 | | | | (0.07) | | | | - | |

| | | | | |

Fair value change in equity appreciation instrument | | | - | | | | - | | | | 0.02 | | | | 0.11 | | | | - | |

| | | | | |

Gain on sale of processing and technology business | | | - | | | | - | | | | - | | | | 1.67 | | | | - | |

| | | | | |

Other non-interest income | | | 2.52 | | | | 1.51 | | | | 1.38 | | | | 1.72 | | | | 1.80 | |

| |

| | | | | |

Total net interest income and non-interest income, net of provision for loan losses | | | 4.52 | | | | 4.13 | | | | 3.90 | | | | 4.14 | | | | 1.62 | |

| | | | | |

Operating expenses | | | (3.56) | | | | (3.52) | | | | (3.20) | | | | (3.50) | | | | (3.16) | |

| |

| | | | | |

Income (loss) from continuing operations before income tax | | | 0.96 | | | | 0.61 | | | | 0.70 | | | | 0.64 | | | | (1.54) | |

| | | | | |

Income tax (benefit) expense | | | (0.69) | | | | (0.07) | | | | 0.30 | | | | 0.28 | | | | (0.02) | |

| |

| | | | | |

Income (loss) from continuing operations | | | 1.65 | | | | 0.68 | | | | 0.40 | | | | 0.36 | | | | (1.52) | |

| | | | | |

Loss from discontinued operations, net of tax | | | - | | | | - | | | | - | | | | - | | | | (0.05) | |

| |

| | | | | |

Net income (loss) | | | 1.65 % | | | | 0.68 % | | | | 0.40 % | | | | 0.36 % | | | | (1.57) % | |

| |

Net interest income on a taxable equivalent basis for the year ended December 31, 2013 amounted to $1.4 billion, an increase of $55.9 million, compared with 2012. Net interest margin, on a taxable equivalent basis, was 4.72% for the year 2013, an increase of 24 basis points from 2012, resulting from a higher yield from the covered portfolio due to higher expected cash flows and loan resolutions, higher yields from the commercial and construction portfolios due to the reduction in non-performing loans and lower cost of funds. Refer to the Net Interest Income section of this MD&A for a discussion of the major variances in net interest income, including yields and costs.

The provision for loan losses for the non-covered portfolio for year ended December 31, 2013 increased by $199.1 million, or 60%, compared with 2012, mainly due to the write downs of $318.0 million recorded in connection with the bulk sales of non-performing loans completed during the first and second quarters of 2013. Excluding the impact of the bulk sales, the provision for loan losses for the non-covered portfolio was down $119.0 million from the year ended December 31, 2012, reflecting a decrease of $67 million in the BPNA and a decrease of $52 million in BPPR. During the second quarter of 2013, the Corporation implemented certain enhancements to the allowance for loan losses methodology which resulted in a net reserve increase of $11.8 million for the non-covered portfolio and $7.5 million for the covered portfolio. Also, the Corporation recorded a recovery of $8.9 million associated with the sale of a portfolio of previously charged-off credit cards and personal loans during 2013. The provision for the covered portfolio was lower by $5.4 million and reflected lower expected losses in loans accounted by ASC Subtopic 310-30, mainly in commercial and construction loan pools.

Non-performing assets, excluding covered assets declined by $1.1 billion, driven by the bulk sales as well as the continuation of aggressive asset resolution strategies. Inflows of non-performing assets were down $492 million, of 42%, from 2012 and the net charge off ratio, excluding the impact of the bulk sales of non-performing assets, was 1.19%, compared to 1.97% in 2012.